barclays ceo energy-power conference · original assumptions: 2017 wti $50bbl /nymex $2.75mcf and...

TRANSCRIPT

CONFERENCESEPTEMBER 4-5, 2018

BARCLAYS CEO ENERGY-POWER

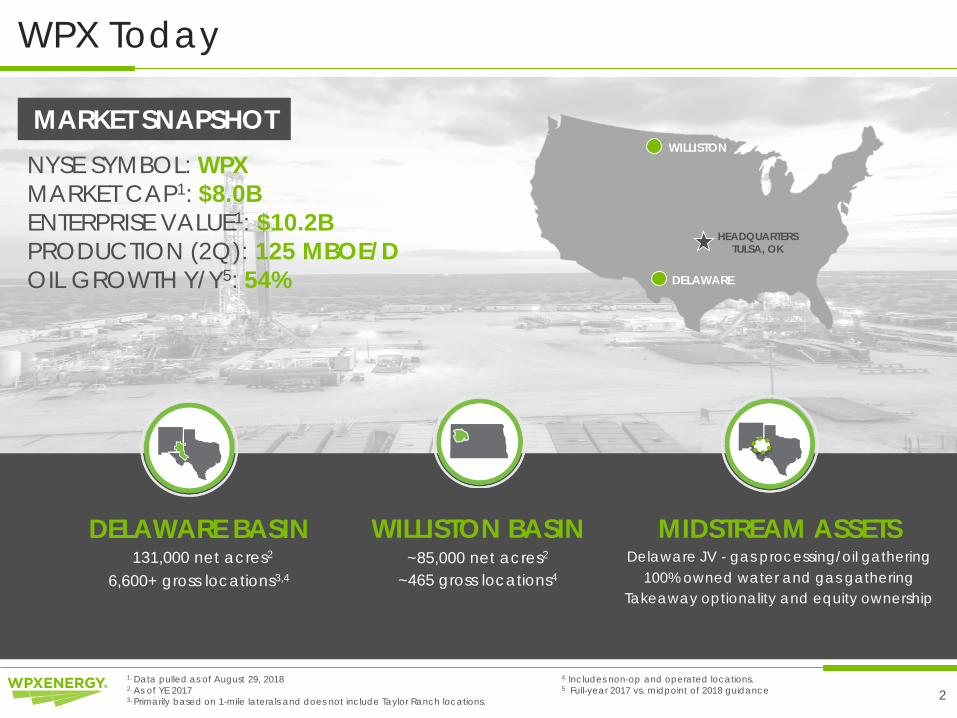

WPX Today

2

HEADQUARTERSTULSA, OK

DELAWARE BASIN~131,000 net acres2

6,600+ gross locations3,4

WILLISTON BASIN~85,000 net acres2

~465 gross locations4

MIDSTREAM ASSETSDelaware JV - gas processing/oil gathering

100% owned water and gas gathering Takeaway optionality and equity ownership

NYSE SYMBOL: WPXMARKET CAP1: $8.0BENTERPRISE VALUE1: $10.2BPRODUCTION (2Q): 125 MBOE/D OIL GROWTH Y/Y5: 54%

MARKET SNAPSHOT

4. Includes non-op and operated locations. 5 Full-year 2017 vs. midpoint of 2018 guidance

1. Data pulled as of August 29, 20182. As of YE 20173. Primarily based on 1-mile laterals and does not include Taylor Ranch locations.

DELAWARE

WILLISTON

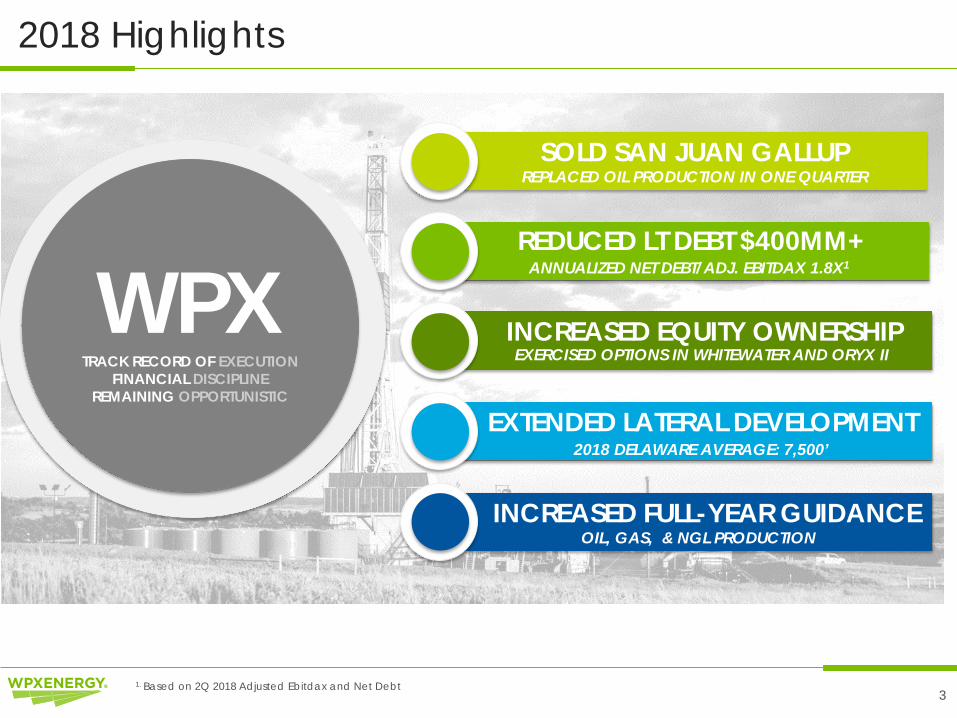

2018 Highlights

3

WPXTRACK RECORD OF EXECUTION

FINANCIAL DISCIPLINEREMAINING OPPORTUNISTIC

INCREASED FULL-YEAR GUIDANCEOIL, GAS, & NGL PRODUCTION

SOLD SAN JUAN GALLUPREPLACED OIL PRODUCTION IN ONE QUARTER

EXTENDED LATERAL DEVELOPMENT2018 DELAWARE AVERAGE: 7,500’

INCREASED EQUITY OWNERSHIPEXERCISED OPTIONS IN WHITEWATER AND ORYX II

REDUCED LT DEBT $400MM+ANNUALIZED NET DEBT/ADJ. EBITDAX 1.8X1

1. Based on 2Q 2018 Adjusted Ebitdax and Net Debt

$-

$5

$10

$15

$20

$25

$30

$35

$40

0

50

100

150

200

250

300

1Q2012

2Q2012

3Q2012

4Q2012

1Q2013

2Q2013

3Q2013

4Q2013

1Q2014

2Q2014

3Q2014

4Q2014

1Q2015

2Q2015

3Q2015

4Q2015

1Q2016

2Q2016

3Q2016

4Q2016

1Q2017

2Q2017

3Q2017

4Q2017

1Q2018

2Q2018

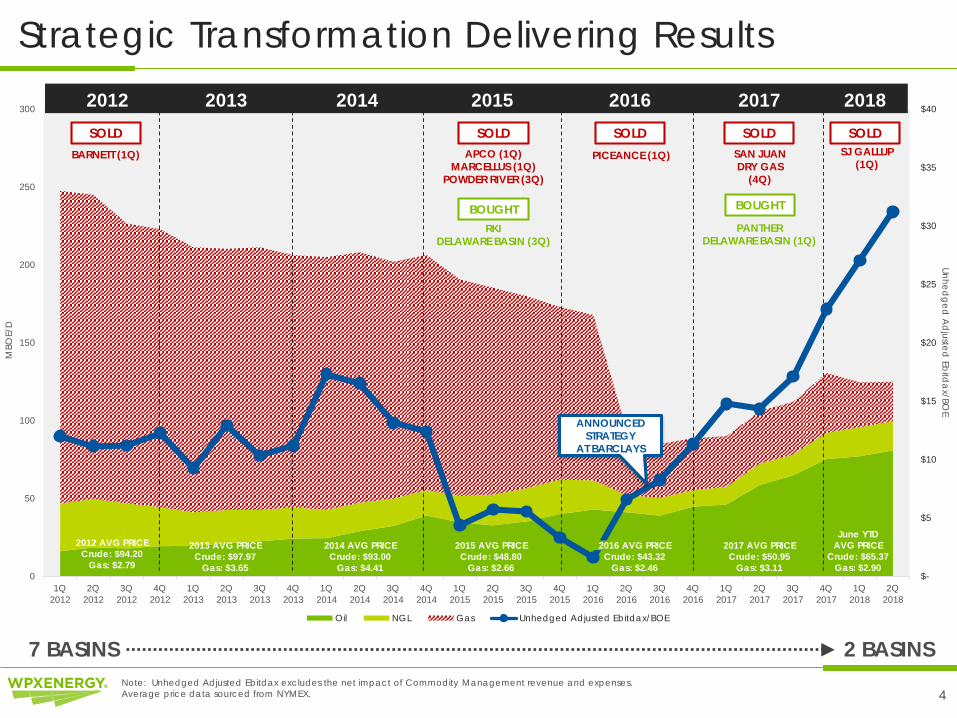

Oil NGL Gas Unhedged Adjusted Ebitdax/BOE

Strategic Transformation Delivering Results

4

Unhedged

Ad

justed Eb

itda

x/BOE

MBO

E/D

APCO (1Q)MARCELLUS (1Q)

POWDER RIVER (3Q)

PICEANCE (1Q) SAN JUAN DRY GAS

(4Q)

2012 AVG PRICECrude: $94.20

Gas: $2.79

2013 AVG PRICECrude: $97.97

Gas: $3.65

2014 AVG PRICECrude: $93.00

Gas: $4.41

2015 AVG PRICECrude: $48.80

Gas: $2.66

2017 AVG PRICECrude: $50.95

Gas: $3.11

June YTDAVG PRICE

Crude: $65.37Gas: $2.90

BARNETT (1Q)

7 BASINS

RKIDELAWARE BASIN (3Q)

2012 2013 2014 2015 2016 2017 2018

2 BASINS

SJ GALLUP (1Q)

SOLD SOLD

BOUGHT

SOLD SOLD

BOUGHT

PANTHERDELAWARE BASIN (1Q)

SOLD

Note: Unhedged Adjusted Ebitdax excludes the net impact of Commodity Management revenue and expenses.Average price data sourced from NYMEX.

2016 AVG PRICECrude: $43.32

Gas: $2.46

ANNOUNCED STRATEGY

AT BARCLAYS

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

20

40

60

80

100

2016 2017 2018LOW CASE HIGH CASE% OIL (PREVIOUS) % OIL (ACTUAL)

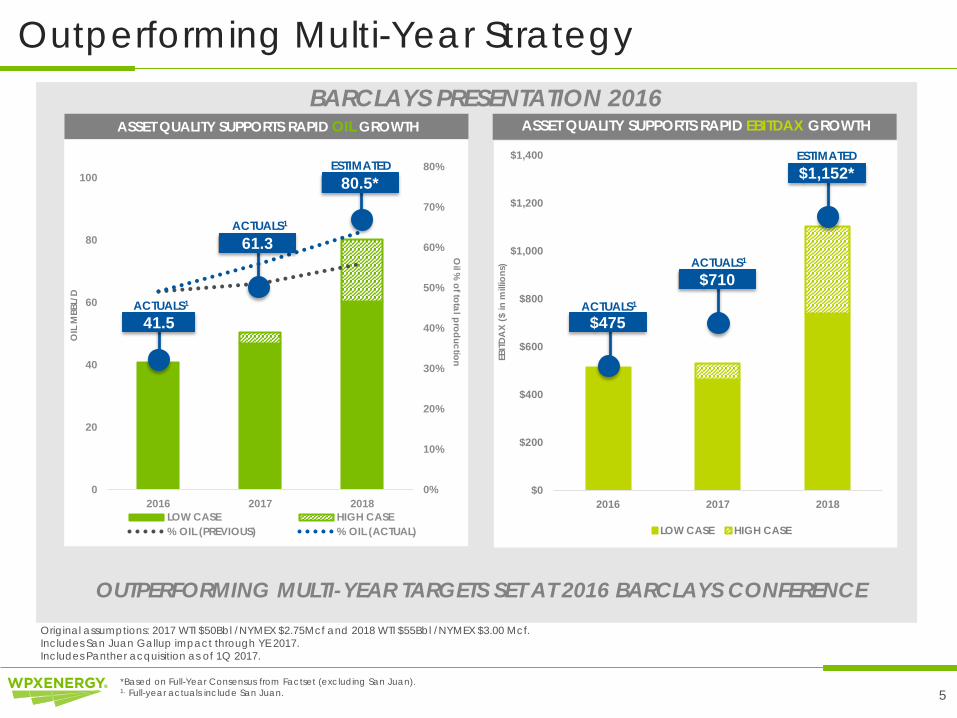

Outperforming Multi-Year Strategy

5

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2016 2017 2018

LOW CASE HIGH CASE

$710

$475

$1,152*

41.5

61.3

80.5*

*Based on Full-Year Consensus from Factset (excluding San Juan).1. Full-year actuals include San Juan.

Oil %

of total production

OIL

MBB

L/D

ASSET QUALITY SUPPORTS RAPID EBITDAX GROWTH

ACTUALS1

ACTUALS1

ESTIMATED

ACTUALS1

ACTUALS1

ESTIMATED

Original assumptions: 2017 WTI $50Bbl /NYMEX $2.75Mcf and 2018 WTI $55Bbl /NYMEX $3.00 Mcf. Includes San Juan Gallup impact through YE 2017.Includes Panther acquisition as of 1Q 2017.

ASSET QUALITY SUPPORTS RAPID OIL GROWTH

BARCLAYS PRESENTATION 2016

OUTPERFORMING MULTI-YEAR TARGETS SET AT 2016 BARCLAYS CONFERENCE

EBITD

AX

($ in

mill

ions

)

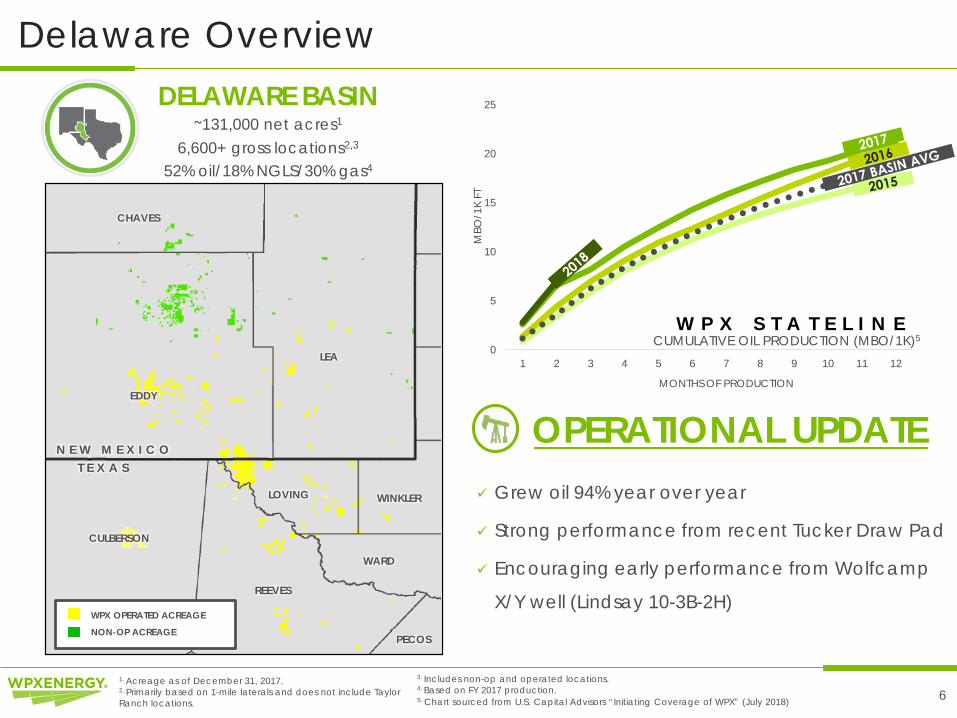

Delaware Overview

6

DELAWARE BASIN~131,000 net acres1

6,600+ gross locations2,3

52% oil/18% NGLS/30% gas4

CULBERSON

LEA

EDDY

WARD

REEVES

LOVING

PECOS

WINKLER

CHAVES

WPX OPERATED ACREAGE

NON-OP ACREAGE

N E W M E X I C OT E X A S

1. Acreage as of December 31, 2017.2. Primarily based on 1-mile laterals and does not include Taylor Ranch locations.

Grew oil 94% year over year

Strong performance from recent Tucker Draw Pad

Encouraging early performance from Wolfcamp

X/Y well (Lindsay 10-3B-2H)

OPERATIONAL UPDATE

0

5

10

15

20

25

1 2 3 4 5 6 7 8 9 10 11 12

MONTHS OF PRODUCTION

MBO

/1K

FT

W P X S T A T E L I N E CUMULATIVE OIL PRODUCTION (MBO/1K)5

5. Chart sourced from U.S. Capital Advisors “Initiating Coverage of WPX” (July 2018)

3. Includes non-op and operated locations. 4. Based on FY 2017 production.

Williston Overview

7

WILLIAMS

MOUNTRAIL

MCKENZIE

DUNN

MCLEAN

MERCER

WILLISTON BASIN~85,000 net acres1

~465 gross locations2

86% oil/7% NGLS/7% gas3

WPX OPERATED ACREAGE

0

50

100

150

200

250

300

0 30 60 90 120 150 180 210 240 270 300 330 360

CUM

MBO

E

NORMALIZED DAYS ON PRODUCTION

7

Grew oil 39% year over year

Continued strong performance from North Sunday

Island wells

Impressive well results from Mandaree South

OPERATIONAL UPDATE

1. Acreage as of December 31, 2017.2. Includes non-op and operated locations. 3. Based on FY 2017 production.

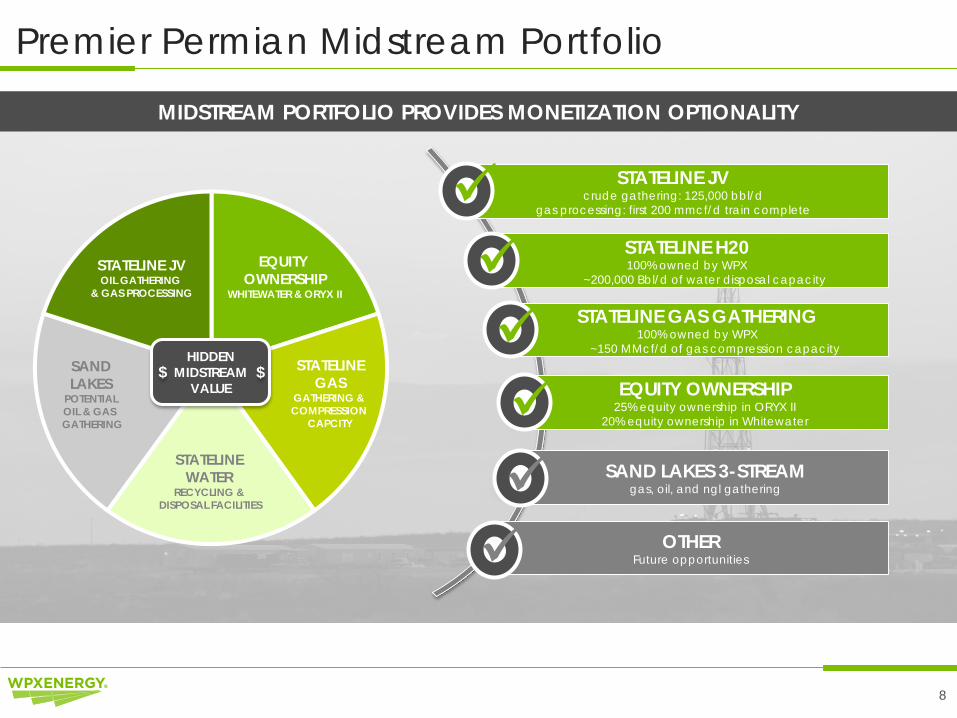

STATELINE JV crude gathering: 125,000 bbl/d

gas processing: first 200 mmcf/d train complete

Premier Permian Midstream Portfolio

8

HIDDEN MIDSTREAM

VALUE

STATELINE JVOIL GATHERING

& GAS PROCESSING

EQUITY OWNERSHIP

WHITEWATER & ORYX II

SAND LAKES

POTENTIALOIL & GAS GATHERING

STATELINE WATER

RECYCLING &DISPOSAL FACILITIES

STATELINE GAS

GATHERING & COMPRESSION

CAPCITY

STATELINE H20100% owned by WPX

~200,000 Bbl/d of water disposal capacitySTATELINE GAS GATHERING

100% owned by WPX~150 MMcf/d of gas compression capacity

EQUITY OWNERSHIP25% equity ownership in ORYX II

20% equity ownership in WhitewaterSAND LAKES 3-STREAM

gas, oil, and ngl gathering

OTHERFuture opportunities

MIDSTREAM PORTFOLIO PROVIDES MONETIZATION OPTIONALITY

$ $

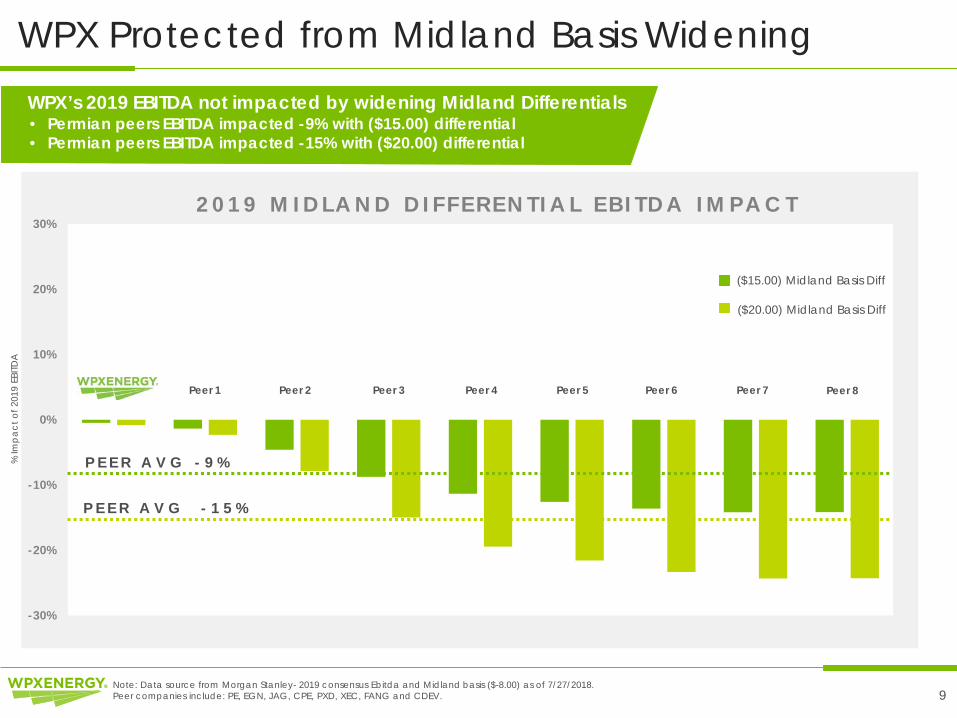

WPX Protected from Midland Basis Widening

9

-30%

-20%

-10%

0%

10%

20%

30%

($15.00) Midland Basis Diff

($20.00) Midland Basis Diff

WPX Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8

WPX’s 2019 EBITDA not impacted by widening Midland Differentials

P E E R A V G - 9 %

P E E R A V G - 1 5 %

Note: Data source from Morgan Stanley- 2019 consensus Ebitda and Midland basis ($-8.00) as of 7/27/2018. Peer companies include: PE, EGN, JAG, CPE, PXD, XEC, FANG and CDEV.

2 0 1 9 M I D L A N D D I F F E R E N T I A L E B I T D A I M P A C T

% Im

pa

ct o

f 201

9 EB

ITDA

• Permian peers EBITDA impacted -9% with ($15.00) differential• Permian peers EBITDA impacted -15% with ($20.00) differential

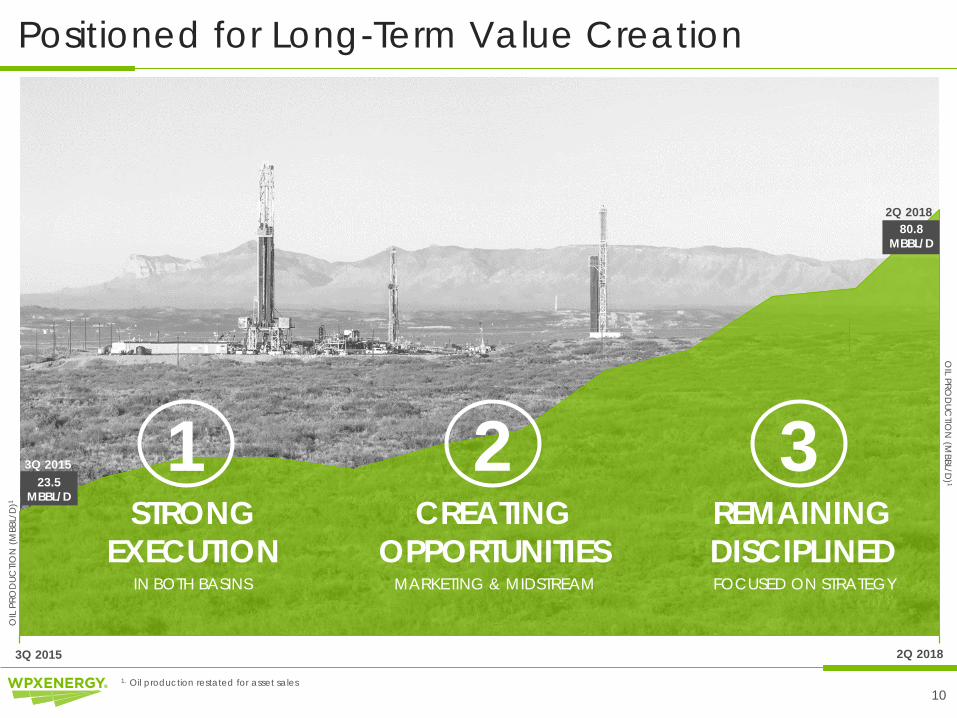

Positioned for Long-Term Value Creation

10

1 2 3STRONG

EXECUTIONCREATING

OPPORTUNITIESREMAINING DISCIPLINED

IN BOTH BASINS MARKETING & MIDSTREAM FOCUSED ON STRATEGY

0-

OIL PRO

DUC

TION

(MBBL/D

) 1

3Q 2015 2Q 2018

80.8MBBL/D

81-23.5

MBBL/D

3Q 2015

2Q 2018

1. Oil production restated for asset sales

OIL

PRO

DUC

TION

(M

BBL/

D)1

DisclaimersThe information contained in this summary has been prepared to assist you in making your own evaluation of the Company and does not purport to contain all of the information you may consider important in deciding whether to invest in shares of the Company’s common stock. In all cases, it is your obligation to conduct your own due diligence. All information contained herein, including any estimates or projections, is based upon information provided by the Company. Any estimates or projections with respect to future performance have been provided to assist you in your evaluation but should not be relied upon as an accurate representation of future results. No persons have been authorized to make any representations other than those contained in this summary, and if given or made, such representations should not be considered as authorized.

Certain statements, estimates and financial information contained in this summary constitute forward-looking statements or information. Such forward-looking statements or information involve known and unknown risks and uncertainties that could cause actual events or results to differ materially from the results implied or expressed in such forward-looking statements or information. While presented with numerical specificity, certain forward-looking statements or information are based (1) upon assumptions that are inherently subject to significant business, economic, regulatory, environmental, seasonal, competitive uncertainties, contingencies and risks including, without limitation, the ability to obtain debt and equity financings, capital costs, construction costs, well production performance, operating costs, commodity pricing, differentials, royalty structures, field upgrading technology, and other known and unknown risks, all of which are difficult to predict and many of which are beyond the Company's control, and (2) upon assumptions with respect to future business decisions that are subject to change.

There can be no assurance that the results implied or expressed in such forward-looking statements or information or the underlying assumptions will be realized and that actual results of operations or future events will not be materially different from the results implied or expressed in such forward-looking statements or information. Under no circumstances should the inclusion of the forward-looking statements or information be regarded as a representation, undertaking, warranty or prediction by the Company or any other person with respect to the accuracy thereof or the accuracy of the underlying assumptions, or that the Company will achieve or is likely to achieve any particular results. The forward-looking statements or information are made as of the date hereof and the Company disclaims any intent or obligation to update publicly or to revise any of the forward-looking statements or information, whether as a result of new information, future events or otherwise. Recipients are cautioned that forward-looking statements or information are not guarantees of future performance and, accordingly, recipients are expressly cautioned not to put undue reliance on forward-looking statements or information due to the inherent uncertainty therein.

11

The SEC requires oil and gas companies, in filings made with the SEC, to disclose proved reserves, which are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible – from a given date forward, from known reservoirs, under existing economic conditions, operating methods, and governmental regulations. The SEC permits the optional disclosure of probable and possible reserves. We have elected to use in this presentation “probable” reserves and “possible” reserves, excluding their valuation. The SEC defines “probable” reserves as “those additional reserves that are less certain to be recovered than proved reserves but which, together with proved reserves, are as likely as not to be recovered.” The SEC defines “possible” reserves as “those additional reserves that are less certain to be recovered than probable reserves.” The Company has applied these definitions in estimating probable and possible reserves. Statements of reserves are only estimates and may not correspond to the ultimate quantities of oil and gas recovered. Any reserve estimates provided in this presentation that are not specifically designated as being estimates of proved reserves may include estimated reserves not necessarily calculated in accordance with, or contemplated by, the SEC’s reserves reporting guidelines. Investors are urged to consider closely the disclosure regarding our business that may be accessed through the SEC’s website at www.sec.gov.

The SEC’s rules prohibit us from filing resource estimates. Our resource estimations include estimates of hydrocarbon quantities for (i) new areas for which we do not have sufficient information to date to classify as proved, probable or even possible reserves, (ii) other areas to take into account the low level of certainty of recovery of the resources and (iii) uneconomic proved, probable or possible reserves. Resource estimates do not take into account the certainty of resource recovery and are therefore not indicative of the expected future recovery and should not be relied upon. Resource estimates might never be recovered and are contingent on exploration success, technical improvements in drilling access, commerciality and other factors.

This presentation may include certain financial measures, including adjusted EBITDAX (earnings before interest, taxes, depreciation, depletion, amortization and exploration expenses), that are non-GAAP financial measures as defined under the rules of the Securities and Exchange Commission.

This presentation is accompanied by a reconciliation of these non-GAAP financial measures to their nearest GAAP financial measures. Management uses these financial measures because they are widely accepted financial indicators used by investors to compare a company’s performance. Management believes that these measures provide investors an enhanced perspective of the operating performance of the company and aid investor understanding. Management also believes that these non-GAAP measures provide useful information regarding our ability to meet future debt service, capital expenditures and working capital requirements. These non-GAAP financial measures should not be considered in isolation or as substitutes for a measure of performance prepared in accordance with United States generally accepted accounting principles.

Reserves Disclaimer

WPX Non-GAAP Disclaimer