adding value through aged care advice rahul singh – anz technical services

TRANSCRIPT

Adding value through aged care advice

Rahul Singh – ANZ Technical Services

3

Recap on means testing of aged care

Strategies

Agenda

4

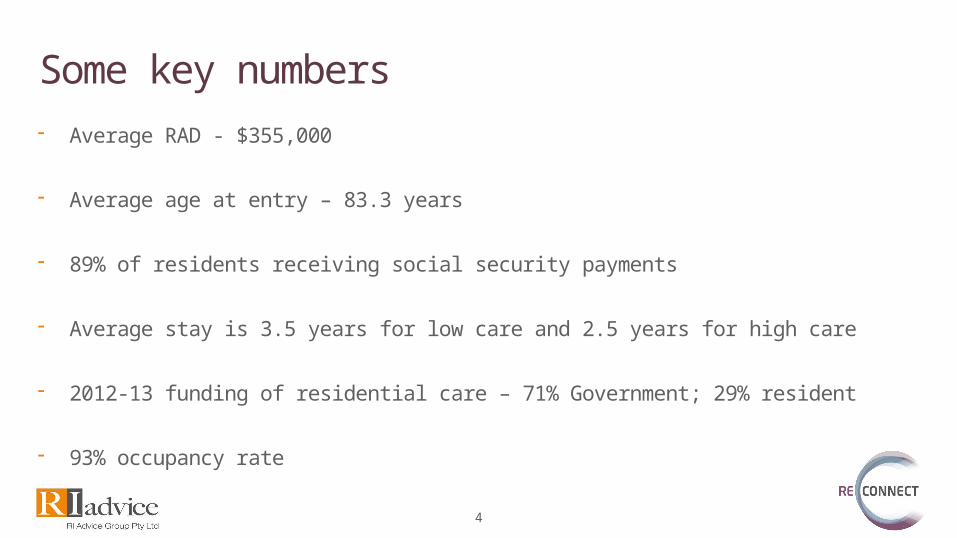

- Average RAD - $355,000

- Average age at entry – 83.3 years

- 89% of residents receiving social security payments

- Average stay is 3.5 years for low care and 2.5 years for high care

- 2012-13 funding of residential care – 71% Government; 29% resident

- 93% occupancy rate

Some key numbers

5

- Basic daily care fee – 85% of the single basic age pension rate

o $47.49 per day or $17,334 per annum

- Accommodation payment – cost of buying into the facility

- Means tested care fee – cost of paying for your care

- Additional charges / extra services fee

- Incidentals

Aged care fee structure

6

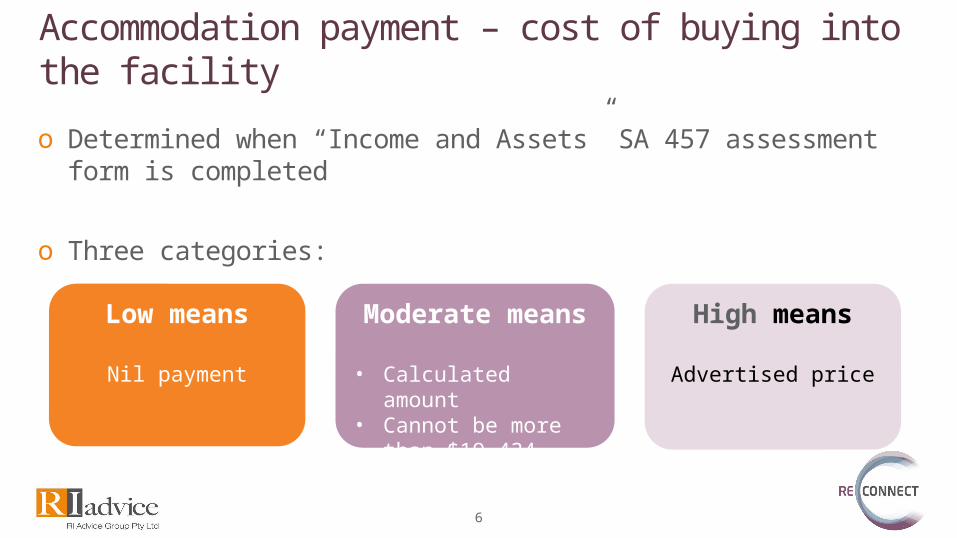

Accommodation payment – cost of buying into the facility

o Determined when “Income and Assets” SA 457 assessment form is completed

o Three categories:

Low means

Nil payment

Moderate means

• Calculated amount• Cannot be more than

$19,434 annually

High means

Advertised price

7

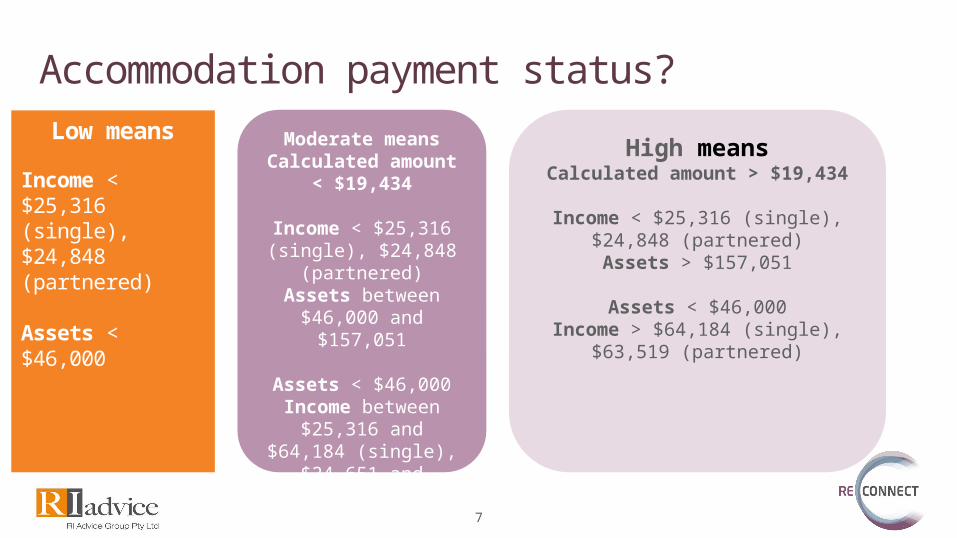

Accommodation payment status?Low means

Income < $25,316 (single), $24,848 (partnered)

Assets < $46,000

Moderate meansCalculated amount <

$19,434

Income < $25,316 (single), $24,848

(partnered)Assets between

$46,000 and $157,051

Assets < $46,000Income between

$25,316 and $64,184 (single), $24,651 and $63,519 (partnered)

High meansCalculated amount > $19,434

Income < $25,316 (single), $24,848 (partnered)

Assets > $157,051

Assets < $46,000Income > $64,184 (single), $63,519

(partnered)

8

Means tested amount calculation

Income

50% of assessed income above the income free area*

(*25,316 for singles, $24,848 each for couple separated by illness)

Assets

17.5% of the value of assets between $46,000 and $157,051+1% of the value of assets between $157,051and $379,154+2% of the value of assets above $379,154

o If the above calculation is > $19,434 (current maximum accommodation supplement), then the person is high means

o If the above calculation is < $19,434 then the person is eligible for government subsidy towards cost of accommodation and is either low or moderate means

9

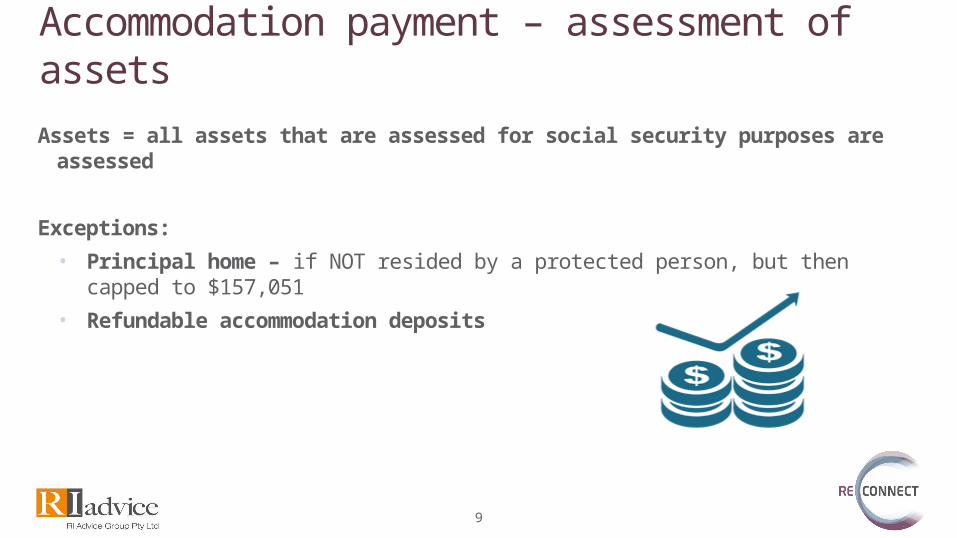

Assets = all assets that are assessed for social security purposes are assessed

Exceptions:

• Principal home – if NOT resided by a protected person, but then capped to $157,051

• Refundable accommodation deposits

Accommodation payment – assessment of assets

10

Income = Assessed by social security + income paid by Centrelink / DVAExceptions:

• Minimum Pension Supplement

• Energy Supplement

• DVA Disability Pension – where the person or their spouse has qualifying service

• DVA War Widow or Widower Pension where the person has qualifying service

• Rent from home where the person or their spouse is paying

o interest on accommodation bond or paying accommodation charge OR

o daily accommodation payment / contribution for their cost of accommodation

•What about account based pensions?

Accommodation payment – assessment of income

11

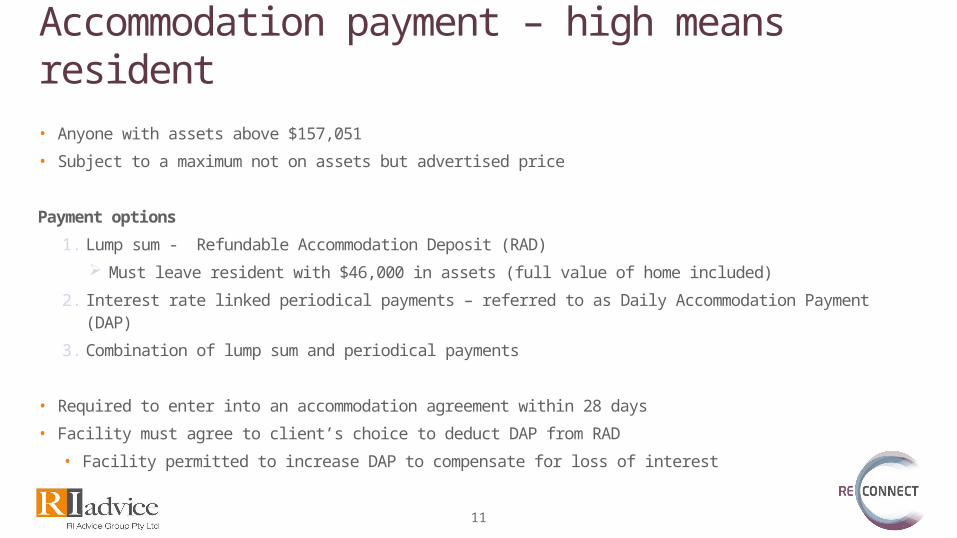

• Anyone with assets above $157,051

• Subject to a maximum not on assets but advertised price

Payment options

1. Lump sum - Refundable Accommodation Deposit (RAD) Must leave resident with $46,000 in assets (full value of home included)

2. Interest rate linked periodical payments – referred to as Daily Accommodation Payment (DAP)

3. Combination of lump sum and periodical payments

• Required to enter into an accommodation agreement within 28 days

• Facility must agree to client’s choice to deduct DAP from RAD

• Facility permitted to increase DAP to compensate for loss of interest

Accommodation payment – high means resident

12

Accommodation contribution – moderate means resident

• Different to accommodation payment for high means resident• Maximum capped to a calculated

amount rather than the advertised price

• Maximum lower of calculated amount and accommodation supplement payable to the facility

• Fluctuates quarterly based on assets and income

• Availability of moderate means beds?

Payment options1. Lump sum - Refundable Accommodation

Contribution (RAC)2. Calculation linked periodical payments –

referred to as Daily Accommodation Contribution (DAC)

3. Combination of RAC & DAC

• Required to enter into an accommodation agreement within 28 days

• Facility must agree to client’s choice to deduct DAC from RAC

Facility permitted to increase DAP to compensate for loss of interest

13

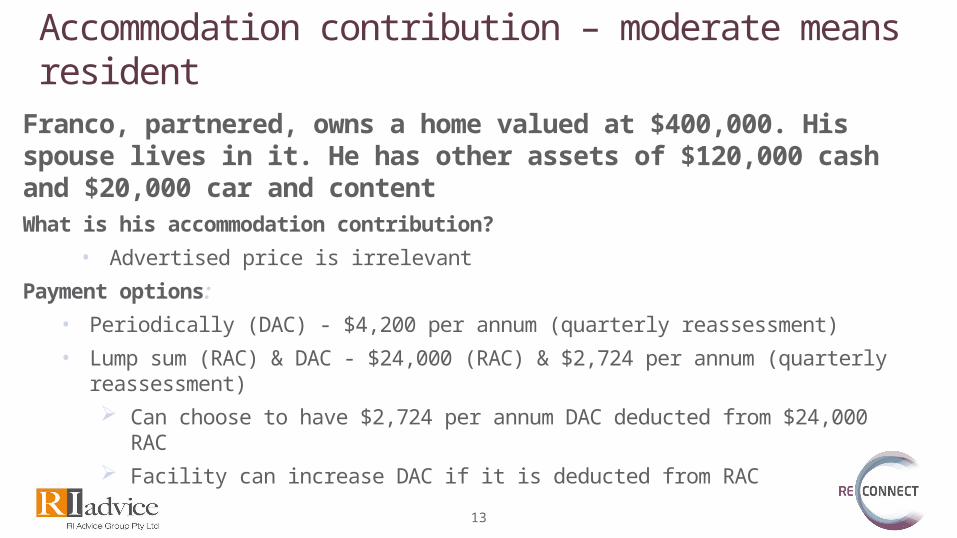

Accommodation contribution – moderate means residentFranco, partnered, owns a home valued at $400,000. His spouse lives in it. He has other assets of $120,000 cash and $20,000 car and contentWhat is his accommodation contribution?

• Advertised price is irrelevant

Payment options:

• Periodically (DAC) - $4,200 per annum (quarterly reassessment)

• Lump sum (RAC) & DAC - $24,000 (RAC) & $2,724 per annum (quarterly reassessment)

Can choose to have $2,724 per annum DAC deducted from $24,000 RAC

Facility can increase DAC if it is deducted from RAC

14

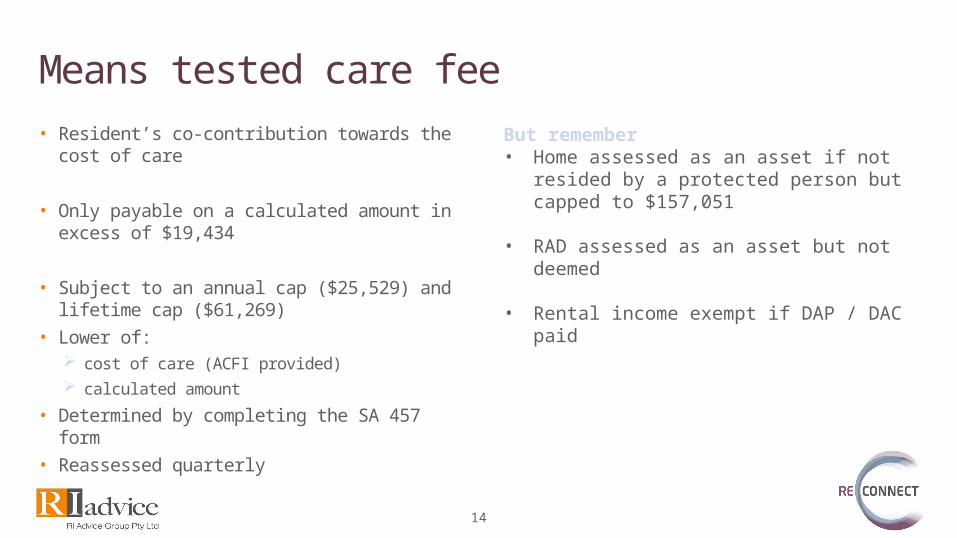

• Resident’s co-contribution towards the cost of care

• Only payable on a calculated amount in excess of $19,434

• Subject to an annual cap ($25,529) and lifetime cap ($61,269)

• Lower of: cost of care (ACFI provided) calculated amount

• Determined by completing the SA 457 form

• Reassessed quarterly

Means tested care fee

But remember• Home assessed as an asset if not resided by a

protected person but capped to $157,051

• RAD assessed as an asset but not deemed

• Rental income exempt if DAP / DAC paid

15

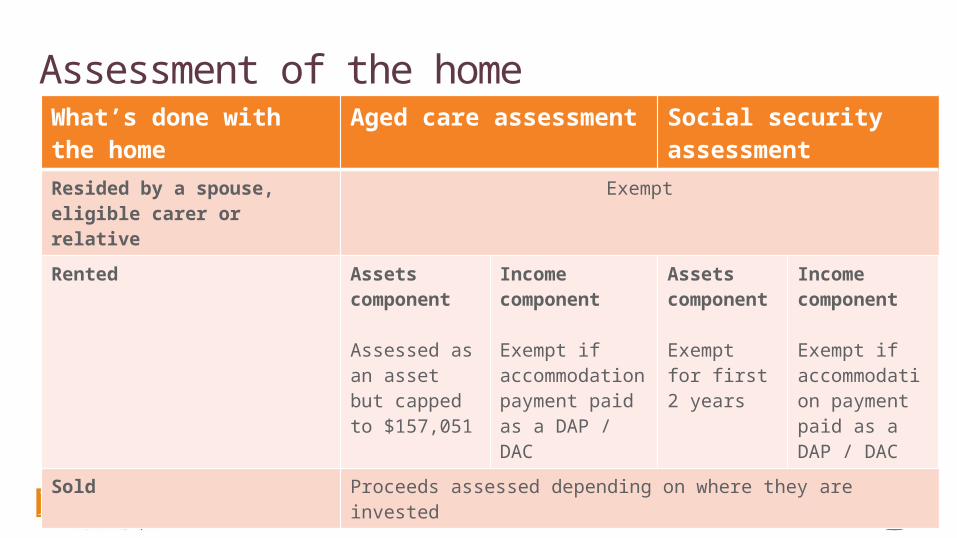

Assessment of the homeWhat’s done with the home

Aged care assessment Social security assessment

Resided by a spouse, eligible carer or relative

Exempt

Rented Assets component

Assessed as an asset but capped to $157,051

Income component

Exempt if accommodation payment paid as a DAP / DAC

Assets component

Exempt for first 2 years

Income component

Exempt if accommodation payment paid as a DAP / DAC

Sold Proceeds assessed depending on where they are invested

16

• An asset reduction opportunity for the purposes of means tested care fee

• Keep & rent the home - ensure the accommodation payment is partly paid by DAP

Selling the home can be detrimental

Maintaining social security entitlements

Reduction in means tested care fee: particularly assets component

• It is not always desired to retain the home

Alternative options?

Value of retaining the home

17

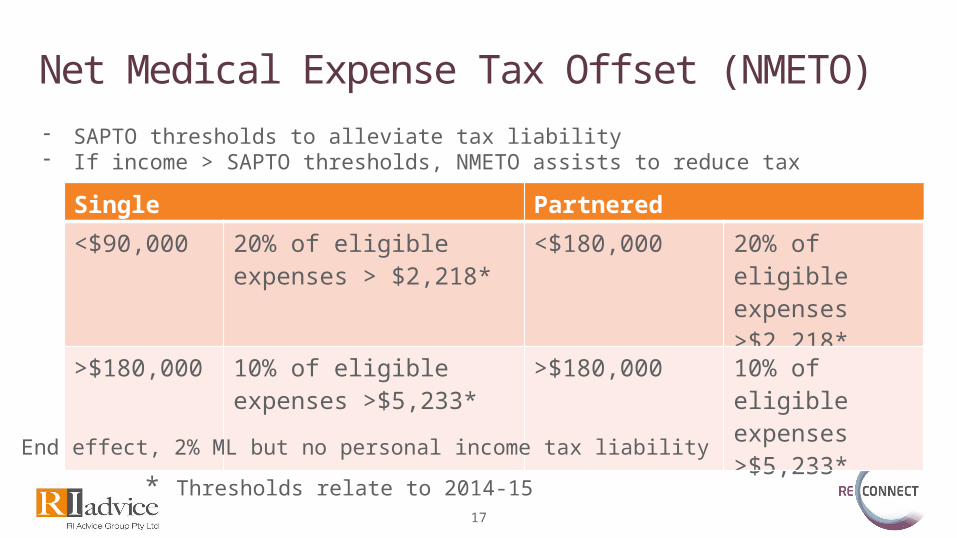

Net Medical Expense Tax Offset (NMETO)

- SAPTO thresholds to alleviate tax liability- If income > SAPTO thresholds, NMETO assists to reduce tax

Single Partnered

<$90,000 20% of eligible expenses > $2,218*

<$180,000 20% of eligible expenses >$2,218*

>$180,000 10% of eligible expenses >$5,233*

>$180,000 10% of eligible expenses >$5,233*

- End effect, 2% ML but no personal income tax liability

* Thresholds relate to 2014-15

18

• Structuring accommodation payment At least some DAP / DAC for couples Cashflow poor clients – DAP / DAC deducted from RAD /

RAC

• Retaining home, renting it and paying some DAP / DAC

• Paying RAD to increase social security entitlements

• Using lifetime / term based annuities

• Insurance bonds in controlled private trusts?

• Sourcing cheaper financing for the RAD borrowing from family, reverse mortgage or bank

Advice opportunities• Gifting within allowable limits

With pre-planning, 5 years before moving for self-funded retirees

• Funeral bonds / burial plots

• Ensure tax advisers are claiming / aware of NMETO !

• Ensure SA 457 form has been completed when relevant

19

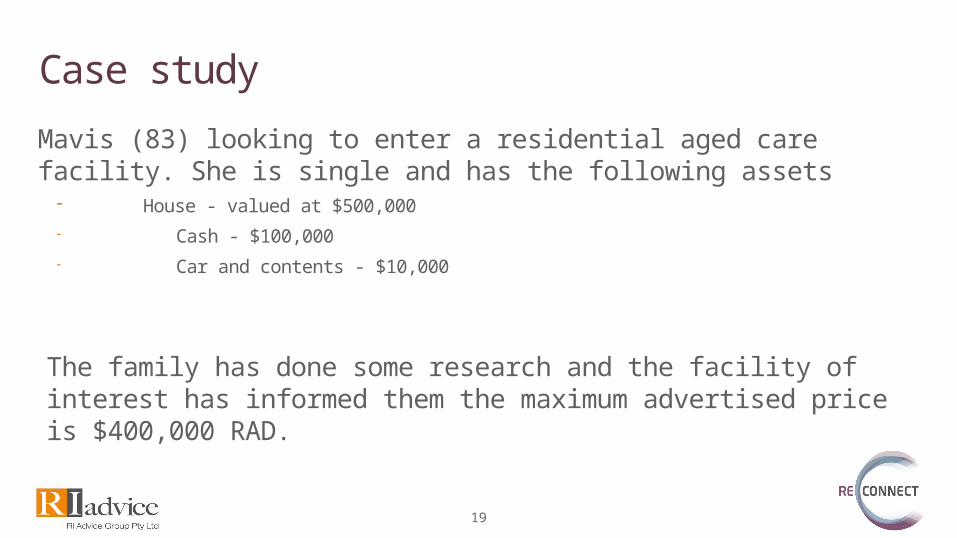

Mavis (83) looking to enter a residential aged care facility. She is single and has the following assets

- House - valued at $500,000

- Cash - $100,000

- Car and contents - $10,000

The family has done some research and the facility of interest has informed them the maximum advertised price is $400,000 RAD.

Case study

20

Case study – no advicePre care ($) In care ($)

Age Pension 22,365 21,423

Investment income 3,000 6,300

Total income 25,365 27,723

Basic Daily Care Fee

Not applicable

17,334

Accommodation payment 400,000 RAD (lump sum paid)

Means tested care fee 7,329

Incidentals 3,000

Total expenses 22,265 27,663

Net income 3,000 60

21

Case study – with advice: retaining home and renting itPre care ($) In care ($) Retain and rent home

Age Pension 22,365 21,423 22,365

Investment income 3,000 6,300 300

Rental income Not applicable 20,000

Total income 25,365 27,723 42,665

Basic Daily Care Fee

Not applicable

17,334 17,334

Accommodation payment 400,000 RAD (lump sum paid) 100,000 RAD paid, 18,450 per annum DAP ($300,000 * 6.15%)

Means tested care fee 7,329 1,103

Incidentals 3,000 3,000

Total expenses 22,265 27,663 39,887

Net income 3,000 60 2,778

22

Case study – with advice: Invest in annuityPre care ($) In care ($) Retain and rent

homeInvest in annuity

Age Pension 22,365 21,423 22,365 22,365

Investment income 3,000 6,300 300 17,371

Rental income Not applicable 20,000 Not applicable

Total income 25,365 27,723 42,665 39,736

Basic Daily Care Fee

Not applicable

17,334

Accommodation payment 400,000 RAD (lump sum paid)

100,000 RAD paid, 18,450 per annum DAP ($300,000

* 6.15%)

400,000 RAD (lump sum paid)

Means tested care fee 7,329 1,103 6,857

Incidentals 3,000

Total expenses 22,265 27,663 39,887 27,191

Net income 3,000 60 2,778 12,545

23

- Many technical issues - Aged Care calculator available through Adviser Advantage- Contact Technical Services if you want to run a scenario

o 1800 444 019

In closing up…..