ammended oct - dec 2016 - journal of islamic...

TRANSCRIPT

Journal of Islamic Banking and Finance Oct – Dec 2016 1

2 Journal of Islamic Banking and Finance Oct – Dec 2016

Journal of Islamic Banking and Finance Oct – Dec 2016 3

In The Name of Allah,

The most Beneficent, The most Merciful

“O Believers: devour not Riba, doubled and redoubled;

and fear Allah, in the hope that you may get prosperity.”

Sura Ale-Imran (verse No. 130)

-------------------------------------------------------------------

The articles published in this Journal contain references from the

sacred verses of Holy Qur’an and Traditions of the prophet (p.b.u.h) printed for the understanding and the benefit of our

readers. Please maintain their due sanctity and ensure that the pages on which these are printed should be disposed of in the

proper Islamic manner

4 Journal of Islamic Banking and Finance Oct – Dec 2016

Journal of Islamic Banking and Finance

Volume 33 Oct - Dec. 2016 No. 4 Founding Chairman Muazzam Ali (Late) Former –Vice Chairman Dar Al-Maal Al-Islami Trust, Geneva, Switzerland

Chairman Basheer Ahmed Chowdry Shariah Advisor Uzair Ashraf Usmani

Board of Editorial Advisors

Ahmed Ali Siddiqui Mufti Bilal Qazi S. A. Q. Haqqani Dr. Hasan uz Zaman Dr. Mohammad Uzair Altaf Noor Ali (ACA) Editor Aftab Ahmad Siddiqi

Associate Editor Seemin Shafi Salman Ahmed Shaikh

Manager Publication Mohammad Farhan

Published by: International Association of Islamic Banks Karachi, Pakistan. Ph: +92 (021) 35837315 Fax: +92 (021) 35837315 Email: ia _ ib @ yahoo.com

[email protected] Website: www.islamicbanking.asia

Follow us on Facebook: http://www.facebook.com/JIBFK http://external.worldbankimflib.org/uhtbin/cgisirsi/x/0/0/5/?searchdata1=37177{ckey}

Registration No. 0154 Printed at M/S Maaz Prints, Karachi.

International Academic Advisory Panel Dr. Mohammad Kabir Hassan Professor of Economics & Finance University of New Orleans, USA.

Dr. Zubair Hasan, Professor Emeritus INCEIF Global University of Islamic Finance, Malaysia. Dr. Rodney Wilson Emeritus Professor, INCEIF, Lorong Universiti A Malaysia/France. Dr. S. Nazim Ali, Professor and Director, Center for Islamic Economics and Finance, Hamad Bin Khalifa University, Doha, Qatar. Professor Dr. Mohd. Ma’sum Billah IEI, King Abdul Aziz University, Kingdom of Saudi Arabia.

Dr. Mehboob ul Hassan Professor, Department of Economics, (CBA) King Saud University, Saudi Arabia. Dr, R. Ibrahim Adebayo Department of Religions, University of Ilorin, Nigeria.

Dr. Huud Shittu Department of Religion and Philosophy, Faculty of Art University of Jos – Plateau State, Nigeria.

National Academic Advisory Panel Dr. Waheed Akhtar Assistant Professor, Comsats Institute of Information Technology (CIIT), Lahore, Pakistan. Dr. Manzoor Ahmed Al-Azhari, Associate Professor (Islamic Law) Ph.D, Legal Policy, Fac. Shariah & Law. Alazhar University, Egypt. Post Doc. Fac. of Law, Univ.of Oxford, UK.

Dr. Muhammad Zubair Usmani Jamia Daraluloom Karachi. Muhammad Zeeshan Farrukh (MBA CPIF) Islamic Banking Group of National Bank of Pakistan Team Leader-Training & Development Unit, Karachi.

Journal of Islamic Banking and Finance Oct – Dec 2016 5

Journal of Islamic Banking and Finance

Volume 33 Oct - Dec. 2016 No. 4

C O N T E N T S 1. Editor’s Note .......................................................................................................... 7 2. Shari’ah Mechanisms of Audit ............................................................................ 11

By Yousef A Basodan & Prof. Dr. Mohd Ma'Sum Billah 3. The Significance of Faith-based Ethical Principles in

Responding to the Recurring Financial Crises .................................................. 26 By S Nazim Ali, Ph.D. and Shariq Nisar, Ph.D.

4. The Impact of Sukuk investment in Developing UAE Economy ..................... 38

By Dr. Abdussalam Ismail Onagun 5. Objectivising the Social Justice Paradigm in Islamic Finance: ....................... 55

[An Appraisal] By Abdul Azeez Maruf Olayemi, Siti Mashitoh Mahamood

Marifatul Haq Yasini, Ahmad Hidayah Buang 6. Crowdfunding and the Opportunity Presented in

the American Islamic Financial Sphere.............................................................. 61 By Husam Suleiman

7. Macro-prudential Supervision in the Indonesia Financial

Services Authority (OJK) and the Role of Sharia Board: A Proposed Framework ....................................................................................... 72 By Muhammad Iman

8. Effect of Quality of Services, Bank Image, Religious Perspective on Bank Customer Loyalty (A mediator role of

customer satisfaction)........................................................................................... 86 By Amin Ur Rahman

9. Country Model: Iraq .......................................................................................... 106

10. Book Review: Adam Smith’s The Wealth of Nations: ...................................... 107 A Modern-day Interpretation

11. Islamic Capital Market Indicators ................................................................... 109

6 Journal of Islamic Banking and Finance Oct – Dec 2016

Journal of Islamic Banking and Finance Oct – Dec 2016 7

Editor’s Note Ever since 2002, Islamic banking has seen impressive and consistent growth in

Pakistan. Now, Islamic banking in Pakistan is an established industry with 12% market share achieved in just over a decade. By year-end 2015, total Islamic banking assets in Pakistan stood at Rs 1.3 trillion while total Islamic banking deposits stood at Rs 1.1 trillion.

In a recently held global conference in Karachi organized by Institution of Business Administration (IBA) Karachi, a roadmap for the future of the industry took the centre of discussions and sessions. This was a mega event in the country and global academic laureates and corporate executives of some of the distinguished institutions from around the world participated in the event from East Asia, GCC, Europe and America. The speech by respected Shaikh Mufti Taqi Usmani was a relevant reality check for the industry from the perspective of regulators. The respected scholar highlighted that Pakistan as the only country which is created on the ideology of Islam and to realize the true practical virtues of Islamic institutions in all fields of the society should have done much better than the current state of affairs.

The country’s banking industry is still being dominated by conventional banks which are explicitly involved in Riba, which is prohibited in Islam. It is unlike the situation in GCC and Malaysia where the Islamic banking industry has more than 25% share. Thus, Islamic banking regulators and patrons in the country must bear in mind that Islamic banking in Pakistan should lift from a small niche for faith-conscious target market to become a key player in the banking industry. Only by doing this, the country could hold onto the promise of being an ideological beacon for the Muslim world. According to respected Shaikh Mufti Taqi Usmani, this requires concrete and objective targets with clear time frames so that a direction is set and the performance could be reevaluated in different phases.

As a nascent industry, Islamic banking would require incentives and equal tax treatment. Islamic banks are required to undertake additional steps, procedures and unique ownership risks in order to offer Shari’ah compliant products. It is important that double taxation on asset ownership transfers and disposals is avoided. Furthermore, the government should provide strong incentives for the expansion of Sukuk market. This step could increase the investment class securities for effective liquidity management of Islamic banks.

Appreciably, with innovative product structures like running Musharakah, the Islamic banking industry has improved its finance to deposit ratio impressively. The

8 Journal of Islamic Banking and Finance Oct – Dec 2016

recent step to introduce a 2 percent tax rebate for Shariah-compliant manufacturing firms to encourage them to eliminate interest-bearing debt from their capital structure is a welcome step. The central bank has also exempted Islamic banks from using interest-based benchmarks for some equity based financing products. The central bank has also helped by lowering Islamic banks' statutory liquidity requirement to 14 percent of total demand liabilities from 19 percent, reducing the amount of liquid assets which banks must maintain as reserves. For conventional banks, the required ratio is 15 percent.

Going forward, there is a need to focus on resolving energy crisis which can improve competitiveness of the manufacturing sector. The recent decline in international oil prices and cut in policy rate by the central bank due to significant decline in inflation bodes well for Islamic banking financing operations in the future.

This issue of Journal of Islamic Banking & Finance documents scholarly contributions from authors around the globe. Contributions in this current issue discuss the theoretical underpinnings of an Islamic economy, contemporary issues in Islamic finance and performance based empirical studies on Islamic banking and finance. Below, we introduce the research contributions with their key findings that are selected for inclusion in this issue.

In their paper “ Shariah Mechanisms of Audit – Saudi Arabia and Malaysian Experiences”, Assistant Professor Yousef A. Basodan and Professor Mohd. Ma’Sum Billah, both associated with King Abdul Aziz Univeristy, Kingdom of Saudi Arabia, put forth at the role that audit plays in establishing the legitimacy of any business and discuss at length the ethical standards and values that an external auditor of an Islamic Bank must display. While these standards and traits should be present in all auditors, they become more important in context of a religion based business such as an Islamic Bank.

The two Phds., Dr. Nizam Ali, Research Professor at Centre for Islamic Economics and Finance, Hamad bin Khalifa University, Doha, Qatar and Shariq Nisar, Professor at Rizvi Institute of Management Studies and Research, Mumbai, India have co-authored a well articulated argument in their paper “The Significance of Faith-based Ethical Principles in Responding to the Recurring Financial Crises”. They present that financial crises have resulted from lack of access to financial information by customers and the regulatory gap which lets greed guide the institutions to make money at the expense of its customers and investors. They put forth their argument in the light of common ethical standards set by major world religions and how these should be built into the financial systems ethics.

In the article “The Impact of Sukuk investment in Developing UAE Economy” Dr. Abdussalam Ismail Onagun, Assistant Professor in the University of Modern Sciences, College of Business, discusses in detail the utility of Sukuk as an alternate to the conventional bond and a Shariah approved tradable instrument. He explains the different structures that Sukuk can take and the reasons that these are acceptable under the Islamic Shariah. He further presents the importance and acceptability of Sukuk in the UAE and other Islamic countries as well as its increasing popularity in western financial markets.

“Objectivising the Social Justice Paradigm in Islamic Finance” co-authored by Abdul Azeez Maruf Olayemi, Siti Mashitoh Mahamood, Marifatul Haq Yasini, Ahmad

Journal of Islamic Banking and Finance Oct – Dec 2016 9

Hidayah Buang, scholars and faculty at Malaysian universities examine the extent to which the acclaimed social justice objective is innate to the services of the Islamic financial institutions. The focal areas they discuss include the provision of benevolent loan, corporate social responsibility, the duty of the payment of Zakat, extermination of debt based instruments, total elimination of interest, gambling and uncertainty from the financial system. However, is it concluded that, although, Islamic finance strives to realize its social justice objective, nevertheless, the institution needs to raise the bar of its acclaimed financial egalitarianism further higher.

The paper “Crowdfunding and the Opportunity Presented in the American Islamic Financial Sphere” by Husam Suleiman explores the next paradigm of evolution regarding Islamic finance products in light of the development and vast success of crowdfunding platforms. The paper examines the shifting paradigm of the Islamic finance lending product in America; the Islamic finance mortgage product. Each subsequent shift in lending procedure has removed Islamic attributes associated therein; resulting with current products that have lost the substance of Islamic teachings and have fundamentally converged to the conventional product in function and form. The paper reviews the methodology and practice of crowdfunding in the current financial landscape. It discusses the advantages and attributes of crowdfunding and Islamic finance, highlighting the overwhelming similarities. The article concludes by calling upon Islamic financial product developers to explore and pursue the current opportunity presented by the natural pairing of crowdfunding and Islamic finance products.

The paper “Macro-prudential Supervision in the Indonesia Financial Services Authority (OJK) and the Role of Shari’ah Board: A Proposed Framework” by Muhammad Iman Sastra Mihajat recommends a more macro prudential framework to address systemic risks and Shari’ah risks. The paper proposes a new macro prudential framework by involving a new Shari’ah Board Authority (DPSN) under the Commissioners of OJK to regulate and supervise the Shari’ah matters for Islamic financial institutions in Indonesia. The paper discusses the challenges in adopting this new framework. The paper concludes that the current shortcomings of the macro prudential approach for Shari’ah supervision and regulation require a new Shari’ah Board Authority under the commissioners of OJK who has full authority over Shari’ah matters.

Amin-ur Rahman, an MS scholar at the International Islamic University, Islamabad, in his paper “Effect of Quality of Service, Bank Image, Religious Perspective on Bank Customer Loyalty” discussed his study on how these variables effect create customer satisfaction which in turn leads to loyalty on part of customer towards the product or service offered. He relates these aspects to banking business and how Islamic Banks can induce customer loyalty through offering good service in order to differentiate their service offering in a more or less homogenous product market.

10 Journal of Islamic Banking and Finance Oct – Dec 2016

Readers Comments

Dr. Zubair Hasan, Professor Emeritus INCEIF, Global University of Islamic Finance, Malaysia.

“The Book Review ‘The Great Escape: Health, Wealth, and the Origins of Inequality’ was brief but relevant. There is a continuing improvement in get up of the journal and the quality of the published material. Congratulations to your team.”

Disclaimer

The authors themselves are responsible for the views and opinions

expressed by them in their articles published in this Journal.

The opinions, suggestions from our worthy readers are welcome, may be communicated on

E-mail: [email protected],

Facebook: http://www.facebook.com/JIBFK, Website: www.islamicbanking.asia

Journal of Islamic Banking and Finance Oct – Dec 2016 11

Shari’ah Mechanisms of Audit Saudi Arabian and Malaysian Experiences

By

Yousef A Basodan* Mohd Ma'Sum Billah**

Abstract

It is the common regulatory culture that, an annual audit is mandatory for every company, regardless of size, that is registered under the Saudi and Malaysian Companies Act1. For this reason, the term ‘auditing’ is most commonly associated with the statutory audit of a company’s accounts or financial statements as provided under the Acts. The Acts also stipulate that an external independent auditor referred to in the Act as ‘approved company auditor’ must perform a company’s annual audit. An audit of financial statements increases the reliability of financial information for users (e.g.: managers, investors, creditors and regulatory agencies). An auditor plays an important role in this process by providing objective and independent reports on the reliability of information2. By adding the audit function in the business environment, the users of the financial statements have reasonable assurance that the financial statements do not contain material misstatements or omissions. The auditing profession is currently operating in a very dynamic environment as numerous forces are affecting the responsibilities and activities of the public accountants. Lately, critics have charged that the current audit has failed to meet user expectations (e.g.: Enron case). Therefore it is important for the profession to reflect as to the nature and ethics of auditing in hope that by practicing ethically this will restore the

* Assistant Professor of Accounting, Dept. of Accounting, Faculty of Economics .&

Administration, King Abdulaziz University, Kingdom of Saudi Arabia. www.ybasudan.kau.edu.sa ** Professor (finance, insurance, investment, capital market & petroleum finance), Islamic

Economics Institute, King Abdulaziz University, Kingdom of Saudi Arabia. www.drmasumbillah.blogspot.com

1 Companies Act 2015, Ministry of Commerce and Industry, Saudi Arabia. Companies Act 1965, Malaysia.

2 Auditing and Assurance services in Malaysia, William F.Messier, Jr. Margaret Boh, McGraw Hill, Malaysia Edition, 2002, Pg 3

12 Journal of Islamic Banking and Finance Oct – Dec 2016

confidence of the public. The purpose of this term paper is to explore auditing under the Shari’ah guidelines. Perhaps the best solution to the above critics is by developing an auditing standard and guidelines with reference to the Shari’ah rulings.

Keywords: audit, Shari’ah, compliance, standard, corporation

Introduction Annual audit has been made compulsory for every company, which is registered

under the Companies Act, both in Saudi Arabia and Malaysia3. In contrast, a business registered as a sole proprietorship or partnership is not required to audit its annual statements annually. In addition, the acts also require that company’s annual audit must be performed by an external independent auditor. This is where the credibility of an auditor is enhanced through the public reliance on the professionalism of audit profession. Traditionally, the essence of auditing is to provide financial control and risk management. The Auditor is deemed to work on the interest of shareholders, by which he/she needs to carry out a systematic process with the objective of accumulating and evaluating evidences regarding the management assertions contained in the financial statements4. Hence, the auditor’s assurance depends on the level of collaborative evidences found during the audit process. However, there’s an increase in audit need since the corporate sector has expanded in parallel to the changes in business activity. Thus, audit provides not only control on financial aspects but furnishes top management with analysis, appraisals, recommendations and advices regarding the company‘s performance and profitability as well5. Moreover, it identifies business opportunities, which will then contribute to adding value across the business. Hence, the most important aspect is that audit serves as a method of corporate governance since audit analytical procedures provide extensive control on the correspondence between management assertions, its authenticity and financial reporting framework6.

3 Companies Act 2015, Ministry of Commerce and Industry, Saudi Arabia. Companies Act

1965, Malaysia. 4 Principles of Auditing: An Introduction to International Standards of Auditing, Rick Hayes,

Philip Wallage, Hans Gortemaker, Third Ed., Pearson Education Limited, United Kingdom, 2014.

5 Accountability, Corporate Social Reporting and the External Social Audit, Gray, R., D. Owen and K. Maunders (1991), iC.R. Lehman (ed.) Advances in Public Sector Accounting, Vol 4., 1991, pg 21.

6 OP. cit, Pg 23

Journal of Islamic Banking and Finance Oct – Dec 2016 13

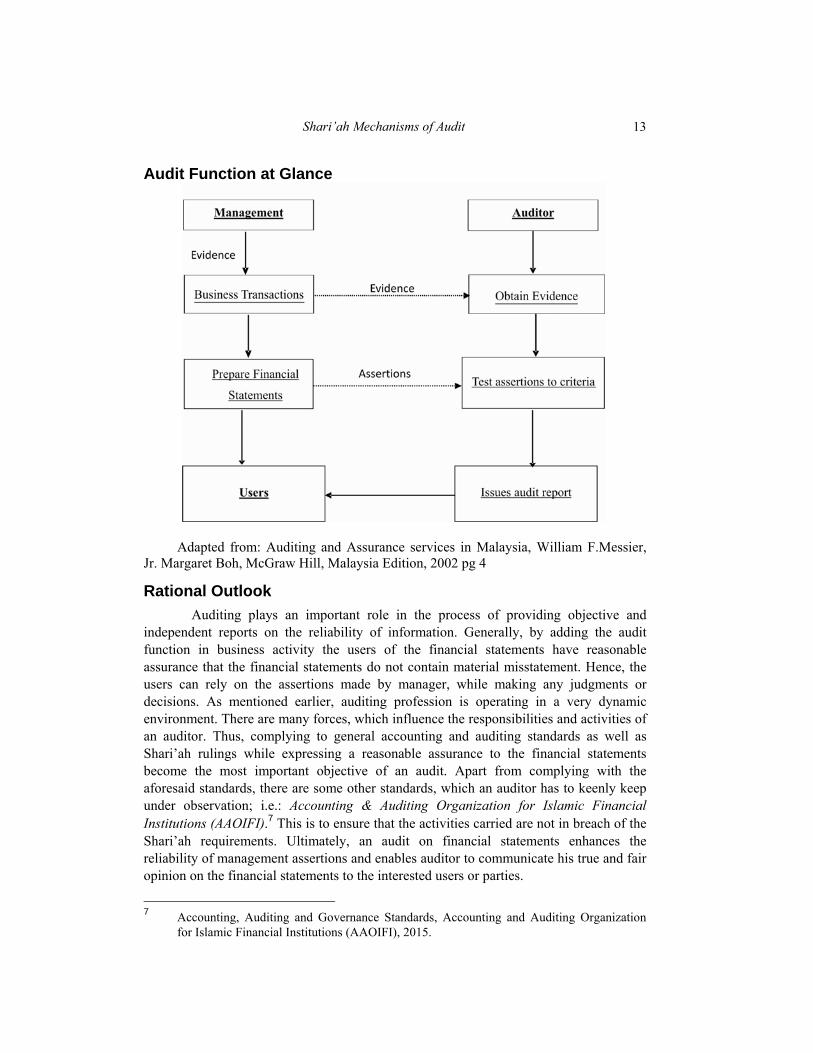

Audit Function at Glance

Adapted from: Auditing and Assurance services in Malaysia, William F.Messier, Jr. Margaret Boh, McGraw Hill, Malaysia Edition, 2002 pg 4

Rational Outlook Auditing plays an important role in the process of providing objective and

independent reports on the reliability of information. Generally, by adding the audit function in business activity the users of the financial statements have reasonable assurance that the financial statements do not contain material misstatement. Hence, the users can rely on the assertions made by manager, while making any judgments or decisions. As mentioned earlier, auditing profession is operating in a very dynamic environment. There are many forces, which influence the responsibilities and activities of an auditor. Thus, complying to general accounting and auditing standards as well as Shari’ah rulings while expressing a reasonable assurance to the financial statements become the most important objective of an audit. Apart from complying with the aforesaid standards, there are some other standards, which an auditor has to keenly keep under observation; i.e.: Accounting & Auditing Organization for Islamic Financial Institutions (AAOIFI).7 This is to ensure that the activities carried are not in breach of the Shari’ah requirements. Ultimately, an audit on financial statements enhances the reliability of management assertions and enables auditor to communicate his true and fair opinion on the financial statements to the interested users or parties.

7 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015.

Shari’ah Mechanisms of Audit

14 Journal of Islamic Banking and Finance Oct – Dec 2016

Organizational Structure of a Financial Statement Audit

Auditor’s Duty Auditing plays an important role in the principal-agent relationship, by which

auditor has a responsibility of determining whether the financial reports prepared by the manager conform to the approved accounting standards and comply with Companies Act. In general, audit is to enable the auditor “ to express an opinion whether the financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework”. This is stated in ISA 200, “Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance With International Standards on Auditing” (Para. 3)8. Thus, auditor’s opinion towards the financial statements adds credibility to the report. Auditing requires auditor to engage in a systematic process of accumulating and evaluating evidences, which relate to the management assertions in the financial statements. Auditor’s reliance on collaborative evidences will influence the auditor’s opinion towards the financial statements.

8 International Standards on Auditing (ISA), ISA 200, Para 3

Journal of Islamic Banking and Finance Oct – Dec 2016 15

Performing professional duties entails a lot of ethical procedural activities. It requires some commitments towards the responsibility, which is shouldered by an auditor. Serving clients to the best and offer management some valuable advices have been highlighted as the primary responsibilities of auditors. This includes a discussion on the current system used by the client. Auditor, who observes and evaluates the management system and control used, may provide value-added advices to his client. For instance, auditor may suggest the use of certain accounting software to the client who is using manual accounting system. To maintain the perception that auditors are credibly reliable in their profession, they should observe ethical values in their duty apart from providing the highest level of trustworthiness, integrity and truthfulness. All information should be disclosed and communicated to the related parties so that it will not reflect any wrong judgments. In addition, auditors should avoid themselves from taking any advantages of the client’s confidentiality of information, either for personal or third party’s interest.

The question of complying with professional ethics depends on the principle of religious legitimacy. Responsibility towards God (Allah) should be put as the priority in one’s consideration followed by responsibility towards society, profession, superiors, client and he himself. Commitment towards Allah generates good ethical appearance, diligent and proper work with high quality, which complies with Shari’ah rules and principles. This applies especially to the auditor, who is Muslim in religion. The emphasis on Shari’ah adherence provides good audit work through the sincerity while performing professional duties. Seeking Allah’s satisfaction becomes a due to good job fulfillment by way of being conscious to the accountability before Allah and the Day of Judgment. For instance, a good auditor will refrain himself from committing any corruption or convicting to any fraudulent activities such as accepting gift, favor or hospitality that would influence his judgment on the assertions contained in the financial statement.

Moreover, auditor is responsible to preserve his independence in either fact (mind) or appearance. Auditor should maintain his mental attitude of being fair and portray his independency. ISA 200 stated that, “the auditor be independent of the entity subject to the audit. . . . The auditor’s independence from the entity safeguards the auditor’s ability to form an audit opinion without being affected by influences that might compromise that opinion. Independence enhances the auditor’s ability to act with integrity, to be objective and to maintain an attitude of professional skepticism”9. This indicates that independence can be in term of mind as well as appearance. The earlier type of independence includes freeing an auditor’s mind from any factors, which will influence or affect his professional judgment. While the later type of independent refers to holding official position which disqualifies a person from being auditor for the particular company as stated in the Company Act. Apart, holding financial interest or having family relationship in the client’s company will disregard one to be the auditor of that company. In addition, auditor should adhere to general accounting and auditing standards while conducting any audit work, even up to the process of evaluating evidences and providing reasonable assurance to the financial statements. Besides, auditor should observe their competency and due care in the profession. It can be attained through updating his technical services and keeping his knowledge up to date. 9 International Standards on Auditing (ISA), ISA 200, Para A16

Shari’ah Mechanisms of Audit

16 Journal of Islamic Banking and Finance Oct – Dec 2016

In conclusion, in the expanse of audit profession, auditor should continuously be aware and observe his function and responsibility towards Allah, society, profession and client in providing a true and fair view on the financial statements through serving client to the best and with the most ethical conduct, which should not contravene the underlying principles.

In short, auditor’s responsibilities include to: • Determine whether the financial reports prepared by the manager conform to

the approved accounting standards and comply with Companies Act.

• Add credibility to the report of financial statements.

• Engage in a systematic process of accumulating and evaluating evidences, which relate to the management assertions in the financial statements.

• Serve clients to the best and offering management valuable advices.

• Observe ethical values in their duty apart from providing the highest level of trustworthiness, integrity and truthfulness.

• Put emphasis on Shari’ah adherence to provide good audit work through the sincerity while performing professional duties.

• Preserve his independence in either fact (mind) or appearance.

• Adhere to general accounting and auditing standards while conducting any audit work, even up to the process of evaluating evidences and providing reasonable assurance to the financial statements.

Auditor should continuously be aware and observe his function and responsibility towards Allah (swt), society, profession and client in providing a true and fair view on the financial statements through serving client to the best and with the most ethical conduct.

Agency Relationship Affecting Audit*

*Source : Auditing and Assurance services in Malaysia, William F.Messier, Jr. Margaret Boh, McGraw Hill, Malaysia Edition, 2002 pg 16

Journal of Islamic Banking and Finance Oct – Dec 2016 17

Audit and its Shari’ah Guidelines

Islam is a comprehensive religion. It provides guidance in all aspects of life including economics, social, political and cultural. Accounting and auditing are parts of economy, which are professions that are required by Shari’ah as Fard kifayah. Both accounting and auditing provide the concept of fairness as they show where the resources have been allocated. The realization of this concept is closely related to the code of ethics for accountant in performing their professional duties and responsibilities. From the Islamic point of view, the ethics of accountants and auditors depend primarily on the principles of Islamic faith and Shari’ah. As ethics are an integral part of Islamic Shari’ah, therefore, Islam strongly emphasizes on that and considers them as one of the objectives of legislation. In short, Islamic Shari’ah provides some foundations of auditors and accountants’ ethics. The major Shari’ah foundations of auditors and accountants’ ethics are as the followings: -

Integrity10

Integrity is an act of honesty and having strong moral principle. In Islam, integrity is highly valued as it governs all acts. It requires accountants and auditors to perform their duties and responsibilities with competency and adequacy. Allah says in the Qur’an,

“Truly the best of men for thee to employ is the man who is strong and trusty”. (Surah Al- Qasas: 26)

Principle of Vicegerency11 Man is the best creation of God (Allah) and Allah has bestowed us with mind (al-

aql). Thus, we serve as vicegerent of Allah. We are entrusted to develop the earth. However, it is important to be aware that the supreme authority belongs to Allah, and that man’s ownership of property is not absolute. We must always observe the orders and prohibitions of Allah regarding property. Objectives in Shari’ah are pervasive and this includes property. Thus, auditors have big roles in making sure that property and funds are not squandered and wasted uselessly or used in prohibited matters (e.g. usurious transactions) or traded unjustly or by denying the rights established in it for Allah. Anything that is prohibited in Shari’ah should not be given neither verbal nor documentary support in anyway whatsoever. Allah says in the Qur’an;

“Behold, thy Lord said to the angles: “I will create a vicegerent on earth”. (Surah Al Baqarah: 30)

“It is He who hath made you (His) agents, inheritors of the earth”. (Surah Al

An’am: 165)

10 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015, Pg 1010 11 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015, Pg 1011

Shari’ah Mechanisms of Audit

18 Journal of Islamic Banking and Finance Oct – Dec 2016

Sincerity12

The Qur’an and Sunnah stress that in what ever we do, we must have good intentions. Good intentions will lead to good performances and commitments in work as they also promote sincerity and avoid hypocrisy. Auditors are not to perform work because of fame, flattery and boasting. Instead, he should regard his work as a religious commitment as well as a performance of his professional duty. This will eventually turn his duty into a form of worship. This is line with the fundamental established in Shari’ah that good intention turns a habit into worship. Subsequently, the auditor becomes worthy of reward from Allah.

Piety13

Piety is refers to a strong belief in religion. It means fearing Allah to protect one’s self from adverse consequences with rules of Shari’ah. This is done by observing Allah’s commandment and to forbid oneself from His prohibitions. Therefore, auditor has to fear Allah in performing his duty especially when dealing with property as it diverts man’s attention and leads him into transgression. As Allah says:

“Let there arise out of you a band of people inviting to all that is good, enjoying what is right and forbidding what is wrong”. (Surah Al- Imran: 104)

Then the Holy Prophet also mentioned that,

“Fear Allah wherever you are, and follow the evil with good to obliterate it, and deal with people in good conduct”.

Righteousness and making one’s work perfect14

According to this principle, one should perform his duties that have been assigned to him in the best manner and that is to attain perfection in his work. This can be achieved through academic qualifications, practical experience and acquisition of religious knowledge. Therefore, auditors must always strive to acquire the above. Allah promotes this principle in the Qur’an:

“And spend of your substance in the cause of God, and make not your own hands contribute to (your) destruction; but do good, for God Loveth those who do good”. (Surah Al Baqarah: 195)

Besides that, Prophet (saw) also mentioned that;

“Allah likes when someone performs his work to do it perfectly and Allah has described righteousness in everything”.

12 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015, Pg 1012 13 Ibid, Pg 1012 14 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015, Pg 1013

Journal of Islamic Banking and Finance Oct – Dec 2016 19

Allah-fearing conduct in everything15

This implies that Allah is constantly watching the acts of His servants. Therefore, it is Allah that the auditors should be afraid of regardless of the opinion of people, which includes his superiors. This principle is absolute and will never change from time to time. Hence, auditors should always practice self-monitoring. And this may weaken unless it is tied to both faith and feeling that one is being observed by Allah. Allah says;

‘Allah ever watches over you” (Surah Al Nisa’: 1)

For verily He knoweth what is secret and what is yet more hidden” (Surah Taha: 7)

Men’s accountability before Allah16 Since Allah is observing all the acts of an auditor, therefore, he will be accountable

to Him on the Day of Judgment for all his deeds. Thus, auditors should always be aware and to avoid doing things that may incur Allah’s punishment. The auditor should always remember that he is accountable before Allah, and before his society, profession, superiors and finally before himself.

“Then shall anyone who has done an atom’s weight of good, see it. And anyone who has done an atom’s weight of evil, shall see it” (Surah Al Zalzalah: 7-8)

Shari’ah’s Code of Ethics in Auditing Auditing is one of the branches of accounting. It is associated with examination of

accounting data. It is a professional service which people put high reliability on. Hence, audit needs to be performed in the most ethical manner since the auditors provide reasonable assurance to the company’s stakeholders. Therefore, based on the ethical principles highlighted in the Qur’an and Sunnah, the following ethical principles for accountants and auditors are derived17: -

Trustworthiness Accountants and auditors should be trustworthy and honest in conducting their

professional duties. However, they are said to be trustworthy by conducting their responsibilities with high degree of integrity and honesty. One way to show their integrity is by protecting client’s interest, which is related to the confidentiality of the information of the clients. For example; they cannot use such confidential information for their personal gain and third party. Besides that, the auditors have to present and provide factual and truthful report so that others can rely on the information while making judgement and decision.

15 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015, Pg 1014 16 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015, Pg 1015 17 Accounting, Auditing and Governance Standards, Accounting and Auditing Organization

for Islamic Financial Institutions (AAOIFI), 2015, Pg 1016-1017

Shari’ah Mechanisms of Audit

20 Journal of Islamic Banking and Finance Oct – Dec 2016

Legitimacy Besides being truthful and honest, auditors also have to comply with certain legal

requirements and procedures including the Shari’ah rules and principles. They have to act and conduct according to the guidelines of Shari’ah principle. Moreover, they also have to comply with standards provided by professional bodies.

Objectivity In conducting an audit work, auditors have to be objective. They have to perform

their professional duties in fair, impartial and unbiased ways. They also have to be free from any conflict of interest in order to ensure their independence. Since independence is a fundamental characteristic and key point of auditing profession, auditors should be independent both in mind and appearance. If the auditor is a member of the board of directors of the auditee company, then, he should not perform or conduct any audit work for that company. This is because he could be involved in providing bias information, as now he is no longer an independent party.

Professional competence and diligence Since auditing is a professional service, it should be conducted in professional

ways. Therefore, auditors should show their credibility in realizing these duties. To ensure work is done in proper manner, they should be professionally competent and well- equipped in carrying out the task assigned. Hence, professional competence can be achieved or obtained through ways like formal education, training, experience and professional education. Besides that, they have to be duly diligent in discharging their responsibilities as they are not only responsible to the stakeholders but ultimately also to Allah the Al-Mighty.

Faith-driven conduct Auditors should behave and conduct his duties in line with the faith values derived

from Shari’ah rules and principles.

Applications Application of ethical conduct based on the principle of trustworthiness

An auditor should refrain oneself from engaging in any activity that would jeopardize the attainment of the institution’s religious and ethical objective. Therefore, an auditor should present and communicate favourable as well as adverse information honestly with complete transparency. He should not disclose confidential information acquired in the course of performing professional duties unless required to do so by the law. He also should not use the information acquired in the course of his duties for the advantage of himself or third parties.

Application of ethical conduct based on the principle of religious legitimacy

An auditor should always remember his responsibilities towards Allah, and towards his society, profession, superior and himself. Therefore, it is his responsibility to verify

Journal of Islamic Banking and Finance Oct – Dec 2016 21

the religious legitimacy of everything relating to his duties. He should be aware of Shari’ah rules and principles relating to jurisprudence of financial transactions. Thus, he should receive formal, adequate training in jurisprudence of financial dealings. He must make sure that he performs his duties in conformity with such rules and principles. Anything that is not in conformity with Shari’ah should be considered illegitimate.

Application of ethical conduct based on the objectivity principle An auditor should be independent in fact as well as appearance. Therefore, he

should not involve himself in a situation whereby there is a conflict of interest. This is because it will threaten his judgment in expressing his opinion. He should also avoid from being influenced by others to ensure he could present information truthfully. In his course of duties, he should refuse any gift or favor. Contingent fees (defining the fees as a percentage of the income number) should also be avoided as it might affect the independence and objectivity of the auditors.

Application of ethical conduct based on the professional competence and diligence principle

An auditor has a responsibility to possess an appropriate level of academic and professional competence. He should uphold his competence by going through skills development constantly and keeping himself updated with the new developments in the auditing as well as accounting profession. Most importantly, he should acquire sufficient working knowledge of Shari’ah aspects relating to financial transactions.

Application of ethical conduct based on the principle of faith-driven conduct

An auditor’s behavior should always be in line with religious values derived from Shari’ah rules and principles. Particularly, he should consistently do self-monitoring (that is always being aware of the existence of Allah (swt). He should be conscious that he is accountable before Allah on the Day of Judgment. Therefore, in his course of duties, he should be seeking Allah’s satisfaction and not to submit to the pressures of others. He also should show love and brotherhood as well as be merciful to the rest of the staffs and whomever he deals with.

Auditor’s Report The auditor’s report is the expression of opinion of the auditor whether the

financial statements audited present fairly the financial position and the result of operations, and have been prepared in accordance with the applicable accounting standards. It is also important to note whether the financial statements comply with the statutory requirements.

Shari’ah Mechanisms of Audit

22 Journal of Islamic Banking and Finance Oct – Dec 2016

The auditor’s report consists of:18

Title E.g. Reports of the Auditors Addressee

The report should be addressed mainly to the shareholders/members of the company audited (as required by the engagement and laws).

Introduction The report needs to identify the financial statements that have been audited and its

notes as well as the date and period covered. There should also be statements regarding the responsibilities of the management and those of the auditors. The management’s responsibility is towards the preparation of the financial statements. Meanwhile, the auditor’s responsibility is to express an opinion on the financial statements.

Scope Paragraph The reports should narrate that the audit was conducted in accordance with the

relevant auditing standards and accounting principles, which do not contravene the Shari’ah Rules, and Principles. The report should also indicate that the audit was planned and performed to obtain reasonable assurance and not an absolute one. The audit also evaluates the overall financial statement presentation.

Opinion Paragraph The auditor’s report must state the auditor’s opinion as to whether the financial

statements give a true and fair view in accordance with the appropriate standards that do not contravene with the Shari’ah rules and principles and statutory requirements.

Auditor’s Address and Signature The report should name the audit firm, personal name of auditor and address of the

audit firm. The report should be signed.

Date of Report The auditor should date the report at the date when the audit was completed. The

date should not be earlier than the date on which the statements are signed or approved by management.

18 Auditing and Assurance services in Malaysia, William F.Messier, Jr. Margaret Boh,

McGraw Hill, Malaysia Edition, 2002, Pg 503

Journal of Islamic Banking and Finance Oct – Dec 2016 23

Audit Process

Recommendations Lately, critics have charged that the current audit has failed to meet user

expectations. It is important for the profession to reflect as to the nature and ethics of auditing in hope that by practicing ethically this will restore the confidence of the public. In order to uphold the integrity of auditors, a separate body should govern ethical principles governing the auditor’s professional responsibilities. Therefore, the best solution is to form the Shari'ah Supervisory Board to govern the ethics of auditors. The ethical principles that should be included are:

• integrity

• trustworthiness

• confidentiality

Shari’ah Mechanisms of Audit

24 Journal of Islamic Banking and Finance Oct – Dec 2016

• professional behavior

• honesty

• righteousness

• fairness

• objectivity

• professional competence

• due care

• independence etc

The question of complying with professional ethics depends on the principle of religious legitimacy. Responsibility towards Allah should be put as the priority in one’s consideration. Commitment towards Allah generates good ethical appearance, diligent and proper work with high quality, which complies with Shariah rules and principles. The emphasis on Shari’ah adherence provides good audit work through the sincerity while performing professional duties. Seeking Allah’s satisfaction becomes a due to good job fulfillment by way of being conscious to the accountability before Allah on the Day of Judgment.

Conclusion Annual audit is mandatory for every company, regardless of size, that is registered

under the Companies Act. An auditing plays an important role in this process by providing objective and independent reports on the reliability of information. Traditionally, the essence of auditing is to provide financial control and risk management. Auditor is deemed to work on the interest of shareholders, by which he/she need to carry out a systematic process with the objective of accumulating and evaluating evidences regarding the management assertions contained in the financial statements. However, there’s an increase in audit need since the corporate sector has expanded in parallel to the changes in business activity. Thus, audit provides not only control on financial aspects but furnishes top management with analysis, appraisals, recommendations and advices regarding the company‘s performance and profitability as well. Thus, complying to general accounting and auditing standards as well as rulings issued by Shari’ah Supervisory Board while expressing a reasonable assurance to the financial statements become the most important objective of an audit. This is to ensure that the activities carried out are not in breach of the Shari’ah requirements. Ultimately, an audit on financial statements enhances the reliability of management assertions and enables auditor to communicate his true and fair opinion on the financial statements to the interested users or parties. To maintain the perception that auditors are credibly reliable in their profession, they should observe ethical values in their duty apart from providing the highest level of trustworthiness, integrity and truthfulness

Journal of Islamic Banking and Finance Oct – Dec 2016 25

References Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI)

(2015) Accounting, Auditing and Governance Standards, Dar AlMaiman for Publishing & Distributing.

Companies Act (1965), Malaysia.

Gray, R., Owen, D. and Maunders, K. (1991) “Accountability, Corporate Social Reporting and the External Social Audit”, I.C.R. Lehman (ed.) Advances in Public Sector Accounting, Vol 4, pg 21.

Hayes, Rick, Wallage, Philip, Gortemaker, Hans (2014) Principles of Auditing: An Introduction to International Standards of Auditing, Third Ed., Pearson Education Limited, United Kingdom.

International Standards on Auditing (ISA), ISA 200.

Messier, William, Boh, , Jr. Margaret (2002) Auditing and Assurance services in Malaysia , McGraw Hill, Malaysian Edition.

Ministry of Commerce and Industry (2015), Companies Act, Saudi Arabia.

Shari’ah Mechanisms of Audit

26 Journal of Islamic Banking and Finance Oct – Dec 2016

The Significance of Faith-based Ethical Principles in Responding to the

Recurring Financial Crises By

Dr. S Nazim Ali,Ph.D*.

Professor Shariq Nisar,Ph.D Abstract: The global financial system has been under tremendous pressure due to recurring financial crises. With nearly every major economy affected, the cost of managing these crises has been enormous. Some studies have identified ethical failure as the root cause of these financial crises, while others have focused on the structural flaws in the system. While both the diagnoses may be correct, the prescription for handling the crises lacks clear direction and consideration for its applicability over the long run. This paper focuses mainly on the ethical aspects and recommends a few long-term measures that seek to improve moral behavior. Few suggestions have also been made to improve financial inclusion based on common religious, social and moral values.

Key Words: Islamic Finance and Stability; Faith-Based Finance: Ethics and Morality

1. introduction The global financial system has been under tremendous pressure in recent years,

affecting many major economies of the world. Due to the interconnected nature of the world economy today, financial crises occurring at one place can quickly engulf other economies. As a result, many economies have suffered enormously due to diversion of precious financial resources to keep the financial system working, not to mention the tremendous suffering and the loss of opportunity. Many can recall when similar crises struck less developed or developing countries (like the four “Asian Tigers”), most financial gurus deemed it a symbol of the structural weakness of those economies. We started taking these challenges seriously only when big and developed economies started * Authors: Dr. S. Nazim Ali, Ph.D., Research Professor & Director, Center for Islamic

Economics &Finance, Hamad Bin Khalifa University, Doha Qatar. Professor Shariq Nisar, Ph.D., Professor,Rizvi Institute of Management Studies and Research, Mumbai, India

Journal of Islamic Banking and Finance Oct – Dec 2016 27

feeling the dominant effect of such crises despite strong regulations in place. The period following the 2008 financial crisis witnessed decelerating growth in many developed economies (US economy contracted by -0.7% in 2009 while the UK was the worst affected of Western European countries with a contraction of -1.3%). We have seen how even strong regulations are not sufficient to insulate economies from being impacted by economic shocks.

A number of structural causes have been identified by various experts (Rajan, 2010). This paper concentrates on the ethical aspect, in particular on dealing with human greed and mischief. The importance of an ethical compass is emphasized by recognizing the fact that after the crisis, the alpha of Social Responsible Investments(SRI) funds, compared to other mutual funds, turned positive(Nieuwenburg,2013).The culture of greed is believed to be one of the main causes leading to financial mischief and ultimately to financial crises over time. Policy makers have to address the fallout of unlimited greed, lack of honesty, selfishness, among others which the recurrent financial crises have revealed. The ‘greed-is-good, greed is right, greed works’ mentality is encouraged in modern financial institutions, but it comes mainly at the expense of consumers and suppliers and the society at large. Customers tend to be the most exposed to risk as they rely almost entirely on the financial service providers. Contrary to their interests, we observe concerted efforts by many stakeholders in the financial system to lure customers into making risky investments. Banks employ shadow banking strategies; rating agencies have often missed the bigger picture, focusing on the wrong metrics; and regulators are found wanting in discharging their responsibilities as the market achieves greater sophistication. According to the Financial Stability Board, shadow banking has become an increasingly popular phenomenon with assets mounting to over $80 trillion as at 2014 with nearly 200% growth between 2002 and 2014(FSB,2015). Another case in point of this phenomenon was clearly evident in the case of the Subprime Mortgage Crises (SMC) in 2008. It is well known now that home loan seekers were tricked into housing mortgage. . Art Perlowrites, “the subprime mortgage crisis is the trigger that has set off a whole number of financial imbalances — it triggered the whole pile to start falling. This crisis was caused by incredible greed and looting by the financial sector….” (Webb, 2007).

The World Economic Forum Report on Faith and the Global Agenda: Values for the Post-Crisis Economy reported, “the majority of people across the globe believe the global economic crisis is related to ethics and values” (World Economic Forum, 2010). In addition, it has been shown that religiosity, ethics and values among corporate workers mitigate unethical behavior of a Corporation as a whole (Grullon, Gustavo, Kanatas, George, and Weston, James, 2009).

This paper is organized into four sections. After this introduction, section 2 attempts to diagnose the causes of recurring financial crises. Section 3 explores the significance of common platforms in reshaping and enhancing best practices in the global financial system. The final section concludes with some policy recommendations.

2. Diagnosing The Causes Of Recurring Financial Crises While many studies have focused on the probable causes of financial crises, this

paper identifies two major factors that are directly related to the central hypothesis of this

The Significance of Faith-based Ethical Principles….

28 Journal of Islamic Banking and Finance Oct – Dec 2016

paper. Lack of access to financial information for consumers, and regulatory gaps and loopholes in the penalty systems for financial misconduct are the two important causes.

2.1 Lack of access to financial information for consumers Poor financial choices due to lack of relevant information has been a major

contributing factor to financial crises (European Commission, 2010). Unequal access to information in respect of financial products constrains use and development of a just and stable economy (Lumpkin, 2010). Consumers may not be well-educated or well versed in financial matters to comprehend financial innovations. As Organization for Economic Co-operation and Development (OECD) points out:

“With the rapid pace of financial innovation, the growing complexity of financial products, and the increasing amount and size of financial risks and responsibilities transferred to households, it has become very difficult for the average consumer to successfully navigate the financial marketplace, let alone for poorly informed individuals” (OECD, 2009).

Financial institutions are also criticized for lacking a sense of social responsibility. Their focus on the profit maximization comes at the expense of consumers, as the disclosures are either insufficient or too complex (Brix et al, 2010). Financial institutions should be required by law to remain transparent. . Regulatory authorities should intervene to ensure that no deception or tricks are used to unfairly attract consumers and key features including the risk factors are revealed to consumers in the language that is understandable for ensuring transparency and clarity.

2.2 Regulatory Gap/Overlap and Loopholes in Penalty Systems for Financial Misconduct Penalties, though in place, have been inadequate in curbing fraud and misconduct.

This poses serious problems for the checks and balances mechanism. Firms have become more sophisticated in their dealings with the penalty systems, implementing a cost-benefit analysis, to get their way around the system. Many big companies consciously violate the law because the profits they reap in doing so are far greater than the fines they might have to pay in case they get caught. (Durden, 2013) (Raice, 2013).

3. EXPLORING COMMON PLATFORMS 3.1 Ethics and Morality

Historically most financial crises exhibit similar patterns and are triggered by almost the same factors (Mian, Atif and Sufi, Amir, 2014). Structural flaws in the financial system as argued by many experts are no doubt inherent which to a large extent could be addressed by policymakers and regulators (IMF, 2012). Masses in general have little role to play in that, but efforts to improve financial literacy with high emphasis on morality in financial systems will go a long way in addressing the challenges of morality in the financial world. Inculcation of good moral values and conduct, developing a sense of social responsibility, transforming the culture and instilling the right type of education among the budding entrepreneurs and financial players could help the future of the financial system in a very positive way.

Journal of Islamic Banking and Finance Oct – Dec 2016 29

The most important challenge in this regard is how to encourage people to behave

ethically and morally. Very often we notice the lack of incentives for those who behave well. Contrarily, those who cross the line are often seen climbing the ranks rather quickly. There is a need for an effective mechanism to address this anomaly. A system is needed where good behavior can be objectively measured and appropriately rewarded at the same time any type of malfeasance is not only restricted but also punished.

Transformation of beliefs, attitudes and mindsets of financial participants across all levels are hoped to bring about greater financial stability. On the other hand provision of rewards and penalties hope to bring greater coherence in compliance with law in its true spirit. Moreover it is felt that the main reason for financial exclusion of a vast majority of people across the globe is not really the lack of resources but the lack of spirit and motivation. Unfortunately, it is generally believed that the current financial system has led to more exploitation and misallocation of financial resources thereby making the rich the greatest beneficiaries (Oxfam 2015).

One cannot ignore the fact that despite having the best of infrastructures ever in human history, modern economy has not been able to show compassion towards the poor, vulnerable and marginalized.

3.2 Ethics, Religious Teachings and Faith Ethics form a greater part of religion and most of the religious beliefs today have

enormous ethical injunctions that followers must adhere to (Dhand, 2002 and Akpinar, 2010). Virtues of loving, kindness, compassion, abstinence from killing, stealing or lying are sacrosanct in Buddhism. In Christianity similar ethical values such as love, mercy, and forgiveness and virtuousness in thoughts and actions are emphasized. Islamic teachings hold high the ethical ethos of justice, mercy, goodness, compassion, avoidance of wastefulness, forbiddance of evil, etc. It is observed that there is good overlap of the ethical values among religions pointing to the universal nature of ethical behavior.

All the Major religions of the world recognize the role of ethical behavior in practice by sharing almost a similar stance on the areas of SRIs. (Bhatt, Sultan, Shah, 2014).

There is a need to establish a common ground that will spell out a code of conduct and establish an agreed-upon ethical system in financial dealings. One way this could be done is by basing it on religious teaching and values which enforces a code of conduct on its followers. A case in this regard that is worth mentioning is the Emotional and Spiritual Quotient (ESQ) training program in Indonesia introduced in the early 2000s. The idea is the combination of business management, life-coaching, and self-help principles with Islamic history and examples from the life of the Prophet Muhammad (Rudnyckyj, 2009). The ESQ is designed to realize a form of effective self-management by making ‘people better from the inside’. Similar actions were taken by some movements who cited separation of religious ethics from economic practice as the main cause of the economic ‘crises’ in Indonesia. They opined that this demerger has resulted in rampant corruption, inefficiency, collusion and a lack of discipline in the workplace. This phenomenon is not limited only to Indonesia, but is increasingly found elsewhere in the world (Haenni 2005 and Wise 2003).

The Significance of Faith-based Ethical Principles….

30 Journal of Islamic Banking and Finance Oct – Dec 2016

There are two competing theories regarding the link between economic growth and religion. The first, known as the secularization hypothesis, (Weber, 1930) postulates that greater economic development causes individuals to abandon their faith and become less religious. This hypothesis also claims that economy as it becomes stronger plays a larger role in the governance of the country than religion. The other theory (Smith, 1790) claims that as a society becomes religiously diverse, the different religions compete which results in stimulating more interest in religion. The latter hypothesis is strengthened by the study of Chaves and Cann (n.d.) who have shown that greater governmental sponsorship of religion paradoxically decreases the individual’s interest in religion. A survey conducted in the United States shows positive relationship between religiosity and poverty.

On the other hand, in some societies, notably among the communist societies, religion is considered as “the opium of the masses”, and thus religious freedom and diversity are suppressed by state as a policy. The above mentioned theories examine religion as an outcome of economic development or policy; comparatively little research (Barro and McCleary, 2013) has been done on religion as an antecedent to economic growth. Alon and Chase (2005) examined political and economic freedoms alongside religious freedom in explaining economic prosperity and found that religious freedom is a significant antecedent of economic prosperity.

Adding to the points on overlap of religious values, it is argued that most of the faith based financial models, be it, Judaism, Christianity, Islam, Hinduism or Budhism, share common goals such as the upliftment of labor and the downtrodden sections of society, abhorring violence, shunning vulgar entertainment etc. These common goals can be conveniently converted into actionable plans in the form of Corporate Social Responsibility, Corporate Governance, Human rights and the care for Environment.

Indeed, there have been clear calls advocating financial regulators to revisit the teachings and wisdom of various faith based traditions in staving off future financial crisis (Steele, 2010). Across religions there are activities which are prohibited or abhorred like interest, gambling and businesses which are discouraged for causing harms to society. At the same time, there are also activities which are encouraged like sharing of risk, helping the poor and needy and donating to charities to help the underprivileged.

There are also religiously sensitive investment strategies that are important in creating a common platform based on religious teaching and values. For example, the practice of excessive and highly speculative risk taking, especially in as much as they are of such a scale that they increase the level of systemic risk, must be examined and monitored in terms of their potential impacts on the common good. In the same way the impacts of the use of derivatives, credit default swaps and other activities such as short selling on the stability and soundness of the financial system and therefore the well-being of communities across the world must be examined and evaluated.

The question one may ask is: How will faith and religion play a part in fostering a common platform in the financial industry? There are several ways this can be achieved. Firstly, faith-based teachings reintroduce the foundational belief and value that gives more emphasis on sustainability than short term profit (Kaye, 2012).A system that has its priorities set over serving the needs of all communities before enriching executives,

Journal of Islamic Banking and Finance Oct – Dec 2016 31

traders and shareowners will be consistent with the vision of the faith traditions. This system will earn confidence of people and hence is more inclusive.

Secondly, faith and religion serve as a reminder to the business and investment community of their responsibility toward the future of Earth and its sustainability for future generations. Financial and economic decisions based on values taught by the religious systems will serve as a moral compass for business community and investors (Chapra, 1995).

Thirdly, religion allows their followers to integrate their beliefs into the management of their financial and commercial affairs. In this innovative space many faith traditions have established funds and innovative credit mechanisms that reflect more faithfully their foundational principles on the practice of credit, borrowing and lending while preserving wealth and posterity. The National Council of Churches, for example, has undertaken shareholder activism, social-purpose mutual funds and the like since the 1970s. Such initiatives are pertinent examples of the integration of Christian beliefs into the financial and commercial aspects in the lives of believers.

Fourthly, religious faiths working together can draw on the principles they hold in common to promote a more humane system and reform the dominant financial system. By working together, they can bring the values of sustainability, social responsibility, and solidarity into a vibrant debate and conversation about the kind of economic model that is consistent with the vision of their beliefs. In the post-World War II period, for instance, we have examples of the modification of a free market individualistic capitalism to a more socially oriented market economy, especially European markets where mutual and cooperatives are more prominent (DGRV Die Genossenshaften, 2016.). Mutual and cooperative insurance accounts for over a quarter of the global market, and is the fastest growing sector of the market (ICIMF, 2014).

Finally, the faiths can likewise find common ground with others in the ongoing process of evaluating the tools and innovations that are introduced into financial system by using the wisdom in their traditions and the environmental, social and governance (ESG) criteria that have been established. For example, using the precautionary principle from risk management in a financial setting may be useful (Schettler, Barrett and Raffensperger, 2002).

As argued above, religious teachings and faith can facilitate the creation of common grounds for financial stability, inclusiveness and sustainability by establishing a more inclusive and morally conscious system rather than conducting financial transactions that merely adopt a legalistic attitude to financial regulation. The idea of faith-based ethical economies has now been espoused by all major faiths. Below we quote various religious experts which clearly indicates the commonality of thoughts on the subject.

Leading Islamic finance expert, Justice Muhammad Taqi Usmani argues:

“The crisis we are facing is not caused by some regulatory mishaps only; there are some systemic errors in our conceptual framework. This framework needs a revival of some noble values and a serious review of some basic principles on which we have constructed the whole edifice

The Significance of Faith-based Ethical Principles ….

32 Journal of Islamic Banking and Finance Oct – Dec 2016

of our economy. There are two basic values of foremost importance that must be reflected in a balanced, sustainable and just economy. First, the common welfare of the society should take precedence over individuals’ selfish objectives. Second, the profit motive should not be extended to unlimited greed of wealth” (Usmani, 2009).

The element of social welfare based on common good as espoused above is also emphasised by Lesley-Anne Knight, Caritasof theVatican City, who contends that:

“During the course of the 20th century, the Catholic Church elaborated a clear set of social values that are increasingly relevant today as we consider the kinds of institutions and governance mechanisms we need to ensure a more humane global economy” (Knight, 2010).

Ensuring a more humane global economy requires sustainable practices that promote equity, fairness and justice without compromising the aspects of environmental conservation. YukeiMatsunaga of the Japan Buddhist Federation argues that:

“….an emphasis on the interdependence of all living things—the vision of life taught in Japanese Buddhism—may provide effective suggestions for handling such pressing issues of modern society as human alienation and environmental destruction”(Matsunaga, 2010)

Rabbi David Rosen of the American Jewish Committee contends:

“If enterprise and industry are detached from the human connection, then they will not be sustainable in the long term. Moreover, in order for there to be a common language—in the deeper sense of the term—that connects the various components of society, it is necessary for the members of that society to have a sense of the transcendent, a sense that there is something more to their existence and activity than purely “the edifice itself”” (Rosen, 2010).

This eschatological basis should be the driving force that will trigger a sense of

care and common good in the society. Rev. Katharine JeffertsSchori, the Presiding Bishop of the Episcopal Church believes that:

“this ethics of care for the least applies to all the major issues facing us: local, national and international economic praxis; ecological and climatic concerns; and the structure of the global market” (Schori, 2010).

The way forward requires concerted efforts among all the stakeholders in promoting shared human values in financial matters. To this end, Sri Ravi Shankar argues that:

“the implementation of these human values in the corporate program…has to be developed holistically by including society’s four pillars: its economic establishments, its faith-based organizations, its political institutions and its social sector…Faith-based institutions can catalyze a huge transformation and engender much needed integrity in people” (Shankar, 2010).

Journal of Islamic Banking and Finance Oct – Dec 2016 33

There should be a way of minimizing the effect of greed in personal behavior.

Reverend Dr Olav FykseTveit, the General Secretary of the World Council of Churches explains:

“Economic laws and principles from beginning to end are also a matter of personal behaviour. Because of the financial crisis, the attitude of greed now has a new face and new dimensions…We will never experience the total disappearance of greed. However, we can work together to define what kinds of attitudes build a sustainable global economy in a sustainable global community” (Tveit, 2010).

Building a sustainable global economy requires long-term plan that will take into consideration several factors, particularly the shared values. This is expected to transform the current socioeconomic model and make it more productive. Kirill I, Patriarch of Russia contends:

“without a solid basis in values, however, any transformation of the existing socioeconomic model cannot be productive. A feasible new model of global development should be based on the principles of justice, efficiency and social solidarity” (Kirill, 2010).

3.3 Culture and Society Various cultures and societies have inherited common values imbibed from their

religious teachings. The way of life, system of beliefs and thoughts of every society forms the social fabric of the community. Creating awareness of cultures around the world helps to build mutual respect and a sense of social responsibility amongst people. Many multinational corporations today tend to adopt the culture of the local environment they are operating in as they recognize how useful these values are for their business prospects. This idea is captured in The Business of Humanity project currently undertaken by the University of Pittsburgh, which seeks to improve strategic decisions made in organizations. It proposes that:

“Strategic decision making that employs criteria falling under the rubric of "humanity" - in its two dimensions of "humaneness" and "humankind" - leads to superior economic performance. Humaneness in business decision-making focuses on criteria and programs related to safety, quality, diversity, environmental sustainability, gender equality, social sustainability, integrity, ergonomics and good design”(University of Pittsburgh, n.d.).

3.4 Education Advancement in education and technology is leading to greater awareness about

environment and inspiring people to adopt more environmentally friendly mechanisms such as ethical, green and SRI movements, etc. Besides the focus on management processes and the technicalities of finance, an integrated education system which inculcates values and ethics to students is also important (Mian and Sufi, 2014). Excellence in business and finance education is about creating value not only to the economy and financial industry, but also to society and contributing to sound economic growth, improving human conditions and balancing between social and economic needs. Management education should focus on deep study of universal laws, philosophy and ethics.

The Significance of Faith-based Ethical Principles ….

34 Journal of Islamic Banking and Finance Oct – Dec 2016

In addition, the syllabus taught in educational institutions should be reviewed to include a component of ethics and morality (Kabir, Rasem, Oseni, 2013). For example, since September 2014 financial education has formed part of the compulsory national curriculum for all maintained schools in England. Students of finance are usually taught the subject with focus on how they could maximize returns. It is not wrong to pursue profit but it should always be reinforced upon them to look at their role and responsibility as financial intermediaries for the general sections of the population who are financially less educated and more vulnerable.

3.5 Environment Nowadays investors do not just look at their cash flows, but are also concerned for

how these cash flows are generated. Many investors abstain from investing in firms that use child labor or adopt heavily polluting technologies (Schwegler and Reutimann, 2014).The investors today distinguish between “sin stocks” and clean investment opportunities (Hong, Kacperczyk, 2009).

There is also an increasing level of awareness of firms to engage in socially-responsible and environmentally-friendly business practices. There have been widespread efforts in the incorporation of sustainability in the strategic vision of many financial institutions, realizing the importance of enabling the future generations to also benefit. For example, The World Bank has already established its own sustainability initiative called Wealth Accounting and the Valuation of Ecosystem Services (WAVES), which seeks to promote accounting methodologies that place value on the environment. Many ecosystems have placed tangible value in the form of tourism, drug development, natural disaster prevention, etc. In new methodologies, environmental assets would be included when calculating GDP.

3.6 Socially Responsible Investments Socially responsible investing, also known as “sustainable”, “socially conscious”,

“green” or “ethical investing”, is a kind of investment strategy which seeks to consider both financial return and social good. These investors encourage corporate practices that promote environmental stewardship, consumer protection and human rights. They avoid businesses that sell or promote alcohol, tobacco, gambling, pornography, weapons, contraception/abortion, fossil fuel production, etc. According to data from the Social Investment Forum Foundation.socially responsible investing nearly quintupled in the U.S. from 1995 to 2010 as measured by the amount of professionally managed dollars invested, growing from 9 percent to 12 percent of the national total. The rise of socially responsible investments could be an indicator of the growing importance of ethics and other social aspects in finance and Statman (2004) and Bollen (2007) opined that investors benefit from some utility from the externalities of investing in a way that is consistent with their beliefs.

4. Conclusion And Policy Recommendations Financial crises have been primarily a result of the personal, organizational and

ethical failures of not only financial players but also of the regulators and other players in the financial system. This paper attempted to highlight some of the important common teachings of various religious communities and how some emphasis on them could help to shape a better financial system that is more inclusive, stable and efficient.

Journal of Islamic Banking and Finance Oct – Dec 2016 35

Ethical values represent a general theme that runs across various faith based

communities, which eventually led to the introduction of SRIs. Similarly, the Islamic concept of economics is built on ethical business practices that promote justice, equity, and fair distribution of economic and financial resources.