adding value development of food processing and supply chain · adding value –development of food...

TRANSCRIPT

Adding Value – Development of Food Processing and Supply Chain

A “Plate to Farm” perspective

Asitava SenSenior Director & Head – Food and Agribusiness Research & Advisory, Rabobank

2

Rabobank Group

From a rural Dutch credit cooperative to a leading full-service financial

group Rabobank Nederland Rabobank International

Coöperative CentraleRaiffeisen-Boerenleenbank, B.A.

Two separate cooperative banks - the Coöperatieve

Centrale Raiffeisen-Bank in Utrecht and the

Coöperatieve Centrale Boerenleenbank in Eindhoven -

were founded by enterprising rural folk, who, with

little access to the capital market, decided to help one

another.

Leading full service financial group in the

Netherlands, holding many subsidiaries

with business in:

Insurance, Pensions, Leasing / trade

& Vendor Finance, Asset

Management/Advice, Real Estate

Project Development/Finance,

Private Banking, Home Broker

Rabobank International (Corporate

Investment Banking)

Largest financial group in the world

specialized in Food and Agribusiness

(F&A) on a Global Basis:

Presence in >42 countries

Over 1,300 F&A clients

Global Approach

Local Relationship

All Industries

Full Service (Corporate and Retail)

Food and Agribusiness Focused

Corporate Investment Banking

Safest privately-owned Bank , more than EUR 700 billion in Assets

1898

2013

Cooperative Principle: long-term relationship

3

Our approach to client relationships

Driven by sector knowledge & supported by product capabilities

Sectors covered:

Dairy

Ingredients & Sugar

Grains & Oilseeds

Value-added Processing

Beverages

Animal Protein

Farm Inputs

Broader sub sector coverage

Sub sector specialists involved in both origination and execution for financing and advisory products

Sub sector coverage bankers cover an entire region (Europe, Americas or Asia)

M&A bankers specialised into 11 sub sectors of the food, drinks and agri spectrum

Access to deeper research

Rabobank has its own unique group of dedicated and highly specialised Food and Agri Research analysts (FAR)

FAR comprises over 70 analysts in 13 countries around the globe

Fundamental research covering the entire food and drinks chain

Output in the form of tailored presentations for internal and external clients, World Maps, Industry Notes, F&A Reviews, Commodity Notes and Regional Banking Reports

4

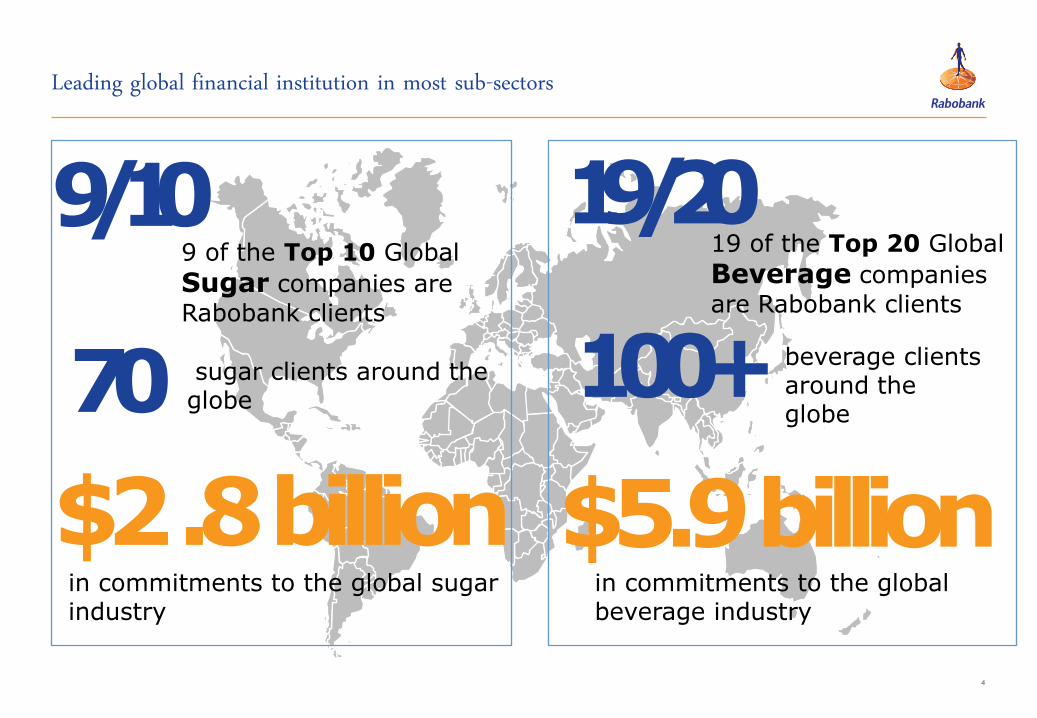

Leading global financial institution in most sub-sectors

9 of the Top 10 Global

Sugar companies are

Rabobank clients

9/10

70 sugar clients around the globe

$2 .8 billionin commitments to the global sugar industry

19/2019 of the Top 20 Global

Beverage companies

are Rabobank clients

100+ beverage clients around theglobe

$5.9 billionin commitments to the global beverage industry

5

•Emerging trends in global food supply chain

•Emerging integrated and dedicated supply chains in India

•Conclusions and questions for panel discussion

Agenda

6

• Four drivers are responsible.

• The first three are well known.

• The fourth – the great crossover – is new.

• As a result, F&A companies are trying to maintain and grow their margins in an increasingly complex operating environment.

F&A supply chains are under unprecedented pressure

Source: Rabobank, 2013

7

• This concept is new, even though the individual elements are well known

• Outside agendas now influence traditional supply and demand dynamics

• Their influence has become material

• The complexity they create is set to remain

The great crossover creates new complexity, adding pressure to the chain

Source: Rabobank, 2013

8

Traditional conflicts in the supply chain - Dilemma

Suppliers are gradually strengthening their

negotiating position – will returns be better in

open market? How much to commit to one

buyer?

Buyers are seeking to protect margin – how much upside to be shared to secure supply and reduce volatility?

9

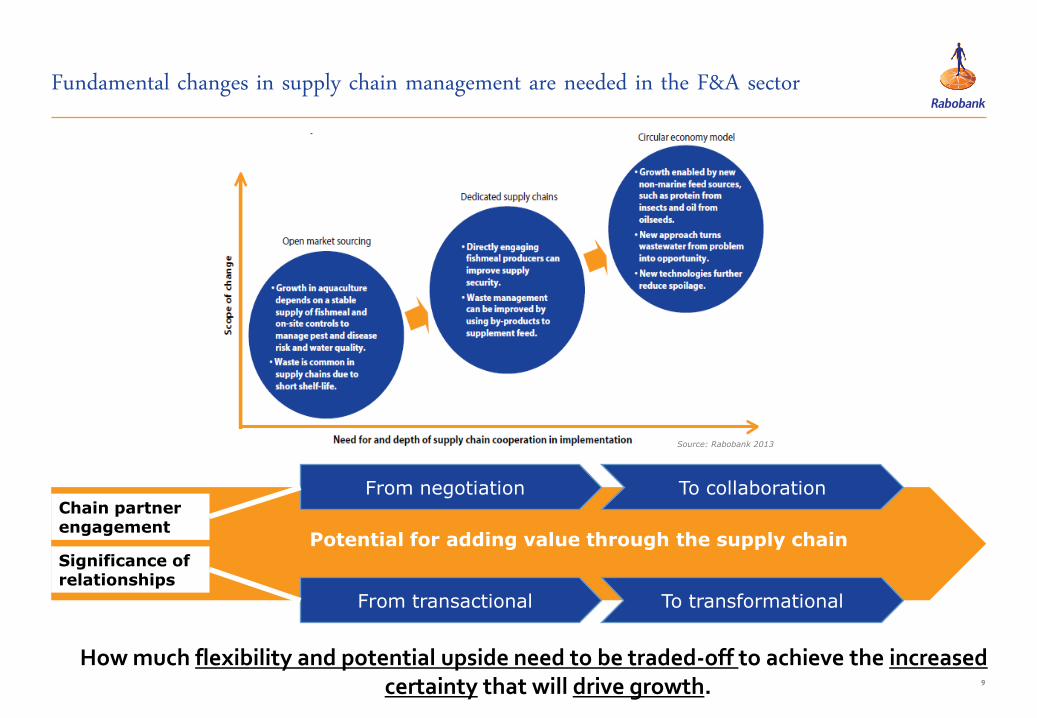

Fundamental changes in supply chain management are needed in the F&A sector

Chain partner engagement

From negotiation

From transactional

To collaboration

To transformational

How much flexibility and potential upside need to be traded-off to achieve the increased certainty that will drive growth.

Significance of relationships

Potential for adding value through the supply chain

Source: Rabobank 2013

10

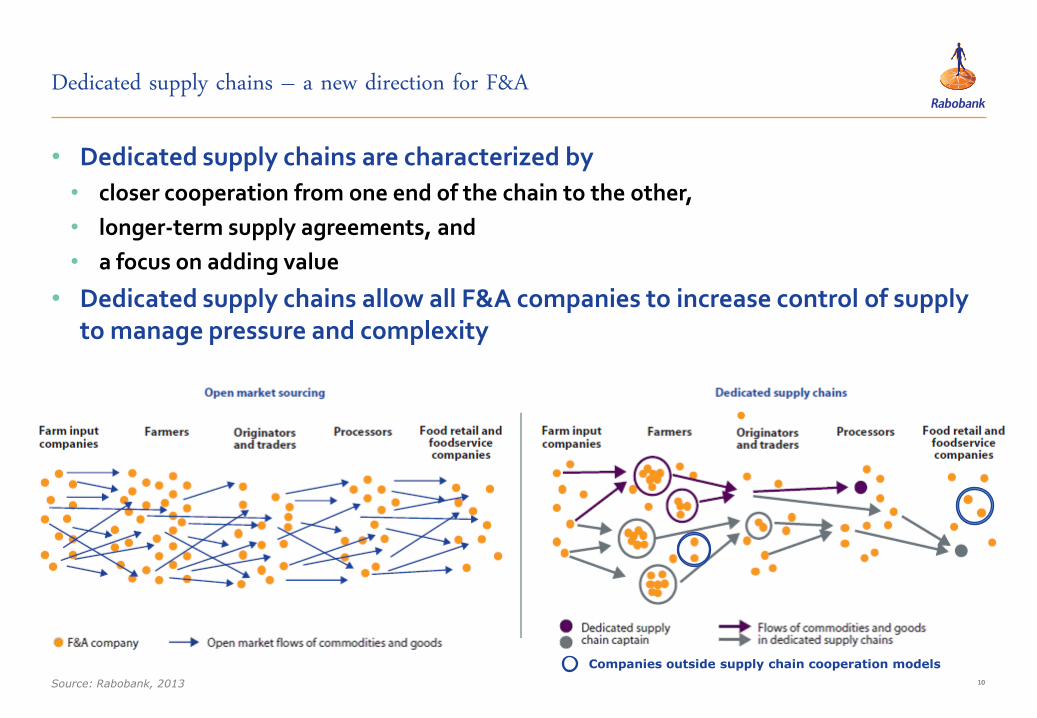

Dedicated supply chains – a new direction for F&A

Source: Rabobank, 2013

• Dedicated supply chains are characterized by

• closer cooperation from one end of the chain to the other,

• longer-term supply agreements, and

• a focus on adding value

• Dedicated supply chains allow all F&A companies to increase control of supply to manage pressure and complexity

Companies outside supply chain cooperation models

11

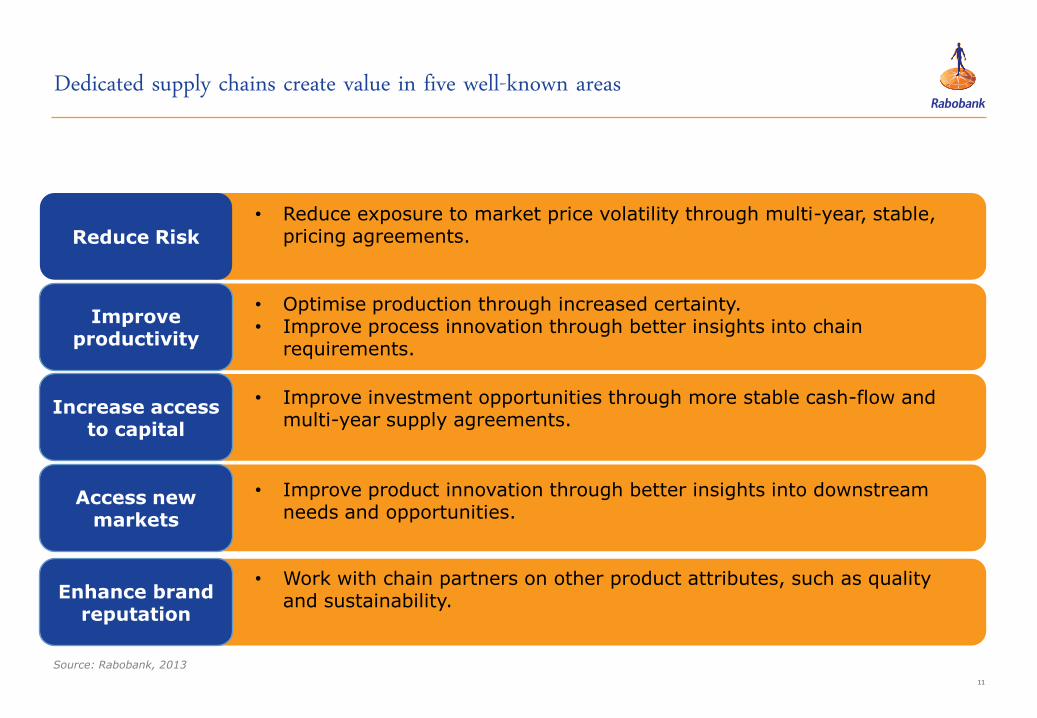

Dedicated supply chains create value in five well-known areas

Source: Rabobank, 2013

• Reduce exposure to market price volatility through multi-year, stable, pricing agreements.

• Optimise production through increased certainty.• Improve process innovation through better insights into chain

requirements.

• Improve investment opportunities through more stable cash-flow and multi-year supply agreements.

• Improve product innovation through better insights into downstream needs and opportunities.

• Work with chain partners on other product attributes, such as quality and sustainability.

Reduce Risk

Improve productivity

Increase access to capital

Access new markets

Enhance brand reputation

12

Leading F&A companies are responding to this concept

McDonald’s has long established close

working relationships with its suppliers,

seeing them more as partners than

transactional counter-parties.

McDonald’s promotes innovation by

specifying what is needed rather than

how partners should deliver its needs.

Bayer Crop Science is strengthening

relationships with growers and retailers

in vegetable supply chains.

Retailers select varieties, Bayer Crop

Science produces seed, and growers

deliver to market specifications,

reducing risk for all involved.

Starbucks is investing in its supply chain

in Yunnan Province, China, to improve

its focus on quality.

Starbucks has established a local coffee

grower training centre to improve local

production. In return Starbucks wants

to market high-quality Yunnan coffee.

Nestlé has formal structures and checks

on suppliers to help manage its chain.

Nestlé directly works with some 45,000

farmers, providing advice on agronomic

practices and support to meet Nestlé's

product quality and sustainability

requirements, and to contribute to local

sustainability.

Coca-Cola is looking double its revenues

by 2020.

Can the supply of agri commodities keep

pace with this sort of target?

This question is already being addressed

in the juice industry, with suppliers and

off-takers adopting novel approaches to

under-write new investments.

India Examples

13

•Emerging trends in global food supply chain

•Emerging integrated and dedicated supply chains

in India

•Conclusions and questions for panel discussion

Agenda

14

A few examples of collaboration in the supply-chain in IndiaQ

uic

k S

ervic

e

Resta

uran

tsG

rain

Sto

rag

eD

air

yB

everag

es

15

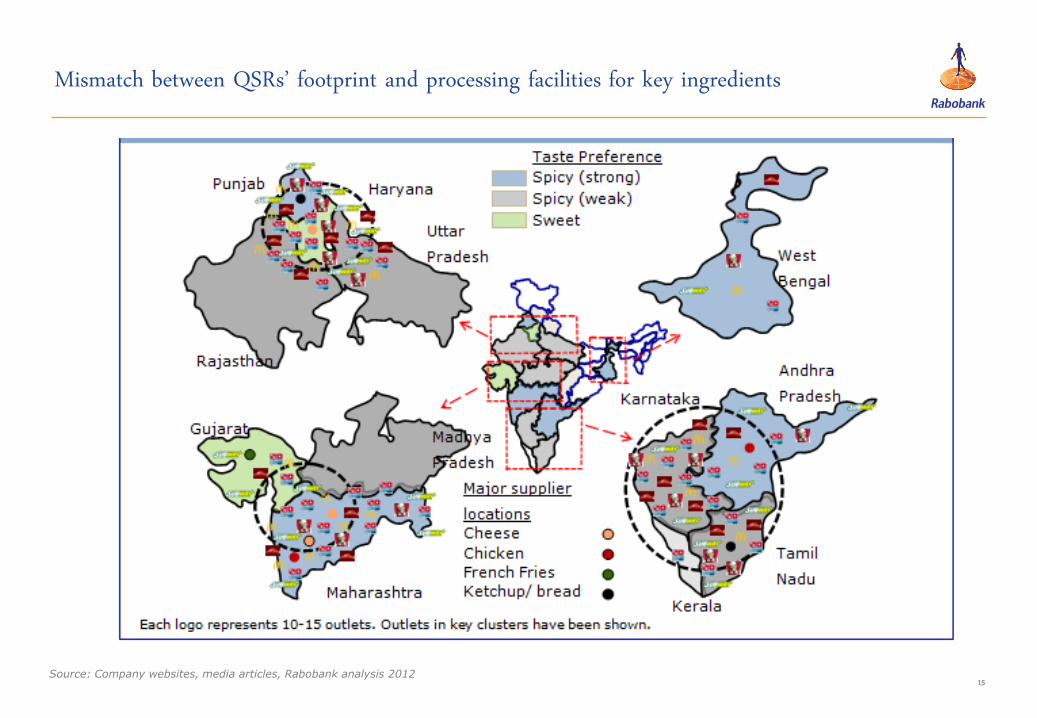

Mismatch between QSRs’ footprint and processing facilities for key ingredients

Source: Company websites, media articles, Rabobank analysis 2012

16

•Emerging trends in global food supply chain

•Emerging integrated and dedicated supply chains in India

•Conclusions and questions for panel discussion

Agenda

17

Conclusions

• A clear view of the chain and getting the business model / focus right is more

important than ever

• Positive outlook in F&A underpinned by demand growth. In a consumption led

economy, demand will always precede supply.

• The question is how would the supply side cope with changing food demand and

consumption?

• There is a case in favour of thinking “Plate to Farm” vis a vis the traditional concept

of “Farm to Fork”

• Role of the “captain” at the downstream end is critical in this transformation.

Growth in demand will lead to investments in upstream and midstream and

compact value chains, which will be beneficial to all stakeholders

18

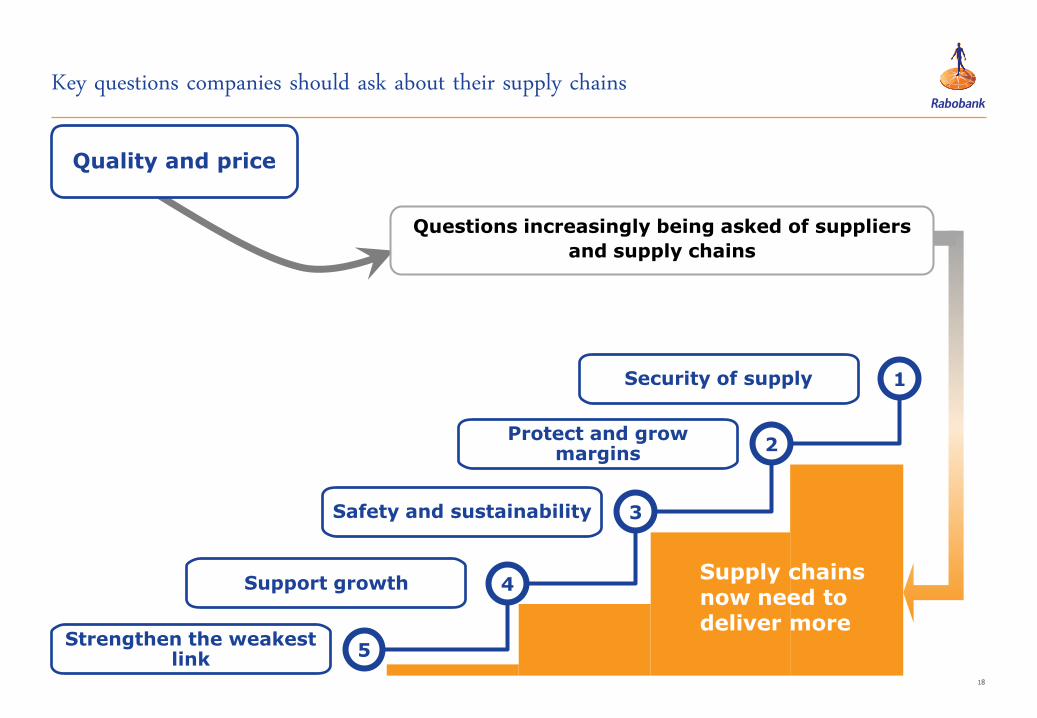

Key questions companies should ask about their supply chains

Quality and price

Questions increasingly being asked of suppliers

and supply chains

Protect and grow margins

Security of supply

Support growth

Safety and sustainability

Strengthen the weakest link

1

2

3

4

5

Supply chains now need to deliver more

19

• For the panel, we would like to understand your viewpoint on the weakest linkages

which need to be addressed first?

• Some more question relevant to our discussion today:

More Questions for the Panel Discussion

Government

• What should be the focus of our policy initiatives to promote the right investments in the supply chain?

• What impact does the Food Safety regulation have on the food supply chain?

Chain Captains Chain Partners

• What are downstream companies in India doing to improve supply chain linkages?

• What are some of the best practices in supply chains from the developed world that can be adopted in the Indian market?

• How do producers capture greater value in the supply chain?

• What other process hurdles need to be managed to make the supply chain dedicated and efficient, in the local context?

20

Contacts

Rabobank International

1/F, Forbes Building

Charanjit Rai Marg

Fort, Mumbai 400 001

India

+91 22 22034567

Rabo India Finance

Asitava SenSenior Director & Head Food & Agribusiness Research, India

Telephone +91 22 2219 7126E-mail [email protected]

Neither this presentation nor any of its contents may be used for any other purpose without the prior written consent of the Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. (“Rabobank” or “Rabobank International”).

The information in this presentation reflects prevailing market conditions and our judgment as of this date, all of which may be subject to change. This presentation is based on public information. The information and opinions contained in this document have been compiled or arrived at from sources believed to be reliable, but no representation or warranty, express or implied is made as to theiraccuracy, completeness or correctness. The information and opinions contained in this document are wholly indicative and for discussion purposes only. No rights may be derived from any potential offers, transactions, commercial ideas et cetera contained in this presentation. This presentation does not constitute an offer or invitation. This document shall not form the basis of or be relied upon inconnection with any contract or commitment whatsoever.