alhuda cibe 6th gimf-islamic microfinance in maldives

TRANSCRIPT

Religiosity and threshold effect in social and financial performance of microfinance institutions

Mohammad Ashraful Mobin

Copyright © 2015 INCEIF e Learning. All rights reserved.

Islamic Microfinance Scheme in Maldives:“Faseyha Madadhu”

Dr Aishath MuneezaAssociate Professor

INCEIF, The Global University of Islamic Finance

AlHuda CIBE FZ LLE - U.A.EP: + 971 56 9286664, + 971 55 938 99 00

AlHuda Center of Islamic Banking & Economics - PakistanPh: (92-42) 35913096 - 98, Fax: (92-42) 35913056

Email: [email protected] Website: www.alhudacibe.com

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 4

Contents Introduction Microfinance in the country Governance System of Islamic Microfinance Scheme in

Maldives “Faseyha Madadhu”Scheme Targeted Sectors, Shariah Contracts & Financial

Requirements Operational Challenges Facing the Scheme Challenges

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 5

Introduction

• Islamic microfinance is a new concept in Maldives. • Maldives is a hundred percent Muslim country with a population of less than four hundred

thousand people. • Maldives can be best described as a geographically scattered island chain with a small population. • Maldives is a small island nation that is located in south-west of Sri Lanka and India in the Indian

Ocean. • The existence of Maldives was not found in the world map until recently as it was too tiny to be

shown visibility in the map. • The population of the country is just 344,023 (National Bureau of Statistics, 2015) and all

Maldivians are Muslims. • Due to limited natural resources available in the 1,190 islands of Maldives, heavy reliance is on

imported goods while the major income to the country in foreign currency is generated from tourism.

• The population that has no means to access commercial banking to upgrade living standards sought an alternative financing scheme that will not be stringent.

• The first ever Islamic microfinance scheme introduced to the country is “FaseyhaMadadhu”scheme that was introduced in 2015 and for the countries that aspire to introduce Islamic microfinance schemes, it is a a good case study to understand.

• The challenges in introducing and implementing such a scheme will definitely assist in learning from the experience of a small island nation.

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 6

Microfinance in the Country

• Microfinance is a nascent concept in the country. • Though there are seven commercial banks operating in the country, there is no financial institution that

is specialised in Islamic microfinance. • However funds received as foreign aid have been disbursed through the Bank of Maldives, the national

bank as it is required by law to disburse such funds through a bank. • The beginning point that led to the formal existence of microfinance in the country is the enactment of

Small and Medium Enterprises (SME) Act (Law No. 6/2013) in 2013. • The objective of this law was to help reduce poverty and related vulnerabilities as well as making the

sector broad based, innovative, resilient and internationally competitive. • The enactment of this legislation proved the importance given to small and medium enterprises by the

government at policy level. The responsible government agency in dealing with SME sector development is Ministry of Economic development (MED).

• Under the significant SME Act, an SME Council was formed and it became a statutory responsibility for the government to allocate Maldivian Rufiyaa Fifty Million each year for disbursements of financing facilities to the sector.

• This is indeed a landmark development in the country towards the development of SME sector with full support and backing from the government.

• In 2015, the first Islamic microfinance scheme was introduced under the name of “FaseyhaMadadhu” with the assistance from Islamic Development Bank.

• The local bank involved in the scheme is Bank of Maldives. • The products developed under this scheme was unique as it was shaped to cater for the local needs.

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 7

Governance System of Islamic Microfinance Scheme in Maldives

• MSME is defined under the SME Act, as an individual or other legal entity carrying on a business enterprise in one of the following categories:

(i) Micro: businesses with up to 5 employees and an annual income of 500,000 Maldivian Rufiyaa (MVR);

(ii) Small: business employing between 6 and 30 persons and an annual income between 500,001 and 5,000,000 MVR; and

(iii) Medium: business that employs between 31 and 100 persons and an annual income between 5,000,001 and 20,000,000 MVR.• SME Council formed under the SME Act plays a vital role in determining the sectors to which

the Islamic microfinance scheme will be directed to. Not only the sectors, but the target audience is also determined by the SME Council. Therefore the influence of SME Council on “FaseyhaMadadhu” scheme is critical.

• Chapter three of SME Act deals with the formation and other matters related to the SME Council. SME Council is formed by the President of the country.

• The main function of the SME Council is to advice the Minister of Economic Development on ways in which the policies of government regarding the development of SME sector could be implemented including formulation of activities related to this. The president of the SME Council is Minister of Economic Development and the vice president as per the statutory requirement must be selected from the members representing civil societies in the Council. There are fourteen members in the SME Council and some of them are ministers holding economy and finance related portfolios.

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 8

Cont…

• The funds used in the project from Islamic Development Bank was approved pursuant to a request made by the government of Maldives to participate in the ‘Micro, Small and Medium-size Enterprise Development project in 2011.

• The affiliation between Islamic Development Group and Maldives began in 1980, after Maldives became a member of Islamic Development Bank Group.

• The funds received from Islamic Development Bank to provide Islamic financing facilities to SME is given to the Bank of Maldives to disburse it in accordance to the conditions agreed by SME Council and the Ministry of Economic Development.

• For this purpose an agreement between Ministry of Finance and Treasury, acting for the government of Maldives was signed with Bank of Maldives. As such, the applicants will apply to the Islamic microfinance facilities via Bank of Maldives.

• It is imperative to note here the Bank of Maldives is the only bank operating in the country that has the largest coverage, with branches in 27 islands.

• Though “FaseyhaMadadhu”Islamic micro finance scheme is managed jointly by Ministry of Economic Development and Bank of Maldives, the administrative matters such as application form acceptance and evaluation of the applicants is carried out by Bank of Maldives.

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 9

“Faseyha Madadhu”Scheme

• “FaseyhaMadadhu” scheme is the first shariah compliant microfinance scheme introduced by the government of Maldives.

• The scheme was introduced in 2015. • “Faseyha” is the Dhivehi (language used in Maldives) word for easy and

“Madadhu” is also a Dhivehi word which means assistance or help. • Hence, “faseyhamadadhu” means easy assistance. Forty percent of the total

financing facility is allocated for women and youth entrepreneurs.• Under “FaseyhaMadadhu” scheme, micro (businesses with up to 5 employees

and an annual income of 500,000 Maldivian Rufiyaa (MVR)) businesses can apply up to Maldivian Rufiyaa hundred thousand; small (business employing between 6 and 30 persons and an annual income between 500,001 and 5,000,000 MVR) businesses can apply up to Maldivian Rufiyaa five hundred thousand; and medium (business that employs between 31 and 100 persons and an annual income between 5,000,001 and 20,000,000 MVR) businesses can apply up to Maldivian Rufiyaa one million. For newly set up businesses the maximum amount of financing that could be given is Maldivian Rufiyaa three hundred thousand.

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 10

Targeted Sectors, Shariah Contracts & Financial Requirements• The targeted sectors in this scheme was tourism, transportation, construction, fisheries and

agriculture. • For tourism sector, shariah compliant financing assistance is only given to purchase or buy

materials to develop guest houses and to purchase equipment to produce handicraft items. • As for the transportation sector, the shariah compliant financing facility is provided only to replace

old taxis with new cars and to purchase vehicles other than cars used for land and sea transportation purposes.

• For construction sector, shariah compliant financing will only be given for the purpose of purchasing machineries or materials used for construction.

• Finally in fisheries and agricultural sector, Islamic finance facility can be given to buy machineries that will be used to process fisheries or agricultural produces or to purchase machineries that will help to value add the fisheries and agricultural produces. In agricultural sector Islamic finance facility can also be obtained if the applicant wishes to produce crops using new innovative technology.

• Except for the agriculture category where applicant wishes to produce crops using new innovative technology, for the rest of categories, murabahah is the underlying contract used.

• There is no additional collateral requirement except for the equipment or assets purchased under the scheme which will be mortgaged as a security. The tenure of the financing facility will be determined based on the financial documents submitted by the applicant and the tenure will not exceed six years. The financing rate is 9% per annum, which is relatively high for a microfinance product.

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 11

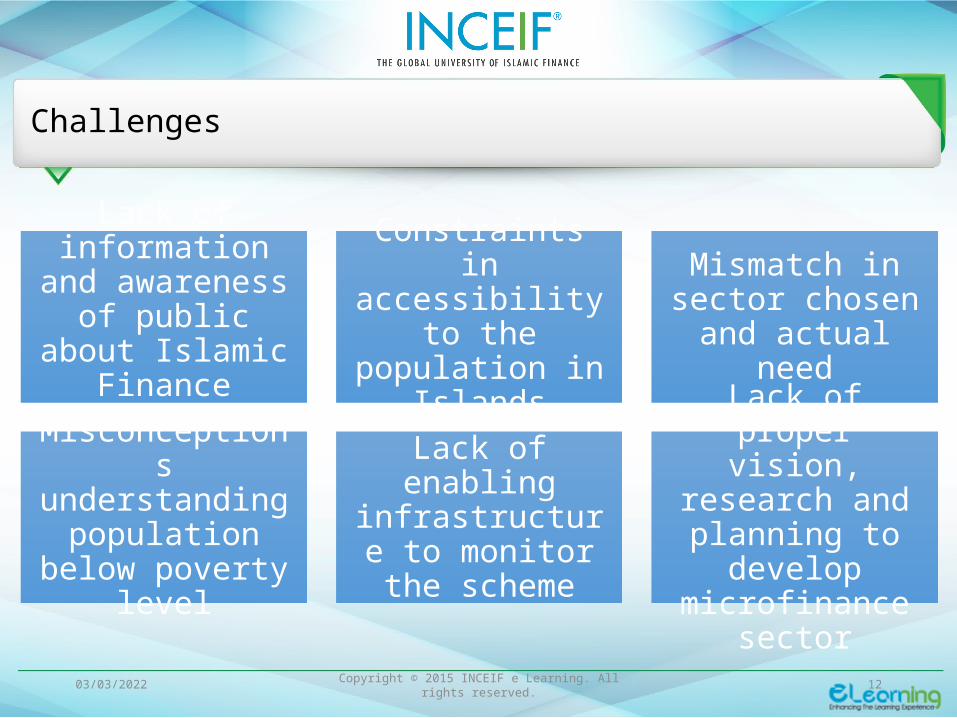

Operational Challenges Facing the Scheme

• Even though “faseyhamadadhu” scheme was successfully launched, the success of these products is yet to be tested as the successful applicant is yet to be chosen by Bank of Maldives.

• As of the closing date, 29th October 2015, Bank of Maldives received 119 applications and the majority of these application was to obtain financing facility for transportation sector.

• However, even at this stage, the challenges facing the scheme can be identified and these challenges need to be properly addressed especially for the successful continuance of the scheme.

05/03/2023 Copyright © 2015 INCEIF e Learning. All rights reserved. 12

Challenges

Lack of information and awareness of

public about Islamic Finance Products

Constraints in accessibility to the

population in Islands

Mismatch in sector chosen and actual

need

Misconceptions understanding

population below poverty level

Lack of enabling infrastructure to

monitor the scheme

Lack of proper vision, research and planning to develop microfinance sector

Copyright © 2015 INCEIF e Learning. All rights reserved.

Thank You

Dr Aishath MuneezaAssociate Professor, INCEIF

AlHuda CIBE FZ LLE - U.A.EP: + 971 56 9286664, + 971 55 938 99 00

AlHuda Center of Islamic Banking & Economics - PakistanPh: (92-42) 35913096 - 98, Fax: (92-42) 35913056

Email: [email protected] Website: www.alhudacibe.com