annual shareholders' presentation

TRANSCRIPT

Annual Shareholders’ Presentation12 May 2014

Strong cashflow, consumer play

Multiple locations, multiple brands

Diversified hospitality portfolio

Leading BPO office space provider

MAJOR DEVELOPMENTS – Recent Business Accolades

3

Robinsons Land was awarded by Euromoney as theOverall Best Managed Company in the Philippines

2013 & 2014

MAJOR DEVELOPMENTS – Recent Business Accolades

4

International Property Awards – Asia PacificMagnolia Town Center (Best Mixed-Use Development in the Philippines)Signa Designer Residences (Best Residential High-Rise Development in the Philippines)

Philippine Retailers Association Shopping Center of the Year 2013Robinsons Magnolia (Medium Malls Category)

Philippine Property AwardsBest Commercial Development 2013 Magnolia Town Center

International Alternative Investment ReviewExcellence in Real Estate Development – Philippines

BCI Asia Top 10 AwardsRecognized as one of the top developers withgreatest impact on the built environment in Southeast Asia

Philippine Quill AwardsBest in Business Communication 2013Robinsons Malls Tenant Conference (Special Events Category)

2013 Asia Pacific Real Estate Association Best Practices AwardBest First-Year Entrant

CNBC AsiaMr. Frederick D. Go - Finalist for CNBC’s 12th Annual Business Leaders Awards

Asia CEO AwardsFinalist for Global Filipino Executive for Mr. Frederick D. GoFinalist for Integrated Marketing Communications for Magnolia Town Center

Quezon City Government - Quezon City Hall of Fame

A LEADING PHILIPPINE PROPERTY COMPANY

National Capital Region

Misamis Oriental

Davao del Sur

Leyte

Cebu

South Cotabato

Negros Occidental

Ilocos Norte

DumaguetePalawan

Iloilo

Laguna

Bulacan

Batangas

PampangaTarlac

Cavite

Pangasinan

•Mall•Go Hotel • Mall

• ResidentialProjects

•Malls•Hotel•Office

•Mall•Hotel

•Malls•Hotel

•Malls•Office Buildings•Hotels•Condominiums

•Malls•Hotel• Residential Projects

•Malls•Residential Projects

•Mall•Hotel

• Mall• Residential

Projects

• Mall•Residential Project

•Mall

•Malls•Residential Projects

•Mall•Hotel

•Mall•Residential Projects

•Mall•Condominiums•ResidentialProjects

• Residential ProjectsRizal•Malls

• Mall

Nueva Ecija• Mall

Agusan del Norte

•Mall

9.1 11.0 13.0 15.5

2010 2011 2012 2013

18.8 20.1 21.2 22.8

2010 2011 2012 2013

94.095.8 96.0

98.7

2010 2011 2012 2013

3.5 3.9 4.6 4.7

2010 2011 2012 2013

Tourist Arrivals (in millions)

BPO Revenues (in US$B)

OFW Remittances (in US$B)

Population (in millions)

7.6%

3.9%6.6% 7.2%

2010 2011 2012 2013

GDP Growth Rate

*2013 Based on Estimates

5

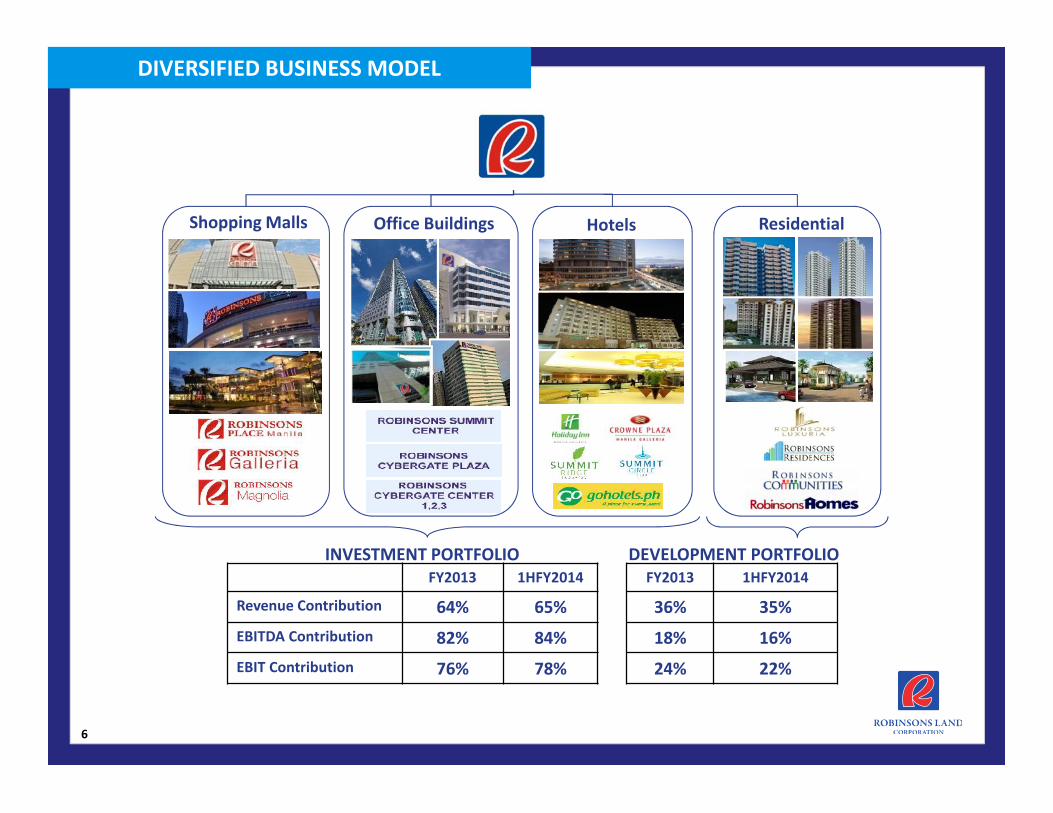

DIVERSIFIED BUSINESS MODEL

6

FY2013 1HFY2014 FY2013 1HFY2014

Revenue Contribution 64% 65% 36% 35%EBITDA Contribution 82% 84% 18% 16%EBIT Contribution 76% 78% 24% 22%

ResidentialShopping Malls Office Buildings Hotels

DEVELOPMENT PORTFOLIOINVESTMENT PORTFOLIO

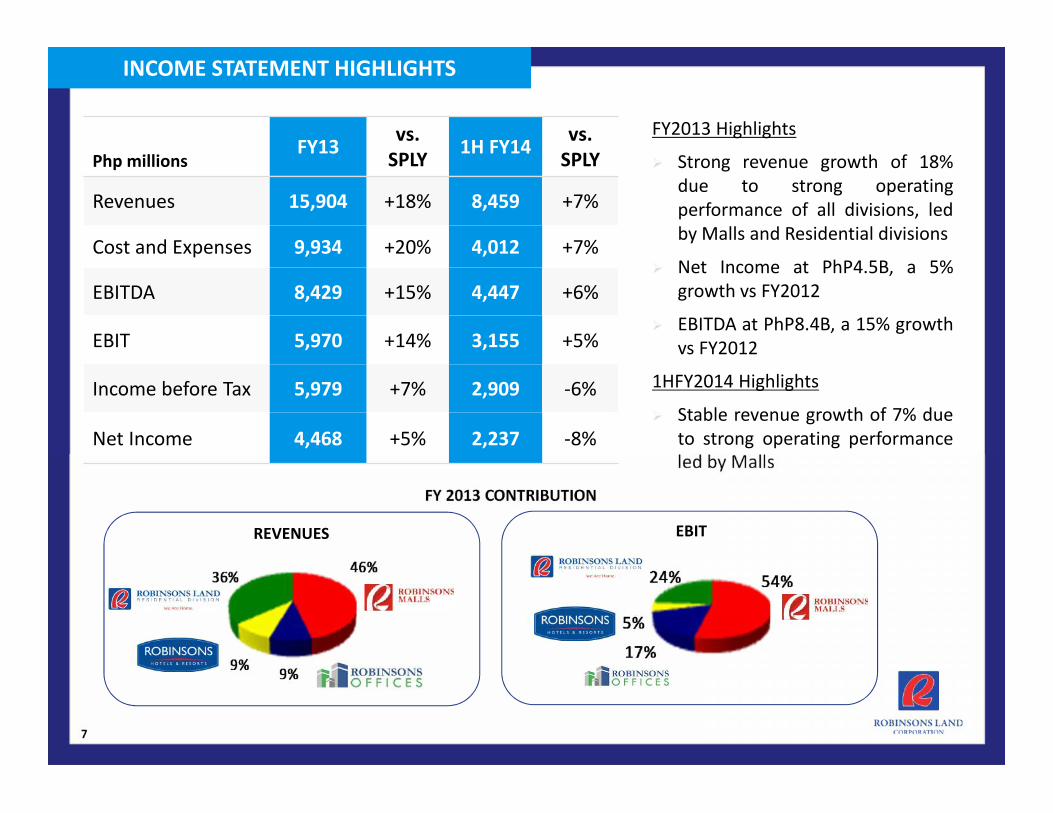

INCOME STATEMENT HIGHLIGHTS

7

FY2013 Highlights

Strong revenue growth of 18%due to strong operatingperformance of all divisions, ledby Malls and Residential divisions

Net Income at PhP4.5B, a 5%growth vs FY2012

EBITDA at PhP8.4B, a 15% growthvs FY2012

1HFY2014 Highlights

Stable revenue growth of 7% dueto strong operating performanceled by Malls

FY 2013 CONTRIBUTION

EBITREVENUES

Php millionsFY13 vs.

SPLY 1H FY14 vs.SPLY

Revenues 15,904 +18% 8,459 +7%

Cost and Expenses 9,934 +20% 4,012 +7%

EBITDA 8,429 +15% 4,447 +6%

EBIT 5,970 +14% 3,155 +5%

Income before Tax 5,979 +7% 2,909 -6%

Net Income 4,468 +5% 2,237 -8%

STRONG BALANCE SHEET POSITION (as of March 31, 2014)

8

TOTAL ASSETS (PhP MM) SHAREHOLDER’S EQUITY (PhP MM)

RETURN ON EQUITY CURRENT NET DEBT TO EQUITY

70,64774,886

80,056

FY12 FY13 1HFY14

46,57349,395

51,632

FY12 FY13 1HFY14

9% 9% 9%

FY12 FY13 1HFY14

13%

23%26%

FY12 FY13 1HFY14

REVENUES

EBITDA

EBIT

9

Second largest mall operator inthe Philippines with 37 malls

1,025,000 sqm in GLA 1,900,000 sqm in GFA 95% latest system-wide

occupancy Approximately 7,000 retailers Same mall revenue growth has

been tracking 8% in the past 5years

6,429 7,390

3,577 3,990

FY12 FY13 1HFY13 1HFY14

4,492 5,063

2,464 2,761

FY12 FY13 1HFY13 1HFY14

2,999 3,202

1,582 1,757

FY12 FY13 1HFY13 1HFY14

15%

12%

13%12%

7%11%

10

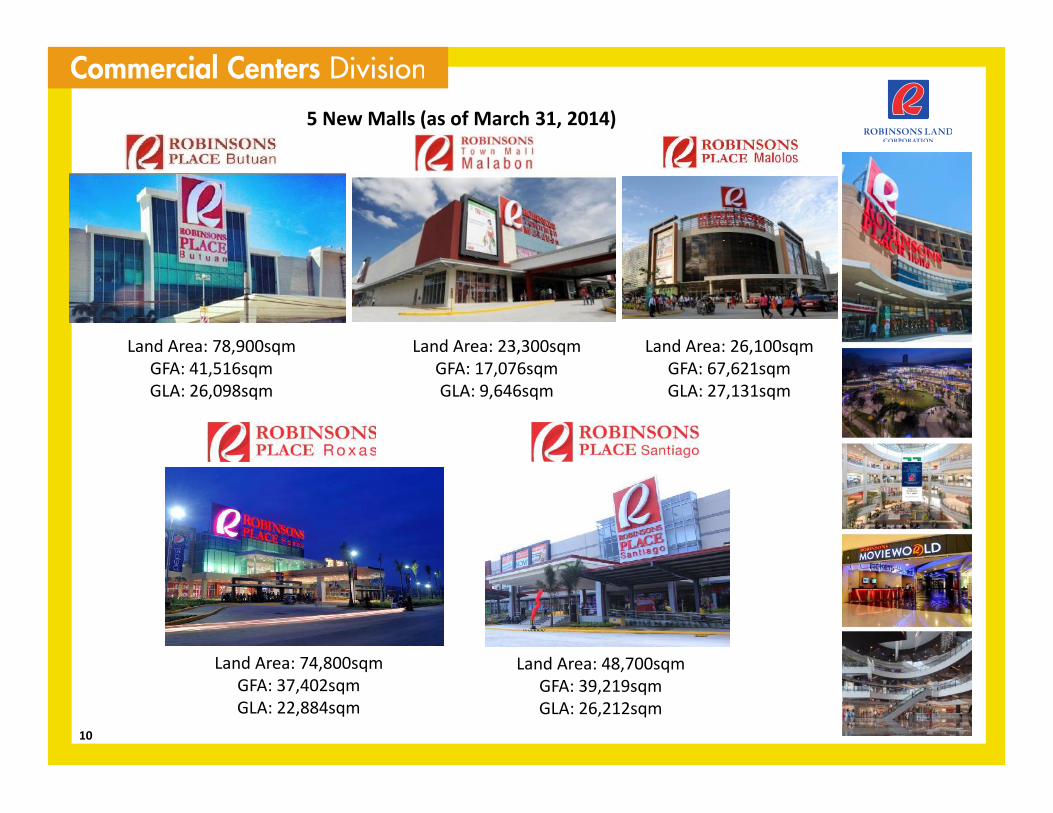

5 New Malls (as of March 31, 2014)

Land Area: 23,300sqmGFA: 17,076sqmGLA: 9,646sqm

Land Area: 78,900sqmGFA: 41,516sqmGLA: 26,098sqm

Land Area: 26,100sqmGFA: 67,621sqmGLA: 27,131sqm

Land Area: 74,800sqmGFA: 37,402sqmGLA: 22,884sqm

Land Area: 48,700sqmGFA: 39,219sqmGLA: 26,212sqm

3,220 3,713 3,9764,492

5,063

2009 2010 2011 2012 2013

4,1275,312 5,759 6,429

7,390

2009 2010 2011 2012 2013

2,048 2,324 2,466 2,999 3,202

2009 2010 2011 2012 2013

CAGR: +16% CAGR: +12%

CAGR: +12%

REVENUES EBITDA

EBIT

11

744,000 813,000 813,000 910,000 913,000

2009 2010 2011 2012 2013

CAGR: +5%

GLA

12

A leading BPO office spaceprovider with 273,000 sqmnet leasable space

Total occupancy is 98% Increased space by 41% or

80,000 sqm in FY 2014 Dominant landlord in the

Ortigas Central BusinessDistrict

REVENUES

EBITDA

EBIT

1,398 1,440

717 729

FY12 FY13 1HFY13 1HFY14

1,345 1,386

691 702

FY12 FY13 1HFY13 1HFY14

961 1,009

497 510

FY12 FY13 1HFY13 1HFY14

3%

2%

3%

2%

5%

3%

13

Cyberscape Alpha33% Leased Out

Cyberscape Beta55% Leased Out

14

CAGR: +7%

1,112 1,182 1,335 1,398 1,440

2009 2010 2011 2012 2013

1,032 1,140 1,302 1,345 1,386

2009 2010 2011 2012 2013

CAGR: +8%

738 842 923 961 1,009

2009 2010 2011 2012 2013

CAGR: +8%

165,000

188,000 193,000 193,000 193,000

2009 2010 2011 2012 2013

CAGR: +4%

REVENUES EBITDA

EBIT GLA

15

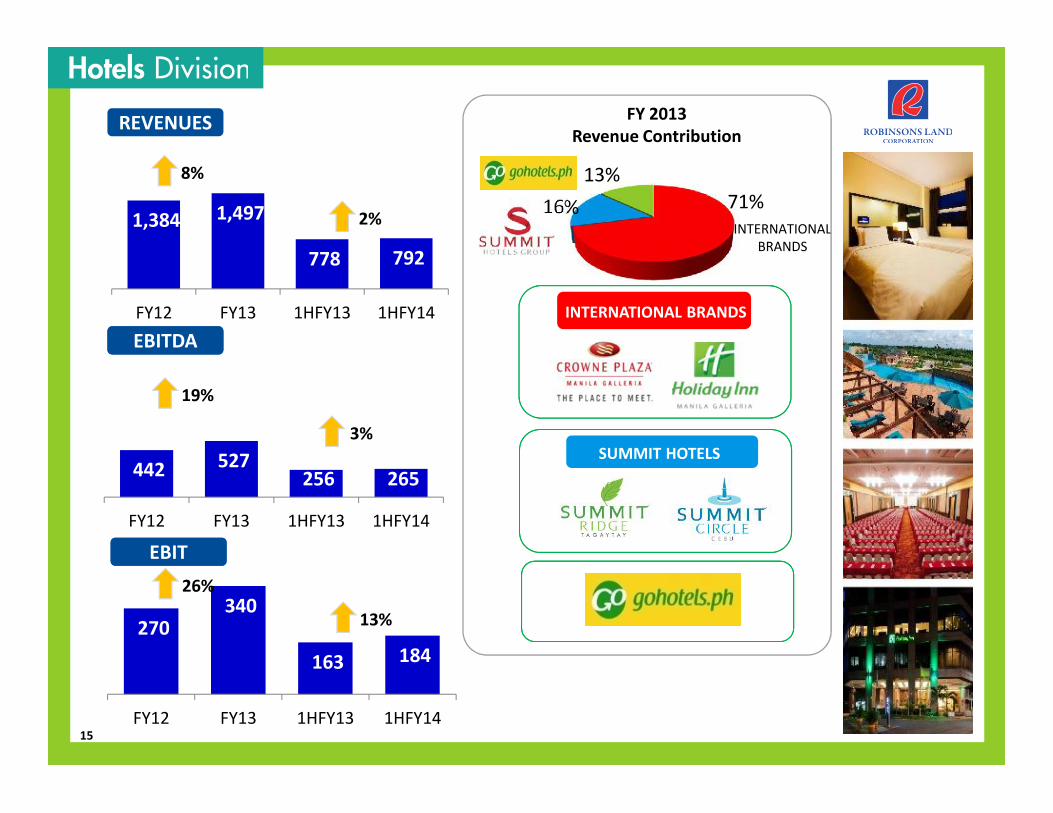

71%16%13%

FY 2013Revenue Contribution

INTERNATIONALBRANDS

INTERNATIONAL BRANDS

SUMMIT HOTELS

REVENUES

EBITDA

EBIT

EBITDA

EBIT

1,384 1,497

778 792

FY12 FY13 1HFY13 1HFY14

442 527256 265

FY12 FY13 1HFY13 1HFY14

270340

163 184

FY12 FY13 1HFY13 1HFY14

8%

2%

19%

3%

26%

13%

16

FY2013 New Hotel

Location: Paco, Manila

Started Operations: June 2013

No. of Rooms: 118

Location: Downtown District of Iloilo City

Started Operations: December 2013

No. of Rooms: 167

FY2014 - New Hotel (as of March 31, 2014)

17

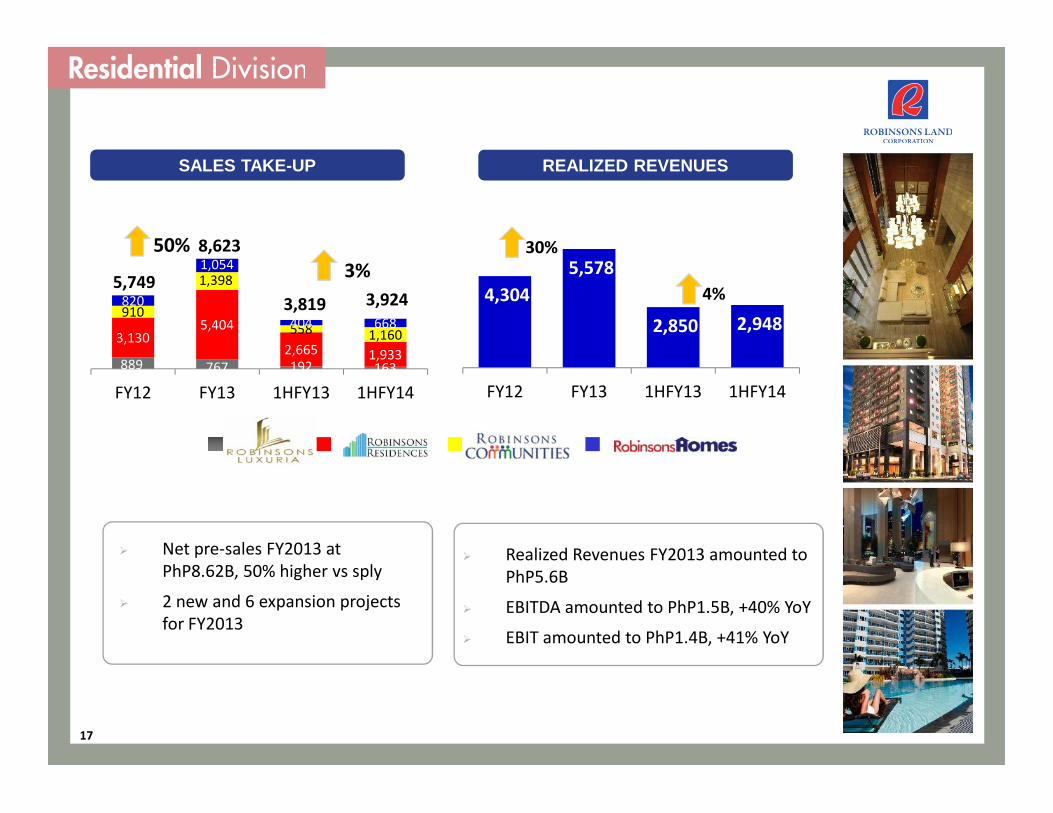

SALES TAKE-UP

5,749

8,623

REALIZED REVENUES

Realized Revenues FY2013 amounted toPhP5.6B

EBITDA amounted to PhP1.5B, +40% YoY

EBIT amounted to PhP1.4B, +41% YoY

Net pre-sales FY2013 atPhP8.62B, 50% higher vs sply

2 new and 6 expansion projectsfor FY2013

30%

4,3045,578

2,850 2,948

FY12 FY13 1HFY13 1HFY14

4%

889 767 192 163

3,1305,404

2,665 1,933

910

1,398

558 1,160

820

1,054

404 668

FY12 FY13 1HFY13 1HFY14

50%3%

3,819 3,924

18

Brighton Parkplace

Brighton Parkplace North

Hanalei Heights

Fernwood Parkhomes

Forest Parkhomes

Forest Parkhomes North

Grand Tierra

Mirada Dos

Rosewood Parkhomes

Robinsons Homes East

San Lorenzo Homes

San Jose Estates

St. Bernice Estates

Bloomfields Cagayan DeOro

Robinsons ResidenzaMilano

Robinsons Vineyard

Southsquare Village

Aspen Heights

Fresno Parkview

Hillsbourough Pointe

Richmond Hills

Robinsons Highlands

Montclair Highlands

Bloomfields Tagaytay

Blue Coast Residences

Bloomfields Davao

Nizanta at Ciudades

Robinsons Place Residences

Fifth Avenue Place

McKinley Park Residences

The Fort Residences

The Magnolia Residences

Vimana Verde Residences

Adriatico Place

East of Galleria

The Trion Towers

Gateway Garden Heights

One Gateway Place

Otis 888

Gateway Regency

The Sapphire Bloc

Woodsville Residences

Azalea Place

Radiance Manila Bay

AmiSa Private Residences

Sonata Private Residences

Signa Designer Residences

Galleria Regency

Gateway Garden Ridge

Woodsville Viverde Mansions

Centennial Place

Bloomfields Novaliches

Escalades at 20th Avenue

Escalades South Metro

The Wellington Courtyard

The Pearl Place

Axis Residences

Escalades East Tower

Acacia Escalades

19

Radiance Manila Bay – North TowerManila

The Sapphire Bloc – West TowerPasig City

Axis ResidencesMandaluyong City

Acacia EscaladesPasig City

The Peal PlacePasig City

Bloomfields Cagayan De OroCagayan De Oro

Bloomfields Heights LipaLipa City

Bloomfields General SantosGeneral Santos City

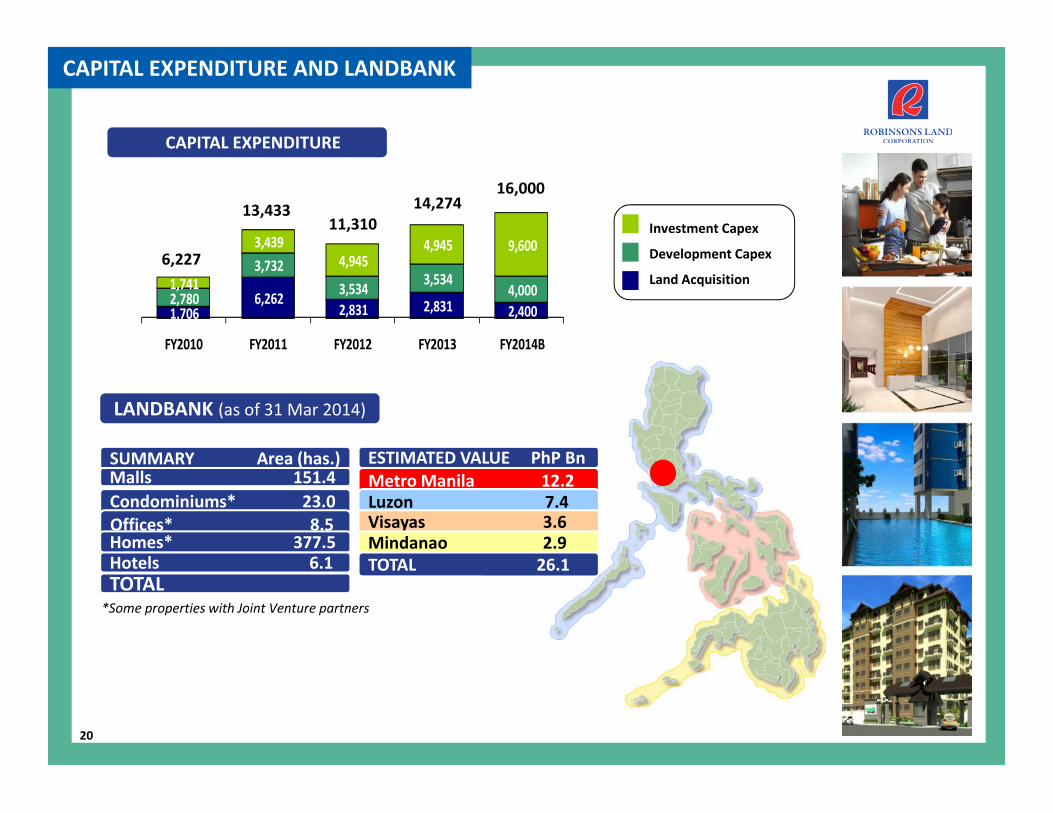

CAPITAL EXPENDITURE AND LANDBANK

20

6,227

13,43311,310 Investment Capex

Development Capex

Land Acquisition

CAPITAL EXPENDITURE

16,000

*Some properties with Joint Venture partners

SUMMARY Area (has.)Malls 151.4Condominiums* 23.0Offices* 8.5Homes* 377.5Hotels 6.1 6.1TOTAL 566.5

ESTIMATED VALUE PhP BnMetro Manila 12.2Luzon 7.4Visayas 3.6Mindanao 2.9TOTAL 26.1

14,274

1,7066,262

2,831 2,831 2,4002,780

3,7323,534 3,534

4,0001,741

3,4394,945

4,945 9,600

FY2010 FY2011 FY2012 FY2013 FY2014B

LANDBANK (as of 31 Mar 2014)

21

MOVING FORWARD – Future Plans & Strategies

FY2013 FY2014 FY2016 FY2017FY2013 FY2014 FY2015 FY2016

GrossLeasableArea(sqm)

1 MallExpansion

+18%

913,0001,077,000

NetLeasableArea(sqm)

+41%

2 New Office BuildingsCyberscape AlphaCyberscape Beta

273,0001,150,000

+12%

7 New Malls

193,000

308,000

1 New OfficeBuilding

Bridgetowne

+7%1,292,000

1 New Mall

FY2011 FY2012 FY2013 FY2014 FY2015

• Palawan• Dumaguete• Tacloban• Bacolod

# of Rooms

• Otis-Manila

233

+26%

7571,122

1,411

Currently evaluating opportunitiesfor 4 new Summit Hotels

• Iloilo• AlphaOrtigas

•Davao•Butuan

639

•Mandaluyong

Beefed up sales force andincreased marketing efforts

3,819 3,924

1HFY13 1HFY14

Sales Take Up(PhPMM)

+11%

+274%+18%

+48%

4 New Malls2 Expansion

343,000+13%

1 New OfficeBuilding

Bridgetowne