alamos corp presentation nov 3 2017 final (1)

TRANSCRIPT

November 2017 Corporate Presentation

2

Cautionary Notes

This presentation, the information contained herein, any other materials provided in connection with this presentation and any oral remarks accompanying this presentation (collectively, this “Presentation”) has been prepared by Alamos Gold Inc. (“Alamos”) solely for information purposes concerning a potential transaction (a “Potential Transaction”) involving Alamos and Richmont Mines Inc. (“Richmont”). No Stock exchange, securities commission or other regulatory authority has approved or disapproved of the information contained herein. This presentation does not constitute an offering of securities and the information contained herein is subject to the information contained in the Company’s continuous disclosure documents at www.sedar.com.

Cautionary NotesCertain statements in this presentation are “forward-looking statements”, including within the meaning of applicable laws. All statements other than statements of historical fact included in this presentation, including, without limitation, statements regarding the timing and closing of the Proposed Transaction, statements regarding synergies resulting from the Proposed Transaction, statements regarding the effect of the Proposed Transaction on Alamos’ net asset value, operating cash flow, free cash flow, forecast gold production, reserves, resources, gold grades, recoveries, waste-to-ore ratios, total cash cost, all-in sustaining costs, debt levels and future plans and objectives of Alamos are forward-looking statements based on forecasts of future operational or financial results, estimates of amounts not yet determinable and assumptions of management that involve various risks and uncertainties. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results “may”, “could”, “would”, “might”, or “will” be taken, occur or be achieved) are not statements of historical fact and may be “forward-looking statements.” Alamos cautions that forward-looking information involves known and unknown risks, uncertainties and other factors that may cause Alamos’ actual results, performance or achievements to be materially different from those expressed or implied by such information, including, but not limited to, that the Proposed Transaction is completed on terms and timeframe contemplated; failure to obtain shareholder approval of Alamos or Richmont; failure to obtain the necessary regulatory and other approvals; conditions to the Proposed Transaction may not be satisfied; anticipated synergies and other benefits of the Proposed Transaction may not be realized; gold and silver price volatility; fluctuations in foreign exchange rates and interest rates; the impact of any hedging activities; discrepancies between actual and estimated production, between actual and estimated reserves and resources or between actual and estimated metallurgical recoveries; costs of production; capital expenditure requirements; the costs and timing of construction and development of new deposits; and the success of exploration and permitting activities. In addition, the factors described or referred to in the section entitled “Risk Factors” in Alamos’ Annual Information Form for the year ended December 31, 2016, which is available on the SEDAR website at www.sedar.com, should be reviewed in conjunction with the information found in thispresentation. Although Alamos has attempted to identify important factors that could cause actual results, performance or achievements to differ materially from those contained in forward-looking information, there can be other factors that cause results,performance or achievements not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate or that management’s expectations or estimates of future developments, circumstances or results will materialize. Accordingly, readers should not place undue reliance on forward-looking information.

Market data and other statistical information used throughout this Presentation are based on internal company research, independent industry publications, government publications, reports by market research firms or their published independent sources. Industry publications, governmental publications, market research surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable. Although Alamos believes such information is accurate and reliable, it has not independently verified any of the data from third party sources cited or used for our management’s industry estimates, nor has Alamos ascertained the underlying economic assumptions relied upon therein. While Alamos believes internal company estimates are reliable, such estimates have not been verified by any independent sources, and Alamos makes no representations as to the accuracy of such estimates.

Note to U.S. InvestorsAlamos prepares its disclosure in accordance with the requirements of securities laws in effect in Canada, which differ from the requirements of U.S. securities laws. Terms relating to mineral resources in this presentation are defined in accordance with National Instrument 43 101 Standards of Disclosure for Mineral Projects under the guidelines set out in the Canadian Institute of Mining, Metallurgy, and Petroleum Standards on Mineral Resources and Mineral Reserves. The Unites States Securities and Exchange Commission (the “SEC”) permits mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. Alamos may use certain terms, such as “measured mineral resources”, “indicated mineral resources”, “inferred mineral resources” and “probable mineral reserves” that the SEC does not recognize (these terms may be used in this presentation and are included in the public filings of Alamos, which have been filed with the SEC and the securities commissions or similar authorities in Canada).

Cautionary non-GAAP Measures and Additional GAAP Measures

Note that for purposes of this section, GAAP refers to IFRS. The Company believes that investors use certain non-GAAP and additional GAAP measures as indicators to assess gold mining companies. They are intended to provide additional

information and should not be considered in isolation or as a substitute for measures of performance prepared with GAAP.

“Cash flow from operating activities before changes in non-cash working capital” is a non-GAAP performance measure that could provide an indication of the Company’s ability to generate cash flows from operations, and is calculated by adding

back the change in non-cash working capital to “Cash provided by (used in) operating activities” as presented on the Company’s consolidated statements of cash flows. “Free cash flow” is a non-GAAP performance measure that is calculated as

cash flows from operations net of cash flows invested in mineral property, plant and equipment and exploration and evaluation assets as presented on the Company’s consolidated statements of cash flows and that would provide an indication of

the Company’s ability to generate cash flows from its mineral projects. “Mine site free cash flow” is a non-GAAP measure which includes cash flow from operating activities at, less capital expenditures at each mine site. Return on Equity is

defined as Earnings from Continuing Operations divided by the average Total Equity for the current and previous year. “Mining cost per tonne of ore” and “Cost per tonne of ore” are non-GAAP performance measures that could provide an

indication of the mining and processing efficiency and effectiveness of the mine. These measures are calculated by dividing the relevant mining and processing costs and total costs by the tonnes of ore processed in the period. “Cost per tonne

of ore” is usually affected by operating efficiencies and waste-to-ore ratios in the period. “Total cash costs per ounce”, “all-in sustaining costs per ounce”, and “mine-site all-in sustaining costs” as used in this analysis are non-GAAP terms

typically used by gold mining companies to assess the level of gross margin available to the Company by subtracting these costs from the unit price realized during the period. These non-GAAP terms are also used to assess the ability of a

mining company to generate cash flow from operations. There may be some variation in the method of computation of these metrics as determined by the Company compared with other mining companies. In this context, “total cash costs”

reflects mining and processing costs allocated from in-process and dore inventory associated and associated royalties with ounces of gold sold in the period. Total cash costs per ounce are exclusive of exploration costs. “All-in sustaining costs

per ounce” include total cash costs, exploration, corporate and administrative, share based compensation and sustaining capital costs. “Mine-site all-in sustaining costs” include total cash costs, exploration, and sustaining capital costs for the

mine-site, but exclude an allocation of corporate and administrative and share based compensation.

Additional GAAP measures that are presented on the face of the Company’s consolidated statements of comprehensive income and are not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather

should be evaluated in conjunction with such IFRS measures. This includes “Earnings from operations”, which is intended to provide an indication of the Company’s operating performance, and represents the amount of earnings before net

finance income/expense, foreign exchange gain/loss, other income/loss, and income tax expense. Non-GAAP and additional GAAP measures do not have a standardized meaning prescribed under IFRS and therefore may not be comparable to

similar measures presented by other companies. A reconciliation of historical non-GAAP and additional GAAP measures are available at www.alamosgold.com.

Technical Information

Chris Bostwick, FAusIMM, Alamos Gold’s Vice President, Technical Services, has reviewed and approved the scientific and technical information contained in this presentation. Chris Bostwick is a Qualified Person within the meaning of Canadian Securities Administrator’s National Instrument 43-101 (“NI 43-101”). The Qualified Persons for the National Instrument 43-101 compliant mineral reserve and resource estimates are detailed in the tables in the appendix of this presentation.

All figures in US$ unless otherwise indicated.

3

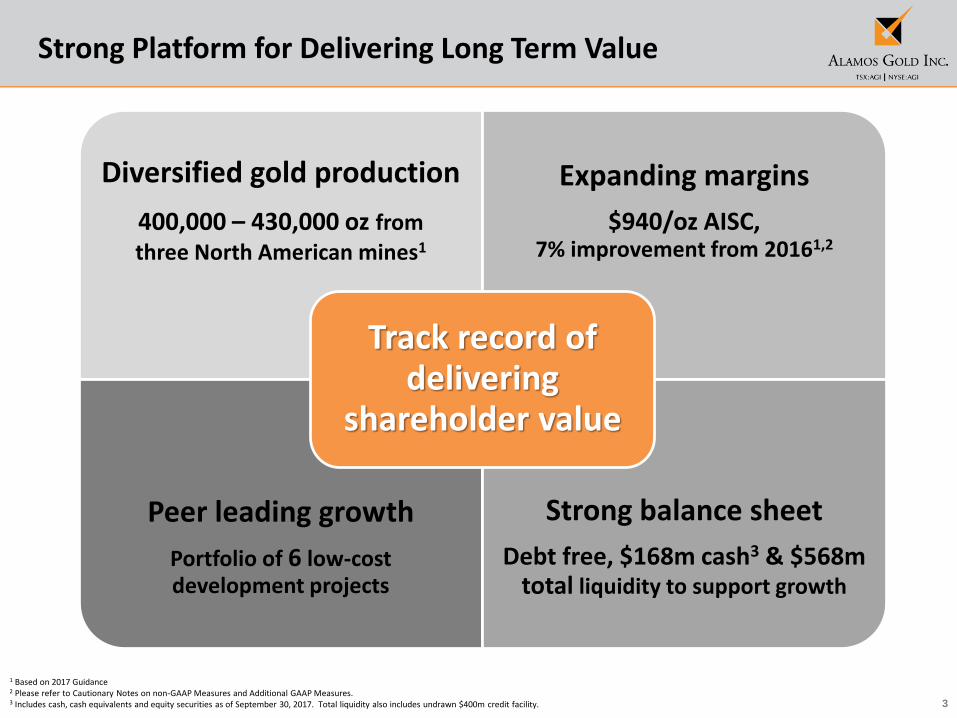

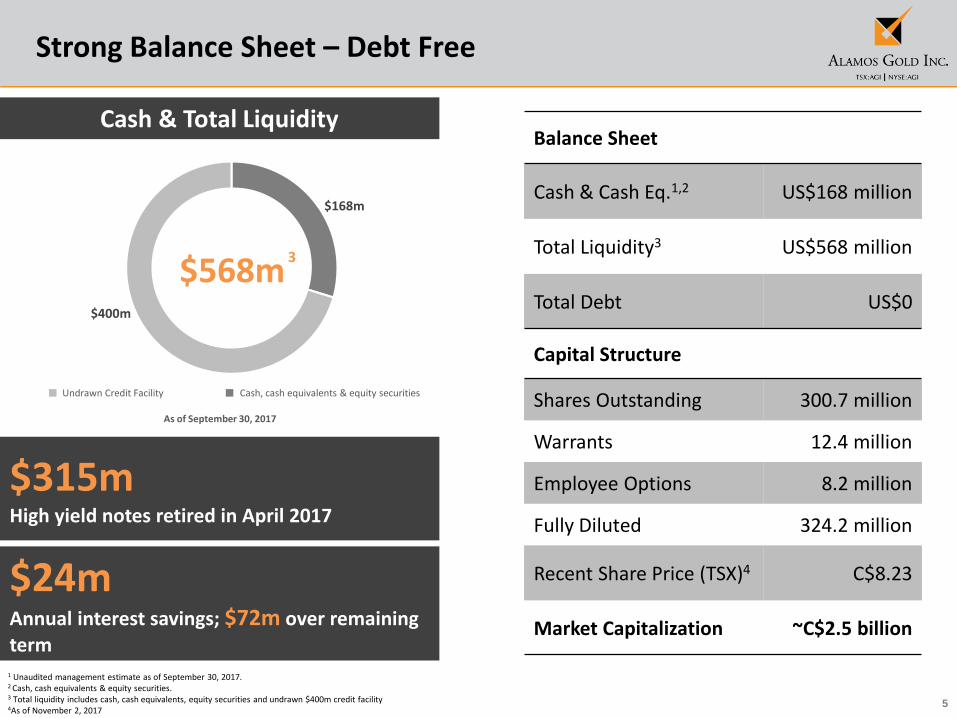

1 Based on 2017 Guidance2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Includes cash, cash equivalents and equity securities as of September 30, 2017. Total liquidity also includes undrawn $400m credit facility.

Strong Platform for Delivering Long Term Value

Diversified gold production

400,000 – 430,000 oz from three North American mines1

Expanding margins

$940/oz AISC, 7% improvement from 20161,2

Peer leading growth

Portfolio of 6 low-cost development projects

Strong balance sheet

Debt free, $168m cash3 & $568m total liquidity to support growth

Track record of delivering

shareholder value

42015A 2016A 2017E

$1,091$1,010

$940

2015A 2016A 2017E

2015A 2016A 2017E

$1,241

$1,103$1,065

2015A 2016A 2017E

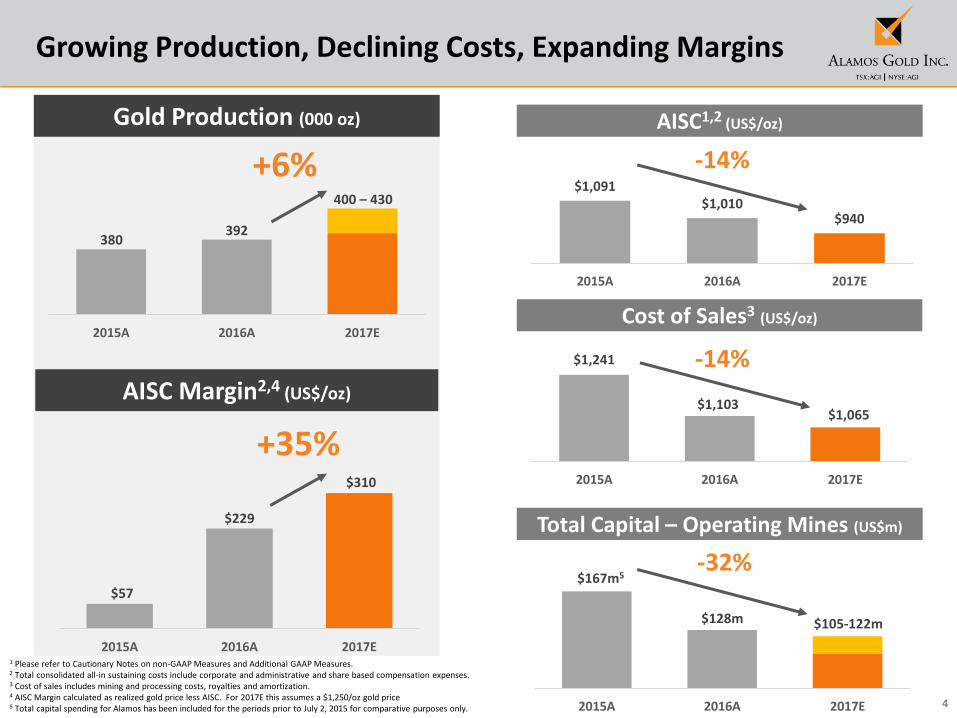

Growing Production, Declining Costs, Expanding Margins

Gold Production (000 oz) AISC1,2 (US$/oz)

-14%

Total Capital – Operating Mines (US$m)

$128m $105-122m

Cost of Sales3 (US$/oz)

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures. 2 Total consolidated all-in sustaining costs include corporate and administrative and share based compensation expenses. 3 Cost of sales includes mining and processing costs, royalties and amortization.4 AISC Margin calculated as realized gold price less AISC. For 2017E this assumes a $1,250/oz gold price5 Total capital spending for Alamos has been included for the periods prior to July 2, 2015 for comparative purposes only.

392

400 – 430

+6%

380

$167m5

$57

$229

$310

2015A 2016A 2017E

+35%

AISC Margin2,4 (US$/oz)

-14%

-32%

5

$315m High yield notes retired in April 2017

Strong Balance Sheet – Debt Free

1 Unaudited management estimate as of September 30, 2017.2 Cash, cash equivalents & equity securities.3 Total liquidity includes cash, cash equivalents, equity securities and undrawn $400m credit facility4As of November 2, 2017

Balance Sheet

Cash & Cash Eq.1,2 US$168 million

Total Liquidity3 US$568 million

Total Debt US$0

Capital Structure

Shares Outstanding 300.7 million

Warrants 12.4 million

Employee Options 8.2 million

Fully Diluted 324.2 million

Recent Share Price (TSX)4 C$8.23

Market Capitalization ~C$2.5 billion

$24m Annual interest savings; $72m over remaining term

$168m

$400m

$568m

As of September 30, 2017

Cash & Total Liquidity

Cash, cash equivalents & equity securitiesUndrawn Credit Facility

3

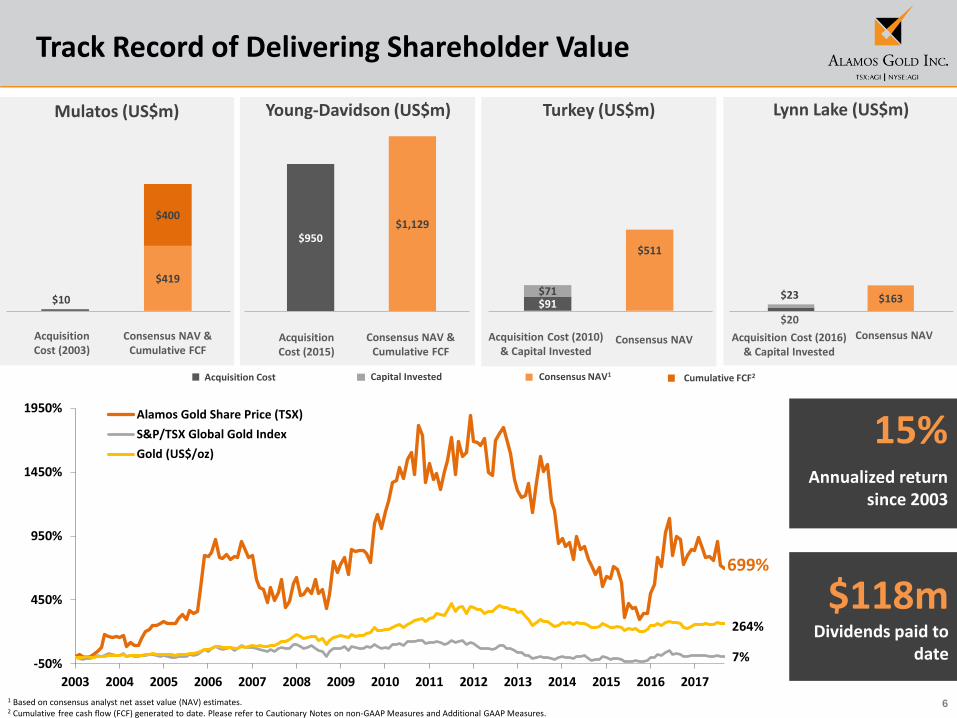

6

699%

7%

264%

-50%

450%

950%

1450%

1950%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Alamos Gold Share Price (TSX)

S&P/TSX Global Gold Index

Gold (US$/oz)

$91

$511

$71$10

$419

$400

$950$1,129

$163

Track Record of Delivering Shareholder Value

1 Based on consensus analyst net asset value (NAV) estimates.2 Cumulative free cash flow (FCF) generated to date. Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

15%Annualized return

since 2003

$118m Dividends paid to

date

Mulatos (US$m) Turkey (US$m)Young-Davidson (US$m) Lynn Lake (US$m)

Acquisition Cost (2003)

Acquisition Cost (2015)

Acquisition Cost (2010) & Capital Invested

Acquisition Cost (2016) & Capital Invested

Consensus NAV & Cumulative FCF

Consensus NAV Consensus NAV

$20

$23

Consensus NAV & Cumulative FCF

Capital Invested Consensus NAV1 Cumulative FCF2Acquisition Cost

7

Richmont Mines Acquisition Highlights

Acquisition of a high quality,

free cash flowing asset in a

world class jurisdiction

• Island Gold is a long-life, high-grade, low-cost underground gold mine located in Ontario, Canada

• Current expansion is anticipated to drive production higher, costs lower & further

free cash flow growth

• Significant exploration potential to extend mine life beyond current resource

Strengthens core portfolio;

solidifies intermediate

producer position

• Adds a third core, long-life producing asset to further diversify asset base

• De-risks portfolio & improves already low risk profile with increased exposure to Canada

Stronger cash flow generation

to support growth

• Immediate earnings & cash flow accretion; stronger operating & free cash flow profile

• Stronger balance sheet & financial flexibility with US$229 million cash1 & no debt

• Better positioned to internally fund portfolio of growth projects

Aligns well with Alamos’ core

competencies• Synergies with a second underground gold mine in Ontario

Enhanced production growth & cost profile

• Island Gold provides near term production growth while lowering the combined

cost profile

Increases scale and capital

markets profile

• Elevates Alamos to a >500 koz per year producer with a peer leading growth profile

• Establishes Alamos as top 10 Canadian and North American gold producer2

1 Cash balance shown as at June 30, 2017 and includes equity securities.2 Based on Wood Mackenzie 2018E estimates for Island Gold and estimates of corporate production in Canada, the United States, and Mexico.

8

35 42

52

82

95 $1,452

$1,192 $1,136

$745 $723

2013A 2014A 2015A 2016A 2017E

Ounces Sold (koz) AISC (US$/oz)

Island Gold Mine Overview

Source: Company filings, SNL, street research1 Ore processed averaged 933 tpd in H1 2017.2 Expansion capital of C$28.2 mm converted at 0.80x US$ per C$.

• High grade underground gold mine located northeast of Wawa, Ontario in a well established gold district

• Began commercial production in October 2007

• Ore currently processed at rate of ~930 tpd1

• Expansion underway to 1,100 tpd as detailed in May 2017 PEA

– Annual production expected to increase to average 125 koz at mine-site AISC of US$550/oz for the period of 2019-2024

– Minimal incremental capital of US$23 mm2 with mill expansion expected to be completed in latter part of 2018

• Upside potential reflecting inclusion of all mineral resources and exploration potential laterally and at depth

Asset Description

Growing Production; Declining Costs

Highly Productive Gold Mining District

4

0 50 100km

Marathon

Wawa

Hearst

Timmins

Iroquois Falls

Smooth Rock Falls

Eagle River, Wesdome

Borden, Goldcorp

Island Gold, Richmont

Magino, Argonaut

Cote, IAMGOLD

Black Fox, McEwen

Timmins West, Tahoe

Holloway, Kirkland Lake

Porcupine, Goldcorp

Bell Creek, Tahoe

Young Davidson, Alamos

Macassa, Kirkland Lake

Holt, Kirkland Lake

Lake Superior

ONTARIO

Hemlo, Barrick

144

101

17

17

11

101

Mine/ProjectCity

Dome Mine, Goldcorp

Hoyle Pond, Goldcorp

Cochrane

Pamour (PJV), Goldcorp

Taylor, Kirkland Lake

Detour Lake Mine, Detour Gold

Recent Operating Performance

Gold Reserves & ResourcesTonnes (000)

Grade (g/t Au)

oz Au(000)

P&P Reserves 2,551 9.17 752M&I Resources 479 5.94 91Inferred Resources 3,042 10.18 996

Q1/17A Q2/17A Q3/17AQ3 YTD

20172017E6

Gold Production (koz) 23.8 26.1 26.7 76.5 87-93Total Cash Costs7 (US$/oz) $504 $431 $532 $487 $550-$590Mine-site AISC7 (US$/oz) $640 $503 $725-$765Sustaining Capital (US$ mm) $3.1 $2.1 $15-$17Expansion Capital (US$ mm) $4.5 $4.4 $25-$27Exploration (US$ mm) $2.8 $3.6 $11-$12RIC Corporate FCF5 (US$ mm) $0.4 $14.3

3 Since 1985.4 Based on analyst consensus estimates.

5 Richmont consolidated corporate OCF less capex.6 Richmont 2017E guidance.

>25 Moz gold produced3

>35 Moz in defined reserves

7 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

9

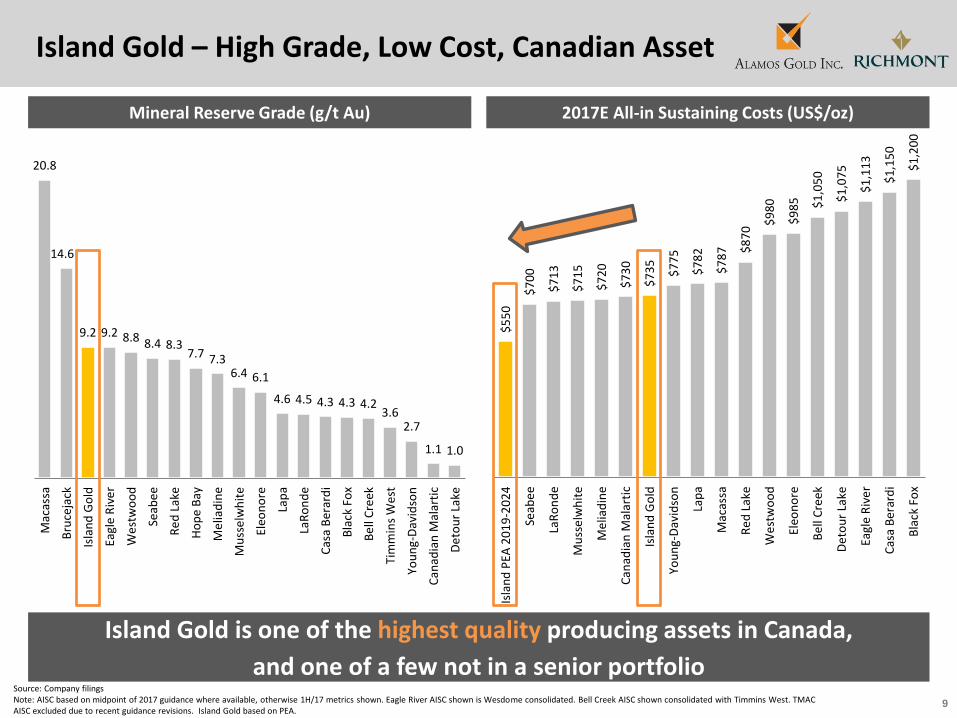

20.8

14.6

9.2 9.2 8.8 8.4 8.3 7.7 7.3

6.4 6.1

4.6 4.5 4.3 4.3 4.2 3.6

2.7

1.1 1.0

Mac

assa

Bru

ceja

ck

Isla

nd

Go

ld

Eagl

e R

ive

r

We

stw

oo

d

Seab

ee

Re

d L

ake

Ho

pe

Bay

Me

liad

ine

Mu

sse

lwh

ite

Eleo

no

re

Lap

a

LaR

on

de

Cas

a B

erar

di

Bla

ck F

ox

Be

ll C

reek

Tim

min

s W

est

You

ng-

Dav

idso

n

Can

adia

n M

alar

tic

De

tou

r La

ke

$7

00

$7

13

$7

15

$7

20

$7

30

$7

75

$7

82

$7

87

$8

70

$9

80

$9

85

$1

,05

0

$1

,07

5

$1

,11

3

$1

,15

0

$1

,20

0

$5

50

$7

35

Isla

nd

PEA

20

19

-20

24

Seab

ee

LaR

on

de

Mu

sse

lwh

ite

Me

liad

ine

Can

adia

n M

alar

tic

Isla

nd

Go

ld

You

ng-

Dav

idso

n

Lap

a

Mac

assa

Re

d L

ake

We

stw

oo

d

Eleo

no

re

Be

ll C

reek

De

tou

r La

ke

Eagl

e R

ive

r

Cas

a B

erar

di

Bla

ck F

ox

Island Gold – High Grade, Low Cost, Canadian Asset

Island Gold is one of the highest quality producing assets in Canada,

and one of a few not in a senior portfolio

2017E All-in Sustaining Costs (US$/oz)Mineral Reserve Grade (g/t Au)

Source: Company filingsNote: AISC based on midpoint of 2017 guidance where available, otherwise 1H/17 metrics shown. Eagle River AISC shown is Wesdome consolidated. Bell Creek AISC shown consolidated with Timmins West. TMAC AISC excluded due to recent guidance revisions. Island Gold based on PEA.

10

Island Gold PEA Highlights & Operating Profile

Source: Company disclosure, street research1 The Expansion Case PEA assumes a spot gold price of C$1,700/oz and US$1,260/oz and a C$:US$ exchange rate of 1.35.2 Excludes the 2017 and 2018 ramp-up period. 3 Project capital includes incremental expansion capital of C$28.2m and accelerated mine development/infrastructure capital of C$40m.4 Net cash flow is undiscounted pre-tax cash flow after all operating costs, project and sustaining capital.5 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

Expansion Case PEA Summary (1,100 tpd)1 Island Gold Operating Profile (PEA)

C$ US$

Targeted mill throughput run-rate year H2 2018 H2 2018

Avg annual production (koz): 2019 – 20242 125 koz 125 koz

Avg operating unit cost ($/t) $191 $141

Avg annual Cash Costs ($/oz): LOM 5 $652 $483

Avg annual AISC ($/oz): 2019 – 20242,5 $743 $550

Avg annual AIC ($/oz): LOM5 $910 $674

Sustaining capital ($m): LOM $168 $124

Project capital ($m)3: LOM $68 $50

Cumulative Net Cash Flow ($m)4 $749 $555

90 94

125

$735

$881

$550

2017E 2018E 2019E - 2024E Average

Gold Production (koz) AISC (US$/oz)

39% Growth

39%

projected

production growth

C$28.2 mm

Low incremental

expansion capital

-25%

expected decrease

in LOM AISC

Significant upside potential

>750 koz of Inferred resources not factored

into mine plan + ongoing exploration potential

11

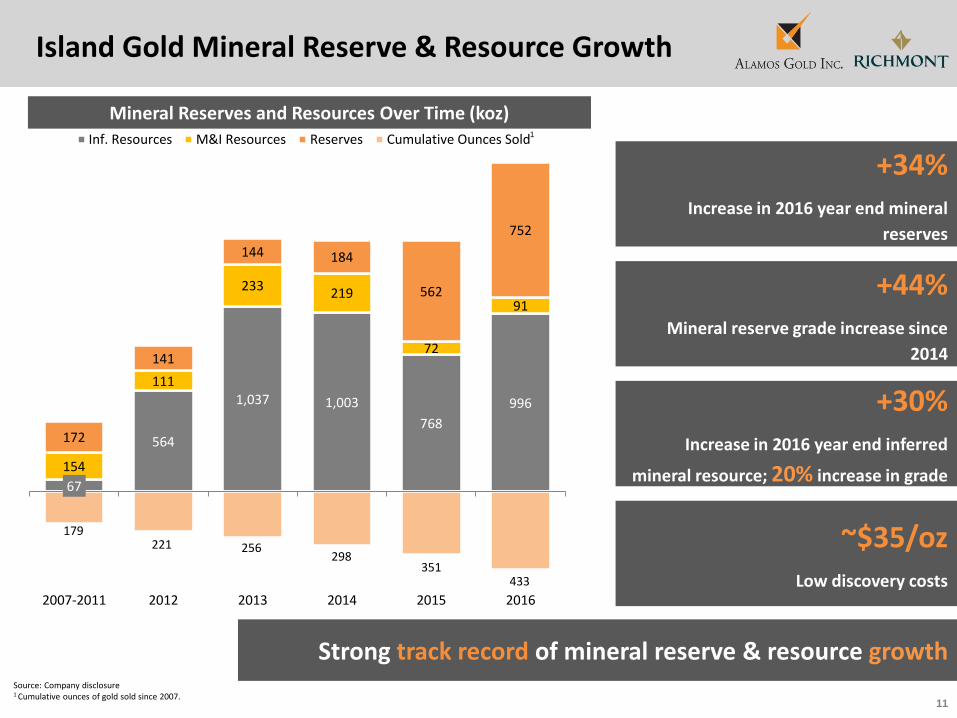

Island Gold Mineral Reserve & Resource Growth

67

564

1,037 1,003

768

996

154

111

233 219

72

91

172

141

144 184

562

752

2007-2011 2012 2013 2014 2015 2016

Inf. Resources M&I Resources Reserves Cumulative Ounces Sold

179 221 256

298 351

433

Source: Company disclosure1 Cumulative ounces of gold sold since 2007.

Mineral Reserves and Resources Over Time (koz)1

+34%Increase in 2016 year end mineral

reserves

Strong track record of mineral reserve & resource growth

~$35/ozLow discovery costs

+30%Increase in 2016 year end inferred

mineral resource; 20% increase in grade

+44%Mineral reserve grade increase since

2014

12

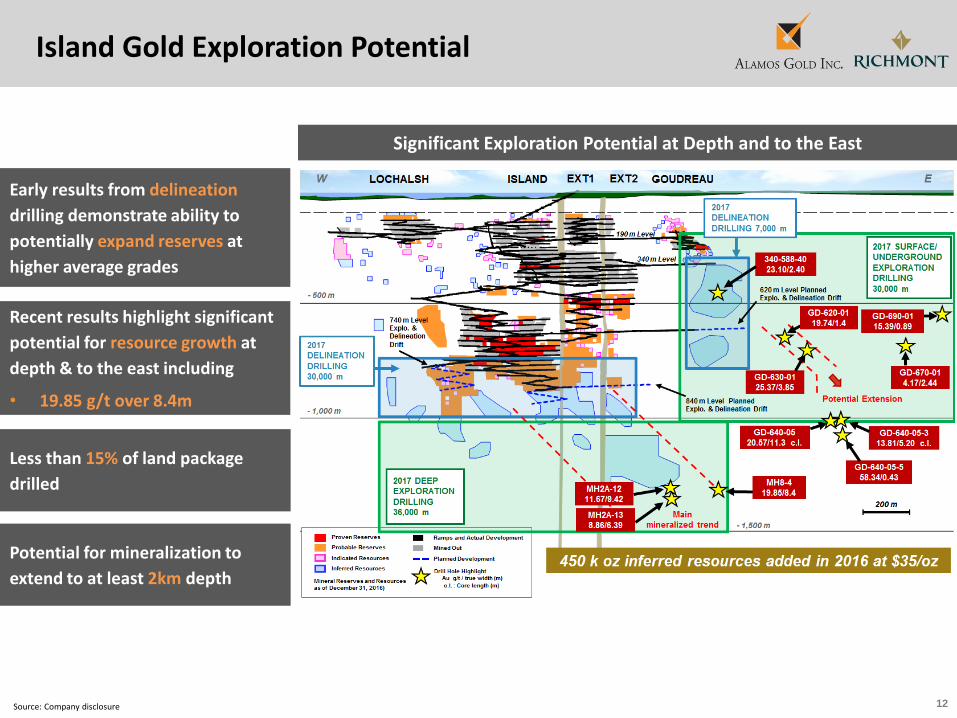

Island Gold Exploration Potential

Source: Company disclosure

Significant Exploration Potential at Depth and to the East

Recent results highlight significant

potential for resource growth at

depth & to the east including

• 19.85 g/t over 8.4m

Less than 15% of land package

drilled

Potential for mineralization to

extend to at least 2km depth

Early results from delineation

drilling demonstrate ability to

potentially expand reserves at

higher average grades

13

AĞI DAĞI (TURKEY)

Stage Permitting

2P Au Reserves 1.2 Moz (54.4 mt @ 0.67 g/t)

Total Au M&I Resources 0.5 Moz (34.9 mt @ 0.46 g/t)

Total Au Inf. Resources 0.2 Moz (16.8mt @ 0.46 g/t)

KIRAZLI (TURKEY)

Stage Permitting

2P Au Reserves 0.7 Moz (26.1mt @ 0.79 g/t)

Total Au M&I Resources 0.1 Moz (6.0mt @ 0.43 g/t)

Total Au Inf. Resources 0.1 Moz (5.7mt @ 0.59 g/t)

ÇAMYURT (TURKEY)

Stage Resource Dev.

Total Au M&I Resources 0.5 Moz (17.7mt @ 0.89 g/t)

Total Au Inf. Resources 0.1 Moz (2.8mt @0.95 g/t)

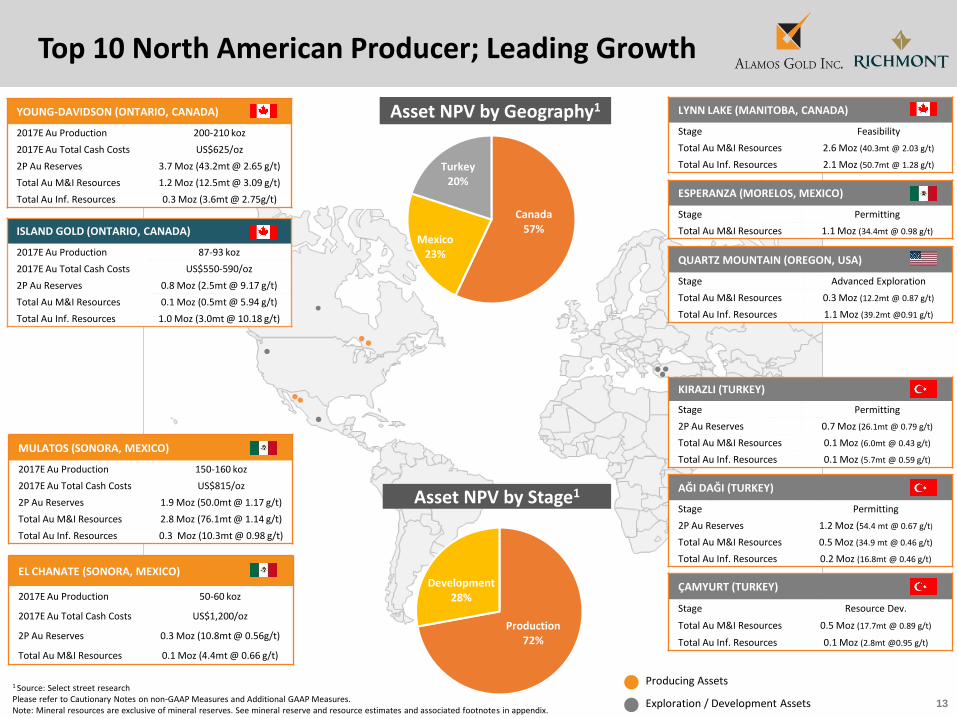

Top 10 North American Producer; Leading Growth

MULATOS (SONORA, MEXICO)

2017E Au Production 150-160 koz

2017E Au Total Cash Costs US$815/oz

2P Au Reserves 1.9 Moz (50.0mt @ 1.17 g/t)

Total Au M&I Resources 2.8 Moz (76.1mt @ 1.14 g/t)

Total Au Inf. Resources 0.3 Moz (10.3mt @ 0.98 g/t)

EL CHANATE (SONORA, MEXICO)

2017E Au Production 50-60 koz

2017E Au Total Cash Costs US$1,200/oz

2P Au Reserves 0.3 Moz (10.8mt @ 0.56g/t)

Total Au M&I Resources 0.1 Moz (4.4mt @ 0.66 g/t)

YOUNG-DAVIDSON (ONTARIO, CANADA)

2017E Au Production 200-210 koz

2017E Au Total Cash Costs US$625/oz

2P Au Reserves 3.7 Moz (43.2mt @ 2.65 g/t)

Total Au M&I Resources 1.2 Moz (12.5mt @ 3.09 g/t)

Total Au Inf. Resources 0.3 Moz (3.6mt @ 2.75g/t)

Producing Assets

Exploration / Development Assets

1 Source: Select street researchPlease refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.Note: Mineral resources are exclusive of mineral reserves. See mineral reserve and resource estimates and associated footnotes in appendix.

ISLAND GOLD (ONTARIO, CANADA)

2017E Au Production 87-93 koz

2017E Au Total Cash Costs US$550-590/oz

2P Au Reserves 0.8 Moz (2.5mt @ 9.17 g/t)

Total Au M&I Resources 0.1 Moz (0.5mt @ 5.94 g/t)

Total Au Inf. Resources 1.0 Moz (3.0mt @ 10.18 g/t)

QUARTZ MOUNTAIN (OREGON, USA)

Stage Advanced Exploration

Total Au M&I Resources 0.3 Moz (12.2mt @ 0.87 g/t)

Total Au Inf. Resources 1.1 Moz (39.2mt @0.91 g/t)

ESPERANZA (MORELOS, MEXICO)

Stage Permitting

Total Au M&I Resources 1.1 Moz (34.4mt @ 0.98 g/t)

LYNN LAKE (MANITOBA, CANADA)

Stage Feasibility

Total Au M&I Resources 2.6 Moz (40.3mt @ 2.03 g/t)

Total Au Inf. Resources 2.1 Moz (50.7mt @ 1.28 g/t)

Asset NPV by Geography1

Asset NPV by Stage1

Canada57%

Mexico23%

Turkey20%

Production72%

Development28%

14

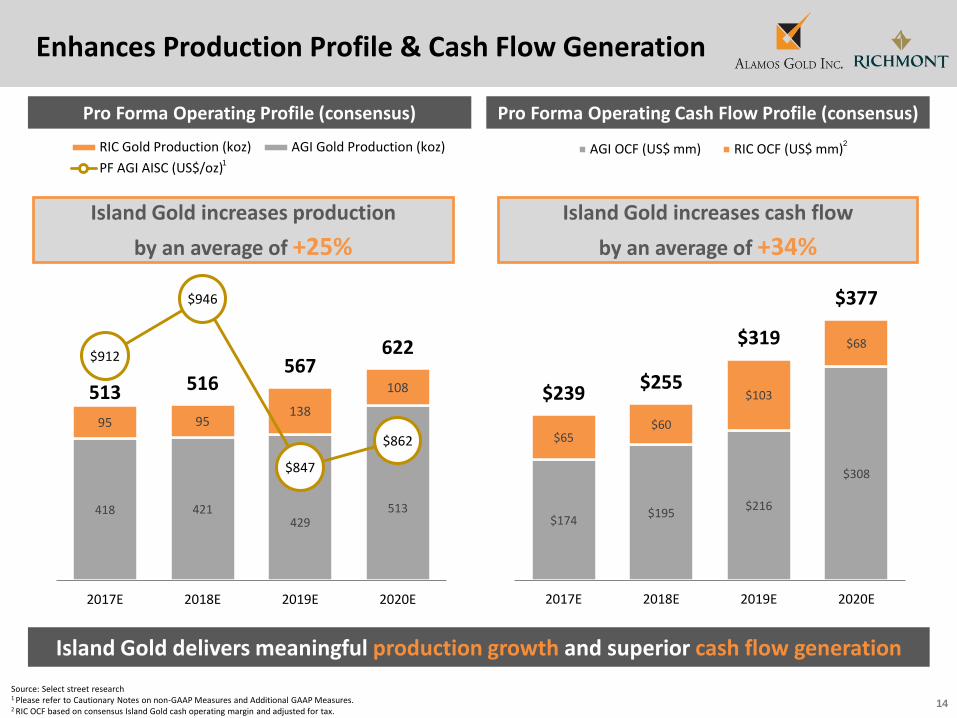

$174 $195

$216

$308

$65 $60

$103

$68

$239 $255

$319

$377

2017E 2018E 2019E 2020E

AGI OCF (US$ mm) RIC OCF (US$ mm)

Enhances Production Profile & Cash Flow Generation

Pro Forma Operating Profile (consensus) Pro Forma Operating Cash Flow Profile (consensus)

418 421 429

513

95 95 138

108 513 516 567

622 $912

$946

$847

$862

2017E 2018E 2019E 2020E

RIC Gold Production (koz) AGI Gold Production (koz)

PF AGI AISC (US$/oz)

Island Gold increases production

by an average of +25%

Island Gold increases cash flow

by an average of +34%

Source: Select street research1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.2 RIC OCF based on consensus Island Gold cash operating margin and adjusted for tax.

Island Gold delivers meaningful production growth and superior cash flow generation

2

1

15

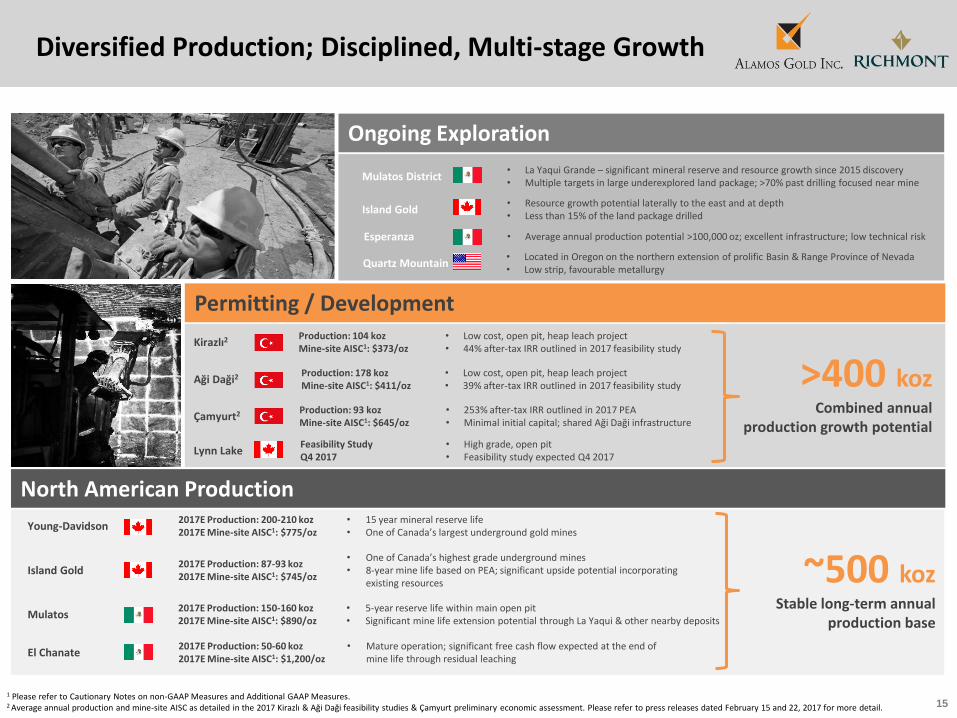

Mulatos District• La Yaqui Grande – significant mineral reserve and resource growth since 2015 discovery• Multiple targets in large underexplored land package; >70% past drilling focused near mine

Quartz Mountain• Located in Oregon on the northern extension of prolific Basin & Range Province of Nevada• Low strip, favourable metallurgy

Island Gold• Resource growth potential laterally to the east and at depth• Less than 15% of the land package drilled

Aği Daği2 Production: 178 kozMine-site AISC1: $411/oz

• Low cost, open pit, heap leach project • 39% after-tax IRR outlined in 2017 feasibility study

Çamyurt2 Production: 93 kozMine-site AISC1: $645/oz

• 253% after-tax IRR outlined in 2017 PEA• Minimal initial capital; shared Aği Daği infrastructure

Lynn LakeFeasibility Study Q4 2017

• High grade, open pit• Feasibility study expected Q4 2017

Kirazlı2Production: 104 kozMine-site AISC1: $373/oz

• Low cost, open pit, heap leach project • 44% after-tax IRR outlined in 2017 feasibility study

Esperanza • Average annual production potential >100,000 oz; excellent infrastructure; low technical risk

~500 koz Stable long-term annual

production base

Diversified Production; Disciplined, Multi-stage Growth

>400 kozCombined annual

production growth potential

Young-Davidson2017E Production: 200-210 koz2017E Mine-site AISC1: $775/oz

• 15 year mineral reserve life• One of Canada’s largest underground gold mines

North American Production

Permitting / Development

Ongoing Exploration

Mulatos2017E Production: 150-160 koz2017E Mine-site AISC1: $890/oz

• 5-year reserve life within main open pit• Significant mine life extension potential through La Yaqui & other nearby deposits

El Chanate2017E Production: 50-60 koz2017E Mine-site AISC1: $1,200/oz

• Mature operation; significant free cash flow expected at the end of mine life through residual leaching

Island Gold2017E Production: 87-93 koz2017E Mine-site AISC1: $745/oz

• One of Canada’s highest grade underground mines• 8-year mine life based on PEA; significant upside potential incorporating

existing resources

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.2 Average annual production and mine-site AISC as detailed in the 2017 Kirazlı & Aği Daği feasibility studies & Çamyurt preliminary economic assessment. Please refer to press releases dated February 15 and 22, 2017 for more detail.

16

Operations – Diversified North American Production

Long life reserve base

Declining costs & capital

Growing free cash flow

Growing production

17

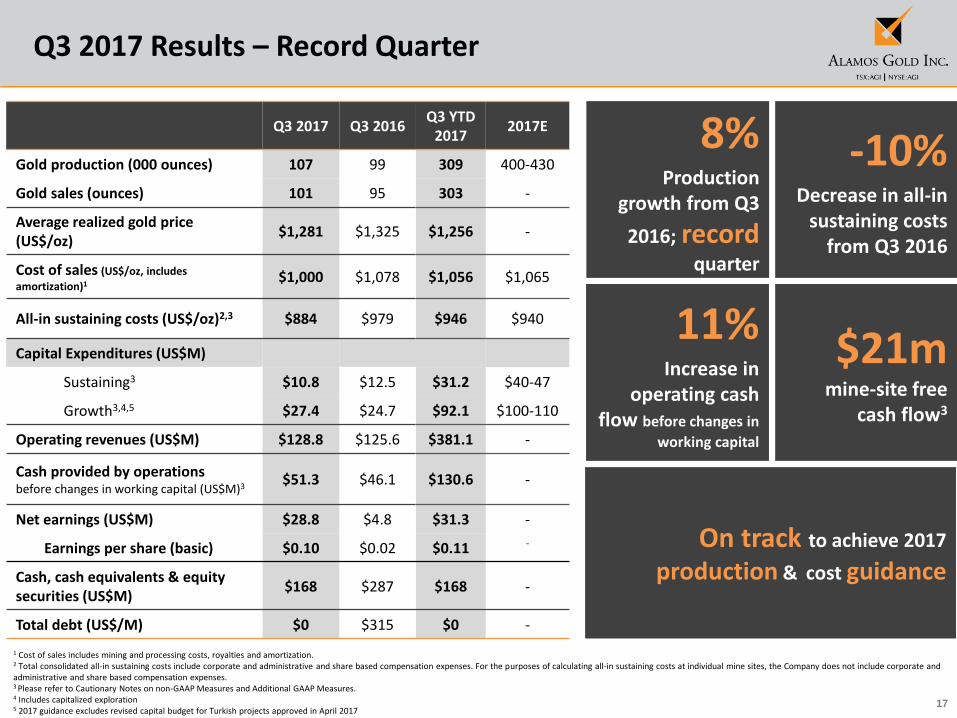

Q3 2017 Results – Record Quarter

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Total consolidated all-in sustaining costs include corporate and administrative and share based compensation expenses. For the purposes of calculating all-in sustaining costs at individual mine sites, the Company does not include corporate and administrative and share based compensation expenses.3 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures. 4 Includes capitalized exploration5 2017 guidance excludes revised capital budget for Turkish projects approved in April 2017

8%Production

growth from Q3

2016; recordquarter

-10%Decrease in all-in

sustaining costs from Q3 2016

11%Increase in

operating cash flow before changes in

working capital

$21mmine-site free

cash flow3

On track to achieve 2017

production & cost guidance

Q3 2017 Q3 2016Q3 YTD

20172017E

Gold production (000 ounces) 107 99 309 400-430

Gold sales (ounces) 101 95 303 -

Average realized gold price (US$/oz)

$1,281 $1,325 $1,256 -

Cost of sales (US$/oz, includes

amortization)1$1,000 $1,078 $1,056 $1,065

All-in sustaining costs (US$/oz)2,3 $884 $979 $946 $940

Capital Expenditures (US$M)

Sustaining3 $10.8 $12.5 $31.2 $40-47

Growth3,4,5 $27.4 $24.7 $92.1 $100-110

Operating revenues (US$M) $128.8 $125.6 $381.1 -

Cash provided by operations before changes in working capital (US$M)3

$51.3 $46.1 $130.6 -

Net earnings (US$M) $28.8 $4.8 $31.3 -

Earnings per share (basic) $0.10 $0.02 $0.11 -

Cash, cash equivalents & equity securities (US$M)

$168 $287 $168 -

Total debt (US$/M) $0 $315 $0 -

18

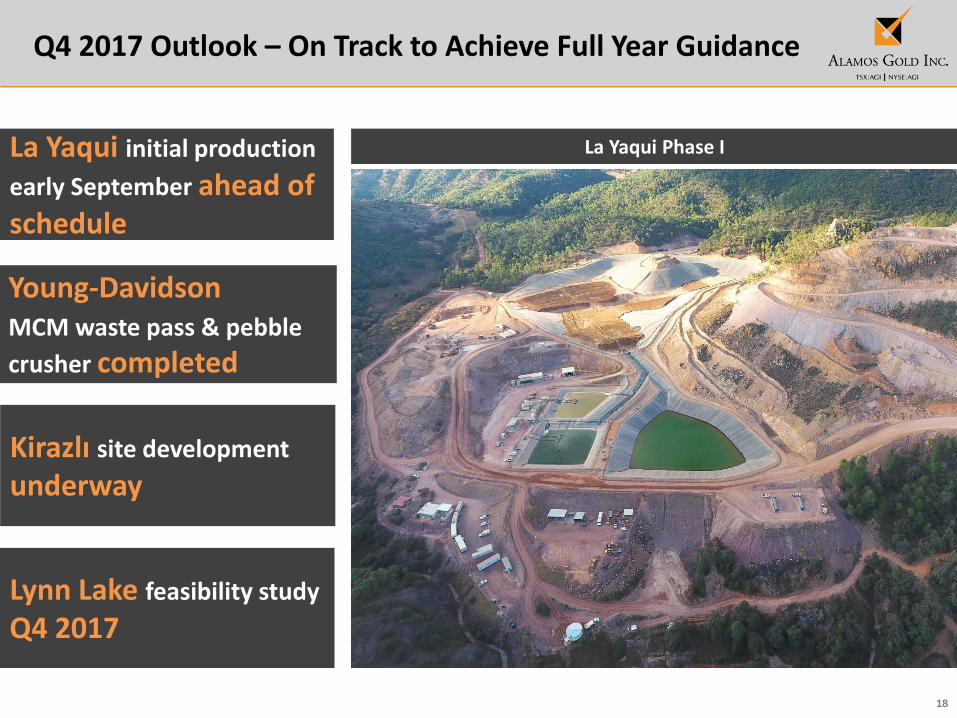

La Yaqui Phase I

Q4 2017 Outlook – On Track to Achieve Full Year Guidance

La Yaqui initial production

early September ahead of schedule

Kirazlı site development

underway

Lynn Lake feasibility study

Q4 2017

Young-Davidson MCM waste pass & pebble

crusher completed

19

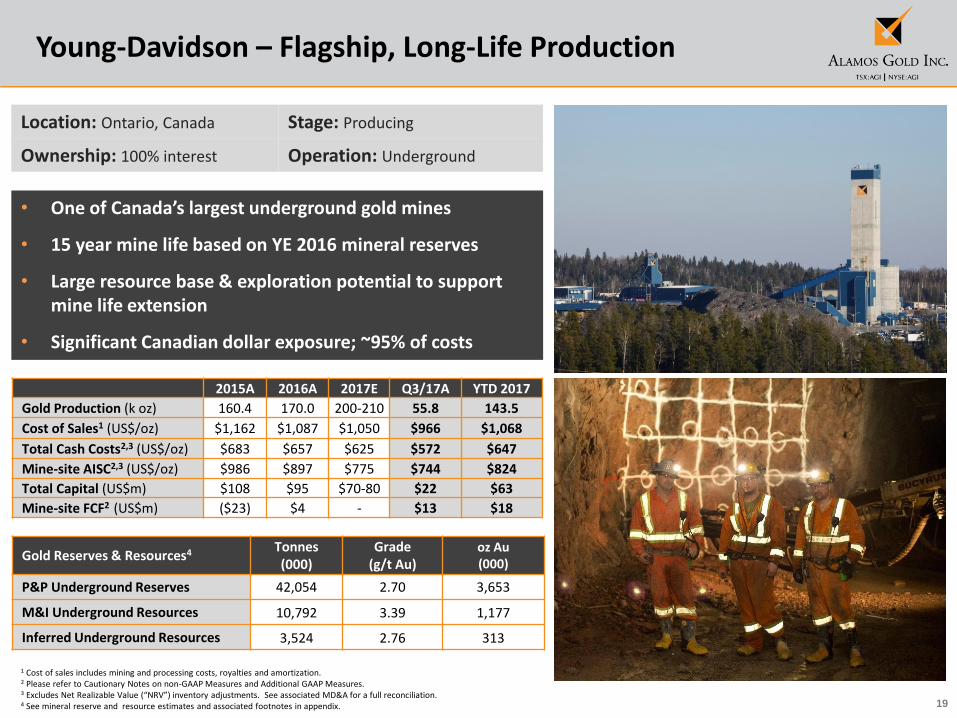

Young-Davidson – Flagship, Long-Life Production

2015A 2016A 2017E Q3/17A YTD 2017

Gold Production (k oz) 160.4 170.0 200-210 55.8 143.5

Cost of Sales1 (US$/oz) $1,162 $1,087 $1,050 $966 $1,068

Total Cash Costs2,3 (US$/oz) $683 $657 $625 $572 $647

Mine-site AISC2,3 (US$/oz) $986 $897 $775 $744 $824

Total Capital (US$m) $108 $95 $70-80 $22 $63

Mine-site FCF2 (US$m) ($23) $4 - $13 $18

• One of Canada’s largest underground gold mines

• 15 year mine life based on YE 2016 mineral reserves

• Large resource base & exploration potential to support mine life extension

• Significant Canadian dollar exposure; ~95% of costs

Location: Ontario, Canada Stage: Producing

Ownership: 100% interest Operation: Underground

Gold Reserves & Resources4 Tonnes (000)

Grade (g/t Au)

oz Au (000)

P&P Underground Reserves 42,054 2.70 3,653

M&I Underground Resources 10,792 3.39 1,177

Inferred Underground Resources 3,524 2.76 313

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Excludes Net Realizable Value (“NRV”) inventory adjustments. See associated MD&A for a full reconciliation.4 See mineral reserve and resource estimates and associated footnotes in appendix.

20

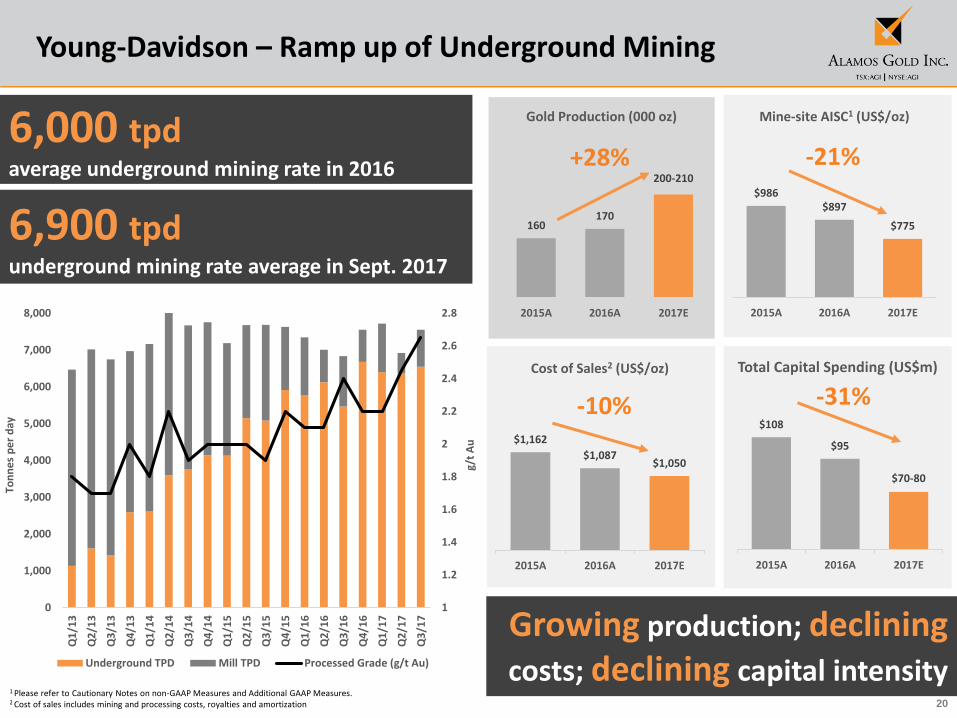

160170

200-210

2015A 2016A 2017E

Gold Production (000 oz)

$1,162

$1,087 $1,050

2015A 2016A 2017E

Cost of Sales2 (US$/oz)

$986 $897

$775

2015A 2016A 2017E

Mine-site AISC1 (US$/oz)

$108

$95

$70-80

2015A 2016A 2017E

-31%

Growing production; decliningcosts; declining capital intensity

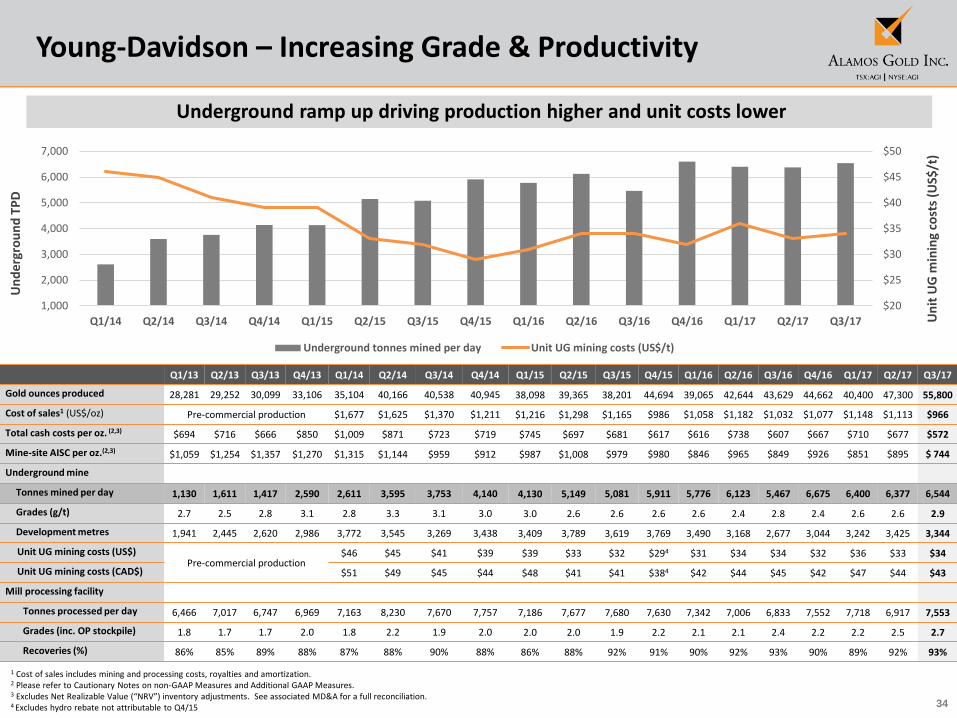

Young-Davidson – Ramp up of Underground Mining

-21%+28%

6,900 tpdunderground mining rate average in Sept. 2017

-10%

6,000 tpdaverage underground mining rate in 2016

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.2 Cost of sales includes mining and processing costs, royalties and amortization

Total Capital Spending (US$m)

1

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

2.8

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Q1

/13

Q2

/13

Q3

/13

Q4

/13

Q1

/14

Q2

/14

Q3

/14

Q4

/14

Q1

/15

Q2

/15

Q3

/15

Q4

/15

Q1

/16

Q2

/16

Q3

/16

Q4

/16

Q1

/17

Q2

/17

Q3

/17

Underground TPD Mill TPD Processed Grade (g/t Au)

Ton

ne

s p

er

day

g/t

Au

21

Mulatos – Our Founding Operation

• Initial production 2005

• ~$400m of free cash flow1 generated to date

• Declining cost profile; 5% NSR royalty nearing completion

• Large underexplored land package (28,773 ha)

Location: Sonora, Mexico Stage: Producing

Ownership: 100% interestOperation: Open pit, heap leach & high grade mill

2015A 2016A 2017E Q3/17A YTD 2017

Gold Production (k oz) 140.3 154.0 150-160 36.3 117.3

Cost of Sales1 (US$/oz) $1,128 $1,088 $1,015 $956 $964

Total Cash Costs2 (US$/oz) $869 $838 $815 $785 $782

Mine-site AISC2 (US$/oz) $1,047 $916 $890 $864 $852

Total Capital3 (US$m) $45 $33 $33-40 $7 $22

Mine-site FCF2,4 (US$m) ($19) $27 - $6 $20

Gold Reserves & Resources5 Tonnes (000)

Grade (g/t Au)

oz Au(000)

P&P Reserves 49,995 1.17 1,885

M&I Resources 76,084 1.14 2,798

Inferred Resources 10,280 0.98 3251 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Capital spending guidance for 2016 and 2017 excludes capitalized exploration. 2017 guidance includes La Yaqui Phase I development capital4 Excluding LY Phase I capital expenditures.5 See mineral reserve and resource estimates and associated footnotes in appendix.

22

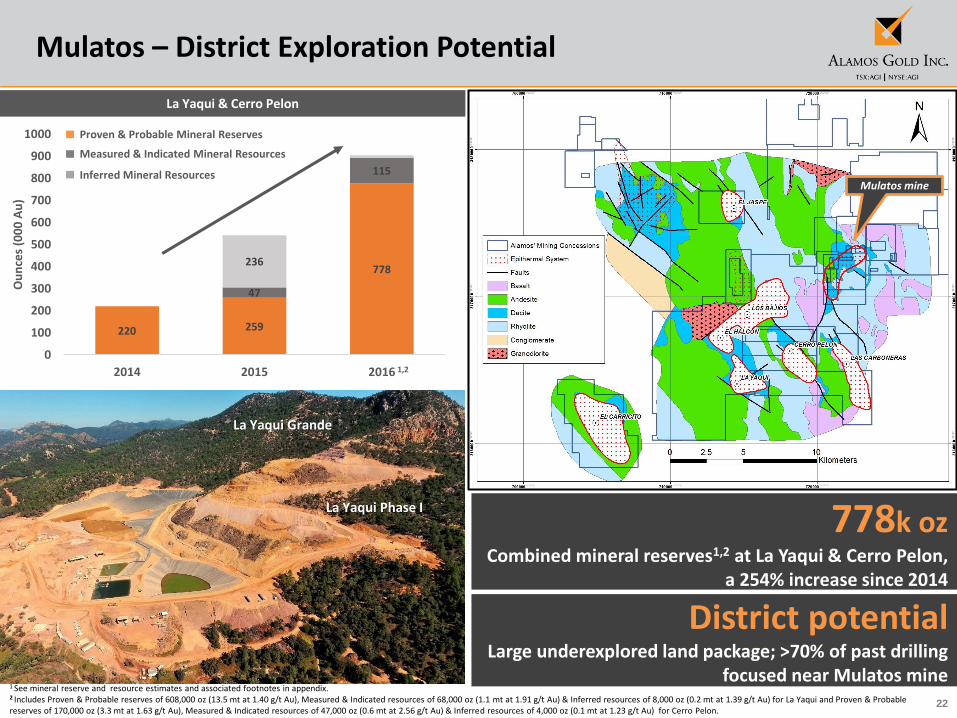

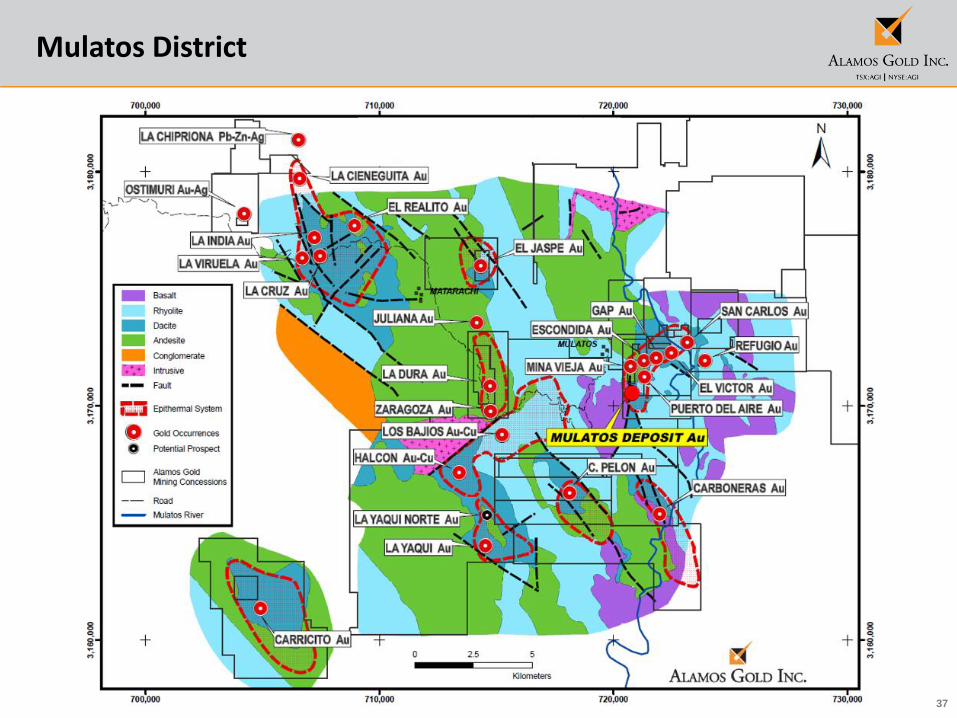

La Yaqui & Cerro Pelon

Mulatos – District Exploration Potential

1 See mineral reserve and resource estimates and associated footnotes in appendix.2 Includes Proven & Probable reserves of 608,000 oz (13.5 mt at 1.40 g/t Au), Measured & Indicated resources of 68,000 oz (1.1 mt at 1.91 g/t Au) & Inferred resources of 8,000 oz (0.2 mt at 1.39 g/t Au) for La Yaqui and Proven & Probable reserves of 170,000 oz (3.3 mt at 1.63 g/t Au), Measured & Indicated resources of 47,000 oz (0.6 mt at 2.56 g/t Au) & Inferred resources of 4,000 oz (0.1 mt at 1.23 g/t Au) for Cerro Pelon.

District potentialLarge underexplored land package; >70% of past drilling

focused near Mulatos mine

Mulatos District

Mulatos mine

220 259

778

47

115

236

0

100

200

300

400

500

600

700

800

900

1000

2014 2015 2016

Ou

nce

s (0

00

Au

)

Proven & Probable Mineral Reserves

Inferred Mineral Resources

Measured & Indicated Mineral Resources

1,2

La Yaqui Phase I

La Yaqui Grande

778k oz Combined mineral reserves1,2 at La Yaqui & Cerro Pelon,

a 254% increase since 2014

23

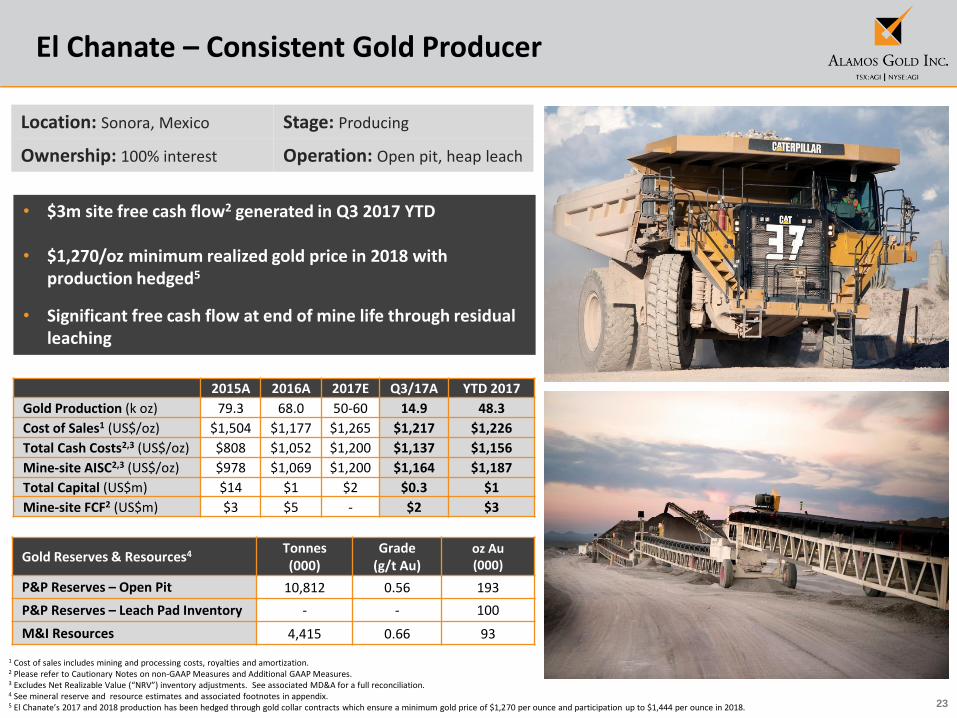

El Chanate – Consistent Gold Producer

• $3m site free cash flow2 generated in Q3 2017 YTD

• $1,270/oz minimum realized gold price in 2018 with production hedged5

• Significant free cash flow at end of mine life through residual leaching

Location: Sonora, Mexico Stage: Producing

Ownership: 100% interest Operation: Open pit, heap leach

Gold Reserves & Resources4 Tonnes (000)

Grade (g/t Au)

oz Au(000)

P&P Reserves – Open Pit 10,812 0.56 193

P&P Reserves – Leach Pad Inventory - - 100

M&I Resources 4,415 0.66 93

2015A 2016A 2017E Q3/17A YTD 2017

Gold Production (k oz) 79.3 68.0 50-60 14.9 48.3

Cost of Sales1 (US$/oz) $1,504 $1,177 $1,265 $1,217 $1,226

Total Cash Costs2,3 (US$/oz) $808 $1,052 $1,200 $1,137 $1,156

Mine-site AISC2,3 (US$/oz) $978 $1,069 $1,200 $1,164 $1,187

Total Capital (US$m) $14 $1 $2 $0.3 $1

Mine-site FCF2 (US$m) $3 $5 - $2 $3

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Excludes Net Realizable Value (“NRV”) inventory adjustments. See associated MD&A for a full reconciliation.4 See mineral reserve and resource estimates and associated footnotes in appendix.5 El Chanate’s 2017 and 2018 production has been hedged through gold collar contracts which ensure a minimum gold price of $1,270 per ounce and participation up to $1,444 per ounce in 2018.

24

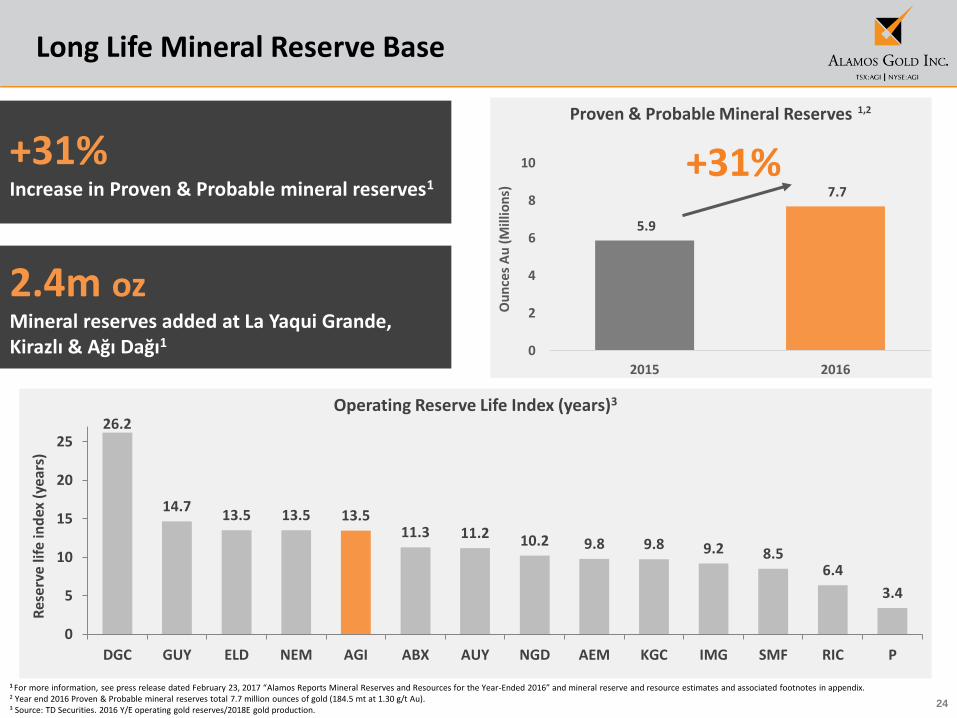

Proven & Probable Mineral Reserves

Long Life Mineral Reserve Base

Operating Reserve Life Index (years)3

1 For more information, see press release dated February 23, 2017 “Alamos Reports Mineral Reserves and Resources for the Year-Ended 2016” and mineral reserve and resource estimates and associated footnotes in appendix.2 Year end 2016 Proven & Probable mineral reserves total 7.7 million ounces of gold (184.5 mt at 1.30 g/t Au).3 Source: TD Securities. 2016 Y/E operating gold reserves/2018E gold production.

5.9

7.7

0

2

4

6

8

10

2015 2016

+31%

Ou

nce

s A

u (

Mill

ion

s)

1,2

+31%Increase in Proven & Probable mineral reserves1

2.4m ozMineral reserves added at La Yaqui Grande, Kirazlı & Ağı Dağı1

26.2

14.713.5 13.5 13.5

11.3 11.2 10.2 9.8 9.8 9.2 8.56.4

3.4

0

5

10

15

20

25

DGC GUY ELD NEM AGI ABX AUY NGD AEM KGC IMG SMF RIC P

Res

erv

e lif

e in

dex

(ye

ars)

25

Development – Peer Leading Growth Profile

Low cost, low capital intensity growth

Capacity to doublecurrent rate of production

6 development projects

26

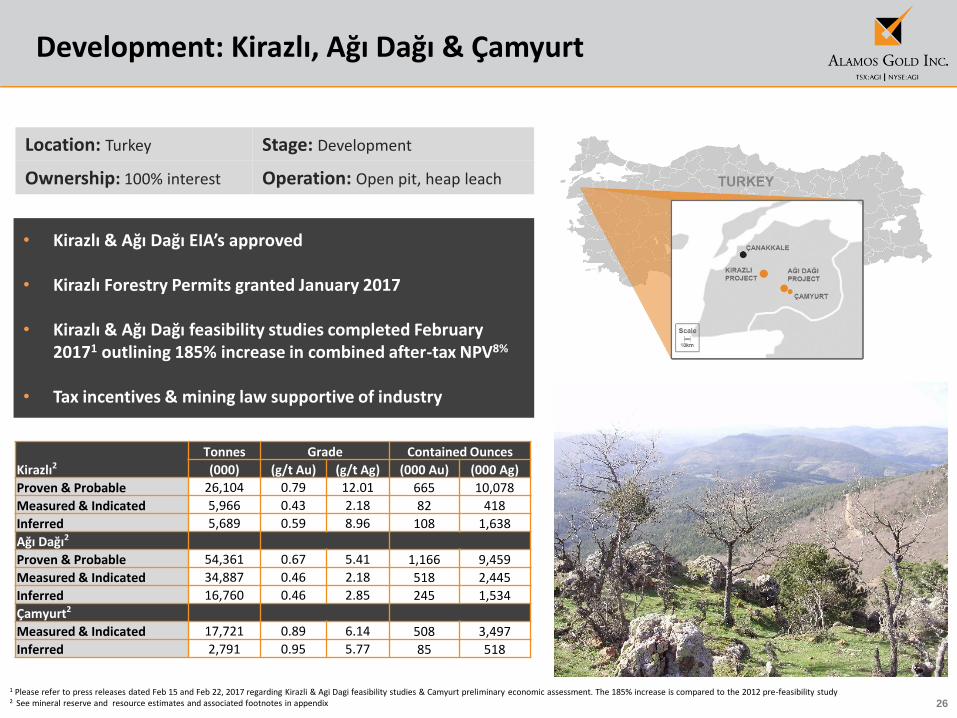

Development: Kirazlı, Ağı Dağı & Çamyurt

Location: Turkey Stage: Development

Ownership: 100% interest Operation: Open pit, heap leach

• Kirazlı & Ağı Dağı EIA’s approved

• Kirazlı Forestry Permits granted January 2017

• Kirazlı & Ağı Dağı feasibility studies completed February 20171 outlining 185% increase in combined after-tax NPV8%

• Tax incentives & mining law supportive of industry

Kirazlı2

Tonnes Grade Contained Ounces

(000) (g/t Au) (g/t Ag) (000 Au) (000 Ag)

Proven & Probable 26,104 0.79 12.01 665 10,078

Measured & Indicated 5,966 0.43 2.18 82 418

Inferred 5,689 0.59 8.96 108 1,638

Ağı Dağı2

Proven & Probable 54,361 0.67 5.41 1,166 9,459

Measured & Indicated 34,887 0.46 2.18 518 2,445

Inferred 16,760 0.46 2.85 245 1,534

Çamyurt2

Measured & Indicated 17,721 0.89 6.14 508 3,497

Inferred 2,791 0.95 5.77 85 518

1 Please refer to press releases dated Feb 15 and Feb 22, 2017 regarding Kirazli & Agi Dagi feasibility studies & Camyurt preliminary economic assessment. The 185% increase is compared to the 2012 pre-feasibility study2 See mineral reserve and resource estimates and associated footnotes in appendix

27

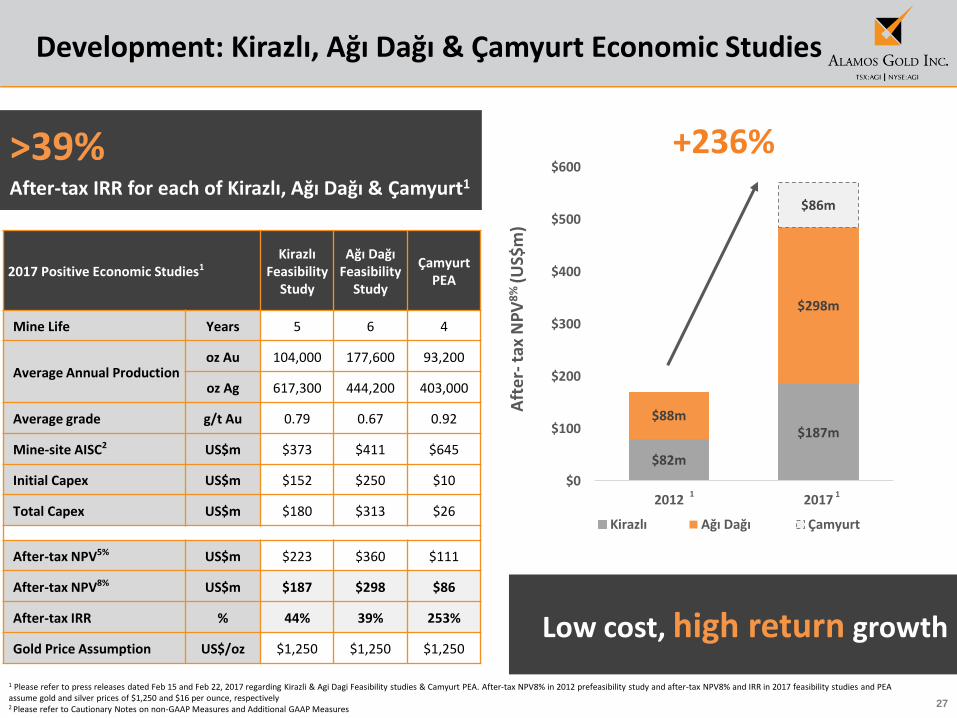

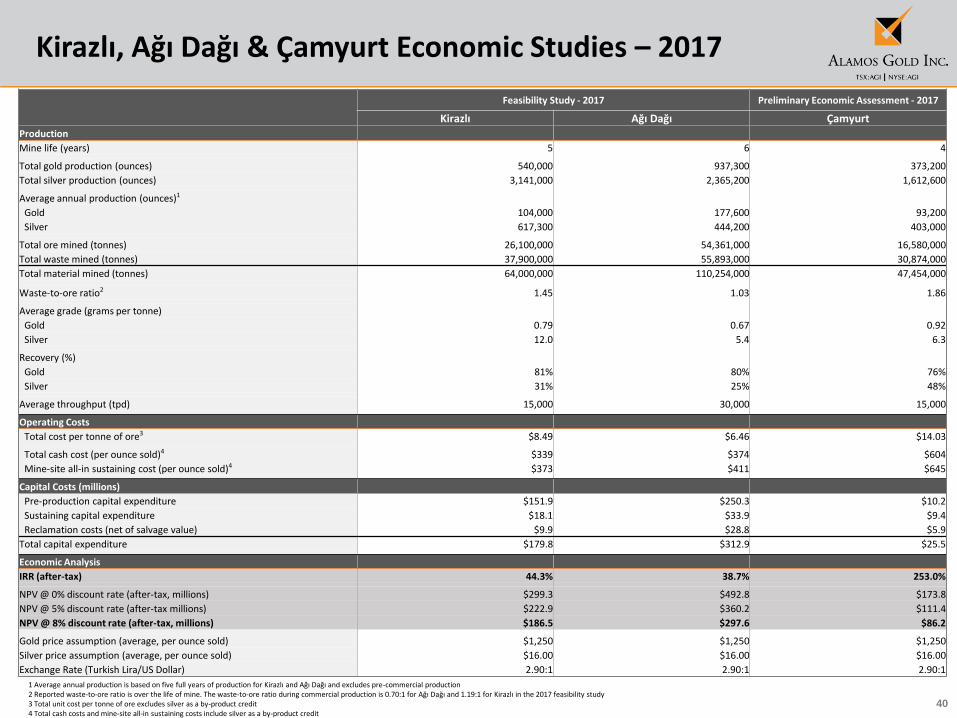

Development: Kirazlı, Ağı Dağı & Çamyurt Economic Studies

Aft

er-

tax

NP

V8

% (U

S$m

)

$82m

$187m$88m

$298m

$86m

$0

$100

$200

$300

$400

$500

$600

2012 2017

Kirazlı Ağı Dağı Çamyurt

+236%

1 Please refer to press releases dated Feb 15 and Feb 22, 2017 regarding Kirazli & Agi Dagi Feasibility studies & Camyurt PEA. After-tax NPV8% in 2012 prefeasibility study and after-tax NPV8% and IRR in 2017 feasibility studies and PEA assume gold and silver prices of $1,250 and $16 per ounce, respectively 2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures

11

2017 Positive Economic Studies1Kirazlı

Feasibility Study

Ağı Dağı Feasibility

Study

ÇamyurtPEA

Mine Life Years 5 6 4

Average Annual Productionoz Au 104,000 177,600 93,200

oz Ag 617,300 444,200 403,000

Average grade g/t Au 0.79 0.67 0.92

Mine-site AISC2 US$m $373 $411 $645

Initial Capex US$m $152 $250 $10

Total Capex US$m $180 $313 $26

After-tax NPV5% US$m $223 $360 $111

After-tax NPV8% US$m $187 $298 $86

After-tax IRR % 44% 39% 253%

Gold Price Assumption US$/oz $1,250 $1,250 $1,250

>39%After-tax IRR for each of Kirazlı, Ağı Dağı & Çamyurt1

Low cost, high return growth

28

Quartz Mountain

Location: Oregon, United States

Ownership: Right to earn a 100% interest4

Stage: Advanced Exploration

Esperanza

Location: Morelos State, Mexico

Ownership: 100% interest

Stage: Development

Operation: Open pit, heap leach

Development: Lynn Lake, Esperanza & Quartz Mountain

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.2 Historic column recovery tests for gold at Quartz Mountain varied between 74% and 88% for the felsic rock hosted mineralization; see Orsa Ventures press release dated February 12, 20133 See mineral reserve and resource estimates and associated footnotes in appendix.4 Additional C$3m due on completion of feasibility study & C$15m or 2% NSR upon successful permitting

Lynn Lake

Location: Manitoba, Canada

Ownership: 100% interest

Stage: Feasibility

Operation: Open pit

Tonnes (000)

Grade (g/t Au)

oz Au (000)

M&I Resources3 40,303 2.03 2,629

Inferred Resources 50,704 1.28 2,089

• Located in highly-prospective Lynn Lake Mining District

• High grade, open pit with significant exploration potential

• Existing infrastructure in place

• Low cost hydroelectric power

• Feasibility study expected Q4 2017

Tonnes Grade Oz Au

(000) (g/t Au) (g/t Ag) (000 Au) (000 Ag)

M&I3 Resources 34,352 0.98 8.09 1,083 8,936

Inf. Resources 718 0.80 15.04 18 347

Tonnes Grade Oz Au

(000) (g/t Au) (000 Au)

M&I Resources3 12,156 0.87 339

Inferred Resources 39,205 0.91 1,147

• Excellent infrastructure; low technical risk

• Low capital intensity & operating costs

• Average annual production potential > 100k oz

• AISC expected to be lowest quartile1

• Located on northern extension of prolific Basin & Range Province of Nevada

• Low strip ratio, favourable metallurgy2

• Acquisition cost $3.5m

29

Alamos – Investment Case

Catalysts

Diversified intermediate gold producer Low-cost growth profile

Strong balance sheet to support growth

Long term track record of delivering shareholder value

✓ Q4 2016: Met consolidated 2016 production guidance

✓ Q1 2017: Received Forestry Permits for Kirazlı project

✓ Q1 2017: Positive Kirazlı & Ağı Dağı feasibility studies & Çamyurt PEA

✓ Q1 2017: 31% increase in combined mineral reserves

✓ Q3 2017: Initial production at La Yaqui

Q4 2017: Closing of Richmont acquisition

Q4 2017: Lynn Lake feasibility study

2017: Ongoing exploration at Mulatos

2017: Receipt of GSM permit for Kirazlı

30

Appendices

31

Board of Directors and Executive and Management Team

Board of Directors

Executive and Management Team

Paul J. Murphy John A.

McCluskey Mark J. Daniel

Patrick D. Downey

David Fleck David GowerClaire M. C.

KennedyRonald E. Smith Kenneth Stowe

Chairman Director Director Director Director Director Director Director Director

John A. McCluskey Jamie Porter Peter MacPhail Christine Barwell Chris Bostwick Luis Chavez

President and CEO Chief Financial Officer Chief Operating Officer VP, Human Resources VP, Technical Services Senior VP, Mexico

Andrew Cormier Nils Engelstad Greg Fisher Aoife McGrath Scott Parsons Colin Webster

VP, Development & Construction VP, General Counsel VP, Finance VP, Exploration VP, Investor Relations VP Sustainability & External Affairs

32

Sustainability

• Our Objectives

• As we pursue further growth, we will continue to measure our success as an

organization by our performance in achievement of our sustainability objectives:

• Protecting the health and well-being of our employees

• Creating shared value with our host communities and countries

• Ensuring that our operations are net-positive for the environment

• Over the years, Alamos has been recognized for its achievements in these areas:

Clean Industry Certification from PROFEPA

• Alamos was certified as an Industria Limpia (clean industry)

in recognition of the excellence of environmental management

at Mulatos

CSR Award from Mexican Center for Philanthropy (CEMEFI)

• Signifies exceptional record of CSR performance;

• 2016 marked the 8th consecutive year for Alamos

33

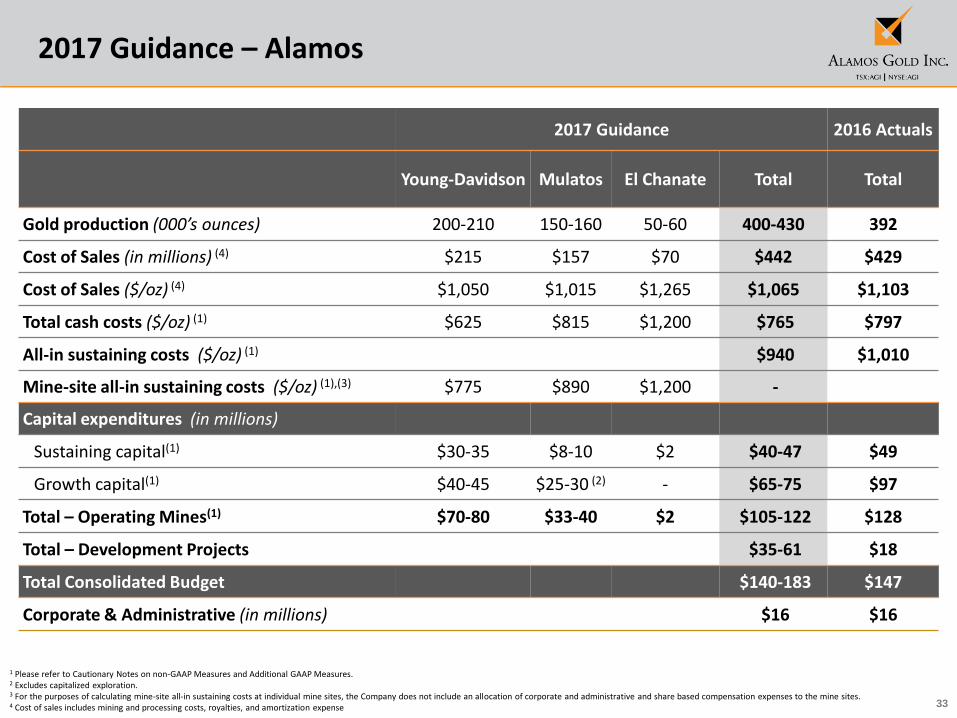

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures. 2 Excludes capitalized exploration.3 For the purposes of calculating mine-site all-in sustaining costs at individual mine sites, the Company does not include an allocation of corporate and administrative and share based compensation expenses to the mine sites.4 Cost of sales includes mining and processing costs, royalties, and amortization expense

2017 Guidance – Alamos

2017 Guidance 2016 Actuals

Young-Davidson Mulatos El Chanate Total Total

Gold production (000’s ounces) 200-210 150-160 50-60 400-430 392

Cost of Sales (in millions) (4) $215 $157 $70 $442 $429

Cost of Sales ($/oz) (4) $1,050 $1,015 $1,265 $1,065 $1,103

Total cash costs ($/oz) (1) $625 $815 $1,200 $765 $797

All-in sustaining costs ($/oz) (1) $940 $1,010

Mine-site all-in sustaining costs ($/oz) (1),(3) $775 $890 $1,200 -

Capital expenditures (in millions)

Sustaining capital(1) $30-35 $8-10 $2 $40-47 $49

Growth capital(1) $40-45 $25-30 (2) - $65-75 $97

Total – Operating Mines(1) $70-80 $33-40 $2 $105-122 $128

Total – Development Projects $35-61 $18

Total Consolidated Budget $140-183 $147

Corporate & Administrative (in millions) $16 $16

34

Young-Davidson – Increasing Grade & Productivity

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Excludes Net Realizable Value (“NRV”) inventory adjustments. See associated MD&A for a full reconciliation.4 Excludes hydro rebate not attributable to Q4/15

Underground ramp up driving production higher and unit costs lower

Q1/13 Q2/13 Q3/13 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17 Q3/17

Gold ounces produced 28,281 29,252 30,099 33,106 35,104 40,166 40,538 40,945 38,098 39,365 38,201 44,694 39,065 42,644 43,629 44,662 40,400 47,300 55,800

Cost of sales1 (US$/oz) Pre-commercial production $1,677 $1,625 $1,370 $1,211 $1,216 $1,298 $1,165 $986 $1,058 $1,182 $1,032 $1,077 $1,148 $1,113 $966

Total cash costs per oz. (2,3) $694 $716 $666 $850 $1,009 $871 $723 $719 $745 $697 $681 $617 $616 $738 $607 $667 $710 $677 $572

Mine-site AISC per oz.(2,3) $1,059 $1,254 $1,357 $1,270 $1,315 $1,144 $959 $912 $987 $1,008 $979 $980 $846 $965 $849 $926 $851 $895 $ 744

Underground mine

Tonnes mined per day 1,130 1,611 1,417 2,590 2,611 3,595 3,753 4,140 4,130 5,149 5,081 5,911 5,776 6,123 5,467 6,675 6,400 6,377 6,544

Grades (g/t) 2.7 2.5 2.8 3.1 2.8 3.3 3.1 3.0 3.0 2.6 2.6 2.6 2.6 2.4 2.8 2.4 2.6 2.6 2.9

Development metres 1,941 2,445 2,620 2,986 3,772 3,545 3,269 3,438 3,409 3,789 3,619 3,769 3,490 3,168 2,677 3,044 3,242 3,425 3,344

Unit UG mining costs (US$)Pre-commercial production

$46 $45 $41 $39 $39 $33 $32 $294 $31 $34 $34 $32 $36 $33 $34

Unit UG mining costs (CAD$) $51 $49 $45 $44 $48 $41 $41 $384 $42 $44 $45 $42 $47 $44 $43

Mill processing facility

Tonnes processed per day 6,466 7,017 6,747 6,969 7,163 8,230 7,670 7,757 7,186 7,677 7,680 7,630 7,342 7,006 6,833 7,552 7,718 6,917 7,553

Grades (inc. OP stockpile) 1.8 1.7 1.7 2.0 1.8 2.2 1.9 2.0 2.0 2.0 1.9 2.2 2.1 2.1 2.4 2.2 2.2 2.5 2.7

Recoveries (%) 86% 85% 89% 88% 87% 88% 90% 88% 86% 88% 92% 91% 90% 92% 93% 90% 89% 92% 93%

$20

$25

$30

$35

$40

$45

$50

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17 Q3/17

Underground tonnes mined per day Unit UG mining costs (US$/t)

Un

der

gro

un

d T

PD

Un

it U

G m

inin

g co

sts

(US$

/t)

35

2016 2017 2018 2019

✓ Commissioning of MCM shaft

✓ Transition to 100% owner development

✓ Ramp up to 7,000 tpd

✓ Raise boring of lower NG shaft

✓ Completion of MCM waste pass

• Shaft bottom infrastructure

• Northgate shaft hoisting from 8900L

Young-Davidson – Development Schedule

Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

Declining capital intensity

36

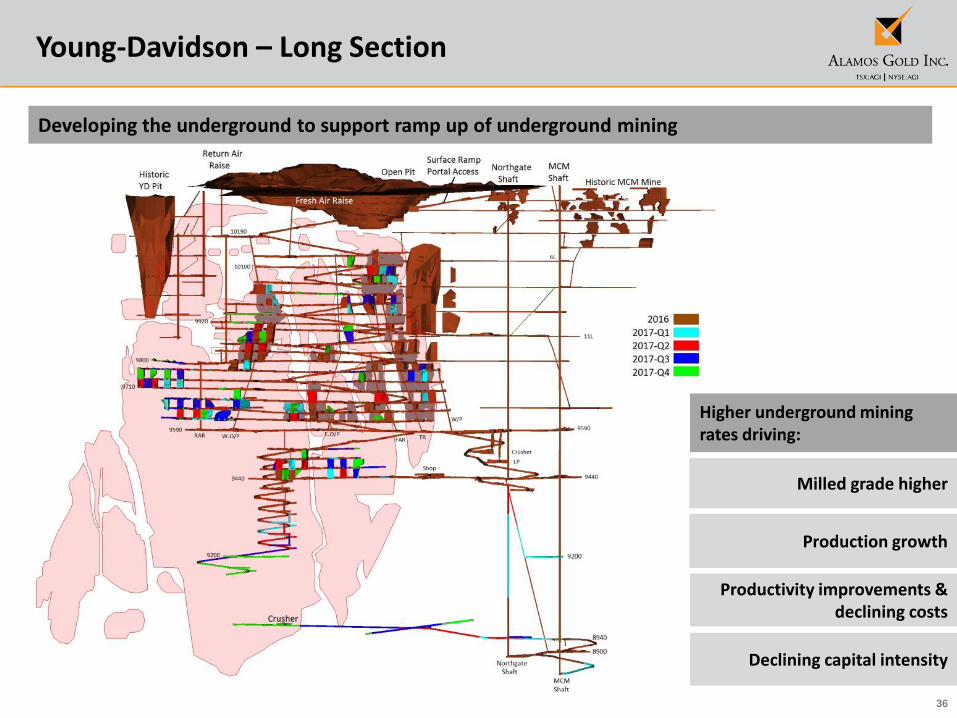

Young-Davidson – Long Section

Productivity improvements & declining costs

Developing the underground to support ramp up of underground mining

Milled grade higher

Declining capital intensity

Higher underground mining rates driving:

Production growth

37

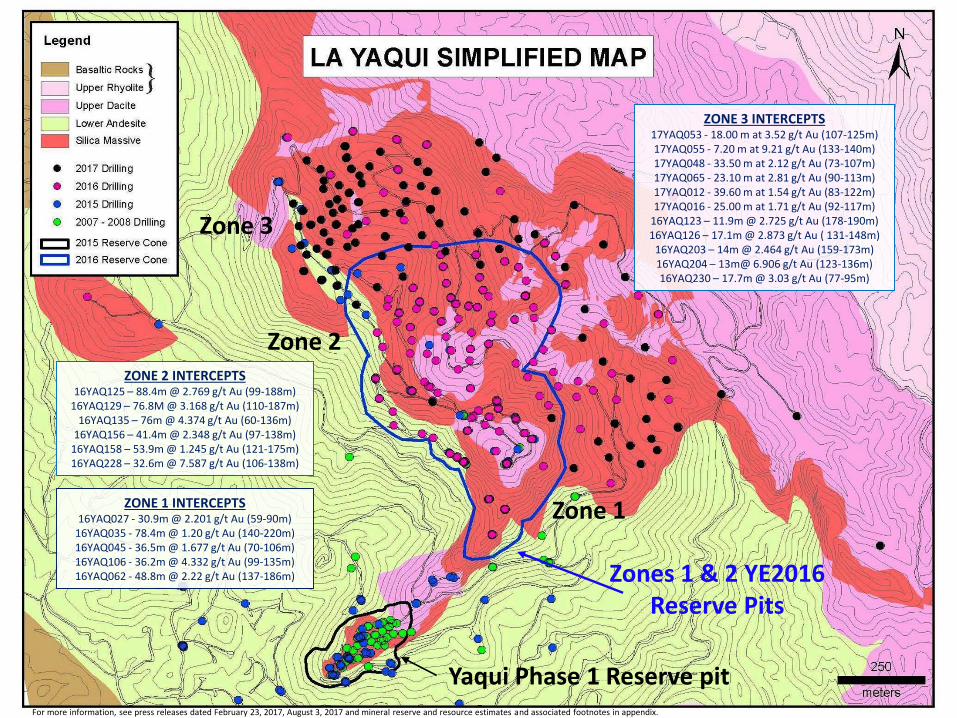

Mulatos District

38

Zone 3

Zone 2

Zone 1

Zones 1 & 2 YE2016 Reserve Pits

ZONE 3 INTERCEPTS17YAQ053 - 18.00 m at 3.52 g/t Au (107-125m)17YAQ055 - 7.20 m at 9.21 g/t Au (133-140m)17YAQ048 - 33.50 m at 2.12 g/t Au (73-107m)17YAQ065 - 23.10 m at 2.81 g/t Au (90-113m)17YAQ012 - 39.60 m at 1.54 g/t Au (83-122m)17YAQ016 - 25.00 m at 1.71 g/t Au (92-117m)

16YAQ123 – 11.9m @ 2.725 g/t Au (178-190m)16YAQ126 – 17.1m @ 2.873 g/t Au ( 131-148m)

16YAQ203 – 14m @ 2.464 g/t Au (159-173m)16YAQ204 – 13m@ 6.906 g/t Au (123-136m)16YAQ230 – 17.7m @ 3.03 g/t Au (77-95m)

ZONE 2 INTERCEPTS16YAQ125 – 88.4m @ 2.769 g/t Au (99-188m)

16YAQ129 – 76.8M @ 3.168 g/t Au (110-187m)16YAQ135 – 76m @ 4.374 g/t Au (60-136m)

16YAQ156 – 41.4m @ 2.348 g/t Au (97-138m)16YAQ158 – 53.9m @ 1.245 g/t Au (121-175m)16YAQ228 – 32.6m @ 7.587 g/t Au (106-138m)

ZONE 1 INTERCEPTS16YAQ027 - 30.9m @ 2.201 g/t Au (59-90m)

16YAQ035 - 78.4m @ 1.20 g/t Au (140-220m)16YAQ045 - 36.5m @ 1.677 g/t Au (70-106m)16YAQ106 - 36.2m @ 4.332 g/t Au (99-135m)16YAQ062 - 48.8m @ 2.22 g/t Au (137-186m)

Yaqui Phase 1 Reserve pit For more information, see press releases dated February 23, 2017, August 3, 2017 and mineral reserve and resource estimates and associated footnotes in appendix.

39

Strong Portfolio of Development Projects

NORTH AMERICA

STAGE CANADA UNITED STATES MEXICO TURKEY

Construction La Yaqui Phase I

Permitting/Feasibility

Lynn LakeKirazlı

Aği DağiÇamyurt

Advanced Exploration/Development

Quartz MountainCerro Pelon

La Yaqui GrandeEsperanza

OtherExplorationOpportunities

Lynn Lake RegionalQuartz Mountain

Targets

Los BajiosSan Carlos Far East

El RefugioEl Carricito

Çamyurt Expansion

Kirazlı Zones

40

Kirazlı, Ağı Dağı & Çamyurt Economic Studies – 2017

Feasibility Study - 2017 Preliminary Economic Assessment - 2017

Kirazlı Ağı Dağı ÇamyurtProduction

Mine life (years) 5 6 4

Total gold production (ounces) 540,000 937,300 373,200

Total silver production (ounces) 3,141,000 2,365,200 1,612,600

Average annual production (ounces)1

Gold 104,000 177,600 93,200

Silver 617,300 444,200 403,000

Total ore mined (tonnes) 26,100,000 54,361,000 16,580,000

Total waste mined (tonnes) 37,900,000 55,893,000 30,874,000

Total material mined (tonnes) 64,000,000 110,254,000 47,454,000

Waste-to-ore ratio2 1.45 1.03 1.86

Average grade (grams per tonne)

Gold 0.79 0.67 0.92

Silver 12.0 5.4 6.3

Recovery (%)

Gold 81% 80% 76%

Silver 31% 25% 48%

Average throughput (tpd) 15,000 30,000 15,000

Operating Costs

Total cost per tonne of ore3 $8.49 $6.46 $14.03

Total cash cost (per ounce sold)4 $339 $374 $604

Mine-site all-in sustaining cost (per ounce sold)4 $373 $411 $645

Capital Costs (millions)

Pre-production capital expenditure $151.9 $250.3 $10.2

Sustaining capital expenditure $18.1 $33.9 $9.4

Reclamation costs (net of salvage value) $9.9 $28.8 $5.9

Total capital expenditure $179.8 $312.9 $25.5

Economic Analysis

IRR (after-tax) 44.3% 38.7% 253.0%

NPV @ 0% discount rate (after-tax, millions) $299.3 $492.8 $173.8

NPV @ 5% discount rate (after-tax millions) $222.9 $360.2 $111.4

NPV @ 8% discount rate (after-tax, millions) $186.5 $297.6 $86.2

Gold price assumption (average, per ounce sold) $1,250 $1,250 $1,250

Silver price assumption (average, per ounce sold) $16.00 $16.00 $16.00

Exchange Rate (Turkish Lira/US Dollar) 2.90:1 2.90:1 2.90:1

1 Average annual production is based on five full years of production for Kirazlı and Ağı Dağı and excludes pre-commercial production2 Reported waste-to-ore ratio is over the life of mine. The waste-to-ore ratio during commercial production is 0.70:1 for Ağı Dağı and 1.19:1 for Kirazlı in the 2017 feasibility study3 Total unit cost per tonne of ore excludes silver as a by-product credit 4 Total cash costs and mine-site all-in sustaining costs include silver as a by-product credit

41

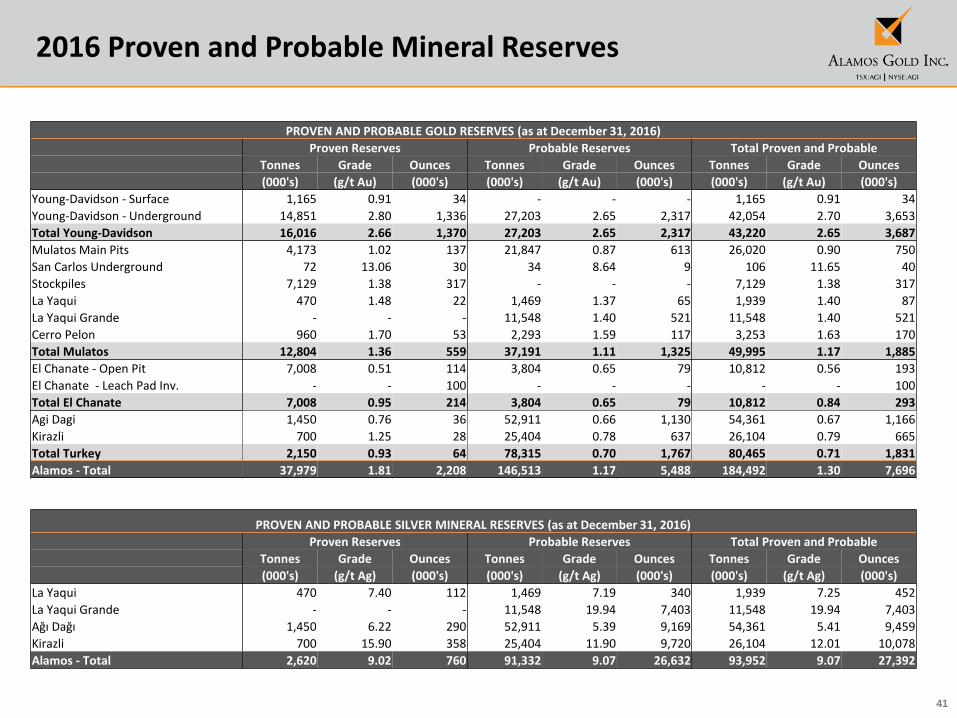

2016 Proven and Probable Mineral Reserves

PROVEN AND PROBABLE GOLD RESERVES (as at December 31, 2016)

Proven Reserves Probable Reserves Total Proven and Probable

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Au) (000's) (000's) (g/t Au) (000's) (000's) (g/t Au) (000's)

Young-Davidson - Surface 1,165 0.91 34 - - - 1,165 0.91 34

Young-Davidson - Underground 14,851 2.80 1,336 27,203 2.65 2,317 42,054 2.70 3,653

Total Young-Davidson 16,016 2.66 1,370 27,203 2.65 2,317 43,220 2.65 3,687

Mulatos Main Pits 4,173 1.02 137 21,847 0.87 613 26,020 0.90 750

San Carlos Underground 72 13.06 30 34 8.64 9 106 11.65 40

Stockpiles 7,129 1.38 317 - - - 7,129 1.38 317

La Yaqui 470 1.48 22 1,469 1.37 65 1,939 1.40 87

La Yaqui Grande - - - 11,548 1.40 521 11,548 1.40 521

Cerro Pelon 960 1.70 53 2,293 1.59 117 3,253 1.63 170

Total Mulatos 12,804 1.36 559 37,191 1.11 1,325 49,995 1.17 1,885

El Chanate - Open Pit 7,008 0.51 114 3,804 0.65 79 10,812 0.56 193

El Chanate - Leach Pad Inv. - - 100 - - - - - 100

Total El Chanate 7,008 0.95 214 3,804 0.65 79 10,812 0.84 293

Agi Dagi 1,450 0.76 36 52,911 0.66 1,130 54,361 0.67 1,166

Kirazli 700 1.25 28 25,404 0.78 637 26,104 0.79 665

Total Turkey 2,150 0.93 64 78,315 0.70 1,767 80,465 0.71 1,831

Alamos - Total 37,979 1.81 2,208 146,513 1.17 5,488 184,492 1.30 7,696

PROVEN AND PROBABLE SILVER MINERAL RESERVES (as at December 31, 2016)

Proven Reserves Probable Reserves Total Proven and Probable

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's)

La Yaqui 470 7.40 112 1,469 7.19 340 1,939 7.25 452

La Yaqui Grande - - - 11,548 19.94 7,403 11,548 19.94 7,403

Ağı Dağı 1,450 6.22 290 52,911 5.39 9,169 54,361 5.41 9,459

Kirazli 700 15.90 358 25,404 11.90 9,720 26,104 12.01 10,078

Alamos - Total 2,620 9.02 760 91,332 9.07 26,632 93,952 9.07 27,392

42

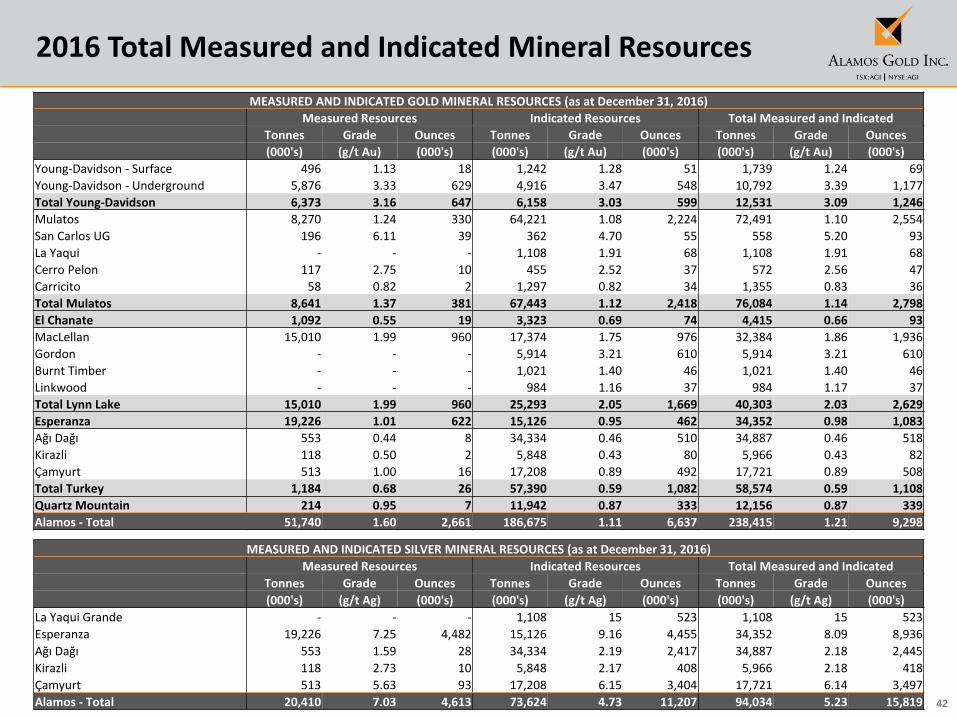

2016 Total Measured and Indicated Mineral Resources

MEASURED AND INDICATED GOLD MINERAL RESOURCES (as at December 31, 2016)

Measured Resources Indicated Resources Total Measured and Indicated

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Au) (000's) (000's) (g/t Au) (000's) (000's) (g/t Au) (000's)

Young-Davidson - Surface 496 1.13 18 1,242 1.28 51 1,739 1.24 69

Young-Davidson - Underground 5,876 3.33 629 4,916 3.47 548 10,792 3.39 1,177

Total Young-Davidson 6,373 3.16 647 6,158 3.03 599 12,531 3.09 1,246

Mulatos 8,270 1.24 330 64,221 1.08 2,224 72,491 1.10 2,554

San Carlos UG 196 6.11 39 362 4.70 55 558 5.20 93

La Yaqui - - - 1,108 1.91 68 1,108 1.91 68

Cerro Pelon 117 2.75 10 455 2.52 37 572 2.56 47

Carricito 58 0.82 2 1,297 0.82 34 1,355 0.83 36

Total Mulatos 8,641 1.37 381 67,443 1.12 2,418 76,084 1.14 2,798

El Chanate 1,092 0.55 19 3,323 0.69 74 4,415 0.66 93

MacLellan 15,010 1.99 960 17,374 1.75 976 32,384 1.86 1,936

Gordon - - - 5,914 3.21 610 5,914 3.21 610

Burnt Timber - - - 1,021 1.40 46 1,021 1.40 46

Linkwood - - - 984 1.16 37 984 1.17 37

Total Lynn Lake 15,010 1.99 960 25,293 2.05 1,669 40,303 2.03 2,629

Esperanza 19,226 1.01 622 15,126 0.95 462 34,352 0.98 1,083

Ağı Dağı 553 0.44 8 34,334 0.46 510 34,887 0.46 518

Kirazli 118 0.50 2 5,848 0.43 80 5,966 0.43 82

Çamyurt 513 1.00 16 17,208 0.89 492 17,721 0.89 508

Total Turkey 1,184 0.68 26 57,390 0.59 1,082 58,574 0.59 1,108

Quartz Mountain 214 0.95 7 11,942 0.87 333 12,156 0.87 339

Alamos - Total 51,740 1.60 2,661 186,675 1.11 6,637 238,415 1.21 9,298

MEASURED AND INDICATED SILVER MINERAL RESOURCES (as at December 31, 2016)

Measured Resources Indicated Resources Total Measured and Indicated

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's)

La Yaqui Grande - - - 1,108 15 523 1,108 15 523

Esperanza 19,226 7.25 4,482 15,126 9.16 4,455 34,352 8.09 8,936

Ağı Dağı 553 1.59 28 34,334 2.19 2,417 34,887 2.18 2,445

Kirazli 118 2.73 10 5,848 2.17 408 5,966 2.18 418

Çamyurt 513 5.63 93 17,208 6.15 3,404 17,721 6.14 3,497

Alamos - Total 20,410 7.03 4,613 73,624 4.73 11,207 94,034 5.23 15,819

43

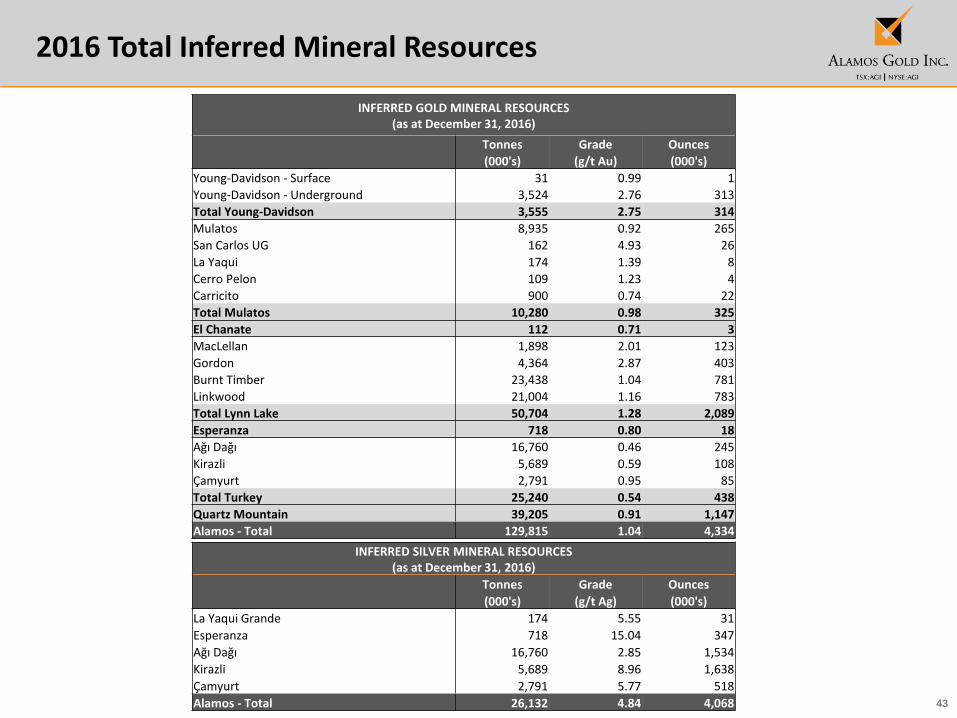

2016 Total Inferred Mineral Resources

INFERRED GOLD MINERAL RESOURCES (as at December 31, 2016)

Tonnes Grade Ounces

(000's) (g/t Au) (000's)

Young-Davidson - Surface 31 0.99 1

Young-Davidson - Underground 3,524 2.76 313

Total Young-Davidson 3,555 2.75 314

Mulatos 8,935 0.92 265

San Carlos UG 162 4.93 26

La Yaqui 174 1.39 8

Cerro Pelon 109 1.23 4

Carricito 900 0.74 22

Total Mulatos 10,280 0.98 325

El Chanate 112 0.71 3

MacLellan 1,898 2.01 123

Gordon 4,364 2.87 403

Burnt Timber 23,438 1.04 781

Linkwood 21,004 1.16 783

Total Lynn Lake 50,704 1.28 2,089

Esperanza 718 0.80 18

Ağı Dağı 16,760 0.46 245

Kirazli 5,689 0.59 108

Çamyurt 2,791 0.95 85

Total Turkey 25,240 0.54 438

Quartz Mountain 39,205 0.91 1,147

Alamos - Total 129,815 1.04 4,334

INFERRED SILVER MINERAL RESOURCES (as at December 31, 2016)

Tonnes Grade Ounces

(000's) (g/t Ag) (000's)

La Yaqui Grande 174 5.55 31

Esperanza 718 15.04 347

Ağı Dağı 16,760 2.85 1,534

Kirazli 5,689 8.96 1,638

Çamyurt 2,791 5.77 518

Alamos - Total 26,132 4.84 4,068

44

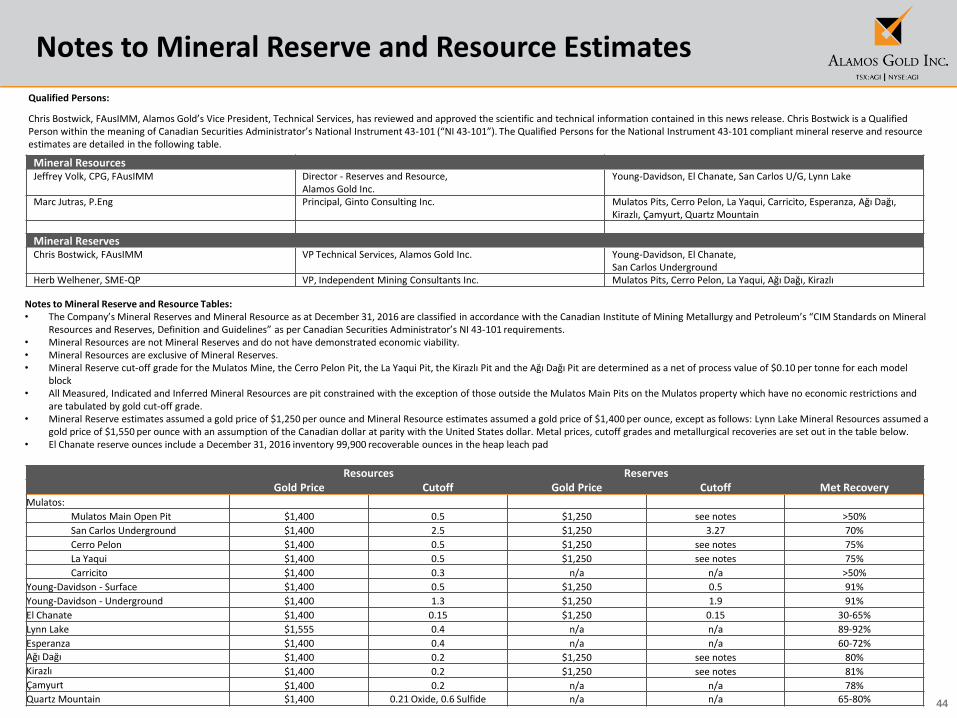

Notes to Mineral Reserve and Resource Estimates

Notes to Mineral Reserve and Resource Tables:• The Company’s Mineral Reserves and Mineral Resource as at December 31, 2016 are classified in accordance with the Canadian Institute of Mining Metallurgy and Petroleum’s “CIM Standards on Mineral

Resources and Reserves, Definition and Guidelines” as per Canadian Securities Administrator’s NI 43-101 requirements. • Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability.• Mineral Resources are exclusive of Mineral Reserves.• Mineral Reserve cut-off grade for the Mulatos Mine, the Cerro Pelon Pit, the La Yaqui Pit, the Kirazlı Pit and the Ağı Dağı Pit are determined as a net of process value of $0.10 per tonne for each model

block• All Measured, Indicated and Inferred Mineral Resources are pit constrained with the exception of those outside the Mulatos Main Pits on the Mulatos property which have no economic restrictions and

are tabulated by gold cut-off grade.• Mineral Reserve estimates assumed a gold price of $1,250 per ounce and Mineral Resource estimates assumed a gold price of $1,400 per ounce, except as follows: Lynn Lake Mineral Resources assumed a

gold price of $1,550 per ounce with an assumption of the Canadian dollar at parity with the United States dollar. Metal prices, cutoff grades and metallurgical recoveries are set out in the table below.• El Chanate reserve ounces include a December 31, 2016 inventory 99,900 recoverable ounces in the heap leach pad

Qualified Persons:

Chris Bostwick, FAusIMM, Alamos Gold’s Vice President, Technical Services, has reviewed and approved the scientific and technical information contained in this news release. Chris Bostwick is a Qualified Person within the meaning of Canadian Securities Administrator’s National Instrument 43-101 (“NI 43-101”). The Qualified Persons for the National Instrument 43-101 compliant mineral reserve and resource estimates are detailed in the following table.

Mineral ResourcesJeffrey Volk, CPG, FAusIMM Director - Reserves and Resource,

Alamos Gold Inc.Young-Davidson, El Chanate, San Carlos U/G, Lynn Lake

Marc Jutras, P.Eng Principal, Ginto Consulting Inc. Mulatos Pits, Cerro Pelon, La Yaqui, Carricito, Esperanza, Ağı Dağı,Kirazlı, Çamyurt, Quartz Mountain

Mineral ReservesChris Bostwick, FAusIMM VP Technical Services, Alamos Gold Inc. Young-Davidson, El Chanate,

San Carlos UndergroundHerb Welhener, SME-QP VP, Independent Mining Consultants Inc. Mulatos Pits, Cerro Pelon, La Yaqui, Ağı Dağı, Kirazlı

Resources ReservesGold Price Cutoff Gold Price Cutoff Met Recovery

Mulatos:

Mulatos Main Open Pit $1,400 0.5 $1,250 see notes >50%

San Carlos Underground $1,400 2.5 $1,250 3.27 70%

Cerro Pelon $1,400 0.5 $1,250 see notes 75%

La Yaqui $1,400 0.5 $1,250 see notes 75%

Carricito $1,400 0.3 n/a n/a >50%

Young-Davidson - Surface $1,400 0.5 $1,250 0.5 91%

Young-Davidson - Underground $1,400 1.3 $1,250 1.9 91%

El Chanate $1,400 0.15 $1,250 0.15 30-65%

Lynn Lake $1,555 0.4 n/a n/a 89-92%

Esperanza $1,400 0.4 n/a n/a 60-72%

Ağı Dağı $1,400 0.2 $1,250 see notes 80%

Kirazlı $1,400 0.2 $1,250 see notes 81%

Çamyurt $1,400 0.2 n/a n/a 78%

Quartz Mountain $1,400 0.21 Oxide, 0.6 Sulfide n/a n/a 65-80%

45

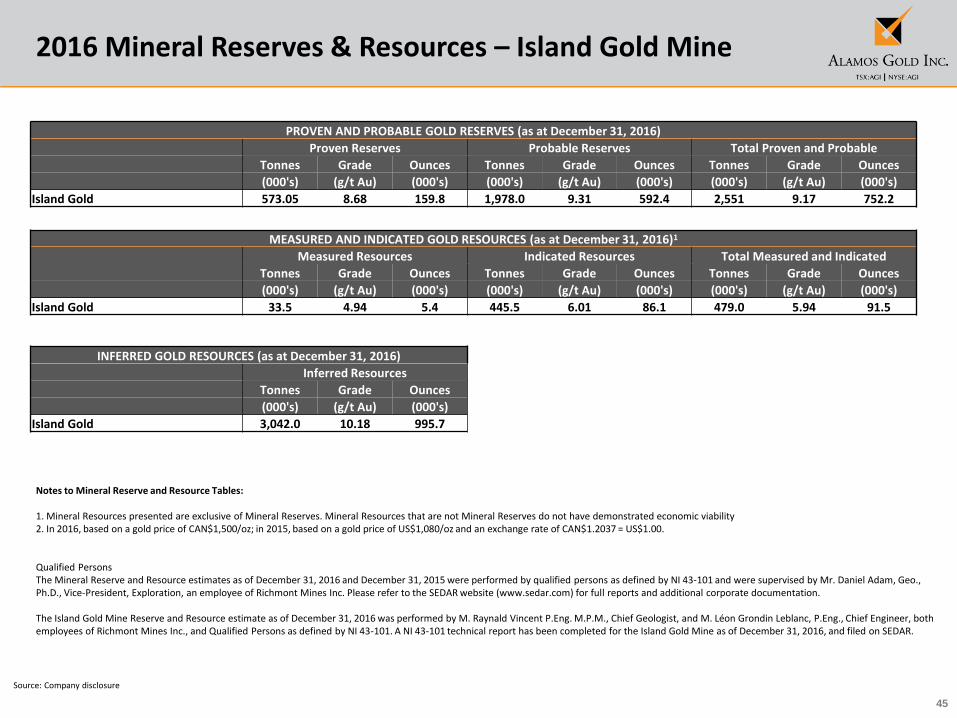

2016 Mineral Reserves & Resources – Island Gold Mine

PROVEN AND PROBABLE GOLD RESERVES (as at December 31, 2016)

Proven Reserves Probable Reserves Total Proven and Probable

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Au) (000's) (000's) (g/t Au) (000's) (000's) (g/t Au) (000's)

Island Gold 573.05 8.68 159.8 1,978.0 9.31 592.4 2,551 9.17 752.2

MEASURED AND INDICATED GOLD RESOURCES (as at December 31, 2016)1

Measured Resources Indicated Resources Total Measured and Indicated

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Au) (000's) (000's) (g/t Au) (000's) (000's) (g/t Au) (000's)

Island Gold 33.5 4.94 5.4 445.5 6.01 86.1 479.0 5.94 91.5

INFERRED GOLD RESOURCES (as at December 31, 2016)

Inferred Resources

Tonnes Grade Ounces

(000's) (g/t Au) (000's)

Island Gold 3,042.0 10.18 995.7

Source: Company disclosure

Notes to Mineral Reserve and Resource Tables:

1. Mineral Resources presented are exclusive of Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability2. In 2016, based on a gold price of CAN$1,500/oz; in 2015, based on a gold price of US$1,080/oz and an exchange rate of CAN$1.2037 = US$1.00.

Qualified Persons The Mineral Reserve and Resource estimates as of December 31, 2016 and December 31, 2015 were performed by qualified persons as defined by NI 43-101 and were supervised by Mr. Daniel Adam, Geo., Ph.D., Vice-President, Exploration, an employee of Richmont Mines Inc. Please refer to the SEDAR website (www.sedar.com) for full reports and additional corporate documentation.

The Island Gold Mine Reserve and Resource estimate as of December 31, 2016 was performed by M. Raynald Vincent P.Eng. M.P.M., Chief Geologist, and M. Léon Grondin Leblanc, P.Eng., Chief Engineer, both employees of Richmont Mines Inc., and Qualified Persons as defined by NI 43-101. A NI 43-101 technical report has been completed for the Island Gold Mine as of December 31, 2016, and filed on SEDAR.