barr today, barr tomorrow -...

TRANSCRIPT

Barr Pharmaceuticals, Inc.

Annual Report 2005

Barr Today, Barr Tomorrow

Questions For and Answers By Bruce L. Downey, CEO

Years Ended June 30,

(Numbers in thousands, except per share data and employee data) 2005 2004

Results of Operations

Total Revenues $1,047,399 $1,309,088

Earnings

Earnings from Operations $ 316,027 $ 192,848

Net Earnings 214,988 123,103

Diluted Earnings per Share 2.03 1.15

Financial Position

Cash Flows from Operations $ 363,035 $ 258,099

Working Capital 780,386 670,601

Total Assets 1,482,846 1,333,269

Shareholders’ Equity 1,233,970 1,042,046

Statistics

Research and Development Expenditures $ 128,384 $ 168,995

Capital Expenditures $ 55,157 $ 46,907

Number of Employees 1,847 1,480

Weighted Average Number of Diluted Common

Shares Outstanding 106,052 106,661

Selected Financial Highlights

Restated to include historicalfinancial data of Duramed

Net Earnings$ in millions

01 02 03 0504

62.6

210.

3

167.

6

123.

1

215.

0

Adjusted to reflect stock splits;restated to include historicalfinancial data of Duramed

Earnings per Share$ per share

01 02 03 0504

0.63

2.06

1.62

1.15

2.03

Restated to include historicalfinancial data of Duramed

Shareholders’ Equity$ in millions

01 02 03 0504

416.

8

666.

5

868.

0 1,04

2.0 1,

234.

0

Restated to include historicalfinancial data of Duramed

Total Revenues$ in millions

01 02 03 0504

593.

2

1,18

9.0

902.

9

1,30

9.1

1,04

7.4

Barr Pharmaceuticals, Inc.Board of Directors

Carole S. Ben-Maimon, M.D.President and Chief Operating OfficerDuramed Research Inc.

Paul M. Bisaro, Esq.President and Chief Operating OfficerBarr Laboratories, Inc.

Harold N. ChefitzChairman of Notch Hill AdvisorsPresident of Chefitz Healthcare Advisors

Bruce L. Downey, Esq.Chairman and Chief Executive OfficerBarr Pharmaceuticals, Inc.

Richard R. FrankovicPharmaceutical Industry Consultant

James S. Gilmore, III, Esq.Partner, Kelley, Drye & Warren;Former Governor, Commonwealth of Virginia

Jacob M. KayPresident & Chief Operating Officer ofApotex, Inc.

Peter R. SeaverHealthcare Industry Consultant

George P. Stephan, Esq.Business ConsultantFormer Director of Kollmorgen Corporation

Management Team

Bruce L. Downey, Esq.Chairman and Chief Executive OfficerBarr Pharmaceuticals, Inc.

Paul M. Bisaro, Esq.Senior Vice President

Carole S. Ben-Maimon, M.D.Senior Vice President

Frederick J. Killion, Esq.Vice President, General Counsel and Secretary

William T. McKeeVice President, Chief Financial Officer andTreasurer

Barr Laboratories, Inc.A subsidiary of Barr Pharmaceuticals, Inc.

Management Team

Paul M. Bisaro, Esq.President and Chief Operating Officer

Salah U. Ahmed, Ph.D.Senior Vice President, Research and Development

Michael J. BogdaSenior Vice PresidentManufacturing and Engineering

Timothy P. CatlettSenior Vice President, Sales and Marketing

Catherine F. HigginsSenior Vice President, Human Resources

Frederick J. Killion, Esq.Senior Vice President, General Counseland Secretary

William T. McKeeSenior Vice PresidentChief Financial Officer and Treasurer

Christine Mundkur, Esq.Senior Vice PresidentQuality and Regulatory Counsel

Emad M. Alkhawam, Ph.D.Vice PresidentAnalytical Research and Development

Jay Bapna, P.E.Vice President, New York Manufacturingand Engineering

Carol A. CoxVice President, Investor Relations andCorporate Communications

Charles E. DiLiberti, M.S.Vice President of Scientific Affairs

Suzanne DonaghyVice President and Chief Information Officer

David J. FurnissVice President, Internal Audit

Phil GioiaVice President, Proprietary Sales

Jake HansenVice President, Government Affairs

J. Gregory JesterVice President and Corporate Controller

Daryl LeSueurVice President, Operations, Ohio Facility

Christopher Mengler, R.Ph.Vice President, Corporate Devlopment

Michael MoorsheadVice President and General Manager,Virginia Facility

Amy NiemannVice President, Proprietary Marketing

Timothy B. SawyerVice President, Sales for Generic Products

Robert WillifordVice President and General Manager,Ohio Facility

Duramed Research Inc.A subsidiary of Barr Pharmaceuticals, Inc.

Management Team

Carole S. Ben-Maimon, M.D.President and Chief Operating Officer

Lance J. Bronnenkant, Ph.D.Vice President of Research and Development,Operations

Howard I. HaitVice President, Data Management andBiostatistics

Wayne S. Mulcahy, Ph.D.Vice President, Clinical Operations

Shareholder InformationInvestor Relations DepartmentContact: Carol A. CoxVice President, Investor Relations andCorporate CommunicationsEmail: [email protected]: 1-800-BARRLABWebsite: www.barrlabs.com

Common StockCommon Stock is traded on the New YorkStock Exchange Symbol: BRL

Registrar and Transfer AgentMellon Investor ServicesP.O. Box 3315South Hackensack, NJ 07606-1915

Annual MeetingThe annual meeting of shareholders will beheld at 10 am on November 3, 2005 at theWoodcliff Lake Hilton, Tice Blvd., WoodcliffLake, NJ.

TrademarksBARR, barr (stylized), the stylized “b”,Duramed, DURAmed (stylized), “four dots”(stylized), “Shaping Women’s Health” (stylized)and the female symbol (stylized) are registeredtrademarks of Barr Pharmaceuticals, Inc. orrelated subsidiaries. APRI, AVIANE,AYGESTIN, BARR, CAMILA, CENESTIN,CRYSELLE, DIAMOX, DOXY-CAP, DOXY-TABS, DURADRIN, DURAMED, ENPRESSE,ERRIN, E.S.P., FEWER PERIODS. MOREPOSSIBILITIES., IT’S NOT TOO LATE TOPREVENT PREGNANCY, JUNEL, KARIVA,LESSINA, NORDETTE, NORTREL, PLAN B,PORTIA, PREFEST, PREVEN, PREVENT,REVIA, REVIA NALTREXONE HCL,SEASONALE, SHAPING WOMEN’S HEALTH,SPRINTEC, TRI-SPRINTEC, VIASPAN,WHEEL OF MENSTRUATION, ZEBETAand ZIAC are registered trademarks, andA.L.E.R.T., ARANELLE, CARE, CLARAVIS,CYPAT, ENJUVIA, FASLIQ, JUNEL FE,KELNOR, MAKING MEDICINES WORKFOR EVERYONE, NEVIS, OUTLOOKS &OPINIONS, SEASONEST, SEASONETTE,TREXALL and VELIVET are trademarks, ofBarr Pharmaceuticals, Inc. or related subsidiaries.LOESTRIN is a registered trademark andLOESTRIN FE is a trademark of WarnerChilcott, licensed for use by DuramedPharmaceuticals, Inc.

All other trademarks referenced herein are theproperty of their respective owners.

10-K Report AvailableThe Company’s 2005 Annual Report on Form10-K, filed with the Securities and ExchangeCommission is available via the Company’sweb site or by writing to the Investor RelationsDepartment at the Company’s headquarters.

® 2005 Barr Pharmaceuticals, Inc. All rights reserved.

Directory

Design: Arnold Saks Associates, NYC Photography: Bill Gallery Product Photography: Jim Barber Printing: PonyXPress Printing Services

1

Questions and Answers...

2005 Business Summary and Financial Performance

Q Please provide your assessment of the Company’s overall financial progress infiscal 2005.

Fiscal 2005 represented another strong year for Barr. Our investment in building avibrant proprietary products pipeline, the expansion of our generic oral contraceptiveproduct line, the addition of several important new generic products, and key businessdevelopment initiatives were among the highlights of the fiscal year.

On a GAAP basis, we reported fully diluted earnings per share of $2.03 for fiscal 2005,compared to $1.15 for fiscal 2004, on net earnings for fiscal 2005 of $215.0 million,compared to $123.1 million in fiscal 2004. Revenues for the year totaled $1.05 billion,compared to $1.31 billion in fiscal 2004. Excluding the approximate $0.37 per sharecharge related to a liability recorded in relation to a letter of intent signed in June 2005regarding a potential litigation settlement and product acquisition related to Organon’sMircette® oral contraceptive, detailed elsewhere in this report, adjusted net earnings forthe fiscal year ended June 30, 2005 were $254.3 million, or $2.40 per fully diluted share.

Strong proprietary product sales, up 91% year-over-year, were $279 million. Thisgrowth was driven by sales of our SEASONALE® extended-cycle oral contraceptiveproduct. We also reported margins of 70%, up from 51% a year ago. We ended thefiscal year with more than $363 million in operating cash flow.

While delivering sound results, we also continued to invest in new product develop-ment – generic and proprietary – and took the first steps into the new and untappedarena of biopharmaceutical products.

Bruce L. DowneyChairman and ChiefExecutive Officer

Barr Pharmaceuticals, Inc. (NYSE-BRL) is a holding companywhose principal subsidiaries, Barr Laboratories, Inc. and DuramedPharmaceuticals, Inc., develop, manufacture and market genericand proprietary pharmaceuticals. Generic products are sold underthe Barr label, while proprietary products are sold under theDuramed label. In a wide-ranging interview, Bruce L. Downey,Chairman and Chief Executive Officer, discussed the Company’sprogress during fiscal 2005, and its opportunities and challengesfor fiscal 2006 and beyond.

Q What do you consider Barr’s major accomplishments for the fiscal year?

In addition to our solid financial performance, we had a number of important achieve-ments across the company. In our generic business, we added two new oral contracep-tives to our product franchise: AranelleTM, the generic version of Watson Laboratories,Inc.’s Tri-Norinyl®-28 oral contraceptive; and KelnorTM, the generic version of Pfizer’sDemulen® 1/35-28 oral contraceptive. This brings to 22 the number of generic oral

contraceptive products we manufacture and market.We also added several generic products to our portfolio, most notably a generic

version of Bristol-Myers Squibb’s Videx® EC, which is used in combination withother antiretroviral agents for the treatment of HIV-1 infection in adults. TheU.S. Food & Drug Administration (FDA) granted expedited review of thisAbbreviated New Drug Application (ANDA) under the President’s EmergencyPlan for AIDS Relief and approved it approximately seven months after filing.

We also received approval for the generic version of Shire Pharmaceutical Group’sAgrylin® blood platelet treatment, and the generic version of Bristol-Myers Squibb’sGlucophage® XR diabetes treatment.

On the first day of fiscal 2006 we received FDA approval for the generic version ofFerring B.V.’s DDAVP® antidiuretic product. In February 2005, a District Court ruledthat the patent alleged to cover DDAVP is unenforceable and not infringed by ourproduct. The Court’s decision ended the 30-month stay and cleared the way for FDAapproval. It is important to note that the District Court’s decision has been appealed,and arguments could be heard later this fall. If we were to lose upon appeal, thecompany might be liable for damages. Because we were the first to file our patentchallenge, we received 180 days of marketing exclusivity and we launched our productimmediately. However, the July approval will transfer the financial benefits of thisproduct into the current fiscal year.

We also announced several agreements, key among them were the agreementsinvolving Kos Pharmaceuticals’ Niaspan® and Advicor ® cholesterol-lowering productsand an agreement with Cephalon, Inc. related to the ACTIQ® cancer pain managementtreatment.

The story in our proprietary products business was the continued growth of ourSEASONALE® extended-cycle oral contraceptive. We also filed our New DrugApplication for SEASONALE® Lo extended-cycle oral contraceptive and continue towork with the FDA to secure approval of SEASONIQUETM, our next generationextended-cycle oral contraceptive, which received an Approvable letter in August 2005.

In the area of biopharmaceuticals, we initiated and completed the Phase I clinicaltrials for the Adenovirus Vaccines Types 4 and 7 during fiscal 2005. We also enteredinto an agreement with PLIVA to develop the generic biopharmaceutical GranulocyteColony Stimulating Factor (G-CSF), the generic version of Amgen’s NEUPOGEN®

which is used in the treatment of neutropenia, which is low white blood cell count incancer patients.

I am proud of the progress we made across the businesses, and believe that theseactivities position us strongly for the future.

2

ExpandingGeneric PortfolioWe expanded our genericproduct portfolio, addingtreatments for AIDS,diabetes, blood platelets,and two additional oralcontraceptives - Kelnorand Aranelle.

3

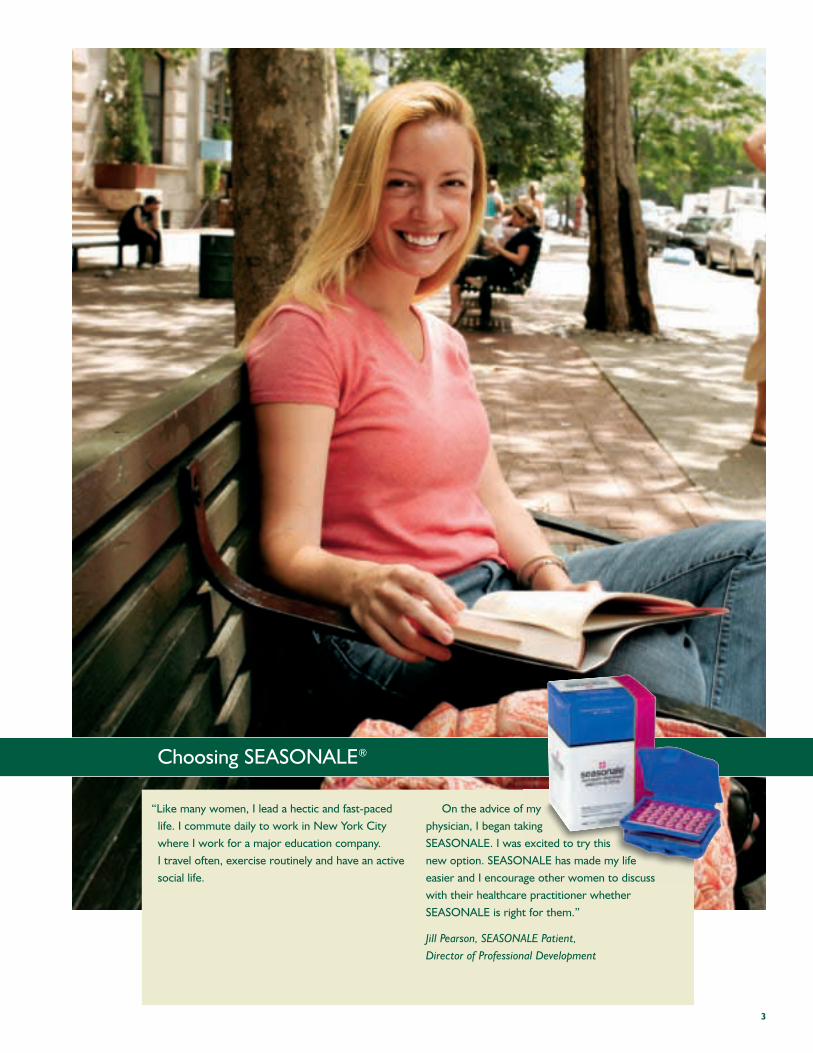

“Like many women, I lead a hectic and fast-pacedlife. I commute daily to work in New York Citywhere I work for a major education company.I travel often, exercise routinely and have an activesocial life.

On the advice of myphysician, I began takingSEASONALE. I was excited to try thisnew option. SEASONALE has made my lifeeasier and I encourage other women to discusswith their healthcare practitioner whetherSEASONALE is right for them.”

Jill Pearson, SEASONALE Patient,Director of Professional Development

Choosing SEASONALE®

4

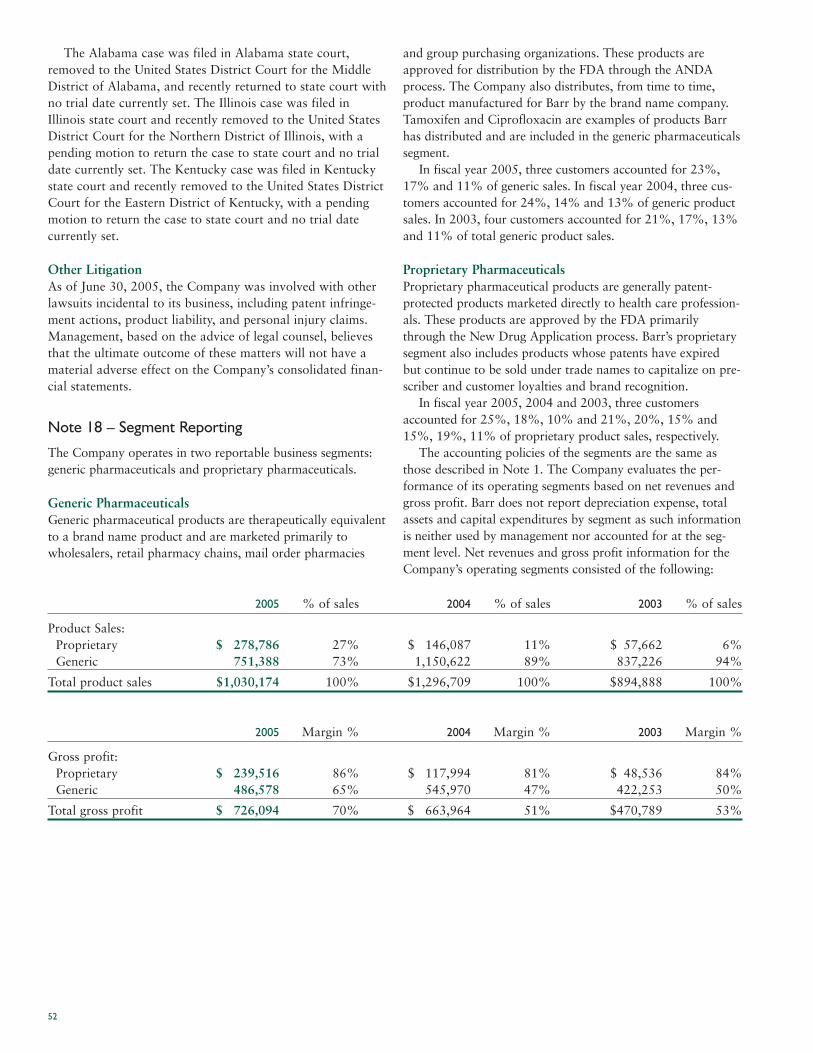

Generic Segment

Q What is the current status of your generic business?

During fiscal 2005, generic product sales contributed approximately $751 million. We cur-rently market 75 unique generic products, representing approximately 150 dosage forms.We are the only provider of nine of these products, and we are the leading supplier, interms of total prescriptions, for more than 50% of our generic products. Female healthcareis our single largest category, totaling 29 products, of which 22 are oral contraceptives.

Q Given the breadth of the Company’s generic oral contraceptive portfolio, is thiscategory maturing?

We are the leader in the oral contraceptive marketplace in the United States. Since welaunched our first oral contraceptive in 2001, we have developed and launched 21 addi-tional oral contraceptives. While we have been aggressively expanding our product line,additional competitors have entered the marketplace and as a result, we have experiencedlower pricing and lower volume. In addition, for many of these products, the genericsubstitution rates in this category have slowed due to many of our large customers maxi-mizing the opportunities for these products. However, we have gained market share oncertain products due to the addition of new customers. As a result, sales of our oral con-traceptives were down slightly in fiscal 2005 compared to the previous year. We anticipatethat sales from our portfolio of generic oral contraceptives will decline in fiscal 2006, asthese trends continue. However, we believe that our large portfolio of generic oral contra-ceptive products will remain a significant component of our total revenues.

Q How much of a role can we expect from the Company’s advance into differentdelivery technologies, and what progress has been made?

At the end of the year, we had approximately 10 products in various stages of devel-opment that utilize dosage forms other than our traditional solid oral tablet or capsuledelivery system, including transvaginal rings, patches, nasal sprays, ophthalmics andcreams. We have development and manufacturing partners for many of these products.Many of these projects will result in patent challenges while others will have variousother issues associated with their development and commercialization. We look for-ward to expanding into these dosage forms.

Q What other generic growth drivers, excluding patent challenges, are on thehorizon for fiscal 2006 and beyond?

At fiscal year-end, we had approximately 35 ANDAs, including tentatively approvedapplications, pending at the FDA. We have more than 40 generic projects in activedevelopment, more than 30 of which are in capsule and tablet dosage forms. We arecommitted to maintaining a full pipeline of generic products and we anticipate anongoing stream of approvals of new generic products in coming years.

DistributionOur Virginia distributioncenter shipped morethan 3.5 billion doses infiscal 2005, including ournew Kelnor and Aranelleoral contraceptives.

Q Barr has always pursued generic products with barriers to entry. How hasthis strategy evolved? How does it relate to new product development in the

generic business?

Developing generic products with barriers to entry remains a cornerstone of our R&Dactivities. These products tend to have a longer lifecycle and generate more value thangeneric products where multiple competitors enter the market simultaneously.

Naturally, our patent challenge activities represent an area where the barrier isintellectual property. Our initiatives in new drug delivery platforms and our businessdevelopment activities also have the potential to bring us additional products wherecompetition will be limited.

Q The Company has publicly stated that asignificant number of its pending ANDAs

represent patent challenge products. Doesthis represent a strength, or weakness, in Barr’sgeneric product selection criteria?

To date, we have publicly announced nine prod-ucts where we are actively challenging thepatents covering these products – includingAllegra® antihistamine products, Adderall® XRproducts for attention deficit and hyperactivitydisorder, and Provigil® treatment for narcolepsy.These nine products have current annual sales of

approximately $5 billion. During the year, we received tentative approvals for fiveapplications, which brings to nine the number of tentative approvals received forANDAs related to patent challenges.

We believe that our expertise in identifying and developing patent challenge candidates,our strength in successfully litigating or settling patent challenges, and our pipeline ofproducts that have intellectual property or patent issues, represent a distinct strength forthe company. As we move into the future, we expect that patent challenge products willrepresent an increasing percentage of our portfolio. Despite recent issues related to author-ized generics, our patent challenge strategy offers a significant growth opportunity for ourcompany, our shareholders, as well as the consumers who benefit when we are successfuland bring a generic product to market earlier than may otherwise have happened.

Q How do authorized generics impact the Hatch/Waxman 180-day incentive,and the strategy to invest in patent challenges?

Authorized generics undermine the 180-day exclusivity incentive that is integral to theHatch/Waxman patent challenge process. Because the “authorized” generic is not soldunder an ANDA, but under the brand pharmaceutical manufacturer’s original NDA,the courts have determined it may compete with the generic product during the 180-day exclusivity period.

Some analysts have estimated that authorized generics can reduce the value of apatent challenge to the generic challenger by as much as 40%. We will continue towork with Congress, the Department of Health and Human Services, and the genericindustry association to seek ways to limit the use of authorized generics.

5

QualityAssuranceMore than 375 peopleare committed toensuring that our phar-maceuticals meet thehighest levels of quality,safety and efficacy.

6

“Since its introduction in 1960, The Pill has evolvedin concert with women’s changing roles – fromdosing to delivery mechanisms and now – regimen.With the FDA approval of SEASONALE in 2003,women have the option to extend the timebetween periods.

While monthly menstruation is normal, physi-cians agree that a monthly period is not necessarywhile on oral contraceptives. When you’re on ThePill, you’re not really getting a menstrual period,

you are getting a Pill period caused by a lack ofhormone during the placebo week.

The evolution to extended-cycle regimens likeSEASONALE is an important progression of ThePill. Women’s evolving responsibilities, both personaland professional, create the need for advancementsin many aspects of their lives, including birth control.Tomorrow, only the future will tell.”

Dr. Nancy Roberson Jasper,Obstetrician and Gynecologist

Extended-Cycle OCs

Q Pricing in the generic industry appears to be a significant current issue. How isthe Company responding to this?

We focus our resources on those potential products that have barriers to entry thatlimit potential competition. In fact, we are the only provider of nine generic products inour portfolio, and are the leader in terms of market share on more than 50% of ourproducts. While barriers continue to include raw material sourcing and unique formu-lations, increasingly these barriers involve resolving highly complex issues related tointellectual property. Barr’s focus on products with barriers to entry is a key competi-tive advantage.

Proprietary Products

Q Some have termed 2005 Barr’s breakout year in terms of proprietary products.Do you agree with this assessment?

We are excited about the progress we have made in growing our proprietarybusiness. Less than six years after initiating activities in this area, we have a growingproprietary products business with significant future potential.

We currently have 13 proprietary products on the market, five of which we activelydetail to physicians. We have four proprietary product applications pending at theFDA and seven in clinical development, one of which is in Phase III studies. We arecommitted to consolidating our leadership position in women’s healthcare, as well aspursuing additional therapeutic categories. Our pipeline includes products in femalehealthcare, including oral contraceptives, hormone therapy and our transvaginal ringtechnology products; oncology; urology; and anti-infective/anti-viral products.

Our SEASONALE extended-cycle oral contraceptive, which created an entirely newcategory when launched in October 2003, continues to gain marketacceptance. Since launch, nearly 1 million prescriptions have been filled.

We will expand this product franchise following the approval of ourSEASONIQUE product and are working with the FDA regarding issues

raised in the Approvable letter. We have also filed a NDAfor the SEASONALE Lo (levonorgestrel/ethinyl estradioltablets 0.1 mg/0.02 mg and ethinyl estradiol tablets)extended-cycle oral contraceptive.

In the area of hormone therapy, we are building a fullline of tablet strengths for our EnjuviaTM (Synthetic

Conjugated Estrogens, B) product. Enjuvia is a plant-derived,synthetic conjugated estrogen product that contains a blend of the ten

estrogenic substances found in the brand Premarin®. This year, the FDA approved ourapplication for the 0.3 mg and 0.45 mg tablets and had previously approved our0.625 mg and 1.25 mg tablets. We are awaiting the approval of the 0.9 mg tabletstrength. Although we were disappointed with the FDA’s Not Approvable letter, whichwe received in April 2005, for our application for our BijuvaTM (Synthetic ConjugatedEstrogens, A) vaginal cream, we continue to work closely with the Agency and we areconfident the outstanding issues can be resolved. Bijuva, if approved, is intended as alocal treatment for vaginal atrophy.

7

Commitmentto FemaleHealthcareWe are committed toleadership in femalehealthcare, includingproprietary oral contra-ceptives and hormonetherapy products.

Q With the introduction of Enjuvia, Barr will be marketing both syntheticconjugated estrogen products – Cenestin® and Enjuvia. What do you see for

the potential for this product franchise, now that we are several years out fromthe Women’s Health Initiative (WHI) study?

While there has been a reduction in the number of women using estrogen replacementtherapy following the publicity surrounding the WHI study, hormone therapy remainsa nearly $2 billion a year market.

We believe that hormone therapy is appropriate for addressing issues associatedwith menopause, and believe that women, in consultation with their physicians, arelooking to these products for shorter terms of usage, and looking for a full range ofdosages in order to select the lowest appropriate dose. Once Enjuvia is launched,women will have two synthetic conjugated estrogen options, Enjuvia and Cenestin,from our company.

Q The Company has spent considerable time and resources in seekingapproval to bring Plan B® Over-The-Counter (OTC). Why?

Plan B meets a significant unmet medical need by providing women with asafe and effective contraceptive option when used within 72 hours of a contra-ceptive failure or incident of unprotected intercourse. As part of our overallcommitment to women’s healthcare, we are committed to enhancing the

availability of emergency contraception for those who would choose to use it.If Plan B were available in a more timely fashion, we believe that more than 70%

of the unintended pregnancies that occur each year could be eliminated. Havingto get a doctor’s prescription can delay timely access, and that is why we continue to

pursue our application with the FDA to make this product available over-the-counter.Although the FDA again deferred a decision on our OTC application in August

of this year, we will continue to work with the Agency to answer their outstandingquestions. While we believe that this recent delay is not justified, we will use theopportunity presented by the FDA’s public comment proceedings to continue to pressfor approval of Plan B as an OTC product. In the meantime, we will continue tomarket Plan B as a prescription drug, and to work to increase consumer and health-care provider awareness. We will also continue to work with states interested in joiningthe seven that already make Plan B available through pharmacy access programs.

Q Looking at the Company’s proprietary pipeline, can you provide an update ofother pipeline products?

While the timing of our pipeline of proprietary products is confidential, we have pro-vided information on the status of our extended-cycle oral contraceptives; our CyPatTM

treatment for the symptoms associated with treatment of prostate cancer; our urinaryincontinence product utilizing our transvaginal ring technology which offers thepotential to deliver higher doses of oxybutynin to the bladder neck with much lowersystemic exposure; and our Adenovirus Vaccine project. A number of other productsare in various stages of development, and will be announced as the applications reachdevelopment milestones.

8

Need forTimely Accessto EmergencyContraceptionTo be most effective inpreventing pregnancyfollowing unprotectedintercourse or contra-ceptive failure, Plan Bneeds to be taken assoon as possible within72 hours.

9

Q Is the Company’s sales force adequately staffed to appropriately detail Barr’sproduct pipeline?

Our 250-person Duramed Pharmaceuticals’ Women’s Healthcare Sales Force currentlypromotes our SEASONALE extended-cycle oral contraceptive product, our Cenestinhormone therapy products and Plan B emergency contraceptive product to femalehealthcare practitioners.

This sales force will market additional female healthcare products, such asSEASONIQUE and SEASONALE Lo if approved. We also expect that as new femalehealthcare products are developed, or acquired, we will add them, where appropriate,to the portfolio of products presented by this team.

Our 43-person Duramed Specialty Sales Force promotes our TrexallTM productdirectly to rheumatologists and dermatologists. As a result of our co-promotionagreement with Kos Pharmaceuticals, Inc., this team also promotes the Niaspan andAdvicor cholesterol treatments to obstetricians, gynecologists and other practitionerswith a focus on women’s healthcare. Additionally, they will communicate the benefitsof extended-cycle contraceptives to this physician audience. We expect to use thissales force to promote additional products as we develop or acquire them.

Q Supporting proprietary products requires a considerable investment inmarketing. Can you discuss the Company’s physician, professional and

Direct-to-Consumer (DTC) marketing initiatives?

Our Women’s Healthcare Sales Force details SEASONALE and other female healthcareproducts directly to more than 40,000 healthcare providers who we have determinedare among the most productive prescribers of oral contraceptive products in theUnited States. SEASONALE is the first extended-cycle oral contraceptive, and withits launch, we created an entirely new product category. As a result, education is asignificant component of our detailing activities.

Marketing support includes professional education materials, published data fromour clinical studies demonstrating the safety and efficacy of the extended-cycle concept,and product sampling kits that contain extensive information for patients. Wereinforce our detailing activities with a trade advertising program in leading medicaljournals and a DTC advertising campaign.

Q How do you view the newopportunity to detail Niaspan and

Advicor?

We are very excited about the opportu-nities that resulted from our agreementswith Kos Pharmaceuticals. Kos will payroyalties calculated as a percentage of thesales of the products, subject to certainmaximum sales levels. Our sales team willfocus on a new population of obstetri-cians, gynecologists and other practitionerswho have a focus on women’s healthcare.

Focused ProductDetailingOur 250-person Women’sHealthcare Sales Forcetakes the message of ourunique products directlyto more than 40,000physicians.

10

As the role of these physicians expands, particularly OB/GYNs who increasinglyserve as a primary physician for many women, they will become more central toaddressing the total health needs for many women. Many of these physicians have notpreviously been detailed about these cholesterol-lowering products.

Biopharmaceuticals

Q Barr has emphasized its entrance into biopharmaceuticals through theAdenovirus Project and the agreement with PLIVA on G-CSF. What is the

status of these projects?

We are very excited about both of these projects. The Adenovirus project, which isbeing completed under contract with the U.S. Department of Defense (DOD), providesus with experience in developing, seeking approval of and manufacturing a biophar-maceutical product. Once approved, we will supply this vaccine to the U.S. armedforces.

The agreement with PLIVA represents a major step in the development of ourgeneric biopharmaceuticals capabilities. In partnership with PLIVA, we intend todevelop and seek approval to market a generic version of Amgen’s NEUPOGEN®

(filgrastim) product in the United States and Canada. NEUPOGEN is primarilyindicated for the regulation of white blood cell production in the treatment of cancerpatients with chemotherapy-induced neutropenia.

Q Biopharmaceuticals have been described as the new frontier for genericcompanies. Why?

There is an urgent need for Congress and the FDA to define an abbreviated pathwayfor the approval of generic versions of biopharmaceuticals. Sales for biopharmaceuti-cals last year were approximately $30 billion and analysts expect this to grow to $60billion by the end of the decade. Biopharmaceuticals are an ever-increasing componentof overall prescription drug spending, and a significant contributor to escalating costs.

As the number of biologics products in America’s medicine cabinets increases, with-out a pathway for generic competition, the price of these products will remain artifi-cially high. Creating a process for the approval of generic versions of biopharmaceuticalswill unleash a flood of significant additional savings for consumers.

It is difficult to predict when a regulatory process will be defined. However, we areaggressively taking the steps necessary to position ourselves as a pioneer and ultimateleader in this potential market.

Adenovirus Vaccines Types 4 and 7 are beingdeveloped under a $42.3 million, six-year contractwith the United States Department of Defense(DOD) to meet a significant unmet medical needfor our Armed Forces. The Adenovirus Vaccines areintended to be dispensed to Armed Forces recruitsto prevent epidemics of an acute respiratorydisease that has been a leading cause of hospitaliza-tions of military trainees. Adenovirus Types 4 and 7can cause contagious illnesses that spread quicklyin settings of close quarters, especially those found

in military bar-racks. Recoverycan take as long as two weeks, which costs theDOD millions of dollars in treatment and lostrecruit training days.

In July 2003, Barr completed construction ofits Adenovirus Vaccine manufacturing and packagingfacility, a 20,000 square-foot building locatedon Barr’s Forest, Virginia campus, that is designedspecifically to produce these vaccines.

Helping Our Armed Forces

11

12

Investing in R & D$ millions invested

01 02 03 0504

57.6

75.7 91

.2

169.

0

128.

4

Restated to include historicalfinancial data of Duramed

Other Corporate Activities

R&D

Q The Company continues to invest heavily in new product development. How isthe money spent?

We continue to increase our investment in both generic and proprietary product develop-ment activities. Our increased investment in generic R&D is driven by the overall numberof generic products in development, as well as higher costs for bioequivalence studiesrelated to the development of products based on new delivery technologies outside ourtraditional focus on tablet/capsule products. Our increased investment in proprietaryproduct development is largely associated with the clinical trials required to provide thedata necessary to support approval of these products. In addition, we continue toexpand the human resources necessary to support both product development functions.We will continue to invest at the levels necessary to achieve our commitment to researchand development during fiscal 2006.

Q Are the levels of R&D spending adequate to support the product developmentnecessary to drive earnings?

We have always stated that we would invest what is necessary to support the growthof our business, even if it was at the expense of short-term earnings results. And wecontinue to increase our annual investment in R&D as necessary to fund these activities.I believe that we have invested what is necessary to ensure a stream of new productintroductions across the business and we will continue to invest what is necessary tomaintain our internal timelines on the development and introduction of new products.

Q The Company has had to build a proprietary development function. Are youhappy with the results to date?

We are very happy with the performance of our proprietary R&D team and ourmarketing teams, and with physician and consumer response to our products. Today,our proprietary products team totals more than 90 people with extensive brand prod-uct experience in the areas of clinical trials, toxicology, regulatory, pharmacokinetics,statistics, medical writing and product commercialization.

Business Development

Q Barr has entered into several business development agreements during fiscal2005. Can you provide some context for the ventures announced this year?

Our business development activities are focused on identifying and executinginitiatives that will strengthen our product portfolio, and include strategic productacquisitions, new technology arrangements including new technology platforms,and corporate mergers and acquisitions.

13

During fiscal 2005, we executed four key business development initiatives, includ-ing the agreements with Kos Pharmaceuticals, PLIVA and Cephalon that I havealready discussed. We also completed an agreement with King Pharmaceuticals, Inc.for exclusive rights in the U.S. for Nordette® oral contraceptive and Prefest® hormonetherapy.

In addition to these developments, we completed the integration of our 250-personDuramed Pharmaceuticals’ Women’s Healthcare Sales Force, and exercised ouroption to make a one-time royalty payment of $19 million to Eastern VirginiaMedical School (EVMS) related to the SEASONALE extended-cycle oral contracep-tive. We also established a $175 million, five-year, senior unsecured revolving creditfacility that will be used for working capital, capital expenditures, acquisitions andother general corporate purposes.

All of these activities meet our objectives of providing additional opportunities forlong-term growth and expansion of our business.

Q Barr’s corporate development activities have added several proprietaryproducts to the Company’s portfolio in recent years. Are these strategic

targets, or targets of opportunity?

Both, actually. Some proprietary products have been added to our portfolio as a resultof agreements that resulted in the settlement of ongoing legal matters. But we areclearly focused on leadership in proprietary female healthcare products, as well ascreating the opportunity to expand into additional therapeutic categories, and businessdevelopment activities are focused on this goal.

Capital Investment

Q Barr continues to invest in capitalexpansion and growth. What is your

strategy in making these investments?

Barr is committed to continuouslyinvesting in facilities to ensure ourleadership as a specialty pharmaceuticalcompany. During fiscal 2005, we contin-ued implementation of our company-wide enterprise resource planning (ERP)system, which will cost approximately$70 million. This system is designed to

allow us to more efficiently manage corporate activities and manage diverse productlines; integrate mergers and acquisitions; and support potential future internationaloperations. The flexibility of this system, and our ability to add new functionality asour business evolves, makes it a critical component of managing growth. Currently,our ERP system is scheduled to be implemented utilizing a phased approach beginningin October 2005. To ensure this project is implemented in a timely fashion and onbudget, we have dedicated approximately 40 full-time employees to the project, alongwith third-party consultants.

ManufacturingExpertiseWe specialize in manu-facturing products thatrequire unique facilities,processes or expertise;and are committed tomaking significant invest-ments in plant andequipment to give us acompetitive edge.

14

We also invested in plant and equipment to increase our production, laboratory,warehouse and distribution capacity. At the end of the fiscal year, we announced plansto invest an additional $15 million at our Forest, Virginia facility. We will continue toinvest in those capabilities necessary to ensure we can meet the expected demand ofour pipeline products and to handle increases in current product sales.

Management

Q Barr has always prided itself on the depth of its management expertise and itsfocus on results. How do you retain this focus as the Company grows larger,

in terms of revenues, products and people?

There is no magic to retaining focus, regardless of the size of an organization. Thechallenge is in communication. Our management team works to ensure that everymember of the Barr team understands their role in achieving our objectives, in meetingdeadlines in a timely fashion, and in ensuring that we maximize the use of availableresources. In addition, we recruit and retain the best, most highly skilled people in thepharmaceutical industry. It is the skills and commitment of our management, and ourpeople, that ensures we remain focused on meeting our objectives.

Q Corporate governance compliance remains in the news. What is the status ofBarr’s activities on these issues?

We are committed to achieving compliance with all applicable securities laws andregulations, accounting standards, controls and audit practices. We have implementedall corporate governance requirements and we will continue to focus on corporategovernance on an ongoing basis. We have posted our committee composition, charters,code of conduct, our corporate governance principles, and information related toreporting of concerns about questionable accounting practices on our website.

We have established a process whereby any person may submit a good faith com-plaint, report or concern regarding accounting or auditing matters relating to Barr.Our Audit Committee has established procedures for the receipt, retention and treat-ment of complaints and potential violations of applicable laws, rules and regulationsof the company’s accounting policies and procedures. Any person may report theirconcerns on a confidential and anonymous basis by calling an independent, toll-freehotline at 1-877-357-2572. We have retained a third-party provider to accept, verifyand log all calls received on the Ethics Line and established a process for this third-party provider to notify our General Counsel, who will log the call and advise theChairman of the Audit Committee of the call.

These compliance activities occupy substantial management and board attention,and we are committed to full compliance.

ResearchLast year we invested$128.4 million in genericand proprietary productdevelopment, to ensurea steady stream of newproduct approvals.

Alternative for the Treatment of AIDS

15

In December 2004, the FDA approved Barr’s appli-cation to market a generic version of Bristol-MyersSquibb’s Videx® EC (Didanosine) Delayed-releaseCapsules, following expedited review underthe President’s Emergency Plan for AIDS Relief(PEPFAR). The product was part of a patentchallenge. Barr was the first to file its application,and received 180 days of exclusivity.

Videx® EC, usedin combination withother antiretroviralagents, is indicated for thetreatment of HIV-1 infectionin adults. Expedited approval of this importantmedicine in the fight against AIDS enabled Barr tobring a more cost-effective version to patients.HIV-1 is the major cause of AIDS in the world, andit is estimated that more than 40 million people areinfected worldwide.

16

Challenges in 2006

Q Competition from new markets and consolidation seem to be among thekey issues in the generic industry, long-term. What are your thoughts on

these issues?

There are really several issues here. The number of potentially profitable genericproducts available is finite. In addition, the trend by brand companies to increase thenumber of patents protecting products has grown dramatically. Both of these actionslimit the universe of generic products with substantial profit potential.

In addition, we are seeing increased potential competition from other internationalmarkets. As a result, it is more difficult to be a true generic player. This is leading toconsolidation within the industry, as well as the move by leading companies, such asBarr, into proprietary product development or the challenging of patents on brandproducts. As a result, the skill set needed for success in the industry has been raisedsignificantly. Barr will be a player in acquisitions and other strategic business ventures,as appropriate, to ensure our ability to deliver long-term shareholder value.

Q What issues at the federal or state governmental levels could impact the futureof the Company?

On a federal level, issues such as patent reform, authorized generics and importationrepresent near-term challenges for our industry. On the state level, undoubtedly theimplementation of the Medicare prescription drug benefit will result in significant tur-moil. Barr has, and will continue, to play a leading role in the resolution of theseissues, and in continuing to communicate the value of increased generic utilization tohelp both federal and state governments expand access to healthcare and prescriptionmedicines while seeking to cap and lower costs.

The long-term issue will involve the passage of regulations or legislation that will openthe biopharmaceutical universe to generic competition. Barr will continue to work withfederal legislators, policymakers and regulators on the codification of a Hatch/Waxman-like process that will support the approval of affordable generic biopharmaceuticals.Once this process is in place, we intend to lead the battle in building legislator, regulatorand consumer confidence in the safety, sameness and savings of generic biopharmaceuti-cals, just as we did in the formation of the traditional generic industry.

Q How would you sum up fiscal 2005?

First, I would like to thank our management team and our approximately 1,850employees for their exceptional efforts and focus on achieving our internal objectives.I would also like to thank our shareholders for their continued confidence in ourstrategies for long-term success. I am proud of our accomplishments in the generic andproprietary operations, in our labs and manufacturing facilities, and in the businessinitiatives we have undertaken to position the company for future growth. Fiscal 2005was a strong year for the company, and has set the stage for additional growth as wemove into fiscal 2006 and beyond. ■

Partnering withGovernmentWe are committed toworking with federal andstate legislators to lowerprescription drug costs,and open the door forthe approval of genericversions of biopharma-ceuticals.

17

18 Management’s Discussion and Analysis of Financial Conditionand Results of Operations

33 Consolidated Balance Sheets

34 Consolidated Statements of Operations

35 Consolidated Statements of Shareholders’ Equity

36 Consolidated Statements of Cash Flows

37 Notes to the Consolidated Financial Statements

54 Report of Independent Registered Public Accounting Firm

55 Management’s Report on Internal Control Over Financial Reporting

55 Selected Financial Data

56 Reconciliation of GAAP EPS to Adjusted EPS for the Fiscal YearsEnded June 30, 2005 and 2004

57 Board of Directors

57 Management Team

57 General Shareholders’ Information

Financial Review

18

Executive Overview

We are a specialty pharmaceutical company that develops,markets and sells both generic and proprietary (or branded)pharmaceutical products. We have a deep, diverse andprofitable generic product portfolio, and have diversified ouroperations by developing and acquiring several proprietaryproducts. Sales of generic products accounted for 73% of ourproduct sales in fiscal 2005, while sales of our proprietaryproducts grew from $57.7 million in fiscal 2003, accountingfor just 6% of our product sales that year, to $278.8 millionin fiscal 2005, accounting for 27% of product sales.

Generic ProductsFor many years, we have successfully utilized a strategy ofdeveloping the generic versions of branded products thatpossess some combination of unique factors that we believehave the effect of limiting competition for generics. Suchfactors include difficult formulation, complex and costlymanufacturing requirements or limited raw material avail-ability. To date, our strategy has focused on developing solidoral dosage forms of products. By targeting products withsome combination of these unique factors, we believe thatour generic products will, in general, be less affected by theintense and rapid pricing pressure often associated with morecommodity-type generic products. As a result of this focusedstrategy, we have been able to successfully identify, developand market generic products that generally have few com-petitors or that are able to enjoy longer periods of limitedcompetition and thus generate profit margins higher thanthose often associated with commodity-type generic products.The development and launch of our generic oral contracep-tive products is an example of our generic developmentstrategy. While we believe there are more tablet and capsuleproducts that may fit our “barrier-to-entry” criteria, werecognize that finding highly profitable generic tablet andcapsule products that will grow our generics business isdifficult. As a result, we have recently expanded our develop-ment resources to include non-tablet and capsule products(such as patches, sterile ophthalmics and nasal sprays).

Challenging the patents covering certain brand productscontinues to be an important component of our genericstrategy. For many products, the patent provides the uniquebarrier that we seek to identify in our product selectionprocess. We try to be the first company to initiate a patentchallenge because in certain cases, we may be able to obtain180 days of exclusivity for selling the generic version of theproduct. For example, this occurred with fluoxetine, ourgeneric version of Eli Lilly’s Prozac®. If we do receive exclu-

sivity for a product, we typically experience significant rev-enues and profitability associated with that product for thesix-month exclusivity period, but at the end of that periodexperience significant decreases in our revenues and marketshare associated with the product as other generic competi-tors enter the market. This happened with our fluoxetineproduct after expiration of our generic exclusivity period.Our record of successfully resolving patent challenges hascontributed to our growth, but has created periods of rev-enue and earnings volatility and will likely do so in thefuture. While earnings and cash flow volatility may resultfrom the launch of products subject to patent challenges, weremain committed to this part of our business.

Macroeconomic factors also continue to favor the use ofgeneric pharmaceutical products. The aging population, ris-ing health care costs and the vigilance of health careproviders, insurance companies and others to lower suchcosts have helped drive an increase in the substitution oflower-cost generic products for higher-cost brand products.As evidence of this, the percentage of overall prescriptionsfilled with generic products grew from 43% in 2000 to 53%by 2004, and is predicted to continue to rise in the future.

Proprietary ProductsTo help diversify our existing revenue base and to providefor additional long-term opportunities, we initiated a pro-gram more than five years ago to develop and market propri-etary pharmaceutical products. We formalized this programin 2001 by establishing Duramed Research. Today we have asubstantial number of employees dedicated to the develop-ment and marketing of our proprietary products includingapproximately 300 sales representatives that promote directlyto physicians four of our products and two products relatedto the Co-Promotion Agreement with Kos Pharmaceuticals.In addition, we sell but do not actively market seven otherproprietary products.

Growth in proprietary product sales over the last threefiscal years has been accomplished through productacquisitions and through higher sales of our first internally-developed proprietary product, SEASONALE®.

CompetitionOne of our greatest challenges is continuing to stay ahead ofthe competition, both for generic and proprietary products.Our successful generic product strategy has attracted newcompetitors seeking to launch competing generic productsas well as to be “first to file” for potentially lucrative patentchallenges. For example, other generic pharmaceuticalcompanies have recently started developing and marketingcompeting generic oral contraceptives in order to capturesome of our market share. In addition, there has been anincrease in the number of competitors in the generic industry

Management’s Discussion and Analysis of Financial Conditionand Results of Operations (dollars in millions)

19

that are based outside U.S., with several of such competitorsbased in India. Many of these companies claim to have equiva-lent technological capabilities to U.S.-based generic companiesbut at significant cost advantages over their U.S. counterparts.

Also, as a detriment to the value of the patent challengestrategy of Barr and other leading generic manufacturers,brand pharmaceutical companies continue to partner with cer-tain generic drug companies to license a so-called “authorizedgeneric” to the generic drug company. The use of authorizedgenerics by certain brand and generic companies underminesthe value of the 180 day exclusivity period enjoyed by the firstcompany to file an ANDA containing a Paragraph IV certifica-tion by providing another company with the ability to havethe generic product on the market at the same time.

Finally, as our proprietary pharmaceutical products grow,we anticipate that competing generic pharmaceutical compa-nies will challenge the patents protecting our branded prod-ucts. For example, one of our competitors, Watson, has fileda Paragraph IV certification challenging the patent onSEASONALE.

To address these and other challenges, we continue to (1)invest aggressively in research and development, (2) developand launch new generic and proprietary products and (3)maintain an active acquisition and licensing effort to comple-ment our internal development activities.

Comparison of the fiscal years ended June 30, 2005and June 30, 2004

The following table sets forth revenue data for the fiscal yearsended June 30, 2005 and 2004:

Change

($’s in millions) 2005 2004 $ %

Generic products:

Distributed alternative

brands:(1) $ – $ 385.3 $(385.3) -100%

Oral contraceptives 396.6 403.9 (7.3) -2%

Other generic(2) 354.8 361.4 (6.6) -2%

Total generic products 751.4 1,150.6 (399.2) -35%

Proprietary products 278.8 146.1 132.7 91%

Total product sales 1,030.2 1,296.7 (266.5) -21%

Alliance, development

and other revenue 17.2 12.4 4.8 39%

Total revenues $1,047.4 $1,309.1 $(261.7) -20%

(1)Reflects sales of Ciprofloxacin sold during Bayer’s pediatric exclusivityperiod which ended on June 9, 2004.

(2)Includes sales of Ciprofloxacin after June 9, 2004.

Revenues – Product Sales

Product sales for the year ended June 30, 2005 decreasedas compared to the prior year primarily due to the expecteddecline in sales of our distributed version of Ciprofloxacin,as discussed in detail below. Partially offsetting the decreasein Ciprofloxacin sales was a significant increase in sales ofour proprietary products.

Generic ProductsDistributed Alternative Brands (Ciprofloxacin)On June 9, 2003 we began distributing Ciprofloxacinhydrochloride tablets and oral suspension pursuant to alicense from Bayer Corporation obtained under a 1997settlement of a patent challenge we initiated regardingBayer’s Cipro® antibiotic. In September 2003, we entered intoan amended supply agreement with Bayer that enabled usto distribute Ciprofloxacin during and after Bayer’s periodof pediatric exclusivity, which ended on June 9, 2004. As aresult of the exclusivity we enjoyed, Ciprofloxacin was ourlargest selling product in fiscal 2004. We have shared andcontinued to share one-half of our profits, as defined, fromthe sale of Ciprofloxacin with Aventis, the contractual succes-sor to our partner in the Cipro patent challenge case. Uponexpiration of Bayer’s period of pediatric exclusivity on June9, 2004, as expected, several other competing Ciprofloxacinproducts were launched. As a result of the flood of compet-ing products, our market share and product pricing declineddramatically for Ciprofloxacin almost immediately. Sincethe expiration of the exclusivity period, we have includedsales of Ciprofloxacin in the “Other generic” line item in thetable above. Such sales were not significant for fiscal 2005.

Oral ContraceptivesSales of our generic oral contraceptive products decreased2% in fiscal 2005 compared to fiscal 2004. Price declines andlower volumes resulting from additional competitors reducedsales on certain of our products, mainly Apri and Aviane,and a slowdown in the growth rate of generic substitutionmore than offset (1) full year contributions from productslaunched during fiscal 2004, (2) two new products launchedin fiscal 2005 and (3) market share gains on other existingproducts.

Oral contraceptives are the most common method ofreversible birth control, used by up to 82% of women in theUnited States at some time during their reproductive years.Oral contraceptives have a long history with widespread useattributed to many factors including efficacy in preventingpregnancy, safety and simplicity in initiation and discontinua-tion, medical benefits and relatively low incidence of sideeffects. From fiscal 2002 to fiscal 2004, sales of our genericoral contraceptive products more than quadrupled. This

20

growth was fueled by new product launches, the addition ofnew customers and by increasing rates of generic substitu-tion. We currently manufacture and market 22 generic oralcontraceptive products under trade names, two of which welaunched during the fiscal year ended June 30, 2005. Thisportfolio now represents nearly all oral contraceptives thatare eligible for generics. Additionally, the growth in genericsubstitution rates for this heavily genericized portfolio ofproducts slowed, even as we continued to gain market shareon certain products within the portfolio. We anticipate thatthese trends will continue in fiscal 2006 as competitorslaunch new products and as the portfolio continues to expe-rience a slowing of overall growth in generic substitution.However, despite our expectation that sales of our genericoral contraceptive portfolio will decline in fiscal 2006 versusfiscal 2005, we believe that we are well positioned to main-tain market share for many of our products and that ourportfolio of oral contraceptives will continue to be a signifi-cant component of our revenues in fiscal 2006.

Generic Products – OtherSales of other generic products decreased 2% in fiscal2005 as compared to the prior year period, as sales fromnew products launched since the end of last year, includingDidanosine and Metformin XR 750mg, were more thanoffset by declines in other existing product sales. The declinein other existing product sales was primarily due to a signifi-cant decrease in sales of our Dextroamphetamine groupof products due to both declining volumes and lower pricescaused by the launch of competing versions in late 2004. InApril 2005, our generic exclusivity period on Metformin XR750mg ended and several other generic companies launchedcompeting versions of the product. As a result, we experi-enced a significant decline in sales of Metformin XR 750mgand would expect that decline to continue during fiscal 2006.However, we expect that higher sales of Didanosine andsales from our generic version of DDAVP, which we launchedin July 2005, will more than offset these declines leading tohigher sales of our other generic products in fiscal 2006.

Proprietary ProductsSales of our proprietary products almost doubled in fiscal2005 as compared to the prior year. This increase relatesprimarily to: (1) higher sales of SEASONALE, which totaled$87.2 million for the fiscal year, reflecting higher unit sales insupport of prescription growth and higher pricing comparedto last year; (2) full year sales of Loestrin/Loestrin Fe andPlan B which we acquired in February 2004 and March2004, respectively; and (3) sales of Nordette and Prefest,which we acquired in November 2004 and December 2004,respectively.

SEASONALE prescriptions, according to IMS data,topped 800,000 for our fiscal year ended June 30, 2005, a370% increase over prescriptions in the prior fiscal year. Thisincrease is a direct result of our significant marketing initia-tives, including direct-to-consumer advertising and the detail-ing efforts by our Women’s Healthcare Sales force. Whilewe look for growth in fiscal 2006 for SEASONALE prescrip-tions and sales, we expect much lower growth rates thanthose achieved in fiscal 2005.

We have been active in acquiring proprietary productsover the last two fiscal years and the contribution fromthose products has increased our proprietary revenues sub-stantially over that period. Certain of the products whichwe have acquired no longer enjoy patent protection and areexperiencing declining prescription volumes. As a result,while these products are expected to still generate healthymargins and predictable cash flows, we do not expect themto generate the year-over-year sales growth we experienced infiscal 2005. In fact, some may show year-over-year decreasesin sales. As a result, growth in our proprietary productsales in fiscal 2006 will be mainly dependent on growth inSEASONALE, Cenestin and Plan B, and the launch of ourEnjuvia product during the second half of fiscal 2006.

Cost of Sales

Our cost of sales includes the cost of products we purchasefrom third parties, our manufacturing and packaging costsfor products we manufacture, profit sharing or royalty pay-ments made to third parties, including raw material suppliersand any changes to our inventory reserve. Amortization costsarising from the acquisition of product rights and our distri-bution costs are included in selling, general and administra-tive costs.

Product mix plays a significant role in our quarterly andannual overall gross margin percentage. In the past, our over-all gross margins have been negatively impacted by sales oflower-margin distributed versions of products such asCiprofloxacin and Tamoxifen, which were manufactured forus by brand companies and distributed by us under the termsof the respective patent challenge settlement arrangements.

The following table sets forth cost of sales data in dollarsas well as the resulting gross margins, for the two yearsended June 30, 2005 and 2004:

Change

($’s in millions) 2005 2004 $ %

Generic products $264.8 $604.6 $(339.8) -56%

Gross margin 65% 47%

Proprietary products $ 39.3 $ 28.1 $ 11.2 40%

Gross margin 86% 81%

Total cost of sales $304.1 $632.7 $(328.6) -52%

Gross margin 70% 51%

21

The decrease in total cost of sales, on a dollar basis, forthe year ended June 30, 2005, as compared to the prior year,was primarily due to the year-over-year decrease in sales ofCiprofloxacin, which in the prior year we had purchasedfrom Bayer.

Margins on our generic products increased significantlyin fiscal 2005 due mainly to the decrease in year-over-yeardistributed Ciprofloxacin sales. As a distributed product forwhich we shared the profits with our partner in the Cipropatent challenge, Ciprofloxacin had a higher cost of sales anda lower margin than our other products.

Margins on our proprietary products increased in fiscal2005 compared to fiscal 2004 due to increased sales ofhigher margin products, primarily SEASONALE and Loestrin/Loestrin Fe.

Selling, General and Administrative Expense

The following table sets forth selling, general and administrativeexpense data for the two years ended June 30, 2005 and 2004:

Change

($’s in millions) 2005 2004 $ %

Selling, general and

administrative $298.9 $314.5 $(15.6) -5%

Charges included in general

and administrative $ 63.2 $ 96.6 $(33.4) -35%

Lower selling, general and administrative expenses in fis-cal 2005 compared to last year were primarily due to lower2005 charges compared to 2004 charges partially offset by(1) $8.1 million in higher marketing costs in fiscal 2005associated with our proprietary product portfolio and (2)$7.1 million in higher product intangible amortizationexpense in fiscal 2005 due to full year amortization onproducts purchased in the prior year and amortization ofproducts purchased in the current year.

Charges taken in the twelve months ended June 30, 2004and 2005 are as follows:

Fiscal 2004:(1) A $16 million valuation allowance we established in

September 2003 for our loans to Natural Biologics, LLC,the raw material supplier for our generic equine-basedconjugated estrogens product, as the result of an unfavor-able court decision rendered in September 2003;

(2) The February 2004 write-off of $4.2 million associatedwith the acquisition of certain emergency contraceptionassets from Gynetics, Inc;

(3) An arbitration panel’s decision in June 2004 to awardSolvay Pharmaceuticals, Inc. $68 million in damages on aclaim that we improperly terminated an agreement withSolvay; and

(4) An $8.5 million charge in June 2004 related to costs asso-ciated with our settlement of the Estrostep and Femhrtpatent challenge litigation against Galen.

Fiscal 2005:On June 15, 2005 we entered into a non-binding Letterof Intent (“LOI”) with Organon (Ireland) Ltd., OrganonUSA and Savient Pharmaceuticals, Inc. to acquire the NDAfor Mircette, obtain an exclusive royalty free license to sellMircette and Kariva in the United States and dismiss allpending litigation between the parties in exchange for a pay-ment by us of up to $155 million. The parties will not becontractually bound unless and until they negotiate and exe-cute definitive agreements. If consummated, the transactionwould permit us to promote Mircette through our Duramedsales force, which could increase sales of both Mircette andKariva. If the transaction is not consummated, we expect tocontinue to vigorously defend our position in the Mircettelitigation.

In July 2005, the parties made the required filings with theFederal Trade Commission (“FTC”) regarding the proposedtransaction. On August 1, 2005, the FTC issued a “secondrequest,” asking the parties to provide detailed informationconcerning the proposed transaction.

The proposed transaction is contingent upon both satis-factory completion of the FTC’s Hart Scott Rodino reviewand the negotiation of mutually satisfactory definitive agree-ments. However, because the proposed transaction includes,as one of its components, a payment in settlement of litiga-tion, it is presumed under GAAP to give rise to a “probableloss,” as defined in Statement of Financial AccountingStandards No. 5, “Accounting for Contingencies”. In consul-tation with outside advisors and based on preliminary valua-tions of the assets we would acquire if the transaction closeson the terms presently contemplated, we have recorded acharge of $63.2 million as of June 30, 2005 to reflect theproposed litigation settlement. We may reverse the charge, inwhole or in part, in the future if the transaction does notclose and we prevail in the litigation or are ultimately heldliable for a lesser amount of damages. If the transaction doesnot close and an unfavorable verdict were to be renderedagainst us at trial, the ultimate amount of damages payableby us could be significantly more or less than the $63.2 mil-lion charge we have recorded in connection with the pro-posed litigation settlement.

22

Research and Development

The following table sets forth research and developmentexpenses for the two years ended June 30, 2005 and 2004:

Change

($’s in millions) 2005 2004 $ %

Research and development $128.4 $169.0 $(40.6) -24%

Charges included in research

and development $ – $ 68.2 $(68.2) -100%

For the year ended June 30, 2004 our total researchand development costs reflected charges relating to strategicacquisitions or similar activities including: (1) a write-offof $22 million in March 2004 resulting from our agreement toacquire Schering’s rights and obligations under a ProductDevelopment and License Agreement that had been capitalizedat the time of our acquisition of Enhance Pharmaceuticals, Inc.in June 2002; (2) a write-off of $10 million for in-processresearch and development acquired in connection with ouracquisition of Women’s Capital Corporation in February 2004;and (3) a write-off of $36 million of in-process research anddevelopment costs in connection with our purchase of substan-tially all of the assets of Endeavor Pharmaceuticals, Inc. inNovember 2003.

The remaining $28 million increase in research and devel-opment for the year ended June 30, 2005 as compared tothe prior year was primarily due to: (1) $9.1 million in higherthird party development costs, including a $5.0 millionpayment to PLIVA related to the development, supply andmarketing agreement that we entered into in March 2005 forthe generic biopharmaceutical Granulocyte Colony StimulatingFactor (“G-CSF”); (2) $9.4 million in higher bioequivalencestudy costs, reflecting both an increase in the number andthe cost of the studies; (3) $5.0 million in higher internalproduction costs in support of internal development projects;and (4) $4.5 million in higher headcount costs in supportof the increased number of products in development.

Income Taxes

The following table sets forth income tax expense and theresulting effective tax rate stated as a percentage of pre-taxincome for the two years ended June 30, 2005 and 2004:

Change

($’s in millions) 2005 2004 $ %

Income tax expense $114.9 $71.3 $43.6 61%

Effective tax rate 34.8% 36.7%

The effective tax rate for fiscal 2005 was favorablyimpacted by the completion of several tax audits, the changeof the mix in income between various taxing jurisdictions

and the enactment of favorable tax legislation in certainjurisdictions.

As indicated above, we have recently completed an auditby the IRS for our federal income tax returns for fiscal years2002 and 2003. The resolution favorably impacted oureffective tax rate for the fiscal year but did not have a materi-al effect on our financial position or liquidity. Periods priorto 2002 have either been audited or are no longer subjectto audit. We are currently being audited by the IRS for ourfiscal year ended June 30, 2004.

Comparison of the fiscal years ended June 30, 2004and June 30, 2003

The following table sets forth revenue data for the fiscalyears ended June 30, 2004 and 2003:

Change

($’s in millions) 2004 2003 $ %

Generic products:

Distributed alternative

brands:(1)

Ciprofloxacin $ 385.3 $111.4 $ 273.9 246%

Tamoxifen(2) – 112.5 (112.5) -100%

Oral contraceptives 403.9 274.4 129.5 47%

Other generic(3) 361.4 338.9 22.5 7%

Total generic products 1,150.6 837.2 313.4 37%

Proprietary products 146.1 57.7 88.4 153%

Total product sales 1,296.7 894.9 401.8 45%

Alliance, development

and other revenue 12.4 8.0 4.4 55%

Total revenues $1,309.1 $902.9 $ 406.2 45%

(1)Distributed alternative brands are distributed by us under terms ofagreements entered into as part of patent challenge settlements.Therefore, for reporting purposes, they are classified as Genericproducts.

(2)Reflects sales of Tamoxifen acquired from innovator.

(3)Includes sales of Tamoxifen manufactured by Barr.

Revenues – Product Sales

Product sales for the year ended June 30, 2004 increased ascompared to the prior year primarily due to the sales of ourdistributed version of Ciprofloxacin and to increased sales ofour generic and proprietary products, which more than offsetthe large decline in sales of our distributed version ofTamoxifen.

Generic ProductsCiprofloxacinOn June 9, 2003, we began distributing Ciprofloxacinhydrochloride tablets and oral suspension pursuant to alicense from Bayer obtained under a 1997 settlement of a

23

patent challenge we initiated against Bayer’s Cipro® antibiotic.In September 2003, we signed an Amended Supply Agreementwith Bayer that enabled us to distribute Ciprofloxacin duringand after Bayer’s period of pediatric exclusivity, which endedon June 9, 2004. As a result, Ciprofloxacin was our largestselling product in fiscal 2004. We have shared one-half of ourprofits, as defined, from the sale of Ciprofloxacin with Aventis,the contractual successor to our partner in the Cipro patentchallenge case. Bayer’s period of pediatric exclusivity expiredon June 9, 2004 and, as we expected, several other competingCiprofloxacin products were launched.

TamoxifenFor most of the first six months of fiscal 2003 we sold adistributed version of Tamoxifen that we purchased fromAstraZeneca under the terms of a 1993 Supply andDistribution Agreement entered into as part of a patent chal-lenge settlement. This Agreement ended in December 2002.We began selling our manufactured Tamoxifen product whenAstraZeneca’s pediatric exclusivity for Nolvadex ended onFebruary 20, 2003. Therefore, we recorded no sales from adistributed version of Tamoxifen in fiscal 2004.

Oral ContraceptivesSales of our generic oral contraceptive products increasedthroughout fiscal 2004 and by June 2004, we became thelargest supplier of oral contraceptives in the U.S. as deter-mined by prescription market share data provided byIMS America.

The revenue growth in fiscal 2004 was fueled by (1)increasing volumes resulting from growth in market shareby products launched in prior periods and (2) first year salesof new generic oral contraceptives launched during fiscal2004. The largest new product addition was Tri-Sprintec, ourgeneric equivalent to Ortho’s Tri-Cyclen oral contraceptive.We launched Tri-Sprintec in December 2003 in accordancewith the terms of a patent challenge settlement we enteredinto with Ortho.

Generic Products – OtherSales of other generic products increased approximately 7% infiscal 2004 as compared to the prior year period, primarily dueto sales of our Mirtazapine Orally Disintegrating Tablet, whichwe launched in December 2003, and sales of Claravis®, whichwe launched in May 2003. These increases were partially offsetby a significant decline in sales of our Dextro salt combo prod-uct due to lower pricing and lower volumes resulting from theentry of two additional generic competitors.

Proprietary ProductsSales of our proprietary products more than doubled in fiscal2004 as compared to the prior year. This increase relatesprimarily to: (1) sales from the four products we purchasedfrom Wyeth in June 2003; (2) the launch of SEASONALE;(3) increased sales of Cenestin; and (4) sales of Loestrin/Loestrin Fe, which we purchased from Galen (Chemicals)Limited (“Galen”) in March 2004.

In September 2003 we received approval for SEASONALE.We began promoting SEASONALE directly to physicians inNovember 2003 and initiated our direct-to-consumer televi-sion and print advertising program during our fourth quarter.Demand for the product as measured by prescription dataobtained from IMS America rose from 1,736 per week forthe week ended December 26, 2003 to 12,731 for the weekended July 30, 2004.

Sales of Cenestin increased at a higher than expected rateof 36% in fiscal 2004 compared to fiscal 2003 primarilydue to year-over-year price increases of approximately 24%,the launch of one additional strength and customer buyingpatterns, which more than offset a 9% decline in Cenestinprescriptions. Prescription declines began after the results ofthe Women’s Health Initiative (“WHI”) study was publishedin July 2002 and continued through fiscal 2004. Since July2002, Cenestin prescriptions declined at a slower rate thanthose written for competing conjugated estrogen products,thus allowing us to increase our market share to 6.8% as ofJune 30, 2004 compared to 5.6% as of June 30, 2003.

Cost of Sales

The following table sets forth cost of sales data in dollars aswell as the resulting gross margins, for the two years endedJune 30, 2004 and 2003:

Change

($’s in millions) 2004 2003 $ %

Generic products $604.6 $415.0 $189.6 46%

Gross margin 47% 50%

Proprietary products $ 28.1 $ 9.1 $ 19.0 209%

Gross margin 81% 84%

Total cost of sales $632.7 $424.1 $208.6 49%

Gross margin 51% 53%

The increase in total cost of sales, on a dollar basis, forthe year ended June 30, 2004, as compared to the prior yearwas primarily due to increased product sales, principallyrelating to Ciprofloxacin.

Margins on our generic products declined slightly in fiscal2004 due mainly to the higher percentage of Ciprofloxacinsales in fiscal 2004 compared to fiscal 2003. As a distributedproduct that had a profit split paid to our partner,

Ciprofloxacin had a higher cost of sales and a lower marginthan our other products.

Margins on our proprietary products declined in fiscal2004 compared to fiscal 2003 as increased sales of somewhatlower margin products, including the products acquired fromWyeth in late fiscal 2003, more than offset higher sales ofCenestin and SEASONALE.

Selling, General and Administrative Expense

The following table sets forth selling, general and administrativeexpense data for the two years ended June 30, 2004 and 2003:

Change

($’s in millions) 2004 2003 $ %

Selling, general and

administrative $314.5 $161.0 $153.5 95%

Charges included in general

and administrative $ 96.6 $ 20.0 $ 76.6 383%

Selling, general and administrative expenses for the yearended June 30, 2004 included charges related to strategicacquisitions or other similar activities including: (1) a $16million valuation allowance we established in September2003 for our loans to Natural Biologics, LLC, the raw mate-rial supplier for our generic equine-based conjugated estro-gens product, as the result of an unfavorable court decisionrendered in September 2003; (2) the February 2004 write-offof $4.2 million associated with the acquisition of certainemergency contraception assets from Gynetics, Inc; (3) anarbitration panel’s decision in June 2004 to award SolvayPharmaceuticals, Inc. $68 million in damages on a claim thatwe improperly terminated an agreement with Solvay; and (4)an $8.5 million charge in June 2004 related to costs associat-ed with our settlement of the Estrostep and Femhrt patentchallenge litigation against Galen. Included in the year endedJune 30, 2003 was a $20 million contingent attorney fee paidin connection with a litigation settlement with Wyeth.

The remaining increase in selling, general and administra-tive expenses for the year ended June 30, 2004 as comparedto the prior year period was primarily due to: (1) increasedmarketing costs for SEASONALE of $28 million; (2) highercosts of $12 million associated with the nearly doubling ofour women’s healthcare sales force; (3) $14 million in higherlegal costs, primarily related to patent matters, the Solvayarbitration and product liability matters; and (4) $8 millionof increased information technology costs, including consult-ing costs related to the initial phases of designing and imple-menting our new enterprise resource planning system.

Research and Development

The following table sets forth research and developmentexpenses for the two years ended June 30, 2004 and 2003:

Change

($’s in millions) 2004 2003 $ %

Research and development $169.0 $91.2 $77.8 85%

Charges included in

research and development $ 68.2 $ 3.9 $64.3 1649%