annual report & accounts 2013

DESCRIPTION

Gibraltar Chamber of Commerce Annual Report & Accounts 2013TRANSCRIPT

ANNUAL REPORT & ACCOUNTS 2013

03

Board Members

President Christian Hernandez

Vice President John Isola

Honorary Treasurer Mike Nicholls

Honorary Secretary Marvin Cartwright

Directors Jose Luis Bonavia

Franco Cassar

George Desoisa

George Dyke

Ernest Felipes

Andrew Haynes

Jeremy Nicholls

E J Nicholas Russo

Registered Office

Watergate House

2/6 Casemates

PO Box 29

Gibraltar

T: +350 200 78376

F: +350 200 78403

www.gibraltarchamberofcommerce.com

Honorary Auditors

Baker Tilly (Gibraltar) Limited

Regal House

Queensway

Gibraltar

THE BOARD

04

FOREWORD

2013 has been a busy year for the Chamber of Commerce. After 7 years Nicholas Russo retired and Christian Hernandez became president. His first few months at the helm saw him busy meeting unions, government ministers, members of the opposition and business leaders. The main message promulgated at those meetings was to make Gibraltar businesses more competitive. In order to achieve this it is imperative that we level the playing field. Business costs need to be reduced by obtaining reductions in rates whilst continuing the trend of successive governments of lowering taxation. Key to levelling the playing field also requires action by government to stop illegal competition from across the border. Firm action also needs to be taken to eradicate illegal labour. However, it is not only reduced business costs or eradication of unfair competition that are central to making us more competitive. It is also crucial for Gibraltar to have modern labour laws that make it attractive for businesses to set up in Gibraltar. In this respect government must resist the urge to cherry pick on aspects of UK legislation in favour of the employee whilst not making corresponding changes to make our legislation more modern from an employer point of view. It is a well

known fact that the private sector is the engine of Gibraltar’s economy and only by ensuring we are competitive can we expect to see that engine continuing to drive Gibraltar from strength to strength.

The announcement by Barclays Bank in March last year that it would be closing its Gibraltar branch was a major set back for Gibraltar businesses. The Chamber immediately got to work on various fronts to try and reverse this decision and lobbied hard, in the absence of any other significant lobbying from trade unions or other business organisations. Meetings were held with senior bank executives, members of UK Parliament and the Gibraltar government to explore different solutions. Unfortunately the announced closure of the main branch was not reversed although the timeframes originally announced were set back so as to give businesses and individual clients alike more time to transfer their business. The announcement by government that they would be setting up a new bank was very welcome news. In response to the announcement and in the context of prior discussions with government on the possibility of a new Government owned bank, the Chamber emphasised the importance of any such bank being operated on an arm’s length basis and

independently of government, managed by suitably qualified professionals and subject to regulation by the Financial Services Commission. The Chamber is pleased that all of these recommendations have been taken on board by government.

Recent problems with Spain have once again reminded us how important it is for the economy to be diversified. 2013 saw an escalation of rhetoric and implementation of oppressive measures by the Spanish PP Government at the frontier and these events and ongoing consequences are referred to in some detail within this year’s report. One consequence was that Chamber was instrumental in forming the Cross Frontier Group, a collaboration of organisations representing employers and employees from Gibraltar and Spain. This is the first time in 40 years that such a group has been created. The Group’s mandate is to raise awareness of the excessive frontier queues and how they impact on the lives of citizens and businesses in Gibraltar and the Campo region. The Chamber believes that the common interests of the Group’s members: economic growth, job creation and a freely flowing frontier cannot be ignored forever by the European Commission and the Madrid government.

0505

CONTENTS

03 Board Members 24 Online Gaming

04 Foreword 26 Environment

05 Contents 27 Port & Shipping

08 Politics

12 The Economy

32 Tourism

17 Wholesale

34 Property

19 Retail

33 Auditors Report

21 Banking

37 Annual Accounts

22 Funds

46 Key Information

Annual Report & Accounts

07

As part of the Chamber’s role in delivering reliable and useful business information, the board took the decision to update the Economic Impact Study which the Chamber first published in 2009. The results whilst historic need to be put into a contemporary context, not least because since the original study there have been important macro-economic events such as the international financial crisis and Spain’s prolonged recession. The results of the updated study should be out in the third quarter of 2014 and all the indications are that Gibraltar’s economy today, despite the frontier checks, is an even more important driver of economic growth in the Campo than it was five years ago.

As ever, there are the unpredictable and unwelcome economic clouds looming on the horizon. The UK government’s plans to introduce a Point of Consumption (POC) tax for non-resident online gaming companies will have a dilatory effect on Gibraltar-based operators. The rate has not been set yet but Gibraltar’s online gaming sector will comply accordingly but adjust their cost lines both in Gibraltar but also in the UK. However, non-UK based operators from other jurisdictions, particularly outside Europe may decide not to comply at all. These recalcitrants will be beyond the reach of UK regulators so the UK government’s claim to be protecting UK punters will be an empty one.

POWER GENERATION

The investment in new buildings continues to make ever greater demands on Gibraltar’s creaking

electricity grid. The government has been quick to bring in additional generating capacity which has been welcome. Fixing the network though is a far bigger issue. The clock in ticking and an announcement is expected imminently about the new power plant but construction is likely to take 18 months at least.

Linked to this is an initiative which the Chamber will be asking its members to be part of in the year ahead. As part of the a company’s corporate and social responsibility we need to have an idea of our own individual corporate footprint. How much do we electricity do we use? how much fuel do we use? Are there areas we can cut down or recycle? The aim is for Gibraltar to be carbon neutral within 6 years. It is a highly ambitious target but we all need to start working towards this for the good of our community. It also makes good business sense. In this light, the Chamber is looking to the Government to entice companies (as well as individuals) to adopt schemes and processes which reduce energy consumption and promote recycling.

TOURISM

Once again some improvements have been made to the installations on the Upper Rock. Whilst the sums of money involved are not huge, the improvements have made a noticeable difference to the accessibility of many areas in the Nature Reserve. Clearing the overgrown paths has also enhanced the variety of flora and fauna too. However, the critical linked up transport arrangements have yet to be addressed for the benefit of all:

tour operator and taxis as well as for the locals and tourists alike.

The Chamber has made representations to the government on suggested uses for the site of the old air terminal. With a clean site there is space for a state of the art visitor information centre as well as a drop off for buses, a dedicated taxi rank and additional car parking. The Chamber would not want to see any development which detracted from visitors coming to Main Street and its environs. This is a great opportunity to make a great first impression on visitors entering Gibraltar and also leave a positive lasting memory. The current state of the border area does anything but this.

SHIPPING

In this year’s report we have an extensive article on the Port and Shipping sector. Gibraltar’s port and the goods and services it supplies is a barometer of world trade. The number of ships calling at Gibraltar is still well below the 2010 peak. But as consumer demand recovers in Europe, other ports have been much more aggressive in attracting shipping business. And the lack of investment in Gibraltar’s port means that business will continue to go elsewhere. Most notably neighbouring Algeciras has invested huge sums in port infrastructure in recent years. As the pie gets smaller some local agents are likely to throw in the towel. The port is a critical logistics lifeline for Gibraltar but its facilities also offer Gibraltar an opportunity to continue diversifying its economy. It needs to be nurtured accordingly.

FOREWORD

In July 2013 Her Majesty’s Government of Gibraltar announced the creation of an artificial reef to the west of the runway. Outside Gibraltar the event should have been of no interest but the response from the Spanish Foreign Secretary was little short of propaganda war, complete with misrepresentations, lies and half truths, all intended to raise the profile of the fishing dispute to an exaggerated level. It became a national story in Spain and dominated the news channels and front pages. It did not end there. The story was picked up by the international press and went ‘viral’. It featured in Taiwan, Australia, New Zealand, North America, Canada, Germany, Italy, Holland, France, and extensively in the United Kingdom. The story reported Spain’s disproportionate reaction to the laying of the artificial reef and the Chief Minister’s robust response. It was not a good story for Spain outside national borders.

The Spanish Foreign Secretary made threats: a toll charge would be

introduced at the frontier and sterner controls would be implemented. The Spanish boast was that the “party” for Gibraltar was over. The rest of the world interpreted events differently. The actions were seen as Spain creating an incident to provide a distraction from an embarrassing corruption scandal (The Barcenas case) that threatened to envelop the leadership of the ruling party. If the Spanish Government was looking for a smokescreen, then the timing of the artificial reef was an opportunity that proved irresistible.

A week later, for the international press, the story had moved on, but not in Spain. It continued, at fever pitch, throughout the summer. Gibraltar was front page, every day, for six consecutive weeks. Every news bulletin and every chat show on radio and television carried variations on the story without any let-up. Gibraltar was being demonised.

The Madrid Government has shown scant regard for international public

opinion. All the same the press cuttings from 2013 as reported around the world must make for very depressing reading to Sr. Margallo. Although he has succeeded in demonising the Chief Minister, whose notoriety has ensured that he has name recognition throughout Spain and they have tried to cast the Gibraltarians as undesirables, it has come at a cost. International opinion and more especially in northern Europe and the USA have been openly critical of Spain’s bullying tactics. It remains to be seen, when Madrid asks for further financial support from Germany and the EU, if its indifference to the economic plight of the Campo de Gibraltar may not haunt them.

The propaganda onslaught started with the accusation of “stealing sand” for reclamation projects; although untrue it gave rise to a prohibition of exports from Spain (to Gibraltar) of boulders and certain building materials. Gibraltarians were classed as pariah’s who are a drain on the Spanish National Health

08

POLITICS

09

Service, also untrue. Gibraltar, it was claimed, is the principal source of illegal weapons entering the EU, nonsense. The list of lies and half truths was long and has had a corrosive effect on relations among the general population of the region. Shame on those whose manipulation of events have put relations back in such a cynical way. It led to some Gibraltarians having their cars torched and hostile graffiti painted on their properties. The campaign of hostility remained intense up till mid-December 2013 and in early 2014, the queues show little tendency to improve. Queues at the frontier for cars and pedestrians can be marathon affairs. The Special Forces police brought in to create the queues were a reminder of the Franco days and the mood on both sides of the frontier was tense.

Gibraltar turned to the British Government and the EU Commission for help. David Cameron’s support was more forthright than that of any Prime Minister in a generation. He has stood

shoulder to shoulder with Gibraltar. His message to Spain was unequivocal and almost certainly persuaded Madrid to pull back from the frontier ‘toll’. By contrast the EU failed to address the issue. The evidence of Spain’s manipulation of the frontier as a tap to be turned “on” and “off” at the whim of Madrid was ignored.

The Spanish onslaught has taken its toll on the economy, more so in neighbouring Spain but Madrid only sheds crocodile tears for the Campo. The outcome of EU and Madrid indifference has been the first ever “Cross-Frontier Association”. This lobby group has come about as a result of the sense of political abandonment and comprises trade union and business representatives, (including Chamber of Commerce), from both Gibraltar and Spain. The Cross Border Group may well play an important role in the months to come.

Another positive from 2013 was the

success of Gibraltar’s bid to become the 54th member of UEFA. It is a credit to all those who worked diligently for so many years to deliver a significant victory in the teeth of Spanish opposition. The outcome of Gibraltar’s membership of UEFA will help promote football in Gibraltar and inspire future generations of players; the admission of Gibraltar in the roster of UEFA members has significant political ramifications. Madrid is only too aware that Gibraltar’s direct relationship with diverse international bodies and Governments all add up incrementally. Collectively they amount to recognition of a modern Gibraltar by the international community. This acceptance has increasingly put the “political” conquest of Gibraltar beyond Spain’s reach.

It is no longer possible for Madrid to have any illusions that for a cosy sovereignty deal all they need is a compliant British Government. Peter Hain’s lamentable “joint sovereignty” initiative was the last such attempt. No future British Government will contemplate entering into any sovereignty arrangements without the consent of the people of Gibraltar, not even in preliminary talks. The assurances given last year by the Prime Minister and supported by all parties in the House of Commons leave Spain no option but to address any sovereignty proposals directly to the Government of Gibraltar. This is now British Government policy. It is not what Madrid or Sr. Margallo wants to hear. The Partido Popular still holds onto the misguided belief that, to achieve their territorial ambitions they only need to persuade the British Government. The acceptance by Spain’s former Foreign Secretary, Sr. Moratinos (PSOE) of the “three voices two flags” approach was politically honest but Sr. Moratinos was no push over. The “three voices two flags” principle, however, appears to be anathema to Margallo and the right wing of his party. It seems that they believe their own propaganda and that to talk to the Gibraltar Government is beneath their dignity.

11

Sr. Margallo is from Melilla one of Spain’s African colonies. No doubt Sr. Margallo believes that his strong stand on Gibraltar helps Melilla by promoting Spanish power in the region. The paradox however is that, as Gibraltar consolidates its position, the weakness’ in Spain’s African colonies become ever more apparent. They only want for Rabat to follow the “Margallo playbook” of populist nationalism and the cracks will appear in a community that is divided along ethnic lines. The recent reports of waves of sub Saharan immigrants breeching the defences to enter Melilla are a worrying sign that Rabat is testing Madrid. Mass movement of sub Saharans within Morocco’s borders only occur because Rabat permits the incursion. In its dealings with Gibraltar, Spain should be providing Rabat with an example to follow for Ceuta and Melilla. Instead it is acting irresponsibly and doing the opposite. News that the Moroccan authorities might launch a diplomatic offensive in 2015 to recover Ceuta and Melilla may serve to curb the worse populist excesses against Gibraltar.

The challenges for the year ahead include the looming threat of over-lapping responsibility for the waters around Gibraltar. Independent of the sovereignty issue, the EU has designated these waters, currently under British supervision, as falling under

Spanish environmental supervision. The non transparent manner in which Spain took the supervisory role is a strong indicator that Madrid’s purpose is to provoke conflict. In particular it is worrying to note that the Spanish Government have now legislated to ban all land reclamation in these waters, and to prohibit specifically the type of bunkering currently being undertaken. These measures, if pursued, will put Gibraltar and Madrid, yet again, on a collision course. It may be, however, that the potentially serious clashes between the Royal Navy and the Guardia Civil during 2013 have persuaded Spain not to pursue whatever mischief they had in mind. What is clear is that Gibraltar has numerous land reclamation projects planned and any attempt by Madrid to interfere with these plans will only serve to put the parties into conflict. The over-lapping responsibility for the waters looks set to provide yet more “grist for the propaganda machine”. It will take a subtle political hand to deflect attention away from the supposed environmental infraction by Gibraltar of whatever Spanish regulation is intended to apply to our waters and point at the machinations of Madrid.

The longer we remain in crisis with Spain the greater the cost, be it political, economic or as is seen every day at the frontier, personal. The Chief Minister has stood up well under pressure,

including intolerable personal attacks in the Spanish media and having to confront an orchestrated mob who used violence to prevent his speaking in Algeciras. The absence of any apology or expression of regret by Sr. Margallo speaks for itself. No doubt the Chief Minister has been tempered by his experience. After the turmoil of the last six months of 2013 it is understandable that the Opposition are looking to examine the political events that lead to the crisis with the Partido Popular but now is not the time for a post mortem. Gibraltar’s economy needs stability. The Chief Minister should be given every assistance in resolving the fishing dispute in a manner that allows both sides to claim success and for this both the Chief Minister and the Leader of the Opposition will need to raise their game and avoid petty point scoring. Reaching a lasting agreement with the Spanish fisherman is the most immediate challenge for the Chief Minister. Once this is achieved, all else is possible. Without it, the situation becomes ever more difficult to resolve.

“The Chief Minister should be given every assistance in resolving the fishing dispute in a

manner that allows both sides to claim success”

POLITICS

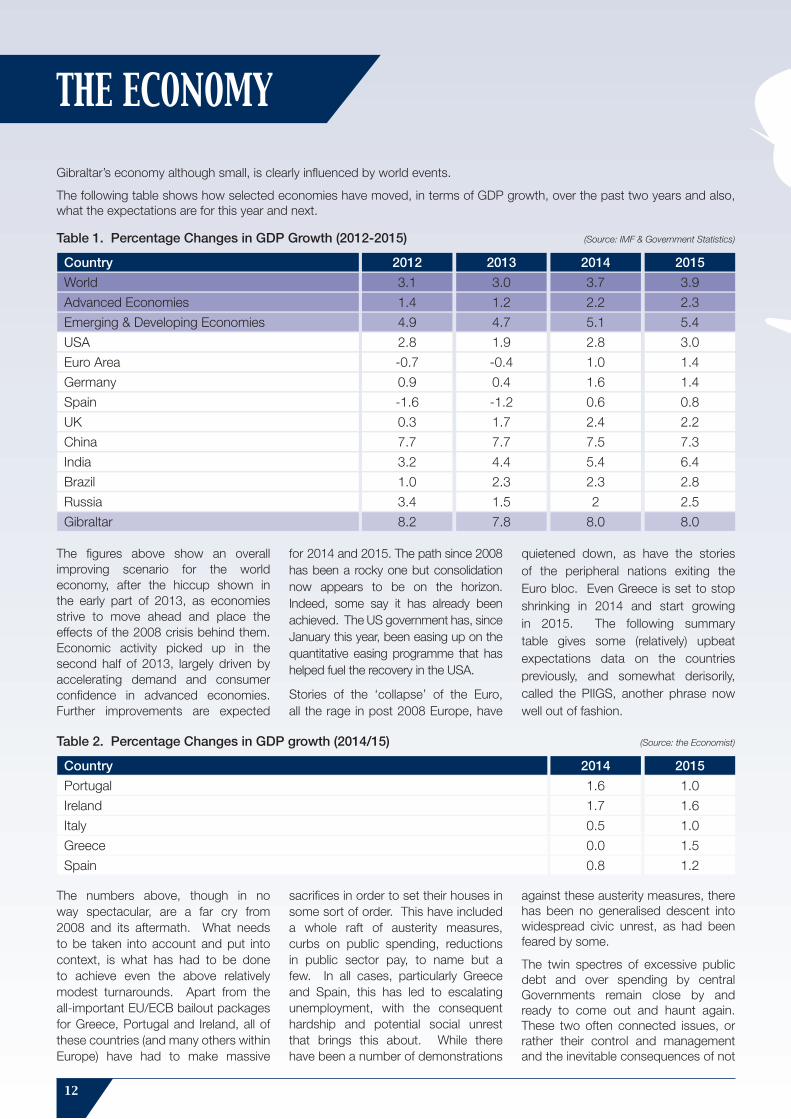

Gibraltar’s economy although small, is clearly influenced by world events.

The following table shows how selected economies have moved, in terms of GDP growth, over the past two years and also, what the expectations are for this year and next.

12

Country 2012 2013 2014 2015

World 3.1 3.0 3.7 3.9

Advanced Economies 1.4 1.2 2.2 2.3

Emerging & Developing Economies 4.9 4.7 5.1 5.4

USA 2.8 1.9 2.8 3.0

Euro Area -0.7 -0.4 1.0 1.4

Germany 0.9 0.4 1.6 1.4

Spain -1.6 -1.2 0.6 0.8

UK 0.3 1.7 2.4 2.2

China 7.7 7.7 7.5 7.3

India 3.2 4.4 5.4 6.4

Brazil 1.0 2.3 2.3 2.8

Russia 3.4 1.5 2 2.5

Gibraltar 8.2 7.8 8.0 8.0

Table 1. Percentage Changes in GDP Growth (2012-2015) (Source: IMF & Government Statistics)

Country 2014 2015

Portugal 1.6 1.0

Ireland 1.7 1.6

Italy 0.5 1.0

Greece 0.0 1.5

Spain 0.8 1.2

Table 2. Percentage Changes in GDP growth (2014/15) (Source: the Economist)

The figures above show an overall improving scenario for the world economy, after the hiccup shown in the early part of 2013, as economies strive to move ahead and place the effects of the 2008 crisis behind them. Economic activity picked up in the second half of 2013, largely driven by accelerating demand and consumer confidence in advanced economies. Further improvements are expected

for 2014 and 2015. The path since 2008 has been a rocky one but consolidation now appears to be on the horizon. Indeed, some say it has already been achieved. The US government has, since January this year, been easing up on the quantitative easing programme that has helped fuel the recovery in the USA.

Stories of the ‘collapse’ of the Euro, all the rage in post 2008 Europe, have

quietened down, as have the stories of the peripheral nations exiting the Euro bloc. Even Greece is set to stop shrinking in 2014 and start growing in 2015. The following summary table gives some (relatively) upbeat expectations data on the countries previously, and somewhat derisorily, called the PIIGS, another phrase now well out of fashion.

THE ECONOMY

The numbers above, though in no way spectacular, are a far cry from 2008 and its aftermath. What needs to be taken into account and put into context, is what has had to be done to achieve even the above relatively modest turnarounds. Apart from the all-important EU/ECB bailout packages for Greece, Portugal and Ireland, all of these countries (and many others within Europe) have had to make massive

sacrifices in order to set their houses in some sort of order. This have included a whole raft of austerity measures, curbs on public spending, reductions in public sector pay, to name but a few. In all cases, particularly Greece and Spain, this has led to escalating unemployment, with the consequent hardship and potential social unrest that brings this about. While there have been a number of demonstrations

against these austerity measures, there has been no generalised descent into widespread civic unrest, as had been feared by some.

The twin spectres of excessive public debt and over spending by central Governments remain close by and ready to come out and haunt again. These two often connected issues, or rather their control and management and the inevitable consequences of not

13

doing so, are set to be engrained in the psyche of economists and planners everywhere. IMF head Christine Lagarde recently said that “high debt levels continue to hold momentum back” Hopefully, these economies have learnt from past mistakes in this respect as they move on. Also hopefully, those countries that have not suffered these problems up to now will be able to learn from these historical facts and manage their economies appropriately so as to avoid similar issues going forward. The problem, as always, remains solving the politician’s dilemma. How do politicians convince the electorate that it is wise to be cautious when times are good so that we are better placed to weather cries when recessions rear their ugly heads? As has been seen in developments over the last few years, this is a monumental task.

The numbers on economic performance do not, of course, tell the whole story.

Many of the advances recently seen in the UK economy, for example, have been centred in the prosperous south

of the country, particularly in the area of greater London. This, together with the Coalition government’s incentives for home ownership, has led to a property boom, which in turn is fuelling the economy. (Shades of 2008, anyone?)

The advances in the euro area shown above ignore the worrying fact that 1 in 4 of Europe’s under 25’s who want a job cannot find one. As Christine Lagarde says “Growth remains too low and unemployment too high for us to declare victory on the crisis”

Many of Spain’s tentative steps on the recovery path are due to an improved export performance in the manufacturing sector. From the IMF “In fact, Spain’s exports have grown faster than Germany’s since the crisis, helping to post a current account surplus for the first time in 20 years”. Also helping have been the extensive reforms put into motion by the Rajoy government. These are based on 3 centres of action: Firstly, bank recapitalisation (including via €100 billion credit line from the ECB)and tightening up of

financial regulations; secondly labour market reform, a long standing Spanish problem and finally, fiscal reform, aimed at restoring the budget surplus that existed in Spain in 2007.

This has been a difficult road to travel on but it is probably the right one. However, as the IMF points out, the rate of economic growth needs to increase substantially if serious inroads are to be made on unemployment in a reasonable time frame. This is the biggest challenge facing Spain and time will tell if it will be achieved. At national level, unemployment is now down to 25.6% (The Economist April 2014), the first time it has been below 26% in some years, but this is small change.

While the picture for Spain nationally is not great, it still compares favourably to Andalucía, where unemployment is over 37%, with 42,000 unemployed in the Campo alone. At this regional level, it is clear that the task facing Spain’s government is harder still.

14

THE ECONOMYSumming up, Gibraltar is facing a world where economic conditions generally are improving, even if the small improvements being seen in Spain are not yet filtering down to the South. Overall we have a mixed bag of an improving global scenario and an ever suffering immediate neighbour.

In light of all this, how is Gibraltar doing, what is the outlook and what are the threats facing us going forward?

Looking at GDP the graph below, which uses data from the Statistics Office, the picture looks very positive, showing steady and sustained economic growth over the last 12 years. Applying a linear trend implies that GDP will reach £1.3 billion in the current financial year. This is an excellent result over a long period of time and shows Gibraltar’s overall economy to be in good health. Certainly, by comparison to other economies since the crisis of 2008, Gibraltar’s performance has been spectacular. On the budget, a record surplus of £37 million was the result for 2012/13 and the indications are that 2013/14 will see another record, again good news.

However, as always, bare figures do not tell the whole story. There are underlying issues that pose threats going forward.

Ongoing Spanish hostilities, were a major issue of concern to businesses, with 20% of respondents naming this as the most important challenge facing business.

It is understood that Main Street trade in many traditional business areas is

down. Across other sectors, the picture remains unclear. Gibraltar residents are spending more in bars, restaurants, shops and supermarkets, as outings to Spain for shopping and lunch are down due to delays. Reduced cross border tourist visitors has led to reduced income from this source across the same sectors. Unfortunately, there is no current data to analyse the overall effect but anecdotal evidence suggests that the border issue has been negative to business.

The question is what to do about this going forward? The whole Spain/UK/Gibraltar equation is out of balance, on land, at sea and in the air, with the EU doing little, if anything, to help solve the issues. It was made quite clear by the Partido Popular, prior to their election victory, that things would get more difficult for Gibraltar should they get elected and this indeed has happened.

At a local level, two interrelated initiatives are worthy of mention and not only because they have been Chamber led. One is the Cross Frontier Group, with representatives from Trade Unions

and business from the (local) Spanish and Gibraltar sides lobbying in London, Madrid and Brussels. This can only be to the good, as it emphasises to the power brokers the close economic interdependency that exists between the two communities. The other is the Economic Impact study of 2009 that quantified the economic relationship between Gibraltar and the Campo. This was a landmark document that

showed, among other things, that Gibraltar was responsible for 13% of the Campo’s economy and accounted for one out of every six jobs. The Chamber is now updating the study and expects publication to be in August 2014.

Apart from the Spanish dimension, there are other threats going forward. One is the point of consumption tax that UK government is contemplating for the gambling sector. It remains to be seen which way this will evolve as it is not good news for the Online Gaming Sector. Another issue is FATCA (Foreign Account Tax Compliance Act or full disclosure reporting) that is being considered by the European Union and the United States. If this proceeds, there will be serious implications for the Company and Trust administration business in Gibraltar.

The whole tobacco issue has been very much in the news recently. Is it perhaps time to revisit this industry so that it can be rebalanced with a view to ensuring its long term sustainability?

Let us now assess the domestic economic and financial picture.

The Chamber has, over the past 8 years or more expressed concern at the level of public debt and the ever rising level of Government recurrent expenditure. These two issues are at the centre of the problems that most of the world’s economies have experienced since the crisis of 2008. Clearly, this is something Gibraltar needs to avoid and learn from the mistakes of others.

From the point of view of national debt, the picture looks promising.

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Gibraltar GDP £m GDP £m Linear (GDP £m)

(Sources: Data Statistics Office; Trend line Chamber of Commerce)

15

The 2013/14 Government estimates show gross debt reducing from an actual £518m as at March 2012 to an estimated £376m as at end March 2013, with a further reduction to £364m forecast for March 2014. Although it is likely that the picture will change once the figures become ‘actual’, it seems that we are heading in the right direction. We shall see what this year’s budget reveals.

However, there is a caveat on the debt figures and that is the whole situation with the Gibraltar Savings Bank and Credit Finance Corporation. The latter has been funded by the Savings Bank to the tune of £344m. The current book value estimated at £45m includes the £30m loaned to Sunborn. This whole issue has caused a lot of controversy at local political level. It is debatable whether taxpayer’s savings should be loaned out to commercial ventures such as Sunborn. Further clarity on this whole issue would be welcome.

The other issue surrounding Credit Finance Corporation is to do with the Government’s liabilities towards the same. At the time the new hospital was built, the Chamber argued that the PFI (Private Finance Initiative) financing arrangements, while not booked as public debt, effectively formed part of it as Government were ultimately liable for it. Surely, this is also the case with Credit Finance Corporation and Government must also be liable for any loans made by the Corporation? There is an argument that this should also be considered as part of National Debt. If so, then the figures stated on National

Debt would need to be augmented. This concept should provide for an interesting debate!

The impact of the funding of the new Power Station on National Debt, as well as other Government projects in the pipeline, also remains to be seen.

The other issue that has concerned us historically is the level of recurrent expenditure, which has been ever increasing. The 2013/2014 estimates show projected expenditure for the current financial year of £470m to be below the £480m for the revised estimate for the 2012/13 financial year. If this were to actually happen, it would be welcome news indeed. The problem is the large gap that tends to exist between actual outcomes and forecasts or estimates. For example, in the 2012/13 estimates, the estimated expenditure for the year 2012/13 was for £440m. As stated above, the revised estimate for the year 2012/13 went up to £480m, or an increase of 9%. If the same increase were to be suffered by the 2013/2014 estimate, expenditure would be up to £512m, in other words an increase. It will be interesting to see the numbers in the June budget.

Another feature that will soon become part of financial life in Gibraltar is the Gibraltar International Bank (or G.I.B.). It has been the ambition of past Governments that there should be a national bank of some sort. The imminent departure of Barclays will leave a hole in local banking that needs to be plugged. The G.I.B. should do precisely that. The initiative has been generally well received locally. There

is one main area of concern and this is that the bank needs to be run on purely commercial terms with no political interference. Government reassures us that this will indeed be the case. This reassurance is welcome.

Summing up, we have an improving world economy, continued problems in Spain, particularly in the South, with Gibraltar currently remaining robust. With prudent financial and economic management, there is no reason for this not to continue to be the case going forward. However, and as touched on above, there are threats to our traditional economic base going forward. How these will manifest themselves in the future is unknown. It could be a good opportunity, therefore, for Government to make good on its manifesto commitment of having an Economic Advisory Council. This body could, among other issues, look at ways of diversifying our economy so that we can be better prepared for any shifts that may arise in the future. This Council must involve business and the Chamber would be delighted to participate.

17

WHOLESALE

The sigh of relief which greeted the end of the 2013 Christmas shopping season was perhaps indicative of the year as a whole: glad that it was over, relieved that the year was not as bad as many had feared and surprise that most traders who began the year were still there at the end. The Wholesale sector and its volatile Retail sector cousin have been feeling the knock-on effects of the fall in consumer spending for the last five years. Speaking to a number of the established retailers on Main Street it seems that the best year ever was in 2009. Since then it has been managing flat or dipping sales against rises in cost bases. The pressure on margins is a continuing battle as traders cannot simply pass on cost increases to customers.

So it was against this tough background that the frontier stop and search regime introduced by the Spanish authorities in August made its unwelcome entrance onto Gibraltar’s tourist stage. And the retail and wholesale sectors noticed its effects almost immediately. The long queues to get into and out of Gibraltar had the deterrent effect on visitors so desired by Madrid’s government. However, the full ramifications which the queues had on Spanish businesses in the Campo region only became clear after several months. And many Gibraltarians

who habitually crossed the frontier into Spain each weekend to shop, go to restaurants or spend some leisure time remained in Gibraltar and spent their money here. The new habit was to stay in Gibraltar. Many people have been delighted by the new-found weekend experience in Gibraltar. It certainly beats sitting in a 4 hour queue. And the bars, cafes and restaurants have all benefitted from this enlarged local custom.

The increased local market certainly helped to offset the sharp fall in tourist visitors in the second half of the year. Nevertheless, Gibraltar cannot sustain its future economic development by only servicing its local population. The Rock’s businesses need to have a truly open frontier where people and goods (not just tourists) can come and go at will.

With the difficulties continuing in Spain’s economy the problem of unregistered businesses plying their trade in Gibraltar persists. What makes it worse are those local companies who rent out their trade licence or operator’s licence to third parties to sell into the local market illegally. Apart from the lack of warranties for the product or service delivered this short-sighted piggy-backing undermines our own economic resilience.

Over the years other sectors such as financial services or online gaming have set their own exacting standards which are recognised internationally. This gives credibility, certainty and enhances the reputation of the jurisdiction. There might be benefits in replicating a similar regime for other sectors, tobacco to name but one. The purpose of such a system of standards is to be recognised by manufacturers, tax authorities and customs official alike. So far the actions of this government and previous ones have all been focused on addressing issues connected to supply: allocating more resources to detect and arrest smugglers, demarking particular zones where loitering is not allowed, eradicating sales of tobacco from housing estates and so forth. All these are welcome and perhaps long overdue. But still the problems of tobacco for the wider population persist. Maybe it is time to introduce measures which address the demand side of the equation. There are serious and delicate issues of public policy to consider in doing this but judging by the arrest rate the measures taken to date are not being sufficiently effective.

The fall in expat tourists and shoppers has been most evident in the fall in the number of euros taken in cash by many

“Many people have been delighted by the new-found weekend experience in Gibraltar.”

18

WHOLESALEshops in Main Street in the second half of the year. Spain is expecting a 10 per cent increase in tourist visitors in the summer of 2014. Many of these will be staying on the Costas. It would be unreasonable for those tourists to expect another summer of 7 hour queues to get in and out of Gibraltar.

Over the longer term there will inevitably be a secondary effect of fewer visitors: those local businesses will begin to cut back on their own expenditure: instead of going to local restaurants two or three times a week, it will be just once. Replacing vehicles or the family car once every three years will be stretched out to every five or six years. Everything starts to slow down.

The withdrawal of Barclays came as another unwelcome blow to local

businesses. Credit has remained tight since the 2008 financial crash but with one less lender, and the most significant one at that, a number of small and medium sized businesses will struggle. New projects will not be funded and expansion and progress will be curtailed.

Rent increases for retail units in the prime parts of Main Street have met some resistance. The smart landlords are those who are reasonable and do not give in to avaricious tendencies. Too often in the recent past rents paid by failed businesses have been used as the basis for further increases. The clicking ratchet of ever upward increases is liable to end in an almighty bang as one or more businesses say “Enough!” and hand the keys back. Where is the virtue in having a

premium rental valuation in a vacant premises? Perhaps the government should consider levying rates on retail premises which remain unoccupied for 6 months or more. Retail space is limited in Gibraltar. It should be put to productive economic use, not land banked by owners hoping to charge upward only rents.

Trading Standards and the related Office of Far Trade are still waiting in the wings. This complex piece of legislation is taking time to come into shape. The Chamber welcomes the consultation from the Minister’s office but some of the initial momentum has been lost. It needs to be regained. We want to have a well regulated and modern system which helps local traders and also offers the necessary protection for consumers.

19

RETAILAnguish among local retailers about the twin effects of the recession in Spain and the slow recovery in the UK was compounded further by the frontier problems at the end of July. Most retailers (at least those not in grocery lines) still look back fondly to the days of 2008 and 2009, the best trading years for many local businesses. Since then turnover for most has been either flat or slightly lower: consumers simply have less money, pay rises are minimal and access to borrowing has been curtailed by the banks. Against such a background the attractiveness of a retail business is not what it was.

Measures introduced by the Spanish authorities to discourage and at times openly intimidate visitors not to come to Gibraltar certainly had their effect: the number of visitors in October and November fell by 40 per cent compared with 2012. The knock on effects of this will be felt increasingly in 2014. Still, at least the checks and queues only started in earnest in August and the months of April to July were relatively buoyant. For many retailers though one bad month can takes many months of lacklustre trading to recover from. Several bad months of trading may prove terminal for some and this is likely to be borne out during 2014.

But the queues did lead many locals to rediscover the delights of Gibraltar’s close-knit community and the majority

opted to remain in Gibraltar on the long hot weekends of the summer. Saturday mornings on Main Street had a renewed buzz and friends and families socialised at leisure. This is the type of atmosphere retailers dream of.

The bars and restaurants may have lost out on the late summer tourist trade but they certainly gained from locals eating out. “Keep it local” became the new watchwords and many refused to queue in order to spend money in the economy of an antagonistic neighbour.

One year on and the same bugbears of traders persist. Rents and rates make up an increasing percentage of operating costs. Landlords need to be more realistic. When inflation is running at 2-3% each year and turnover is down or flat there is little justification for annualised increases equivalent to 10 or 15 per cent. The number of unoccupied shops on Main Street (and elsewhere) should give them a clue and that is before the problems of the frontier queues are taken into account.

Another bugbear is the nonstop rise of online shopping. In isolation people are free to buy what they want from where they want. However, the inequality is that local traders pay import duty on the items which they import to sell in their stores. Duty on personal imports either at the frontier or at the Post Office is often waived. And yet there is

a cost of operating and handling this huge increase in parcel volume. The government should levy a minimum handling charge to help offset the increased costs of all the extra staff needed to handle these shipments.

As mentioned elsewhere in this report, the announcement that Barclays was significantly scaling back its Gibraltar operations was met by local traders with a grim sense of the inevitable. The reality for a number of businesses is that they have little choice of taking their business elsewhere although at the time of going to press plans to open a Gibraltar International Bank were accelerating well. In time this might offer a viable alternative to Barclays.

Mention must be made of MinIster Costa’s efforts to try and capitalise on the renewed vibrancy in Main Street among locals which the frontier queues has created. Many of the retail outlets in Gibraltar are owner-managed and they can and do react nimbly as market conditions dictate. Others though are tied to large international retail chains and their buying and promotional schedules are agreed 9 -12 months in advance. An opportunity to mount sales pushes which include as many shops as possible needs to take this into account as having universal participation in such events will benefit Gibraltar even more.

21

BANKING

The big news of the year came in March when Barclays announced it was undertaking a 3-month review of its Gibraltar operations and all options as to the bank’s future presence in Gibraltar would be considered. The review came as the bank reached 125 years of unbroken service on the Rock. Perhaps not the best way to celebrate such a milestone.

Fears and expectations grew in equal measure as the outcome of the review approached in June only for the review period to be extended. In the intervening months your board established a sub-committee dedicated to lobby the bank both locally and at board level in the UK to minimise any cutbacks. Considerable effort and time was expended by the Chamber to explore every possible avenue with the bank, the governments of both Gibraltar and UK, MPs in London as well as others in an attempt to persuade the bank of the significance of its continued presence in Gibraltar and the value and profitability of Gibraltar to the Bank.

But it was not to be. The bank announced that as a result of a review of all its operations in the Barclays Wealth brand around the world, the Main Street branch would close and by October 2014 and the Bank would be left with a token presence in the jurisdiction. It became clear that Gibraltar was one of over 30 jurisdictions which would suffer the Barclay’s axe. The fall-out from the 2008 financial crisis continues to affect communities far and wide.

Retail customers and corporate customers really only had one option: move their business to Natwest. Many already had accounts there and others

tried to open ones as soon as they could. The management and staff at Natwest did their best to cope but concentration risk quickly became an issue. Jyske Bank has also played its part in terms of its offering to the corporate sector but its criteria are at times more selective than a conventional UK high street bank.

The Gibraltar government moved swiftly in response and by the year end it had announced that it would look to set up a locally-owned and controlled bank, the Gibraltar International Bank using the appropriate mnemonic GIB. By its own admittance the Government was not keen to get into the banking business but there are wider issues of national importance at stake.

A fully functioning financial services sector requires a full range of banking facilities. as do local businesses who need to pay staff, suppliers, tax as well as send payments abroad.

The details are sketchy as we go to press but the Chamber understands that good transitional arrangements are being established between Barclays and the GIB and it is set to open as Barclays winds down. Some staff have been hired from Barclays already and there is good understanding as to the importance of providing a seamless transition for clients. This will help minimise the disruption.

Albert Isola the new Minister for Financial Services has had a baptism of fire in his first six months in government and appears to be dealing with a multitude of challenges effectively and with speed. Coming from a commercial background he fully understands the importance of moving quickly to address concerns as they arise.

There remain a number of questions for members about banking provision in Gibraltar. The Barclays affair has given Gibraltar’s business community a jolt and a reminder that nothing is forever and self-reliance, as with so much else on the Rock, is often the best policy. Nevertheless, the old ways of doing things in much of finance such as payments by cheques or by cash are fast becoming outmoded elsewhere. The new local bank has a clean sheet and will not be encumbered by legacy issues so instead of adopting traditional practices it should fully embrace all the opportunities which modern technology has to offer. This will be to the benefit of Gibraltar overall.

It is also worth taking the opportunity to create something that is truly embedded in to the local community. The days of the larger international banks being able to cut their cloth to match local needs are over as global institutions pay more attention to the need to be seen to be consistent in applying risk models across all their operations in ways that make local nuances impossible to support.

A more local, perhaps regional institution is likely to be much better at delivering local solutions. The GIB is an important initiative that has been forced upon a Gibraltar Government which has risen to the occasion. Nevertheless it is important that whilst Government provides the initial impetus it quickly steps back and ensures the new operation is entirely independent of Government influence and is run on entirely commercial lines.

Go

rdo

n B

ell /

Shu

tter

sto

ck.c

om

22

FUNDSGibraltar continues to see a steady increase in the number of registered Experienced Investor Funds (EIFs) setting up in the jurisdiction. By the end of 2013 there were 94 EIFs registered in Gibraltar and when one includes the number of sub-funds the level of funds under management in Gibraltar is valued at £2.7 billion. Many EIFs in Gibraltar are structured as protected cell companies, each with a number of sub-funds or cells, statutorily segregated from each other. Including the various cells in the PCCs, Gibraltar has roughly 200 fund strategies in operation.

Gibraltar EIFs invest globally in a wide range of asset classes. Almost half of Gibraltar’s EIFs are structured as hedge funds investing in tradeable securities, commodities and currencies. The remaining funds mainly run real estate, private equity and fund of fund strategies. Non vanilla or exotic investment strategies make up just 9% of EIFs.

Fund Administration

Fund administration in Gibraltar has enjoyed a sharp increase in the number of funds and capital managed since the sector’s humble beginnings in 2006 when only 20 investment funds were administered in the jurisdiction. There are now ten licensed fund administrators in Gibraltar and they administer 218 funds valued at £3.7bn. Gibraltar fund administrators comprise accountancy firms, specialist fund administrators and corporate service providers.

Funds also redomicile to Gibraltar from elsewhere due to similar factors which attract newly established funds to the jurisdiction – namely the fiscally effective legislative framework for funds and managers, robust regulatory standards, economic stability, accessibility, European time zone and the high quality professional services infrastructure.

Additionally, the pressure of the AIFMD

is likely to increase the harmonization of fund regulation across Europe. Alternative Investment Funds located outside the EU who need to market their funds to EU-based investors find Gibraltar an experienced and well-regulated jurisdiction in which to establish a European feeder fund structure. This addresses the restrictions on fund managers marketing non-EU domiciled funds in Europe and provides funds with an EU marketing passport based on AIFMD. However, as the June 2014 deadline for full AIFMD approaches there are still around one fifth of fund managers who are not in a position to comply with the new rules of the directive. These managers run the risk of falling foul of the new regime as applications can cause significant delays.

All non-UCITS funds domiciled in the EU will eventually have to register with a local regulator or regulators and all non-UCITS funds managed by an EU

23

based manager, wherever the fund is domiciled, will also eventually be subject to registration, even if the fund managed is out of scope of AIFMD.

Once AIFMD is in full force, the choice of whether fund managers manage vehicles domiciled and regulated in an EU location will be important. Historically, Dublin and Luxembourg have been preferred jurisdictions for funds. But the drawbacks of these two centres have been rising costs and limited capacity of existing providers. Gibraltar offers a cost-effective and experienced alternative and critically it is within the EU.

The renewed vigour and focus on marketing Gibraltar’s Finance Centre will continue to generate new business for the funds sector and this coupled with the marketing efforts of individual firms and by the association, the GFIA, Gibraltar will continue to be an attractive jurisdiction for the funds industry.

24

ONLINE GAMING

The UK’s draft Gambling Bill and Finance Bill are in advanced stages as part of the UK government’s plans to introduce a point of consumption (POC) regime to licence, regulate and tax all remote gambling firms operating in the UK market. The UK government’s proposals are supposedly intended to protect consumers and provide a fairer basis for competition. The reality is that they have not been thought through properly as they are likely to harm rather than protect consumers, undermine the competitiveness of responsible regulated operators and also reduce the expected receipts to UK Treasury. The Gibraltar Betting & Gaming Association (GBGA) has previously advised the UK that it may seek judicial review on the POC regime if the UK government goes ahead as planned. Any judicial review challenge would need to be undertaken very quickly once the Gambling Bill achieves Royal Assent to be in the spring of 2014.

The POC proposals suggest UK regulations apply to all operators who will now need to be directly licensed by the

UK Gambling Commission. Tax will be levied against operators based outside the UK transacting with UK customers – all in an attempt to create a level playing field in the UK industry. However, without some modification the current proposals will create a chain of confused regulatory supervision and market disruption that will only benefit those operators based outside British jurisdiction and its overseas territories. The UK punter will be the loser.

The GBGA is concerned that the UK government and the Gambling Commission cannot oversee remote operators effectively if they do not have local oversight of a UK nexus or mutual recognition with effective local regulators in the territory where the operator is based. Such operators may be based anywhere in the world including in places having no legal and cultural fit with the UK and where UK consumers and the UK Gambling Commission will have no effective rights of redress and enforcement.

The POC regime will result in an increase in remote regulatory supervision, with

foreign operators obtaining a UK licence to transact with UK consumers but without the UK having any real ability to properly supervise those operators. The GBGA also believes the proposals will also result in a large number of UK licensed but entirely unregulated and untaxed foreign operators buying a British licence merely as a ‘flag of convenience’. Such operators will use their UK brand in order to supply consumers outside of the UK with gambling services without any UK supervision or taxation.

Gibraltar has developed a world leading internationally recognised centre of excellence in online gambling, where operators provide customers with a safe and secure environment in which to bet. The UK punter has considerable trust in Gibraltar licensed operators and have voted with their feet. The POC regime proposals would undermine the local licensing regime here and it abandons the recognition of licences and local supervision by suitable jurisdictions such as Gibraltar.

In the online gambling world, price and

25

promotions are key and with limited brand loyalty and almost unlimited choice of suppliers based around the world punters will follow the best value. Therefore, there is a real danger that consumers will be captured by black market affiliates and operators, who are able to offer better value as they will not play the UK’s POC licensing and taxation regime. This has been clearly supported in a report by Deloitte, which found that even with a point of consumption tax at a rate of 10 per cent, 27 per cent of consumers would drift into the black market. The evidence that a POC regime with a high tax rate will put the consumer at real risk is overwhelming. For example, in Italy there is point of consumption licensing and tax and the Italian regulator estimates that up to 50 per cent of the market is unregulated (and therefore also untaxed). In France, the situation is even worse and it has been estimated that 70 per cent of sports betting takes place with unlicensed regulators. The UK government’s own analysis proceeds on the basis that approximately 20 per cent of the UK

market will be unregulated and would not pay UK gaming duties under its own taxation proposals.

UK consumers will not be winners under the current proposals. The UK government’s stated public policy aims and its wider policy objectives could be much better met with a more carefully constructed POC regime that took account of the existing online gambling eco-system and sought to ensure it was not seriously undermined in any transition.

The potential effect of these proposals on the territory of Gibraltar itself should also not be under-estimated. Currently only a small number of gambling firms have been allowed to obtain a licence here and yet we have an estimated 60 per cent of all bets placed by UK consumers through these operators. The online gambling industry is a significant contributor to Gibraltar’s economy, comprising more than 20 per cent of total GDP and an estimated 11 per cent of its total workforce. The damage to Gibraltar of the proposed POC regime, both in terms of economic

output and total employment, could be very significant.

In addition, whilst the UK has consistently stated that Gibraltar has an excellent regulatory regime, we are mindful of the potential for the POC regime to be purposefully misused and mistaken as a disavowal by the UK of Gibraltar’s outstanding regulatory reputation in this field.

The GBGA has tried to engage in a constructive dialogue with the UK government to ensure that they create legislation that actually helps the regulated gambling industry, the government and, most importantly, the consumer. Given the regulatory experience and expertise that exists on The Rock, we are well placed and willing to help the UK make the move to a world leading regulatory environment for online gambling. Effective supervision of the online gambling sector requires greater cross-border regulatory cooperation, recognition and oversight, not less.

“Gibraltar hasdeveloped a world

leading internationallyrecognised centre of

excellence in online gambling”

ENVIRONMENTGibraltar has always lagged behind the rest of Europe in matters to do with the environment which is understandable given its unique situation and the various constraints both physical and political that this has placed on the community.

It is therefore unsurprising that at the last election, the environment was one of the topics at the top of the political agenda. However, this in itself, whilst undoubtedly well intentioned, has the potential of turning into another one of those political footballs that often results in slow progress at best and confusion at worst. The advantage which Gibraltar has is that being small we can move quickly to address issues. The political challenge is to be clear in one’s policies and whilst some may be unpopular have the tenacity to tough it out. Unfortunately the benefits of addressing climate change are unlikely to be enjoyed after a single term of political office. But this increasingly contentious issue trumps politics. We all have a responsibility to act on this.

Since it was elected in 2011 the government has certainly made progress in creating public awareness

with such events as the Thinking Green conference in 2012 but real tangible changes have been few and far between. Perhaps this is why in 2013 the government has taken the further step of setting up the Climate Change Task Force which is chaired by the Deputy Chief Minister and consulted by Mr Geoff Lye, who is an expert in this field and holds a Research Fellowship at Green College, Oxford. Your President has been invited to form part of the committee as business has an important responsibility and role to play in helping to protect and improve the environment that we work and live in.

The Chamber welcomes the setting up of the Climate Change Task Force but it is of paramount importance that it should recognise the need to sustain competitiveness, jobs and investment. All parts of the community including business should be consulted and allowed ample time to adapt if sustainability is to be achieved. One area of concern is in onshore storage for bunkers. for example, that due to lack of action in the past on the development of onshore bunker storage, the more

current issue of capacity in the port and the government’s decision not to open up the East side anchorage even on a limited temporary basis to alleviate the problem, has led to a decline in volumes after a decade of growth, only for Gibraltar’s competitors to pick up the business.

Whilst the Government would appear to have made the greenest possible choice given the circumstances for the new power station, traffic is another matter of concern. One has to question whether our politicians across the political spectrum have the will to tackle this issue responsibly. Surely building more car parks is not the responsible, long-term and greenest solution.

Clearly businesses will not only need to adapt and change but must also make substantial investment to make the necessary changes if they are to make a positive contribution towards the Government’s aspirational policy of a carbon neutral Gibraltar. However if real progress is to be made the Government will need to stretch itself to offering financial subsidies as opposed to just offering small tax breaks.

26

PORT & SHIPPING

The importance of this sector to our community

Sr. Garcia Margallo’s words “The party’s over” were received in Gibraltar as part and parcel of his, and the PP’s vociferous manner of expression, when it comes to Gibraltar related matters.

Most, if not all of the fronts the Spanish Govt have been attacking Gibraltar on, despite the difficulties each of them present, may be legally and morally defendable, however the one on bunkering arises out of a process in which the British Government were apparently caught napping, with respect to the EU’s allocation of Spanish management of British Gibraltar Territorial Waters, under the Special Area of Conservation (SAC) within the EU Habitats Directive.

Many sometimes wonder why this sector, which is defined as one of the pillars of our economy is so important to Gibraltar. They question what benefits our economy receives from it and some argue that the only beneficiaries are the few bunker suppliers.

In an attempt to highlight the importance of this business field and the seriousness that should be attached to securing it’s continued prosperity, it was considered opportune in this year’s report to take a few minutes to analyse and understand who derive benefits out of this industry and how it helps Gibraltar’s economy.

In addition to the main firms directly involved (i.e. the bunker suppliers,

view bunkering last year was the main purpose of call for over 75% of all ships calling Gibraltar Port) and the Port Authority/Pilots, who receive the pertinent Dues and Charges for these ship calls, the below also derive direct benefits out of Gibraltar’s Maritime industry. For this, we should highlight several categories by way of direct and indirect involvement in this sector.

It is hard to produce any exact figures on number of companies directly or indirectly involved, but whern a vessel calls at Gibraltar there could be well over 20 companies that might be involved in providing goods or services to that single vessel.

The following is an inexhaustive list of Shipping dependant companies additional to the bunkering companies and the Port Authority itself:

Pilots: employing 8 persons

Ship agents: last count, 23 operating licences

Bunker suppliers: Five main physical suppliers operating

Rope Handlers: 2 companies operating

Luboil Suppliers: Several leading brands delivering at Gibraltar.

Launch and Barge Operators: Several companies operating, one of which does not provide ship agency services or other shipping related services, and is therefore totally dependant on this line of business.

Tug Operators: There is one main company dedicated to harbour towage and berthing/unberthing assistance services and a couple of others offering alternative tug support services.

Stevedores: There is one company operating in this field.

Shipchandlers: There are nine operational licences, with three companies exclusively dedicated to this service.

Fendering and STS Operators: There are three companies offering these services.

Counter Pollution Services: There are two companies operating in this field.

Surveyors: There is at least one company which is totally dedicated to the provision of services to the Maritime industry.

Chart Agency: Just the one company dedicated to this service, which could make Gibraltar totally dependant on a hinterland port on this service if this one disappeared.

Underwater cleaning and repairs: there are several companies operating in this field.

Slop handling installation

27

“there could well be over 20 companies that might be

involved in providing goods or services to that single vessel.”

29

PORT & SHIPPING

Year Cruise Ships Cargo Bunkers Repairs Off Limits Other Total No Calls Gross Tonnage

2008 222 253 5965 154 2006 301 9749 288,409,608

2009 238 193 6712 132 1460 543 10042 276,370,000

2010 175 178 6724 128 1365 505 11134 258,148,181

2011 187 164 6181 117 1492 597 10350 275,168,505

2012 173 161 6362 127 1259 444 9581 277,483,060

2013 180 164 5988 115 1175 248 9140 253,843,589

2013 Analysis (Source: Gibraltar Port)

Highly involved companies in Shipping generated Business:

Customs Clearance and Transport - There are several companies involved in this line of business, we have been in contact with the leading company in this field who informs us that 40% of their business is Shipping related, with a third of his 26 strong staff directly employed to cater for this service.

Hotels: Several hotels derive a good part of their business from the Maritime industry. We have been in contact with two of the main operators and confirm that one of them derives 55% and the other a 27% of their businesses from this sector.

Airlines: Official figures available of crew members, or shipping related personnel, arriving/departing by air directly into/out of Gibraltar are restricted to just those who are visa nationals. Using this as a base for estimating those non-visa nationals, a conservative estimate would be that between an 8.5 to 10.5% of airline seats are occupied by shipping related personnel.

Taxi Association: All crew movements

for the majority of ship agents are carried out by the Taxi Association, usually at a premium to the rates charged to the general public.

Waste Management and Refuse Collection: There are several companies involved in this service.

Repairers: There are several companies providing electronic, electric and other types of general repairs to ships, other than those provided by Messrs. Gibdock.

Courier Companies: Ships continuously receive and send courier packages (including fuel samples for analysis), we have been in contact with one of the main ones who inform us that approximately half of the weight handled by them is shipping related business.

Airfreight: A considerable proportion of the business undertaken these days in/out of Gibraltar is shipping related.

Doctors, Dentists, Hospital and Pharmacies: Gibraltar has traditionally been one of the best ports in the Med for Medical assistance to shipping with a substantial amount of business derived

by service providers in this sector.

Gasses and Chemicals: Additional to stores and provisions normally supplied by Shipchandlers, there are also companies who derive some business out of the delivery of these items.

Lawyers & Ship Registration Agents: Several companies provide a variety of services to this business sector including the valuable ship arrest business.

Maritime Training: There is one company offering services.

Additionally there could be a number of others e.g. carpet cleaning, pest control companies, Postal Services, newsagents etc. who also receive business occasionally.

The above is without taking into consideration the cruise liner calls and the obvious benefits within that market.

In summary the port generats considerable direct and indirect business for local companies. Although the port is small by international standards its dynamism makes it a critical part of the Rock’s economic infrastructure.

Bunkering

Volumes of bunkers delivered are down for a third consecutive year. This was to be expected due to a number of reasons, amongst them the continuing recession. However, what needs to be considered and closely monitored is the decrease in bunker calls being attributable to the Vopak Terminal at neighbouring Algeciras since it came into operation last March.

The construction of this 403,000 CBM terminal has brought new players into Algeciras. Where there had traditionally been only two physical suppliers, now there are six, some of whom are also still

operating in Gibraltar. Moreover, it was recently announced that an extension to the terminal, doubling it’s size had been approved by Algeciras Port Authority. Furthermore, there are also confirmed plans for the constructions of yet another terminal, similar in size to the current Vopak Terminal, in the area, by another renowned organisation.

Floating storage at Gibraltar has been reduced to two vessels, one of which has been shifted from it’s anchorage position to alongside the Detached Mole. On the one hand this will free up badly needed anchorage space for callers to the port, but on the other hand will greatly diminish berth capacity

for ships wishing to undertake their own repairs at a lay-up berth. It also reduces available berthing for vessels being placed under arrest, all of which brings about lucrative business to Gibraltar.

As was included in our report last year, renewed consideration should be given to the construction of onshore storage facilities. It is obvious that having large shore tank facilities permits operators to purchase fuel parcels on a large scale, allowing them better margins than those who require to purchase smaller quantities and have to endure the overheads of having to operate a floating storage. This and other possible circumstances could see

30

PORT & SHIPPING

these operators seek onshore storage facilities elsewhere, making Gibraltar reliant and dependant on hinterland facilities, which could prove very detrimental to the local bunkering trade.

The only positive side for Gibraltar on the construction of so many onshore storage facilities in the hinterland, is that they would require substantial anchorage ground and quick turnarounds to ensure a cost effective throughput. This is something they are lacking which would probably ensure that most of the suppliers would continue keeping an ongoing operation at Gibraltar.

The Chamber feels that government should actively seek a solution to this situation, through willing investors. Once more we reiterate that the primary reason for 75% of calls to the port are for bunkers and this generates significant additional business for other local companies directly and indirectly.

Cruise Liners

The Cruise industry has experienced a slight improvement from the previous year irrespective of the circumstances and problems encountered by some operators. Despite these difficulties, government, through their marketing initiatives and strategies, has managed to succeed in their aims of maintaining and even improving figures over the previous year this is to be welcomed.

Although Gibraltar receives substantial cruise passenger repeat business each year, it is also a fact that cruise operators would like to see an increase in numbers of passengers participating in excursions. This would obviously also be beneficial for Gibraltar as a whole. There have been innovations and improvements to the shore excursion

product, but much more needs to be done in order to achieve a product that would achieve a level of excellence which exceeds the visitors expectations.

Ferry and Cargo services

Cargo related calls have increased very slightly equalling the 164 calls of 2011. However, what is interesting to note is that despite the negative expectations, given the recession, container numbers are slightly up to 407 Teu’s as compared to 390 the previous year. Perhaps, the reason for this increase might be directly related to the uncertainties at the frontier, but whatever the reason, no efforts should be spared in attempting to increase this trend and maintaining a regular liner service. government might do well in considering incentivising traders for carriage of goods by sea.

Ship to Ship transfers

As was to be expected, the reigning in of these operations to within port limits as opposed to offshore at the end of 2012, has seen one of the operators opting to stop operating completely at Gibraltar. A second operator maintains the harbour fender for hire and others also keep equipment at hinterland ports, from where they continue providing offshore services. Yet not all has been negative as there have been STS operations carried out within the sheltered waters of the Bay, with a certain frequency, which does generate income to the Port whereas before this was restricted to a ship entering to collect the fenders and hoses.

Other Services

Gibdock continues being busy and even though there seems to have been a small decline in the number of vessels calling for repairs, it does not mean

that the actual overall volume of work undertaken has varied.

Several Board members of the Chamber have been working closely with government, Port Authority, HM Customs and the Income Tax Dept in an attempt to stamp out any activities by foreign companies operating illegally within Gibraltar.

At a GPOA dinner the government announced some cuts to Off Port Limits (OPL) fees, with the aim of countering advantages at competing ports. However it is felt that these do not go far enough to make these operations competitive enough against these ports, where no fees are applicable. This matter should be addressed at the earliest possible opportunity. There are indications that some chandlers with a presence in both ports on this side of the Straits are diverting business to Algeciras in order to take advantage of this issue.

Crew changes

Substantial crew changes are effected each year at Gibraltar, with 5,225 crew members/personnel having arrived in Gibraltar during 2013 via London, principally due to Schengen Visa requirements for some nationalities to travel via Spain. This means that since most of these personnel arriving are replacing others, the total number of ships’ personnel arriving/departing via Gibraltar airport must have been in the region of 10,450, with a conservative estimate of 90% requiring hotel accommodation for at least one night but often more. Additionally there are those crew members that arrive via the land frontier, which are difficult to quantify but could well be an additional 5000 persons, plus personnel also

31

arriving by air. Whatever the total, these are transferred locally by the Taxi Association, upto 4 times if they require hotel accomodation (Airport or Frontier to Hotel and then Hotel to pier for those arriving, then from pier to Hotel and Hotel to Airport or Frontier for those repatriating). It is worth mentioning that in the majority of cases Shipowners take advantage that the ship is calling at Gibraltar to effect these crew changes. Were they to call Algeciras or Ceuta

and have Visa difficulties, due to their Nationality, they would probably defer the changes until the vessel reaches the load or discharge port. We have to make the most of Gibraltar’s unique advantage in this respect and continue to market the benefits of Gibraltar to ship owners and to charterers worldwide. However, there is one point that government should take into consideration in respect to these crew changes, which is the lack of a budget

hotel for seafarers. This situation will only deteriorate if one of the most popular hotels currently catering for this market, were to disappear. It is critical that serious thought is given to this issue so that the port does not lose any more business.

“We have to make the most of Gibraltar’s unique advantage in this respect and continue to market the benefits of Gibraltar to ship owners

and to charterers worldwide”

32

TOURISM

Some of the key data available does not paint a pretty picture and show the impact of the heightened frontier issues since the end of July. They also highlight

a significant downturn in coach and private car visitors in the second half of the year. The knock-on effects to Gibraltar’s economy are being felt

directly by many traders but businesses in other sectors are also feeling the effects of reduced trade.