africa: tapping into the untapped

TRANSCRIPT

Africa: Tapping into the UntappedAfrica: Tapping into the Untapped

Growing Consumer Demand Driving Mega Growth OpportunitiesGrowing Consumer Demand Driving Mega Growth Opportunities

2020--21 March 201221 March 2012

Surfactants HPC, DubaiSurfactants HPC, Dubai

Agenda

1. Frost & Sullivan - Introduction

2. Mega Trends - How do we define it and why does it really matter?

3. Mega Trends in Africa and its Impact on Various Sectors

4. 4W - What, When, Where and Why of the Mega Trends on Key Sectors

– Home and Personal care – Home and Personal care

– Future outlook

– Demand and supply projections

5. Conclusions - Is Africa the Next Frontier ?

2

`̀

The Frost & Sullivan Story

3

Pioneered Emerging Market & Technology Research

• Global Footprint Begins

• Country Economic Research

• Market & Technical Research

• Best Practice Career Training

• MindXChange Events

Partnership Relationship with Clients

• Growth Partnership Services

• GIL Global Events

• GIL University

• Growth Team Membership™

• Growth Consulting

Visionary Innovation

• Mega Trends Research

• CEO 360 Visionary Perspective

• GIL Think Tanks

• GIL Global Community

• Communities of Practice

Our Industry Coverage

Automotive

&

Transportation

Aerospace & Defense Measurement &Instrumentation

Information &Communication Technologies

ConsumerTechnologies

4

HealthcareEnvironment & BuildingTechnologies

Energy & PowerSystems

Chemicals, Materials& Food

Electronics &Security

Industrial Automation& Process Control

AutomotiveTransportation & Logistics

Minerals & Mining

Our Services

Growth Partnership GIL University

GIL Global Community

5

Growth PartnershipServices

Growth Consulting

GIL University

Events

Our Global Footprint 40+ OfficesScanning the Globe for Opportunities and Innovation

6

2. Mega Trends - How do we define it and why does it really matter?

7

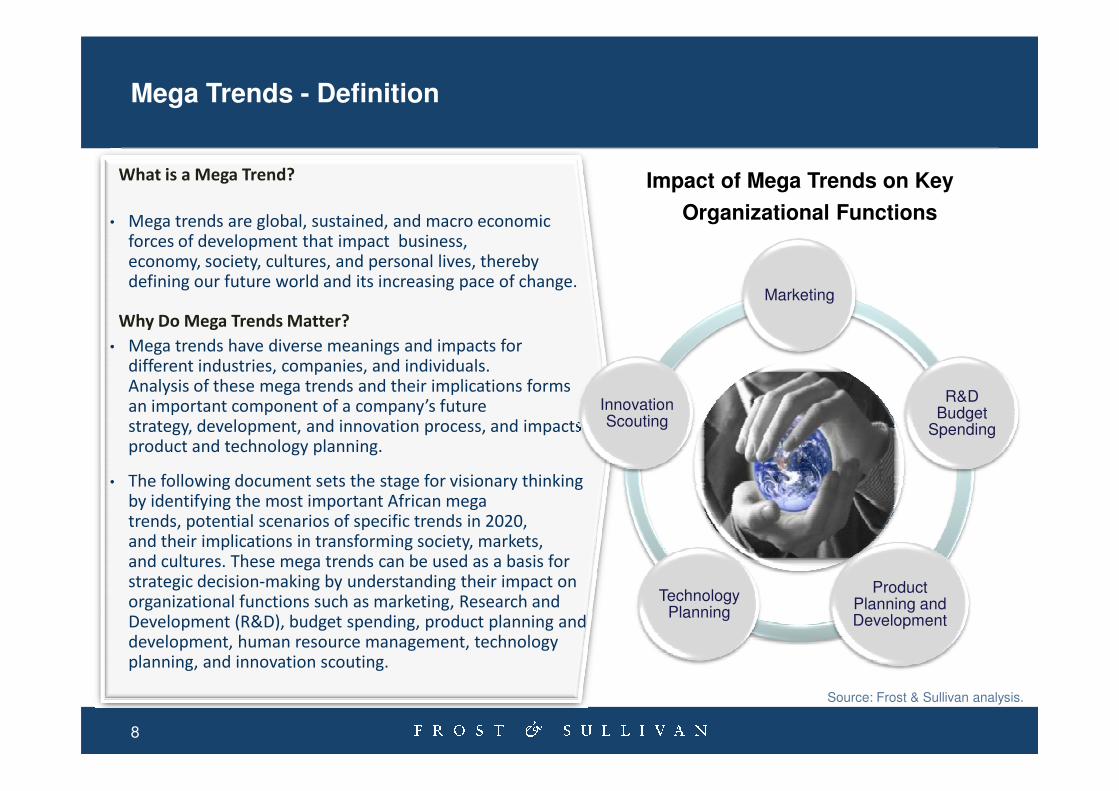

What is a Mega Trend?

• Mega trends are global, sustained, and macro economic forces of development that impact business, economy, society, cultures, and personal lives, thereby defining our future world and its increasing pace of change.

• Mega trends have diverse meanings and impacts for different industries, companies, and individuals.Analysis of these mega trends and their implications forms an important component of a company’s future

Impact of Mega Trends on Key

Organizational Functions

Marketing

R&D Innovation

Why Do Mega Trends Matter?

Definition of a Mega TrendMega Trends - Definition

Analysis of these mega trends and their implications forms an important component of a company’s future strategy, development, and innovation process, and impacts product and technology planning.

• The following document sets the stage for visionary thinking by identifying the most important African mega trends, potential scenarios of specific trends in 2020,and their implications in transforming society, markets, and cultures. These mega trends can be used as a basis for strategic decision-making by understanding their impact on organizational functions such as marketing, Research and Development (R&D), budget spending, product planning and development, human resource management, technology planning, and innovation scouting.

R&D Budget

Spending

Product Planning and Development

Technology Planning

Innovation Scouting

Source: Frost & Sullivan analysis.

8

Global Mega Trends Driving Growth

URBANIZATION

ENERGYSMART

FACTORY

GLOBAL MEGA

E-MOBILITY

SOCIAL

ECONOMY

TECHNOLOGY

INFRASTRUCTURE

BUSINESS

HEALTH &

WELLNESS

GLOBAL MEGA TRENDS - 2020

9

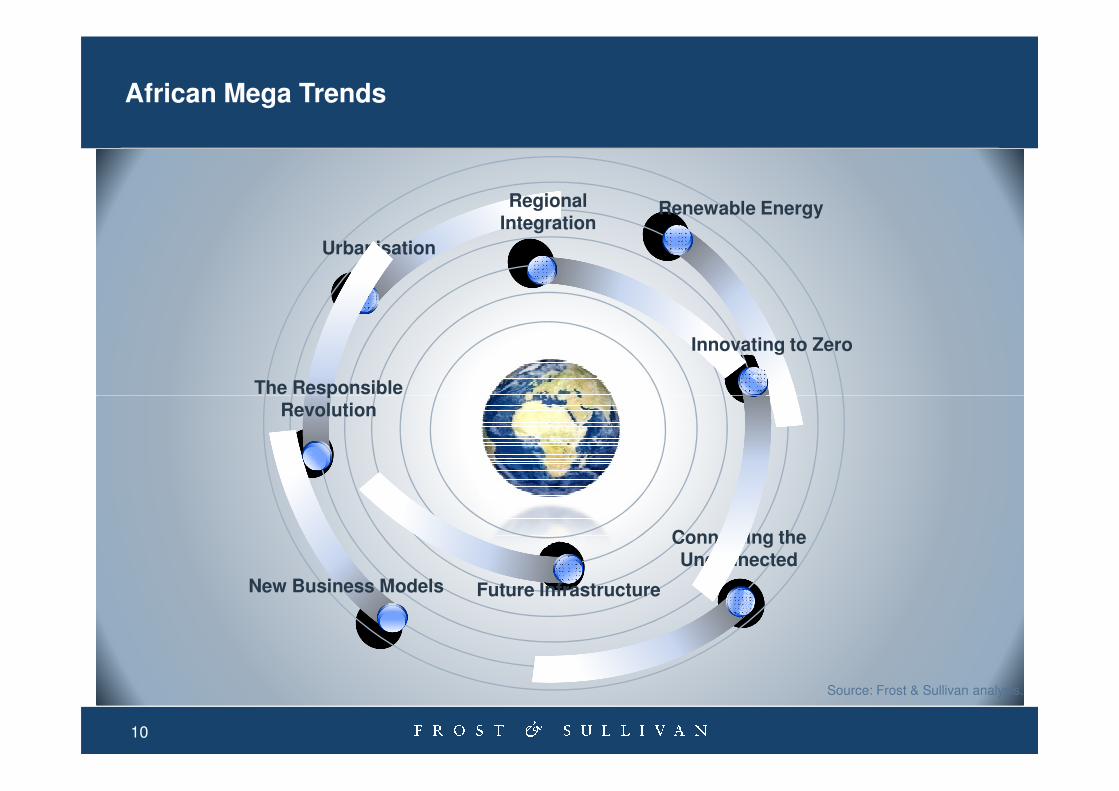

African Mega Trends

Urbanisation

Regional Integration

Renewable Energy

Innovating to Zero

The Responsible

Connecting the Unconnected

New Business Models Future Infrastructure

Source: Frost & Sullivan analysis.

The Responsible Revolution

10

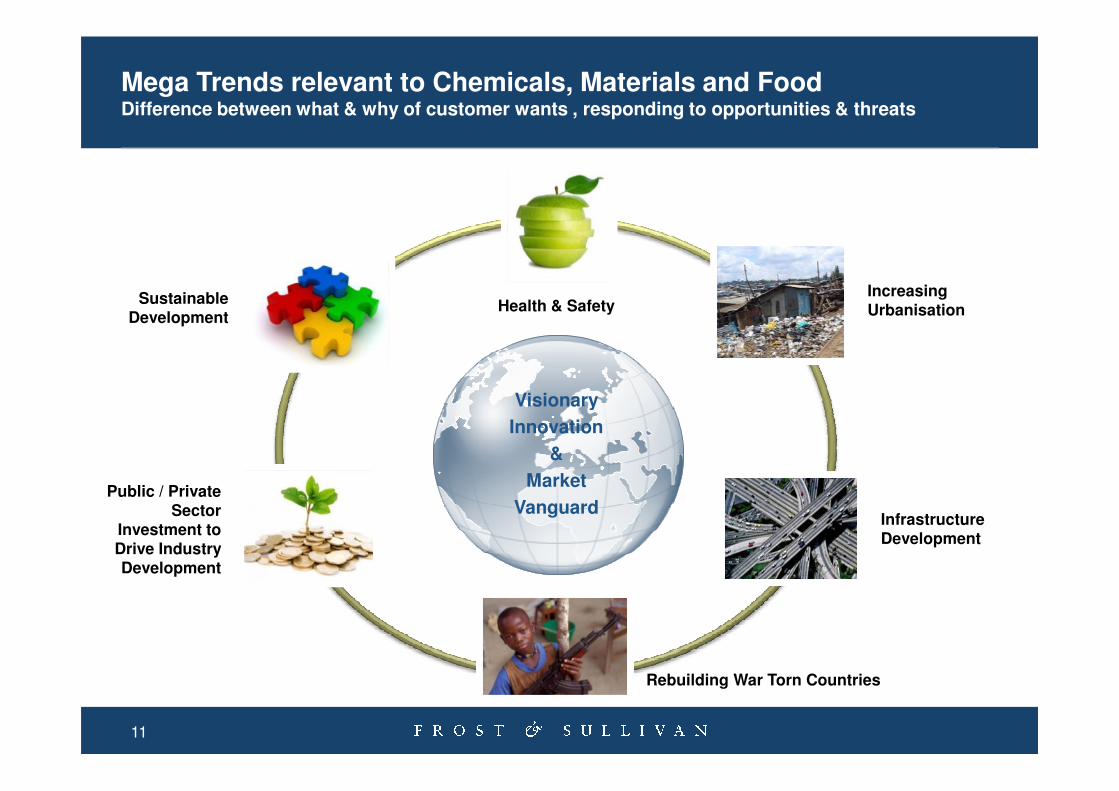

Mega Trends relevant to Chemicals, Materials and Food Difference between what & why of customer wants , responding to opportunities & threats

Increasing Urbanisation

Visionary

Health & SafetySustainable Development

Infrastructure Development

Visionary

Innovation

&

Market

VanguardPublic / Private

Sector Investment to Drive Industry Development

Rebuilding War Torn Countries

11

3. Mega Trends in Africa and its Impact on Various Sectors

12

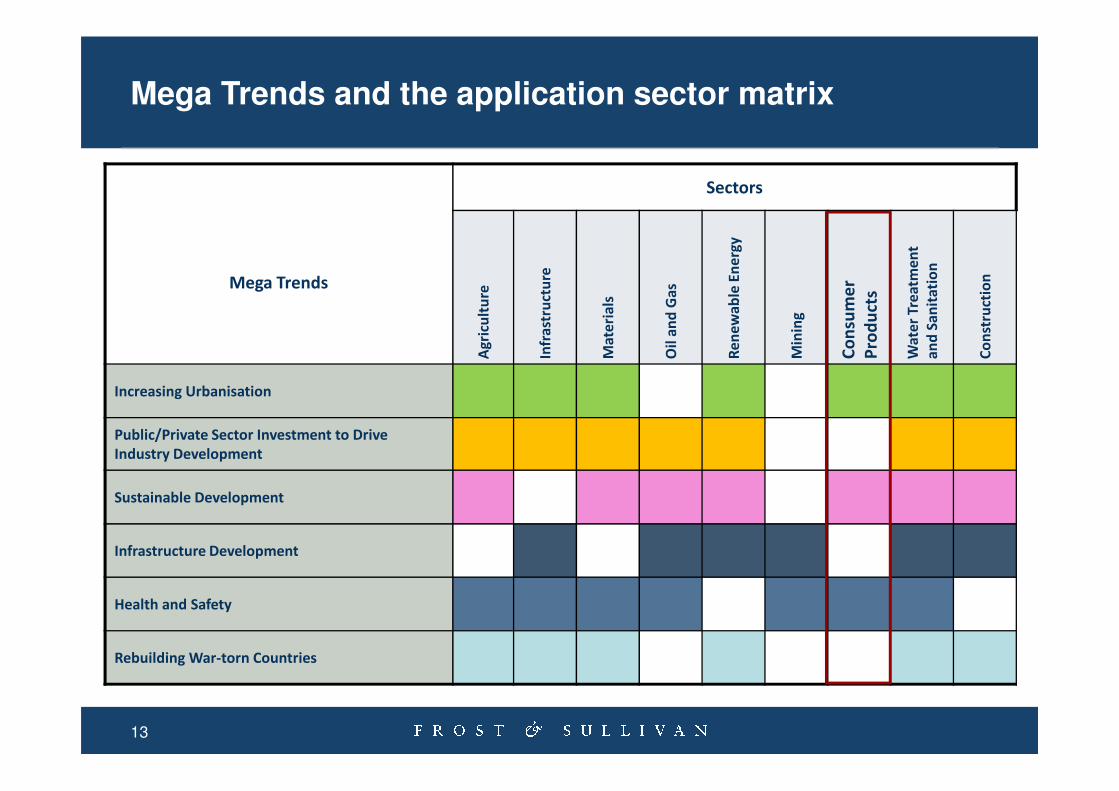

Mega Trends and the application sector matrix

Mega Trends

Sectors

Ag

ricu

ltu

re

Infr

ast

ruct

ure

Ma

teri

als

Oil

an

d G

as

Re

ne

wa

ble

En

erg

y

Min

ing

Co

nsu

me

r

Pro

du

cts

Wa

ter

Tre

atm

en

t

an

d S

an

ita

tio

n

Co

nst

ruct

ion

Increasing UrbanisationIncreasing Urbanisation

Public/Private Sector Investment to Drive

Industry Development

Sustainable Development

Infrastructure Development

Health and Safety

Rebuilding War-torn Countries

13

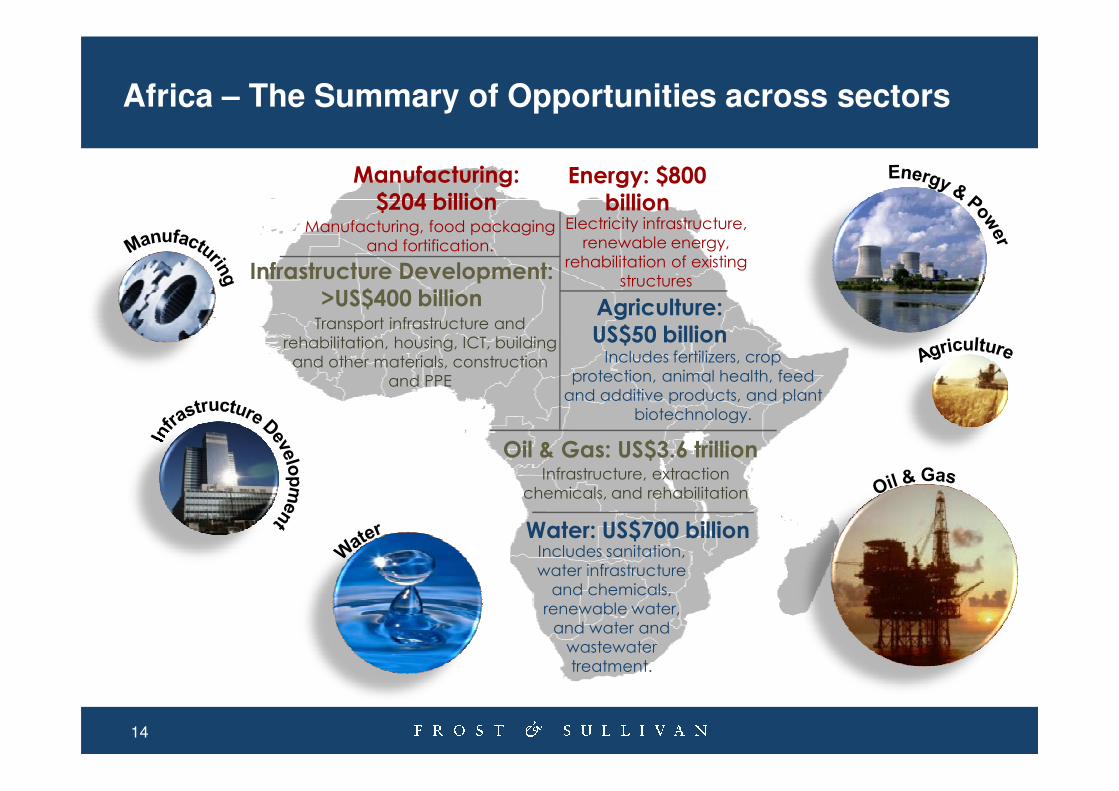

Energy: $800 billion

Electricity infrastructure,

renewable energy,

rehabilitation of existing

structures

Agriculture: US$50 billionIncludes fertilizers, crop

protection, animal health, feed

and additive products, and plant

Infrastructure Development: >US$400 billionTransport infrastructure and

rehabilitation, housing, ICT, building

and other materials, construction

and PPE

Manufacturing: $204 billion

Manufacturing, food packaging

and fortification.

Africa – The Summary of Opportunities across sectors

Water: US$700 billionIncludes sanitation,

water infrastructure

and chemicals,

renewable water,

and water and

wastewater

treatment.

Oil & Gas: US$3.6 trillionInfrastructure, extraction

chemicals, and rehabilitation

and additive products, and plant

biotechnology.

14

Key Mega Trends to Drive Home and Personal Care Sectors

African Mega TrendsMost Relevant

to Surfactants

1. Increasing urbanisation

2. Infrastructure development -

3. Rebuilding war-torn countries -

4. Public/private sector

investment to drive industry -

Increasing Urbanisation

• By 2020, 43 per cent of the people living in

Africa will live in urban areas. This presents a

growth opportunity for FMCG manufacturers

and their suppliers in the home and personal

care market, as increased usage is forecasted.

Sustainable Developmentinvestment to drive industry

development

-

5. Sustainable development

6. Health and safety

• This refers to using sustainable and

environmentally-friendly raw materials and

processes in the production of home care and

personal care products. Resources are limited.

Health and Safety

• To protect employees, consumers, and the

environment during the manufacturing and

consuming of home care and personal care

products.Urban population in Africa (millions): 205

1990

2010

400

2050

1,230

Fast Facts about Africa:

Source: Frost & Sullivan analysis.

15

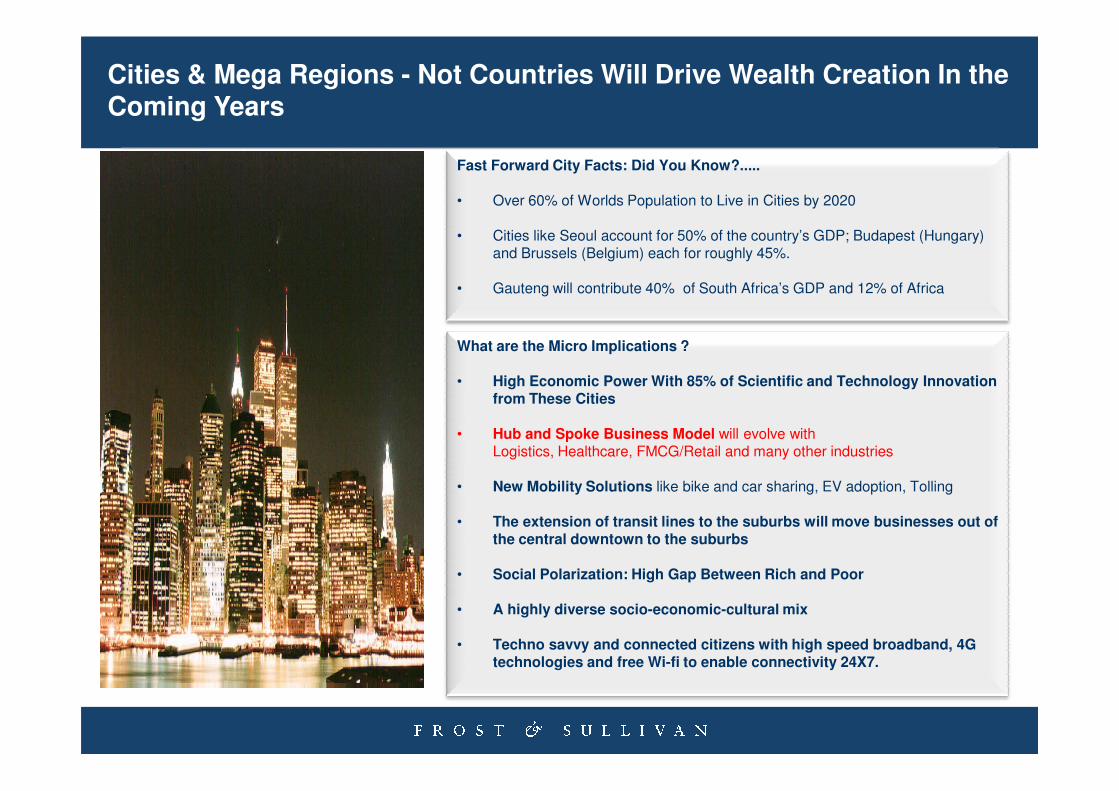

Cities & Mega Regions - Not Countries Will Drive Wealth Creation In the Coming Years

Fast Forward City Facts: Did You Know?.....

• Over 60% of Worlds Population to Live in Cities by 2020

• Cities like Seoul account for 50% of the country’s GDP; Budapest (Hungary) and Brussels (Belgium) each for roughly 45%.

• Gauteng will contribute 40% of South Africa’s GDP and 12% of Africa

What are the Micro Implications ?

• High Economic Power With 85% of Scientific and Technology Innovation from These Cities from These Cities

• Hub and Spoke Business Model will evolve with Logistics, Healthcare, FMCG/Retail and many other industries

• New Mobility Solutions like bike and car sharing, EV adoption, Tolling

• The extension of transit lines to the suburbs will move businesses out of the central downtown to the suburbs

• Social Polarization: High Gap Between Rich and Poor

• A highly diverse socio-economic-cultural mix

• Techno savvy and connected citizens with high speed broadband, 4G technologies and free Wi-fi to enable connectivity 24X7.

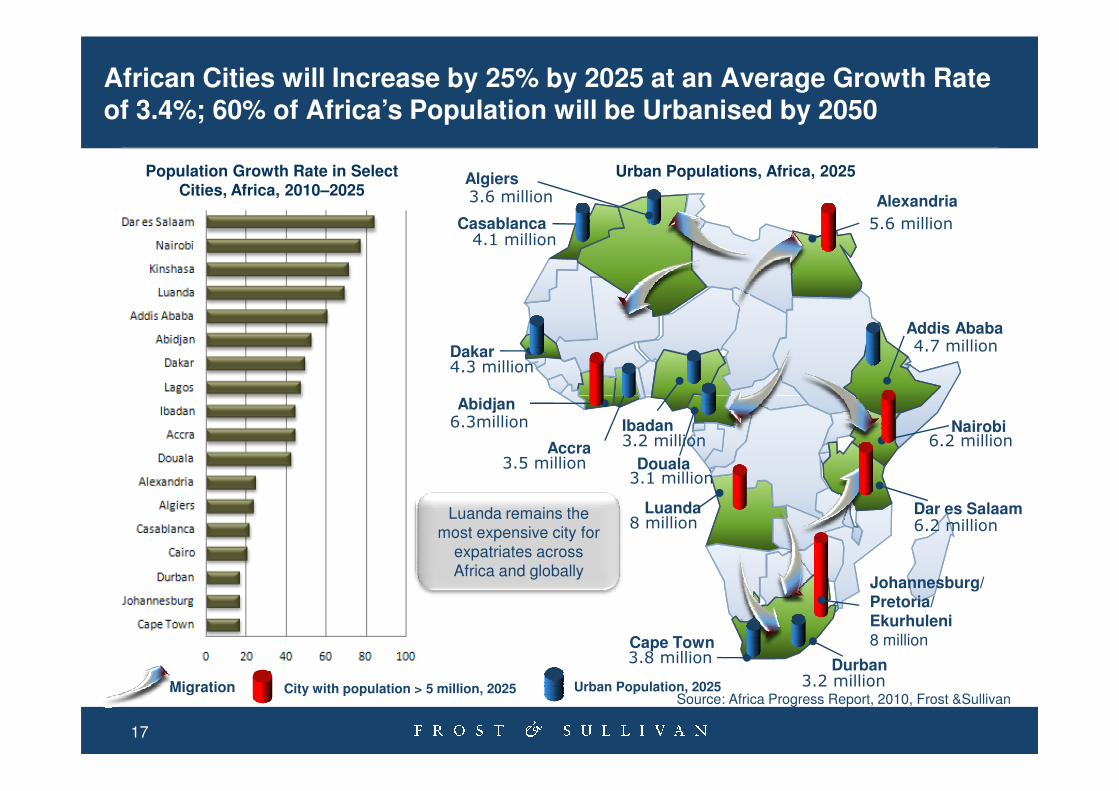

African Cities will Increase by 25% by 2025 at an Average Growth Rate of 3.4%; 60% of Africa’s Population will be Urbanised by 2050

Population Growth Rate in Select Cities, Africa, 2010–2025

Algiers

Alexandria

Casablanca

Abidjan

Addis Ababa

Dakar

5.6 million

3.6 million

4.1 million

4.3 million

4.7 million

Urban Populations, Africa, 2025

Source: Africa Progress Report, 2010, Frost &Sullivan

Dar es Salaam

Nairobi

Accra

Abidjan

Ibadan

Douala

Cape Town

Durban

3.2 million

3.1 million

6.2 million

6.2 million

3.8 million

3.2 million

3.5 million

6.3million

Luanda8 million

Migration Urban Population, 2025City with population > 5 million, 2025

Luanda remains the most expensive city for

expatriates across Africa and globally

Johannesburg/Pretoria/Ekurhuleni8 million

17

4000

5000

6000

7000

Upper middle class

Middle class

Lower middle class

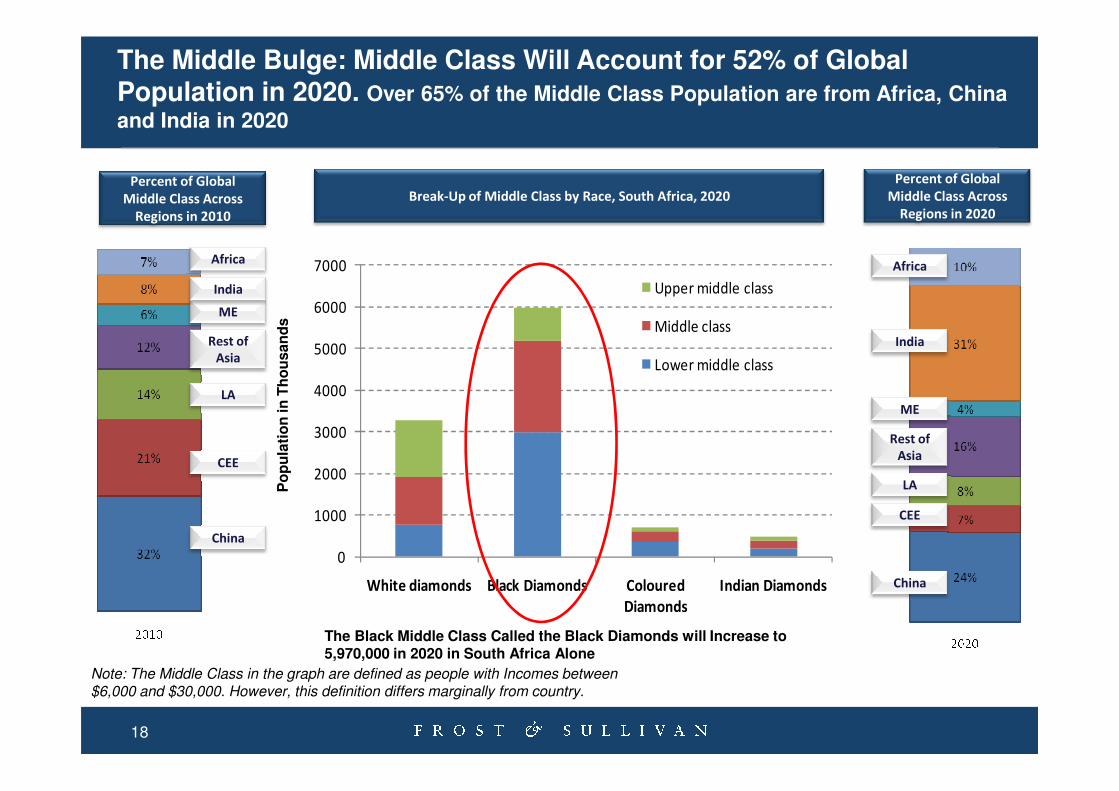

The Middle Bulge: Middle Class Will Account for 52% of Global Population in 2020. Over 65% of the Middle Class Population are from Africa, China

and India in 2020

LA

Rest of

Asia

ME

India

Africa

India

Africa

Percent of Global

Middle Class Across

Regions in 2010

Percent of Global

Middle Class Across

Regions in 2020

Break-Up of Middle Class by Race, South Africa, 2020

Po

pu

lati

on

in

Th

ou

san

ds

0

1000

2000

3000

4000

White diamonds Black Diamonds Coloured

Diamonds

Indian Diamonds

China

CEE

LA

China

CEE

LA

Rest of

Asia

ME

The Black Middle Class Called the Black Diamonds will Increase to 5,970,000 in 2020 in South Africa Alone

Po

pu

lati

on

in

Th

ou

san

ds

Note: The Middle Class in the graph are defined as people with Incomes between$6,000 and $30,000. However, this definition differs marginally from country.

18

4. 4W - What, When, Where and Why of the Mega Trends on Key Sectors

19

Unlocking the Opportunities presented by Mega Trends

Where are the

Why is Africa the next big

opportunity for home and

How can you adapt your

strategies to tap into this massive

opportunity Africa presents?

What are the key mega trends that would drive business for home and

personal care companies in

Africa ?

When can you expect to see the impact of

micro trends on the business environment?

Where are the key

opportunities that would manifest in

Africa by 2020?

home and personal care

suppliers?

Source: Frost & Sullivan analysis.

20

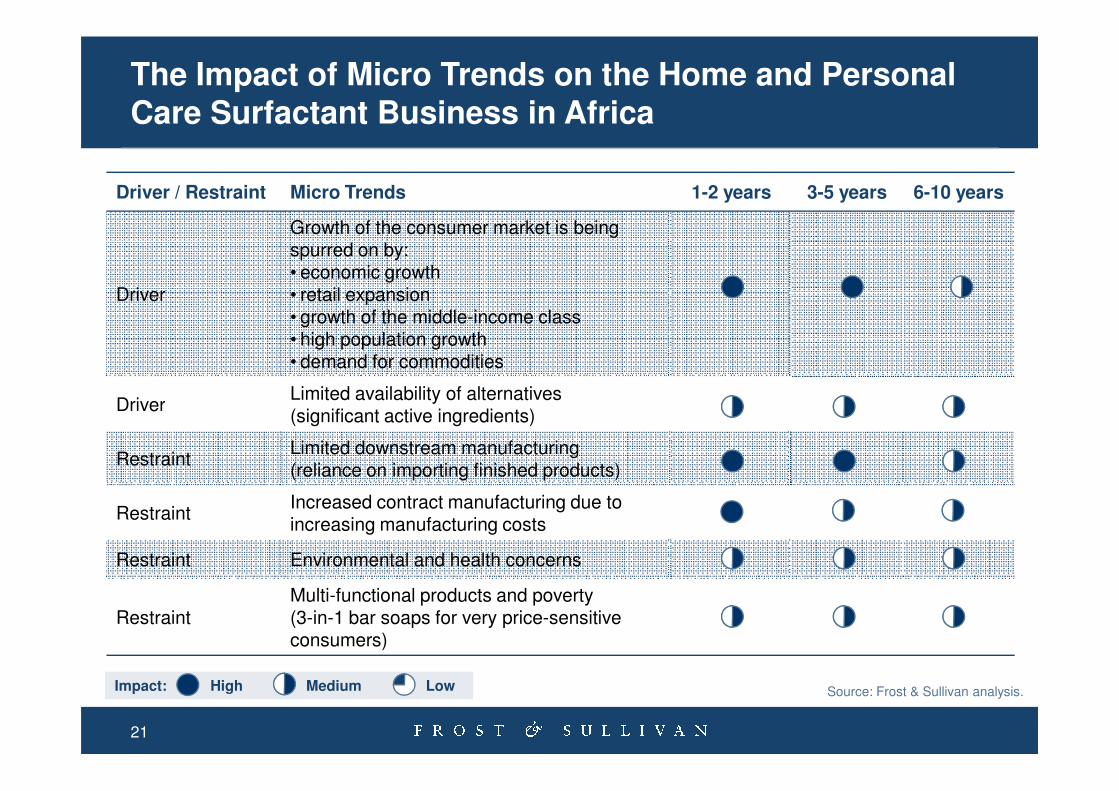

The Impact of Micro Trends on the Home and Personal Care Surfactant Business in Africa

Driver / Restraint Micro Trends 1-2 years 3-5 years 6-10 years

Driver

Growth of the consumer market is being spurred on by: • economic growth • retail expansion• growth of the middle-income class• high population growth• demand for commodities

DriverLimited availability of alternatives

21

Source: Frost & Sullivan analysis.

DriverLimited availability of alternatives (significant active ingredients)

RestraintLimited downstream manufacturing(reliance on importing finished products)

RestraintIncreased contract manufacturing due to increasing manufacturing costs

Restraint Environmental and health concerns

RestraintMulti-functional products and poverty(3-in-1 bar soaps for very price-sensitive consumers)

Impact: High Medium Low

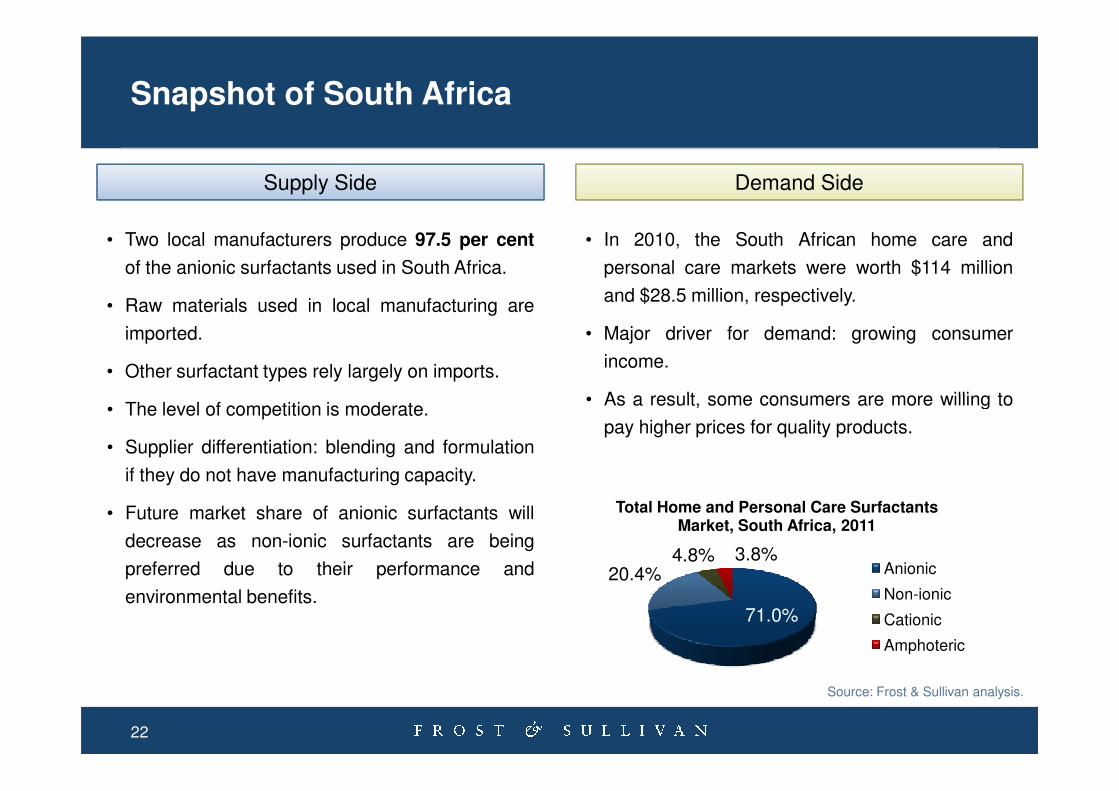

Snapshot of South Africa

Supply Side Demand Side

• Two local manufacturers produce 97.5 per cent

of the anionic surfactants used in South Africa.

• Raw materials used in local manufacturing are

imported.

• Other surfactant types rely largely on imports.

• In 2010, the South African home care and

personal care markets were worth $114 million

and $28.5 million, respectively.

• Major driver for demand: growing consumer

income.

• As a result, some consumers are more willing to

22

Source: Frost & Sullivan analysis.

71.0%

20.4%4.8% 3.8%

Total Home and Personal Care Surfactants Market, South Africa, 2011

Anionic

Non-ionic

Cationic

Amphoteric

• The level of competition is moderate.

• Supplier differentiation: blending and formulation

if they do not have manufacturing capacity.

• Future market share of anionic surfactants will

decrease as non-ionic surfactants are being

preferred due to their performance and

environmental benefits.

• As a result, some consumers are more willing to

pay higher prices for quality products.

Future Outlook for Surfactants in South Africa

0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%

30.0

60.0

90.0

120.0

150.0

180.0

Re

ven

ue

Gro

wth

Ra

te (

%)

Re

ven

ue

s ($

Mil

lio

n)

Total Home and Personal Care Surfactants Market: Revenue Forecasts,

South Africa, 2007-2015

23

2007 2008 2009 2010 2011 2012 2013 2014 2015

HPC Surfactant Revenue 135.7 141.2 142.5 144.8 148.9 153.7 158.9 164.3 170.0

Revenue Growth Rate (%) 4.1% 0.9% 1.6% 2.8% 3.2% 3.4% 3.4% 3.5%

0.0%0.5%

0.0

30.0

Re

ven

ue

Gro

wth

Ra

te (

%)

Re

ven

ue

s ($

Mil

lio

n)

• In 2011, the South African home and personal care surfactant market generated revenues of $148.9

million with 2.8 per cent growth year on year.

• The South African home and personal care surfactant market is expected to generate revenues worth

$170 million in 2015.

Source: Frost & Sullivan analysis.

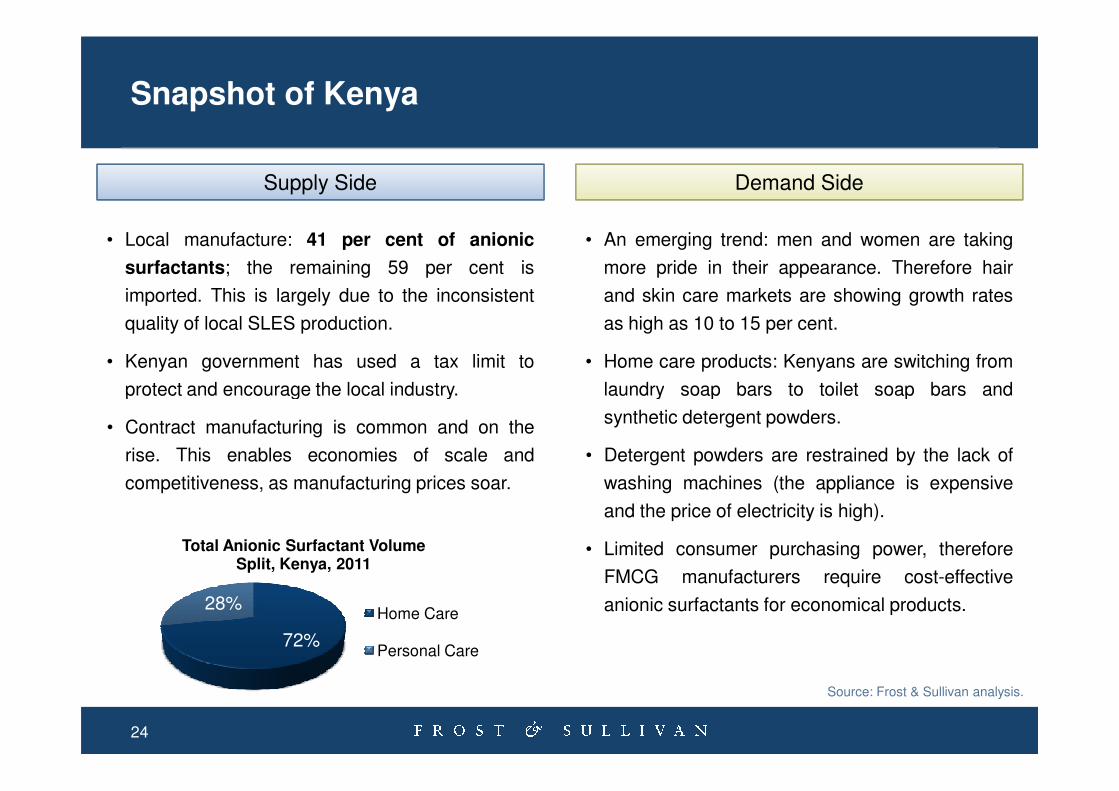

Snapshot of Kenya

Supply Side Demand Side

• Local manufacture: 41 per cent of anionic

surfactants; the remaining 59 per cent is

imported. This is largely due to the inconsistent

quality of local SLES production.

• Kenyan government has used a tax limit to

protect and encourage the local industry.

• An emerging trend: men and women are taking

more pride in their appearance. Therefore hair

and skin care markets are showing growth rates

as high as 10 to 15 per cent.

• Home care products: Kenyans are switching from

laundry soap bars to toilet soap bars and

24

protect and encourage the local industry.

• Contract manufacturing is common and on the

rise. This enables economies of scale and

competitiveness, as manufacturing prices soar.

laundry soap bars to toilet soap bars and

synthetic detergent powders.

• Detergent powders are restrained by the lack of

washing machines (the appliance is expensive

and the price of electricity is high).

• Limited consumer purchasing power, therefore

FMCG manufacturers require cost-effective

anionic surfactants for economical products.

72%

28%

Total Anionic Surfactant Volume Split, Kenya, 2011

Home Care

Personal Care

Source: Frost & Sullivan analysis.

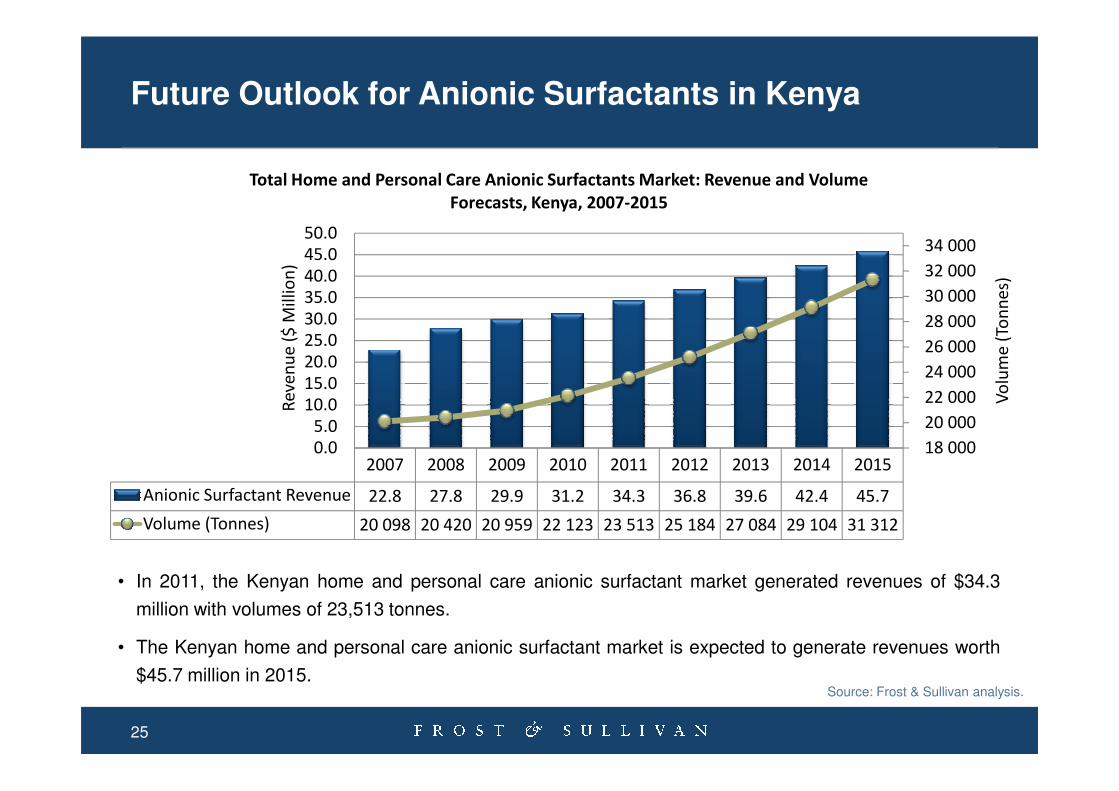

Future Outlook for Anionic Surfactants in Kenya

22 000

24 000

26 000

28 000

30 000

32 000

34 000

10.015.0

20.0

25.030.0

35.040.0

45.050.0

Vo

lum

e (

Ton

ne

s)

Re

ven

ue

($

Mil

lio

n)

Total Home and Personal Care Anionic Surfactants Market: Revenue and Volume

Forecasts, Kenya, 2007-2015

25

• In 2011, the Kenyan home and personal care anionic surfactant market generated revenues of $34.3

million with volumes of 23,513 tonnes.

• The Kenyan home and personal care anionic surfactant market is expected to generate revenues worth

$45.7 million in 2015.

2007 2008 2009 2010 2011 2012 2013 2014 2015

Anionic Surfactant Revenue 22.8 27.8 29.9 31.2 34.3 36.8 39.6 42.4 45.7

Volume (Tonnes) 20 098 20 420 20 959 22 123 23 513 25 184 27 084 29 104 31 312

18 000

20 000

22 000

0.05.0

10.0 Vo

lum

e (

Ton

ne

s)

Re

ven

ue

($

Mil

lio

n)

Source: Frost & Sullivan analysis.

Snapshot of Nigeria

• Revenues in the Nigerian personal and home

care sector were valued at $1.09 billion in 2010.

• Relatively high economic growth along with the

steady growth of the middle class have been key

drivers for this market.

• Of the over 150 million people living in Nigeria, a

Supply Side Demand Side

• Tariffs on imported manufactured goods have

supported the growth of local manufacturing of

home and personal care products.

• However, cost of production is high due to high

energy costs and importing raw materials for

manufacturing.

26

• Of the over 150 million people living in Nigeria, a

large proportion use only bar soaps, mostly multi-

purpose, for home and personal care.

manufacturing.

• A mark-up of at least 40.0% is implemented to

avoid revenue loss due to high production costs.

• More than 63% of the home and personal care

market is catered for by multi-nationals who use

complex formulations as a means of

differentiation.

• Local manufacturers produce products with very

limited properties by using basic formulations.

Source: Frost & Sullivan analysis.

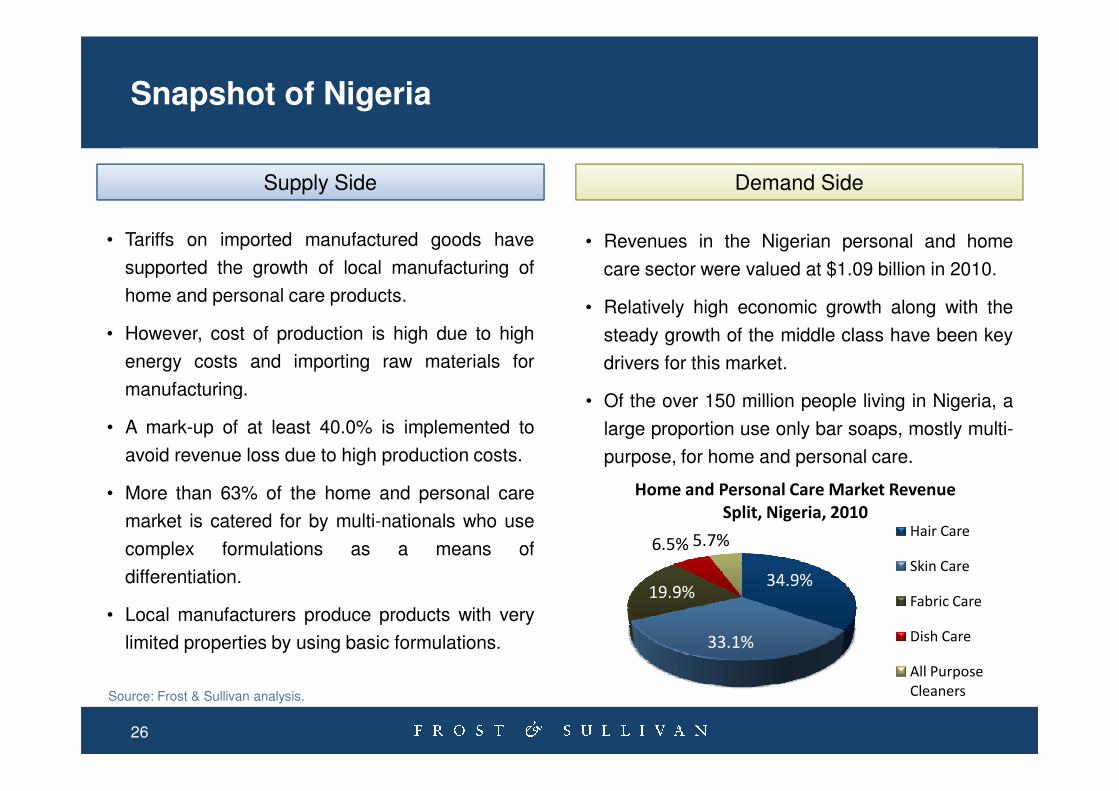

34.9%

33.1%

19.9%

6.5% 5.7%

Home and Personal Care Market Revenue

Split, Nigeria, 2010Hair Care

Skin Care

Fabric Care

Dish Care

All Purpose

Cleaners

Future Outlook for Surfactants in Nigeria

2.0%

4.0%

6.0%

8.0%

10.0%

20.0

30.0

40.0

50.0

60.0

Re

ven

ue

Gro

wth

(%

)

Re

ven

ue

($

Mil

lio

n)

Total Home and Personal Care Surfactants Market: Revenue Forecasts,

Nigeria, 2007-2015

27

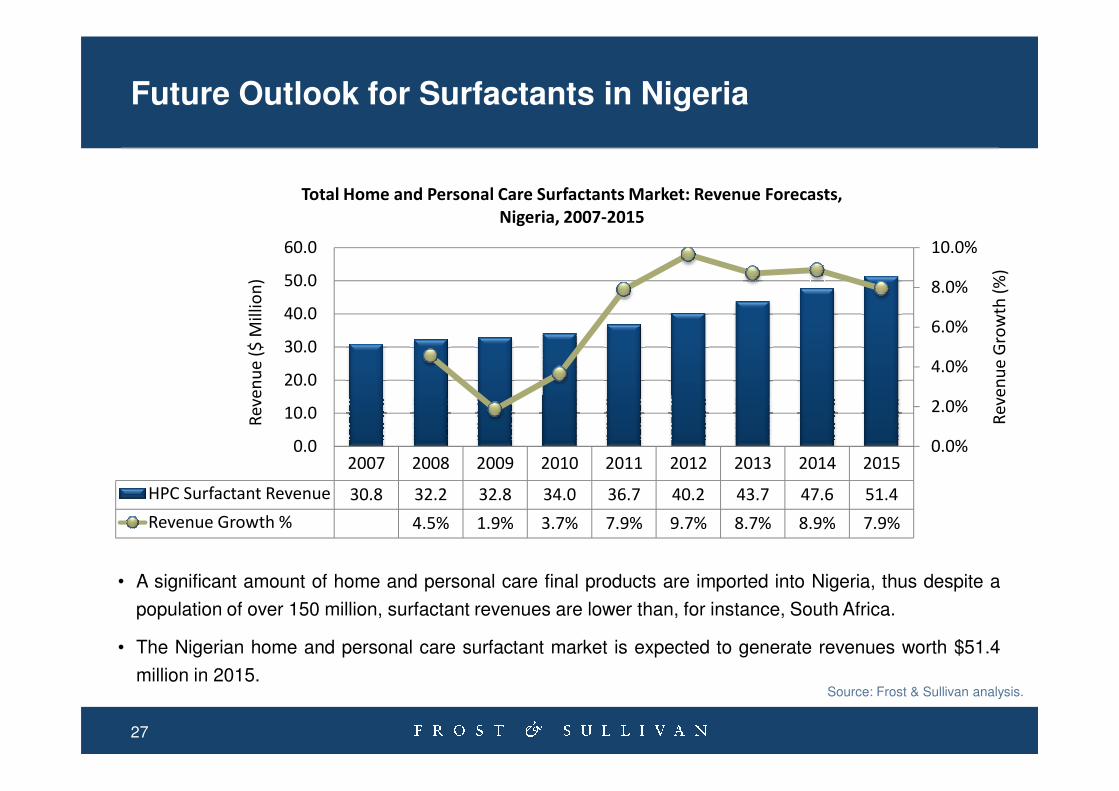

• A significant amount of home and personal care final products are imported into Nigeria, thus despite a

population of over 150 million, surfactant revenues are lower than, for instance, South Africa.

• The Nigerian home and personal care surfactant market is expected to generate revenues worth $51.4

million in 2015.

2007 2008 2009 2010 2011 2012 2013 2014 2015

HPC Surfactant Revenue 30.8 32.2 32.8 34.0 36.7 40.2 43.7 47.6 51.4

Revenue Growth % 4.5% 1.9% 3.7% 7.9% 9.7% 8.7% 8.9% 7.9%

0.0%

2.0%

0.0

10.0 Re

ven

ue

Gro

wth

(%

)

Re

ven

ue

($

Mil

lio

n)

Source: Frost & Sullivan analysis.

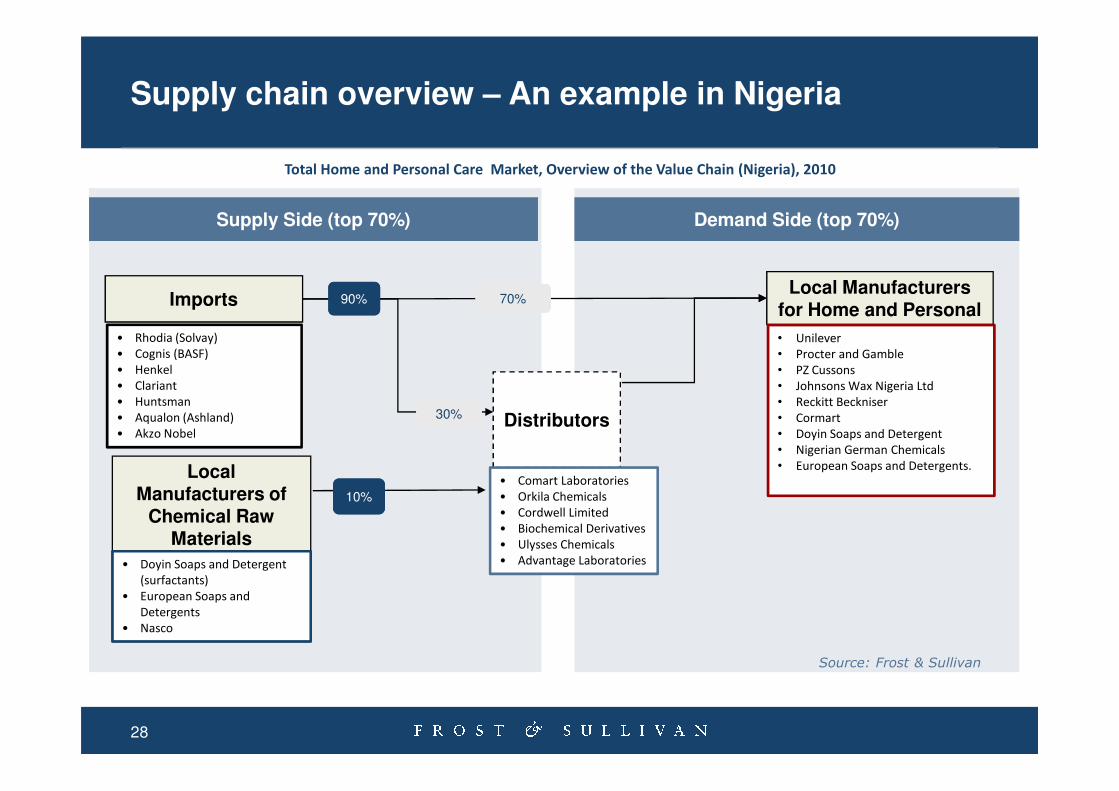

Supply chain overview – An example in Nigeria

Local Manufacturers for Home and Personal

Demand Side (top 70%)

90%

• Unilever

• Procter and Gamble

• PZ Cussons

• Johnsons Wax Nigeria Ltd

• Reckitt Beckniser

Imports

• Rhodia (Solvay)

• Cognis (BASF)

• Henkel

• Clariant

• Huntsman

Supply Side (top 70%)

70%

Total Home and Personal Care Market, Overview of the Value Chain (Nigeria), 2010

28

.Distributors

Local Manufacturers of

Chemical Raw Materials

30%• Reckitt Beckniser

• Cormart

• Doyin Soaps and Detergent

• Nigerian German Chemicals

• European Soaps and Detergents.

• Huntsman

• Aqualon (Ashland)

• Akzo Nobel

10%

• Doyin Soaps and Detergent

(surfactants)

• European Soaps and

Detergents

• Nasco

• Comart Laboratories

• Orkila Chemicals

• Cordwell Limited

• Biochemical Derivatives

• Ulysses Chemicals

• Advantage Laboratories

Source: Frost & Sullivan

5. Conclusions - Is Africa the Next Frontier?

29

`̀

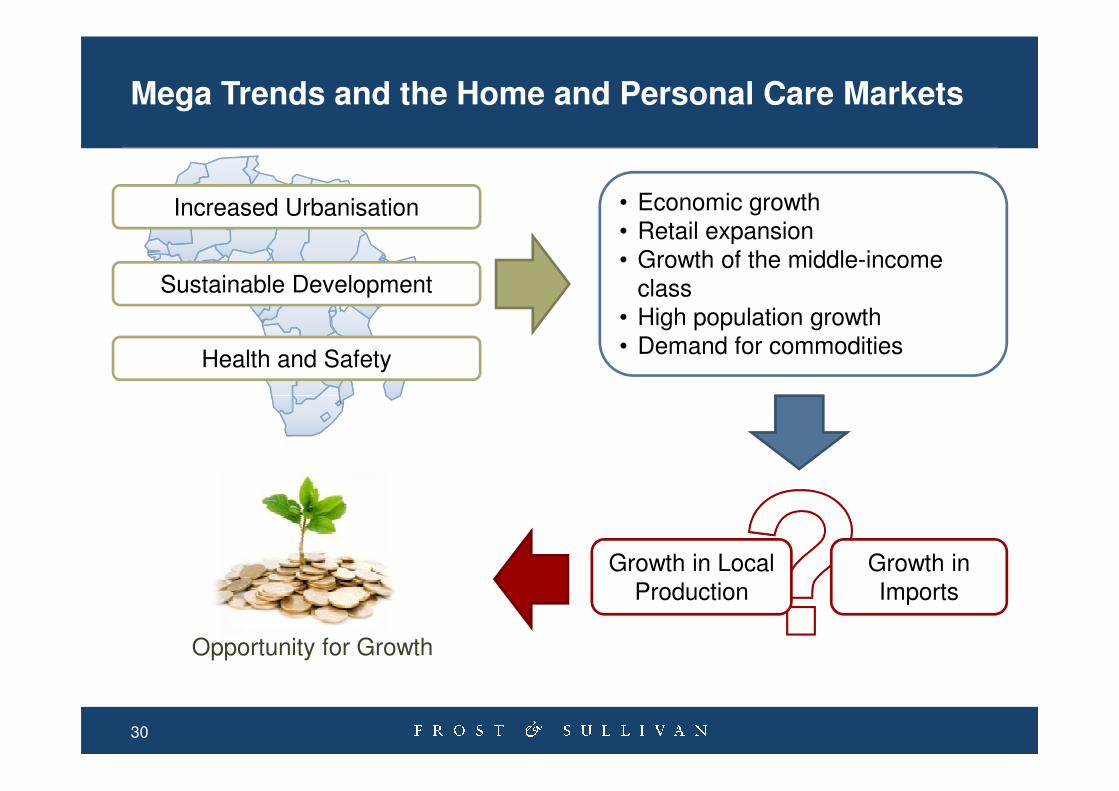

Mega Trends and the Home and Personal Care Markets

Increased Urbanisation

Sustainable Development

Health and Safety

• Economic growth • Retail expansion• Growth of the middle-income

class• High population growth• Demand for commodities

Growth in Local Production

Growth in Imports

Opportunity for Growth

30

The Value of Emerging Markets – Are you ready ?

`̀

Emerging markets offer significant growth opportunity, as mature markets stagnate.

Africa could be the most promising.

Why Africa?

• Total population: 1.28 billion by 2020

.

• Total population: 1.28 billion by 2020

• Spending from the top 18 cities:

$1.3 trillion by 2020

• African middle class: 360 million by 2020

• Africans living in urban areas:

43% by 2020

• Sub-Saharan Africa is one of the fastest-

growing regions globally.

Sources: UN Department of Economic and Social Affairs; Frost & Sullivan analysis.

Key Concepts:

• Find the unmet, distinctive needs

• Target the correct consumer segment

• Understand your consumers, their

preferences, and how to conduct

business with them

• First-mover advantage

http://www.frost.com

Mani JamesRegional Director – Frost & Sullivan AfricaTel: +27 21 680 3208Email: [email protected]

Contact For Additional Information

http://www.frost.comVishnu ShankarIndustry Manager – Frost & Sullivan Middle East & North Africa Tel: +971.4.4331882Email: [email protected]