auxiliary organizations update chapter 8 presented by lily wang chancellor’s office kpmg llp

Post on 21-Dec-2015

214 views

TRANSCRIPT

Auxiliary Organizations UpdateChapter 8

Presented by Lily WangChancellor’s Office

KPMG LLP

2

May 2008 GAAP Reporting Workshop

© 2

00

8 K

PM

G L

LP,

the U

.S.

mem

ber

firm

of

KPM

G In

tern

ati

on

al, a

Sw

iss

coop

era

tive.

All

rig

hts

rese

rved

. Pri

nte

d in

U.S

.A.

KPM

G a

nd

th

e K

PM

G log

o a

re r

eg

iste

red

tra

dem

ark

s of

KPM

G In

tern

ati

on

al.

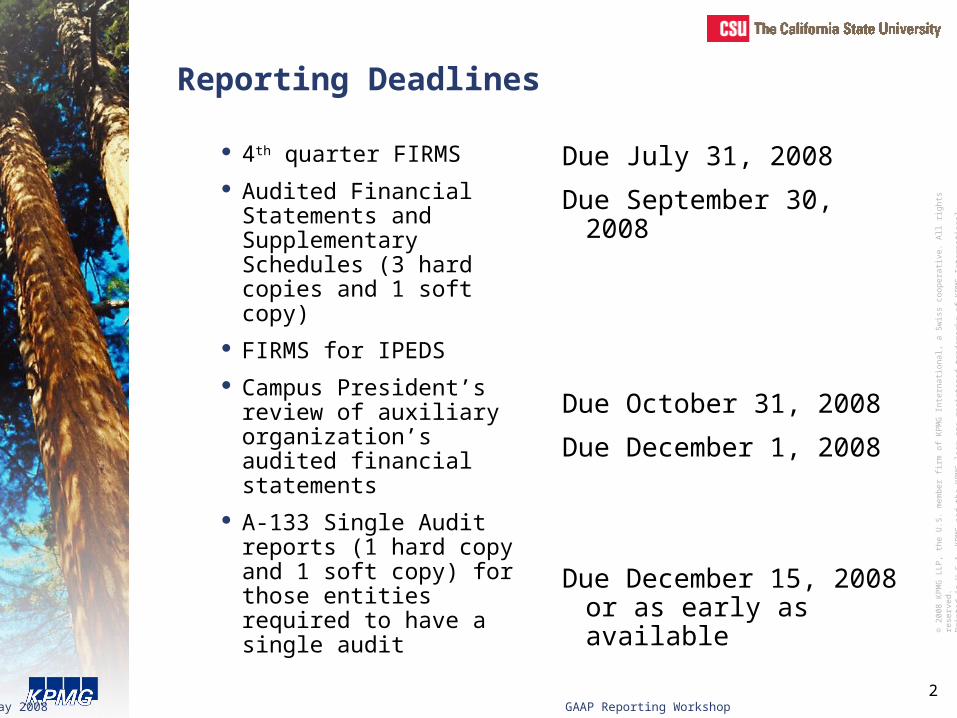

Reporting Deadlines

4th quarter FIRMS

Audited Financial Statements and Supplementary Schedules (3 hard copies and 1 soft copy)

FIRMS for IPEDS

Campus President’s review of auxiliary organization’s audited financial statements

A-133 Single Audit reports (1 hard copy and 1 soft copy) for those entities required to have a single audit

Due July 31, 2008

Due September 30, 2008

Due October 31, 2008

Due December 1, 2008

Due December 15, 2008 or as early as available

3

May 2008 GAAP Reporting Workshop

© 2

00

8 K

PM

G L

LP,

the U

.S.

mem

ber

firm

of

KPM

G In

tern

ati

on

al, a

Sw

iss

coop

era

tive.

All

rig

hts

rese

rved

. Pri

nte

d in

U.S

.A.

KPM

G a

nd

th

e K

PM

G log

o a

re r

eg

iste

red

tra

dem

ark

s of

KPM

G In

tern

ati

on

al.

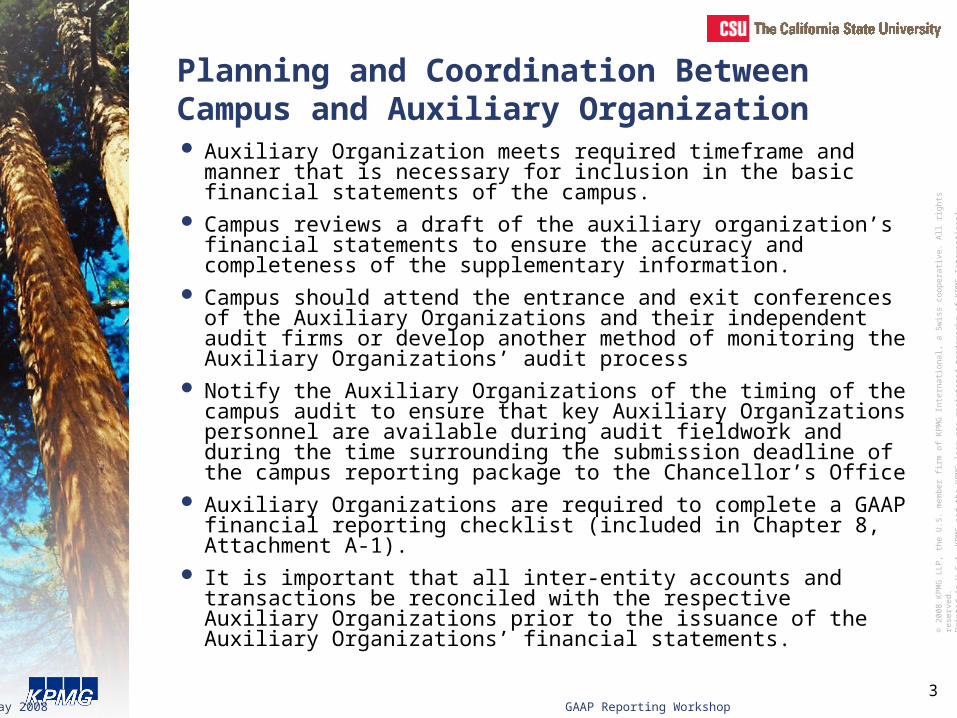

Planning and Coordination Between Campus and Auxiliary Organization Auxiliary Organization meets required timeframe and manner that is

necessary for inclusion in the basic financial statements of the campus. Campus reviews a draft of the auxiliary organization’s financial statements

to ensure the accuracy and completeness of the supplementary information.

Campus should attend the entrance and exit conferences of the Auxiliary Organizations and their independent audit firms or develop another method of monitoring the Auxiliary Organizations’ audit process

Notify the Auxiliary Organizations of the timing of the campus audit to ensure that key Auxiliary Organizations personnel are available during audit fieldwork and during the time surrounding the submission deadline of the campus reporting package to the Chancellor’s Office

Auxiliary Organizations are required to complete a GAAP financial reporting checklist (included in Chapter 8, Attachment A‑1).

It is important that all inter-entity accounts and transactions be reconciled with the respective Auxiliary Organizations prior to the issuance of the Auxiliary Organizations’ financial statements.

4

May 2008 GAAP Reporting Workshop

© 2

00

8 K

PM

G L

LP,

the U

.S.

mem

ber

firm

of

KPM

G In

tern

ati

on

al, a

Sw

iss

coop

era

tive.

All

rig

hts

rese

rved

. Pri

nte

d in

U.S

.A.

KPM

G a

nd

th

e K

PM

G log

o a

re r

eg

iste

red

tra

dem

ark

s of

KPM

G In

tern

ati

on

al.

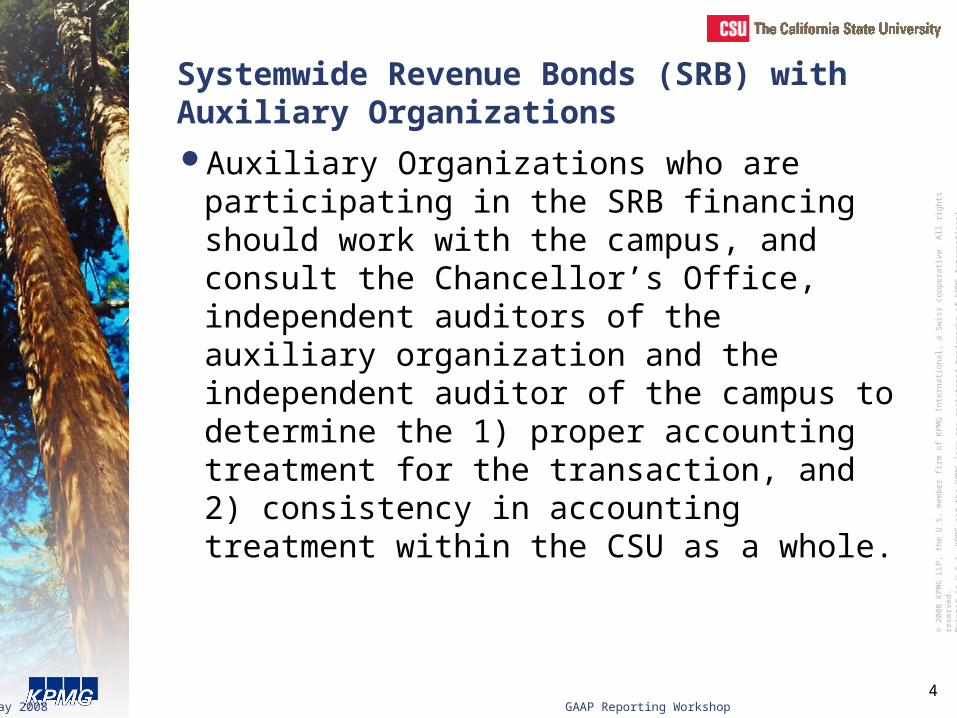

Systemwide Revenue Bonds (SRB) with Auxiliary OrganizationsAuxiliary Organizations who are participating in

the SRB financing should work with the campus, and consult the Chancellor’s Office, independent auditors of the auxiliary organization and the independent auditor of the campus to determine the 1) proper accounting treatment for the transaction, and 2) consistency in accounting treatment within the CSU as a whole.

5

May 2008 GAAP Reporting Workshop

© 2

00

8 K

PM

G L

LP,

the U

.S.

mem

ber

firm

of

KPM

G In

tern

ati

on

al, a

Sw

iss

coop

era

tive.

All

rig

hts

rese

rved

. Pri

nte

d in

U.S

.A.

KPM

G a

nd

th

e K

PM

G log

o a

re r

eg

iste

red

tra

dem

ark

s of

KPM

G In

tern

ati

on

al.

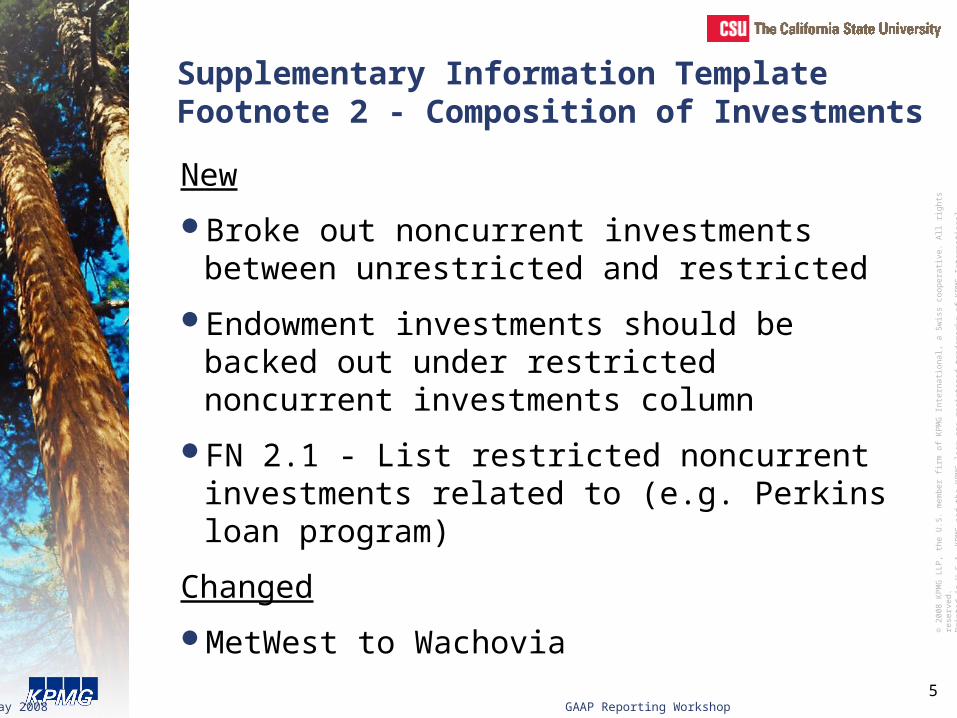

Supplementary Information Template Footnote 2 - Composition of Investments

New

Broke out noncurrent investments between unrestricted and restricted

Endowment investments should be backed out under restricted noncurrent investments column

FN 2.1 - List restricted noncurrent investments related to (e.g. Perkins loan program)

Changed

MetWest to Wachovia

6

May 2008 GAAP Reporting Workshop

© 2

00

8 K

PM

G L

LP,

the U

.S.

mem

ber

firm

of

KPM

G In

tern

ati

on

al, a

Sw

iss

coop

era

tive.

All

rig

hts

rese

rved

. Pri

nte

d in

U.S

.A.

KPM

G a

nd

th

e K

PM

G log

o a

re r

eg

iste

red

tra

dem

ark

s of

KPM

G In

tern

ati

on

al.

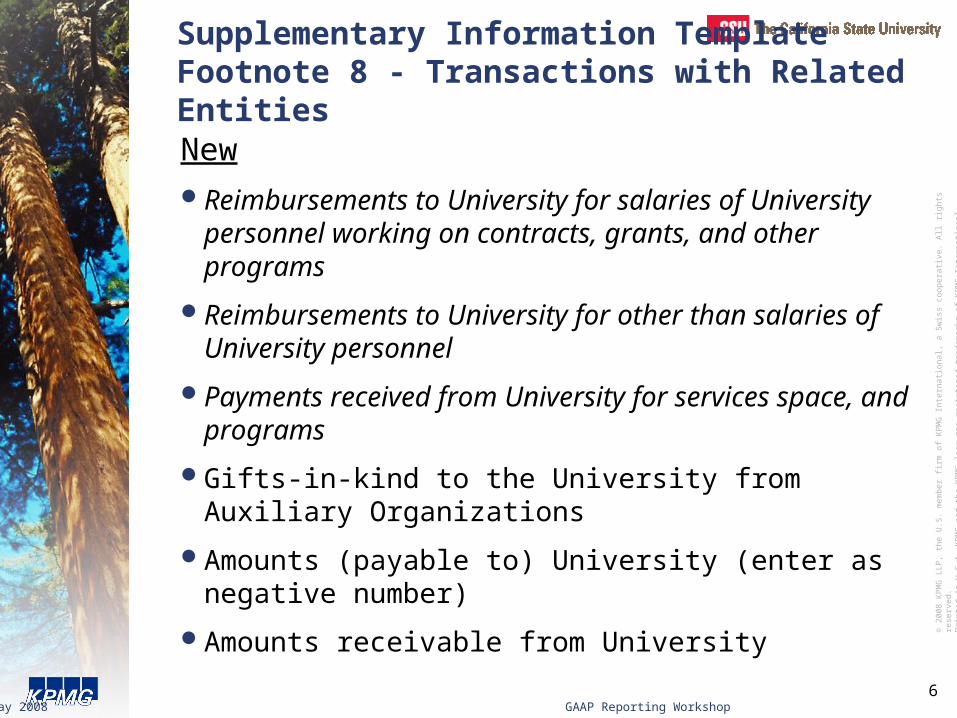

Supplementary Information Template Footnote 8 - Transactions with Related EntitiesNewReimbursements to University for salaries of University

personnel working on contracts, grants, and other programs

Reimbursements to University for other than salaries of University personnel

Payments received from University for services space, and programs

Gifts-in-kind to the University from Auxiliary Organizations

Amounts (payable to) University (enter as negative number)

Amounts receivable from University

7

May 2008 GAAP Reporting Workshop

© 2

00

8 K

PM

G L

LP,

the U

.S.

mem

ber

firm

of

KPM

G In

tern

ati

on

al, a

Sw

iss

coop

era

tive.

All

rig

hts

rese

rved

. Pri

nte

d in

U.S

.A.

KPM

G a

nd

th

e K

PM

G log

o a

re r

eg

iste

red

tra

dem

ark

s of

KPM

G In

tern

ati

on

al.

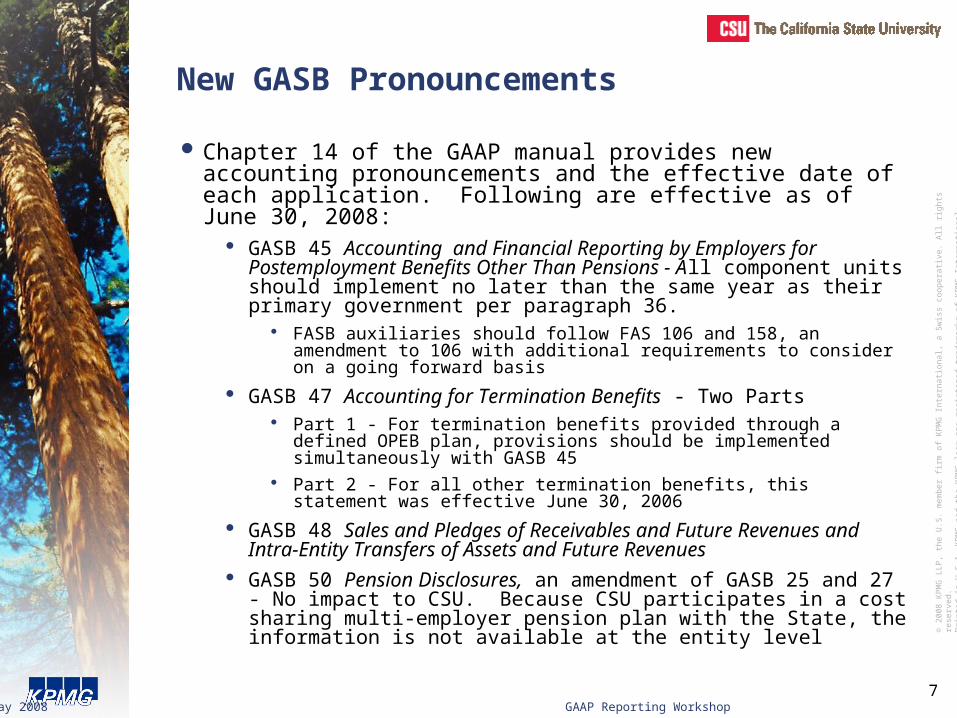

New GASB Pronouncements

Chapter 14 of the GAAP manual provides new accounting pronouncements and the effective date of each application. Following are effective as of June 30, 2008:

GASB 45 Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions - All component units should implement no later than the same year as their primary government per paragraph 36.

FASB auxiliaries should follow FAS 106 and 158, an amendment to 106 with additional requirements to consider on a going forward basis

GASB 47 Accounting for Termination Benefits - Two Parts Part 1 - For termination benefits provided through a defined OPEB plan,

provisions should be implemented simultaneously with GASB 45 Part 2 - For all other termination benefits, this statement was effective

June 30, 2006

GASB 48 Sales and Pledges of Receivables and Future Revenues and Intra-Entity Transfers of Assets and Future Revenues

GASB 50 Pension Disclosures, an amendment of GASB 25 and 27 - No impact to CSU. Because CSU participates in a cost sharing multi-employer pension plan with the State, the information is not available at the entity level

8

May 2008 GAAP Reporting Workshop

© 2

00

8 K

PM

G L

LP,

the U

.S.

mem

ber

firm

of

KPM

G In

tern

ati

on

al, a

Sw

iss

coop

era

tive.

All

rig

hts

rese

rved

. Pri

nte

d in

U.S

.A.

KPM

G a

nd

th

e K

PM

G log

o a

re r

eg

iste

red

tra

dem

ark

s of

KPM

G In

tern

ati

on

al.

References

Financial Accounting Services Training, Education & Development Portal

https://zeta.calstate.edu:8250/portal/page?_pageid=74,1&_dad=portal&_schema=PORTAL

GAAP Manual 2008 http://www.calstate.edu/SFSR/GAAP/Manual2008/GA

AP_Manual.shtmlAuxiliary Organization FIRMS Template 2008

http://www.calstate.edu/SFSR/y-e-r_instructions/2007-2008/index.shtml

IPEDS Template 2008 http://www.calstate.edu/sfsr/