berlin, 18 june 2015 - shw automotive · 1.9%% 5.0 4.2 2014 2017 5.2 3.8 2016 2018 cagr cagr cagr...

TRANSCRIPT

dbAccess German, Swiss & Austrian Conference

Berlin, 18 June 2015

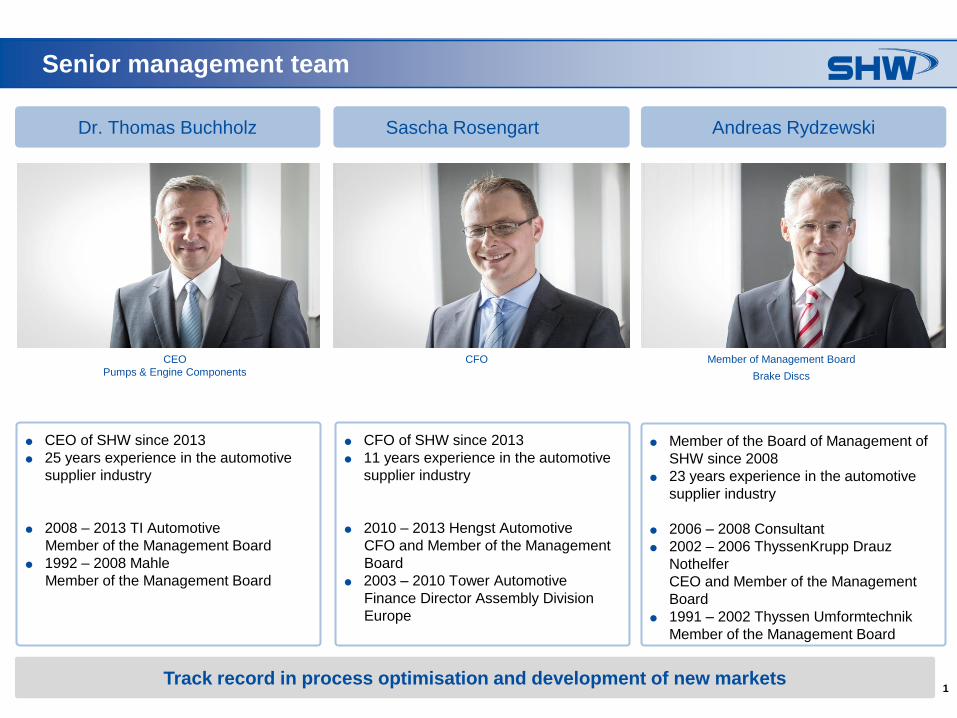

1Track record in process optimisation and development of new markets

Senior management team

Andreas Rydzewski

Member of the Board of Management of

SHW since 2008

23 years experience in the automotive

supplier industry

2006 – 2008 Consultant

2002 – 2006 ThyssenKrupp Drauz

Nothelfer

CEO and Member of the Management

Board

1991 – 2002 Thyssen Umformtechnik

Member of the Management Board

Member of Management Board

Brake Discs

Sascha Rosengart

CFO

Dr. Thomas Buchholz

CEO of SHW since 2013

25 years experience in the automotive

supplier industry

2008 – 2013 TI Automotive

Member of the Management Board

1992 – 2008 Mahle

Member of the Management Board

CEO

Pumps & Engine Components

CFO of SHW since 2013

11 years experience in the automotive

supplier industry

2010 – 2013 Hengst Automotive

CFO and Member of the Management

Board

2003 – 2010 Tower Automotive

Finance Director Assembly Division

Europe

2Operational success story with strong financial results

Pumps & Engine Components

Brake Discs

Key product strength: high fuel saving

potential

Two plants in Germany, one plant in

Brazil (Sao Paulo), one in China

(Kunshan)

Sales and development centre in

Canada (Toronto)

Number of employees: approx. 830

Product advantage: weight reduction

Casting and machining in Germany

First JV in China with foundry capacity

Number of employees: approx. 380

Long-standing relationships as Tier 1 supplier

Focus on customised products for CO2-reduction

Origin in 1365

Cutting-edge technology for environmental friendly mobility

Total turnover 2014: € 430m

Pumps & Engine Components

78.0% Brake Discs

22.0%

3

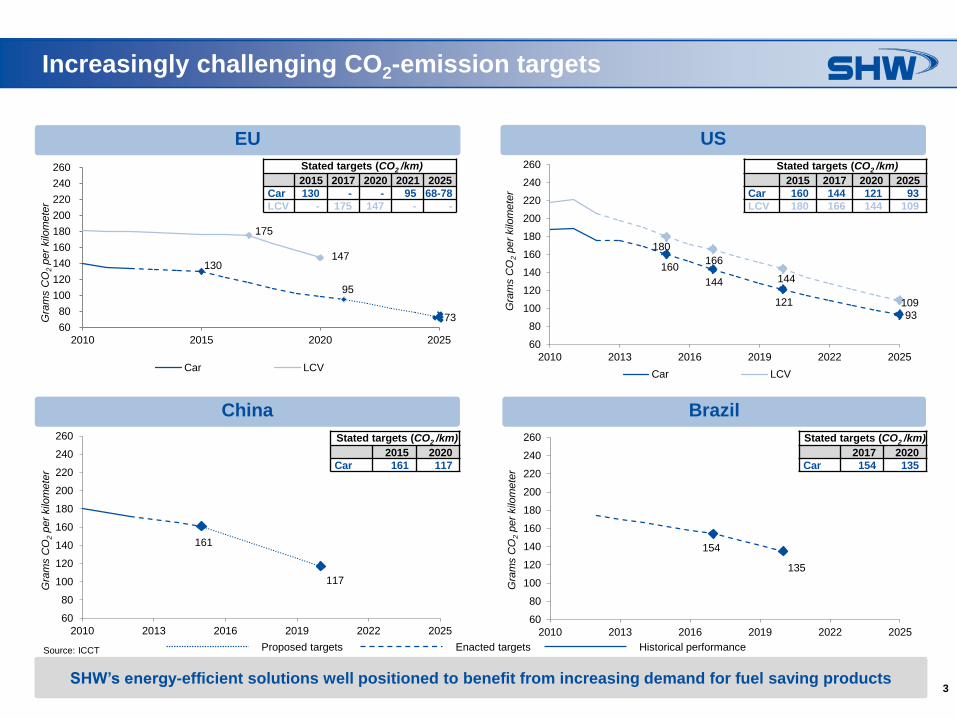

Increasingly challenging CO2-emission targets

USEU

China Brazil

SHW’s energy-efficient solutions well positioned to benefit from increasing demand for fuel saving products

Proposed targets Historical performanceEnacted targets

154

135

60

80

100

120

140

160

180

200

220

240

260

2010 2013 2016 2019 2022 2025

Gra

ms C

O2

per

kilo

mete

r

161

117

60

80

100

120

140

160

180

200

220

240

260

2010 2013 2016 2019 2022 2025

Gra

ms C

O2

per

kilo

mete

r

Stated targets (CO2 /km)

2015 2020

Car 161 117

Stated targets (CO2 /km)

2017 2020

Car 154 135

Source: ICCT

160

144

121

93

180

166

144

109

60

80

100

120

140

160

180

200

220

240

260

2010 2013 2016 2019 2022 2025

Gra

ms C

O2

per

kilo

mete

r

Car LCV

Stated targets (CO2 /km)

2015 2017 2020 2021 2025

Car 130 - - 95 68-78

LCV - 175 147 - -

Stated targets (CO2 /km)

2015 2017 2020 2025

Car 160 144 121 93

LCV 180 166 144 109

130

95

73

175

147

60

80

100

120

140

160

180

200

220

240

260

2010 2015 2020 2025

Gra

ms C

O2

per

kilo

mete

r

Car LCV

4

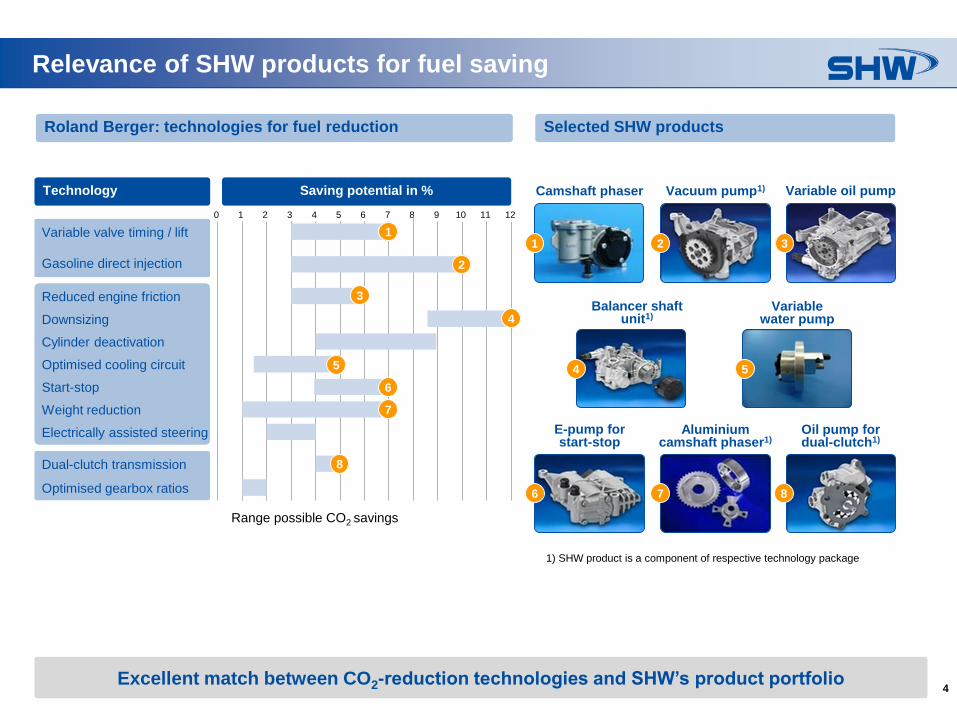

Relevance of SHW products for fuel saving

Excellent match between CO2-reduction technologies and SHW’s product portfolio

1) SHW product is a component of respective technology package

Roland Berger: technologies for fuel reduction

Range possible CO2 savings

Technology

12

Saving potential in %

0 6 7 8 94 51 2 3 10 11

Camshaft phaser

1

Vacuum pump1)

2

Variable oil pump

Balancer shaftunit1)

3

4

Variablewater pump

E-pump forstart-stop

5

6

Aluminiumcamshaft phaser1)

Oil pump fordual-clutch1)

7 8

Variable valve timing / lift

Gasoline direct injection

1

2

Reduced engine friction

Downsizing

Cylinder deactivation

Start-stop

Optimised cooling circuit

Weight reduction

Electrically assisted steering

3

4

5

6

7

Dual-clutch transmission

Optimised gearbox ratios

8

Selected SHW products

5

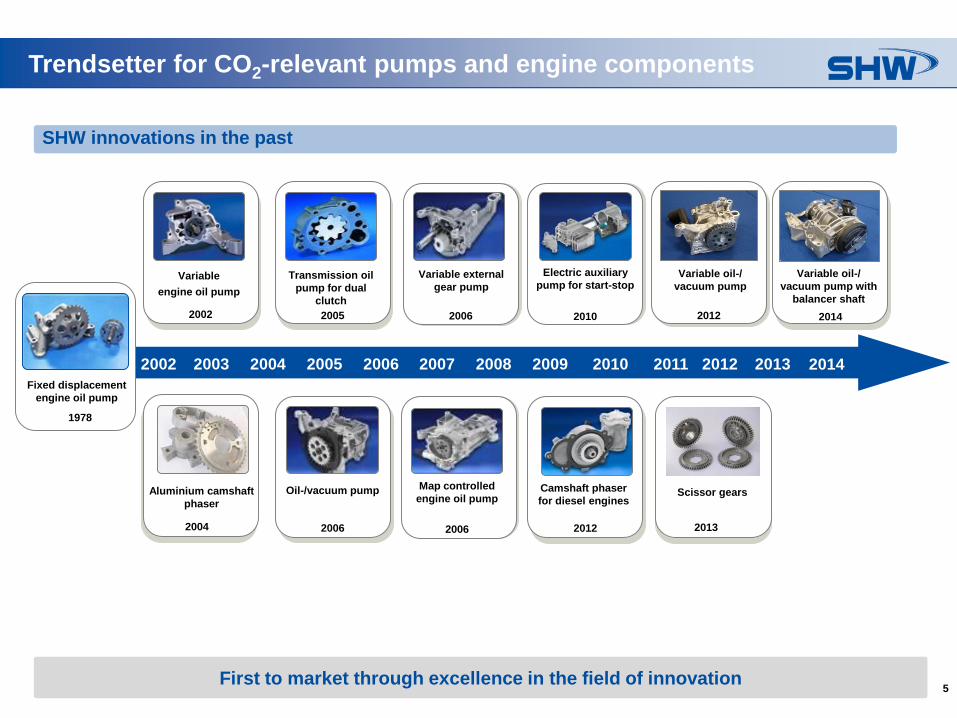

Trendsetter for CO2-relevant pumps and engine components

SHW innovations in the past

2010

Electric auxiliary

pump for start-stop

2006

Oil-/vacuum pump

2006

Map controlled

engine oil pump

2006

Variable external

gear pump

2002

Variable

engine oil pump

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fixed displacement

engine oil pump

First to market through excellence in the field of innovation

2004

Aluminium camshaft

phaser

2005

Transmission oil

pump for dual

clutch

2012

Camshaft phaser

for diesel engines

2012

Variable oil-/

vacuum pump

2013

Scissor gears

2014

Variable oil-/

vacuum pump with

balancer shaft

1978

2014

6Gaining market share with innovative capacity and product optimisation

Ongoing trendsetter for CO2-relevant automobile components

SHW innovations in the future

2015 CO2 reduction by lower weight, friction and input power as well as fully variable settings and hybrid concepts 2020

Gerotor

for plastic pump

2014

Fully variable vane

pump module

2nd generation

Valve integration Fully variable

cooling-fluid

pump

2014

Electrical pre-

feed-pump

for commercial

vehicles

Camshaft phaser

without pressure

vessel

2014

Variable oil pump

reduced friction and

weight

2014

Camshaft phaser

reduced mass inertiaElectrical trans-

mission oil pump

for hybrid vehicles for electric motor support

Electric auxiliary

pump for start-

stop-sailing

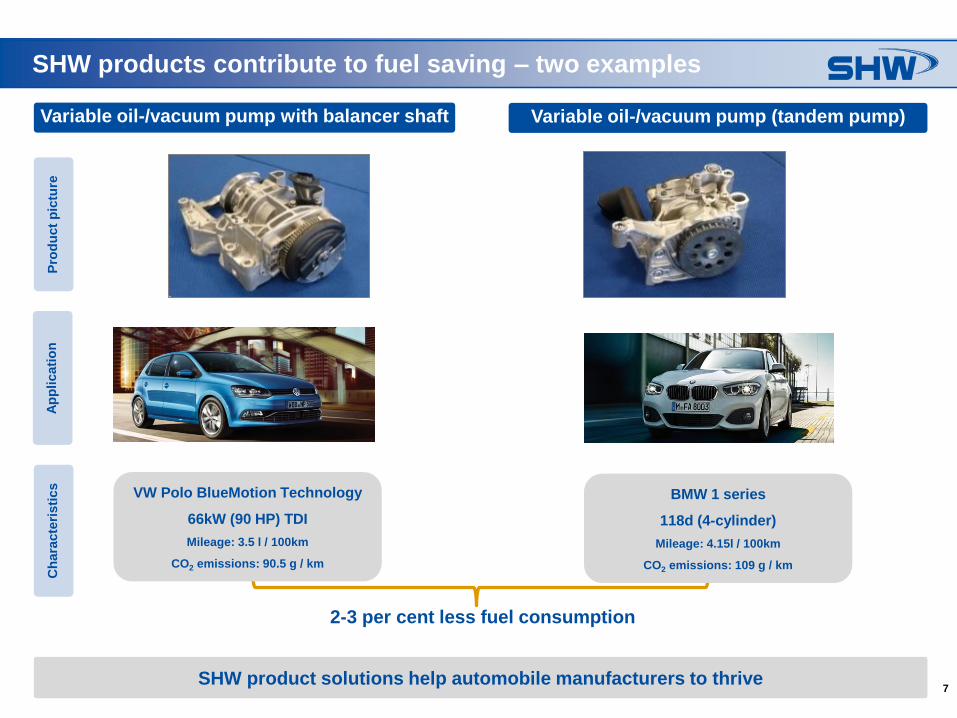

7SHW product solutions help automobile manufacturers to thrive

SHW products contribute to fuel saving – two examplesP

rod

uct

pic

ture

Variable oil-/vacuum pump (tandem pump)Variable oil-/vacuum pump with balancer shaft

Ap

plicati

on

Ch

ara

cte

risti

cs

2-3 per cent less fuel consumption

VW Polo BlueMotion Technology

66kW (90 HP) TDI

Mileage: 3.5 l / 100km

CO2 emissions: 90.5 g / km

BMW 1 series

118d (4-cylinder)

Mileage: 4.15l / 100km

CO2 emissions: 109 g / km

8Pioneer in oil pumps applications for hybrids

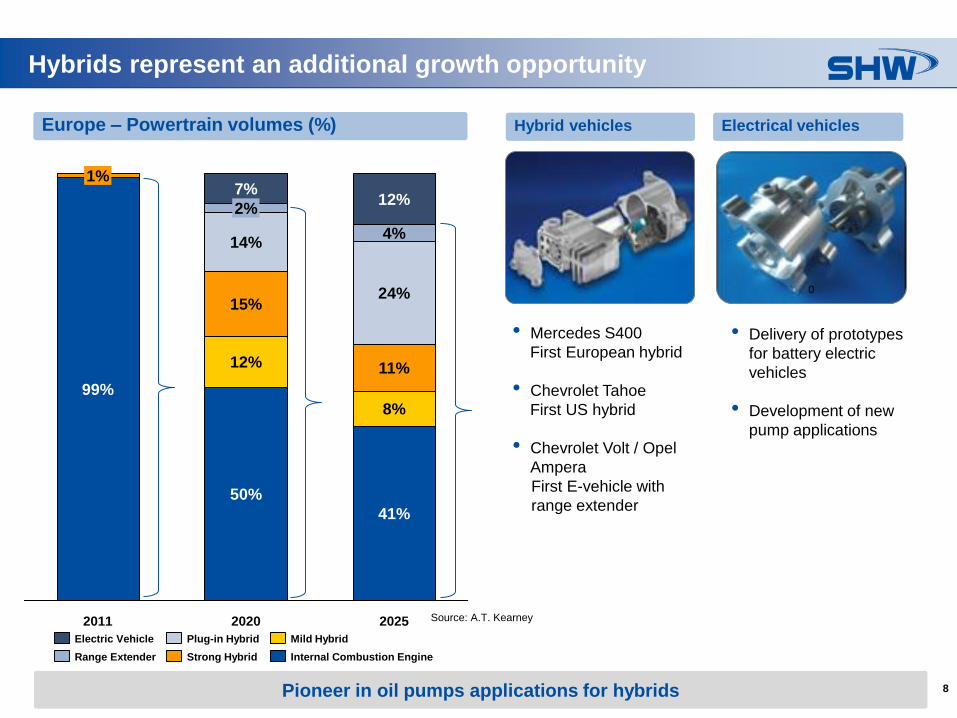

Hybrids represent an additional growth opportunity

Europe – Powertrain volumes (%)

2025

41%

8%

11%

24%

4%

12%

2020

50%

12%

15%

14%

2%

7%

2011

99%

1%

Internal Combustion Engine

Mild Hybrid

Strong Hybrid

Plug-in Hybrid

Range Extender

Electric Vehicle

Source: A.T. Kearney

Hybrid vehicles Electrical vehicles

0

• Mercedes S400

First European hybrid

• Chevrolet Tahoe

First US hybrid

• Chevrolet Volt / Opel

Ampera

First E-vehicle with

range extender

• Delivery of prototypes

for battery electric

vehicles

• Development of new

pump applications

9Oil-/vacuum pumps and camshaft phasers are major growth drivers in 2015

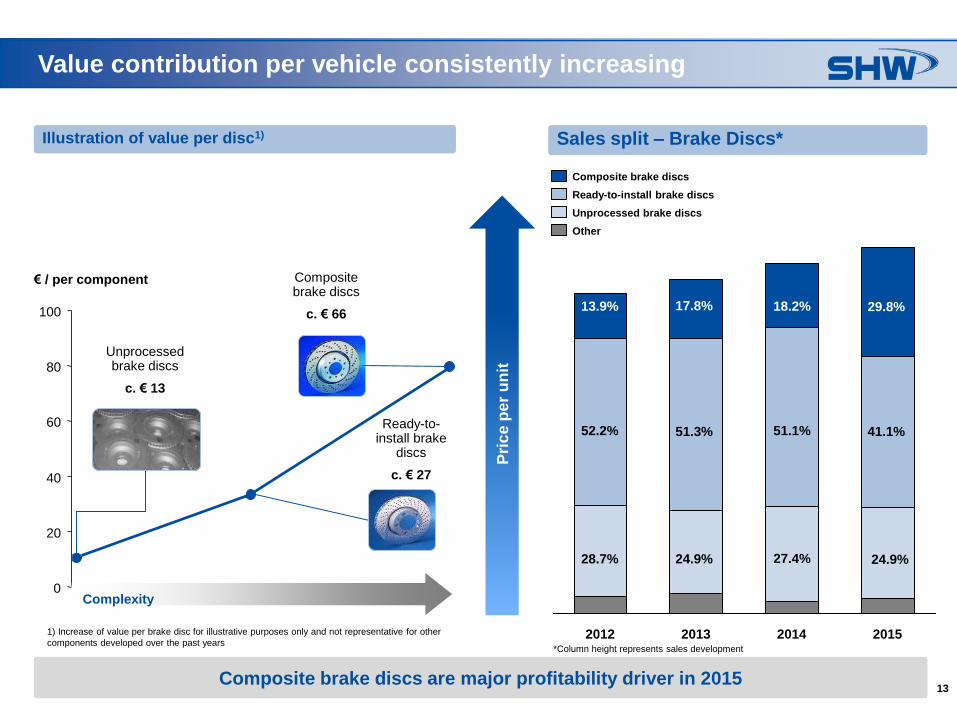

Value contribution per vehicle consistently increasing

1) Increase of value per pump for illustrative purposes only and not representative for other components

developed over the past years

Illustration of value per pump1)

0

20

40

60

80

100

Complexity

€ / per component

Fixed displacement

engine oil pump

c. € 12

Variable engine oil pump

c. € 20

Electric auxiliary oil pump for start-stop

c. € 70Variable oil-/

vacuum pump

c. € 38

Sales split – Pumps Passenger Cars*

Pri

ce

pe

r u

nit

2015201420132012

Camshaft phaser

Variable oil pumps

Fixed displacement pumps

Oil-/vacuum pumps

Transmission oil pumps

Other

34.0%

38.1%

13.9%

12.6%

24.6%

21.6%

35.5%

34.4%

19.5%

22.4%

18.8%

11.5%

11.8%10.7%

17.5%20.1%

31.5% 25.7%

12.0%

*Column height represents sales development

6.4%

4.0%

10

2008

Tube-disc

Trendsetter for CO2-relevant composite brake discs

SHW innovations

2005 2006 2007 2008 2009 2010 2011 2012 2013

SHW

composite disc

1993

Future focus lies on cost reduction by further automation of the production process

2007

Weight-optimized

disc

2010

Air-flow optimized

disc

2005

Riveted discs

2008

Friction-welded

disc

2012

Sheet-disc

2011

Hybrid-forged disc

2006

Ex-centrical

Bell-joint

2011

Hybrid-disc

2013

Wave disc

2014

Ford Mustang

lightweight

brake disc

2009

Metal-spinning

disc

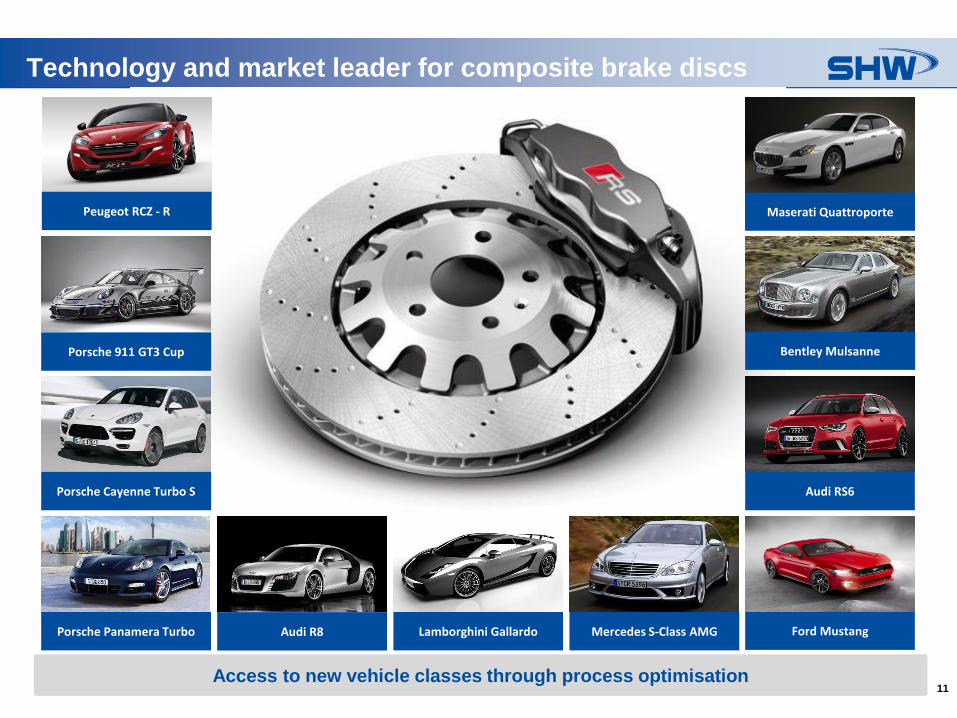

11Access to new vehicle classes through process optimisation

Technology and market leader for composite brake discs

Porsche 911 GT3 Cup

Porsche Cayenne Turbo S Audi RS6

Porsche Panamera Turbo Audi R8 Ford Mustang

Bentley Mulsanne

Mercedes S-Class AMGLamborghini Gallardo

Peugeot RCZ - R Maserati Quattroporte

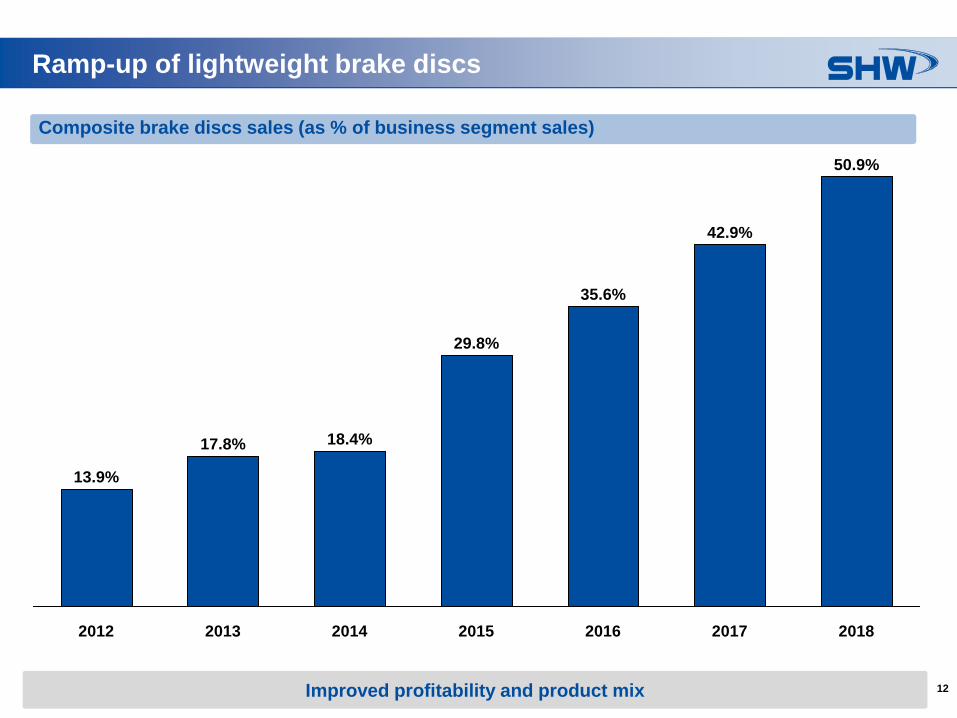

12Improved profitability and product mix

Ramp-up of lightweight brake discs

Composite brake discs sales (as % of business segment sales)

17.8% 18.4%

29.8%

2017 20182016

50.9%

42.9%

2015

35.6%

20142012

13.9%

2013

13Composite brake discs are major profitability driver in 2015

Value contribution per vehicle consistently increasing

Illustration of value per disc1)

0

20

40

60

80

100

€ / per component

Unprocessed brake discs

c. € 13

Ready-to-install brake

discs

c. € 27

Composite brake discs

c. € 66

Complexity

Sales split – Brake Discs*

Pri

ce

pe

r u

nit

2015201420132012

Other

Ready-to-install brake discs

Unprocessed brake discs

Composite brake discs

29.8%18.2%17.8%13.9%

41.1%51.1%51.3%52.2%

24.9%27.4%24.9%28.7%

1) Increase of value per brake disc for illustrative purposes only and not representative for other

components developed over the past years*Column height represents sales development

14

Internationalisation

15

16.0

20172016 2018

17.7

19.3 19.4

20192013

16.7

18.6

2015

3.2%

2014

17.7

Source: PwC Autofacts – January 2015

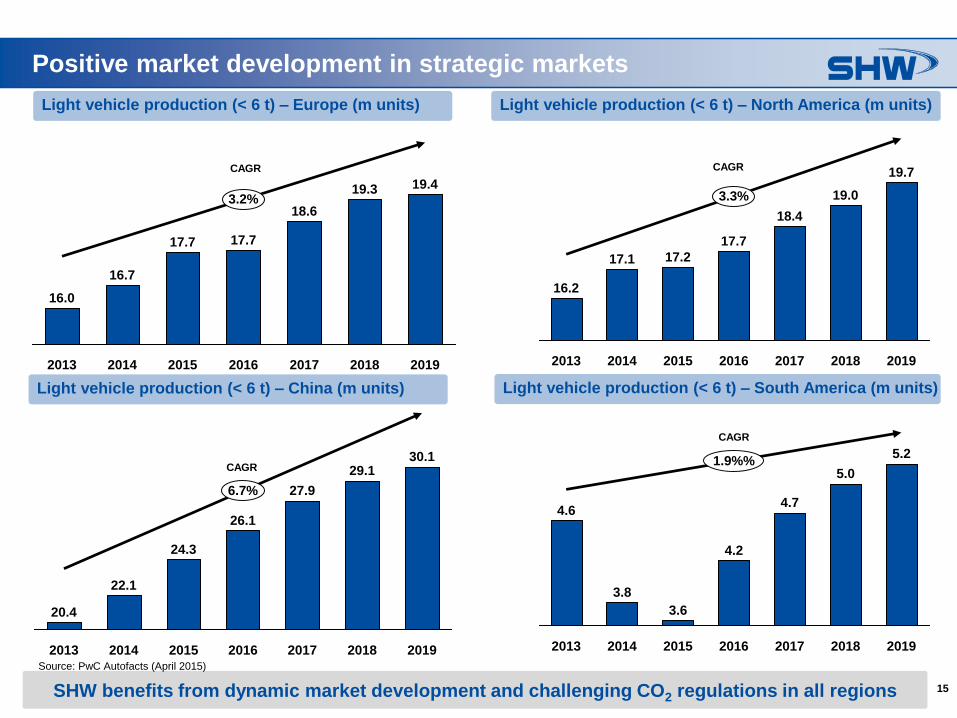

Positive market development in strategic markets

Light vehicle production (< 6 t) – Europe (m units) Light vehicle production (< 6 t) – North America (m units)

18.4

16.2

17.2

2019

3.3%

19.7

17.7

17.1

2017

19.0

2013 2014 20182015 2016

2019

30.1

24.3

6.7%

22.1

2013 2014

26.1

2015 2018

29.1

20172016

20.4

27.94.7

3.6

20192013 2015

4.6

1.9%%5.0

4.2

2014 2017

5.2

3.8

20182016

CAGR CAGR

CAGR

CAGR

Light vehicle production (< 6 t) – China (m units) Light vehicle production (< 6 t) – South America (m units)

SHW benefits from dynamic market development and challenging CO2 regulations in all regions

Source: PwC Autofacts (April 2015)

16

Presence established in strategic relevant markets

Serial production of oil pumps started in Brazil in June 2014

Bad Schussenried

Employees: 556

Wasseralfingen incl. HQ

Employees: 328

Neuhausen

Employees: 142

Tuttlingen

Employees: 236

Shanghai, China

Employees: 5

São Paulo, Brazil

Employees: 5

Detroit, U.S.

Employees: 1

Toronto, Canada

Employees: 5Status: 31.03.2015

17

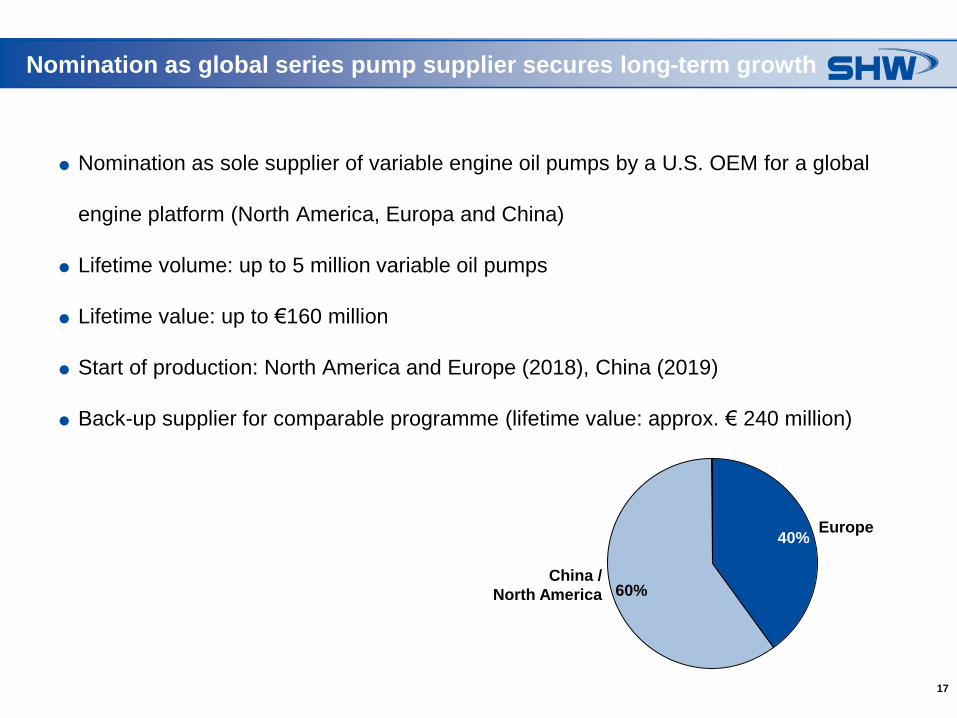

Nomination as global series pump supplier secures long-term growth

Nomination as sole supplier of variable engine oil pumps by a U.S. OEM for a global

engine platform (North America, Europa and China)

Lifetime volume: up to 5 million variable oil pumps

Lifetime value: up to €160 million

Start of production: North America and Europe (2018), China (2019)

Back-up supplier for comparable programme (lifetime value: approx. € 240 million)

40%

60%

Europe

China /

North America

18

Status internationalisation: Pumps and Engine Components

China:

Successful delivery of prototypes of electric auxiliary pumps for start-stop function

as well as transmission oil pumps for dual-clutch

Nomination as serial supplier shortly before completion

Active preparation for the start of serial production in the second half of 2015

Positive results expected promptly

Brazil:

In 2014 successful start of operation; 2015 seems to be characterised by a

challenging market environment

Europe:

• Intensified search for best cost country locations in South-Eastern and Eastern

Europe for capacity expansion

19

SHW Longji Brake Discs JV – a capital optimised cooperation

* Amount is based on the RMB/EUR exchange as of 27.01.2015

Chinese OEM market for quality brake discs offers significant growth potential

(Light vehicle production 2014 - 2019: increase by 40 per cent from 21.3 million to 29.9 million units)

Sino-Foreign Equity Joint Venture: SHW share (51 per cent)

Shandong Longji share (49 per cent)

Business focus: Ready-to-install brake discs for passenger cars and light commercial

vehicles (OEM/OES)

Total equity: RMB 215.5 million (approx. € 31.9 million*)

SHW: cash contribution splitted over two years

Shandong Longji: foundry plus associated machinery, equipment and land use rights

JV partner guarantees to fill the existing production capacity with fixed profit margin

Production capacity from existing aftermarket business will be shifted to OE

business as required SHW Longji

Brake Disc JV

Joint Venture profitable from day one

Capital efficient and profitable milestone of brake discs internationalisation

20

NAFTA:

Execution of numerous exploratory negotiations with potential cooperation partners to

exploit the market potential for lightweight brake discs in a capital efficient manner

China:

Joint Venture focuses on the production and supply of high quality, ready-to-install

brake discs to Chinese OEMs

Concrete customer enquiries received shortly after start of operation

Status internationalisation: Brake Discs

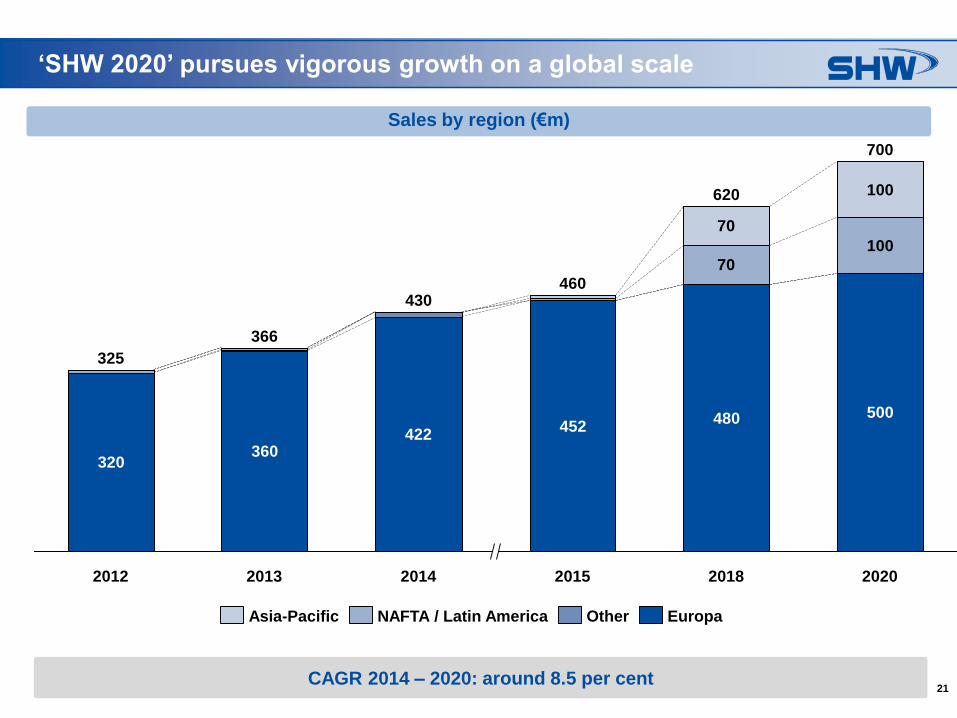

21CAGR 2014 – 2020: around 8.5 per cent

‘SHW 2020’ pursues vigorous growth on a global scale

320360

422452

480 500

100

70

100

70

366

2012

325

2018

620

2015

460

2014

430

700

2013 2020

NAFTA / Latin America OtherAsia-Pacific Europa

Sales by region (€m)

22

Financials

23

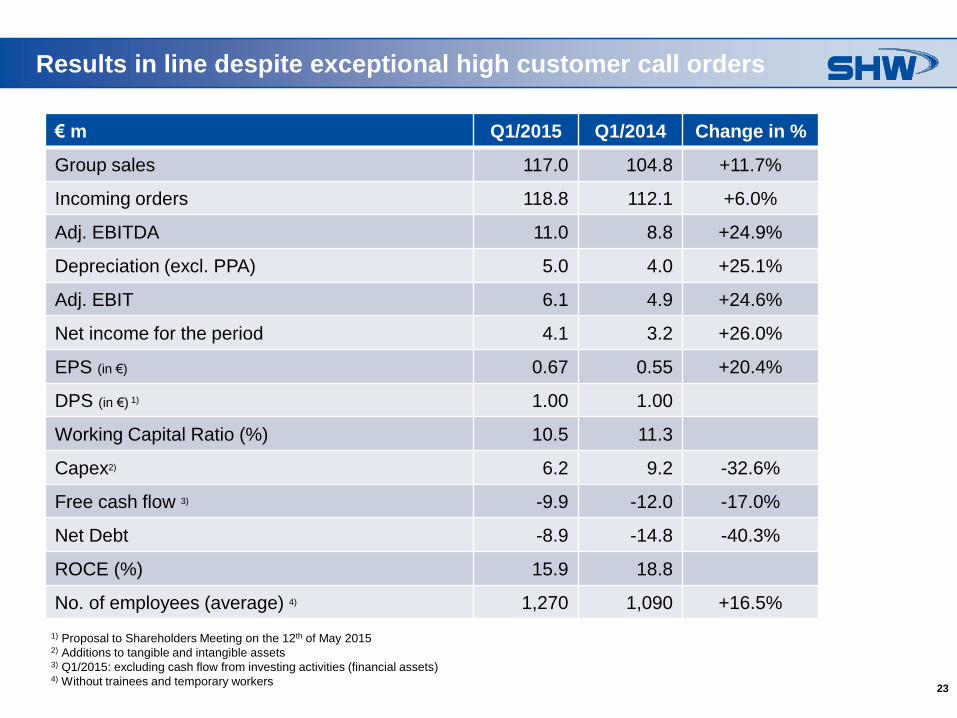

Results in line despite exceptional high customer call orders

€ m Q1/2015 Q1/2014 Change in %

Group sales 117.0 104.8 +11.7%

Incoming orders 118.8 112.1 +6.0%

Adj. EBITDA 11.0 8.8 +24.9%

Depreciation (excl. PPA) 5.0 4.0 +25.1%

Adj. EBIT 6.1 4.9 +24.6%

Net income for the period 4.1 3.2 +26.0%

EPS (in €) 0.67 0.55 +20.4%

DPS (in €) 1) 1.00 1.00

Working Capital Ratio (%) 10.5 11.3

Capex2) 6.2 9.2 -32.6%

Free cash flow 3) -9.9 -12.0 -17.0%

Net Debt -8.9 -14.8 -40.3%

ROCE (%) 15.9 18.8

No. of employees (average) 4) 1,270 1,090 +16.5%

1) Proposal to Shareholders Meeting on the 12th of May 20152) Additions to tangible and intangible assets3) Q1/2015: excluding cash flow from investing activities (financial assets)4) Without trainees and temporary workers

24

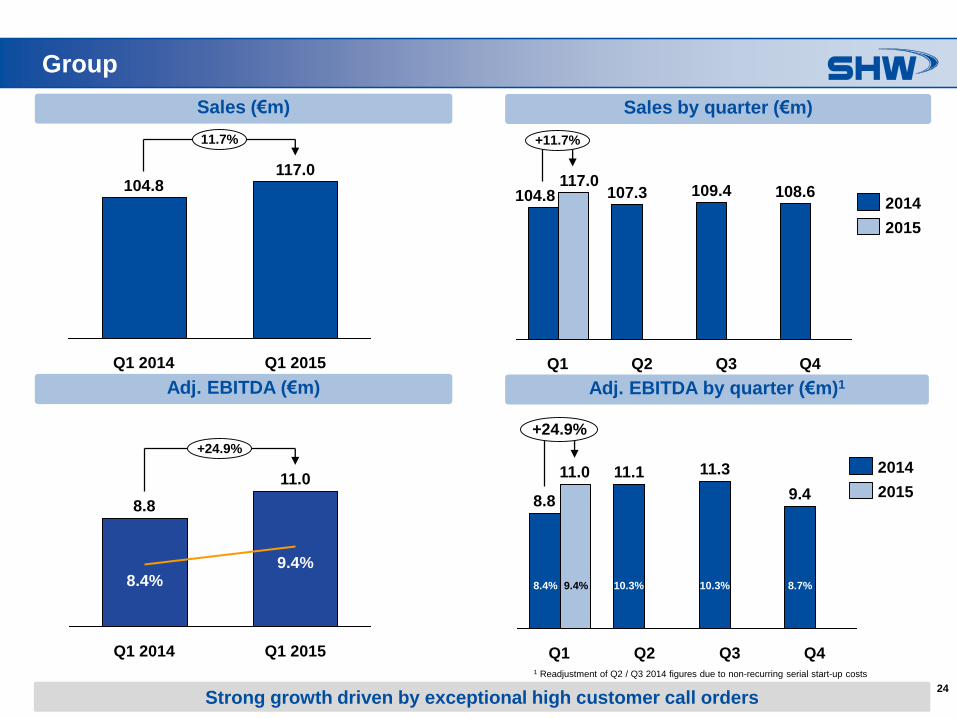

Group

Sales by quarter (€m)

+11.7%

Q4

108.6

Q3

109.4

Q2

107.3

Q1

117.0104.8

2015

2014

11.7%

Q1 2015

117.0

Q1 2014

104.8

Sales (€m)

Strong growth driven by exceptional high customer call orders

Q3

11.3

Q2

11.1

Q1

11.0

8.8

Q4

9.4

+24.9%

2015

2014

Adj. EBITDA (€m) Adj. EBITDA by quarter (€m)1

11.0

9.4%

Q1 2014

8.8

8.4%

+24.9%

Q1 20151 Readjustment of Q2 / Q3 2014 figures due to non-recurring serial start-up costs

8.4% 10.3% 10.3% 8.7%9.4%

25

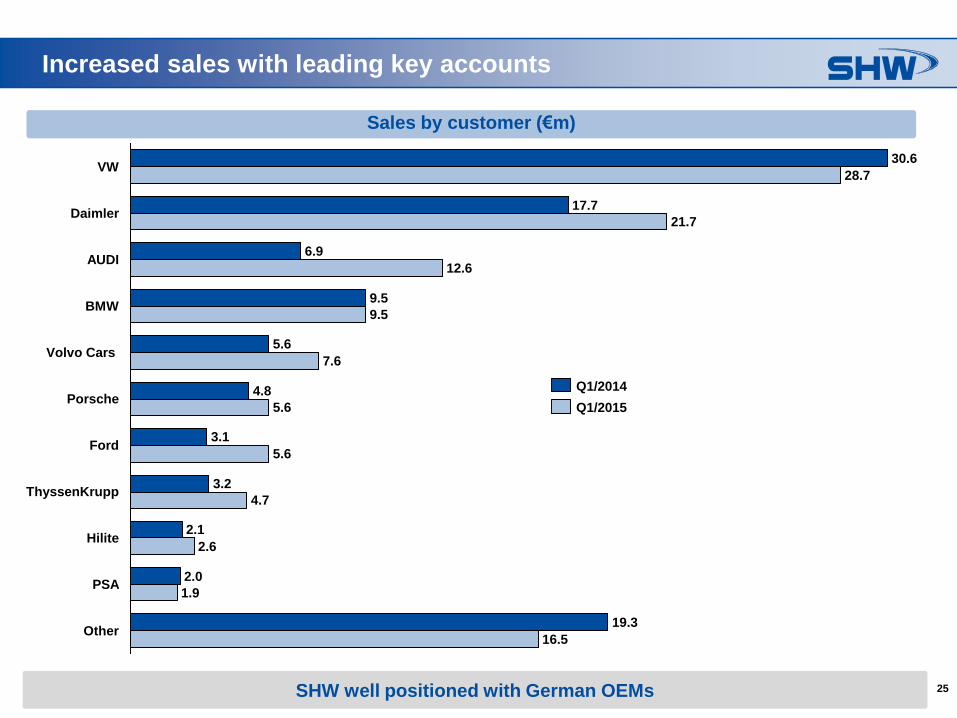

Increased sales with leading key accounts

14.7

1.9

14.7

2.2

14.7 17.5

2.3

2.2

14.7 17.5

2.3

Sales by customer (€m)

SHW well positioned with German OEMs

12.6

Porsche

3.1

5.6

16.5Other

19.3

PSA1.9

2.0

Hilite2.6

2.1

ThyssenKrupp4.7

3.2

6.9

5.6

4.8

Volvo Cars7.6

5.6

BMW9.5

9.5

Daimler21.7

17.7

VW28.7

30.6

Ford

AUDI

Q1/2015

Q1/2014

26

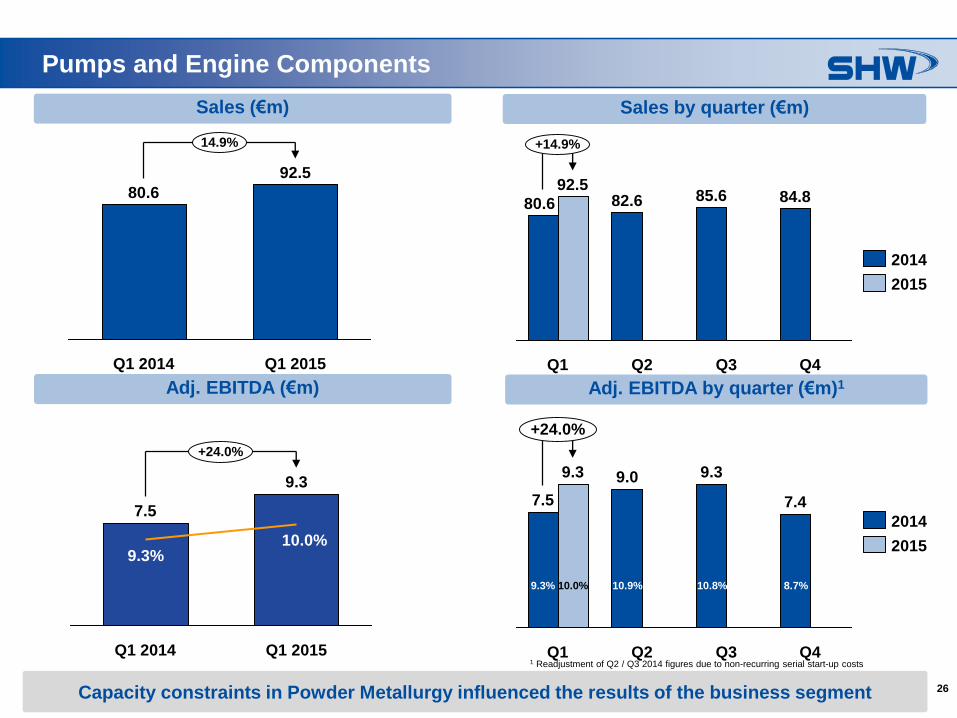

Pumps and Engine Components

Sales by quarter (€m)

+14.9%

Q4

84.8

Q1

80.6

92.582.6

Q3

85.6

Q2

2014

2015

Sales (€m)

9.3 9.0

7.4

9.3

Q2

7.5

Q3 Q4Q1

+24.0%

2014

2015

Adj. EBITDA (€m) Adj. EBITDA by quarter (€m)1

7.5

9.3

Q1 2014

9.3%

+24.0%

10.0%

Q1 2015

14.9%

Q1 2015

92.5

Q1 2014

80.6

Capacity constraints in Powder Metallurgy influenced the results of the business segment

1 Readjustment of Q2 / Q3 2014 figures due to non-recurring serial start-up costs

9.3% 10.9% 10.8% 8.7%10.0%

27

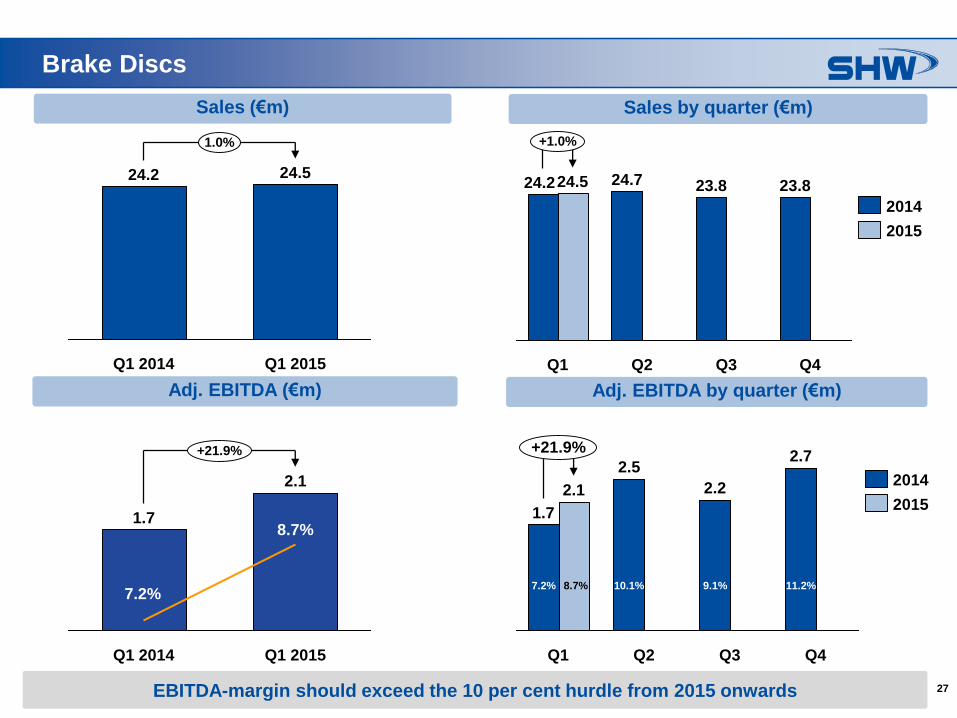

Brake Discs

Sales by quarter (€m)

23.8

Q4

+1.0%

Q3

24.7

Q1

24.5

Q2

23.824.2

Sales (€m)

2.1

1.7

Q4Q2

2.5

Q1

2.2

Q3

2.7+21.9%

Adj. EBITDA (€m) Adj. EBITDA by quarter (€m)

2014

2015

2015

2014

7.2%

1.7

Q1 2014

8.7%

2.1

Q1 2015

+21.9%

24.2

Q1 2014 Q1 2015

1.0%

24.5

EBITDA-margin should exceed the 10 per cent hurdle from 2015 onwards

7.2% 10.1% 9.1% 11.2%8.7%

28

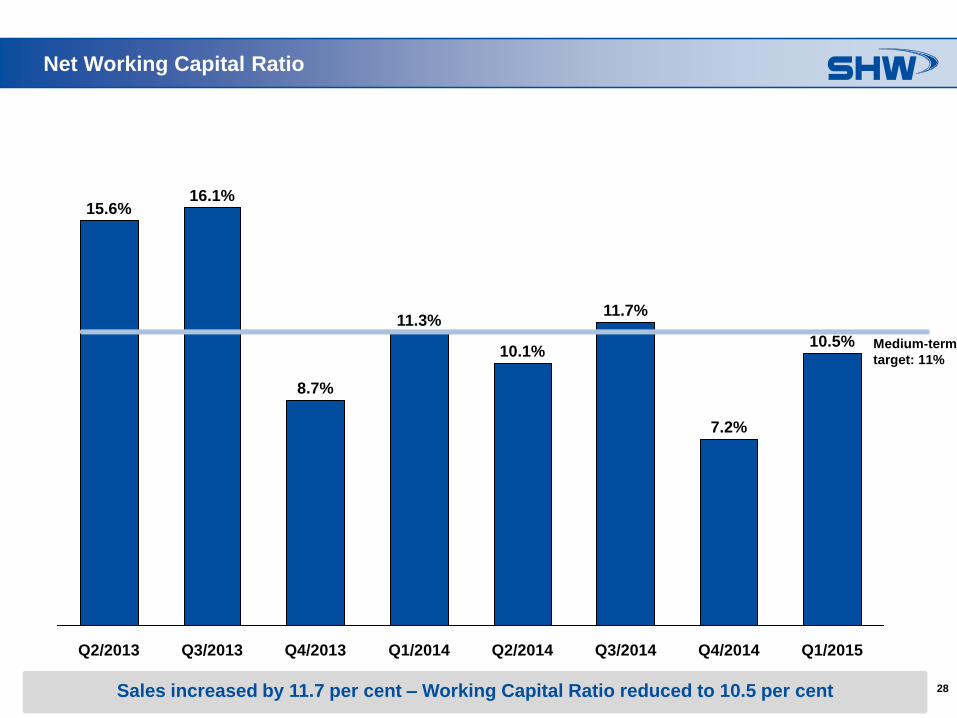

Net Working Capital Ratio

Q3/2013

11.3%

10.1%

7.2%

11.7%

15.6%

Q2/2013

8.7%

Q1/2014 Q4/2014 Q1/2015Q3/2014Q2/2014

16.1%

Q4/2013

10.5%

Sales increased by 11.7 per cent – Working Capital Ratio reduced to 10.5 per cent

Medium-term

target: 11%

29

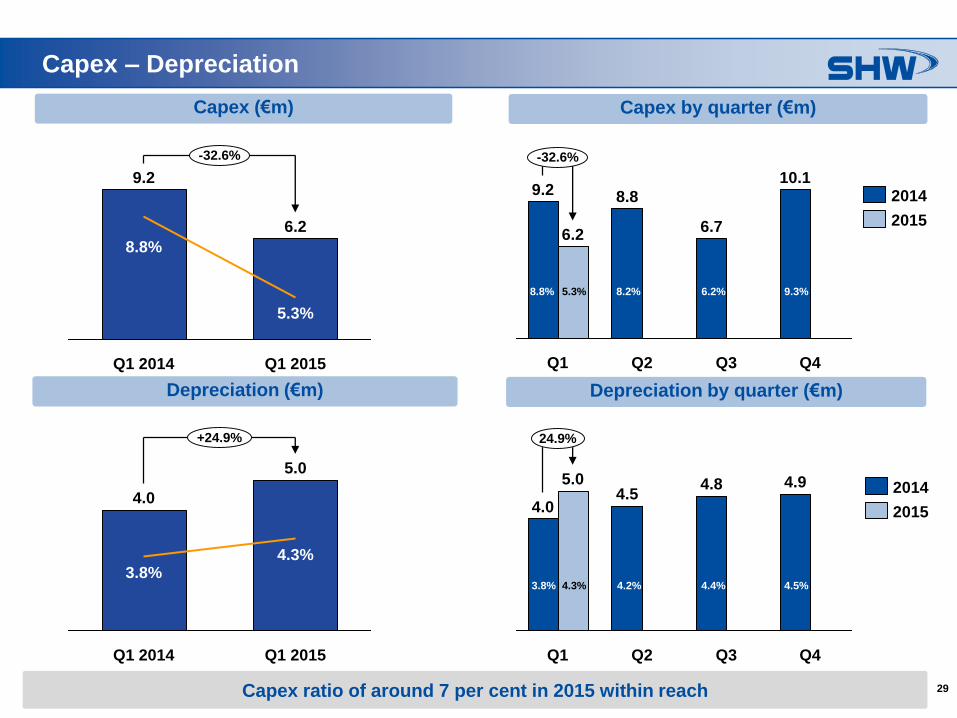

Capex – Depreciation

14.714.7

Capex by quarter (€m)

Q3

6.2

8.8

Q1

-32.6%

9.2

6.7

10.1

Q2 Q4

2014

2015

Capex (€m)

4.0

5.0

Q3

4.9

Q4

24.9%

Q1 Q2

4.84.5

Depreciation (€m) Depreciation by quarter (€m)

2014

2015

8.8%

5.3%

-32.6%

Q1 2015

6.2

Q1 2014

9.2

Q1 2014

4.3%

5.0

+24.9%

4.0

Q1 2015

3.8%

Capex ratio of around 7 per cent in 2015 within reach

3.8% 4.2% 4.4% 4.5%4.3%

8.8% 8.2% 6.2% 9.3%5.3%

30

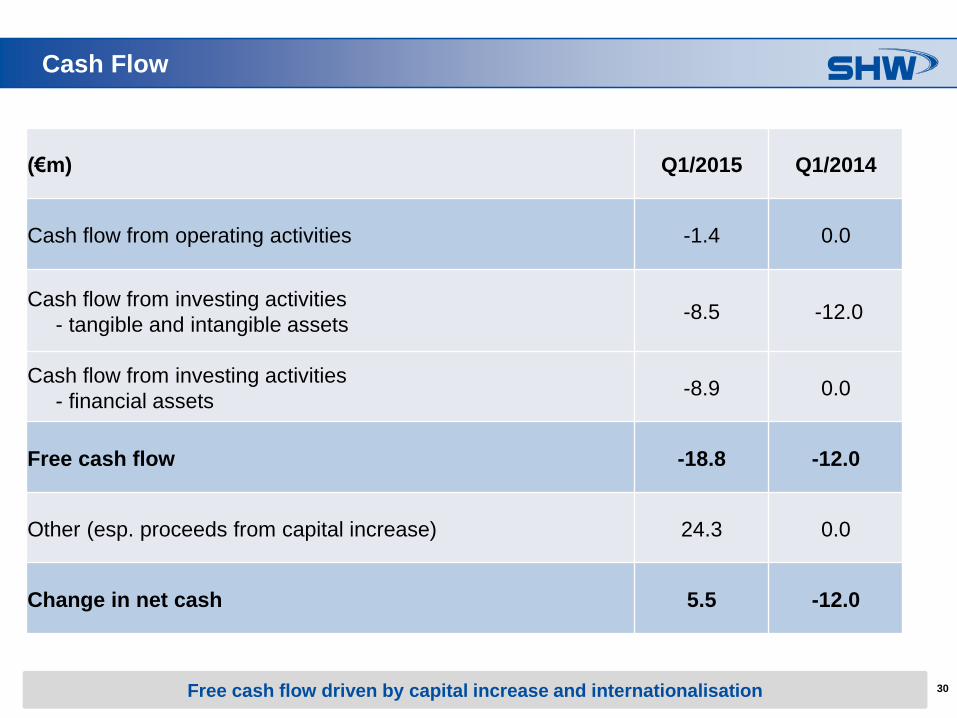

Cash Flow

5.(€m) Q1/2015 Q1/2014

Cash flow from operating activities -1.4 0.0

Cash flow from investing activities

- tangible and intangible assets-8.5 -12.0

Cash flow from investing activities

- financial assets-8.9 0.0

Free cash flow -18.8 -12.0

Other (esp. proceeds from capital increase) 24.3 0.0

Change in net cash 5.5 -12.0

Free cash flow driven by capital increase and internationalisation

31

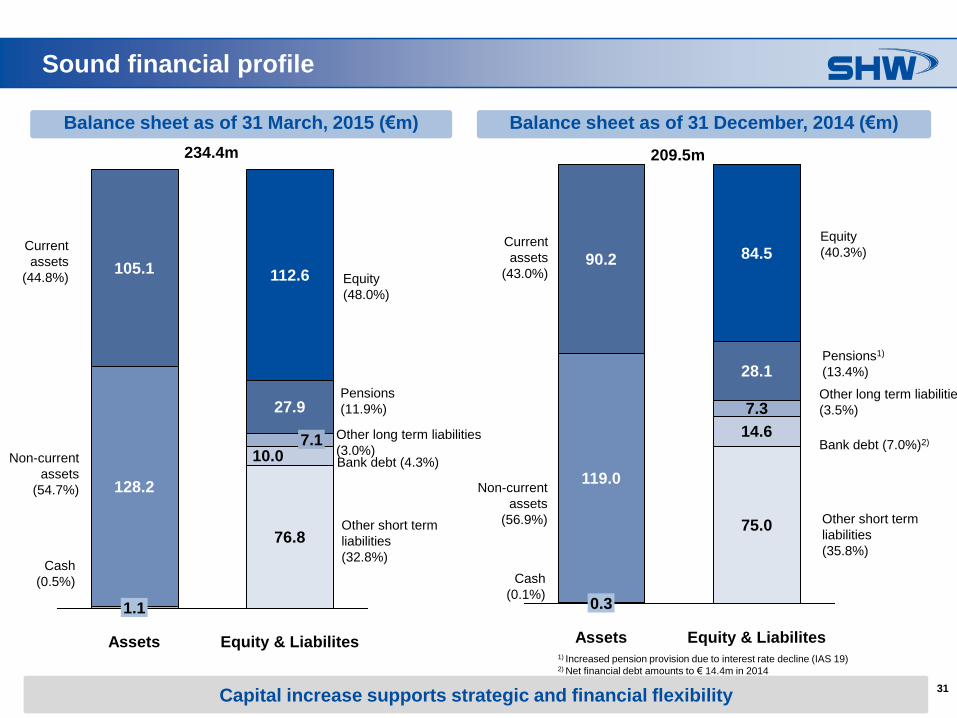

Sound financial profile

Balance sheet as of 31 March, 2015 (€m) Balance sheet as of 31 December, 2014 (€m)

Other short term

liabilities

(35.8%)

Pensions1)

(13.4%)

Current

assets

(43.0%)

Non-current

assets

(56.9%)

Equity

(40.3%)

37.9

209.5m

Equity & Liabilites

75.0

14.6

7.3

28.1

84.5

Assets

0.3

119.0

90.2

Cash

(0.1%)

Other long term liabilities

(3.5%)

Bank debt (7.0%)2)

Capital increase supports strategic and financial flexibility

1) Increased pension provision due to interest rate decline (IAS 19)2) Net financial debt amounts to € 14.4m in 2014

Equity & Liabilites

76.8

10.07.1

27.9

112.6

Assets

1.1

128.2

105.1

Current

assets

(44.8%)

Non-current

assets

(54.7%)

Cash

(0.5%)

Equity

(48.0%)

Pensions

(11.9%)

Other long term liabilities

(3.0%)Bank debt (4.3%)

Other short term

liabilities

(32.8%)

234.4m

32

Outlook – forward going with vigour and consistency

33

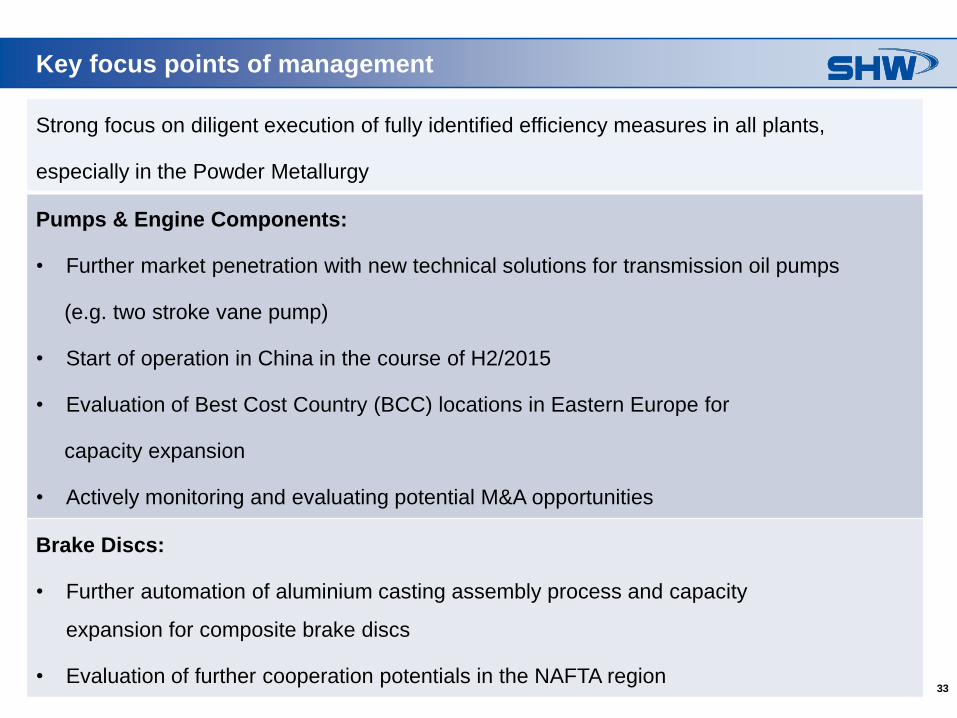

Key focus points of management

Strong focus on diligent execution of fully identified efficiency measures in all plants,

especially in the Powder Metallurgy

Pumps & Engine Components:

• Further market penetration with new technical solutions for transmission oil pumps

(e.g. two stroke vane pump)

• Start of operation in China in the course of H2/2015

• Evaluation of Best Cost Country (BCC) locations in Eastern Europe for

capacity expansion

• Actively monitoring and evaluating potential M&A opportunities

Brake Discs:

• Further automation of aluminium casting assembly process and capacity

expansion for composite brake discs

• Evaluation of further cooperation potentials in the NAFTA region

34

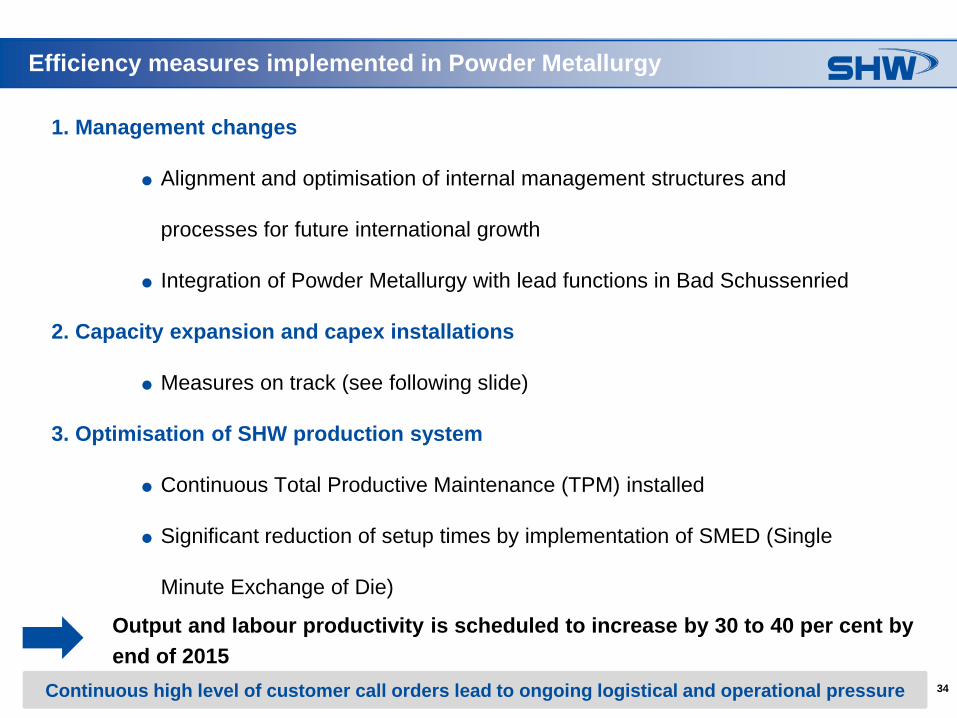

Efficiency measures implemented in Powder Metallurgy

1. Management changes

Alignment and optimisation of internal management structures and

processes for future international growth

Integration of Powder Metallurgy with lead functions in Bad Schussenried

2. Capacity expansion and capex installations

Measures on track (see following slide)

3. Optimisation of SHW production system

Continuous Total Productive Maintenance (TPM) installed

Significant reduction of setup times by implementation of SMED (Single

Minute Exchange of Die)

Output and labour productivity is scheduled to increase by 30 to 40 per cent by

end of 2015

Continuous high level of customer call orders lead to ongoing logistical and operational pressure

35

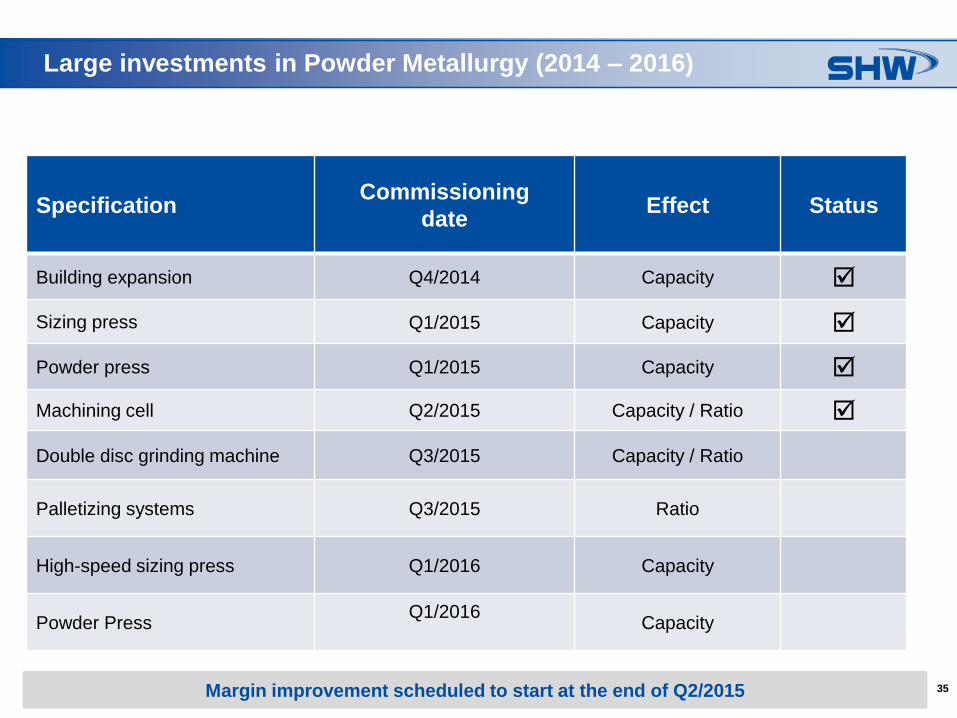

Large investments in Powder Metallurgy (2014 – 2016)

SpecificationCommissioning

dateEffect Status

Building expansion Q4/2014 Capacity

Sizing press Q1/2015 Capacity

Powder press Q1/2015 Capacity

Machining cell Q2/2015 Capacity / Ratio

Double disc grinding machine Q3/2015 Capacity / Ratio

Palletizing systems Q3/2015 Ratio

High-speed sizing press Q1/2016 Capacity

Powder PressQ1/2016

Capacity

Margin improvement scheduled to start at the end of Q2/2015

36

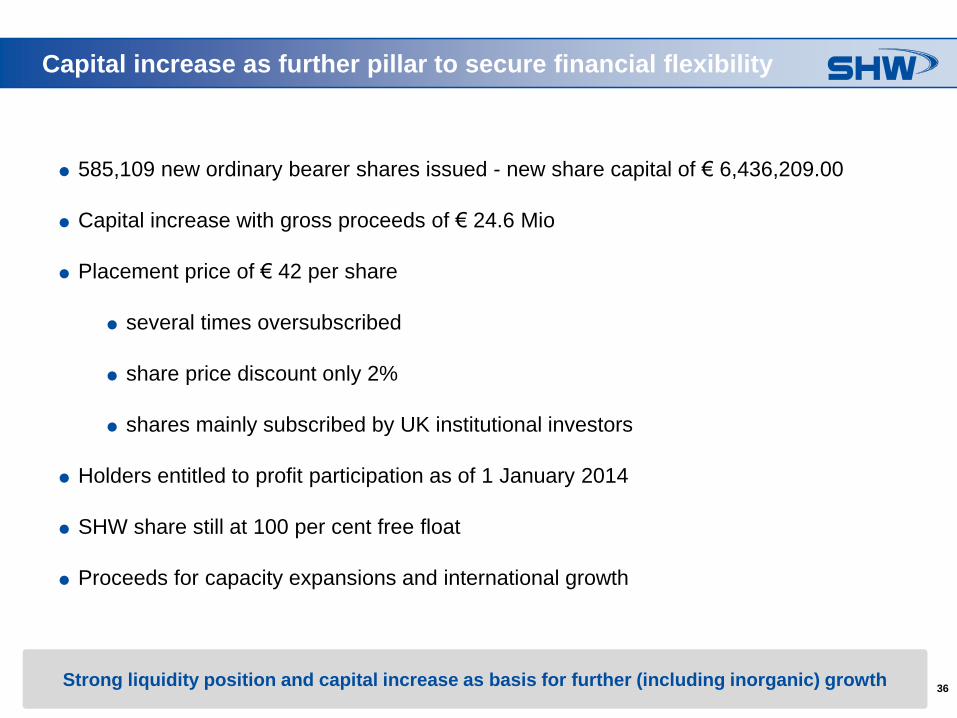

Capital increase as further pillar to secure financial flexibility

585,109 new ordinary bearer shares issued - new share capital of € 6,436,209.00

Capital increase with gross proceeds of € 24.6 Mio

Placement price of € 42 per share

several times oversubscribed

share price discount only 2%

shares mainly subscribed by UK institutional investors

Holders entitled to profit participation as of 1 January 2014

SHW share still at 100 per cent free float

Proceeds for capacity expansions and international growth

Strong liquidity position and capital increase as basis for further (including inorganic) growth

37

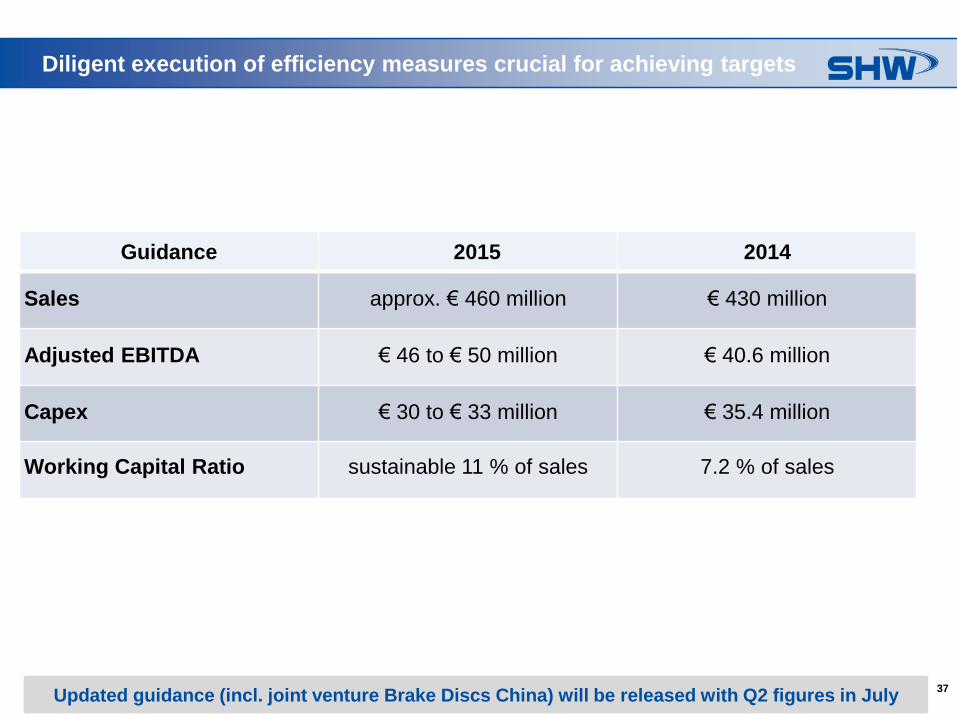

Diligent execution of efficiency measures crucial for achieving targets

Guidance 2015 2014

Sales approx. € 460 million € 430 million

Adjusted EBITDA € 46 to € 50 million € 40.6 million

Capex € 30 to € 33 million € 35.4 million

Working Capital Ratio sustainable 11 % of sales 7.2 % of sales

Updated guidance (incl. joint venture Brake Discs China) will be released with Q2 figures in July

38

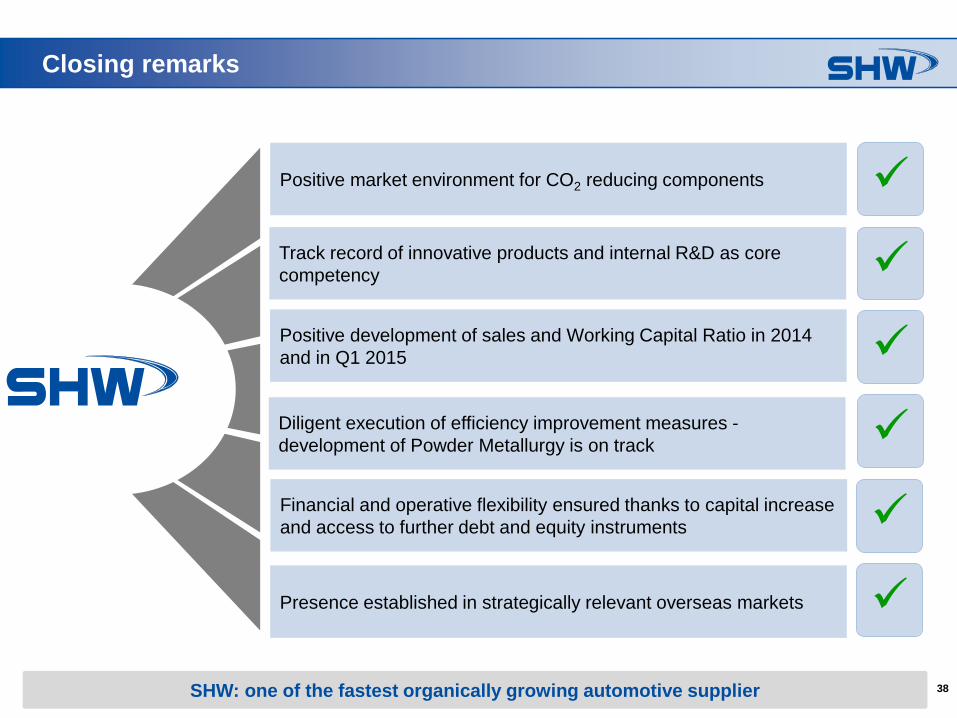

Closing remarks

Positive market environment for CO2 reducing components

Track record of innovative products and internal R&D as core

competency

Positive development of sales and Working Capital Ratio in 2014

and in Q1 2015

Diligent execution of efficiency improvement measures -

development of Powder Metallurgy is on track

Financial and operative flexibility ensured thanks to capital increase

and access to further debt and equity instruments

Presence established in strategically relevant overseas markets

SHW: one of the fastest organically growing automotive supplier

39

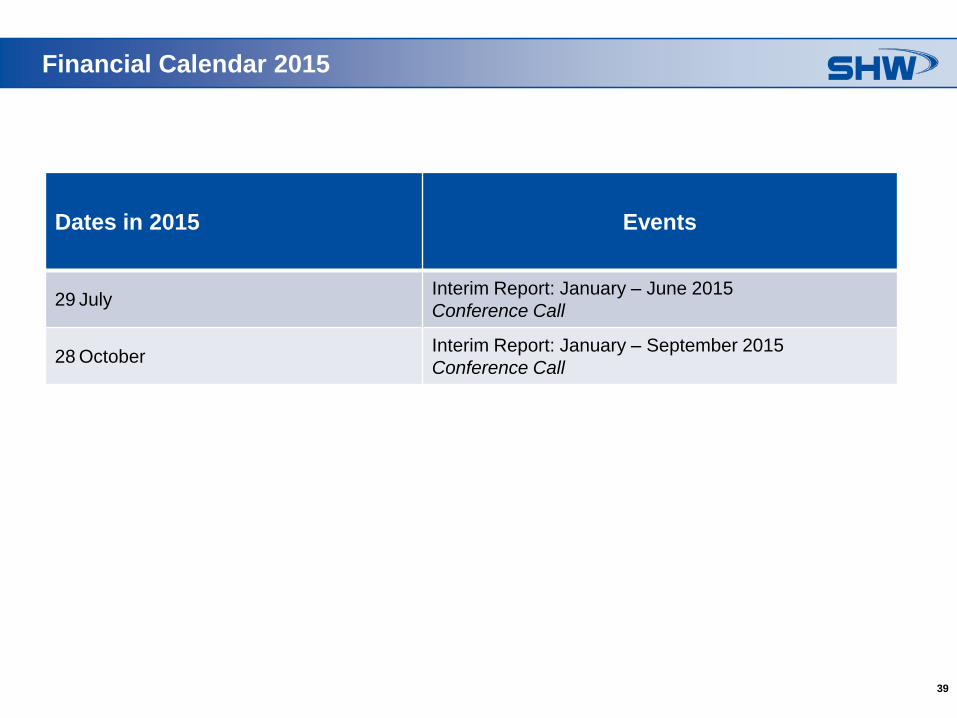

Financial Calendar 2015

Dates in 2015 Events

29 JulyInterim Report: January – June 2015

Conference Call

28 October Interim Report: January – September 2015

Conference Call

40

Michael SchicklingHead of Investor Relations & Corporate Communications

Telephone: +49 (0) 7361 502-462

E-Mail: [email protected]

Anja K. SiehlerSenior Manager Investor Relations & Corporate

Communications

Telephone: +49 (0) 7361 502-469

E-Mail: [email protected]

Contact Investor Relations

41

Back-up

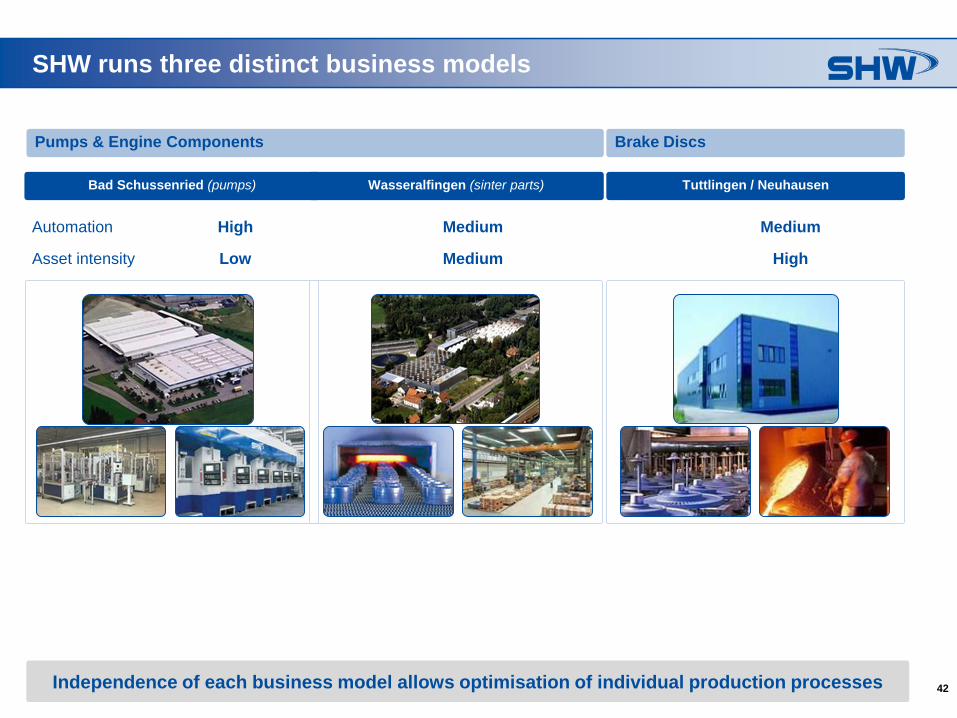

42Independence of each business model allows optimisation of individual production processes

SHW runs three distinct business models

Brake DiscsPumps & Engine Components

Asset intensity MediumLow High

Bad Schussenried (pumps) Wasseralfingen (sinter parts) Tuttlingen / Neuhausen

Automation High Medium Medium

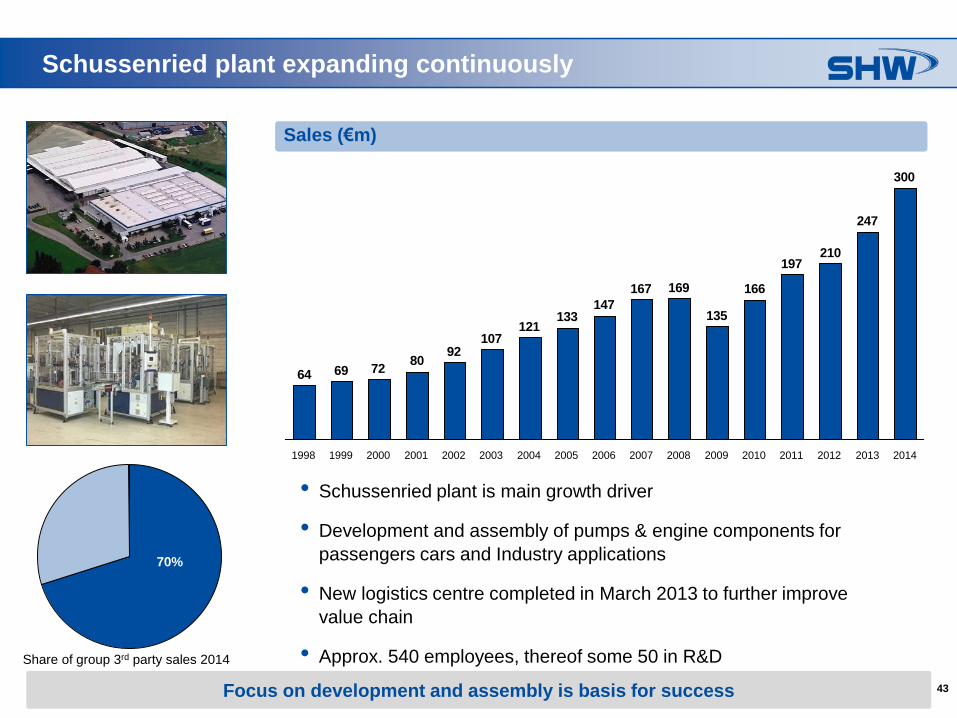

43Focus on development and assembly is basis for success

Schussenried plant expanding continuously

• Schussenried plant is main growth driver

• Development and assembly of pumps & engine components for

passengers cars and Industry applications

• New logistics centre completed in March 2013 to further improve

value chain

• Approx. 540 employees, thereof some 50 in R&D

300

247

210197

166

135

169167

147133

121107

9280

726964

2004200320022001200019991998 201320122011201020092008200720062005 2014

Sales (€m)

Share of group 3rd party sales 2014

70%

44

Wasseralfingen plant: production of sinter metal components

• Press - Sinter - Sizing produces near net shape

components, ready for assembly with minimum or no

machining

• Steel and aluminium sinter components for engines

and transmissions

• Approx. 290 employees excl. Corporate Functions

• 38 employees in Corporate Center (Finance, Tax,

Legal and Human Resources)

7%

Continuous high level of customer call orders led to ongoing logistical and operational pressure

Share of 3rd party sales 2014

45

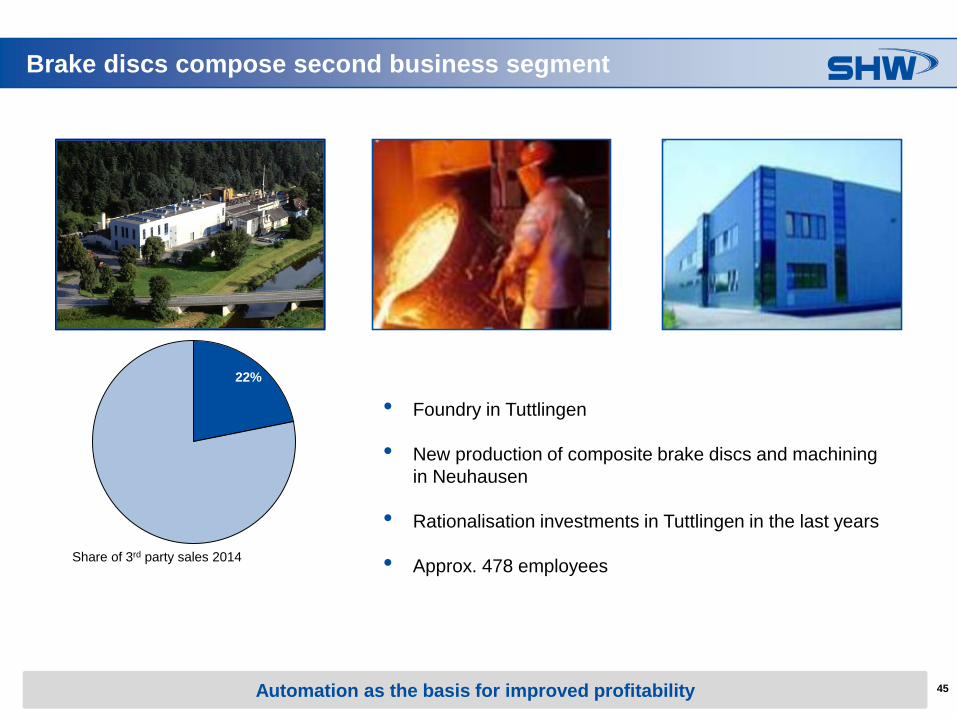

Brake discs compose second business segment

• Foundry in Tuttlingen

• New production of composite brake discs and machining

in Neuhausen

• Rationalisation investments in Tuttlingen in the last years

• Approx. 478 employees

22%

Automation as the basis for improved profitability

Share of 3rd party sales 2014

46

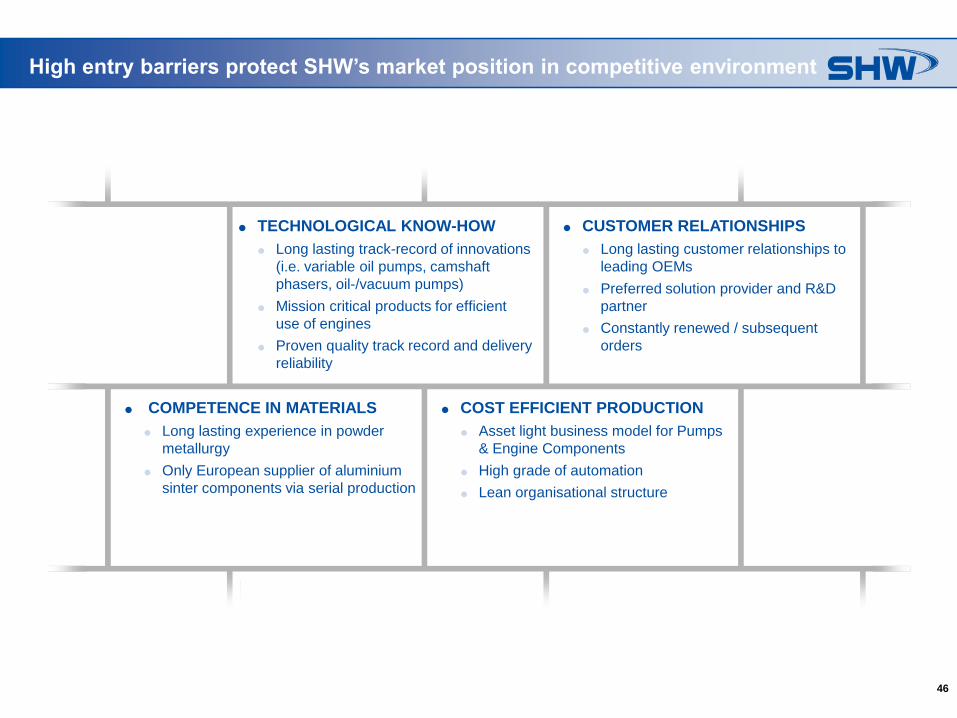

CUSTOMER RELATIONSHIPS

Long lasting customer relationships to

leading OEMs

Preferred solution provider and R&D

partner

Constantly renewed / subsequent

orders

TECHNOLOGICAL KNOW-HOW

Long lasting track-record of innovations

(i.e. variable oil pumps, camshaft

phasers, oil-/vacuum pumps)

Mission critical products for efficient

use of engines

Proven quality track record and delivery

reliability

COST EFFICIENT PRODUCTION

Asset light business model for Pumps

& Engine Components

High grade of automation

Lean organisational structure

COMPETENCE IN MATERIALS

Long lasting experience in powder

metallurgy

Only European supplier of aluminium

sinter components via serial production

High entry barriers protect SHW’s market position in competitive environment

47

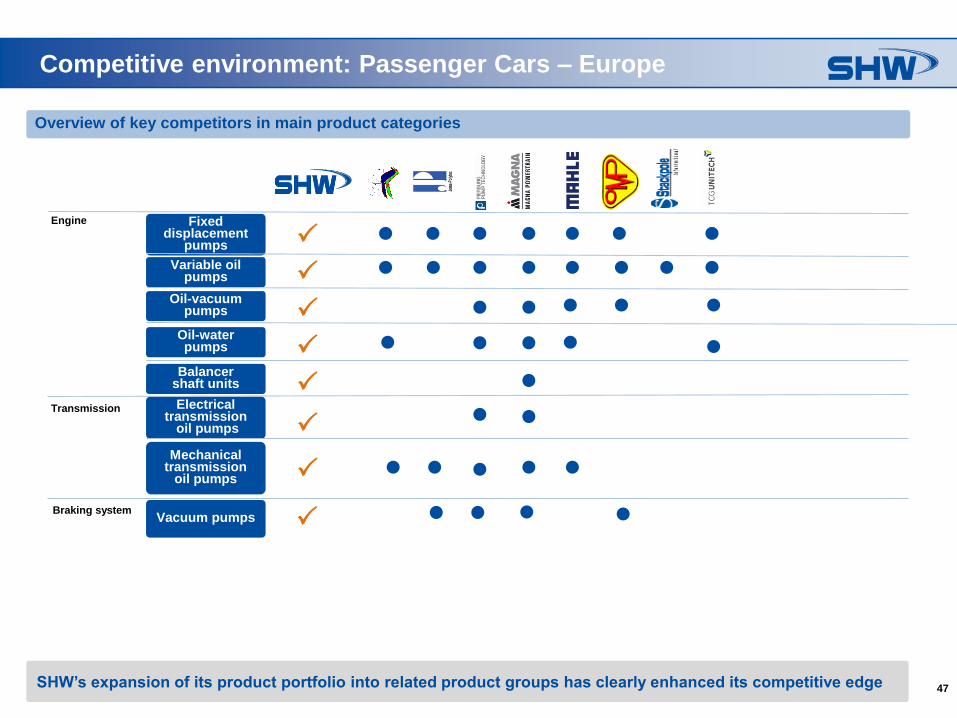

Competitive environment: Passenger Cars – Europe

Overview of key competitors in main product categories

Fixed displacement

pumps

Variable oil pumps

Oil-vacuum pumps

Oil-water pumps

Balancer shaft units

Electrical transmission

oil pumps

Mechanical transmission

oil pumps

SHW’s expansion of its product portfolio into related product groups has clearly enhanced its competitive edge

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

P

P

P

P

P

P

P

Vacuum pumps P

Engine

Transmission

Braking system

48

Competitive environment: Passenger Cars – North America

Overview of key competitors in main product categories

Fixed displacement

pumps

Variable oil pumps

Oil-vacuum pumps

Oil-water pumps

Balancer shaft units

Electrical transmission

oil pumps

Mechanical transmission

oil pumps

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

P

P

P

P

P

P

P

Vacuum pumps P

Engine

Transmission

Braking system

49

Competitive environment: Truck & Off-Highway

Overview of key competitors in main product categories

Engine oil pumps

Transmission oil pumps

Fuel pumps

Engine oil pumps

Transmission oil pumps

Fuel pumps

Engine oil pumps

Transmission oil pumps

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

P

P

P

P

P

P

P

Fuel pumps

Agricultural /

Construction

vehicles

Trucks

Stationary

engines

P

50

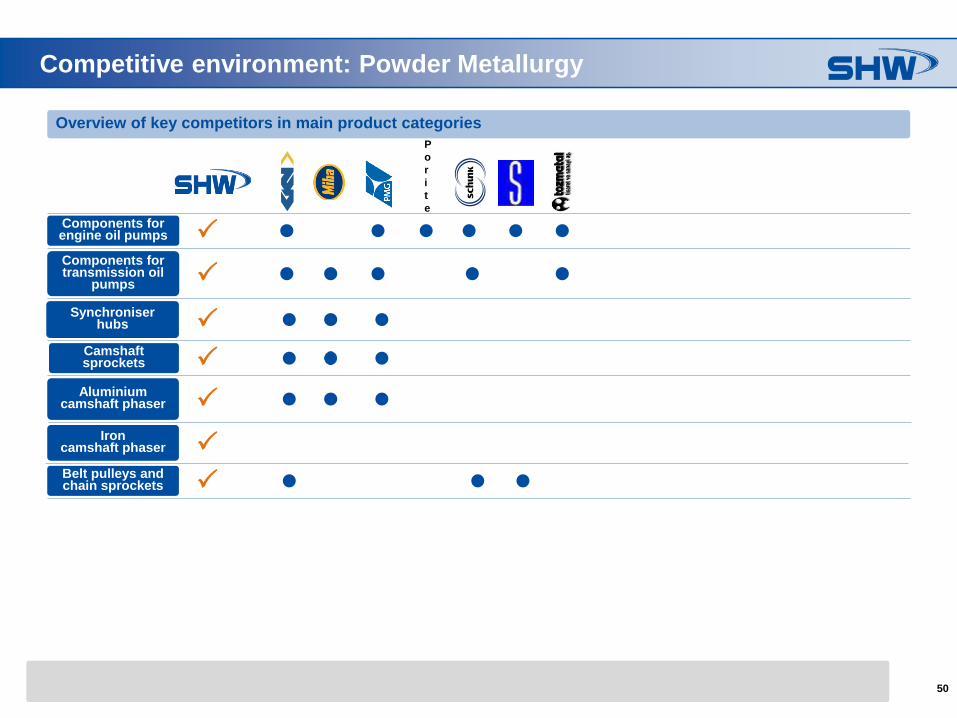

Competitive environment: Powder Metallurgy

Overview of key competitors in main product categories

Components for engine oil pumps

Components for transmission oil

pumps

Synchroniser hubs

Camshaftsprockets

Aluminium camshaft phaser

Iron camshaft phaser

Belt pulleys and chain sprockets

Sales (€m)

(Year)

290

(2010a)n/a n/a

4,693

(2009)n/a

213

(2009)

31

(2009)

12,117

(2009)

3,864

(2009)

312

(2009)

293

(2009)

150

(n/a)

26

(2008)

840

(2010e)n/a

826

(2009)n/a

405

(2009)

Variable oil

pump

Invariable oil

pump

Electrical oil

pump

Vacuum

pump

Balancer shaft

unit

Camshaft

phaser

Water pump

Sinter

products

Lightweight

brake discs

P

P

P

P

P

P

P

P

o

r

i

t

e

51

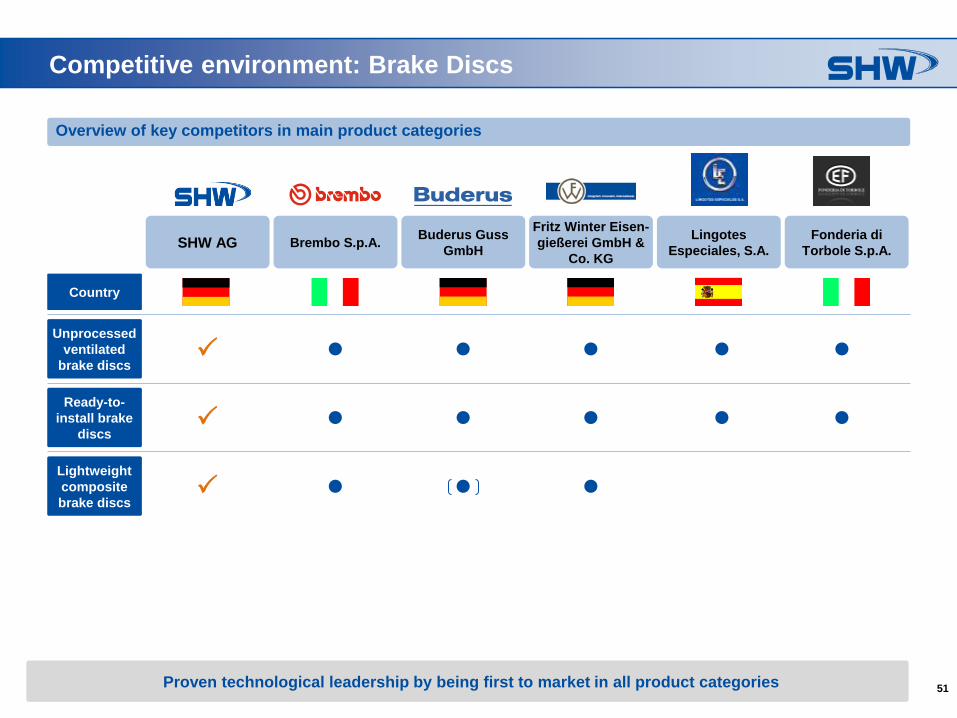

Competitive environment: Brake Discs

Overview of key competitors in main product categories

Proven technological leadership by being first to market in all product categories

P

P

P

Sale

s (€m

)

(Year)

290

(2010a)

n/a

n/a

4,6

93

(2009)

n/a

213

(2009)

31

(2009)

12,1

17

(2009)

3,8

64

(2009)

312

(2009)

293

(2009)

150

(n/a

)

26

(2008)

840

(2010e)

n/a

826

(2009)

n/a

405

(2009)

Varia

ble

oil

pum

p

Inva

riable

oil

pum

p

Ele

ctrical o

il

pum

p

Vacu

um

pum

p

Bala

nce

r shaft

unit

Cam

shaft

phase

r

Wate

r pum

p

Sin

ter

pro

ducts

Lig

htw

eig

ht

bra

ke d

iscs

Lightweight

composite

brake discs

Ready-to-

install brake

discs

Unprocessed

ventilated

brake discs

Country

SHW AG Brembo S.p.A.Buderus Guss

GmbH

Fritz Winter Eisen-

gießerei GmbH &

Co. KG

Lingotes

Especiales, S.A.

Fonderia di

Torbole S.p.A.

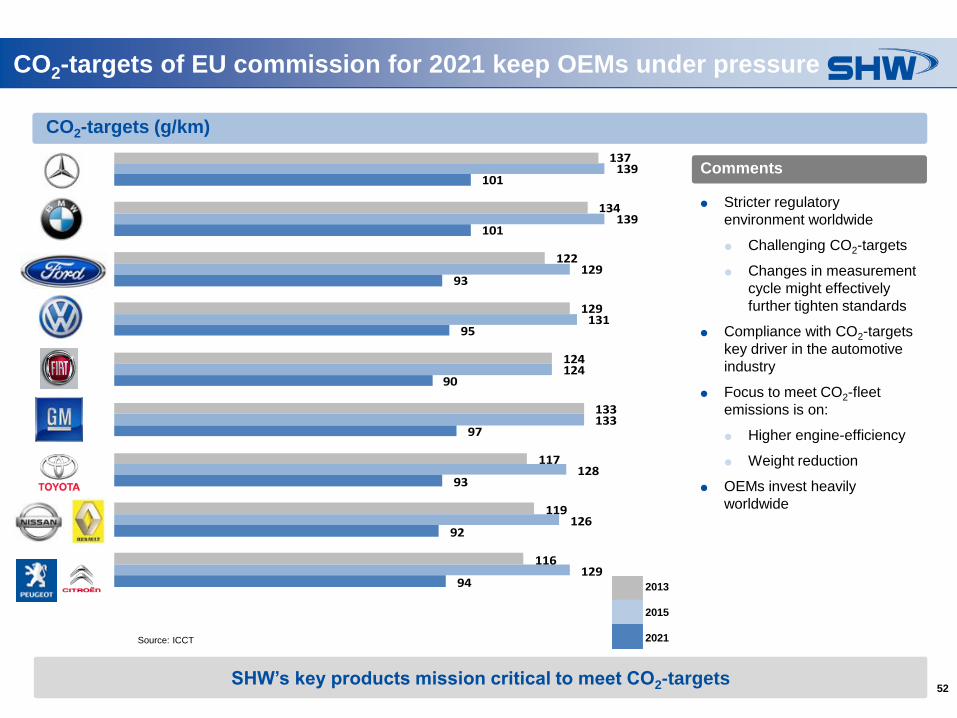

52SHW’s key products mission critical to meet CO2-targets

CO2-targets of EU commission for 2021 keep OEMs under pressure

CO2-targets (g/km)

Source: ICCT

2011

2015

2020

2013

2015

2021

137

134

122

129

124

133

117

119

116

139

139

129

131

124

133

128

126

129

101

101

93

95

90

97

93

92

94

Stricter regulatory

environment worldwide

Challenging CO2-targets

Changes in measurement

cycle might effectively

further tighten standards

Compliance with CO2-targets

key driver in the automotive

industry

Focus to meet CO2-fleet

emissions is on:

Higher engine-efficiency

Weight reduction

OEMs invest heavily

worldwide

Comments

53SHW components enable an achievement of more than 10% in fuel reduction

Key products mission critical to meet CO2-targets of clients

Reduced engine friction

through controlled oil

supply for engines1 - 2%

Variable valve timing 2 - 3%

Start-stop function for

automatic transmissions,

also applicable in hybrids3 - 6%

Selected key components Bottom line

1) New European Driving Cycle (“NEDC”)

Vari

ab

le

oil p

um

p

Fuel reduction potential1)ApplicationSHW product

Cam

sh

aft

p

haser

Ele

ctr

ical

oil p

um

p

BLUE TECHNOLOGY

Focus on hybrids to reduce luxury

segment CO2-emissions

Dual clutch transmissions and

downsized gasoline engines>10%

54

Financials 2014

55

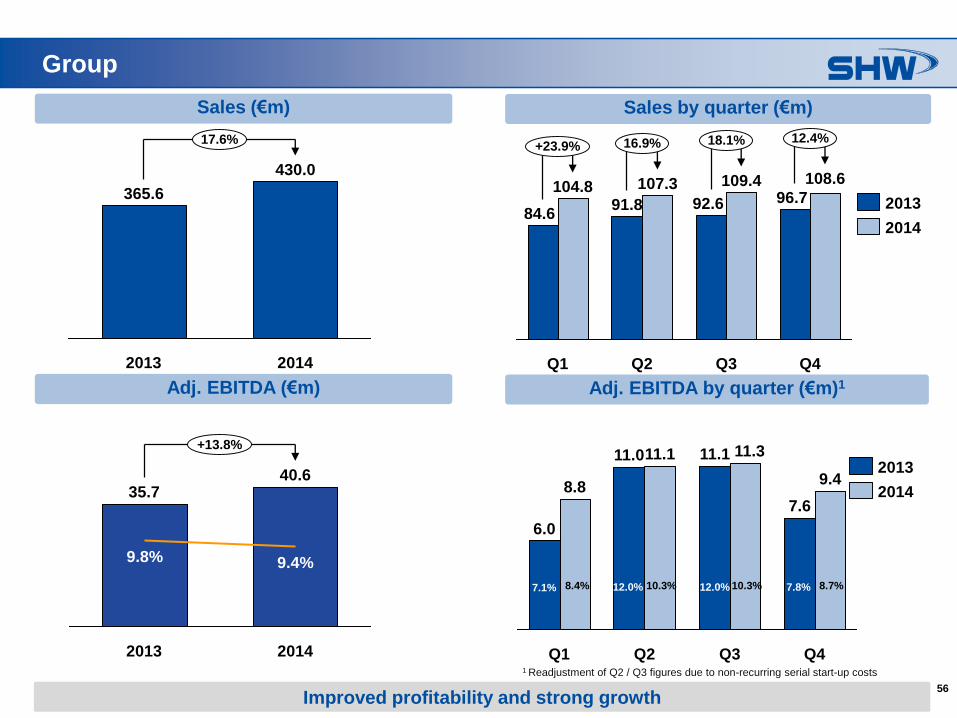

Strong sales lead to “growth pains”

€m 2014 2013 Change in %

Group sales 430.0 365.6 +17.6%

Incoming orders 452.7 388.8 +16.4%

Adj. EBITDA 40.6 35.7 +13.8%

Depreciation (excl. PPA) 18.1 14.0 +29.1%

Adj. EBIT 22.5 21.7 +3.9%

Net income for the period 10.7 13.4 -20.3%

Adj. EPS (in €) 1.83 2.29

DPS (in €) 1.001 1.00

Working Capital Ratio (%) 7.2 8.7

Capex2 34.8 32.8 +6.1%

Free cash flow -5.6 0.4

Net Debt -14.4 -2.9

ROCE (%) 17.7% 19.7%

No. of employees (average) 1,173 1,059 +10.8 %

1 Proposal to Shareholders Meeting on 12 May 20152 Additions to tangible and intangible assets

56

Group

Sales by quarter (€m)

12.4%18.1%16.9%+23.9%

Q4

108.6

96.7

Q3

109.4

92.6

Q2

107.3

91.8

Q1

104.8

84.62014

2013365.6

17.6%

430.0

2013 2014

Sales (€m)

Improved profitability and strong growth

Q1

11.111.0

6.0

Q2

8.89.4

7.6

Q3

11.1 11.3

Q4

2014

2013

Adj. EBITDA (€m) Adj. EBITDA by quarter (€m)1

7.1% 8.4% 12.0% 10.3% 12.0% 10.3% 7.8%

1 Readjustment of Q2 / Q3 figures due to non-recurring serial start-up costs

8.7%

2014

40.635.7

9.8%

2013

+13.8%

9.4%

57

Increased sales with leading key accounts

14.7

1.9

14.7

2.2

14.7 17.5

2.3

2.2

14.7 17.5

2.3

ThyssenKrupp11.1

Ford11.4

Audi22.4

BMW40.1

Daimler60.3

VW92.9

19.9Volvo Cars

72.4

PSA

32.6

23.4

12.3

6.2Hilite

Other71.4

36.0

13.2

83.8

9.7

113.4

11.49.3

Porsche21.8

20.5

2013

2014

Sales by customer (€m)

SHW well positioned with German OEMs

58

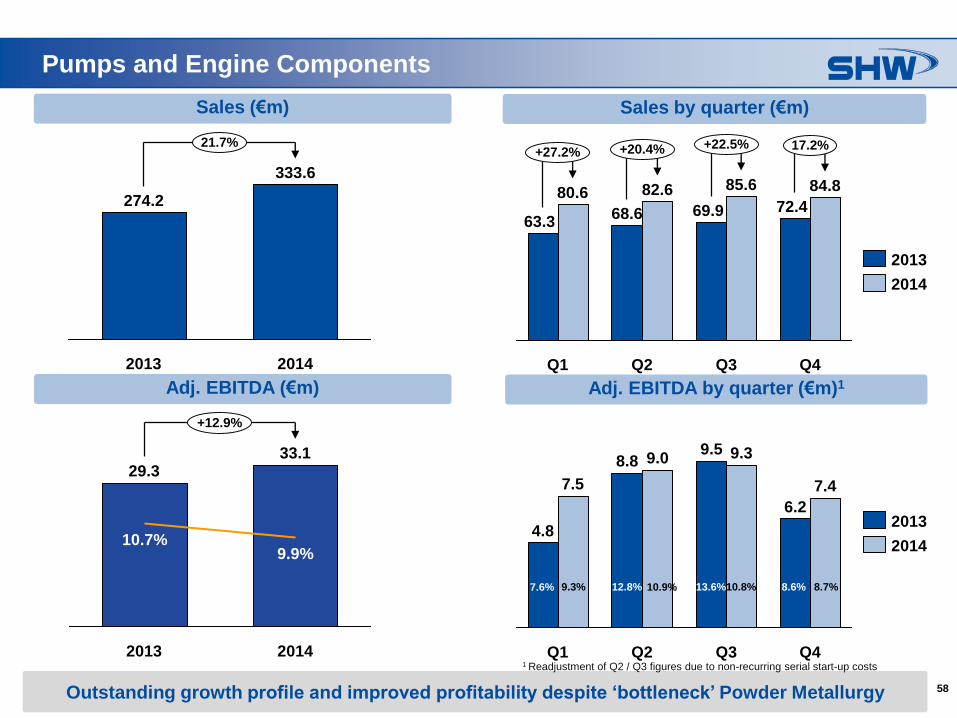

Pumps and Engine Components

Sales by quarter (€m)

+20.4%

72.4

Q4

+22.5%

68.6

Q2

+27.2%

80.669.9

Q3

17.2%

84.8

Q1

63.3

85.682.6

2013

2014

Sales (€m)

Q1

7.5

8.89.5

4.8

Q2

9.0

7.4

6.2

Q4

9.3

Q3

2014

2013

Adj. EBITDA (€m) Adj. EBITDA by quarter (€m)1

2014

33.129.3

10.7%

2013

+12.9%

9.9%

274.2

2013

21.7%

333.6

2014

7.6% 9.3% 12.8% 10.9% 13.6%10.8% 8.6% 8.7%

Outstanding growth profile and improved profitability despite ‘bottleneck’ Powder Metallurgy

1 Readjustment of Q2 / Q3 figures due to non-recurring serial start-up costs

59

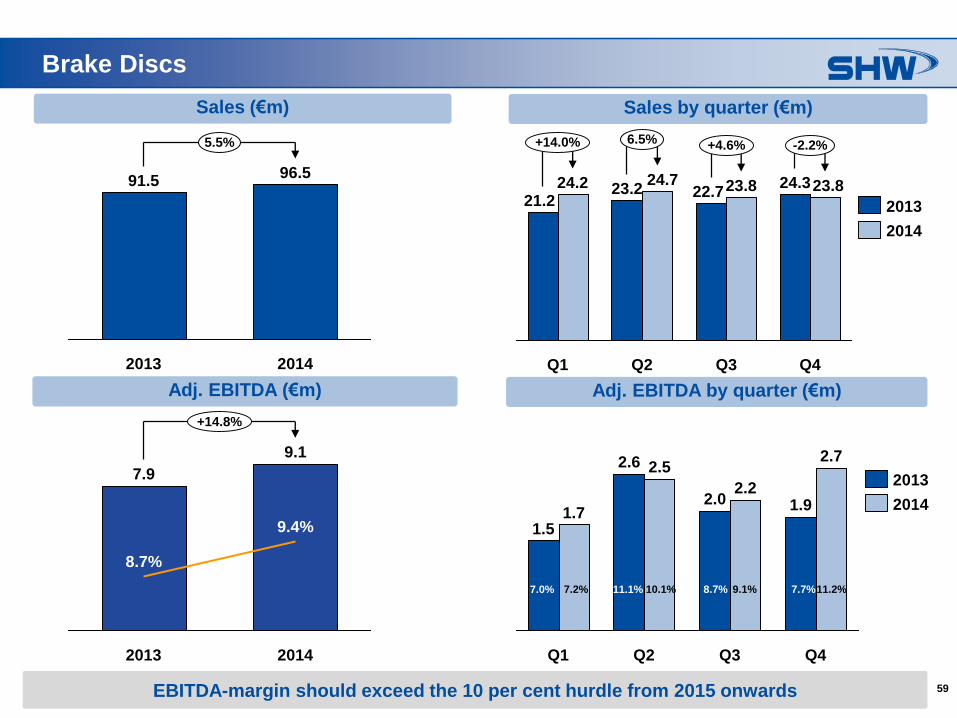

Brake Discs

Sales by quarter (€m)

23.8 24.3

Q3

22.7

-2.2%

21.224.2

Q1

23.2

Q2

24.7

+4.6%6.5%+14.0%

Q4

23.8

Sales (€m)

Q3

2.22.0

Q2

2.5

1.9

2.7

Q4

1.51.7

Q1

2.6

Adj. EBITDA (€m) Adj. EBITDA by quarter (€m)

2013

2014

2014

2013

9.1

2013

7.9

8.7%

9.4%

2014

+14.8%

96.5

5.5%

2014

91.5

2013

7.0% 7.2% 11.1% 10.1% 8.7% 9.1% 7.7%11.2%

EBITDA-margin should exceed the 10 per cent hurdle from 2015 onwards

60

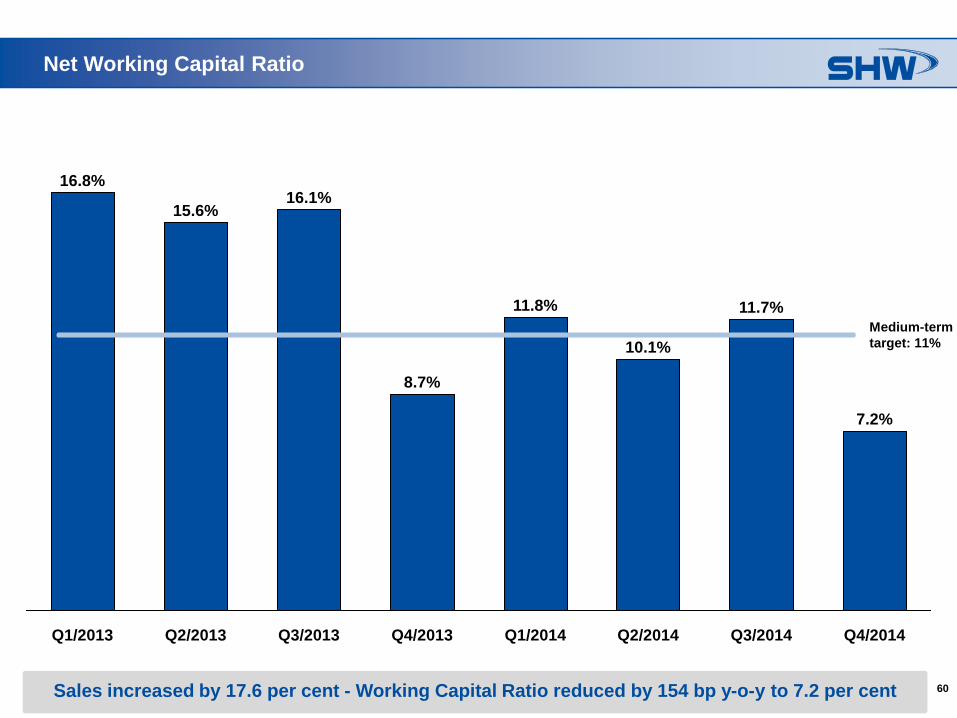

Net Working Capital Ratio

Medium-term

target: 11%

Q1/2014

11.8%

Q4/2013

8.7%

Q3/2013

16.1%

Q2/2014 Q3/2014

11.7%

10.1%

Q2/2013

15.6%

Q1/2013

16.8%

Q4/2014

7.2%

Sales increased by 17.6 per cent - Working Capital Ratio reduced by 154 bp y-o-y to 7.2 per cent

61

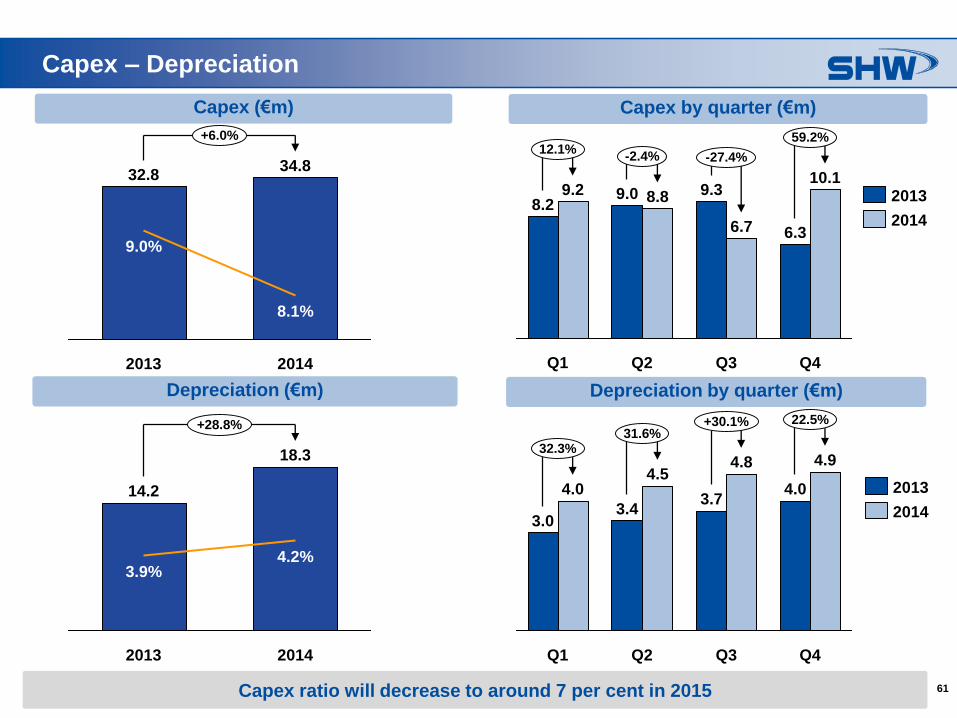

Capex – Depreciation

14.714.7

Capex by quarter (€m)

Q4

10.1

6.3

Q3

6.7

9.3

Q2

8.89.0

Q1

9.28.2

59.2%

-27.4%-2.4%12.1%

2014

2013

Capex (€m)

31.6%32.3%

Q4

4.0

Q3

4.8

22.5%+30.1%

4.9

3.7

Q2

4.5

3.4

Q1

4.0

3.0

Depreciation (€m) Depreciation by quarter (€m)

2014

2013

2013

32.8

9.0%

+6.0%

2014

34.8

8.1%

18.3

4.2%

2013

+28.8%

2014

14.2

3.9%

Capex ratio will decrease to around 7 per cent in 2015

62

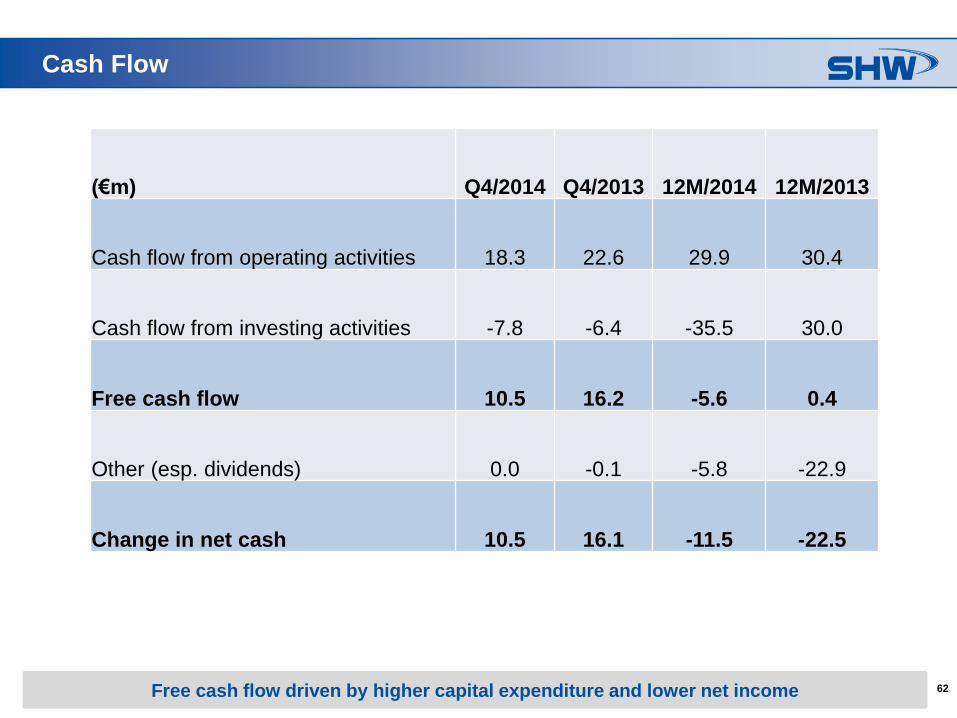

Cash Flow

5.

(€m) Q4/2014 Q4/2013 12M/2014 12M/2013

Cash flow from operating activities 18.3 22.6 29.9 30.4

Cash flow from investing activities -7.8 -6.4 -35.5 30.0

Free cash flow 10.5 16.2 -5.6 0.4

Other (esp. dividends) 0.0 -0.1 -5.8 -22.9

Change in net cash 10.5 16.1 -11.5 -22.5

Free cash flow driven by higher capital expenditure and lower net income

63

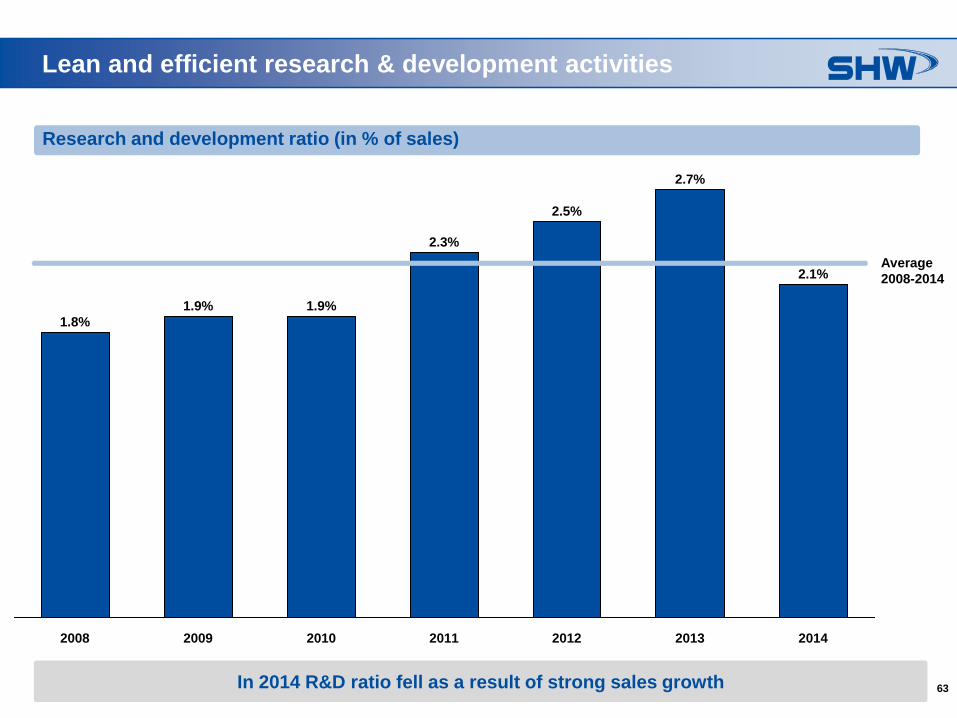

Lean and efficient research & development activities

2014

2.1%

2013

2.7%

2012

2.5%

2011

2.3%

2010

1.8%

2008

1.9%

2009

1.9%

Research and development ratio (in % of sales)

Average

2008-2014

In 2014 R&D ratio fell as a result of strong sales growth

64

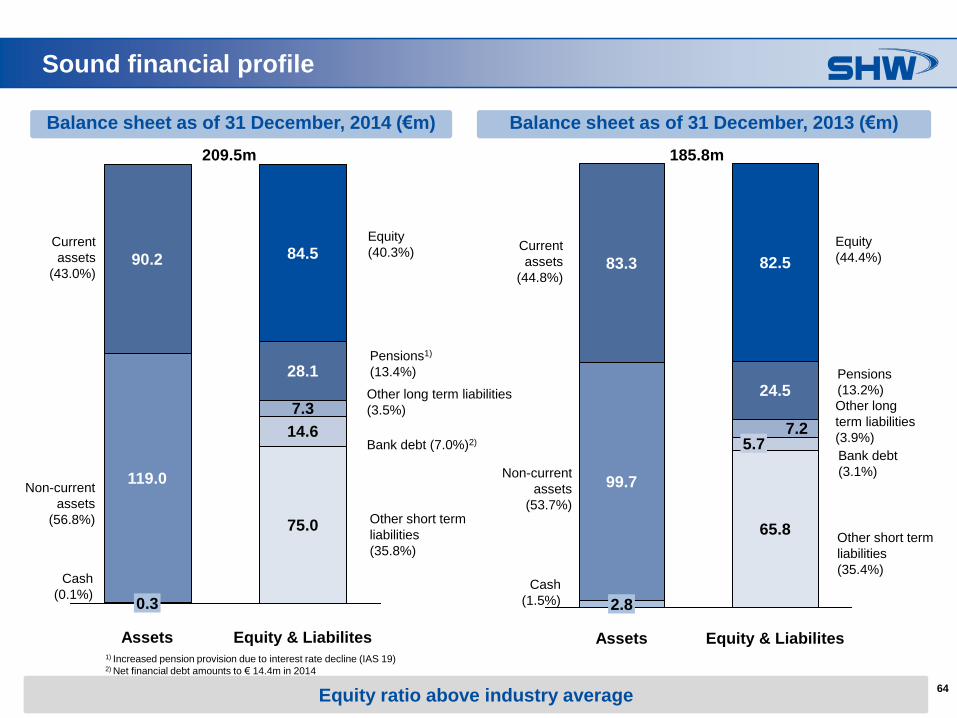

Sound financial profile

Balance sheet as of 31 December, 2014 (€m) Balance sheet as of 31 December, 2013 (€m)

Other short term

liabilities

(35.8%)

Pensions1)

(13.4%)

Current

assets

(43.0%)

Non-current

assets

(56.8%)

Equity

(40.3%)

37.9

209.5m

Equity & Liabilites

75.0

14.6

7.3

28.1

84.5

Assets

0.3

119.0

90.2

Cash

(0.1%)

Other short term

liabilities

(35.4%)

Pensions

(13.2%)

Current

assets

(44.8%)

Non-current

assets

(53.7%)

Equity

(44.4%)

37.9

185.8m

Equity & Liabilites

65.8

5.77.2

24.5

82.5

Assets

2.8

99.7

83.3

Other long

term liabilities

(3.9%)

Cash

(1.5%)

Other long term liabilities

(3.5%)

Bank debt (7.0%)2)

Bank debt

(3.1%)

Equity ratio above industry average

1) Increased pension provision due to interest rate decline (IAS 19)2) Net financial debt amounts to € 14.4m in 2014

65

Disclaimer

No offer or investment recommendation

This document, which has been issued by SHW AG (the “Company” or “SHW”), does not constitute an offer to sell, or the solicitation of an offer to subscribe for or

buy, any shares in the Company, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or

investment decision in relation thereto.

The contents of this presentation are may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part,

for any purpose. Neither the Company nor any other party is under any duty to update or inform you of any changes to such information. In particular, it should be

noted that financial information relating to the Company contained in this document has not been audited and in some cases is based on management information

and estimates.

This material is given in conjunction with an oral presentation and should not be taken out of context.

Certain market data and financial and other figures (including percentages) in this document were rounded in accordance with commercial principles. Figures

rounded may not in all cases add up to the stated totals or the statements made in the underlying sources. For the calculation of percentages used in the text, the

actual figures, rather than the commercially rounded figures, were used. Accordingly, in some cases, the percentages provided in the text may deviate from

percentages based on rounded figures.

Future Oriented Statements

Certain statements in this presentation are forward-looking statements. By their nature, forward-looking statements involve a number of risks, uncertainties and

assumptions that could cause actual results or events to differ materially from those expressed or implied by the forward‐looking statements. These risks,

uncertainties and assumptions could adversely affect the outcome and financial consequences of the plans and events described herein.

No obligation to update the information

The Company does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or

otherwise, except as otherwise required by applicable laws and regulations. You should not place undue reliance on forward-looking statements, which speak as

only of the date of this presentation. Statements contained in this presentation regarding past trends or events should not be taken as a representation that such

trends or events will continue in the future.