ann joo 120220 - i3investorklse.i3investor.com/files/my/ptres/res6064.pdf · ann joo is one of only...

TRANSCRIPT

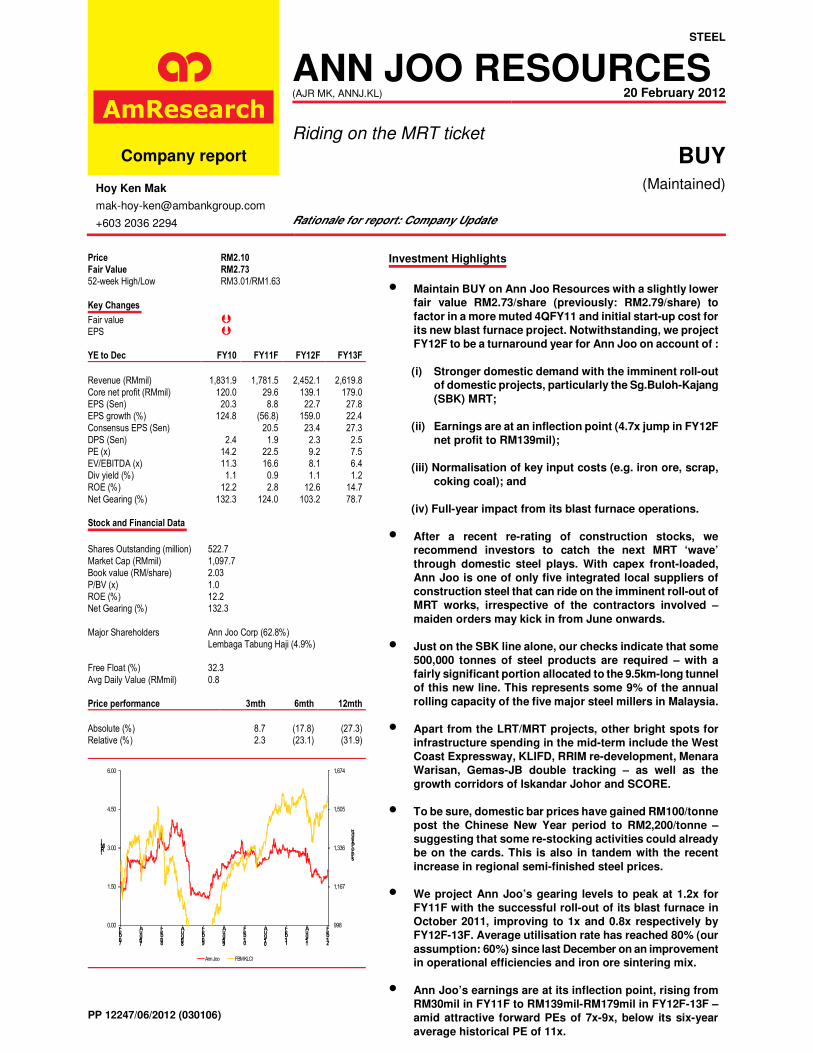

STEEL

ANN JOO RESOURCES (AJR MK, ANNJ.KL) 20 February 2012

Riding on the MRT ticket

Company report BUY

Hoy Ken Mak

+603 2036 2294

(Maintained)

Rationale for report: Company Update

Price RM2.10

Fair Value RM2.73

52-week High/Low RM3.01/RM1.63

Key Changes

Fair value �

EPS �

YE to Dec FY10 FY11F FY12F FY13F

Revenue (RMmil) 1,831.9 1,781.5 2,452.1 2,619.8

Core net profit (RMmil) 120.0 29.6 139.1 179.0

EPS (Sen) 20.3 8.8 22.7 27.8

EPS growth (%) 124.8 (56.8) 159.0 22.4

Consensus EPS (Sen) 20.5 23.4 27.3

DPS (Sen) 2.4 1.9 2.3 2.5

PE (x) 14.2 22.5 9.2 7.5

EV/EBITDA (x) 11.3 16.6 8.1 6.4

Div yield (%) 1.1 0.9 1.1 1.2

ROE (%) 12.2 2.8 12.6 14.7

Net Gearing (%) 132.3 124.0 103.2 78.7

Stock and Financial Data

Shares Outstanding (million) 522.7

Market Cap (RMmil) 1,097.7

Book value (RM/share) 2.03

P/BV (x) 1.0

ROE (%) 12.2

Net Gearing (%) 132.3

Major Shareholders Ann Joo Corp (62.8%)

Lembaga Tabung Haji (4.9%)

Free Float (%) 32.3

Avg Daily Value (RMmil) 0.8

Price performance 3mth 6mth 12mth

Absolute (%) 8.7 (17.8) (27.3)

Relative (%) 2.3 (23.1) (31.9)

998

1,167

1,336

1,505

1,674

0.00

1.50

3.00

4.50

6.00

Feb-07

Aug-07

Feb-08

Aug-08

Feb-09

Aug-09

Feb-10

Aug-10

Feb-11

Aug-11

Feb-12

Index Points

(RM)

Ann Joo FBM KLCI

PP 12247/06/2012 (030106)

Investment Highlights

• Maintain BUY on Ann Joo Resources with a slightly lower

fair value RM2.73/share (previously: RM2.79/share) to

factor in a more muted 4QFY11 and initial start-up cost for

its new blast furnace project. Notwithstanding, we project

FY12F to be a turnaround year for Ann Joo on account of :

(i) Stronger domestic demand with the imminent roll-out

of domestic projects, particularly the Sg.Buloh-Kajang

(SBK) MRT;

(ii) Earnings are at an inflection point (4.7x jump in FY12F

net profit to RM139mil);

(iii) Normalisation of key input costs (e.g. iron ore, scrap,

coking coal); and

(iv) Full-year impact from its blast furnace operations.

• After a recent re-rating of construction stocks, we

recommend investors to catch the next MRT ‘wave’

through domestic steel plays. With capex front-loaded,

Ann Joo is one of only five integrated local suppliers of

construction steel that can ride on the imminent roll-out of

MRT works, irrespective of the contractors involved –

maiden orders may kick in from June onwards.

• Just on the SBK line alone, our checks indicate that some

500,000 tonnes of steel products are required – with a

fairly significant portion allocated to the 9.5km-long tunnel

of this new line. This represents some 9% of the annual

rolling capacity of the five major steel millers in Malaysia.

• Apart from the LRT/MRT projects, other bright spots for

infrastructure spending in the mid-term include the West

Coast Expressway, KLIFD, RRIM re-development, Menara

Warisan, Gemas-JB double tracking – as well as the

growth corridors of Iskandar Johor and SCORE.

• To be sure, domestic bar prices have gained RM100/tonne

post the Chinese New Year period to RM2,200/tonne –

suggesting that some re-stocking activities could already

be on the cards. This is also in tandem with the recent

increase in regional semi-finished steel prices.

• We project Ann Joo’s gearing levels to peak at 1.2x for

FY11F with the successful roll-out of its blast furnace in

October 2011, improving to 1x and 0.8x respectively by

FY12F-13F. Average utilisation rate has reached 80% (our

assumption: 60%) since last December on an improvement

in operational efficiencies and iron ore sintering mix.

• Ann Joo’s earnings are at its inflection point, rising from

RM30mil in FY11F to RM139mil-RM179mil in FY12F-13F –

amid attractive forward PEs of 7x-9x, below its six-year

average historical PE of 11x.

Ann Joo Resources 20 February 2012

AmResearch Sdn Bhd 2

MAINTAIN BUY ON ANN JOO

� Turnaround year

We maintain our BUY recommendation on Ann Joo

Resources with a slightly lower fair value RM2.73/share

(previously: RM2.79/share), but with our target PE lifted by

a notch to 12x.

While the lower fair value is to account for start-up cost in

its blast furnace which was successfully commissioned in

4QFY11, we raise our target PE to account for better

demand prospects with an expected re-acceleration of

domestic contract flows.

We expect FY12F-13F to be turnaround years for Ann Joo,

particularly the latter. Key reasons are:

(i) The group would reap a full-year impact from its new

plant;

(ii) Domestic steel demand should be on the ascendency,

particularly with the roll-out of the MRT project

(iii) A normalisation of key input costs (e.g. coal, scrap,

iron ore) since 4QFY11.

The key risk in our view is a deterioration in global macro

conditions within the Eurozone and slower-than-expected

economic growth in China.

TURNAROUND YEAR

� Order flows are returning

We draw comfort that domestic steel demand remained

relatively stable in 2011 despite an apparent lack of large-

scale infrastructure projects, delays in some others and

worsening global macro positions towards the second half

of last year.

In fact, our channel checks indicate that the average

utilisation of the major rolling mill players in Malaysia

was still a respectable 70%-75% on average.

Progress on select infrastructure projects is expected to go

into full-swing this year (e.g. Ipoh-Rawang double tracking

project, Second Penang Bridge, Klang Valley LRT

Extension works).

On other hand, our optimism on order flows has been

further boosted by an imminent roll-out of other big ticket

jobs in the pipeline (Klang Valley MRT, West Coast

Expressway, Menara Warisan and the KL Integrated

Financial District, re-development of RRIM land, Gemas-

JB double tracking). This is in addition to rising

infrastructure activities within the SCORE and Iskandar

growth corridors in Sarawak and Johor respectively.

CHART 1: MRT STATION MAP

Source: SPNB, AmResearch

Ann Joo Resources 20 February 2012

AmResearch Sdn Bhd 3

RIDING ON THE MRT TICKET

� Bulk of major contracts to be awarded by 2012

Earlier this week, the MMC-JV Gamuda JV signed a

project delivery partner (PDP) agreement for the Sg.Buloh-

Kajang (SBK) MRT line. The JV will lead manage the

overall project in return for a 6% fee and allowable claims

for contingency cost of up to 15%. In addition, the JV

would receive ~RM2.8bil in reimbursement for overheads

and engineering-related fees (See Chart 1).

At the same time, MRT Co had also revealed details of the

entire 90 packages for the SBK line. These would include

information on when the tenders will be opened, its

evaluation and award periods, as well as the estimated

completion time of the said projects.

Excluding land cost of ~RM2bil, we estimate that there are

over RM20bil worth of construction jobs available. These

would include opportunities for ground works, mechanical

& electrical (M&E), ICT systems, viaducts and stations.

In August last year, the Federal government shortlisted 28

contractors for 25 work packages that consist of elevated

civil works, stations and depots (See Table 1).

MRT Co had indicated that the balance of over 80 work

packages should be awarded by year-end.

Thus far, preliminary works involving the relocation of

utilities and land clearing – in areas such as Sg.Buloh,

Semantan portal as well as Cochrane portal – have

commenced.

For the big packages, both IJM Corp and Ahmad Zaki

Resources (AZRB) had in February started the ball rolling

when they clinched the elevated contracts for Package V5

and V6 worth RM974mil and RM764mil, respectively, for

the above-ground sections in Cheras.

Not long after, Kim Lun Corp announced that the group

had been appointed as designated supplier of segmental

box girders (SBG) for certain parts of the SBK MRT line.

For the balance six packages under the elevated portion,

we understand that the bulk of them could be tendered out

by end-June. We also expect tenders for the stations (8

packages) and depots (2 packages) to be dished

progressively by 2Q 2012 to keep within the estimated

project dateline in July 2017.

For the underground works, the MMC-Gamuda JV has

reportedly submitted the lowest bid among the five

contractors shortlisted for the tunnelling works (~RM7bil-

RM8bil) – where a decision should be known by April.

� LRT extension gathering momentum

On the Klang Valley LRT extensions, a total of RM6.5bil

representing up to 90% of the project hasbeen awarded:

- Ampang line (RM2bil)

- Kelana Jaya Line (RM2.5bil)

TABLE 1: PRE-QUALIFIED COMPANIES FOR MRT ELEVATED WORKS

Elevated Civil Works (8 packages)

Open Category (5 packages)

1. Sunway Construction Sdn Bhd 1. Trans Resources Corp Sdn Bhd 1. Sunway Construction Sdn Bhd

2. Mudajaya Corp 2. Sunway Construction Sdn Bhd 2. Trans Resources Corp Sdn Bhd

3. Tran Resources Corp Sdn Bhd 3. Naim Engineering Sdn Bhd 3. Naim Engineering Sdn Bhd

4. Muhibbah Engineering (M) Sdn Bhd 4. Fajarbaru Builders Sdn Bhd 4. Muhibbah Engineering (M) Sdn Bhd

5. IJM Construction Sdn Bhd 5. IJM Construction Sdn Bhd 5. IJM Construction Sdn Bhd

6. Ahmad Zaki Sdn Bhd 6. Loh & Loh Construction Sdn Bhd 6. Fajarbaru Builders Sdn Bhd

7. MTD Construction Sdn Bhd 7. Muhibbah Engineering (M) Sdn Bhd 7. Loh & Loh Construction Sdn Bhd

8. MRCB Engineering Sdn Bhd 8. Gadang Engineering (M) Sdn Bhd 8. Gadang Engineering (M) Sdn Bhd

9. Gadang Engineering (M) Sdn Bhd 9. Pembinaan Mitrajaya Sdn Bhd 9. Kencana Torsco Sdn Bhd - Al Ambia JV

10. Loh & Loh Construction Sdn Bhd 10. WCT Bhd

11. 11. Kencana Torsco Sdn Bhd - Al Ambia JV

12. Konsortium PPC - WB JV (Putra Perdana

Const. & Worthy Builders S/B)

Bumiputra Category (1 package)

1. Naim Engineering Sdn Bhd 1. Trans Resources Corp Sdn Bhd 1. Trans Resources Corp Sdn Bhd

2. Trans Resources Corp Sdn Bhd 2. Naim Engineering Sdn Bhd 2. Naim Engineering Sdn Bhd

3. TSR Bina Sdn Bhd 3. TSR Bina Sdn Bhd 3. Ahmad Zaki Sdn Bhd

4. Ahmad Zaki Sdn Bhd 4. Ahmad Zaki Sdn Bhd 4. TSR Bina Sdn Bhd

5. HRA Teguh Sdn Bhd 5. HRA Teguh Sdn Bhd 5. HRA Teguh Sdn Bhd

6. MTD Construction Sdn Bhd 6. SN Akmida Holdings Sdn Bhd 6. Perkasa Sutera Sdn Bhd

7. Syarikat Muhibah Perniagaan &

Pembinaan Sdn Bhd7. Kembang Serantau Sdn Bhd 7.

Syarikat Muhibah Perniagaan &

Pembinaan Sdn Bhd

8. Zecon Sdn Bhd 8. Apex Communication Sdn Bhd 8. Dekon Sdn Bhd

9. Cergas Murni Sdn Bhd 9. Pembinaan Bukit Timah Sdn Bhd

10. Tidal Marine Engineering Sdn Bhd 10. Perkasa Sutera Sdn Bhd

11. Dekon Sdn Bhd

12. Syarikat Muhibah Perniagaan &

Pembinaan Sdn Bhd

Open Category (5 packages)

Bumiputra Category (3 packages)

Stations (8 packages)

Bumiputra Category (3 packages)

Konsortium Putra Perdana Const &

Worthy Builder JV

Depots (2 packages)

Open Category (1 package)

Source: SPNB, AmResearch

Ann Joo Resources 20 February 2012

AmResearch Sdn Bhd 4

- 20 new trains for the Ampang line (RM1bil)

- System works (including signalling and tele-

communication): RM1bil

TRC Synergy and the Bina Puri-Tim Sekata JV had earlier

won Package A of the civil works for the Kelana Jaya

(RM950mil) and Ampang lines (RM634mil), respectively, in

October 2010.

Then in August last year, both Sunway and MRCB won the

RM569bil and RM1.3bil contracts for the remaining portion

of works for both lines under Package B.

Meanwhile, some 20% of the main works along both lines

have commenced, with the Ampang and Kelana Jaya lines

due to be completed by October 2014 and December

2014, respectively. What will remain from the tendering

process are two stations and the main depot for the

Ampang line.

THE NEXT MRT WAVE – SUPPLIERS OF STEEL

� Maiden orders as early as June

We expect the rising proliferation of infrastructure roll-outs

– notably for the MRT/LRT projects – to prod a stronger re-

acceleration in domestic steel consumption from 2HFY12

onwards.

Under the Klang Valley MRT project, all procurement of

raw materials that would include steel is to be centralised

under MRT Co. With MRT Co in the picture, this would

effectively reduce collection risk among suppliers of local

steel.

Just on the SBK MRT alone, our channel checks

indicate that some 500,000 tonnes of steel products

are required – with a fairly significant portion allocated

to the 9.5km-long tunnel of this new line. This

represents some 9% of the annual rolling capacity of

the five major steel millers in Malaysia.

With this, we reckon that the maiden orders for steel will

come in thick-and-fast when the major MRT project work

packages are rolled-out in stages by the end of this year,

starting with the Package V5 and V6 (awarded to IJM and

Ahmad Zaki) elevated contracts and the supply of SBG by

Kim Lun.

� Another RM30bil in spending with additional two MRT lines

There is further upside for local steel consumption if the

Federal government approves another two new MRT plans

worth a combined RM30bil – i.e. Circle line and the

Sg.Buloh-Serdang line (which has an option to expand to

Putrajaya).

The project schedule is to be broken down as follows:-

(i) Underground portion (RM12bil): 2013-2019

(ii) Elevated portion 2020-2030 (RM18bil): 2020-2030

From our checks on the ground, MRT Co has already

outlined the designated corridors for development, and will

seek feedback from various stakeholders in order to

finalise the route alignment.

We gather that Cabinet approval is to be sought by early

next year. If everything goes as planned, both projects are

tipped to kick-off by 2H 2013.

Interestingly, the government’s priority is to complete the

underground portion of the both lines by 2020 to clear up

congestion within the KL city centre, where the bulk of the

tunnelling works would come from.

If approved, the front-loading of the underground portion

over the next eight years would prod a multi-year re-rating

TABLE 3: SCHEDULE FOR ELEVATED WORKS

Source: MRT Co, AmResearch

TABLE 2: SCHEDULE FOR STATION WORKS

Source: MRT Co, AmResearch

Ann Joo Resources 20 February 2012

AmResearch Sdn Bhd 5

in domestic steel consumption, where there is a higher

content of steel usage for tunnelling works.

� Ann Joo – top pick for leverage into Malaysian steel plays

After the recent re-rating of construction-related stocks, we

therefore recommend investors to catch the next MRT

‘wave’ through domestic steel plays for direct exposure

irrespective of the contractors involved.

With its capex already front-loaded, Ann Joo is one of

only five integrated local suppliers of construction

steel that is well-poised to ride on an accentuation in

demand – with the imminent roll-out of the MRT

project.

To be sure, domestic bar prices have gained

RM100/tonne post the Chinese New year period to

RM2,200/tonne – suggesting that some re-stocking

activities could already be on the cards. This is also in

tandem with the recent increase in regional semi-

finished steel prices.

EARNINGS AND RECOMMENDATION

� Earnings at inflection point

We are cutting our FY11F net profit forecast by 57% to

RM30mil. This is to account for:

(i) Start-up cost (e.g. depreciation, interest) that relates

to the commissioning of its blast furnace which was

successfully commissioned on 16 October 2011.

(ii) Write-down on certain higher-cost inputs (e.g. coking

coal) secured earlier during the plant’s kick-off

programme.

But we expect FY12F earnings to stage a strong recovery

(+3.7x) on an expected resurgence in domestic steel

demand, particularly with the LRT/MRT projects gathering

pace.

The upward momentum in earnings should extend further

to FY13F (+33%) and FY14F (+15%) when the cost-

savings improvements from its blast furnace begin to filter

through more meaningfully.

(1) Net gearing should peak in FY12F

With the successful roll-out of Ann Joo’s blast furnace –

costing ~RM650mil under Phase 1 – we expect Ann Joo’s

net gearing ratio to peak at 1.2x in FY12F, before

improving further to 1x and 0.8x, respectively, in FY13F-

14F.

Thus far, the average utilisation rate has reached 80% (our

assumption: 60%) since last December on an improvement

in operational efficiencies and iron ore sintering mix.

CHART 2: PB BAND CHART

Avg

+1s

-1s

0.0

0.6

1.2

1.8

2.4

3.0

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

(x)

CHART 3: PE BAND CHART

Avg

+1s

-1s

4.0

14.2

24.4

34.6

44.8

55.0

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

(x)

Ann Joo Resources 20 February 2012

AmResearch Sdn Bhd 6

CHART 4: ANN JOO HISTORICAL PE

PE µ, 11.4

PE +1σ, 19.1

PE -1σ, 3.6

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Feb

-06

Ap

r-06

Jun

-06

Au

g-06

Oct-0

6

De

c-06

Feb

-07

Ap

r-07

Jun

-07

Au

g-07

Oct-0

7

De

c-07

Feb

-08

Ap

r-08

Jun

-08

Au

g-08

Oct-0

8

De

c-08

Feb

-09

Ap

r-09

Jun

-09

Au

g-09

Oct-0

9

De

c-09

Feb

-10

Ap

r-10

Jun

-10

Au

g-10

Oct-1

0

De

c-10

Feb

-11

Ap

r-11

Jun

-11

Au

g-11

Oct-1

1

De

c-11

PE

(x)

Source: Bloomberg, AmResearch

Ann Joo Resources 20 February 2012

AmResearch Sdn Bhd 7

TABLE 2: FINANCIAL DATA

Income Statement (RMmil, YE 31 Dec) 2009 2010 2011F 2012F 2013F

Revenue 1,303.0 1,831.9 1,781.5 2,452.1 2,619.8

EBITDA 124.4 222.3 145.8 282.6 331.1

Depreciation (65.5) (65.4) (82.9) (93.2) (96.6)

Operating income (EBIT) 58.9 157.0 63.0 189 234.4

Other income & associates 0.3 0.4 0.0 0.0 0.0

Net interest (22.8) (17.4) (28.1) (25.9) (22.7)

Exceptional items 0.0 0.0 0.0 0.0 0.0

Pretax profit 36.3 139.9 34.9 163.5 211.7

Taxation (5.5) (19.3) (7.3) (24.4) (32.6)

Minorities/pref dividends 0.8 (0.6) 2.1 0.0 (0.1)

Net profit 31.6 120.0 29.6 139.1 179.0

Core net profit 31.6 120.0 29.6 139.1 179.0

Balance Sheet (RMmil, YE 31 Dec) 2009 2010 2011F 2012F 2013F

Fixed assets 873.7 1,078.9 1,116.6 1,103.9 1,047.9

Intangible assets 9.1 8.6 8.0 7.5 6.9

Other long-term assets 28.7 20.8 20.8 20.8 20.8

Total non-current assets 911.5 1,108.3 1,145.4 1,132.2 1,075.6

Cash & equivalent 31.8 61.6 43.6 74.7 128.3

Stock 882.0 1,239.0 1,120.4 1,099.6 1,097.3

Trade debtors 133.6 298.6 292.9 356.1 380.4

Other current assets 8.0 1.7 1.7 1.7 1.7

Total current assets 1,055.4 1,600.8 1,458.4 1,532.0 1,607.7

Trade creditors 128.8 142.4 134.4 208.0 219.5

Short-term borrowings 893.1 1,414.5 500.5 475.5 450.5

Other current liabilities 1.2 2.4 2.4 2.4 2.4

Total current liabilities 1,023.0 1,559.3 637.4 685.9 672.4

Long-term borrowings 0.0 46.6 860.6 785.6 685.6

Other long-term liabilities 22.9 28.4 28.4 28.4 28.4

Total long-term liabilities 22.9 75.0 889.0 814.0 714.0

Shareholders’ funds 906.6 1,060.0 1,064.8 1,151.6 1,284.2

Minority interests 14.3 14.7 12.6 12.6 12.6

BV/share (RM) 1.73 2.03 2.04 2.20 2.46

Cash Flow (RMmil, YE 31 Dec) 2009 2010 2011F 2012F 2013F

Pretax profit 36.3 139.9 34.9 163.5 211.7

Depreciation 227.5 (398.3) 254.9 289.3 287.8

Net change in working capital 150.6 (508.3) 116.4 31.1 (10.7)

Others 30.6 (44.2) 20.8 1.5 (9.9)

Cash flow from operations 283.1 (347.3) 254.9 289.3 287.8

Capital expenditure (130.9) (161.4) (120.0) (80.0) (40.0)

Net investments & sale of fixed assets 11.6 5.2 0.0 0.0 0.0

Others (0.2) 0.7 0.0 0.0 0.0

Cash flow from investing (119.5) (155.5) (120.0) (80.0) (40.0)

Debt raised/(repaid) (141.4) 568.0 (100.0) (100.0) (125.0)

Equity raised/(repaid) 0.0 0.0 0.0 0.0 0.0

Dividends paid (11.3) (33.9) (24.9) (52.3) (46.4)

Others (19.9) (0.8) (28.1) (25.9) (22.7)

Cash flow from financing (172.5) 533.3 (152.9) (178.2) (194.2)

Net cash flow (8.9) 30.5 (18.0) 31.1 53.6

Net cash/(debt) b/f 40.7 28.7 59.2 41.1 72.2

Net cash/(debt) c/f 31.8 59.2 41.1 72.2 125.9

Key Ratios (YE 31 Dec) 2009 2010 2011F 2012F 2013F

Revenue growth (%) n/a 40.6 n/a 37.6 6.8

EBITDA growth (%) n/a 78.7 n/a 93.8 17.2

Pretax margins (%) 2.8 7.6 2.0 6.7 8.1

Net profit margins (%) 2.4 6.6 1.7 5.7 6.8

Interest cover (x) 2.5 8.5 2.2 7.0 9.4

Effective tax rate (%) 15.2 13.8 21.1 14.9 15.4

Net dividend payout (%) 7.0 7.7 33.7 6.4 5.4

Debtors turnover (days) 39 43 61 48 51

Stock turnover (days) 263 211 242 165 153

Creditors turnover (days) 32 27 28 25 30

Source: Ann Joo, AmResearch

Ann Joo Resources 20 February 2012

AmResearch Sdn Bhd 8

Anchor point for disclaimer text box

Published by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

Printed by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

The information and opinions in this report were prepared by AmResearch Sdn Bhd. The investments discussed or recommended in this report may not be suitable for all investors. This report has been prepared for information purposes only and is not an offer to sell or a solicitation to buy any securities. The directors and employees of AmResearch Sdn Bhd may from time to time have a position in or with the securities mentioned herein. Members of the AmInvestment Group and their affiliates may provide services to any company and affiliates of such companies whose securities are mentioned herein. The information herein was obtained or derived from sources that we believe are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. No liability can be accepted for any loss that may arise from the use of this report. All opinions and estimates included in this report constitute our judgement as of this date and are subject to change without notice.

For AmResearch Sdn Bhd

Benny Chew Managing Director