agribusiness development - texas a&m universityafcerc.tamu.edu/publications/publication-pdfs/mrc...

TRANSCRIPT

RESEARCH REPORT lVRC 86-2

AGRIBUSINESS DEVELOPMENT DUVAL COlJNTY

PHASE I STUDY

----------~----'A'---DEPAR1MEI'....r OF AGRIOJLlURAL E(l)i\(M1CS IN CJX)PERATI ()N" WI 1H VCENfER ~ ECINMIC DEVEWH\.£NT L'NIVERSIT'{ OF TEXAS AT SA\; AN1Ul'HO

TEXAS A&M UNIVERSITY TEXAS AGRICULTURAL EXPERIMENT STATION TEXAS AGRICULTURAL EXTENSION SERVICE College Srallon. -exas

AGRIBUSINESS DEVELOPMENT DUVAL COUNTY, TEXAS

PHASE I STUDY

Prepared by Texas Agricultural Market Research Center

Task Force Comprised of

Texas Agricultural Experiment station Robert E. Branson

H.L. Goodwin John Heleman

Texas Agricultural Extension Service Gordon R. Powell

Robert B. Schwart, Jr. David B. Mellor

Fred D. Thornberry

Department of Agricultural Economics Texas A&M Univerity in cooperation with

Center for Economic Development Uuiversity of Texas at San Antonio

December 1986

THE TEXAS AGRICULTURAL MARKET RESEARCH AND DEVELOPMENT CENTER

An Education and Research Service of

The Texas Agricultural Experiment Station and

The Texas Agricultural Extension Service

The purpose of the Center to be of service to agricultural producers, groups and organizations, as well as processing and marketing firms in the solution of present and emerging market problems. Emphasis is given to research and educational activities designed to improve and expand the markets for food and fiber products related to Texas agriculture.

The Center staffed by a basic group of professional agricultural and marketing economists from both the Experiment station and Extension Service. In addition, support is provided by food technologists, statisticians and specialized consultants as determined by the requirements of individual projects.

Robert E. Branson Coordinator

- ii

Acknowledgements

s research was made possible by a grant from the Texas Department of Community Affairs. Judge Gilbert Uresti and the Duval County Commissioners Court were involved in the initiation of the study. The project was under contract with the Center for Economic Development, University of Texas at San Antonio. The Center is funded by a grant from the U.S. Economic Development Administration.

Appreciation is expressed for the cooperation of the Economic Development Office of Duval County and its staff members Alfredo Gonzales, Presc la Garza and Mary Lee Perez, who assisted in the agribusiness firms survey.

Thanks go also to Morrison Woods of the Center for Economic Development UT-SA, for his support in this project.

Finally credit is due to Janice Clark for her considerable efforts in preparing the report for printing with the assistance of other Department of Agricultural Economics staff members.

- 111

TABLE OF cnNTENTS

Page

Purpose of the study . . . . . . . . . . . . . 1 Eoonomio D9soription of Duval C01.Ulty . . . . . 1 The Economic D9veloprrent Analysis Plan . . . . 6 Alternative AgribusineSs System Opport1.IDities 20 Preliminary Fea.sibility Analysis of Milk ProceSSing in Duval C01.Ulty 21

The Market 22 Operating Costs . . . . . . . . . . . . 25 Employnent Impact . . . . . . . . . . . 26 Startup Costs . . . . . . . . . . . . . 29 Raw Milk Supplies aIXi Procu.reIOOIlt Costs 30 SUmming up Cost . . . . . . . . . . . . 33

Results of the Agribusiness Firms Survey . . 33 Kini or 'IY.J?e of Agribusiness Estahlishnent 35 Where Supply Purchase D3cisions are Made . 35 Geographio Location and 'I'yp3 of Supplier . 39 Trade Area Se:r'VOO. am Business Ex:pansiOIl Plans 45

Egg Production-Marketing . . . . . . . . . . . 47 Egg Production-Marketing Unit . . . . . . 53 Egg Marketing Strategy Requirenents . . . 53 Cost of a Production-Marketing Eco-System 54

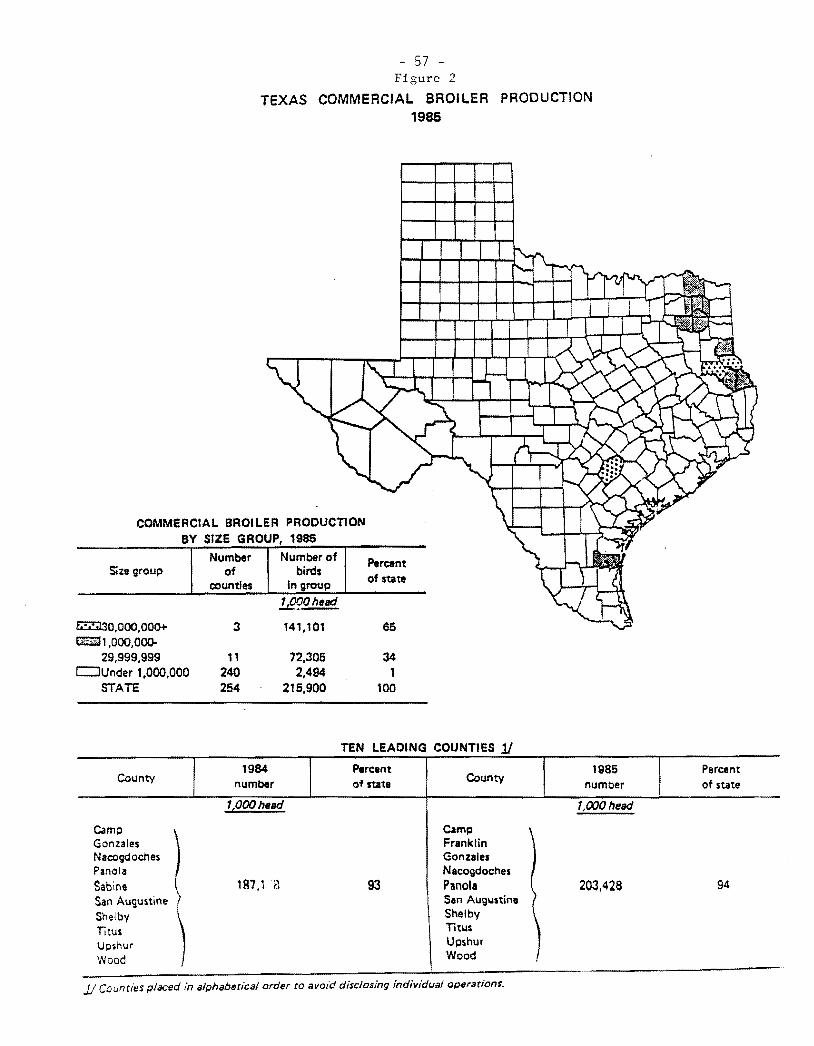

Poultry Prcrluction-Marketing . . . . . . . . 55 Market Size and Strategy . . . . . . . . 55 Cost of Production-Marketing Eco-System . 56

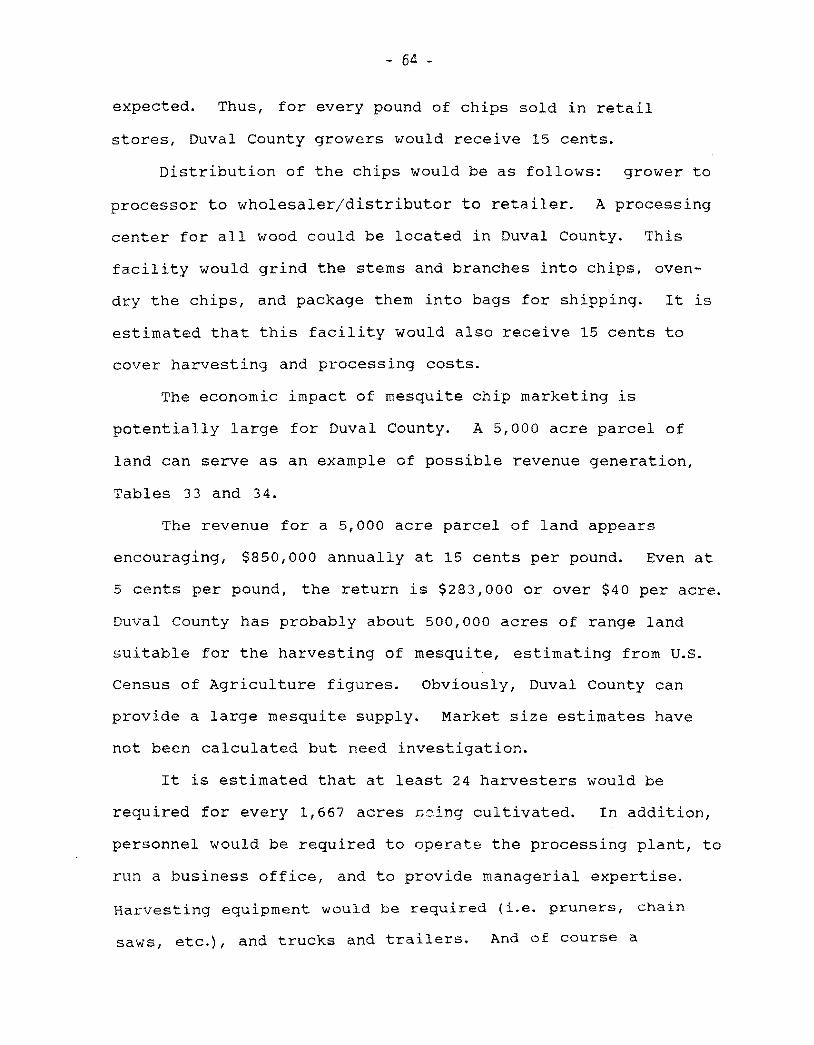

'l'hE;! COlTlIIV3rcial utilization of Mesquite as a Revenue Source for Duval County . . . . 58 Type of Crop Growth . . . . . . 60 Number of Trees per Acre 60 Plant Growth cycle . . . . . . 61 Care and Managenent of the Crop 61 Harvesting . . . . . . . . . . 62

Horticultural La.rxiscape Plants . . . 66 The Production-Marketing Systems 66 Costs and Returns Estimate 67

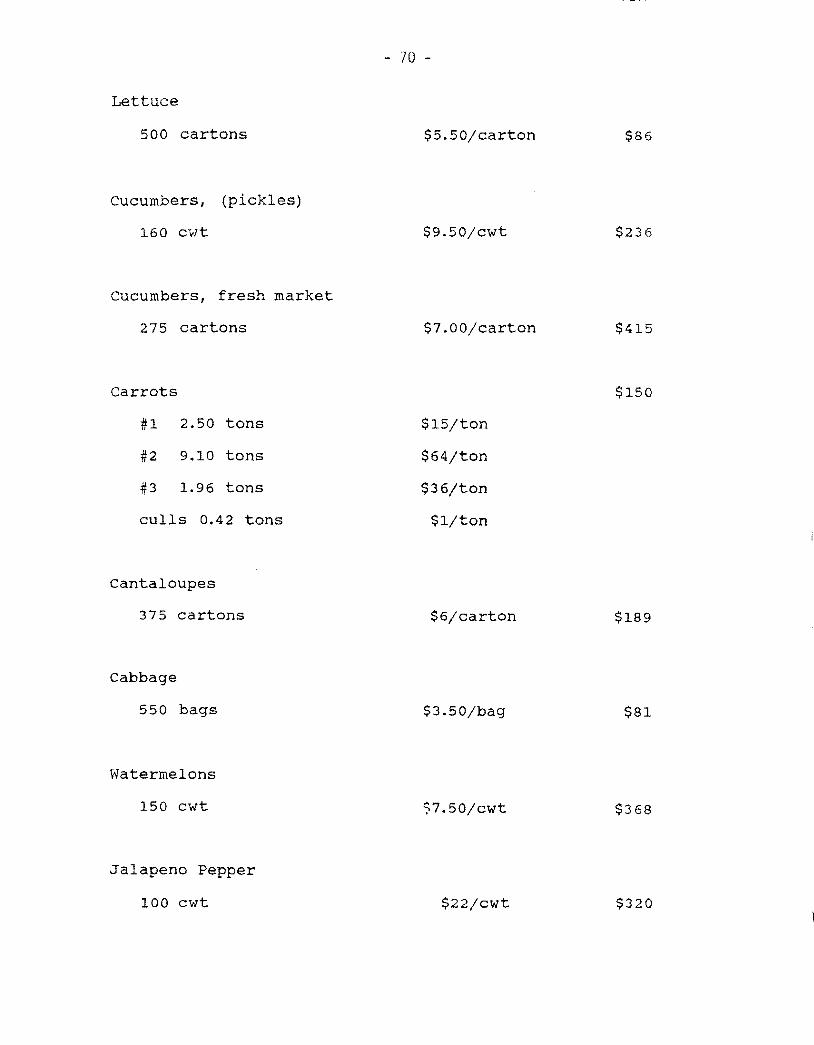

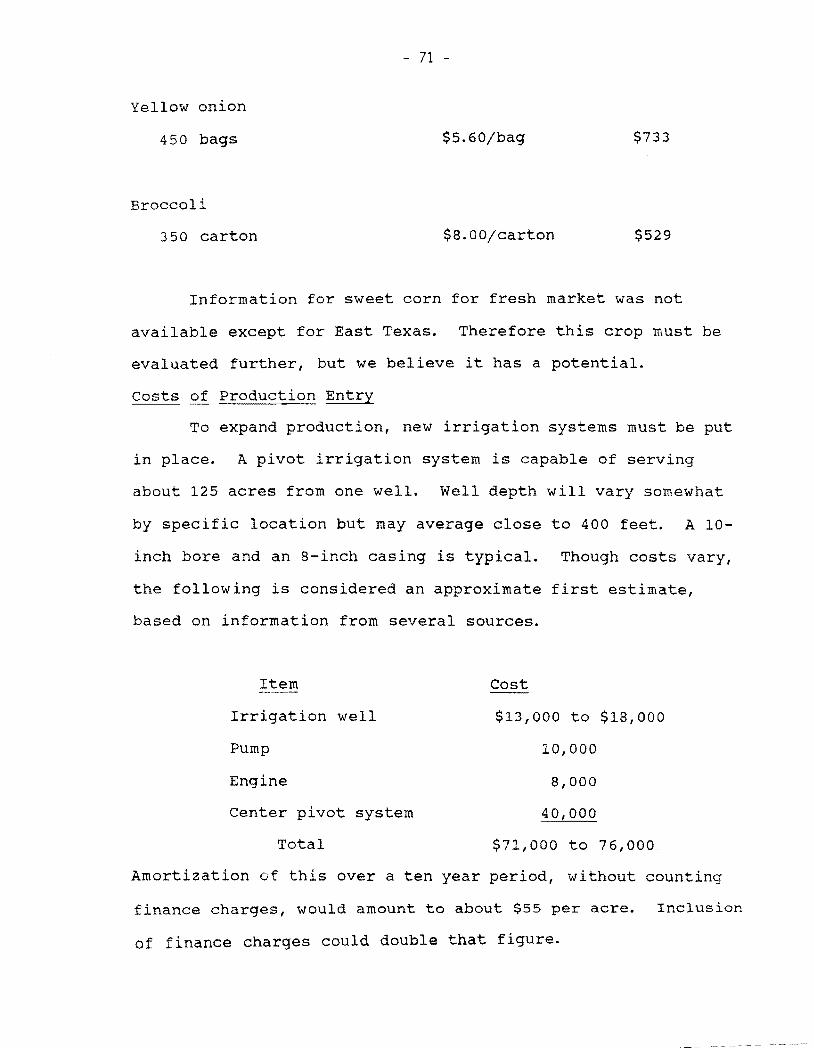

Vegetable Production-Marketing 68 Costs of Prcrluction Entry 71 Marketing Fa.cilities . . 72

- iv

LIST OF TABLES

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

Agricultural Primary Incazre Sources Duval County 1980 and 1984 . . . . . . . . 3

Business Firms Summa.ry DuvaJ. County 1972 and 1982 . . . . . . . . . ..... 4

Emp10ynent by Business Category DuvaJ. County, First Quarter 1980 arrl 1986 . . . . 5

Age Distribution of DuvaJ. arrl Jim Wells County Population, 1985 . . . . . . 7

Incazre levels of DuvaJ. COunty ani Te:xa.s Households, 1985 . . . . . . . . . . 7

Population of DuvaJ. and Nearby Counties, 1970 to 1990 . . . . . . . . . . . . 13

Population of IndicatOO Cities-DuvaJ. County and Mjacent Counties ........ . 14

Estimatoo Market Size for Indicatoo Prcxiucts Duval County Primary Market. . . . . . 16

Prcxiuction Output Per U1.y to Equal Market I:emand-Se1ectOO Focxi Prcxiucts . . . . 17

Estimatoo Fluid Milk COn.sumption by Month and Year for Duval COunty Region, 1985 24

Range in Cost Per Gallon for Se1ectOO Account Items, All Fluid Milk Plants, Unitoo States, 1986 27

Costs of Op3rating a Typica.l Small to Me1ium Size Fluid Milk Processing Plant, Unitoo States, 1986. 28

Seasonal Index of caw Milk Prcxiuction .. 32

Location of Firms Surveyed by City. 1985. 32

Kinds of Firms Surveyed in Agribusiness Study for DuvaJ. County, 1986 .... 36

Location of Agribusiness Firm Ownership, DuvaJ. COunty Study, 1986 . . . . . . 37

Kind of Business Managenent, DuvaJ.. County Study, 1986 37

- v

LIST OF TABLES (Cont I d)

18 Where Prcrluct Procurerrent D3cisioIlS are Made, Duval County. 1986 . . . . . . 38

19 Geographio Sources of Purchased Supplies. Duval County Business Establisbnents, 1986 . . . . . 40

20 Geographio Sources of Purchased Supplies, Alice Business Establishments, 1986 ............... . 41

21 'I)rpe of Supplier to AgribusineSS Establishments, Duval County, 1986 . . . . . . . . . . . . . 43

22 Type of Supplier to Agribusiness Establishments. Alice, 1986 ............ . 44

23 Trade Area Servai. Duval COunty Agribusiness Establishments, 1986 . . .. . . . 46

24 Trade Area Servai, Alice Agribusiness Establishments, 1986 . . . . . . . 46

25 Number of Years in Business, Agribusiness Establisb.loonts, 1986 . . . . . . . . . 48

26 Plans for Business Expansion by AgribusineSS Establisb.loonts, 1986 . . . . . . . . . . 48

27 L:iInitations to Business Expansion, AgribusineSS Firms, 1986 . . . . . . . . . . . . . . . 49

28 Kind of Business Expansion Assistance Needed by Agribusiness Establishment, 1986 49

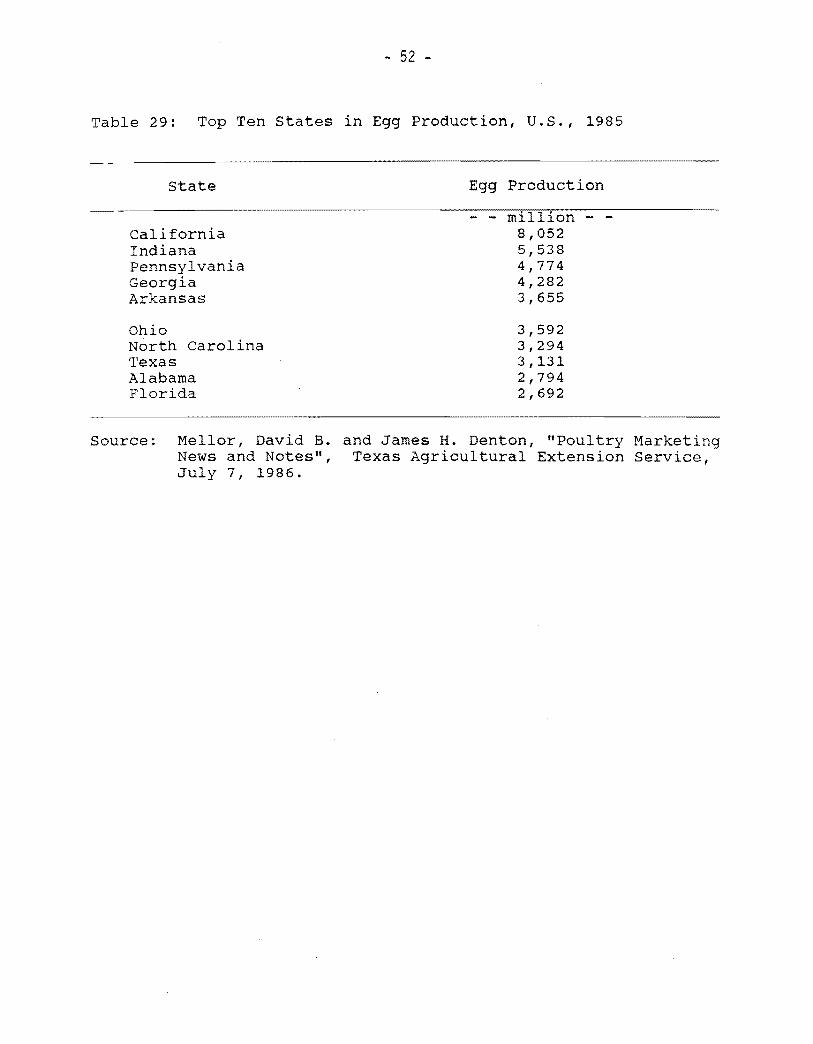

29 Top Ten States in Egg Prcrluction, U.S., 1985 . 52

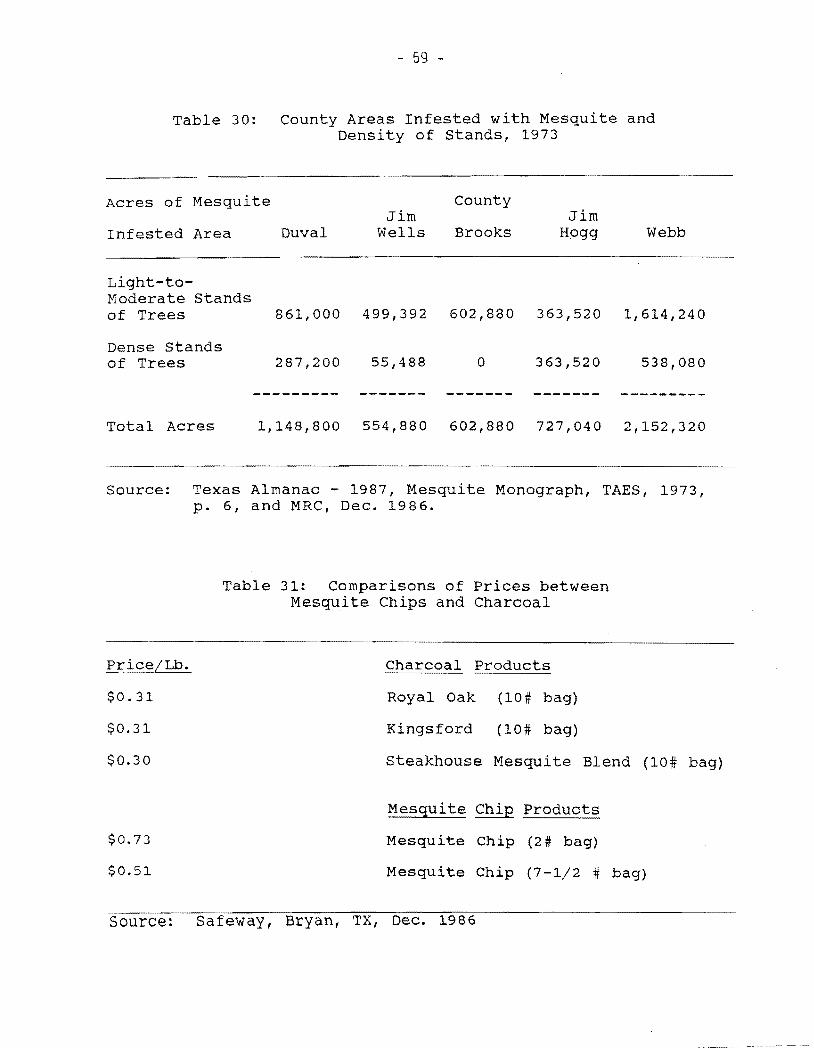

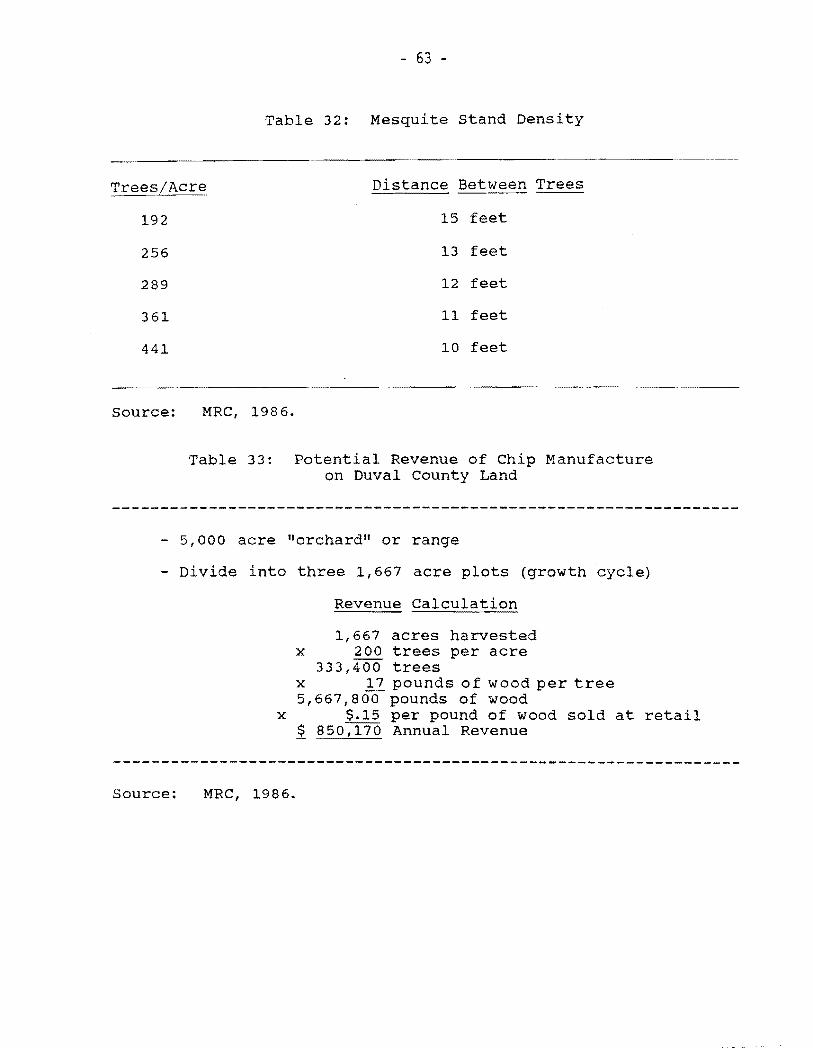

30 County Areas In£ested with Mesquite and D:msity of Stands, 1973 . . . . . 59

31 Comparisons of Prices Between Mesquite Chips and Charooal, 1986 59

32 Mesquite Stand D:msity . . . . . . . . 63

33 Potential Revenne of Chip Manufacture on Duval County Land . . . . . . . . . 63

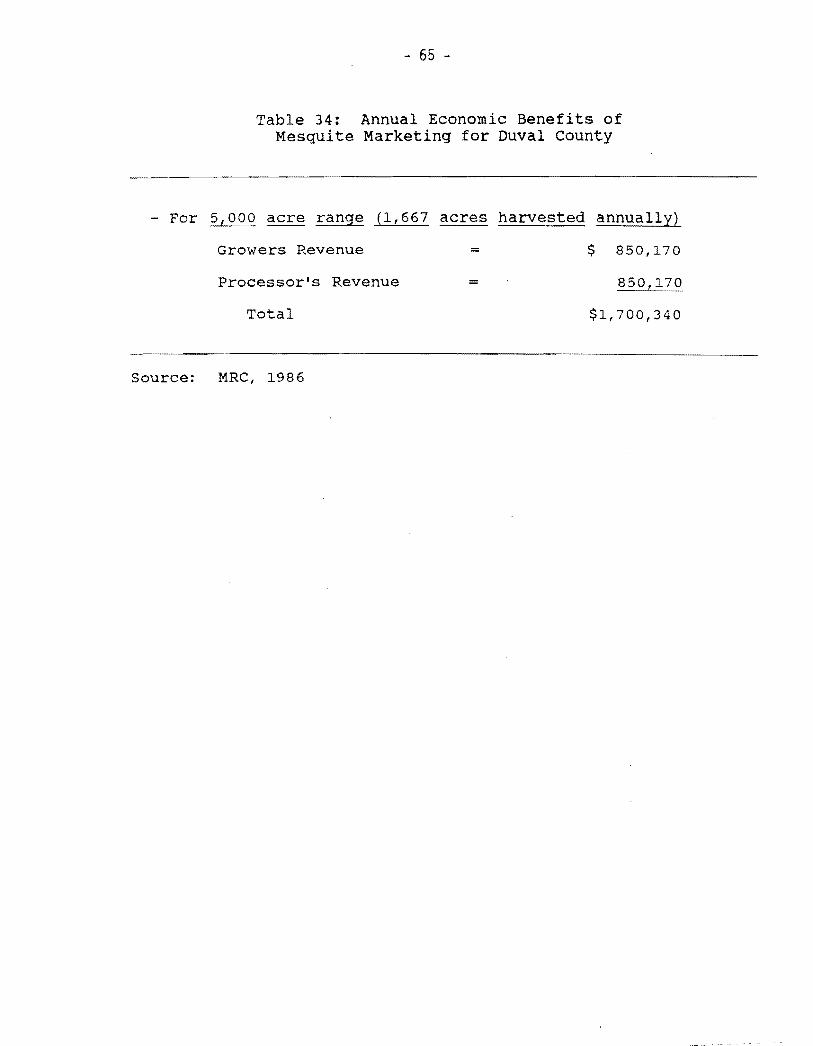

34 Annual Eoonomio Benefits of Mesquite Marketing for Duval County Marketing for DLlVal County . . . . . . . . . . . . . . .. 65

- vi -

LIST OF FIGURES

Figure ~e

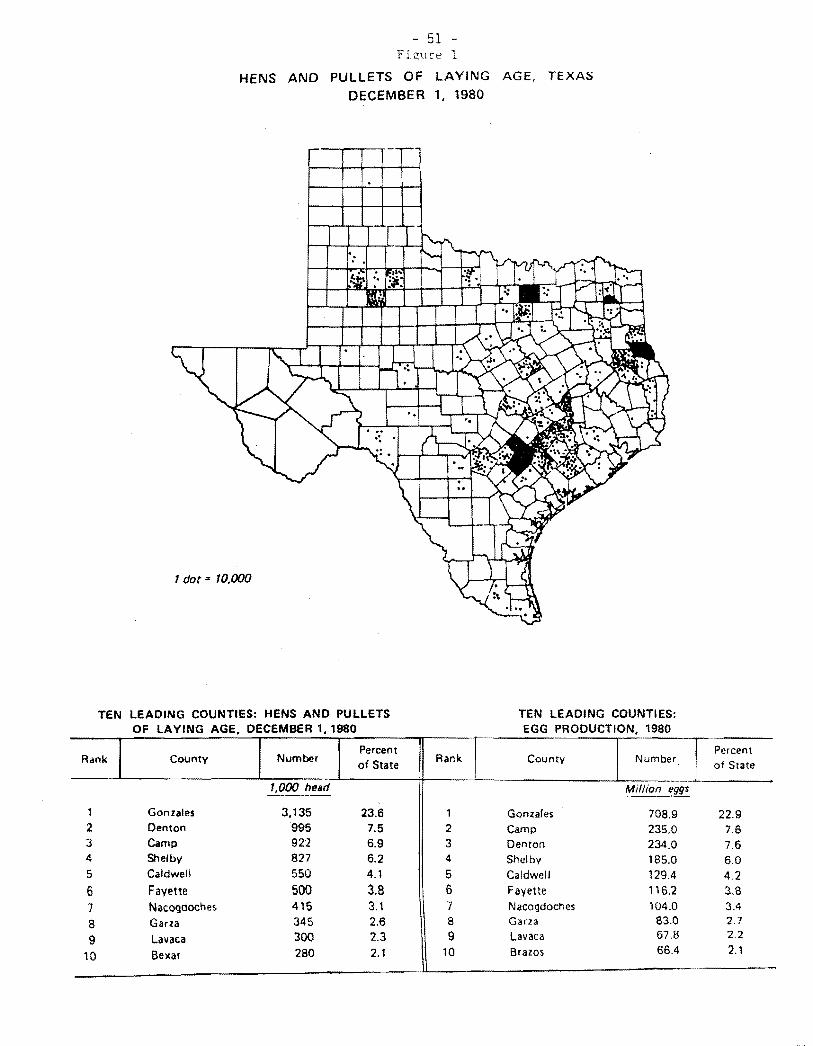

1 Hens Pullets of Laying Age, Texas, 1980 . 51

2 Texas Commercial Broiler Prcx:luction, 1985 57

- vii

DUVAL COUNTY

AGRIBUSINESS ECONOMIC DEVELOPMENT

PHASE I RESEARCH REPORT

EXECUTIVE SUMMARY

Research Objective

The objective of this research was to provide an overview

analysis of the potential for increasing the economic base in

Duval county. The county previously has not been addressed by

such an analysis. In 1982, a retail trade study was made to

determine the presence of shopping out of the county by Duval

residents. The objective was to establish some indications of

what retail establishments were possibly needed and

recommendations were made for an audit of the existing

establishments to seek ways of increasing their marketing

skills versus outside competitors. Therefore the present

agribusiness study is a further commitment toward seeking the

means of improving the economy of Duval County through

expansion of its agribusiness potentials.

The Research Need

The instructions for this agribusiness analysis as

- V111

provided to the Texas Agricultural Market Research center at

Texas A&M University by the Economic Development Center,

university of Texas at San Antonio may be summarized as

follows.

1. Duval county is recognized as one of the less

developed areas of the state in terms of its record of

economic progress and the prevalence of a relatively high

rate of persistent unemployment. Conditions have been

worsened by the major economic recession, if not outright

depression, in the oil and gas industry and in agriculture

in Texas. These unfavorable developments reflect both

national and international difficulties in these two major

sectors of the overall economy.

2. In view of the economic conditions in Duval County

there is urgent need for the development of expansion of

agribusiness activity where promise of profitability

appears possible. To do so would add to personal and

business incomes in the County and, if properly directed,

should provide increased employment opportunities in the

area.

3. It was indicated that Duval County could qualify

for federal economic development aids for depressed areas.

The greatest need was centered in the central and southern

portions of the county, in the area in and adjacent to the

- IX

city of Benavidas.

4. The question posed was whether a potential existed

for the development of an agribusiness park, as contrasted

to a general industrial park, in the Benavidas area of

Duval County. However, any potential elsewhere in the

county should also be considered and addressed.

The Research Plan

several facets were developed by the Market Research

Center for the research plan.

1. Three field trips were made to Duval County and

the adjacent areas in order to obtain familiarity with the

general economy and the communities involved. In these,

discussions were held with the relevant government

representatives in the Economic Development Office, County

political representatives, the agricultural county agent,

and those in the local U.s. Department of Agriculture office

of the Agricultural Stabilization and Conservation service.

2. A further facet of the field trips was to contact

selected agricultural marketing firms in order to

determine what marketing channels were available to serve

the Duval county area. This involved primarily contacting

- x

firms in Jim Wells, Webb and Nueces counties, where

marketing firms are located in or near the cities of

Laredo, Alice and Corpus Christi. Further contacts were

made in Pearsal (Frio County) and in Uvalde (Uvalde

County) .

3. A review was made of the agricultural production

data for crops and livestock as reported by official

government sources. Present levels as well as trends in

production were evaluated.

4. An analysis was made of population and income

levels and the direction of movement in these in recent

years for Duval, Brooks, Jim Hogg, Jim Wells, Webb,

McMullen and Nueces counties. Data from the Bureau of

Economic Analysis of the U. S. Department of Commerce and

from the ~~~y.§y of ~~yi!:!9. f~~.§~ report of Sales and

Marketing Management were both reviewed.

5. Demand estimates for selected food products in

Duval County and the surrounding areas were prepared. In

these, consumer purchase rates as reported by the National

Consumer Expenditure Surveys of the Bureau of Labor

statistics and the Food Consumption studies of the U. S.

Department of Agriculture were utilized.

6. The expertise of personnel on the research task

- Xl

force for this study was utilized to evaluate several

alternative agribusiness enterprises as to their possible

potential in Duval county.

7. General cost budgets for several potential

agricultural crops were obtained and adapted to conditions

in Duval county.

8. Finally a special survey was made of the

principal agribusiness firms in Duval and Jim Wells

counties. The objective was to obtain a measurement of the

volume of agribusiness products moved through existing

operating firms.

Establishments were surveyed that belonged to the

following ten categories of business:

Fast food establishments

Restaurants

Institutional food services

Grain and feed dealers

Livestock auctions

Farm supply firms

Farm equipment dealers

Food super markets

Drive-in food markets

Food processing establishments

- xii

Research Conclusions

and Recommendations

** Development of any broadly based agribusiness park

in Duval County does not appear feasible, based upon the

findings of this Phase I study overview of the local

area resources, and the market demand that can be

brought to bear in the County.

** The above conclusion, however, does not mean

that Duval County is lacking economic development

opportunities. Several of these are outlined in the

following conclusions. Similarly some are highly

improbable.

** The potential for a small beef slaughter plant is

not favorable because of three negative factors.

1. The major part of the beef retail sales in the area are

through supermarket food stores.

2. Of the supermarket food stores in the immediate or

closely adjacent area, the dominant volume ones are

members of a major food chain. That means that highly

specific quality standards are used in buying dressed

beef. The major food chain in Alice, Texas markets

- X!ll

beef from grain fed cattle, U.S. Choice grade, probably

yield grade 3 or better.

3. Cattle sold from local ranchers are mostly stocker calves or

yearlings and not suited for a beef processing

plant in Duval County. These animals move on to heavy

pastures and to feedlots elsewhere in Texas before going

to a packing plant.

4. Cattle feeding is not generally present in the area.

Therefore slaughter weight fed cattle of 1,000 to 1,200

pounds are not available. Local auctions are markets

for stocker calves going back to ranches and mid-weight

feeder animals going to feed lots. These classes of

animals do not usually provide either competitively

priced beef or the quality needed.

5. The volume of fresh beef sold through retail market

outlets in San Diego, Freer, Benavidas and Alice (Jim

Wells County) is not sufficient to support an

efficient small beef slaughter plant.

** specialized canned, or frozen type, food processing plants

are out of the question. The production base for raw

material supply is not available in adequate supply to

support the large size plants necessary to be competitive

or efficient in present day markets.

- xiv

** Given the foregoing competitive status of Duval County,

it is necessary to consider the possibility of specialized

product processing and marketing that can be keyed to

existing agricultural resources and marketing channels.

Another alternative is have only selected very small,

custom processing facilities that can survive on

the small nearby market demand. Other opportunities than

those are worth consideration and would contribute to an

agribusiness park.

** Duval County presently has watermelon production that has

persisted over a number of years. The Phase I survey

suggests that there is a potential to expand production and

marketing of this product. Interviews with existing

produce marketing firms serving the areas indicate that an

increased supply from Duval County would be desirable.

Producers need assistance on marketing contracts.

Crop production budgets of Texas Agricultural

Extension Service relevant to South Texas indicate that

dryland watermelons can return, on an average over a period

of years, between $130 and $225 net profit per acre.

Irrigated land has the potential of returning $200 to $340

per acre. These figures assume a land return,

additionally, of $30 to $40 per acre. Prices can vary

considerably from year to year. Therefore finances should

be such that success depends not on a single year's

- xv

operations, but rather the average over a period of years.

** Another vegetable crop that shows! on a preliminary

assessment basis, an excellent potential is the growing of

broccoli. The market demand for this crop has been

steadily increasing nationwide for the past several years.

Preliminary indications are that a net returns of from $400

to $BOO per acre are achievable. This is in addition to a

$30 to $40 per acre return to the land used.

** Further irrigated crops that should be considered are the

following:

CROP Net Return Per Acre

Spinach $-13 to $603

Peppers $-67 to $217

Sweet corn $603

cantaloupes $-74 to $337

** Increased production of irrigated vegetable crops will

require an expansion of the present vegetable acreage in

southeastern Duval County. Whereas some B,OOO acres were

reported in earlier years, the more recent total is about

3,000 acres. It is possible that production and harvesting

practices need to be reviewed and brought up to current

state-of-the-art standards in order to be competitive. It

appears that the minus returns (losses) indicated by one

- xvi

research source reflect the use of overly conservative

product prices. The upper levels were based on ten-year

price averages, using the latest U. S. Department of

Agriculture reports.

** Budgets for the above crops reflect as nearly, as possible,

currently reported operating costs. These have been

adjusted upward to reflect the cost of newly installed

irrigation systems. Contacts made with Texas Agricultural

Extension specialists and commercial equipment dealers

indicate that a new pivot irrigation system will cost

$60,000 to $80,000. These are designed to be ten inch

wells with eight inch pipe casings capable of irrigating a

quarter of a section of land, or 100 to 125 acres. The

cost of the systems were amortized over a ten year period.

** It is strongly cautioned that none of the above or

following preliminary findings are considered either

sufficiently accurate or complete enough to warrant their

use without a further detailed, in depth production

enterprise study and analysis, such as would be included in

a Phase Two economic feasibility development study.

** Initial estimates of demand for poultry (broilers) were not

favorable to any further consideration as a profitable

broiler production enterprise. However it was subsequently

determined that a broiler growing cooperative has a unit

- xvii

member near Kingsville, Texas. Processing occurs at a

plant outside the area which also serves other cooperative

members. This raises the possibility that a broiler

growing facility tied to that cooperative might be

considered for Duval county.

Market analysis does not show sufficient local or

nearby demand to justify a broiler processing plant. Such

plants are now relatively large scale operations that

require sufficient volume to warrant a full-time federal

inspection crew that inspects each bird and certifies its

food use safety.

Feeding rations are predominantly grain sorghum,

production of which occurs in Duval, and other feed

supplies would be available from Corpus Christi sources.

** An egg production facility has potential and should also be

evaluated. Though an optimum size operation is at least

250,000 hens, size is not as critical as in broiler

processing. The egg production facility would operate its

own washing, grading and packing plant on or near the

premises. The growing population of South Texas and the

more likely possibility of marketing to food chains makes

this worth consideration.

Establishment of a local area brand of fluid milk produced** by a comparatively small, fluid milk only, processing plant

offers another possibility for consideration in Duval

- xviii

county. The sales volume of the local area market, already

served by at least four brands, is not large enough to

support a plant, so market entry and product distribution

would have to be established over a mUlti-county area.

Advertising support would be a necessity in order to

establish and support market entry into Corpus Christi,

Kingsville and Laredo as well as in the local area.

possible sales to military bases in South Texas is another

option. This agribusiness possibility is based on the

current presence of some dairying in Duval County and the

success of similar based enterprises elsewhere in Texas.

** Ranchlands in this portion of the state abound with

mesquite trees, which are an obstacle to grass production

on rangeland. This agribusiness study has determined that

marketing channels are in place and available to harvest

mesquite for the charcoal cookery market nation-wide.

Contract arrangements are necessary between the harvesting

firm and local ranch owners. Future systems of mesquite

production and harvesting are presently being researched.

** Texas sage harvesting, culture and marketing is a

relatively recent development. This plant is a premium

priced item at landscape nurseries and plant retail

establishments. Originally thought not to be

transplantable, this now is not the case. Consideration

should be directed toward harvest of the abundant stock of

- xix

native sage plants in the Duval and nearby county areas. A

wholesale nursery or nursery supply business should be

given consideration for the business park.

Implications for an

Agribusiness Park

** Some of the foregoing agribusiness possibilities are not

well adapted to an agribusiness park concept. However,

several are. Based upon an analysis of the market data

generated in this Phase I study, the following park

location possibilities could be considered.

(1) Fruit and vegetable

packing shed and hydrocooler

(2) Mesquite harvest

assembly and shipping facility

(3) Egg grading and

packing facility

(4) Fluid milk processing plant

Except for the mesquite handling facility, these facilities

- xx

would be utilizing production primarily from the southeastern

section of Duval County. Because of the road network in the

county, development of the agribusiness park in or near

Benavidas or San Diego appears to be a feasible location.

Agribusiness Development

cautions and Problems

** None of the foregoing enterprises should be attempted

without a detailed feasibility study of whichever ones are

selected for further consideration. Detailed feasibility

studies are costly and should not be initiated until the

recommendations in this report are reviewed, discussed and

evaluated in terms of whether there are people, finances, and

sufficient business expertise that could be available, or

possibly obtainable, to assure the success of any of the

selected ventures.

** Capital requirements are sUbstantial for some of the

proposed agribusinesses. preliminary discussions would be

essential to ascertain what funding sources are available and

under what conditions and terms. Insufficient capital to see a

business through the initial years of business development is

one of the major causes of new business failures.

** Some of these marketing facilities are large users of

water and generate a sUbstantial amount of waste water

- XXI

requiring sewage plant treatment. These costly facilities must

be provided for the agribusiness park, or the city must have

such facilities already available.

Employment Impact

** Several economic development possibilities were eliminated

because the market research findings did not indicate

sufficient market potential for their success. Of the set of

possibilities discussed herein, most are more capital intensive

than labor intensive. Consequently the monetary flows

generated are low generators of local employment. Also some,

such as the vegetable (including watermelon) production and

marketing are seasonal in nature. It is strongly recommended

that opportunities for substantial employment be sought in the

manufacturing subcontracting businesses. Thus both

agribusiness and general manufacturing possibilities should be

pursued simultaneously.

- xxii

I

Duval County

Agribusiness Feasibility study

Purpose of the study

It has become increasingly evident that business and

economic development seldom spontaneously happens. Expansion

of the economic base of a city, county, or state, usually

results from intensive analysis, research, preplanning,

promotional and developmental effort. That effort preferably

starts with an audit of the basic resources of the target

area. A target area's resources consist not only of those on

the supply side but also those on the demand side. The purpose

of economic and market research, in these instances, is to

target any existing inefficiencies and missed opportunities in

the optimum coordination of the supply and demand of goods and

services.

The purpose of this particular study is to identify

economic development opportunities for Duval County and the

potential market area it can serve. This is a report for Phase

which is directed at identifying what are considered to be

principal economic development opportunity possibilities. Any

decision to undertake detailed feasibility studies of any of

the specific opportunities would be the task of Phase II, a

further project. Only Phase I was contracted for at this time.

Economic Description

of Duval County

Duval County is located in South Texas about midway between

- 2

Corpus Christi and Laredo. It is basically an agricultural

county with ranching the principal activity. A more

diversified agriculture, including dairying and field crops of

grain, hay and vegetables is in the southeastern part of the

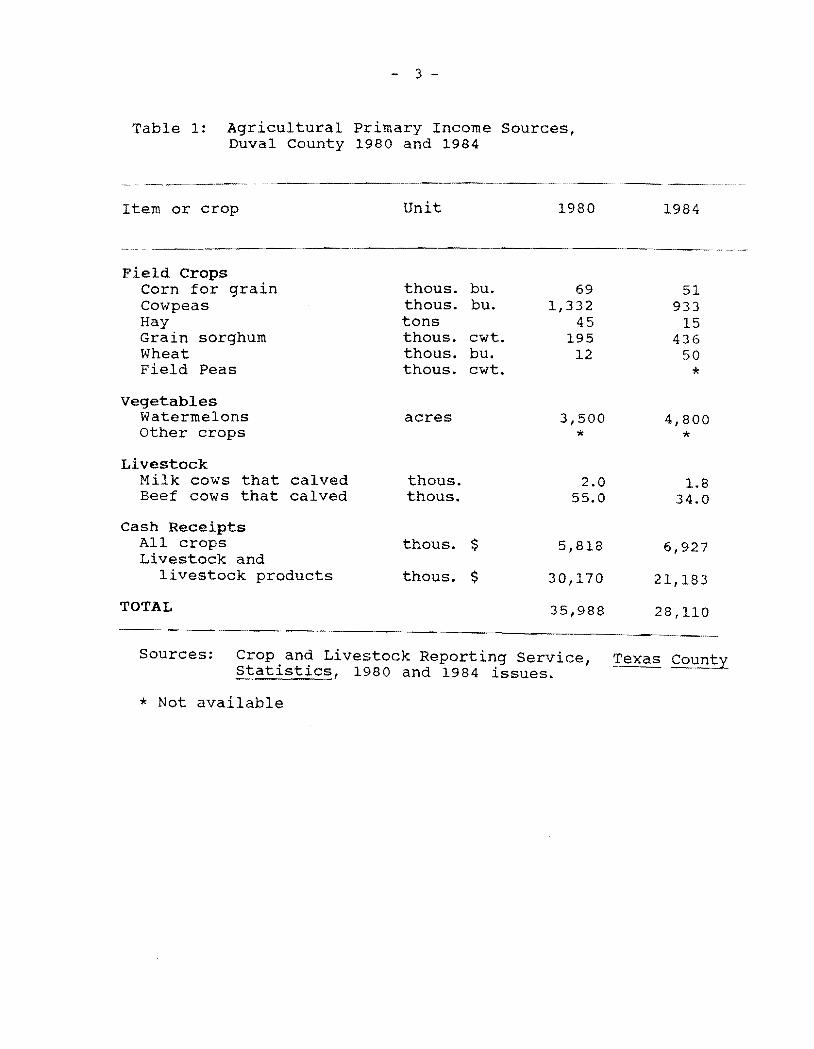

county. The primary agricultural income sources are noted in

Table 1, which affirms the predominance of agricultural income

from livestock. Ranches operate with commercial herds, usually

cross-bred herds of cattle. Beef cows that calved dropped from

55,000 to only 34,000 between 1980 and 1984. Vegetable

production, which has declined, grain crops and some dairying

is limited at the present to the southeastern section of the

county. The number of calving dairy cows decreased somewhat,

but probably was offset by the general trend for more milk

production per cow in the dairy herds.

Non-agricultural economic activity in Duval County is of

limited size. Business establishments primarily serve the

local population, which totals only about 13,000 persons.

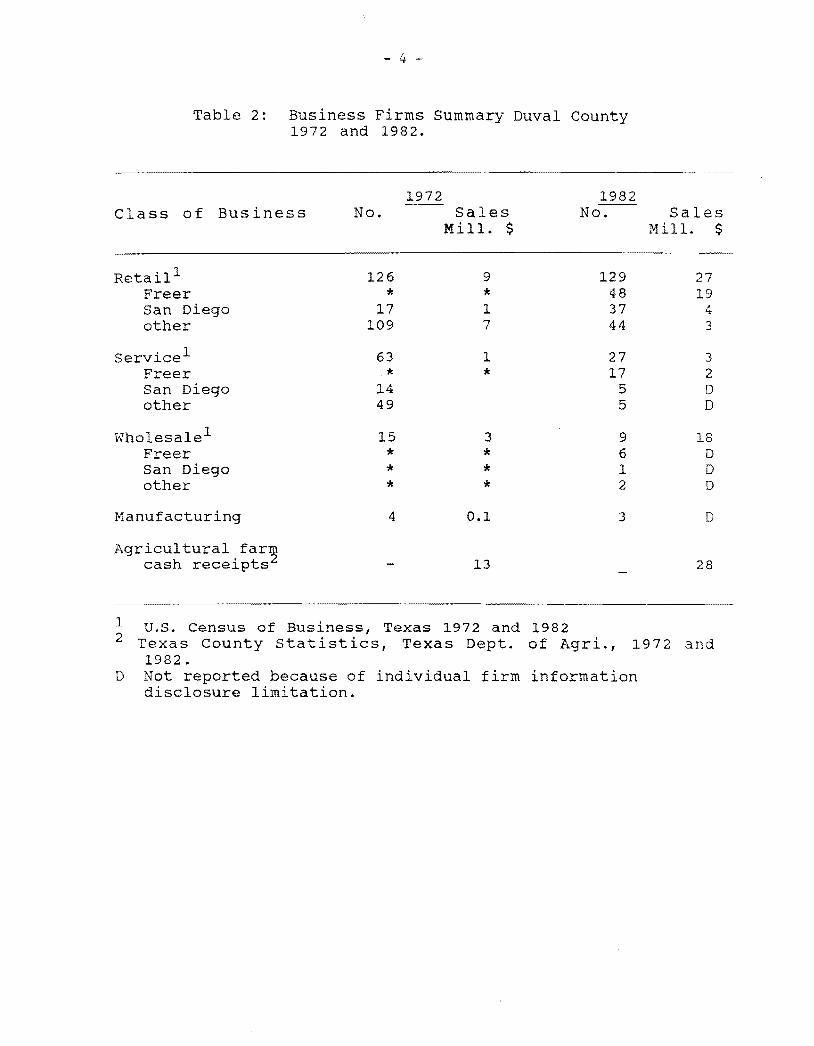

Manufacturing and service sales are also small, Table 2.

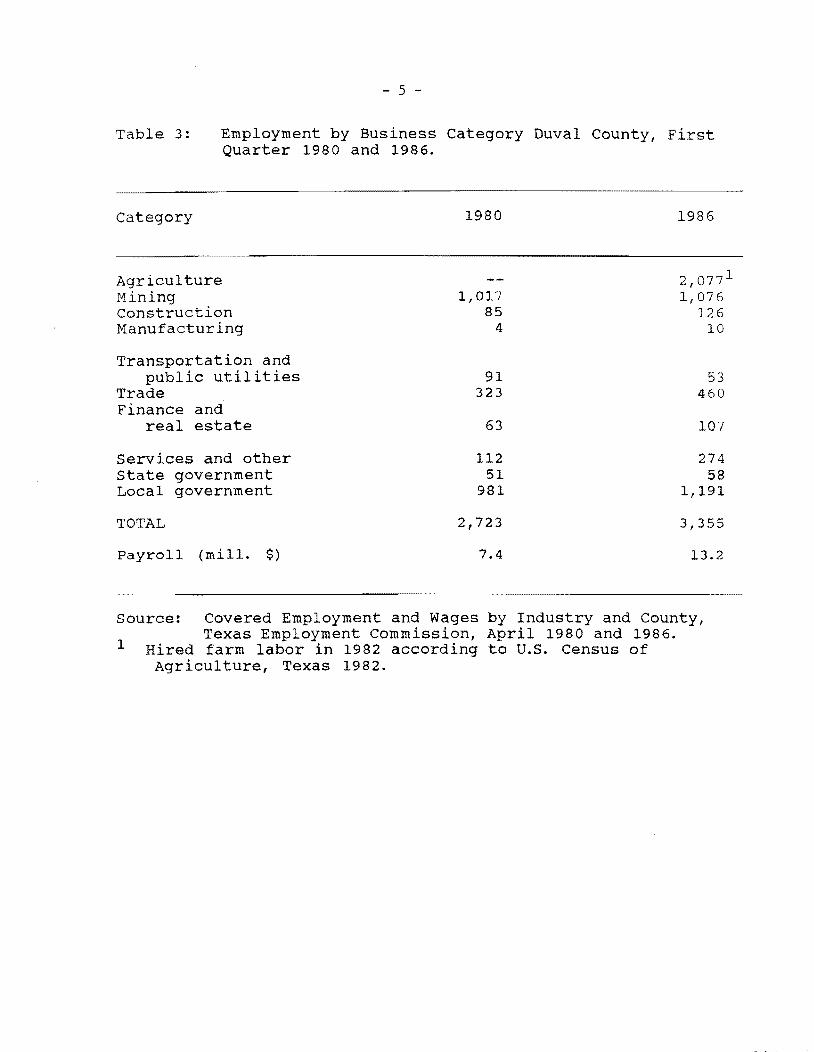

Employment in April 1986 totaled 3,355, with most of that being

associated with the oil industry (mining), and governmental

offices and services, Table 3. with both of these sectors

under economic pressure, there is a clear need for a broader

economic base. These figures ac not include agriculture.

Duval, according to the U.s. Census of Agriculture, had 1,074

farms or ranches in 1982, with an average of 904 acres. The

number of farm/ranches was up fractionally and the average size

was slightly less than in 1978.

3

Table 1: Agricultural Primary Income Sources, Duval county 1980 and 1984

Item or crop Unit 1980 1984

Field Crops Corn for grain Cowpeas Hay Grain sorghum Wheat Field Peas

thous. thous. tons thous. thous. thous.

bu. bu.

cwt. bu. cwt.

69 1,332

45 195

12

Vegetables Watermelons other crops

acres 3,500 *

Livestock Milk cows Beef cows

that calved that calved

thous. thous.

2.0 55.0

Cash Receipts All crops Livestock and

livestock products

thous.

thous.

$

$

5,818

30,170

TOTAL 35,988

51 933

15 436

50

*

4,800 *

1.8 34.0

6,927

21,183

28,110

Sources: Crop and Livestock Reporting Service, Texas Countystatistics, 1980 and 1984 issues.

* Not available

- 4

Table 2: Business Firms Summary Duval County 1972 and 1982.

1972 1982 Class of Business No. Sales No. Sales

Mill. $ Mill. $

Retail 1 126 9 129 27 Freer * * 48 19 San Diego 17 1 37 4 other 109 7 44 3

service1 63 1 27 3 Freer * * 17 2 San Diego 14 5 D other 49 5 D

Wholesale1 15 3 9 18 Freer * * 6 D San Diego * * 1 D other * * 2 D

Manufacturing 4 0.1 3 D

Agricultural far~ cash receipts 13 28

1 u.S. Census of Business, Texas 1972 and 1982 2 Texas County Statistics, Texas Dept. of Agri., 1972 and

1982. D Not reported because of individual firm information

disclosure limitation.

1

- 5

Table 3: Employment by Business Category Duval County, First Quarter 1980 and 1986.

category 1980 1986

Agriculture 2,077 1

Mining 1,017 1,076 Construction 85 126 Manufacturing 4 10

Transportation and public utilities 91 53

Trade 323 460 Finance and

real estate 63 107

Services and other 112 274 State government 51 58 Local government 981 1,191

TOTAL 2,723 3,355

Payroll (mill. $) 7.4 13.2

Source: Covered Employment and Wages by Industry and County, Texas Employment Commission, April 1980 and 1986.

Hired farm labor in 1982 according to U.S. Census of Agriculture, Texas 1982.

- 6

Most of the County is ranchland, which does not offer an

intensive labor use. Hired farm workers, reported in the 1982

Agricultural Census totaled 1,589, or an average of 1.5 persons

per farm/ranch that payroll was slightly over two million

dollars. That averages about $2,000 per year per farm/ranch.

Doubtless some of this is part-time, seasonal employment.

Unemployment in Duval County as of July 1986 totaled 1,067

persons according to the Texas Employment Commission, or 16

percent of the labor force. It is the hope of those interested

in the establishment of an agri-business park that such a

development would help provide relief from this high

unemployment situation. Agricultural prices have generally not

been favorable in recent years in comparison to production

costs. Therefore the Duval County agricultural and oil

resources are both operating in badly depressed markets.

Because of the lack of sufficient economic development and

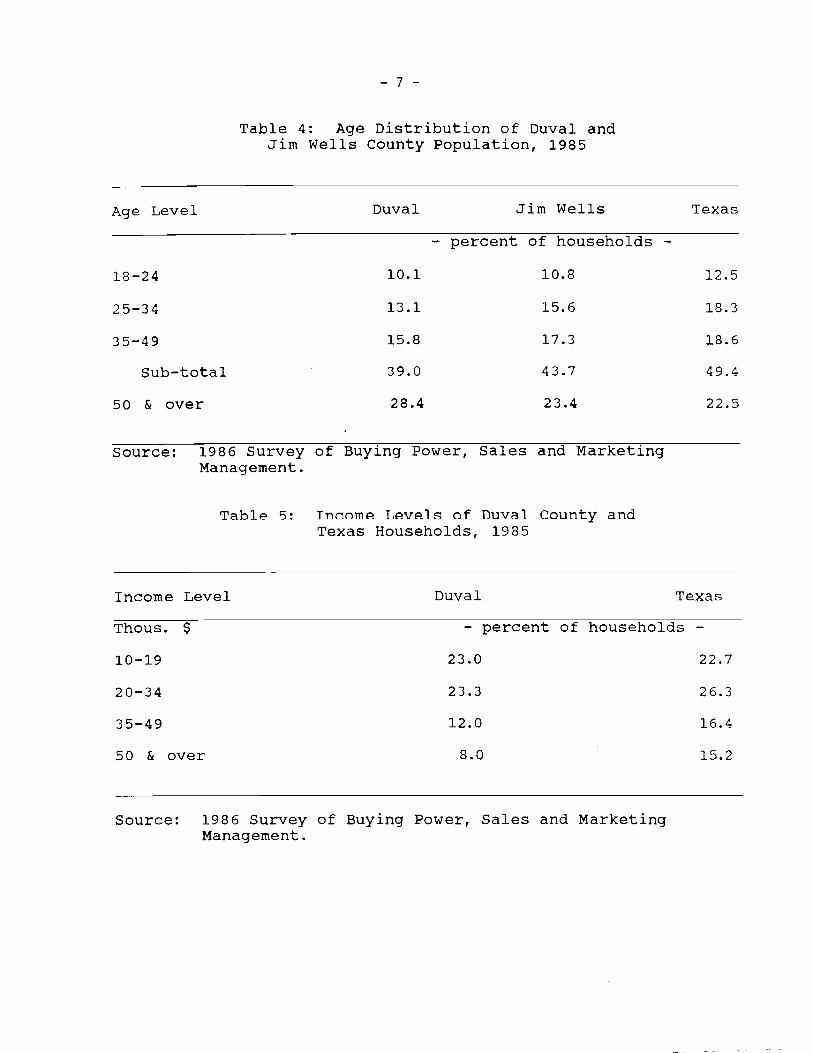

employment opportunities, the population in Duval County

reflects a below average percentage of persons in the younger

age groups and a higher than average among older age levels

compared with state averages, Table 4. The adjacent Jim Wells

County has a more developed, balanced economy because of the

greater diversity of activity in Alice, its principal city.

The imbalance of the Duval ece .lCTI1Y is also reflected in more

households having lower incomes than the State as a whole,

Table 5.

The Economic Development Analysis Plan

This Phase I preliminary market and economic analysis is

- 7

Table 4: Age Distribution of Duval and Jim Wells County Population, 1985

Age Level Duval Jim Wells Texas

- percent of households

18-24 10.1 10.8 12.5

25-34 13.1 15.6 18.3

35-49 15.8 17.3 18.6

SUb-total 39.0 43.7 49.4

50 & over 28.4 23.4 22.5

Source: 1986 Survey of Buying Power, Sales and Marketing Management.

Tab1/? 5: Tnr.nmp T,pvpl s; of nuv~l county and Texas Households, 1985

Income Level Duval Texas

Thous. $ - percent of households -

10-19 23.0 22.7

20-34 23.3 26.3

35-49 12.0 16.4

50 & over 8.0 15.2

Source: 1986 Survey of Buying Power, Sales and Marketing Management.

- 8

designed as a three sector analysis. The three sectors are

identified as follows:

1. An overview of the size of the principal agribusiness

product markets in and near Duval County.

2. A survey of agribusiness firms in the area.

3. A search for new business concepts that appear to have

promise for fitting the resource and/or market base

in and near Duval County.

The procedure for the first sector involves basically

matching the population of the principal market areas and its

economic demographics with products purchase rates associated

with the relevant income levels in the repective markets.

Purchase rates of most consumer products are directly

responsive to household income levels. Purchase rates by

income level reported in the Bureau of Labor Statistics'

national Consu~er Expenditure Survey and in the Food

Consumption study of the u.s. Department of Agriculture were

used as the principal data sources. In this preliminary study,

only average household incomes were used for the respective

county or city markets. Development of estimates by individual

income classes at this stage is not warranted. That 1S

deferred to whatever specific feasibility studies may be made

for individual agribusiness er~~rprises, as a follow-up to this

study.

Household income data were obtained from several sources.

principal reliance was on the reports of individual County

income levels from the Bureau of Economic Analysis of the U.S.

- 9

Department of Commerce. BEA income estimates include both cash

and income in kind. Estimates on a county by county basis are

prepared by BEA on a year by year basis.

Decisions in this study also were required as to the

geographic markets to be considered as a sales outlet for any

expanded or new Duval agribusinesses. Relevant market areas

vary by kind of product, because the competitive environment

changes by product and/or product class. However, Duval

County's location clearly makes the primary intital market that

within Duval and its immediately adjacent counties. Analyses

therefore were directed mostly to the following set of

counties: Duval, Brooks, Jim Hogg, Jim Wells, Webb, and

McMullen. Secondary markets outside these counties are Corpus

Christi (Nueces County), Kingsville (Kleberg County) and San

Antonio in Bexar County. For some products, national markets

were considered to be relevant.

The field survey conducted under objective two was directed

primarily toward agribusiness firms within Duval County, and

those in the city of Alice (Jim Wells Co.). Alice, population

of about 20,000, is only ten miles from San Diego, the county

seat of Duval County. Firms selected for the survey were

identified through the current business directory listings

within relevant telephone directories.

A questionnaire was designed to obtain information

concerning the ?rincipal products purchased and/or sold by the

local establishments. Another purpose was to obtain additional

estimates of the size of the market for agricultural products,

10

as well as farm and ranch production inputs. Additionally,

attitudes were obtained with respect to what may be limiting

business volume expansion. The Market Research Center's

experience from previous studies is that internal or external

needs required to expand operations are often either not

available or clearly recognized by agribusiness managers.

Results of field survey questionnaires were coded and

computer entered, as well as being subjected to personal staff

evaluation and analysis.

Establishments surveyed were divided into the following

primary categories.

1. Retail supermarkets and general food stores.

2. Drive-in food markets.

3. Restaurants.

4. Fast food - American menu.

5. Fast food - Hispanic menu.

6. Food processors.

7. Farm supplies.

8. Farm equipment and repairs.

9. Grain, feed and seed dealers.

10. Livestock auctions.

11. Institutional food service.

All eligible businesses WBrc surveyed in Duval County,

which included those in San Diego, Freer and Benavidas. A

sample of the establishments was surveyed in Alice. A listing

of the eligible businesses in Al ice was prepared based on a

complete listing of firms under any related commercial category

- 11

listing in the 1986 directory. A probability sample of firms,

by category, was selected using a computerized random number

generator.

The main focus of the agribusiness firms survey was to

identify those marketing products that can feasibly be produced

and processed in Duval County. The field survey interviews

were designed and implemented under the direction of the Texas

Agricultural Market Research Center staff. Interviewing was

conducted by the staff and members of the Economic Development

Office of Duval County. A copy of the survey questionnaire

appears in the appendix of this report.

The categories of products or product lines considered were

as follows.

Food Category

1. Beef processing

2. Poultry processing

3. Egg processing

4. Bread processing

5. Ice cream processing

6. Fruit and vegetable packing house

7. Hispanic food processing

8. Milk processing

9. Vegetable processing, canned or frozen

10. Candy processing

11. Flour processing or milling

- 12

Non-Food category

1. Mesquite wood for barbecuing

2. Floriculture and landscape supplies shipping

facility

Farm Supply Category

1. Feed, seed and fertilizers

2. Farm and ranch equipment and repair

3. Farm and ranch supplies

The prospects for an agribusiness firm for most of these

products condidered is heavily dependent upon the size of the

local primary market. Insofar as Duval and the local counties

is concerned, it is important to consider population growth

trends. Presence of population growth makes ease of entry less

difficult since competition with existing firms over time would

be less of a problem.

From a product processing and marketing standpoint, the

population of all of the counties excluding Webb County and

Nueces County, does not represent a very significant market,

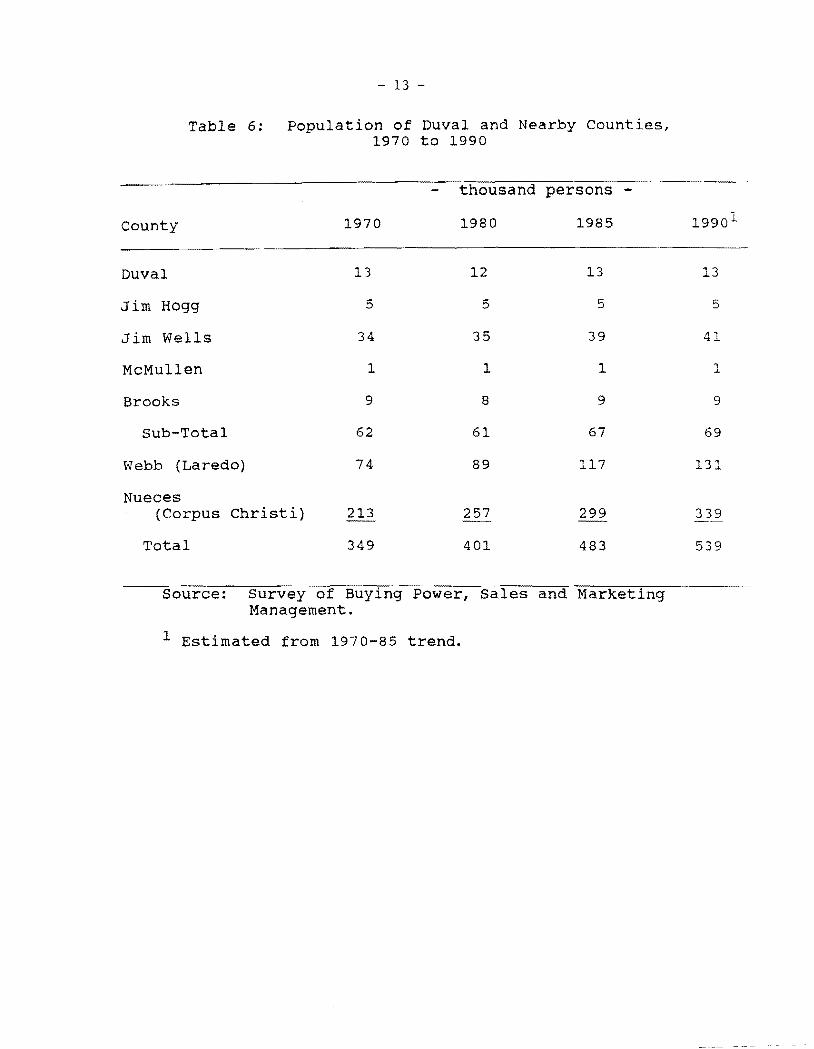

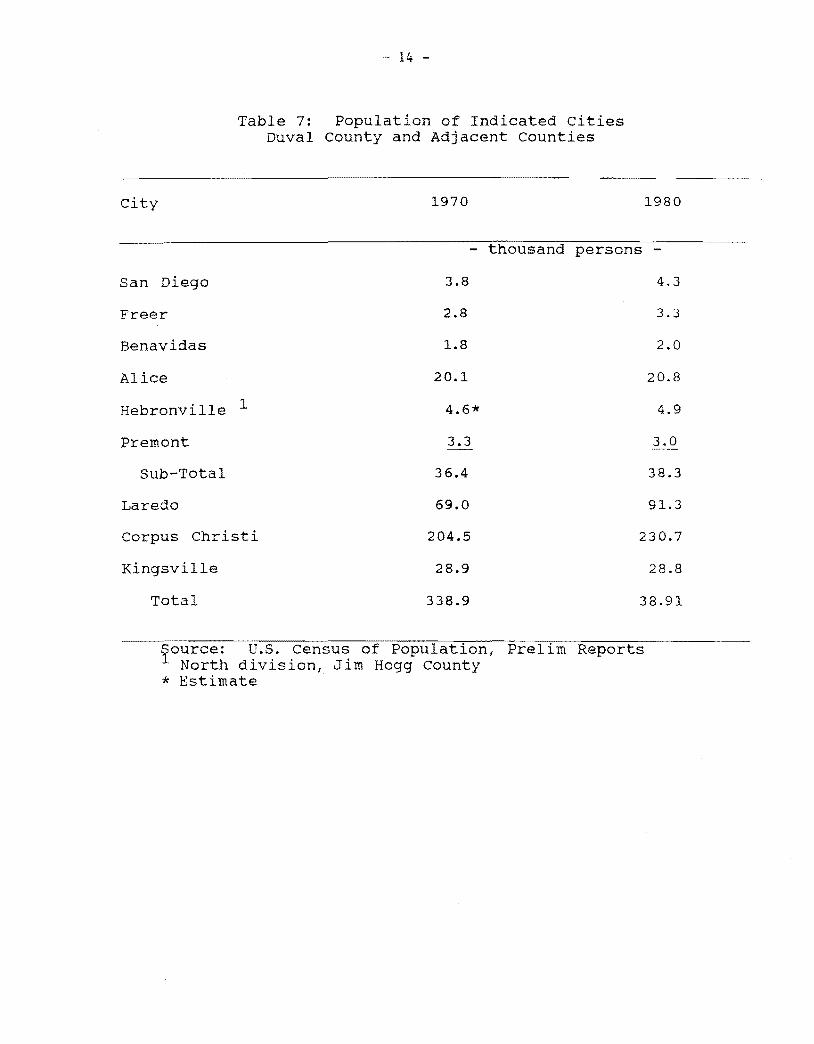

Table 6. A total of 67,000 persons in about 21,500 households

spread over five counties clearly is a limited market base. It

is even more so because this population is scattered among

comparatively small towns, TaLl~ 7. The more important markets

are in Corpus Christi (Nueces County) and Laredo (Webb County).

If the market showed promise of considerable growth that in

itself would be encouraging. Instead growth in the five county

area may be able to reach 69,000 population by 1990, compared

- 13

Table 6: population of Duval and Nearby Counties, 1970 to 1990

persons

County 1970 1980 1985 1990 1

Duval

Jim Hogg

Jim Wells

McMullen

Brooks

Sub-Total

Webb (Laredo)

Nueces (Corpus Christi)

Total

13

5

34

1

9

62

74

213

349

12

5

35

1

8

61

89

257

401

13

5

39

1

9

67

117

299

483

13

5

41

1

9

69

131

339

539

Source: Survey of Buying Power, sales and Marketing Management.

1 Estimated from 1970-85 trend.

14 -

Table 7: Population of Indicated cities Duval County and Adjacent Counties

city 1970 1980

persons

San Diego 3.8 4.3

Freer 2.8 3.3

Benavidas 1.8 2.0

Alice 20.1 20.8

1Hebronville 4.6* 4.9

Premont 3.3 3.0

Sub-Total 36.4 38.3

Laredo 69.0 91.3

Corpus Christi 204.5 230.7

Kingsville 28.9 28.8

Total 338.9 38.91

rource: U.S. Census of Population, Prelim Reports North division, Jim Hogg County

* Estimate

- 15

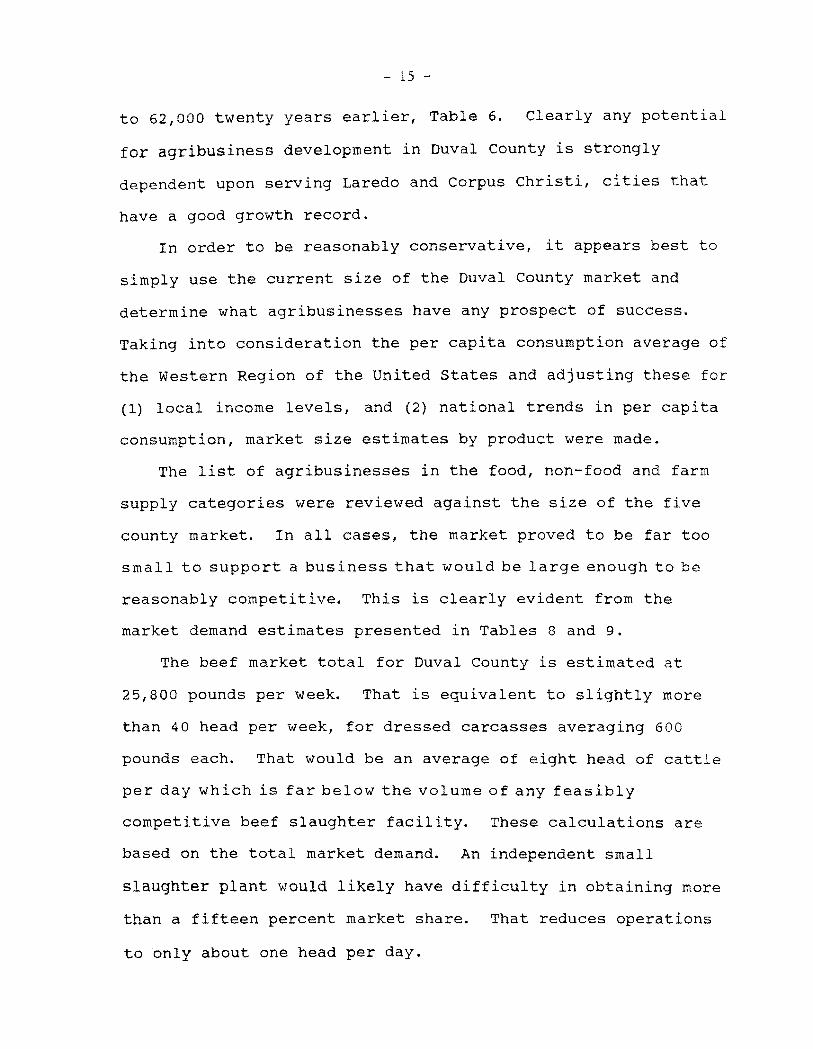

to 62,000 twenty years earlier, Table 6. Clearly any potential

for agribusiness development in Duval County is strongly

dependent upon serving Laredo and Corpus Christi, cities that

have a good growth record.

In order to be reasonably conservative, it appears best to

simply use the current size of the Duval County market and

determine what agribusinesses have any prospect of success.

Taking into consideration the per capita consumption average of

the Western Region of the United states and adjusting these for

(1) local income levels, and (2) national trends in per capita

consumption, market size estimates by product were made.

The list of agribusinesses in the food, non-food and farm

supply categories were reviewed against the size of the five

county market. In all cases, the market proved to be far too

small to support a business that would be large enough to be

reasonably competitive. This is clearly evident from the

market demand estimates presented in Tables 8 and 9.

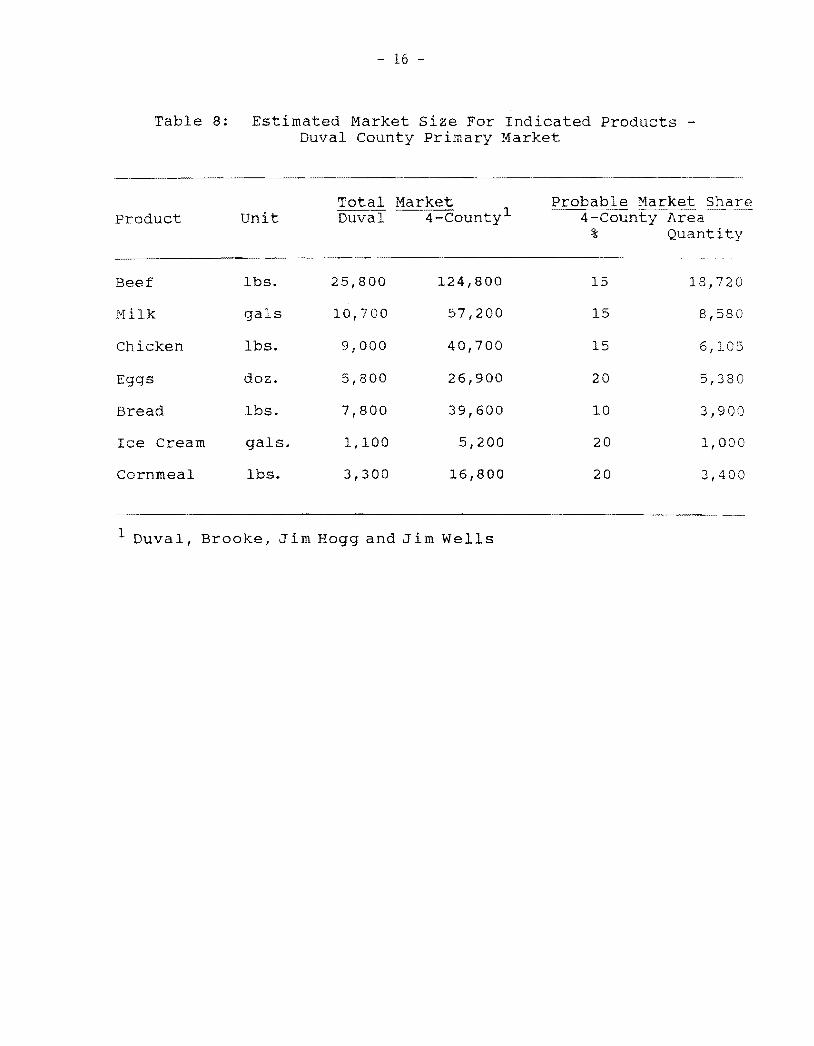

The beef market total for Duval County is estimated at

25,800 pounds per week. That is equivalent to slightly more

than 40 head per week, for dressed carcasses averaging 600

pounds each. That would be an average of eight head of cattle

per day which is far below the volume of any feasibly

competitive beef slaughter facility. These calculations are

based on the total market demand. An independent small

slaughter plant would likely have difficulty in obtaining more

than a fifteen percent market share. That reduces operations

to only about one head per day.

- 16 -

Table 8: Estimated Market Size For Indicated Products Duval County Primary Market

-

Product unit Total Market Duval 4-County1

----_._--_..._

Probable Market Share 4-County Area

% Quantity .. _._._..

Beef lbs. 25,800 124,800 15 18,720

Milk gals 10,700 57,200 15 8,580

Chicken lbs. 9,000 40,700 15 6,105

Eggs doz. 5,800 26,900 20 5,380

Bread Ibs. 7,800 39,600 10 3,900

Ice Cream gals. 1,100 5,200 20 1,000

Cornmeal lbs. 3,300 16,800 20 3,400

1 Duval, Brooke, Jim Hogg and Jim Wells

- 17

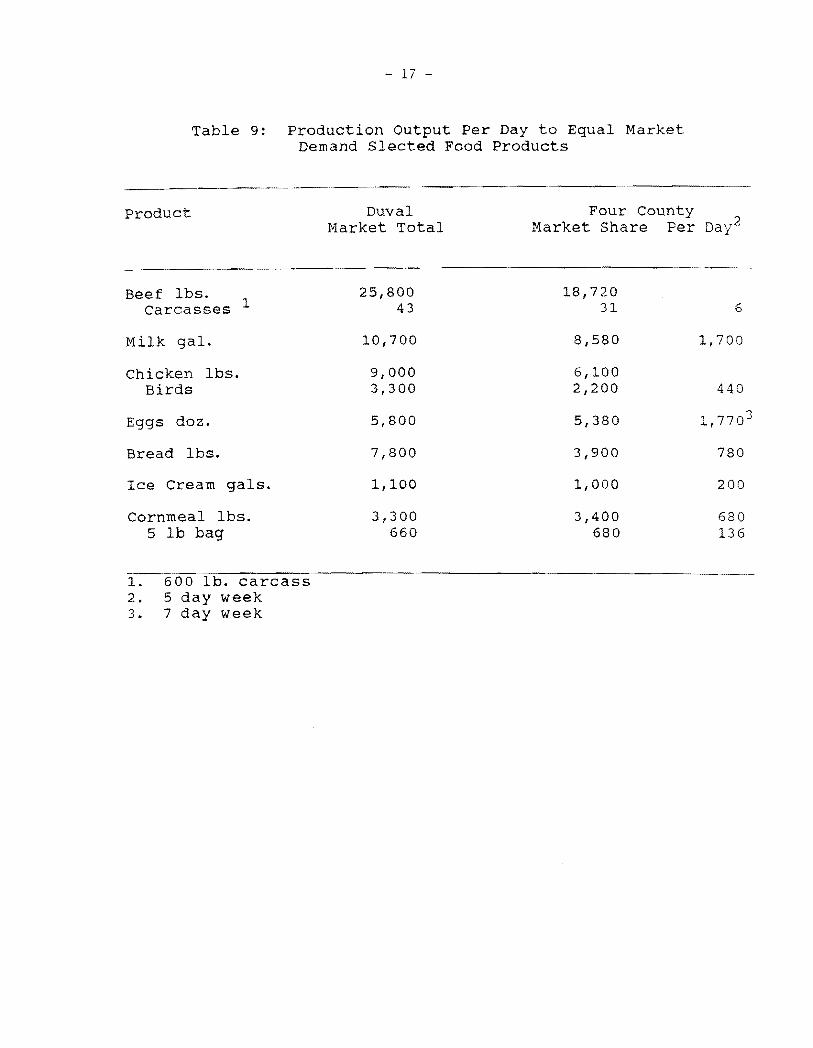

Table 9: Production Output Per Day to Equal Market Demand Slected Food Products

Product Duval Four county Market Total Market Share Per oay2

Beef lbs. 1Carcasses

Milk gal.

Chicken lbs. Birds

Eggs doz.

Bread lbs.

Ice Cream gals.

Cornmeal lbs. 5 lb bag

25,800 43

10,700

9,000 3,300

5,800

7,800

1,100

3,300 660

18,720 31 6

8,580 1,700

6,100 2,200 440

5,380 1,7703

3,900 780

1, 000 200

3,400 680 680 136

1. a . carcass 2. 5 day week 3. 7 day week

- 18

The above analysis clearly demonstrates why small markets,

population-wise, do not have their own food processing plants.

There simply is not enough product demand there to sustain

them. As a consequence, food processing plants generally must

serve multi-county, if not mUlti-state markets. Given that

requirement, plants are usually built to take advantages of

economies of scale so that any other competing plant cannot

have a lower cost per unit of product output.

What are known as economies of scale are inherent in the

nature of the equipment needed to do the food processing.

Economists sometimes illustrate this point with the example of

a steam boiler to provide steam for cooking or cleaning

operations. A medium size boiler can produce steam at a lower

cost per unit than a small one, simply because of physical

advantages of the larger one. For example, as you double size

you quadruple the capacity.

The next step is to consider market demand in a larger

area. The demand in Duval plus Brooks, Jim Hogg and Jim Wells

was examined as an alternative and will be referred to as the

Duval primary market. It is selected in order to determine

what market demand can be tapped without having to go into

either the Laredo (Webb County) or Corpus Christi (Nueces

County) markets. Results are ~lesented in Table 8. Beef total

demand increases to an estimated 124,800 pounds. Initially it

would be diff icul t to obtain more than a 15 percent share of

this larger market, which means the total would be about 18,000

pounds. As may be seen in Table 9, that is equal to only 31

- 19

head of cattle per week, or a kill of six head per day. This

can be feasible for the operation of a custom slaughter

facility where customers bring in cattle for dressing and cuts

prepared as they direct. Some retailing is feasible if a

butcher shop is operated on the premises. However, any beef

retailed has to be from carcasses that have been federally

inspected. That is accommodated by arranging the processing of

those animals all in one day and paying a federal inspector to

be there and approve the carcasses and the plant sanitation

operations. A federal inspectors transportation plus time on

the job must be paid for each inspection visit. An inspector

likely could be sent from Corpus Christi.

But the foregoing does not provide the kind of operation

that can be expected to wholesale meat to retailers. If any

employment impact is to be achieved, it must come from a

commercial size plant that is prepared to deliver product to

its customers.

Based on the foregoing preliminary market analysis, it is

evident that only a small, mostly custom, slaughter facility

could be considered in Duval County at this time. Only a

limited quantity could be wholesaled to retail stores,

restaurants or any general public customers. Even the

investment in this small facility would likely be between

$150,000 and $200,000. Investment in a plant to have a kill

rate of about 170 head per week can range between $350,000

and $500,000 (Farris).

Examination of the market share volume for the other

- 20

foods listed in Table 9, also discloses that the four-county

primary market is below minimum volume requirements for

support of a reasonable size processing plant. Again only a

custom service type of establishment might operate, that does

not have a sales force nor delivery costs.

ALTERNATIVE AGRIBUSINESS

SYSTEM OPPORTUNITIES

Because the primary market surrounding Duval County is

not large enough to support other than very small custom

service firms, it is necessary to look at alternative

possibilities. In other words, the question that arises is

whether new agribusiness eco-systems can be developed and

literally inplanted, as it were, in Duval County?

As noted at the outset of this report, the geographic

market required to sustain a competitive agribusiness plant

varies with the individual product. In considering eco

systems that can be implanted into Duval County, the market

area involved is either South Texas, Texas, the Southwest

Region or the U.S. market. The relevant one will be

indicated in the individual eG~-8ystem analysis.

The reason for using the term aco-system is because three

components are necessary to make the operation viable -- (1)

the raw material production base, (2) the processing facility

and (3) an available marketing channel system through which the

- 21

output can be profitably moved. With this concept in mind, a

somewhat detailed example is presented based on building a milk

production, processing and marketing system as a further

enlargement of the present dairying farms in Duval County.

Preliminary Feasibility

Analysis of Milk Processing

in Duval County

According to the 1984 Texas County statistics report from

the Texas Agricultural statistician's office in Austin, there

were about 2,000 dairy cows in Duval County in 1984. Milk

from these dairy herds is going primarily to the Rio Grande

Valley processing plants, according to reports from Duval

County. It is upon this base that it is suggested and

proposed that a dairy product production-processing-marketing

eco-system might be built.

It must be clearly understood that the following general

analysis is not in any way, a fully developed economic

feasibility study. Therefore no one should take this as a

signal to do any more than consider whether a final

feasibility study would be warranted.

The retail dairy product market is extremely competitive.

Fluid milk marketing can be easier to enter than for ice cream

or other produ:t sales. These other products require

considerably more market development in terms of (1)

establishing product characteristics that are acceptable to

- 22

consumers in the market, (2) maintaining product consistency in

the manufacturing processes and (3) in achieving brand

recognition in the market.

Because of the competitive nature of the dairy product

market probably the most logical kind of dairy processing plant

to consider is a fluid milk bottling plant. Such an operation

would produce a limited line of beverage milk products such as:

1. Homogenized whole milk

2. Low fat milk

3 . Skim milk

4. Buttermilk

5. Chocolate flavored milk product whether a whole milk

product or a low fat or skim product

As expertise and market share develop, it may be possible to

produce additional products such as half and half cream,

cottage cheese and ice cream. Some local fluid processing

plants buy aseptically packaged half and half products, sour

creams, coffee creamers, whipping cream and other fluid

specialty products from firms that specialize in aseptic

products. In addition these plants may buy packaged ice cream,

cheese or butter. This strategy allows the smaller milk

processor to offer clientele a full line of products without

investing the resources or acqLlring the expertise necessary

to produce these.

The Market:

There are approximately 612,000 people living in the

- 23

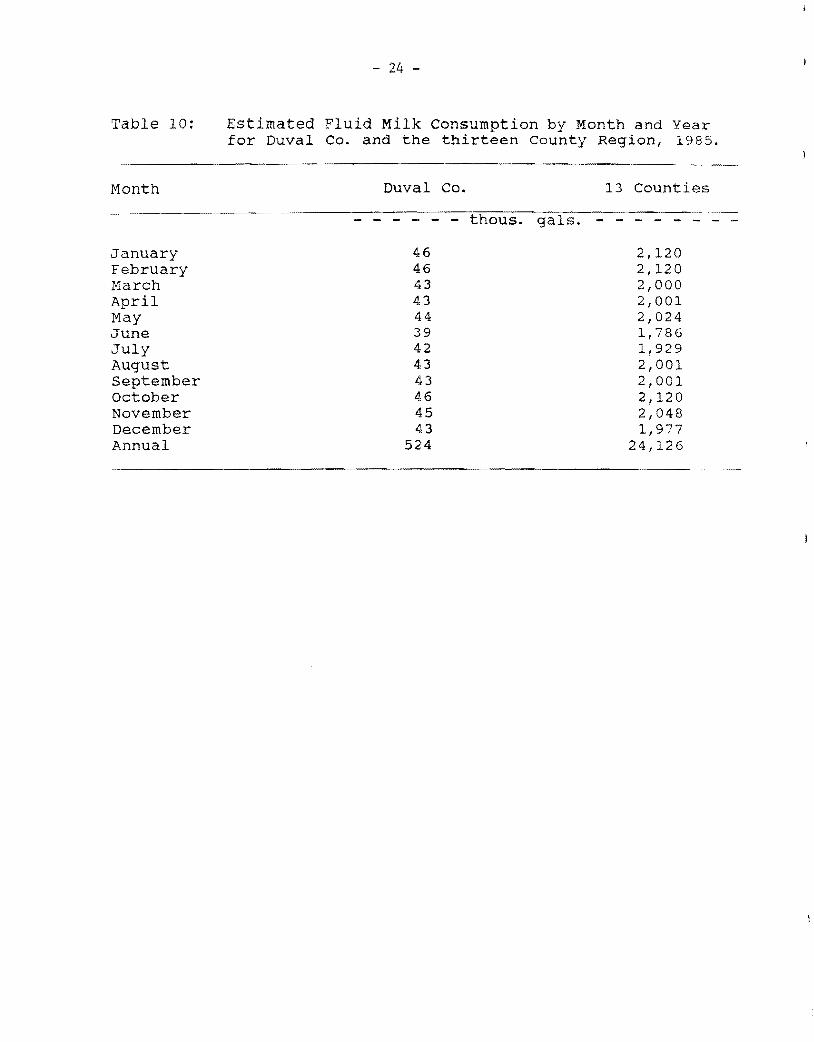

counties that are within 50 miles of Benevidas in Duval County.

No current data are available on fluid milk consumption in the

13-county area. However, using the 1977 USDA Consumer Survey

data, an estimate was made of total fluid (beverage) milk

consumption patterns, Table 10. Normally, consumption is

lighter in the summer months.

An inventory of milk processing capacity within a 150

mile radius of Duval Co. indicates a more than adequate

beverage milk supply to meet the 13-county area demand.

Furthermore, regional supermarket chains with stores in the

area will process their store label in their own plants and

bring it into the region. It is quite common for packaged milk

products to move as much as 400 miles from the point of

processing to a retail outlet. Often times the processed milk

is delivered to a central receiving warehouse owned by a chain

store. The chain then uses its own facilities and distribution

equipment to distribute the milk to its retail outlets.

Eight fluid milk processing plants are located within a

150 mile radius of Duval County. These plants process an

estimated combined total of from 5 million to 7 million

gallons of fluid milk per month. Much of this milk is

consumed in other areas of Texas. Some of this milk moves as

far north as Bryan, Texas. Much of this fluid milk moves

through supermarket chain stores. This milk is sold under

several brand n~mes. At least two are supermarket labels,

one is a local label, and at least two are national labels.

One national supermarket in the market area processes its own

- - - - - - - - - - - -

- 24

Table 10: Estimated Fluid Milk Consumption by Month and Year for Duval Co. and the thirteen county Region, 1985.

Month Duval Co. 13 Counties

January 46 2,120 February 46 2,120 March 43 2,000 April 43 2,001 May 44 2,024 June 39 1,786 July 4:2 1,929 August 4:3 2,001 September 43 2,001 October 4:6 2,120 November 45 2,048 December 43 1,977 Annual 524 24,126

..~-.-

- 25

brand label in Dallas. One of the other supermarket labels

sold in one of the locally controlled food stores 1S processed

in either San Antonio or Corpus Christi by one of the

national brand processors under contract. Another processor

in the area markets most of its fluid product through its own

convenience stores, hotels, restaurants, institutions, and

other mass food distribution outlets. A new processing plant

in the area would likely have to concentrate on marketing to

locally owned supermarkets and convenience stores. Entry

into the retail stores owned by either regional or national

chains may be difficult.

A review of processing plants in other areas of Texas

suggests that a local independent processor selling under its

own brand label can probably expect, at best, only about a 15

percent share of the market. A similar study in North

Carolina (Knutson) suggests a local processor can expect, at

the worst, 2 percent, and at best a 20 percent market share

An average of about 15 percent is obtained in its well

established markets. If a processing plant in Duval Co. were

to capture 15 percent of the market in the 13-county area, it

would be processing about 302,000 gallons a month. Allowing

for normal product waste output, this means a run of about

310,000 gallons a month,

Operating Costs '.

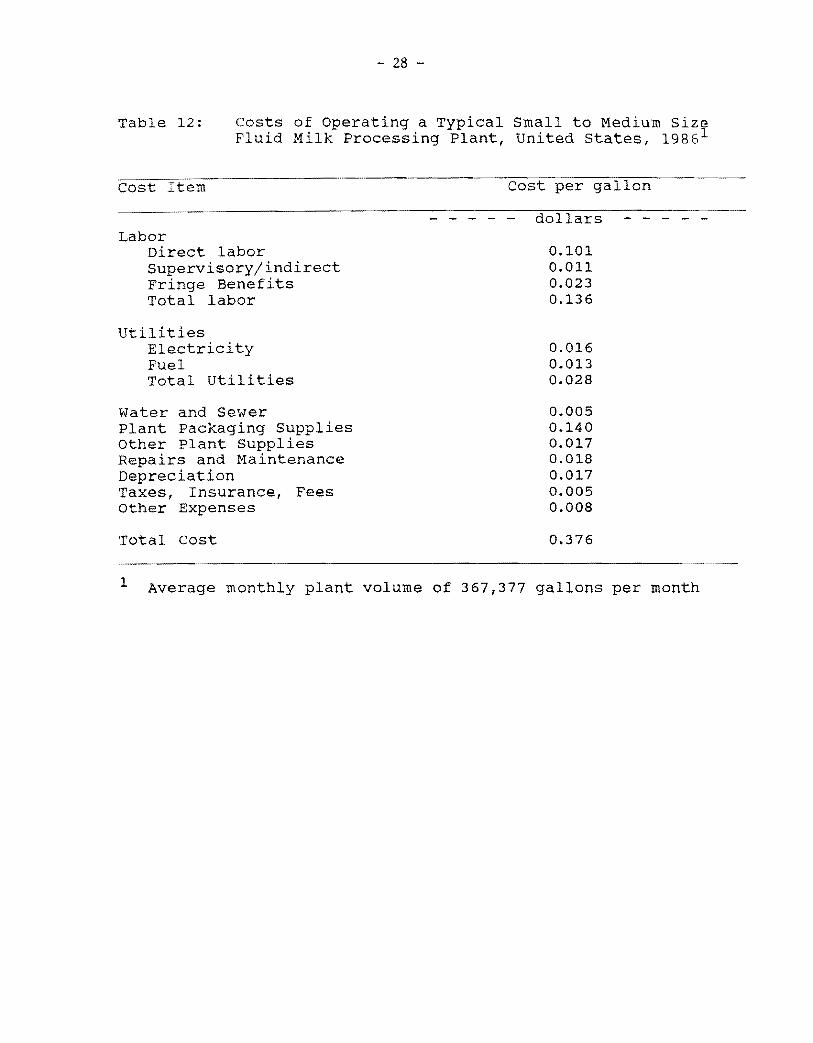

Current cost data indicate that the cost of operating

a milk processing plant does not change dramatically over a

- 26

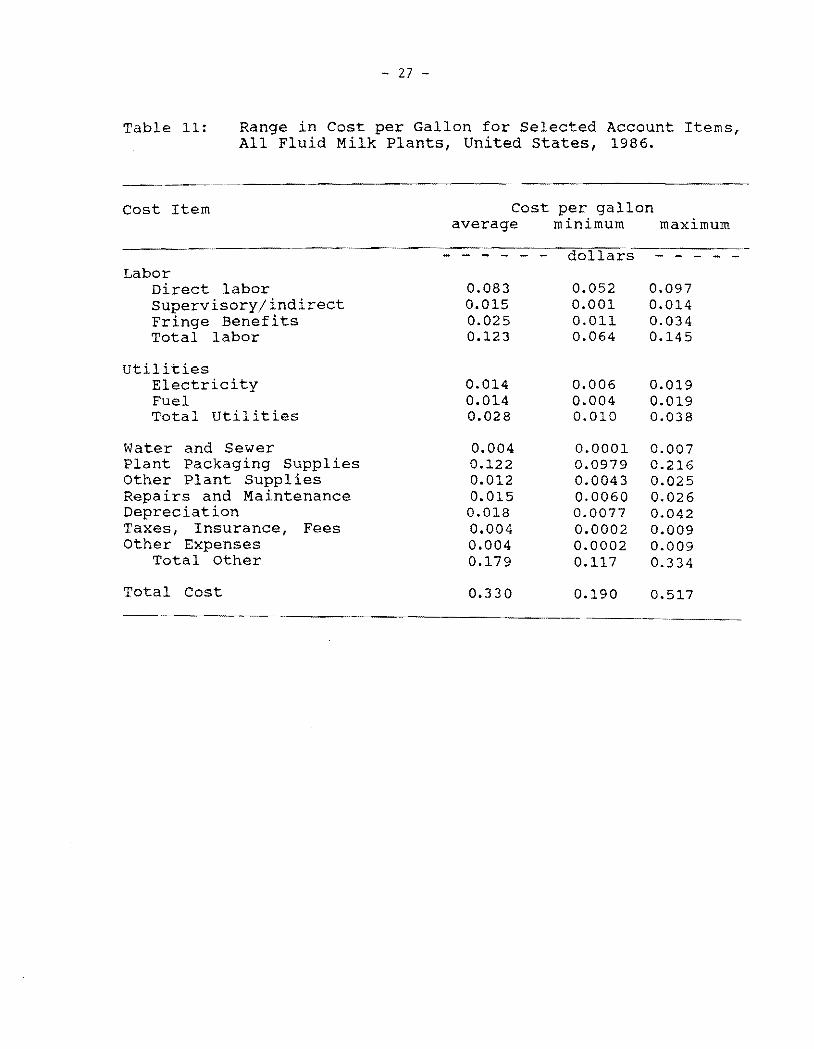

wide range of capacities. The average cost per gallon over

all sizes of plants is about 33 cents per gallon, excluding

raw milk cost. The range in operating costs varies from a

minimum of 19 cents/gallon to a maximum of 52 cents/gallon.

For a typical small to medium size plant, the cost is about

35 cents. This does not include sales force or distribution

costs. Distribution costs would likely be about 11

cents/gallon, based on the assumption the average milk route

is 200 miles long and the truck has a capacity of 30,000

pounds of milk, excluding the weight of cartons and cases.

These costs do not include sales commissions or other sales

expenses, they only include truck and driver costs.

Although the costs in Table 12 are averages for the

United states, they have been varified as representative of

the costs of processing fluid milk in Texas.

Employment Impact

The typical small to medium processing plant illustrated

in the accompanying table would employ a total of 12 to 16

people. Plant and milk cooler operations would require about

8 or 9 people. A minimum of two supervisory personnel would

be required to operate the plant. The plant functions

include receiving and storing ra~ milk, clearifying,

separating, homoginizing, pasturizing, standardizing, and

filling, shipping case sort and storage, returned and damaged

product disposal, and clean up. In addition, the plant would

require an engineer and maintenance man, and quality control

- 27

Table 11: Range in Cost per Gallon for Selected Account Items, All Fluid Milk Plants, United States, 1986.

Cost Item Cost per gallon average minimum maximum

Labor Direct labor Supervisory/indirect Fringe Benefits Total labor

utilities Electricity Fuel Total utilities

Water and Sewer Plant Packaging Supplies other Plant Supplies Repairs and Maintenance Depreciation Taxes, Insurance, Fees Other Expenses

Total Other

Total Cost

0.083 0.015 0.025 0.123

0.014 0.014 0.028

0.004 0.122 0.012 0.015 0.018 0.004 0.004 0.179

0.330

0.052 0.001 0.011 0.064

0.006 0.004 0.010

0.0001 0.0979 0.0043 0.0060 0.0077 0.0002 0.0002 0.117

0.190

0.097 0.014 0.034 0.145

0.019 0.019 0.038

0.007 0.216 0.025 0.026 0.042 0.009 0.009 0.334

0.517

1

- 28

Table 12: Costs of Operating a Typical Small to Medium Size Fluid Milk Processing Plant, United states, 1986 1

Labor Direct labor Supervisory/indirect Fringe Benefits Total labor

Utilities Electricity Fuel Total utilities

Water and Sewer Plant Packaging Supplies Other Plant Supplies Repairs and Maintenance Depreciation Taxes, Insurance, Fees Other Expenses

Total Cost

0.101 0.011 0.023 0.136

0.016 0.013 0.028

0.005 0.140 0.017 0.018 0.017 0.005 0.008

0.376

Average monthly plant volume of 367,377 gallons per month

- 29

and laboratory personnel. At least two of the plant

operations people should be skilled in stainless steel

techniques, including welding. The cooler operation would

require three people to handle product in and out of the

cooler. Allowance must be made in personnel numbers to cover

vacations. In smaller plants, plant operating personnel are

trained to interchange among the various processing tasks

required in operating the plant. A minimum of two people

would be required to perform clerical and secretarial tasks

related to the milk processing operations. These personnel

totals do not include sales staff or distribution staff.

Labor costs associated with the processing operations

essentially become fixed because a processing machine

requires an operator whether or not milk is processed or the

machine is operated at capacity.

startup costs:

startup plant costs will vary, and it is very difficult

to get solid cost estimates when new construction is

involved. These estimates are based on conversations with

people who are familiar with milk processing but who have not

been associated with constructing and operating a new

facility. It is estimated that the cost of a typical small to

medium plant will vary from about 2.5 to 7.0 million dollars

for a plant wit~ a capacity of 380,000 gallons a month. The

plant would be constructed with 25% excess capacity. Costs are

calculated on the plant processing 310,000 gallons milk. Of

- 30

that total, the milk processing equipment required is estimated

to make up about 50% of the cost and the land, physical plant,

and mechanical equipment such as electrical hardware,

refrigeration, heating, air conditioning and other non-milk

related equipment would make up the other 50%.

Because of the nature of food processing, the processing

equipment is normally revamped or replaced on a regular

basis. According to conversations with processors, the

typical milk processing firm depreciates the plant building

over 30 years and mechanical and milk processing equipment

over 10 years. It is estimated that the depreciation costs

figure presented above will have to be increased about $.044

per gallon to cover the depreciation of the higher cost for

new construction and milk processing and mechanical

equipment. A minimum of 5 straight trucks equipped with

refrigerated bodies would be needed to deliver the daily

output of the plant. It is estimated that these trucks would

cost a total of $350,000. The depreciation on the trucks is

included in the cost of milk sales distribution.

Raw Milk ~lies and Procurement Costs

USDA estimates indicate there are about 2000 milk cows in

Duval Co. These cows produce a~~ut 92.9 gallons a month,

according to the USDA estimates. This level of production

per cow in the South Texas area suggests about 3300 cows

could meet the monthly milk needs of the plant. Seasonal

demand surges and seasonal production declines occur

- 31

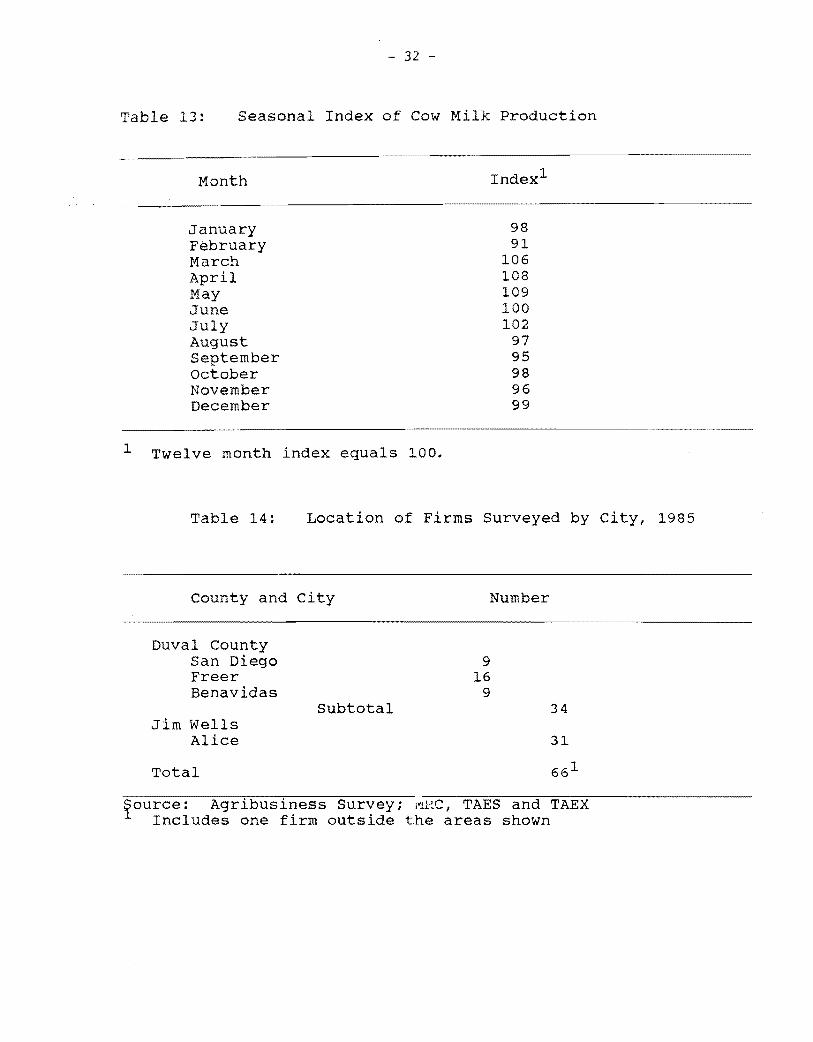

together, Table 13. To compensate about 3500 cows would be

needed to meet plant needs during cow production slumps.

There are an estimated 2900 milk cows in Jim wells Co. Duval

and Jim Wells Counties together produce an estimated 5.4

million gallons a year. While these data indicate an ample

supply of raw milk available in the area, just one of the

existing plants within 60 miles of Duval Co. can process 81

percent of the production in the 15 county crop reporting

district containing Duval and Jim Wells Co.

Most of the milk processed in South Texas plants comes

from the north and central areas of Texas. Much of the milk

produced in South Texas is marketed by producers through the

two producer cooperatives in the area. The remaining

producers market directly to processors. competition between

cooperative and independents for producer milk is strong in

the region. While a new entrant in this market could buy

milk directly from non-cooperative affiliated producers, it

will likely purchase its milk from a cooperative. The

cooperative can offer balancing services and may prove

attractive as a shield against direct competition for raw

milk. Nevertheless, at current prices, raw milk from any

source will cost a minimum of $16.11 per cwt., about $1.387

per gallon. Since the processing plant will be selling all

of its finished product in the local area, it will be

regulated by Federal Milk Marketing Order 126. The Order

sets the minimum raw milk price the firm will pay. The

minimum order price in the area for raw milk for beverage use

- 32

Table 13: Seasonal Index of Cow Milk Production

Month

January February March April May June July August September october November December

98 91

106 108 109 100 102

97 95 98 96 99

1 Twelve month index equals 100.

Table 14: Location of Firms Surveyed by City, 1985

County and City Number

Duval County San Diego Freer Benavidas

Jim Wells Alice

Subtotal

9 16

9 34

Total

fource: Agribusiness Survey; ·iVll~C, TAES and TAEX Includes one firm outside the areas shown

- 33

is $15.78. Competition for producer milk results in the

cooperative charging an additional 33 cents per cwt.

sul11ming 'Q£ Costs

Total costs, exluding sales force costs and commissions,

for the new firm are estimated to be from $1.87 to $2.06 per

gallon. The cost for the average small to medium plant is

estimated at $1.92 per gallon. These costs assume the plant

will attain a 15% market penetration. If this sales level is

not achieved the costs per gallon could range from $2.57 to

$4.25 with small to medium plant costs around $4.09.

Excessive product waste could also push costs up. These

costs can be considered wholesale breakeven prices.

Retailers must add their markup. Not only will the new firm

have to compete for raw milk by paying premiums, but it will

likely be forced to make price concessions to retailers. It

must be repeated these costs do not include sales force costs

and commissions.

RESULTS OF THE AGRIBUSINESS

FIRMS SURVEY

The reason for concluding that new or expanded

enterprises, or eco-systems, are needed if Duval County is to

be further developed arose from two facets of the study. One

was the examination of the kinds and sizes of the agricultural

- 34

production bases and the associated business enterprises, which

clearly revealed a very small base upon which to build further

economic development. Second was the results of the

agribusiness firms survey. Attention is now directed to the

latter and its implications regarding economic development.

The purpose of the survey was to obtain an up to date

reading as to the kinds of establishments operating presently

in Duval County and in Alice, which is a focal shopping point

in the area. As noted elsewhere, a copy of the questionnaire

appears in the appendix of this report.

An effort was made to survey all of the agribusiness

establishments in Duval County. These ,almost entirely, are

located in the cities of San Diego, Freer and Benavidas.

Partly because of the current depressed local business

climate, several of the establishments were uneasy about

participating in the survey, and therefore refused to

cooperate. Nonetheless, the relatively small number not

cooperating did not materially affect the survey results.

Because of the larger number of agribusiness

establishments in Alice, only a sample was taken of the more

common type businesses such as drive-in groceries and fast food

outlets. In Alice, as well, some refused to cooperate in the

survey. Again, refusals were comparatively small part of the,t

total. Therefore the survey results are considered valid.

Approximately eighty percent of all of the Duval County

agribusiness firms cooperated in the study.

In Alice, the sample coverage averaged about thirty percent of

- 35

all eligible businesses.

Thirty-four businesses were interviewed in Duval County

and 31 in Alice, making a total of 66 establishments, Table 14.

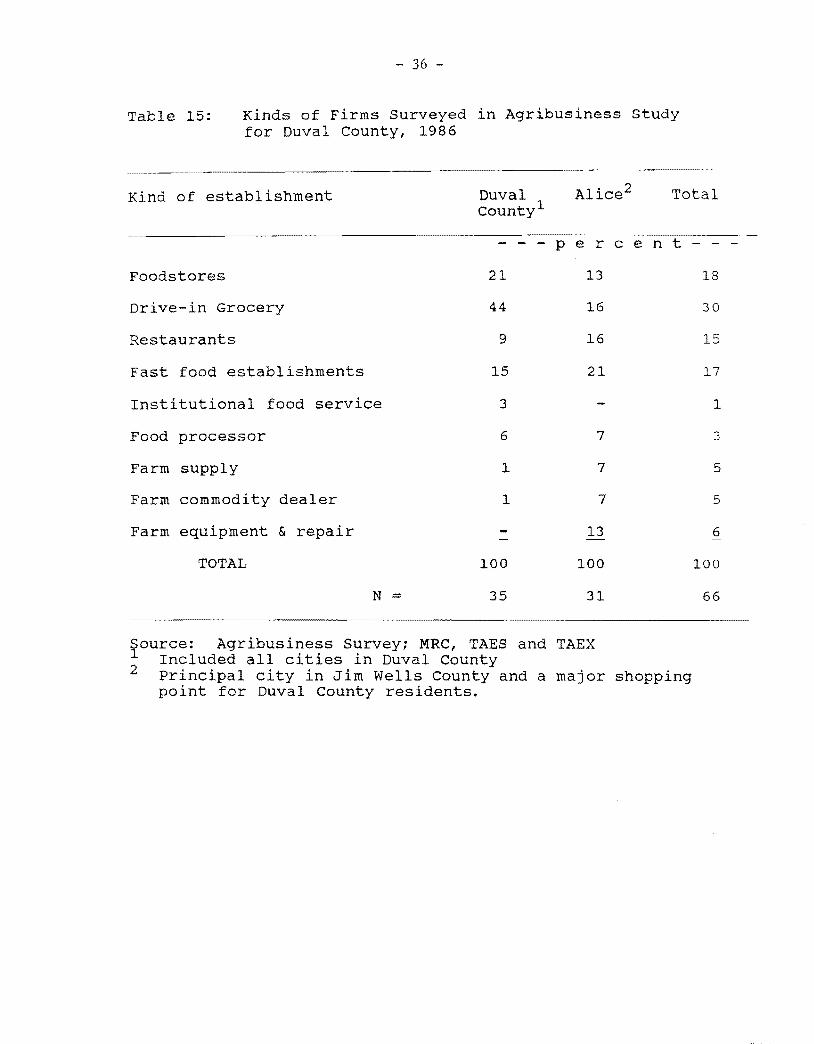

Kind or ~ of ~gribusiness Establish..~~!l.:t::

An indication of the kinds of business in the area is

shown in Table 15. Most of the activity concerns local

retailing operations. The institutional establishments are

local schools and their food service lunch rooms. Nursing

homes are in the same category although none participated in

the survey_

The food processor category included mostly local retail

bakery shops that made their own wares. No evidence was found

that they were endeavoring to expand beyond their own retailing

quantities, by selling wholesale to other outlets.

Farm supply firms were primarily feed and seed stores and

lumber yards marketing fencing and other miscellaneous farm

supplies. Equipment dealers were those selling and/or

servicing mostly tractors, trucks and trailers.

About three-fourths of the firms were locally owned.

outside ownership, in part, was related to franchise-type

businesses that are common for fast-food service businesses,

Table 16 and 17.

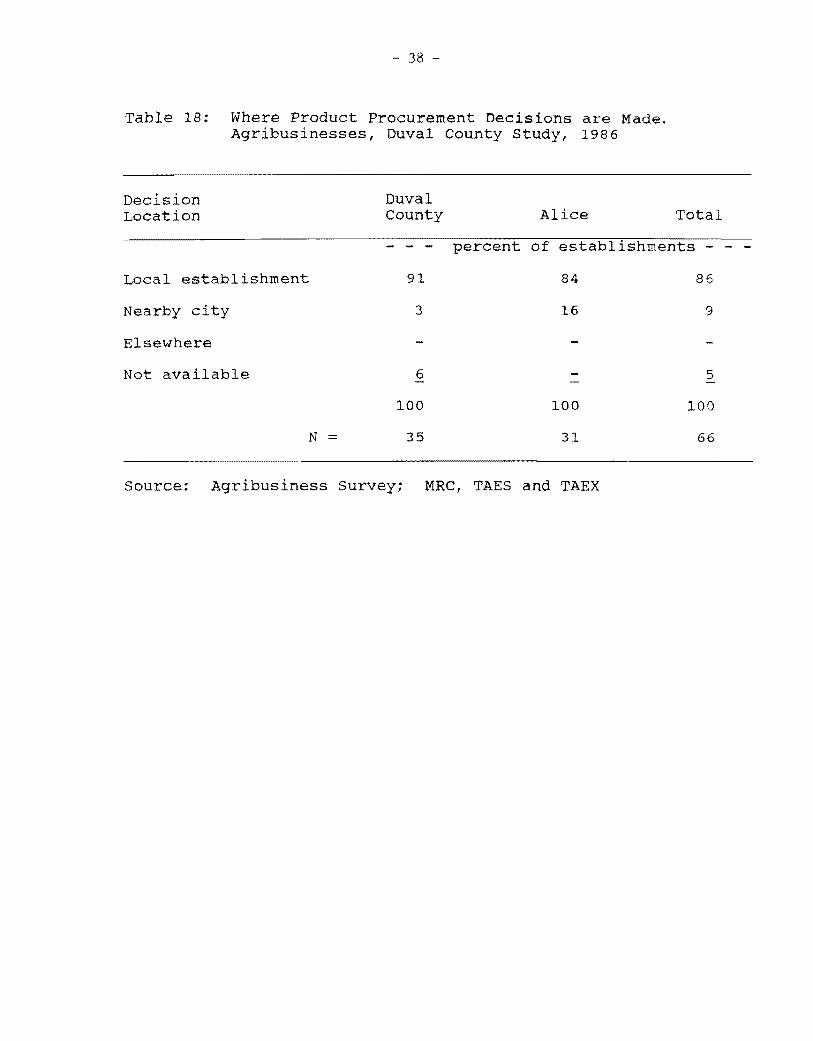

~here Supply Purchase Decisions are ~ade

Almost 90 percent of the purchase decisions regarding

ordering of sUfplies were said to be made by the manager of the

local business units. In the ordering of individual quantities

of products, this doubtless was true, Table 18. That,

- 36

Table 15: Kinds of Firms Surveyed in Agribusiness study for Duval County, 1986

TotalKind of establishment Duval county1

per c e n

Foodstores 21 13 18

Drive-in Grocery 44 16 30

Restaurants 9 16 15

Fast food establishments 15 21 17

Institutional food service 3 1

Food processor 6 7 3

Farm supply 1 7 5

Farm commodity dealer 1 7 5

Farm equipment & repair 13 6

TOTAL 100 100 100

N = 35 31 66

rource: Agribusiness Survey; MRC, TAES and TAEX Included all cit in Duval County

2 Principal city in Jim Wells County and a major shopping point for Duval County residents.

- - - -

- 37

Table 16: Location of Agribusiness Firm ownership, in Duval County, 1986.

Duval ownership County Alice Total

- - - percent of establishmentS-=-~--=-

Local 76 77 76

outside 21 23 21

N = 35 31 66

Source: Agribusiness Survey~ MRC, TAES and TAEX.

Table 17: Kind of Agri-Business Firm Management in Duval County, 1986.

Management Duval County Alice Total

Independent 88

Franchise Local 3 Outside 3

Chain Local 3 Outside

No reply 3

TOTAL 100

N = 35

percent of establishments-- -

61 73

13 8 10 6

6 5 10 5

3

100 100

31 66

Source: Agribusiness Survey: NRC, TAES and TAEX

- - - - - -

38

Table 18: Where Product Procurement Decisions are Made. Agribusinesses, Duval County study, 1986

Decision Duval Location County Alice Total

Local establishment 91 84 86

Nearby city 3 16 9

Elsewhere

Not available 6 5

100 100 100

N 35 31 66

Source: Agribusiness Survey; MRC, TAES and TAEX

- 39

however, should not be confused with the more important

decisions as to from whom supplies are ordered. Local

franchise fast-food shops, for example, reported that they

turned in their own orders. The source of supply in these

cases though is usually determined for them. This is important

because it means that the supply source has been pre-selected

for them based upon particular buying specifications and

pricing arranged by an outside central office. Such

arrangements are important because it means that some newly

developed local agribusiness processor or wholesaler faces

difficulties trying to make sales, and claiming thereby a share

of the total local market.

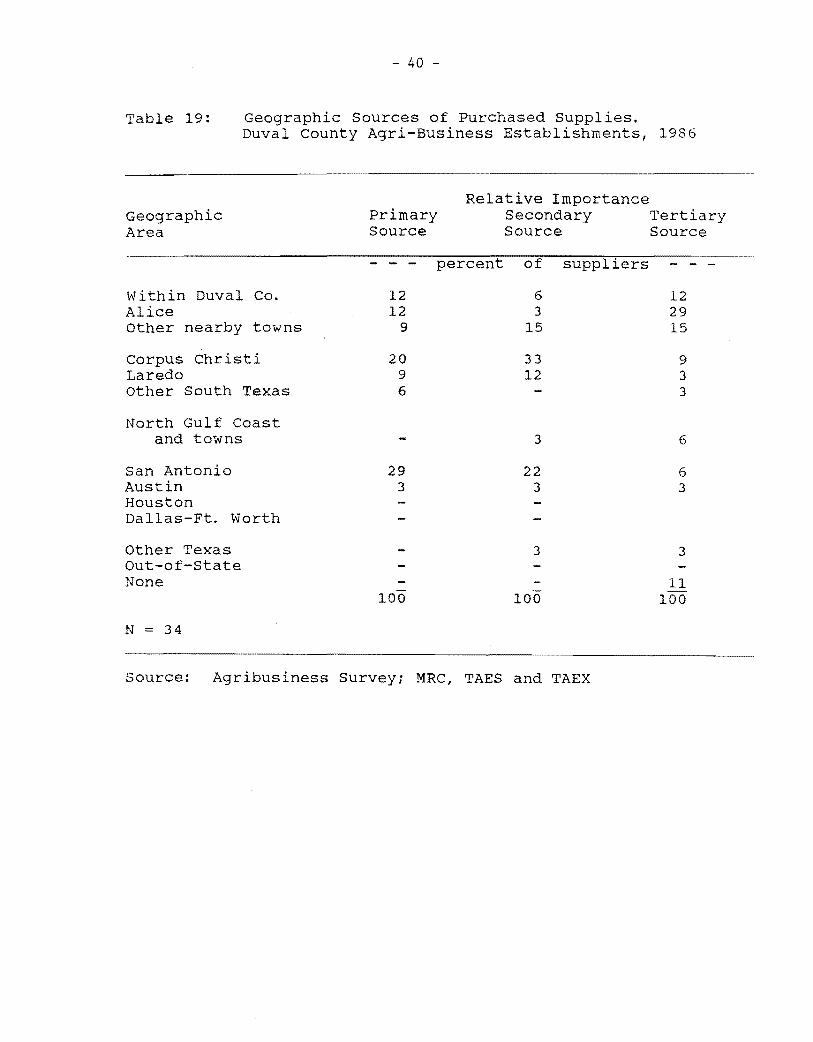

Geographic Location and ~ of Supplier

The foregoing problem is further underlined by the

consideration of the geographic sources from which supplies are

received. Corpus Christi, Laredo and San Antonio are

frequently mentioned sources, Tables 19 and 20. Suppliers in

those cities are mostly independent, sizable wholesalers.

Competition with these usually is not easy.

In those cases where local supply sources are indicated,

many are local salesmen for processor-distributor companies.

Good examples are bread, milk, and bottled drinks salesmen who

operate from a local office but represent a major food

processing firm with a processing plant and headquarters

elsewhere.

Added insight as to the structure of the marketing

channels serving Duval and Jim Wells counties is avaiable from

- - -

- 40

Table 19: Geographic Sources of Purchased Supplies. Duval County Agri-Business Establishments, 1986

Geographic Area

Within Duval Co. Alice Other nearby towns

corpus Christi Laredo other South Texas

North Gulf Coast and towns

San Antonio Austin Houston Dallas-Ft. Worth

Other Texas Out-of-State None

N 34

Relative Importance primary Secondary Source Source

- - percent of suppliers

12 6 12 3

9 15

20 33 9 12 6

3

29 22 3 3

3

100 100

Tertiary Source

12 29 15

9 3 3

6

6 3

3

11 00

Source: Agribusiness SurveYi MRC, TAES and TAEX

- 41

Table 20: Geographic Sources of Purchased Supplies Alice Agri-Business Establishments, 1986

Relative Importance Geographic Primary Secondary Tertiary Area Source Source Source

- - - percent of suppliers - -

Within Duval Co. 3 13 10 Alice 46 7 13 Other nearby towns 7 13

Corpus Christi 14 36 10 Laredo 3 7 7 Other South Texas 3 7

North Gulf Coast and towns

San Antonio 13 3 Austin 6 3 Houston 6 Dallas-Ft. Worth 3 7

6 3 17

100 100

N 31

Source: Agribusiness Survey; MRC, TAES and TAEX

- 42

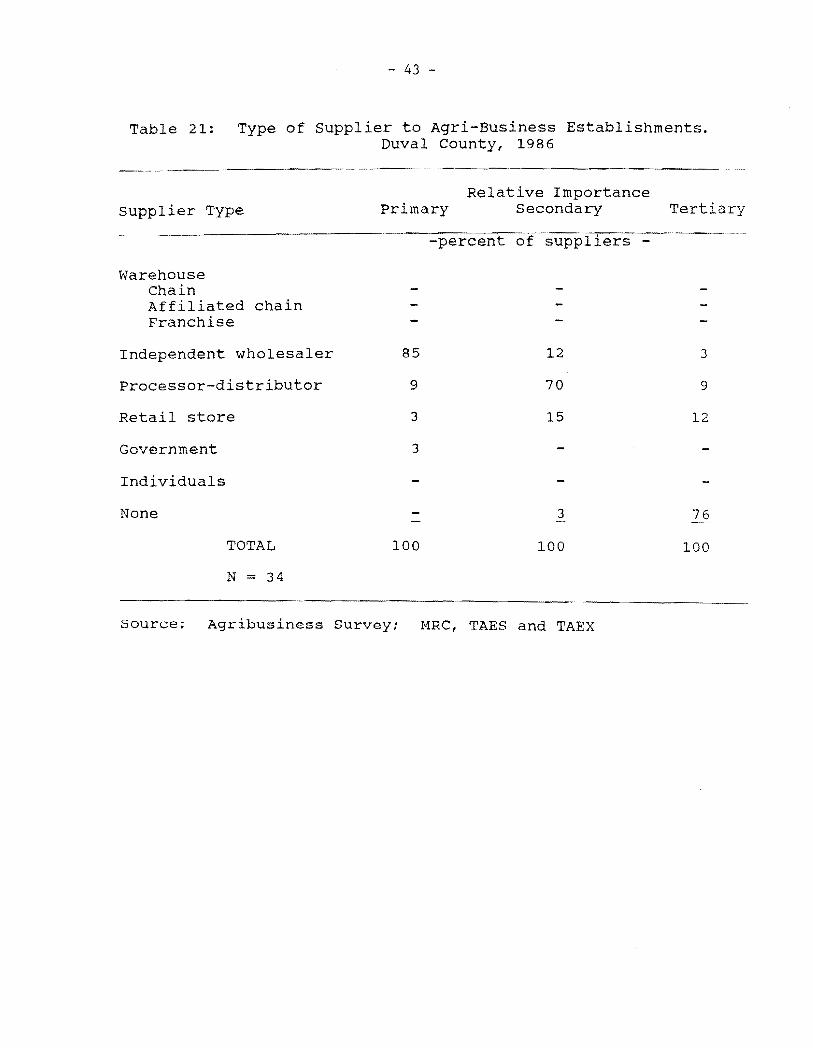

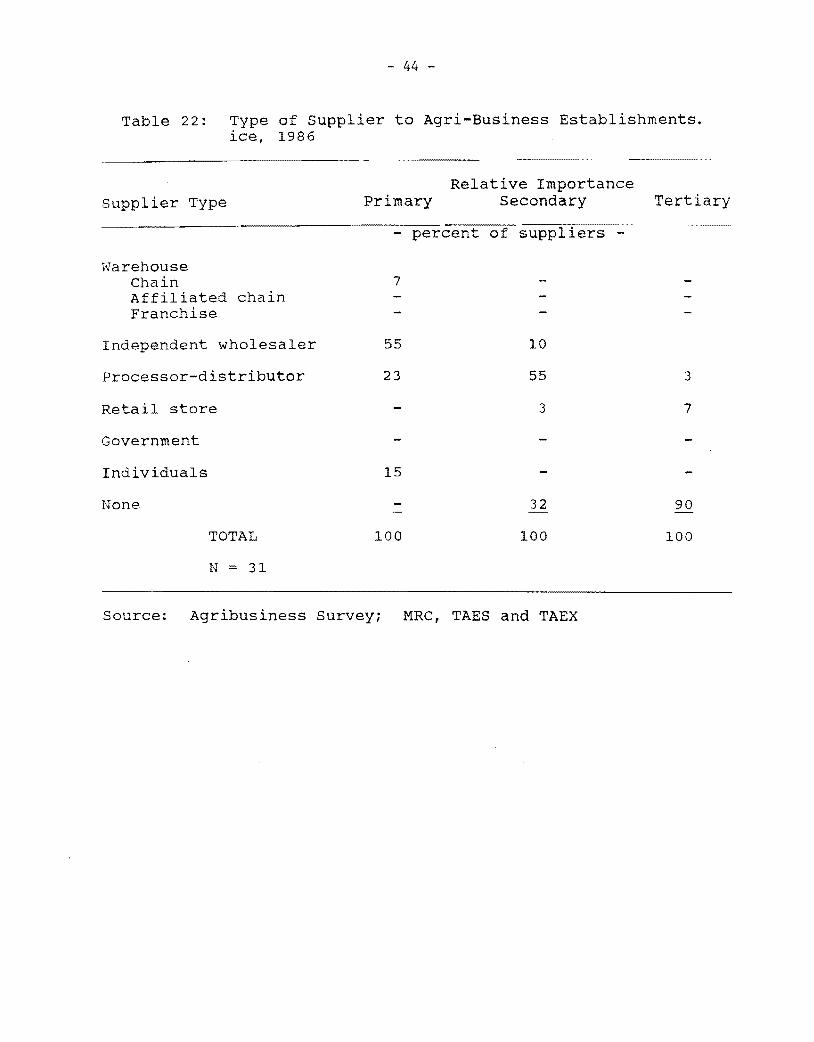

a classification of the suppliers, Tables 21 and 22. Most of

the food products are moving through independent wholesalers

located in Corpus Christi or San Antonio. Such wholesalers

have a sUbstantial volume of business over a mUlti-county area.

The volume of products handled allows advantages in their

buying and selling prices compared to what could be achieved by

any small local distributor. For that reason local wholesalers

are not generally found. However, one small grocery wholesaler

is located in Alice. It offers a cash and barry service which

allows it to be more competitive with delivery service

wholesalers from San Antonio and Corpus Christi.

An excellent decision was made when the pair of local

supermarkets, Model Markets, were developed, one in San Diego

and another in Freer. Although these can not be fully

competitive with national food chain stores in Alice, they do

keep a significant amount of food retail sales within the

County. Both the internal appearance, maintenance of

equipment, and overall management of the Model Markets should

be kept at a high level to keep them as competitive as

possible.

The processor-distributor has already been discussed and

as the figures in Tables 21 and 22 show, this is an important

marketing channel to the area r :3 retail establishments. Those

supplies indicated from government channels are commodities

going to school cafeteria lunch and other feeding programs.

Retail food stores are supply sources for small restaurants

because wholesale quantities exceed their needs and would

- 43

Table 21: Type of Supplier to Agri-Business Establishments. Duval County, 1986

Relative Importance supplier Type Primary Secondary Tertiary

---~-----~~--'--------------p-e-r-c-e-n-:-t-of suppl iers

~<Jarehouse

Chain Affiliated chain Franchise

Independent wholesaler 85 12 3

Processor-distributor 9 70 9

Retail store 3 15 12

Government 3

Individuals

None 3 76

TOTAL 100 100 100

N = 34

Source; Agribusiness Survey: MRC, TAES and TAEX

- 44

Table 22: Type of supplier to Agri-Business Establishments. ice, 1986

Relative Importance Supplier Type Primary Secondary Tertiary

Warehouse Chain Affiliated chain Franchise

7

Independent wholesaler 55

Processor-distributor 23

Retail store

Government

Individuals 15

None

TOTAL 100

N 31

10

55

3

3

7

32

100

90

100

Source: Agribusiness Survey; MRC, TAES and TAEX

- 45

result only in spoilage.

Individual suppliers, is a category used for farmers,

ranchers and others who are marketing their products at local

establishments such as through livestock auctions and grain

dealers.

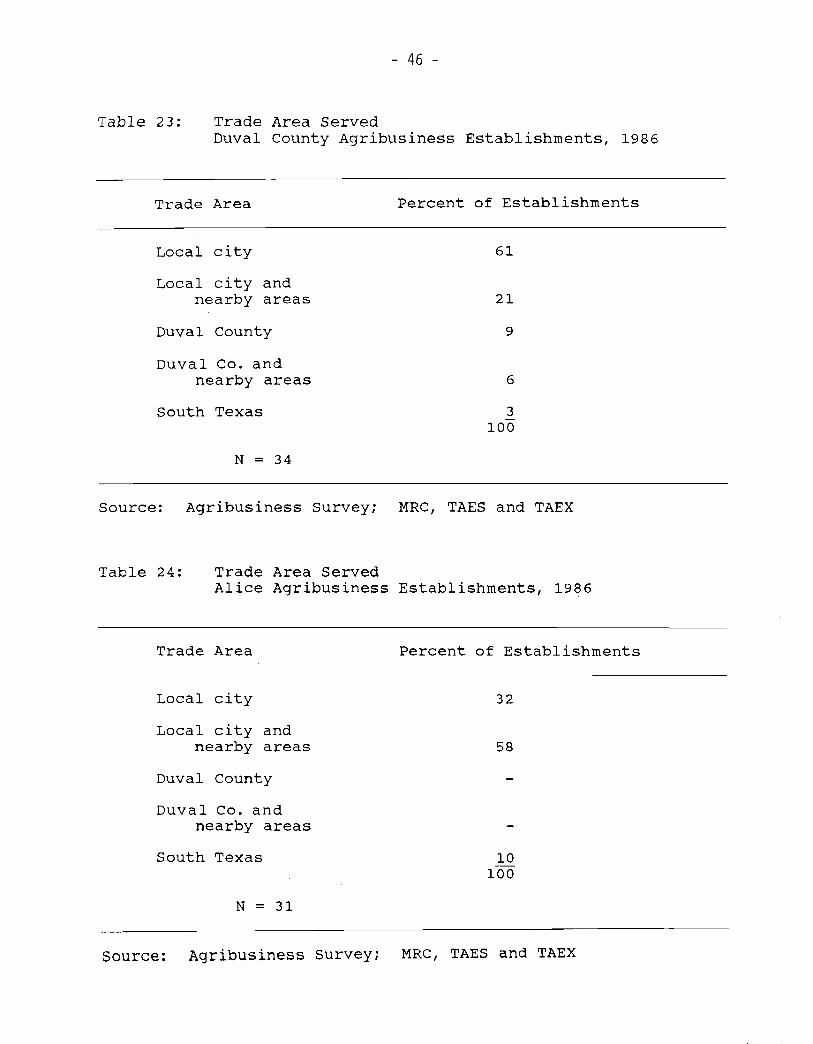

Trade Area Served and

Business Expansion Plans

outreach of the Duval County agribusiness firms very

seldom extends beyond the local county. Only ten percent of

the businesses indicated any outside customers, Table 23. The

same prevailed in Alice. This was as expected, but it points

to a key regarding the economic growth problem. Duval County

cannot achieve any decisive economic growth with its businesses

looking only inward to county area support. It must move

forward to finding a product or service that it can provide to

a much broader geographic market. Thus the search for

alternative enterprise eco-systems, in the judgement of the

Market Research Center, became an essential phase of this

study.

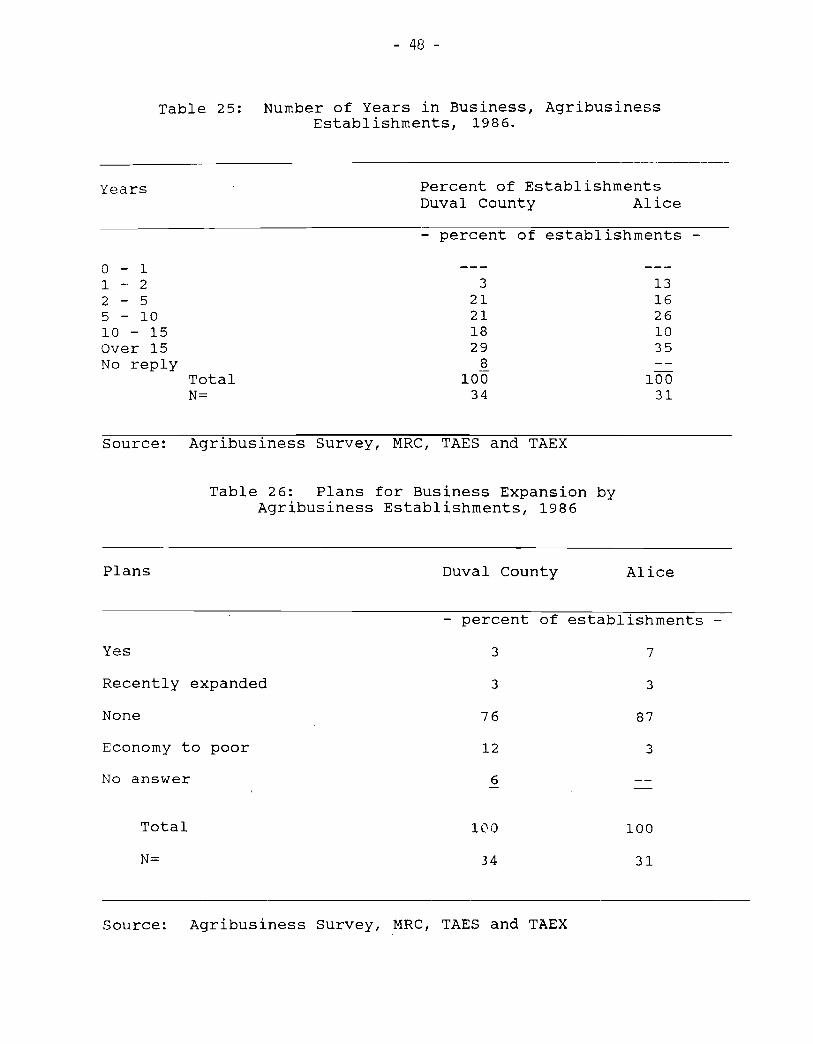

New endeavors to build the business base of the area is

implied by about a fourth of the businesses having started

within the last five years, Table 25. Unfortunately the result

is one of subdividing existing business VOlume, more than

creating any new sales volume from a larger market territory.

since expanded business territory is so important to

bringing more dollars into the local economy, an effort was

- 46

Table 23: Trade Area Served Duval County Agribusiness Establishments, 1986

Trade Area Percent of Establishments

Local city