back to basics: mortgage lending 101

TRANSCRIPT

Back to Basics:Mortgage Lending

101June 16, 2015

Emily C IngramNew American Funding

Who is Emily C Ingram?• Local mortgage lender with New

American Funding

• 14+ years experience

• Loan originator, processor, and underwriter

• Bachelor’s degree in mathematics

• Board member, Jefferson Co Home Builders Association

• Board member, Real Estate Professionals for Affordable Housing

• Occasionally skips work to go sailing.

Obligatory Disclosures

• I’m pretty smart, but I don’t know everything.• Change is inevitable.

Objectives

• Discuss types of mortgage lenders• Recognize categories of mortgage products• Identify (and sell) “problem” property types• Utilize mortgage programs and products to

increase buyer’s purchasing power.

Types of Mortgage Lenders

Origination Underwriting Funding Servicing

Depository Institution X X X X

Mortgage Bank/Lender X X X X

Correspondent Lender X X X

Mortgage Broker X

Categories of Mortgage Loans

• Conventional ConformingFNMA / FHLMC

• GovernmentFHA / VA / USDA

• Conventional Non-ConformingFunky Products / Funky People / Funky Properties

Conventional Conforming• Who is Fannie Mae & Freddie Mac?• Guidelines established by FNMA and FHLMC• Popular vanilla loan choice• Make sure your lender can choose!

The GSEs asset holdings – either through mortgage securitizations or direct portfolio holdings – have increased from approximately 7% of total residential mortgage market originations in 1980 ($78 billion) to 46.7% in 2010 ($5.3 trillion).- Federal Housing Finance Agency

Features & Benefits“Standard”

Conventional ConformingMy CommunityHome Possible

Minimum Down Payment 5% 3%

Up Front Mortgage Ins private MI required with < 20% down

lower private MI requirementsMonthly Mortgage Ins

Income Limits none $72,680

Property Type SFR, 2-4 units, manuf, condo SFR, condo

Occupancy primary, 2nd, non owner primary

Interested Party Contribution 2% - 9% 3%

Max Loan Amount $417,000 $417,000

Max DTI 45% 43-45%

Credit Score 620 660

FTHB Restriction no yes and no

Home Buyer Education not required required

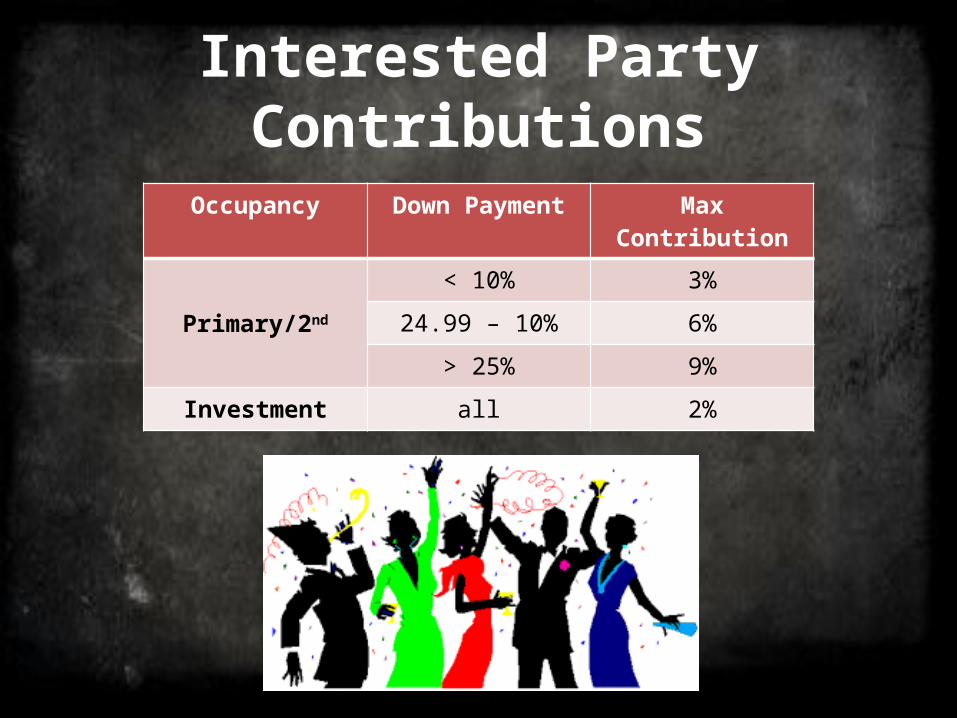

Interested Party Contributions

Occupancy Down Payment Max Contribution

Primary/2nd

< 10% 3%

24.99 – 10% 6%

> 25% 9%

Investment all 2%

Government - FHA

• Who is FHA?• More lenient guidelines• Have a bad rap• Guidelines will change in September

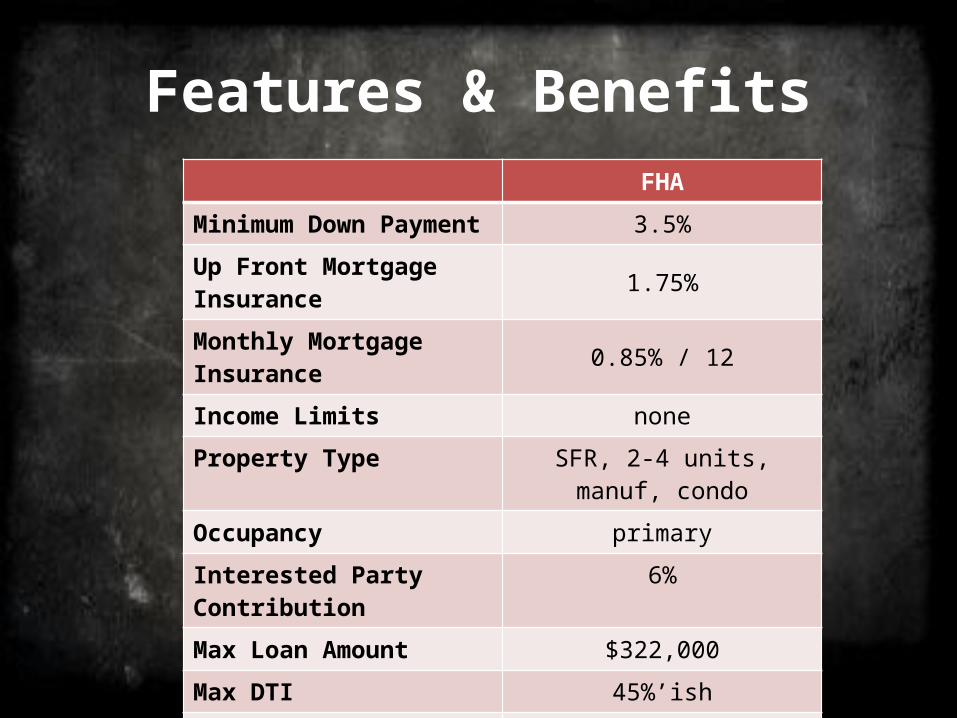

Features & BenefitsFHA

Minimum Down Payment 3.5%Up Front Mortgage Insurance 1.75%Monthly Mortgage Insurance 0.85% / 12Income Limits noneProperty Type SFR, 2-4 units, manuf, condo

Occupancy primaryInterested Party Contribution 6%Max Loan Amount $322,000Max DTI 45%’ishCredit Score 580FTHB Restriction noHome Buyer Education not required

Government - VA

• Who is VA• Eligible veterans (COE)• Big draw = 0% down• Non-allowable fees• Tougher appraisals

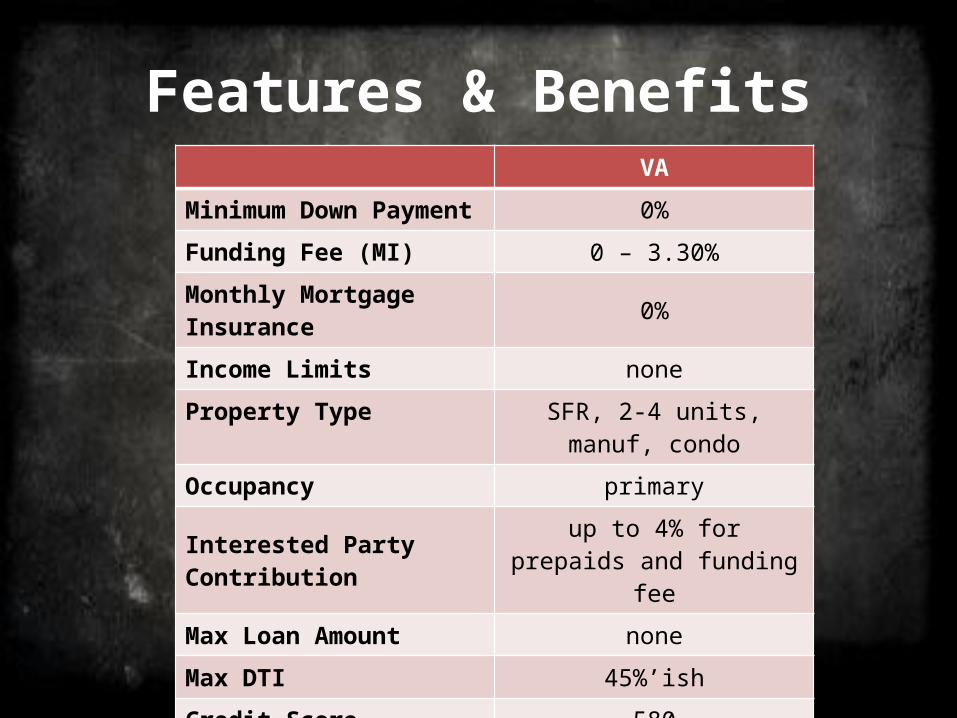

Features & BenefitsVA

Minimum Down Payment 0%Funding Fee (MI) 0 – 3.30%Monthly Mortgage Insurance 0%Income Limits noneProperty Type SFR, 2-4 units, manuf, condo

Occupancy primary

Interested Party Contribution up to 4% for prepaids and funding fee

Max Loan Amount noneMax DTI 45%’ishCredit Score 580FTHB Restriction noHome Buyer Education not required

Government - USDA

• Who is USDA?• Rural properties / income limits• No down payment• Allow additional time for closing• No income producing properties

Features & BenefitsUSDA

Minimum Down Payment 0%Guarantee Fee (MI) 2.0%Monthly Mortgage Insurance 0.5% / 12Income Limits $75,650Property Type SFR, condo

Occupancy primaryInterested Party Contribution 6%Max Loan Amount noneMax DTI 29/41% (32/44%)Credit Score 620FTHB Restriction noHome Buyer Education not required

Condominiums• Condo project must be eligible• No “spot” approvals• FNMA/FHLMC, FHA, and VA all have slightly

different guidelines• If you list a condo, have it pre-approved by

your lender!

Manufactured Homes

• Fewer options• Doublewide• Built after June, 1976• Moved only once• Permanent foundation• Foundation inspection• L&I inspections

Down Payment Assistance

• Available through WSHFC • Second mortgage used for down payment• Some have deferred payments/no interest• Follow standard underwriting guidelines • No FTHB requirement• Must work with an “approved” lender• Income limits• Home buyer education

required• Higher interest rates

Mortgage Credit Certificate

• Tax credit equal to 20% of annual interest• Afford a slightly larger home• Program can be combined with any mortgage• Must work with an “approved” lender• First time home buyer• Income limit $70,000 (1-2 people)• Acquisition limit $310,000• Home buyer education required

Conventional Non-Conforming

• Funky products, people, or property

• Lenders determine guidelines

• Lenders determine interest rates

• Fewer options

Funky Products

Jumbo Loans• Loan amounts > $417,000• Intense competition• 20-25% down payment• Credit scores 680+• Lower debt to income ratios• Reserves required

Other funky products: interest only, construction loans, lines of credit

Funky People

• Recent major derogatory credit

• Asset dissipation• High debt to income ratio• Stated income• Foreign national

Funky Properties

• Non-warrantable condos• Hobby farms• Log homes• Handled case-by-case

Refer to New American Funding!(aka Shameless Self Promotion)

• More product options• Better customer service• Who ya’ gonna call?• Local appraisers• Go the extra mile• 40 years combined experience in Port Townsend

Referral Best Practices

“The first lender I would have you talk to would be : Emily Ingram of New American Funding, her phone number is 360-531-1934 and I have seen her follow through and admire her work style and dedication.

I, by office policy, must recommend two other lenders for you to contact. Acme Bank has a good reputation (www.acme.com). And also USA Mortgage Co, specifically, Jane Doe at 360-555-1212.”

• Call with the buyer sitting in the office• Give the referral partner the buyer’s

name/number• The “multiple business cards” scenario

Contact Me!

www.facebook.com/emilycaryl

www.linkedin.com/in/emilycaryl

www.slideshare.net/EmilyCIngram1