book keeping and accountancy - council of engineers and...

TRANSCRIPT

Book Keeping and Accountancy

- The meaning and objects of Book Keeping, Double Entry Book

Keeping.

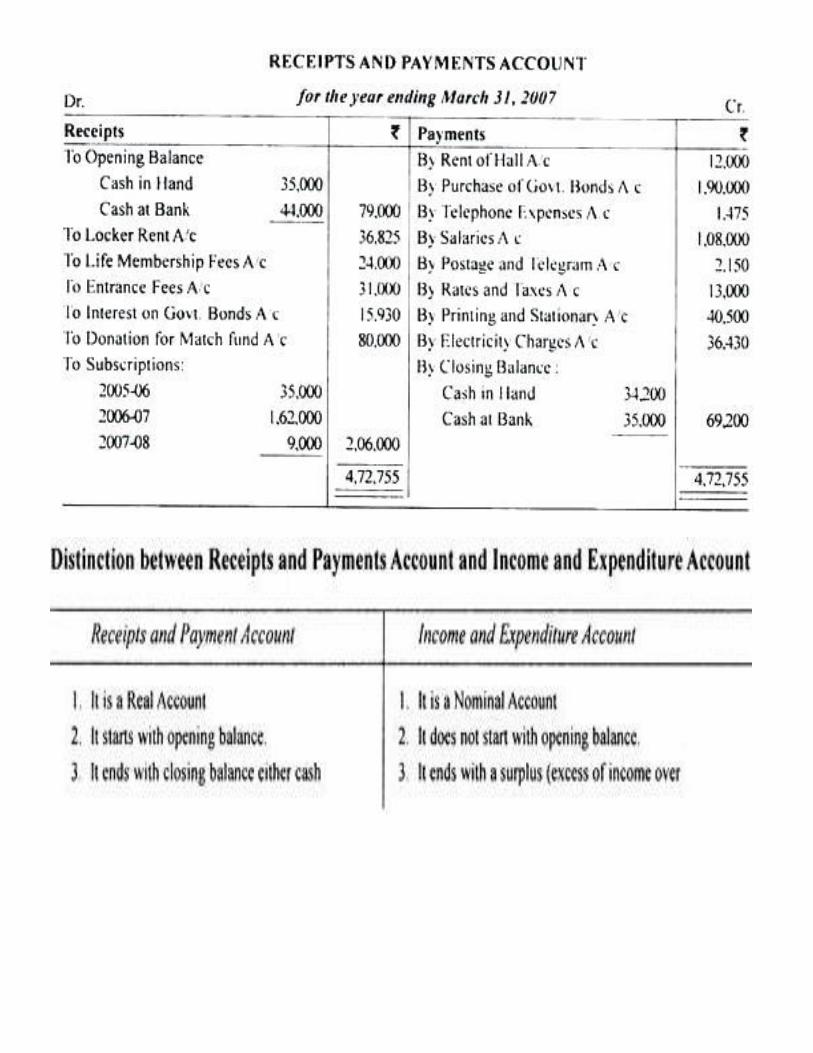

- Books of Prime Entry and Subsidiary Books: Cash Book, Bank

Book, Journal, Ledger, Purchase and Sale -- Books, Debit and Credit

Notes Register, Writing of Books, Posting and Closing of Accounts.

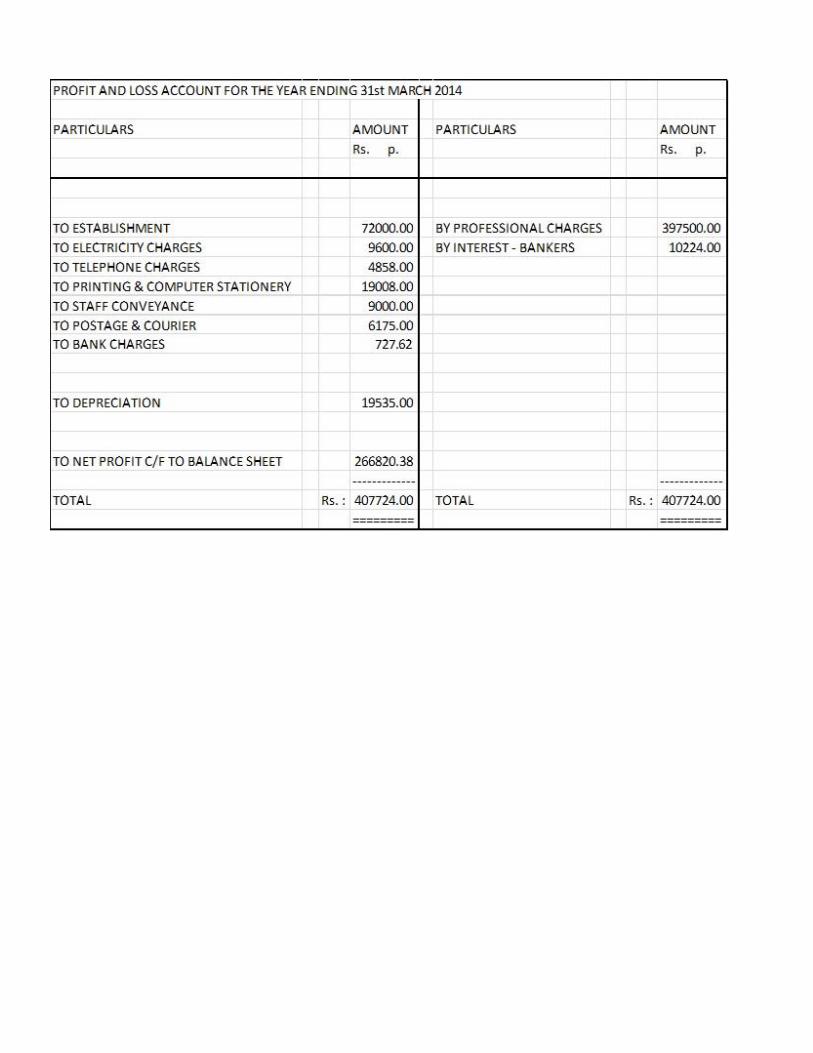

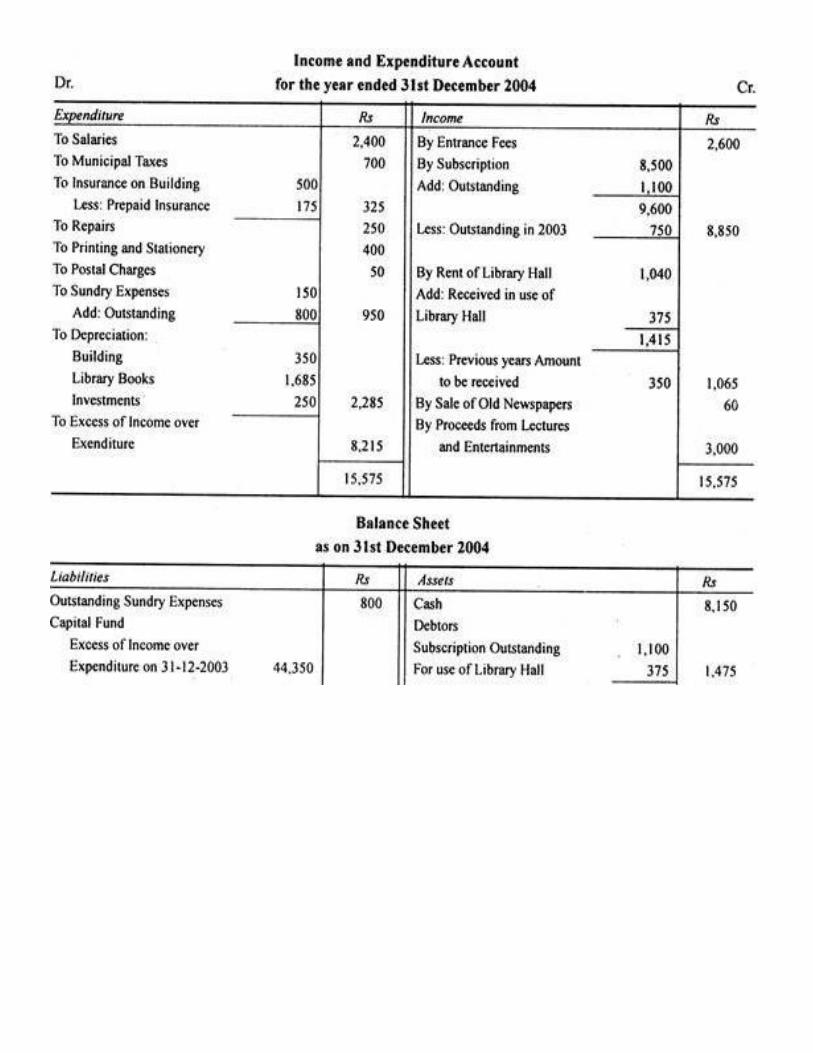

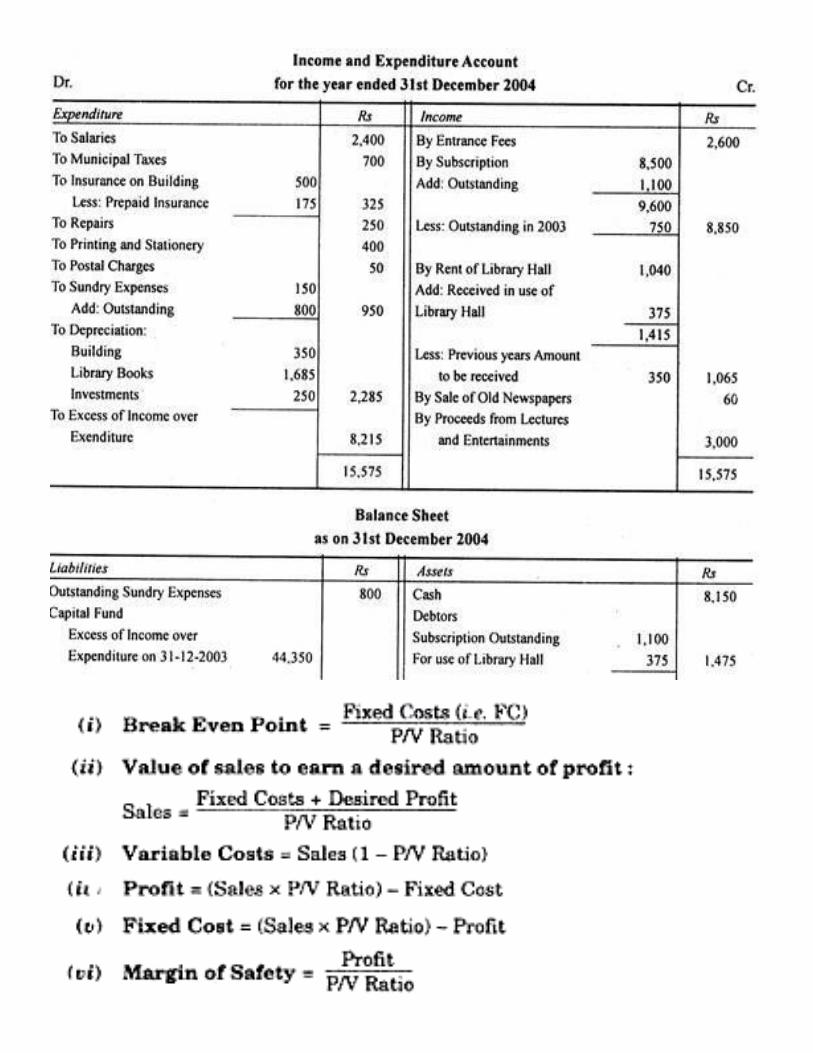

- Trading Account, Profit and Loss Account, Income and

Expenditure Account,

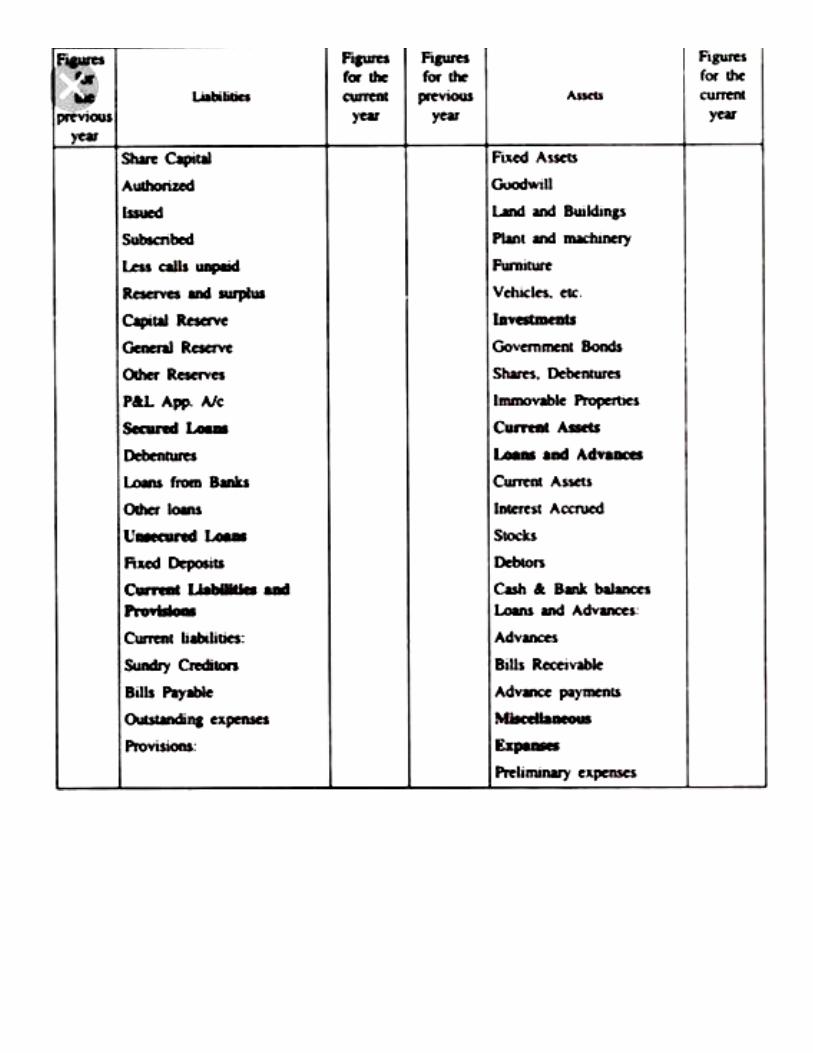

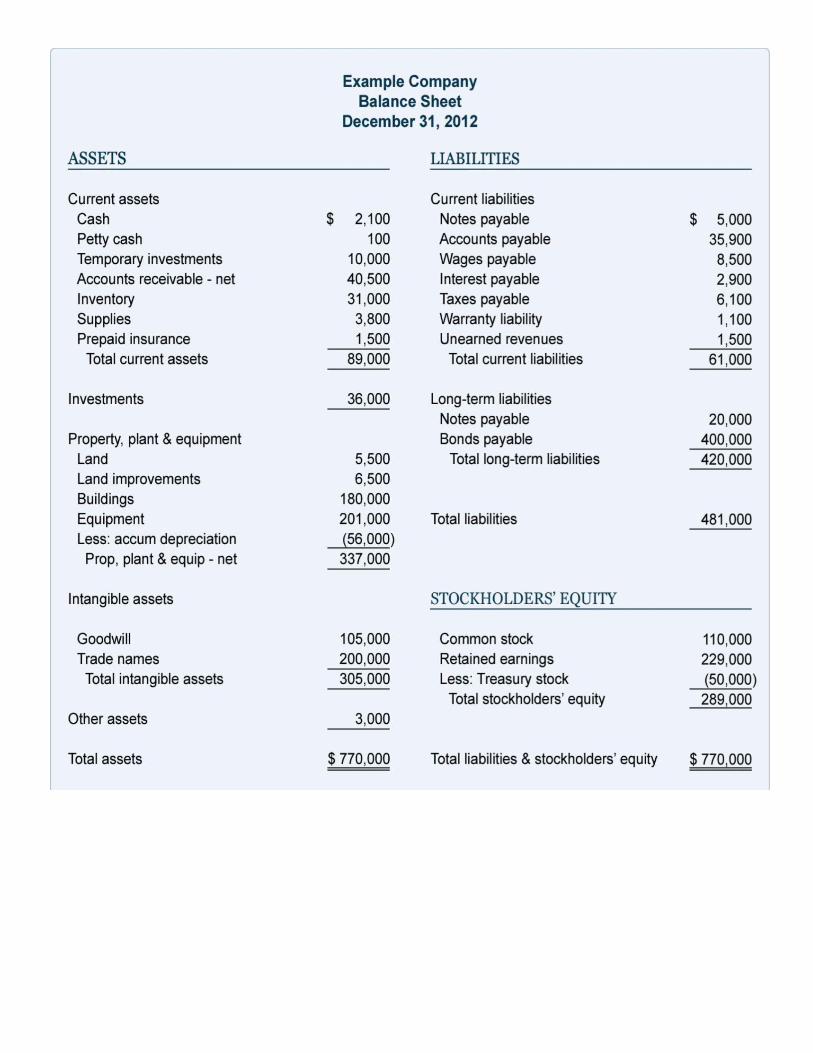

- Preparation of Balance Sheet for Individuals and Companies and

Disclosure Requirements.

- Cost, Costing and Elements of Cost, Fixed Expenses, Variable

Expenses, Break-Even Point.

The meaning and objects of Book Keeping, Double Entry Book Keeping.

Bookkeeping is the recording, on a day-to-day basis, of the financial

transactions and information pertaining to a business. It ensures that records of

the individual financial transactions are correct, up-to-date and comprehensive.

Accuracy is therefore vital to the process.

Bookkeeping provides the information from which accounts are prepared. It is

a distinct process, that occurs are within the broader scope of accounting.

Each transaction, whether it is a question of purchase or sale, must be

recorded. There are usually set structures in place for bookkeeping that are

called ‘quality controls’, which help ensure timely and accurate records.

Bookkeeping tasks

Essentially, bookkeeping means recording and tracking the numbers involved

in the financial side of the business in an organised way. It is essential for

businesses, but is also useful for individuals and non-profit organisations.

The person(s) responsible for bookkeeping for a business would record all

transactions that are related, including but not limited to:

• Expense payments to suppliers

• Loan payments

• Customer payments for invoices

• Monitoring asset depreciation

• Generating financial reports

Bookkeeping and accounting are often heard being used interchangeably,

however, accounting is the overall practice of managing finances of a

business or individual, while bookkeeping refers more specifically to the

tasks and practices involved in recording the financial activities.

Why bookkeeping matters

While it may seem obvious, detailed, thorough bookkeeping is crucial for

businesses of all sizes. Seemingly straightforward, bookkeeping quickly

becomes more complex with the introduction of tax, assets, loans, and

investments.

Tracking the financial activities of a business is the truest purpose of

bookkeeping, meaning it allows you to keep an up-to-date record of the

current incoming and outgoing amounts, amounts owed by customers and

by the business, and more.

Traditional bookkeeping

Bookkeeping has a long history as an integral part of accounting.

Traditionally, it involves ledgers, charts of accounts, and a tedious double-

entry system.

Here we'll cover how the main activities are recorded in traditional

bookkeeping practices, which are still used to this day.

Recording transactions

In principle, transactions must be recorded daily into the books or the

accounting system.

For each transaction, there must be a document that describes the business

transaction. This could include a sales invoice, sales receipt, a supplier

invoice, a supplier payment, bank payments and journals.

These accompanying documents provide the audit trail for each transaction

and are an important part of maintaining accurate records in the event of an

audit.

Double-entry bookkeeping

The double entry system of bookkeeping is based on the fact that every

transaction has two parts, which therefore affects two ledger accounts.

Every transaction involves a debit entry in one account and a credit entry in

another account. This serves as a kind of error-detection system: if, at any

point, the sum of debits does not equal the corresponding sum of credits, then

an error has occurred

Real Account:-

Personal Account :-

Nominal Account:-

Revenue,

Differed Revenue Expenditure and

Capital Expenditure

Debit:.........Credit....... Journal Entries

Owners Account and Bank account

Cash Book/Bank Account and Books of Account

Here are basics of the 10 most common types of bookkeeping accounts for

a small business that you should know:

▪ Cash. It doesn’t get more basic than this. All of your business

transactions pass through the Cash account, which is so important

that often bookkeepers actually use two journals -- Cash Receipts and

Cash Disbursements -- to track the activity.

▪ Accounts Receivable. If your company sells products or services and

doesn’t collect payment immediately you have “receivables” and you

must track Accounts Receivable. This is money due from customers,

and keeping it up to date is critical to be sure that you send timely

and accurate bills or invoices.

▪ Inventory. Products you have in stock to sell are like money sitting

on a shelf and must be carefully accounted for and tracked. The

numbers you have in your books should be periodically tested by

doing physical counts of inventory on hand.

▪ Accounts Payable. No one likes to send money out of the business.

But it’s a little less painful if you have a clear view of everything via

your Accounts Payable. Good bookkeeping helps assure timely

payments and – importantly – that you don’t pay anyone twice.

Paying bills early can also qualify your business for discounts.

▪ Loans Payable. If you’ve borrowed money to buy equipment,

vehicles, furniture or other items for your business, this is the account

that tracks what’s owed and what’s due.

▪ Sales. The Sales account is where you track all incoming revenue

from what you sell. Recording sales in a timely and accurate manner

is critical to knowing where your business stands.

▪ Purchases. The Purchases Account is where you track any raw

materials or finished goods that you buy for your business. It’s a key

component of calculating “Cost of Goods Sold” (COGS), which you

subtract from Sales to find your company’s gross profit.

▪ Payroll Expenses. This is the biggest cost of all for many

businesses. No matter how much you beg, few people want to work

for nothing. Keeping this account accurate and up to date is essential

for meeting tax and other government reporting requirements.

Shirking those responsibilities will put you in serious hot water.

▪ Owners’ Equity. This account has a nice ring to it. Basically, it

tracks the amount each owner puts into the business. “Many small

businesses are owned by one person or a group of partners; they’re

not incorporated, so no stock shares exist to divide up ownership,”

says Epstein. “Instead, money put into the business is tracked in

Capital accounts, and any money taken out appears in Drawing

accounts. In order to be fair to all owners, your books must carefully

record all Owners’ Equity accounts.

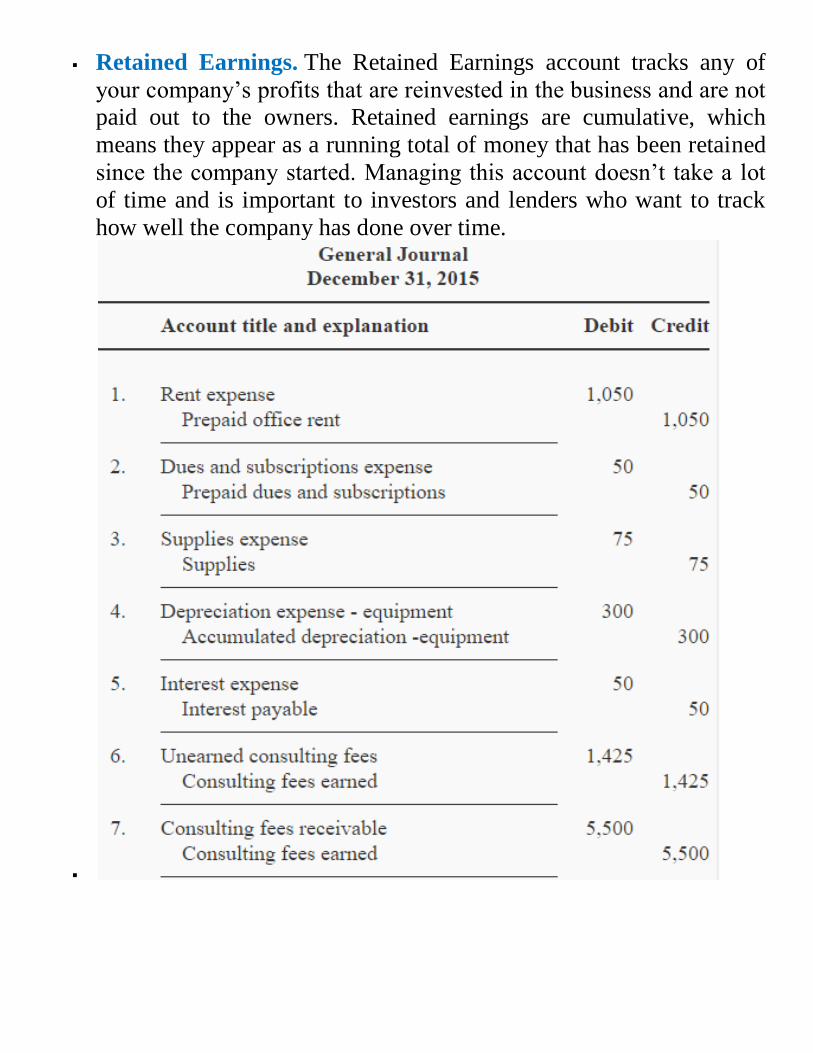

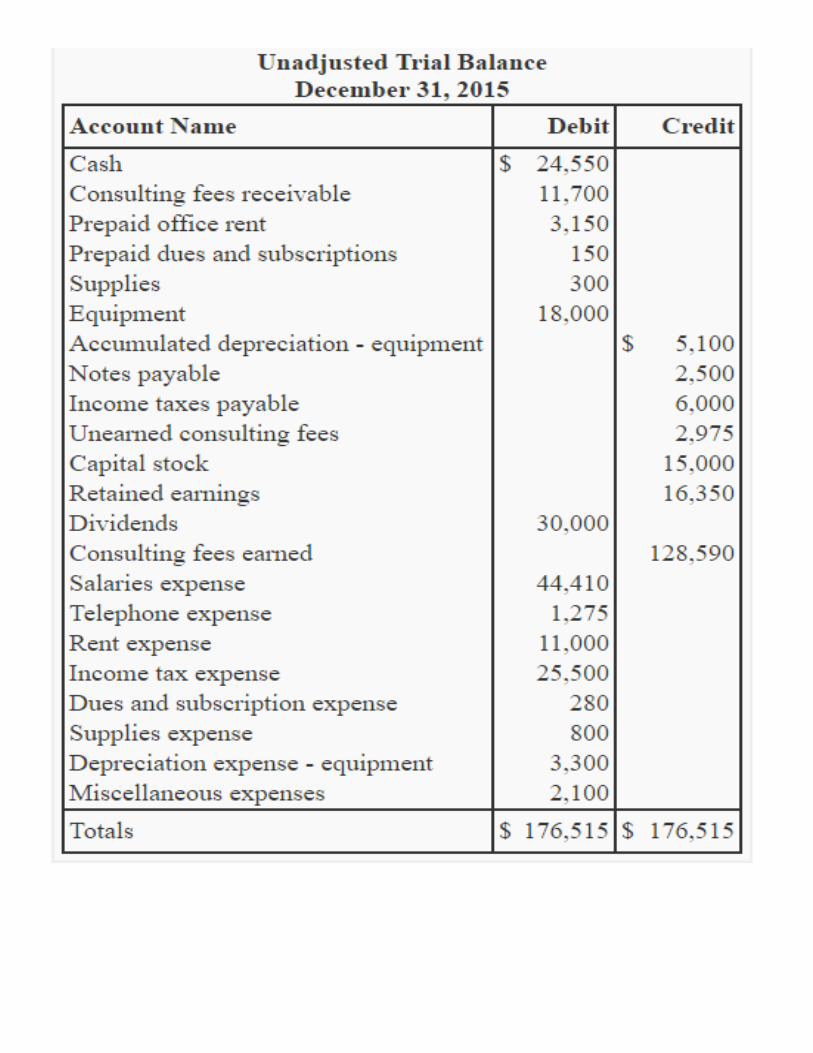

▪ Retained Earnings. The Retained Earnings account tracks any of

your company’s profits that are reinvested in the business and are not

paid out to the owners. Retained earnings are cumulative, which

means they appear as a running total of money that has been retained

since the company started. Managing this account doesn’t take a lot

of time and is important to investors and lenders who want to track

how well the company has done over time.

▪

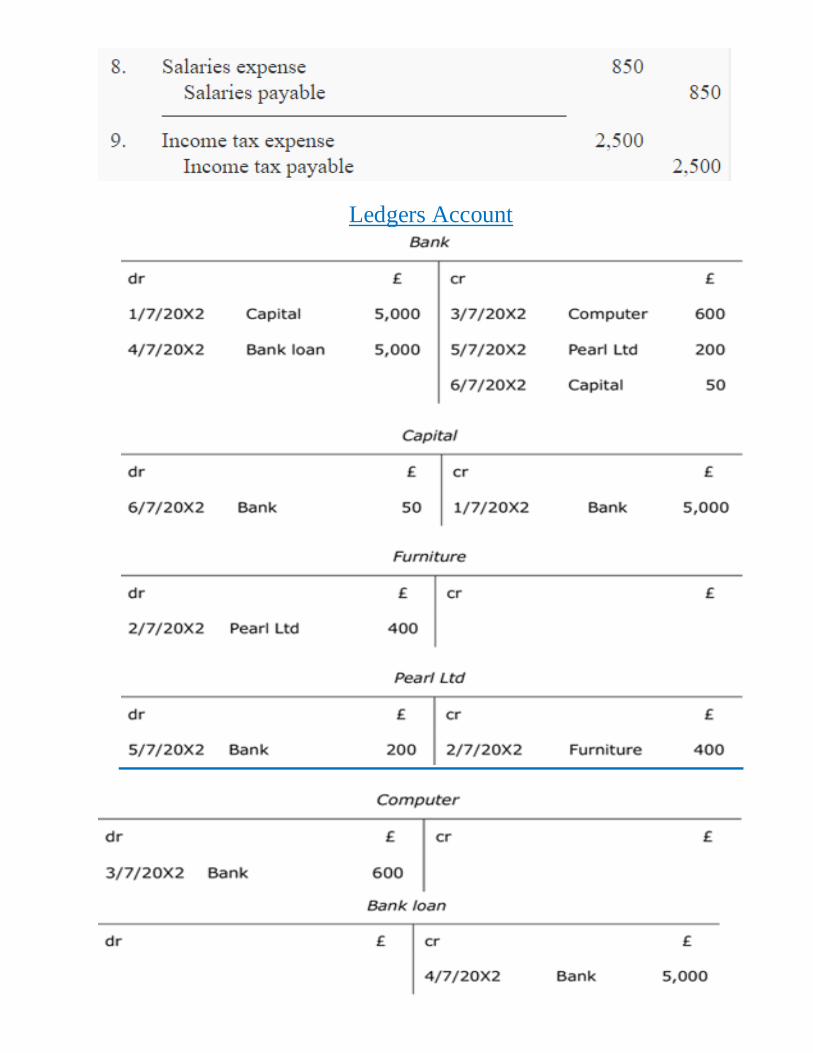

Ledgers Account

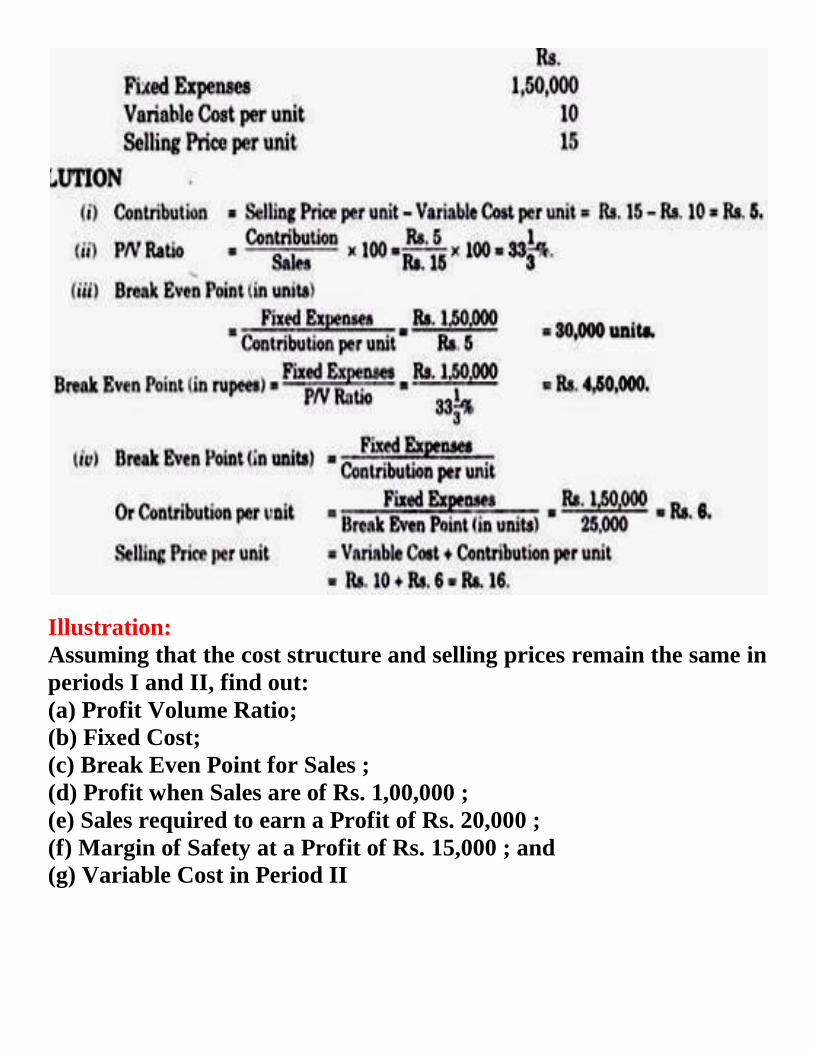

Illustration:

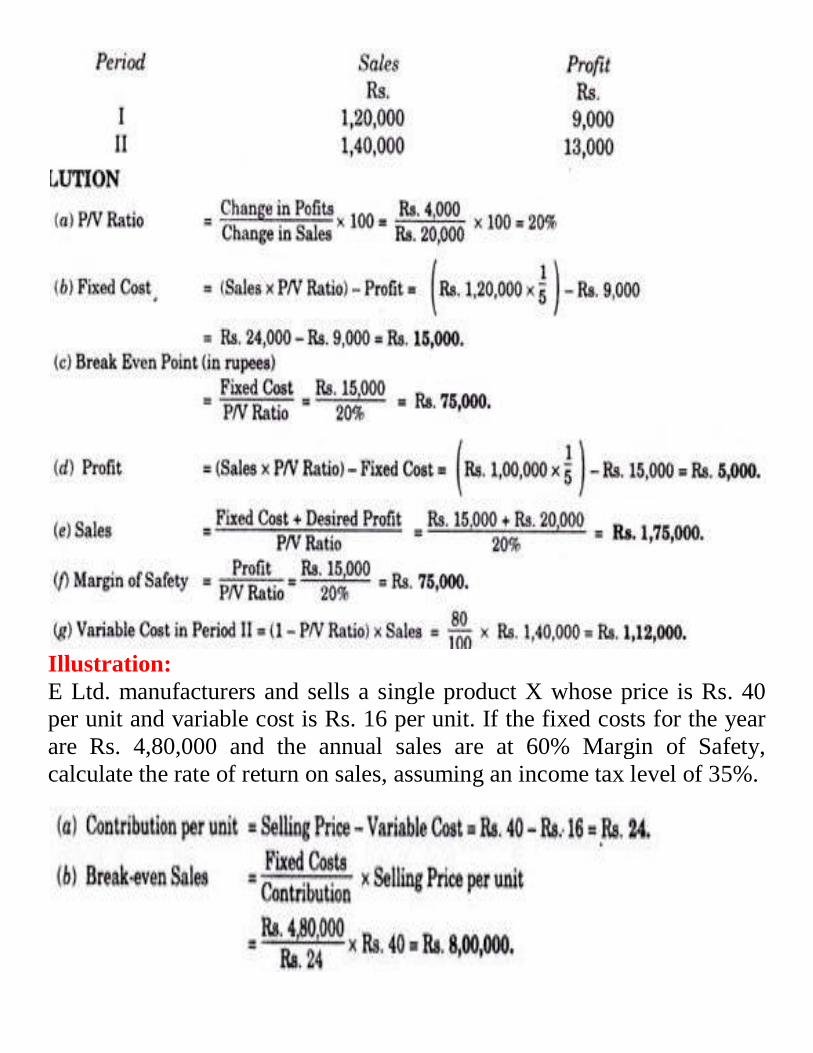

Assuming that the cost structure and selling prices remain the same in

periods I and II, find out:

(a) Profit Volume Ratio;

(b) Fixed Cost;

(c) Break Even Point for Sales ;

(d) Profit when Sales are of Rs. 1,00,000 ;

(e) Sales required to earn a Profit of Rs. 20,000 ;

(f) Margin of Safety at a Profit of Rs. 15,000 ; and

(g) Variable Cost in Period II

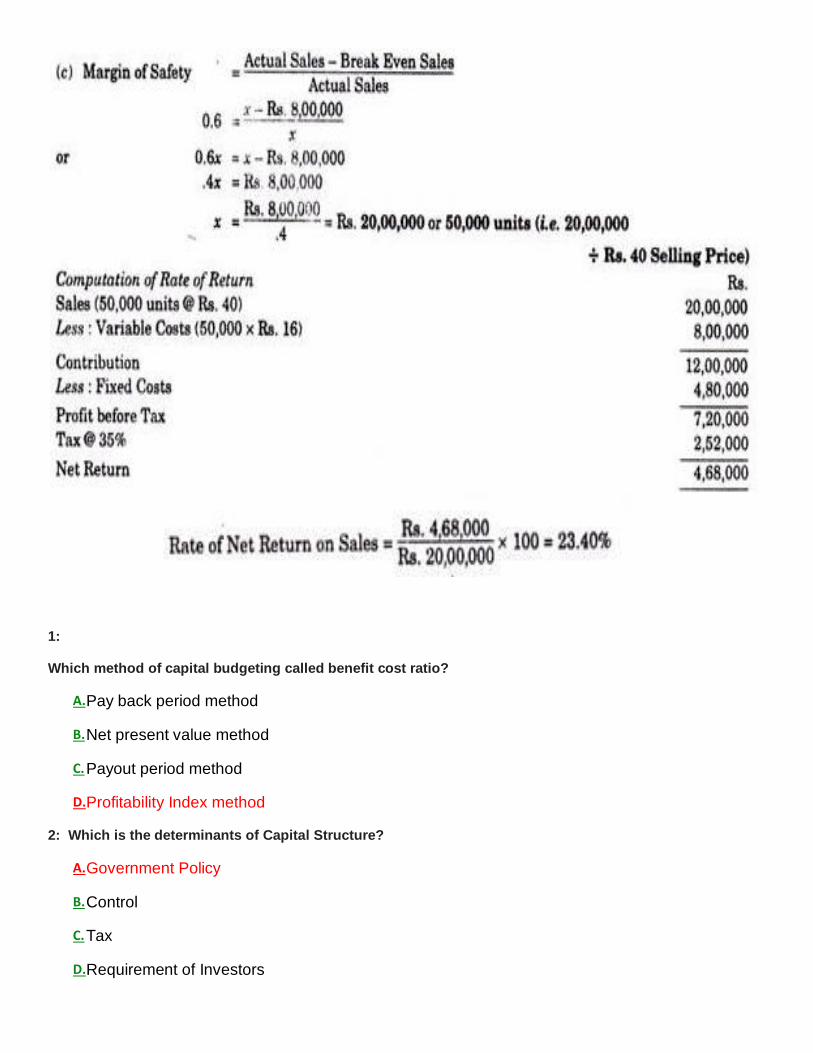

Illustration:

E Ltd. manufacturers and sells a single product X whose price is Rs. 40

per unit and variable cost is Rs. 16 per unit. If the fixed costs for the year

are Rs. 4,80,000 and the annual sales are at 60% Margin of Safety,

calculate the rate of return on sales, assuming an income tax level of 35%.

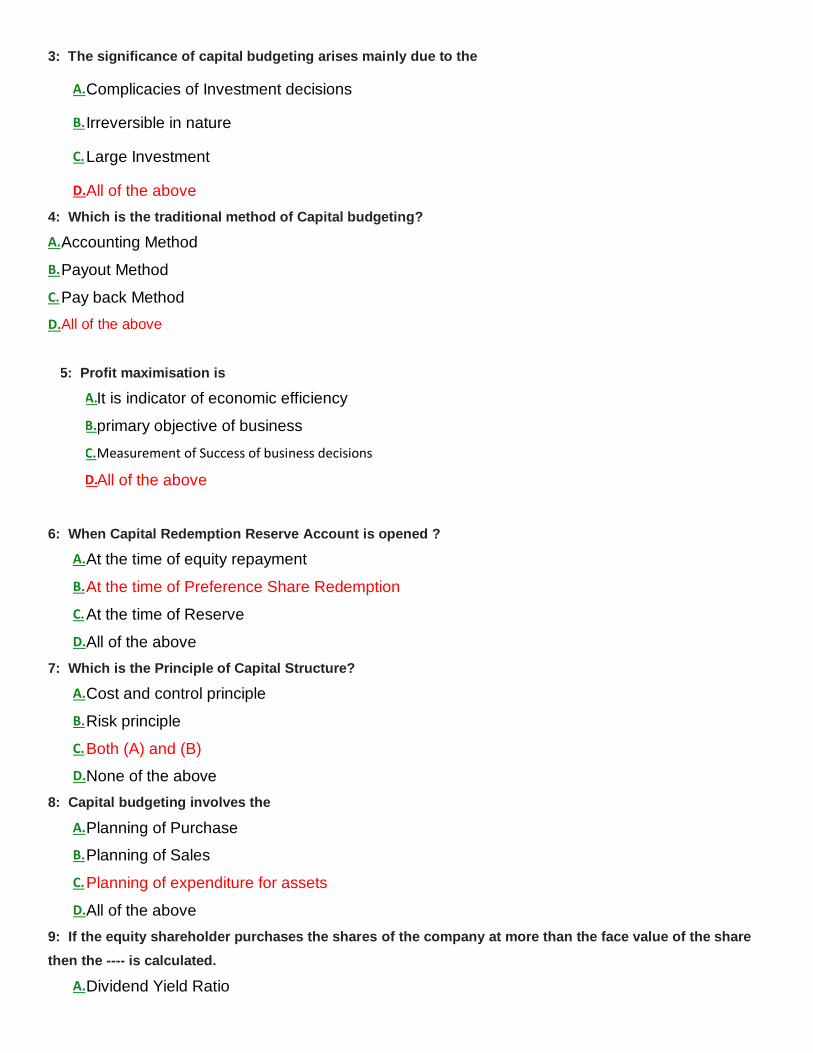

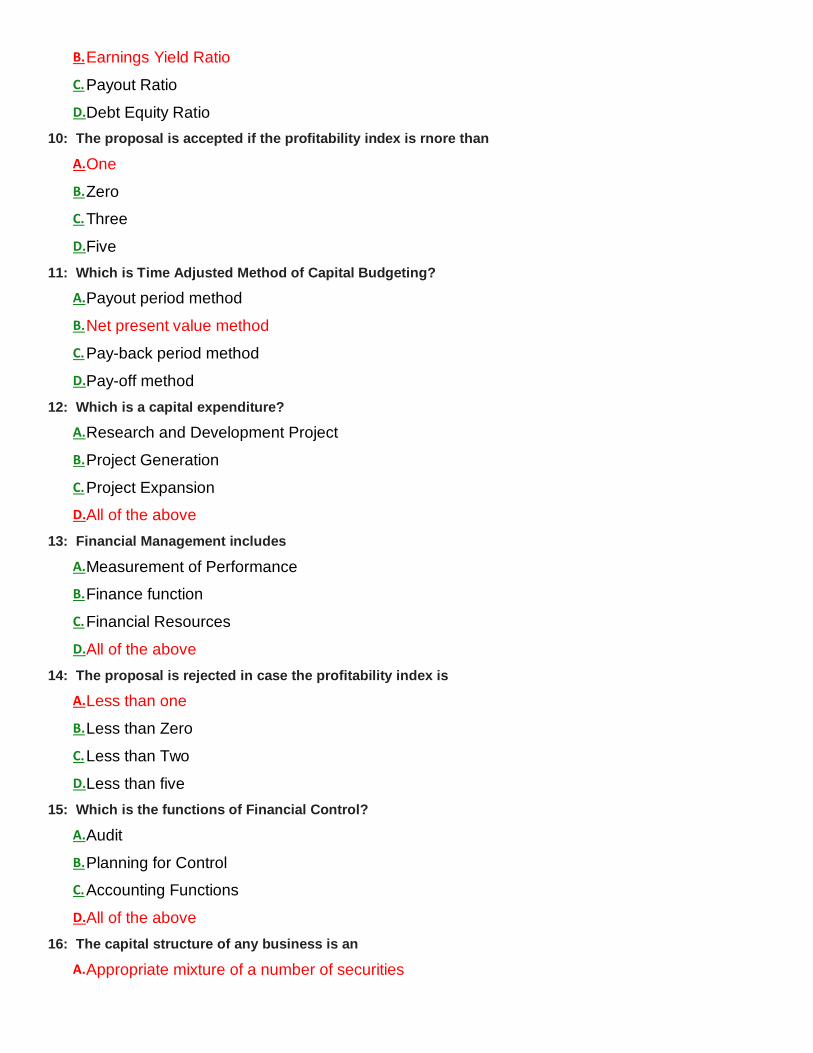

1:

Which method of capital budgeting called benefit cost ratio?

A. Pay back period method

B. Net present value method

C. Payout period method

D. Profitability Index method

2: Which is the determinants of Capital Structure?

A. Government Policy

B. Control

C. Tax

D. Requirement of Investors

3: The significance of capital budgeting arises mainly due to the

A. Complicacies of Investment decisions

B. Irreversible in nature

C. Large Investment

D. All of the above

4: Which is the traditional method of Capital budgeting?

A. Accounting Method

B. Payout Method

C. Pay back Method

D. All of the above

5: Profit maximisation is

A. It is indicator of economic efficiency

B. primary objective of business

C. Measurement of Success of business decisions

D. All of the above

6: When Capital Redemption Reserve Account is opened ?

A. At the time of equity repayment

B. At the time of Preference Share Redemption

C. At the time of Reserve

D. All of the above

7: Which is the Principle of Capital Structure?

A. Cost and control principle

B. Risk principle

C. Both (A) and (B)

D. None of the above

8: Capital budgeting involves the

A. Planning of Purchase

B. Planning of Sales

C. Planning of expenditure for assets

D. All of the above

9: If the equity shareholder purchases the shares of the company at more than the face value of the share

then the ---- is calculated.

A. Dividend Yield Ratio

B. Earnings Yield Ratio

C. Payout Ratio

D. Debt Equity Ratio

10: The proposal is accepted if the profitability index is rnore than

A. One

B. Zero

C. Three

D. Five

11: Which is Time Adjusted Method of Capital Budgeting?

A. Payout period method

B. Net present value method

C. Pay-back period method

D. Pay-off method

12: Which is a capital expenditure?

A. Research and Development Project

B. Project Generation

C. Project Expansion

D. All of the above

13: Financial Management includes

A. Measurement of Performance

B. Finance function

C. Financial Resources

D. All of the above

14: The proposal is rejected in case the profitability index is

A. Less than one

B. Less than Zero

C. Less than Two

D. Less than five

15: Which is the functions of Financial Control?

A. Audit

B. Planning for Control

C. Accounting Functions

D. All of the above

16: The capital structure of any business is an

A. Appropriate mixture of a number of securities

B. Interest

C. Income

D. All of the above

17: Capital budgeting investment decision involve

A. Capital expenditure

B. Long term assets

C. A long term function

D. All of the above

18: The arrangement of working capital and current assets can be done only by

A. Short-term sources

B. Cost of capital

C. Long term sources

D. Financial Plan

19: Which is the limitation of Traditional approach of Financial Management?

A. More emphasis on long term problems

B. One-sided approach

C. Ignores allocation of resources

D. All of the above

20: Dividends are the ------ of a company distributed amongst members in proportion to their shares.

A. Divisible Profits

B. Assets with Cash and Bank

C. Reserve

D. Undivisible Profits

21: Which is the element of capital budgeting decision?

A. Capital expenditure project

B. A long term investment

C. A long term effect

D. All of the above

22: The cost of depreciation funds is calculated according to

A. Opportunity Cost Theory

B. Flow

C. Accounting Theory

D. Reserve Theory

23: Role of finance manager includes?

A. Investing and Financing Decisions

B. Financial analysis

C. All of the above

D. None of the above

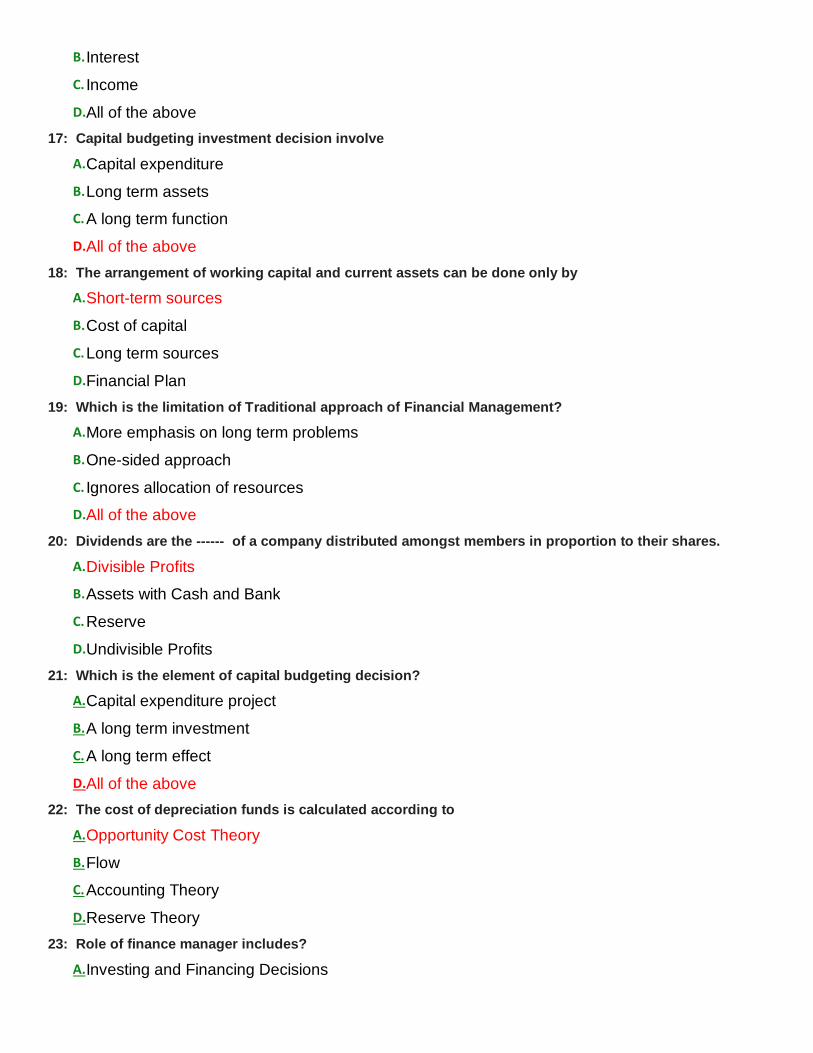

24: Which method of capital budgeting is known as 'Accounting Rate of Return Method'?

A. Average Rate of Return Method

B. Return on Investment

C. Rate of Return Method

D. All of the above

25: Financial Management is a part of

A. Accounting

B. Business Management

C. Financial Accounting

D. All of the above

26: Capital budgeting is

A. Actually the process of making investment decisions in capital expenditure

B. A profit

C. A sales

D. A cost

27: There is deterioration in the management of work capital of XYZ Ltd. What does it refer to?

A. That capital employed has reduced

B. That the profitability has gone up

C. That sales has decreased

D. That debtors collection period has increased

28: Payback reciprocal method of ranking investment proposals should be used only when

A. Annual savings are even for the entire period

B. The econontic life of the project is at least twice of the pay back period

C. (A) and (B) both

D. None of the above

29: Working capital can be used for the purchase of

A. machinery

B. goodwill

C. raw material

D. land & building

30: Capital budgeting is known as

A. Cost of Product

B. Capital Expenditure

C. Cost of Sales

D. Profit

The cost of Air-Conditioning of the Manager’s office will be..

1. a capital expenditure

2. a revenue expenditure

3. a deferred revenue expenditure

4. none of these

Calls in advance’ is shown under..

1. share capital

2. reserve and surplus

3. current liabilities

4. loans and advances

A loan can be described as a short-term loan if the period is ..

1. three years

2. less than one year

3. over one year

4. more than two years

How many parties are there in Consignment?

1. 1

2. 2

3. 3

4. 5

The Total Tax of an assesses has been computed as Rs. 36,523.40. After rounding

off, the total tax will be taken as…

1. Rs. 36520

2. Rs. 36,525

3. Rs.36,530

4. None of these

In the absence of any agreement, partners are liable to receive interest on their

loans@

1. 12%

2. 10%

3. 6%

4. 8%

Goods Costing Rs. 1,00,000 are consigned at 20% on invoice price. What is its

Load?

1. 1,25,000

2. 25,000

3. 75,000

4. 20,000

What time would be taken into consideration if equal monthly amount is drawn as

drawing at the beginning of each month?

1. 7

2. 6

3. 5

4. 6.5

Companies profit divided among shareholder is ..

1. interest

2. reserve

3. dividend

4. surplus

Debenture carrying charge on particular asset on the company is know as..

1. fixed

2. mortgage

3. naked

4. floating

Operating profit is

1. profit after deducting financial costs

2. profit after deducting taxes

3. profit after deducting normal operating expenses including depreciation

4. equal to net profit

Retained earning is synonymous to..

1. accumulated profit and loss account

2. profit for the year

3. operating profit

4. gross profit

Dividends are usually paid as a percentage of ..

1. authorized shares capital

2. net profit

3. paid up capital

4. called up capital

Economic life of an enterprise is split into the periodic interval as per..

1. Money measurement concept

2. Matching concept

3. Going concern concept

4. Accrual Concept

What is the amount of gross profit/loss when opening stock is Rs. 18,000, purchases

Rs. 78,000, cost of good sold Rs. 1,06,000 and sales Rs. 1,49,000?

1. Rs. 44,000 profit

2. Rs. 42,000 profit

3. Rs. 43,000 profit

4. Rs. 43,000 loss

Which of the following is an example of fictitious assets?

1. Machinery

2. Stock

3. Patent

4. Preliminary Expenses

What is the main purpose of Bank Reconciliation?

1. To locate cashier’s mistake

2. Reconciliation of the cash book and bank balances

3. To find out bank balances

4. to find out cash balances

Double entry book-keeping was started by

1. F.W Taylor

2. Henry Fayol

3. Lucas Pacioli

4. Adam Smith

Which financial statement is used to show what the firm owns?

1. income statement

2. balance sheet

3. statement of retained earnings

4. cash flow statement

According to accounting equation assets are equal to?

1. liabilities

2. liabilities and equities

3. equities

4. none of these

The accounting cycle represents a series of steps that a business uses

1. to record and classify the transactions

2. to summarize the transactions

3. to communicate financial events

4. for all of these

The cost concept states that all goods and services purchased should be recorded at

1. historical cost

2. market cost

3. both 1 and 2

4. none of these

The matching principle attempts to find satisfactory bases of association between

1. assets and liabilities

2. expenses and revenues

3. internal equities and external liabilities

4. none of these

The Statement that shows the cause of change in the financial position of an

organization is known as

1. balance sheet

2. funds flow statement

3. statement of financial position

4. none of these

The results of business activities are reflected in

1. profit and loss account

2. profit and loss appropriation account

3. balance sheet

4. none of these

Balance sheet is a statement which discloses an organization’s

1. assets

2. liabilities

3. owner’s equity

4. all of these

Current liabilities need to be paid

1. within one accounting cycle

2. beyond one accounting cycle

3. within 3 years

4. within 6 months

Revenue

1. causes a decrease in shareholder’s equity

2. causes a decrease or an increase in shareholder’s equity

3. has no impact on shareholder’s equity

4. causes an increase in shareholders’ equity

Financially, shareholders are rewarded by

1. interest

2. profits

3. dividends

4. none of these

Which of the following is not a current assets?

1. Accounts receivable

2. Inventory of finished products

3. Inventory of raw materials

4. Land

Which of the following is a financial asset?

1. Inventories

2. Equipment

3. Loan to an associate

4. Accounts receivable

The cash flow statement consists of which of the following sections?

1. Operating and non-operating

2. current and non-current

3. operating, investing and financing

4. trading and financial

Which of the following is not a long-term liability?

1. Accounts payable (for payable due in more than one year)

2. Bank borrowings reimbursable in more than one year

3. Bank overdrafts

4. Cash Ratio

When does an accountant record a transaction?

1. If it is materialized by a concrete document

2. if it has a tax implication

3. on Manager’s demand

4. None of these

Which of the following equations represents the balance sheet?

1. Assets + Liabilities = Shareholders’ equity

2. Assets = Liabilities = shareholders’ equity

3. Assets = Liabilities – Shareholders’ equity

4. Assets = Liabilities + Shareholders’ equity

Which of the following describes a record of the transactions?

1. General ledger

2. Income statement

3. Balance sheet

4. Journal

The Four principal qualitative characteristics of useful financial statements are

1. understandability, relevance, reliability, comparability

2. timeliness, relevance, reliability, comparability

3. understandability,relevance, accuracy, comparability

4. understandability, relevance, reliability, simplicity

Earnings are the result of the difference between

1. revenue and assets

2. revenue and liabilities

3. liabilities and expenses

4. revenue and expenses

In Which order does the journal list transactions?

1. alphabetical

2. decreasing

3. increasing

4. chronological

1. Question

The accounting profession can be divided into three major categories; specifically,

the practice of public accounting, private accounting, and governmental accounting.

A somewhat unique and important service of public accountants is:

o Financial accounting.

o Managerial accounting.

o Auditing.

o Cost accounting.

2. Question

The primary private sector agency that oversees external financial reporting

standards is the:

o Financial Accounting Standards Board.

o Federal Bureau of Investigation.

o General Accounting Office.

o Internal Revenue Service. The Financial Accounting Standards Board is the private sector oversight group for

accounting standards. The Federal Bureau of Investigation is a government organization

that employs many accountants, but has little to do with accounting rule development.

The General Accounting Office and Internal Revenue Service are also government

agencies. The GAO serves Congress and the IRS administers tax law.

3. Question

Which of the following equations properly represents a derivation of the

fundamental accounting equation?

o Assets + liabilities = owner's equity.

o Assets = owner's equity.

o Cash = assets.

o Assets – liabilities = owner's equity.

The normal expression of the accounting equation is: assets = liabilities + owners’

equity. The only choice which is a correct mathematical expression is “d.” In “d,”

liabilities are subtracted from both sides of the “normal” accounting equation.

4. Question

Wilson Company owns land that cost $100,000. If a “quick sale” of the land was

necessary to generate cash, the company feels it would receive only $80,000. The

company continues to report the asset on the balance sheet at $100,000. Which of

the following concepts justifies this?

o The historical-cost principle.

o The value is tied to objective and verifiable past transactions.

o Neither of the above.

o Both "a" and "b".

Both of these concepts justify the continued reporting at $100,000, as this amount is

an objective and verifiable historical-cost measurement.

5. Question

Retained earnings will change over time because of several factors. Which of the

following factors would explain an increase in retained earnings?

o Net loss.

o Net income.

o Dividends.

o Investments by stockholders.

Net income would cause increases in retained earnings. In contrast, losses and

dividends are factors that will cause decreases in retained earnings. Investments by

stockholders’ would cause an increase in capital stock, not retained earnings.

6. Question

Which of these items would be accounted for as an expense?

o Repayment of a bank loan.

o Dividends to stockholders.

o The purchase of land.

o Payment of the current period's rent.

Payment of rent for the current period would be accounted for as rent expense. The

repayment of a bank loan is the reduction of a liability, dividends are a distribution

of equity, and the purchase of land establishes an asset.

7. Question

Which of the following transactions would have no impact on stockholders’ equity?

o Purchase of land from the proceeds of a bank loan.

o Dividends to stockholders.

o Net loss.

o Investments of cash by stockholders.

The purchase of land would cause assets to increase and liabilities to increase.

Dividends and net losses cause reductions in total equity, while investments cause

increases.

8. Question

Which of the following would not be included on a balance sheet?

o Accounts receivable.

o Accounts payable.

o Sales.

o Cash.

Sales is a revenue item for the income statement. Accounts receivable and cash are

assets and accounts payable is a liability.

9. Question

Remington provided the following information about its balance sheet:Based on the

information provided, how much are Remington’s liabilities?

o $200.

o $900.

o $1,200.

o $1,700.

$1,200. The only liabilities listed are accounts payable ($200) and bank loans

($1,000).

10. Question

Gerald had beginning total stockholders’ equity of $160,000. During the year, total

assets increased by $240,000 and total liabilities increased by $120,000. Gerald’s

net income was $180,000. No additional investments were made; however,

dividends did occur during the year. How much were the dividends?

o $20,000.

o $60,000.

o $140,000.

o $220,000. $60,000. Because total assets increased $240,000 and liabilities increased $120,000, the increase in equity

must have been $120,000 ($240,000 – $120,000). Net income increases equity ($180,000) and dividends

decrease equity. The increase in equity of $120,000 is therefore comprised of $180,000 in income (add)

and $60,000 of dividends (subtract).

1. Accounting provides information on

A. Cost and income for managers

B. Company's tax liability for a particular year

C. Financial conditions of an institutions

D. All of the above

2.The long term assets that have no physical existence but are rights that have

value is known as

A. Current assets

B. Fixed assets

C. Intangible assets

D. Investments

3.The assets that can be converted into cash within a short period (i.e. 1 year or

less) are known as

A. Current assets

B. Fixed assets

C. Intangible assets

D. Investments

4.Patents, Copyrights and Trademarks are

A. Current assets

B. Fixed assets

C. Intangible assets

D. Investments

5.The debts which are to be repaid within a short period (year or less) are known

as

A. Current liabilities

B. Fixed liabilities

C. Contingent liabilities

D. All of the above

6.The sales income (Credit and Cash) of a business during a given period is

called

A. Transactions

B. Sales Returns

C. Turnover

D. Purchase Returns

7.Any return evidence in support of a business transaction is called

A. Journal

B. Ledger

C. Ledger posting

D. Voucher

8.The account that records expenses, gains and losses is

A. Personal account

B. Real account

C. Nominal account

D. None of the above

9.Real account records

A. Dealings with creditors or debtors

B. Dealings in commodities

C. Gains and losses

D. All of the above

10. In Journal, the business transaction is recorded

A. Same day

B. Next day

C. Once in a week

D. Once in a month

11.The following is (are) the type(s) of Journal

A. Purchase Journal

B. Sales Journal

C. Cash Journal

D. All of the above

12.The process of entering all transactions from the Journal to Ledger is

called

A. Posting

B. Entry

C. Accounting

D. None of the above

13.The following is a statement showing the financial status of the comapany

at any given time

A. Trading account

B. Profit & Loss statement

C. Balance Sheet

D. Cash Book

14.The following is a statement of revenues and expenses for a specific

period of time

A. Trading account

B. Trial Balance

C. Profit & Loss statements

D. Balance Sheet

15.Balance sheet is a statement of

A. Assets

B. Liabilities

C. Capital

D. All of the above

16.Balance sheets are prepared

A. Daily

B. Weekly

C. Monthly

D. Annually

17.The ratios that refer to the ability of the firm to meet the short term

obligations out of its short term resources

A. Liquidity ratio

B. Leverage ratio

C. Activity ratio

D. Profitability ratio

18.The measure of how efficiently the assets resources are employed by the

firm is called

A. Liquidity ratio

B. Leverage ratio

C. Activity ratio

D. Profitability ratio

19.The following is (are) the current liability (ies)

A. Bills payable

B. Outstanding expenses

C. Bank Overdraft

D. All of the above

20.Current ratio =

A. Quick assets/Current liabilities

B. Current assets/Current liabilities

C. Debt/Equity

D. Current assets/Equity