assessing sources of funding for insurance risk based capital · assessing sources of funding for...

TRANSCRIPT

Assessing Sources of

Funding for Insurance

Risk Based Capital

Louis Lee

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Session Number: (ex. MBR4)

AGENDA for Today

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

1. Motivations of Capital Needs

2. Practical Risk Based Capital Funding Options

3. Types of Reinsurance Solutions

4. Worked Example

AGENDA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

1. Motivations of Capital Needs

2. Practical Risk Based Capital Funding Options

3. Types of Reinsurance Solutions

4. Worked Example

MOTIVATIONS OF CAPITAL NEEDS

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Strain from New Business growth

Efficient use of Existing Capital

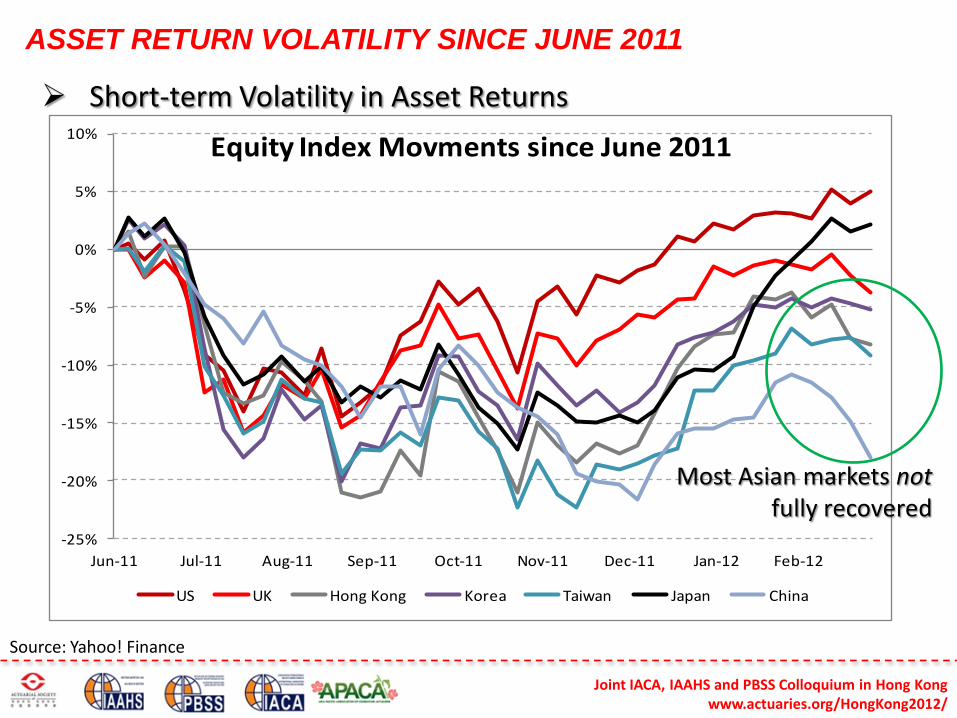

Short-term Volatility in Asset Returns

Earnings volatility, volatility from catastrophic events

Rating Agency requirement

Changes in Regulatory Capital requirements and Accounting

standards

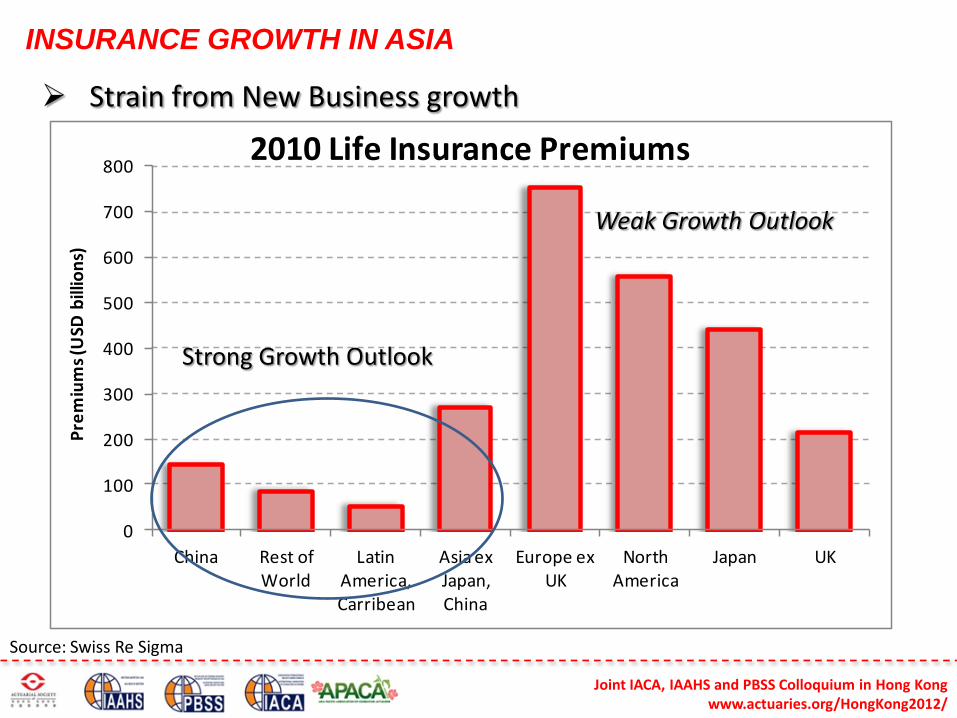

INSURANCE GROWTH IN ASIA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Strain from New Business growth

0

100

200

300

400

500

600

700

800

China Rest of World

Latin America, Carribean

Asia ex Japan, China

Europe ex UK

North America

Japan UK

Pre

miu

ms

(USD

bill

ion

s)

2010 Life Insurance Premiums

Strong Growth Outlook

Weak Growth Outlook

Source: Swiss Re Sigma

ASSET RETURN VOLATILITY SINCE JUNE 2011

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Short-term Volatility in Asset Returns

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12

Equity Index Movments since June 2011

US UK Hong Kong Korea Taiwan Japan China

Source: Yahoo! Finance

Most Asian markets not fully recovered

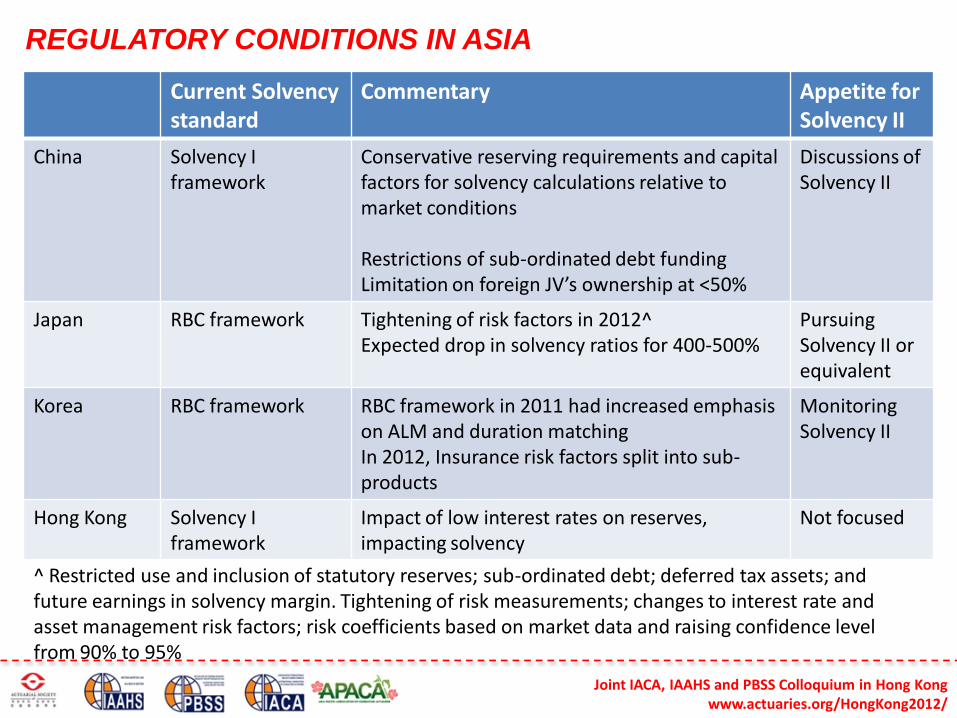

REGULATORY CONDITIONS IN ASIA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Current Solvency standard

Commentary Appetite for Solvency II

China Solvency I framework

Conservative reserving requirements and capital factors for solvency calculations relative to market conditions Restrictions of sub-ordinated debt funding Limitation on foreign JV’s ownership at <50%

Discussions of Solvency II

Japan RBC framework Tightening of risk factors in 2012^ Expected drop in solvency ratios for 400-500%

Pursuing Solvency II or equivalent

Korea RBC framework RBC framework in 2011 had increased emphasis on ALM and duration matching In 2012, Insurance risk factors split into sub-products

Monitoring Solvency II

Hong Kong Solvency I framework

Impact of low interest rates on reserves, impacting solvency

Not focused

^ Restricted use and inclusion of statutory reserves; sub-ordinated debt; deferred tax assets; and future earnings in solvency margin. Tightening of risk measurements; changes to interest rate and asset management risk factors; risk coefficients based on market data and raising confidence level from 90% to 95%

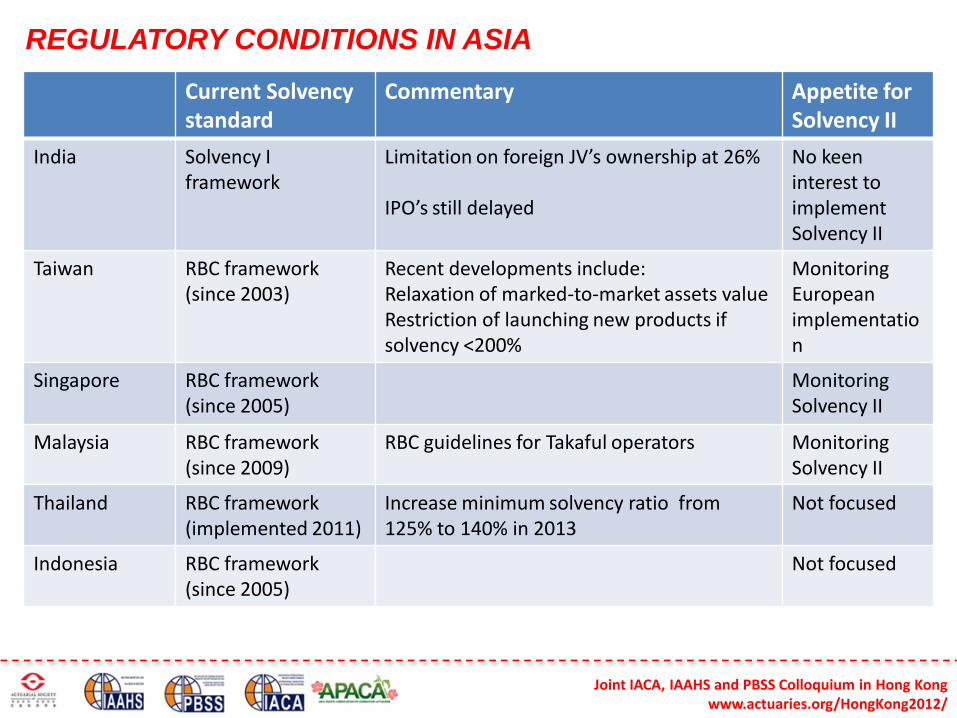

REGULATORY CONDITIONS IN ASIA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Current Solvency standard

Commentary Appetite for Solvency II

India Solvency I framework

Limitation on foreign JV’s ownership at 26% IPO’s still delayed

No keen interest to implement Solvency II

Taiwan RBC framework (since 2003)

Recent developments include: Relaxation of marked-to-market assets value Restriction of launching new products if solvency <200%

Monitoring European implementation

Singapore RBC framework (since 2005)

Monitoring Solvency II

Malaysia RBC framework (since 2009)

RBC guidelines for Takaful operators Monitoring Solvency II

Thailand RBC framework (implemented 2011)

Increase minimum solvency ratio from 125% to 140% in 2013

Not focused

Indonesia RBC framework (since 2005)

Not focused

AGENDA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

1. Motivations of Capital Needs

2. Practical Risk Based Capital Funding Options

3. Types of Reinsurance Solutions

4. Worked Example

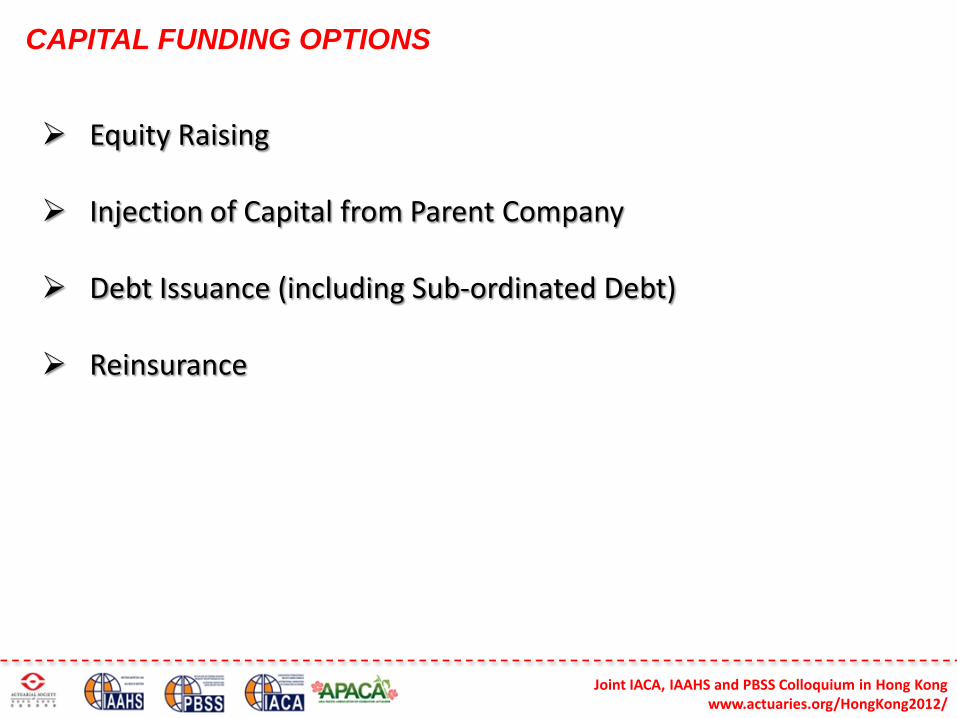

CAPITAL FUNDING OPTIONS

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Equity Raising

Injection of Capital from Parent Company

Debt Issuance (including Sub-ordinated Debt)

Reinsurance

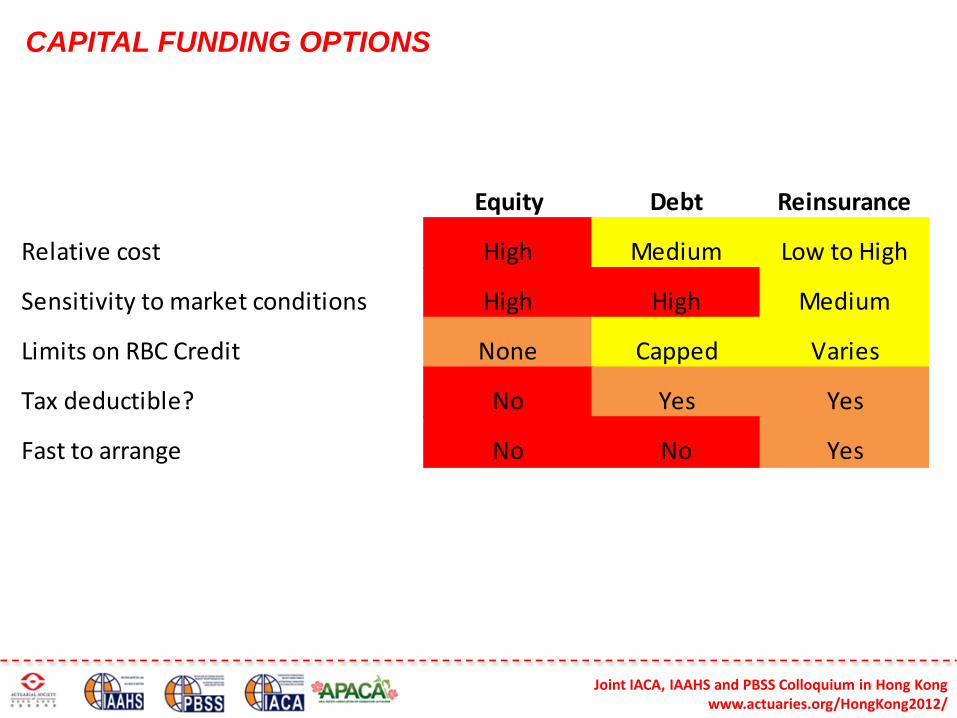

CAPITAL FUNDING OPTIONS

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Equity Debt Reinsurance

Relative cost High Medium Low to High

Sensitivity to market conditions High High Medium

Limits on RBC Credit None Capped Varies

Tax deductible? No Yes Yes

Fast to arrange No No Yes

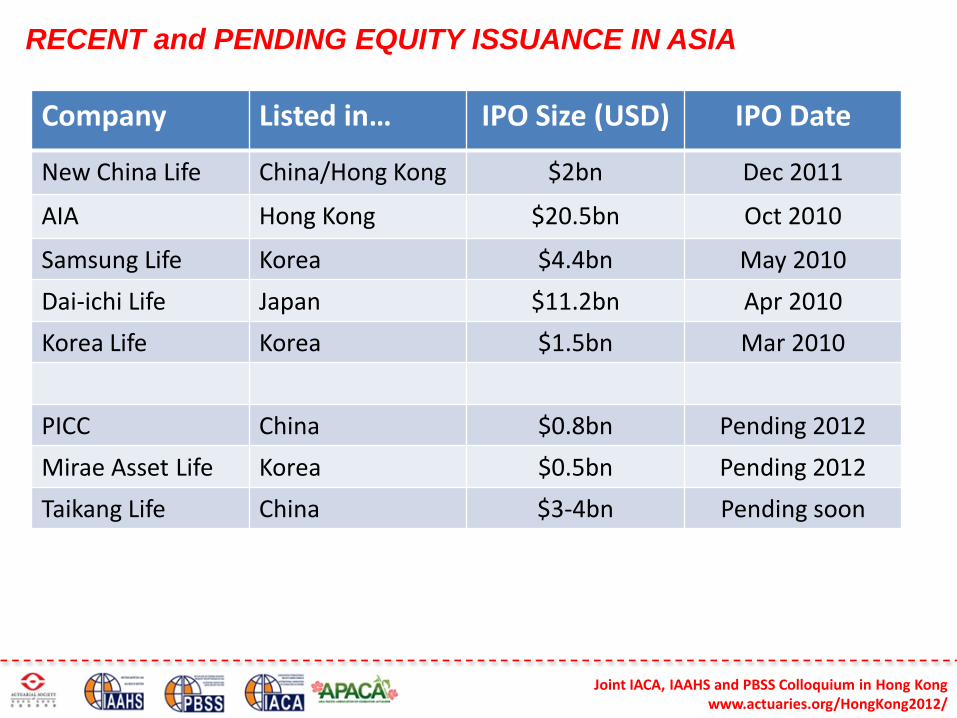

RECENT and PENDING EQUITY ISSUANCE IN ASIA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Company Listed in… IPO Size (USD) IPO Date

New China Life China/Hong Kong $2bn Dec 2011

AIA Hong Kong $20.5bn Oct 2010

Samsung Life Korea $4.4bn May 2010

Dai-ichi Life Japan $11.2bn Apr 2010

Korea Life Korea $1.5bn Mar 2010

PICC China $0.8bn Pending 2012

Mirae Asset Life Korea $0.5bn Pending 2012

Taikang Life China $3-4bn Pending soon

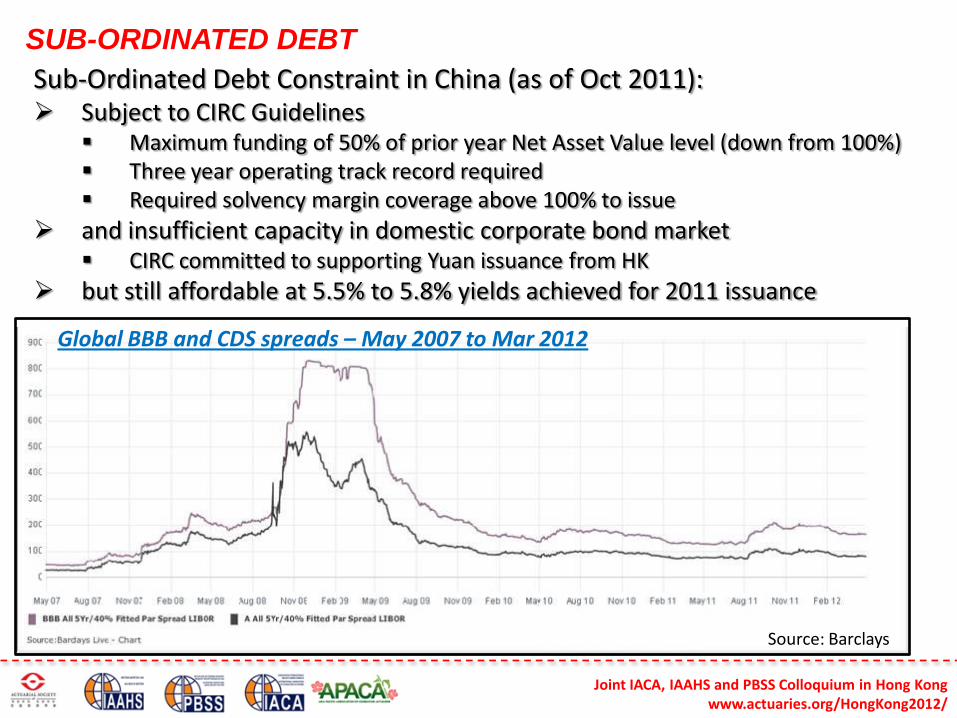

SUB-ORDINATED DEBT

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Sub-Ordinated Debt Constraint in China (as of Oct 2011): Subject to CIRC Guidelines

Maximum funding of 50% of prior year Net Asset Value level (down from 100%) Three year operating track record required Required solvency margin coverage above 100% to issue

and insufficient capacity in domestic corporate bond market CIRC committed to supporting Yuan issuance from HK

but still affordable at 5.5% to 5.8% yields achieved for 2011 issuance

Source: Barclays

Global BBB and CDS spreads – May 2007 to Mar 2012

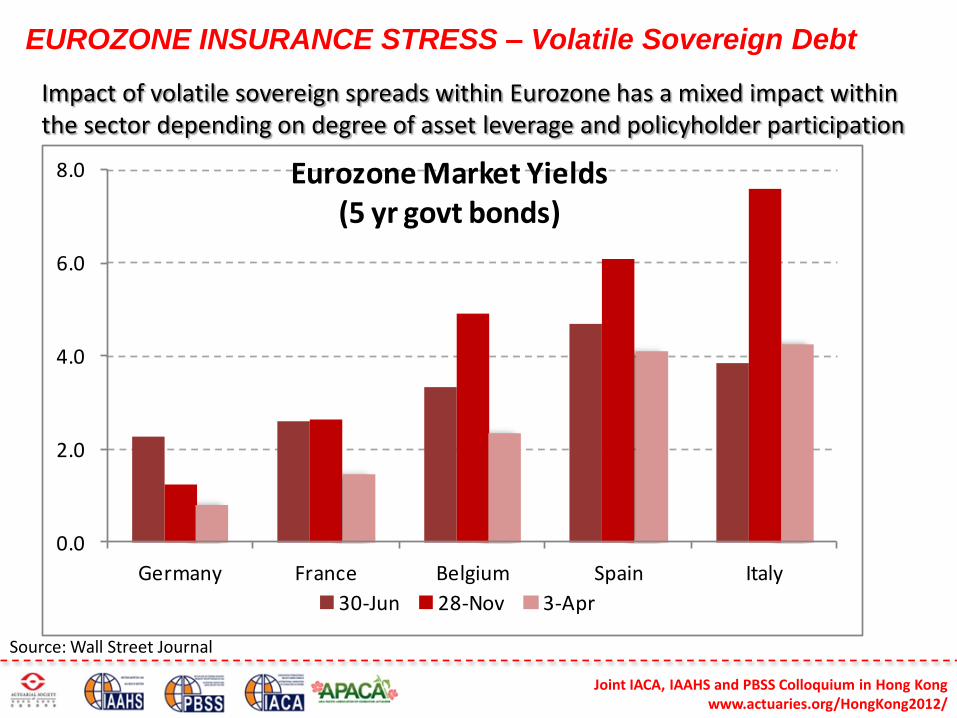

EUROZONE INSURANCE STRESS – Volatile Sovereign Debt

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Impact of volatile sovereign spreads within Eurozone has a mixed impact within the sector depending on degree of asset leverage and policyholder participation

0.0

2.0

4.0

6.0

8.0

Germany France Belgium Spain Italy

Eurozone Market Yields(5 yr govt bonds)

30-Jun 28-Nov 3-Apr

Source: Wall Street Journal

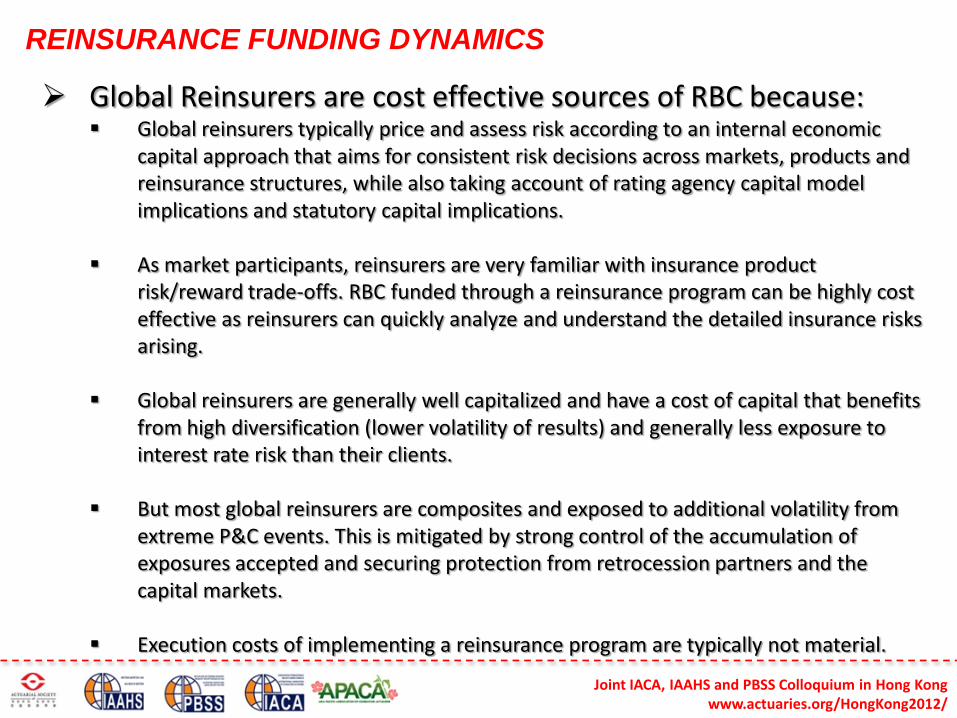

REINSURANCE FUNDING DYNAMICS

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Global Reinsurers are cost effective sources of RBC because: Global reinsurers typically price and assess risk according to an internal economic

capital approach that aims for consistent risk decisions across markets, products and reinsurance structures, while also taking account of rating agency capital model implications and statutory capital implications.

As market participants, reinsurers are very familiar with insurance product risk/reward trade-offs. RBC funded through a reinsurance program can be highly cost effective as reinsurers can quickly analyze and understand the detailed insurance risks arising.

Global reinsurers are generally well capitalized and have a cost of capital that benefits from high diversification (lower volatility of results) and generally less exposure to interest rate risk than their clients.

But most global reinsurers are composites and exposed to additional volatility from extreme P&C events. This is mitigated by strong control of the accumulation of exposures accepted and securing protection from retrocession partners and the capital markets.

Execution costs of implementing a reinsurance program are typically not material.

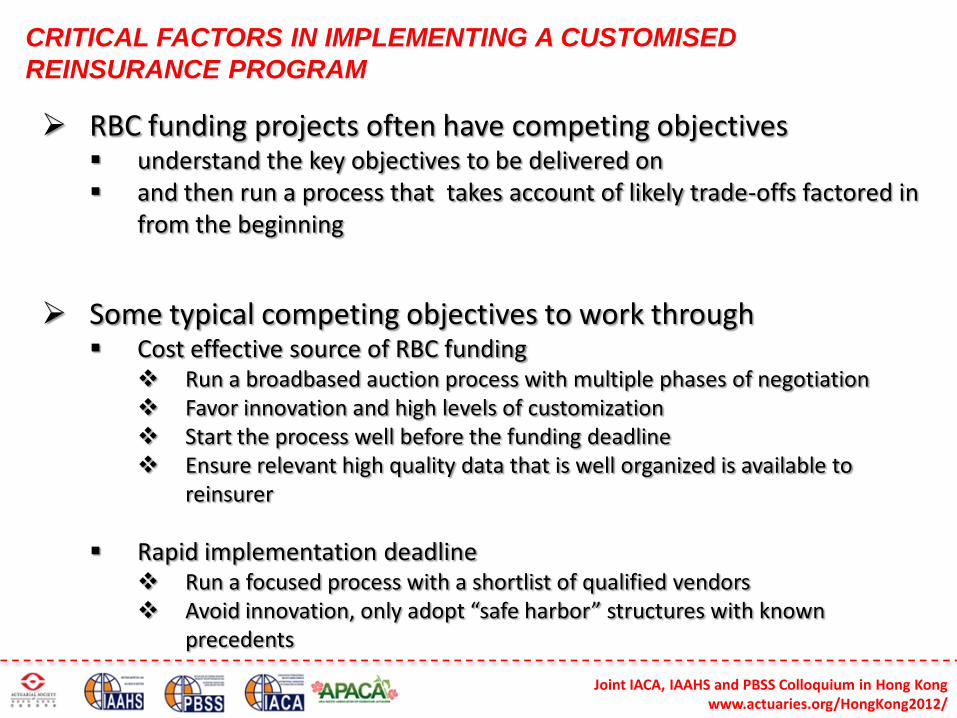

CRITICAL FACTORS IN IMPLEMENTING A CUSTOMISED

REINSURANCE PROGRAM

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

RBC funding projects often have competing objectives understand the key objectives to be delivered on and then run a process that takes account of likely trade-offs factored in

from the beginning

Some typical competing objectives to work through Cost effective source of RBC funding

Run a broadbased auction process with multiple phases of negotiation Favor innovation and high levels of customization Start the process well before the funding deadline Ensure relevant high quality data that is well organized is available to

reinsurer

Rapid implementation deadline Run a focused process with a shortlist of qualified vendors Avoid innovation, only adopt “safe harbor” structures with known

precedents

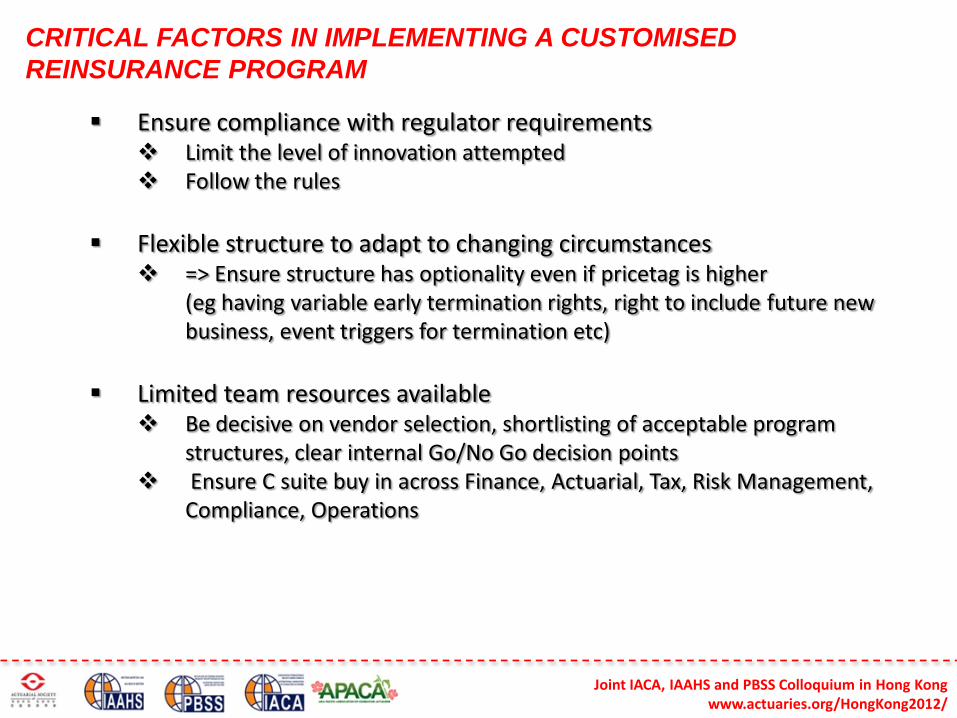

CRITICAL FACTORS IN IMPLEMENTING A CUSTOMISED

REINSURANCE PROGRAM

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Ensure compliance with regulator requirements Limit the level of innovation attempted Follow the rules

Flexible structure to adapt to changing circumstances

=> Ensure structure has optionality even if pricetag is higher (eg having variable early termination rights, right to include future new

business, event triggers for termination etc)

Limited team resources available

Be decisive on vendor selection, shortlisting of acceptable program structures, clear internal Go/No Go decision points

Ensure C suite buy in across Finance, Actuarial, Tax, Risk Management, Compliance, Operations

AGENDA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

1. Motivations of Capital Needs

2. Practical Risk Based Capital Funding Options

3. Types of Reinsurance Solutions

4. Worked Example

TYPES OF REINSURANCE TRANSACTIONS

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Quota share of block of business (inforce and/or new business)

Monetize Embedded Value

Upfront financing solutions

Modified Coinsurance

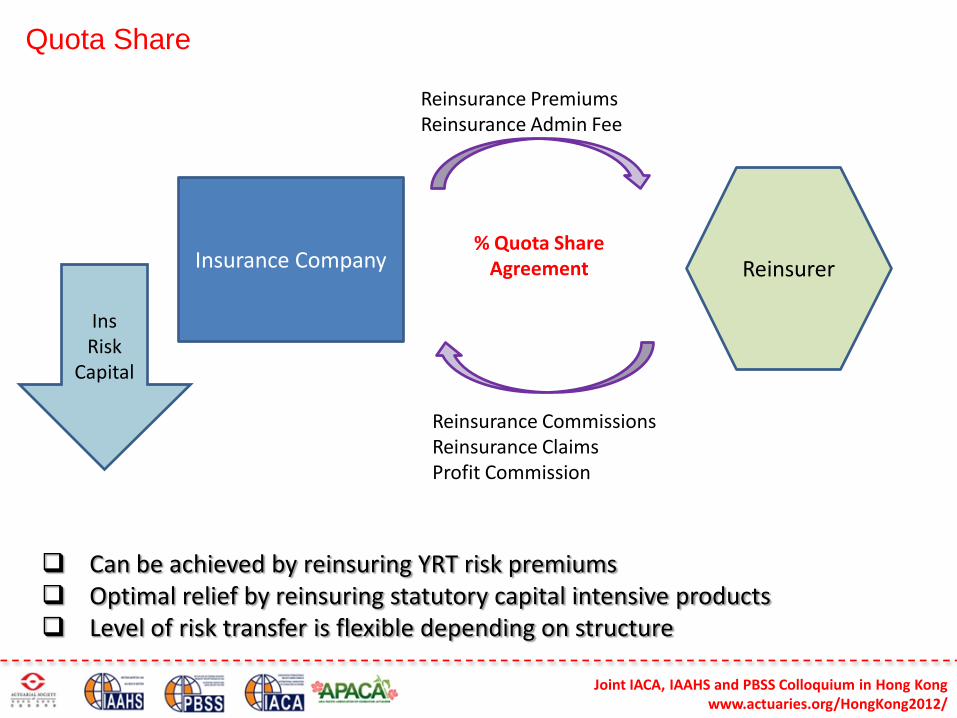

Quota Share

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Can be achieved by reinsuring YRT risk premiums Optimal relief by reinsuring statutory capital intensive products Level of risk transfer is flexible depending on structure

Insurance Company Reinsurer

Reinsurance Premiums Reinsurance Admin Fee

Reinsurance Commissions Reinsurance Claims Profit Commission

% Quota Share Agreement

Ins Risk

Capital

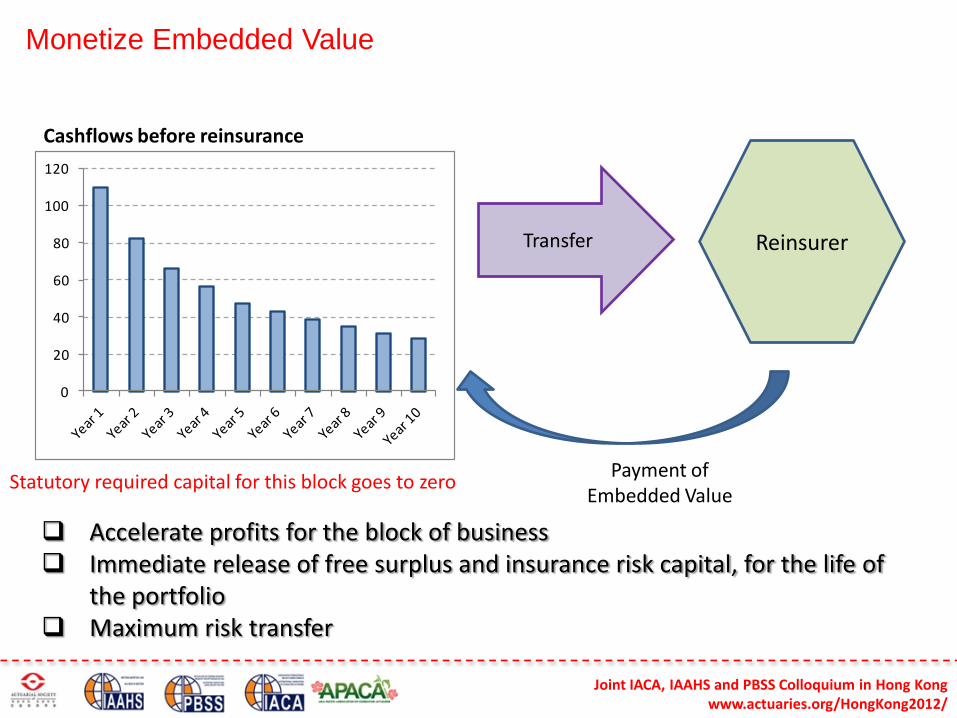

Monetize Embedded Value

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Accelerate profits for the block of business Immediate release of free surplus and insurance risk capital, for the life of

the portfolio Maximum risk transfer

0

20

40

60

80

100

120

Cashflows before reinsurance

Transfer Reinsurer

Payment of Embedded Value

Statutory required capital for this block goes to zero

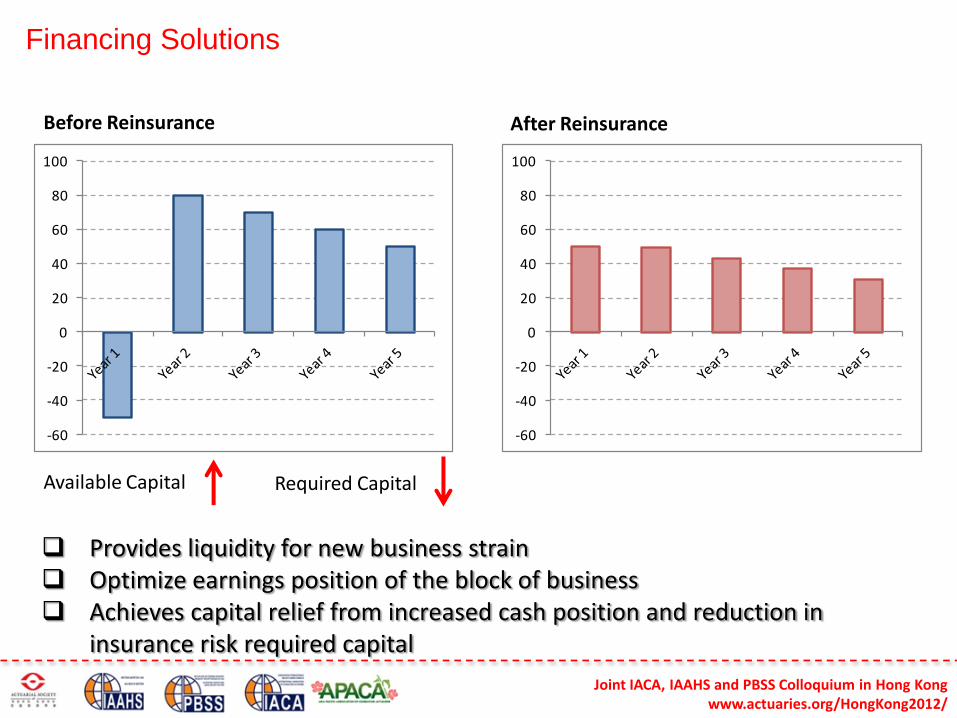

Financing Solutions

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Provides liquidity for new business strain Optimize earnings position of the block of business Achieves capital relief from increased cash position and reduction in

insurance risk required capital

-60

-40

-20

0

20

40

60

80

100

-60

-40

-20

0

20

40

60

80

100

Before Reinsurance After Reinsurance

Available Capital Required Capital

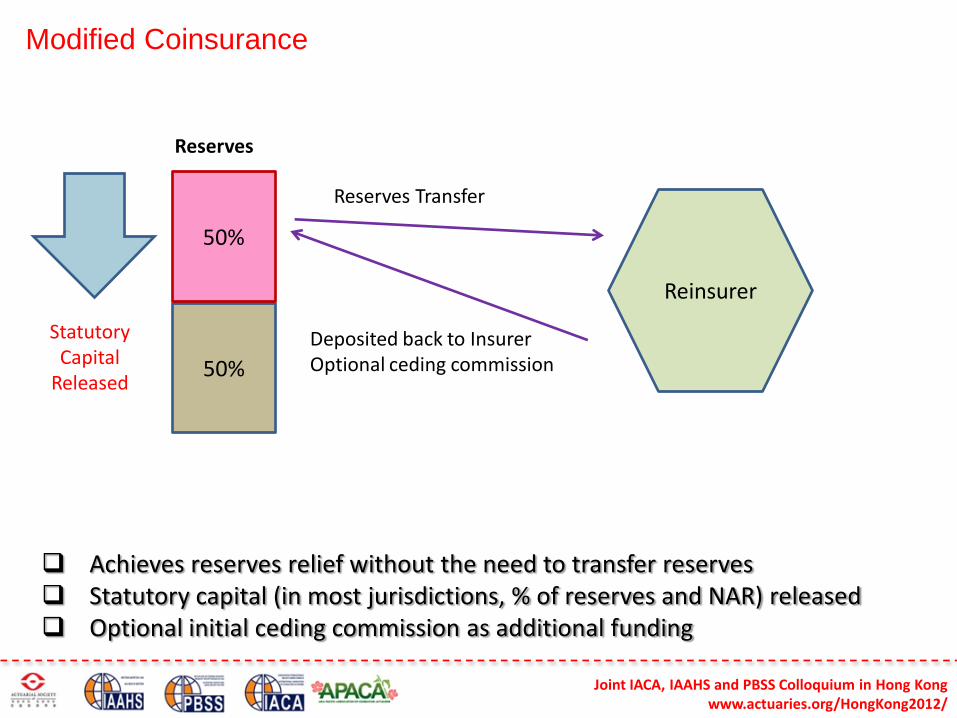

Modified Coinsurance

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Achieves reserves relief without the need to transfer reserves Statutory capital (in most jurisdictions, % of reserves and NAR) released Optional initial ceding commission as additional funding

50%

50%

Reserves

Statutory Capital

Released

Reinsurer

Reserves Transfer

Deposited back to Insurer Optional ceding commission

AGENDA

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

1. Motivations of Capital Needs

2. Practical Risk Based Capital Funding Options

3. Types of Reinsurance Solutions

4. Worked Example

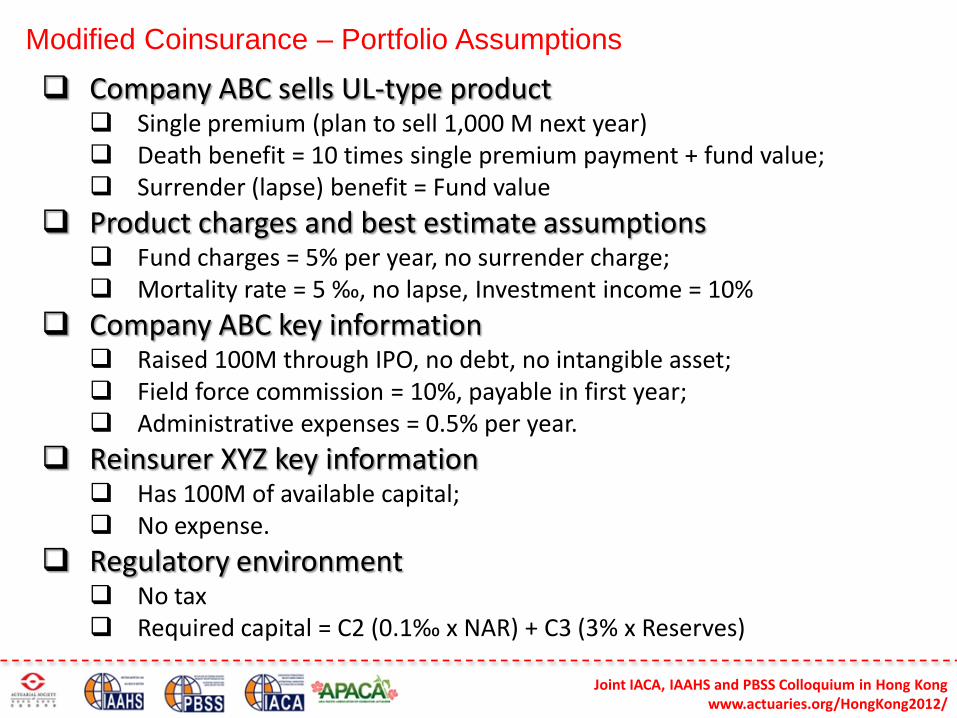

Modified Coinsurance – Portfolio Assumptions

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Company ABC sells UL-type product Single premium (plan to sell 1,000 M next year) Death benefit = 10 times single premium payment + fund value; Surrender (lapse) benefit = Fund value

Product charges and best estimate assumptions Fund charges = 5% per year, no surrender charge; Mortality rate = 5 ‰, no lapse, Investment income = 10%

Company ABC key information Raised 100M through IPO, no debt, no intangible asset; Field force commission = 10%, payable in first year; Administrative expenses = 0.5% per year.

Reinsurer XYZ key information Has 100M of available capital; No expense.

Regulatory environment No tax Required capital = C2 (0.1‰ x NAR) + C3 (3% x Reserves)

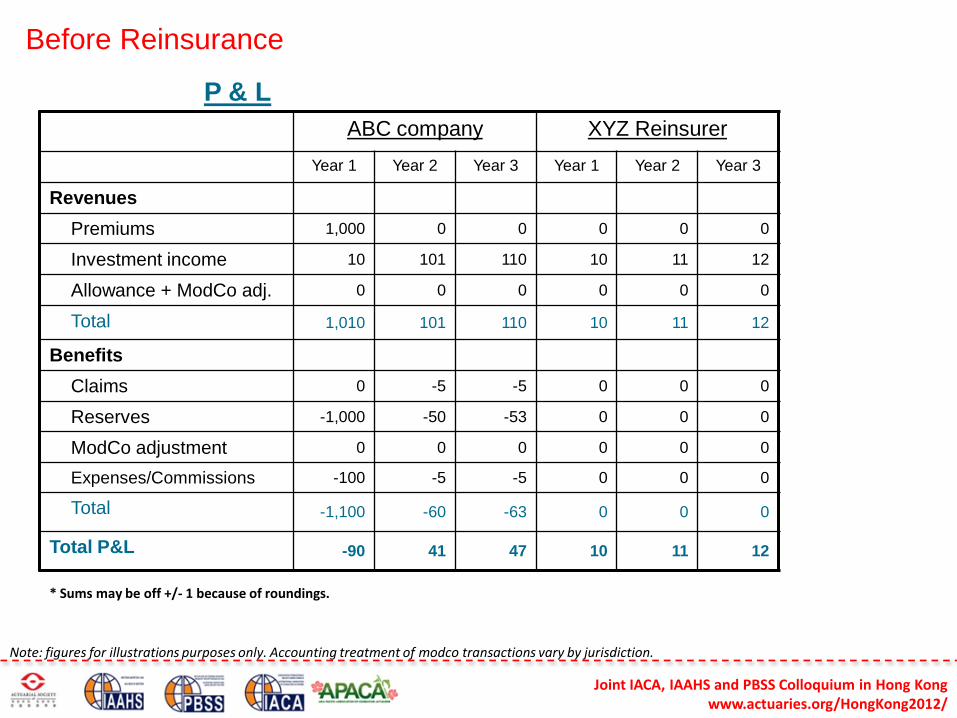

Before Reinsurance

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

P & L

ABC company XYZ Reinsurer

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Revenues

Premiums 1,000 0 0 0 0 0

Investment income 10 101 110 10 11 12

Allowance + ModCo adj. 0 0 0 0 0 0

Total 1,010 101 110 10 11 12

Benefits

Claims 0 -5 -5 0 0 0

Reserves -1,000 -50 -53 0 0 0

ModCo adjustment 0 0 0 0 0 0

Expenses/Commissions -100 -5 -5 0 0 0

Total -1,100 -60 -63 0 0 0

Total P&L -90 41 47 10 11 12

* Sums may be off +/- 1 because of roundings.

Note: figures for illustrations purposes only. Accounting treatment of modco transactions vary by jurisdiction.

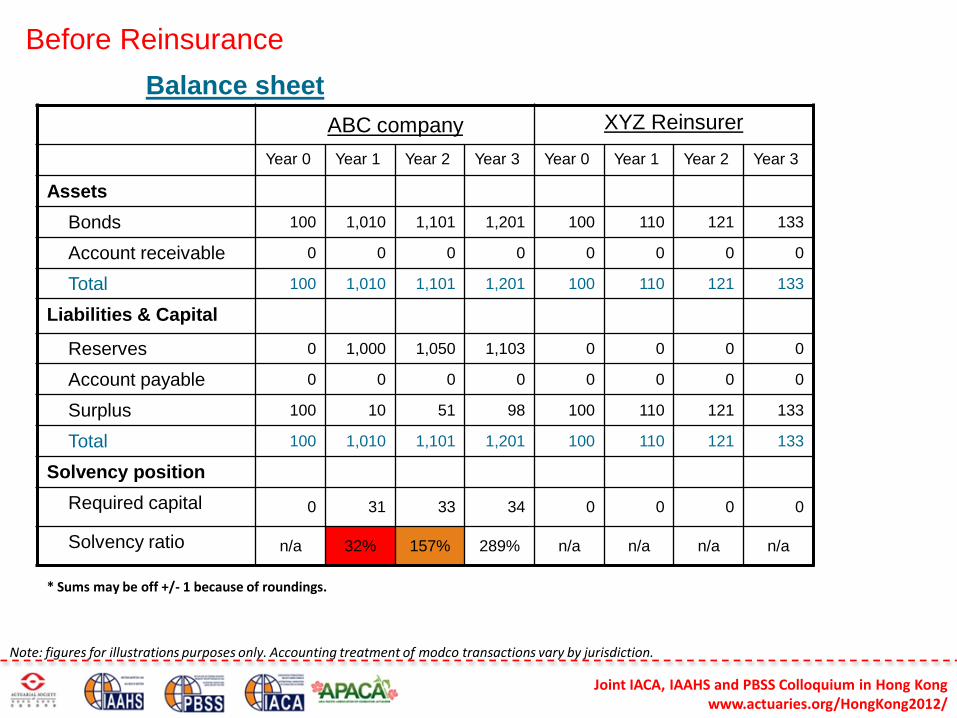

Before Reinsurance

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Balance sheet

ABC company XYZ Reinsurer

Year 0 Year 1 Year 2 Year 3 Year 0 Year 1 Year 2 Year 3

Assets

Bonds 100 1,010 1,101 1,201 100 110 121 133

Account receivable 0 0 0 0 0 0 0 0

Total 100 1,010 1,101 1,201 100 110 121 133

Liabilities & Capital

Reserves 0 1,000 1,050 1,103 0 0 0 0

Account payable 0 0 0 0 0 0 0 0

Surplus 100 10 51 98 100 110 121 133

Total 100 1,010 1,101 1,201 100 110 121 133

Solvency position

Required capital 0 31 33 34 0 0 0 0

Solvency ratio n/a 32% 157% 289% n/a n/a n/a n/a

* Sums may be off +/- 1 because of roundings.

Note: figures for illustrations purposes only. Accounting treatment of modco transactions vary by jurisdiction.

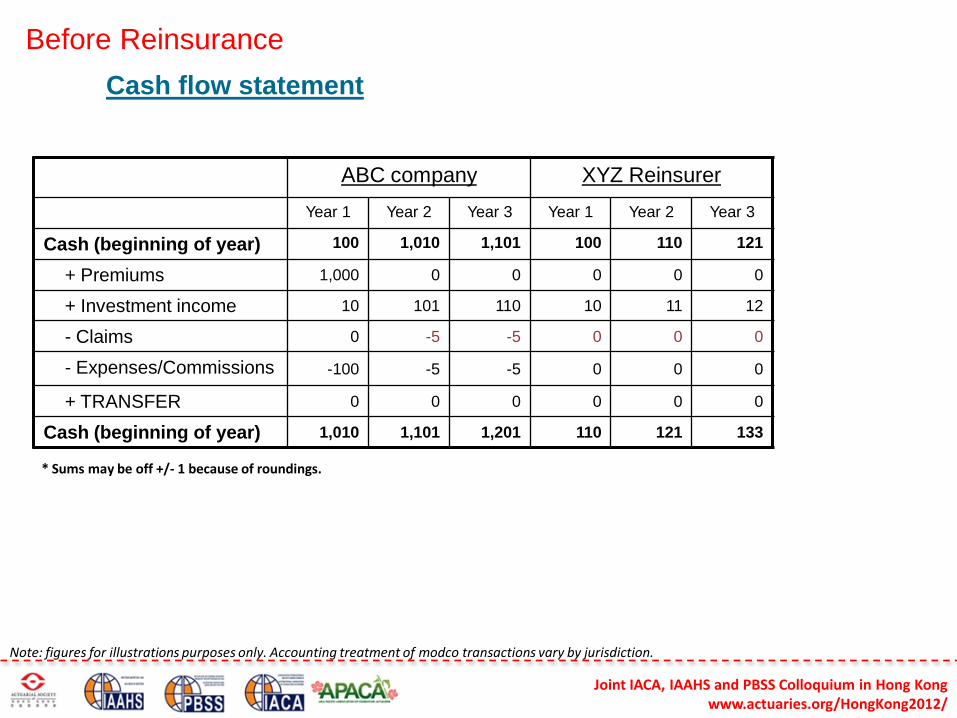

Before Reinsurance

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Cash flow statement

ABC company XYZ Reinsurer

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Cash (beginning of year) 100 1,010 1,101 100 110 121

+ Premiums 1,000 0 0 0 0 0

+ Investment income 10 101 110 10 11 12

- Claims 0 -5 -5 0 0 0

- Expenses/Commissions -100 -5 -5 0 0 0

+ TRANSFER 0 0 0 0 0 0

Cash (beginning of year) 1,010 1,101 1,201 110 121 133

* Sums may be off +/- 1 because of roundings.

Note: figures for illustrations purposes only. Accounting treatment of modco transactions vary by jurisdiction.

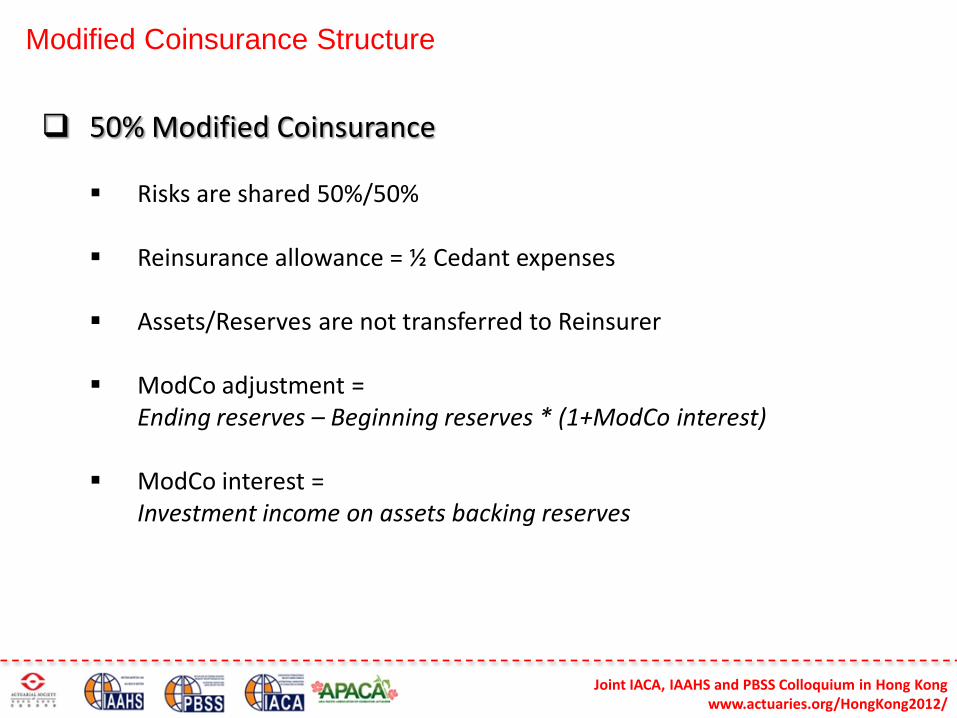

Modified Coinsurance Structure

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

50% Modified Coinsurance

Risks are shared 50%/50%

Reinsurance allowance = ½ Cedant expenses

Assets/Reserves are not transferred to Reinsurer

ModCo adjustment = Ending reserves – Beginning reserves * (1+ModCo interest)

ModCo interest = Investment income on assets backing reserves

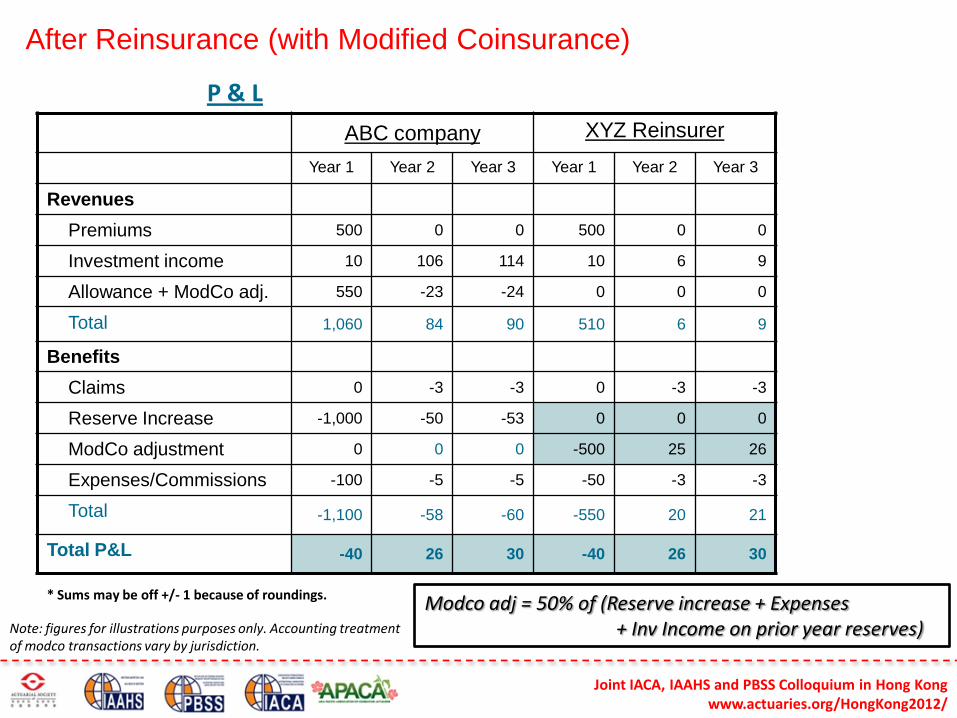

After Reinsurance (with Modified Coinsurance)

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

P & L

ABC company XYZ Reinsurer

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Revenues

Premiums 500 0 0 500 0 0

Investment income 10 106 114 10 6 9

Allowance + ModCo adj. 550 -23 -24 0 0 0

Total 1,060 84 90 510 6 9

Benefits

Claims 0 -3 -3 0 -3 -3

Reserve Increase -1,000 -50 -53 0 0 0

ModCo adjustment 0 0 0 -500 25 26

Expenses/Commissions -100 -5 -5 -50 -3 -3

Total -1,100 -58 -60 -550 20 21

Total P&L -40 26 30 -40 26 30

* Sums may be off +/- 1 because of roundings.

Note: figures for illustrations purposes only. Accounting treatment of modco transactions vary by jurisdiction.

Modco adj = 50% of (Reserve increase + Expenses + Inv Income on prior year reserves)

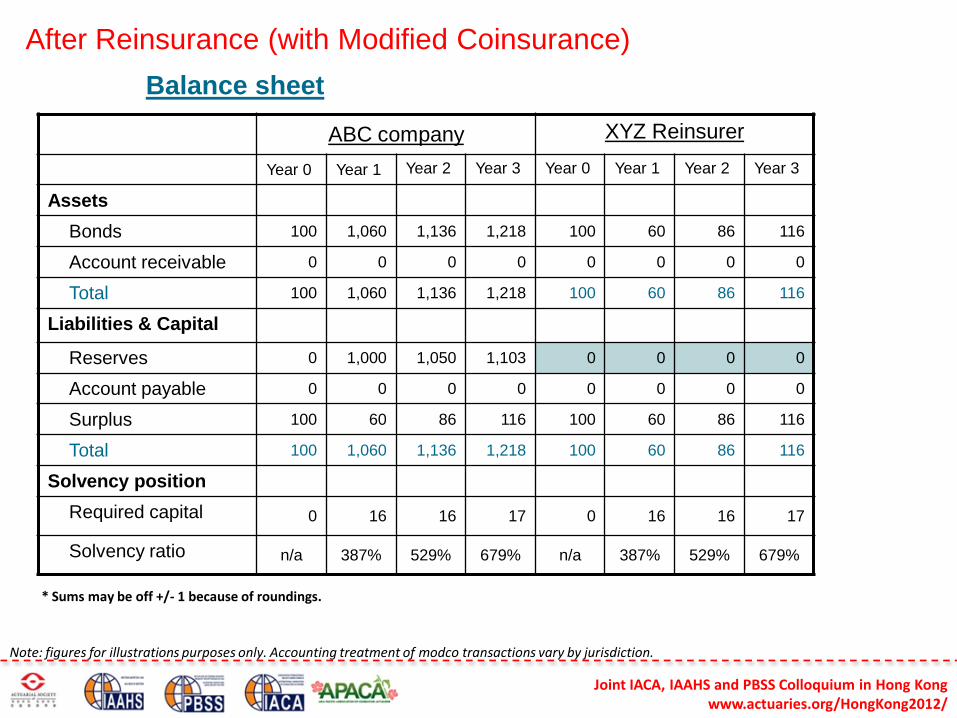

After Reinsurance (with Modified Coinsurance)

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Balance sheet

* Sums may be off +/- 1 because of roundings.

ABC company XYZ Reinsurer

Year 0 Year 1 Year 2 Year 3 Year 0 Year 1 Year 2 Year 3

Assets

Bonds 100 1,060 1,136 1,218 100 60 86 116

Account receivable 0 0 0 0 0 0 0 0

Total 100 1,060 1,136 1,218 100 60 86 116

Liabilities & Capital

Reserves 0 1,000 1,050 1,103 0 0 0 0

Account payable 0 0 0 0 0 0 0 0

Surplus 100 60 86 116 100 60 86 116

Total 100 1,060 1,136 1,218 100 60 86 116

Solvency position

Required capital 0 16 16 17 0 16 16 17

Solvency ratio n/a 387% 529% 679% n/a 387% 529% 679%

Note: figures for illustrations purposes only. Accounting treatment of modco transactions vary by jurisdiction.

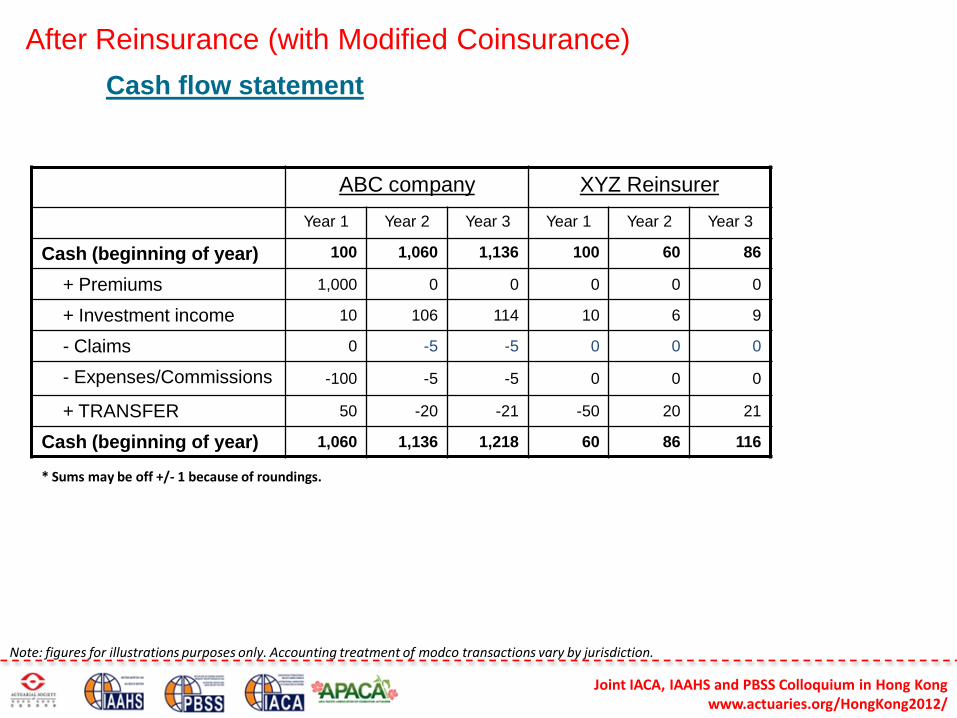

After Reinsurance (with Modified Coinsurance)

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Cash flow statement

* Sums may be off +/- 1 because of roundings.

ABC company XYZ Reinsurer

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Cash (beginning of year) 100 1,060 1,136 100 60 86

+ Premiums 1,000 0 0 0 0 0

+ Investment income 10 106 114 10 6 9

- Claims 0 -5 -5 0 0 0

- Expenses/Commissions -100 -5 -5 0 0 0

+ TRANSFER 50 -20 -21 -50 20 21

Cash (beginning of year) 1,060 1,136 1,218 60 86 116

Note: figures for illustrations purposes only. Accounting treatment of modco transactions vary by jurisdiction.

THANK YOU

Joint IACA, IAAHS and PBSS Colloquium in Hong Kong www.actuaries.org/HongKong2012/

Contact Details: Louis Lee +852 2588 7138 [email protected]