asia pacific aviation · asia pacific aviation opportunities and challenges andrew herdman,...

TRANSCRIPT

1

Asia Pacific Aviation Opportunities and Challenges

Andrew Herdman, Director General3rd Annual Asia Pacific & Middle East Aviation Outlook Summit

Singapore, 9-10 November 2006

Contents Asia Pacific airline industry

AAPA carriers

Chinese carriers

Low-cost carriers

Regulatory Framework

US, EU perspectives

Asia Pacific perspectives

Market outlook

Economic and tourism trends

Traffic outlook

2

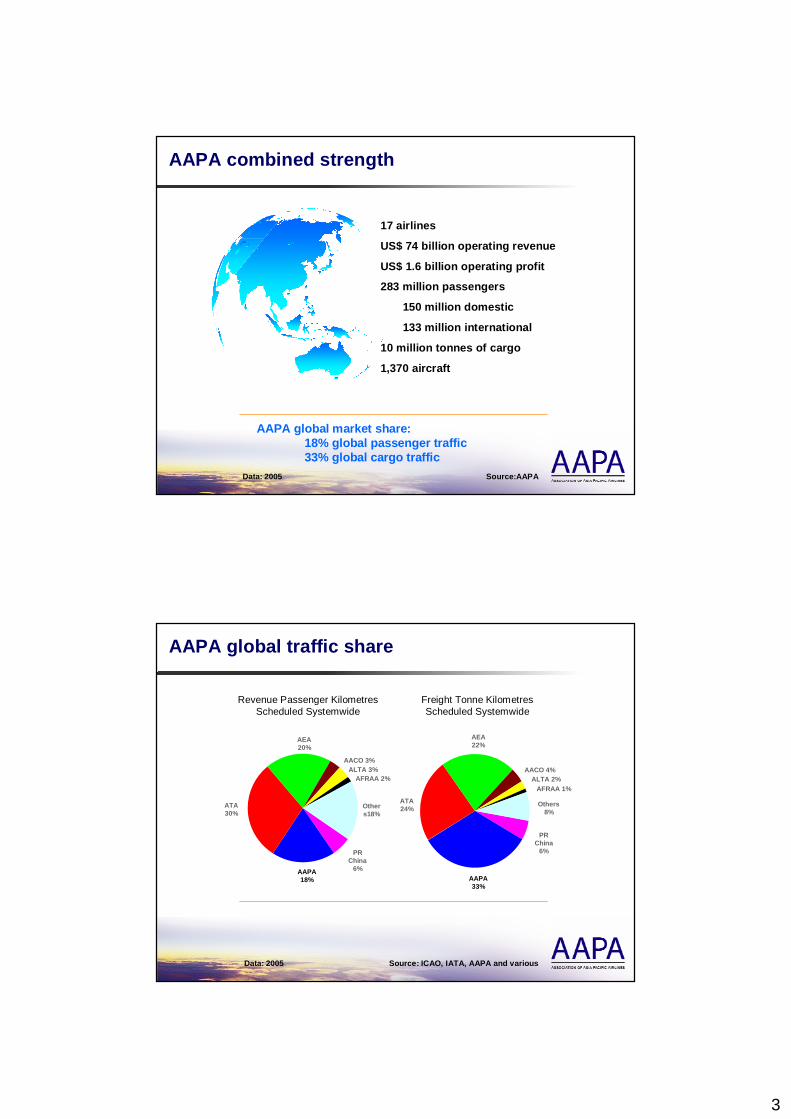

The global airline industry

Source: IATA

US losses slowly reducing

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

2000 2001 2002 2003 2004 2005 2006E

US Europe Asia

$ billion

+$3.7 :Industry profits

Industry losses: -$13.0 -$11.3 -$7.6 -$5.6 -$3.2 -$1.7

Asia Pacific AviationAAPA carriers

3

AAPA combined strength

17 airlines

US$ 74 billion operating revenue

US$ 1.6 billion operating profit

283 million passengers

150 million domestic

133 million international

10 million tonnes of cargo

1,370 aircraft

Data: 2005 Source:AAPA

AAPA global market share: 18% global passenger traffic 33% global cargo traffic

AAPA global traffic share

Data: 2005 Source: ICAO, IATA, AAPA and various

AFRAA 2%

AAPA 18%

ATA 30%

AEA 20%

AACO 3%ALTA 3%

Others18%

PR China

6%

Freight Tonne Kilometres Scheduled Systemwide

ATA 24%

AEA 22%

AACO 4%ALTA 2%

AFRAA 1%

Others 8%

PR China

6%

AAPA 33%

Revenue Passenger Kilometres Scheduled Systemwide

4

AAPA financial results for FY2006

FY2006 = April 2005 to March 2006 Source: AAPA

- 69%1.1Net Income

-2.2%Operating margin

+ 12%72.1Total op. expenses

-1.5%Net margin

- 59%1.6Operating Profit

+ 8%73.7Total op. revenue

+ 5%10.0Other revenue

+ 11%13.1Cargo revenue

+ 8%50.6Passenger revenue

% ChgUS$ billionFY2006

Falling margins as yields fail to keep pace with rising fuel costs

AAPA revenue trends

FY1997-2004 exclude KA and NZ, FY2005-2006 exclude KA Source: AAPA

Robust revenue growth in FY2006

$0

$10

$20

$30

$40

$50

$60

$70

FY1997 FY1998 FY1999 FY2000 FY2001 FY2002 FY2003 FY2004 FY2005 FY2006

US billion

CG

O

18%

PAX

reve

nue:

69%

of to

tal r

even

ue

PAX

reve

nue:

77%

of to

tal r

even

ue

CG

O

15%

5

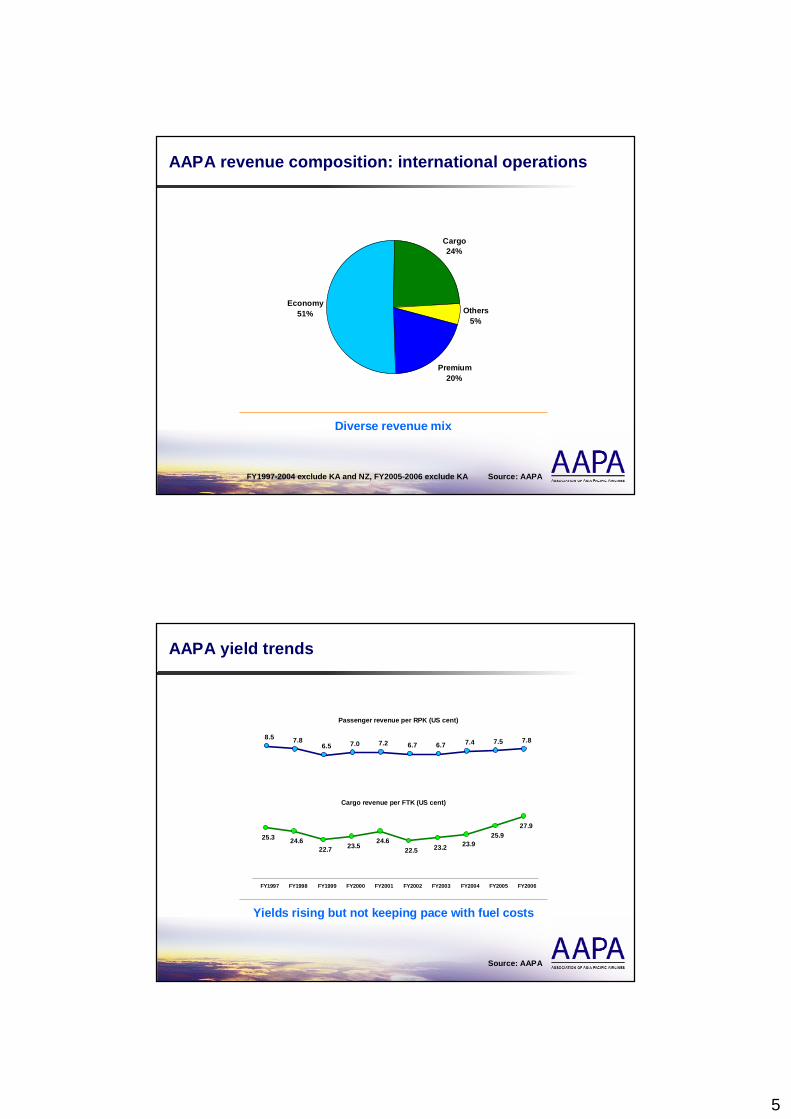

AAPA revenue composition: international operations

FY1997-2004 exclude KA and NZ, FY2005-2006 exclude KA Source: AAPA

Diverse revenue mix

Premium20%

Economy51%

Cargo24%

Others5%

AAPA yield trends

Source: AAPA

Yields rising but not keeping pace with fuel costs

FY1997 FY1998 FY1999 FY2000 FY2001 FY2002 FY2003 FY2004 FY2005 FY2006

8.5 7.86.5 7.0 7.2 6.7 6.7 7.4 7.5 7.8

Passenger revenue per RPK (US cent)

25.3 24.622.7 23.5

24.622.5 23.2 23.9

25.927.9

Cargo revenue per FTK (US cent)

6

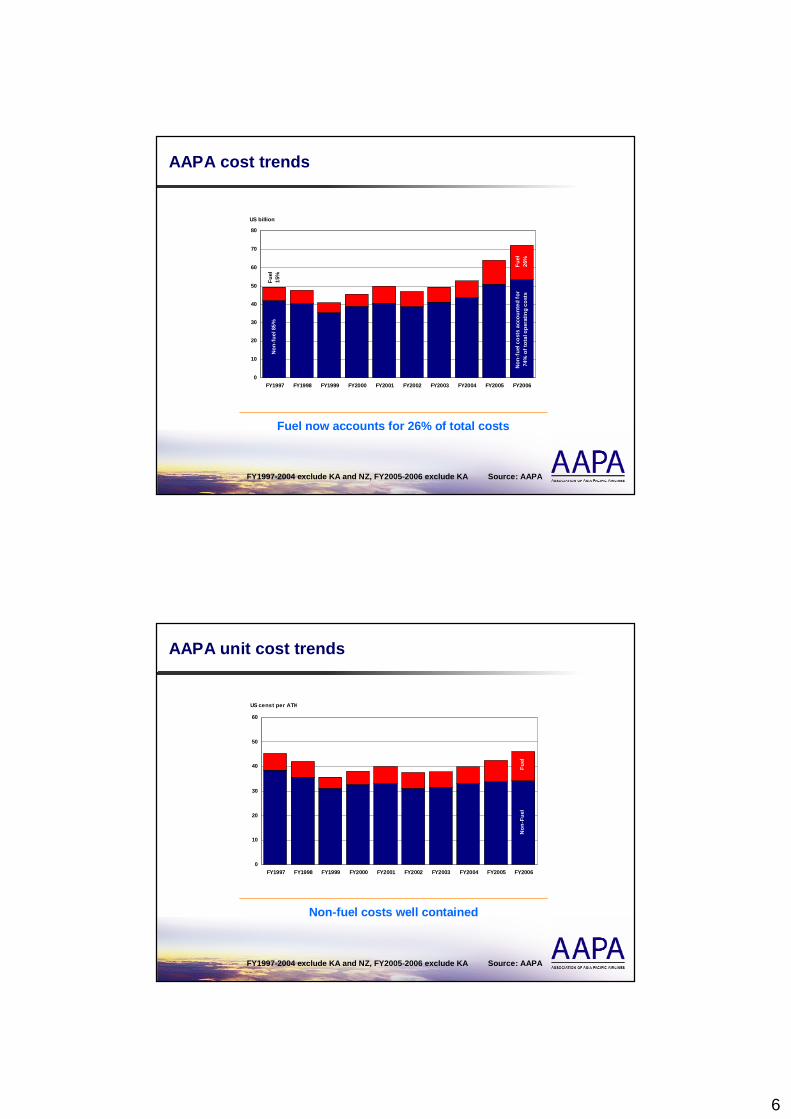

AAPA cost trends

FY1997-2004 exclude KA and NZ, FY2005-2006 exclude KA Source: AAPA

Fuel now accounts for 26% of total costs

0

10

20

30

40

50

60

70

80

FY1997 FY1998 FY1999 FY2000 FY2001 FY2002 FY2003 FY2004 FY2005 FY2006

US billion

Non

-fue

l cos

ts a

ccou

nted

for

74%

of t

otal

ope

ratin

g co

sts

Fuel

26

%

Fuel

15

%N

on-f

uel 8

5%

AAPA unit cost trends

Non-fuel costs well contained

FY1997-2004 exclude KA and NZ, FY2005-2006 exclude KA Source: AAPA

0

10

20

30

40

50

60

FY1997 FY1998 FY1999 FY2000 FY2001 FY2002 FY2003 FY2004 FY2005 FY2006

US censt per ATK

Non

-Fue

lFu

el

7

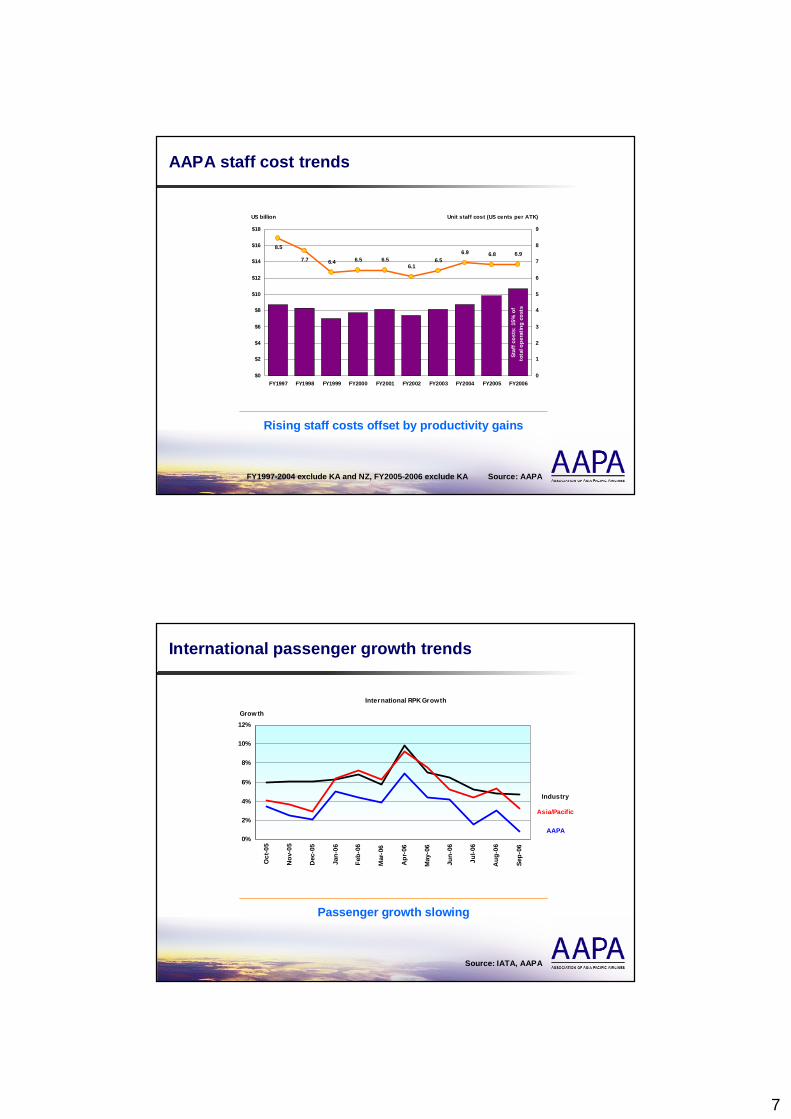

AAPA staff cost trends

Rising staff costs offset by productivity gains

FY1997-2004 exclude KA and NZ, FY2005-2006 exclude KA Source: AAPA

6.4 6.5 6.56.1

6.56.9 6.8 6.9

7.7

8.5

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

FY1997 FY1998 FY1999 FY2000 FY2001 FY2002 FY2003 FY2004 FY2005 FY20060

1

2

3

4

5

6

7

8

9

US billion Unit staff cost (US cents per ATK)

Staf

f cos

ts: 1

5% o

f to

tal o

pera

ting

cost

s

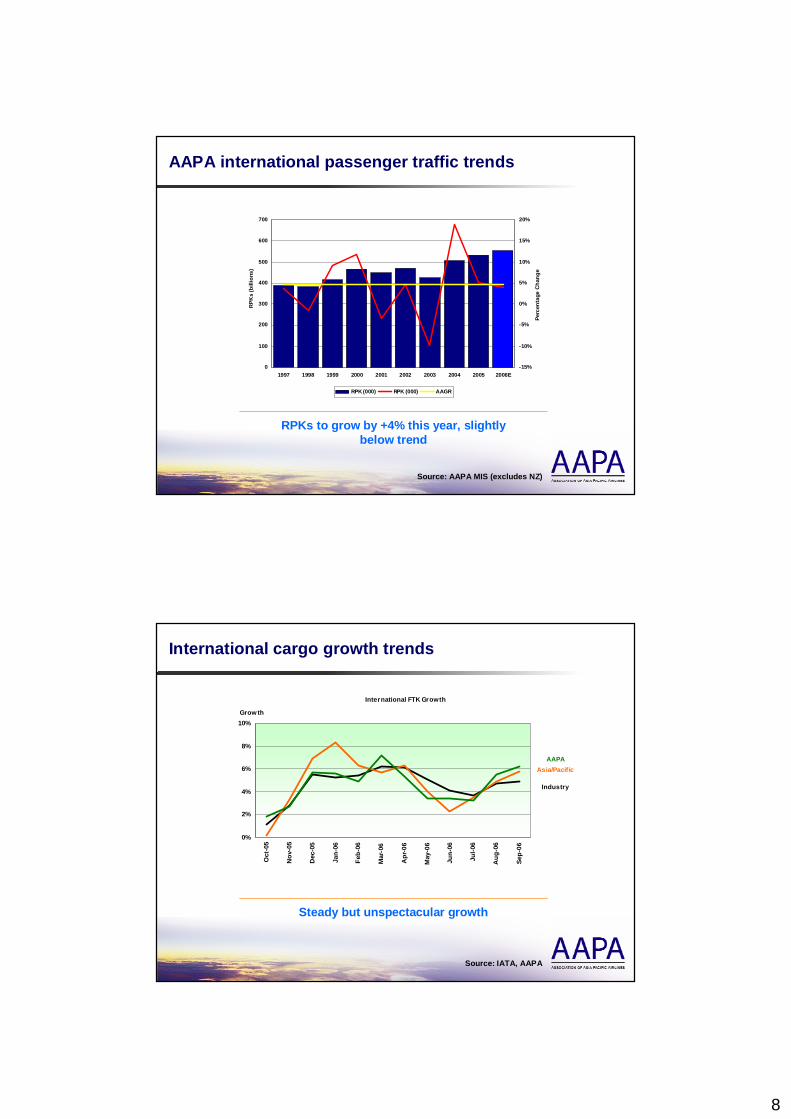

International passenger growth trends

Source: IATA, AAPA

Passenger growth slowing

International RPK Growth

0%

2%

4%

6%

8%

10%

12%

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Feb-

06

Mar

-06

Apr

-06

May

-06

Jun-

06

Jul-0

6

Aug

-06

Sep-

06

Grow th

Industry

Asia/Pacific

AAPA

8

AAPA international passenger traffic trends

Source: AAPA MIS (excludes NZ)

RPKs to grow by +4% this year, slightly below trend

0

100

200

300

400

500

600

700

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006E

RPK

s (b

illio

ns)

-15%

-10%

-5%

0%

5%

10%

15%

20%

Perc

enta

ge C

hang

e

RPK (000) RPK (000) AAGR

International cargo growth trends

Source: IATA, AAPA

Steady but unspectacular growth

International FTK Growth

0%

2%

4%

6%

8%

10%

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Feb-

06

Mar

-06

Apr

-06

May

-06

Jun-

06

Jul-0

6

Aug

-06

Sep-

06

Grow th

Industry

Asia/PacificAAPA

9

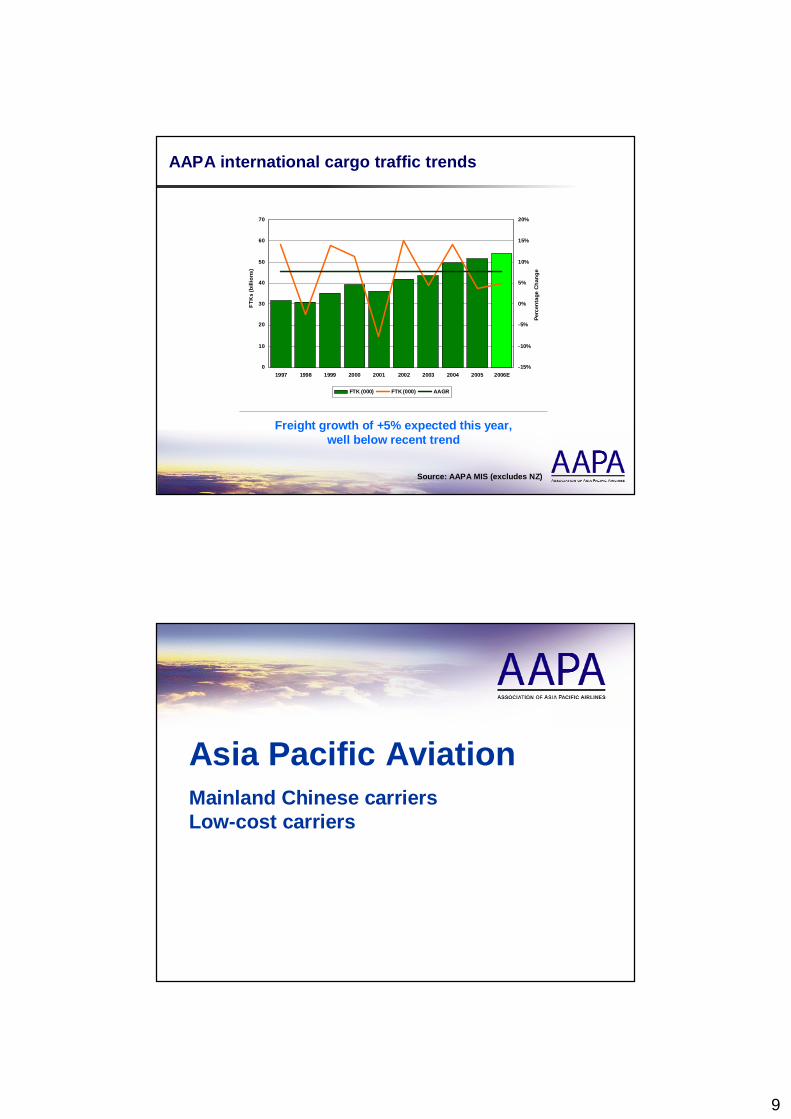

AAPA international cargo traffic trends

Freight growth of +5% expected this year, well below recent trend

Source: AAPA MIS (excludes NZ)

0

10

20

30

40

50

60

70

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006E

FTK

s (b

illio

ns)

-15%

-10%

-5%

0%

5%

10%

15%

20%

Perc

enta

ge C

hang

e

FTK (000) FTK (000) AAGR

Asia Pacific AviationMainland Chinese carriers Low-cost carriers

10

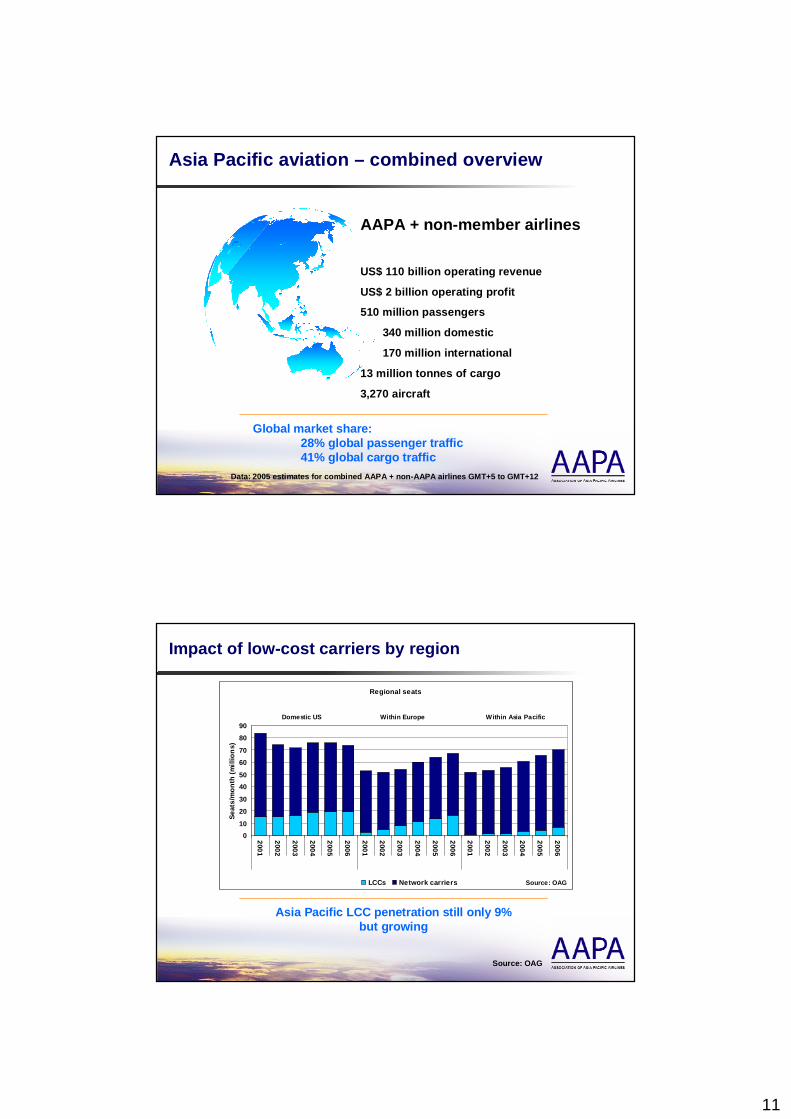

Chinese carriers

Source: ATI

Chinese airlines profitability improving

US$ 58 m- US$ 230 m

- US$ 123 m- US$ 58 m

US$ 426 mUS$ 300 m

Jan-Sep 20062005Profitability

Quoted Asia Pacific LCCs

* FY2006 = July 2005 to June 2006 Source: ATI

18-mth to Sep05

9-mth to Jun06

US$ 130 mUS$ 2.0 b

US$ 65 mUS$ 1.1 b

ProfitRevenue

FY 2005

FY2006*

US$ 31 mUS$ 184 m

US$ 35 mUS$ 236 m

ProfitRevenue

11

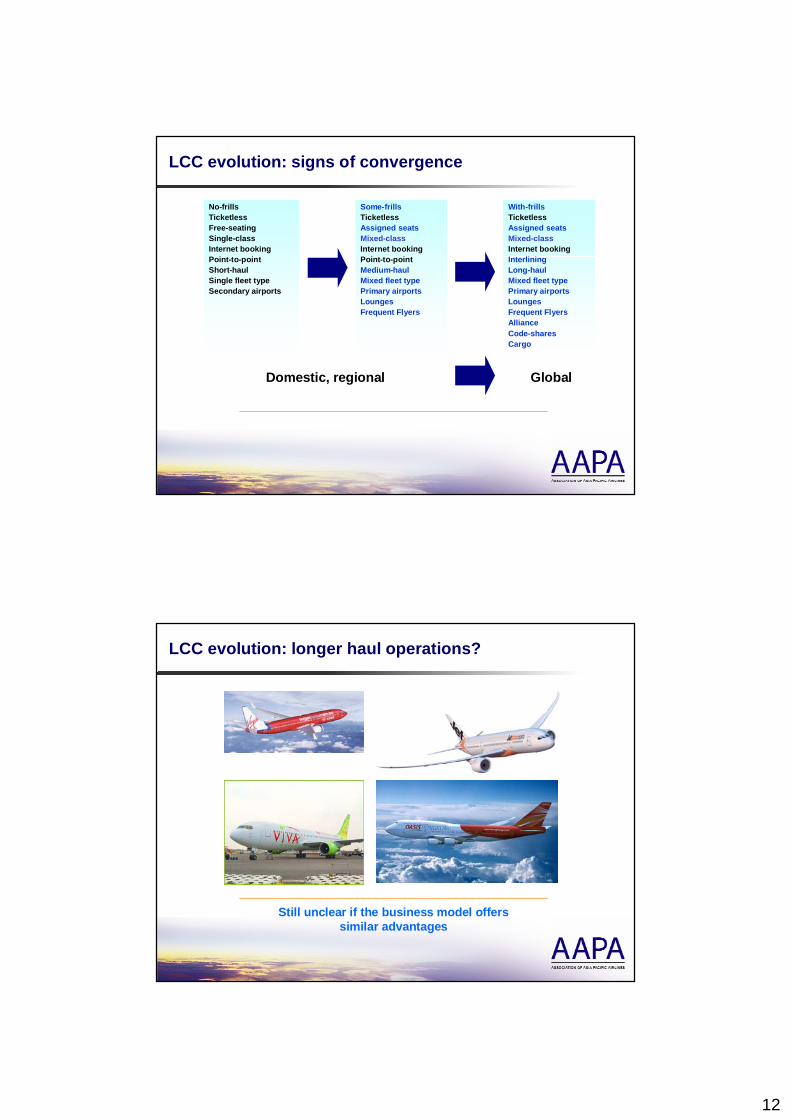

Asia Pacific aviation – combined overview

AAPA + non-member airlines

US$ 110 billion operating revenue

US$ 2 billion operating profit

510 million passengers

340 million domestic

170 million international

13 million tonnes of cargo

3,270 aircraft

Global market share: 28% global passenger traffic 41% global cargo traffic

Data: 2005 estimates for combined AAPA + non-AAPA airlines GMT+5 to GMT+12

Impact of low-cost carriers by region

Source: OAG

Asia Pacific LCC penetration still only 9% but growing

Regional seats

010

20

30

4050

60

70

80

90

2001

2002

2003

2004

2005

2006

2001

2002

2003

2004

2005

2006

2001

2002

2003

2004

2005

2006

Domestic US Within Europe Within Asia Pacific

Seat

s/m

onth

(mill

ions

)

LCCs Network carriers Source: OAG

Domestic US Within Asia PacificWithin Europe

12

LCC evolution: signs of convergence

No-frillsTicketlessFree-seatingSingle-class Internet bookingPoint-to-pointShort-haulSingle fleet typeSecondary airports

With-frillsTicketlessAssigned seatsMixed-classInternet bookingInterliningLong-haulMixed fleet typePrimary airportsLoungesFrequent FlyersAlliance Code-sharesCargo

Some-frillsTicketlessAssigned seatsMixed-classInternet bookingPoint-to-pointMedium-haulMixed fleet typePrimary airportsLoungesFrequent Flyers

GlobalDomestic, regional

Still unclear if the business model offers similar advantages

LCC evolution: longer haul operations?

13

Regulatory framework

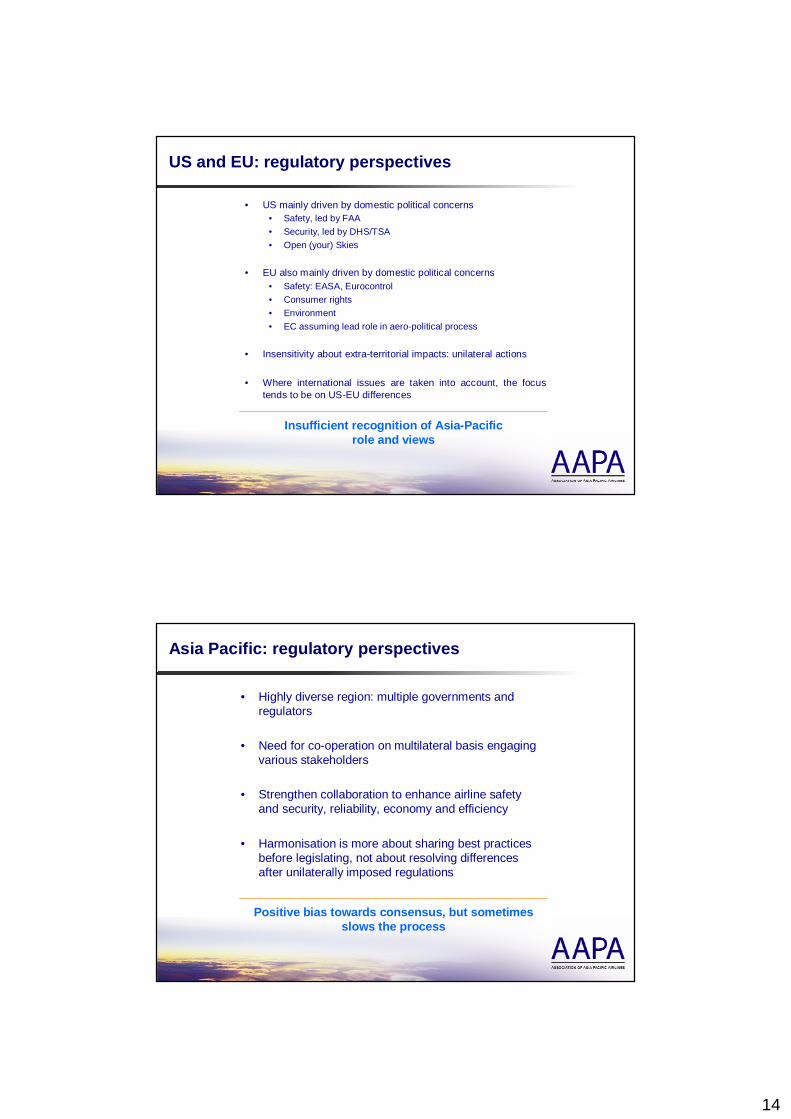

Wider impact of US and EU regulations: need for better global harmonisation

Global regulatory influences

Asia Pacific

14

Insufficient recognition of Asia-Pacific role and views

US and EU: regulatory perspectives

• US mainly driven by domestic political concerns• Safety, led by FAA• Security, led by DHS/TSA • Open (your) Skies

• EU also mainly driven by domestic political concerns• Safety: EASA, Eurocontrol • Consumer rights• Environment• EC assuming lead role in aero-political process

• Insensitivity about extra-territorial impacts: unilateral actions

• Where international issues are taken into account, the focus tends to be on US-EU differences

Positive bias towards consensus, but sometimes slows the process

Asia Pacific: regulatory perspectives

• Highly diverse region: multiple governments and regulators

• Need for co-operation on multilateral basis engaging various stakeholders

• Strengthen collaboration to enhance airline safety and security, reliability, economy and efficiency

• Harmonisation is more about sharing best practices before legislating, not about resolving differences after unilaterally imposed regulations

15

Working together

Industry Partners

Regulators Airlines

Associations

Need to ensure that the evolution of the regulatory framework keeps pace with industry needs

Aviation: aeropolitical regulations

• Still governed by an outdated bilateral framework

• National ownership and control restrictions

• Holds back consolidation

• Progressive liberalisation, but protectionist sentiments often still evident

• Affects all airlines, both established carriers and new entrants

16

Market outlook

Economic trends

Source: IMF

IMF forecast global growth of +4.9% and Asia +7.1% in 2007

• Growth in Asia this year remains robust, especially in China and India

• Japan’s recovery boosts imports from Asia

• Inflation in the region well contained, despite higher oil prices

• Investors positive on regional fundamentals

• Outlook for exports positive, but expected to moderate in 2007 in line with the slowdown in the US

17

Tourism trends

Source: UNWTO

• Worldwide arrivals +5.5% to over 800 million

• Annual growth rate +6.5%• Asia Pacific +13%

Global tourism to grow 4-5% in 2006 Asia Pacific +9%

Traffic outlook: 2005-2009

Source: IATA

Intra Asia Pacific growth expected to remain strong

AAGR 2005-09

Passenger Freight

North Atlantic 5.3% 4.6%

Trans Pacific 5.8% 6.0%

Within Europe 5.1% 4.1%

Within Asia Pacific 6.8% 8.5%

Europe to Asia Pacific 5.9% 5.7%

Europe to Africa 5.7% 4.5%

Middle East to Europe 6.6% 5.1%

Middle East to Asia Pacific 6.7% 8.8%

North America to Latin America 4.6% 3.7%

Within Latin America 4.2% 5.0%

All International Routes 5.6% 6.3%

18

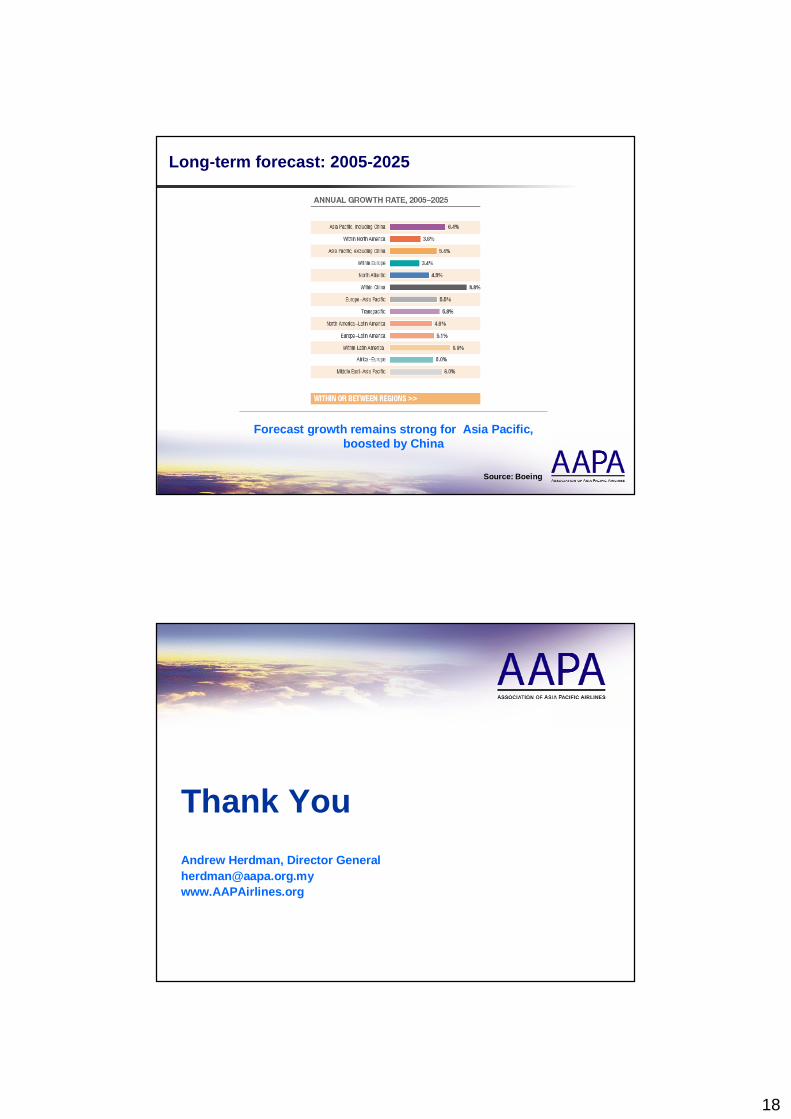

Long-term forecast: 2005-2025

Source: Boeing

Forecast growth remains strong for Asia Pacific, boosted by China

Thank YouAndrew Herdman, Director General [email protected] www.AAPAirlines.org