ap automation: why initiatives fail and best practices for ... · best practices for achieving...

TRANSCRIPT

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

Sponsored byAn AP & P2P white paper

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

2

Executive SummaryAccounts Payable is responsible for paying the supplier accurately and on time but does not have the ability to approve invoices and must rely on those who procure the goods/services to validate the charges before payment can be processed. Many organizations have a negative view of AP and traditionally view it as overhead. AP consistently hears: “You people never pay the supplier on-time”. AP is often viewed as a department that only pays invoices and is perceived to be out-of-control and never meets expectations. The CFO wonders, “How hard can it be to ‘just’ pay invoices?” and, as a result, the only communication that AP receives from the CFO is a directive for them to reduce processing costs.

AP has reacted to that directive by attempting (but generally failing) to implement best practices. These initiatives are typically not successful, and may have failed for one or more of the following reasons:

• AP is the last step of a very chaotic purchasing process.

• AP does not have ownership of the process.

• Procurement & AP have an at-arm’s-length, or even adversarial, relationship.

• AP is not aligned with the business.

• The solution didn’t solve the real issue because AP reacted to noise rather than root cause analysis and metrics.

• The proposed solution was hard to use or didn’t perform as expected.

• AP was working on too many disjointed best practice projects all at once.

• AP has not been groomed to lead a cross-functional project of this scale.

Defining the ProblemMost companies procure goods and services under two categories:

1. Inventory, which is well controlled by a purchase order and receipt of goods. AP receives the invoice directly from the supplier, matches to the PO and receipt, and payment is made on time. This usually accounts for 20% of the invoice volume.

2. Non-Inventory, which can be purchased by anyone in the organization, who can order whatever they want, whenever they want, at whatever price, and shipped mostly by overnight carrier. No one in the organization knows these orders were placed until a phone call comes into the company about a past due invoice. AP requests a copy of the invoice and the search begins for who purchased the items, seeking budget approvals and validation that the items were received in good order. Non-inventory is about 80% of invoice volume. (The percentage of PO vs NonPO varies within companies.)

I N V E N TO RY N O N - I N V E N TO RY

Inventory usually accounts for 20% of invoice volume. Non-inventory is about 80% of invoice volume.

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

3

The point is that Non-PO invoices, which are uncontrolled spend, trigger the series of events that gives AP their poor reputation. Non-PO invoices can also have a negative effect on the budget, cash management operations, and have a higher risk of being in direct violation of laws and regulations. (OFAC, 1099/1042, Sales & Use Tax, etc.)

Since AP has no control over the purchasing process, any and all attempts to improve the process are often faced with great resistance, which makes acquiring a budget to implement best practices and technology difficult, if not impossible.

You can’t see the forest for the trees.Driven by the directive from their CFO, AP focuses on fixing all the ills of the chaotic purchasing process (the trees) so they can pay invoices timely and accurately. This approach has not been successful because it focuses on the symptoms of a poor process and not the underlying problem. An approach that has worked for best-in-class benchmark companies is to align across the finance organization and develop a holistic end-to-end AP process including supplier setup, invoicing, payments, and reporting. This is the forest, the bigger picture: from “thought of need” through settlement. This comprehensive approach considers the questions: What are the needs of the organization? Are these suppliers legitimate? What technologies can be implemented to communicate with those suppliers effectively and efficiently? Are the transactions compliant with laws and regulations? What is the best method of payment? Is the process cost effective and are internal controls over the entire process to prevent fraud?

The path to success must start by educating the organization with metrics on how their purchasing habits affect the company’s profit margin and their reputation with suppliers. AP must understand that the CFO is focused on reducing cost because they are far removed from the process and don’t understand that the process is chaotic, manual, and laden with errors and inefficiencies. AP has the power to bring their knowledge to the table to not only reduce cost but also to control risk and increase bottom line savings.

AP is responsible for protecting the company’s cash. But, if AP only concentrated on reducing cost, typically via headcount reduction, they would be doing a great disservice to their company.

Indeed, best-in-class companies have paved the way for transitioning AP from invoice processor to strategic business partner by taking the responsibility to reengineer the process end-to-end, which has proven bottom-line savings.

Protect against fraud and financial control risks

Pay suppliers on time

Positively improve the bottom line

Reduce costs

Improve efficiencies

Ensure compliance with laws and regulations

Their true value is in leading the organization through an AP reengineering process that sets policies around how the organization will manage the workflow in a way that will:

Improve Payment Strategy

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

4

Best Practices to Achieve SuccessMost process improvement initiatives never get off the ground because they take determination and strong change agents. Indeed, it’s nearly impossible to find the time in a very busy work day to develop the idea, justify expenditures, calculate an ROI, gain support, benchmark and get proof of concept, lead a team through the development and design phases of a best-in-class AP and supplier payments process, research and build regulatory compliance, test the system, train the organization, and execute, monitor and control the process — all while keeping everyone informed and overcoming resistance. Many give up reengineering the workflow because it is a large undertaking, is met with a lot of resistance, is easily overwhelming and, most importantly, because they don’t have the technology in place to provide solid metrics that prove the business case.

Most requests for process improvements that require technology are not approved because they are presented to fit only one need, making the ROI difficult to achieve. However, if the technology is seen as part of a business plan and it supports the big picture, it is easier to sell to upper management because the benefits can be tied to the projected savings.

This is a journey, not a destination. Finance leaders need to change their approach by creating a business strategy that incorporates the end-to-end AP process and sets the vision on the benefits that can be achieved by such an approach. Building an alliance across finance and with parties who influence the holistic AP process and creating a business plan to have full agreement on how all goods and services are paid for in the future is critical to success. If the steps are broken down into phases, aligning the end-to-end process will not seem so overwhelming and can achieve real bottom-line savings, which is worth fighting for.

Phase I: Identify Opportunities by Aligning AP, Finance & Purchasers

AP’s PerspectiveThe organization, especially Purchasers, often sees AP’s efforts as a nuisance. AP engages purchasing folks because, in most organizations, the purchasing department’s own the relationship with the company’s suppliers. The reality is, when AP requests help with handling and managing Non-PO invoices, Purchasers see this as busy work because the purchase has already been made. The assumption, by Purchasing, is that these requests are for small, insignificant dollars and subsequently put the AP requests into a work-bin, unanswered.

This becomes a vicious circle of rework, laden with errors and delays that cause late supplier payments. Most importantly, it is driven by unapproved spend, which could be for an inappropriate item — one that may not have been accounted for in the budget or may violate government trading laws — and likely jeopardizes the relationship with the supplier.

How do you change the organization’s perception of AP? Start by changing AP’s view of themselves. They’ve been told for so long that they are overhead, an expense generator, so they believe this to be true. Of course, AP is responsible for ‘processing’ invoices, but by flipping the image of the department, they can portray that their real value is in gaining control over the chaotic supplier payments operation and then mining the data on the invoice.

First, AP will need a workflow system that integrates with the company’s ERP system to gain control over supplier onboarding, processing paper invoices, tax compliance and track every possible path the invoice takes to the point that it is ‘ready-to-pay.’ A system that can provide metrics on various volume types and ideally help avoid bottlenecks and errors that occur is imperative to driving the right solutions.

For example, technology can provide statistics that point out the real issues rather than effects of those issues (the noise). It takes the conversation from “AP never pays the invoice on time” to data such as: x% of invoices are not sent to the AP address, x% is received after the due date, 80% of blocked invoices is lack of receipt, 80% of invoices are less than $1,000 and so on.

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

5

Implementing this type of automation in the past usually gained ROI through reducing headcount. Best practices organizations, on the other hand, keep their current employees but shift their role to work on initiatives that will truly impact bottom-line savings such as supplier onboarding, payment strategies, discount management, spend management, and dynamic discounts and early payment programs.

Best practices organizations keep their current employees but shift their role to work on initiatives that will truly impact bottom-line savings such as: Dynamic Discounts and

Early Payment Programs

Spend ManagementDiscount Management

Supplier Onboarding Payment Strategies

AP needs to step outside their comfort zone and become the end-to-end process owner so they can design a holistic AP process that removes bottlenecks and ensure an efficient, compliant and cost effective process. Once this is complete, they can analyze the data to lead projects to further improve the company’s profit margin.

This will require educating the AP team in best practices, project management, presentation skills, the needs of the C-suite, budgeting, benchmarking methods, new technologies, internal controls, and compliance. Transitioning the AP staff from transaction processing to finance experts is the key to changing the perception of AP and creating a lasting and positive impact to the bottom line.

In some cases, it may even be possible to start moving AP into either a neutral cost operation (“AP Free”) or possibly a revenue driver.

AP’s vision will be achieved by aligning and partnering with the rest of Finance, Purchasers, and the requesters of goods and services.

Supplier OnboardingAP should first build a strong relationship with Procurement by demonstrating how AP’s data can support Procurement’s mission. In an organization that allows Non-PO purchases, the procurement system does not have total spend and most likely doesn’t have actual spend either. Preparing and presenting this information will be an eye-opening experience for Procurement. It is extremely important for purchasing and AP to join ranks to develop a purchasing business plan around how employees will procure all goods and services in the future by commodity and how non-compliance will be handled.

One example of collaboration between AP and Procurement:Every U.S. Company (and individuals) is required by law to comply with the Office of Foreign Asset Control (OFAC). Governed by the U.S. Treasury and in cooperation with the United Nations, it restricts doing business with anyone on the OFAC list which contains countries, groups, and individuals involved in terrorism, narcotics, weapons of mass destruction, cyber warfare, and the black diamond market. This law is strictly enforced and has enormous fines and imprisonment for noncompliance. Companies need to be able to control the suppliers they trade with and ensuring that all suppliers are vetting against the various OFAC and AML (Anti-Money Laundering) databases prior to onboarding can go a long way toward this goal.

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

6

Developing an explicit policy on supplier onboarding is critical to ensuring compliance. There are several ways procurement and AP can support this endeavor. The company can use their ERP system and thoroughly document and execute an onboarding policy. However, this is one area where it is difficult to keep current on laws and regulations and ERP systems don’t typically have the tools necessary to validate suppliers. A best practice would be to engage a business partner who has thorough knowledge and expertise to conduct the research and validation on your behalf.

Most companies charge AP with making sure payments don’t go out to anyone on the OFAC list. However, this occurs too late in the purchasing process. The supplier/person is already in the database and business transactions have already occurred. Are you confident that every employee who is buying goods and services is aware of this law?

There are three key supplier onboarding best practices AP can enforce to ensure a best-in-class AP and supplier payments operation:

1. Check suppliers against OFAC and international “Do Not Pay” lists at the point of onboarding and prior to payment: This reduces risk of fraud and regulatory penalties.

2. Collecting and validating tax forms during onboarding: This step reduces risk of fraud, FATCA tax compliance penalties, and ensures an accurate and timely 1099 / 1042-S tax reporting process.

3. Validating Payment Details: There are about 26,000 variations of remittance rules when considering different payment methods and country requirements. Generally, the AP departments collects payment details via unsecure email and processes this information as they receive it. Instituting a proactive payment information vetting process will eliminate payment errors, which result in delayed payments, finance bank fees, and frayed supplier relationships.

Without establishing a strong Vendor Master Record upfront, AP Automation initiatives will fail so the accounts payable and finance department should include supplier onboarding in their holistic end-to-end approach. By joining forces with purchasers, AP can evaluate the company’s current end-to-end buying practices through payment and, together, they can intrigue and engage the C-suite to support their efforts to reengineer the process. Demonstrating how this joint undertaking upholds the vision and goals of the C-suite officers is key to garnering support for changing company purchasing behaviors which will lead to profitable best practice initiatives. The presentation to the CFO should be compelling and should ask them to be the Executive Sponsors, which means when a person or department does not comply to the buying policy, the CFO will back AP & Procurement and enforce the policy.

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

7

Phase II: Gain Executive SponsorshipMost project startups are pitched from a “what’s in it for me” perspective. To gain support and alliance from the officers of the company, you must pitch this from a “what’s in it for the company” perspective. Understanding what keeps the officers of the company up at night will help AP and Procurement sell the idea of reengineering the end to end process by aligning it to the needs of those in the C-suite. Here is a list of some C-suite goals and areas of focus:

• Accurate and timely financial statements

� C+1 accurate closing

� Streamline payment reconciliation: a critical element of the financial close cycle

� Improve 1042-S and 1099 tax reporting

• Intensely focused on working capital

� Earnings Performance (Preserving margins)

� Earnings per share

• Need to free up cash to

� Pay down debt

� Finance strategic initiatives

� Invest in new product and markets

� Avoid additional AP headcount as company grows

� Enable expansion of your global supplier base

• Increasing cash flow and profitability

� Reduce expenses / waste

� Make AP more cost-neutral and possibly profitable

� Reduce costs from payment errors

� Reduce costs related to tax, regulatory, and fraud

• Compliant processes

� Avoid audits; Establish best-in-class AP financial controls

• Avoid FATCA tax compliance penalties

• Avoid OFAC regulatory fines

• Real time data

� Focus AP talent on higher impact financial analysis and initiatives

� Strategic Planning

� Cash flow forecasting, savings, cost reduction

� Budgeting

� Performance management

� Sustain/improve earnings

• Satisfied customers and suppliers

• Eliminate potential fraud

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

8

Create a business case that shows how the reengineered AP process will support the goals of the C-suite. For example: Eliminating maverick spending will provide data to manage the cash from “thought of need” rather than when the invoice is entered into the AP system. This helps the organization manage the cash instead of managing the debt.

By aligning the goals of the C-suite, you gain their full support and sponsorship to begin the reengineering project.

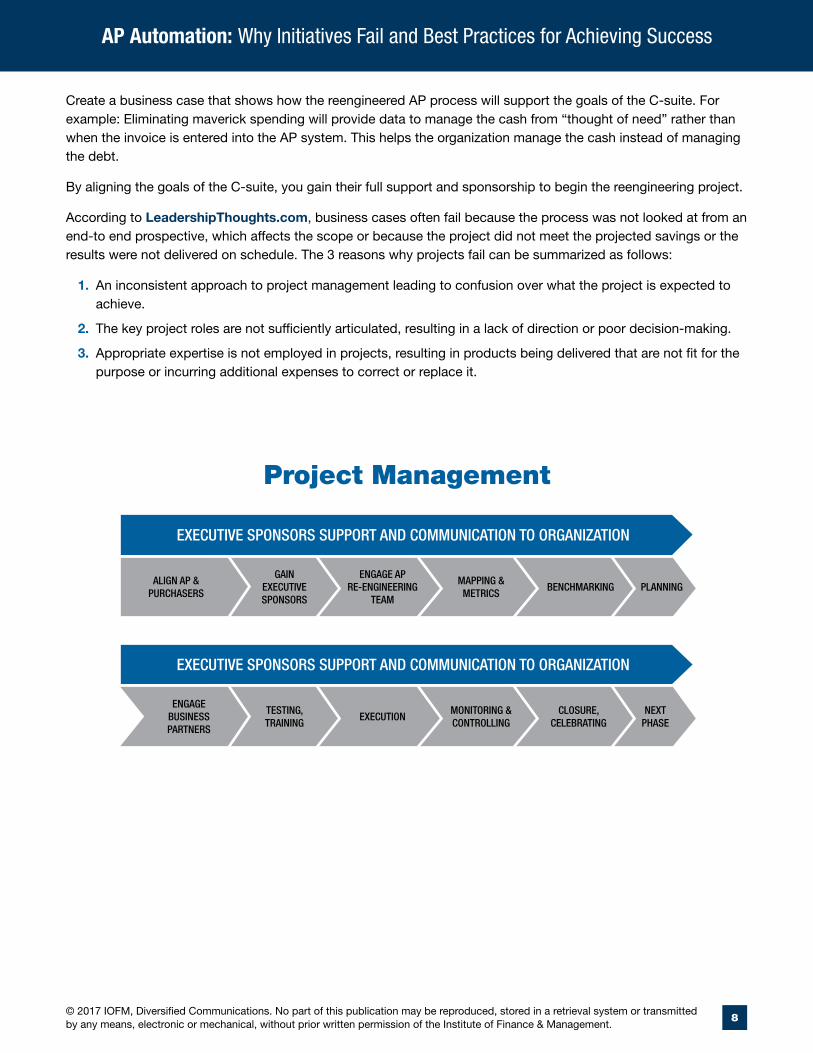

According to LeadershipThoughts.com, business cases often fail because the process was not looked at from an end-to end prospective, which affects the scope or because the project did not meet the projected savings or the results were not delivered on schedule. The 3 reasons why projects fail can be summarized as follows:

1. An inconsistent approach to project management leading to confusion over what the project is expected to achieve.

2. The key project roles are not sufficiently articulated, resulting in a lack of direction or poor decision-making.

3. Appropriate expertise is not employed in projects, resulting in products being delivered that are not fit for the purpose or incurring additional expenses to correct or replace it.

Project Management

EXECUTIVE SPONSORS SUPPORT AND COMMUNICATION TO ORGANIZATION

NEXT PHASE

TESTING, TRAINING

MONITORING & CONTROLLING

CLOSURE, CELEBRATING

EXECUTION

EXECUTIVE SPONSORS SUPPORT AND COMMUNICATION TO ORGANIZATION

PLANNINGGAIN

EXECUTIVE SPONSORS

MAPPING & METRICS

BENCHMARKINGENGAGE AP

RE-ENGINEERING TEAM

ALIGN AP & PURCHASERS

ENGAGE BUSINESS PARTNERS

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

9

Phase III: Reengineering TeamIt is important to bring team members together from each step in the process, from “thought of need” through payment. To identify who should be on the team, define who are the stakeholders of the holistic AP process and who does the process affect? Finance, requestors of goods and services, budget holders, approvers, receiving, treasury, tax department, compliance, legal… AP touches everyone in the company and has a major impact on the supplier’s cash flow. Members are usually chosen because they are seen as business partners, but you should also include those who are the biggest complainers on the team. They will help you build a process that will meet everyone’s needs and increase the acceptance rate.

On the first day that you gather the team, have the Executive Sponsor kick off the meeting by explaining why this project is important to them, what they expect from the team, and what support they will provide. A CFO or COO is an ideal leader for this role.

It is extremely important to have a dedicated work place for the team to meet and work together along with getting their managers’ commitment to protecting the time they are assigned to work on the project.

Holistic AP Team

COMMUNICATIONCOMMUNICATION

COMMUNICATIONCOMMUNICATION

EXECUTIVE SPONSOR AND

STAKEHOLDERS

PURCHASERS

AUDIT APPROVERS

RECEIVINGIT -

TECHNOLOGY

ACCOUNTS PAYABLE

CUSTOMER SERVICE

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

10

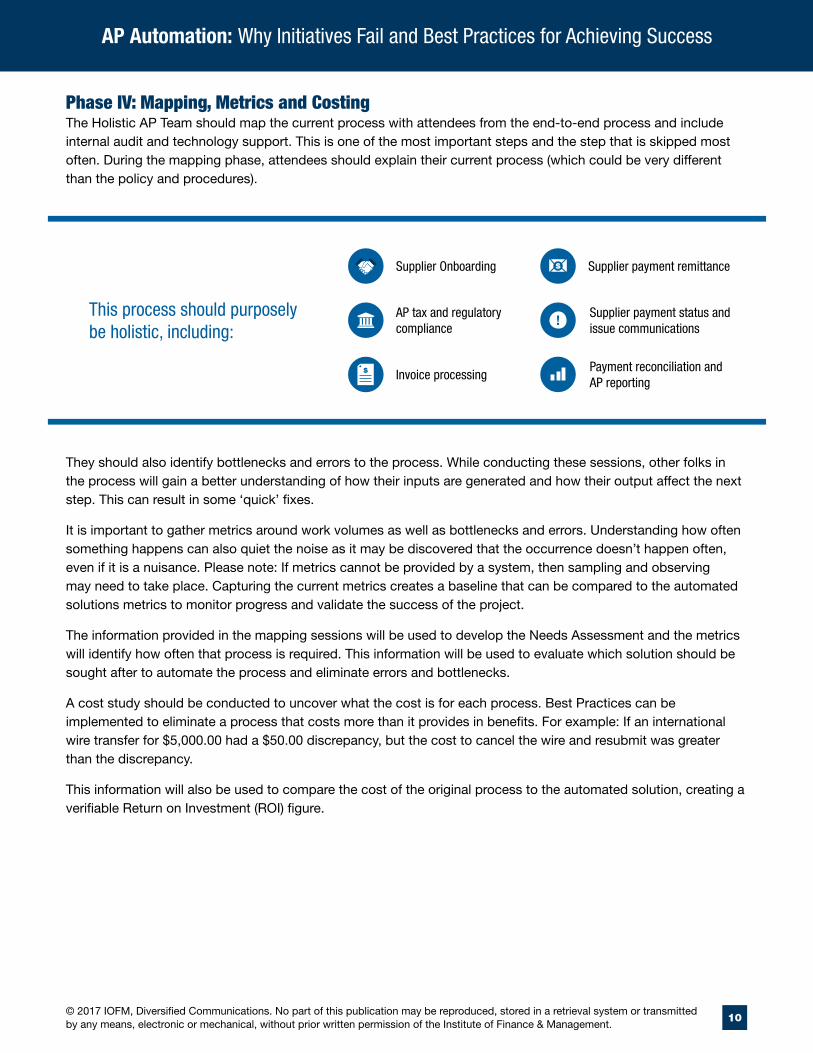

Phase IV: Mapping, Metrics and CostingThe Holistic AP Team should map the current process with attendees from the end-to-end process and include internal audit and technology support. This is one of the most important steps and the step that is skipped most often. During the mapping phase, attendees should explain their current process (which could be very different than the policy and procedures).

This process should purposely be holistic, including:

They should also identify bottlenecks and errors to the process. While conducting these sessions, other folks in the process will gain a better understanding of how their inputs are generated and how their output affect the next step. This can result in some ‘quick’ fixes.

It is important to gather metrics around work volumes as well as bottlenecks and errors. Understanding how often something happens can also quiet the noise as it may be discovered that the occurrence doesn’t happen often, even if it is a nuisance. Please note: If metrics cannot be provided by a system, then sampling and observing may need to take place. Capturing the current metrics creates a baseline that can be compared to the automated solutions metrics to monitor progress and validate the success of the project.

The information provided in the mapping sessions will be used to develop the Needs Assessment and the metrics will identify how often that process is required. This information will be used to evaluate which solution should be sought after to automate the process and eliminate errors and bottlenecks.

A cost study should be conducted to uncover what the cost is for each process. Best Practices can be implemented to eliminate a process that costs more than it provides in benefits. For example: If an international wire transfer for $5,000.00 had a $50.00 discrepancy, but the cost to cancel the wire and resubmit was greater than the discrepancy.

This information will also be used to compare the cost of the original process to the automated solution, creating a verifiable Return on Investment (ROI) figure.

Invoice processing

Supplier payment status and issue communications

Payment reconciliation and AP reporting

AP tax and regulatory compliance

Supplier Onboarding Supplier payment remittance

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

11

Phase V: BenchmarkingBenchmarking is a fantastic approach to finding solutions, discovering best practices, and gaining insight into technology and business solution partners who can provide cost effective solutions, with proven ROIs and fast deployment. There is no reason to reinvent the wheel if you can leverage someone else’s successful system.

Phase VI: Developing Goals, Mission and VisionMost likely, the current goals, mission, and vision are very specific to each department. Now is the time to rewrite the goals, mission, and vision to align the Holistic AP process. Start by requesting copies from the companies you benchmark to serve as a guideline. The mission and vision should serve to keep everyone focused on a united goal(s).

Phase VII: PlanningBegin by creating a Gantt Chart that details every step of the project against a timeline. A team member(s) should be assigned to each step. At least weekly, hold progress meetings to have a report on each step. Is the development on target? Are there any roadblocks that need to be dealt with to keep the project on schedule?

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

12

• Buying Strategies by commodity

� What should be purchased on a PO

� What should be purchased as a Non-PO

� Dollar Only

� Is there technology that can support and ensure compliance to the process? Can ERP handle this process while integrating with an AP and Supplier Payments Automation solution?

• How will suppliers be onboarded to meet regulations, streamline data entry, and reduce risk?

� Ownership of a Master File

� Format to Accept Supplier Information

� Supplier and Payment Information Validation Requirements

� Tax Form Collection

� Supplier Self-Service Access

• Supplier Management

� Contractors Services

� International Suppliers: How can this process make it easier to procure goods and services overseas, when this is beneficial to the organization?

� Reporting Requirements

� 1099/1042-S: online validation

� DeadBeat Parent Reporting (Child Support Enforcement)

� Minority Suppliers

• Compliance

� OFAC compliance: Blocked, Denied Parties

� Tax Regulations: FATCA / S&U / VAT / GST

� Sarbanes Oxley Act (SOX)

� Privacy Laws

• Internal Financial Controls to reduce risk, improve efficiencies, accurate data

� Invoice approval workflows

� Tax compliance validation

� Payment approval workflows

� Positive Pay

� Supplier and AP audit trails

� Signatory rights

� Role-based views and rights

� Overdraft controls

• Financial Statements

� Closing Requirements C+1

� Payment Reconciliation

• Cash Management from commitment of spend vs. ‘late’ invoice

• Approval prior to spending

� Budget compliance

� Appropriate spend

• Best Practices

� Spend Management

� Make productivity decisions

� Negative Receipt Notice

� Header match vs. line level

� Tolerance

� Sort: FIFO (first in, first out), then high dollars - get it on the books

� Escalation

• Payment Strategy

� Terms

� Payment methods (e.g., checks, EFT, wire, eCheck, LC, Pcard, Vcard, Commercial card)

� Foreign currency management

� Payment and Bank Reconciliation

� Early Payment Incentives

• Improve Supplier Relationships

� Company credit rating: inflated prices, shipments held, loss of terms, loss of discounts, account closed

� Supplier cooperation with purchasing policy

� Communications to suppliers (status, reporting, etc.)

• Profitability: bringing purchases under control

• Humanize the Process

� Unspoken:

� Fear of job loss

� Change means: the old way was wrong – be careful what you communicate

� PAPERless is harder than giving up smoking

� Supplier payments are not fun – ever!

When remapping the process to procure goods and services through payment, here are some points to consider:

Phase VII: Planning Guide

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

13

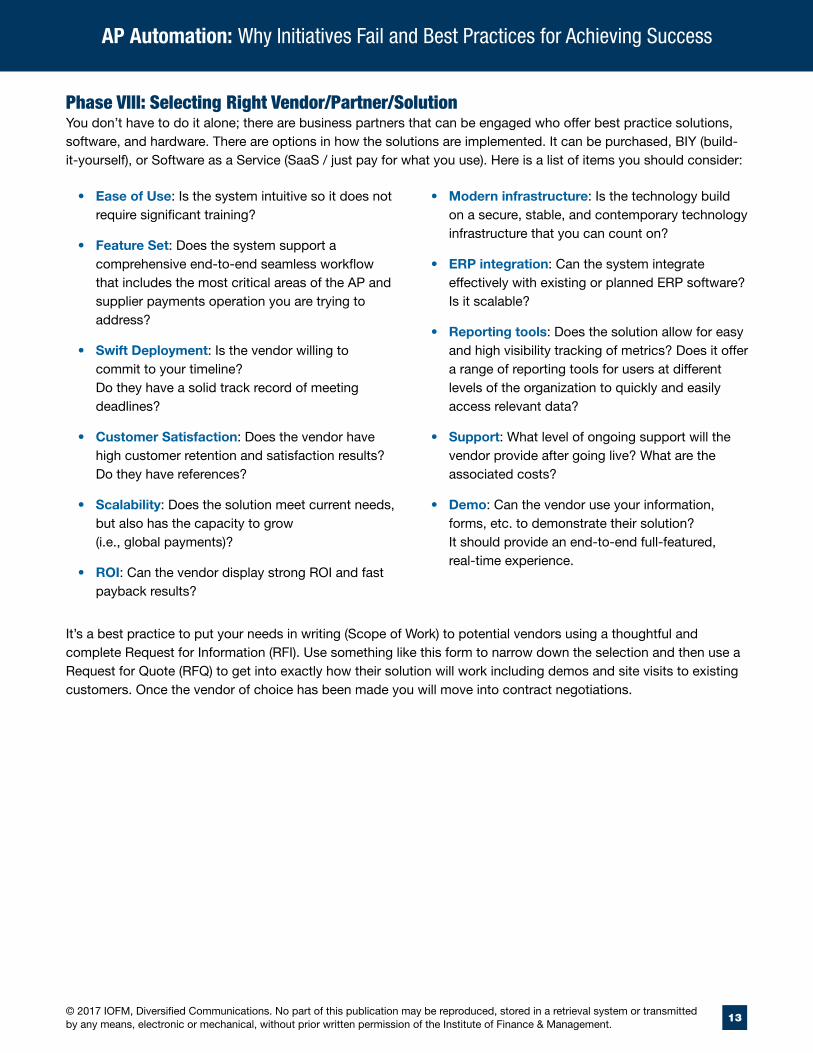

Phase VIII: Selecting Right Vendor/Partner/SolutionYou don’t have to do it alone; there are business partners that can be engaged who offer best practice solutions, software, and hardware. There are options in how the solutions are implemented. It can be purchased, BIY (build-it-yourself), or Software as a Service (SaaS / just pay for what you use). Here is a list of items you should consider:

• Ease of Use: Is the system intuitive so it does not require significant training?

• Feature Set: Does the system support a comprehensive end-to-end seamless workflow that includes the most critical areas of the AP and supplier payments operation you are trying to address?

• Swift Deployment: Is the vendor willing to commit to your timeline? Do they have a solid track record of meeting deadlines?

• Customer Satisfaction: Does the vendor have high customer retention and satisfaction results? Do they have references?

• Scalability: Does the solution meet current needs, but also has the capacity to grow (i.e., global payments)?

• ROI: Can the vendor display strong ROI and fast payback results?

• Modern infrastructure: Is the technology build on a secure, stable, and contemporary technology infrastructure that you can count on?

• ERP integration: Can the system integrate effectively with existing or planned ERP software? Is it scalable?

• Reporting tools: Does the solution allow for easy and high visibility tracking of metrics? Does it offer a range of reporting tools for users at different levels of the organization to quickly and easily access relevant data?

• Support: What level of ongoing support will the vendor provide after going live? What are the associated costs?

• Demo: Can the vendor use your information, forms, etc. to demonstrate their solution? It should provide an end-to-end full-featured, real-time experience.

It’s a best practice to put your needs in writing (Scope of Work) to potential vendors using a thoughtful and complete Request for Information (RFI). Use something like this form to narrow down the selection and then use a Request for Quote (RFQ) to get into exactly how their solution will work including demos and site visits to existing customers. Once the vendor of choice has been made you will move into contract negotiations.

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

14

Evaluation Form

Build Requirements and score as follows: required

0 - doesn’t have 5 - has this feature 10 - has exactly as

Score Total: 100% - excellent match 80% - a good match 70% - not a match

Item: this should come from mapping the P2P and the Voice of the Customer (VOC)

Number Item Rating 0-10 Notes:

1Invoice scanned within 3 days or less from date of invoice

2 Supplier Portal

3 XXXXXX

4 XXXXXX

5 XXXXXX

6 XXXXXX

7 XXXXXX

8 XXXXXX

9 XXXXXX

10 Price within budget

Phase VII: Evaluation Form

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

15

Phase IX: Testing, Training & ExecutionDuring this phase, the team needs to develop test case scenarios based on actual work and needs. These scenarios will be used to test how well the process and/or system executes the scenario and documents the results. It is critical to try and ‘break’ the system. For example: Type poorly formed ACH bank routing data in the supplier portal where they’re expected to provide banking details to see if it catches the error. Or enter inappropriate EIN/SSN numbers when asking for W9 information. The team should try and think of possible processing errors that could occur and test them. Don’t discover these types of problems after going live, as the employees will lose confidence in the system.

These test cases can then be converted into examples for the detailed policy and procedures manual and used during training.

Execution is your go-live date. At all cost, do not move the go-live date. It sends a very bad message to the organization. Keep in mind that a project will never be perfect. Create a punch list with dates for each item that needs to be completed.

Phase X: Communication, Monitoring & ControllingThroughout the project, it is critical to keep communications open and delivered in different styles to keep the Executive Sponsor(s), Stakeholders, the Reengineering Team and those affected by the Holistic AP process informed and up-to-speed. This is the best way to gain support and keep resistance to a minimum. Assigning this role on the Gantt Chart will make sure that the communication is happening on a regular basis. Depending on the message, one or more of the following could be implemented:

To help suppliers navigate the new system and processes, the AP automation plan should include necessary materials and guidance to articulate benefits of the new system (e.g. greater transparency, more accurate payments, more payment method and currency options, convenient self-service, issue resolution, early payments, etc.).

Meetings:

Executive Sponsor, Team Members,

Stakeholders, Town Hall (those affected by Holistic AP),

One on One (influencers, disrupters)

In Writing:

Emails, Newsletter, Project Wall

Live Sessions:

Demos, Test System

Supplier Communications:

Emails, FAQs, Documentation

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

16

Phase XI: Closure, CelebratingHave a formal closing report for the project that highlights challenges, key takeaways and successes. Include a comparison of the baseline metrics and the progress that has been made to date.

Have a celebration with those who worked on the project and those who supported the effort.

Phase XII: Next PhaseThere will always be a next phase as technology rapidly changes the process. Metrics need to continuously inform the process owners of what is working and what needs improvement. Use the 80/20 rule to determine which process needs the most attention. Don’t work on too many issues at once or the results will take too long and you will lose the support of the organization.

In Conclusion:To avoid failure and to ensure your project is successful, it must include the end-to-end AP and supplier payments process, commitment of time and resources to properly evaluate the opportunity, and alignment with the goals of the C-suite to gain their dedication and support.

Since this holistic process touches just about everyone in the organization, this is a critical undertaking. The goals of the project must be in the forefront to keep the team focused and engaged as they overcome challenges and resistance. Even though the team may be tempted to skip steps to lessen the timeline and costs, this is a risk that most likely will leave the project short of achieving its goals.

Transition AP from transaction processing by developing a strong relationship between purchasers and also the rest of the finance organization. Allow them to become subject matter experts and business partners to the C-suite. Aligning AP with the organization will ensure that a robust end-to-end AP process is developed, resulting in the implementation of the right automation solution for the company and the engagement of business solution partners. Together, this team can deliver real bottom-line savings through best practices and process improvements by:

• Gaining control over what is being purchased, from whom and at what cost.

• Cash management: From managing the debt (where the invoice is the first notification that there is an expense) to managing the cash (where the purchase order documents committed spending) and by providing:

• Real Time Information to make critical business decisions

• Timely accurate financial close and reporting

• Ability to forecast and manage the cash,

• Budget control

• Compliance to tax and regulatory laws

• Fraud elimination

• Less resource intensive AP processes as the supplier base grows

• Establishing a Payment Strategy that achieves cash flow control, eliminates potential for fraud, and opens the door to efficient future company growth (global).

Success requires implementing technologies to improve efficiencies and reduce cost, not just in the AP department (the trees) but stepping back and reengineering the process from thought of need through payment. Challenging the existing buying and payment practices to unleash their true potential through collaboration with initiatives that will have a positive impact on the bottom line such as; Discount Management, Early Payments, and Spend Management.

AP Automation: Why Initiatives Fail and Best Practices for Achieving Success

© 2017 IOFM, Diversified Communications. No part of this publication may be reproduced, stored in a retrieval system or transmitted by any means, electronic or mechanical, without prior written permission of the Institute of Finance & Management.

17

About the Sponsor:Tipalti is the only supplier payments solution to automate all phases of the AP workflow in one holistic cloud platform. Tipalti makes it painless for finance departments to manage their entire global supplier payments operations, while strengthening financial, fraud, tax and regulatory controls and enhancing the supplier payment experience. Leading companies like GoDaddy, Nikon, Twitter, GoPro, Eventbrite, Zumba and Amazon use Tipalti to eliminate up to 80% of their workload spent managing supplier payments, so they can scale their business rapidly and efficiently with global growth. www.Tipalti.com.

About the AP & P2P NetworkThe AP & P2P Network is the leading provider of training, education and certification programs specifically for Accounts Payable, Procure-to-Pay, Global and Shared Services professionals as well as Controllers and their F&A teams.

Membership to the AP & P2P Network (www.app2p.com) provides comprehensive tools and resources to financial operations professionals who manage or are deeply involved in the Accounts Payable and Procure-to-Pay process.

Focus areas include best practices for every AP & P2P function; AP & P2P metrics and benchmarking data; tax and regulatory compliance (e.g. 1099, 1042-S, W-9, W-8, Sales & Use Tax, Escheatment, VAT, Canadian Tax, Internal Controls); solutions to real-world problems challenging your department; AP & P2P automation case studies; member Q&A networking forums, Ask the Experts, calculators, and more than 300 downloadable, customizable AP & P2P policies, flowcharts, templates and internal control checklists.

A membership to the AP & P2P Network provides tangible ROI to any organization – saving your organization time, money and keeping you compliant.

Over 10,000 professionals have been certified as an Accredited Payables Specialist or Manager (available in English, Simple Chinese and Spanish), and Certified Professional Controller through the AP & P2P Network and its parent company, the Institute of Finance & Management.

AP & P2P Network also hosts the Accounts Payable and Procure-to-Pay Conference and Expo (Spring and Fall), designed to facilitate education and peer networking.

The AP & P2P Network is produced by the Institute of Finance and Management (IOFM), which is the leading organization providing training, education and certification programs specifically for professionals in Accounts Payable, Procure-to-Pay, Accounts Receivable and Order-to-Cash, as well as key tax and compliance resources for Global and Shared Services professionals, Controllers and their F&A teams. With a universe of over 100,000 financial operations professionals, IOFM is the trusted source of information in the rapidly evolving field of financial operations.