agilent corporation and aerospace and defense directions

TRANSCRIPT

Agilent Corporation and Aerospace and Defense Directions

Aerospace/Defense DirectionsApril 2002

To revolutionize the way people live and work through technology

Agilent’s Purpose

Aerospace/Defense DirectionsApril 2002

Agilent’s Fields of Focus

Electronics

Communications

Life Sciences andChemical Analysis

Aerospace/Defense DirectionsApril 2002

Agilent’s Organization

Test & Measurement

President and CEOEdward W. (Ned) Barnholt

Electronic Productsand Solutions

Byron J. Anderson

Automated TestJohn Scruggs

CommunicationsSolutions

Thomas (Tom) White

SemiconductorProducts

Dick M. Chang

Life Sciences and Chemical Analysis

Chris van IngenGeneral CounselD. Craig Nordlund

CFOAdrian T. Dillon

HRJean M. Halloran

Corporate RelationsWilliam R. (Bill) Hahn

CTOThomas A. (Tom) Saponas

COOWilliam P. (Bill) Sullivan

Sales, Mktg. &Customer SupportLarry C. Holmberg

Agilent Laboratories

Aerospace/Defense DirectionsApril 2002

EPSG Aerospace and Defense

Marsh Faber - Messaging

Mike Granieri – U.S.

Guy Harris - Satellite

Bob Smallwood- Europe

Bill Smith- Surveillance

Orion Wood – Japan/Asia

Carl SmolkaAerospace/Defense Manager

Lynne Camp, V.P.

Outbound/Channel Manager

Mike Gasparian, V.P. & G.M.Multi Industries Business Unit

Byron Anderson, S.V.P. & G.M.Electronic Products and Solutions Group

Aerospace/Defense DirectionsApril 2002

Agilent Around the World

Customers in more than 120 countries

More than half of revenue generated outside U.S.

Global manufacturing and R&D

Aerospace/Defense DirectionsApril 2002

Innovation and contributionTrust, respect and teamworkUncompromising integritySpeedFocusAccountability

Agilent’s Values

Aerospace/Defense DirectionsApril 2002

Business Segments as a Percentage of FY01 Net Revenue*

100% = $8.4 billion

SemiconductorProductsTest and

Measurement

Life Sciences and Chemical Analysis

13%

22%65%

*See note 2

Aerospace/Defense DirectionsApril 2002

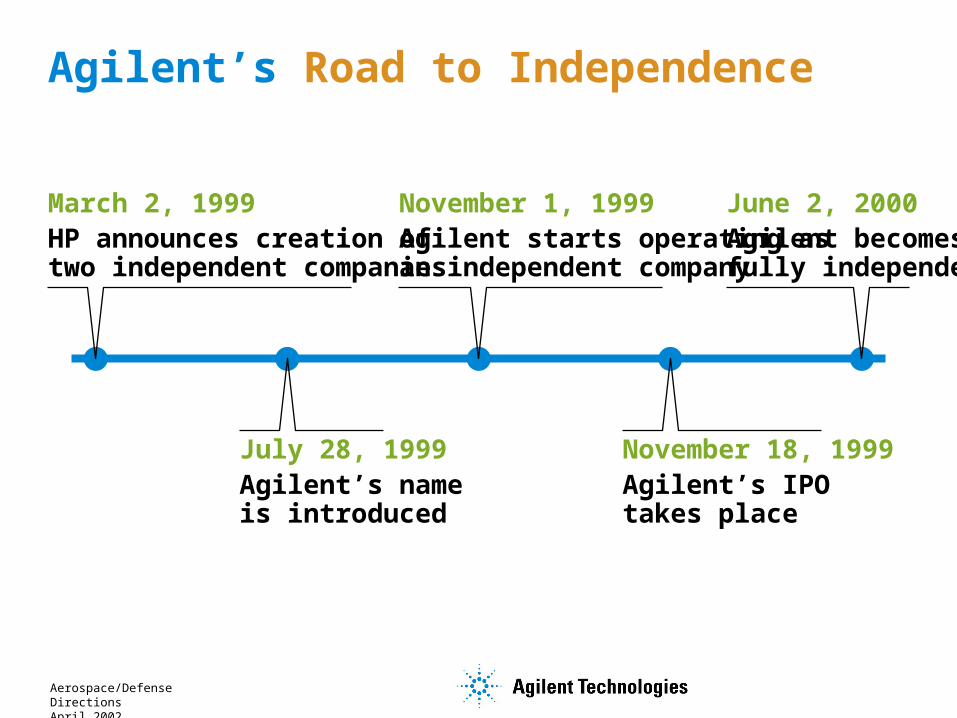

Agilent’s Road to Independence

March 2, 1999HP announces creation of two independent companies

July 28, 1999Agilent’s name is introduced

November 18, 1999Agilent’s IPO takes place

June 2, 2000Agilent becomes fully independent

November 1, 1999Agilent starts operating as an independent company

Aerospace/Defense DirectionsApril 2002

Agilent’s History

Agilent dates back to the earliest days of Hewlett-Packard, which started as a test and measurement company in 1939

Agilent embodies historical commitment to innovation and contribution, uncompromising integrity, teamwork, trust and respect for the individual

Agilent’s headquarters is erected on the site of the first HP headquarters.

Aerospace/Defense DirectionsApril 2002

Innovation and contributionTrust, respect and teamworkUncompromising integritySpeedFocusAccountability

Agilent’s Values

Aerospace/Defense DirectionsApril 2002

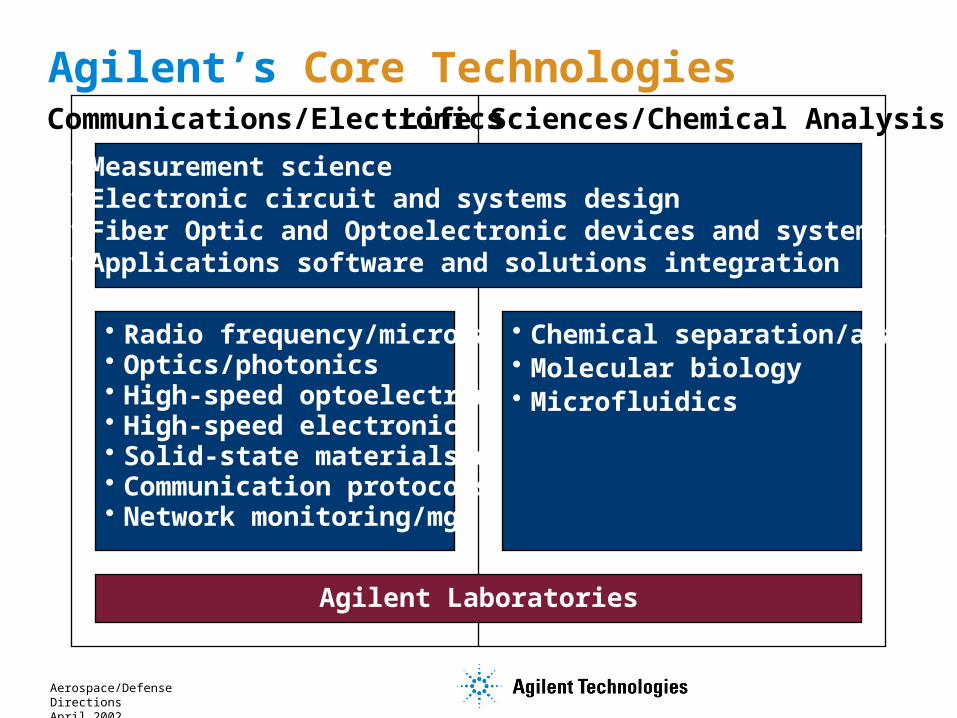

Agilent’s Core TechnologiesCommunications/ElectronicsLife Sciences/Chemical Analysis

Agilent Laboratories

Measurement science Electronic circuit and systems design Fiber Optic and Optoelectronic devices and systems Applications software and solutions integration

Radio frequency/microwave Optics/photonics High-speed optoelectronics High-speed electronics Solid-state materials/devices Communication protocols Network monitoring/mgt.

Chemical separation/analysis Molecular biology Microfluidics

Aerospace/Defense DirectionsApril 2002

Aerospace and Defense Directions

Aerospace/Defense DirectionsApril 2002

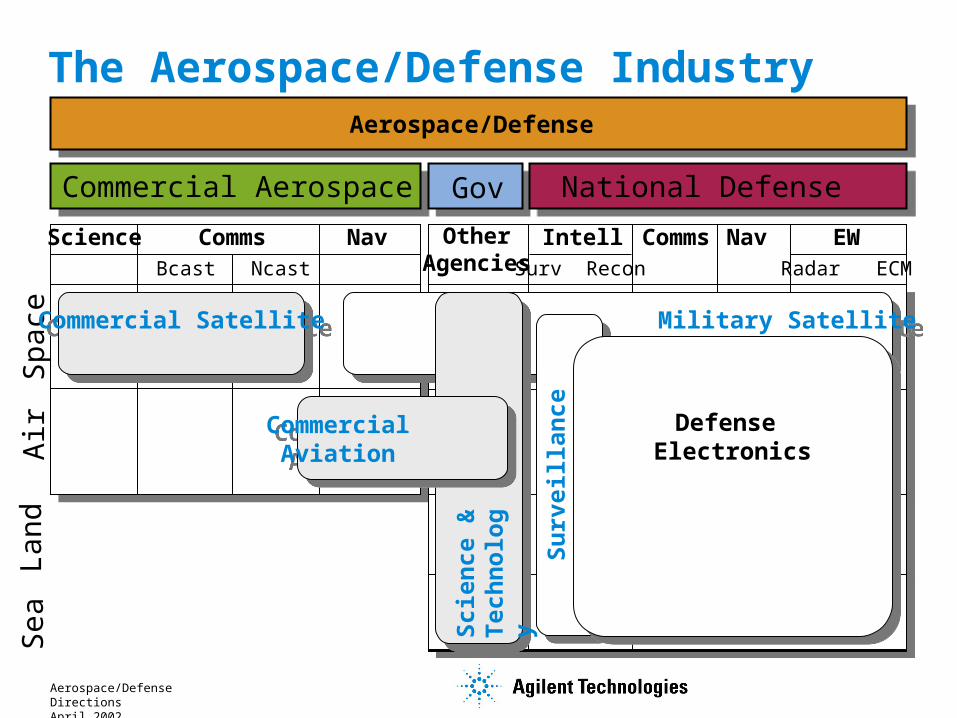

The Aerospace/Defense Industry Sectors

Space

Air

Land

Sea

NavCommsScience Intell NavCommsRadar ECMBcast

Commercial SatelliteCommercial Satellite

Ncast

EWOtherAgenciesSurv Recon

Aerospace/Defense Aerospace/Defense

Commercial Aerospace Gov National Defense

Military Satellite Military Satellite

Commercial Aviation

Commercial Aviation

Su

rveilla

nce

Su

rveilla

nce

Defense Electronics

Defense Electronics

Scie

nce &

Tech

nolo

gy

Aerospace/Defense DirectionsApril 2002

Worldwide Defense Spending Distribution

25

50

75

100

125

150

175

200

225

250

275

300

Un

ited

Sta

tes

PR

C

Ru

ssia

Fra

nce

Jap

an

Un

ited

Kin

gd

om

Germ

an

y

Italy

Sau

di A

rab

ia

S.

Kore

a

Bra

zil

Taiw

an

Ind

ia

Isra

el

Au

str

alia

139 O

thers

Total for 154 Nations:$ 922 B in $FY ‘01

Source: “World Military Expenditures and Arms Transfers 1998”, dated January 2000

US = 32%$301B in

FY’01

Western Europe

Japan – Asia/Pacific

Aerospace/Defense DirectionsApril 2002

AD Industry Money FlowDefenseAgencies

“Platform”

Providers

Sub-system

Providers

Assembly Providers

Component

Providers

Subs Primes Government

Commodities

Test & Measurement Equipment ManufacturersTest & Measurement Equipment Manufacturers

DefenseSpending

Platform Spendin

g

Defense Electronic

s

Assemblies

Components

All T&M Channels

Aerospace/Defense DirectionsApril 2002

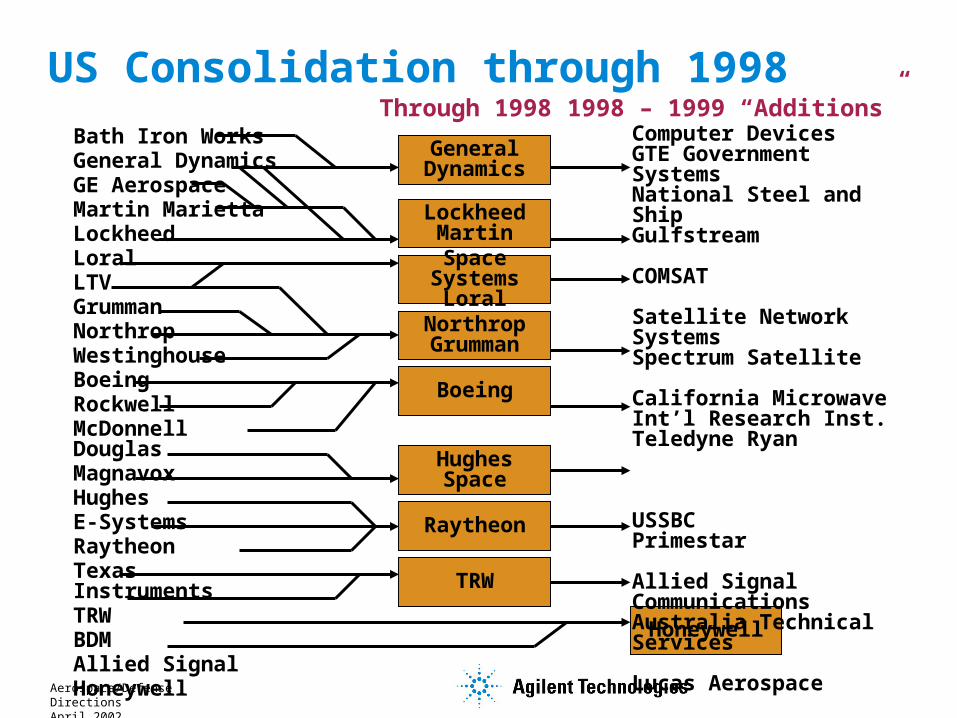

US Consolidation through 1998

General Dynamics

LockheedMartinSpace

Systems Loral

Northrop Grumman

Boeing

TRW

Raytheon

Hughes Space

Honeywell

Through 1998 1998 – 1999 “Additions”Bath Iron WorksGeneral DynamicsGE AerospaceMartin MariettaLockheedLoralLTVGrummanNorthropWestinghouseBoeingRockwellMcDonnell DouglasMagnavoxHughesE-SystemsRaytheonTexas InstrumentsTRWBDMAllied SignalHoneywell

Computer DevicesGTE Government SystemsNational Steel and ShipGulfstream

COMSAT

Satellite Network SystemsSpectrum Satellite

California MicrowaveInt’l Research Inst.Teledyne Ryan

USSBCPrimestar

Allied Signal CommunicationsAustralia Technical Services

Lucas Aerospace

Aerospace/Defense DirectionsApril 2002

Source: DFI International

Saab/CelsiusSaab/

Celsius

RheinmetallRheinmetall

EADSEADS

DassaultAviationDassaultAviation

FinnmeccanicaFinnmeccanica

MilitaryAircraft

JointVenture

DassaultOwns 6%

RacalRacal

The European Situation – Complex and Dynamic

EADSOwns 4%

EADSOwns 4% EADS

Owns 47%EADS

Owns 47%

BAESystems

BAESystems

BAEOwns 35%

BAEOwns 35%

STNAtlasSTNAtlas

ThomsonMarconi Sonar

ThomsonMarconi Sonar

Alenia MarconiSystems

Alenia MarconiSystems

AstriumEurofighter

AstriumEurofighter

New MBDAirbus

Industrie

New MBDAirbus

Industrie

Thales

Aerospace/Defense DirectionsApril 2002

Industry Attributes

Reliability perspective

MTBF often measured in hours; Failures place lives in jeopardy and impact READINESS

Test and evaluation vitalNeed to be on leading edge of diagnostic technologies

Security & Interoperability“Paradox”

Security places lives in jeopardySelective interoperability critical to effective coalition operations

Clearances often required; software configurability and interoperability testing criticalIndustry Use

ModelsAll of the “normal” in food chain +2/3 of end user lifecycle cost in O&M phase

Contractors look like high tech manufacturers; End user focused on ATE and O&M

Attribute State and Trend Business ImplicationsIndustry “Cycle Time”

Slow (3-4 X other high tech)15 Year Development Cycles> 30 Year Operational Life

Long support life Forward/backward compatibility Looking for “reliable” partners

Industry Volume and Complexity

Low volume (fly prototype)Extreme complexity (Aircraft cost is > 50% electronics)

Manufacturing looks like R&D –No One-box specialization

Aerospace/Defense DirectionsApril 2002

Defense Electronics Equipment – History + Forecast

$20

$40

$60

$80

$100

$120

$140

1980 1985 1990 1995 2000 2005

Western Europe

Japan – A/P

Former USSR

Cold War Scenario

World PeaceScenario

Rogues & Terrorists Scenario

Aerospace/Defense DirectionsApril 2002

US Consolidation through 1998

General Dynamics

LockheedMartinSpace

Systems Loral

Northrop Grumman

Boeing

TRW

Raytheon

Hughes Space

Honeywell

Through 1998 1998 – 1999 “Additions”Bath Iron WorksGeneral DynamicsGE AerospaceMartin MariettaLockheedLoralLTVGrummanNorthropWestinghouseBoeingRockwellMcDonnell DouglasMagnavoxHughesE-SystemsRaytheonTexas InstrumentsTRWBDMAllied SignalHoneywell

Computer DevicesGTE Government SystemsNational Steel and ShipGulfstream

COMSAT

Satellite Network SystemsSpectrum Satellite

California MicrowaveInt’l Research Inst.Teledyne Ryan

USSBCPrimestar

Allied Signal CommunicationsAustralia Technical Services

Lucas Aerospace

Aerospace/Defense DirectionsApril 2002

Source: DFI International

Saab/CelsiusSaab/

Celsius

RheinmetallRheinmetall

EADSEADS

DassaultAviationDassaultAviation

FinnmeccanicaFinnmeccanica

MilitaryAircraft

JointVenture

DassaultOwns 6%

RacalRacal

The European Situation – Complex and Dynamic

EADSOwns 4%

EADSOwns 4% EADS

Owns 47%EADS

Owns 47%

BAESystems

BAESystems

BAEOwns 35%

BAEOwns 35%

STNAtlasSTNAtlas

ThomsonMarconi Sonar

ThomsonMarconi Sonar

Alenia MarconiSystems

Alenia MarconiSystems

AstriumEurofighter

AstriumEurofighter

New MBDAirbus

Industrie

New MBDAirbus

Industrie

Thales

Aerospace/Defense DirectionsApril 2002

Defense Electronics and Defense Platforms Aircraft

Includes UAV’s and Helicopters

Ships Primary Shipboard

EquipmentVehicles

Wheeled and Tracked Terrestrial Platforms

Space Lift, Payloads And

Supporting InfrastructureLow Mobility

Electronic /IT/ SW Systems not platform specific

MissilesOrdnance / Weapons

Radar Search, Detection and

TrackingElectronic

Countermeasures Detection and Deception

Communications Voice and Data

Surveillance & Reconnaissance

Identification and LocationNavigation and

Guidance GPS and Landing Systems

Control and Computation

Control, Displays, Processors

WeaponsAmmunition and Armor

PropulsionEngines, Fuel, Drive Train, Suspension

Aerospace/Defense DirectionsApril 2002

Aerospace/Defense ExampleDefenseAgencies

“Platform”

Providers

Sub-system

Providers

Assembly Providers

Component

Providers

Subs Primes Government

Commodities

Fighter Fighter Air Forc

e

Air Forc

e

Radar Radar

EnginesEngines

Airframe Airframe

EW systemEW system

Navigation &Guidance

Navigation &Guidance

LOs and exciters

•Processors •Power Supplies •Power Converters•A/D, D/A Converters•Antennas

•Processors •Power Supplies •Power Converters•A/D, D/A Converters•Antennas

Test & Measurement Equipment ManufacturersTest & Measurement Equipment Manufacturers

T&M ChannelsT&M Channels

MMICs•Power Transistors•Circulators •Interconnect / Substrates•Optoelectro Amplifiers•SAW Devices•ASICs•Oscillators•Phase Shifters

•Power Transistors•Circulators •Interconnect / Substrates•Optoelectro Amplifiers•SAW Devices•ASICs•Oscillators•Phase Shifters

CommsComms

Reconn & Surveillance

Transmitter/ Receivers

Mod/demodSignal

Processing

Aerospace/Defense DirectionsApril 2002

AD Industry Value Delivery System

DefenseAgencies

“Platform”

Providers

Sub-system

Providers

Assembly Providers

Component

Providers

Subs Primes Government

Commodities

Test & Measurement Equipment ManufacturersTest & Measurement Equipment Manufacturers

T&M ChannelsT&M Channels

•Processors •Power Supplies •Power Converters•A/D, D/A Converters•Antennas

•Processors •Power Supplies •Power Converters•A/D, D/A Converters•Antennas

•Power Transistors•Circulators Interconn/ Substrates•OE Amplifiers•SAW Devices•ASICs•Oscillators•Phase Shifters

•Power Transistors•Circulators Interconn/ Substrates•OE Amplifiers•SAW Devices•ASICs•Oscillators•Phase Shifters

Lockheed Martin

RaytheonITT Industries

Northrop Grumman

LittonTRW

L-3 CommsGeneral

DynamicsDaimlerChrysler

BAE SystemsThales

Lockheed MartinRaytheonBoeingBAE SystemsEADSThales

ArmyNavyAir Force

Aerospace/Defense DirectionsApril 2002

AD Industry Test And Measurement Perspective Defense

Agencies“Platform

” Providers

Sub-system

Providers

Assembly Providers

Component

Providers

Subs Primes Government

Commodities

Test & Measurement Equipment ManufacturersTest & Measurement Equipment Manufacturers

T&M ChannelsT&M Channels

G.P. Instruments

Application Specific Instruments

“SIMPLE” Parametric and

Functional Test Systems” En

vir

on

me

nt

An

aly

sis

&

Sim

ula

tio

n

“COMPLEX” Parametric & Functional Test Systems

IntegratedMaintenance

Portable

ATE/ATS

Bench Rep & Cal

(GPTE)

Aerospace/Defense DirectionsApril 2002

Key Forces, Trends and Implications

Reliability

Complexity

Longevity

Branch Centric

Firepower

Readiness

Reliability

Complexity

Longevity

Network-Centric

Precision Force

Affordability

People die when

systems fail

15 year developments30 + year life-cycles

System of Electronic systems

Joint OperationsCoalitions &

Information Warfare(Sensor to Shooter)

“Cold War” ScenarioTo “World Peace”

To Rogues & Terrorists

Manual repair & calibration moving to ATS & integrated diagnostics

Signal/systemsimulation and analysis functionality & performance

Seamless product migration plans

Reduced test costs over all elements of system life-cycle

From To T&M Implication Driver

Aerospace/Defense DirectionsApril 2002

Defense Electronics – Key Technology TrendsRadar

EW

CommsTac

Nav/Guide

Surveillance

Sat

ATS/ATE

Bench Rep/Cal

Single T/RSingle mode

Conformal digital Fully integrated

Phased Array (AESA)Multiple modes

Specific Function

Multimode Fully Integrated

Single Signal Type(“hardwired”)

Multiple Signal Types(reconfigurable)GPS infrastructure

upgrades

Per sub-system testers

Per service comprehensive ATS

Joint synthetic instrument ATS

Wide variety of test equipment

Few, highly capable instruments

Low BW analog

High BW secure digitalAnalog Radio Digital radio Software-Defined radio

‘80s and ‘90s Today Future

Aerospace/Defense DirectionsApril 2002

Radar Performance Evolution

Fixed channel analog receiver

Simple waveform set

Low noise RF Standard A/D

and D/A conversion

Fixed multi-channel analog receiver

Complex waveform set

Very low noise RF High speed large

dynamic range A/D and D/A conversion

Variable channel digital receiver

Direct digital synthesis waveforms

Extremely low noise RF

Module level high speed A/D & D/A conversion

PastMechanically Steered

Antenna (MSA)

CurrentActive Electronically

Steered Antenna (AESA)

FutureDigital Radar

Aerospace/Defense DirectionsApril 2002

EW Performance Evolution

Single mode and single function

Dedicated “aperture”

Little attention to power management

Focus on detection

Loose integration

Mode switching

Focus on power management

Focus on friend or foe determination

Fully integrated system

Multiple modes

Shared “apertures”

Focus on identification and discrimination

PastSingle Function

CurrentMultifunction

FutureFully Integrated

Aerospace/Defense DirectionsApril 2002

Tactical Radio EvolutionPast

Analog RadioCurrent

Digital radioFuture

Software Defined radio

Analog (voice) traffic

Designed in interoperability (stovepipe)

Point-to-Point

Analog and Digital traffic (voice/data)

Limited interoperability

Some network client capability

Multimedia traffic (voice/data/video)

Software defined security and interoperability

Full network participant

Aerospace/Defense DirectionsApril 2002

Signal Monitoring/Intelligence Evolution

PastAnalog Channels

CurrentAnalog & Digital Channels

FutureSoftware Defined Channels

Unique “hardwired” configuration per signal type

Custom “Rack and Stack” receivers

Analog signal processing

Software configurable signal types

Wider bandwidth down conversions

More sophisticated digital signal processing

Unique “Firmware” configuration per signal type

Analog block down conversion

Digital signal processing

Aerospace/Defense DirectionsApril 2002

Military Communications Satellite EvolutionPast

Analog “Bent Pipe”Current

Digital TransparentFuture

Digital Regenerative

Analog (voice & video) traffic

Analog modulation

Signal amplification in satellite

36 MHz channels

Analog and digital traffic

Vector modulation

Analog signal amplification in satellite

36 MHz channels

Wideband digital traffic

Vector modulation

Digital signal regeneration in satellite

36-72-120 MHz channels

Aerospace/Defense DirectionsApril 2002

Automatic Test System EvolutionPast

Per Service and Per Platform ATS

CurrentPer Service but Platform

Common ATS

FutureJoint Service

Common Platform ATS

Unique configuration per system

Primarily “Rack and Stack” instruments

Unique Test Program Sets (TPS) of fixturing, and SW

Focus on “long-life” HW architectures

Hybrid mix of instruments and “modules”

Preserve TPS investment

Focus on more capable HW architectures

Any signal on any pin at any time

Optimize TPS coverage

Aerospace/Defense DirectionsApril 2002

Repair & Calibration Test System EvolutionPast

Hundreds ofMakes/Models

CurrentTens of

Makes/Models

FutureOne Very Capable

Make/Model

Test equipment specified by equipment supplier

Cost plus focus discourages commonality

Test equipment constrained by equipment buyer

Affordability realized by inventory reduction

Test equipment capability a given

Affordability and Readiness maximized

Technology refresh paths enhanced

Multimeters = 100

Oscilloscopes = 250

Aerospace/Defense DirectionsApril 2002

Thank you