amp retirement adequacy index€¦ · 1 amp retirement adequacy index the amp retirement index (the...

TRANSCRIPT

AMP Retirement Adequacy IndexSummary of trends July - December 2009

C o n t e n t S

executive Summary

1 overall Retirement Adequacy 2

2 Contribution Rates - comparative periods 3

3 Contribution Rates - 6 months to December 2009 4

4 Average Superannuation Balances - by age group 5

5 Retirement Balance estimate - by age group 6

6 estimated Retirement Income - by age group 7

7 Females - account balances by age group 8

8 Adequacy - workers above and below target 9

1

AMP Retirement Adequacy Index

The AMP Retirement Index (the Index) compares the savings of Australians against a target for an adequate income in retirement - set at 65% of an individual’s pre-retirement living standards. The Index uses data from more than 328,000 AMP members, along with estimates of the age pension (for those who qualify) and “other investments” (excluding the family home), to estimate whether Australians are on track for an adequate retirement.This issue of the Index draws on data for the 6 months from July to December of 2009.Following the recent announcements by the Government in response to the Henry Review’s final report, AMP has commissioned a second Index that models the effect the proposed changes would have. The proposed changes modelled are:

Increase in Superannuation Guarantee (SG) rate to 12% by 2019. Low income earner concessional contribution tax offset - this would equate to a maximum rebate of $500 for workers

earning up to $37,000 per annum, and A permanent increase in the concessional contribution cap for over-50s with superannuation balances less than $500,000.

This Index summary provides an overview of both the “before and after” picture of retirement adequacy as at 31 December 2009.

A tale of 2 adequacy outcomes...

The proposed increase in the Superannuation Guarantee (SG) to 12% announced recently by the Government in response to the Henry Review’s recommendations will have a significant impact on retirement adequacy.

However, prior to this announcement, average retirement adequacy had plummeted since our last report, falling to one of its lowest levels since the commencement of the Index.

While investment values continue to improve...

Strong gains in investment markets have seen average member balances increase by approximately 6% over the period. However, a fall in contribution levels has outweighed the improvements in investment balances, leading to an overall substantial fall in adequacy.

Changes in contribution rules prove most significant...

The 2009 Budget announcing cuts to the concessional contribution caps available for members appears to have had a real and immediate impact on voluntary contribution levels. Coupled with the cuts to the co-contribution scheme announced at the same time, members at either end of the income spectrum have curtailed their level of voluntary contributions, directly impacting on their ability to achieve adequate retirement savings through superannuation.

The future of superannuation...

The 2010 Budget announcements lifting the Superannuation Guarantee (SG) to 12% by 2019 and the low-income concessional tax rebate will stimulate a significant rise in adequacy for members. Based on current contribution levels, there is an immediate uplift of nearly 3% to 71.3%. However, the greatest beneficiaries will be those yet to enter the workforce, who - in the fullness of time - will be more likely to achieve overall adequacy rates closer to 75%.

Executive Summary

2

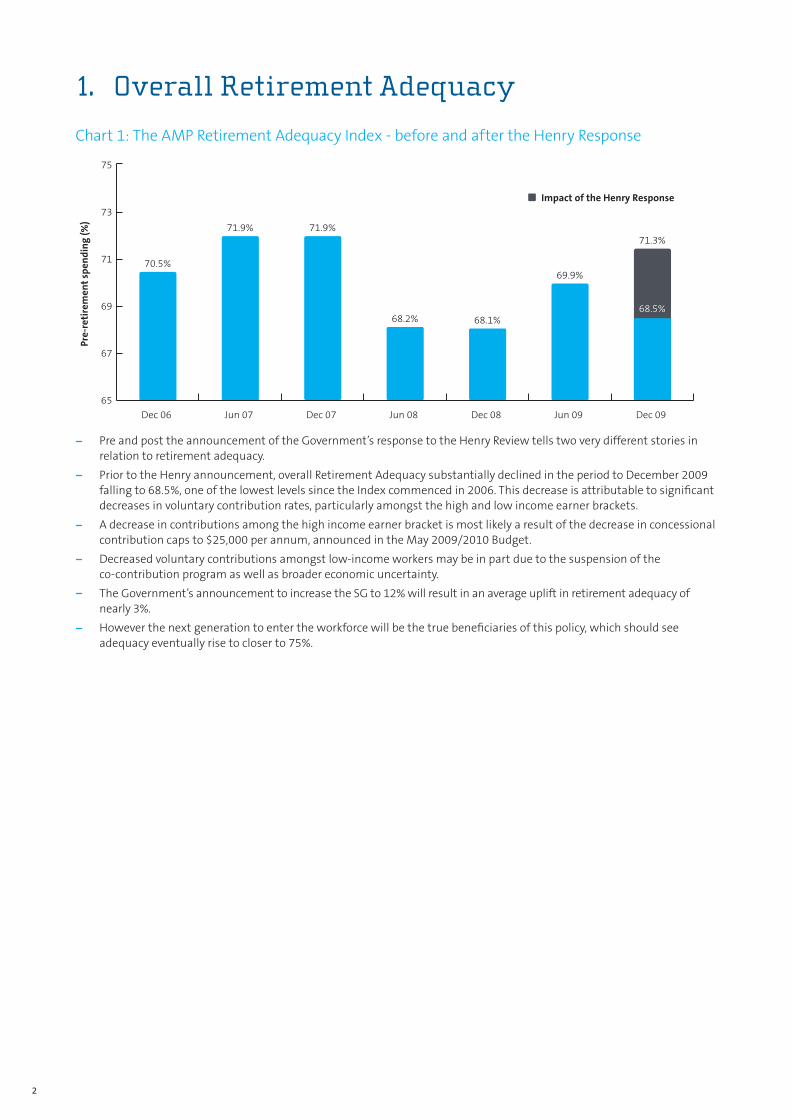

1. Overall Retirement Adequacy

Chart 1: The AMP Retirement Adequacy Index - before and after the Henry Response

Impact of the Henry Response

Pre-

reti

rem

ent

spen

din

g (%

)

65

67

69

71

73

75

70.5%

Dec 06 Jun 07 Dec 07 Jun 08 Dec 08 Jun 09 Dec 09

71.9% 71.9%

68.2% 68.1%

69.9%

71.3%

68.5%

Pre and post the announcement of the Government’s response to the Henry Review tells two very different stories in relation to retirement adequacy.

Prior to the Henry announcement, overall Retirement Adequacy substantially declined in the period to December 2009 falling to 68.5%, one of the lowest levels since the Index commenced in 2006. This decrease is attributable to significant decreases in voluntary contribution rates, particularly amongst the high and low income earner brackets.

A decrease in contributions among the high income earner bracket is most likely a result of the decrease in concessional contribution caps to $25,000 per annum, announced in the May 2009/2010 Budget.

Decreased voluntary contributions amongst low-income workers may be in part due to the suspension of the co-contribution program as well as broader economic uncertainty.

The Government’s announcement to increase the SG to 12% will result in an average uplift in retirement adequacy of nearly 3%.

However the next generation to enter the workforce will be the true beneficiaries of this policy, which should see adequacy eventually rise to closer to 75%.

3

2. Contribution Rates - comparative periods

TABLE 1: CONTRIBUTION RATES BY AGE, DECEMBER 2006 TO DECEMBER 2009

AGE DEC 06 (%) JUN 07 (%) DEC 07 (%) JUN 08 (%) DEC 08 (%) JUN 09 (%) DEC 09 (%)

20-24 10.1 11.0 10.1 10.3 10.1 10.0 10.0

25-29 10.2 11.0 10.2 10.4 10.3 10.1 10.4

30-34 10.7 11.4 10.6 10.7 10.4 10.2 10.5

35-39 10.8 12.4 10.9 10.8 10.8 10.5 10.6

40-44 11.3 16.7 11.6 11.4 11.5 11.4 11.3

45-49 13.7 17.7 12.8 12.2 12.1 12.1 11.9

50-54 14.4 21.5 16.0 14.3 13.7 13.9 13.4

55-59 18.1 28.4 19.4 18.2 17.6 18.4 17.7

60-64 21.6 40.0 25.0 22.2 22.8 23.5 21.3

65-69 25.5 56.5 24.4 25.7 25.6 28.6 25.1

All workers 12.6 17.2 13.0 12.6 12.5 12.5 12.4

Contribution rates fell overall due to decreases in contributions in all 40+ age groups. Slight increases in contribution levels in each age group under 40 have not been significant enough to offset impact of the decline among older workers.

The most significant falls in contributions have been recorded in the 60+ age categories with falls of 9.4% and 12.2% when compared to June 2009 contribution levels.

The halving of the transitional concessional contribution caps has impacted members aged 60+. This is likely to have been further compounded by the broader economic environment that has seen a reduction in the availability of part-time or casual work.

3. Contribution Rates - 6 months to June 2009

TABLE 2: CONTRIBUTION RATES BY AGE, DECEMBER 2009

AGE SUPER GUARANTEE (SG)/ AWARD (%)

SALARY SACRIFICE (%) AFTER TAX (%) TOTAL (%)

20-24 9.5 0.4 0.4 10.3

25-29 9.6 0.6 0.5 10.6

30-34 9.5 0.7 0.5 10.7

35-39 9.5 0.8 0.5 10.8

40-44 9.4 1.2 0.6 11.2

45-49 9.4 1.7 0.7 11.8

50-54 9.4 3.1 0.9 13.3

55-59 9.4 6.9 1.3 17.5

60-64 9.3 10.2 1.5 21.0

65-69 9.3 12.3 3.0 24.6

All workers 9.4 2.2 0.7 12.4

The overall contribution rate of 12.4% is marginally down on the same rate for the 6 months ending June 2009 (12.5%).

SG and salary sacrifice contribution rates have decreased by 0.1 and 0.2 percentage points respectively compared with the June 2009 period. These decreases were offset by a minor increase (0.1 percentage points) in after-tax contributions.

Substantial increases in contribution rates for workers under the age of 40 may be a reaction to the decreases in concessional contribution caps, however future editions of the Index will show whether this is a long-term trend.

4

4. Average Superannuation Balances - by age group

TABLE 3: AVERAGE SUPER BALANCES (9% SG) - ACTIVE MEMBERS, DECEMBER 2006 TO DECEMBER 2009

AGE BALANCE ($)

DEC 06 JUN 07 DEC 07 JUN 08 DEC 08 JUN 09 DEC 09

20-24 5,246 5,110 5,277 5,184 4,838 5,341 6,159

25-29 13,131 13,052 13,573 13,278 11,725 12,420 13,678

30-34 24,076 24,799 26,352 25,948 22,777 23,140 24,617

35-39 34,486 35,829 38,850 38,747 34,257 34,206 36,069

40-44 44,233 46,621 51,319 50,622 45,151 44,408 46,599

45-49 54,991 57,507 63,314 62,706 56,682 55,227 57,874

50-54 69,025 75,247 79,534 77,905 71,267 69,076 71,762

55-59 81,257 90,244 91,638 85,561 76,925 75,692 79,245

60-64 93,331 96,494 88,684 79,446 71,014 70,470 73,754

65-69 86,927 98,160 83,767 71,097 66,766 66,741 73,285

Average 39,663 42,226 44,013 42,651 38,447 37,939 40,132

In the 6 months to December 2009, super balances rose by an average of $2,192 per member, or 5.8%.

The increase in average super balances was mainly due to continued gains in the underlying value of investments.

Younger members saw the biggest gains in relative terms, while those aged 55 and over achieved the greatest dollar increases in super balances.

5

5. Retirement Balance Estimate - by age group

TABLE 4: AVERAGE ASSETS AT RETIREMENT (12% SG) - TODAY’S DOLLARS

AGE SUPER ($) OTHER ASSETS ($) TOTAL ($)

20-24 829,894 152,981 982,876

25-29 712,821 133,405 846,226

30-34 600,633 148,291 748,924

35-39 496,672 146,820 643,492

40-44 401,993 169,479 571,473

45-49 303,350 166,594 469,944

50-54 221,830 184,706 406,536

55-59 172,635 192,874 365,508

60-64 139,028 201,682 340,710

65-69 112,744 185,689 298,433

All workers 489,089 161,648 650,737

TABLE 5: AVERAGE ASSETS AT RETIREMENT (9% SG) - TODAY’S DOLLARS

AGE SUPER ($) OTHER ASSETS ($) TOTAL ($)

20-24 722,360 152,981 875,341

25-29 630,293 133,405 763,698

30-34 540,896 148,291 689,187

35-39 456,489 146,820 603,308

40-44 377,942 169,479 547,421

45-49 292,560 166,594 459,155

50-54 219,676 184,706 404,381

55-59 172,763 192,874 365,636

60-64 139,137 201,682 340,819

65-69 113,005 185,689 298,694

All workers 442,801 161,648 604,449

Increasing the SG to 12% would deliver an immediate uplift of an additional $46,000 in projected retirement assets.

However, without the increase in SG, projected average retirement assets fell nearly 1% since June 2009.

This projected decrease is a result of a significant fall (3.4%) in average superannuation savings, stemming from the diminished contributions levels seen during this period.

Average other assets increased 6.9% off the back of stronger investment performance during the 6 months to December 2009.

6

6. Estimated Retirement Income - by age group

TABLE 6: AVERAGE RETIREMENT INCOME (12% SG) - TODAY’S DOLLARS

AGE SUPER INCOME ($) OTHER INVESTMENTS ($)

AGED PENSION ($) INCOME TAX ($) NET RETIREMENT INCOME ($)

20-24 41,344 7,607 13,613 1,776 60,788

25-29 36,514 6,815 14,256 1,566 56,019

30-34 30,778 7,575 14,079 1,516 50,915

35-39 25,462 7,500 14,214 1,405 45,770

40-44 20,616 8,655 13,924 1,418 41,777

45-49 15,328 8,379 13,715 1,311 36,112

50-54 11,012 9,113 12,751 1,277 31,599

55-59 8,886 9,832 13,276 1,313 30,681

60-64 7,861 11,215 14,864 1,602 32,338

65-69 7,433 11,730 15,634 1,812 32,984

Average 25,008 8,299 13,909 1,505 45,710

TABLE 7: AVERAGE RETIREMENT INCOME (9% SG) - TODAY’S DOLLARS

AGE SUPER INCOME ($) OTHER INVESTMENTS ($)

AGED PENSION ($) INCOME TAX ($) NET RETIREMENT INCOME ($)

20-24 35,992 7,607 15,269 2,234 56,634

25-29 32,291 6,815 15,650 1,916 52,840

30-34 27,719 7,575 15,115 1,780 48,629

35-39 23,403 7,500 14,925 1,585 44,242

40-44 19,382 8,655 14,357 1,536 40,858

45-49 14,780 8,379 13,898 1,363 35,695

50-54 10,901 9,113 12,790 1,291 31,513

55-59 8,888 9,832 13,273 1,314 30,678

60-64 7,860 11,215 14,859 1,601 32,334

65-69 7,427 11,730 15,630 1,811 32,976

Average 22,646 8,299 14,682 1,711 43,915

7

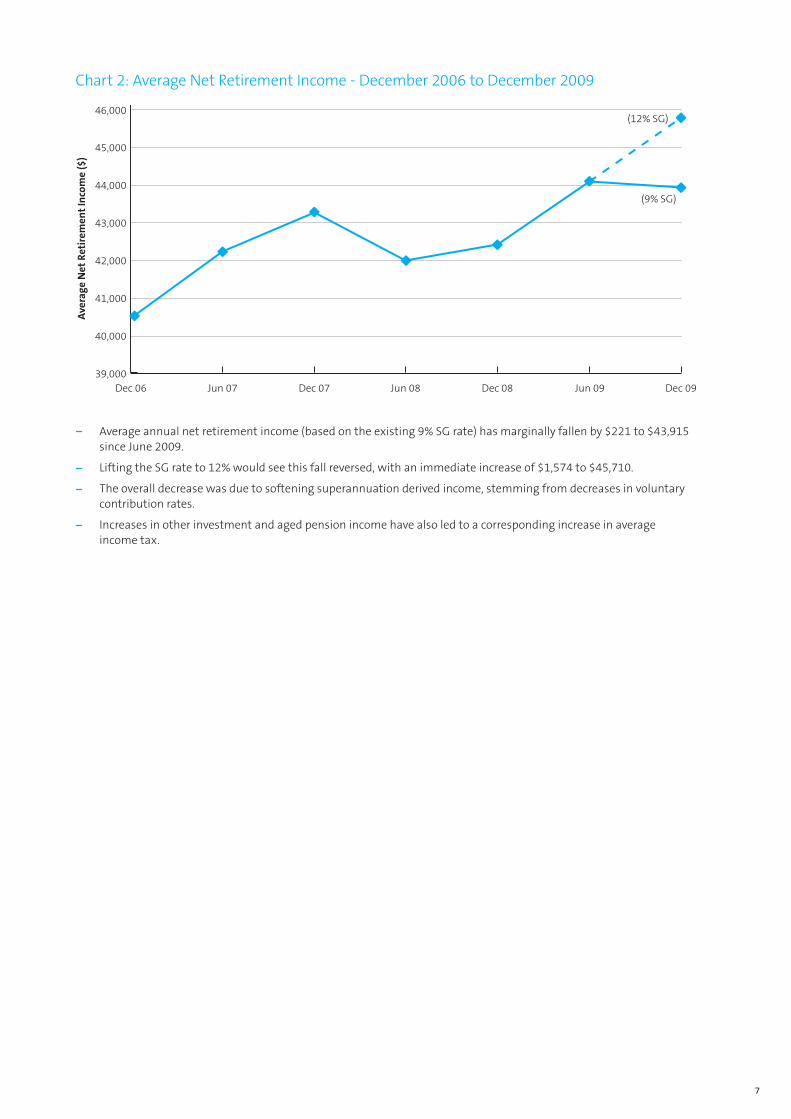

Chart 2: Average Net Retirement Income - December 2006 to December 2009A

vera

ge N

et R

etir

emen

t In

com

e ($

)

39,000

40,000

41,000

42,000

43,000

44,000

45,000

Dec 06 Jun 07 Dec 07 Jun 08 Dec 08 Jun 09 Dec 09

46,000(12% SG)

(9% SG)

Average annual net retirement income (based on the existing 9% SG rate) has marginally fallen by $221 to $43,915 since June 2009.

Lifting the SG rate to 12% would see this fall reversed, with an immediate increase of $1,574 to $45,710.

The overall decrease was due to softening superannuation derived income, stemming from decreases in voluntary contribution rates.

Increases in other investment and aged pension income have also led to a corresponding increase in average income tax.

8

7. Females - account balances by age group

TABLE 8: AVERAGE SUPER BALANCE - ACTIVE MEMBERS, DECEMBER QUARTER 2009

AGE BALANCE ($) SHORTFALL (%)

MALES FEMALES

20-24 6,270 5,854 7

25-29 13,839 13,222 4

30-34 24,999 23,450 6

35-39 37,280 32,043 14

40-44 49,803 35,582 29

45-49 63,236 40,121 37

50-54 79,448 47,374 40

55-59 87,338 53,985 38

60-64 78,533 57,351 27

65-69 77,405 54,637 29

Average 43,840 28,534 35

Chart 3: Average Super Balance - Female Members, December Quarter 2009

Ave

rage

Su

per

Bal

ance

- Fe

mal

e M

embe

rs ($

)

0Dec 06 Jun 07 Dec 07 Jun 08 Dec 08 Jun 09 Dec 09

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

This table shows the average account balance as at 31 December 2009. The chart shows how the average balance has moved over each period since the inception of the Index.

Female superannuation account balances overall have decreased slightly from June 2009.

However, strong increases in average balances were recorded in the “under 30” and “over 60” age categories largely due to increases in the underlying asset values.

9

8. Adequacy - workers above and below target

TABLE 9: WORKERS ABOVE AND BELOW THE ADEQUACY “TARGET”, DECEMBER 2009

AGE

ON OR ABOVE TARGET BELOW TARGET

% OF WORKERS NUMBER (000s) % OF WORKERS NUMBER (000s) SHORTFALL AGAINST TARGET (%)

20-24 46.3 554.2 53.4 635.6 15.2

25-29 52.9 642.7 46.3 561.2 17.5

30-34 55.4 677.8 43.9 535.8 17.0

35-39 55.8 715.2 43.8 560.3 17.2

40-44 56.7 740.3 43.2 558.7 16.3

45-49 48.0 642.1 51.9 688.3 16.2

50-54 45.5 519.2 54.6 616.8 17.7

55-59 53.6 489.4 46.6 421.0 17.8

60-64 63.1 361.3 32.9 166.4 15.3

65-69 77.4 153.4 20.2 35.2 11.4

All workers1 54.3 6,114.6 45.6 5,073.0 13.0

Chart 4: Workers below the adequacy “target”, December 2009

Wor

kers

bel

ow a

dequ

acy

targ

et (%

)

5Dec 06 Jun 07 Dec 07 Jun 08 Dec 08 Jun 09 Dec 09

15

25

35

45

55

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

1. Note that, as with all tables in this report, the “all workers” total includes some workers under the age of 20 and some aged 70 and over. It is therefore not the sum of the identified age groups. For example, there are more than 200,00 workers aged under 20 who are below the adequacy target (and therefore included in relevant totals - such as 4 million Australians falling below the adequacy target).

The number of Australians falling short of achieving an adequate retirement has increased significantly in the 6 months to December 2009.

This represents the most significant deterioration in adequacy since the commencement of the Index.

While the June 2009 Index estimated approximately 4.5 million Australians would not achieve an adequate level of retirement income, this has now blown out to approximately 5 million.

This is directly due to the fall in voluntary contributions experienced over the current period.

The proposed increase in SG should counter this fall - future editions of the Index will substantiate the extent of this counter.

NS5501 06/10