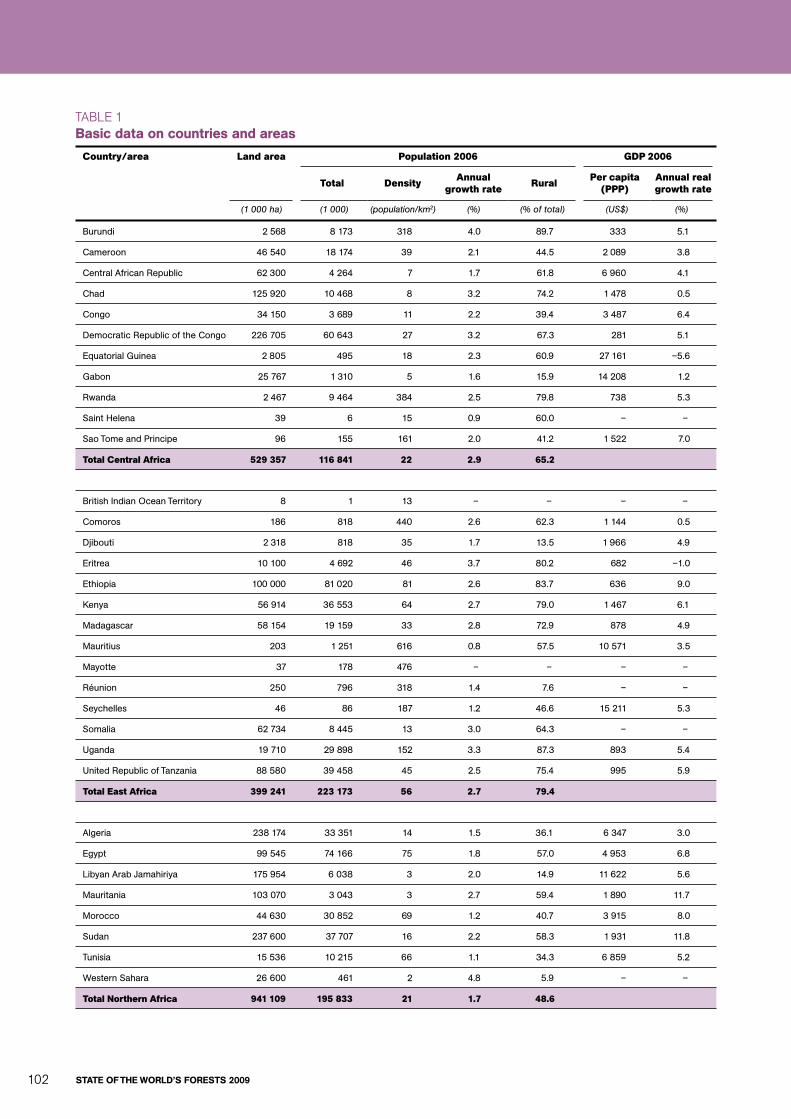

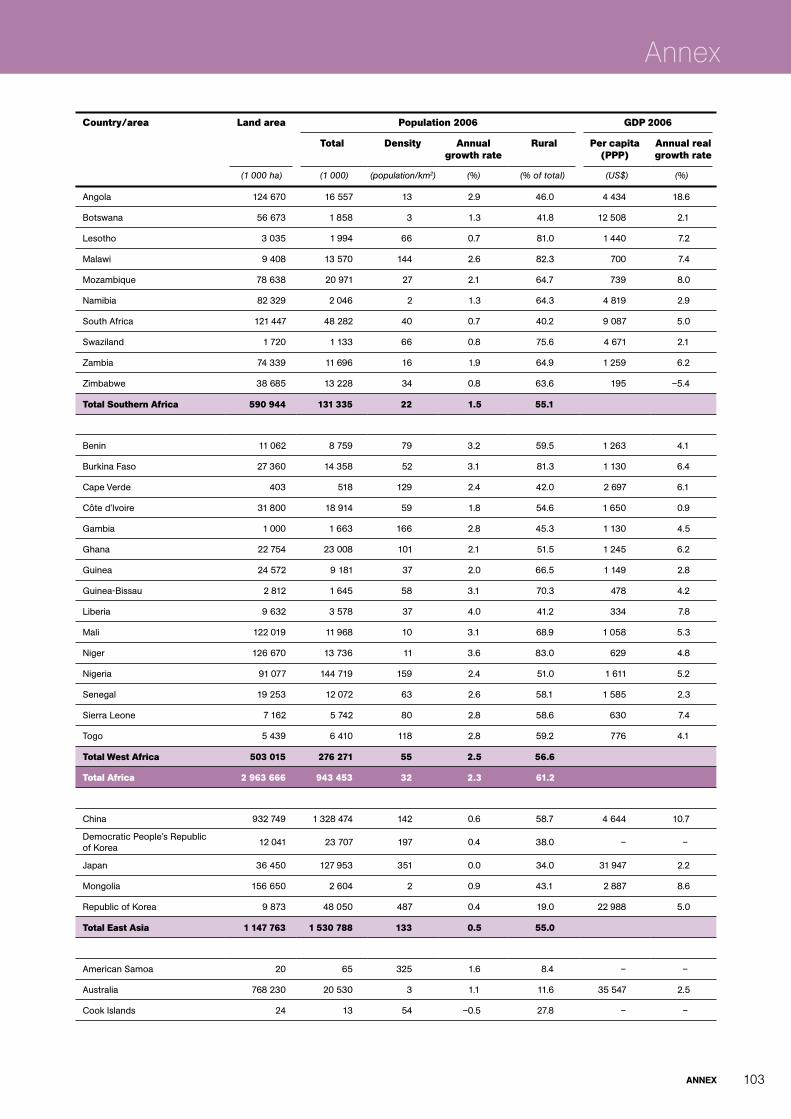

algeria egypt libyan arab jamahiriya mauritania morocco sudan

TRANSCRIPT

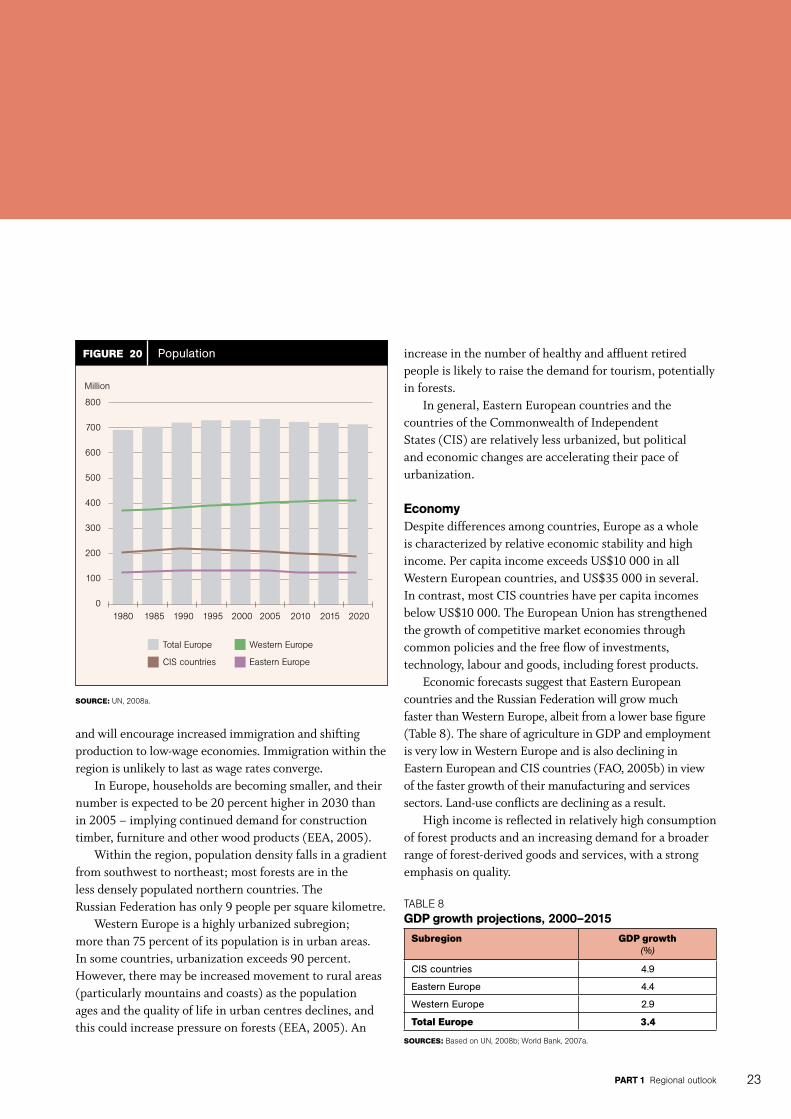

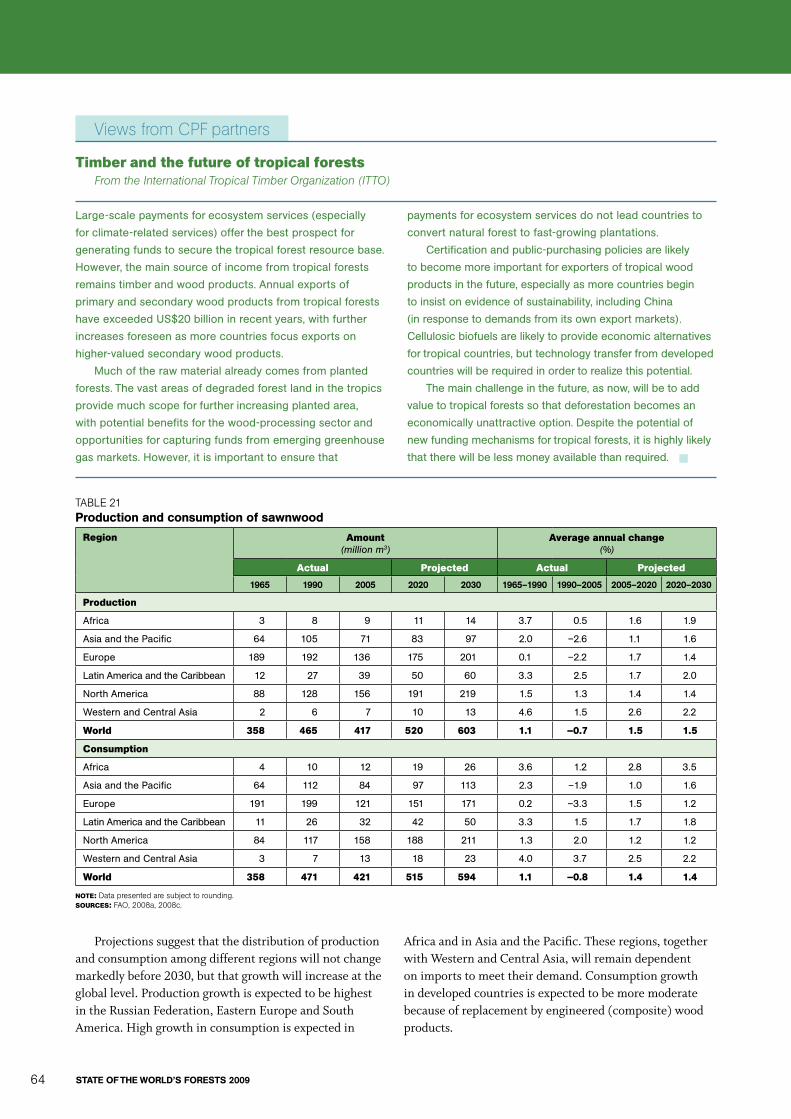

What will be the impact on forests of future economic development, globalized trade and

increases in the world’s population? The 2009 edition of the biennial State of the World’s Forests

looks forward, with the theme “Society, forests and forestry: adapting for the future”.

Part 1 summarizes the outlook for forests and forestry in each region, based on FAO’s periodic

regional forest sector outlook studies. Past trends and projected demographic, economic,

institutional and technological changes are examined to outline the scenario to 2030.

Part 2 considers how forestry will have to adapt for the future, focusing on: the global outlook for

wood products demand; mechanisms for meeting the demand for environmental services

of forests; changes in forest sector institutions; and developments in science and technology.

This volume will serve as a source of information to support forest-related policy and research.

It is hoped that it will also stimulate creative thinking and debate to enhance the future of the

world’s forests. 2009

STATe OF The

World’s Forests

STATe O

F The

Wo

rld

’s Fo

re

sts

2009

Iss

N 1020-5705

FAoTC/M/I0350E/1/01.09/7000

ISBN 978-92-5-106057-5 ISSN 1020-5705

9 7 8 9 2 5 1 0 6 0 5 7 5

Cover photos:

Front, left: FAO/FO-6120/M.C. Yang

Front, centre: R. Faidutti

Front, right: FAO/FO-6664/M. Kashio

Copies of FAo publications can be requested from:

SALES & MARKETING GROUP

Communication Division

Food and Agriculture Organization of the United Nations

Viale delle Terme di Caracalla - 00153 Rome, Italy

E-mail: [email protected]

Fax: (+39) 06 57053360

Web site: www.fao.org

Back, left: FAO/FO-5043/B. héois

Back, centre: UK Forestry Commission/1057657/J. McFarlane

Back, right: FAO/FO-6003/B. Vivattana

2009State of the

World’s Forests

food and agriculture organization of the united nationS

rome, 2009

Produced by the

electronic Publishing Policy and support Branch

Communication division

FAo

the designations employed and the presentation of material in this information product do not imply the expression of any opinion whatsoever on the part of the food and agriculture organization of the united nations (fao) concerning the legal or development status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. the mention of specific companies or products of manufacturers, whether or not these have been patented, does not imply that these have been endorsed or recommended by fao in preference to others of a similar nature that are not mentioned.

the designations employed and the presentation of material in the maps do not imply the expression of any opinion whatsoever on the part of fao concerning the legal or constitutional status of any country, territory or sea area, or concerning the delimitation of frontiers.

iSBn 978-92-5-106057-5

all rights reserved. reproduction and dissemination of material in this information product for educational or other non-commercial purposes are authorized without any prior written permission from the copyright holders provided the source is fully acknowledged. reproduction of material in this information product for resale or other commercial purposes is prohibited without written permission of the copyright holders. applications for such permission should be addressed to the chief, electronic Publishing Policy and Support Branch, communication division, fao, Viale delle terme di caracalla, 00153 rome, italy or by e-mail to [email protected]

© FAO 2009

Contents

foreword vacknowledgements viabbreviations and acronyms viiSummary viii

Part 1regional outlook 1

Africa 2AsiaandthePacific 12Europe 22LatinAmericaandtheCaribbean 32NorthAmerica 42WesternandCentralAsia 52

Part 2adapting for the future 61

Globaldemandforwoodproducts 62Meetingthedemandforenvironmentalservicesofforests 72Changinginstitutions 80Developmentsinforestscienceandtechnology 88

Postscript challenges and opportunities in turbulent times 98

Annex

table 1Basicdataoncountriesandareas 102

table 2Forestareaandareachange 109

table 3Forestgrowingstock,biomassandcarbon 116

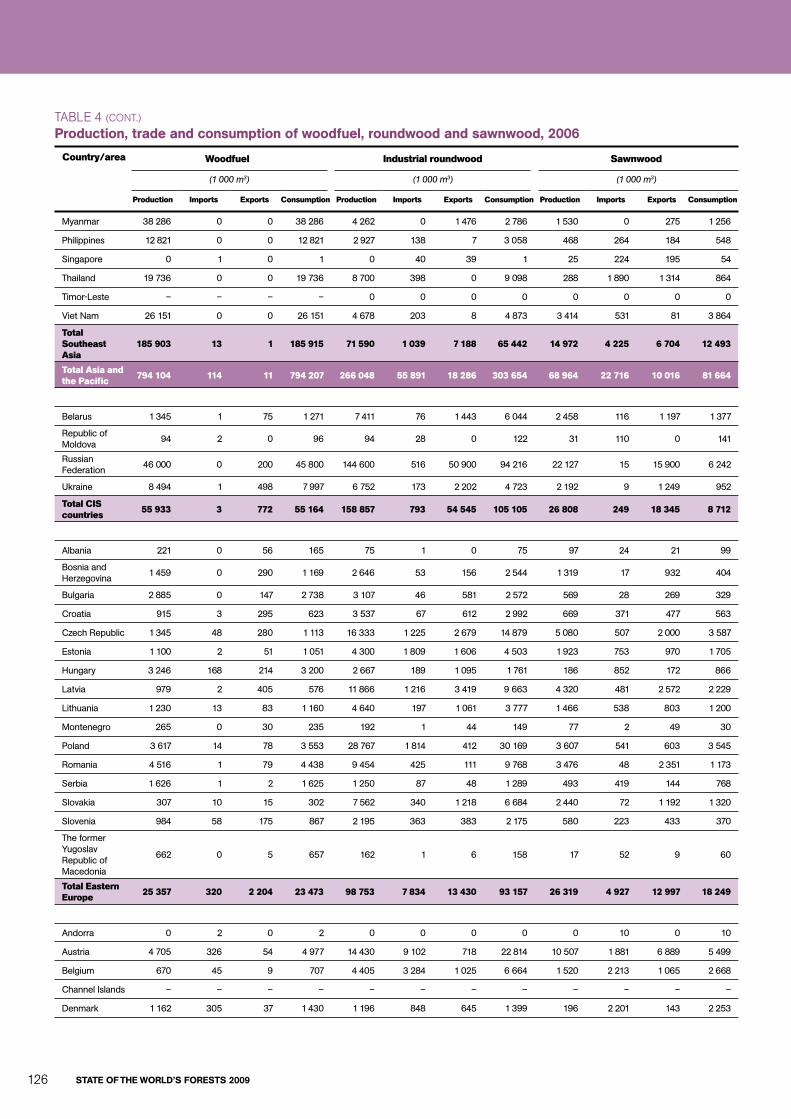

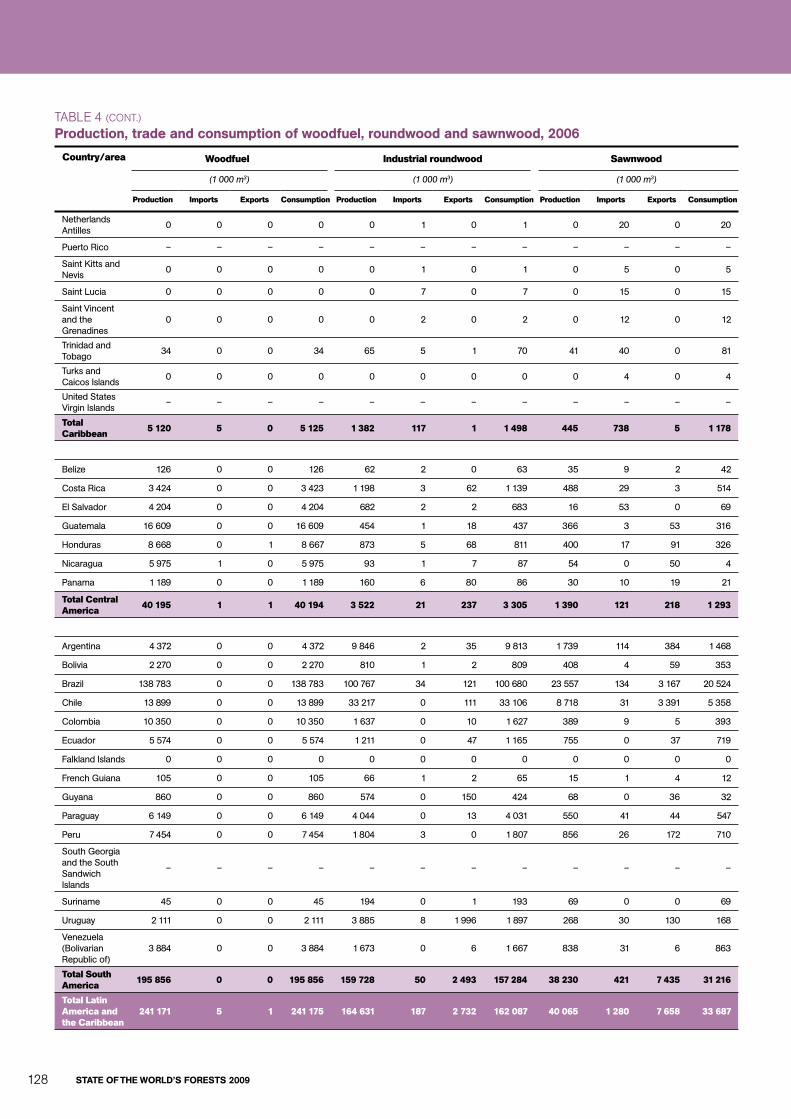

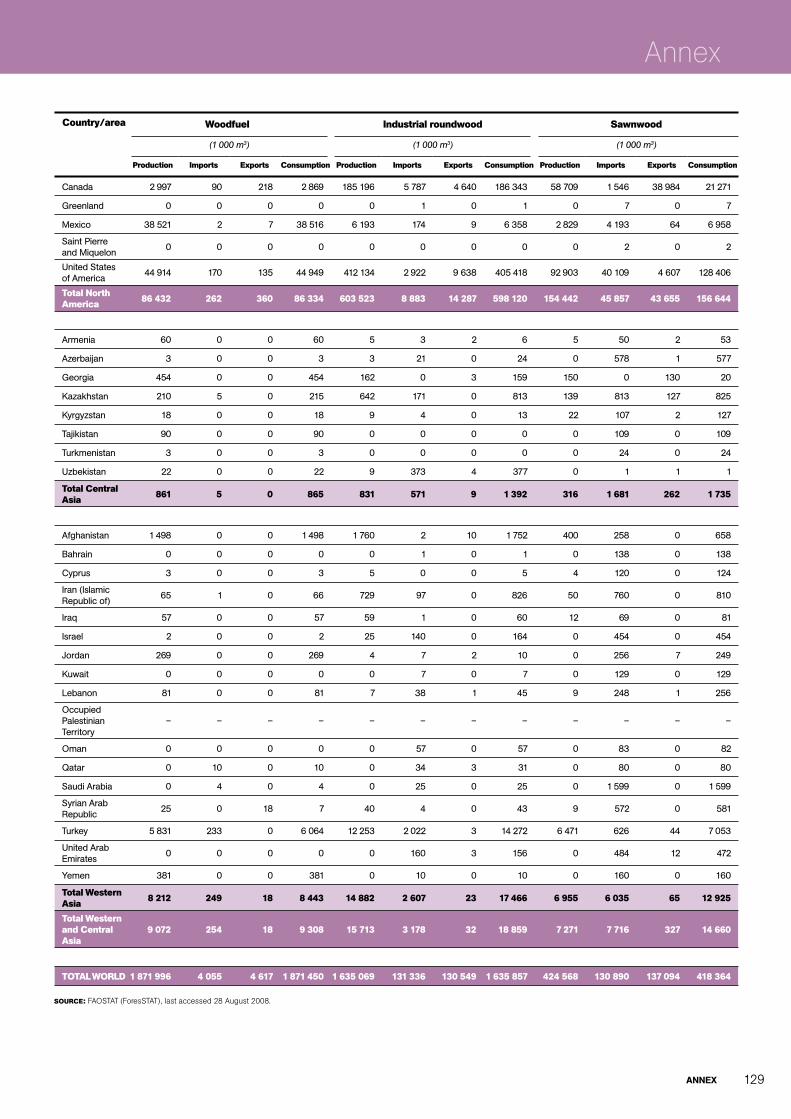

table 4Production,tradeandconsumptionofwoodfuel,roundwoodandsawnwood,2006 123

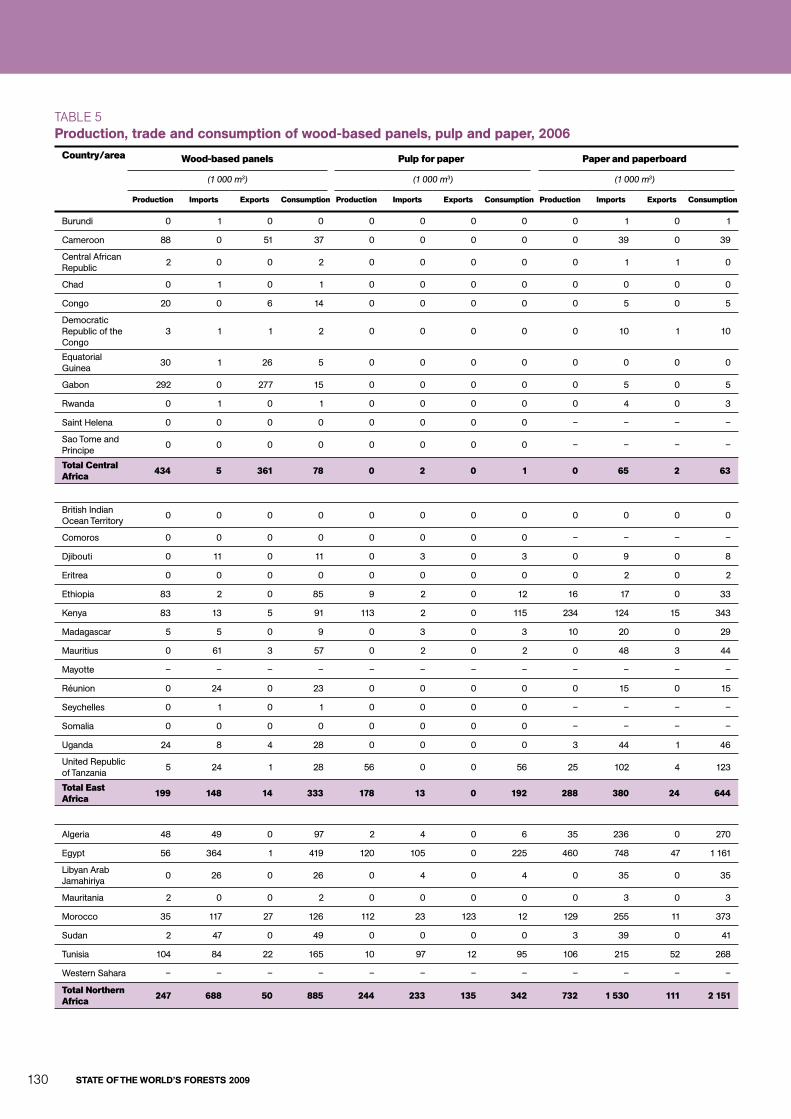

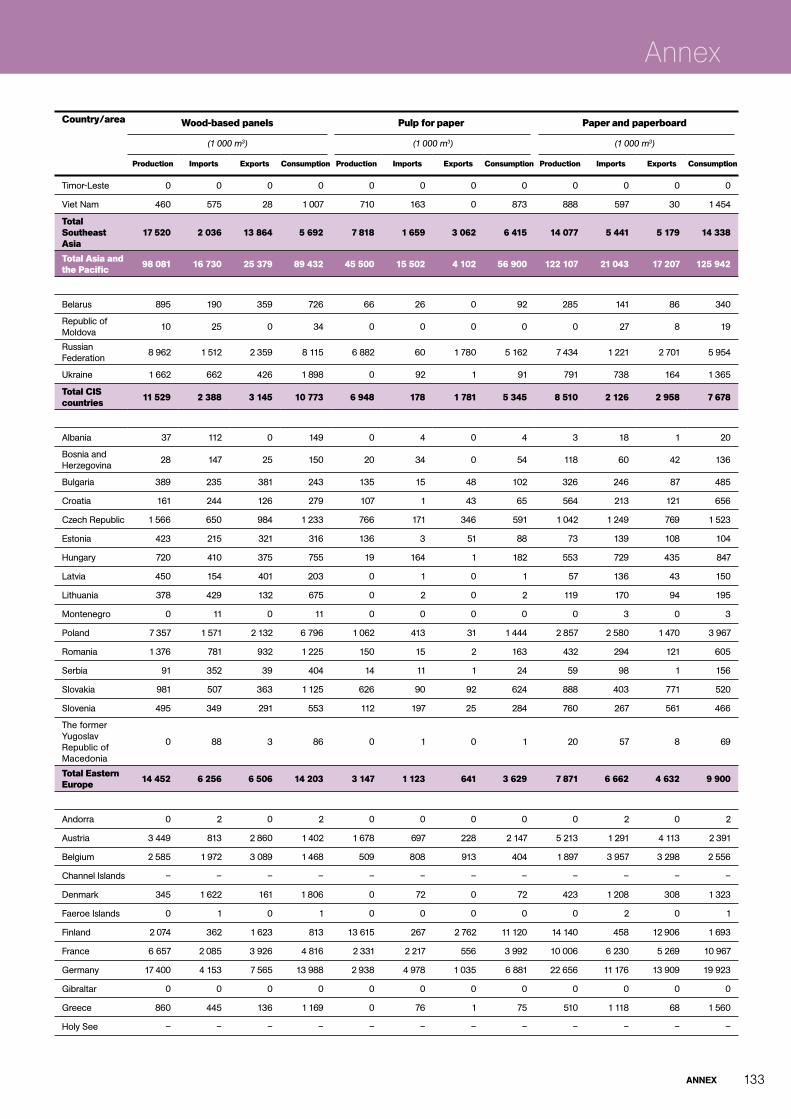

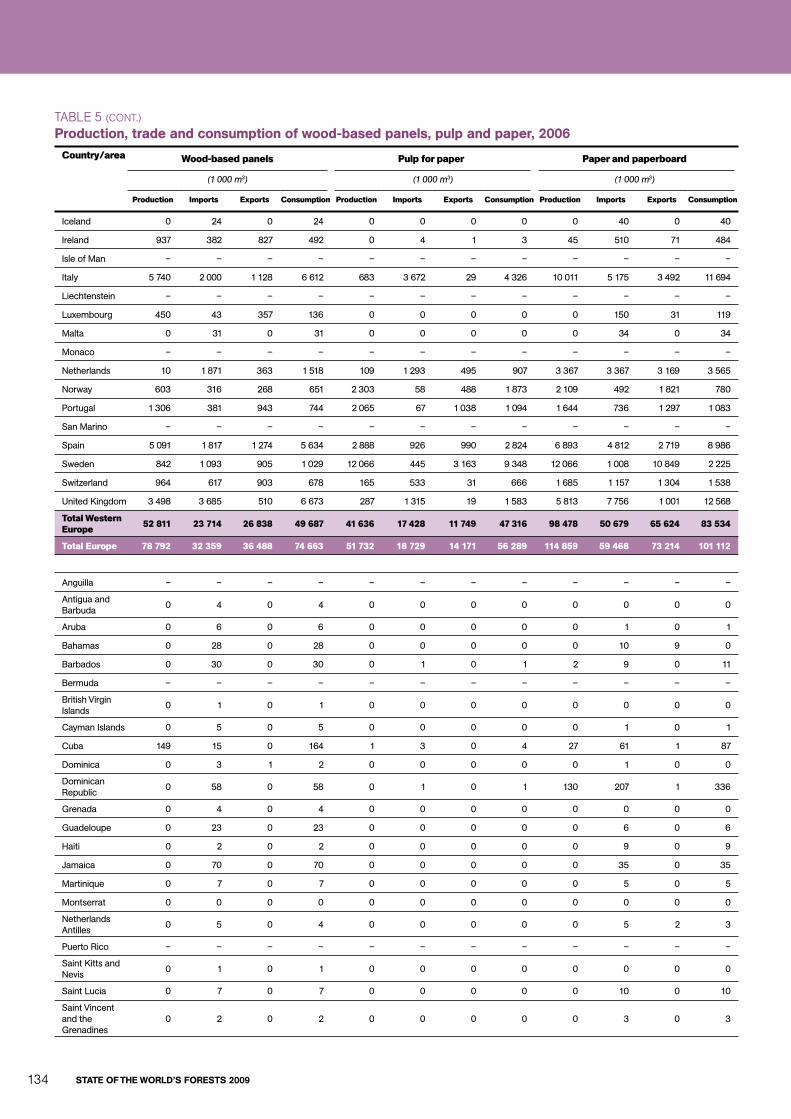

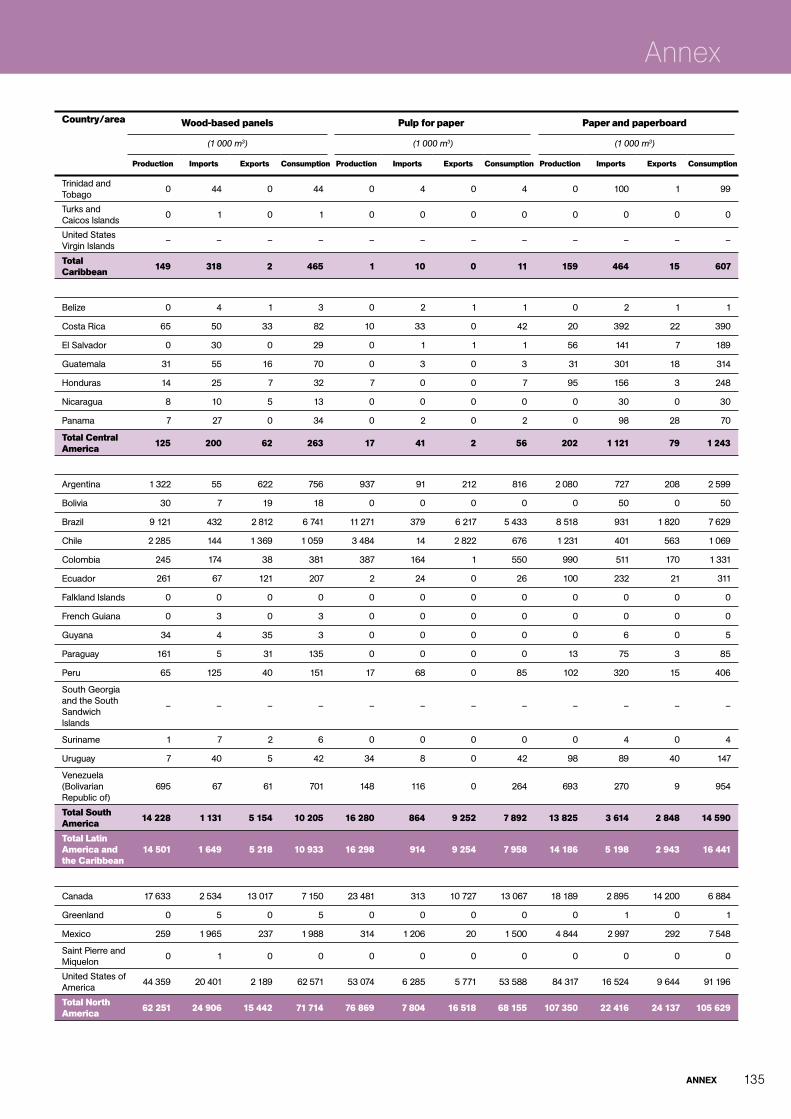

table 5Production,tradeandconsumptionofwood-basedpanels,pulpandpaper,2006 130

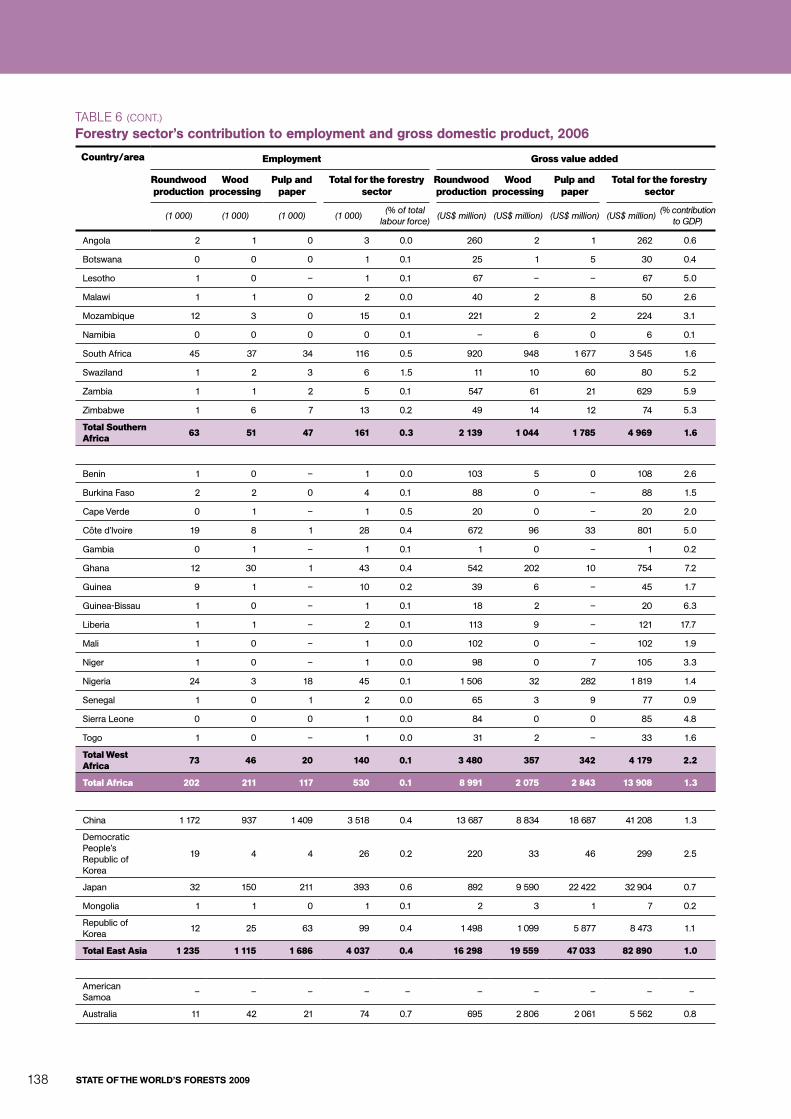

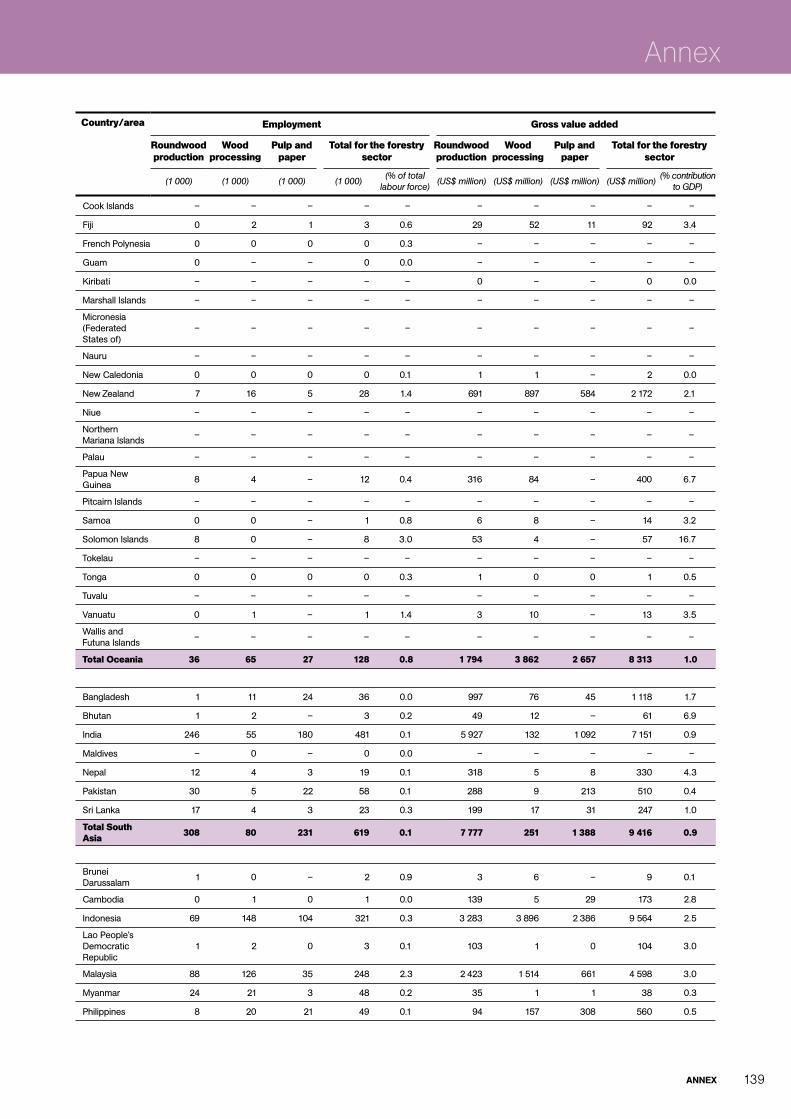

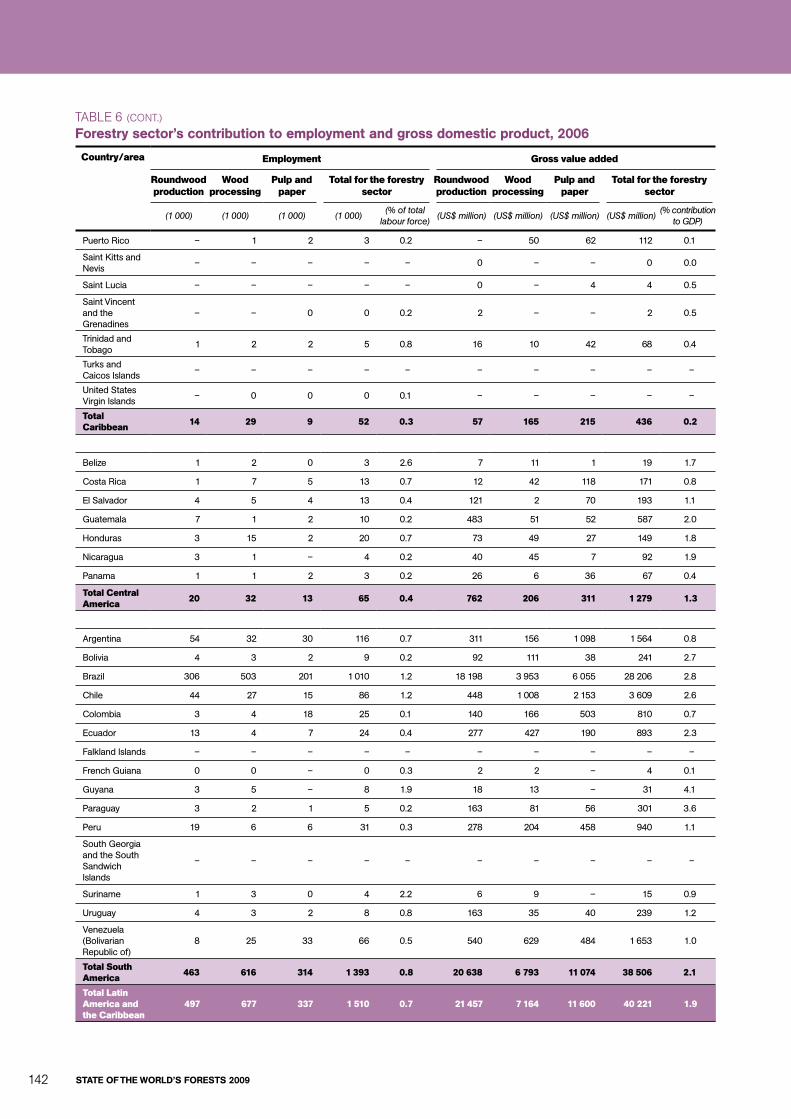

table 6Forestrysector’scontributiontoemploymentandgrossdomesticproduct,2006 137

references 145

iv

Contents

v

Contents

state of the World’s Forests,publishedbiennially,providesaglobalviewofmajordevelopmentsaffectingforests.Thethemeforthe2009editionis

“Society,forestsandforestry:adaptingforthefuture”.The2007issuereviewed“Progresstowardssustainable

forestmanagement”withanemphasisonthe“supplyside”,inparticularforestresources.State of the World’s Forests 2009placesmoreemphasisonthe“demandside”:Whatwillbetheimpactonforestsoffutureincreasesinglobalpopulation,economicdevelopmentandglobalization?Istheexplosioninglobaltradehavingpositiveornegativeeffectsontheworld’sforests?Willtheforestsectorcontinuetohaveamajorroleinprovidinglivelihoodsforruralcommunities?

Thiseightheditionlooksforward.Part1summarizestheoutlookforforestsandforestryineachregionoftheworld.FAOperiodicallycarriesoutregionalforestsectoroutlookstudiesincollaborationwithcountriesandorganizationsineachregion.Theresultsofstudiesforallregionsaresummarizedandpresentedhereforthefirsttimeinasinglepublication.Amainpatternthatemergesisastrongcorrelationbetweeneconomicdevelopmentandthestateofforests.Countriesthatareundergoingrapideconomicgrowthtendtostrugglewithimmensepressuresontheirforests.Incontrast,regionsthathavealreadyachievedahighlevelofeconomicdevelopmentareusuallyabletostabilizeorincreasetheirforestarea.However,thefactorsaffectingforestsarenumerousandcomplex,makingitdifficulttodrawsimpleconclusionsortomakereliableprojections.

Part2considershowforestrywillhavetoadaptforthefuture.Itbeginswithaglobaloutlookforwoodproductsdemandto2030,notingchangingpatternsinproduction,consumptionandtrade.Next,achapteronenvironmentalservicesofforestsprobesthevariousmarketandnon-marketmechanismsevolvingtohelpforestsandtreesfulfiltheirenvironmentalservicefunctionsofland,water

andbiodiversityprotection,carbonstorageandothers.Alookatprogressininstitutionaladaptationnotesthatmanyforestryinstitutionsarehavingdifficultyinadaptingtorapidchangesincommunications,globalizationandsociety’sexpectations.Thoseinstitutionsthatarewillingandabletoadaptaremorelikelytobesuccessfulinthefuture.Finally,Part2examinesdevelopmentsinscienceandtechnology,whichwillcontinuetohaveanenormousimpactonthefutureofforestsandforestry.Imagineaworldinwhichtreesareamajorsourceoffuelforcars,replacingoil.Onlyafewyearsago,thisseemedlikefantasy,buttodaythepossibilitymustbeseriouslyconsidered.

Asthiseditionwasgoingtopressinlate2008,theglobaleconomyhadspunintosharpdecline,sparkedbythecontractionofthehousingsectorandthesubprimemortgagecrisisintheUnitedStatesofAmerica.Almostallcountrieshavebeenaffectedbythisdownturn.WhiletheseeventsoccurredtoolatetobeincorporatedinthemaintextofState of the World’s Forests 2009,apostscripthasbeenaddedaddressingtheobservedandlikelyimpactsoftheeconomiccrisisonforestsandforestry.Itnotesthatwhilethereisconsiderableuncertaintyabouthowthesituationwillunfoldinthecomingyears,thecrisiscouldalsoprovideanopportunitytochartanewpathforthedevelopmentoftheforestsector.

State of the World’s Forests 2009hastwomaingoals.Aswithpasteditions,itisintendedtoserveasasourceofinformationtosupportpolicyandresearchrelatedtoforests.Inaddition,Ihopethatithelpstostimulatecreativethinkinganddebateaboutthefutureoftheworld’sforests.

Jan HeinoAssistantDirector-GeneralFAOForestryDepartment

Foreword

stAte oF the World’s Forests 2009vi

t hepreparationofState of the World’s Forests 2009wascoordinatedbyC.T.S.Nair.SpecialthanksgotoA.Perlis,whoeditedthepublication,andto

R.Rutt,whoprovidedresearchsupport.ThefollowingFAOstaffwroteorreviewedsectionsof

thereportorassistedwithtables,maps,graphicsorotherinformation:M.Achouri,G.Allard,B.Amado,S.Appanah,J.L.Blanchez,M.Boscolo,S.Braatz,A.Branthomme,J.Broadhead,C.Brown,J.Carle,C.Carneiro,F.Castañeda,M.Chihambakwe,R.Czudek,P.Durst,C.Eckelmann,T.Etherington,P.Evans,V.Ferreira,B.Foday,M.Gauthier,A.Gerrand,S.Grouwels,J.Heino,S.Hetsch,T.Hofer,P.Holmgren,A.Inoguchi,O.Jonsson,R.Jonsson,F.Kafeero,W.Killmann,D.Kneeland,P.Koné,M.Laverdiere,A.Lebedys,M.Lobovikov,Q.Ma,L.Marklund,R.M.Martin,M.Morell,E.Muller,F.Padovani,M.Paveri,E.Pepke,J.A.Prado,C.Prins,D.Reeb,D.Rugabira,O.Serrano,O.Souvannavong,R.Suzuki,T.Vahanen,P.Vantomme,A.Whiteman,M.L.WilkieandJ.Zapata-Andia.

FAOspecificallythanks,forcontributionsandreviews:L.AldenWily,D.BaskaranKrishnapillay,S.Boucher,M.Boyland,J.Campbell,J.Cinq-Mars,A.Kaudia,R.Keenan,L.Langner,J.Maini,E.Mansur,P.O’Neill,J.Parrotta,R.Persson,F.RagaCastellanos,M.A.Razak,R.Sedjo,J.SeverinoRomo,H.C.SimandE.Sirin.

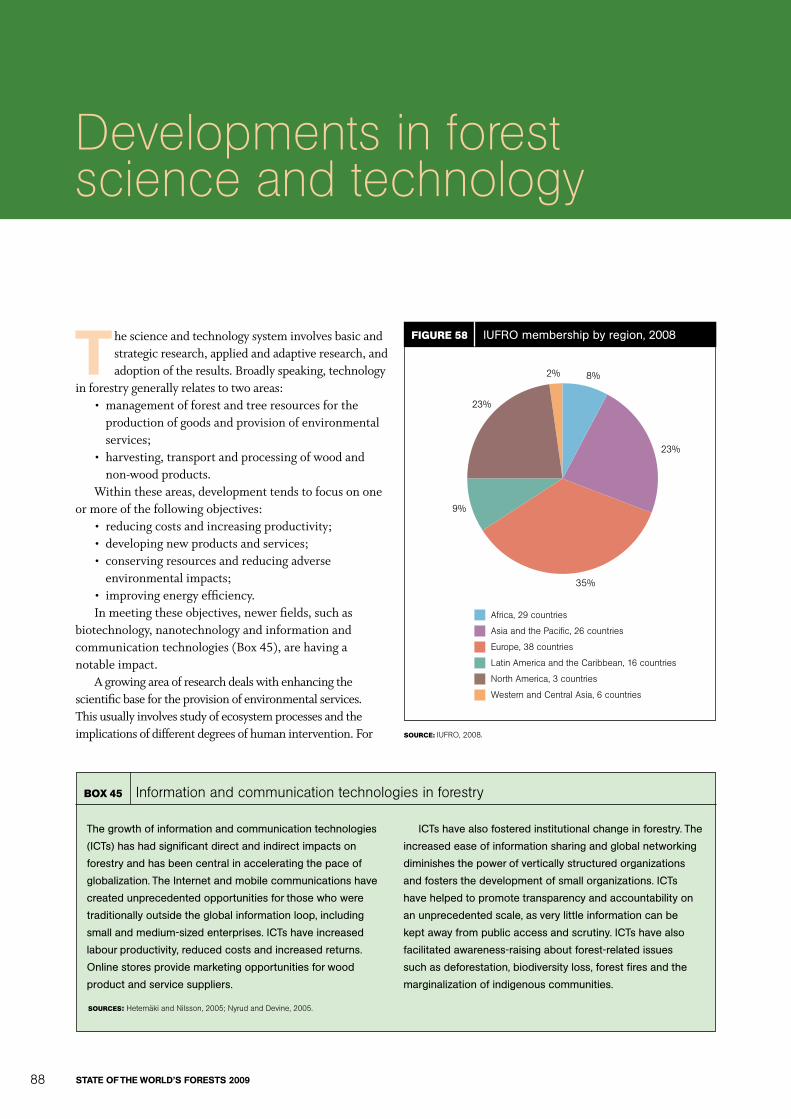

FAOalsoacknowledgesmembersoftheCollaborativePartnershiponForests(CPF)fortheircontributionspresentedinPart2,specificallytheConventiononBiologicalDiversity(CBD),theCenterforInternationalForestryResearch(CIFOR),theInternationalTropicalTimberOrganization(ITTO),theInternationalUnionofForestResearchOrganizations(IUFRO),theGlobalMechanismoftheUnitedNationsConventiontoCombatDesertification(UNCCD),theUnitedNationsEnvironmentProgramme(UNEP),theUnitedNationsForumonForests(UNFF)andtheUnitedNationsFrameworkConventiononClimateChange(UNFCCC).

ThestaffoftheFAOElectronicPublishingPolicyandSupportBranchprovidededitorialandproductionsupport.

Acknowledgements

vii

Abbreviations and acronyms

CAMPFIRE CommunalAreasManagementProgrammeforIndigenousResources

CBD ConventiononBiologicalDiversityCDM CleanDevelopmentMechanismCIFOR CenterforInternationalForestryResearchCIS CommonwealthofIndependentStatesCPF CollaborativePartnershiponForestsECOWAS EconomicCommunityofWestAfricanStatesEFSOS EuropeanForestSectorOutlookStudyFECOFUN FederationofCommunityForestUsersNepalFLEG forestlawenforcementandgovernanceFSC ForestStewardshipCouncilGCC GulfCooperationCouncilGDP grossdomesticproductGIS geographicinformationsystemICT informationandcommunicationtechnologyIEA InternationalEnergyAgencyIIED InternationalInstituteforEnvironmentand

DevelopmentIPCC IntergovernmentalPanelonClimateChangeITTO InternationalTropicalTimberOrganizationIUCN InternationalUnionforConservationof

NatureIUFRO InternationalUnionofForestResearch

OrganizationsLULUCF landuse,land-usechangeandforestryMCPFE MinisterialConferenceontheProtectionof

ForestsinEuropeMTOE milliontonnesoilequivalentNAFTA NorthAmericanFreeTradeAgreementNGO non-governmentalorganization

NLBI Non-LegallyBindingInstrumentonAllTypesofForests

NWFP non-woodforestproductPEEN Pan-EuropeanEcologicalNetworkPEFC ProgrammefortheEndorsementofForest

CertificationSchemesPES paymentsforenvironmentalservicesR&D researchanddevelopmentREDD reducingemissionsfromdeforestationand

forestdegradationREIT realestateinvestmenttrustSADC SouthernAfricanDevelopmentCommunitySWF sovereignwealthfundTIMO timberinvestmentmanagementorganizationUN UnitedNationsUNCCD UnitedNationsConventiontoCombat

DesertificationUNCED UnitedNationsConferenceonEnvironment

andDevelopmentUNECE UnitedNationsEconomicCommissionfor

EuropeUNEP UnitedNationsEnvironmentProgrammeUNESCAP UnitedNationsEconomicandSocial

CommissionforAsiaandthePacificUNESCO UnitedNationsEducational,Scientificand

CulturalOrganizationUNFCCC UnitedNationsFrameworkConventionon

ClimateChangeUNFF UnitedNationsForumonForestsWRI WorldResourcesInstituteWRME woodraw-materialequivalent

viii

Summary

thiseighthbiennialissueofState of the World’s Forestsconsiderstheunfoldingfutureofforestsandforestryatthesubregional,regionalandgloballevels.Based

onthemostrecentofFAO’speriodicforestsectoroutlookstudies,itexaminestheimpactsthatexternalfactorssuchasdemographic,economic,institutionalandtechnologicalchangesmayhaveonforests.Withglobalizationandimprovedcommunications,theregionalscenarioswillbeincreasinglyinterlinked.However,somecountriesandregionsarebetterpreparedtofacetheupcomingchallengesandtakeadvantageofemergingopportunities,whileothersstilllackessentialinstitutional,legalandeconomicconditionstomanagetheirforestresourcesinasustainablemanner.

PArt 1: regionAl outlookAfricaTheforestsituationinAfricapresentsenormouschallenges,reflectingthelargerconstraintsoflowincome,weakpoliciesandinadequatelydevelopedinstitutions.Thegrowingpopulationandrisingpricesoffoodandenergywillexacerbatethesituation,especiallyasincreasedinvestmentsininfrastructureopenupnewareas.Progressinimplementingsustainableforestmanagementisexpectedtobeslow,withforestlosslikelytocontinueatcurrentrates.

Theforestoutlookwilldependgreatlyonpoliticalandinstitutionaldevelopments–onimprovedefficiencyandaccountabilityinthepublicsector;greaterinclusiveness,competitivenessandtransparencyinmarketinstitutions;andaninformalsectorthatprovidesincreasedlivelihoodopportunitiesforthepoor.Focusingonproductsandservicesrequiredlocallyandgloballyandstrengtheninglocalinstitutionscanbeimportantwaysofaddressingforestresourcedepletion.Sucheffortsshouldbuildonlocalknowledgeandexperienceofsustainableresourcemanagementintegratingagriculture,animalhusbandryandforestry.

Asia and the PacificConsideringthegreatdiversityinAsiaandthePacific,severalscenariosareexpectedtounfold.Whileforestareawillstabilizeandincreaseinmostofthedevelopedcountriesand

someoftheemergingeconomies,thelow-andmiddle-incomeforest-richcountrieswillwitnesscontinuingdeclinesasaresultofexpansionofagriculture,includingtheproductionofbiofuelfeedstock.

Demandforwoodandwoodproductswillcontinuetoincreaseinlinewiththegrowthinpopulationandincome.Growthinthedemandforprimarycommoditiesowingtorapidindustrializationofemergingeconomiesislikelytoresultinforestconversioninothercountrieswithinandoutsidetheregion.Whiletheregionisaleaderinplantedforestdevelopment,itwillcontinuetodependonwoodfromotherregions,aslandandwaterconstraintswilllimitthescopeforself-sufficiencyinwoodandwoodproducts.Thedemandforforestenvironmentalserviceswillincreaseasincomesrise,andconservationinvolvinglocalcommunitiesislikelytoreceivegreateremphasis.

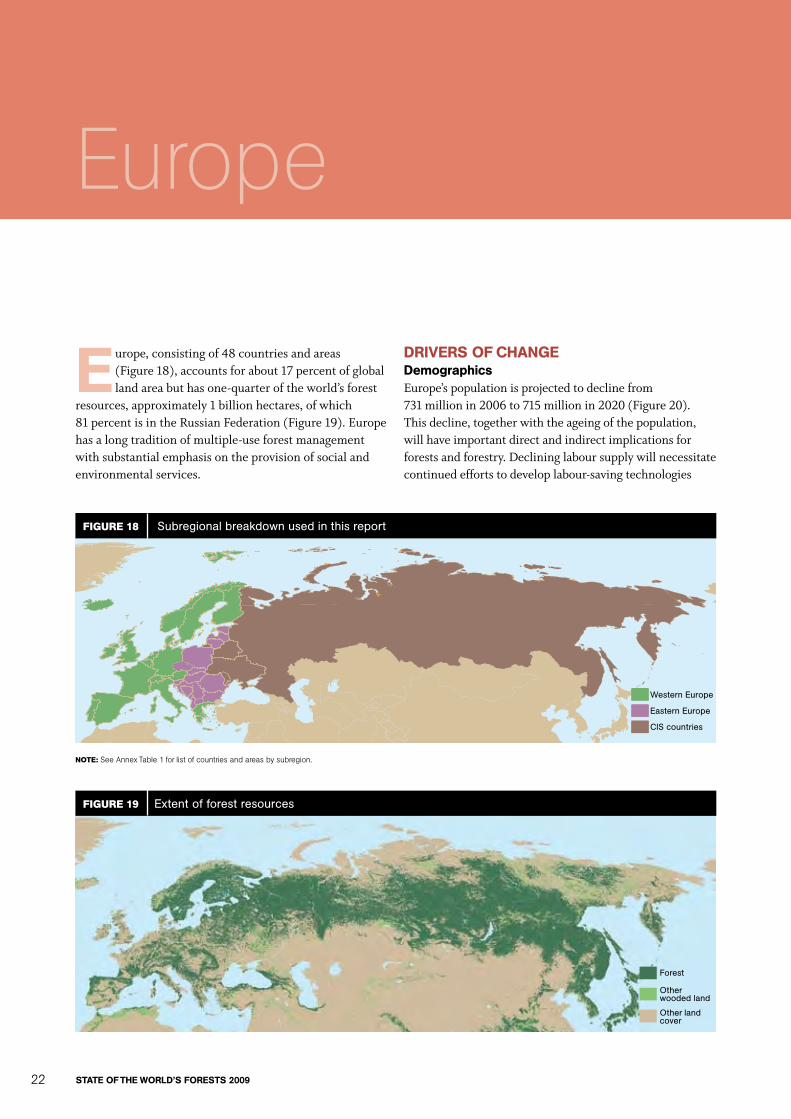

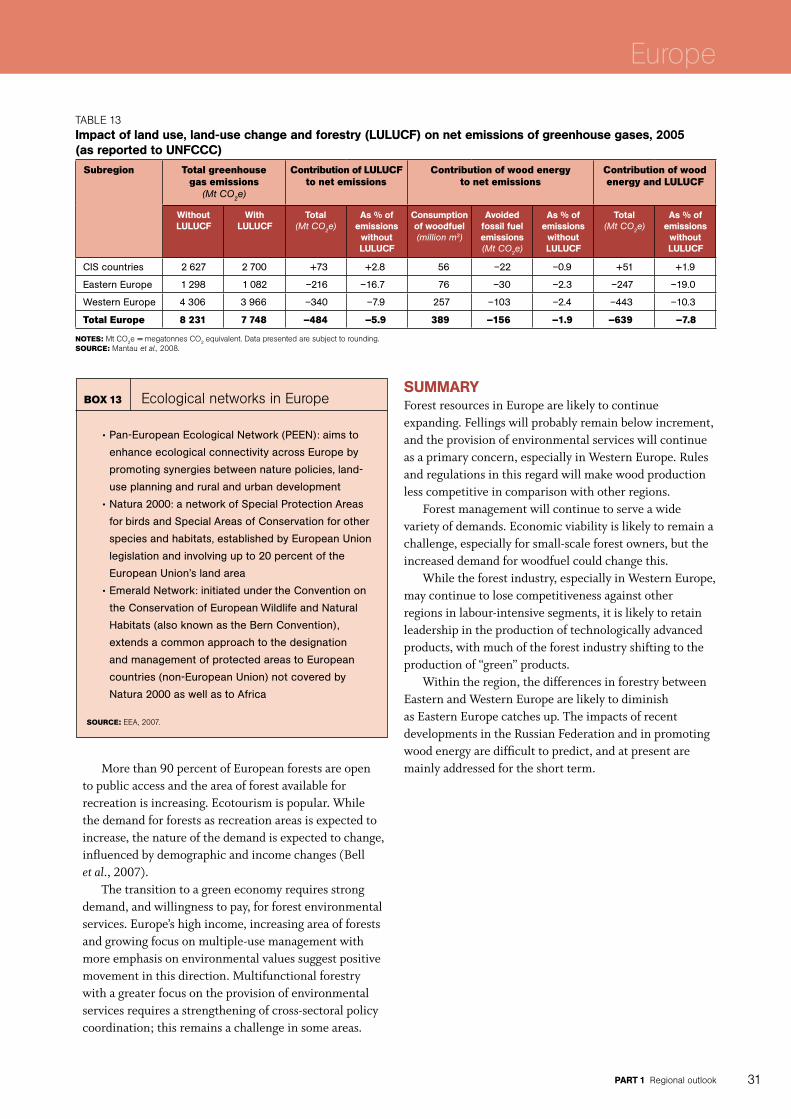

europeForestresourcesinEuropeareexpectedtocontinuetoexpandinviewofdeclininglanddependence,increasingincome,concernforprotectionoftheenvironmentandwell-developedpolicyandinstitutionalframeworks.Theprovisionofenvironmentalserviceswillremainaprimaryconcern,especiallyinWesternEurope,andrulesandregulationswillmakewoodproductionlesscompetitivethaninotherregions.

Forestmanagementwillcontinuetoserveawidevarietyofpurposes.Economicviabilityislikelytoremainachallenge,especiallyforsmall-scaleforestowners,buttheincreaseddemandforwoodfuelcouldchangethis.Whiletheforestindustry,especiallyinWesternEurope,maycontinuetolosecompetitivenesswithotherregionsinlabour-intensivesegments,itislikelytoretainleadershipintheproductionoftechnologicallyadvancedproducts.Withintheregion,thedifferencesinforestrybetweenEasternandWesternEuropearelikelytodiminishasEasternEuropecatchesupeconomically.

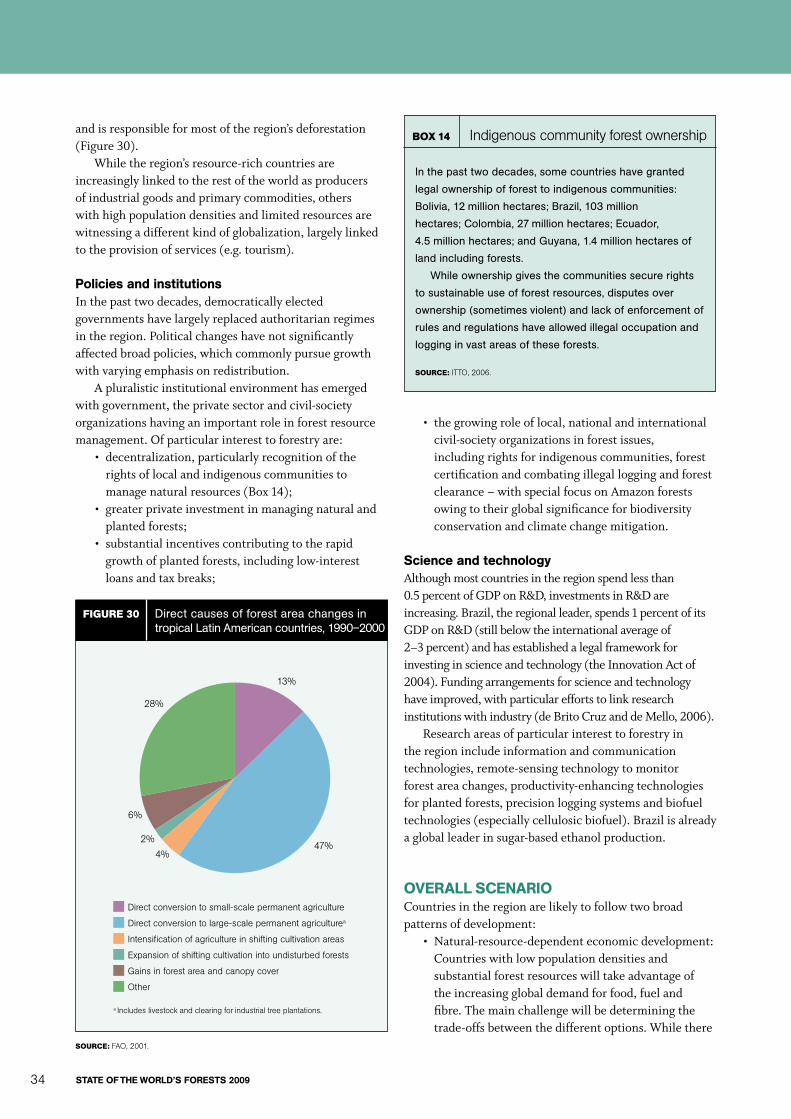

latin America and the CaribbeanForestsandforestryinLatinAmericaandtheCaribbeanwillbeinfluencedbythepaceofeconomicdiversificationandchangesinlanddependence.InCentralAmerica

stAte oF the World’s Forests 2009

ix

andtheCaribbean,wherepopulationdensitiesarehigh,increasingurbanizationwillcauseashiftawayfromagriculture,forestclearancewilldeclineandsomeclearedareaswillreverttoforest.However,inSouthAmerica,thepaceofdeforestationisunlikelytodeclineinthenearfuturedespitelowpopulationdensity.Highfoodandfuelpriceswillfavourcontinuedforestclearanceforproductionoflivestockandagriculturalcropsforfood,feedandbiofueltomeettheglobaldemand.Sustainableforestmanagementwillcontinuetobeachallengeinanumberofcountrieswherelandtenureispoorlydefined.

LatinAmericaandtheCaribbeanhasconsiderableopportunitiestobenefitfromthegrowingdemandforglobalpublicgoodsprovidedbyforests,especiallycarbonsequestrationandstorage,butrealizingthepotentialwillrequiresubstantialimprovementsinpolicyandinstitutionalframeworks.Plantedforestswillincrease,promotedbyprivateinvestmentsandcontinuingglobaldemandforwoodandwoodproductsfromAsia.However,itisunlikelythattheincreasedplantingratewillbesufficienttooffsetcontinuingdeforestation.

north AmericaThenearfutureofNorthAmericanforestrywilldependonhowquicklytheregionreversestherecenteconomicdownturnanditsimpactonthedemandforwoodandwoodproducts,especiallyintheUnitedStatesofAmerica.Theforestsectorwillalsoneedtoaddresschallengesofclimatechange,includingincreasingfrequencyandseverityofforestfiresanddamagebyinvasivepestspecies.Woodwillbeincreasinglydemandedasasourceofenergy,especiallyifcellulosicbiofuelproductionbecomescommerciallyviable;thisdevelopmentwouldlikelyresultinmuchlargerinvestmentsinplantedforests.

CanadaandtheUnitedStatesofAmericawillcontinuetohavefairlystableforestareas,althoughthedivestmentofwoodlandsownedbylargeforestcompaniescouldaffecttheirmanagement.InMexico,changesinthedeforestationratewilldependonthepaceoftransitionfromanagrariantoanindustrialeconomyandreduceddependenceonlandasasourceofincomeandemployment.Whilethe

economicviabilityoftheforestindustrymayfluctuateandevendecline,theprovisionofenvironmentalserviceswillcontinuetogaininimportance,drivenbypublicinterest.

Western and Central AsiaTheoutlookforforestsandforestryinWesternandCentralAsiaismixed.Incomegrowthandurbanizationsuggestthattheforestsituationwillimproveorremainstableinsomecountries,butthepictureislesspromisingforanumberoflow-incomeagriculture-dependentcountries.Forestdegradationwillpersistincountriesthatarerelativelywelloffbuthaveweakinstitutions.Overall,theforestsectorisgivenlowpriorityinpublicinvestments.

Adversegrowingconditionslimittheprospectsforcommercialwoodproduction.Rapidlyincreasingincomesandhighpopulationgrowthratessuggestthattheregionwillcontinuetodependonimportstomeetdemandformostwoodproducts.Provisionofenvironmentalserviceswillremainthemainjustificationforforestry,especiallyarrestinglanddegradationanddesertification,protectingwatershedsandimprovingtheurbanenvironment.Institutionbuilding,particularlyatthelocallevel,isneededinordertofacilitateanintegratedapproachtoresourcemanagement.

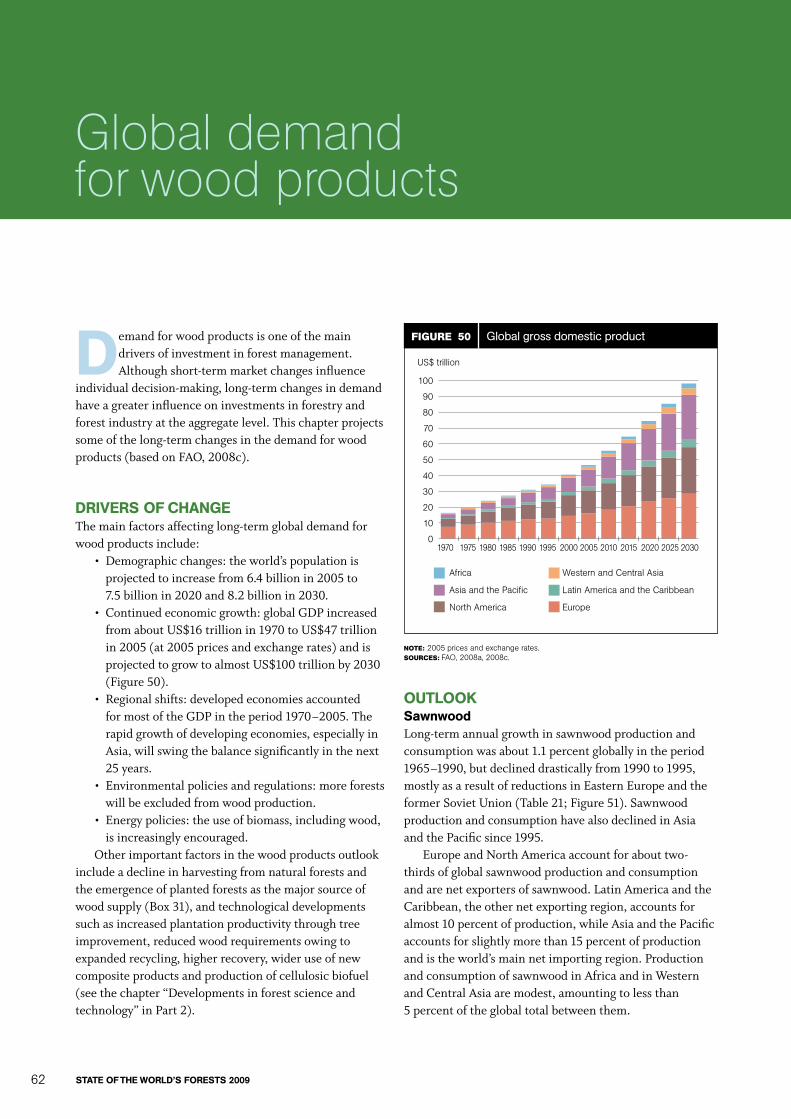

PArt 2: AdAPting For the Futureglobal wood products demandTheincomethatownersderivefrommanagingforeststomeetthedemandforgoodsandservicesisaprimarydeterminantofinvestmentinforestmanagement.Demographicchanges,economicgrowth,regionaleconomicshiftsandenvironmentalandenergypolicieswillbedecisiveinthelong-termglobaldemandforwoodproducts.

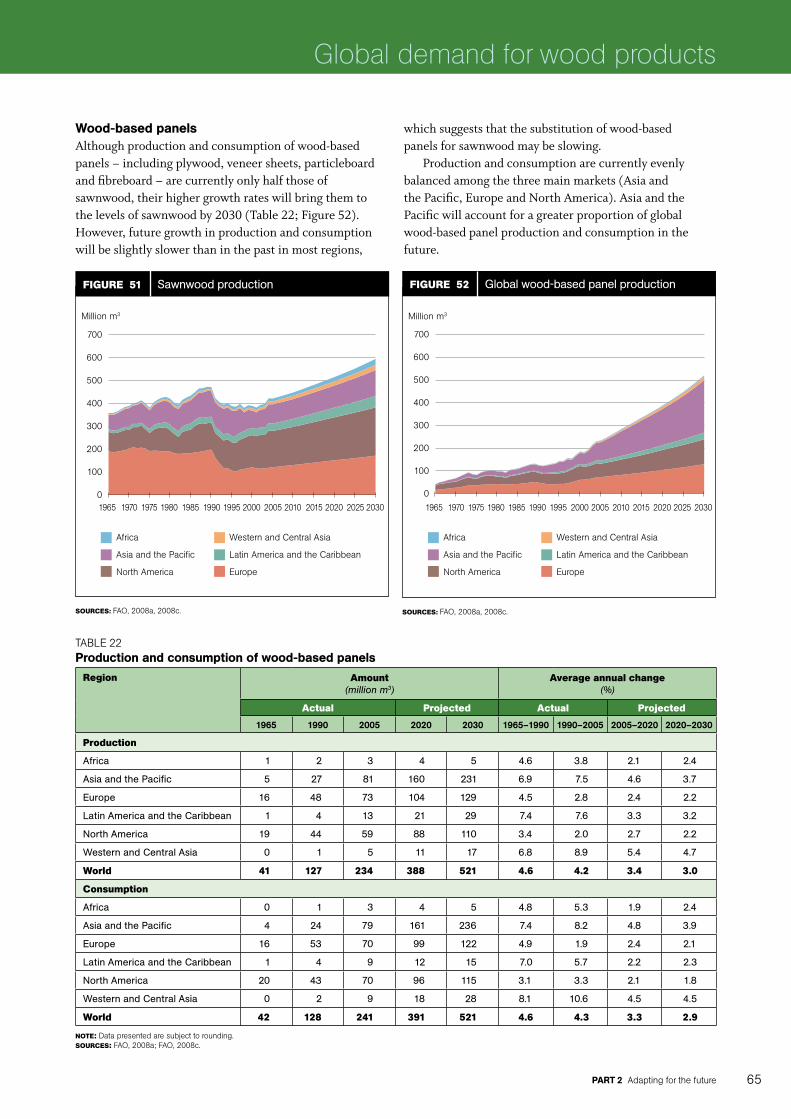

Productionandconsumptionofkeywoodproductsandwoodenergyareexpectedtorisefromthepresentto2030,largelyfollowinghistoricaltrends.Themostdramaticchangewillbetherapidincreaseintheuseofwoodasasourceofenergy,particularlyinEurope,asaresultofpoliciespromotinggreateruseofrenewableenergy.ThehighestgrowthrateswillcontinuetobeinAsia,whichwill

summAry

stAte oF the World’s Forests 2009x

bethemajorproducerandconsumerofwood-basedpanelsandpaperandpaperboard(althoughpercapitaconsumptionwillremainhigherinEuropeandNorthAmerica).IndustrialroundwoodproductioninAsiawillbefarshortofconsumption,increasingthedependenceonimports.

Thepotentialforlarge-scalecommercialproductionofcellulosicbiofuelwillhaveunprecedentedimpactsontheforestsector.Increasingtransportcostswillalsoinfluencethedemandforwoodproducts.Thesefactorsandothers,includingchangesinexchangerates,willinfluencethecompetitivenessoftheforestsectorandaffectproductionandconsumptionofmostforestproducts.

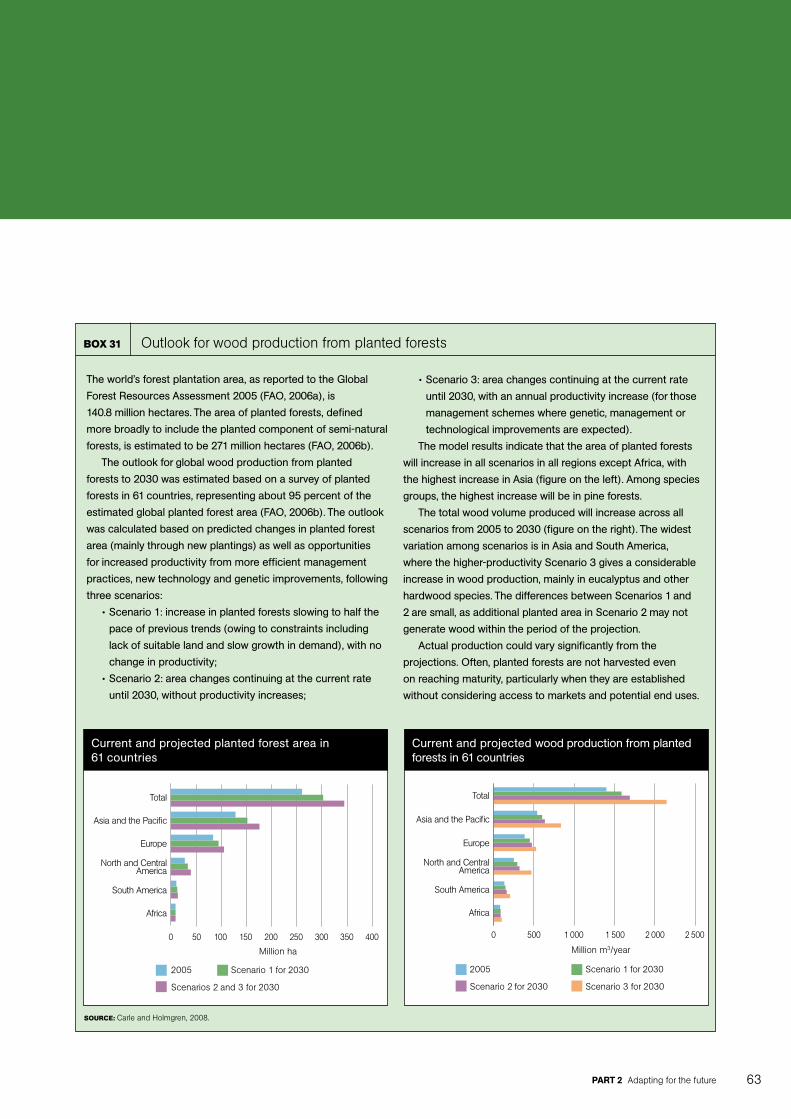

Industrialroundwoodwillbeincreasinglylikelytocomefromplantedforestsinthefuture.Thiscontinuingshiftpresentsinterestingopportunitiesandchallengesforforestmanagement.

meeting the demand for environmental services of forestsGrowthinincomecoupledwithgreaterawarenesswillincreasethedemandforenvironmentalservicesprovidedbyforestssuchascleanairandwater,mitigationofclimatechangeandunspoiltlandscapes.Whileincomegrowthalsoenhancestheabilityofsocietytomeetthecostsofenvironmentalprotection,economicgrowthisoftenaccompaniedbyincreasedenvironmentalimpacts.Inparticular,countrieswithrapidlygrowingeconomiesoftengothroughaperiodwhenforestresourcesareexploitedandtheirenvironmentalservicesdeclineaccordingly.Maintainingforestenvironmentalservicesrequiresstrikingabalancebetweentheproductionofgoodsandtheprovisionofservices.

Regulatoryapproachesforhelpingtosecureforests’abilitytomeetthedemandforenvironmentalservicesincludeprotectedareas,instrumentsforsustainableforestmanagementandgreenpublicprocurementpolicies.

Marketapproachesincludecertification,carbonmarketsandpaymentsforenvironmentalservices(PES).Third-partycertificationofforestswillcontinuetospread,althoughobtainingapremiumtocoverimplementationcostsremainsachallenge.Systemsforprovidingappropriatepaymentstoforestownersasameansofsupportingforestconservationarereceivingconsiderableattention;theyhavelongexistedforrecreationalservicesandarenowbeingadoptedforwatershedprotection,biodiversityconservationandcarbonsequestration.Suchschemesareexpectedtoincreaseinnumber;stableinstitutionalandlegalframeworksareaprerequisitefortheirsuccess.

Ongoingdiscussionsaboutincludingoptionsforreducingemissionsfromdeforestationandforestdegradation(REDD)inglobalclimatechangenegotiationshaveraisedmanyhopes.However,providingincentivestodesistfromdeforestationinvolvescomplexpolicy,institutionalandethicalissuesthatmustbeconsidered.

Changing institutionsTheshiftingbalanceamongforestsectorinstitutions–publicagencies,theprivatesector,civil-societyorganizations,theinformalsectorandinternationalorganizations–willplayanimportantpartinsociety’sadaptationtosocial,economicandenvironmentalchange.Withtheemergenceofnewplayers,theinstitutionallandscapehasbecomemorecomplex.Ingeneral(althoughnotinallcountries),theplayingfieldisbecomingmorelevel,partlyasaresultofnewinformationandcommunicationtechnologies.Much-neededpluralismprovidesnewopportunitiesforsmallandmediumenterprisesandcommunityorganizations.Ifgovernmentforestryagenciesthathavehistoricallydominatedthescenefailtoadapttochange,theycouldfadeintoirrelevance.

Withtheincreasingpaceofglobalization,newplayerssuchastimberinvestmentmanagementorganizations(TIMOs),realestateinvestmenttrusts(REITs),sovereignwealthfundsandcarbon-tradinginstitutionscouldaltertheglobalinstitutionalmap.Institutionswillfacetremendouspressuretobalancefragmentationandtoconsolidateefforts.

developments in forest science and technologyVisualizingthefutureofforestscienceandtechnologyisdifficultgiventherapidpaceofchange.Innovationhassignificantlyimprovedthecapacityoftheforestsectortomeetthechangingdemandsofsocietyandwillcontinuetodoso.However,manydevelopingcountrieshavelittleornocrediblesciencecapacity,andthislackhinderstheirlong-termdevelopment.Eveninmanydevelopedcountries,forestscienceandtechnologycapacitieshaveeroded.

However,researchcontinuestobreaknewgroundinallareasofforestry,fromproduction,harvestingandprocessingtowoodenergyandtheprovisionofenvironmentalservices.Relativelynewfieldssuchasbiotechnology,nanotechnologyandinformationandcommunicationtechnologiescontributetothesedevelopments.Thevalueofindigenousknowledgeisincreasinglybeingrecognized.

Thegrowthofcommerciallydrivenprivate-sectorresearchandthedecliningcapacityofpublic-sectorresearchraiseanumberofissues.Vastpopulationsthatcannotaffordtopayforimprovedtechnologiesareoftenexcludedfromthebenefitsofprivate-sectorresearch.Thisaccentuatesdisparitiesinaccesstoknowledge,withconsequencesforincomeandlivingstandards.

Moreconcertedeffortsareneededtoaddressimbalancesanddeficienciesinscientificandtechnologicalcapacity.Challengesincludereducingbarrierstotheflowoftechnologiesamongandwithincountries,ensuringthatsocialandenvironmentalissuesaremainstreamed,andtranscendingtraditionalsectoralboundariestotakeadvantageofscientificandtechnologicaldevelopmentsoutsidetheforestsector.

xi

Postscript: challenges and opportunities in turbulent timesAsState of the World’s Forests 2009goestopress(late2008),theworldisexperiencingasteepeconomicdecline.ThecontractionofthehousingsectorandthesubprimemortgagecrisisintheUnitedStatesofAmericahaveseverelyaffectedfinancialmarkets,triggeringaneconomicslowdowninvolvingalmostallcountriesandtransformingpreviouslyupbeateconomicforecasts.

Whatimpactswillthesechangeshaveontheforestsector?Thecollapseofthehousingsectorhasreducedthedemandforawidearrayofwoodandwoodproducts,leadingtomillclosuresandunemployment.Newinvestmentsareslowingasaresult,affectingallwoodindustries.

Thedemandforenvironmentalserviceshasalsochangedasaresultofreducedabilityandwillingnesstopayforsuchservices.Carbonpriceshaveremainedhighlyvolatile.Futureclimatechangearrangementsmayfacechallengesascountriesgiveprioritytotacklingtheeconomiccrisis.

Potentialnegativeimpactsonforestresourcescouldincludereducedinvestmentinsustainableforestmanagementandariseinillegalloggingasthedecline

intheformaleconomicsectoropensopportunitiesforexpansionoftheinformalsector.Landdependence,whichhadbeeneasing,couldincrease,raisingtheriskofagriculturalexpansionintoforests,deforestationandreversalofpreviousforestgains.However,therecouldalsobepositiveimpacts–reducedwooddemandcouldlessenpressureonforests,whileconversionofforestforlarge-scalecultivationofcommercialcropssuchasoil-palm,soybeansandrubbercouldslowastheirpricesfall.

Itisimpossibletoknowwhentheglobaleconomywillbegintorecover.However,suchcrisesalsoofferopportunitiestochartnewpathsofdevelopment.Theforestsectorcouldbenefitfromthepursuitofa“greenpath”todevelopment–throughbuildingupofnaturalresourcecapital(e.g.throughafforestationandreforestationandincreasedinvestmentsinsustainableforestmanagement),generationofruralemploymentandactivepromotionofwoodingreenbuildingpracticesandrenewableenergy.Certainly,thischangeofpathwillrequirefundamentalinstitutionalchanges,butthecrisismaybringaboutgreaterwillingnesstoacceptandimplementlong-overduereforms.

summAry

regional outlook

Part

Changes in society, which have accelerated in recent decades with the rapid growth in information and communication technologies and globalization, are bringing about important changes in the forest sector at all levels. Demographic, economic, institutional and technological changes have altered the pattern of demand for forest products and services.

Considering the long-term nature of forestry, a better understanding of the potential directions of change is crucial to developing appropriate priorities and strategies for the future of the sector. In particular, the growing interaction of societies through globalization compels forestry professionals to acquire a broader perspective beyond national borders.

Part 1 has been developed largely based on ongoing and completed regional forest sector outlook studies. For each region, the drivers of change external to the forest sector are first examined in the areas of demographics, economy, policies and institutions, and science and technology. All demographic data are from World Urbanization Prospects: The 2007 Revision Population Database (UN, 2008a). All gross domestic product (GDP) and value-added figures are in 2006 constant United States dollars.

For each region, there is a section outlining an overall scenario of societal changes that can be expected up to 2030. Taking the predicted changes and previous trends into account, the future for the forest sector is then projected, tracing developments in:

• forest area, based – unless otherwise noted – on statistics from the Global Forest Resources Assessment 2005 (FAO, 2006a);

• forest management, addressing both natural and planted forests;

• wood products (production, consumption and trade), with projections based on econometric modelling, taking into particular account the changes in population, income and other parameters that influence demand;

• woodfuel, looking at both traditional woodfuel (fuelwood and charcoal) and modern biofuels, including the “wild card” of eventual commercial production of cellulosic biofuel;

• non-wood forest products (NWFPs), identifying broad patterns only, as the diversity of NWFPs in all regions makes it extremely difficult to provide a comprehensive outlook;

• environmental services of forests, including biodiversity conservation, climate change mitigation, protection against desertification and land degradation, watershed services and nature tourism. Protected areas are given as a rough indicator of conservation status; as recent reliable statistics do not exist by country for forest protected areas, figures are given for terrestrial protected areas (which include but are not limited to forests).

The aim has been to capture the main trends despite diversity within and among regions and countries which made the task a great challenge. An effort has also been made to provide a balanced perspective between short-lived changes, which usually capture most of the attention, and the less perceptible long-term changes, which are often neglected.

1

S. V

erve

r

stAte oF the World’s Forests 20092

Africa

t heAfricancontinent(Figure1),consistingof58countriesandareas(seeAnnex),containshighlydiverseecosystems.Thecontinentaccounts

for14percentoftheglobalpopulation.Theregion’s635millionhectaresofforestsaccountfor21.4percentofitslandarea.TheCongoBasinhoststhesecond-largestcontiguousblockoftropicalforest(Figure2).

drivers oF ChAngedemographicsAfrica’spopulationgrewfrom472millionin1980to943millionin2006andisexpectedtoriseto1.2billionby2020(Figure3).Althoughtheannualgrowthrateisdeclining(from2.5percentbetween1990and2000toaprojected2.1percentbetween2010and2020),theincreaseinabsolutenumbersimpliesfurtherpressureonitsresources.

Africaisurbanizingrapidly.By2020,about48percentofthetotalpopulationwillbeurban.However,withtheexceptionofmostofNorthernAfrica,Africawillremain

Africa

largelyruralinthenextdecadeandbeyond.Theruralpopulationisprojectedtoincreaseby94millionbetween2005and2020.

HIV/AIDSwillcontinuetoaffectthehumanandfinancialresourcesofanumberofcountries(Box1).

economyIn2006,Africaaccountedforabout2.3percentofglobalGDP.Since2000,theoveralleconomicsituationhasimproved.GDPgrowthrateshaverisenfrom2.3percentonaveragebetween1990and1999tomorethan5percentsince2000,reaching6.2percentin2007(IMF,2008).Highgrowthratesarelikelytopersistinthemediumterm(Figure4).However,despiteincreasedGDPgrowth,thepercapitaincomegrowthrateremainslowbecauseofpopulationgrowth(exceptinSouthAfrica).

Lowdomesticsavingsandinvestments,unevengrowthandskeweddistributionofincomeremainconcerns.Recentgrowthspurtsarepartlyaconsequenceofthehighpricesofoilandotherprimarycommodities.

Figure 2 Extent of forest resources

ForestOther wooded landOther land cover

Central AfricaEast AfricaNorthern AfricaSouthern AfricaWest Africa

Figure 1 Subregional breakdown used in this report

Note: See annex table 1 for list of countries and areas by subregion.

PArt 1 regional outlook 3

Agriculture’sshareingrossvalueaddedhasdeclined,fromabout20percentinthe1990sto15percentin2006.However,agricultureisvitalforlivelihoods;itaccountedfor70percentofruralemploymentin2005.Percapitaproductivityofagricultureisextremelylowincomparisonwithotherregions,anddecliningagriculturalincomehasenhanceddependenceonoff-farmemployment,includingcollectionoffuelwoodandNWFPsandproductionofcharcoal.

MuchofAfrica’seconomicgrowthsince2000hasbeendrivenbyexportsofprimarycommoditiestotheemergingAsianeconomies,andthisislikelytocontinue.Africa’sindustriesfacemajorchallenges,especiallyfromincreasingcompetitionindomesticandglobalmarkets.Participationinglobalmarketsisexpectedtoremainunevenbecauseoflimitationsinpolicyandinstitutionalframeworks,infrastructure,humanresourcedevelopment,theinvestmentclimateandcompetitiveness.Africanmarketsremainsmallandfragmented,althoughmechanismsforregionalandsubregionalintegrationsuchasthe

Figure 3 Population

Source: un, 2008a.

1 3001 2001 1001 000

900800700600500400300200100

0

Million

1980 1985 1990 1995 2000 2005 2010 2015 2020

Figure 4 Gross domestic product

SourceS: Based on un, 2008b; World Bank, 2007a.

2 000

1 800

1 600

1 400

1 200

1 000

800

600

400

200

0

uS$ billion

1980 1985 1990 1995 2000 2005 2010 2015

•Drastic decline in resources – human and financial –

leaving less for long-term investments

•Increased dependence on forest products, especially

those that are easy to collect

•Loss of traditional knowledge

•Shortage of skilled and unskilled labour –

undermining forestry by affecting all key sectors such

as wood industries, research, education, training,

extension and forest administration

•Increased costs to industry on account of

absenteeism and higher bills for treatment

•Reduced public-sector investment in forestry, as

most governments will have to devote more of their

budgets to health care and combating HIV/AIDS

Source: fao, 2003a.

BoX 1 impacts of hiV/aidS

total africa West africa northern africa

east africa Southern africa central africa

total africa northern africa Southern africa

West africa east africa central africa

stAte oF the World’s Forests 20094

EconomicCommunityofWestAfricanStates(ECOWAS)andtheSouthernAfricanDevelopmentCommunity(SADC)arebeginningtobearfruit.

Policies and institutionsCivilsociety’sdemandfortransparencyandgoodgovernanceisbringingaboutfundamentalchangesinAfrica.Decentralizationofauthorityandparticipatoryapproachestoresourcemanagementarefindingwideracceptance.However,conflictsunderminesocialandeconomicdevelopmentinanumberofcountries.

CommunityinvolvementinnaturalresourcemanagementhasalonghistoryinAfrica,andpolicyandlegalchangesinrecentyearshavehelpedtoacceleratedevolution.However,forestryfacessomeenduringinstitutionaldifficultiessuchas:

• poorintersectorallinkages,withhigh-prioritysectorssuchasagriculture,mining,industrialdevelopmentandenergyeffectivelyhavingagreaterimpactonforeststhanforestpolicy;

• inconsistenciesinlawsgoverningtheenvironmentandthosegoverninginvestments;

• poorgovernanceandcorruptioninsomecountries;• landtenureuncertainties,weaklegalframeworksand

otherhindrancestothedevelopmentofacompetitiveprivatesector;

• decliningcapacityofpublicforestryagencies,includingresearch,education,trainingandextension.

science and technologyWiththeexceptionofSouthAfricaandsomecountriesinNorthernAfrica,scienceandtechnologydevelopmentintheregionhasbeenrelativelyslow,largelybecauseof:

• lowinvestmentsinscienceeducationandinresearch;• thehighshareofeconomicactivitiesremainingin

theinformaldomain,whichcurbsinteresttoinvestininnovations;

• afailuretodevelopanduseAfrica’sstrongbaseoftraditionalknowledgetodealwithmodernproblems.

Furthermore,researchandsystematicenquirydonottendtobefullymainstreamedindevelopmentplanningandpolicy-making.

However,mobilecommunicationsandtheInternetareimprovingaccesstoinformation.

Theforestsectorreflectsthegeneralsituation.Substantialeffortsarerequiredtorevamptheinstitutionalframeworktostrengthenthescienceandtechnologybaseofforestry.Otherwise,majorbreakthroughsarelikelytobypasstheAfricanforestsectororatbestwillbenefitonlyasmallsegmentofthepopulation.

overAll sCenArioPoliticalandinstitutionaldevelopmentswillhavethegreatestinfluenceontheforestryoutlookandarethemostuncertain(FAO,2003a).Amajortransition–onethatwouldfavourbalancedandequitablenaturalresourcemanagement–woulddependon:improvedefficiencyandaccountabilityinthepublicsector;greaterinclusiveness,competitivenessandtransparencyinmarketinstitutions;andaninformalsector(i.e.arrangementsoutsidethepublicandmarketdomains)thatprovideslivelihoodopportunitiesforthepoor,especiallywherethesearelackingintheformalsector.Whileimprovementsarebeingmadeinthisdirection,substantialeffortswouldbeneededtoeffectarealturnaroundbefore2020.Inmostcases,acontinuationalongthecurrentdevelopmentpath–a“businessasusual”scenario–appearsmorelikely.

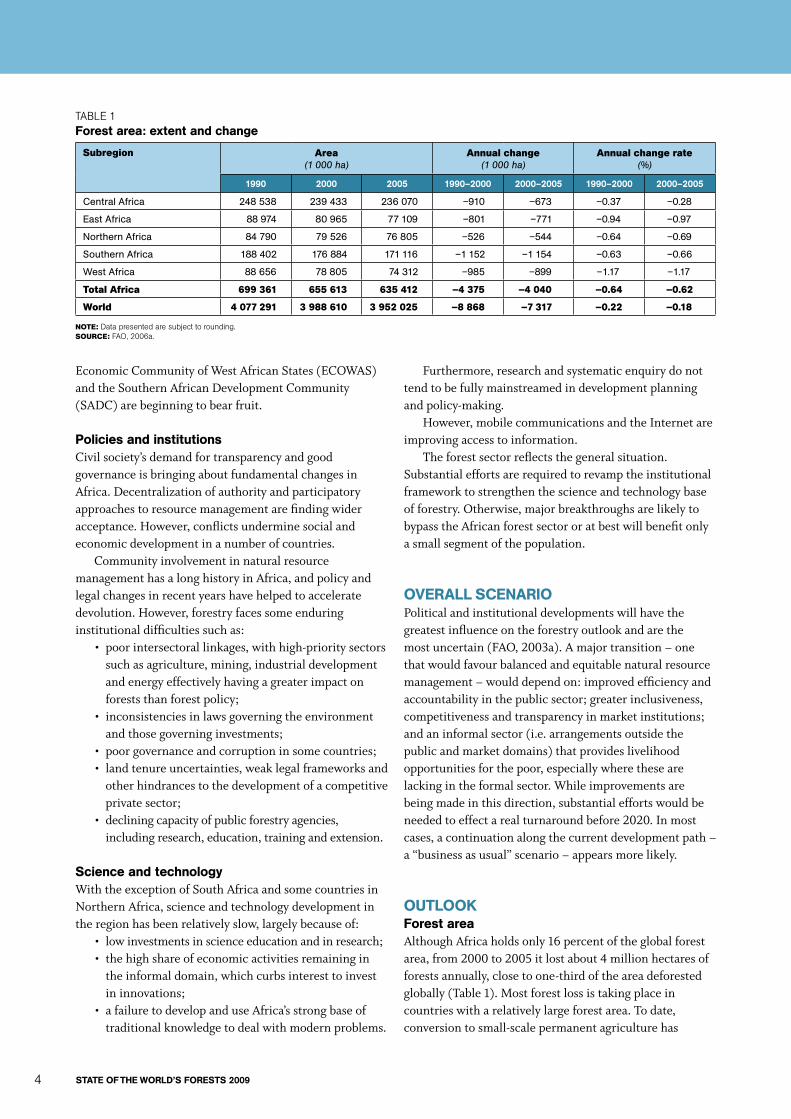

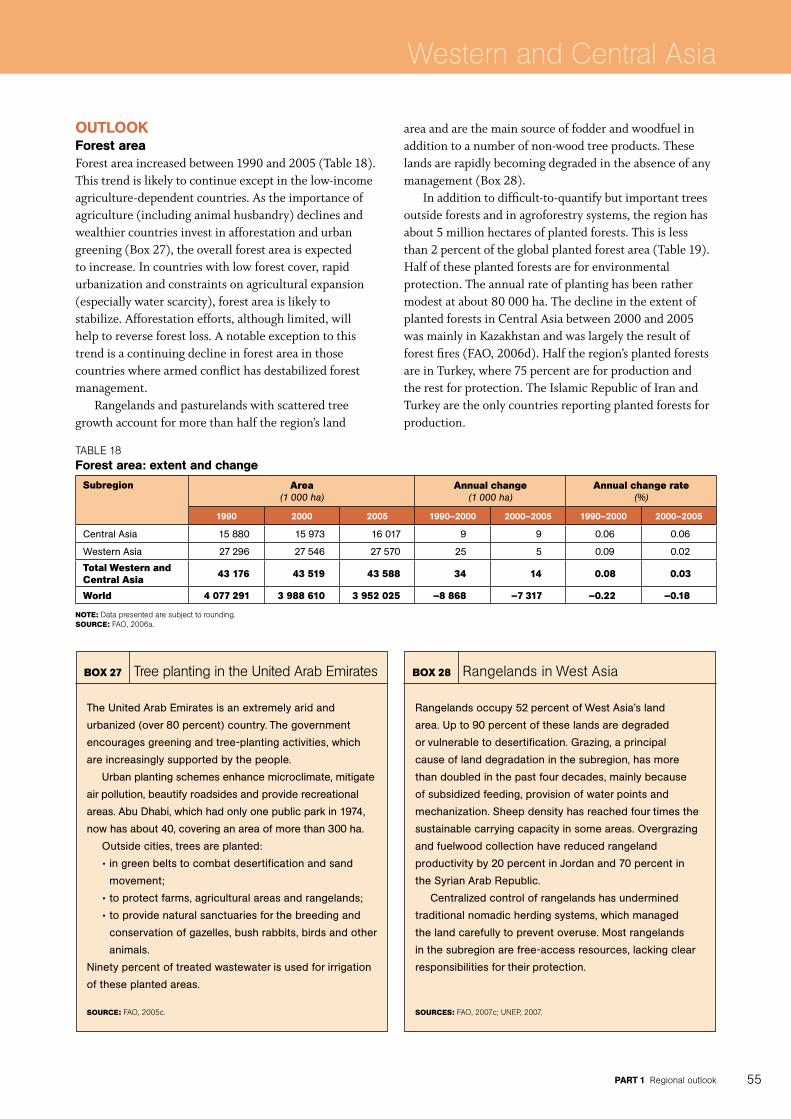

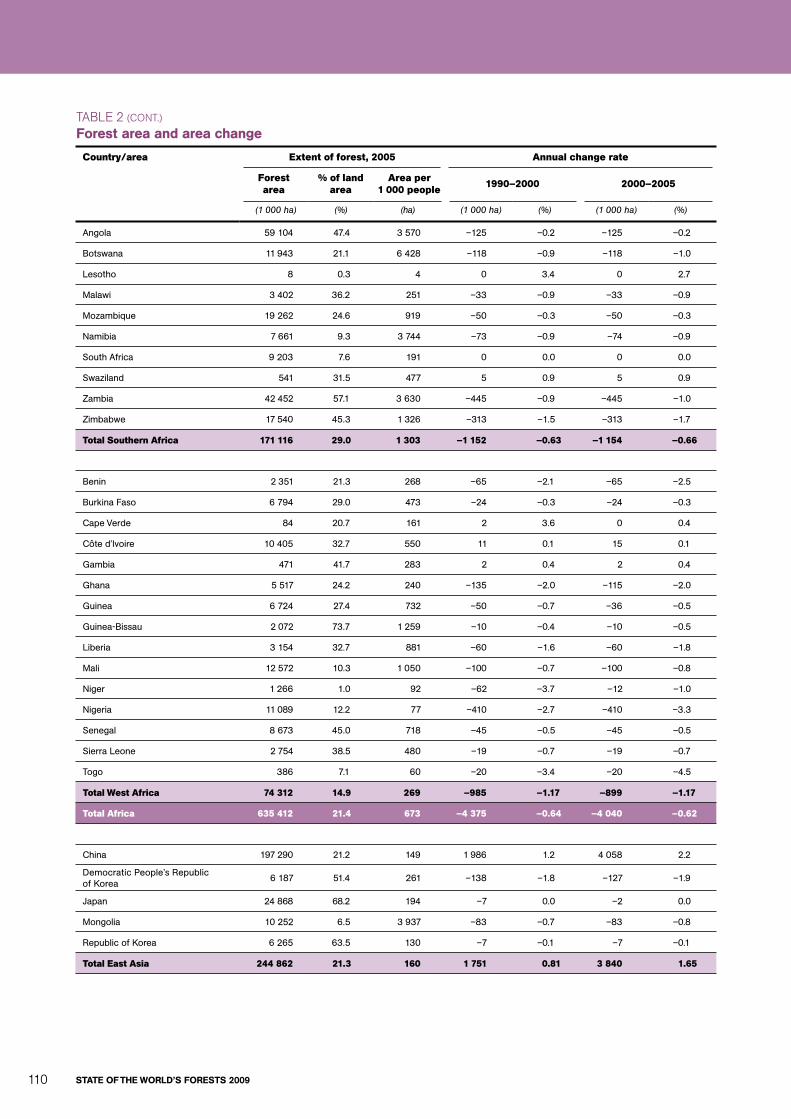

outlookForest areaAlthoughAfricaholdsonly16percentoftheglobalforestarea,from2000to2005itlostabout4millionhectaresofforestsannually,closetoone-thirdoftheareadeforestedglobally(Table1).Mostforestlossistakingplaceincountrieswitharelativelylargeforestarea.Todate,conversiontosmall-scalepermanentagriculturehas

taBle 1Forest area: extent and change

Subregion Area(1 000 ha)

Annual change(1 000 ha)

Annual change rate(%)

1990 2000 2005 1990–2000 2000–2005 1990–2000 2000–2005

Central Africa 248 538 239 433 236 070 –910 –673 –0.37 –0.28

East Africa 88 974 80 965 77 109 –801 –771 –0.94 –0.97

Northern Africa 84 790 79 526 76 805 –526 –544 –0.64 –0.69

Southern Africa 188 402 176 884 171 116 –1 152 –1 154 –0.63 –0.66

West Africa 88 656 78 805 74 312 –985 –899 –1.17 –1.17

total Africa 699 361 655 613 635 412 –4 375 –4 040 –0.64 –0.62

World 4 077 291 3 988 610 3 952 025 –8 868 –7 317 –0.22 –0.18

Note: data presented are subject to rounding.Source: fao, 2006a.

PArt 1 regional outlook 5

Africa

beenthemaincontributortoforestloss(Figure5),butinvestmentinlarge-scaleagriculturecouldbecomeamajordriverofdeforestationinthefuture.

Forestlossislikelytocontinueatcurrentrates.Thegrowingdemandfor,andrisingpriceof,foodandenergywillexacerbatethesituation,especiallyasincreasedinvestmentsininfrastructureopenupnewareas.Climatechangewillalsohaveanimpact.Increasingfrequencyofdroughts,decliningwatersuppliesandfloodsstraincopingmechanismsatthelocalandnationallevelsandundermineeffortstomanageforestssustainably.

Bysubregion,thefollowingpictureislikely:• AnimprovementintheeconomicsituationinNorthern

Africacouldhelptoreducethepressureonlandandreversepasttrendsofforestclearance,particularlyintheSudan.However,externalinvestmentsinlarge-scaleagricultureinresponsetohighfoodpricescouldhaveanegativeimpactonforests.

• InEastandSouthernAfrica,highpopulationdensitiesandhighlanddependencecoupledwithland-useconflictsandlimitedopportunitiesforeconomicdiversificationarelikelytoreduceforestareafurther.

• InCentralAfrica,lowpopulationdensities,largeexpansesoflandandimprovedaccessibilitymayfavourforestclearanceforcommercialandsubsistenceagriculture.Improvedmarketabilityofless-commercialspeciesmayleadtointensive

unsustainablelogging,especiallyinthecontextofweakpoliciesandinstitutions.

• InWestAfrica,rapidlygrowingurbandemandforwoodfuelandincreasingagriculturaldemandislikelytoresultincontinuedreductioninforestcover.

Forest managementNaturalforestscontinuetobethemainsourceofwoodsupplies.TheInternationalTropicalTimberOrganization(ITTO,2006)foundthatonlyabout6percentofthenaturaltropicalproductionforestsinthepermanentforestestateofitstenAfricanmembercountriesweresustainablymanaged.Reduced-impactloggingandharvestingcodesareyettofindwideapplication,andinvestmentinregenerationofloggedareasisminimal.

GlobalconcernaboutsourcingwoodfromsustainablymanagedareasisencouragingtheadoptionofcertificationinAfrica.However,theextentofcertificationremainslowbecauseofthehightransactioncosts(Box2).

Giventhelikelihoodofa“businessasusual”scenario,progressinimplementingsustainableforestmanagementisexpectedtobeslow,primarilybecauseof:

• thegenerallyunfavourableinvestmentclimate;• severeinstitutional,financialandtechnical

constraintshinderingforestryadministrations’abilitytomanageloggingconcessions,whichhaveoftenexpandedsofastthatgovernmentscannotenforcerulesandregulationsandfullyrecoverpotentialincome;

• illegalactivitiesandcorruption;• policiesandinstitutional,technicalandeconomic

hurdleslimitingwideradoptionofcommunity-basedforestmanagement,andatendencytotransferonlydegradedforeststolocalcommunities,whichlacktheinvestmentcapacitytorehabilitatethem.

Alloftheabovefavourunsustainableexploitation.Dependingonhowcommunitycapacityisbuiltup,someprogressinsustainableforestmanagementisexpectedinthesavannahwoodlands,especiallyinEastandSouthernAfrica,althoughitmaybehinderedbylowreturnsfromtheseforests.

Withanestimated14.8millionhectaresofplantedforests(FAO,2006b),Africaaccountsforonlyabout5percentofthe

Of the 306 million hectares of certified forests in the world

(June 2007), Africa accounts for about 3 million hectares

(about 1 percent). Most of Africa’s certified forests are

planted forests, and about half are in South Africa.

Source: itto, 2008.

BoX 2 forest certification in africa

Figure 5 Direct causes of forest area changes in tropical African countries, 1990–2000

direct conversion to small-scale permanent agriculture

direct conversion to large-scale permanent agriculturea

intensification of agriculture in shifting cultivation areas

expansion of shifting cultivation into undisturbed forests

gains in forest area and canopy cover

other

Source: fao, 2001.

4%

8%

59%

12%

8%

9%

a includes livestock and clearing for industrial tree plantations.

stAte oF the World’s Forests 20096

globaltotal.Ofthis,about3millionhectareswereplantedforprotectionandtherestforproductionofwoodandnon-woodforestproducts(e.g.gumarabic).MostofAfrica’swoodisproducedfromnaturalforests;investmentsinplantedforestshaveoccurredmainlyincountrieswithrelativelylowforestcover(Algeria,Morocco,Nigeria,SouthAfricaandtheSudan).AverageannualplantinginAfricafrom1990to2005wasestimatedatabout70000ha,lessthan2percentoftheglobalplantingrate.Inseveralcountries,plantedforestareahasdeclinedinrecentyears.

WiththeexceptionofSouthAfrica,mostplantedforestsareestablishedandmanagedbypublicforestryagencies.Expansionofforestplantingandintensivemanagementforproductionwilllargelydependonplantationprofitabilityasperceivedbytheprivatesector,takingintoaccounttheglobaldemandforwoodproducts.Realizationofthepotentialinsomeofthecountriesrequiressignificantimprovementsinthepolicyandinstitutionalframework,includinglandownership.

Growingdemandforwoodhasencouragedfarmplantinginmostcountries,andtreesoutsideforestshavebecomeanincreasinglyimportantsourceoftimberandfuelwood(Box3).Thistrendisexpectedtointensifyinthecomingyears.Thepotentialoffarmplantingtosupply

industrialroundwoodandtheconstraintsinobtaininglandforlarge-scaleplantedforestshaveencouragedindustriestoenterintopartnershipwithcommunities,forexampleinSouthAfrica.Improvedtenureandsupportivelegislationcouldconsiderablyboosttreeplantingonfarms,asisalreadyhappeninginmanycountries(e.g.Ghana,KenyaandUganda).

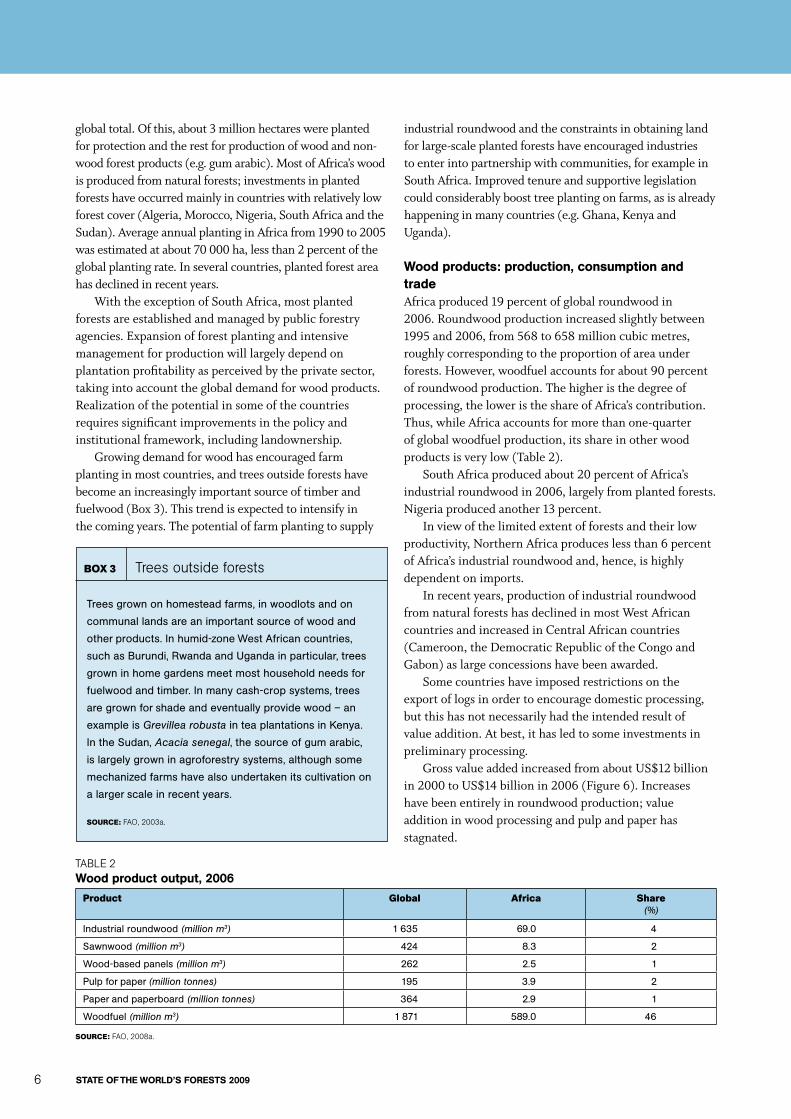

Wood products: production, consumption and tradeAfricaproduced19percentofglobalroundwoodin2006.Roundwoodproductionincreasedslightlybetween1995and2006,from568to658millioncubicmetres,roughlycorrespondingtotheproportionofareaunderforests.However,woodfuelaccountsforabout90percentofroundwoodproduction.Thehigheristhedegreeofprocessing,theloweristheshareofAfrica’scontribution.Thus,whileAfricaaccountsformorethanone-quarterofglobalwoodfuelproduction,itsshareinotherwoodproductsisverylow(Table2).

SouthAfricaproducedabout20percentofAfrica’sindustrialroundwoodin2006,largelyfromplantedforests.Nigeriaproducedanother13percent.

Inviewofthelimitedextentofforestsandtheirlowproductivity,NorthernAfricaproduceslessthan6percentofAfrica’sindustrialroundwoodand,hence,ishighlydependentonimports.

Inrecentyears,productionofindustrialroundwoodfromnaturalforestshasdeclinedinmostWestAfricancountriesandincreasedinCentralAfricancountries(Cameroon,theDemocraticRepublicoftheCongoandGabon)aslargeconcessionshavebeenawarded.

Somecountrieshaveimposedrestrictionsontheexportoflogsinordertoencouragedomesticprocessing,butthishasnotnecessarilyhadtheintendedresultofvalueaddition.Atbest,ithasledtosomeinvestmentsinpreliminaryprocessing.

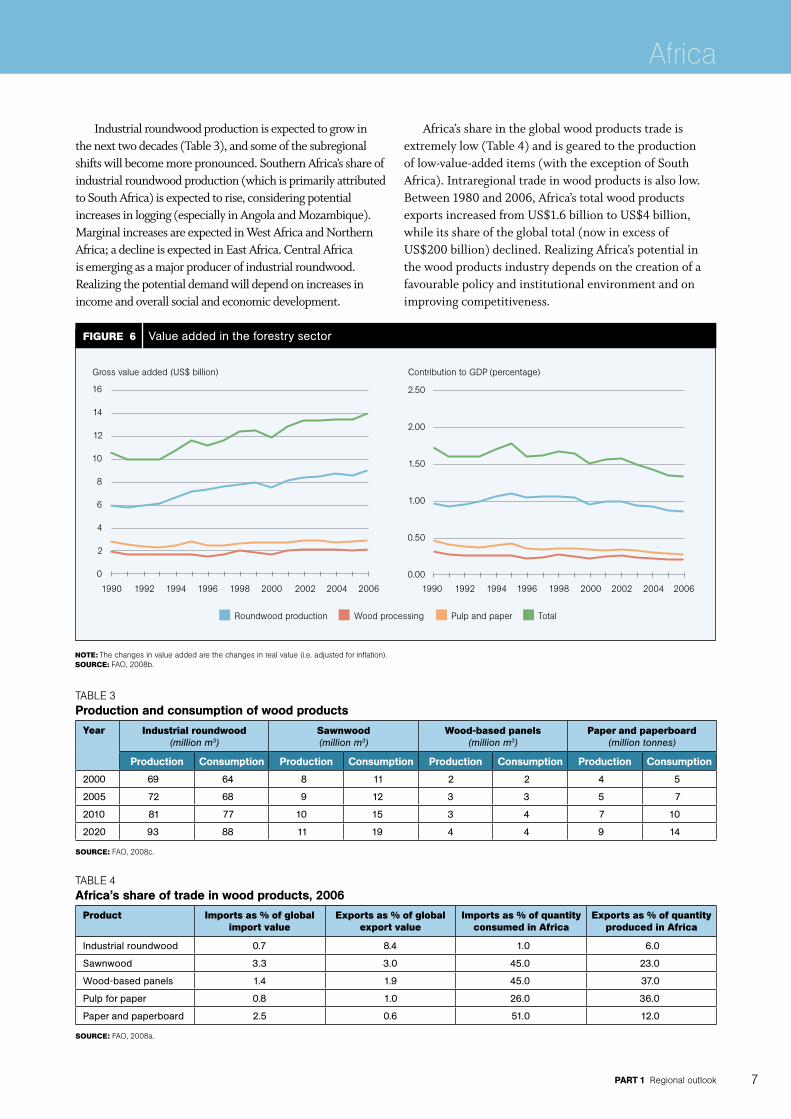

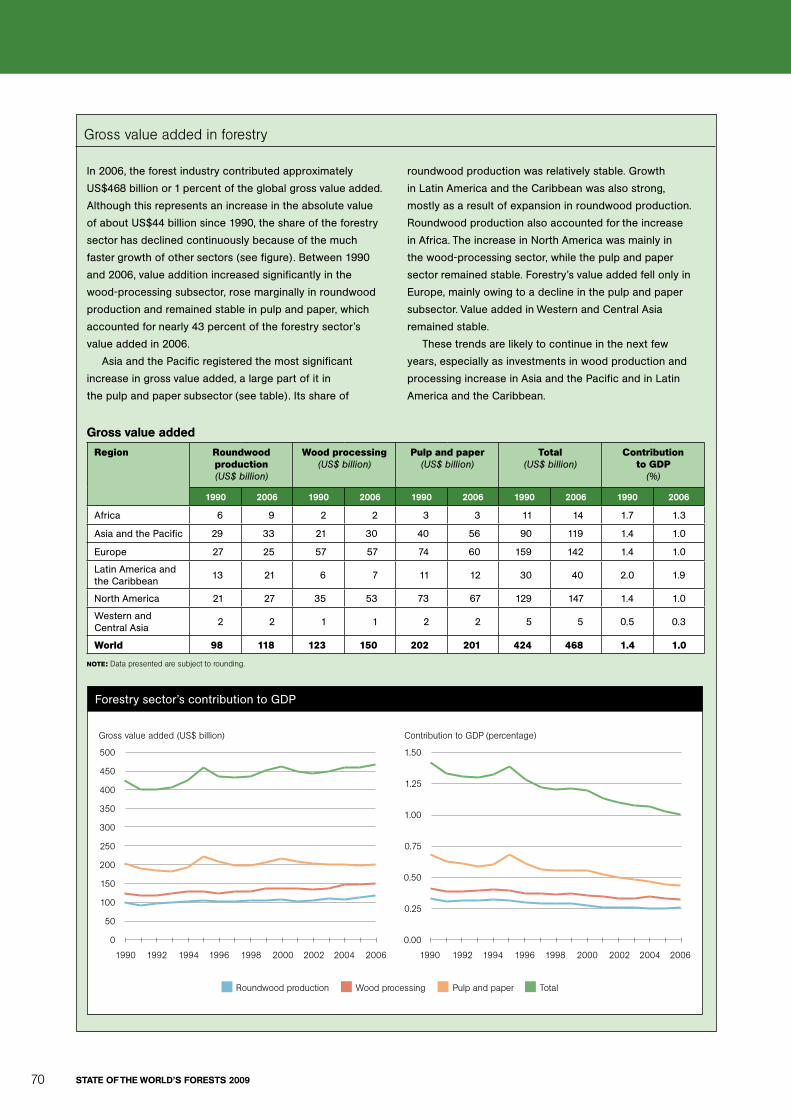

GrossvalueaddedincreasedfromaboutUS$12billionin2000toUS$14billionin2006(Figure6).Increaseshavebeenentirelyinroundwoodproduction;valueadditioninwoodprocessingandpulpandpaperhasstagnated.

Trees grown on homestead farms, in woodlots and on

communal lands are an important source of wood and

other products. In humid-zone West African countries,

such as Burundi, Rwanda and Uganda in particular, trees

grown in home gardens meet most household needs for

fuelwood and timber. In many cash-crop systems, trees

are grown for shade and eventually provide wood – an

example is Grevillea robusta in tea plantations in Kenya.

In the Sudan, Acacia senegal, the source of gum arabic,

is largely grown in agroforestry systems, although some

mechanized farms have also undertaken its cultivation on

a larger scale in recent years.

Source: fao, 2003a.

BoX 3 trees outside forests

taBle 2Wood product output, 2006

Product global Africa Share(%)

Industrial roundwood (million m3) 1 635 69.0 4

Sawnwood (million m3) 424 8.3 2

Wood-based panels (million m3) 262 2.5 1

Pulp for paper (million tonnes) 195 3.9 2

Paper and paperboard (million tonnes) 364 2.9 1

Woodfuel (million m3) 1 871 589.0 46

Source: fao, 2008a.

PArt 1 regional outlook 7

Africa

Industrialroundwoodproductionisexpectedtogrowinthenexttwodecades(Table3),andsomeofthesubregionalshiftswillbecomemorepronounced.SouthernAfrica’sshareofindustrialroundwoodproduction(whichisprimarilyattributedtoSouthAfrica)isexpectedtorise,consideringpotentialincreasesinlogging(especiallyinAngolaandMozambique).MarginalincreasesareexpectedinWestAfricaandNorthernAfrica;adeclineisexpectedinEastAfrica.CentralAfricaisemergingasamajorproducerofindustrialroundwood.Realizingthepotentialdemandwilldependonincreasesinincomeandoverallsocialandeconomicdevelopment.

Africa’sshareintheglobalwoodproductstradeisextremelylow(Table4)andisgearedtotheproductionoflow-value-addeditems(withtheexceptionofSouthAfrica).Intraregionaltradeinwoodproductsisalsolow.Between1980and2006,Africa’stotalwoodproductsexportsincreasedfromUS$1.6billiontoUS$4billion,whileitsshareoftheglobaltotal(nowinexcessofUS$200billion)declined.RealizingAfrica’spotentialinthewoodproductsindustrydependsonthecreationofafavourablepolicyandinstitutionalenvironmentandonimprovingcompetitiveness.

Figure 6 Value added in the forestry sector

gross value added (uS$ billion) contribution to gdP (percentage)

roundwood production Wood processing Pulp and paper total

1990 1992 1994 1996 1998 2000 2002 2004 2006

Note: the changes in value added are the changes in real value (i.e. adjusted for inflation). Source: fao, 2008b.

1990 1992 1994 1996 1998 2000 2002 2004 2006

16

14

12

10

8

6

4

2

0

2.50

2.00

1.50

1.00

0.50

0.00

taBle 3Production and consumption of wood products

Year industrial roundwood(million m3)

Sawnwood(million m3)

Wood-based panels(million m3)

Paper and paperboard(million tonnes)

Production Consumption Production Consumption Production Consumption Production Consumption

2000 69 64 8 11 2 2 4 5

2005 72 68 9 12 3 3 5 7

2010 81 77 10 15 3 4 7 10

2020 93 88 11 19 4 4 9 14

Source: fao, 2008c.

taBle 4Africa’s share of trade in wood products, 2006

Product imports as % of global import value

exports as % of global export value

imports as % of quantity consumed in Africa

exports as % of quantity produced in Africa

Industrial roundwood 0.7 8.4 1.0 6.0

Sawnwood 3.3 3.0 45.0 23.0

Wood-based panels 1.4 1.9 45.0 37.0

Pulp for paper 0.8 1.0 26.0 36.0

Paper and paperboard 2.5 0.6 51.0 12.0

Source: fao, 2008a.

stAte oF the World’s Forests 20098

WoodfuelTraditionalenergysources(mainlybiomass)dominatetheenergysector,especiallyinsub-SaharanAfrica,whereonly7.5percentoftheruralpopulationhasaccesstoelectricity(WorldEnergyCouncil,2005).Ashouseholdincomesandinvestmentinappropriatealternativesremainlow,woodislikelytoremainanimportantenergysourceinAfricainthecomingdecades(FAO,2008d).Forecastsmadein2001suggesteda34-percentincreaseinwoodfuelconsumptionfrom2000to2020(Figure7).However,theriseinfuelpricesinthepasttwoyearssuggeststhatthisincreaseislikelytobeevengreater.Theshareofwoodfuelinthetotalenergysupplyislikelytodecline,buttheabsolutenumberofpeopledependentonwoodenergyispredictedtogrow(FAO,2008d).

Althoughwoodfuelsupplyanddemandarebalancedattheaggregatelevel,thereareareasofacutedeficit,resultinginunsustainableremovals,particularlyaroundurbancentres.Mostcountrieshaveattemptedtoboostsupplythroughimprovedmanagementofforestsandwoodlandsandtheestablishmentofwoodfuelplantations,andtoreducedemandbypromotingmore-efficientcookingdevicesandalternativefuels.

Globalinterestinbiofuelsasaresultofrisingfossilfuelpriceshasincreasedinvestmentsinbiofueldevelopment,forexamplethroughtheplantingofJatrophaspecies.Itisuncertainwhethertheseinvestmentswillprovidealong-termsolutiontoAfrica’senergyproblems,andtherearegrowingconcernsaboutadverseimplicationsforfoodsecurity.

non-wood forest productsAfricanNWFPs(gumsandresins,honeyandbeeswax,dyingandtanningmaterials,bambooandrattan,bushmeat,fodderandaconsiderablenumberofmedicinal

plants)arelargelyusedforsubsistenceandtradedinformally.Thus,theirlivelihoodcontributionandlocalsignificanceexceedthatwhichmaybeapparentfromofficialstatistics(Shackleton,ShanleyandNdoye,2007).

Withincreasedopportunitiesforlocal,regionalandinternationaltrade,theNWFPsectorinAfricaisundergoingperceptiblechanges.AfricangovernmentsareincreasinglydevelopingpoliciesandlegislationaimedatformalizingNWFPvaluechains.Ofparticularsignificanceistheemergenceofmarketsfor“ethnicfoods”,medicinalplantsandnaturalororganicgoods,suchashoney,beeswaxandsheabutter(Box4).Severalproductsthataretradednationallyandinternationallystraddletheinformalandformalsectors.Forexample,collectionfromthewildmayremainintheinformalsector,whileprocessingandtradeareintheformalsector.

Inviewofthewiderangeofproductsandenduses,itisdifficulttomakeawidelyapplicableforecast,buttheoutlookislikelytoinclude:

• subsistenceconsumptionofmostproductswithlittleattentiontomanagementoftheresources;

• overexploitationanddepletionofsomewildresourcescollectedforcommercialproducts;

• furtherpressureonbushmeatresourcesasaresultofincreasedpopulation;

• domesticationandcommercialcultivationandprocessingofasmallnumberofproductsbyentrepreneursorlocalcommunities;

Cosmetics such as oils, creams and dyes represent one

of the fastest-emerging global markets for non-wood

forest products. Shea butter, derived from the fruit of the

shea tree (Butyrospermum parkii or Vitellaria paradoxa)

and commonly known as karité, is one of the most

popular ingredients in skin care today. The shea tree is

found only in Africa’s Sahel belt, and it is estimated that

3 million rural African women are involved in the export of

shea products, which were valued at US$100 million for

2007–2008. In Burkina Faso, karité is the second-largest

export item after cotton, and several projects are focusing

on developing the sector. For example, Burkina Faso’s

Project Karité organizes local women’s associations that

collect and process shea nuts and karité for international

markets. As the women run their own operations, activities

typically comply with “fair trade” conditions. In addition,

most of the small village enterprises supported by

TREE AID in Burkina Faso are based on karité.

SourceS: fao, 2007a; uSaid, 2008.

BoX 4 Shea-butter-based cosmetic products

Figure 7 Woodfuel consumption

Source: fao, 2003b.

900

800

700

600

500

400

300

200

100

0

Million m3

2000 2010 2020

northern africa Southern africa central africa

West africa east africa

PArt 1 regional outlook 9

Africa

• growingdemandfromnichemarketsforcertifiedandfair-tradeproducts(WelfordandLeBreton,2008).

environmental services of forestsUndera“businessasusual”scenario,forestbiodiversitylossislikelytocontinue.EffortstoreversethesituationshouldbuildonthesuccessesofcommunitymanagementinitiativessuchastheCommunalAreasManagementProgrammeforIndigenousResources(CAMPFIRE)inZimbabwe(FrostandBond,2008).Biodiversityconservationalsoneedstobeaddressedoutsideprotectedareasandintegratedintokeyeconomicactivities.

Protectedareascurrentlycoverabout320millionhectares(11percentoftheregion’slandarea),butAfrica’sinvestmentandstaffinginparkmanagementremainthelowestintheworld.Majorchallengestoprotectedareamanagementincludeincreasinghuman–wildlifeconflict(FAO,2008e)andresource-useconflicts,whichoftenworsenintheeventofdrought.InKenya,theUnitedRepublicofTanzaniaandZimbabwe,amongothers,localcommunitiesareinvolvedinmanagingprotectedareasortourismfacilitiesforashareoftheincome.LeasingofprotectedareasformanagementhasnotyettakenholdinAfrica.

ClimatechangewillhavesignificantimpactsonAfricaneconomiesandontheforestsector.TheCleanDevelopmentMechanism(CDM)oftheKyotoProtocolandrecentinitiativesforreducingemissionsfromdeforestationandforestdegradation(REDD)openupnewfundingopportunities.Hitherto,AfricahasnotbenefitedmuchfromtheCDMorvoluntarycarbonmarkets(Box5),suggestingthatvigorouseffortsareneededtoaddresstheinadequatetechnicalcapacityandpolicyandinstitutionalconstraintsiftheregionistobeabletotakeadvantageofREDD.

AcutewaterscarcityaffectsbothruralandurbanareasinseveralAfricancountries,anditisexpectedtoworsenasdemandincreases.Poorwatershedmanagementhasresultedinheavysiltationanddiminishedstoragecapacityinmanyreservoirs.Fragmentedresponsibilitiesandconflictingusesarethemainconstraintsinwatershedmanagement,especiallyfortheseveraltransboundarywatershedsintheregion.Themainchallengesaretoadoptintegratedlanduseandtodevelopinstitutionalarrangementslinkingupstreamlandusersanddownstreamwaterusers.

Interestinamarketapproachforprovisionofwatershedservicesisjustbeginningtogrow.Theregionhasonlytwoprogrammesofpaymentforenvironmentalservices(PES)involvingwatersheds,bothinSouthAfrica,andneitherisstrictlymarket-basedastheydependongeneraltaxrevenue.Severalotherinitiativesareinthe

planningstage.Themainchallengesforsuchschemesareusers’inabilitytopayforwatershedservices,hightransactioncostsandinstitutionaldeficiencies(Dillahaet al.,2007).

DesertificationandlanddegradationaffectmostAfricancountriesandareexpectedtoworsenwithclimatechange,grazingexpansionandincreasingpressuretocultivatemarginallands.Treesplantedinwindbreaksandshelterbeltsprotectagriculturallandandinfrastructure.Addressingdesertificationandlanddegradationrequiresanintegratedapproachtoagriculture,animalhusbandryandforestry–asadoptedinregionalandsubregionalprojectssuchastheGreenWallfortheSaharaInitiative(seeUNU,2007)andtheTerrAfricapartnership(TerrAfrica,2006).AlmostallcountriesintheregionaresignatoriestotheUnitedNationsConventiontoCombatDesertification(UNCCD)andhavedevelopednationalactionplans(oftenwithexternalsupport).However,economicandinstitutionalconstraintslimittheabilityofgovernments,theprivatesectorandcommunitiestoaddressthechallengessystematically.

Nature-basedtourismandemergingprivate-sector-ledandcommunity-basedecotourisminitiatives,primarilycentredonprotectedareas,makeasignificantcontributiontoAfricaneconomies.Therichwildlifeisamajorsourceofincomeandemployment.Africahasconsiderablepotentialtotakeadvantageofgrowthinglobaltourism.However,theoveralltrendofcontinueddeforestationandforestdegradationimpliesadiminishingsupplyofforest-derivedenvironmentalservices.WhetherincreasingawarenessoftheenvironmentalservicesprovidedbyAfricanforestswillinfluencetheirconservationdependsonthecostsinvolved.

•Global total registered Clean Development

Mechanism (CDM) projects to 30 April 2008: 1 068

•CDM projects in Africa: 25 (2.3 percent of the total),

most in South Africa (where institutional capacity is

relatively well developed)

•Approved afforestation/reforestation projects in

Africa: none (in the world: one [in China])

•Africa’s share in voluntary carbon markets: 2 percent

of the volume transacted in 2007, with the highest-

priced credits because of high transaction costs

•Africa’s share in voluntary carbon markets in land

use, land-use change and forestry in 2007: 5 percent

of the global total

Source: hamilton et al., 2008.

BoX 5 carbon markets in africa: an overview

stAte oF the World’s Forests 200910

summAryTheforestsituationinAfricapresentsenormouschallenges,reflectingthelargerconstraintsoflowincome,weakpoliciesandinadequatelydevelopedinstitutions.Successstoriesexistbutremainisolatedbecauseoffundamentaleconomicandinstitutionalweaknesses.Obstaclesinclude:

• highdependenceonlandandnaturalresourcesandscantinvestmentindevelopmentofhumanresources,skillsandinfrastructure;

• thelowlevelofvalueadditionintheeconomy,includingtheforestsector;

• thevastnessoftheinformalsector,stemmingfromtheweaknessesinthepublicsectorandmarketmechanisms.

Focusingontheuniqueproductsandservicesrequiredlocallyandgloballyandstrengtheninglocalinstitutionscanbeimportantwaysofaddressingforestresourcedepletion.Sucheffortsshouldbuildonsuccessfulexperiencewithlocallybasedsustainableresourcemanagementintegratingagriculture,animalhusbandryandforestry,andtakeadvantageoflocalknowledge.Thegrowingdemandforenvironmentalservices–especiallybiodiversityandcarbonsequestration–providesaparticularopportunityforAfrica.

PArt 1 regional outlook 11

Africa

stAte oF the World’s Forests 200912

Africa

Figure 9 Extent of forest resources

ForestOther wooded landOther land cover

East AsiaSouth AsiaSoutheast AsiaOceania

Figure 8 Subregional breakdown used in this report

Note: See annex table 1 for list of countries and areas by subregion.

Asia and the Pacific

t heAsiaandthePacificregion(Figure8),consistingof47countriesandareas,ishometomorethanhalfoftheworld’spopulationandhassomeof

themostdenselypopulatedcountriesintheworld.Ithas18.6percentoftheworld’sforestareainawidearrayofecosystemsincludingtropicalandtemperateforests,coastalmangroves,mountainsanddeserts(Figure9).Rapidsocio-economicchangesintheregionarehavingprofoundimpactsonallsectors,includingforestry.Whilewoodproductsdemandisincreasing,soisthedemandforenvironmentalservicesofforests.

drivers oF ChAngedemographicsThepopulationofAsiaandthePacificisprojectedtoreach4.2billionby2020,anincreaseof600millionfrom2006(Figure10).TheannualpopulationgrowthrateinJapanisclosetozeroanddeclining,butinseveralcountries–particularlylow-incomecountries–thegrowthrateexceeds2percent.

Populationdensityintheregionvariesenormously,fromfewerthan2peoplepersquarekilometreinMongoliatomorethan1000peoplepersquarekilometreinBangladeshandtomorethan6300peoplepersquarekilometreincompletelyurbanSingapore.

TheurbanpopulationinAsiaandthePacificisexpectedtorisefrom38percentin2005to47percentin2020.ItisincreasingespeciallyrapidlyinChina–by2020,China’surbanpopulationisexpectedtohavegrownby230millionanditsruralpopulationtohavedecreasedby122millionrelativeto2005figures.SouthAsia,where65percentofthepopulationisrural,isexpectedtoremaintheleasturbanizedsubregion.

Anotherimportantdemographicchangeistheageingofthepopulation.InAustralia,Japan,Malaysia,NewZealandandThailand,morethan15percentofthepopulationisover65yearsold;inJapan,morethanone-quarterofthepopulationisover60yearsold.Thereductionintheproportionofworking-ageadultsinthesecountries,aswellasinChina(whereastrictpopulationpolicyisimplemented),willhaveimportantimplicationsforproductivityandthedemandforgoodsandservices.

PArt 1 regional outlook 13

Figure 10 Population

total asia and the Pacific east asia South asia

Southeast asia oceania

Source: un, 2008a.

5

4

3

2

1

0

Billion

1980 1985 1990 1995 2000 2005 2010 2015 2020

Figure 11 Gross domestic product

SourceS: Based on un, 2008b; World Bank, 2007a.

18

16

14

12

10

8

6

4

2

0

uS$ trillion

1980 1985 1990 1995 2000 2005 2010 2015

economyAsiaandthePacifichasthefastesteconomicgrowthofallregions.ChinaandIndia,whichaccountfortwo-thirdsoftheregion’spopulation,haveregisteredannualGDPgrowthratesof8–11percentduringthepastdecade.Whilesomeslowdownispossible,mostcountriesareexpectedtohavegrowthrateswellabovetheglobalaverage(Figure11).

However,despitenotablepovertyreductionsincethe1990s,theregionstillhas640millionpeoplelivingonlessthanUS$1perday(UNESCAP,2007).Withpovertymorepervasiveinforestedareas,manypeopledependinlargepartonforestsfortheirlivelihood.

Inmostdevelopingcountriesintheregion,themanufacturingandservicessectorsaregrowingrapidly,withacorrespondingdeclineintheshareofagricultureinincomeandemployment(UN,2006a;FAO,2007b).Thesechangesinthestructureoftheeconomywillhavedifferenteffectsonforestsandforestrydependingontheirpace:

• Severalcountriesintheregionwillremainlargelydependentonagriculture.Highpopulationgrowthandcontinueddependenceonlandwillraisethe

pressureonforests,especiallyindenselypopulatedcountries.Effortstoimproveagricultureinresponsetorecentlyescalatingfoodpricescouldincreasetheimpactonforests.

• Incountrieswhereindustrializationisreducingthepaceofagriculturalexpansion,otherfactorssuchasmining,infrastructuredevelopmentandurbanization,aswellasplantationcrops,arebecomingimportantcausesofforestclearance.

• Somecountrieshavebecome,orarebecoming,knowledgeeconomies,largelyfocusedontechnologyandservices.Withhighincomes,mostoftheprimarycommoditiesareimportedanddependenceonforestsisreduced.Forestsarethenusedprimarilyfortheprovisionofenvironmentalservices.

Globalizationhasplayedanimportantroleintheregion’srapideconomicgrowthandwillbecomemorepronouncedinthecomingyears,withcontinuedimpactontheforestsector,includingincreasedtransnationalinvestments.Relativepoliticalstability,largemarkets,highinvestmentsinhumanresources,regionalandsubregionaltradeandeconomiccooperationagreements,improved

total asia and the Pacific east asia South asia

Southeast asia oceania

stAte oF the World’s Forests 200914

transportationinfrastructureandrapiddevelopmentofinformationandcommunicationtechnologieshaveallpromotedglobalization.

Policies and institutionsImportantchangesunderwayinthepolicyandinstitutionalarenainAsiaandthePacificinclude:

• changesinpoliciesandlegislationenablinggreaterinvolvementofdiversestakeholdersinforestry,especiallythroughprivatizationandcommunityparticipation,includingtherestorationofrightstoindigenouscommunities(Box6);

• improvementintenureconditionsprovidingmoreincentiveforlandownerstogrowtrees;

• increasedcorporateinvestmentsinforestry,oftenthroughpartnerships;

• greaterinvolvementofcivil-societyorganizationsinpolicyformulation,forestmanagement,research,extensionandawarenessgeneration;

• weakeningoftheauthorityofpublicforestryagencies,largelybecauseoftheemergenceofotherplayers.

Governanceproblemsencumbertheforestsectorinsomecountries,oftenthosewiththemostforests.Combatingcorruptionandillegallogginghasbeenafocusofrecentnationalandinternationalefforts(Box7).Conflictsdisruptforestmanagementinseveralcountries,andthesecouldescalateaspressuresonnaturalresourcesincrease,especiallyifeffectiveinstitutionalarrangementsarenotinplacetoresolvethem.

science and technologyTheregionhasbeenattheforefrontofthedevelopmentandadoptionofgreenrevolutiontechnologies,whichhaveslowedorevenreversedthehorizontalexpansionof

agriculture.Technologicaladvanceshaveenhancedtheregion’scompetitivenessinthemanufacturingandservicessectors.Investmentsinbiotechnology,nanotechnology,informationandcommunicationsandalternativeenergytechnologieswillallhaveimportantimpactsonforestry.However,differencesintheadoptionoftechnologieswillpersistamongcountries,sectorsandsubsectors.

overAll sCenArioTheAsiaandthePacificregionisextremelydiverse.Countries,orevenareaswithincountries,arelikelytofollowoneofthreemaindevelopmentpaths.

Intherapidlyemergingindustrialeconomies,continuedindustrializationwillresultinanexpandedmiddleclass.Aconsequentincreaseinthedemandforfood,fuel,fibreandenvironmentalserviceswillexerttremendouspressureonthenatural-resource-richcountriesinandoutsidetheregion.Agriculturalexpansionwillslow;non-agriculturallandusessuchasminingandurbanexpansionmaycontinuetoplacepressureonforests.

Intheagrariansocieties,agriculturewillremainthemainstayoflivelihoodsandmayevenexpandinthecontextofhighpopulationgrowthrates.Increasingglobalandregionaldemandforfood,fuelandfibre,especiallyfromrapidlyindustrializingcountries,couldbeeitheranopportunityorachallengedependingonthestateofgovernanceandinstitutionaldevelopment.

Inthehigh-income,postindustrialsocieties,growthwillbebasedontechnologicallyadvancedmanufacturing

Of the estimated 210 million to 260 million indigenous

people in Asia and the Pacific, about 60 million are

forest-dependent. Many countries have policies and

laws to remedy their marginalization (e.g. Australia, India,

Malaysia, New Zealand, Papua New Guinea and the

Philippines). For example, the Scheduled Tribes and Other

Traditional Forest Dwellers (Recognition of Forest Rights)

Act enacted by India in 2006 recognizes the rights of

traditional forest-dwelling communities, including title over

land that they have been cultivating (up to a maximum of

4 ha per family) and the right to collect and use non-wood

forest products.

Source: asia forest network, 2008.

BoX 6 restoration of rights to indigenous communities

In Asia, multilateral arrangements on forest law

enforcement and governance (FLEG) target explicit

improvements in reducing corruption and illegal

activities in, and associated with, forests and forestry.

The East Asian FLEG process emerged from a series

of multistakeholder consultations in 2001. A ministerial

FLEG meeting held in Bali, Indonesia, in 2001 affirmed

commitments to eliminate illegal logging and associated

illegal trade and corruption. It also developed a

comprehensive list of actions – encompassing political,

legislative, judicial, institutional and administrative actions

as well as associated research, advocacy, information

disclosure and sharing of knowledge and expertise – to be

undertaken nationally and internationally. However, while

the FLEG process has helped to draw attention to forest

governance, it is difficult to ascertain its impacts on the

ground.

BoX 7 forest law enforcement and governance in asia

PArt 1 regional outlook 15

Asia and the Pacific

andtheprovisionofhigh-qualityservices.Populationswillberelativelystable(andinsomecasesdeclining)andtechnicallyskilled.Improvingthequalityoftheenvironmentwillbeamajorconcern,andhighincomewillprovidethenecessarymeanstodoso.

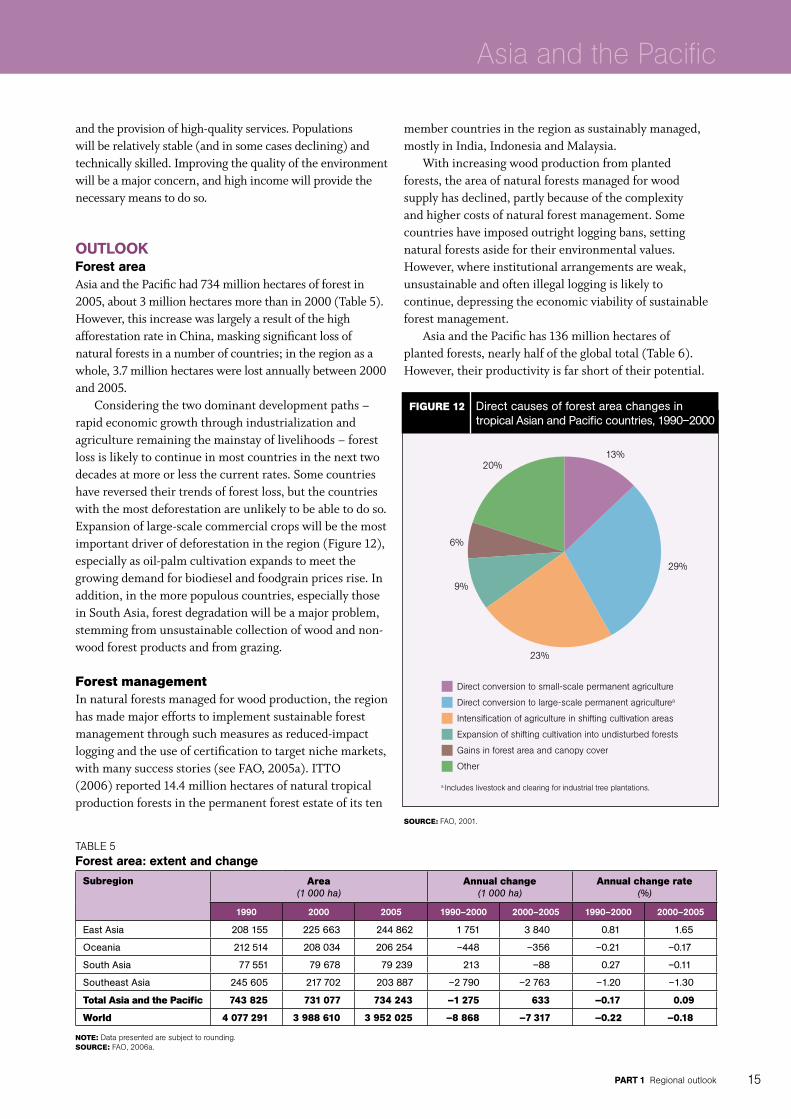

outlookForest areaAsiaandthePacifichad734millionhectaresofforestin2005,about3millionhectaresmorethanin2000(Table5).However,thisincreasewaslargelyaresultofthehighafforestationrateinChina,maskingsignificantlossofnaturalforestsinanumberofcountries;intheregionasawhole,3.7millionhectareswerelostannuallybetween2000and2005.

Consideringthetwodominantdevelopmentpaths–rapideconomicgrowththroughindustrializationandagricultureremainingthemainstayoflivelihoods–forestlossislikelytocontinueinmostcountriesinthenexttwodecadesatmoreorlessthecurrentrates.Somecountrieshavereversedtheirtrendsofforestloss,butthecountrieswiththemostdeforestationareunlikelytobeabletodoso.Expansionoflarge-scalecommercialcropswillbethemostimportantdriverofdeforestationintheregion(Figure12),especiallyasoil-palmcultivationexpandstomeetthegrowingdemandforbiodieselandfoodgrainpricesrise.Inaddition,inthemorepopulouscountries,especiallythoseinSouthAsia,forestdegradationwillbeamajorproblem,stemmingfromunsustainablecollectionofwoodandnon-woodforestproductsandfromgrazing.

Forest managementInnaturalforestsmanagedforwoodproduction,theregionhasmademajoreffortstoimplementsustainableforestmanagementthroughsuchmeasuresasreduced-impactloggingandtheuseofcertificationtotargetnichemarkets,withmanysuccessstories(seeFAO,2005a).ITTO(2006)reported14.4millionhectaresofnaturaltropicalproductionforestsinthepermanentforestestateofitsten

membercountriesintheregionassustainablymanaged,mostlyinIndia,IndonesiaandMalaysia.

Withincreasingwoodproductionfromplantedforests,theareaofnaturalforestsmanagedforwoodsupplyhasdeclined,partlybecauseofthecomplexityandhighercostsofnaturalforestmanagement.Somecountrieshaveimposedoutrightloggingbans,settingnaturalforestsasidefortheirenvironmentalvalues.However,whereinstitutionalarrangementsareweak,unsustainableandoftenillegalloggingislikelytocontinue,depressingtheeconomicviabilityofsustainableforestmanagement.

AsiaandthePacifichas136millionhectaresofplantedforests,nearlyhalfoftheglobaltotal(Table6).However,theirproductivityisfarshortoftheirpotential.

taBle 5Forest area: extent and change

Subregion Area(1 000 ha)

Annual change(1 000 ha)

Annual change rate(%)

1990 2000 2005 1990–2000 2000–2005 1990–2000 2000–2005

East Asia 208 155 225 663 244 862 1 751 3 840 0.81 1.65

Oceania 212 514 208 034 206 254 –448 –356 –0.21 –0.17

South Asia 77 551 79 678 79 239 213 –88 0.27 –0.11

Southeast Asia 245 605 217 702 203 887 –2 790 –2 763 –1.20 –1.30

total Asia and the Pacific 743 825 731 077 734 243 –1 275 633 –0.17 0.09

World 4 077 291 3 988 610 3 952 025 –8 868 –7 317 –0.22 –0.18

Note: data presented are subject to rounding.Source: fao, 2006a.

29%

Figure 12 Direct causes of forest area changes in tropical Asian and Pacific countries, 1990–2000

direct conversion to small-scale permanent agriculture

direct conversion to large-scale permanent agriculturea

intensification of agriculture in shifting cultivation areas

expansion of shifting cultivation into undisturbed forests

gains in forest area and canopy cover

other

Source: fao, 2001.

13%20%

23%

9%

6%

a includes livestock and clearing for industrial tree plantations.

stAte oF the World’s Forests 200916

MostoftheplantedforestsareinAustralia,China,India,Indonesia,NewZealand,thePhilippines,ThailandandVietNam.Investmentsinplantedforests,especiallybytheprivatesector,haveincreasedinthepasttwodecades.Asmoreofthenaturalforestsareexcludedfromproduction,plantedforestsarebecomingthemainstayofwoodproductionintheregion.Therehasalsobeensubstantialinvestmentinplantingforprotectivepurposes;almostone-thirdoftheplantedforestsintheregionhavebeenestablishedforenvironmentalprotection,mostlyinChinaandIndia(FAO, 2006b).

However,thescopeforexpansionofplantedforestsforproductionislimited,especiallywithcurrentwoodprices.Wateravailabilityisalreadyamajorconstraintandwillbemoreproblematicinthefuture.Thecostsofproductivelandaresteep,inflatedbyhighagriculturalpricesanddemandforbiofuelfeedstocks.Althoughmarginallandisextensivelyavailable,itrequireshighinvestments.Thus,futurewoodsupplywilldependonimprovingtheproductivityofexistingplantedforestsandonencouragingfarmforestryasanimportantsourceofwood,includingforlarge-scaleindustrialprocessing(Box8).

Wood products: production, consumption and tradeRegionally,largeincreasesinindustrialroundwoodconsumptionandproductionareprojectedto2020(Table7).China,Indiaandotheremergingeconomieswillaccountformuchofthegrowthinconsumption.Trendsinindustrialroundwoodimportsareincontrastingdirections.Netimportstotheadvancedindustrializedeconomies(especiallyJapan)have

declined,whilethosetotheemergingeconomies(ChinaandIndia)havegreatlyincreasedasaresultofsurgingdomesticdemandanddeclinesindomesticsupplycausedbyloggingbans.

Growthindemandforwoodproducts(Figure13)willlargelybeacontinuationofrecenttrendsandwillbesimilartotheglobaloutlook(seePart2),withsubstantialexpansionexpectedintheconsumptionofwood-basedpanelsandpaperandpaperboard,andmoremodestgrowthinsawnwoodconsumption.Sawnwoodandplywoodwillcontinuetoaccountformostoftheconsumptionofsolidwoodproducts,althoughsomesubstitutionof

taBle 6Planted forest area change

Year extent of planted forestsglobal total Annual change in

Asia and the PacificProductive Protective total

(million ha)

1990 67 36 103 209 –

2000 78 41 119 247 1.4

2005 90 46 136 271 2.8

Source: fao, 2006b.

taBle 7Production and consumption of wood products

Year industrial roundwood (million m3)

Sawnwood (million m3)

Wood-based panels (million m3)

Paper and paperboard (million tonnes)

Production Consumption Production Consumption Production Consumption Production Consumption

2005 273 316 71 84 81 79 121 128

2020 439 498 83 97 160 161 227 234

2030 500 563 97 113 231 236 324 329

Source: fao, 2008c.

Trees are an integral part of homestead farming systems

in many Asian countries, particularly Bangladesh,

Indonesia, the Philippines, Sri Lanka and certain parts of

India. Past investments in social or community forestry

have helped to make farms important sources of wood

supply. Several industries have established partnership

arrangements with farmers to source wood supplies from

farms. Farm forestry is expected to continue to expand as

a result of:

•improving security of land tenure;

•declining profitability of agriculture, which

encourages farmers to invest in forest crops (which

are less labour-intensive than agriculture);

•increasing demand for wood products and

consequent increases in their prices, making farm

forestry more profitable.

BoX 8 farm forestry

PArt 1 regional outlook 17

Asia and the Pacific

reconstitutedpanelsforsawnwoodandplywoodisexpected.Consumptionofpaperandpaperboardisexpectedtogrowmarkedly,andrecoveredpaperandwoodproducedinplantedforestsoffast-growingspecieswillprovidemostofthefibreusedintheirproduction.

Rapideconomicgrowthhasboostedtheregion’sshareintheglobaltradeinwoodproducts,especiallyinthepasttwodecades.Risingprosperitygenerallyimplieshigherdisposableincome,increasingthedemandforproductsandconsequentlyimports(Figure14).Chinaaccountsforalargepartofthegrowthintrade;itstotalwoodproductsimportsrosefromUS$5.4billionin1990toUS$20.6billionin2006.India’swoodproductsimportshavealsoincreasednotably,fromaboutUS$587millionin1990toUS$2.4billionin2006.China’srecoveredpaperimports(mainlyfromtheUnitedStatesofAmerica)grewfrom5milliontonnesin2000to16.7milliontonnesin2006.

Theregionisalsobecominganimportantexporterofwoodproducts,withanincreasingshareofhigh-valueproducts.MostremarkableistheemergenceofChinaastheleadingglobalexporteroffurniture,overtakingsomeofthetraditionalfurnitureproducersinEurope.Since2005,VietNamhasalsoemergedasamainexporterofwoodenfurniture.

Thetrendsindemandandtradehaveseveralinterestingimplicationsforthefutureofforestsintheregion:

• Theboomindemandcreatesopportunitiesforforestedcountries,butalsochallengesforsustainableforestmanagementandcontrolofillegallogging,

especiallyincountrieswithweakinstitutionsandpoorgovernance.

• Growthintrademayhaveimpactsonforestmanagementoutsidetheregion.

• Someofthedemandmaybemetthroughimprovementsinefficiency.

WoodfuelAlmostthree-quartersofthewoodproducedinAsiaandthePacificisburnedasfuel.InSouthandSoutheastAsia,woodfuel’sshareintotalwoodproductionis93and72percent,respectively.Incontrast,woodfuelaccountsforlessthan1percentofthewoodproducedinJapan.

Woodfuelconsumptionintheregiondeclinedbetween1980and2006fromabout894millionto794millioncubicmetres.SouthAsiawastheonlysubregionthatregisteredanincrease.

Asincomesandurbanizationincrease,woodfuelwillbesubstitutedwithelectricity,keroseneandgas.ThisisalreadyevidentinmostofAsiaandthePacific,althoughtherearesomedifferencesinthepredictedtrendsamongsubregions(Figure15).Forexample,SouthAsianwoodfuelconsumptionisexpectedtogrowandthenstarttodeclinefromaround2015.However,risingfossilfuelpricescouldleadtoadifferentscenario,andthepredictedfuelswitchingmaynottakeplace.Insomecases,therecouldbeashiftbacktowoodfuel,withconsequencesofincreasedcollectionandforestdegradation.

Recentoilpriceincreaseshavealreadyledtosubstantialpublicandprivateinvestmentsinbiofuelproduction.Oil-yieldingspeciessuchasJatropha curcasarebeingplantedondegradedlandforbiodieselproduction.Asbiodieselismainlyusedonlyintransportation,this

Figure 13 Raw material demand

Source: fao, 2008c.

2 000

1 800

1 600

1 400

1 200

1 000

800

600

400

200

0

Million m3 wood raw-material equivalent

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Paper and paperboard

net wood pulp exports (net exporters only)

Particleboard and fibreboard

Sawnwood and plywood

other industrial roundwood

Figure 14 Wood products imports

asia and the Pacific other regions

Source: fao, 2008a.

400

350

300

250

200

150

100

50

0

uS$ billion

1965 1970 1975 1980 1985 1990 1995 2000 2005

stAte oF the World’s Forests 200918

developmentmaynotalleviatethetraditionalwoodfuelproblem.

Ifcellulosicbiofuelproductionbecomescommerciallyviable,thedemandforwoodasasourceofenergywillincreasesignificantly.

non-wood forest productsNon-woodforestproductsfromtheregionarediverse–food,medicines,fibres,gums,resins,cosmeticsandhandicrafts.Mostareusedforsubsistence,collectedandconsumedlocallyortradedinlimitedquantities.Morethan150NWFPsfromAsiaandthePacificaretradedinternationally,althoughapartfrombambooandrattanthequantitiesareusuallysmall.Increasinginterestin“naturalproducts”,owingtotheirperceivedhealthandenvironmentalbenefits,isdrawingattentiontothemultitudeofNWFPscommonlyusedbylocalcommunities.

TheconsumptionofmanysubsistenceNWFPsislikelytofallinthelongterm becauseof:

• decliningsupplyfromthewild,largelybecauseofreductioninforestcoverandpoormanagement;

• developmentofsyntheticmaterialsandtheirsubstitutionforNWFPsasaresultofincreasingincomesandconsumeraccess;

• thedecreasingattractivenessofNWFPcollectionrelativetomoreremunerativeandlessarduousoccupationsavailablewhenincomesrise.

SeveralNWFPs–especiallymedicinalplants–havebeencommercializedandaretradednationallyandglobally.Increasingdemandhasledtotheirintensivecollectionandtodepletionofwildstock.Productsfromopen-accesspublicforestsareparticularlyvulnerable.Inmanycases,collectionandtradeareinformal,offeringminimalfinancialbenefitstocollectors.