auvs and rovsauvs and rovs – global market prospects · auvs and rovsauvs and rovs – global...

TRANSCRIPT

AUVs and ROVsAUVs and ROVs ––AUVs and ROVs AUVs and ROVs

Global Market ProspectsGlobal Market Prospectspp

Paul NewmanPaul Newman

John WestwoodJohn Westwood

UUV OI London

1UUV OI, London13 Mar 2012

UUV OI London13 Mar 2012

www.dw‐1.com

Our Business

History and Office Locations• Established 1990• Aberdeen Canterbury London• Aberdeen, Canterbury, London, New York & Singapore

Activities & Service Linesoffshore power• Business strategy & advisory

• Commercial due‐diligence• M k t h & l i• Market research & analysis• Published market studies

Large Diversified Client Base

LNGonshore LNG

Large, Diversified Client Base• 750 projects, >400 clients, >70 countries

• Leading global corporates• Energy majors and their suppliers• Investment banks & PE firms

2UUV OI, London13 Mar 2012downstream renewables

Investment banks & PE firms• Government agencies

© Douglas-Westwood Limited 2011

3UUV OI, London13 Mar 2012

4UUV OI, London13 Mar 2012

From man to machine

Market drivers

Work class ROVs

AUVs

C l iConclusions

5UUV OI, London13 Mar 2012

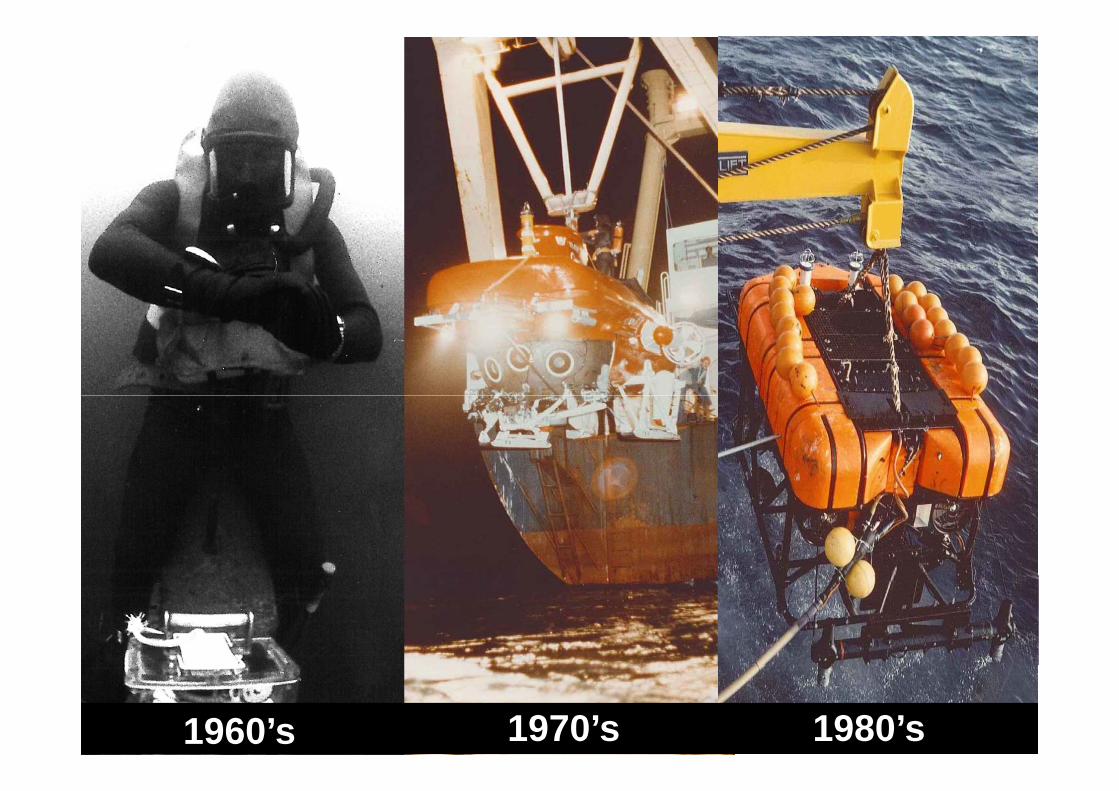

From man to machine

•Offshore•Offshore

6UUV OI, London13 Mar 2012 61960’s 1970’s 1980’s

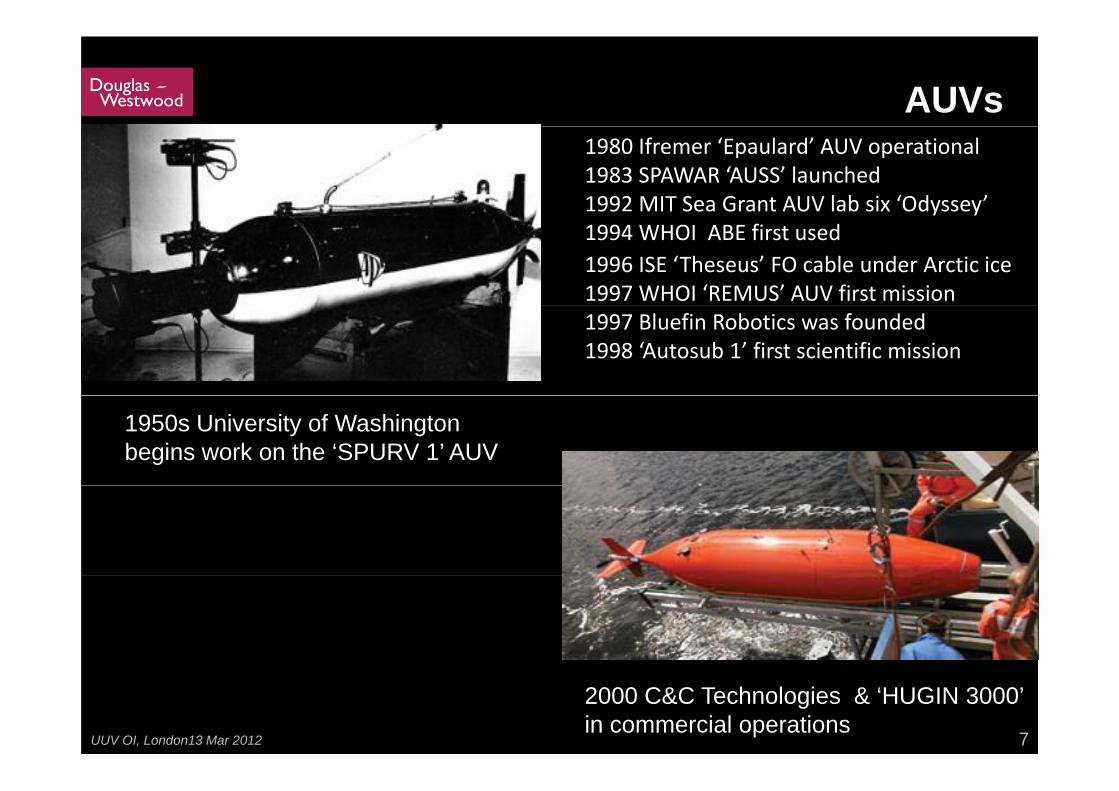

AUVs1980 Ifremer ‘Epaulard’ AUV operational1983 SPAWAR ‘AUSS’ launched1992 MIT Sea Grant AUV lab six ‘Odyssey’1994 WHOI ABE first used1996 ISE ‘Theseus’ FO cable under Arctic ice 1997 WHOI ‘REMUS’ AUV first mission1997 Bluefin Robotics was founded 1998 ‘Autosub 1’ first scientific mission

1950s University of Washington begins work on the ‘SPURV 1’ AUV

7UUV OI, London13 Mar 2012

2000 C&C Technologies & ‘HUGIN 3000’ in commercial operations

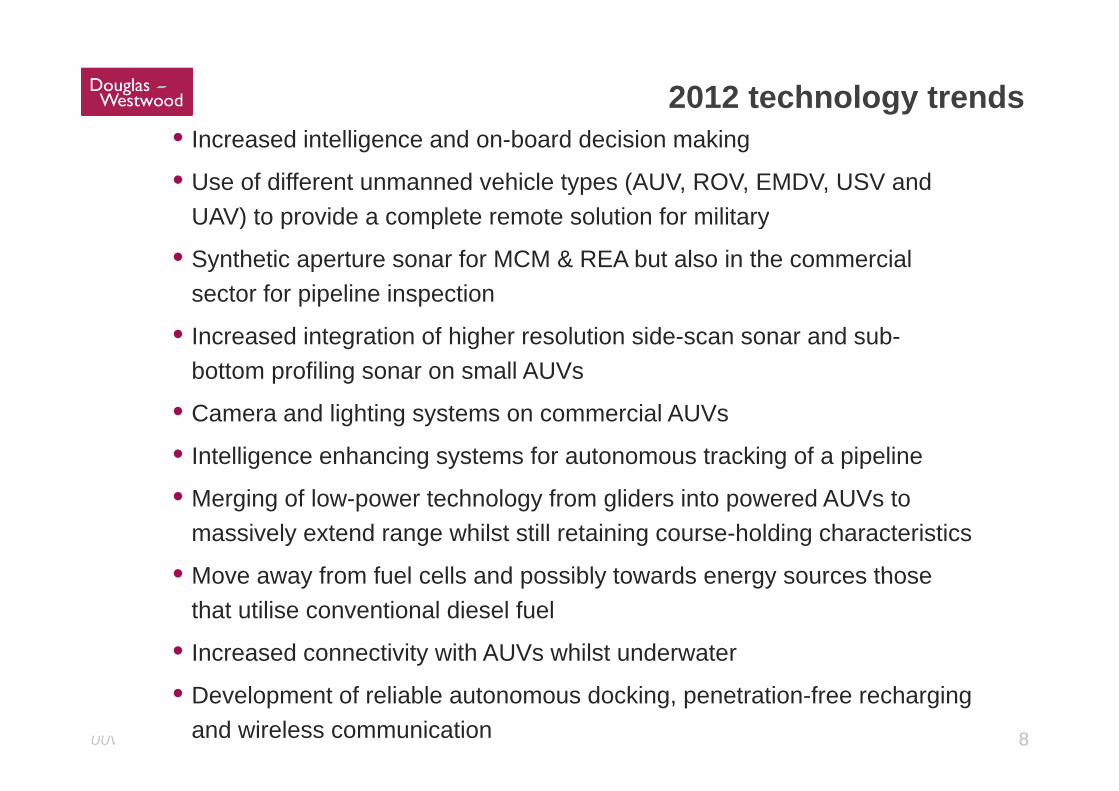

2012 technology trends• Increased intelligence and on-board decision making

• Use of different unmanned vehicle types (AUV, ROV, EMDV, USV and UAV) to provide a complete remote solution for militaryUAV) to provide a complete remote solution for military

• Synthetic aperture sonar for MCM & REA but also in the commercial sector for pipeline inspectionp p p

• Increased integration of higher resolution side-scan sonar and sub-bottom profiling sonar on small AUVs

• Camera and lighting systems on commercial AUVs

• Intelligence enhancing systems for autonomous tracking of a pipeline

• Merging of low-power technology from gliders into powered AUVs to massively extend range whilst still retaining course-holding characteristics

• Move away from fuel cells and possibly towards energy sources those• Move away from fuel cells and possibly towards energy sources those that utilise conventional diesel fuel

• Increased connectivity with AUVs whilst underwater

8UUV OI, London13 Mar 2012

y

• Development of reliable autonomous docking, penetration-free recharging and wireless communication

From man to machine

Market drivers

Work class ROVs

AUVs

C l iConclusions

9UUV OI, London13 Mar 2012

Three key marketsMarket sectors

Offshore O&GOffshore O&GResearchResearch

Offshore O&GOffshore O&G

10UUV OI, London13 Mar 2012

DefenceDefenceHydrographyHydrography

Offshore oil & gas market drivers

• Growing offshore E&P programmes

• Deeper waters, remote and harsh environments (e.g. Arctic)

• P t ti l f lif f fi ld i ti• Potential for life-of-field inspection solutions

• High costs of pipeline inspection using• High costs of pipeline inspection using conventional systems

• Drives for efficiency and cost reductionDrives for efficiency and cost reduction with respect to vessel time

11UUV OI, London13 Mar 2012

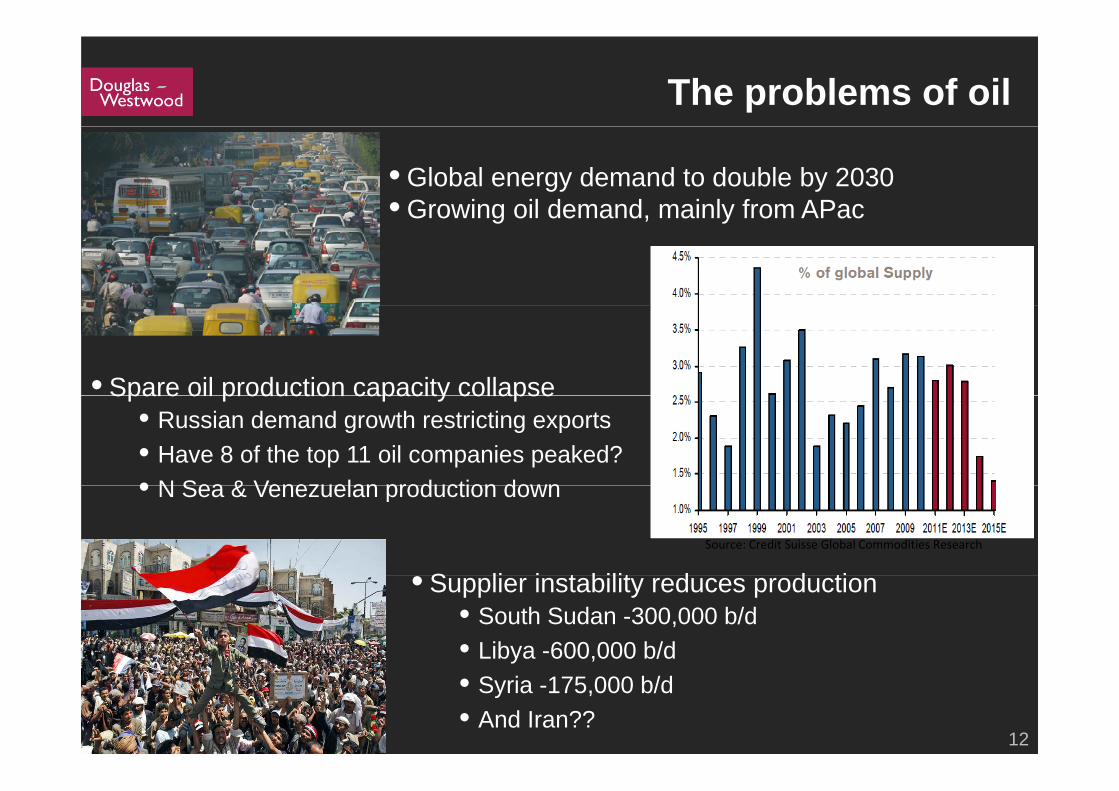

The problems of oil

• Global energy demand to double by 2030• Growing oil demand, mainly from APacGrowing oil demand, mainly from APac

• Spare oil production capacity collapseSpare oil production capacity collapse• Russian demand growth restricting exports• Have 8 of the top 11 oil companies peaked?• N Sea & Venezuelan production down• N Sea & Venezuelan production down

S li i t bilit d d tiSource: Credit Suisse Global Commodities Research

• Supplier instability reduces production• South Sudan -300,000 b/d• Libya -600,000 b/d

12UUV OI, London13 Mar 2012

• Syria -175,000 b/d• And Iran??

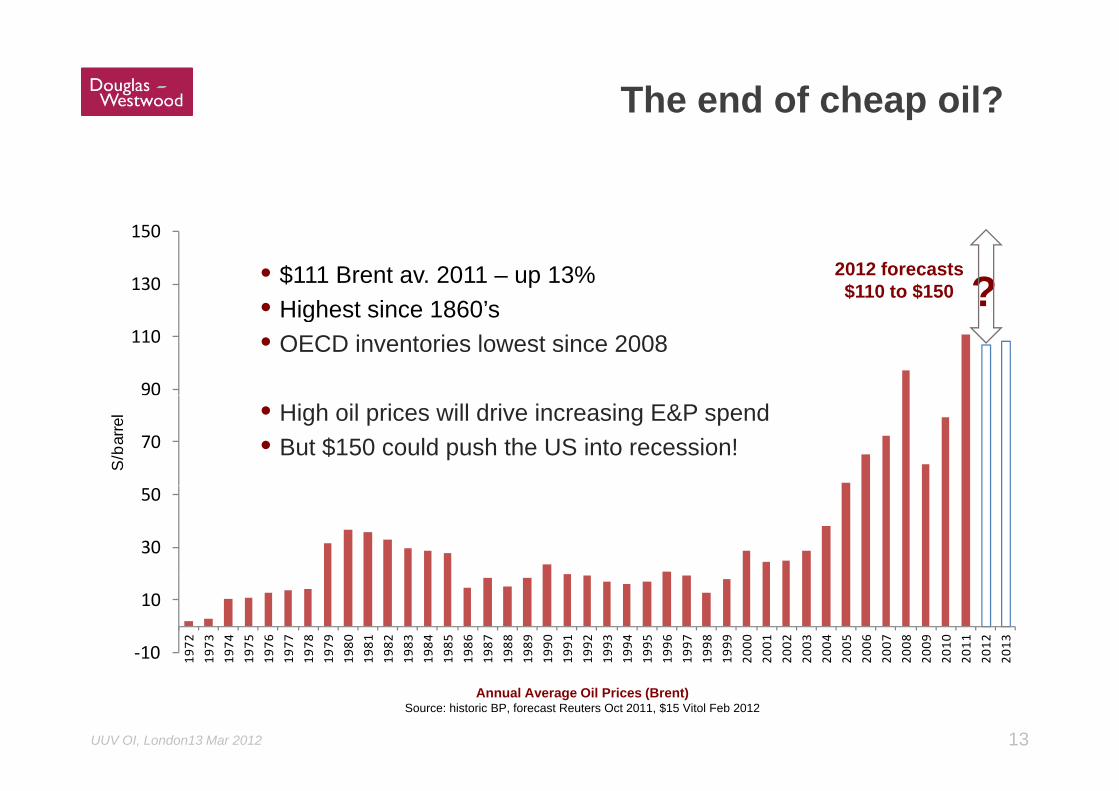

The end of cheap oil?

130

150

• $111 Brent av. 2011 – up 13%• Highest since 1860’s ?

2012 forecasts$110 to $150

90

110• Highest since 1860 s• OECD inventories lowest since 2008

?

70

S/b

arre

l • High oil prices will drive increasing E&P spend• But $150 could push the US into recession!

30

50

‐10

10

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

13UUV OI, London13 Mar 2012

Annual Average Oil Prices (Brent) Source: historic BP, forecast Reuters Oct 2011, $15 Vitol Feb 2012

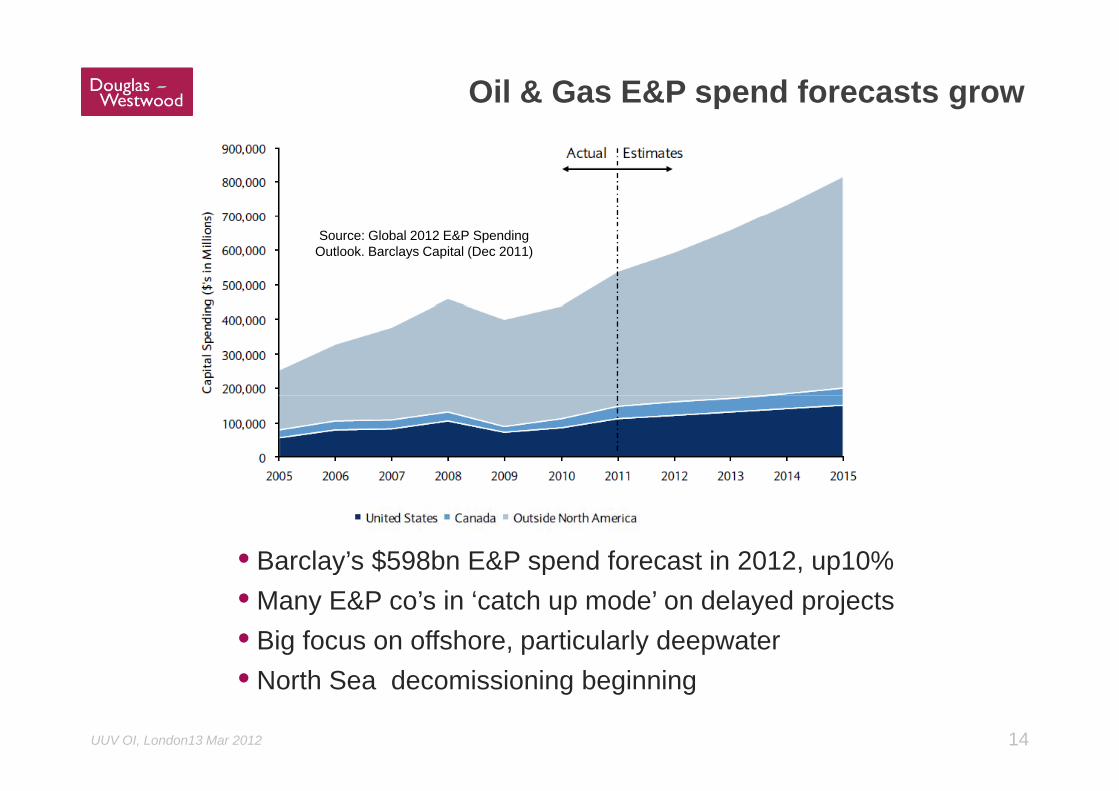

Oil & Gas E&P spend forecasts grow

Source: Global 2012 E&P Spending Outlook. Barclays Capital (Dec 2011)

• Barclay’s $598bn E&P spend forecast in 2012, up10%y• Many E&P co’s in ‘catch up mode’ on delayed projects• Big focus on offshore, particularly deepwater

14UUV OI, London13 Mar 2012

• North Sea decomissioning beginning

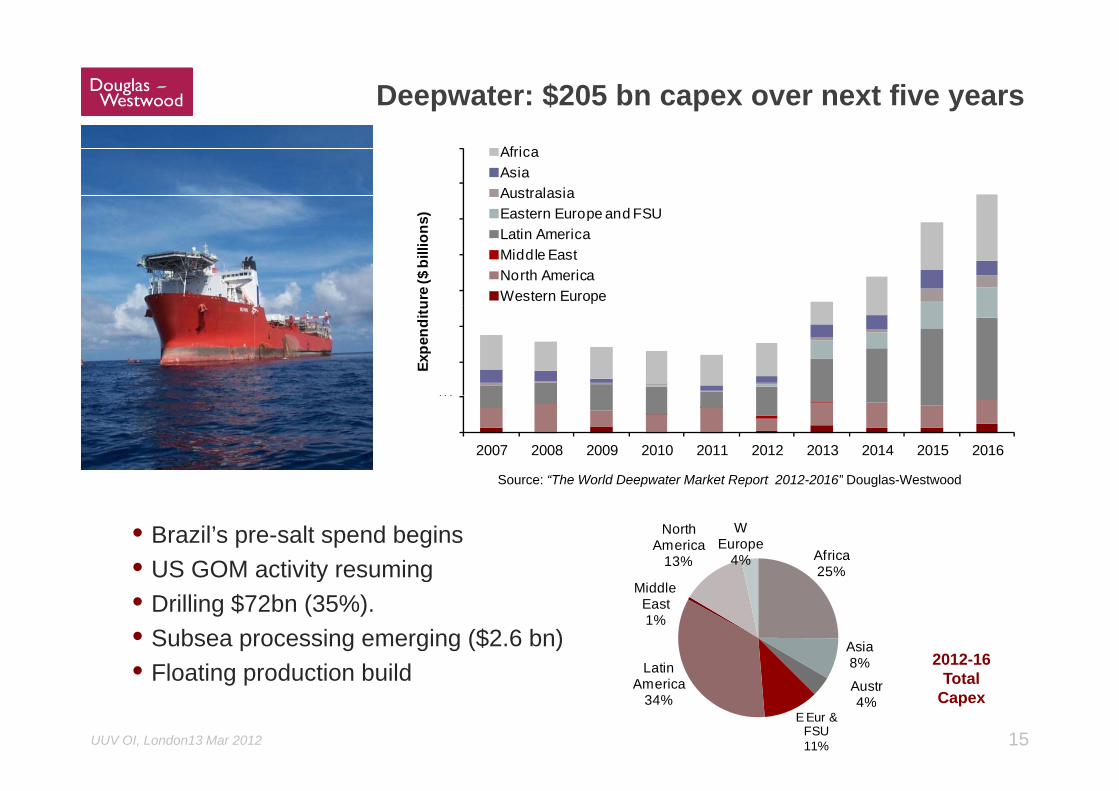

Deepwater: $205 bn capex over next five years

60

70

80

)

AfricaAsiaAustralasiaEastern Europe and FSU

40

50

60

ure

($ b

illio

ns

Eastern Europe and FSULatin AmericaMiddle EastNorth AmericaWestern Europe

10

20

30

Expe

nditu

Source: “The World Deepwater Market Report 2012-2016” Douglas-Westwood

0

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

p p g

Africa25%

North America

13%

W Europe

4%• Brazil’s pre-salt spend begins• US GOM activity resuming

2012-16

25%

Asia8%L ti

Middle East1%

US GOM activity resuming• Drilling $72bn (35%). • Subsea processing emerging ($2.6 bn)

Fl ti d ti b ild

15UUV OI, London13 Mar 2012

Total Capex

8%

Austr4%

E Eur & FSU11%

Latin America

34%

• Floating production build

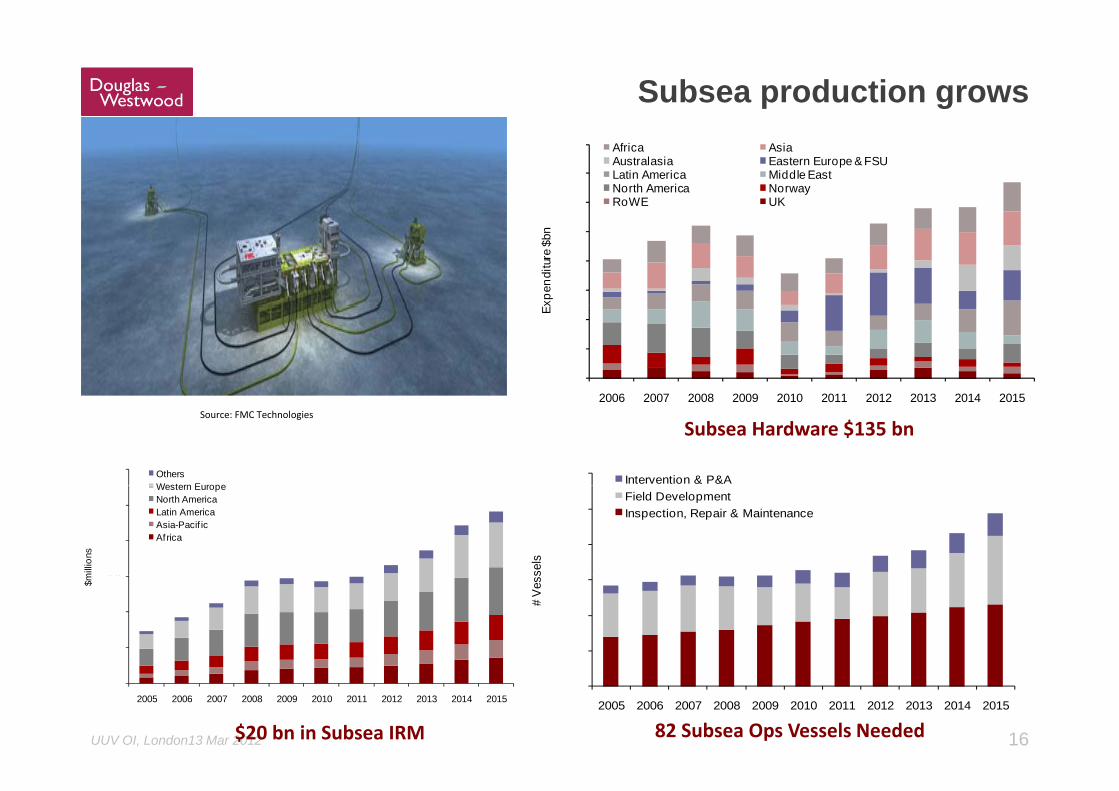

Subsea production grows

$30

$35

$40 Africa AsiaAustralasia Eastern Europe & FSULatin America Middle EastNorth America NorwayRoWE UK

$15

$20

$25

xpen

ditu

re $

bn

$0

$5

$10

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ex

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Source: FMC Technologies

Subsea Hardware $135 bn

300 Intervention & P&A6.0 Others

Western Europe

200

250

sels

Field DevelopmentInspection, Repair & Maintenance

3 0

4.0

5.0

mill

ions

Western EuropeNorth AmericaLatin AmericaAsia-Pacif icAfrica

50

100

150

# Ve

ss

1.0

2.0

3.0$m

16UUV OI, London13 Mar 2012

-2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

82 Subsea Ops Vessels Needed

0.02005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$20 bn in Subsea IRM

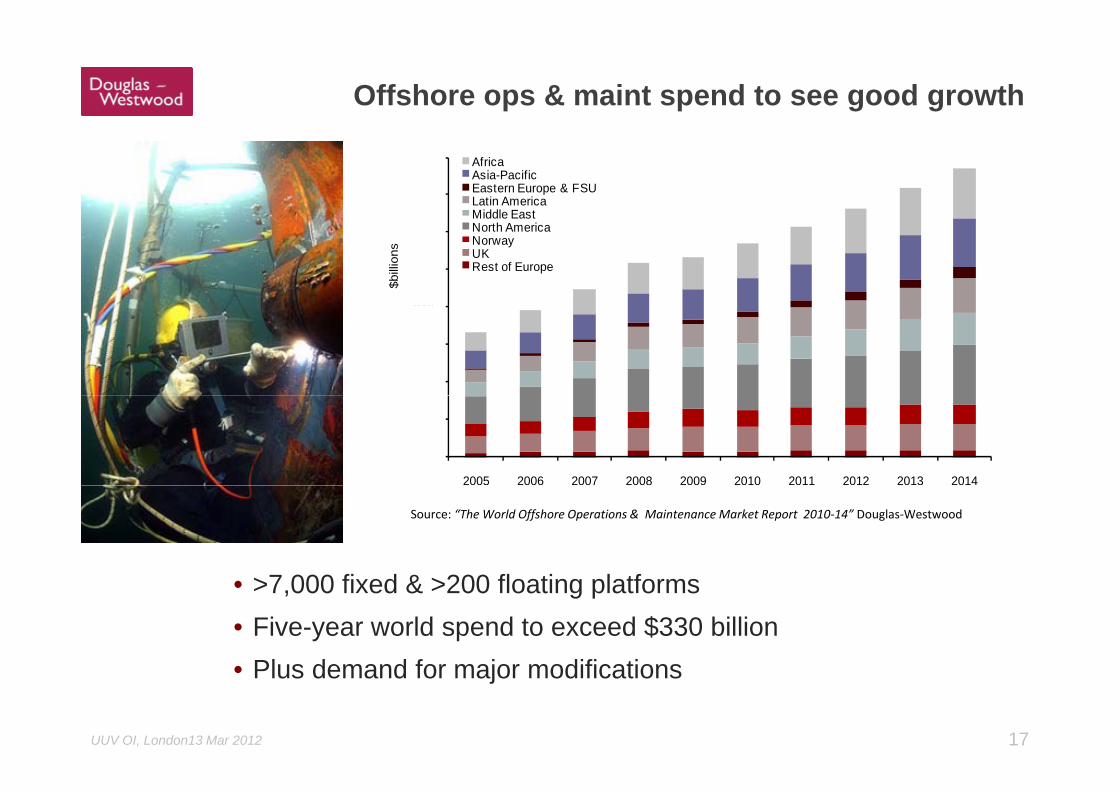

Offshore ops & maint spend to see good growth

$70

$80 AfricaAsia-PacificEastern Europe & FSULatin AmericaMiddle East

$40

$50

$60

$bill

ions

Middle EastNorth AmericaNorwayUKRest of Europe

$20

$30

$40

$0

$10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: “The World Offshore Operations & Maintenance Market Report 2010‐14” Douglas‐Westwood

7 000 fi d & 200 fl ti l tf• >7,000 fixed & >200 floating platforms• Five-year world spend to exceed $330 billion

Plus demand for major modifications

17UUV OI, London13 Mar 2012

• Plus demand for major modifications

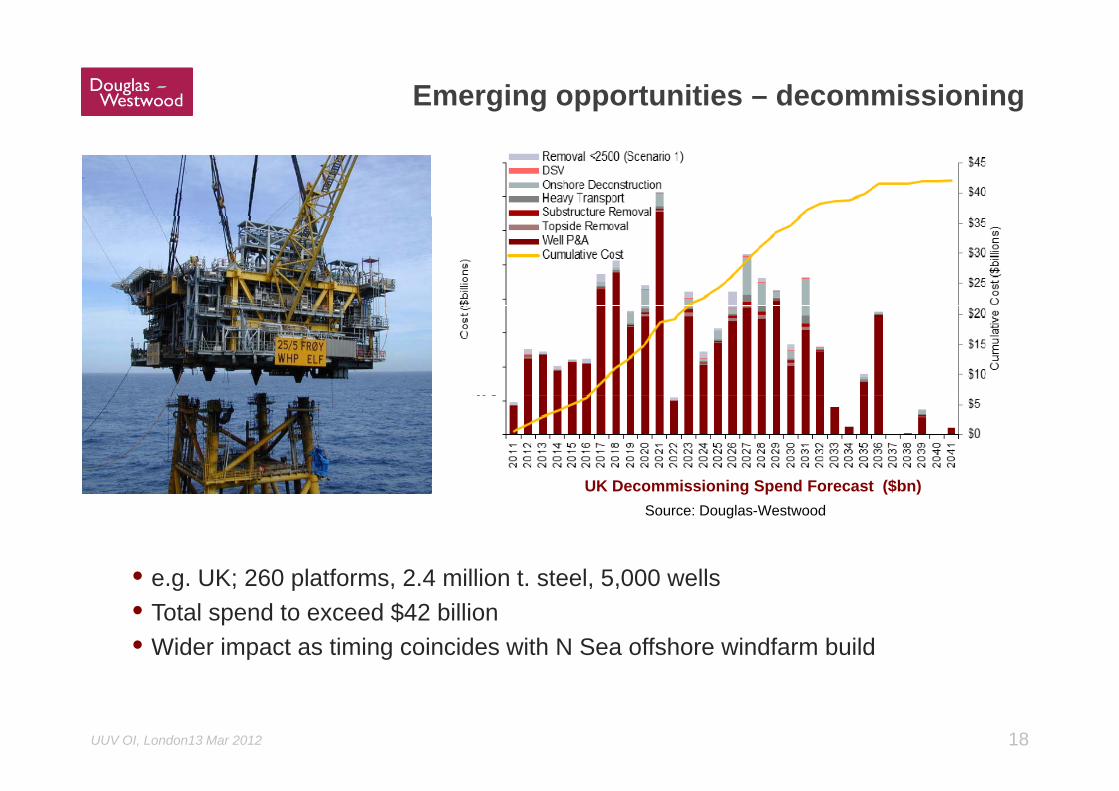

Emerging opportunities – decommissioning

UK Decommissioning Spend Forecast ($bn)

• e g UK; 260 platforms 2 4 million t steel 5 000 wells

Source: Douglas-WestwoodUK Decommissioning Spend Forecast ($bn)

• e.g. UK; 260 platforms, 2.4 million t. steel, 5,000 wells• Total spend to exceed $42 billion• Wider impact as timing coincides with N Sea offshore windfarm build

18UUV OI, London13 Mar 2012

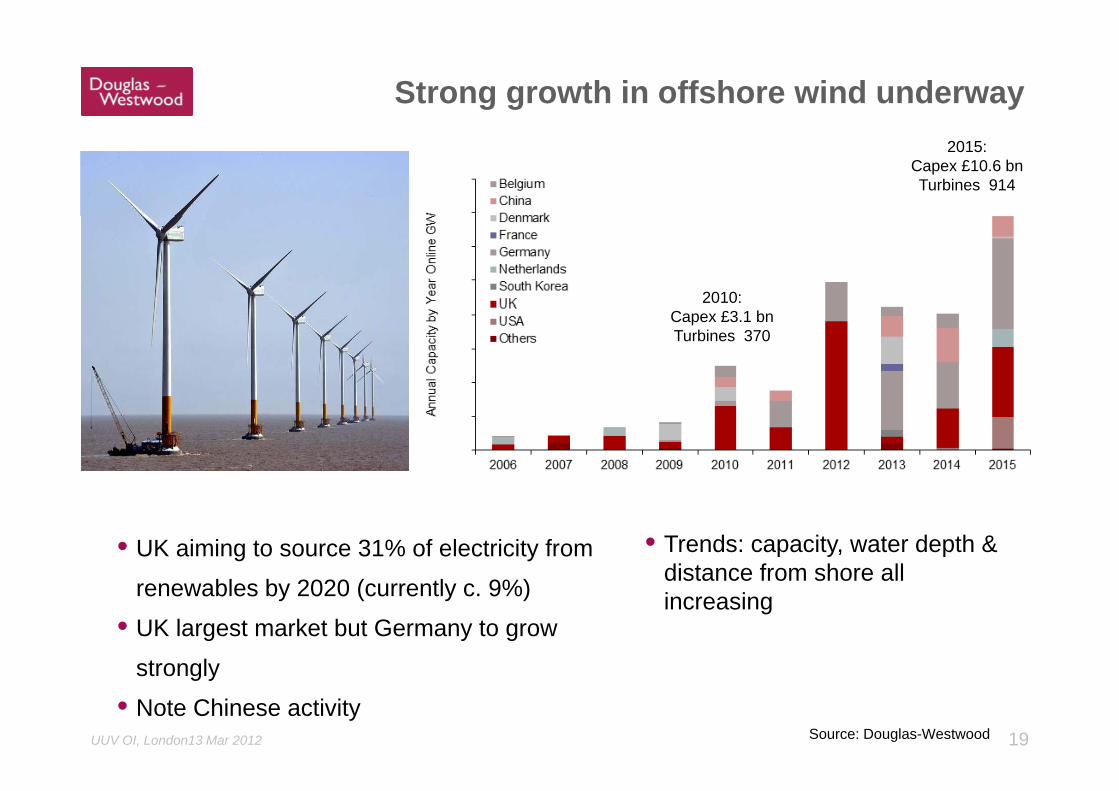

Strong growth in offshore wind underway2015:

Capex £10.6 bnTurbines 914

2010:Capex £3.1 bnTurbines 370

• UK aiming to source 31% of electricity from • Trends: capacity, water depth & distance from shore allrenewables by 2020 (currently c. 9%)

• UK largest market but Germany to grow

strongly

distance from shore all increasing

19UUV OI, London13 Mar 2012

strongly

• Note Chinese activity Source: Douglas-Westwood

Defence market drivers

• Defence industry faces budgetary cuts

• Literal zone operations

• Fleet reduction strategies promoting the use of multi-role platforms

• Integrated MCM systems, with a single command control interface

• Quieter submarine propulsion require new d t ti th d ldetection methodology

• Higher resolution sensors

• Widespread acceptance of unmanned technology

20UUV OI, London13 Mar 2012

Research sector drivers

• Catastrophic events: the Macondo oil spill and the Japanese Tsunami bringing new p g gfocus and funding into marine science

• Regional, national & international research ocean observation systems

• Large-scale, long-term global issues such as climate change

• Local, small-scale research activities

• Desire for increased density and frequency of observations

• Research needs in previously hard-to reach areas such as under-ice that can only be met by unmanned systems

21UUV OI, London13 Mar 2012

met by unmanned systems.

Cross-sector drivers

• Demanning to reduce costs & increase safetyg y

• Reducing the impact of high vessel costs

• Improving reliability of remote systems• Improving reliability of remote systems

• Advances in autonomous technology

• Increasing awareness & acceptance of unmanned systems

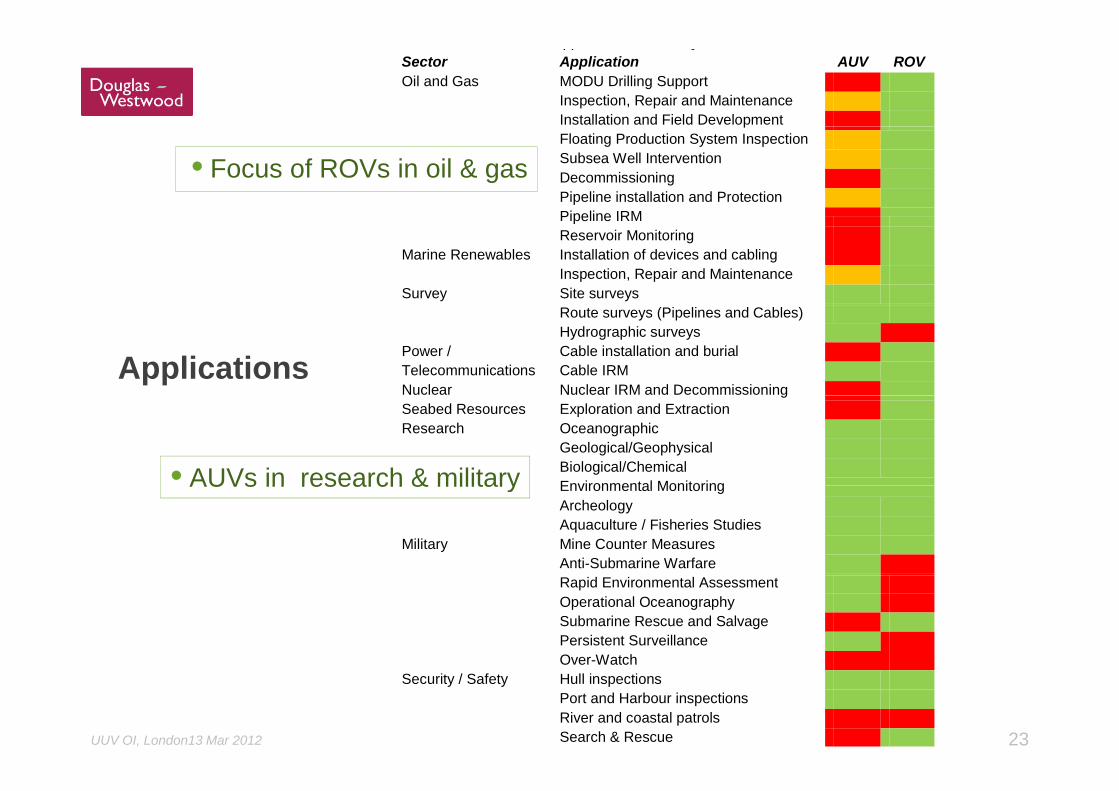

22UUV OI, London13 Mar 2012 SBS Bathymetry from SRDUK / Tritech

pp ySector Application AUV ROV Oil and Gas MODU Drilling Support

Inspection, Repair and Maintenance Installation and Field DevelopmentpFloating Production System Inspection Subsea Well Intervention Decommissioning Pipeline installation and Protection Pipeline IRM

• Focus of ROVs in oil & gasPipeline IRM Reservoir Monitoring

Marine Renewables Installation of devices and cabling Inspection, Repair and Maintenance

Survey Site surveys

Applications

Route surveys (Pipelines and Cables)Hydrographic surveys

Power / Telecommunications

Cable installation and burial Cable IRM

Nuclear Nuclear IRM and DecommissioninggSeabed Resources Exploration and Extraction Research Oceanographic

Geological/Geophysical Biological/Chemical Environmental Monitoring• AUVs in research & military Environmental MonitoringArcheology Aquaculture / Fisheries Studies

Military Mine Counter Measures Anti-Submarine Warfare

AUVs in research & military

Rapid Environmental AssessmentOperational Oceanography Submarine Rescue and Salvage Persistent Surveillance Over-Watch

23UUV OI, London13 Mar 2012

Security / Safety Hull inspections Port and Harbour inspections River and coastal patrols Search & Rescue

From man to machine

Market drivers

Work class ROVs

AUVs

C l iConclusions

24UUV OI, London13 Mar 2012

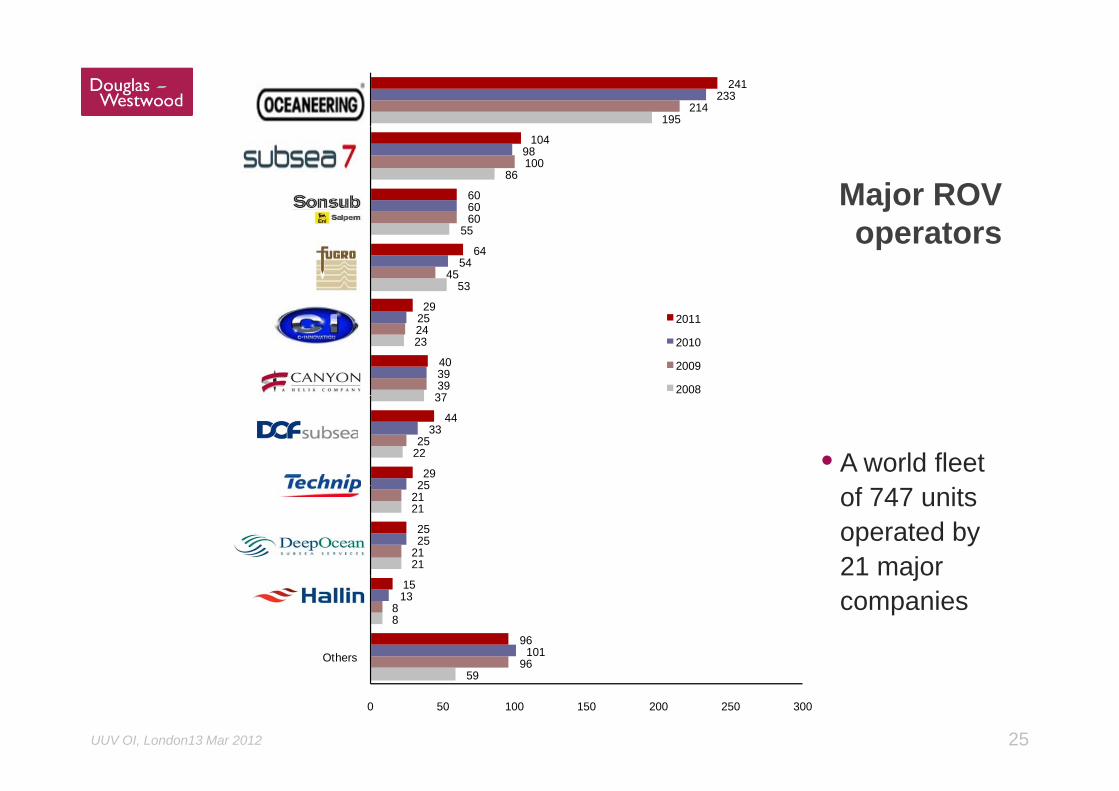

195214

233241

Oceaneering

Major ROV 86

60

100

60

98

60

104

Sonsub

Subsea 7 (inc. i-Tech)

operators53

55

45

60

54

29

64Fugro

Sonsub

37

23

39

24

39

25

40

29

Helix (Canyon)

C-Innovation 2011

2010

2009

2008

22

37

25

25

33

29

44DOF Subsea

• A world fleet

21

21

21

21

25

25

25Trico

Technip of 747 units operated by 21 major

8

96

8

101

13

96

15

Others

Hallin

21 major companies

25UUV OI, London13 Mar 2012

5996

0 50 100 150 200 250 300

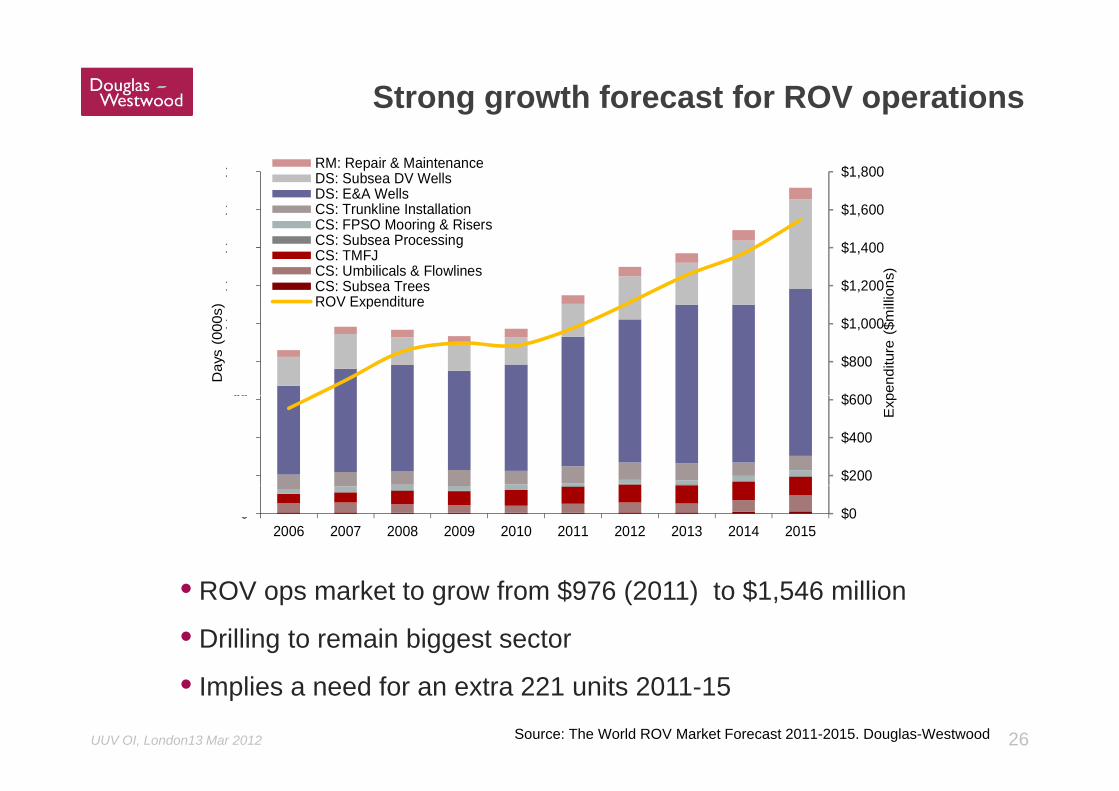

Strong growth forecast for ROV operations

$1,600

$1,800

160

180 RM: Repair & MaintenanceDS: Subsea DV WellsDS: E&A WellsCS: Trunkline Installation

$1,200

$1,400

,

120

140

llion

s)

)CS: FPSO Mooring & RisersCS: Subsea ProcessingCS: TMFJCS: Umbilicals & FlowlinesCS: Subsea TreesROV Expenditure

$600

$800

$1,000

60

80

100

pend

iture

($m

i

Day

s (0

00s ) ROV Expenditure

$200

$400

$600

20

40

60

Exp

$002006 2007 2008 2009 2010 2011 2012 2013 2014 2015

• ROV ops market to grow from $976 (2011) to $1,546 million

• Drilling to remain biggest sector

26UUV OI, London13 Mar 2012

• Implies a need for an extra 221 units 2011-15 Source: The World ROV Market Forecast 2011-2015. Douglas-Westwood

From man to machine

Market drivers

Work class ROVs

AUVs

C l iConclusions

27UUV OI, London13 Mar 2012

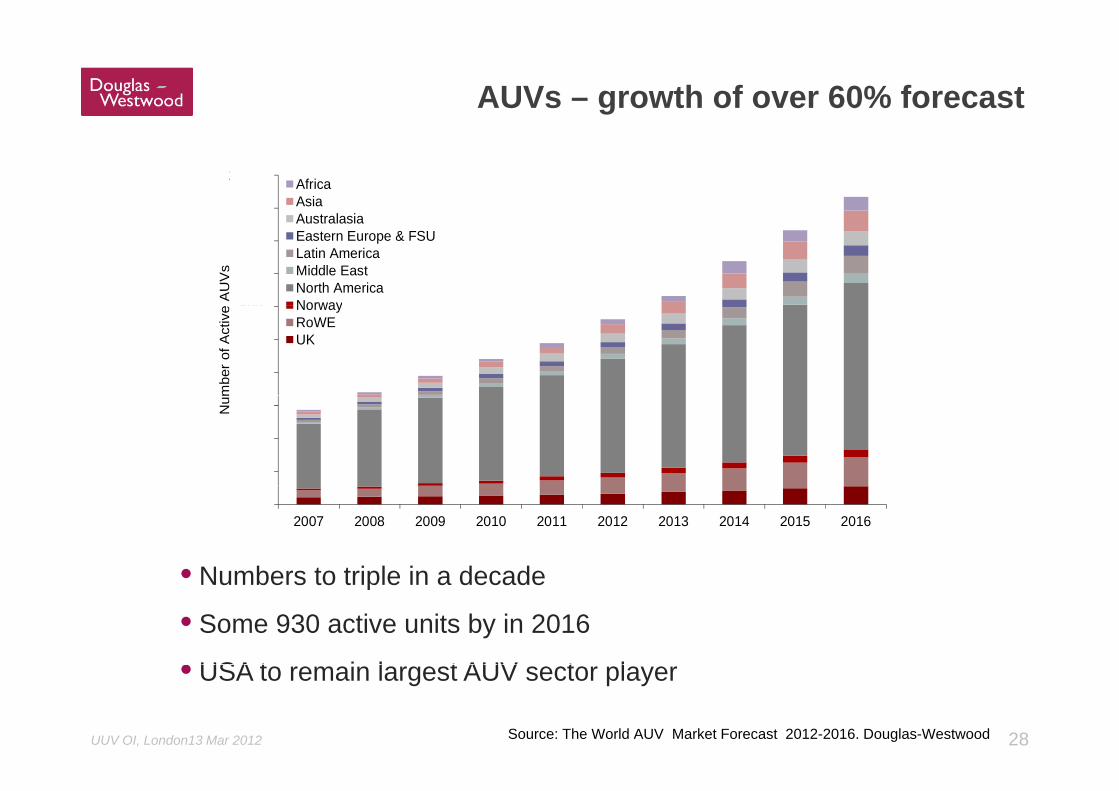

AUVs – growth of over 60% forecast

900

1,000 AfricaAsiaAustralasia

600

700

800 A

UV

sAustralasiaEastern Europe & FSULatin AmericaMiddle EastNorth AmericaNorway

400

500

600

mbe

r of A

ctiv

e NorwayRoWEUK

100

200

300Num

• Numbers to triple in a decade

02007 2008 2009 2010 2011 2012 2013 2014 2015 2016

• Numbers to triple in a decade

• Some 930 active units by in 2016

• USA t i l t AUV t l

28UUV OI, London13 Mar 2012

• USA to remain largest AUV sector player

Source: The World AUV Market Forecast 2012-2016. Douglas-Westwood

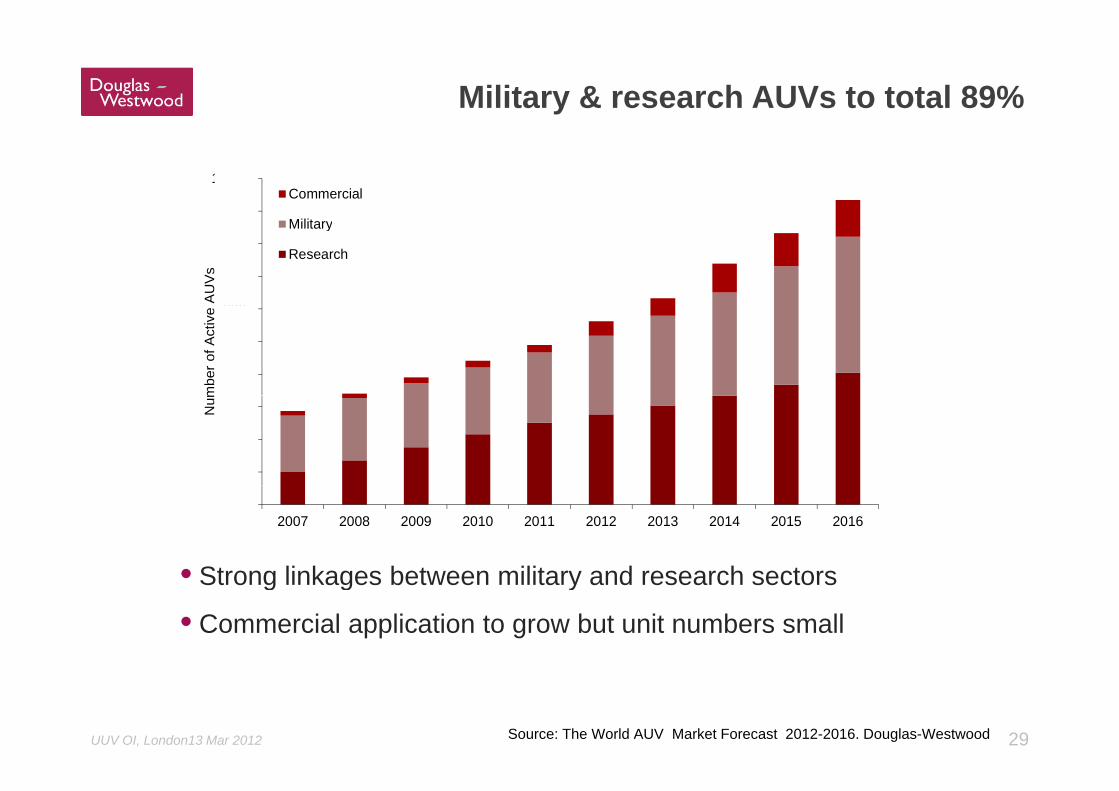

Military & research AUVs to total 89%

900

1,000Commercial

600

700

800

AU

Vs

Military

Research

400

500

600

mbe

r of A

ctiv

e

100

200

300Num

• Strong linkages between military and research sectors

02007 2008 2009 2010 2011 2012 2013 2014 2015 2016

• Strong linkages between military and research sectors

• Commercial application to grow but unit numbers small

29UUV OI, London13 Mar 2012 Source: The World AUV Market Forecast 2012-2016. Douglas-Westwood

From man to machine

Market drivers

Work class ROVs

AUVs

C l iConclusions

30UUV OI, London13 Mar 2012

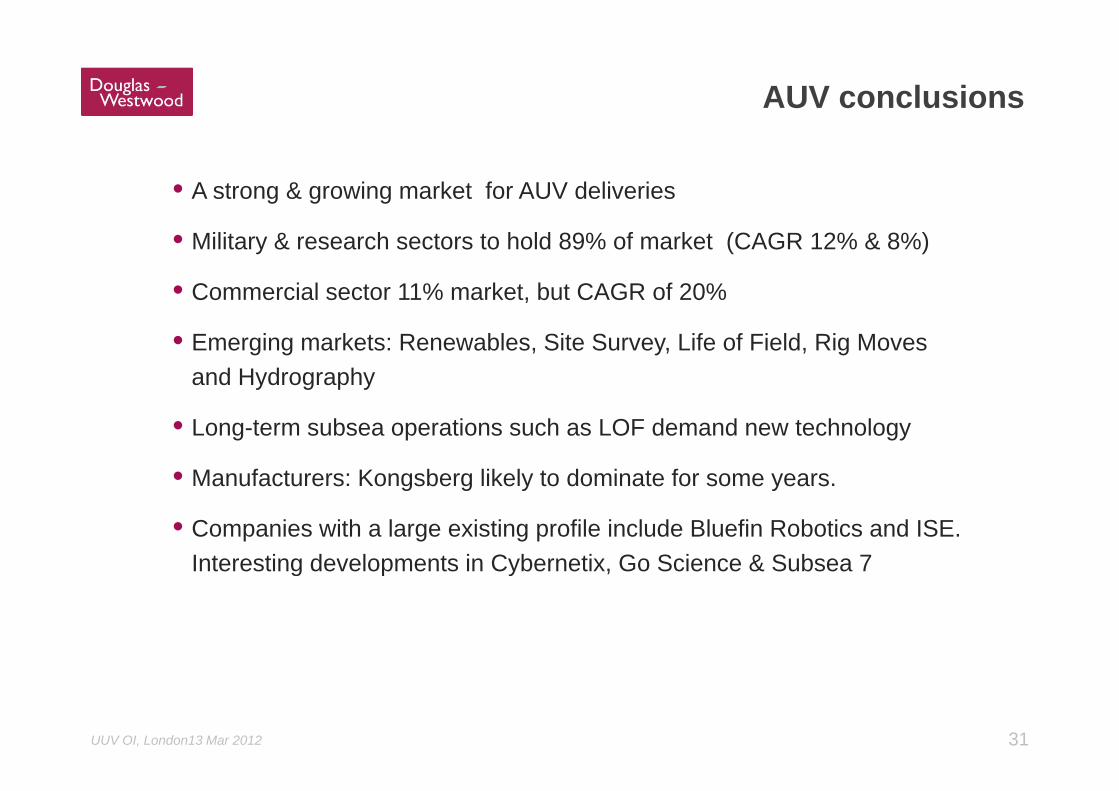

AUV conclusions

• A strong & growing market for AUV deliveries

• Military & research sectors to hold 89% of market (CAGR 12% & 8%)

• Commercial sector 11% market, but CAGR of 20%

• Emerging markets: Renewables, Site Survey, Life of Field, Rig Moves and Hydrography

• Long-term subsea operations such as LOF demand new technology

• Manufacturers: Kongsberg likely to dominate for some years.Manufacturers: Kongsberg likely to dominate for some years.

• Companies with a large existing profile include Bluefin Robotics and ISE. Interesting developments in Cybernetix, Go Science & Subsea 7g p y

31UUV OI, London13 Mar 2012

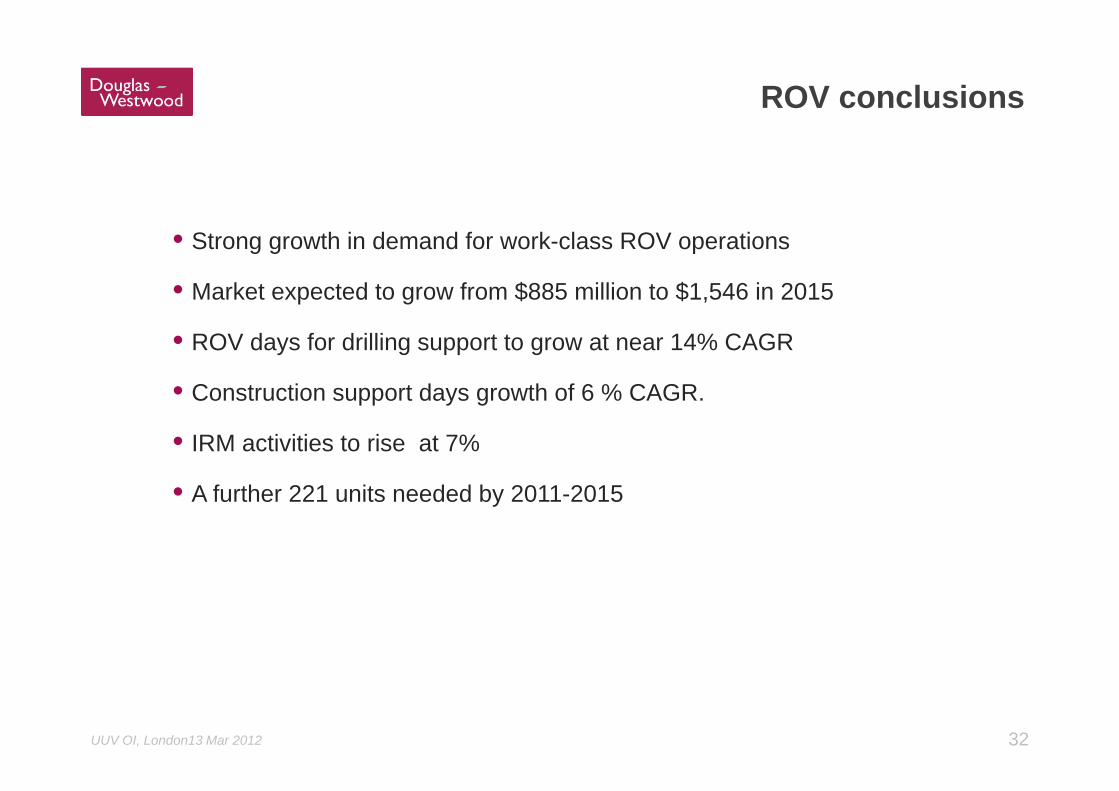

ROV conclusions

• Strong growth in demand for work-class ROV operations

• Market expected to grow from $885 million to $1,546 in 2015

• ROV days for drilling support to grow at near 14% CAGR

• Construction support days growth of 6 % CAGRConstruction support days growth of 6 % CAGR.

• IRM activities to rise at 7%

A f th 221 it d d b 2011 2015• A further 221 units needed by 2011-2015

32UUV OI, London13 Mar 2012