asset/liability management - year 2 · 2 asset/liability management: proce ss, positioning, &...

TRANSCRIPT

ASSET/LIABILITY MANAGEMENT - YEAR 2

“ALM Process, Positioning & Profitability”

Darren Herrmann Executive Vice President & Treasurer

UMB Financial Corporation & UMB Bank Corporate Treasury

Kansas City, MO [email protected]

816-860-7195

July 30, 2018

1

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 1

Asset/Liability Management:Process, Positioning, & Profitability

Darren D. Herrmann

Executive Vice President & Treasurer

UMB Financial Corporation

Graduate School of Banking

Madison, Wisconsin

July 30, 2018

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 2

Year 2 OverviewDarren Herrmann—Day 1

• Asset/Liability Management (ALM): Positioning, Profitability & Process

Andy Trovillion—Day 2

• Interest Rate Risk Measurement and Management

John McQueen—Day 3

• Developing an Effective Liquidity Strategy

Dave Koch—Day 4

• Putting it all together: Implementation of a Risk-Return Framework

2

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 3

DisclosuresThe information and opinions expressed in this message are solely those of the author and do not necessarily state or reflect the opinion of UMB Bank, n.a. or UMB Financial Corporation. This communication is provided for informational purposes only. UMB Bank, n.a. and UMB Financial Corporation are not liable for any errors, omissions, or misstatements.

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 4

Overview• ALM Overview

• ALM and Positioning in the Current Environment

• ALM & Profitability• Drivers of Net Interest Income (NII)

• A Case Study

• Marginal Cost of Funding

• Simple Derivatives to Manage the ALM Profile

• Intersession Project Part 1

• The ALM Process• Structure, responsibilities

• Seven Steps to an Improved ALCO

• Intersession Project Part 2

3

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 5

ALM Overview

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 6

ALM

Definition

• The term “asset/liability management” refers to the processes of acquiring and deploying funds to maximize net interest income, and thereby profitability and the value of the bank, while managing related financial risks and constraints.

4

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 7

ALM

Net Interest Margin

Interest Rate Risk

Liquidity Risk

ROE

LeverageROA

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 8

ALM’s Primary Areas of Responsibility• Net Interest Income & Net Interest Margin

• Balance Sheet & Off Balance Sheet Structure• ALM Mix

• Loan and Deposit Pricing

• Investment Portfolio Management

• Wholesale Funding

• Capital/Leverage

• Derivatives

• Risk Measurement and Management/Constraints• Interest Rate Risk

• Liquidity Risk

• Capital

5

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 9

ALM Levers

• Balance Sheet Composition/Mix Optimization

• Pricing

• Capital/Leverage

• Interest Rate Risk

• Liquidity Risk

• Derivatives

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 10

ALM and the Current Environment

6

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 11

Questions for the Current ALM Environment• Should I keep making fixed-rate loans?

• Should I add funding with tenor now?

• Will my deposit mix shift back toward my pre-crisis position?

• Am I modeling deposit sensitivity appropriately?

• Should I lever or delever my balance sheet?

• What could happen to my liquidity as rates increase and the Fed shrinks its balance sheet?

• How has technology changed the competitive landscape in terms of raising deposits, rate sensitivity, switching costs (remote deposit capture, mobile banking, Kasasa)?

• Do I know who my large funds providers are and how they might behave?

• Do I know the trend in uninsured deposits at my institution?

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 12

• What is the marginal cost of new deposits raised?

• The Fed has increased 175 basis points since December 2015, has the expected impact materialized in your bank’s NIM?

• Do I have exposure to a flattening yield curve and if so which kind?

• Am I using derivatives to enable loan growth and/or provides protection during a flat curve period?

• What is my bond portfolio’s exposure to rising rates and what are the market value and liquidity implications?

• What will be the impact of no more Reg. D?

• Do I have a Liquidity Coverage Ratio (LCR) bank in any of my markets and how could that impact deposit rates?

Questions for the Current ALM Environment

7

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 13

Is This Time Different?

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 14

Yield Curve Is Flat by Historical Norms

1.16

1.31

1.74

1.41

0.69

0.36

Last 30 years Last 20 years Last 10 years Last 5 years Last year Current

10‐2 Slope Over Time

8

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 15

Interest Rates: Past, Present, Future?

‐

1.00

2.00

3.00

4.00

5.00

6.00

3 MO 6 MO 1 YR 2 YR 3 YR 5 YR 7 YR 10 YR 30 YR

Percen

t

2007 2013 2018 1 Year Forward Rates

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 16

Cost of Funds vs. Market Rates Will Be Key to Interest Rate Risk Sensitivity—Historically 55% of Market Rates

‐

1.00

2.00

3.00

4.00

5.00

6.00

2005Q1

2005Q2

2005Q3

2005Q4

2006Q1

2006Q2

2006Q3

2006Q4

2007Q1

2007Q2

2007Q3

2007Q4

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

2017Q3

2017Q4

2018Q1

Percen

t

Cost of Funds with DDA Comparison

UMB Financial Corporation 1 Month Libor

Credit Crisis

9

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 17

30%36% 41%

35%

19%18%

22% 35%20%

23%

22%18%

9%

8%

6%6%22%

15%9% 6%

2008 2011 2014 2018

Funding Mix More Indeterminate, Less Term

DDA NOW MMDA Savings CDs

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 18

ALM & Profitability

10

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 19

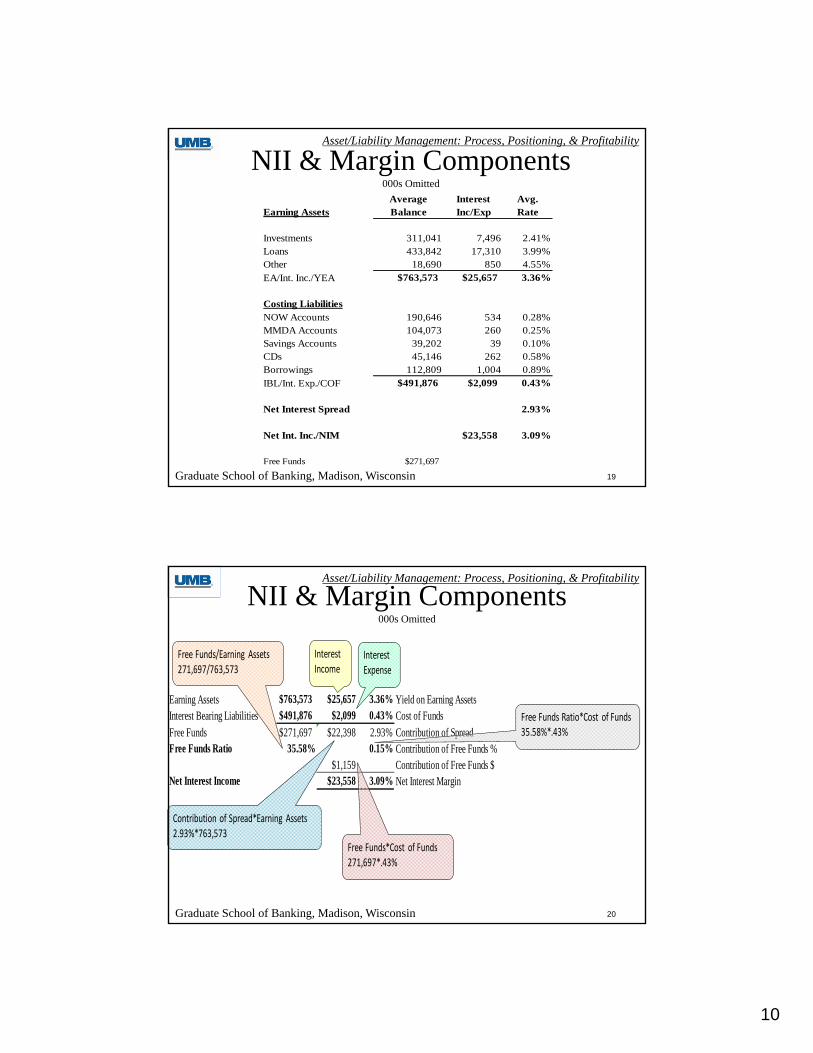

NII & Margin Components000s Omitted

Average Interest Avg.Earning Assets Balance Inc/Exp Rate

Investments 311,041 7,496 2.41%Loans 433,842 17,310 3.99%Other 18,690 850 4.55%EA/Int. Inc./YEA $763,573 $25,657 3.36% Costing LiabilitiesNOW Accounts 190,646 534 0.28%MMDA Accounts 104,073 260 0.25%Savings Accounts 39,202 39 0.10%CDs 45,146 262 0.58%Borrowings 112,809 1,004 0.89%IBL/Int. Exp./COF $491,876 $2,099 0.43%

Net Interest Spread 2.93%

Net Int. Inc./NIM $23,558 3.09%

Free Funds $271,697

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 20

NII & Margin Components000s Omitted

Earning Assets $763,573 $25,657 3.36% Yield on Earning AssetsInterest Bearing Liabilities $491,876 $2,099 0.43% Cost of FundsFree Funds $271,697 $22,398 2.93% Contribution of SpreadFree Funds Ratio 35.58% 0.15% Contribution of Free Funds %

$1,159 Contribution of Free Funds $Net Interest Income $23,558 3.09% Net Interest Margin

InterestIncome

InterestExpense

Free Funds/Earning Assets271,697/763,573

Contribution of Spread*Earning Assets2.93%*763,573

Free Funds*Cost of Funds271,697*.43%

Free Funds Ratio*Cost of Funds35.58%*.43%

11

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 21

Drivers of Net Interest Income

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 22

Drivers of NII

• Rate (Pricing, credit risk interest rate risk, liquidity risk)

• Volume of assets and liabilities

• Mix of assets and liabilities

12

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 23

Net Interest Income Variance Equations

Avg. Avg. Avg. Avg.Balance Rate Balance Rate309,937 2.07% Investments 311,041 2.41%719,755 Earning Assets 763,573

Investments Rate M2 * L2 * R2 - M2 * L2 * R1

Variance 311,041 / 763,573 763,573 2.41% - 311,041 / 763,573 763,573 2.07% = 1,058

Investments Volume M2 * L2 * R1 - M2 * L1 * R1

Variance 311,041 / 763,573 763,573 2.07% - 311,041 / 763,573 719,755 2.07% = 369

Investments Mix M2 * L1 * R1 - M1 * L1 * R1

Variance 311,041 / 763,573 719,755 2.07% - 309,937 / 719,755 719,755 2.07% = -347

Total Investments Variance 1,080

Net Interest Income Variance Analysis Calculation ExampleDollars 000s Omitted

Period 1 Period 2

Rate Variance = M(2)*L(2)*R(2) - M(2)*L(2)*R(1) Volume Variance = M(2)*L(2)*R(1) - M(2)*L(1)*R(1) Mix Variance = M(2)*L(1)*R(1)* - M(1)*L(1)*R(1)

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 24

Net Interest Income Variance Analysis

Period 1 Period 2 Rate + Volume + Mix = TotalAmount Rate Amount Rate Variance Variance Variance Variance

Earning Assets309,937 2.07% 311,041 2.41% Investments 1,058 369 -347 1,080

391,643 3.68% 433,842 3.99% Loans 1,345 916 637 2,898

18,176 4.60% 18,690 4.55% Other -9 49 -26 14

$719,755 3.01% $763,573 3.36%

$21,664 $25,657 Interest Income $2,393 $1,335 $264 $3,993

Costing Liabilities167,524 0.15% 190,646 0.28% NOW Accounts 248 16 18 283123,014 0.11% 104,073 0.25% MMDA Accounts 146 7 -27 125

34,318 0.09% 39,202 0.10% Savings Accounts 4 2 2 842,064 0.51% 45,146 0.58% CDs 32 13 3 4790,593 0.45% 112,809 0.89% Borrowings 496 29 71 596

$457,513 0.23% $491,876 0.43%

$1,040 $2,099 Interest Expense $925 $67 $67 $1,059

$20,625 2.87% $23,558 3.09% Variance $1,468 $1,268 $198 $2,933

Sample BankNet Interest Income Variance Analysis

(000s Omitted)

13

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 25

Case Study

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 26

Year-to-Date -- Jun 2009 Year-to-Date -- Jun 2008AVG AVG VARIANCE ANALYSISRATE RATE

AVERAGE INTEREST EARNED/ AVERAGE INTEREST EARNED/ RATE BASIS VOLUME MIX TOTALASSETS: BALANCE INC/EXP PAID BALANCE INC/EXP PAID VARIANCE VARIANCE VARIANCE VARIANCE VARIANCE Net Loans 436,723 10,013 4.58% 405,634 11,702 5.74% (2,704) (70) 2,240 (1,154) (1,688) Total Investment Securities 446,703 7,048 3.51% 313,818 6,601 4.64% (2,278) (5) 1,634 1,095 447 Other Earning Assets 43,277 97 .57% 44,635 609 2.86% (489) (3) 103 (123) (512) Total Earning Assets 932,151 17,159 3.87% 768,882 18,912 5.12% (5,471) (78) 3,977 (182) (1,754) Int Inc

LIABILITIES: - - - - - - - - - Total Demand Deposits 235,101 - 189,917 - - - - - - Total Transaction Accounts 368,692 929 .51% 284,896 1,825 1.29% (1,317) (12) 396 38 (896) Total Time Deposits 148,622 1,714 2.33% 147,947 3,055 4.15% (1,336) (17) 537 (525) (1,341) Total Interest Bearing Deposits 517,314 2,643 1.03% 432,843 4,879 2.27% (2,652) (29) 933 (487) (2,236) Total Borrowings 150,951 197 .26% 137,335 1,627 2.38% (1,595) (10) 316 (141) (1,430) Total Interest Bearing Liabilities 668,265 2,841 .86% 570,178 6,507 2.29% (4,247) (39) 1,248 (628) (3,666) Int Exp

Interest Income & Rate Earned 17,159 3.87% 18,912 5.12% - - - - - Interest Expense & Rate Paid 2,841 .86% 6,507 2.29% - - - - - Net Interest Income & Rate Spread 14,318 3.01% 12,406 2.83% (1,224) (39) 2,729 446 1,912 NII

Net Interest Margin 3.25% 3.41%

Net Interest Income Variance Analysis

14

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 27

Drivers of NII Observations• Fairly large negative rate variance during period of

declining rates becoming a drag on net interest income growth

• What does that indicate?• The bank has seen its spread widen but its net interest

margin decline• What explains this?• What does this indicate about this bank’s interest rate risk

exposure?• The bank’s volume variance offset the negative rate

variance due to significant asset growth, what happens if this growth slows and rates stay low?

• What levers remain for this bank to pull?

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 28

Net Interest Income Variance Analysis$ In Thousands

Year-to-Date -- 2013 Year-to-Date -- 2012AVG AVG VARIANCE ANALYSIS

RATE RATEAVERAGE INTEREST EARNED/ AVERAGE INTEREST EARNED/ RATE VOLUME MIX TOTAL

ASSETS: BALANCE INC/EXP PAID BALANCE INC/EXP PAID VARIANCE VARIANCE VARIANCE VARIANCE

Net Loans 585,582 9,267 3.78% 502,719 9,023 4.26% (988) 1,078 154 244 Investment Securities 679,385 4,544 1.90% 611,730 4,839 2.22% (833) 591 (54) (295)Other Earning Assets #1 21,721 248 3.55% 16,896 211 3.77% (26) 30 32 36 Other Earning Assets #2 81,706 98 .29% 85,313 115 .32% 7 10 (34) (17) Total Earning Assets 1,376,012 14,156 2.64% 1,224,685 14,187 2.95% (1,839) 1,709 99 (31)LIABILITIES: - - - - - Total Demand Deposits 465,905 403,855 - - - - Total Rate Bearing Transaction Accts. 588,867 247 .10% 497,235 293 .14% (98) 38 14 (46)Total Time Deposits 112,048 357 .77% 133,181 505 .91% (68) 47 (127) (148)Total Int Bearing Deposits 700,915 603 .21% 630,417 798 .30% (167) 85 (113) (195)Total Borrowings 170,871 100 .14% 153,066 105 .17% (5) 12 (12) (5)Total Interest Bearing Liabilities 871,787 704 .20% 783,483 903 .28% (171) 96 (125) (200)

Interest Income & Rate Earned 14,156 2.64% 14,187 2.95%Interest Expense & Rate Paid 704 .20% 903 .28%Net Interest Income & Rate Spread 13,452 2.44% 13,284 2.67% (1,668) 1,613 223 168 Net Interest Margin 2.52% 2.77%

15

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 29

Drivers of NII Observations• Bank continues to offset negative rate variance with

positive volume variance and positive mix variance• What constraints could this bank face in trying to continue

this strategy?• The bank is sacrificing net interest margin for net interest

income, what financial goals must be a priority (ROA vs. ROE vs. EPS)?

• As you survey the regulatory and competitive landscape what if anything concerns you about the bank’s funding base?

• What levers remain for this bank to pull?

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 30

$ In ThousandsYear-to-Date -- 2018 Year-to-Date -- 2017

AVG AVG VARIANCE ANALYSISRATE RATE

AVERAGE INTEREST EARNED/ AVERAGE INTEREST EARNED/ RATE VOLUME MIX TOTALASSETS: BALANCE INC/EXP PAID BALANCE INC/EXP PAID VARIANCE VARIANCE VARIANCE VARIANCE

Net Loans 1,123,626 21,630 4.61% 1,057,795 18,186 4.12% 1,985 432 1,026 3,444 Investment Securities 614,401 5,036 2.29% 642,474 4,796 2.12% 404 105 (269) 241 Other Earning Assets #1 135,721 1,490 3.91% 131,855 1,353 3.64% 90 32 15 137 Other Earning Assets #2 51,162 396 1.87% 49,672 238 1.16% 179 5 (25) 158 Total Earning Assets 1,924,910 28,553 3.75% 1,881,795 24,573 3.33% 2,659 574 747 3,980 LIABILITIES:Total Demand Deposits 592,719 592,498 Total Rate Bearing Transaction Accts. 973,433 2,222 .55% 848,939 823 .23% 1,266 22 112 1,400 Total Time Deposits 103,973 320 .74% 115,075 272 .57% 75 6 (32) 49 Total Int Bearing Deposits 1,077,406 2,542 .57% 964,014 1,094 .27% 1,341 27 80 1,448 Total Borrowings 167,846 1,080 1.55% 252,902 865 .83% 491 13 (290) 215 Total Interest Bearing Liabilities 1,245,252 3,622 .70% 1,216,916 1,959 .39% 1,832 41 (210) 1,663

Interest Income & Rate Earned 28,553 3.75% 24,573 3.33%Interest Expense & Rate Paid 3,622 .70% 1,959 .39%Net Interest Income & Rate Spread 24,931 3.05% 22,614 2.94% 827 533 957 2,317 Net Interest Margin 3.30% 3.08%

Net Interest Income Variance Analysis

16

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 31

Drivers of NII Conclusions• Determine what has been driving net interest income• Has rate variance been positive or negative as rates have

increased—how fits with interest rate risk results?• Assess what levers exist to alter this• Assess likelihood of offsetting if negative rate variance through

growth or mix changes• If already highly loaned, assess likelihood of improving mix

variance on the liability side of the balance sheet• Assess the impact of any changes on the institution’s risk profile• Model forward results and load into simple comparison• Consider the potential impact of sustained high or low rate

environments

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 32

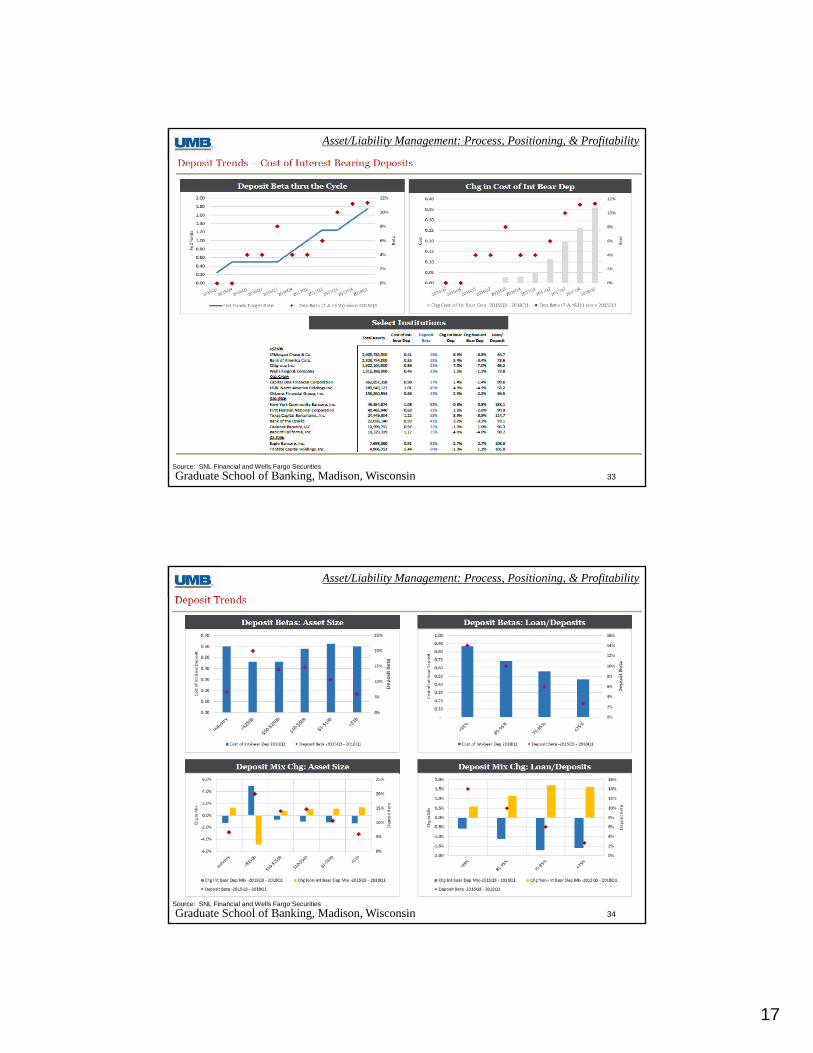

Marginal Cost Funding

17

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 33Source: SNL Financial and Wells Fargo Securities

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 34Source: SNL Financial and Wells Fargo Securities

18

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 35

Marginal Cost Funding AnalysisNo Growth Strategy

Interest Interest InterestBalance Rate Expense Balance Rate Expense Balance Rate Expense

MMDA 15,000,000 0.25% 37,500 15,000,000 0.75% 112,500 13,500,000 0.25% 33,750 Wholesale Funding 1,500,000 1.90% 28,500 Combined Position 15,000,000 0.25% 37,500 15,000,000 0.75% 112,500 15,000,000 0.42% 62,250

Marginal Cost Savings 50,250 Marginal Cost Break Even 5.25%

Growth StrategyInterest Interest Interest

Balance Rate Expense Balance Rate Expense Balance Rate ExpenseExisting CDs 15,000,000 1.00% 150,000 13,500,000 1.00% 135,000 15,000,000 1.00% 150,000 New Money 37 Month CD Special 1,500,000 2.25% 33,750 Old Money 37 Month CD Special 1,500,000 2.25% 33,750 Wholesale Funding 1,500,000 2.90% 43,500 Combined Position 15,000,000 1.00% 150,000 16,500,000 1.23% 202,500 16,500,000 1.17% 193,500

Marginal Cost of Funds $ 52,500 43,500 Marginal Cost of Funds Rate 3.50% 2.90%

Comments:75% new money assumption gets the special CD option down to a marginal cost of 2.33%.Breakeven new money percentage equals 60.33%.

Current Position Rates Up 50bp Match Rate Rates Up 50bp Don't Match Rate

Current Position Special Nets $3 Million 50/50 Split No Special, Fund Wholesale

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 36

• What is my expected range of new money to be raised?

• What is my expected range of existing deposit cannibalization?

• Am I raising in all locations or the cheapest?

• What is my expected rate of outflow if don’t match rate?

• How much outflow can I tolerate?

• What would my wholesale funding options cost?

• What are my breakeven results?

Key Considerations

19

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 37

Simple Derivatives to Manage the ALM Profile

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 38

• Bank has experienced margin expansion as rates rise

• Two thirds of loan book reprices or cash flows within 12 months

• Believes Fed will increase another 100 basis points over the next year

• Late in economic cycle and flat curve raises likelihood of lower rates to come which would be adverse to margin

• Bank has experience with embedding loan rate floors, but averse to doing so presently

Context

20

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 39

Interest Rate Swaps Overview

Initial cost is 80 basis points

Initial benefit is 80 basis points

1 Month Libor

2.10%

5 year bullet

2.90%

1 Month Libor

2.10%

5 year bullet

2.90%

Your Bank1. Pay Fixed, Receive Float2. Convert fixed rate loans

or bonds to floating rate3. Convert floating rate

funding to fixed4. Expect rates to rise

and/or want to limit exposure to rising rates

Counterparty

Receive FixedPay Float

Your Bank1. Pay Float, Receive Fixed2. Convert floating rate

loans or bonds to fixed3. Convert fixed rate

funding to floating4. Expect rates to fall

and/or want to limit exposure to falling rates

Counterparty

Receive FloatPay Fixed

Fixed Rate Loan or BondFloating Rate Funding

Floating Rate Loan or BondFixed Rate Funding

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 40

Interest Rate Cap

Interest Rate Floor

5 Year ATM Cap Rate = 2.77%

Pay 2.08%

Receive Amount 1ML

Exceeds Strike

Receive Amount 1ML

Below Strike

Your Bank1. Long (Buys) Cap2. Pays Option Premium3. If 1 Month Libor goes

above strike price, Your Bank receives payment

4. Used to limit exposure to 1 Month Libor rising above a certain level

Counterparty1. Short (Sells) Cap2. Receives Option

PremiumFixed Rate Loan or BondFloating Rate Funding

Your Bank1. Long (Buys) Floor2. Pays Option Premium3. If 1 Month Libor goes

below strike price, Your Bank receives payment

4. Used to limit exposure to 1 Month Libor falling below a certain level

Counterparty1. Short (Sells) Floor2. Receives Option

PremiumFloating Rate Loan or BondFixed Rate Funding (DDAs)

21

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 41

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 42

Intersession Project Part 1

Analysis of Financial Performance

22

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 43

Equity Multiplier

Total Assets 100,000,000$ Total Equity 8,000,000$ Equity Ratio 8%Equity Multiplier 12.5

Peer Total Assets 100%Peer Equity 8%Equity Multiplier 12.5

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 44

Seven Steps to a Better ALCO

23

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 45

Seven Steps to a Better ALCO• Step 1: Make your policies metric driven• Step 2: Get your membership right• Step 3: Focus your agenda on risk/return metrics

and action items• Step 4: Build meeting information around agenda• Step 5: Review Your Risk/Return Profile

--Is the bank measuring the opportunity cost of its current interest rate risk position?

• Step 6: Pricing methodologies should be robust and reflect metrics

• Step 7: Have action items--Meeting should not just be a history lesson

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 46

Setting Limits

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

‐

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Base Case 20% NII Limits 0.80% ROA

Comparison of Base Case to Limit Methodologies

NII ROA

Base Case 20% NII LimitsMinimum .80%

ROA MetricTotal Assets 100,000,000 100,000,000 100,000,000 NII 3,500,000 2,800,000 3,192,308 NI 1,000,000 545,000 800,000 Tax Rate 35% 35% 35%ROA 1.00% 0.55% 0.80%

ROA metric requires NII limit of < 9%, not 10%-20%

24

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 47

Expected Outcomes

• More engaged ALCO

• Better questions

• Increased volume and quality of ideas

• Greater strategic focus

• Improved financial results

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 48

Intersession Project Part 2

ALCO Responsibilities and Tools

25

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 49

Conclusions• ALM’s primary responsibilities center on

• Net interest income and net interest margin

• Rate, volume, mix

• Interest rate risk

• Liquidity risk

• Capital Management

• Levers—Balance Sheet Mix Composition, Capital/Leverage, Pricing, Interest Rate Risk, Liquidity Risk, Derivatives

• Understand the interest rate cycles and what the yield curve is saying

• Follow the 7 steps for an improved ALM process

Asset/Liability Management: Process, Positioning, & Profitability

Graduate School of Banking, Madison, Wisconsin 50

Questions?

Darren Herrmann

Executive Vice President & Treasurer

UMB Financial Corporation

816-860-7195