banana skins template 07.pmd 1 16/05/2007, 11:11 - pwc · pdf filebanana skins template 07.pmd...

TRANSCRIPT

The CSFI's survey of the risks facing insurers

InsuranceBananaSkins2007

������������������������������������� ����������

��������

Banana Skins Template 07.pmd 16/05/2007, 11:111

The CSFI's survey of the risks facing insurers

InsuranceBananaSkins2007

������������������������������������� ����������

Banana Skins Template 07.pmd 16/05/2007, 11:112

Banana Skins Template 07.pmd 15/05/2007, 16:513

�����������������������

����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

����������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������

��������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������

��������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�������������������������������������������������������

����������������������

�������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�������������������������������������������������������������������

Banana Skins Template 07.pmd 15/05/2007, 16:514

�������������������������������������������������������������������

Banana Skins Template 07.pmd 15/05/2007, 16:515

��������������������� ���������������������������������������������� �

������������������������������������������ ����������������

���������������������������

Banana Skins Template 07.pmd 15/05/2007, 16:516

��������This is a companion piece to the Banking Banana Skins survey that my colleague David Lascelles has been preparing for the CSFI, more or less annually, since 1996. The last BBS report was published in June 2006, and it prompted PricewaterhouseCoopers (which has supported the survey financially for some years) to suggest that we apply the same methodology to the insurance industry.

We were happy to agree – and not just because PwC is again providing financial support. The insurance industry is all about risk – to paraphrase the unlamented Mr Rumsfeld, both the risks we know and the risks we don’t. And the links with the banking industry are obvious.

So, too, are the differences. Indeed, the CSFI is shortly to publish another report (by an insurance industry lifer) which makes a powerful case that bankers and insurers speak completely different languages and are unable to communicate with each other except by semi-human grunts.

This makes it rather remarkable that David has been able to carry over, largely intact, the model that we have developed over the years for identifying the banana skins (banana peels, for our American cousins) on which the hapless banker, or insurer, is likely to slip. Of course, the carry-over isn’t perfect, but it has worked better than I had expected – and I am impressed by the fact that over-regulation is almost as big a bugbear in the insurance sector as it is in banking. True, it is a concern that is particularly dominant in the life sector – which is as much about savings as it is about insurance. But, in this year’s sample at least, it is at the top of the list.

Other risks – notably the quality of management within the industry, the complexity of insurance products, the insurance cycle itself – are perhaps more predictable, at least to an outsider. On the other hand, I was certainly surprised that there wasn’t more concern about the mispricing of new risks (No 17 on our list) and about the spread of a litigation culture.

Whatever, the intention of this report is not to be a dry-as-dust academic analysis. It is to provide a good, lively tour d’horizon of where a range of insurance practitioners and observers believe the major risks in their industry lie – and to provoke thought, discussion and (perhaps) apoplexy. As always, I am very grateful to my colleague, David Lascelles, for the time and effort he puts into preparing the questionnaire, analysing the (very high-level) responses and writing up the report. I am also very grateful to PwC for providing the financial assistance that makes the whole exercise possible.

Andrew Hilton Director, CSFI.

This report was written by David LascellesCover design by Octavius Murray

��������������������� �����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:517

ForewordWelcome to Insurance Banana Skins 2007, the inaugural survey of the risks facing insurers worldwide, which has been produced by CSFI in association with PricewaterhouseCoopers.

PricewaterhouseCoopers is delighted to be sponsoring this valuable initiative, following our longstanding support for the Banking Banana Skins surveys. The unique format of the Banana Skins series provides a fascinating insight into the emerging and ever-present risks and concerns at the top of the boardroom agenda and how these perceptions change over time. The overall ranking of risks is augmented by individual sections for particular sectors (life, reinsurance, property & casualty etc), along with key stakeholders such as brokers and observers (analysts, regulators etc).

While risk is clearly at the heart of insurance business, growing compliance and competitive pressures are creating fresh headaches for the insurance industry. The number one banana skin in this survey, as with banking, is concern about over-regulation. Such misgivings can only increase over the next few years as insurers face a number of new demands, not least the coming overhaul of financial reporting and capital controls in many parts of the world. The key challenge going forward is how to develop effective enterprise-wide risk management systems capable of providing both a sound platform for complex and multifaceted compliance and an enhanced basis for decision-making and strategic execution.

The other prominent Banana Skins at the top of the survey are equally revealing. The threat from natural catastrophes (second ranked risk overall) and associated climate change (fourth ranked risk overall) clearly requires ever more careful risk selection, control and diversification. The terrible losses arising from Hurricane Katrina, the European floods and other recent disasters also underline the immense and all too easily forgotten importance of insurance to the social and economic fabric of everyday life. As Adam Smith said, ‘insurance gives great security to the fortunes of private people, and by dividing among a great many that loss which would ruin an individual makes it full light and easy upon the whole society’.

Areas where the perceived Banana Skins differ from banking include its greater focus on management quality (number three in the insurance survey, but not even in the top 30 for banking). The insurance industry clearly needs to be able to offer the rewards, both financial and professional, to attract and retain the brightest and the best.

I hope that you find this survey insightful and thought-provoking, If you have any feedback or would like to discuss any of the issues raised in more detail please do not hesitate to contact myself or one of my colleagues.

Finally, I would like to thank Jeremy Jensen, one of our partners in London, for the original idea of taking ‘banana skins’ into the world of insurance, and the CSFI for producing such an interesting read. I am looking forward to the second edition.

Ian Dilks Global Insurance Leader PricewaterhouseCoopers

��������������������� ���������������������������������������������� �

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:518

Broking6%

Life34%

Property & casualty

35%

Observers11%

Reinsurance14%

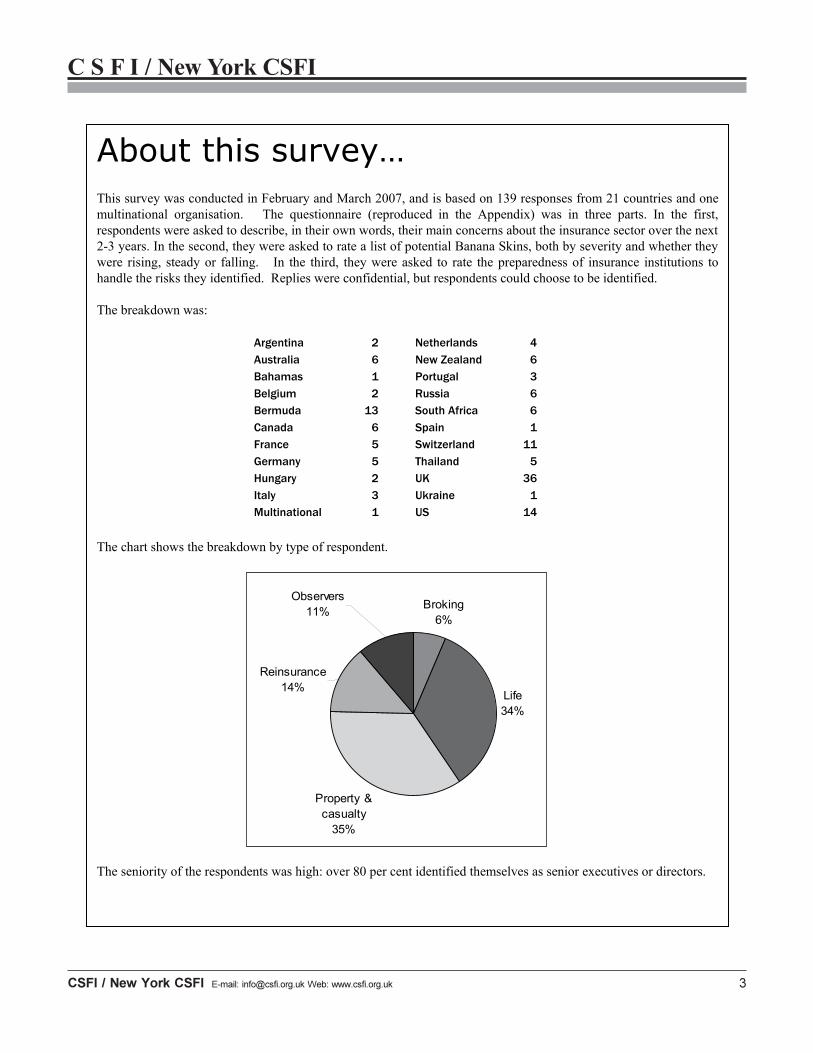

About this survey… This survey was conducted in February and March 2007, and is based on 139 responses from 21 countries and one multinational organisation. The questionnaire (reproduced in the Appendix) was in three parts. In the first, respondents were asked to describe, in their own words, their main concerns about the insurance sector over the next 2-3 years. In the second, they were asked to rate a list of potential Banana Skins, both by severity and whether they were rising, steady or falling. In the third, they were asked to rate the preparedness of insurance institutions to handle the risks they identified. Replies were confidential, but respondents could choose to be identified.

The breakdown was:

Argentina 2 Netherlands 4Australia 6 New Zealand 6Bahamas 1 Portugal 3Belgium 2 Russia 6Bermuda 13 South Africa 6Canada 6 Spain 1France 5 Switzerland 11Germany 5 Thailand 5Hungary 2 UK 36Italy 3 Ukraine 1Multinational 1 US 14

The chart shows the breakdown by type of respondent.

Broking6%

Life34%

Property & casualty

35%

Observers11%

Reinsurance14%

The seniority of the respondents was high: over 80 per cent identified themselves as senior executives or directors.

��������������������� �����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:519

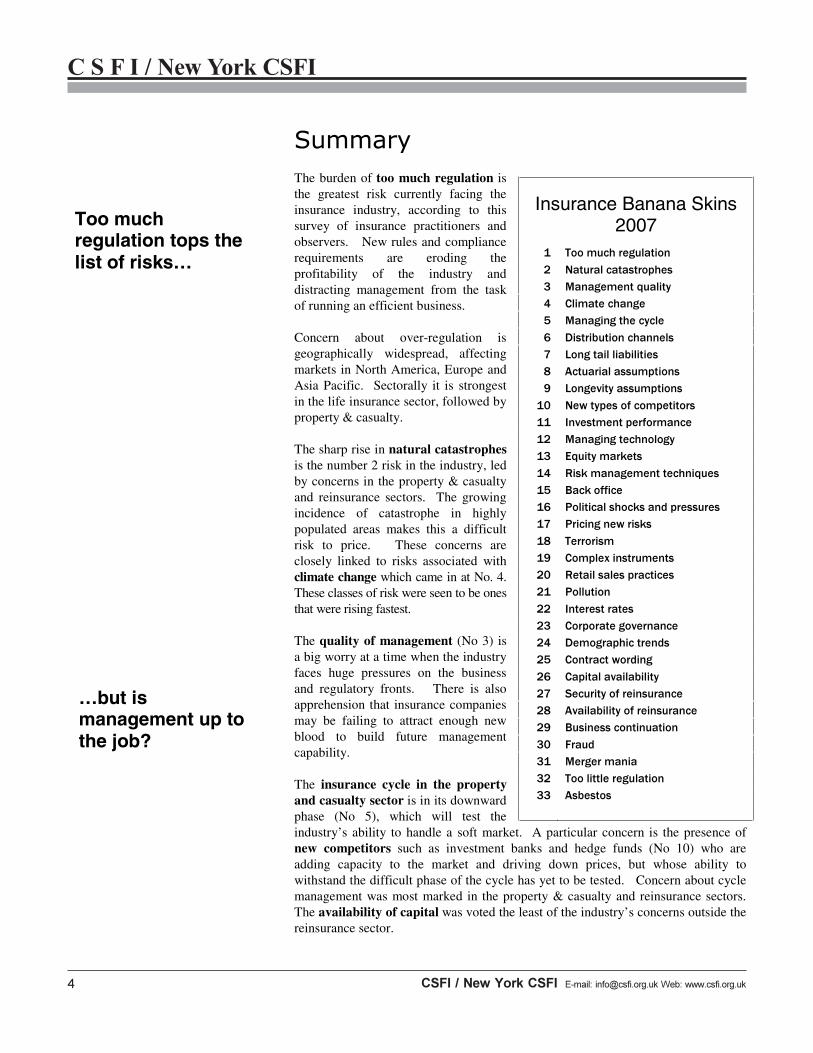

���������The burden of too much regulation is the greatest risk currently facing the insurance industry, according to this survey of insurance practitioners and observers. New rules and compliance requirements are eroding the profitability of the industry and distracting management from the task of running an efficient business.

Concern about over-regulation is geographically widespread, affecting markets in North America, Europe and Asia Pacific. Sectorally it is strongest in the life insurance sector, followed by property & casualty.

The sharp rise in natural catastrophes is the number 2 risk in the industry, led by concerns in the property & casualty and reinsurance sectors. The growing incidence of catastrophe in highly populated areas makes this a difficult risk to price. These concerns are closely linked to risks associated with climate change which came in at No. 4. These classes of risk were seen to be ones that were rising fastest.

The quality of management (No 3) is a big worry at a time when the industry faces huge pressures on the business and regulatory fronts. There is also apprehension that insurance companies may be failing to attract enough new blood to build future management capability.

The insurance cycle in the property and casualty sector is in its downward phase (No 5), which will test the industry’s ability to handle a soft market. A particular concern is the presence of new competitors such as investment banks and hedge funds (No 10) who are adding capacity to the market and driving down prices, but whose ability to withstand the difficult phase of the cycle has yet to be tested. Concern about cycle management was most marked in the property & casualty and reinsurance sectors. The availability of capital was voted the least of the industry’s concerns outside the reinsurance sector.

Insurance Banana Skins 2007

� ��������������������

� ���������������������

� �������������������

� ���������������

� �������������������

� ����������������������

� ����������������������

� ����������������������

� ����������������������

�� �������������������������

�� �����������������������

�� ��������������������

�� ���������������

�� ���������������������������

�� ������������

�� �������������������������������

�� ������������������

�� ����������

�� ��������������������

�� �����������������������

�� ����������

�� ���������������

�� ���������������������

�� �������������������

�� �����������������

�� ���������������������

�� ������������������������

�� �����������������������������

�� ����������������������

�� ������

�� �������������

�� ����������������������

�� ���������

Too much regulation tops the list of risks…

…but is management up to the job?

��������������������� ���������������������������������������������� �

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5110

The survey exposed questions about the industry’s management of longer term risks and the impact of greater longevity. Many respondents felt the industry was being slow to adjust to changes in how long people live, and that its dependence on actuarial assumptions was both excessive and a sign of its conservatism. Longevity issues (No 9) were of particular concern to the life sector, while the property & casualty/reinsurance sectors focused on long tail liabilities (No 7).

Questions about the industry’s investment performance (No 11) centred mainly on its ability to manage some of the new-fangled investment classes which have appeared on the market, such as derivatives and hedge funds. There was less concern about its exposure to more conventional investment markets such as equities (No 13) and interest rates (No 22).

Outside the tops risks, notable findings included political shocks and pressures(No 16) which showed the industry to be facing strong governmental interference in many countries: the US, Canada, New Zealand, Russia and several emerging markets. This pressure usually takes the form of obligations to provide insurance of a type and at a price set by government.

Although concern about the quality of corporate governance (No 23) in insurance companies is relatively low, the survey showed that the industry is worried about its reputation, both as a business partner, and as a career prospect.

Striking too are the lowest risks: too little regulation came one from the bottom at No 32 (though some respondents felt more could be done to increase international cooperation) and asbestos (No 33), once the scourge of the industry but now distinctly passé.

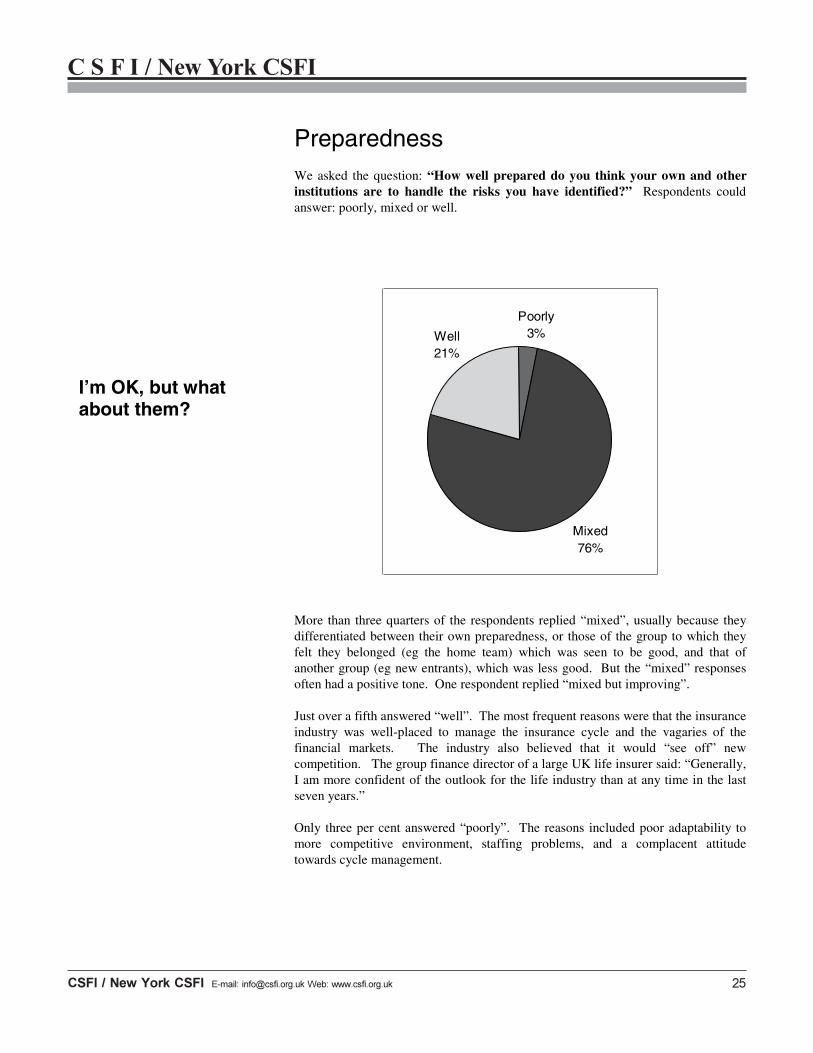

Preparedness The survey sought views on how well prepared the insurance industry was to handle the risks that had been identified. The majority of the respondents felt preparedness was “mixed”. Just over a fifth answered “well”, and only three per cent thought the industry was poorly prepared.

Political pressures are building up

The industry’s state of preparedness is ‘mixed’

��������������������� �����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5111

��������������

Brokers Brokers were concerned about the quality of management in the primary insurance companies: how well they were run, how they managed the cycle and secured capital. They were also interested in processes: distribution and the back office. The specific risks that concerned them were the growing use by insurance companies of complex instruments, climate change, long tail liabilities and catastrophe risk. They were conspicuously less worried than other groups by over-regulation (which came 13th on their list).

Life insurance The life insurance industry had the strongest concerns about over-regulation and the related risk of political pressure. Other worries lay close to the nature of the business: distribution, interest rates, equity markets, policyowner longevity and investment performance. Life insurers also saw new competitors in the savings market posing a risk. They showed the strongest concern with retail sales practices among the respondent groups.

Property & casualtyThe property & casualty sector was concerned with major sources of loss: catastrophes and climate change. It also focused on the challenge of managing the insurance cycle, the problems of long tail liabilities, and distribution channels. P&C insurers shared other sectors’ concerns with the quality of management in the industry, but were less bothered than the life sector about over-regulation.

� �������������������

� ��������������������

� �������������������

� ���������������

� ���������������������

� ����������������������

� ������������

� ����������������������

� �������������������������

�� ���������������������

� ��������������������

� ����������������������

� ���������������

� ����������������������

� ������������������������������

� �����������������������

� �������������������

� �����������������������

� ���������������

�� �������������������������

� ���������������������

� ���������������

� �������������������

� ��������������������

� �������������������

� ����������������������

� ����������������������

� �����������������������

� ��������������������

�� �������������������������

Over-regulation is the bugbear of the life industry…

…while property & casualty has its eye on natural catastrophes

��������������������� ���������������������������������������������� �

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5112

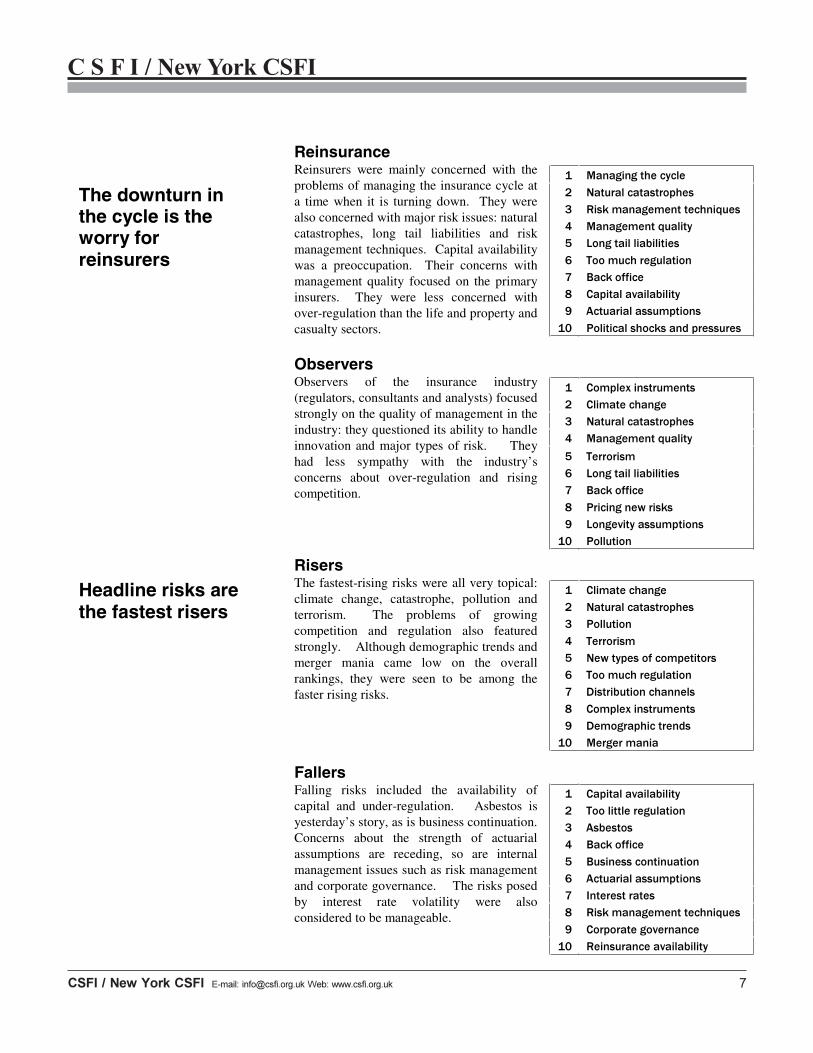

Reinsurance Reinsurers were mainly concerned with the problems of managing the insurance cycle at a time when it is turning down. They were also concerned with major risk issues: natural catastrophes, long tail liabilities and risk management techniques. Capital availability was a preoccupation. Their concerns with management quality focused on the primary insurers. They were less concerned with over-regulation than the life and property and casualty sectors.

Observers Observers of the insurance industry (regulators, consultants and analysts) focused strongly on the quality of management in the industry: they questioned its ability to handle innovation and major types of risk. They had less sympathy with the industry’s concerns about over-regulation and rising competition.

Risers The fastest-rising risks were all very topical: climate change, catastrophe, pollution and terrorism. The problems of growing competition and regulation also featured strongly. Although demographic trends and merger mania came low on the overall rankings, they were seen to be among the faster rising risks.

Fallers Falling risks included the availability of capital and under-regulation. Asbestos is yesterday’s story, as is business continuation. Concerns about the strength of actuarial assumptions are receding, so are internal management issues such as risk management and corporate governance. The risks posed by interest rate volatility were also considered to be manageable.

� �������������������

� ���������������������

� ���������������������������

� �������������������

� ����������������������

� ��������������������

� ������������

� ���������������������

� ����������������������

�� �������������������������������

� ��������������������

� ���������������

� ���������������������

� �������������������

� ����������

� ����������������������

� ������������

� ������������������

� ����������������������

�� ����������

� ���������������

� ���������������������

� ����������

� ����������

� �������������������������

� ��������������������

� ����������������������

� ��������������������

� �������������������

�� �������������

� ���������������������

� ����������������������

� ���������

� ������������

� ����������������������

� ����������������������

� ���������������

� ���������������������������

� ���������������������

�� �������������������������

The downturn in the cycle is the worry for reinsurers

Headline risks are the fastest risers

��������������������������������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5113

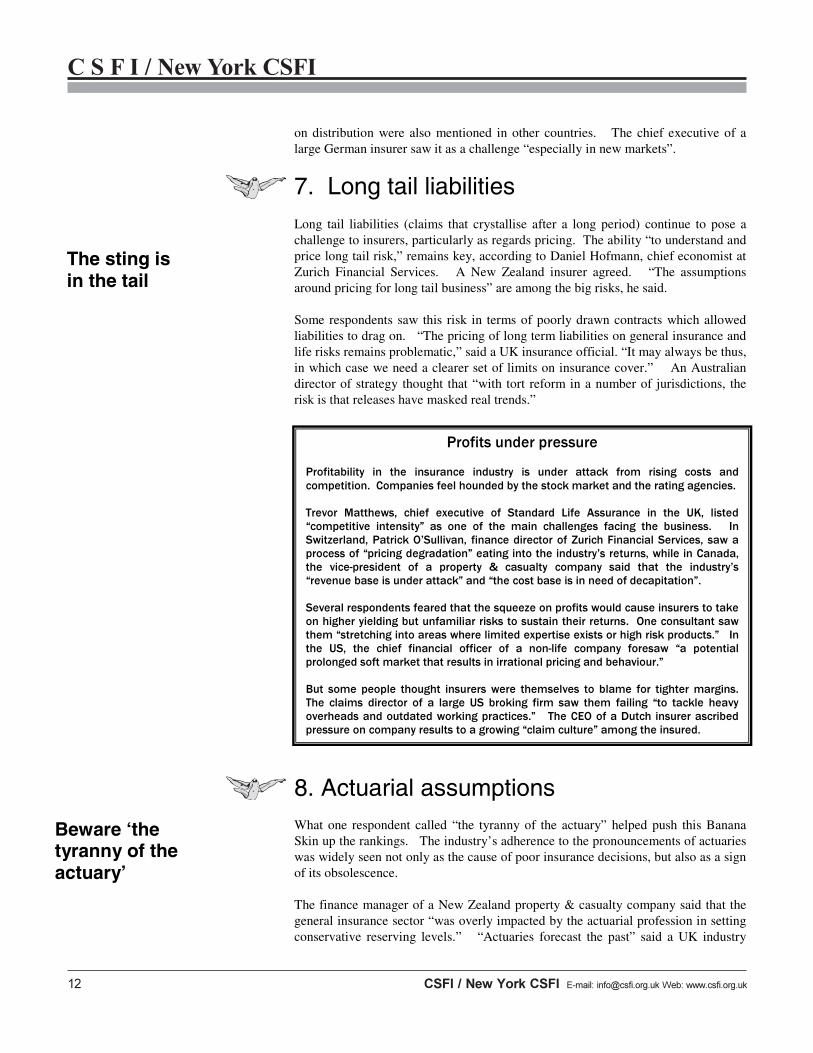

1. Too much regulation The rising burden of regulation emerges as the greatest risk currently facing the insurance industry. The steady flow of new laws and rules is piling costs on to insurance companies, stretching their resources and diverting management from running the business. The chief executive of a major UK life insurer said regulation was becoming “ever more intrusive, time-consuming and box-ticking. This is despite the rhetoric about principles-based regulation.”

Regulatory overload is a worldwide phenomenon: it was cited by respondents from most of the countries in the survey. The chief executive of a large South African insurer complained of “regulatory strangling”, while his opposite number at a New Zealand property & casualty company saw “regulatory overkill which adds no further to consumer protection but which stifles innovation and responsiveness.” Comments in a similar vein were received from countries such as the US, Italy, Switzerland, Australia, Portugal, Hungary, Thailand and Russia.

The over-regulation issue came through particularly strongly from the life insurance sector, which voted it top Banana Skin. The chief executive of a large Canadian life company said: “The overall regulatory burden is growing alarmingly. The zealousness of regulators, the activism of corporate governance ‘pundits’ […] are creating a nightmare scenario.” Other sectors placed it lower: property & casualty 4th, reinsurance 6th and brokers 13th.

Among the specific concerns were:

Too much change. The sheer volume of regulatory change – new rules on capital, conduct of business, accounting and governance – is seen as a major intrusion. The chief executive of business strategy at a South African life company said the industry could barely keep pace with new initiatives. In the US, the chief financial officer of a life company tried to take a balanced view. “The changes in regulatory, rating agency and accounting will provide some benefits and improvements, but will be a major distraction and resource drain.” The pace of regulatory change was particularly emphasised in countries where insurance regulation is under review, including South Africa, Canada, New Zealand, Hungary, Argentina, Thailand and the Ukraine.

Quality. The quality of regulation was widely questioned. In Bermuda, a respondent complained of the “inconsistent and opaque notions” of rating agencies and regulators. From Hungary, the chief financial officer of a general insurance company said that “regulation does not fit the needs of the industry, both customers and insurers”. In Russia, Gennadiy Galperin, executive director of Rosgosstrakh, saw “weak regulation of the insurance market by the Federal Services for Insurance Supervision, also the Ministry of Finance.” Several respondents said regulation had become too prescriptive and rule-driven. The “gold plating” of EU regulations, was a particularly British concern. Adrian Colosso, chief executive of insurance brokers Heath Lambert complained of “over-regulation from Europe being excessively implemented within the UK”.

Lack of consistency. Rules differ from country to country, and even within jurisdictions, for example between domestic and foreign firms. A Swiss reinsurer complained of the “burden of inconsistent national requirements”. There was “too much in US, too little in the global markets,” said a Bermuda-based respondent. The burden also fell heaviest on smaller companies. In Portugal, the executive director of a domestic insurer was concerned about “the ability of small but efficient

Regulation is ‘strangling’ the industry

Too many bad and inconsistent rules

���������������������������������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5114

companies to survive in a global market where regulatory and capital exigencies are rising.”

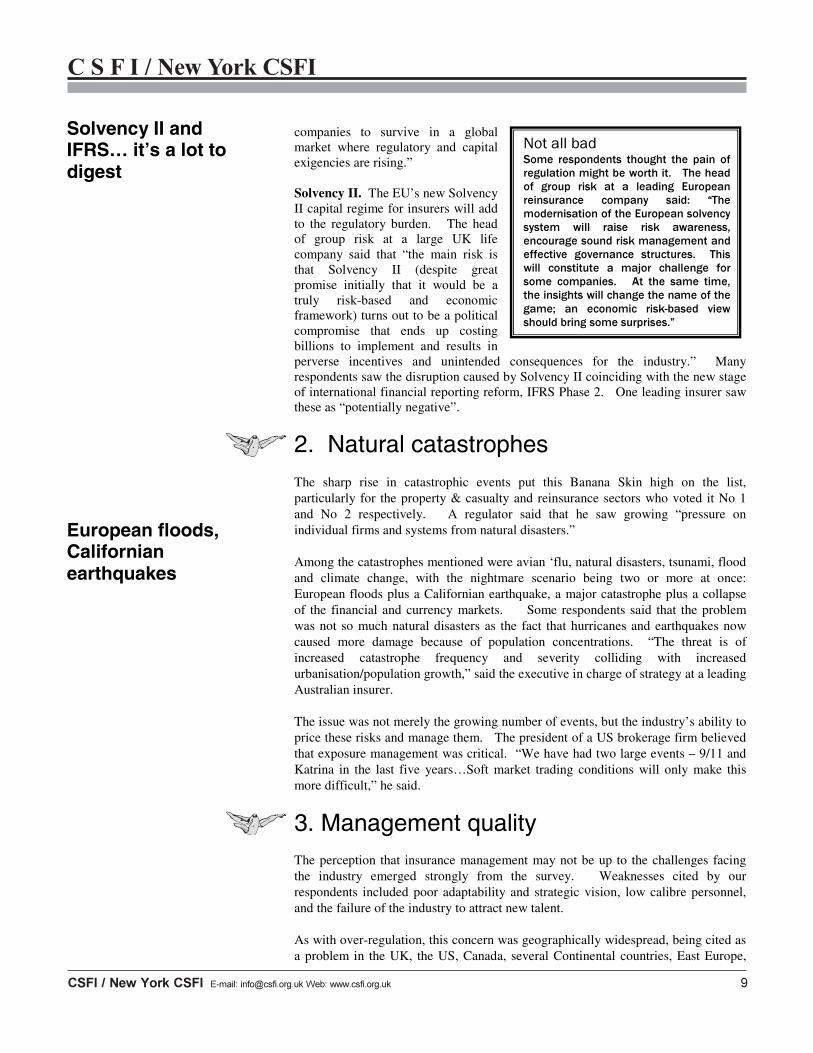

Solvency II. The EU’s new Solvency II capital regime for insurers will add to the regulatory burden. The head of group risk at a large UK life company said that “the main risk is that Solvency II (despite great promise initially that it would be a truly risk-based and economic framework) turns out to be a political compromise that ends up costing billions to implement and results in perverse incentives and unintended consequences for the industry.” Many respondents saw the disruption caused by Solvency II coinciding with the new stage of international financial reporting reform, IFRS Phase 2. One leading insurer saw these as “potentially negative”.

2. Natural catastrophes The sharp rise in catastrophic events put this Banana Skin high on the list, particularly for the property & casualty and reinsurance sectors who voted it No 1 and No 2 respectively. A regulator said that he saw growing “pressure on individual firms and systems from natural disasters.”

Among the catastrophes mentioned were avian ‘flu, natural disasters, tsunami, flood and climate change, with the nightmare scenario being two or more at once: European floods plus a Californian earthquake, a major catastrophe plus a collapse of the financial and currency markets. Some respondents said that the problem was not so much natural disasters as the fact that hurricanes and earthquakes now caused more damage because of population concentrations. “The threat is of increased catastrophe frequency and severity colliding with increased urbanisation/population growth,” said the executive in charge of strategy at a leading Australian insurer.

The issue was not merely the growing number of events, but the industry’s ability to price these risks and manage them. The president of a US brokerage firm believed that exposure management was critical. “We have had two large events – 9/11 and Katrina in the last five years…Soft market trading conditions will only make this more difficult,” he said.

3. Management quality The perception that insurance management may not be up to the challenges facing the industry emerged strongly from the survey. Weaknesses cited by our respondents included poor adaptability and strategic vision, low calibre personnel, and the failure of the industry to attract new talent.

As with over-regulation, this concern was geographically widespread, being cited as a problem in the UK, the US, Canada, several Continental countries, East Europe,

����������������� ������������ �������� ���� ����� ������������������� ��������������������������� ������ ����� ��� �� �������� ��������������������� �������� ������ ��������������������������������������������������� ����� ������ ����� ��������������������������������������������������������� ����������� ������������ � ���������� ����������� �� ������ ���������� ��������� ����������� � � ��� ���� ����� ����������������������������������������������������� ��� ��������� ����������� ����������������� ������������������

Solvency II and IFRS… it’s a lot to digest

European floods, Californian earthquakes

�� ��������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5115

South East Asia, Australia and New Zealand. Sectorally, it was most marked among insurance brokers (who voted it No. 1) followed by reinsurance (4th), property & casualty (5th) and life (7th).

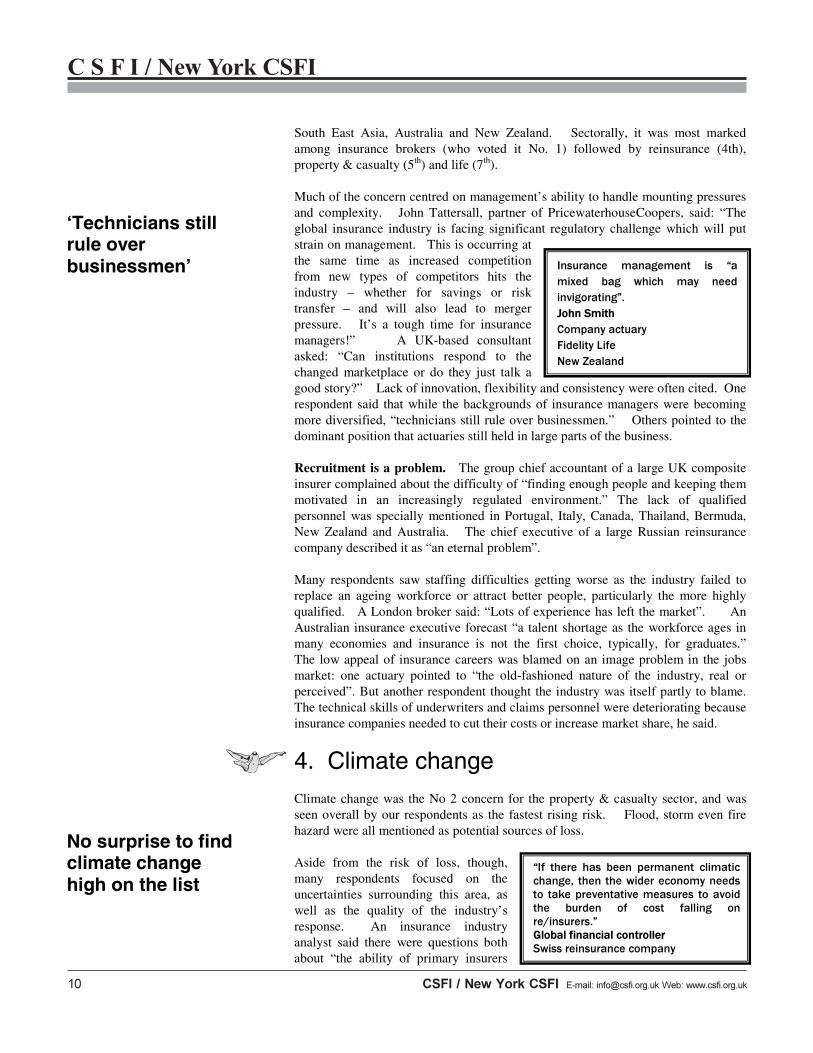

Much of the concern centred on management’s ability to handle mounting pressures and complexity. John Tattersall, partner of PricewaterhouseCoopers, said: “The global insurance industry is facing significant regulatory challenge which will put strain on management. This is occurring at the same time as increased competition from new types of competitors hits the industry – whether for savings or risk transfer – and will also lead to merger pressure. It’s a tough time for insurance managers!” A UK-based consultant asked: “Can institutions respond to the changed marketplace or do they just talk a good story?” Lack of innovation, flexibility and consistency were often cited. One respondent said that while the backgrounds of insurance managers were becoming more diversified, “technicians still rule over businessmen.” Others pointed to the dominant position that actuaries still held in large parts of the business.

Recruitment is a problem. The group chief accountant of a large UK composite insurer complained about the difficulty of “finding enough people and keeping them motivated in an increasingly regulated environment.” The lack of qualified personnel was specially mentioned in Portugal, Italy, Canada, Thailand, Bermuda, New Zealand and Australia. The chief executive of a large Russian reinsurance company described it as “an eternal problem”.

Many respondents saw staffing difficulties getting worse as the industry failed to replace an ageing workforce or attract better people, particularly the more highly qualified. A London broker said: “Lots of experience has left the market”. An Australian insurance executive forecast “a talent shortage as the workforce ages in many economies and insurance is not the first choice, typically, for graduates.” The low appeal of insurance careers was blamed on an image problem in the jobs market: one actuary pointed to “the old-fashioned nature of the industry, real or perceived”. But another respondent thought the industry was itself partly to blame. The technical skills of underwriters and claims personnel were deteriorating because insurance companies needed to cut their costs or increase market share, he said.

4. Climate change Climate change was the No 2 concern for the property & casualty sector, and was seen overall by our respondents as the fastest rising risk. Flood, storm even fire hazard were all mentioned as potential sources of loss.

Aside from the risk of loss, though, many respondents focused on the uncertainties surrounding this area, as well as the quality of the industry’s response. An insurance industry analyst said there were questions both about “the ability of primary insurers

���������� ����������� ��� ��������� ���� ������ ���� ��������������������������������������������������������������������������

���� ������ ���� ����� ���������� ����������������� ����� ��������������������������� ��������������������������� ������������� ������� ��� ����� �������� �����������������������������������������������������������������������

‘Technicians still rule over businessmen’

No surprise to find climate change high on the list

������������������������ ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5116

and reinsurers to manage risks associated with climate change, and concerns about the extent and cost of coverage from the perspective of consumers and business.” The strategy director of an Australian company said this was “the hot topic as the industry tries to understand in detail its impacts and strategic responses, including opportunities,” but a UK insurance company director added: “It is almost impossible for the insurance industry to predict its effect and to react.”

Looking beyond the immediate impact, a UK respondent feared that climate change would give people “new opportunities to claim compensation,” and that the industry might suffer “adverse consumer and media comment linked to this”.

5. Managing the cycle The ups and downs of the insurance cycle are a major challenge for the property & casualty and reinsurance industries, particularly now that the market is softening again. Declining premiums, plentiful capital and the possibility of a global economic downturn all threaten insurance company performance.

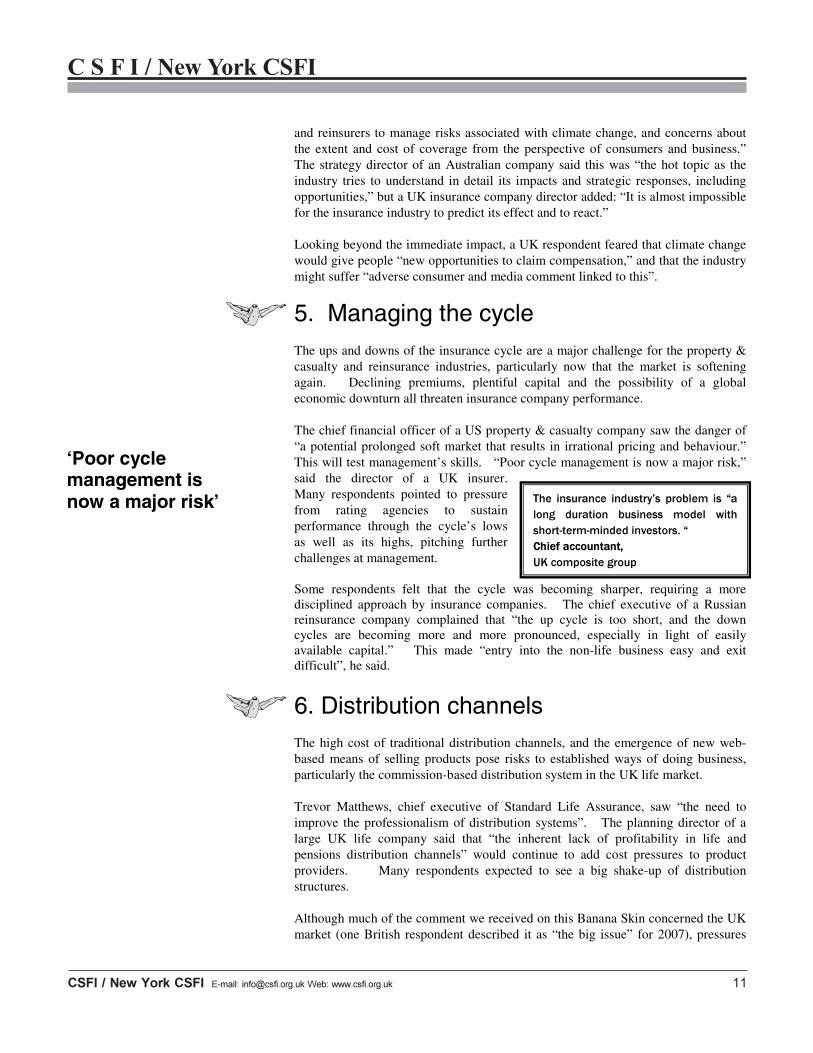

The chief financial officer of a US property & casualty company saw the danger of “a potential prolonged soft market that results in irrational pricing and behaviour.” This will test management’s skills. “Poor cycle management is now a major risk,” said the director of a UK insurer. Many respondents pointed to pressure from rating agencies to sustain performance through the cycle’s lows as well as its highs, pitching further challenges at management.

Some respondents felt that the cycle was becoming sharper, requiring a more disciplined approach by insurance companies. The chief executive of a Russian reinsurance company complained that “the up cycle is too short, and the down cycles are becoming more and more pronounced, especially in light of easily available capital.” This made “entry into the non-life business easy and exit difficult”, he said.

6. Distribution channels The high cost of traditional distribution channels, and the emergence of new web-based means of selling products pose risks to established ways of doing business, particularly the commission-based distribution system in the UK life market.

Trevor Matthews, chief executive of Standard Life Assurance, saw “the need to improve the professionalism of distribution systems”. The planning director of a large UK life company said that “the inherent lack of profitability in life and pensions distribution channels” would continue to add cost pressures to product providers. Many respondents expected to see a big shake-up of distribution structures.

Although much of the comment we received on this Banana Skin concerned the UK market (one British respondent described it as “the big issue” for 2007), pressures

���� ���������� ����������� �������� ��� �������� ��������� ��������� ������ ������������������������������������������������������������������������

‘Poor cycle management is now a major risk’

�� �������������������������������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5117

on distribution were also mentioned in other countries. The chief executive of a large German insurer saw it as a challenge “especially in new markets”.

7. Long tail liabilities Long tail liabilities (claims that crystallise after a long period) continue to pose a challenge to insurers, particularly as regards pricing. The ability “to understand and price long tail risk,” remains key, according to Daniel Hofmann, chief economist at Zurich Financial Services. A New Zealand insurer agreed. “The assumptions around pricing for long tail business” are among the big risks, he said.

Some respondents saw this risk in terms of poorly drawn contracts which allowed liabilities to drag on. “The pricing of long term liabilities on general insurance and life risks remains problematic,” said a UK insurance official. “It may always be thus, in which case we need a clearer set of limits on insurance cover.” An Australian director of strategy thought that “with tort reform in a number of jurisdictions, the risk is that releases have masked real trends.”

8. Actuarial assumptions What one respondent called “the tyranny of the actuary” helped push this Banana Skin up the rankings. The industry’s adherence to the pronouncements of actuaries was widely seen not only as the cause of poor insurance decisions, but also as a sign of its obsolescence.

The finance manager of a New Zealand property & casualty company said that the general insurance sector “was overly impacted by the actuarial profession in setting conservative reserving levels.” “Actuaries forecast the past” said a UK industry

����������������������

�������������� ��� ���� ���������� ��������� ��� ������ ������� ����� ������� ������ �������������������������������������������������������������������������������������

������� ���������� ������ ���������� ��� ��������� ����� ���������� ��� ���� ���� �������������������� ����������� ��� ���� ��� ���� ����� ����������� ������� ���� ���������� � � ������������������������������������ ����������������������������������������������������������������������������������������������������������������������������������������������� ��������������� ��� �� ��������� �� ��������� �������� ����� ����� ���� ��������������������������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ���� ���� ������ ���������� �������� ��� �� ��������� �������� �������� ��� ����������������������������������������������������������������������������������������� ����� ������� �������� �������������� ����������� ��� ������ ���� ���������������������� ������� ��������� ��� �� ������ ��� �������� ����� ���� ����� �������� ���� ������� ������������������������������������������������� � �������������������� ����������������������������������������������������������������������������������������������

The sting is in the tail

Beware ‘the tyranny of the actuary’

��������������������� ���������������������������������������������� ��

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5118

expert. An Australian insurance executive said “the problem is not so much the accuracy of estimates, rather the failure to act quickly when error is spotted.”

Several respondents made the point that the accuracy of actuarial assumptions will become more critical in the period ahead as the insurance industry enters a softening market.

9. Longevity assumptions As people live longer, longevity risk for health care and life insurers is rising. As might be expected, this Banana Skin was a particular concern for the life sector which voted it 4th.

The focus of many responses was the impact of longer life on the savings side of the business, annuities and pensions, and insurers’ ability to fund their obligations. A London insurer said: “With improvement in health care (and potential advancement of cures for the major terminal illnesses) longevity is a key risk for the industry.” Another UK insurer saw this risk particularly “in the context of pricing in the growing bulk annuity market” where poor longevity assumptions could oblige companies “to pay out too much in annuities.” A Swiss respondent saw longevity risk turning into “a killer” for a potentially underfunded pensions business.

The growing use of genetics to predict life expectancy could make product development more difficult, according to one consultant.

10. New types of competitors Insurance is under attack from new competitors on many fronts. On the wholesale side, hedge funds and venture capitalists are creating new capacity, and investment banks are inventing new risk management products. On the retail front, banks are eating into the savings market, supermarkets are selling insurance, and the Internet is providing a platform for electronic distribution channels and price aggregators (web sites which collect and compare prices). The responses to this Banana Skin conveyed a sense of an industry under siege.

It is not merely the fact of new competition that causes concern, also its potentially low quality. Many respondents felt new competitors might fail when the going got tough, causing losses and bringing the industry into disrepute.

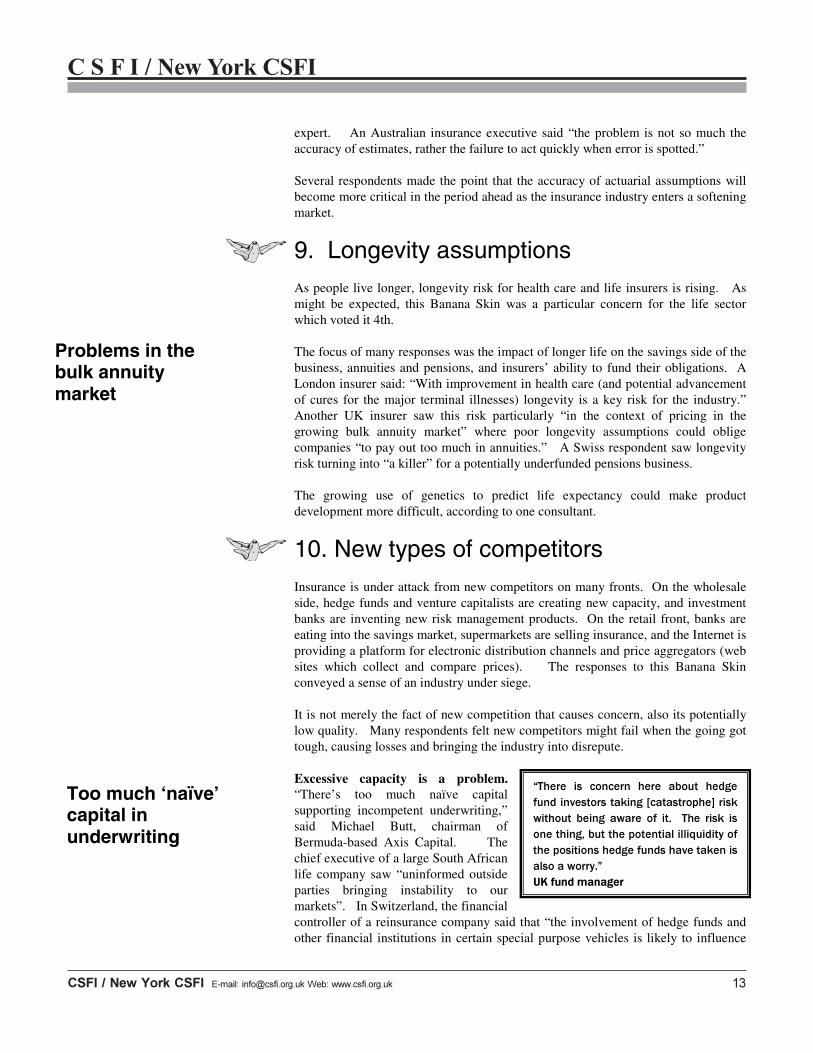

Excessive capacity is a problem.“There’s too much naïve capital supporting incompetent underwriting,” said Michael Butt, chairman of Bermuda-based Axis Capital. The chief executive of a large South African life company saw “uninformed outside parties bringing instability to our markets”. In Switzerland, the financial controller of a reinsurance company said that “the involvement of hedge funds and other financial institutions in certain special purpose vehicles is likely to influence

������� ��� �������� ����� ������ ������������������������������������������������������� ������ ������ ��� ���� � ���� ����� �������������������������������������������������������������������������������������������������������������������������

Problems in the bulk annuity market

Too much ‘naïve’ capital in underwriting

�� ��������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5119

the pricing level and duration of future cycles. It is unclear how these companies will respond to a major catastrophe.”

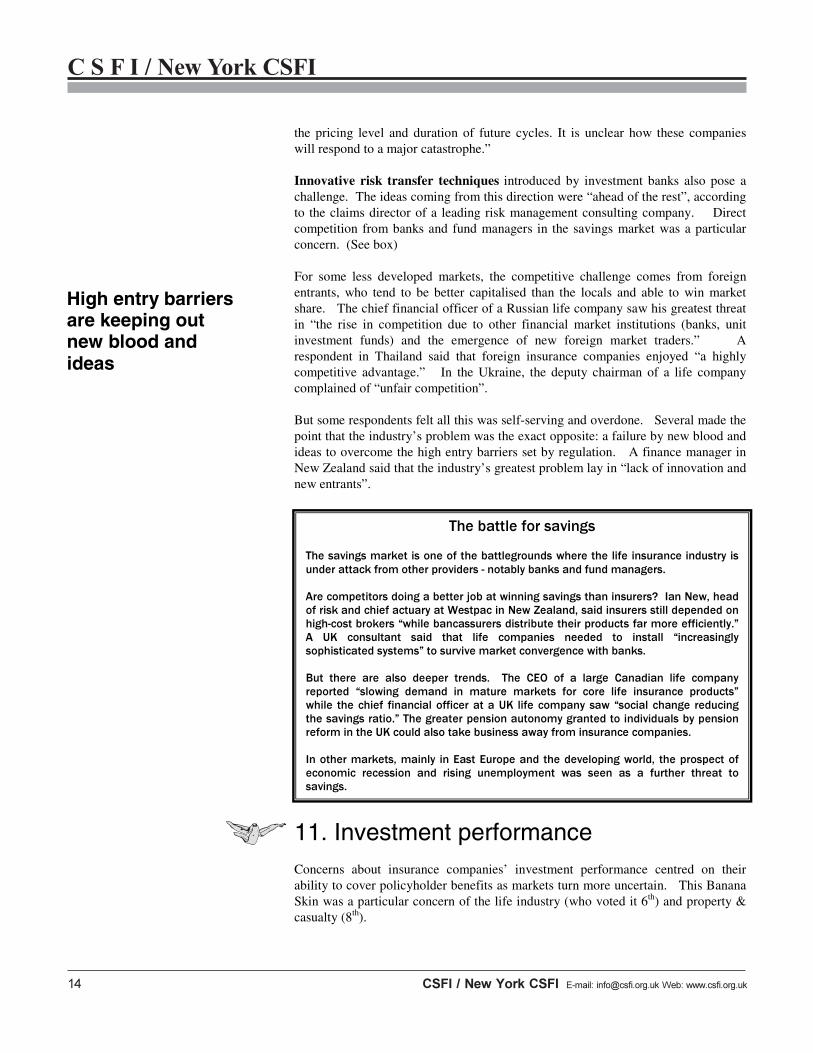

Innovative risk transfer techniques introduced by investment banks also pose a challenge. The ideas coming from this direction were “ahead of the rest”, according to the claims director of a leading risk management consulting company. Direct competition from banks and fund managers in the savings market was a particular concern. (See box)

For some less developed markets, the competitive challenge comes from foreign entrants, who tend to be better capitalised than the locals and able to win market share. The chief financial officer of a Russian life company saw his greatest threat in “the rise in competition due to other financial market institutions (banks, unit investment funds) and the emergence of new foreign market traders.” A respondent in Thailand said that foreign insurance companies enjoyed “a highly competitive advantage.” In the Ukraine, the deputy chairman of a life company complained of “unfair competition”.

But some respondents felt all this was self-serving and overdone. Several made the point that the industry’s problem was the exact opposite: a failure by new blood and ideas to overcome the high entry barriers set by regulation. A finance manager in New Zealand said that the industry’s greatest problem lay in “lack of innovation and new entrants”.

11. Investment performance Concerns about insurance companies’ investment performance centred on their ability to cover policyholder benefits as markets turn more uncertain. This Banana Skin was a particular concern of the life industry (who voted it 6th) and property & casualty (8th).

����������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ��� ����������� ����� ����� ����� ���������� ������� ��� �������� ��������������������������������������������������������������������������������������� ������ ���� ����� ������� �������� � ���� ���� ��� �� ������ ��������� ����� ����������������� ��������� ������� ��� ������� �������� ���� ����� ����� ���������� ������������������ ���������� �������������������������� ����� ������������ �������� ������� ������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ���������������������� ������������������� ���������������������� ������������������������� ���������� ���� ������� ������������� ���� ����� ��� �� �������� ������� ������������

High entry barriers are keeping out new blood and ideas

����������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5120

“It is difficult to outperform cash!” said a UK respondent of the challenge facing the industry from the low investment yields currently available in many markets.

But there was an additional concern over market innovation, and the new but risky investment propositions this was throwing up, for example in the areas of private equity and hedge funds.. “It is becoming a challenge for senior management to understand new investment categories”, said a respondent from one of the big rating agencies. An industry analyst wondered whether insurers would be able “to manage new financial risks … (eg credit risk acquired through buying credit derivatives) and exposure of investment portfolios to certain types of investments (eg hedge funds, sub prime mortgages).”

If companies failed to earn sufficiently high returns, it was not always their fault. One UK respondent blamed external influences (the Financial Services Authority etc.) for trying to “influence their investment criteria.”

12. Managing technology Weaknesses on the technology front are a problem, particularly the obsolescence of IT systems, and the risks that insurers run when trying to update them. This Banana Skin came highest for the property & casualty sector (9th, versus life 16th).

Many respondents said the industry was hampered by paper-based or antiquated IT systems which failed to track data and keep management properly informed. “The rate of adoption of new technology is low,” said a UK insurer. One UK broker feared the situation was so bad that the industry faced “technology meltdown”. A Portuguese respondent described data quality as “abominable”.

One of the concerns was that technological backwardness would hamper the industry as it sought to compete with better-equipped new entrants to the business. According to a UK consultant, the convergence of savings products provided by insurers and banks meant that life insurers “will require increasingly sophisticated systems”. The vice-president in charge of risk controls at a Canadian non-life company said the industry “requires huge reinvestments to achieve real time information and a reduction of its cost base.”

13. Equity markets With their heavy dependence on investment performance, the growing uncertainty surrounding the outlook for equities poses a potential risk for the industry, particularly the life sector which put this risk in 9th place. “Rising equity markets have improved capital availability and delivered good investment performance,” said the planning director of a UK life company. “But market risks are on the rise.” Respondents saw the possibility of greater turbulence in equity prices, even of a market crash, with UK companies more exposed than most.

Geographically, the focus is on the US markets, from which most other markets will take their lead, though the growing linkage between equity markets also makes it harder for insurance companies to diversify their equity risks.

Fears of ‘technology meltdown’

Insurers are better at handling volatility

�� ��������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5121

But other respondents viewed this risk as less of a threat than in past economic cycles, with insurers now more sheltered from equities, and wiser at managing difficult markets. “There is better matching across the industry,” said the chief risk officer of a large UK life company. A New Zealand CEO agreed. “There is greater [market] volatility, but companies can diversify their risks,” he said.

14. Risk management techniques The challenges in this area were summed up by a European underwriter: “Can [the insurance industry] develop strong and flexible risk management processes/models that are able respond in an effective way to a fast-changing environment?”

Some respondents were doubtful. The chief financial officer of a US life group said that “companies are offering very complex products, often with limited ability to understand and quantify risks”. A London-based consultant wondered whether it was even known “where risk sits and who owns it in each institution”. The director of strategic options at a large UK insurance group felt that risk management was still not built deeply enough into the day-to-day management of the business. Insurance companies should “articulate [their] appetite for risk in a measurable way” and make the risk assessment process more challenging so that it was not just “a routine form-filling exercise”.

In the less developed world, this was one of the areas where the shortage of qualified and experienced personnel was most keenly felt and where, therefore, concerns about the strength of risk management were highest.

One dissident from these views – a UK insurer – said that “insurers have moved beyond insurance risks and have made significant progress managing other risks.”

15. Back office Risks are high in the back office because the volume of processing and product innovation is overtaking the ability of systems to handle them. The concern was particularly high among reinsurers and insurance brokers who both voted it No. 7.

A UK technology provider highlighted the problem. “In the world of life and pensions distribution, many larger firms are using functionality which, through poor design or simple age, is limiting rather than enabling their business strategy. At the smaller end of the market it is estimated that fully 30 per cent of intermediaries don’t use a back office system at all.”

A UK insurer saw risks rising “due to the increasing complexity of products and investments.” In Switzerland, the head of group risk reporting at a large reinsurer said that “ever increasing information requirements are a challenge.” A further concern was the amount of regulatory change, and the extra pressure this put on already overstretched systems.

Nonetheless, respondents tended to rank this as a receding risk. It was voted among the fastest fallers, mainly because of the investment that is being made to improve back office systems.

Do insurers understand complex products?

Many intermediaries ‘don’t use a back office system at all’

������������������������ ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5122

16. Political shocks and pressures Political interference in the insurance industry is growing and putting the business at risk. Pressure from governments and politicians, tax changes, regulatory requirements, corruption and instability were all mentioned by our respondents. One said his concern was “misguided and inappropriate legislation, based on political correctness, which could remove or restrict the right to underwrite effectively.” The chief executive of a large German insurance company said that while political risk was steady in Germany “it is rising elsewhere”.

The developed world is particularly worried about tax. Amendments to US tax laws on life and annuity products were cited as a major business risk. In the UK, heavier taxation of insurance premiums was seen as a possibility. New Zealand has embarked on a review of the taxation of the life business which one respondent expected to have “a very significant negative financial impact on the industry.” In Europe, EU pressure on tax havens is a concern.

In North America, several respondents cited the state-sponsored Florida Hurricane Catastrophe Fund as an example of unhelpful government intrusion in the insurance market. The fund underpins the insurance market, but also regulates its prices. Canadian respondents also reported that politicians tried to influence their business.

In emerging markets the concern is with bad government, particularly in the area of obligatory insurance where availability and price are politically managed. “Corruption, political pressure and instability” were on the risk list of the chief executive of a Russian life company. In Hungary, the key risk was “the unstable political environment”, according to the CEO of a life company.

17. Pricing new risks The emergence of new risks, particularly from disease, natural catastrophe and new technology, poses a pricing challenge to insurers. If they get it wrong, losses quickly follow. A regulator saw “mispricing of risk” as one of the big Banana Skins facing the industry.

In the natural catastrophe area, a rating agency analyst said insurance companies were having difficulty pricing risks “owing to rapid changes in frequency and severity of catastrophic events.” The actuary of a New Zealand property & casualty company said there was “insufficient recognition of the true cost of insurance in high risk environments, eg flood, storm.”

��� ���������� ����� ���������� �������������� ��������� ��� ���������� ���������������������������������������������������������������������������������������������� ����� �� ������� ��� ����� �� �����������������������������������������������������������������������

‘Corruption, political pressure and instability’

�� ��������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5123

Other hard-to-price areas included pandemics, electro-magnetic radiation, nanotechnology (see box), genetic testing, genetically modified foods and weight-related health insurance. A US respondent said the industry should be particularly concerned with risks that “cannot be reinsured or diversified (and are difficult to model), eg equity risk guarantee products.”

But the chief executive of a large German insurer felt this was a low risk area “because new risks are a small percentage of the portfolio”.

18. Terrorism Though low in the rankings, this emerged as one of the fastest-rising risks (4th on the risers list), not surprisingly given recent events. “Given Afghanistan, Iraq and Iran, terrorism remains a key concern,” said one respondent. “It will continue to rise” predicted another. Much of the difficulty surrounding this risk lies in predicting what form it will take when terrorists strike. The chief financial officer of a US property & casualty company said it could be “nuclear, biological, chemical, radioactive.”

Even so, many insurers felt this risk was manageable. One insurance company CEO said it had “limited insurance impact”, and another said the real risk was “Paranoia!”, the irrational fear that often surrounds shadowy and unquantifiable threats. It was notable that outside observers of the industry placed this risk much higher (5th) than insurance practitioners (20th), suggesting that the actual incidence of terrorist events may rather lower than it is perceived to be in the public mind.

19. Complex instruments Innovation in the insurance industry is throwing up novel instruments, and with them new challenges, not least the need to understand them.

The chief executive of a Canadian life company said: “New products have many complex and potentially very risky options embedded in them.” The chief financial officer of a US life insurer offered a similar view: “The capital markets are generating ever-increasingly complex financial instruments, many untested in times of stress…Companies are offering very complex products, often with limited ability to understand and quantify risks.”

Andrew Power, a partner at Deloitte consultancy, thought insurers lacked “the savvy” of the investment banks who were creating many of these new instruments. He asked: “Are insurers the dumb capital which investment banks feed off?” A regulator said that the use of complex instruments could add to the legal risks faced by insurers.

��������������� �������� ����� ������������������������� ��� ������ ����� ����������������������������������������������������� � ������ ������ ���� �������� ������������ ���������� ���� �������� ������������ ������ ���� ������� �� ����������������� ���������� ������� ��� �������������� ����� ��� ������ �������� ���������� ���� ���������� ������������� ���������������������������������������������� ��������� �� ���� ����� ����� ���� ��� ��������� ����� ����������� ���������� ������������ ���������� ������ ������������������ ��� �������� ����� ��������� ���������������

Terrorism takes many forms

Who’s more savvy: insurers or investment banks?

����������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5124

But some respondents felt the dangers here were contained. Regulators generally put limits on the use of derivatives by insurance companies, while “treating customer fairly” rules should ensure that consumers are only offered products they can understand. The chief executive of a large European insurer said some of the complexity was driven from the bottom up. “Consumer demand for product features in life could lead to the increased complexity of the life insurance business,” he said.

20. Retail sales practices High pressure retail sales practices continue to be seen as a risk in the industry, particularly by the life sector which put them in 8th place.

Although this was a well-flagged risk with a strong recent history in the UK, respondents felt it was not truly over. “Mis-selling will hit the insurance market directly,” said the chief executive of a large London-based insurance broker. A UK insurer even saw this risk rising because of the Financial Services Authority’s emphasis on financial institutions “treating customers fairly”, and uncertainty over precisely what this meant, increasing the scope for legal actions. Several respondents felt this issue was linked to the insurance industry’s reputational problems. (See box)

But some felt that the worst was past. “The impact of regulation has reduced this risk,” said a New Zealand CEO.

21. Pollution Though low down the rankings, pollution risk was high among the risers (in 3rd

place) and seen as an area of growth and uncertainty. It ranked highest with property & casualty insurers (13th). The concern was as much with sudden pollution risks as with longer-standing latent risks, such as lead.

While much of the pollution risk business is now well-established, it is constantly evolving, throwing up new risks. One observer questioned whether insurers could “foresee and manage evolving pollution risks (eg nanotechnology, air pollution, genetically modified foods) as governments may not take preventative action.”

Others felt this was an area of legal risk because legislative changes were constantly leading to the creation of new liabilities. One said: “Environmental liability in general may change due to changes in the legal environment, leading to cases of indemnity which would not be possible in today’s legal landscape.”

22. Interest rates The prospect of an extended period of low interest rates is a worry because it will dampen down returns and reduce the appeal of life insurance products. The group finance director of a large UK life insurer felt that “long term low interest rates” were among the greatest risks facing the sector.

Mis-selling hasn’t gone away

What about negative interest rates?

�� ��������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5125

A secondary concern was that low yields would add to pressures on the sector to take higher risks. A Belgian composite insurer saw low interest rates among the factors encouraging insurance companies to buy investments “which are not yet proven to be stable in a real financial market crisis.” Other concerns included the possibility of negative interest rates, the risks in guaranteed interest rate products, and exposure to defaults on the corporate bond market.

But as with equities, many respondents tended to play down this risk, saying that insurance companies were much better at managing swings in interest rates. “Asset and liability management is now widely used”, said a Swiss reinsurer.

23. Corporate governance Some respondents felt that corporate governance was still a problem area for the insurance sector. An executive from a large US broker said: “A number of syndicate/insurers fail to recognise this concept.”

Transparency is also an issue. One insurance company director said the complexities of insurance reporting meant that accounts and performance measurements “are not transparent to non-insiders”. An industry observer felt that greater transparency in corporate governance and accounting “could have an impact

���������������������������������������������������

���� ���������� ��������� ����� ������� �������������� ����������������������� ��������������������������������������������������������������������������������������������������� ����������� ��� ��� ����������� �������� ����� ���� ������ ���������� �������� ��� ����������� ����� ��������� � ���� ������ ���������� ��� �� ������ ��������� �������� ���� ����������������� ��� ��������� ��� ��� ����� ���� ��� �������� ����������� ���������� ���� ������������������������������������ ��������� �� ��� ��������� ���������� ������� ����� ��������� ������� ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ������� ������ ������� ���� ����������� ����������� ���� ����� ��� �� ��������� ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������ ��� ��������� ������ ��� ��������� ������ ������ ������ ������������� � ���� ��������������������� ������������������������ ��������� �������������� ������������������������� ������ ������� ���������� ���� ����� ���������� ��� ����� ����������� ���������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�������� ������� ���� ��� ���� �������� ���� ����� ����������� ���������������� ��������������� ������� ���� ��������� ��� ��������� ������� ����� ���� ��������� ������ �������������������������������� ����� ��������������������������� ����� ��� ������ ��������� ���������������������������������������������������������

Consumerism is on the rise

Corporate governance is off the boil

����������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5126

on the types of risk that the industry is willing to assume, and on capital management.”

But some comments were tinged with impatience. “There is too much focus on corporate governance to the detriment of running the insurance operations and quality underwriting,” said a New Zealand finance manager.

24. Demographic trends Changes in demographics, with people needing different types of insurance, will impact the insurance market heavily in the longer term. They will increase longevity risk for life insurers, and lead to greater claims on health insurance and care policies, and generally challenge the industry’s ability to adapt to changing demand.

However it was not clear whether the industry sees this as a threat or an opportunity. Many respondents were concerned that the industry might baulk at the challenge, by failing to offer appropriate products, or by mispricing evolving risks. A respondent from a Canadian life insurer feared that change in demographics might not be reflected in actuarial data, “resulting in mispriced products”.

But others saw demographic changes triggering demand for new types of insurance protection which far-sighted insurance companies could meet, for example in the areas of long-term care, “dread disease” insurance and disability income coverage. Stan Leslie, general manager of retail solutions at South Africa’s Old Mutual, said insurers must strive to “retain clients over the client life cycle, as their needs change with improvements in financial circumstance.” The group chief accountant at a large UK composite saw “a need for new consumer friendly products” to meet changing customer behaviour.

��������������������

������������������������������������������������������ ������� ��������� ������� �������� ��� ����� ������� � � ����� ������������ ���� ������������� �������� ��� ������������� ��������� ������ �������� ��� ���� ������������� ����������������� ���� ������������� �������� ���� ���� ����������� ����� ���������� ������ ����������������� ��� ��� ������������ ��� �������� ������������ �������� � � � � ������ ������� ������������ ���� ��������� ��� ������������ ����� ���������� ��������� ���� ������������ ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� � � � ��� ���� ���� ����� ����� ��� ������ ���������� ����������� ���� ��������������� ��� ���� ����� ���� ���� ����������� ��� ������������� ����� ����� ������ ������ ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ��� ������� ����������� � � � ����� ���������� ��� ���������� ��� ��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� � � � � ��������� ������� �� ���� ���� ����� ��������� ����������� ����� ��� �������������������������������������������������������������������������������������������������������������������������������������������������������������

Industry reputation under threat

�� �������������������������������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5127

25. Contract wording The wording of insurance contracts is becoming more of a problem as the market softens and insurers allow definitions to widen.

“The softer the market, the broader the coverage” said a London broker. An underwriter with a large German property & casualty company saw contract wording “broadening the scope of cover to unacceptable levels.” One broker blamed it all on policy negotiators who, he said, were often “poor quality”.

Some respondents saw insurers taking a tougher line. Improvements in contract certainty would be among the “key differentiators” in the period ahead, according to the director of risk management at a UK insurer. But there was also concern that the FSA’s insistence on the “treating customers fairly” rule would undermine contract certainty by introducing elements of subjective judgment. Others noted that the industry would respond to pressure from brokers to standardise contracts, and reinforce certainty.

26. Capital availability The problem at this – advanced - stage of the property and casualty insurance cycle is that there is too much capital in the market rather than too little, creating overcapacity and sharpening competition. Many of our respondents saw margins being cut to the bone. “There’s too much capital chasing bulk annuity deals,” said the non-executive director of a reinsurance company. “This is a soft market, so availability is not an issue,” said a New Zealand CEO.

Much of this extra capital comes from hedge funds and private equity But will it survive the down side of the cycle? “At present capital (traditional, retained earnings and new such as hedge funds) is relatively plentiful,” said the chief executive of a brokerage specialising in capital markets. “But new capital could disappear if we have a prolonged soft market and/or a series of major losses.”

However, the capital surplus is not evenly spread. In several emerging markets in East Europe and South East Asia, respondents said that capital was tight, usually because of a lack of foreign investment.

27. Security of reinsurance The main concern over the security of reinsurance (insurance for insurers) is the replacement of traditional providers by new sources of capital, particularly hedge funds and private investors who might not have the same level of commitment or understanding of the market. “Who really owns reinsurance companies?” wondered one respondent.

����� ������� ��� ��������� ���� ������������������������������ ����������������������������� ��� �������� ������������ ������������� ��� ����� ���������� � ����� �������������� ���� ����� ��� ������� ��������������� ������ ������ ���� �������� ���������������� ���� ���� ��� ����������������������������������������������������������

Contracts are softening under pressure

Hedge funds are stepping up with new capital

����������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5128

An industry observer “the capacity and resilience of international reinsurance markets in respect of large-scale risks” could be a problem as markets become more difficult. A Swiss reinsurer said the market should be differentiated: the problem of reinsurance security lay more in the area of long tail than short tail risks because of questions about the sustainability of new capacity.

28. Availability of reinsurance Though low in the Banana Skins rankings, a reduction in the availability of reinsurance is a potential risk. The number of major reinsurers in the world is small, and capital to underpin the business could be in short supply. Although this is not currently the case because of the inflow of capital from hedge funds and private investors, “some of the ‘hot’ money could disappear again”, according to a UK broker.

Bertrand Wollner, chief executive of Signal Iduna Insurance in Switzerland, said that the risk profile of professional reinsurers had changed dramatically. “Insurers have increased their retentions and pushed reinsurers up the risk scale. At the same time, many insurance companies have stopped writing reinsurance and the risks are concentrated among a few players in the reinsurance markets. The risk of a big failure is increasing. I’m concerned that the insurance industry is getting less choice to place its risks. The new set-ups in Bermuda are not an alternative.”

Some respondents were more sanguine. “There are new players in some lines, and balance sheets are stronger,” was one comment.

29. Business continuation The ability to overcome severe business disruptions, for example from terrorism, might have been a big deal after 9/11, but not any more. Few of our respondents bothered to comment on this Banana Skin. “Most insurers have suitable business continuation plans,” said a UK insurer.

30. Fraud Fraud is a problem, but the industry feels it can handle it, as its low place in the rankings suggests. The chief risk officer at a large UK life company put “financial crime” among his top Banana Skins and the head of group risk reporting at a large Swiss reinsurer said that while the frequency of fraud might be low, the “reputational impact is high”. But the chief executive of a large German insurance company thought this risk was falling. ”Awareness has increased,” he said. Several insurers made a point of saying that their staff and agents were honest.

But looking ahead, there was concern among some respondents about new types of fraud, particularly as a result of new technology. The chief financial officer of a large UK life insurer expected fraud to become “more sophisticated” with a greater risk of people hacking into databases. A supplier of technology to the industry also pointed out that “the push towards operational simplicity is creating new fraud risks.” There was a concern that the growing “claims culture” among the insured would encourage fraudulent claims.

Fraud is seen as a very low level risk

�� ��������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5129

31. Merger mania Although this was low in the rankings, merger mania was seen as one of the faster rising risks. Further consolidation in the insurance industry is expected, raising the spectre of mergers that increase concentration in the business, or don’t work out.

A UK consultant saw “a continued focus on consolidating balance sheets and outsourcing of business processes.” In Switzerland, a reinsurer said that consolidation would result in “concentration of risk for reinsureds and strain on balance sheets.”

Several respondents expected to see consolidation among broking houses. The group strategist of a major Australian insurer was concerned that this would lead to “increased commoditisation” of the business and a shift towards standard wordings and aggregation price comparators.

Some respondents noted that pressure to merge was very strong, and that management would need self-discipline to resist it. But one insurance chief executive felt that the danger of bad deals was small. “The capital market should control that,” he said.

32. Too little regulation The problem with regulation is too much rather than too little. Nonetheless, regulation could be inadequate in two respects: international coordination, and in emerging markets.

There was “too much in Europe and too little in the Third World,” said the finance director of a UK insurer. Respondents from countries such as Russia and Thailand said regulation in their countries was inadequate, though they were referring to the quality rather than the quantity. A Swiss reinsurer complained of “the burden of inconsistent national requirements,” though he added: “But too little regulation endangers the reputation of whole industry.”

A regulator said that there was too little regulation of the reinsurance market. “Many of the largest reinsurance companies are located in jurisdictions that either deliberately have minimal regulatory oversight or, if they do, they lack the regulatory muscle. If things get really bad they also lack the financial muscle to sort things out. A major reinsurer in a G10 country may well get bailed out if the worst comes to the worst. Bermuda can’t afford it.”

33. Asbestos Once the terror of the insurance world, asbestos risk has dropped to the bottom of the list. Time has done its work, and exposures are down, though one respondent cautioned: “Stable, but always a risk.”

���� ������ ��� �������� ������������������������ ���� ������ �����������������������������������������������������������������������������������������������������

Further consolidation is expected

More regulation needed in the Third World

����������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5130

Preparedness We asked the question: “How well prepared do you think your own and other institutions are to handle the risks you have identified?” Respondents could answer: poorly, mixed or well.

Poorly3%

Mixed76%

Well21%

More than three quarters of the respondents replied “mixed”, usually because they differentiated between their own preparedness, or those of the group to which they felt they belonged (eg the home team) which was seen to be good, and that of another group (eg new entrants), which was less good. But the “mixed” responses often had a positive tone. One respondent replied “mixed but improving”.

Just over a fifth answered “well”. The most frequent reasons were that the insurance industry was well-placed to manage the insurance cycle and the vagaries of the financial markets. The industry also believed that it would “see off” new competition. The group finance director of a large UK life insurer said: “Generally, I am more confident of the outlook for the life industry than at any time in the last seven years.”

Only three per cent answered “poorly”. The reasons included poor adaptability to more competitive environment, staffing problems, and a complacent attitude towards cycle management.

I’m OK, but what about them?

�� ��������������������� ����������������������������������������������

�����������������������

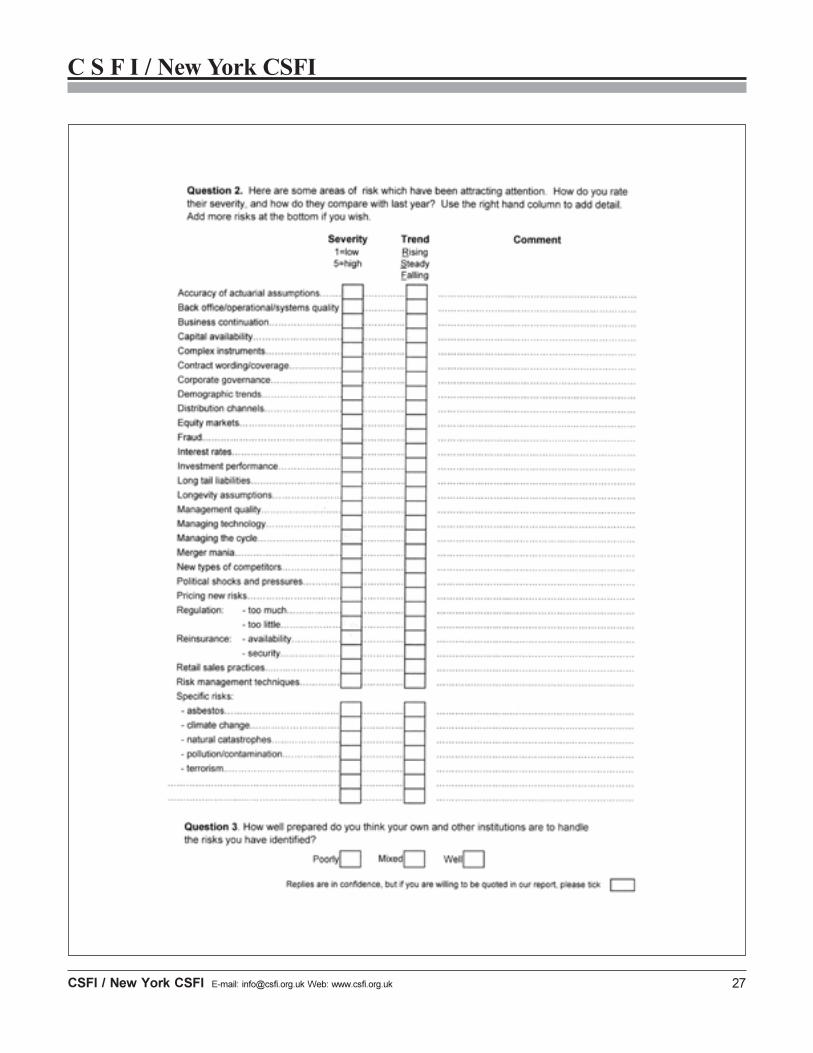

APPENDIX: The questionnaire

Banana Skins Template 07.pmd 15/05/2007, 16:5131

����������������������� ����������������������������������������������

�����������������������

Banana Skins Template 07.pmd 15/05/2007, 16:5132

�����������������

�� ����������������������������������������������� ��������������������������������������� ��������������������������������� ����� ������������ ���������������������������������������������������� ����

�� ����������������� ������������������������������� ���������� ������� ����������������� ��� ������������������� �������� ��� ���������� ������������� ���������� ���������� ����� ��� �������������� ��������������������������������� ���������������� ����������

�� ���������������������������������������� ����������������������������������������������������� �������������� ��������� �������� ���� ���������� �������� ���������� ����� ������������������������������������������

�� �������������������������� ���� ������������ �������������������������������������� ����������������� ����������������� ������ ������ �������������������������������������������� ������� �������� ����

�� ����������������������������� ���� �������������������������������������� ����� �������������������������������� ����� ����������������� ���� �����������������������������������������������

�� ���� ���������� ���������������� �������� ��������� ���� ������������� ���������� �������������������������������������� ����� ������� ����������� �����������������

�� ���������������������������� ������ ������������������������������� ����������������� ������������������ ������� ��� ������� ��� ������� ������ ���������

�� ����������������������������������������������������������� �������������������������������������� �������������� ����������������� ��� ��������������������������������������� ��� ������������� �������� �������������������������������� ����� ����