all about your retirement benefits 4 new-look scheme introduced 1 april 2008 retirement 6 when can i...

TRANSCRIPT

All about your retirementbenefits

West Midlands Pension Fund

The Local Government Pension Scheme (LGPS)

October 2008

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 1

Introduction 4New-look Scheme introduced 1 April 2008

Retirement 6When can I retire?

What are my retirement benefits?

Membership

Final pay

How your benefits are worked outwhen you retire changes from1 April 2008

How are my benefits worked out?

Can I give up some of my pension toincrease my lump-sum?

How will my pension be paid?

What if I am paying extra?

Will my pension increase?

Guaranteed minimum pension (GMP)

HM Revenue and Custom (HMRC)controls and your LGPS benefits

Ill-health retirement

Can I retire early?

Are there any penalties for retiringearly and drawing immediatebenefits?

Early retirement through redundancyor business efficiency

Flexible retirement

Retiring after age 65

Your state retirement benefits

Protection For Your Family 24What benefits will be paid if I dieafter retiring on pension?

How do I know if my children areclassed as eligible children?

Who is the lump-sum death grantpaid to?

What are the conditions for anominated cohabiting partner’ssurvivor’s pension?

What happens if I marry afterretirement?

Pension sharing order

How Your Pension Will Be Paid 29Your payslip explained

Voluntary payroll deductions

2

Contents

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 2

3

Minimum pensions

Pensions increase

Planning a marriage or civilpartnership after retirement?

Pensions and divorce or dissolutionof a civil partnership

Some other LGPS provisions

Customer charter

Standards of service

Our commitment to our pensioners

Superlink - our pensioners’ newsletter

Pensions AdministrationService 41

Help With Pension Problems 38

Minimum Pensions and Pensions Increase 34

Retirement Annuity Service 44About the service

What is an annuity?

Providers

What are my options?

Tax-free cash

Special annuities

Help and information

Frequently Asked Questions (FAQs) 49

Some Terms We Use 52

Other Matters 36

Your New Income Tax Office 33

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 3

4

The information in this booklet isbased on the Local Government Pension Scheme (Administration)Regulations 2008 and the Local Government Pension Scheme (Benefits, Membership and Contributions) Regulations 2007 (asamended).

It applies to individuals who were contributing members of the LGPSon 1 April 2008 or who have sincejoined the Scheme.

The booklet was up-to-date at thetime of publication in October 2008. It is for general use and cannot coverevery personal circumstance, nordoes it cover specific protected rights

that apply to a very limited numberof employees. In the event of anydispute over your pension benefits,the appropriate legislation will prevail, as this booklet does not confer any statutory rights and isprovided for information purposesonly. This booklet has been issued bythe West Midlands Pension Fund (theFund) whose contact details appearon the back page.

The administering authority for thisFund is Wolverhampton City Council.

This booklet does not cover the benefits afforded to councillor members of the Local GovernmentPension Scheme.

Introduction

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 4

New-look Scheme introduced 1 April 2008On 1 April 2008, a new-look LocalGovernment Pension Scheme (LGPS)was introduced and all memberswho were paying into the Schemeon 31 March 2008 automatically became members under the newScheme and had the benefits in respect of their membership before 1 April 2008 banked, based on therules under the ‘old’ Scheme.

From 1 April 2008, the LGPS benefits will be:

• An improved pension based onfinal pay

• Survivor’s pensions

• Children’s pensions

• Cohabiting partner’s benefits

• Three times pay death in servicegrant

• Full inflation-proofing

• An option to give up part of thepension for a bigger lump-sum

• Flexible retirement

• Voluntary retirement from age 60

• Increased benefits with additionalcontributions

• Facility to retire early with employer’s consent

• Banked benefits for service up to31 March 2008

The new LGPS is still a final salaryscheme. This means that your benefits are normally based on yourfinal year’s pay and the number ofyears you have been a member ofthe Scheme.

5

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 5

6

When can I retire?You can retire and receive your LGPS benefits in full from age 65.The Scheme also makes provisionsfor the early payment of your LGPSbenefits and these are detailed in therelevant sections later on in thisguide.

What are my retirementbenefits?When you retire, you will receive a pension and if you have any pre-1 April 2008 membership a tax-free lump-sum from the LGPS. At state pension age you will also receive the basic flat-rate state

pension, if you have paid sufficientnational insurance contributions during your working life.

You can look forward to enjoying aguaranteed package of benefitswhen you retire.

Here, we look at how your retirement benefits are worked outand when you can retire if you payinto the LGPS on or after 1 April2008.

Your LGPS benefits are made up of:

• An annual pension that, after leaving, increases every year in linewith the cost of living for the restof your life, and

• The option to exchange part ofyour pension for a tax-free lump-sum paid on retirement.

The two main factors used to calculate your LGPS pension are:

• Your membership in the Scheme,and

• Your final pay.

RetirementTo be entitled to LGPS retirement benefits, you have to haveat least three months’ membership or have transferred other pension rights into the LGPS.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 6

7

If you joined the LGPS on or after 1 April 2008, for each year of membership you receive a pensionbased on 1/60th of your final pay –so if you have 40 years’ membershipyou get 40/60ths or two thirds ofyour final year’s pay as an annualpension.

If you joined the LGPS before 1 April2008, your benefits for membershipbefore 1 April 2008 are calculateddifferently as you will automaticallyhave banked the right to a tax-freelump-sum, for your membershipprior to 1 April 2008. In these circumstances, your benefits will bemade up of two parts to account forthe two periods of service pre- andpost-April 2008.

MembershipThe first important element used inworking out your pension is yourmembership. This normally includes:

• How long you have been a member of the LGPS worked out inyears and days – not includingmembership for which you already receive a LGPS pension orhold an LGPS deferred pension, normembership from any concurrent job you may have andexcluding any LGPS membership inrespect of which you have

received a refund or have transferred the pension rights toanother scheme.

• Membership purchased by a transfer from another scheme.Membership from a transfer in will count as pre-1 April 2008membership if you were contributing to the LGPS on 31March 2008 – otherwise it willcount as post-31 March 2008membership.

• Any extra membership you havebought with additional contributions or by converting in-house additional voluntary contributions (AVCs) into membership.

• Any extra membership awarded byyour employer.

• Any extra membership awarded bythe Scheme if you are retired because of permanent ill-health.

This could be different to your actual calendar length membershipof the LGPS. For example:

If you work part-time, your membership is reduced to its whole-time equivalent length to calculate retirement benefits, although calendar length membership is used to decide if you are eligible for a benefit.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 7

8

For example, if you work half-timefor 10 years, your benefits would be calculated on five years’ membership.

If you were in the LGPS before 1 April 2008, you should have beenmade aware about how previousmembership counts – if not, contactthe Fund for more details.

Final payThe other important element used inworking out your benefits is yourfinal pay.

This is usually the pay in respect of the final year of Scheme membership on which you paid contributions, or one of the previoustwo years if this is higher, and includes your:

• Normal pay

• Contractual shift allowance

• Bonus

• Contractual overtime

• Maternity pay, paternity pay, adoption pay, and

• Any other taxable benefit specifiedin your contract as being pensionable.

This may not include all your pay.We don’t include such things as carallowances (other than in some historical protected cases), casualovertime, travelling or subsistenceallowances, pay in lieu of notice orpay in lieu of loss of holidays.

If you are working part-time whenyou leave the LGPS, or worked part-time at some point during yourlast year of membership, your finalpay is the whole-time pay that youwould have received, if you hadworked whole-time.

If your pay is reduced in this periodbecause of sickness your final paywill be the pay that you would havereceived if you had not been off sickor on leave.

If you have maternity, paternity oradoption leave in this period forwhich you paid (or are deemed tohave paid) pension contributions,final pay includes the pay you wouldhave received had you not been onmaternity, paternity or adoptionleave.

If you downgrade or move to a jobwith less responsibility with youremployer in your last ten years, youhave the option to have your finalpay calculated as the average of anythree consecutive years in the lastten years (ending on a 31 March).

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 8

9

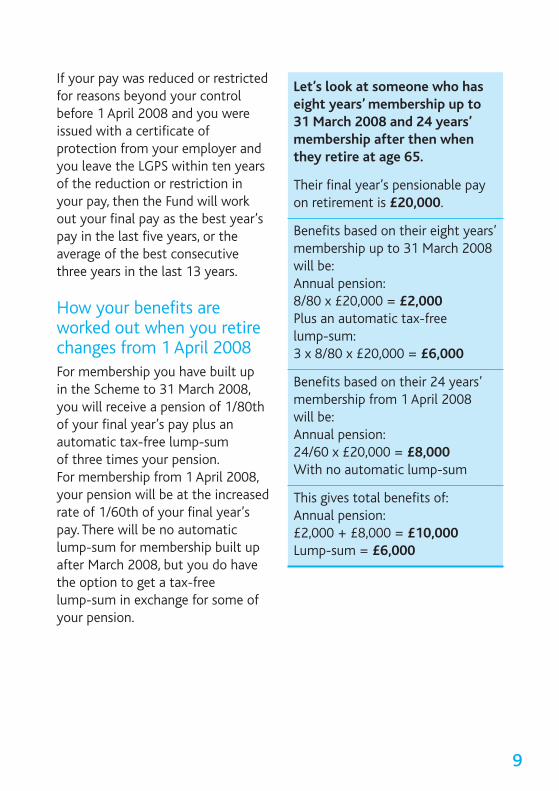

If your pay was reduced or restrictedfor reasons beyond your control before 1 April 2008 and you were issued with a certificate of protection from your employer andyou leave the LGPS within ten yearsof the reduction or restriction inyour pay, then the Fund will workout your final pay as the best year’spay in the last five years, or the average of the best consecutivethree years in the last 13 years.

How your benefits areworked out when you retirechanges from 1 April 2008For membership you have built up in the Scheme to 31 March 2008,you will receive a pension of 1/80thof your final year’s pay plus an automatic tax-free lump-sum of three times your pension. For membership from 1 April 2008,your pension will be at the increasedrate of 1/60th of your final year’spay. There will be no automaticlump-sum for membership built upafter March 2008, but you do havethe option to get a tax-free lump-sum in exchange for some ofyour pension.

Let’s look at someone who haseight years’ membership up to 31 March 2008 and 24 years’membership after then whenthey retire at age 65.

Their final year’s pensionable payon retirement is £20,000.

Benefits based on their eight years’membership up to 31 March 2008will be:Annual pension: 8/80 x £20,000 = £2,000Plus an automatic tax-free lump-sum:3 x 8/80 x £20,000 = £6,000

Benefits based on their 24 years’membership from 1 April 2008 will be:Annual pension: 24/60 x £20,000 = £8,000With no automatic lump-sum

This gives total benefits of:Annual pension: £2,000 + £8,000 = £10,000Lump-sum = £6,000

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 9

10

How are my benefits workedout?For membership you build up after31 March 2008:Your annual pension is calculated bydividing your total membership by60 and multiplying this figure byyour final pay.

You can take a tax-free lump-sum by giving up some of your annualpension. You can take up to 25% ofthe capital value of your LGPS benefits as a lump-sum. For every £1 of annual pension that you giveup you will receive an extra £12lump-sum. In the same way, givingup £100 of your annual pensionwould give you an extra £1,200lump-sum, and so on.

Here are examples of how your pension and lump-sum option isworked out for membership after 31 March 2008:

If you work full-time:

Let’s look at someone retiring at age 65 with 20 years’ full-timemembership in the Scheme and a final year’s pay of £18,000.

Their annual pension is:20 years x 1/60th x £18,000 = £6,000

If they decide to give up £1,500 pension for a cash lump-sum, then:

Their reduced annual pension is:£6,000 less £1,500 = £4,500

And they will get a tax-free lump-sum of: £1,500 x 12 = £18,000

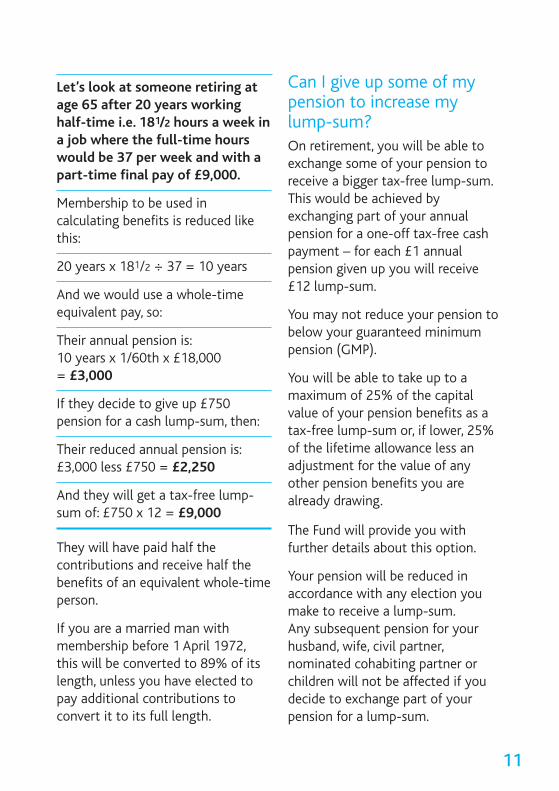

If you work part-time:

The same calculation is used, butyour membership is scaled down tothe whole-time equivalent lengthbased on your contractual hours andyour final pay is scaled up to the whole-time equivalent rate.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 10

11

Let’s look at someone retiring atage 65 after 20 years workinghalf-time i.e. 181/2 hours a week ina job where the full-time hourswould be 37 per week and with apart-time final pay of £9,000.

Membership to be used in calculating benefits is reduced likethis:

20 years x 181/2 ÷ 37 = 10 years

And we would use a whole-timeequivalent pay, so:

Their annual pension is:10 years x 1/60th x £18,000 = £3,000

If they decide to give up £750 pension for a cash lump-sum, then:

Their reduced annual pension is:£3,000 less £750 = £2,250

And they will get a tax-free lump-sum of: £750 x 12 = £9,000

They will have paid half the contributions and receive half thebenefits of an equivalent whole-timeperson.

If you are a married man with membership before 1 April 1972,this will be converted to 89% of itslength, unless you have elected topay additional contributions to convert it to its full length.

Can I give up some of mypension to increase mylump-sum?On retirement, you will be able to exchange some of your pension toreceive a bigger tax-free lump-sum.This would be achieved by exchanging part of your annual pension for a one-off tax-free cashpayment – for each £1 annual pension given up you will receive£12 lump-sum.

You may not reduce your pension tobelow your guaranteed minimumpension (GMP).

You will be able to take up to a maximum of 25% of the capitalvalue of your pension benefits as atax-free lump-sum or, if lower, 25%of the lifetime allowance less an adjustment for the value of anyother pension benefits you are already drawing.

The Fund will provide you with further details about this option.

Your pension will be reduced in accordance with any election youmake to receive a lump-sum. Any subsequent pension for yourhusband, wife, civil partner, nominated cohabiting partner orchildren will not be affected if youdecide to exchange part of your pension for a lump-sum.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 11

12

You may also elect to take up to100% of the accumulated fund inyour in-house AVC as a tax-freelump-sum, if you draw it at the sametime as your LGPS pension benefits,provided that when added to theLGPS lump-sum, it does not exceed25% of the overall value of yourLGPS benefits including your AVCfund. See the section on ‘What if Iam paying extra?’ in the next column.

How will my pension bepaid?Monthly pension payments will bemade, in arrears, direct into yourbank or building society account, although in some circumstancespayments can be made quarterly orannually. Similar arrangements canalso be made to pay your pensioninto your account should you moveabroad. Please see the section ‘HowYour Pension Will Be Paid’ on page29.

What if I am paying extra?If you are buying extra LGPS pension (additional regular contributions)Your contributions will cease whenyou retire (or cease the day beforeage 75 if you carry on in work beyond that age). You will be credited with the extra pension thatyou have paid for at the time ofleaving. This will increase the valueof your retirement benefits.

If you qualify for the type of ill-health pension where your benefits are based on enhancedmembership, you will be creditedwith all the extra pension that youset out to buy, even if you have notcompleted full payment for it.

If you retire early and draw yourbenefits before age 65, or retire onredundancy or business efficiencygrounds, the extra pension you havebought will be reduced for early payment.

If you draw your benefits on flexibleretirement, you will be able to drawthe extra pension you have paid for,although it will be reduced for earlypayment.

You can choose to exchange some ofthe extra pension you have boughtfor a cash lump-sum in the sameway as your main LGPS pension.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 12

13

If you are buying extra years inthe LGPS (added years) Your contributions will stop whenyou retire (or cease the day beforeage 75 if you carry on in work beyond that age) - but see below forthe rules on flexible retirement.

If you die in service, you will be credited with the whole extra periodof membership that you set out tobuy.

If you retire on ill-health grounds,you will normally be credited with the whole extra period of membership that you set out to buy, even if you have not completedfull payment for it.

In all other circumstances, you willbe credited with the extra period ofmembership that you have paid forat the time of leaving. This will increase the value of your retirement benefits.

If you retire early because of redundancy or business efficiency,you will have the opportunity to paythe remaining contributions due in alump-sum in order to complete yourcontract provided you retire at least12 months after making your election to pay extra.

If you draw your benefits on flexibleretirement you will continue to payfor any extra years you are buying.

The benefits from the extra membership will not be paid untilyou finally retire, unless you haveopted to stop paying the extra contributions before you take flexible retirement.

If you are paying in-house additional voluntary contributions(AVCs) If you are paying AVCs arrangedthrough the LGPS (in-house AVCs),your contributions will cease whenyou retire (or cease the day beforeage 75 if you carry on in work beyond that age).

Here are the different ways you canuse your in-house AVC fund:

∑• Buy an annuity This is where an insurance company,bank or building society of yourchoice takes the value of your AVC fund and pays you a pension inreturn.

You can do this at the same time asyou draw your LGPS benefits or youcan choose to delay payment untilany time up to the eve of your 75th birthday. An annuity is paidcompletely separately to your LGPSbenefits.

The amount of annuity depends onseveral factors, such as interest ratesand your age. You also have somechoice over the type of annuity – for

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 13

example, whether you want annualincreases, and whether you alsowant to provide for dependants’ benefits.

• Buy extra membership in theLGPSIf your election to start paying AVCswas made before 13 November2001, you may be able in certain circumstances, such as retirement on ill-heath grounds or on ceasingpayment of your AVCs before retirement, to convert your AVCfund into LGPS extra membership in order to increase your LGPS benefits. This membership counts as pre-1 April 2008 membership inthe calculation of your benefits.

• Take your AVCs as cashIf you draw your AVCs at the sametime as your LGPS pension, you maybe able to take some or all of yourAVCs as a tax-free lump-sum. Provided, when added to your LGPSlump-sum, it does not exceed 25%of the overall value of your LGPSbenefits (including your AVC fund)and the total lump-sum does not exceed £412,500 (2008/2009 figure) less the value of any otherpension rights you have in payment.

If you decide to draw your AVCslater, you can normally have up to25% of your AVC fund as a lump-sum.

You may be able to draw your AVCbenefits on flexible retirement.

• If you are paying for extra lifecover through AVCs.Any extra life cover paid for throughAVCs will stop on leaving (or ceasethe day before age 75 if you carryon in work beyond that age). You canno longer pay AVCs after leaving/after age 75.

Will my pension increase?Your LGPS pension increases in linewith the retail prices index (RPI)every year throughout your retirement. As the cost of living increases, so will your pension.If you retire early before age 55,apart from ill-health retirement,your pension is normally paid at aflat rate until age 55, when it will beincreased every year by the rise inthe cost of living since your early retirement. If you are retired on ill-health grounds, your pension isincreased each year regardless ofyour age.

14

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 14

Guaranteed minimum pension (GMP)If your membership in the LGPS includes a GMP, at state pension ageyour LGPS pension will be comparedwith your GMP and increased to therate of your GMP should this behigher. In most cases, your LGPSpension is higher than your GMP.See the section on ‘Minimum Pensions and Pensions Increase’ onpage 34.

HM Revenue and Custom(HMRC) controls and yourLGPS benefits There are HMRC controls on thepension savings you can have beforeyou become subject to a tax charge(over and above any tax due underthe PAYE system on a pension inpayment).

The lifetime allowance is the totalcapital value of all your pensionarrangements which you can buildup without paying extra tax.

If the value of your benefits whenyou draw them (not including anystate retirement pension, state pension credit or any spouse’s, civilpartner’s or dependant’s pension you may be entitled to) exceed your lifetime allowance a tax chargewill be made against the excess.

The lifetime allowance for2008/2009 is £1.65 million. MostScheme members’ pension savingswill be significantly less than thelifetime allowance.

There are protections for benefitsearned up to 5 April 2006 in respectof those high earners affected by the introduction of the lifetime allowance from 6 April 2006. We will let you know the value ofyour LGPS benefits on retirementand ask you about any other pensions you may have in payment,so we can work out whether weneed to deduct a recovery taxcharge. If you do not provide this information promptly it could delaythe payment of your pension.

Also, under HMRC rules, if the LGPSmakes an unauthorised payment orif you pay some or all of your LGPSlump-sum back into a pensionarrangement, there will be a taxcharge.

15

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 15

Ill-health retirement

What happens if I have to retireearly due to permanent ill-health?If you have to leave work due to illness, you may be able to receiveimmediate payment of your benefits.

To qualify for ill-health benefits,your employer, based on an opinionfrom an independent specially qualified doctor, must be satisfiedthat you will be permanently unableto do your own job and that youhave a reduced likelihood of beingcapable of obtaining gainful employment before age 65.

Ill-health benefits can be paid at anyage and are not reduced on accountof early payment – in fact, your benefits could be increased to makeup for your early retirement.

There are graded levels of benefitbased on how likely you are to becapable of obtaining gainful employment after you leave.

The different levels of benefit are:

Tier 1

If you have no reasonable prospectof being capable of obtaining gainful employment before age 65,ill-health benefits are based on themembership you would have had ifyou had stayed in the Scheme untilage 65.

Tier 2

If you are unlikely to be capable ofobtaining gainful employmentwithin three years of leaving, butyou may be capable of doing so before 65, then ill-health benefitsare based on your membership builtup to leaving plus 25% of your prospective membership from leaving to age 65.

Tier 3

If you are likely to be capable of obtaining gainful employmentwithin three years of leaving,ill-health benefits are based on your membership at leaving. Payment of these benefits will bestopped after three years, or earlierif you are in gainful employment or become capable of getting such employment.

16

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 16

Gainful employment means paidemployment for not less than 30hours in each week for a period ofnot less than 12 months.

If you are part-time, any extra membership awarded due to ill-health retirement will be reducedto reflect your part-time hours atleaving, disregarding any reductionin hours due to your illness.

Example Tier 1

A Scheme member aged 53 with five years’ calendar length membership retires due to permanent ill-health and is found to be incapable of any work beforeage 65.

Membership used to work out themember’s retirement benefits:

Actual membership: 5 years

Extra membership: 12 years (100%of membership to age 65)

Total membership used in workingout benefits: 17 years

Example Tier 2

If the same Scheme member aged53 with five years’ calendar lengthmembership retires due to permanent ill-health, but is found tobe incapable of some gainful employment after three years, themembership used to work out themember’s retirement benefits wouldbe as follows:

Actual membership: 5 years

Extra membership: 3 years (25% ofmembership to age 65 – 12 years)

Total membership used in workingout benefits: 8 years

*Please note that members agedover 45 at 1 April 2008 retired onhealth grounds will be granted theextra years they would have received under the regulations priorto April 2008. So, for this example,an additional 62/3 years, making112/3 in total.

If you are part-time, any extra membership awarded due to ill-health retirement will be reducedto reflect your part-time hours atleaving, disregarding any reductionin hours due to your illness.

17

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 17

Tier 1 – Part-time

Once again, the Scheme memberaged 53, but this time with fiveyears’ part-time membership (jobshare – 50%) retires due to permanent ill-health and is found to be incapable of any work beforeage 65.

Membership used to work out themember’s retirement benefits:

Calendar length membership isreduced to work out benefits

Actual calendar length membership= 5 years which is reduced to 21/2

years to work out benefits.

Extra membership = 12 years whichis reduced to 6 years for part-timeworkers.

Total membership used in workingout benefits is 21/2 + 6 = 81/2 years.

If you were paying extracontributions to buy added years,you will be credited with the wholeextra period of membership that youset out to buy, even if you have notcompleted your full contract.

Your increased membership, however, must not exceed the totalmembership you would have accrued had you continued in employment until age 65 (or, in the case of coroners, until age 70).

If you qualify for the type of ill-health pension where your benefits are based on enhancedmembership, you will be creditedwith all the extra pension that youset out to buy, even if you have notcompleted full payment for it.

Ill-health pensions are increasedeach year in line with the RPI regardless of age.

Can I retire early?You can elect to retire and receiveyour LGPS benefits from age 60 onwards. You may be able to retireand receive your LGPS benefits fromage 55 (or from age 50 if you joinedthe LGPS before 1 April 2008 and retire and elect to receive your benefits before 1 April 2010), butonly if your employer agrees. This isan employer discretion; they mustset out their policy on this in a published statement.

18

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 18

Are there any penalties forretiring early and drawingimmediate benefits?If you retire before age 65, yourLGPS benefits, initially calculated asset out earlier, will be reduced totake account of their early paymentand the fact that your pension willbe payable for longer.

If you were in the LGPS on 30 September 2006, some or all of yourbenefits paid early could be protected from the reduction underwhat is called the 85-year rule.

The 85-year rule is satisfied if yourage at the date you draw your benefits and your Scheme membership (each in whole years)add up to 85 or more.

If you are part-time, your membership counts towards therule of 85 at its full calendar length.

Not all membership may count towards working out whether youmeet the 85-year rule.

Working out how you are affectedby the 85-year rule can be quitecomplex, but this should help youwork out your general position.

• If you would not satisfy the 85-year rule by the time you are 65,then all your benefits are reduced ifyou choose to retire before 65. The reduction will be based on howmany years before 65 you draw yourbenefits.

• If you will be age 60 or over by 31 March 2016 and choose to retirebefore age 65, then, provided yousatisfy the 85-year rule when youstart to draw your pension, the benefits you build up to 31 March2016 will not be reduced.

• If you will be under age 60 by 31 March 2016 and choose to retirebefore age 65, then, provided yousatisfy the 85 year rule when youstart to draw your pension, the benefits you build up to 31 March2008 will not be reduced. Also, if you will be aged 60 between 1 April2016 and 31 March 2020 and meetthe 85-year rule by 31 March 2020,some or all of the benefits you build up between 1 April 2008 and31 March 2020 will not have a full reduction.

The early retirement reduction iscalculated in accordance with guidance issued by the GovernmentActuary’s Department from time totime. Further reductions apply wherethe number of years paid early is between 6 and 15.

19

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 19

Your employer can agree not tomake these reductions on compassionate grounds. This is anemployer discretion. You can askthem what their policy on this is.

You can reduce or avoid the reductions by not taking immediatepayment of your benefits on retirement (i.e. by delaying paymentuntil a later date). If you decide notto draw immediate benefits, thebenefits would normally becomepayable at age 65, but you can deferpayment beyond that age, althoughbenefits must be paid by age 75. If benefits are deferred beyond age65 they will be increased accordinglyto reflect late payment. If you are awoman and you defer payment afteryour state pension age, we have topay you the GMP element (if any) ofyour pension from your retirementdate or state pension age if later.

Generally, if you were a member ofthe Scheme before 6 April 1997,your pension must not be reducedlower than a minimum level.

This will equal 1/80th of your finalpay for each year of your totalmembership in contracted-out employment on and between:

• 6 April 1978 and 30 April 1995 ifyou are female, and

• 17 May 1990 and 30 April 1995 ifyou are male.

In addition, once you have attainedstate pension age, the LGPS mustguarantee to pay your pension atleast at the level of your GMP.

A female Scheme member whochooses to receive her benefits before her normal retirement date incircumstances where her pension is

20

No. of years Pensions reduction Lump-sumpaid early Men Women reduction

0 0% 0% 0%1 6% 5% 2%2 11% 10% 5%3 16% 15% 7%4 20% 19% 9%5 24% 23% 12%

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 20

reduced to less than the level of herGMP, will have her pension increasedimmediately to the level of her GMPon attaining state pension age.

A male Scheme member will receivea reduced pension until age 65,when it will be increased to matchhis GMP if greater.

If a female Scheme member leavesher employment, but defers payment of her benefits after statepension age, then her GMP ispayable from the later of state pension age or her date of leaving. If employment continues for morethan five years beyond state pensionage, payment of the GMP cannot bedelayed beyond five years unless theScheme member agrees to the postponement.

If your employer gives consent toyour early voluntary retirement onor after age 55 and before age 60,your pension will be increased eachyear in line with the RPI.

Early retirement through redundancy or business efficiencyIf you are aged 55 or over (or 50 orover if you joined the LGPS before 1 April 2008 and retire on grounds of redundancy or business efficiencybefore 1 April 2010), you will be entitled to the immediate unreduced payment of your LGPSbenefits.

Your employer may also enhanceyour benefits at their discretion. Your employer can award you withup to ten years’ additional membership to improve your retirement benefits. They can alsogrant you up to £5,000 extra annualpension. These are discretions youremployer can use if they so wishand they will publicise their policyon this for your information.

Flexible retirementCan I have a gradual move into retirement?Rather than continuing in your jobto 65 or beyond you may wish toconsider the possibility of flexible retirement. From age 55, if you reduce your hours or move to a lesssenior position, and provided youremployer agrees, you can draw some

21

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 21

or all of the pension benefits youhave built up – helping you ease intoretirement. Your employer will have apolicy on flexible retirement. You canask your employer for details of theirpolicy.

If your employer agrees to flexibleretirement you can still draw yourwages/salary from your job on thereduced hours or grade and continuepaying into the LGPS, building upfurther benefits in the Scheme. Your election to receive benefits has to be made to your fund administrator – for instance, theWest Midlands Pension Fund.

If you were in the LGPS on 31 March2008, you may have an earlier ageyou can ask for flexible retirement.You can find out more about thisfrom the Fund.

Will my pension and lump-sum be reduced if I take flexible retirement?If you take flexible retirement beforeage 65, your benefits initially will becalculated as detailed in the section‘Are there any penalties for retiringearly’ on page 19 and will be reduced for early payment.

Your employer may, however, determine not to apply all or part ofany reduction. You can ask themwhat their policy on this is.

If you receive payment of your benefits on flexible retirement, thenyour benefits will not be subject toreduction or suspension for re-employment while you are in ajob with the employer that allowedyou to take flexible retirement.

If you take flexible retirement afterage 65, your benefits initially calculated, – as detailed in the section on ‘Retirement’ on page 6 –will be increased to reflect late payment.

Membership built up to the date offlexible retirement will count in yourcontinuing employment to decidewhether you have the three monthsminimum membership to qualify fora benefit when you finally leave yourcontinuing employment.

Retiring after age 65What if I carry on working afterage 65?If you choose to carry on workingafter age 65 you will continue to payinto the LGPS, building up furtherbenefits. You can receive your pension when you retire althoughyour pension has to be paid by your75th birthday. Also, if you retire at orafter age 65 you can, if you wish, defer drawing your pension but youmust draw it by age 75.

22

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 22

23

Because you will have already passedage 65 when you retire, there are noearly retirement reductions to yourbenefits, no matter how little membership you have. In fact, if youdraw your pension after age 65 yourbenefits will be paid at an increasedrate.

Your state retirement benefitsThe state pension age is 65 for menand 60 for women. However, fromthe year 2020, the Government willhave equalised the state pension agefor both men and women at 65. Theincrease in the state pension age forwomen will be phased in graduallyfrom the year 2010 as shown below.

Date of birth State pension age

Before 6 April 1950 606 April 1950 - 5 April 1951 Between 60 & 616 April 1951 - 5 April 1952 Between 61 & 626 April 1952 - 5 April 1953 Between 62 & 636 April 1953 - 5 April 1954 Between 63 & 646 April 1954 - 5 April 1955 Between 64 & 65After 5 April 1955 65

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 23

24

Protection For Your Family

What benefits will be paid if I die after retiring on pension?If you die after retiring on pension,your benefits will no longer bepayable.

Your husband, wife, civil partner, cohabiting partner, next-of-kin orperson dealing with your estate must immediately inform the Fundof your date of death as otherwisean overpayment could occur. Contact details appear on the back page of this booklet.

The following benefits may then bepayable on your death:

If you ceased membership of theScheme before 1 April 2008, thedeath grant and benefits payable toyour survivor may differ as they areapplicable to the LGPS regulations inforce at the time of leaving theScheme.

A lump-sum death grant will be paidif you die within the first ten yearson pension, and you are under age75. The amount payable would beten times your annual pensionreduced by any pension already paid to you (ignoring any reduction

in your pension as a result of re-employment by an employer offering membership of the LGPS).

A survivor's pension: a pension willbe paid to your husband, wife, registered civil partner or, subject tocertain qualifying conditions, yournominated cohabiting partner. This pension is payable immediatelyafter your death for the rest of theirlife and will increase every year inline with the cost of living.

For your husband or wife: the pension payable is equal to 1/160thof your final pay times the membership your pension is basedon, unless you marry after retirement, in which case it could beless. If you marry after retiring:

- your husband’s pension is based onyour membership after 5 April1988, (excluding, unless you weremarried to your husband at sometime whilst you paid into the LGPS,additional membership purchasedby you or granted to you by youremployer or the Scheme),

- your wife’s pension is based onyour contracted-out membershipafter 5 April 1978.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 24

25

- your membership of the LGPS includes a GMP, your wife’s pension must not be less than halfyour GMP. Your husband’s or civilpartner’s pension must not be lessthan half your GMP built up after 5 April 1988.

For your civil partner or nominatedcohabiting partner: the pensionpayable is equal to 1/160th of yourfinal pay times your membership inthe Scheme after 5 April 1988.

Children's pension: these are payableto eligible children and increaseevery year in line with the cost ofliving.

The amount of pension depends onthe number of eligible children youhave:

• If a survivor's pension is being paidto your husband, wife, civil partneror nominated cohabiting partner,one child would receive 1/320th of your final pay times the membership your pension is basedon, while two or more childrenwould receive 1/160th sharedequally between them.

• If there is no husband’s, wife’s, civilpartner’s or nominated cohabitingpartner's pension being paid, one child would receive 1/240th ofyour final pay times the membership your pension is basedon, while two or more children

would receive 1/120th sharedequally between them.

If you paid additional contributionsto buy extra LGPS pension and youopted to pay for dependant's benefits when you took out youroriginal contract, then extra benefitswill be payable to your husband,wife, registered civil partner or nominated cohabiting partner and to eligible children.

How do I know if my children are classed as eligible children?Eligible children are your children.They must, at the date of your death:

• be under 18 and be wholly ormainly dependant on you, or

• be aged 18 or over and under 23,be dependent on you, and be infull-time education or undertakingvocational training (although a dependant child who commencesfull-time education or vocationaltraining after the date of yourdeath may be treated as an eligiblechild up to age 23), or

• in some cases, a dependent childof any age who is disabled may beclassed as an eligible child.

In all cases, the children must havebeen born before or within a year ofyour death.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 25

Who is the lump-sum deathgrant paid to?The LGPS allows you to say who youwould like any death grant to bepaid to by completing a nominationform.

The Fund has absolute discretionover who receives any lump-sumdeath grant – they can pay it to yournominee or personal representativesor to any person who appears, at anytime, to have been your relative ordependant. If any part of the deathgrant has not been paid by the second anniversary of your death, itmust be paid to your personal representatives, i.e. to your estate.

If you have not already made yourwishes known, or you wish to changea previous nomination, a form isavailable from the Fund. Remember to complete a new formif your wishes change.

If you have not previously completed a nomination form, orwish to revise your nomination,please contact the helpdesk on 0300111 1665 who will arrange for a form to be sent to you.

Your personal representatives willhave to determine whether, with thelump-sum death grant, the capital

value of your overall pension benefits (not including any spouse’s,civil partner’s or dependant’s pensions) exceeds the HMRC allowance. Under HMRC rules, any excess will be subject to a recoverytax charge. Most Scheme members’pension savings will be significantlyless than the allowance. You can findmore information on this from theFund.

What are the conditions fora nominated cohabitingpartner’s survivor’s pension?To be able to nominate a cohabitingpartner, of either opposite or samesex, to receive a survivor's pensionon your death, all of the followingconditions must have applied toboth you and your nominated cohabiting partner for a continuousperiod of at least two years on thedate you both sign the nominationform:

• You must have been a contributingmember of the LGPS on or after 1 April 2008.

• Both you and your nominated cohabiting partner are, and havebeen, free to marry each other orenter into a civil partnership witheach other, and

26

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 26

• You and your nominated cohabiting partner have been living together as if you werehusband and wife, or civil partners, and

• Neither you or your nominatedcohabiting partner have been living with someone else as ifyou/they were husband and wifeor civil partners, and

• Either your nominated cohabitingpartner is financially dependent on you or you are financially interdependent on each other.

You make a nomination bycompleting a nomination form available from the Fund. A nomination is only valid if all ofthe above conditions have been metfor a continuous period of at leasttwo years on the date you both signthe form.

On your death, a survivor’s pensionwould be paid to your nominatedcohabiting partner if:

• The nomination has effect at thedate of your death, and

• Your nominated cohabiting partner satisfies us that the aboveconditions had also been met for acontinuous period of at least two

years immediately prior to yourdeath.

• Widow’s,widower’s, civil partner’s,children's and nominated cohabiting partner’s pensions are increased each year in line withthe RPI, regardless of age.

• Since 1 April 1998, widow's, widower's and civil partner’s pensions are payable for life even if your widow, widower or civilpartner remarries, enters into anew civil partnership or cohabits.

This applies where you are a contributing member of the LGPS on or after 1 April 1998 and yourwidow or widower or civil partner remarries, enters into a new civilpartnership or cohabits after 1 April 1998. Your administering authority has the discretion to allowwidow’s, widower’s and civil partner’s pensions to continue inpayment where the remarriage, civil partnership or cohabitationcommenced after 31 March 1998,but you ceased to be a contributingmember of the Scheme earlier. This is an administering authoritydiscretion; you can ask your administering authority what theirpolicy is on this matter.

27

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 27

What happens if I marryafter retirement?If you marry after retirement, awidow's pension based on your contracted-out membership after 5 April 1978, or a widower’s pension based on your membershipafter 5 April 1988, (excluding additional membership purchased by you or granted to you by youremployer or the Scheme), will bepayable. If you enter into a civil partnership after retirement, a civilpartner’s pension based on your total membership after 5 April 1988 will be payable.

Pension sharing orderIf your pension benefits are subjectto a pension sharing order issued bythe court following a divorce or annulment of marriage or the making of an order for the dissolution or nullity of a civil partnership, or are subject to a qualifying agreement in Scotland,your benefits will be reduced in accordance with the court order oragreement. In consequence, if youremarry or enter into a new civilpartnership, any spouse's pension or civil partner’s pension payable following your death will also be reduced. Benefits payable to eligible children will not, however, be reduced because of a pensionshare.

28

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 28

29

Your pension will normally be paidon the 25th of each month by directcredit to your nominated bank,building society or post office account. Your payslip will be sent toyour home address. Consequently,you should inform us immediately(using the back of your payslip) ifyou change your banking details oryour address. Alternatively, contactthe helpdesk on 0300 111 1665.

If the 25th falls during a weekend orbank holiday, your pension will becredited on the previous workingday.

Your first payment of pension maybe for a part of or for more than onemonth.

If you are planning to live abroad,and wish your pension to be paid toyour foreign bank account, yourpension will be paid to you on aquarterly basis each March, June,September and December.

There are three methods of payment:

To a bank or building society inthe UK.

Direct into a foreign bank account via the TranscontinentalAutomated Payment System(TAPS).

If you live in Jamaica, there are alternatives to TAPS. Please contact the Fund direct if you require details of these options.

TAPS application forms, togetherwith details of the costs of this service, are available from the Fund.For small pensions, one payment ismade per year, in March. You are advised to check that your pensionhas credited your account beforemaking any withdrawals.

Please note:We cannot accept liability for delaysin either the banking or postal system.

How Your Pension Will Be Paid

1

2

3

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 29

30

Your payslip explained

1 Your name and address:If you move house, please write to us to let us know your new address. (The reverse side of your payslip has a cut-off section for this purpose). Alternatively, you can contact us bytelephone.

2 Our address:Where to address all correspondence

3 Personal reference number:This number helps us to identify youquickly. Please quote this number when you telephone or write to us.

4 Contact details:Telephone, fax, e-mail and website contact details.

5 Our location:Where our offices are located.

6 Messages:Space for periodic messages giving useful information.

7 National Insurance number:Always quote this number when raising queries with the tax office.

8 Method of payment: How your pension is paid.

9 Gross pension/other payments:Total pension/other payments this pay date.

10 Income tax:Tax this pay date. When a tax refund is payable the amount shown will be followed by the letter ‘R’.

11 Other deductions:Details of other deductions.

12 Total deductions:Total deductions made this pay date.

13 Net pension:This is the amount of your payment.

14 Tax queries:This is the address and telephone number of the tax office responsible for dealing with your pension.

15 P45 gross pay and tax:Figures notified to us by the tax office.

16 Tax paid to date:Total amount of tax paid - since April of the current financial year.

17 Gross pension to date:Total pension - before tax - since April of the current financial year.

18 Pension date:This is the date of payment.

19 Tax period:Tax period of the current year.

20 Tax code/basis:Your personal tax code as notified by the tax office.

21 Notification of change of addressand/or banking details:The reverse side of your payslip has a cut-off section which you should complete and return to us following any change to your address orbank/building society details. Alternatively, if you have registered a password, you can contact us by telephone.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 30

31

21

1

2

3

5

4

6

718 19 20 8

9

10

11

12

13

14

15

16

17

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 31

Voluntary payroll deductionsIf you have been paying contributions to any of the schemesshown on this page from your wagesor salary and have requested thatyour membership be transferred, adeduction at the appropriate ratewill be made from your monthlypension.

Please note: If this arrangement applies in yourcase any request for claim forms(and information) should be madedirect to the organisation concerned.

The SecretaryPaycarePaycare House, George Street,Wolverhampton WV2 4DXTel: 01902 371000

HSA Personal Medical PlansHambleden House,Waterloo Court, Andover, Hampshire SP10 1LQTel: 0800 328 1202

32

The Subscriptions Co-ordinatorForester Health, Forester House,Cromwell Avenue, BromleyBR2 9BFTel: 0800 073 0303

BHSF LtdGamgee House, 2 Darnley Road,Birmingham B16 8TETel: 0800 622552

Completed claim forms must be returned direct to the organisationsconcerned.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 32

33

Please note that the income tax office responsible for dealing withyour pension is:

HM Revenue & CustomsBirmingham Solihull Area ServiceCity Centre House30 Union StreetBirminghamB2 4AE

Tax reference: 068/W105

Tel: 0845 302 1437

In accordance with tax office instructions, you will be taxed onmonth 1 basis until further instructions are received from them.

If parts 2 and 3 of your P45 are notreceived by us, your pension will betaxed using BR code until further instructions are received from thetax office. You should retain part 1a of your P45.

A BR code shows that the basic rateof income tax (20% as at April 2008)is to be applied and that no ‘free pay’allowance or lower rate relief isgiven.

If you are moving overseas, any application for exemption from UKincome tax should be sent to:

HM Revenue & Customs Centrefor Non-ResidentsFitzroy HousePO Box 46NottinghamNG2 1BD

Tel: (from within UK) 0845 070 0040(from outside UK) +44 151 210 2222

Contact us:Emails can be sent via the website:www.hmrc.gov.uk/cnr

Your New Income Tax Office

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 33

34

Minimum pensionsThe LGPS is a pay-related schemeand is contracted-out of the statesecond pension (S2P). This meansthat you must receive a minimumlevel of pension from us at leastequivalent to the additional pensionyou would have received from thestate (at state pension age) had youbeen in S2P or other state provisionduring your LGPS membership.

The S2P is the additional pensionprovided by the state in respect ofan employee’s national insuranceearnings, between lower and upper limits, from 6 April 1978 for each year of their working life.Employees who are not in a contracted-out scheme will be automatically in the S2P. Employees who have a period ofcontracted-out employment willhave their state additional pensionreduced accordingly.

The minimum level of pension youare entitled to receive (at state pension age) is based on your GMPentitlement for employment between 6 April 1978 and 5 April1997.This is broadly equivalent tothe additional pension you wouldhave received from S2P or otherstate provision.

Minimum Pensions and Pensions Increase

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 34

35

Pensions increaseThe law says that all LGPS pensionsin payment must be fully increasedin line with the RPI which measuresprice inflation, so that they maintain their purchasing power.These increases are paid by us upuntil your state pension age, atwhich time the state then becomesjointly responsible for pensions increase.

N.B. LGPS pensions paid followingretirement before age 55, except inthe case of ill-health retirement,are not increased until age 55.

When you reach state pension age,the law says that the part of yourpension which relates to your GMPmust be increased overall in linewith RPI. As mentioned, the responsibility for increasing the part of your LGPS pension that relates to your GMP is then sharedbetween us and the state. Therefore,responsibility for pensions increase(from state pension age) will be asfollows:

(i) for that part of your GMP thatrelates to employment from 6 April 1978 to 5 April 1988, the increases will be made entirely by the state,

(ii) for that part of your GMP thatrelates to employment from 6 April 1988 to 5 April 1997, theincreases will be made by us upto a maximum of 3% a year - the state pays anything above3%, and

(iii) for that part of your LGPS pension, in excess of your GMP,the increases will be madeentirely by us in line with RPI -these increases are not limitedto a 5% maximum as in manyother schemes.

N.B. Pensions increase, paid by thestate, is paid in addition to yourbasic state pension. However, special conditions apply if you liveabroad in certain countries.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 35

36

Planning a marriage or civilpartnership after retirement?If you decide to enjoy the rest ofyour retirement by sharing it with anew husband, wife or civil partner,don’t forget to let us know and sendyour marriage/civil partnership certificate for registration.

It is necessary for you to keep us informed of any changes in your circumstances, so that we can keepyour pension record up to date and,when you are no longer around, wewill be able to finalise your affairswith the minimum of worry and

inconvenience to your family andfriends.

State pension benefitsIf you have reached state pensionage, any queries regarding state benefits should be addressed to your local office of The PensionsService (The Pensions Service is partof the Department for Work andPensions).The address and telephonenumber can be found in your telephone directory.

ModificationIf you joined the LGPS before April1980 and left the Scheme before 1 April 1998, your pension may besubject to a small reduction to takeaccount of state benefits.

Other Matters

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:02 Page 36

Pensions and divorce or dissolution of a civil partnershipYou may wish to get legal advicefrom your solicitor on how to dealwith your LGPS benefits and youand your partner will need to consider how to treat your pensionrights as part of any divorce/dissolution settlement.

What is the process to be followed?You will need specific informationabout your LGPS benefits as part ofthe proceedings for a divorce, judicial separation or nullity of marriage, or for dissolution, separation or nullity of a civil partnership.

You or your solicitor should contactthe Fund for this information, including an estimate of the cashequivalent value (CEV) of your pension rights.

The court will take this value intoaccount in your settlement. In Scotland, only the pension rightsbuilt up during your marriage/civilpartnership are taken into account.

All correspondence received by theFund in connection with divorce ordissolution proceedings will be acknowledged in writing. If no acknowledgement is received, youshould contact the Fund to ensurethat your correspondence has beenreceived.

37

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 37

38

Some other LGPS provisions

The LGPS requires your administering authority to:

• pay interest on lump-sum benefits that are paid more thanone month after they should havebeen paid.

• pay interest on pensions that arepaid more than a year after theyshould have been paid.

The LGPS allows your administering authority to:

• reduce pension benefits if a LGPSmember ceases to be employed asa result of a criminal, negligent orfraudulent act, or omission.

• forfeit a LGPS member’s pensionrights if the Secretary of State forthe Department for Communitiesand Local Government agrees andthe member has been convicted ofa serious offence connected withtheir employment.

The LGPS does not allow you to:

• assign your benefits. Your LGPSbenefits are strictly personal andcannot be assigned to anyone elseor used as security for a loan.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 38

39

In this section, we look at what youcan do if you are not happy about adecision made about your LGPS pension position.

Who can help me if I have aquery or complaint? If you are in any doubt about yourLGPS benefit entitlements, or have a problem or question about yourLGPS membership or benefits, please contact the Fund in the firstinstance. Contact details can befound on the reverse of this publication. We will seek to clarify or put right any misunderstandingsor inaccuracies as quickly and efficiently as possible.

If your query is about your contribution rate, or relates to thecontributions you have paid, pleasecontact your employer’s personnel/human resources or payroll section, so they can explain how they havedecided which contribution bandyou are in.

If you are still dissatisfied with anydecision made in relation to theScheme you have the right to have

your complaint independently reviewed under the Scheme’s internal disputes resolution procedure.

There are also a number of otherregulatory bodies that may be ableto assist you.

Here are the various ways you canask for help with a pension problem.

Internal disputes resolution procedure (IDRP)In the first instance you should writeto the person nominated by thebody who made the decision aboutwhich you wish to appeal, eitheryour employer or your pension fundadministering authority. You must dothis within six months of the date ofthe notification of the decisionabout which you are complaining.This is a formal review of the initialdecision and is an opportunity for itto be reconsidered. The nominatedperson will consider your complaintand notify you of his/her decision. If you are dissatisfied with that person’s decision, you may, withinsix months of the date of the decision, apply to the Fund’s

Help With Pension Problems

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 39

40

administering authority – in the caseof the West Midlands Pension Fund,this is Wolverhampton City Council –to have it reconsidered.

The Fund can tell you who your employer's/the Fund’s administeringauthority’s nominated person is andsupply you with a more detailedleaflet on the IDRP together with aform to fill in, or you can ask youremployer. Contact details for theFund are on the reverse of this publication.

The Pensions Advisory Service(TPAS) TPAS is available at any time to assist members and beneficiaries ofthe Scheme in connection with anypensions query they may have orany difficulty which they cannot resolve with their scheme administrators. TPAS can be contacted at:

11 Belgrave Road London SW1V 1RBTel: 0845 601 2923

Pensions OmbudsmanIn cases where a complaint or dispute cannot be resolved after theintervention of TPAS, an applicationcan be made, within three years ofthe event, to the Pensions Ombudsman for an adjudication.

The Ombudsman can investigateand determine any complaint or dispute involving maladministrationof the Scheme or matters of fact orlaw and his or her decision is finaland binding (unless the case is takento the appropriate court on a pointof law). Matters where legal proceedings have already startedcannot be investigated by the Pensions Ombudsman. The PensionsOmbudsman can be contacted at:

11 Belgrave Road London SW1V 1RBTel: 020 7834 9144

The Pensions Regulator This is the regulator of work-basedpension schemes. The Pensions Regulator has powers to protectmembers of work-based pensionschemes and a wide range of powersto help put matters right, whereneeded. In extreme cases, the regulator is able to fine trustees oremployers, and remove trusteesfrom a scheme. You can contact thePensions Regulator at:

Napier House Trafalgar Place Brighton BN1 4DW Tel: 0870 606 3636

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 40

41

How can I trace my pension rights? The Pension Tracing Service holdsdetails of pension schemes, includingthe LGPS, together with contact addresses. It provides a tracing service for ex-members of schemeswith pension entitlements (and their dependants) who have losttouch with previous employers. All occupational and personal pension schemes have to register ifthe pension scheme has currentmembers contributing to theirscheme or people expecting benefitsfrom the scheme. If you need to usethis tracing service, please write to:

The Pension Tracing Service The Pension Service Tyneview Park Whitley Road Newcastle upon Tyne NE98 1BATel: 0845 600 2537

Also, don’t forget to keep your pension providers up to date withany change in your home address.

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 41

42

Customer charter

• To deal with you promptly, fairlyand efficiently at all times and togive you the best possible service in accordance with thestandards.

• To give you the standard of serviceyou want.

• To consult you wherever possibleand to take account of your viewsbefore we make any changes.

• To be accountable to you for whatwe do by monitoring the quality of our service and reporting onhow well we’ve lived up to ourstandards.

Standards of serviceOur standards of service are set outon the following pages. They specifythe maximum turnround times inwhich we aim to take the action indicated. Better turnround timesmay be achieved in practice. In anyevent, the stated times will be reviewed at regular intervals. The target days stated are workingdays.

Our commitment to ourpensionersChanges in personal particularsWe will acknowledge receipt of apensioner’s written notification of achange in name, address, bank orbuilding society details and make theappropriate amendments to the pensioner’s payroll record withinthree days of receiving the writtennotification.

Deaths of pensionersWe will acknowledge receipt of a notification of the death of a pensioner and start action to putinto payment any dependants’ benefits within five days of receiving the notification.

Change of tax codeWe will update a pensioner’s payroll record with a revised tax code, within two days of receiving notice of the change from HMRC.

Pensions Administration Service

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 42

At least four times a year, we willsend you a copy of our pensioners’newsletter, Superlink, coveringtopical pension stories along withcontributions from Fund pensioners.

Superlink is usually issued in December, March, June and September.

Autumn 2008

West Midlands Pension Fund Pensioners’ Newsletter

superlink

rlink Autumn 2008:Layout 1 20/8/08 15:44 Page 1

Summer 2008

West Midlands Pension Fund Pensioners’ Newsletter

superlink

43

Spring 2008

West Midlands Pension Fund Pensioners’ Newsletter

superlink

S 147 Sup Sp

ring 2008:La

yout 1 25/9

/08 14:22

Page 1

“Exploitative, banal, vacuous, boring,

stupid.” I’ve just asked John Humphrys

what he thinks of reality TV and he’s

told me in no uncertain terms. Well,

what did I expect? He’s not known as

someone who minces words. “I’m a

grumpy old man,” he admits. “Not only

that,” he adds as he sits in his west

London study, “I was a grumpy young

man. Argumentative too. Always have

been. I get it from my father. And I’m

worst in the mornings. Well, wouldn’t

you be if you got up at three thirty?”

Humphrys’ early start is due to his

role as presenter on Radio 4’s Today

programme. You’d think he would be

used to it by now. March sees him

21 years in the role. With its mix of

news, current affairs and debate, the

Today programme is essential listening

for every part of the Establishment,

from City boardrooms to Westminster

corridors of power, and what’s more, it’s

the most popular radio current affairs

programme in the UK, attracting more

Summer 2008 Superlink 5

“I am at least as active,physically and mentally,as most 20 year olds.”

4 Superlink Summer 2008

Interview and words: Nic Kynaston than 6 million listeners every week.

Humphrys was born in the unlovely

district of Splott in Cardiff to solidly

working-class parents. His mother was

a hairdresser and his father a French

polisher. He says he always wanted to

be a journalist right from the days of

reading Superman comics and wishing

he was Clark Kent. He left school at 15

to get a job as a reporter on the

Penarth Times and soon ended up at

the BBC, where he became the

corporation’s youngest ever foreign

correspondent, covering stories from

the Watergate scandal to the end of

apartheid. Towards the end of the

1980s he landed the plum job of

presenting BBC1’s main Nine O’clock

News and it seemed like he had

exchanged the cut and thrust of

hard-nosed reporting for less hectic

presenting work. A life of televisual

celebrity beckoned. But Humphrys got

bored. So when a job on Radio 4’s

Today programme came up, he jumped

at the chance.

A privileged position

“My job on the Today programme is the

best in journalism,” he opines, a lilt of

pride in his voice. “It allows me to

indulge my curiosity. The core of

journalism is curiosity. If you’re not

curious about how the world works,

then you won’t make a good journalist.

On the Today programme I’m given

the opportunity to talk to the great and

the good and the powerful in a way

that almost nobody else can. It’s a

singularly privileged position to be in.

The one downside? Getting up in the

bloody mornings. I usually complain

about half a dozen different things,

mostly unjustifiably, because I am so

easily irritated at that time of the day.”

Humphrys uses this irascibility to

good effect though, and is famous for

his no-nonsense style of questioning

and persistence in getting answers.

It’s a role that he’s in no hurry to leave

either. A self-confessed workaholic,

he took over presenting TV quiz show

Mastermind in addition to his radio

work in 2003, just at the age when

most people start winding down the

workload. Though he turns 65 in August

he won’t be in discussions with the BBC

about his future either – firstly because

he’s under freelance contract to them

so doesn’t have to, and secondly

because it seems he genuinely enjoys

what he does, loves his life and doesn’t

want to change it. But that doesn’t stop

him feeling indignant that over-65s

working for an employer don’t have an

automatic right to carry on.

“I think a mandatory retirement age

is nonsense,” he says, giving a trademark

He thinks mandatory retirement ages are nonsense and plans tokeep the ‘best job in journalism’ as long as he can. John Humphrystells Heyday what drives him on.

Summer 2008 Superlink 13

Savings credit can be claimed bysingle people with an income of£87.30 - £167 per week, or by couples with a combined income of£139.60 to £245.00 per week.Savings credit can be paid up to amaximum of £19.05, if you are single and £25.26, if you are a couple (only one of you need be 65 years old), depending on youractual income between these figures.

The Pension Service operates atelephone service between 8am to8pm Monday to Friday and 9am to1 pm on Saturdays. The telephonenumber is 0800 169 0133. Calls arefree and staff will take you throughthe calculation and assist you toclaim.

For people wanting to do their owncalculation there is quick calculatoron www.direct.gov.uk under thesection about pension credit. It canbe a bit tedious taking you through10 pages of questions, but they arestraightforward and the system calculates for you whether it ispossible for you to claim.

People with capital or savings oftenthink they won’t qualify for assistance. However, the allowancefor savings or capital in pensioncredit is far more generous thanpreviously. People who have been

told in the past that they have toomuch income or savings for assistance could well find, with thechanges to older people’s benefitentitlement, they now qualify.

Pension credit assumes an incomeof £1 for every £500 of capital/savings - above £6,000. The first£6,000 of savings does not count.(This is £10,000 if someone is permanently in a care home.)Hence someone with £70,000 ofcapital is assumed to have £128 inincome, but they could still qualifyfor pension credit guarantee creditif they received DLA/AA (as in theparagraph above) and had no othersource of income. They would alsostill qualify for £15.47 savings credit if they were 65 years orolder.

12 Superlink Summer 2008

People over 60 years of age are entitled to claim pension credit iftheir income does not total£119.05 for a single person and£181.70 for a married couple.(These amounts are increased eachApril 08, in line with inflation.)People who have caring responsibilities are entitled to anadditional amount of £27.15 perweek and people who receive disability living allowance (DLA) orattendance allowance (AA) – wholive alone – with no one claimingcarers allowance to care for them,can claim an additional £48.50 ontop of these basis figures. Wherecouples both claim DLA or AA, thisamount is increased to an extra£97.00.

You can claim from four monthsbefore your 60th birthday. If youare a couple, only one of you needsto be 60 years to claim.

Many older people miss out on thisextra income, as they do notunderstand or have had a poor

experience of, the benefits system.This article seeks to explain morefully the assistance available andguides people to seek advice topursue their full entitlement.

Pension credit is made up from twoelements: a) Guarantee credit – which brings

entitlement to full rent and council tax rebate as well as access to other additional benefits such as cold weather payments or access to the socialfund for community care grants.

b) Savings credit – only payable to people over 65 years old (who have made some provision themselves for their retirement).

Pension creditYvonne Davis

1

2

3

4

5

6

7

8

9

Part of the Department for Work and Pensions

Superlink – our pensioners’ newsletter

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 43

44

Your company AVC pension will havebuilt up a ’pot’ of money for your retirement. There are currently anumber of options available to convert your AVC pension schemeinto an income when you retire.

With this in mind, Hargreaves Lansdown offer a special retirement service to help you.

They will explain the retirementservice and answer any initial questions you may have.

About the serviceAt retirement, the accumulated fundin your account is used to buy youan annuity from an insurance company, bank or building society(but you can defer purchasing an annuity until the day before your75th birthday at the latest). If youcarry on contributing to the LGPSbeyond age 65, you will not be ableto purchase an annuity untilwhichever of these occurs first:

• You retire, or

• You reach the eve of your 75thbirthday, or

• You have your employer’s consentfor flexible retirement – see pages21 to 22

What is an annuity?An annuity is a fixed amount ofadditional pension benefit, althoughyou may be able to choose to include guaranteed annual increasesand dependants' benefits.

Annuities are subject to annuityrates which, in turn, are affectedby interest rates. When interestrates rise, the organisation selling annuities is able to obtain agreater income from each poundin your AVC fund and, therefore,can provide a higher pension.Conversely, a fall in interest ratesreduces the pension which can bepurchased.

ProvidersAnnuities are provided by insurancecompanies such as Prudential, Standard Life, Norwich Union andLegal & General. Different insurancecompanies offer different annuityrates and these change frequently.

Retirement Annuity Service

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 44

45

This means that at any particulartime, some companies will be morecompetitive than others. HargreavesLansdown’s comprehensive annuityservice takes care of sorting out acompetitive retirement income for you – so you can sit back andenjoy your retirement.

You can use this service for:

• Group personal pensions

• Stakeholder pensions

• AVCs

• FSAVCs

• Company money purchaseschemes

• Personal pensions

What are my options?There are currently a number of options available when setting upyour annuity using Hargreaves Lansdown’s service. This gives yougreater flexibility over your futureincome.

For instance, you may be able to:

• Choose an income which continues to be paid at a reducedrate to your spouse or partner ifyou die before them.

• Choose an income which moveseach year in line with inflation.

• Choose an income which pays outfor your lifetime only.

• Choose an income which remainsat a constant amount each year.

• Choose an income which is guaranteed to be paid for a minimum of five or ten years, evenif you die before then.

• Alternatively, upon leaving theLGPS with an immediate paymentof pension benefits you will beable to use the accumulated fundin your AVC account to buy a top-up pension from the LGPS oruse part to buy a top-up pensionfrom the LGPS and part to purchase an annuity. The top-uppension from the LGPS will provide an inflation-proofed pension and dependants’ benefits.

These are just some of the optionscurrently available. This service willprovide you with a number of comparisons, so you can decidewhat option to choose. (Annuitiesfrom occupational schemes may besubject to scheme rules.)

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 45

Tax-free cashOn retirement, you will normally be given the option of taking a tax-free cash lump-sum which youcan spend or save as you wish.Under the LGPS, the tax-free lump-sum is automatically included in the ‘package’ of benefits awarded. The tax-free cashis, as the name suggests, totally tax-free.

You may also elect to take up to100% of the accumulated fund inyour in-house AVC as a tax-free lump-sum if you draw it at the sametime as your LGPS pension benefits,provided when added to the LGPSlump-sum it does not exceed 25%of the overall value of your LGPSbenefits (including your AVC fund)or, if less, 25% of the lifetime allowance, less an adjustment forthe value of any other pension benefits you are already drawing. If you defer drawing your AVC, you can draw up to 25% of thevalue of your AVC fund as a tax freelump-sum at the time you decide totake benefits from your AVC fund.Taking tax-free cash will reduce theincome you receive from your annuity. Not taking tax-free cashwill increase the income you receivefrom your annuity.

For more information, please callHargreaves Lansdown on 0845 3453501.

In certain circumstances, such as retirement on ill-health grounds orcessation of payment of AVCs beforeretirement, the LGPS makes provision for AVCs to be convertedinto LGPS membership provided youcommenced payment of the AVCsprior to 13 November 2001.

Further information is available fromthe administering authority.

Special annuitiesDo you smoke?If you smoke cigarettes regularly andhave done for the last ten years,please let Hargreaves Lansdownknow, as they are likely to be able toget a higher income for you.

Do you qualify for special rates?Some annuity providers will pay youa higher income if you have certainmedical conditions or carry out particular occupations.

Make sure you take this opportunityto obtain the maximum incomepossible by declaring any lifestyle ormedical conditions when setting upyour annuity.

If you can answer yes to any of thequestions shown below, they maywell be able to obtain a better income for you.

46

PAS 182 Retirement Benefits:Layout 1 20/10/08 16:03 Page 46

Please note, they will treat the information you send them in thestrictest confidence.

• Do you take regular medication?

• Do you suffer from chronic asthma?

• Do you have complications arising from high blood pressure?