automated trading: fueling global fx market growth · pdf fileautomated trading in fx is not...

TRANSCRIPT

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

Automated Trading: Fueling Global FX

Market Growth

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

2

TABLE OF CONTENTS EXECUTIVE SUMMARY .................................................................................................................................... 3

INTRODUCTION .............................................................................................................................................. 5

MARKET TRENDS ............................................................................................................................................ 6

GLOBAL FX MARKET GROWTH .................................................................................................................. 6

DIVERSIFICATION OF MARKET PARTICIPANTS .......................................................................................... 6

MARKET FRAGMENTATION....................................................................................................................... 7

INCREASED ADOPTION IN ELECTRONIC TRADING .................................................................................... 8

INCREASED ADOPTION IN AUTOMATED TRADING ................................................................................... 9

INCREASED INTERNALIZATION BY SINGLE BANK PLATFORMS ................................................................ 10

NEW OPPORTUNITIES AND CHALLENGES ..................................................................................................... 11

OPPORTUNITIES IN PRICE AGGREGATION .............................................................................................. 11

CHALLENGES IN MANAGING MULTIPLE TRADING VENUES .................................................................... 11

CHANGING RELATIONSHIP BETWEEN BANKS AND AUTOMATED TRADING FIRMS ................................ 12

DECLINING SHELF-LIFE OF TRADING STRATEGIES ................................................................................... 12

KEY INGREDIENTS IN AUTOMATED TRADING ............................................................................................... 14

UNDERSTANDING THE STRATEGY DEVELOPMENT WORKFLOW ............................................................ 14

CHALLENGES IN FX FOR AUTOMATED TRADING .................................................................................... 15

AUTOMATED FX TRADING INFRASTRUCTURE ........................................................................................ 16

CASE STUDY .................................................................................................................................................. 19

CONCLUSION ................................................................................................................................................ 20

ABOUT QUANTHOUSE: ................................................................................................................................. 21

QUANTFACTORY – AUTOMATED TRADING PLATFORM ......................................................................... 21

DATACENTER SERVER ........................................................................................................................ 22

DEVELOPMENT PLATFORM ............................................................................................................... 22

EXECUTION PLATFORM ..................................................................................................................... 23

QUANTFEED – ULTRA LOW LATENCY MARKET DATA ............................................................................. 21

QUANTLINK – ULTRA LOW LATENCY TRADING INFRASTRUCTURE ......................................................... 24

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

3

EXECUTIVE SUMMARY

Automated Trading: Fueling Global FX Market Growth commissioned by QuantHouse and

produced by Aite Group, analyzes the rapidly evolving automated trading in the global FX

market. The study examines the background behind the overall growth of automated trading in

FX and highlights key technology components that are needed build an effective presence in the

marketplace. The study concludes with a case study.

Key takeaways from the study include the following:

• During the latter part of 2008 and well into 2009, customers faced a much different

market from previous years, marked by wider spreads and declining liquidity.

Consequently, average daily trade volume returned to earth in 2009, standing at

approximately US$3.7 trillion. However, the global FX market bounced back quite

nicely with a strong volume growth in 2010, reaching US$4.1 trillion.

• One of the most significant changes that the FX market is currently undergoing is the

substantial increase in trading activities from non-bank financial institutions. In

1995, banks accounted for 64% of all trading, but that figure declined to below 40%

by 2010. During the same time period, trading from non-bank financial institutions

increased to 48% from 20% in 1995, thereby becoming the largest counterparty in

the FX market.

• Electronic trading adoption continues to increase in the global FX market. Given that

markets remain fragmented, the need to source multiple liquidity pools

simultaneously has only strengthened the overall position of electronic trading. At

the end of 2010, electronic trading accounted for 68% of all FX trading.

• In recent years, a new breed of actively trading market participants has driven

significant innovation in trading technology. As traders navigate through growing

complexity within the marketplace, development and implementation of automated

trading strategies have become vital part of some of the more sophisticated FX

traders.

• Automated trading in FX is poised to grow quite rapidly over the next few years, as

the first-generation automated trading firms are joined by an influx of next-

generation equity and futures automated trading firms looking to capture

uncorrelated alpha in FX. At the end of 2010, automated trading accounted for 29%

of overall trade volume. This figure is expected to hit more than 40% by the end of

2012

• Challenges in automated FX trading include 1) latency; 2) decentralized, highly

fragmented across numerous single bank and ECN execution venues; 3) largely

unregulated market with lack of an industry benchmark and best execution

obligation; 4) venue-specific market structure and communication standards; 5) lack

of a comprehensive, consolidated view into the entire market; and 6) dispersed price

discovery process.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

4

• Despite existing challenges, firms have been implementing automated FX trading for

many years and developing and maintaining a robust automated FX trading

infrastructure has been vital to their continuing success. Key components of

automated FX trading infrastructure include the following:

• Access to real-time and historical data

• Robust strategy development framework

• Trading engine

• Low latency connectivity

• Trade analytics

Automated trading in FX is not driven entirely by independent low latency proprietary shops or

hedge funds. In fact, most of the global FX banks have either acquired or developed robust low

latency FX prop desks to compete in the marketplace and account for a significant percentage of

the overall market share.

In recent months, several traders from major banks have left to start their own firms, taking with

them not only their quantitative skills, but also their market structure knowledge, which could

potentially pave the way for the next phase in automated trading, in which non-bank trading

firms play a larger role in liquidity provision. The first round may be over in FX automated

trading, but many more remain before the real winners can be determined in this rapidly

evolving marketplace.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

5

INTRODUCTION

After robust market growth in 2007 and 2008, the global FX market experienced lower volatility,

lower volume, and in most cases, wider spreads in 2009. The global FX market fared much better

in 2010, resuming its overall growth and seeing volume levels skyrocket, returning to close to its

record 2008 level.

In the meantime, large FX banks have pressed on, maintaining the global FX market’s overall

market dominance, increasingly relying on internalization to manage their P&L. The global FX

market remains highly fragmented with single bank, multi-bank, and interbank execution venues

vying for precious market share. On the exchange-traded market, the CME Group has developed

a formidable FX futures franchise that currently has a virtual monopoly.

With the client-to-dealer market outpacing the growth of inter-dealer market in terms of overall

trading volume, much focus has been placed on the dynamic changes within the different client

segments. In recent years, a new breed of actively trading market participants has driven

significant innovation in trading technology. As traders navigate through growing complexity

within the marketplace, development and implementation of automated trading strategies have

become vital part of some of the more sophisticated FX traders.

Another important thing to note is that automated trading in FX is not driven entirely by

independent low latency proprietary shops or hedge funds. In fact, most of the global FX banks

have either acquired or developed robust low latency FX prop desks to compete in the

marketplace and account for a significant percentage of the overall market share.

Under this competitive environment, this study analyzes the rapidly evolving automated trading

in the global FX market. The study examines the background behind the overall growth of

automated trading in FX and highlights key technology components that are needed build an

effective presence in the marketplace.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

6

MARKET TRENDS

G LOBAL FX MARKET GROWTH

Thanks in large part to high volatility, 2008 yielded historical highs in terms of overall trading

volume, followed by an inevitable decline in 2009. The industry averaged approximately US$4.3

trillion in daily trading volume in 2008 compared to about US$4 trillion in 2007. During the latter

part of 2008 and well into 2009, customers faced a much different market from previous years,

marked by wider spreads and declining liquidity. Consequently, average daily trade volume

returned to earth in 2009, standing at approximately US$3.7 trillion. However, the global FX

market bounced back quite nicely with a strong volume growth in 2010, reaching US$4.1 trillion

(Figure 1).

Figure 1: Growth of Global FX Market

Source: BIS, Bank of England Foreign Exchange Joint Standing Committee (JSC),New York Foreign Exchange Committee, Singapore

Foreign Exchange Market Committee, Canadian Foreign Exchange Committee, Tokyo Foreign Exchange Joint Standing Committee,

and Aite Group

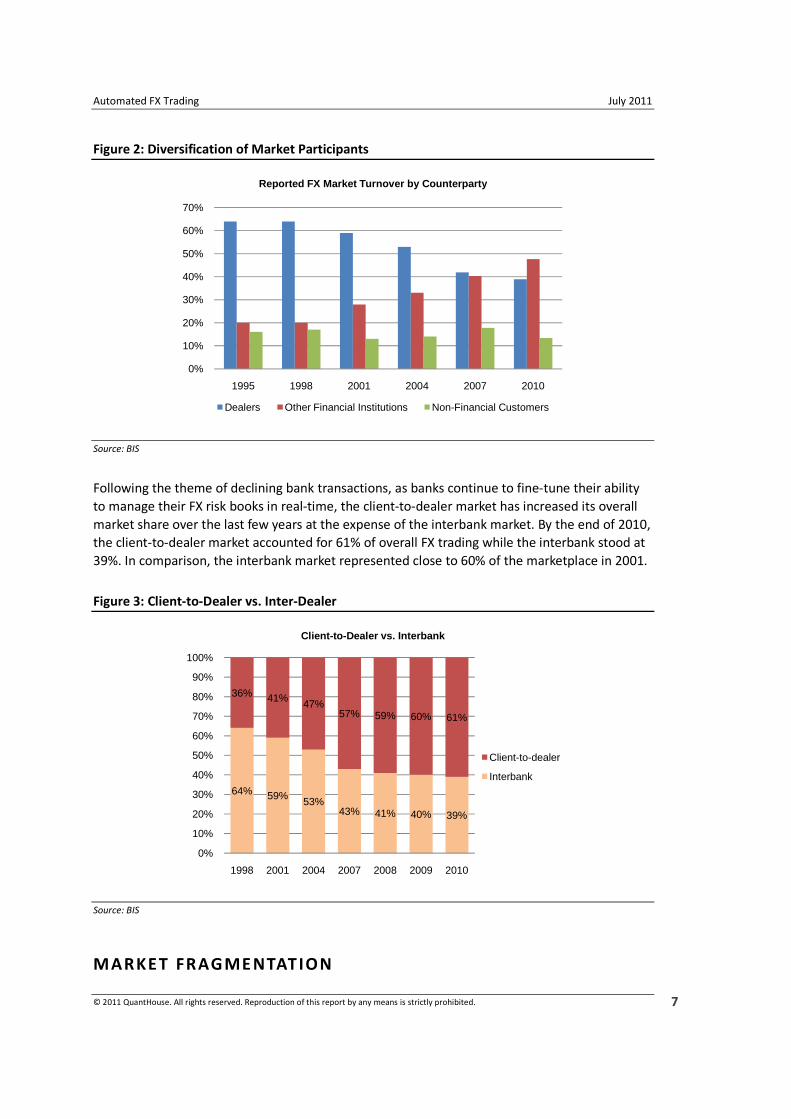

D IVE RS IF ICATION OF MARKET PARTIC IPAN TS

One of the most significant changes that the FX market is currently undergoing is the substantial

increase in trading activities from non-bank financial institutions (i.e., other financial institutions

in Figure 2). In 1995, banks accounted for 64% of all trading, but that figure declined to below

40% by 2010. During the same time period, trading from non-bank financial institutions

increased to 48% from 20% in 1995, thereby becoming the largest counterparty in the FX

market.

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

1998 2001 2004 2007 2008 2009 2010

Average Daily Trade Volume(In US$ Billions)

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

7

Figure 2: Diversification of Market Participants

Source: BIS

Following the theme of declining bank transactions, as banks continue to fine-tune their ability

to manage their FX risk books in real-time, the client-to-dealer market has increased its overall

market share over the last few years at the expense of the interbank market. By the end of 2010,

the client-to-dealer market accounted for 61% of overall FX trading while the interbank stood at

39%. In comparison, the interbank market represented close to 60% of the marketplace in 2001.

Figure 3: Client-to-Dealer vs. Inter-Dealer

Source: BIS

MARKET FRAGME NTATION

0%

10%

20%

30%

40%

50%

60%

70%

1995 1998 2001 2004 2007 2010

Reported FX Market Turnover by Counterparty

Dealers Other Financial Institutions Non-Financial Customers

64% 59% 53%43% 41% 40% 39%

36% 41% 47%57% 59% 60% 61%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1998 2001 2004 2007 2008 2009 2010

Client-to-Dealer vs. Interbank

Client-to-dealer

Interbank

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

8

The global FX market remains highly fragmented, represented by the still significant voice

market, as well as numerous electronic venues, including single bank, multi-bank, and interbank

venues. In recent years, the term FX ECNs has emerged to describe mixture of multi-bank and

interbank venues that support ECN-like functionality, including streaming live quotes.

Examining the FX ECN market alone, EBS currently holds the top spot with 23% market share

followed very closely in second place by Thomson Reuters. While the CME Group is an exchange

with its FX futures product compared to the OTC products of the other FX ECNs, it is clear from a

trading value perspective that the CME Group has become a major player in the global FX market

(Figure 4).

Figure 4: Market Fragmentation in FX ECN Market

Source: ECNs, Aite Group

INCREASED ADOPTION IN ELECTRONIC TRADING

Unlike other over-the-counter (OTC) markets, driven by early acceptance in the interbank

market, electronic trading adoption continues to increase in the global FX market. Given that

markets remain fragmented, the need to source multiple liquidity pools simultaneously has only

strengthened the overall position of electronic trading. At the end of 2010, electronic trading

accounted for 68% of all FX trading. This figure is expected to reach more than 70% by end of

2012 (Figure 5).

ICAP (EBS)20%

Thomson Reuters

19%

CME Group17%

Currenex14%

FX Connect13%

Fxall10%

Hotspot FX7%

FX Venues Competitive Landscape(As of January 2011)

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

9

Figure 5: Projected Electronic Trading in FX

Source: Aite Group

INCREASED ADOPTION IN AUTOMATED TRAD ING

Automated trading in FX is poised to grow quite rapidly over the next few years, as the first-

generation automated trading firms are joined by an influx of next-generation equity and futures

automated trading firms looking to capture uncorrelated alpha in FX. In addition, new

automated trading firms have emerged in recent months, formed by FX quants and traders who

have left large banks looking to capture new opportunities on the other side of the market. At

the end of 2010, automated trading accounted for 29% of overall trade volume. This figure is

expected to hit more than 40% by the end of 2012 (Figure 6).

0%

10%

20%

30%

40%

50%

60%

70%

80%

Projected Electronic Trading in FX

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

10

Figure 6: Projected Adoption of Automated Trading in FX

Source: Aite Group

INCREASED INTER NALIZATION BY S INGLE BANK P LAT FORMS

Another key trend over the last few years has been the increasing effectiveness of large FX banks

in managing their risk books when trading against customers. By utilizing sophisticated pricing

engine and real-time internalization capabilities, large FX banks have become quite adept at

showing varying prices to different types of customer segments as well as efficient at deciding

when to internalize vs. utilize traditional interbank markets to lay off their risk. In a way, the

aftermath of the credit crisis of 2008 has only reinforced banks’ need to internalize, particularly

as regulators and politicians continue to emphasize banks’ need to lower their overall risk

profile. Consequently, the need to better segment customer flow has been on top of banks’

overall client-facing trading strategy so that they can optimize their balance sheets and better

manage their profit and loss (P&L).

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2003 2004 2005 2006 2007 2008 2009 2010 e2011 e2012

Estimated Automated Trading in FX

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

11

NEW OPPORTUNITIES AND CHALLENGES

Against these diverse market realities, plenty of opportunities currently exist for those firms

looking to capture alpha in the global FX market. At the same time, however, obvious challenges

exist, driven by the OTC nature of the FX market.

OPPORTUNIT IES IN PRICE AGGREGATION

From a technology perspective, clear opportunities currently exist in the FX market in terms of

providing effective price aggregation services to overcome the challenges that stems from

market fragmentation and lack of industry-wide consolidated tape. Price aggregation is a difficult

proposition in the FX market due to the differences that exist across multiple venues and how

they operate. While the larger FX players have developed price aggregation capabilities

internally, recent efforts made by third-party vendors hold hope for those smaller players looking

for a level playing field. From strategy development to actual execution, getting the price

aggregation piece right is the first important steps towards developing a winning automated

trading operations.

CH AL LENGES IN MANAGING MULTIPLE TRADING VE NUES

Not so long ago, the traditional FX venues, such as EBS and Reuters dominated the market,

making it less cumbersome for traders to figure out where the market is headed. However, the

recent trend of growing market presence of newer ECNs as well as single bank platforms,

coinciding with declining market share of EBS and Reuters have made it essential that firms

attempt to source liquidity from various venues. A few of the challenges arising from multiple

trading venues include the following:

• Different locations and built-in distance latency: FX execution venues are located in

many different regional and financial centers, resulting in inherent distance latency

for most firms.

• Different frequency of price distribution: Each venue has its own timeframes in

terms of price distribution. In cases of single bank platforms, they will be distributing

prices to many different FX ECNs, in addition to their own in different latency.

• Depth of book: Wide differences exist in terms how much of the order book is

actually represented in each venue.

• Tick size and order types: FX venues also support different tick sizes and order

types, adding another layer complexity in terms of firms trying to figure out the best

location for execution at any given time.

• Constant upgrades: Venues are constantly going through enhancements of new

functionality, order types, reduction in latency and more. These changes could have

an impact on effectiveness of strategies so firms need to stay on top of these

changes and tweak strategies as needed.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

12

CH ANGING RELATIO NSHIP BETWEE N BANKS AND AUTOMATE D TRAD ING FIRMS

While the banks have gone through a series of consolidations, leading to fewer banks making

markets, the FX market continues to evolve with new types of customer segments beyond the

traditional corporate and asset manager customer base. Since 2002, actively trading hedge funds

and proprietary trading firms have made a huge impact in the FX market, driven by a robust IT

infrastructure and development of automated trading strategies.

In fact, some would argue that the large FX banks learned a painful lesson between 2002 and

2006, driven by latency arbitrage strategies in the first wave of automated trading firms. As a

direct consequence of this experience, the banks initiated massive overhaul of their trading

infrastructure, not only focusing on drastically lowering latency levels within the single bank

platforms, but also on developing more efficient pricing engine and internalization capabilities to

better manage their risk books against different types of customer segments. It was also during

this time that the banks decided to kick out those automated trading firms whose relationships

they deemed unprofitable.

Since 2008, however, banks and certain segments of the automated trading community are

attempting to peacefully co-exist. As banks continue to increase their internalization efforts,

potential liquidity from automated trading firms has become more attractive. On the other

hand, automated trading firms have come to realize that banks have a vital position in the FX

market; in order to ensure continued success, co-opetition has become a competitive necessity.

One potential change that could change the balance in the market is successful implementations

of centralized clearing in the OTC marketplace. If non-bank automated trading firms can become

direct clearing members for OTC products, and also illustrate their commitment to taking more

risk as a legitimate liquidity provider, banks’ stranglehold in the FX market could be weakened

and hence open up a new phase of intense competition.

DECLINING SHE LF- L IFE OF TRAD ING STRATEGIES

While there are long-term quant strategies that have generated great returns, there is a growing

group of high-frequency trading shops relying on implementation of short-term alpha discovery

strategies. This requires constant monitoring of the strategies, and the ability to isolate

ineffective variables or assumptions rapidly so that the strategy can be fine-tuned and launched

live into the market again.

With a notable increase in the total number of quantitatively-driven funds, the pressure to come

up with the next big quant model has grown exponentially. This reality has also fueled the need

to streamline the overall workflow process and shorten the duration of the entire investment

selection life cycle to compete more effectively. On average, the entire process of idea

generation to implementation can take anywhere from 10 to 28 weeks. Given the fact that

certain short-term strategies only remain effective for three to four months, rapid construction

and implementation of alpha models become that much more urgent. As a result, the search for

a single unifying platform that can create a more centralized and streamlined process and

functionality appears inevitable.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

13

And as the shelf life of alpha strategies continues to decrease driven by competition and

changing market conditions, there is growing recognition that the links between alpha discovery

and execution cannot be ignored.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

14

KEY INGREDIENTS IN AUTOMATED TRADING

UNDERSTANDING THE STRATEGY DEVELOPMENT WORKFLOW

There is no industry standard when it comes to strategy analysis workflow. Depending on the

firm — and also depending very much on whether or not they have long-term or short-term

trading philosophies — specific steps within the workflow and their duration will vary.

Figure 7: Alpha Generation Workflow

Source: Aite Group

A high-level, generally accepted alpha discovery workflow goes as follows:

• Alpha thesis/philosophy: The initial starting point for most firms is the basic thesis

or philosophy of alpha discovery. During this abstract phase, analysts and managers

are contemplating basic questions like instrument alternatives, value versus growth,

domestic versus international and other items such as decisioning variables. All

funds are built around a specific alpha philosophy.

• Data acquisition and preparation: Perhaps the most time-consuming and tedious

part of the entire workflow, in order to accommodate testing and analysis of a given

model, appropriate data must be acquired, typically transformed and normalized,

and then stored and ready to be mined and manipulated. Depending on the type of

firm, types of data would include fundamental and technical data as well as

historical and real-time tick data. In addition, firms have used a wide variety of data

storage options (including Excel, proprietary programs, relational databases, and

high performance databases) depending on the type of data, size of data sets, and

acceptable level of latency in testing and analysis.

• Alpha discovery: Once the data has been loaded properly, quants will mine the data

sets to identify patterns, events, and market conditions that may lead to alpha

discovery. During this phase, the quants will also either acquire or code various

mathematical, statistical, and technical functions and routines to be used to

formulate their alpha models. Typically using C, C++, C#, Java or other languages,

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

15

quants will create specific parameters for the models. Most quants use popular

third-party statistical packages (i.e., MATLAB, S+, and R) during this process; often

the same package they have used during their academic training.

• Back-testing: Using relevant sets of historical data, quants will back-test alpha

models through varied market and economic conditions, multiple combinations of

parameters, different portfolio attributes and more to validate or debunk the various

alpha models.

• Analysis and optimization: The results from back-testing are analyzed, and new

factors are added and/or additional coding takes place to fine-tune and optimize the

alpha model. Use of visualization and various portfolio optimization tools would be

used during this phase to ensure appropriate risk parameters and diversifications.

• Simulations: Once the alpha model has been tightened up, intensive simulation

takes place using either historical or live data under varying known and hypothetical

market conditions. These simulations determine the appropriate levels of risk and

investment parameters to ensure effectiveness and profitability of given alpha

models.

• Production and live launch: Once the alpha model has been validated, it will be

coded into production, after which integration work takes place to create an

automated investment environment. In order to ensure automated trading, the

model also needs to communicate with execution management systems (EMS)

typically via FIX.

The entire workflow in quantitative modeling is an iterative process, a system of continuous fine-

tuning. The quant manager tests the investment model for validation in light of ever-changing

market conditions.

CH ALLENGES IN FX FOR AUTOMATED TRAD ING

While there is certainly a growing market demand for low latency trading infrastructure within

the FX market, the FX market is relatively slow compared to the U.S. cash equities market (where

the accepted level of latency has fallen below hundreds of microseconds), typically operating in

the hundreds-of-milliseconds range. Still, continuing efforts to eliminate precious milliseconds

off matching engines and trading infrastructure have led to most firms being able to develop

internal trading latency levels of single-digit milliseconds.

Unfortunately, the globally distributed nature of the FX market with three major FX centers —

New York, London, and Tokyo — has made it tough to alleviate latency caused by physical

distance. As a result, depending on the location of the trader and the matching engine, latency

levels can vary widely from less than 15 milliseconds (i.e., local transaction) to close to 300

milliseconds (cross-border transactions).

In the short-term, basic latency issue is faced by all market participants. As a result, most firms

have focused on addressing the three major technology areas to address the latency issue:

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

16

• Network optimization;

• Low latency connectivity; and

• Colocation/proximity solution.

In addition to the obvious latency struggles, traders in the global FX market face more pressing

issues, driven largely by the fact that the FX market is still an OTC marketplace. Consequently,

firms engaged in automated FX trading must overcome the following barriers to ensure that

their trading needs are met:

• Decentralized, highly fragmented across numerous single bank and ECN execution

venues;

• Unregulated for the most part, with lack of an industry benchmark and best

execution obligation;

• Venue-specific market structure and communication standards;

• Lack of a comprehensive, consolidated view into the entire market; and

• Dispersed price discovery process.

A trader attempting to trade even a very liquid currency pair might need to capture market data

from numerous locations scattered around the different time zones to ensure optimal trading

execution. Balancing between the inherent distance latency hurdles and decentralized nature of

the FX market is not a simple chore. For most of the large automated trading firms, solving the

market fragmentation and latency issues has meant mostly internal development with close

cooperation between FX ECNs. In recent years, however, a few technology service providers have

emerged to provide trading infrastructure to facilitate those firms looking to jumpstart in

automated FX trading.

AUTOMATE D FX TRADING INFRASTR UCTURE

Despite these obstacles, firms have been implemented automated FX trading for many years and

developing and maintaining a robust automated FX trading infrastructure has been vital to their

continuing success. Some of the key components of an automated FX trading infrastructure

include the following:

Automated FX Trading

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited

Figure 8: Automated FX Trading Infrastructure

Source: Aite Group

• Access to real-time and historical data

of the automated trading environment, access to accurate real

data drives the development of strategies as well as live implementation of those

strategies to capture alpha.

• Ability to capture,

• Support for handling different time slices and types

• Integration with market leading data vendors and feeds

• Robust strategy development framework

firms can start developing, back

live production. In today’s automated t

third-party alpha generation platforms that help quants move from idea generation

and development to production in a seamless fashion.

include the following:

• Support for industry standar

• Seamless workflow from development and testing to optimization and

production

• Support for multiple asset classes and currencies

. All rights reserved. Reproduction of this report by any means is strictly prohibited.

: Automated FX Trading Infrastructure

time and historical data: Considered to be the most important piece

of the automated trading environment, access to accurate real-time and historical

development of strategies as well as live implementation of those

strategies to capture alpha. Key features of this would include the following:

Ability to capture, store, replay and update live data

Support for handling different time slices and types

egration with market leading data vendors and feeds

Robust strategy development framework: Once normalized data can be acquired,

firms can start developing, back-testing, and optimizing strategies prior to going into

live production. In today’s automated trading technology market, there are viable

party alpha generation platforms that help quants move from idea generation

and development to production in a seamless fashion. Key features of this would

include the following:

Support for industry standard development languages

Seamless workflow from development and testing to optimization and

Support for multiple asset classes and currencies

July 2011

.

17

: Considered to be the most important piece

time and historical

development of strategies as well as live implementation of those

Key features of this would include the following:

Once normalized data can be acquired,

testing, and optimizing strategies prior to going into

rading technology market, there are viable

party alpha generation platforms that help quants move from idea generation

Key features of this would

Seamless workflow from development and testing to optimization and

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

18

• Full integration with external applications, including leading statistical

packages, such as MATLAB

• Robust back-testing and optimization environment

• Trading engine: Once the strategy has been thoroughly back-tested and optimized,

traders can put it into production and leverage the trading engine to send out and

manage orders to various execution venues. Key features of this would include the

following:

• Seamless transition from development to production

• Ability to start, modify, and stop strategies

• Position and order management capabilities

• Integration with third-party trading front ends

• Low latency connectivity: Firms must have access to low latency connectivity to

ensure that opportunities can be identified and acted upon in a timely manner. Key

features of this would include the following:

• Global connectivity to leading execution venues and brokers

• Access to colocation and/or proximity services

• Reliability and predictability of connectivity

• Trade analytics: As executions take place, firms can utilize various trade analytics to

measure overall performance of automated trading strategies. Intraday trade

analytics can provide real-time feedback on overall execution quality so that the

trader can make necessary adjustments to underlying strategy assumptions. Key

features of this would include the following:

• Real-time monitoring of live orders and positions

• Ability to tweak working strategies on the fly

• Feeding performance measurement data back to development environment to

improve effectiveness of strategies

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

19

CASE STUDY

Founded in November 2009, Fisycs Capital is a Paris-based systematic, quantitative hedge fund

focusing exclusively on liquid markets. Fisycs Capital is currently authorized and regulated by the

AMF (Autorité des Marchés Financiers) in France. Current list of strategies implemented by

Fisycs Capital include the following:

• FX Intraday

• U.S. Equity Market Neutral

• Global Macro

• FX Fundamental

In the process of setting up its investment and trading technology infrastructure, Fisycs Capital

examined many different options, both in-house and vendor supplied platforms. At the end of its

analysis, Fisycs selected the QuantHouse’s QuantFACTORY platform for various reasons:

• Ability to connect strategy to multiple venues and brokers at the same time.

• Fisycs Capital has a reasonable number of strategies and QuantFACTORY makes

message loading quite simple and seamless

• Ability to customize and the vendor’s receptiveness to incorporating requested new

features into their development plans.

Focusing on the automated FX market, Fisycs Capital believes that the ultimate benefits of

leveraging the QuantFACTORY platform are the following:

• As a multi-strategy hedge fund, very easy to support multi-desk trading activities

and also very easy to support risk management and asset allocation off the same

platform.

• Fairly shallow learning curve in grasping the code needed to test and very easy to

use.

• QuantFACTORY is very good at handling data; can take in multiple data sources very

quickly.

• All strategies’ modules are separated but can communicate with each other.

• Openness of the platform, enabling Fisycs Capital to link their own execution algos.

• Helps Fisycs Capital to quickly improve trading ideas, thus shortening the time from

research or recalibration to live execution.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

20

CONCLUSION

Despite the influx of automated trading flow, the banks still maintain enough market clout to

hold onto their competitive edge. In fact, the FX market remains very much a two-tiered market;

single bank platforms tend to interact against customers who can be perceived either as less

sophisticated or less sensitive to explicit transaction costs (i.e., willing to take wider spreads to

get the trades done). On the other hand, most automated trading is occurring on FX ECNs. While

the liquidity ultimately comes from banks, this two-tiered approach has enabled banks to be

more efficient in trading against different types of end customers.

In this rapidly evolving automated trading marketplace, technology has become a competitive

differentiator, enabling firms to quickly develop and launch new strategies to take advantage of

changing market conditions. While the initial stage of technology development has been driven

by large firms with significant in-house application development capabilities, the availability of

cost effective, robust third-party solutions will go a long way in leveling the playfield for the rest

of the marketplace moving forward.

In recent months, several traders from major banks have left to start their own firms, taking with

them not only their quantitative skills, but also their market structure knowledge, which could

potentially pave the way for the next phase in automated trading, in which non-bank trading

firms play a larger role in liquidity provision. The first round may be over in FX automated

trading, but many more remain before the real winners can be determined in this rapidly

evolving marketplace.

Automated FX Trading

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited

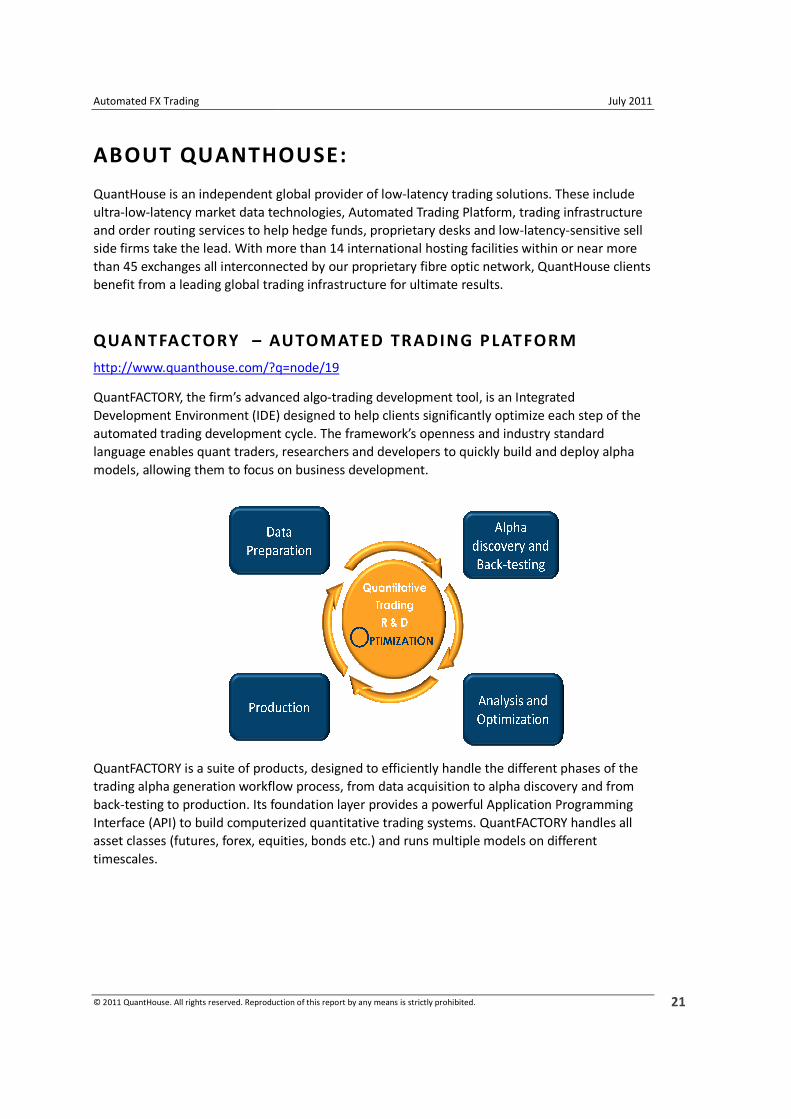

ABOUT QUANTHOUSE:

QuantHouse is an independent global provider of low

ultra-low-latency market data technologies, Automated Trading Platfo

and order routing services to help hedge funds, proprietary desks and low

side firms take the lead. With more than 14 international hosting facilities within or near more

than 45 exchanges all interconnecte

benefit from a leading global trading infrastructure for ultimate results.

QUA NTFACTORY – AUTOMATED TRADING P L

http://www.quanthouse.com/?q=node/19

QuantFACTORY, the firm’s advanced algo

Development Environment (IDE) designed to help

automated trading development cycle. The framework’s openness and industry standard

language enables quant traders, re

models, allowing them to focus on business development.

QuantFACTORY is a suite of products, designed to efficiently handle the different phases

trading alpha generation workflow

back-testing to production. Its foundation layer

Interface (API) to build computerized quantitative trading systems.

asset classes (futures, forex, equities, bonds etc.) and runs multiple models on different

timescales.

. All rights reserved. Reproduction of this report by any means is strictly prohibited.

ABOUT QUANTHOUSE:

QuantHouse is an independent global provider of low-latency trading solutions. These include

latency market data technologies, Automated Trading Platform, trading infrastructure

and order routing services to help hedge funds, proprietary desks and low-latency

side firms take the lead. With more than 14 international hosting facilities within or near more

than 45 exchanges all interconnected by our proprietary fibre optic network, QuantHouse clients

benefit from a leading global trading infrastructure for ultimate results.

AUTOMATED TRADING P LATFORM

http://www.quanthouse.com/?q=node/19

the firm’s advanced algo-trading development tool, is an Integrated

Environment (IDE) designed to help clients significantly optimize each step of

automated trading development cycle. The framework’s openness and industry standard

enables quant traders, researchers and developers to quickly build and deploy

to focus on business development.

QuantFACTORY is a suite of products, designed to efficiently handle the different phases

generation workflow process, from data acquisition to alpha discovery and from

to production. Its foundation layer provides a powerful Application Programming

Interface (API) to build computerized quantitative trading systems. QuantFACTORY

asset classes (futures, forex, equities, bonds etc.) and runs multiple models on different

July 2011

.

21

latency trading solutions. These include

rm, trading infrastructure

latency-sensitive sell

side firms take the lead. With more than 14 international hosting facilities within or near more

d by our proprietary fibre optic network, QuantHouse clients

ATFORM

is an Integrated

significantly optimize each step of the

automated trading development cycle. The framework’s openness and industry standard

and deploy alpha

QuantFACTORY is a suite of products, designed to efficiently handle the different phases of the

data acquisition to alpha discovery and from

provides a powerful Application Programming

QuantFACTORY handles all

asset classes (futures, forex, equities, bonds etc.) and runs multiple models on different

Automated FX Trading

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited

D A T A C E N T E R S E R V E R

Data acquisition and preparation

With its plug-in architecture, QuantFACTORY can communicate with any market data prov

broker, and new plug-ins can easily be written to connect to new providers.

Clients can import historical data and store real

tests. Clients can also store low latency market data,

Reuters RMTD and IDC) and be connected to liquidity platforms

Trayport). The data capture configuration

timescales). QuantFACTORY can handle diff

tick-data, best bid-offer and order

D E V E L O P M E N T P L A T F O R M

Alpha discovery

The QuantFACTORY development platform is a Visual Studio

powerful IDE. It provides several tools to ease the model development process. This combination

allows clients to manage referential and historical market data and to develop and test models.

QuantFACTORY then analyzes the performance of clients’ models and e

execution platform.

Develop, record and bask-test your alpha models

Within the same application, a list of instruments (equities, derivatives, bonds, swaps,

legged instruments, FX, commodities e

In addition, the ‘Indicator Editor’ window contains a library with more than

but clients can also customize and add indicators.

an event-based application, provid

any .Net language within the Visual Studio environment. Using the libraries

. All rights reserved. Reproduction of this report by any means is strictly prohibited.

reparation

in architecture, QuantFACTORY can communicate with any market data prov

ins can easily be written to connect to new providers.

can import historical data and store real-time data in the datacentre server to run back

can also store low latency market data, third party vendors’ data (e.g. Bloomberg,

and be connected to liquidity platforms (e.g. Currenex, Hotspot

he data capture configuration is managed through a web interface (instruments

timescales). QuantFACTORY can handle different timescales, ranging from daily to intraday bars,

offer and order-book updates or custom data.

D E V E L O P M E N T P L A T F O R M

QuantFACTORY development platform is a Visual Studio add-in and as such benefits from its

It provides several tools to ease the model development process. This combination

allows clients to manage referential and historical market data and to develop and test models.

QuantFACTORY then analyzes the performance of clients’ models and exports them to a live

test your alpha models

a list of instruments (equities, derivatives, bonds, swaps,

instruments, FX, commodities etc.) and trading rules (mono- or multi-asset)

the ‘Indicator Editor’ window contains a library with more than 60 listed indicators

can also customize and add indicators. The QuantFACTORY development platform is

based application, providing convenient and sophisticated ways of writing

any .Net language within the Visual Studio environment. Using the libraries and third

July 2011

.

22

in architecture, QuantFACTORY can communicate with any market data provider or

datacentre server to run back-

(e.g. Bloomberg,

Currenex, Hotspot, EBS or

hrough a web interface (instruments and

erent timescales, ranging from daily to intraday bars,

and as such benefits from its

It provides several tools to ease the model development process. This combination

allows clients to manage referential and historical market data and to develop and test models.

xports them to a live

a list of instruments (equities, derivatives, bonds, swaps, multi-

asset) are available.

60 listed indicators

QuantFACTORY development platform is

of writing models in

third party add-

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

23

ons (for MATLAB, R…), clients can import mathematical and statistical functions that will be

integrated in to the model.

Debug and improve models

To further enhance models, a debugging mode is included. Alpha models will run at a time step

interval to trace internal events, signals and execution flow with high resolution, allowing clients

to easily detect any bugs.

Simulate model results

Continue by choosing the timescales, parameters for different models and the historical data

chosen to back-test models. Models will then be executed. The application has a range of

different back-testing statistics views: Performance Summary for Curves and Indicators, Portfolio,

Bar Chart, Global Trade Statistics and Equity Curve Statistics.

Optimize models

With an optimization procedure clients can define and test parameter values in order to obtain

the best results and determinate the appropriate levels of risk.

E X E C U T I O N P L A T F O R M

Produce and launch model

To start trading, clients simply load their precompiled strategy component (generated in the

development platform) into the execution platform, configure the adapter that will be used to

connect the model to the market data provider and broker or EMS. In addition, clients can create

their own alert conditions to warn about position items based on P&L value, set-up notification

mode (auditory alerts, via email, color codes), and program actions. From there, clients can

monitor orders and observe in real-time the full cycle of orders’ execution, from order sending

to position updates in the model.

Q UA NTFEED – ULTR A LOW LATE NCY MARKET DATA

http://www.quanthouse.com/low-latency-market-data

To enable our customers to manage the ever-increasing demand for low latency market data and

to meet the changing requirements of today’s trading environment with new trading venues,

fragmentation of liquidity and rapidly increasing volumes of data, QuantHouse has developed an

end-to-end product offering encompassing data capture within the exchange, ultra-fast data

normalization and dissemination over QuantHouse’s proprietary fibre optic network. Since we

design, implement and maintain every single element of the market data chain, we can offer our

customers an ultra-low-latency solution, accessible through one single connection to our

network, using a unique API, making it very easy to access any market using the same

application.

Automated FX Trading July 2011

© 2011 QuantHouse. All rights reserved. Reproduction of this report by any means is strictly prohibited.

24

Q UA NTLINK – ULTR A LOW LATENCY TR ADING INFRASTR UCTURE

http://www.quanthouse.com/QuantLink

QuantLINK is QuantHouse’s trading infrastructure service to help buy side and sell side trading

firms improve their infrastructures to keep up with market demand. Whether you use Smart

Order Routing or algorithmic trading applications, your overall performance is linked to the

quality of your trading infrastructures. QuantLINK combines QuantHouse’s proprietary fibre

optic network interconnecting the heart of the exchanges with proximity hosting at the source.