adviser easy reference guide for individual...

TRANSCRIPT

Adviser Easy Reference Guide for Individual InsuranceIssue date July 2008

i

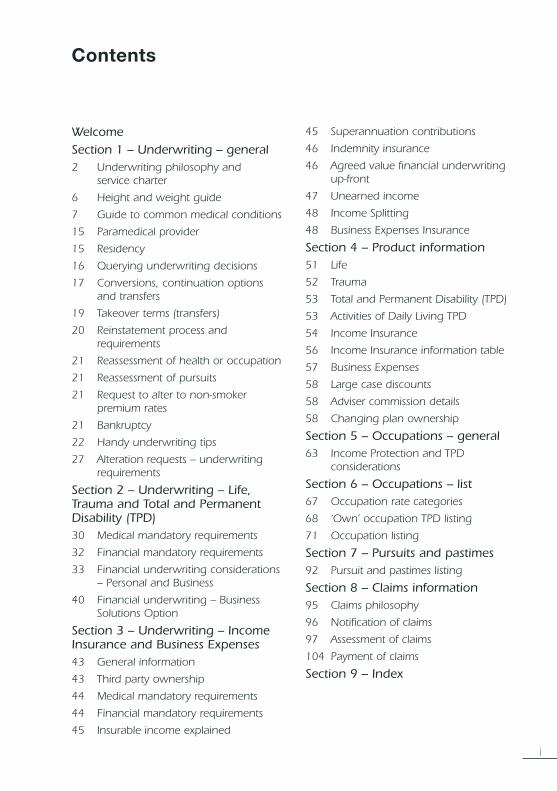

Welcome Section 1 – Underwriting – general2 Underwriting philosophy and

service charter

6 Height and weight guide

7 Guide to common medical conditions

15 Paramedical provider

15 Residency

16 Querying underwriting decisions

17 Conversions, continuation options and transfers

19 Takeover terms (transfers)

20 Reinstatement process and requirements

21 Reassessment of health or occupation

21 Reassessment of pursuits

21 Request to alter to non-smoker premium rates

21 Bankruptcy

22 Handy underwriting tips

27 Alteration requests – underwriting requirements

Section 2 – Underwriting – Life, Trauma and Total and Permanent Disability (TPD)30 Medical mandatory requirements

32 Financial mandatory requirements

33 Financial underwriting considerations – Personal and Business

40 Financial underwriting – Business Solutions Option

Section 3 – Underwriting – Income Insurance and Business Expenses43 General information

43 Third party ownership

44 Medical mandatory requirements

44 Financial mandatory requirements

45 Insurable income explained

45 Superannuation contributions

46 Indemnity insurance

46 Agreed value financial underwriting up-front

47 Unearned income

48 Income Splitting

48 Business Expenses Insurance

Section 4 – Product information51 Life

52 Trauma

53 Total and Permanent Disability (TPD)

53 Activities of Daily Living TPD

54 Income Insurance

56 Income Insurance information table

57 Business Expenses

58 Large case discounts

58 Adviser commission details

58 Changing plan ownership

Section 5 – Occupations – general63 Income Protection and TPD

considerations

Section 6 – Occupations – list67 Occupation rate categories

68 ‘Own’ occupation TPD listing

71 Occupation listing

Section 7 – Pursuits and pastimes92 Pursuit and pastimes listing

Section 8 – Claims information95 Claims philosophy

96 Notification of claims

97 Assessment of claims

104 Payment of claims

Section 9 – Index

Contents

ii

This page has been left blank intentionally

1

Welcome to your Adviser Easy Reference GuideThis reference guide provides you with information about how we manage our individual insurance business.

We understand that to best manage your client’s expectations, you need transparency in the guidelines we use. In this guide, you will find some useful tools to help you write individual business with us.

For information regarding our Group Life products, please refer to the Group Life Underwriting Guide. For Platform insurance and Super Directions products, please refer to the relevant administration areas.

We encourage you to call us about any underwriting or claims enquiries you may have. You can contact us at:

AXA Australia PO Box 14330 Melbourne VIC 8001 Telephone 1800 655 655 www.axaadvantage.com.au

Underwriting – generalAdviser Easy Reference Guide to Insurance

Important information

This publication has been prepared for distribution to professional financial advisers only and is intended to provide factual information. AXA Australia does not authorise the distribution of this publication to or use by existing or potential investors. Existing or potential investors should base their investment decision on the detailed information contained in the current Product Disclosure Statement (PDS) and should consult their financial adviser. Applications for the issue of AXA Australia products will only be accepted on receipt of an application form accompanying a current PDS. The National Mutual Life Association of Australasia Limited and its associates derive income from issuing interests in the products, full details of which are contained in the PDSs This information is provided for persons in Australia only and is not being provided for the use of any person who is in any other country.

2

Underwriting philosophyWe have a duty to you and your clients to thoroughly evaluate each Application we receive and to offer underwriting terms, based on a thoughtful and reasonable assessment of the evidence presented and having regard to the individual circumstances of the case.

We will keep you fully informed about the progress of your Applications and will provide you with a logical reason for any decisions we make. It will not always be possible to offer terms that are agreeable to every applicant who submits a proposal, but we will seek to offer alternatives whenever it is practicable and sensible to do so.

We are committed to providing an efficient and competitive underwriting service and will work with you to provide a solution to the insurance needs of your clients.

Underwriting Service CharterThis Underwriting Service Charter affirms our commitment to providing you and your clients with a professional, timely and transparent underwriting service.

Our team

We have a team of Underwriters committed to you and your clients.

Underwriters Our Underwriters are located across Australia and New Zealand. We share a sophisticated work allocation system designed to treat all applications in the most efficient way possible. In the vast majority of cases, your applications will be assessed in a region near you. We can also call on resources in other regions in times of high demand.

Senior Underwriters

Our most experienced Underwriters handle your large and complex cases. Their knowledge means that the right questions are asked at the right time, ensuring that high value cases are addressed professionally and efficiently.

Field Underwriters Our Underwriters are supported by Field Underwriters, who are able to partner with you to assist with complex or large cases. These cases may require highly technical underwriting involvement, and our Field Underwriters are on hand to help.

Chief Medical Officer and Senior Medical Officers

All our underwriting sites benefit from the experience of our resident Chief Medical Officer in the assessment of complex medical histories. Each underwriting site also has access to visiting Senior Medical Officers, who are specially trained in insurance medicine.

Underwriting – generalAdviser Easy Reference Guide to Insurance

3

Our commitment to you

Communication We will keep you fully informed of the progress of your risk applications. This includes:

*Advise and explain any adverse decisions.

* Advise and explain any further underwriting requirements, if the reasons for the request are not clear.

* Advise any alternative offers if we are unable to offer the proposed cover.

* We offer these services by telephone where possible to minimise delays.

Progress and enquiries

Our online enquiry system, AXA Online, allows you to view the status of your applications, and lodge underwriting and claims enquiries, which are automatically directed to our work management system.

Our commitment to your client

The decision We will thoroughly review each application and provide the best decision possible, consistent with our risk management philosophy. Before declining any proposal we will explore alternative solutions through our Alternative Offer Forum. We will also seek the guidance of our Medical Consultants and Reinsurers where appropriate.

Alternative Offer Forum

The Alternative Offer Forum is a daily discussion group lead by our more Senior Underwriters. In the Forum, the Senior Underwriters discuss Individual Insurance cases that may be declined or offered with non standard terms with a view to considering alternative solutions.

Where appropriate, an adverse decision will be referred to our Alternative Offer Forum to discuss alternative terms that may be available. These alternatives could include offering loadings, exclusions, adjustments of the plan term (referred to as limited term plans), adjustment of benefit or waiting periods or even other types of cover.

Medical Information

We will advise your client’s doctor directly (where authorised) of the reasons behind our decisions. This avoids undue delays and worry for the client while waiting for explanation of decisions or test results. Should an issue relating to your client’s health come to light during the medical assessment of their application, we will ensure that the information is relayed to their doctor urgently (where authorised).

4

Contact us

Contact Centre Our Contact Centre is staffed with fully qualified consultants ready to assist you with your query. Please ensure that you have your adviser number ready.

1800 655 655

AXA Online Go to AXA Online for a view on the status of your applications and to submit underwriting and claims enquiries on specific proposal and policy numbers.

www.axaonline.com.au

Underwriting For Underwriting queries, please contact the Underwriter assigned to your client. This information can be located through AXA Online. For pre-lodgement enquiries, please telephone our Contact Centre. To submit underwriting evidence please fax documentation where possible to expedite the process.

www.axaonline.com.au

1800 674 684 (fax)

Underwriting Forms

For underwriting related forms, please refer to website for downloads.

www.axaadvantage.com.au

Field Underwriting Should you need assistance with large and complex cases, a Field Underwriter can assist you.

Contact your Business Development Manager

Underwriting – generalAdviser Easy Reference Guide to Insurance

Our commitment to your client (continued)

Financial Information

We will contact your client’s accountant directly (where authorised) to expedite the financial underwriting process.

Telephone Underwriting

We will contact your client directly (if an authority is provided), to obtain the answers to missing questions, and to seek clarification of information provided, in order to expedite the processing of the application.

5

Our

Un

der

wri

tin

g p

roce

ss

Step

Task

Met

hod o

f D

eliv

ery

of

Serv

ice

Con

tact

Poin

tC

on

tact

D

etai

ls

1A

pplic

atio

n L

odg

ed –

Com

plet

ed a

pplic

atio

n de

liver

ed to

AXA

Mai

lA

dvi

ser

&

Cu

sto

mer

Ser

vice

Mai

ling

ad

dre

ss:

PO

Bo

x 14

330

Mel

bou

rne

VIC

80

01Fa

csim

ile:

1800

674

684

Tele

ph

on

e:

1800

655

655

2A

pplic

atio

n R

egiste

red –

Pla

n N

umbe

r al

loca

ted,

app

licat

ion

imag

ed a

nd

reg

ister

ed o

nto

the

Wor

k M

anag

emen

t Sys

tem

N/A

Vie

w p

rog

ress

on

A

XA O

nlin

eC

on

tact

Cen

tre

3In

itial

Ass

essm

ent

– If

ther

e ar

e no

furt

her

requ

irem

ents

go

to s

tep

5.

Requ

est m

issin

g r

equi

rem

ents

, if u

nabl

e to

obt

ain

thro

ugh

tele

phon

e un

derw

ritin

g. C

all a

nd e

xpla

in a

ny fu

rthe

r re

quire

men

ts if

the

reas

ons

for

the

requ

est a

ren’

t cle

ar.

Med

ical

rep

orts

, par

amed

ical

s an

d pa

thol

ogy

requ

este

d an

d ar

rang

ed th

roug

h

Uni

fied

Hea

lthca

re G

roup

(UH

G).

Requ

est i

nfor

mat

ion

from

clie

nt’s

acco

unta

nt

(whe

re a

utho

rised

).

A fa

x is

sent

to th

e Ad

vise

r ou

tlini

ng th

e re

quire

men

ts th

at

cann

ot b

e ob

tain

ed

thro

ugh

Tele

phon

e U

nder

writ

ing

4Re

quire

men

ts R

ecei

ved

– C

omp

lete

d r

equ

irem

ent(s

) ob

tain

ed a

nd

del

iver

ed

to A

XAM

ail,

Fax

or T

elep

hone

Ad

vise

r &

C

ust

om

er S

ervi

ce

5Fi

nal

Ass

essm

ent

Mad

e –

If st

anda

rd a

ccep

tanc

e g

o to

ste

p 10

Oth

erw

ise a

ll av

enue

s to

ach

ieve

the

best

pos

sible

dec

ision

are

pur

sued

, inc

ludi

ng:

Pres

enta

tion

to th

e Al

tern

ativ

e O

ffer

Foru

mC

onsu

ltatio

n w

ith th

e C

hief

Med

ical

Offi

cer

Refe

rral

to th

e Re

insu

rers

if r

equi

red

N/A

Vie

w p

rog

ress

on

A

XA O

nlin

e C

on

tact

Cen

tre

6D

ecisio

n e

xpla

ined

– A

dvise

r co

ntac

ted

to d

iscus

s fin

al d

ecisi

on, i

f dec

ision

is

adve

rse

Tele

phon

e /

Fax

(if

cont

act b

y ph

one

not

poss

ible

)

Vie

w p

rog

ress

on

A

XA O

nlin

e C

on

tact

Cen

tre

7Le

tter

sent

to c

lient

’s D

octo

r ex

plai

ning

rea

son(

s) fo

r de

cisio

n (if

aut

horis

ed/

requ

este

d) a

nd w

e ar

e un

able

to d

isclo

se to

clie

nt d

irect

lyM

ail

8Re

vise

d T

erm

s O

ffer

– Re

vise

d Te

rms

offe

r se

nt to

Adv

iser

Fax

9Re

vise

d T

erm

s A

gre

ed –

Rev

ised

Term

s of

fer

signe

d an

d re

turn

ed to

AXA

Mai

l / F

axA

dvi

ser

&

Cu

sto

mer

Ser

vice

10Pl

an C

omple

ted

– P

lan

is co

mpl

eted

on

syst

em, c

onfir

mat

ion

is iss

ued

to A

dvise

r, co

mm

issio

n pa

id a

nd p

lan

docu

men

t sen

t to

clie

ntM

ail /

Fax

Vie

w p

rog

ress

on

A

XA O

nlin

eC

on

tact

Cen

tre

Not

e: A

sm

all n

um

ber

of r

equ

irem

ents

(eg

ban

k d

ebit

auth

ority

form

) m

ay s

till b

e re

ques

ted

bef

ore

com

plet

ion

, if

not

su

bmitt

ed w

ith t

he

appl

icat

ion

.

6

Height and Weight Guide

Overweight

Research has shown that being overweight is associated with being at an increased risk of a number of diseases such as heart attack, stroke, diabetes and hypertension.

The Body Mass Index (BMI) has become widely accepted as a way to measure body weight in comparison to height. The BMI is easy to calculate and can be applied regardless of gender. A BMI within the range of 20 to 25 is considered healthy while greater than 25 is considered overweight. A BMI greater than 30 is considered obese and a premium loading may apply depending on the benefit type, the terms and conditions applied for and the presence of any other risk factors. Other risk factors may include high blood pressure, raised cholesterol or family history of heart disease. BMI is calculated by dividing the body weight in kilograms by the square of the height in metres (kg/m2).

For example:

Weight 90kg and Height 180cm BMI = Weight / Height x Height BMI = 90 / (1.8x1.8) = 28 BMI

We are now using the BMI as a simple way to indicate to you when a mandatory medical examination or mini check examination may be required. Our general approach is described below:

All Products – All Ages

BMI range Requirements

BMI up to 32 Personal statement

BMI between 33 and 39* Personal statement and Mini Check Examination**

BMI 40+ Personal statement, full Medical Examination/Paramedical and MBA20

* An MBA20 will be requested where the BMI is 35 or above

** Mini Check Examination: an abridged version of the medical examination that can be performed by a registered nurse

Please note that the Underwriter may call for a medical examination at a lesser BMI at their discretion, taking into account all risk factors that may be present. In some instances the Underwriter may be able to offer your client a choice of assessments. For example, a longer waiting period for Income Insurance may mean that a premium loading may not be necessary or can be reduced.

Underwriting – generalAdviser Easy Reference Guide to Insurance

7

Underweight

Being underweight may be associated with, or a sign of a number of diseases including cancer, bowel disease or an eating disorder.

A BMI of less than 20 is considered underweight. A medical examination may be required when the BMI is 18 or less. Please contact an Underwriter to discuss.

Guide to common medical conditions

Legend

Medical evidence

PS Personal Statement ECG Electrocardiogram PMAR Private Medical Attendant’s Report ME Medical Examination Mini Check An abridged version of the Medical Examination that can be performed Examination by a registered nurse Q’re Questionnaire or full details on personal statement if no specific questionnaire available Q’re/PMAR Questionnaire first then possibly a PMAR MBA20 Multiple Biochemical Analysis blood test Lipid Profile Cholesterol and triglyceride blood test

Assessments

Std Standard rates will usually apply (that is, standard mortality or morbidity) +50* 50% extra mortality/morbidity +75* 75% extra mortality/morbidity +100* 100% extra mortality/morbidity +150* 150% extra mortality/morbidity# +200* 200% extra mortality# +250* 250% extra mortality# +300* 300% extra mortality# +350* 350% extra mortality# +400* 400% extra mortality# +450* 450% extra mortality# +500* 500% extra mortality# E Cover may be offered with an exclusion clause PP Cover not available at this time D Cover will be declined IC Individual Consideration

* An extra premium loading will apply

# Inbuilt Convertibility and CPI are not available

8

This section following provides you with a guide to more common medical conditions. It is intended as a guide only and individual circumstances will vary.

Please note the assessments indicated are a guideline only. Underwriters also take into account what are known as ‘credit’ and ‘debit’ factors in the person’s risk profile. Alternative assessments may be offered (for example limited terms, exclusions, loadings, longer waiting periods and shorter benefit periods) or cover may be declined depending on the presence of these other factors. Limited plan terms may be offered as alternatives on Life, TPD or Trauma insurance. At this time limited plan terms are not available for Income Protection.

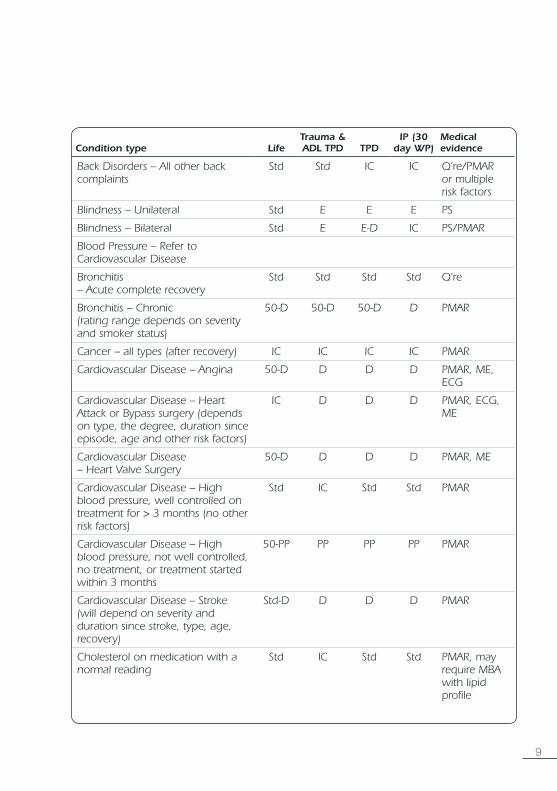

Condition type LifeTrauma & ADL TPD TPD

IP (30 day WP)

Medical evidence

Alcohol dependence normal liver tests, no neurological or mental disorder. Total abstinence for 0 – 3 years

200-PP

PP PP D PMAR and MBA

Alcohol dependence normal liver tests, no neurological or mental disorder. Total abstinence for 4 – 6 years

50-100

50-100 IC D PMAR and MBA

Anxiety (well treated or fully recovered)

Std-D Std-D IC IC Q’re/PMAR

Arthritis – osteoarthritis Std Std E-D E-D PMAR

Arthritis – psoriatic 50-100

50-D E-D E-D PMAR

Arthritis – rheumatoid 50-100

50-D E-D E-D PMAR

Asthma mild Std Std Std Std-50 Q’re

Asthma moderate 50 50 50-100

50-100 PMAR

Asthma severe 100-D 50-D D D PMAR

Back Disorders – Disc Prolapse Std Std E E Q’re/PMAR

Back Disorders – Laminectomy Std Std E E Q’re/PMAR

Back Disorders – Scheuermann’s Std Std E E Q’re/PMAR

Back Disorders – Severe Scoliosis Std Std E E Q’re/PMAR

Back Disorders – Spinal Fusion Std Std E E Q’re/PMAR

Back Disorders – Spinal Stenosis Std Std E E Q’re/PMAR

Back Disorders – Spondylolisthesis Std Std E E Q’re/PMAR

Back Disorders – Spondylosis Std Std E E Q’re/PMAR

Underwriting – generalAdviser Easy Reference Guide to Insurance

9

Condition type LifeTrauma & ADL TPD TPD

IP (30 day WP)

Medical evidence

Back Disorders – All other back complaints

Std Std IC IC Q’re/PMAR or multiple risk factors

Blindness – Unilateral Std E E E PS

Blindness – Bilateral Std E E-D IC PS/PMAR

Blood Pressure – Refer to Cardiovascular Disease

Bronchitis – Acute complete recovery

Std Std Std Std Q’re

Bronchitis – Chronic (rating range depends on severity and smoker status)

50-D 50-D 50-D D PMAR

Cancer – all types (after recovery) IC IC IC IC PMAR

Cardiovascular Disease – Angina 50-D D D D PMAR, ME, ECG

Cardiovascular Disease – Heart Attack or Bypass surgery (depends on type, the degree, duration since episode, age and other risk factors)

IC D D D PMAR, ECG, ME

Cardiovascular Disease – Heart Valve Surgery

50-D D D D PMAR, ME

Cardiovascular Disease – High blood pressure, well controlled on treatment for > 3 months (no other risk factors)

Std IC Std Std PMAR

Cardiovascular Disease – High blood pressure, not well controlled, no treatment, or treatment started within 3 months

50-PP PP PP PP PMAR

Cardiovascular Disease – Stroke (will depend on severity and duration since stroke, type, age, recovery)

Std-D D D D PMAR

Cholesterol on medication with a normal reading

Std IC Std Std PMAR, may require MBA with lipid profile

10

Condition type LifeTrauma & ADL TPD TPD

IP (30 day WP)

Medical evidence

Cholesterol – Abnormal reading IC IC IC IC PMAR, may require MBA with lipid profile

Coeliac Disease – Well controlled with diet or medication, no symptoms or complications

Std-100

Std-100 Std-100

50-D PMAR

Coeliac Disease – With symptoms, not well controlled

100 D D D PMAR or ME

Crohn’s Disease (Rating will depend on complications, number of episodes, treatment and time elapsed since last episode)

50-250

50-D E-D E-D PMAR or ME

Deafness – Progressive (cause known)

IC IC IC IC PMAR

Deafness – Unilateral (cause known) Std E Std-E E PMAR

Deafness – Bilateral (cause known) Std-50 E E E PMAR

Depression (well treated or fully recovered)

Std-D Std-D IC IC Q’re/PMAR

Dermatitis/Eczema (See Skin Disorders)

Diabetes Type I (Insulin Dependent) 50-D E-D 75-D D PMAR or ME, and results of most recent blood tests

Diabetes Type II (Non-Insulin Dependent)

50-D E-D 75-D D PMAR or ME, and results of most recent blood tests

Drug Abuse – current D D D D Nil

Drug Abuse – within 3 years last use PP D D D Nil

Drug Abuse – Total abstinence 3 – 5 years

IC D D D Q’re, PMAR

Drug Abuse – Total abstinence > 5 years

IC IC IC IC Q’re, PMAR

Emphysema – Mild 50-100

100-D 100-D D PMAR or ME

Emphysema – Moderate to Severe 100-D D D D PMAR or ME

Underwriting – generalAdviser Easy Reference Guide to Insurance

11

Condition type LifeTrauma & ADL TPD TPD

IP (30 day WP)

Medical evidence

Endometriosis – full recovery Std Std-E Std-E Std-E Nil

Endometriosis – Under treatment Std-50 Std-50 50-E 50-E PMAR

Epilepsy – within 1 year of diagnosis PP PP PP PP Nil

Epilepsy – > 1 year since diagnosis, depending on number of attacks

Std-PP Std-D 50-D 50-D/E Q’re, PMAR

Gall Stones – removed, full recovery Std Std Std Std PS, may require PMAR if recent

Gall Stones – present 50-100

Std-50 E E PMAR

Gout – depending on uric acid levels and presence of arthritis

Std-150

Std-100 Std-E Std-E Q’re, PMAR

Haemochromatosis – under medical supervision

Std-D IC IC IC PMAR

Haemorrhoids Std Std Std-E Std-E PS/PMAR

Hay Fever Std Std Std Std Q’re/PMAR

Hepatitis A – full recovery, > 6 months

Std Std Std Std Q’re/PMAR

Hepatitis B – full recovery, > 6 months

Std Std-PP Std-50 Std-PP PMAR, MBA, Hepatitis serology

Hepatitis B – carrier 50-D 75-D 50-D 50-D PMAR, MBA, Hepatitis serology

Hepatitis C 50-D 50-D IC IC PMAR, MBA, Hepatitis serology

Hernia – 3 months post operation or no operation planned

Std-50 Std-50 Std-E Std-E Q’re

Hysterectomy – for benign disease, full recovery

Std Std Std Std Q’re/PMAR

Indigestion Std-50 Std-50 Std-50 Std-100

Q’re/PMAR

Iritis – no underlying disease, full recovery, no residual visual impairment

Std Std Std Std PS, PMAR

Iritis – present, no underlying disease Std E E-PP E-PP PS, PMAR

12

Condition type LifeTrauma & ADL TPD TPD

IP (30 day WP)

Medical evidence

Irritable Bowel Syndrome – Mild, fully investigated (this rating excludes any additional rating for any underlying cause)

Std Std Std 0-50 PS/PMAR

Irritable Bowel Syndrome Moderate, fully investigated (this rating excludes any additional rating for any underlying cause)

Std Std Std 50-100 PMAR

Irritable Bowel Syndrome, not investigated

IC IC IC IC PMAR

Kidney Stones – History of, no kidney damage, blood pressure and urine normal

Std-50 Std-50 Std-50 Std-E PMAR or ME

Kidney Stones – Present, recurrent or with symptoms/kidney damage

IC IC-D PP PP PMAR or ME

Knee disorders – Cartilage, ligament, recurrent pain, unstable joint, reconstruction, or other surgery. No manual work

Std Std IC IC Q’re

Knee disorders – Cartilage, ligament, recurrent pain, unstable joint, reconstruction, or other surgery. Manual work

Std Std E E Q’re

Lupus – Discoid Lupus (SLE excluded)

Std-50 Std-50 PP-E PP-E PMAR

Lupus – Systemic Lupus Erythematous (SLE)

PP-100

IC IC IC PMAR

Leukaemia – Acute or chronic (Fully recovered)

IC IC IC IC PMAR

Malignant Melanoma – All types, adequate follow up. Rating will depend on staging of tumour

IC IC IC IC Q’re/PMAR or pathology results

Meniere’s Disease – Tumour and cardiovascular disorder ruled out

Std Std E-D E-D PMAR

Multiple Sclerosis, Mild to Severe 50-D D D D PMAR

Paralysis as a result of trauma IC IC D D PMAR

Parkinson’s Disease, Mild to Severe (ages >40 only)

50-D D D D PMAR

Underwriting – generalAdviser Easy Reference Guide to Insurance

13

Condition type LifeTrauma & ADL TPD TPD

IP (30 day WP)

Medical evidence

Pleurisy (Dry Pleurisy) – fully recovered

Std Std Std Std PS/PMAR

Pleurisy (Exudative Pleurisy) – fully recovered

Std-50 Std-50 50-PP IC PMAR

Pneumonia – History of, full recovery Std Std Std Std PS/PMAR

Prostatitis – Acute, Mild to Moderate Std Std-50 Std-50 Std-E PMAR

Prostatitis – Chronic 50 50-100 E E PMAR

Psoriasis – No arthritis, Mild Std Std Std Std Q’re

Psoriasis – No arthritis, Moderate to Severe

Std Std E E Q’re/PMAR

Psoriasis – Psoriatic Arthritis 50-100 50-D E-D E-D Q’re, PMAR

Pterygium – Present Std E E E PS

Pterygium – History of Std Std Std Std PS

Ross River Virus – Present PP PP PP PP PS

Ross River Virus – History of, full recovery, no complications, > 6 months since last symptoms

Std Std IC IC PMAR

Sleep Apnoea – Sleep Study performed

Std-D Std-D 50-D 50-D PMAR

Skin Disorders Eczema/Dermatitis, See also Psoriasis

Std Std Std-E Std-E Q’re

Tendinitis Present Std Std E E Q’re

Tendinitis – History of, no time off work, 12 months symptom free, no manual work

Std Std Std Std-E Q’re

Thyroid Disorder – Hyperthyroid (Graves Disease) – Present, Mild

Std-50 50 PP PP PMAR

Thyroid Disorder – Hyperthyroid (Graves Disease) – Moderate – Severe

100-D D D D PMAR

Thyroid Disorder – Hyperthyroid (Graves Disease) – History of, well controlled on treatment for > 6 months

Std-50 Std-50 Std-50 Std-50 PMAR

Thyroid Disorder – Hyperthyroid (Graves Disease) – History of, surgical treatment > 12 months ago

Std Std Std Std PMAR

14

Condition type LifeTrauma & ADL TPD TPD

IP (30 day WP)

Medical evidence

Thyroid disorder – Hyperthyroid – Congenital

50-100

50-100 IC IC PMAR

Thyroid disorder – Hyperthyroid – Acquired, with successful treatment

Std Std Std Std PMAR

Thyroid disorder – Hypothyroid – Untreated

P P P P PMAR

Thyroid disorder – Hypothyroid – Successful treatment, no

symptoms, no complications

Std Std Std Std PMAR

Thyroid disorder – Hypothyroid – Other cases

+100 to D

D D D PMAR

Tinnitus – Present Std-50 IC E-D E-D PS/PMAR

Tinnitus – History of, > 6 months symptom free, no underlying cause

Std Std Std Std PS/PMAR

Ulcer (Peptic) – History of, fully recovered

Std-50 Std-50 Std-50 Std-E Q’re/PMAR

Ulcer (Peptic) – Present, Mild Std-50 Std Std-50 E Q’re, PMAR

Ulcer (Peptic) – Present, Moderate/Severe

Std-50 IC E D Q’re, PMAR

Ulcer (Peptic) – Present, Chronic 50-100 IC D D Q’re, PMAR

Ulcerative Colitis – Medically treated, Mild

Std-100

50-100 E IC PMAR or ME

Ulcerative Colitis – Medically treated, Moderate

50-150

100-D E-D IC PMAR or ME

Ulcerative Colitis – Medically treated, Severe

50-D 100-D D D PMAR or ME

Ulcerative Colitis – Surgically treated < 6 months

PP PP D D PMAR

Ulcerative Colitis – Surgically treated > 6 months

Std-50 50-100 D D PMAR or ME

Ulcerative Colitis – Surgically treated > 5 years

Std Std E E PMAR or ME

Varicose Veins – Legs Std Std Std Std-E PMAR

Varicose Veins – Haemorrhoids Std Std Std Std-E PMAR

Underwriting – generalAdviser Easy Reference Guide to Insurance

15

Paramedical providerWe have available a mobile pathology/paramedical provider, Unified Healthcare Group (UHG), to assist with the provision of medical requirements.

In most cases your client can have a required medical examination and any blood samples taken at a time and place convenient for them. The pathology/paramedical provider will look after the appointment and medical requirements for you.

In some instances a client will reside in an area not serviced by the pathology/paramedical provider. On these occasions the client will need to be examined by a general practitioner. In these circumstances UHG will arrange the general practitioner examination.

You may wish to make alternative arrangements yourself for medical examinations and tests. Please ensure our Administration area is notified by noting this clearly in the Application Form under the Adviser and Commission details. This ensures that we do not inconvenience your client by duplicating arrangements and requirements.

Unified Healthcare Group UHG (preferred provider)

Phone: 1800 101 984 Fax: 1800 707 697 Website: www.uhg.com.au/lifetrack

Online tracking of all your client’s medical requirements arranged through UHG is available using the above website.

Should you require an alternative provider please contact Pathrec on 1800 066 895.

Residency

Availability of cover

Generally, only Applicants with permanent Australian residency status may be considered for insurance cover. Non-residents who return to their own countries are subject to different insurance legislation and disputes forums.

Terms for Life, Trauma and TPD may be considered for temporary residents seeking permanent residence in Australia, subject to underwriting approval prior to lodgement of the Application. Details will be required including:

full details of the type and nature of visa (please provide a copy)•copy of the letter from the Immigration Department with details of and status of •permanent residence application

any other information that could be helpful including details of any assets held in •Australia or other family members who are permanent residents etc.

Terms for income insurance may be considered for some temporary residents on working visas. Conditions apply, please contact your business development representative for further details.

16

Australian residents working or travelling overseas

Cover for Australian residents who are travelling or working overseas will need to be approved by the Underwriter, and will be considered on an individual basis. In some instances cover will not be available and will be declined until return to Australia, or an extra premium or exclusion may apply to cover any extra risk such as political unrest.

Australian residents who intend to work or travel overseas for extended periods of time are usually not eligible for Trauma, TPD or Income Protection.

Generally we are guided by the advice of our Reinsurers and the Department of Foreign Affairs and Trade (www.dfat.gov.au) in considering these applications.

The DFAT website has been updated and now includes five levels of advice which are allocated to any areas around the world that may be of concern to individuals when travelling. They are:

1 Be alert to your own security

2 Exercise caution

3 High degree of caution

4 Reconsider your need to travel

5 Do not travel

Applications will be declined for clients travelling to areas covered by Level 4 or 5 advices. Exclusions will apply to clients travelling to areas covered by a Level 3 advice. Country specific exclusions are available for short term travel subject to confirmation that insurance will not be cancelled on return.

Querying underwriting decisionsPlease refer all queries regarding underwriting decisions to the Underwriter who made the decision. They will be able to explain the assessment to you to assist you in your discussions with your client.

There may be circumstances where you understand and agree with the assessment however feel an adverse underwriting decision may have a detrimental effect on AXA. For example, any future business this client may generate (additional cover, investments and superannuation schemes etc.) could be dependent on the acceptance of the risk business.

In these instances, we ask that you submit in writing an explanation as to why an alternative assessment should be considered.

The following criteria will be used when assessing a business case:

the value of your current or future related business;•current value of the client, including business contained within other product lines or •AXA companies; and

the future potential of this client.•

Underwriting – generalAdviser Easy Reference Guide to Insurance

17

The business case should be referred to the Underwriting Manager for consideration. Business decisions of this nature will be discussed with the Product Manager.

Conversions, transfers and continuation options

Conversion and transfer of individual insurance cover

AXA and AC&L Individual Life, Trauma and TPD may be converted to an AXA Individual Insurance plan subject to certain requirements (listed below).

Plans that can be converted include AXA Individual Insurance, AC&L Individual Insurance, Flexipol, Provider, Goldline, FSP, RSP and Conventional Plans (such as Whole of Life and Endowment). The requirements include:

Any loadings, restrictions or exclusions on the existing cover will apply to the •new plan

If the existing plan has been loaded greater than 100%, conversions are not allowed •unless the existing plan has inbuilt convertibility which has not been deleted

An increase in the term of cover is only allowed for stepped plans•If the current plan is reinsured then automatic conversion may not be available. •Further information may be required and will be determined by the Underwriter once the application form has been received and may involve a request for medical and financial information. Permission will also need to be obtained from the reinsurer.

The life insured must be the same on both plans•New business commission is only payable on any increase in premium•The commission structure of the converted plan must be the same as the plan that it •is replacing

Any increase to the sum insured will require underwriting•Income Protection and Business Expenses Protection cannot be converted•Age rules and other conditions apply.•

All conversions are subject to the following underwriting requirements:

Application summary of the current application form•Signed and dated Declaration & Consent section.•

Conversions or transfers into Platform Insurance

A conversion into Summit or Generations is not automatically available. A transfer declaration is required in the first instance in all situations.

Please talk to your BDM regarding your specific case.

18

Conversions or transfers from Business Super

Transfer of insurance cover to an AXA Individual Insurance Plan may be available to a member from Super Directions for Business, Simple Super (SS), Tailored Super (TS) subject to the following requirements:

Full underwriting will be required if the existing sum insured was not underwritten or •for any increase in the sum insured

Any loadings, restrictions or exclusions on the existing cover will apply to the •new plan

If the existing plan has been loaded 100% or greater, a conversion exclusion will be •applied to the new plan

The life insured must be the same on both plans•New business commission is only payable on any increase in premium•Limitations may apply to reinsured business. Permission will have to be obtained from •the relevant reinsurer

Temporary but Total Disablement (TTD) cover cannot be converted•Age rules and other conditions apply.•

All transfers are subject to the following underwriting requirements:

Application summary of the current application form•Residence and travel details•Insurance details•Smoking question•Sports and pastimes details•Occupation details (TPD and Salary Continuance)•Income details • (TPD and Salary Continuance)

Signed and dated Declaration & Consent section.•

Inbuilt Convertibility and CPI

Inbuilt convertibility and CPI are not available for cover exceeding 100% extra mortality.

Continuation options

A Continuation option may be available when a member leaves an AXA group plan such as their employer’s Group insurance plan, Summit or Business Superannuation fund. The member may wish to continue their insurance cover through an AXA Individual Insurance Plan.

Provided a Continuation Option is available from the plan and the requirements applicable to the benefits are met, the continuation of cover to AXA Individual Insurance Plan will be available without the need for additional medical evidence. We must be in receipt of a Continuation Option form signed by the member

Underwriting – generalAdviser Easy Reference Guide to Insurance

19

All continuation options are subject to the following underwriting requirements:

Application summary of the current application form•Residence and travel details•Insurance details•Smoking question•Sports and pastimes details•Signed and dated Declaration & Consent section•

In addition, if the Continuation Option is for Salary Continuance or TPD the following is also required:

in the first instance the full completion of the occupation and income sections of the •personal statement will be required and is subject to underwriting

The Continuation Option expiry date will be 60 days (depending on the conditions of the plan) after ceasing employment with the employer who is the owner of (or party to) the Group Insurance plan. No extensions to this date will be available. Continuation Options are not available upon the closure of a plan.

Takeover terms (from another insurer)We may accept individual risk insurance that has been underwritten by any other insurance company provided the conditions below are met. Transfers are only allowed for Life, Trauma and TPD Insurance. Transfer terms are not available for Income Protection or Business Expenses.

Takeover criteria

The plan being transferred must satisfy the following criteria before a transfer can take place:

the maximum transfer age for the person to be insured is 60 years;•the transferring plan must be in force;•the transferring plan must have been fully underwritten within the last 5 years;•the transferring plan must have been accepted at standard rates;•the transferring plan must transfer to a similar type of contract, for example Stand •Alone Trauma may not be automatically transferred to a plan containing Life cover;

any existing exclusions on the transferring plan will apply to the new plan;•for Life cover the maximum sum insured cannot exceed $3 million;•for Trauma cover the maximum sum insured cannot exceed $1 million;•for TPD cover the maximum sum insured cannot exceed $2 million; and•the 13 month suicide clause on Life cover and the 90 day waiting period on Trauma •cover will be waived as long as the transferring plan and equivalent benefits have been in force for this period of time.

20

Takeover requirements

If the Takeover criteria are fully satisfied, the following evidence is required:

Life and TPD cover only up to $2 million

fully completed Takeover of Life and TPD Cover up to $2 million only form (containing •short form personal statement);

the original policy schedule; and•the most recent renewal notice.•

All other requests

fully completed application form (and full personal statement);•the original policy schedule; and•the most recent renewal notice.•

Mandatory medical and financial evidence will be waived, however full discretionary underwriting still applies. The Underwriter may still request medical or financial evidence on a discretionary basis.

The original policy schedule and latest renewal notice are required to provide evidence of:

the transferring policy being currently in force and premiums paid;•the benefit amount and type (including CPI increases);•acceptance at standard rates and details of any exclusions or restrictions; and•confirmation that the policy is not being transferred to another insurer.•

If these pieces of evidence are not available we may be able to accept alternative evidence, provided the above information is adequately disclosed to the satisfaction of the Underwriter.

Reinstatement process and requirementsThere are some circumstances in which a plan may lapse. Reasons this may occur include:

an inability to pay premiums;•alteration of bank account details that have not been advised to us;•renewal notices not being actioned; or•a change of address has not been advised to us.•

Provided six months has not passed since the plan ‘date paid to’ the plan may be reinstated as per the table on the next page.

Plans that have been cancelled on request of the policy owners cannot be reinstated. Full underwriting will be required to establish a new plan.

Underwriting – generalAdviser Easy Reference Guide to Insurance

21

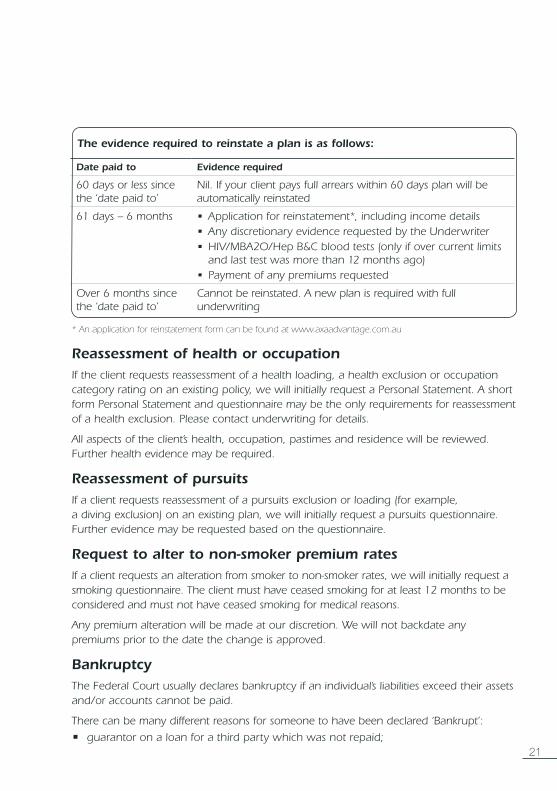

The evidence required to reinstate a plan is as follows:

Date paid to Evidence required

60 days or less since the ‘date paid to’

Nil. If your client pays full arrears within 60 days plan will be automatically reinstated

61 days – 6 months Application for reinstatement*, including income details•Any discretionary evidence requested by the Underwriter •HIV/MBA2O/Hep B&C blood tests (only if over current limits •and last test was more than 12 months ago)Payment of any premiums requested•

Over 6 months since the ‘date paid to’

Cannot be reinstated. A new plan is required with full underwriting

* An application for reinstatement form can be found at www.axaadvantage.com.au

Reassessment of health or occupationIf the client requests reassessment of a health loading, a health exclusion or occupation category rating on an existing policy, we will initially request a Personal Statement. A short form Personal Statement and questionnaire may be the only requirements for reassessment of a health exclusion. Please contact underwriting for details.

All aspects of the client’s health, occupation, pastimes and residence will be reviewed. Further health evidence may be required.

Reassessment of pursuitsIf a client requests reassessment of a pursuits exclusion or loading (for example, a diving exclusion) on an existing plan, we will initially request a pursuits questionnaire. Further evidence may be requested based on the questionnaire.

Request to alter to non-smoker premium ratesIf a client requests an alteration from smoker to non-smoker rates, we will initially request a smoking questionnaire. The client must have ceased smoking for at least 12 months to be considered and must not have ceased smoking for medical reasons.

Any premium alteration will be made at our discretion. We will not backdate any premiums prior to the date the change is approved.

BankruptcyThe Federal Court usually declares bankruptcy if an individual’s liabilities exceed their assets and/or accounts cannot be paid.

There can be many different reasons for someone to have been declared ‘Bankrupt’:

guarantor on a loan for a third party which was not repaid;•

22

small business unable to pay their bills;•silent partner in an investment/business which fails; or•major investment error, poor management of company funds.•

Life and Trauma Cover

When there is a current or past history of bankruptcy, life and trauma benefits for family protection will be assessed on their merits. Consideration will be given to any health problems that could be aggravated by financial crisis, including circulatory disorders, anxiety and depression.

Income Protection and Total and Permanent Disability Cover

We do not offer Income Protection or Total and Permanent Disability cover if a client is currently bankrupt and has not been discharged. If there has been a history of bankruptcy, further evidence will be requested and cover may not be available.

Requirements

The circumstances vary significantly from case to case so it is difficult to take a direct approach. However, it is important we obtain the right information to enable the best assessment of the situation. In most cases the client will be requested to provide a statement which should include the following:

reason and full details of ‘bankruptcy’ including amounts of money involved;•if criminal proceedings have followed and are pending (in these cases generally no •cover will be offered);

whether the client still has financial commitments to the other parties involved and if •so, how much? Will it impact current business or lifestyle?

proof of income for last 5 years including employment history; and•a Private Medical Attendant’s Report from the usual doctor will usually be requested •by the Underwriter.

Handy underwriting tipsIf you have any queries about a client you are advising in relation to insurance, call an Underwriter. The Underwriter can provide the right advice up front. Here are some handy tips to guide you through the underwriting process.

A brief client background

The Underwriter does not know the client. The only information we have about your client is what they supply in the Personal Statement. A note from you briefly outlining the client’s background is often invaluable and can minimise the number of phone calls and requests for additional information. A note providing extra background details may make all the difference. Please use the ‘Adviser notes’ section at the back of the Personal Statement.

Underwriting – generalAdviser Easy Reference Guide to Insurance

23

Adviser checklist for correct completion of the application and Personal Statement

Application summary

Have you shown occupation and industry in which applicant works?•Have you shown insurable income for last 12 months?•If applying for an alteration or increase to an existing plan, please make sure you •clearly state what the existing benefits are and what the new benefits being proposed are. It is also helpful to summarise the changing situation in the adviser notes.

Have you shown all benefits required on this page? In particular the type of plan, •occupation class, and when applying for income protection and/or business expenses, the monthly benefit, waiting period and benefit period.

Residence

If applicant is not an Australian resident have you included information as to what •visa is held, country of residency, date of arrival in Australia and date of intended departure from Australia?

If applicant intends travelling overseas have you supplied details of destinations also •reason for and dates of intended travel?

Other insurance

If there is other current insurance involved have you shown the sum insured and •indicated whether that cover is to be replaced or not?

If applicant has been accepted at other than standard rates or been declined in the •past have you included details of that assessment including the company involved and the date of the assessment?

If there are concurrent Applications being submitted for this life, have all details been •cross referenced on all Application Forms?

Health details

When completing the details of the applicant’s current doctor, have you included the •date, reason and result of last consultation?

If applicant has answered yes to having received advice to reduce alcohol or tobacco •intake have you supplied details of the doctor involved and date advice was received?

If any questions relating to any joint disorders, asthma, back or neck disorders, •depression, anxiety or nervous conditions, cyst/mole/skin lesions, blood pressure or cholesterol have been answered ‘yes’, have you completed the appropriate questionnaire?

If the applicant has answered ‘yes’ to any of the medical questions, please ensure that •full details of dates, the condition, results of all investigations and who was consulted are provided.

24

Sports and Pastimes

If applicant is involved in any sports and pastimes, have you completed the •appropriate questionnaire where applicable?

Questionnaires

If a questionnaire is required to be completed in regard to either health or pursuits or •pastimes have you had all questions answered and any additional information that may clarify the risk included in the adviser notes?

If more that one questionnaire is required (eg for several joint related issues), •additional forms can be downloaded from our website at www.axaadvantage.com.au.

Occupation and income details

Have you completed the full occupation history, not just the current occupation details?•Have full occupational duties been specified?•For employees, have you completed the income details for the last 2 financial years as •well as the current income details?

In the case of self employed applicants, have you completed the income details for •the last 2 financial years?

Business Expenses

If the applicant is applying for business expense cover have you fully completed •the questionnaire?

Authorities and Declarations

Have you had medical authorities signed and dated?•Where applicable have you had the financial authority signed and dated?•Has the applicant provided the name and contact details of their accountant, •if applicable?

Has the applicant authorised us to forward medical information to their usual •general practitioner?

Has the applicant provided the name of their usual general practitioner?•Have you had the declaration and consent both signed and dated?•

Adviser, commission details and notes

Have you indicated what the intention is in regard to existing business?•Have you indicated if you have or are having mandatory medical examinations or •pathology tests arranged?

Have you attached any additional information (such as financial evidence) that you •wish to submit with this application?

Have you used the adviser notes section to provide any additional information or •explain any unusual aspects of the risk?

Underwriting – generalAdviser Easy Reference Guide to Insurance

25

Have you made reference to any conversations you may have had with the office •prior to submitting business including name of person you spoke to and date of conversation?

Applications completed in full

A quick check that the Application has been fully completed before submitting it can help save time during the underwriting process.

Please check that:

all questions have been answered (refer to section below regarding the personal •statement on the medical examination form);

alterations are signed by your client – signatures to alterations are critical, as the •Underwriter must make sure the disclosure is legally compliant before finalising the Application. The Application and all the supporting documentation are the basis of the contract, so the normal legal contractual requirements exist.

Medical examination personal statement

The personal statement section of the current AXA medical examination form will not be required when the following criteria have been met:

full medical examination completed by a fully qualified doctor; •a copy of the fully completed application form personal statement is presented with •the medical examination form to the doctor prior to examination; and

signed declaration by the doctor, that the application form personal statement has •been sighted

This concession does not apply if a Mini Check examination is performed.

Telephone underwriting

Telephone underwriting is a great way to save time when we need to obtain additional information from your client. When you provide your client’s telephone numbers in the Personal Statement, we can contact your client directly to obtain the additional information (for example, clarification of a medical condition). This can sometimes remove the need for other more complex and time consuming requirements such as doctor’s reports.

Obviously if your client does not wish us to call them, we will respect this and follow the normal ‘paper’ process.

Type of insurance and information required

When completing the Application, keep in mind the type of insurance you are recommending to the client and pass on as much information as possible to the Underwriter. For example, if your client is applying for Income Protection, we are covering the client for their income and their occupation, therefore we need as much detail as possible regarding their occupation, employment history (and prospects if appropriate) and income.

26

Attaching additional information

If you find there is insufficient space when completing any section(s) of the Application form, you can attach a page(s) containing further information to the Application. Where multiple pages are attached please ensure that the client signs and dates each page.

If your client has any additional information relevant to their Application, please include it with the Application. This information may include copies of medical records, flying or diving logbooks, financial records and tax returns. Remember, if a client can substantiate their disclosure at underwriting stage, it minimises calls for additional underwriting requirements and makes the claims process easier. For example, in some instances a copy of the following can be accepted instead of a discretionary Personal Medical Attendant’s report:

an x-ray report;•blood test; •specialist doctor letter; or•pathology report.•

Questionnaires

The Personal Statement includes some questionnaires that we ask your client to complete at the point of sale where appropriate. Fully completing these at the point of sale will save time during the underwriting process.

Further requirements

It is always best to follow up any requirements immediately and not wait until a ‘final reminder’ is issued. If you need to query anything, call the Underwriter of the application immediately, they will be happy to help.

Occupations

If you are unsure of the occupation rating for your client and are unable to contact an Underwriter, some advisers have suggested you rate your client more conservatively. Then you may be able to return to your client with a lesser premium.

New business administration requirementsDirect debit or credit card authority is to be completed where required.•Your adviser number is also required.•The first premium is to be enclosed with the application for direct methods or debit/•credit card authority for direct debit methods.Multiple applications are to be lodged together.• Ensure that the Insurance quote from the PQT is completed and enclosed with •the application.

Underwriting – generalAdviser Easy Reference Guide to Insurance

27

Alteration requests – underwriting requirements

Alteration requested Initial requirementsUnderwriting required?

Smoker to Non-Smoker Application for Smoker to Non-Smoker Yes

Review of Health Loading Application details and Personal Statement Yes

Review of Pursuits Exclusion Relevant questionnaire Yes

Review of Health Exclusion Review of health exclusion form Yes

Review of Occupation Category

Application details and Personal Statement Yes

Waiting Period Increase Letter from client No

Waiting Period Decrease Application details and Personal Statement Yes

Sum Insured Increase Application details and Personal Statement Yes

Sum Insured Decrease Letter from client No

Increase in Benefit Period Application details and Personal Statement Yes

Decrease in Benefit Period Letter from client No

Exercising Buy Back Option Application details No

Exercising Trauma Reinstatement Option

Application details No

Addition of Children’s Trauma Option

Children’s Trauma Personal Statement Yes

From Indemnity Option to Agreed Value (applies to plans from August 2005 to current series only)

Application details, Occupation and Income details section, residence, pursuits, other insurance, relevant financial evidence and declarations

Yes

Exercising the Business Solutions Option

Application details, relevant financials, details of occupation, residence, other insurance, and pursuits

Yes

Conversion to Senior Professionals Plan

Application details, Occupation and Income sections of the Personal Statement

Yes

Increase through Future Insurability (inc YN option)

Please refer to client’s plan document as requirements vary depending on product series

No

Addition of any Option Application details and Personal Statement Yes

Take up of Benefit Booster Option

Benefit Booster Application Yes

Cover Boost Option Application details, income section of the Personal Statement

Yes

Adding Indemnity Option Application details No

Out of Working Hours cover to 24 Hour cover

Letter from client No

Change of plan ownership Refer to page 58 —

28

This page has been left blank intentionally

29

Underwriting – Life, Trauma and Total and Permanent Disability (TPD)Adviser Easy Reference Guide to Insurance

Medical limits – mandatory requirements

Definition of requirements

Medical examination

The medical examination is to be performed by the usual general practitioner

Mini Check Examination

An abridged version of the Medical Examination that can be performed by a registered nurse

Paramedical examination

The medical examination can be performed by a registered nurse

Specialist medical examination

The medical examination is to be performed by a Specialist Physician such as a Cardiologist (not a General Practitioner). Where a specialist medical examination is required, a medical examination by the usual doctor will not be required

Blood screen

HIV MBA20 Hep B & C

HIV blood test, Fasting MBA20, Hepatitis B & C serology

HIV (AIDS) Antibody Test Fasting Multiple Biochemical Analysis Hepatitis B Surface Antigen (HbsAg) and Hepatitis C Antibody (anti-HCV) tests

Resting ECG Resting ECG with interpretation

Exercise ECG Exercise/Stress ECG – incorporates a Resting ECG

PMAR Personal Medical Attendant’s Report

PSA Prostate Specific Antigen (Males only)

Cotinine Detects nicotine (may be a blood or urine test)

FBC Full Blood Count/Analysis/Examination

MSU Microscopic Urinalysis

For Medical Requirements for Life and TPD cover please refer to Table A. For Trauma cover please refer to Table B.

A Personal Statement is required for all applications. In addition, the following mandatory requirements must be provided at the stated sums insured. The tables over the page are a guide to minimum requirements only. The circumstances of each case will determine the need for further tests or reports. The following requirements relate to total cover with AXA and AC&L.

Special note for increases

Mandatory requirements may be waived depending on the time since commencement of the plan (or past increases) and the evidence previously requested. Our Underwriters will be able to assist you with these queries.

30

Table A – Medical Requirements – Life and TPD

Current age Blood screen Mini-check

Medical examination by usual General Practitioner or Paramedical facility evaluation

Usual General Practitioner examination#

Personal Medical Attendant’s Report (PMAR)* Resting ECG

Specialist medical examination and Exercise ECG

Up to 40 $1,000,001 $1,000,001 $1,500,001 $2,000,001 $3,000,001 Not a mandatory requirement

$5,000,001**

41 – 45 $1,000,001 $1,000,001 $1,500,001 $2,000,001 $3,000,001 $2,500,001 $5,000,001**

46 – 50 $1,000,001 $750,001 $1,000,001 $1,500,001 $3,000,001 $2,500,001 $5,000,001**

51 – 55 $750,001 N/A $750,001 $1,000,001 $3,000,001 $1,500,001 $5,000,001**

56 – 60 $500,001 N/A $500,001 $1,000,001 $3,000,001 $1,000,001 $5,000,001**

61 – 65 $500,001 N/A $100,001 $1,000,001 $3,000,001 $750,001 $5,000,001**

66 + $500,001 N/A $1 $500,001 $3,000,001 $750,001 $5,000,001**

# Where the client does not have a usual General Practitioner (GP), an examination by another GP is acceptable. Should a client with a usual GP choose to be examined by another GP, we may obtain a Personal Medical Attendant’s Report from their usual GP. If an examination is performed by a GP, a Paramedical examination will not be required.

* A PMAR may not be required at these levels if the medical examination was performed by a usual doctor of at least 2 years. PMARs will be requested and organised by AXA.

** Additional medical evidence is required for cover between $5,000,001 and $10,000,000:

• Medical Examination – to be completed by a Specialist Physician (for example Cardiologist, FRACP) in all cases.

• Blood tests – PSA (if male), FBC.

• Urine tests – MSU, Cotinine (if a non-smoker).

For cover in excess of $10,000,000 please contact underwriting for requirements

Table B – Medical Requirements – Trauma

Current age Blood Screen

Medical Examination by usual General Practitioner

Full Blood Count Resting ECG PSA Mammogram

Up to 40 $1,000,001 $1,000,001 $1,000,001 $1,000,001 N/A N/A

41 – 45 $750,001 $750,001 $1,000,001 $1,000,001 N/A N/A

46 – 50 $500,001 $750,001 $750,001 $1,000,001 N/A N/A

51 – 55 $500,001 $500,001 $500,001 $750,001 $500,001 $500,001

56 – 60 $250,001 $250,001 $250,001 $250,001 $500,001 $500,001

61 – 67 $1 $1 $1 $1 $1 $1

Underwriting – Life, Trauma and Total and Permanent Disability (TPD)Adviser Easy Reference Guide to Insurance

31

Important notes

Please read the following notes carefully:

1 These medical requirements relate to total standalone cover – proposed and existing with AXA and AC&L. Table A is based on the highest sum insured between Life and TPD. Table B is based on total Trauma insurance.

2 Medical examiners must not be a relative of the proposed insured, the Adviser, Broker or their families, nor a business associate of the proposed insured.

3 The maximum TPD sum insured available from all sources is $3,000,000.

4 The maximum Trauma Recovery sum insured available from all sources is $2,000,000.

5 Half of Double TPD sum insured and Double Trauma sum insured will be taken into consideration for the purposes of calculating the total sum insured.

6 For applications for Trauma cover in excess of $1,000,000, please contact the Underwriting Department for specific requirements.

7 A Personal Medical Attendant’s Report (PMAR) may be obtained on a discretionary basis where any required medical examination was not performed by the proposed insured’s usual General Practitioner and more specific information is required.

8 A Blood Screen plus Hepatitis B Surface Antibody (anti-HBS) test will be required in all cases for doctors, dentists and surgeons applying for:

Occupationally Acquired HIV, Hepatitis B and C Option under the Income •

Insurance Plus Plan.

9 For the Business Solutions Option, medical requirements will be requested up-front based on the original sum insured plus the Business Solutions Option sum insured amount.

This option is only available to medically standard lives•

Medical evidence is generally not required when exercising the Business Solutions •

Option (some exceptions apply based on the amount of the increase)

Please refer to the relevant Product Disclosure Statement or plan document

10 Cotinine blood testing may be randomly requested at sums insured over $750,000 for non-smokers.

Financial limits – mandatory requirements

Financial requirements for life cover

The table overleaf is a guide to minimum financial requirements. The circumstances of each case will determine the need for further evidence. The following requirements relate to total cover with all companies.

32

Sum InsuredFinancial requirements for Life cover and TPD cover (based on highest sum insured)

Up to $2,000,000

1 Occupation and income details to be disclosed on the personal statement

$2,000,001 to $5,000,000 for Personal Insurance

1 Adviser Report2 Financial Questionnaire

$5,000,001 and over for Personal Insurance

1 Adviser Report2 Financial Questionnaire (signed by Accountant)3 Individual Income Tax returns and assessment notices for the last

two years4 If self-employed or employed by own company, audited detailed Profit

and Loss Accounts, Balance Sheets, notes to accounts for the last two years for all business entities and Company Tax Returns

$5,000,001 and over for Personal Loan Insurance

1 Adviser Report2 Financial Questionnaire (signed by Accountant) including an

explanation of why this person is responsible for the loan repayment to the extent of the sum insured applied for

3 Copy of Loan Agreement showing approval and all loan details4 If self-employed or employed by own company, audited detailed Profit

and Loss Accounts, Balance Sheets and notes to accounts for the last two years for all business entities

$2,000,001 to $3,000,000 for Business Insurance

1 Adviser Report2 Financial Questionnaire

$3,000,001 and over for Key Person Insurance

1 Adviser Report 2 Financial Questionnaire (signed by Accountant) 3 Audited detailed Profit and Loss Accounts, Balance Sheets and notes to

accounts for the last two years for all business entities$3,000,001 and over for Business Succession Insurance

1 Adviser Report2 Financial Questionnaire (signed by Accountant) 3 Audited detailed Profit and Loss Accounts, Balance Sheets and notes to

accounts for the last two years for all business entities4 Copy of buy-sell agreement (if applicable)5 Independent business valuation

$3,000,001 and over for Business Loan Insurance

1 Adviser Report2 Financial Questionnaire (signed by Accountant) 3 Audited detailed Profit and Loss Accounts, Balance Sheets and notes to

accounts for the last two years for all business entities4 Copy of loan agreement showing approval and all loan details

Underwriting – Life, Trauma and Total and Permanent Disability (TPD)Adviser Easy Reference Guide to Insurance

33

Please note that any additional documentation may help to streamline the underwriting process, as the Underwriter must establish that the benefits and the amount applied for match the need.

Financial underwriting considerations – personal and businessBy financially underwriting, we aim to identify and accept risks on the basis of a clearly illustrated need for the cover being sought.

Although financial underwriting is generally applied to large sums insured, the need should be clear with all risks regardless of the sum insured. Sums insured in excess of need, in some instances, are associated with ‘anti-selection’ and a higher rate of claim.

The Underwriter must establish that:

premium payments can be sustained by the premium payer; and•a claim will not leave the policy owner/beneficiary in a better financial position than •they would have been in if the person insured had continued to live or had remained in good health.

Insurance needs generally fall into the categories of Personal Insurance (refer to page 35) or Business Insurance (refer to page 36).

The sum insured is usually based on the income an individual generates by his or her own activity (after expenses but before tax). This income is referred to as ‘personal exertion income’. Unearned income (for example, interest, rent or dividends) is not taken into consideration when calculating the sum insured unless it ceases on the insured’s death or disablement.

Maximum cover amounts

TPD

The maximum cover amount for TPD is currently $3,000,000 (from all sources) for income earning applicants. Non-income earning applicants (other than home makers) are generally restricted to $750,000 (from all sources). Refer to page 36 for details regarding home makers.

Activities of Daily Living (ADL) TPD

The maximum cover for ADL is $2,000,000 and may be used to increase the total TPD cover to $5,000,000.

Please note, to choose both types of TPD, you must first select $3,000,000 worth of TPD before you can select any ADL TPD amount. This is not necessary where you are purchasing ADL TPD only.

34

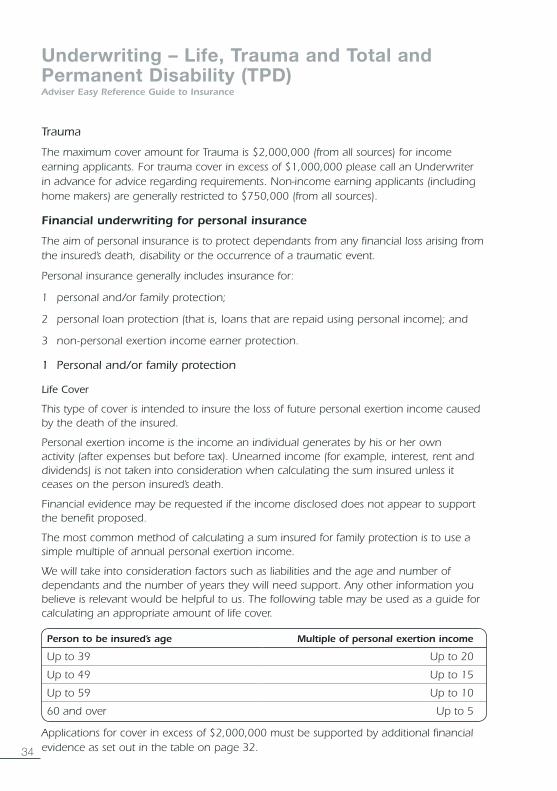

Trauma

The maximum cover amount for Trauma is $2,000,000 (from all sources) for income earning applicants. For trauma cover in excess of $1,000,000 please call an Underwriter in advance for advice regarding requirements. Non-income earning applicants (including home makers) are generally restricted to $750,000 (from all sources).

Financial underwriting for personal insurance

The aim of personal insurance is to protect dependants from any financial loss arising from the insured’s death, disability or the occurrence of a traumatic event.

Personal insurance generally includes insurance for:

personal and/or family protection;1

personal loan protection (that is, loans that are repaid using personal income); and2

non-personal exertion income earner protection.3

1 Personal and/or family protection

Life Cover

This type of cover is intended to insure the loss of future personal exertion income caused by the death of the insured.

Personal exertion income is the income an individual generates by his or her own activity (after expenses but before tax). Unearned income (for example, interest, rent and dividends) is not taken into consideration when calculating the sum insured unless it ceases on the person insured’s death.

Financial evidence may be requested if the income disclosed does not appear to support the benefit proposed.

The most common method of calculating a sum insured for family protection is to use a simple multiple of annual personal exertion income.

We will take into consideration factors such as liabilities and the age and number of dependants and the number of years they will need support. Any other information you believe is relevant would be helpful to us. The following table may be used as a guide for calculating an appropriate amount of life cover.

Person to be insured’s age Multiple of personal exertion income

Up to 39 Up to 20

Up to 49 Up to 15

Up to 59 Up to 10

60 and over Up to 5

Applications for cover in excess of $2,000,000 must be supported by additional financial evidence as set out in the table on page 32.

Underwriting – Life, Trauma and Total and Permanent Disability (TPD)Adviser Easy Reference Guide to Insurance

35

Trauma

This type of cover is intended to assist the person insured with the expenses and associated lifestyle changes expected in the event of a major trauma.

Unlike Life and TPD insurance, a trauma event does not necessarily result in the insured’s death or inability to work.

The sum insured should not represent a ‘wind fall’ gain to the policy owner or beneficiary. For this reason, total Trauma insurance will generally be calculated using up to 50% of the multiple used to calculate life cover.

For cover in excess of these multiples, we will initially require an Adviser Report to explain how the sum insured was determined and the need for the cover, before consideration is given.

The current maximum sum insured for income earning applicants for Trauma is $2,000,000 (from all sources). Additional requirements are necessary over $1,000,000 and must be discussed in advance with an Underwriter.

TPD

This type of cover is intended as a lump sum income replacement so it is important to ensure the cover is not excessive when compared to personal exertion income.

As a guide, the total TPD sum insured will generally be restricted to a multiple of up to 10 times annual personal exertion income. The multiple may vary depending on the age of the insured, financial needs, commitments and the total number of dependants and their ages.

For cover in excess of these multiples, we will initially require an Adviser Report detailing the reason for cover and explaining how the sum insured was calculated.

The current maximum sum insured for income earning applicants for TPD is $3,000,000 (from all sources).

2 Personal Loan Protection

In the majority of cases, personal loan protection is requested to cover a mortgage. This type of cover is intended to protect the lender from financial loss upon the premature death or disablement of the borrower.

The Underwriter will take into consideration the amount of the loan, the duration of the loan, the reason for the loan, the reputation of the lending service, the capacity to repay the loan and any other insurance on the life or disablement of the person insured.

Generally, the amount of loan cover required will be adequately accommodated when using the multiple of personal exertion income method mentioned in the Personal and/or Family Protection section above.

Applications for cover in excess of $2,000,000 will need to be supported by additional financial evidence as set out in the table on page 32.

36

3 Non-personal exertion income earner protection

This type of cover is usually proposed to insure joint debt commitments and/or the financial responsibility for dependants. Applicants for this type of insurance include home makers and students. Cover for students will generally be limited to $500,000.

For home makers, Life, Trauma and TPD amounts up to $750,000 will generally be considered on the basis of information in the personal statement. However, higher amounts of Life and TPD cover* may be considered subject to the receipt of statement from the person to be insured containing the following information:

the need for the cover and how the cover amount was determined;•the personal exertion income of the income generating spouse/partner, if applicable;•unearned income details (for example, interest, rent or dividends);•assets and liabilities of the family unit;•the total number and type of dependants and their ages; •any existing insurance in force on both the income-generating spouse/partner. It •is preferable that the income-generating spouse/partner has at least an equivalent amount of cover; and

any other helpful information (for example, a child with an ongoing sickness).•