auto dealer advertising compliance

TRANSCRIPT

Auto Dealer Advertising Compliance

Getting Customers on the Lot Without Crossing the Line

There’s no doubt that the right advertising program can make you

plenty of money. But as they say, it’s not how much money you make

but how much you get to keep that counts. You have to get customers

on the lot, but if you cross the line you may face bad publicity and

lawsuits. Auto dealers are a favorite target of both state and federal

regulators hunting for advertising violations and are often blindsided

by expensive fines, lawsuits and bad publicity. While the various laws

and regulations covering automotive advertising can be confusing, it

can be helpful to understand how lawmakers view advertising in

general and what triggers their wrath.

5 Reasons Why Advertising Compliance is Challenging

1. Regulators frequently cite dealers for advertising violations even though there are no customer complaints. Since statements and representations in advertisements are evaluated based on their tendency to deceive, no actual harm to consumers need occur for there to be a violation.

2. Despite your best intentions, you may be held accountable for advertising errors. If an ad is deemed deceptive, an advertiser has liability regardless of whether there was intent to deceive.

3. If the first contact with a consumer is secured by deception, a violation may occur even though the true facts are made known to the buyer before he or she enters into the contract of purchase or lease. In the infamous “we’ll pay off your trade no matter how much you owe” ads, the dealers were found to be in violation even though they disclosed that negative equity is added to the amount financed at the time of sale.

4. Advertising violations are easy to find and difficult to defend against. Often, all the proof a regulator or attorney needs is the ad itself.

5. The rules aren’t always clear & new technologies bring new challenges - It’s easy to get blindsided!

The Dodd-Frank Consumer Protection Act enhanced the FTC’s existing authority over motor vehicle advertising, sales and lease practices .

State AGs can now enforce FTC Act. Violations can bring fines of up to $16,000 per violation, or per day of a continuing violation.

Said David Vladeck, Director of the FTC's Bureau of Consumer Protection. "The Federal Trade Commission is constantly on the lookout for potentially deceptive ads, and brings actions to stop them when appropriate."

The Feds have traditionally gone after bigger fish and left car dealers to state regulators. But the game has changed - last year’s advertising cases were the first of their kind brought by the FTC.

Federal enforcement leads to more local enforcement. Attorneys general in many states identify accusations against dealerships as being their #1 concern, and recognize the political capital in going after dealers.

The Rest of The Story…

Besides federal and state regulatory agencies, consumer law firms that

specialize in auto dealer-related legal issues continue to flourish. Car

dealerships are a prime target for these type of firms due to very

complicated consumer-based laws. Many legal action against dealers

these days is the result of mistakes or omissions in the way vehicles

are advertised, or the statements made by dealership staff. Even more

disturbing is the fact that many lawsuits by plaintiff's attorneys

frequently have the ability to be rolled into a class action, and may

prove very costly to the defending dealer. Attorneys are generating

massive settlements and legal fees from class action lawsuits for

seemingly minor issues.

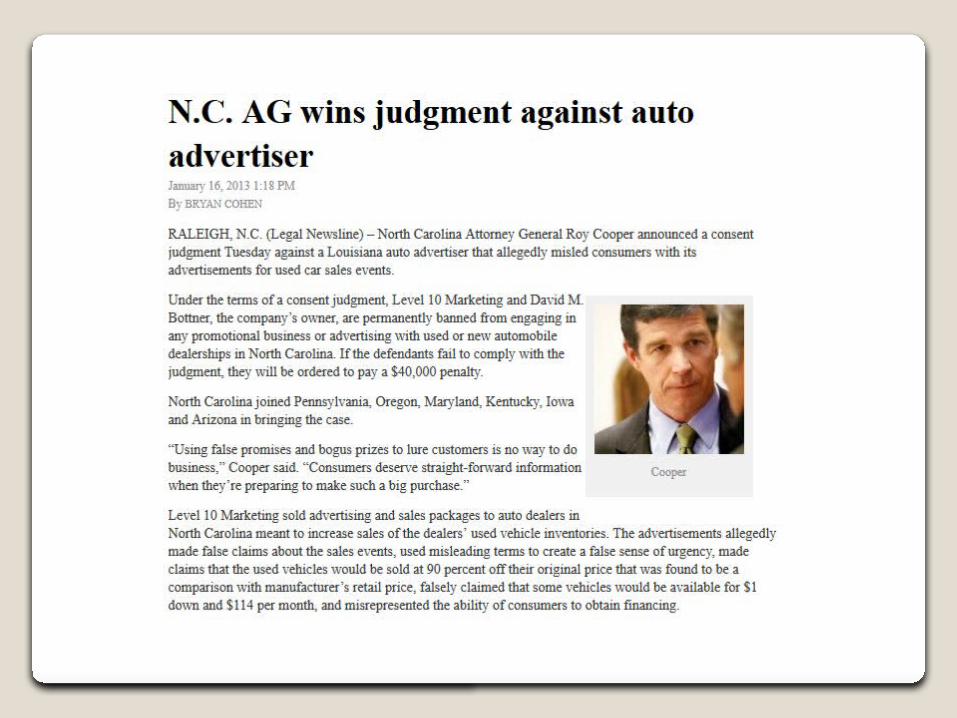

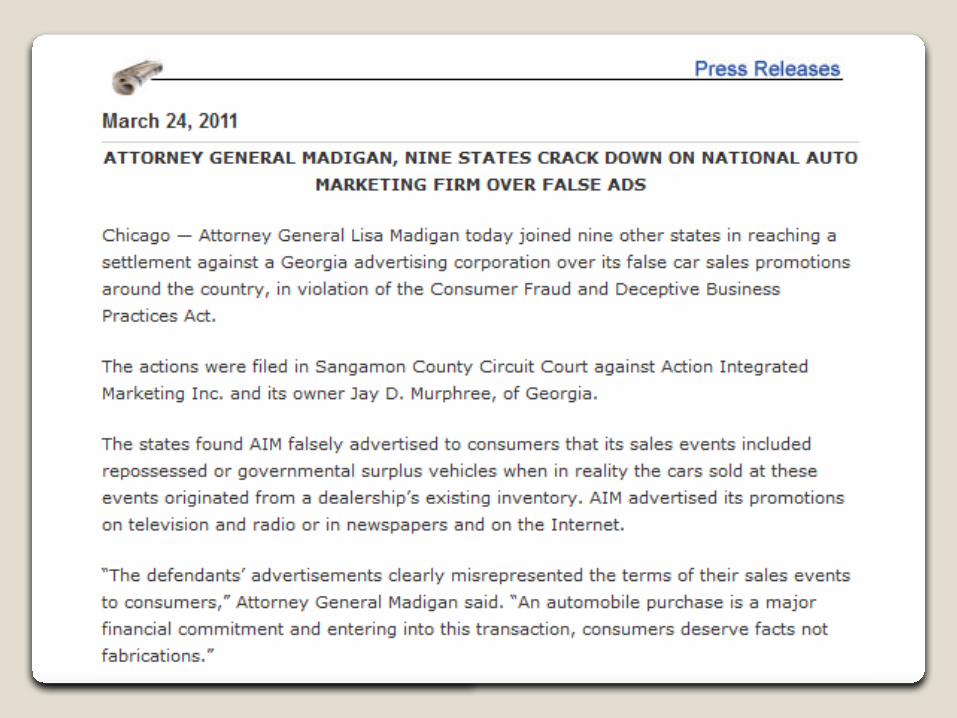

In addition, the dealer had to sign a Consent Decree with the Attorney General that stated among other things: “Any violation committed after the date of entry of this Consent Decree of any of the injunctive terms of this Consent Decree shall constitute a violation of an injunction for which civil penalties of up to $25,000 per violation may be sought by the Attorney General”. In other words, any advertising missteps this dealer makes will cost it dearly. This injunction is permanent by the way. How would you like your state’s attorney general breathing down your neck?

This same marketing company was busted by the state of Washington back in 2007. In that case, the dealer ended up paying almost twice the amount in penalties and legal fees as the marketing company did.

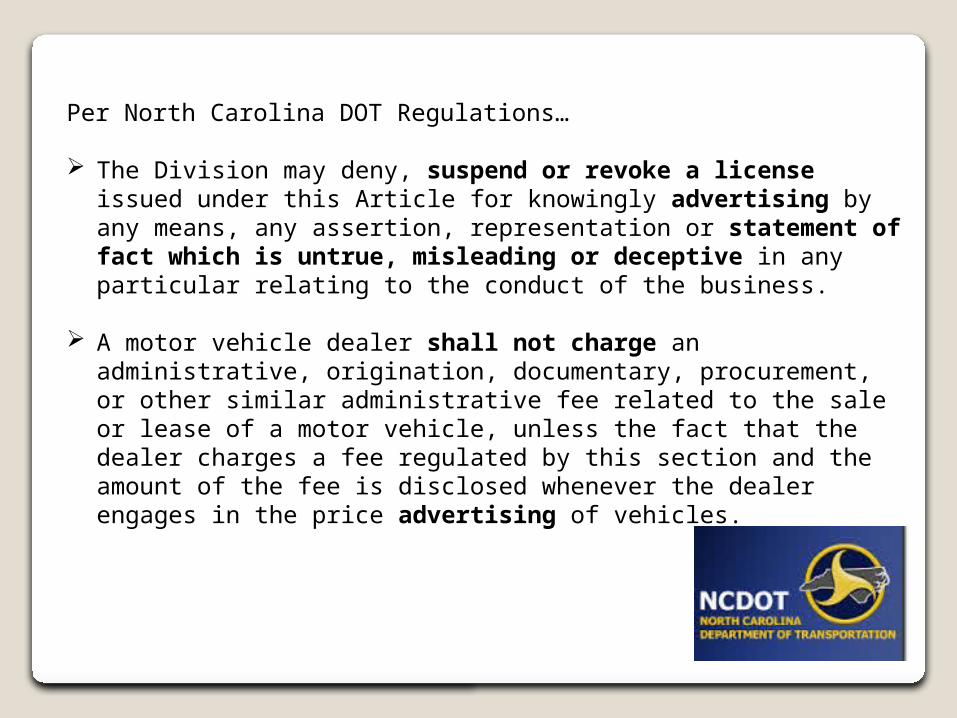

Per North Carolina DOT Regulations…

The Division may deny, suspend or revoke a license issued under this Article for knowingly advertising by any means, any assertion, representation or statement of fact which is untrue, misleading or deceptive in any particular relating to the conduct of the business.

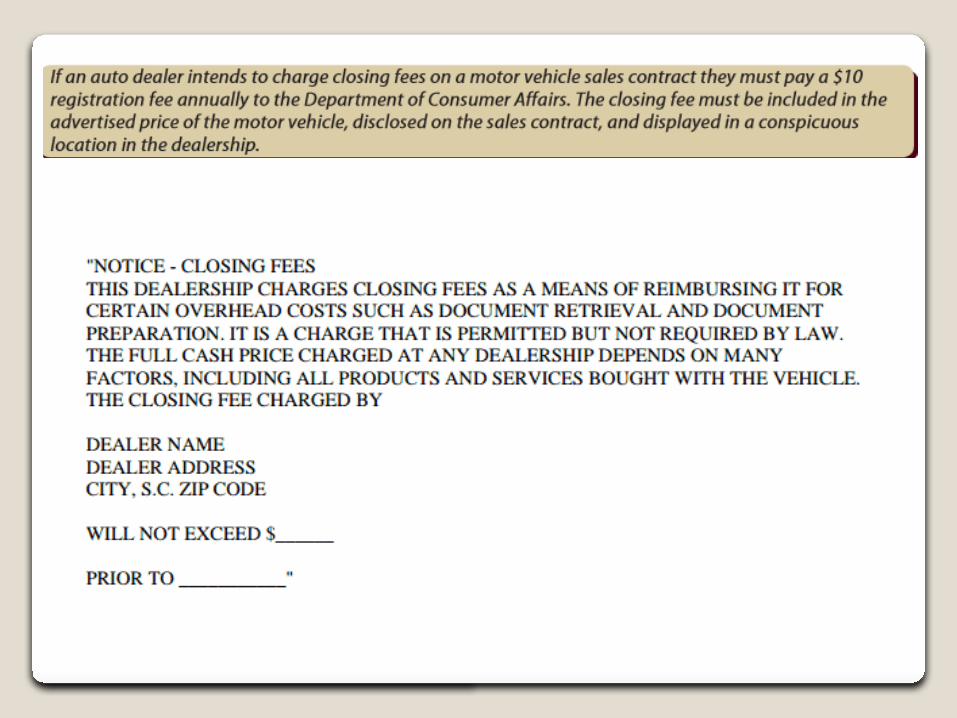

A motor vehicle dealer shall not charge an administrative, origination, documentary, procurement, or other similar administrative fee related to the sale or lease of a motor vehicle, unless the fact that the dealer charges a fee regulated by this section and the amount of the fee is disclosed whenever the dealer engages in the price advertising of vehicles.

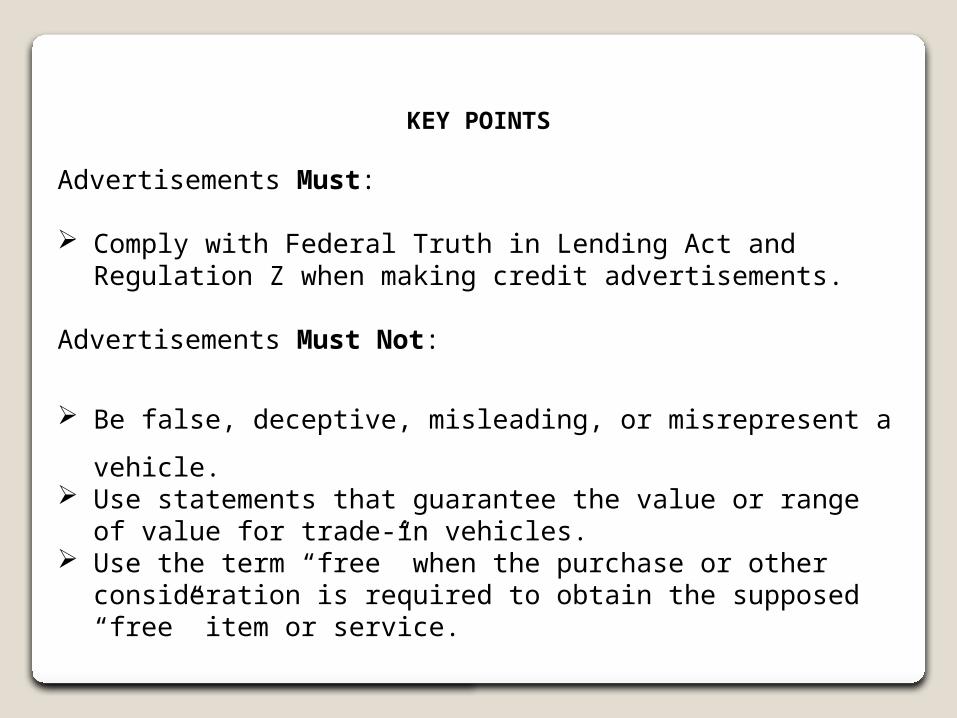

KEY POINTS

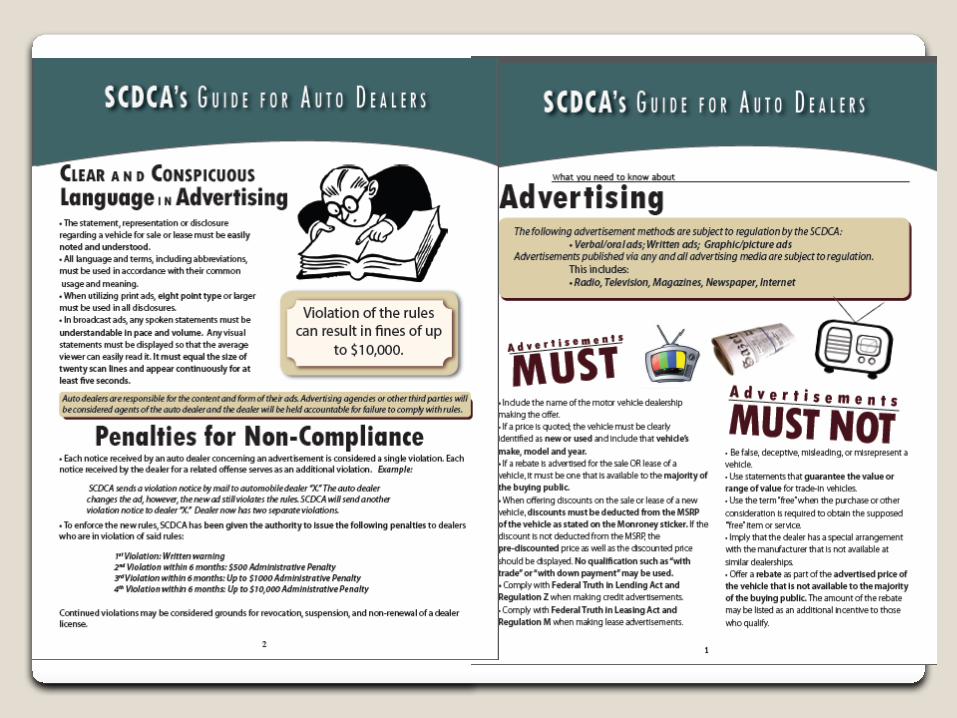

Advertisements Must:

Comply with Federal Truth in Lending Act and Regulation Z when making credit advertisements.

Advertisements Must Not:

Be false, deceptive, misleading, or misrepresent a vehicle. Use statements that guarantee the value or range of value

for trade-in vehicles. Use the term “free” when the purchase or other

consideration is required to obtain the supposed “free” item or service.

Even if it’s not written in the law, you can get stung…

Advertising Concepts Every Dealer Employee Should Know

While regulations and “hot buttons” vary by state, keep in mind that attorneys general frequently compare notes with their peers, and follow the lead of the federal regulatory agencies, so you never know when your state’s AG is going to get a bee in his or her bonnet about a new issue…

Even though the meaning of statements in an ad seems obvious to you, it may still be considered deceptive. Statements susceptible to both a misleading and a truthful interpretation are typically considered to be misleading by regulators. A good example is when the FTC cited a number of dealers for ads stating “we’ll pay off your trade no matter how much you owe”. While this statement may be technically true, lawmakers are of the opinion that these ads imply that the dealer will buy the trade for the amount the customer owes, regardless of its real value.

It’s all about the big picture. An advertisement as a whole may be misleading although every sentence separately considered is literally true. The key is to make sure your message is clear, truthful, easy to understand, and not subject to multiple interpretations.

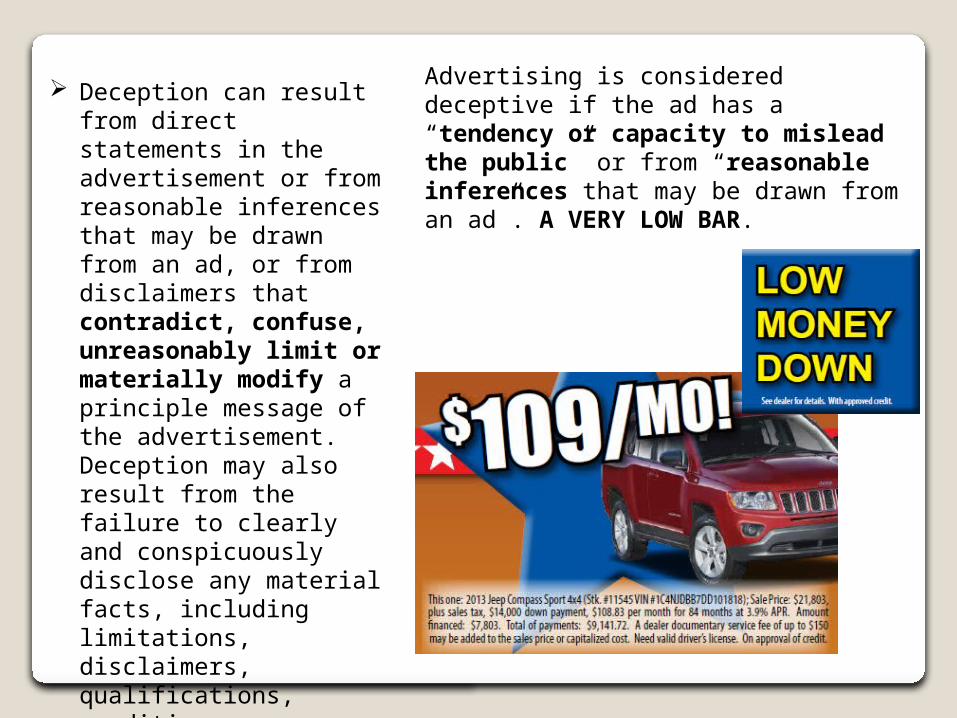

Deception can result from direct statements in the advertisement or from reasonable inferences that may be drawn from an ad, or from disclaimers that contradict, confuse, unreasonably limit or materially modify a principle message of the advertisement. Deception may also result from the failure to clearly and conspicuously disclose any material facts, including limitations, disclaimers, qualifications, conditions, exclusions or restrictions.

Advertising is considered deceptive if the ad has a “tendency or capacity to mislead the public” or from “reasonable inferences that may be drawn from an ad”. A VERY LOW BAR.

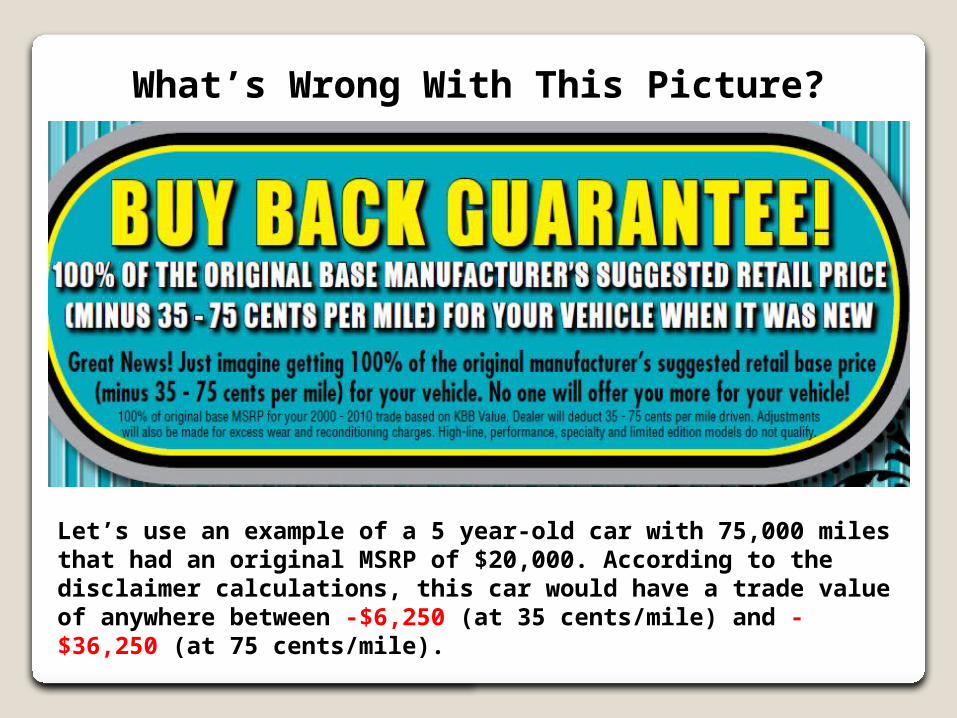

Let’s use an example of a 5 year-old car with 75,000 miles that had an original MSRP of $20,000. According to the disclaimer calculations, this car would have a trade value of anywhere between -$6,250 (at 35 cents/mile) and -$36,250 (at 75 cents/mile).

What’s Wrong With This Picture?

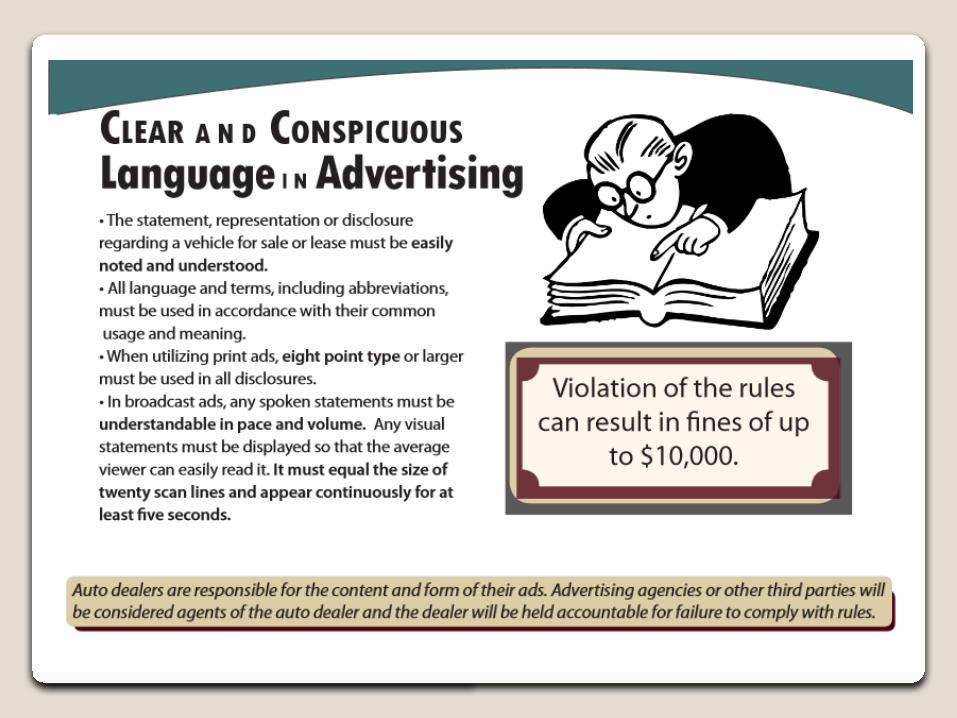

Your disclosures must be made in a clear and conspicuous manner to minimize the possibility of misunderstanding by the consumer public. It’s vital to clearly and conspicuously disclose any material facts, including limitations, disclaimers, qualifications, conditions, exclusions or restrictions.

Be sure that all disclaimers are clearly and conspicuously displayed and not buried away in difficult-to-read fine print or a difficult-to-find links on websites. In general, the “clear and conspicuous standard” means that the disclosures in any media must be reasonably understandable. NOTE: South Carolina requires a minimum type-size of 8 points.

Disclaimers in themselves won’t always protect against advertising violations. A disclaimer must not contradict, confuse, unreasonably limit, materially modify a principle message, or substantially change the meaning of any advertised statements.

The FTC has developed what it refers to as “THE FOUR Ps” to describe what the clear and conspicuous standard requires:

Prominence. The type size should be big enough to read easily. There should be a sharp contrast between the disclosure and the background. The should be a clear type face. For TV (and video) ads, the consumer must have enough time to read the disclosure.

Presentation. The wording must be easy to understand. The format should not discourage careful reading. The advertisement should be free of distractions that compete for consumer attention. Consumers are more likely to understand the disclosure or qualifiers if it is in the same mode (visual and/or audio) as the advertising to which it relates.

Placement and Proximity. The disclosure or qualifier should be in a place where consumers will read it. The disclosure or qualifier should be near the advertising to which it relates.

The words “No Credit Rejected“, “Guaranteed Financing” or words of similar import should not be used unless true, since they imply that consumer credit will be extended to anyone regardless of the person's credit worthiness or financial ability to pay.

A dealer should not offer any free goods or services conditioned on the purchase of a vehicle. However, free goods or services may be offered as incentive to take a test drive or visit the dealership. According to FTC guidelines, “If a product or service usually is sold at a price arrived at through bargaining, rather than at a regular price, it is improper to represent that another product or service is being offered “Free” with the sale”.

There’s no safety net in the “but everybody does it this way” mindset. Regulators have made it clear that the fact that others were, are, or will be engaged in like practices will not be considered a defense in a legal action.

TRUTH IN LENDING DISCLOSURES

If payments are advertised, the following disclosures must be stated in the advertisement:

a) The amount or percentage of the downpaymentb) The terms of repaymentc) The “annual percentage rate” using that term or the

abbreviation “APR”, and if the rate may be increased after consummation, that fact.

For example, it would be deceptive to advertise a low monthly payment based on 84 month financing on an amount financed of $5,000 if all of the financial institutions that you normally assigns contracts to require a minimum amount financed of $10,000 for 84 month terms.

Only offer credit terms that are actually available to a reasonable amount of consumers. Per federal Regulation Z, if an advertisement for credit states specific credit terms, it must state only those terms that actually are or will be arranged or offered by the dealer.

No customer should be encouraged to not purchase the advertised vehicle, nor should there be any acts attempted by the sales staff to prevent the sale.

Ensure that vehicles are promptly removed from the websites after they have been sold.

If a car has already been sold when a customer calls or emails, your staff should tell the customer it’s sold!

Regulators have taken action against businesses for having a sales compensation plan designed to penalize salespersons who sell the advertised merchandise or service.

Bait & Switch advertising is a hot button with lawmakers and must be avoided. It’s unlawful to advertise for sale any vehicle that the dealer does not intend to sell because the true intention is to switch the customer to another vehicle.

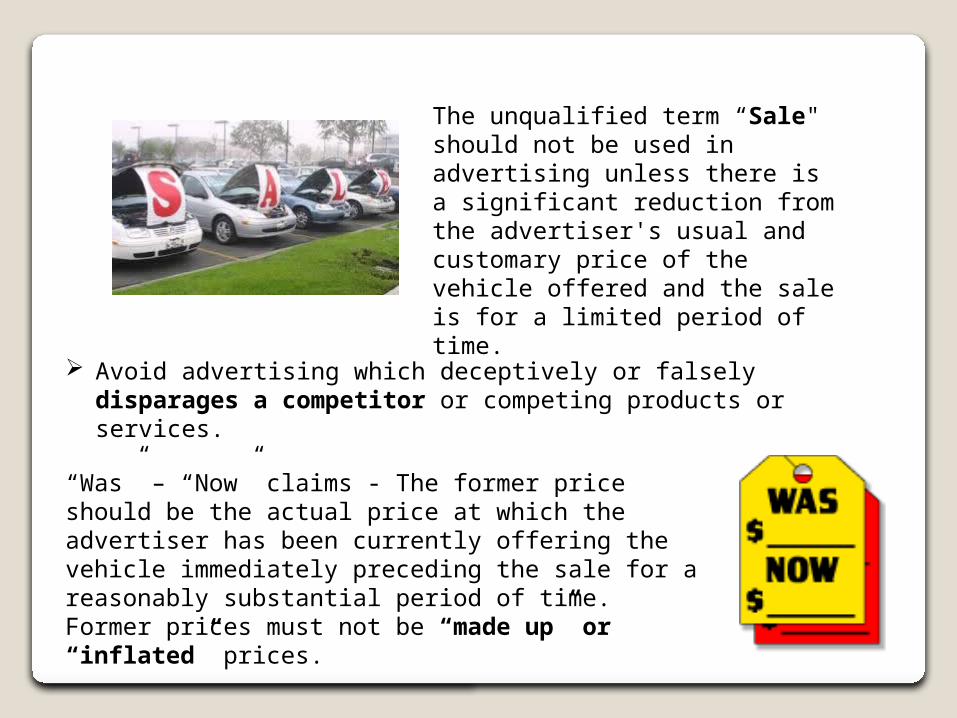

The unqualified term “Sale" should not be used in advertising unless there is a significant reduction from the advertiser's usual and customary price of the vehicle offered and the sale is for a limited period of time.

“Was” – “Now” claims - The former price should be the actual price at which the advertiser has been currently offering the vehicle immediately preceding the sale for a reasonably substantial period of time. Former prices must not be “made up” or “inflated” prices.

Avoid advertising which deceptively or falsely disparages a competitor or competing products or services.

Don't forget your digital marketing. Websites, videos, email, and even social media are considered advertising mediums and may be targeted by regulators. Don’t assume that your website provider is utilizing language that is acceptable in your particular state and including all of the required disclosures. BOTTOM LINE – They don’t care where you advertise, you’d better do it right!

Never assume that advertising agencies or vendors know all the laws and regulations governing advertising compliance. This is particularly true of companies based in other states, such as internet and direct mail providers. The primary responsibility for compliance lies with the dealership, not the advertising agency or vendor. According to the law, a dealer has the duty to investigate the accuracy of any statements made in advertising.

Advertising laws apply to all forms of advertising, including radio, television, print, electronic, direct mail, flyers, billboards, showroom and other dealership displays. Even Oral statements can be considered advertising.

Other Advertising Hot-Buttons

• Falsely representing that vehicles are from sources such as rental car company bankruptcies, bank repossessions, or fleet liquidations when the vehicles sold came from the dealers’ usual inventories.

• Falsely representing that a sale is being sponsored or conducted by a bank, lending institution, fleet, repossession, or liquidation company.

• Using deceptive promotions, including mailers that state “Urgent Recall-Official Notice” or otherwise imply it is from a government agency.

• Ads that guarantee a minimum trade-in value.• Failing to state the odds of a winning a prize, the value of that prize, and all

material conditions required to obtain a prize.• Making statements that the dealer could not substantiate through its

business records.

Advertising compliance isn’t rocket science. The rules for good advertising are mostly common sense. It’s all about being truthful and easy to understand. A good practice is to have a friend or family member not involved in the car business look at your ads. If they don’t get it, your customers probably won’t either!

Depending on the dealership, advertising may be handled by any number of people such as sales managers, internet staff, or a marketing department. Any employee or vendor involved in advertising should be properly trained on federal and state advertising regulations.

If you’re not sure about an advertisement, don’t guess! It’s a good idea to have your advertising reviewed by a qualified professional – it may end up costing quite a bit less than a legal action.

Getting “caught” is no longer a just a fine and slap on the wrist. Regulators have begun using the media to penalize those dealers caught in order to intimidate others. Regulators want press, and the tougher the press is on the offending dealers the better it is for the regulators in charge.

The severity of the offenses is often exaggerated.

The social media age brings �more long-term consequences and public humiliation than businesses have ever seen before.

Do you want your customers seeing YOUR dealership on the 6 o’clock news?

Thanks For Attending!

Please feel free to call or drop an me a line if you ever have any questions…

Jim Radogna(858) 722-2726Email: [email protected]: http://www.facebook.com/jimradognaTwitter: @jradognaLinkedIn: www.linkedin.com/in/jimradogna/Compliance Blog: http://collegeofautomotivemanagement.blogspot.com/

www.CollegeofAutomotive.com