asset liability risk management.. risk identification risk measure risk monitor risk manage

TRANSCRIPT

Compiled By:Janata Bank Staff College, Dhaka

Asset Liability Risk Management.

Risk and Risk Management Steps

Risk Identification Risk Measure Risk Monitor Risk Manage

Asset Liability Management (ALM) is an integral part of bank management. Banks should have a structured and systematic process of managing the Balance sheet (Assets , Liabilities & Owner’s equity) risks.

ALM is a process to manage the composition and pricing of the assets, liabilities and off balance sheet items and aims to control Bank’s exposure to market risks, with the objective of optimizing net income and net equity value within the overall risk preferences of the Bank.

Asset-Liability Risk Management

Contents:

1. Policy

2. Organizational Structure

3. Process

Assets for BankLoans and Advances,Investments

Liability for BankDeposits and other liabilities

Risk in Assets-Liabilities

Liquidity Risk ManagementManagement of Market RiskFunding and Capital planningProfit Planning and Growth

ProjectionTrading Risk Management

Contents of ALM GuidelinesPolicy StatementObjective of the ALM PolicyALM OrganizationFramework for MeetingsRoles and Responsibilities of ALCOALCO Paper

POLICY STATEMENT

ALCO of Janata Bank Limited set out the following policies, which should be, reviewed annually taking into consideration of changes in Balance sheet and market dynamics.

Loan Deposit (LD) Ratio The Loan Deposit Ratio should be

81% (changeable according to SLR).

LD ratio should not exceed 85%

At present the desired level is 70%.

Commitments A bank's liquidity is very much

vulnerable to undrawn commitments by customers.

Customers have the right to ask for this funds at any point in time

Bank is obligated to pay the customers.

The commitments shall not exceed 200% of the unused wholesale borrowing capacity for the last twelve months .

Whole sale Borrowing Guidelines (WBG)

The guideline should be set in absolute amount depending on bank’s borrowing capacity, historic market liquidity

At present the wholesale borrowings capacity of the bank should not exceed its paid up capital excluding borrowing against securities.

Maximum cumulative outflow (MCO)

Maximum cumulative outflow (MCO) guidelines control the net outflow (inflow from asset maturity minus outflow from liability maturity) over the following periods : overnight, one week and one month.

Standard (20%).

Medium Term Funding Ratio, (MTF) This ratio is intended to highlight the extent to

which Banks are dependent on being able to roll over short term deposits in order to fund medium term assets.

The minimum MTF ratio the bank must maintain is 30%.

However the ideal MTF rate should be 45%.

Liquidity Contingency Plan A liquidity contingency plan needs to

be approved by the ALCO. A contingency plan needs to be prepared keeping in mind that enough liquidity is available to meet the fund requirements in liquidity crisis situation.

Local Regulatory Compliance

There is a firm policy on compliance to the Bangladesh Bank in respect of CRR, SLR, Capital adequacy etc.

Objective of the ALM Policy

Liquidity Risk ManagementInterest Rate Risk ManagementForeign Exchange Risk ManagementMaximization of profit of the bank

Liquidity Risk Management

Providing adequate liquidity to the Bank by reducing maturity mismatches to within manageable permitted levels to ensure that the current and potential demand for funds is supported by cash and liquid assets.

Interest Rate Risk Management

Proper pricing of assets and liabilities.Portfolio review of both assets and liabilities.Regular review of interest rate outlook.To keep the level of interest rate risk within

the manageable level.Maximization on net interest margin.

Foreign Exchange Risk Management

Measurement and control of Foreign Exchange risk.

Profit Planning

Budgeting, strategic planning and monitoring of net profit, interest rate and other balance sheet ratios.

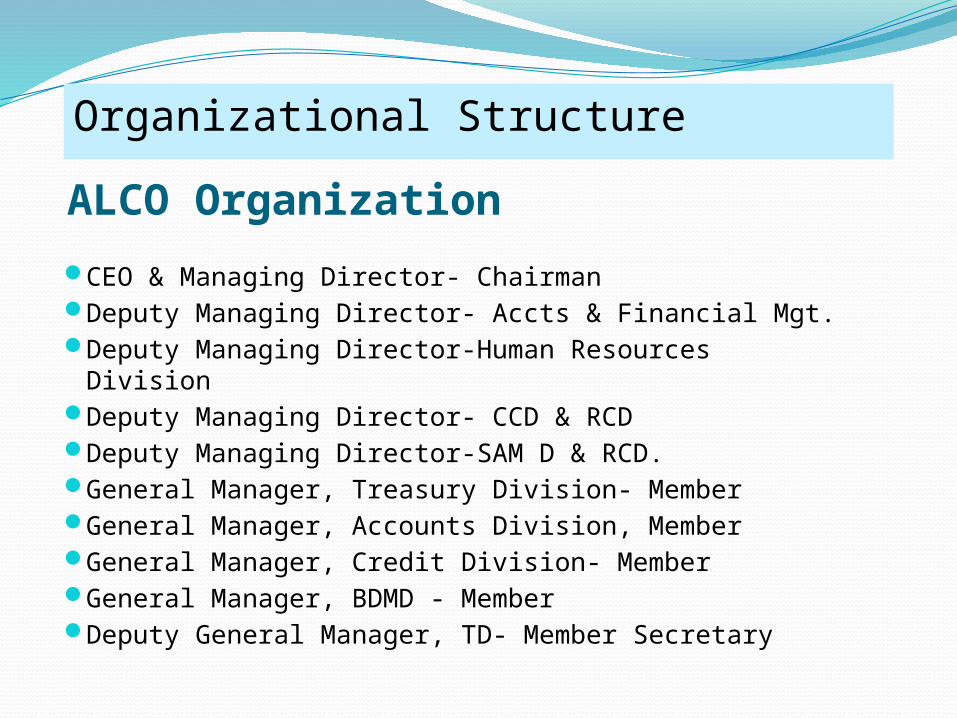

Organizational Structure

ALCO Organization

CEO & Managing Director- ChairmanDeputy Managing Director- Accts & Financial Mgt. Deputy Managing Director-Human Resources DivisionDeputy Managing Director- CCD & RCD Deputy Managing Director-SAM D & RCD.General Manager, Treasury Division- MemberGeneral Manager, Accounts Division, MemberGeneral Manager, Credit Division- Member General Manager, BDMD - MemberDeputy General Manager, TD- Member Secretary

Framework for Meetings

Each meeting will be chaired by the CEO & MD

The Convener of the meeting- DGM (Treasury).

The Committee will meet at least once a month.

The minimum quorum four members.The ALCO will be supported by the ALCO

Unit

Roles and Responsibilities of ALCOThe ALCO is a decision-making unit. Measurement and management of liquidity and interest rate

risks.Profit planning and growth projection.Interest rate forecasting and movement of interest rates.Deciding the business strategy of the Bank in line with the

Bank’s budget.Decision on sources of funds, mix of liabilities and their

maturity profiles.Product pricing of both assets and liabilities. Monitor the activities of the Bank’s treasury and returns

objectives.Approval of pricing of financial services i.e. Fees & Com.,

ALCO Paper To facilitate a purposeful and effective

discussion in ALCO meetings, the agenda papers of the ALCO meeting will be prepared and circulated to the members at least a day prior to the meeting.

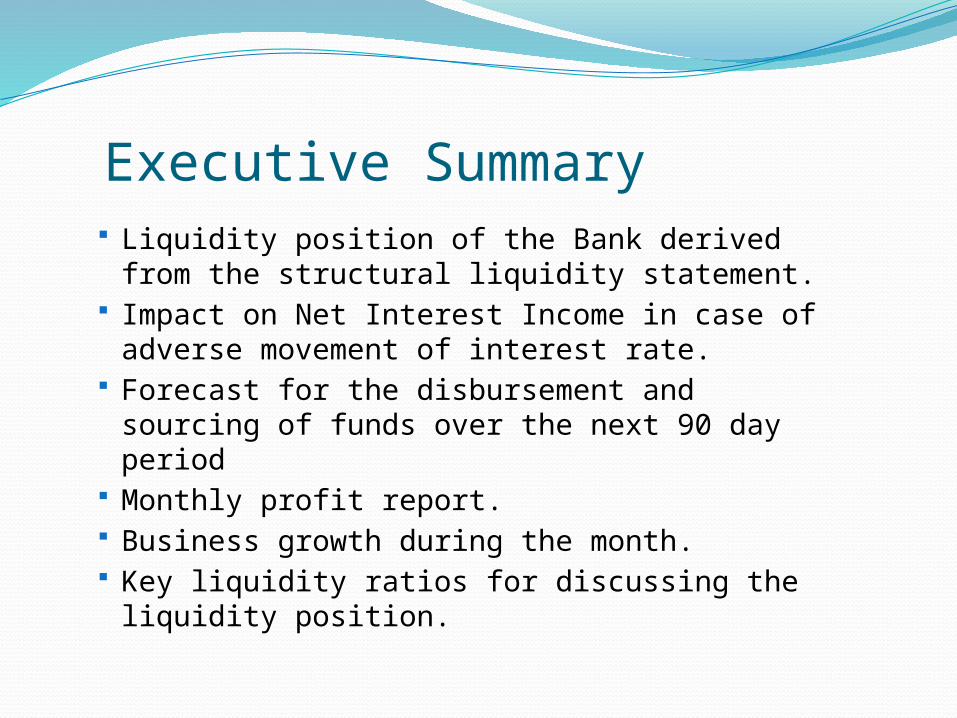

Executive Summary Liquidity position of the Bank derived from

the structural liquidity statement. Impact on Net Interest Income in case of

adverse movement of interest rate. Forecast for the disbursement and sourcing

of funds over the next 90 day period Monthly profit report. Business growth during the month. Key liquidity ratios for discussing the

liquidity position.

Thank You ALL