adapting management accounting knowledge needs to functional and economic change

TRANSCRIPT

This article was downloaded by: [Moskow State Univ Bibliote]On: 07 February 2014, At: 10:50Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Accounting Education: An InternationalJournalPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/raed20

Adapting management accountingknowledge needs to functional andeconomic changePhilip Cooper aa University of Bath , UKPublished online: 20 Nov 2006.

To cite this article: Philip Cooper (2006) Adapting management accounting knowledge needs tofunctional and economic change, Accounting Education: An International Journal, 15:3, 287-300

To link to this article: http://dx.doi.org/10.1080/09639280600850760

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoeveror howsoever caused arising directly or indirectly in connection with, in relation to orarising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Adapting Management Accounting

Knowledge Needs to Functional and

Economic Change

PHILIP COOPER

University of Bath, UK

Received: 23 September 2005

Revised: 31 January 2006; 10 April 2006; 20 April 2006

Accepted: 21 April 2006

ABSTRACT Changes in the function of the management accountant and in the economicenvironment, particularly the shift of economic activity away from manufacturing and theinternationalisation of education, raise issues of the breadth and diversity of knowledge needs formanagement accounting. The impact of these issues is investigated using data on perceived topicimportance from an international survey of over 1600 members of the Chartered Institute ofManagement Accountants. The substantial importance attached to a range of topics from outsidethe management accounting discipline itself, and to more strategic topics from within it, isconsistent with a developing function for the practitioner associated with a broadening set ofknowledge needs, since these topics add to rather than supplant many traditional coremanagement accounting topics. Variation in the importance of topics among economic sectorstends to be specific to certain topics, such as costing, although the public sector has distinctivepriorities. Diversity in knowledge needs is also apparent internationally, particularly in terms ofthose working in developing economies, who attach greater importance to many topics in financeand financial accounting than others do.

KEY WORDS: Management accounting education, knowledge needs, internationalisation, CIMA

Introduction

A lack of clear boundaries to management accounting has inspired efforts over an

extended period to identify a ‘common body of knowledge’ (Lander and Reinstein,

1987) that defines its educational scope by reference to practice. The current reliability

of this approach is called into question by Boer’s (2000, p. 324) observation that prac-

titioners ‘seem confused about . . . what the field of management accounting should be

about’ but the perspective offered by IFAC (1998) suggests rather that practice may be

diversifying in response to functional and economic changes, with quite distinct

implications for accounting education.

Accounting Education: an international journal

Vol. 15, No. 3, 287–300, September 2006

Correspondence Address: Philip Cooper, School of Management, University of Bath, Bath BA2 7AY, UK.

Email: [email protected]

0963-9284 Print=1468-4489 Online=06=030287–14 # 2006 Taylor & FrancisDOI: 10.1080=09639280600850760

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

The evolution towards a more strategic function for the management accountant

described by IFAC (1998) and reflected in the academic literature (Maskell and Baggaley,

2000; Kaplan, 1995) implies not only that the scope of what constitutes education in

management accounting should be developing accordingly but also that management

accountants need to be able to demonstrate competencies relying on knowledge outside

the discipline in both education (van den Brink et al., 2003) and practice (IFAC, 2002).

Thus, educators should be concerned with the breadth of education needed for

management accounting.

IFAC (1998) also reports that practice may vary among ‘different countries, cultures

and organizations’, and the potential need to recognize this diversity in management

accounting education is reinforced by global economic change in two key ways:

1. The relative economic importance of business sectors is changing in many countries,

particularly with a shift away from manufacturing (see, for example, Yuskavage and

Pho, 2004; and ONS, 2004, p. 9, dealing with the USA and UK respectively).1

2. With globalization and the internationalisation of education, many students are likely

to be educated and work in different countries. This is most especially an issue in the

USA, UK and Australia, the three largest exporters of higher education (Harman,

2004), where international student numbers grew over the five years to 2002/03 by

21.8%, 29.1% and 123% respectively and such students were disproportionately

represented on business/management courses (IIE, 2003; HESA, 2004, 1999; DEST,

2004).

This study aims to assess the effect of these developments on knowledge needs through

an investigation of practitioners’ views of the importance of a broad range of topics from

within and outside the management accounting discipline, and of the extent to which these

views vary internationally and among sectoral groups. Data were obtained from a survey

of its members conducted for the UK’s Chartered Institute of Management Accountants

(CIMA), which is described below after a review of previous relevant empirical work.

The subsequent section presents an analysis of the relative importance of the topics and

of how views of topic importance vary dependent on respondents’ characteristics. The

final section provides a discussion and conclusions in terms of educational implications.

Empirical Investigations of Management Accountants’ Knowledge Needs

The identification of curricular content by reference to practice has been the subject of

empirical research since at least the 1970s when Deakin and Summers (1975) produced

a ranking of 39 management accounting topics based on a survey of accountants and stu-

dents in Texas. Subsequent studies, summarised by Novin et al. (1990), pursued a similar

approach but that of Lander and Reinstein (1987) was notable in seeking to establish a

comprehensive ‘common body of knowledge’ based on 168 topics, including topics

from outside the discipline, grouped under Management Accounting Objectives

(MAOs). However, their survey of members of the National Association of Accountants

investigated the relative importance of the MAOs rather than individual topics.

An understanding of the relative significance of knowledge outside management

accounting per se was targeted by Novin et al. (1990) and Novin (1997) in US surveys

of Certified Management Accountants (CMAs). These studies underlined the importance

of broad areas such as financial accounting and information systems but did not involve a

detailed consideration of topics.

288 P. Cooper

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

Research outside the USA has been less extensive. Such studies (e.g. Tan et al., 2004;

Dugdale, 1994) have revealed consistencies (for example, in the key importance ascribed

to capital budgeting and working capital management), but they have been confined to

other developed economies.

Variations in topic importance across business sectors have only been considered in

certain more recent studies, which have emphasised the distinctiveness of the manufactur-

ing sector. Khan et al. (2000) found that those in this sector tend to attribute much greater

importance to costing techniques and inventory control and less to implementing strategy.

Furthermore Tan et al. (2004) using three categories (manufacturing, retail and service)

identified a tendency for those in manufacturing to rate process costing more highly

than those from other sectors, and to rate cost-volume-profit analysis and standard

costing more highly than those from the retail sector. Tan et al. (2004) also detected

some variation in importance for a small number of topics according to the respondent’s

work experience, although with uncertain interpretation.

Overall, therefore, previous studies have tended to be circumscribed by a focus on more

traditional topics within the management accounting discipline, a restricted geographical

scope and relatively little attention to the type of organization within which management

accountants works. Furthermore, many of those involving surveys had limited sample

sizes. Consequently, there remains a need for a large-scale, comprehensive view of the

breadth of practitioners’ needs and of their international and sectoral variation. This is

met by the survey reported here, which follows precedent research in surveying prac-

titioners, notwithstanding that the views of educators and academic researchers are also

relevant and may differ from those of practitioners (see, for example, Tan et al., 2004;

Edwards and Emmanuel, 1990).2

Method

The survey was undertaken as part of a project commissioned by CIMA to review the

curriculum for its professional qualification. The instrument was developed in conjunction

with CIMA and informed by focus group consultation with its members. To facilitate a

relatively rapid response from members around the world, a web-based administration

format was adopted. Members for whom an e-mail address was held by CIMA (over

20% of the membership) were contacted by the organization and invited to complete

the questionnaire on-line.

The questionnaire firstly elicited the respondent’s personal details and secondly asked

how important specified topics were ‘to the work carried out in your organization’. The

topics were defined by reference to the headings used in CIMA’s professional qualification

syllabus (CIMA, 2000), so that respondents would be broadly familiar with the relevant

content, and were presented in four subject areas: Financial Accounting (topics 12a to i),

Finance (topics 13 a to g), Management Accounting (topics 14 a to m) and Management

(topics 15 a to h). To indicate level of importance, the following response categories were

offered throughout, 1 ¼ ‘of critical importance’; 2 ¼ ‘very important’; 3 ¼ ‘of some

importance’; 4 ¼ ‘of little or no importance’.

After rating the topics, respondents were asked to indicate any important topics not covered

in the CIMA syllabus and any that could be excluded. A minority responded to these ques-

tions, in most cases using the opportunity to highlight the importance of particular areas

within topics or to restate the low importance attributed to topics in the earlier questions.

To validate responses and obtain further information, 25 respondents who had indicated

a willingness to do so were interviewed by telephone. These interviews confirmed the

validity of the responses given by the individuals and did not reveal any difficulties

Adapting Management Accounting Knowledge Needs 289

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

with completion of the instrument that would affect the interpretation of the survey results

as discussed below.

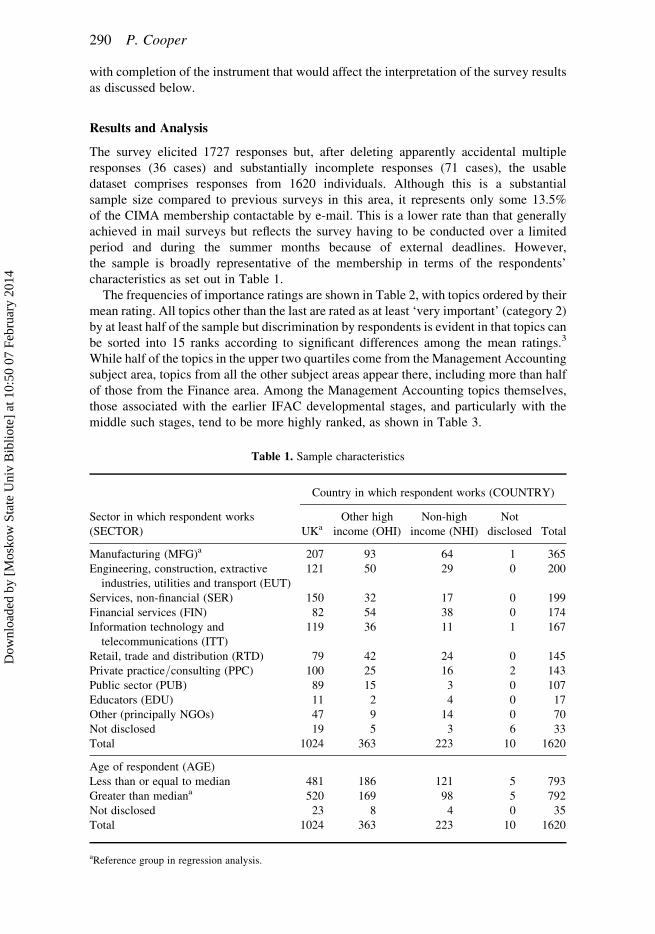

Results and Analysis

The survey elicited 1727 responses but, after deleting apparently accidental multiple

responses (36 cases) and substantially incomplete responses (71 cases), the usable

dataset comprises responses from 1620 individuals. Although this is a substantial

sample size compared to previous surveys in this area, it represents only some 13.5%

of the CIMA membership contactable by e-mail. This is a lower rate than that generally

achieved in mail surveys but reflects the survey having to be conducted over a limited

period and during the summer months because of external deadlines. However,

the sample is broadly representative of the membership in terms of the respondents’

characteristics as set out in Table 1.

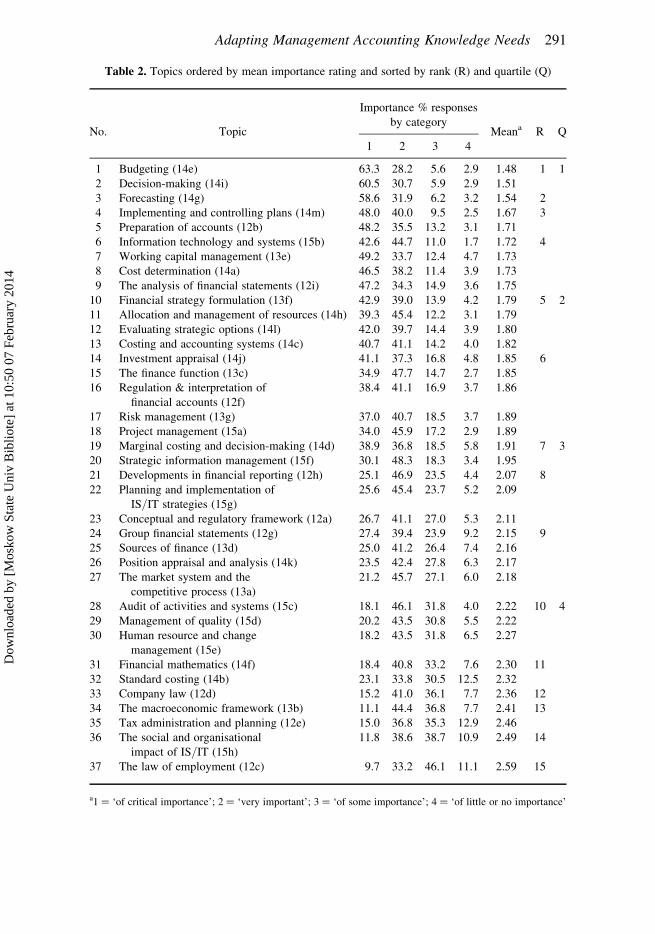

The frequencies of importance ratings are shown in Table 2, with topics ordered by their

mean rating. All topics other than the last are rated as at least ‘very important’ (category 2)

by at least half of the sample but discrimination by respondents is evident in that topics can

be sorted into 15 ranks according to significant differences among the mean ratings.3

While half of the topics in the upper two quartiles come from the Management Accounting

subject area, topics from all the other subject areas appear there, including more than half

of those from the Finance area. Among the Management Accounting topics themselves,

those associated with the earlier IFAC developmental stages, and particularly with the

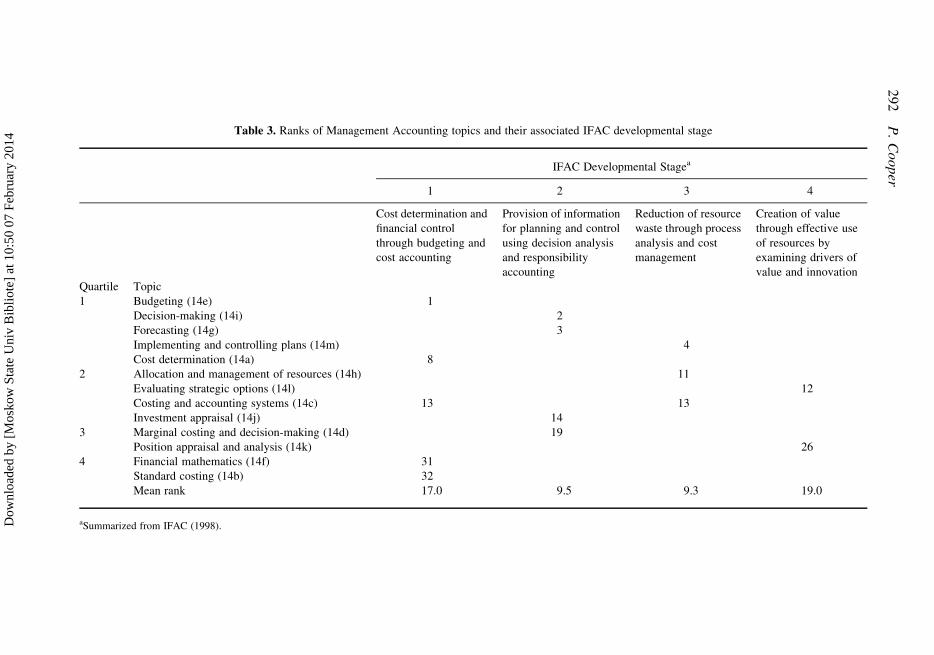

middle such stages, tend to be more highly ranked, as shown in Table 3.

Table 1. Sample characteristics

Country in which respondent works (COUNTRY)

Sector in which respondent works

(SECTOR) UKaOther high

income (OHI)

Non-high

income (NHI)

Not

disclosed Total

Manufacturing (MFG)a 207 93 64 1 365

Engineering, construction, extractive

industries, utilities and transport (EUT)

121 50 29 0 200

Services, non-financial (SER) 150 32 17 0 199

Financial services (FIN) 82 54 38 0 174

Information technology and

telecommunications (ITT)

119 36 11 1 167

Retail, trade and distribution (RTD) 79 42 24 0 145

Private practice/consulting (PPC) 100 25 16 2 143

Public sector (PUB) 89 15 3 0 107

Educators (EDU) 11 2 4 0 17

Other (principally NGOs) 47 9 14 0 70

Not disclosed 19 5 3 6 33

Total 1024 363 223 10 1620

Age of respondent (AGE)

Less than or equal to median 481 186 121 5 793

Greater than mediana 520 169 98 5 792

Not disclosed 23 8 4 0 35

Total 1024 363 223 10 1620

aReference group in regression analysis.

290 P. Cooper

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

Table 2. Topics ordered by mean importance rating and sorted by rank (R) and quartile (Q)

No. Topic

Importance % responses

by categoryMeana R Q

1 2 3 4

1 Budgeting (14e) 63.3 28.2 5.6 2.9 1.48 1 1

2 Decision-making (14i) 60.5 30.7 5.9 2.9 1.51

3 Forecasting (14g) 58.6 31.9 6.2 3.2 1.54 2

4 Implementing and controlling plans (14m) 48.0 40.0 9.5 2.5 1.67 3

5 Preparation of accounts (12b) 48.2 35.5 13.2 3.1 1.71

6 Information technology and systems (15b) 42.6 44.7 11.0 1.7 1.72 4

7 Working capital management (13e) 49.2 33.7 12.4 4.7 1.73

8 Cost determination (14a) 46.5 38.2 11.4 3.9 1.73

9 The analysis of financial statements (12i) 47.2 34.3 14.9 3.6 1.75

10 Financial strategy formulation (13f) 42.9 39.0 13.9 4.2 1.79 5 2

11 Allocation and management of resources (14h) 39.3 45.4 12.2 3.1 1.79

12 Evaluating strategic options (14l) 42.0 39.7 14.4 3.9 1.80

13 Costing and accounting systems (14c) 40.7 41.1 14.2 4.0 1.82

14 Investment appraisal (14j) 41.1 37.3 16.8 4.8 1.85 6

15 The finance function (13c) 34.9 47.7 14.7 2.7 1.85

16 Regulation & interpretation of

financial accounts (12f)

38.4 41.1 16.9 3.7 1.86

17 Risk management (13g) 37.0 40.7 18.5 3.7 1.89

18 Project management (15a) 34.0 45.9 17.2 2.9 1.89

19 Marginal costing and decision-making (14d) 38.9 36.8 18.5 5.8 1.91 7 3

20 Strategic information management (15f) 30.1 48.3 18.3 3.4 1.95

21 Developments in financial reporting (12h) 25.1 46.9 23.5 4.4 2.07 8

22 Planning and implementation of

IS/IT strategies (15g)

25.6 45.4 23.7 5.2 2.09

23 Conceptual and regulatory framework (12a) 26.7 41.1 27.0 5.3 2.11

24 Group financial statements (12g) 27.4 39.4 23.9 9.2 2.15 9

25 Sources of finance (13d) 25.0 41.2 26.4 7.4 2.16

26 Position appraisal and analysis (14k) 23.5 42.4 27.8 6.3 2.17

27 The market system and the

competitive process (13a)

21.2 45.7 27.1 6.0 2.18

28 Audit of activities and systems (15c) 18.1 46.1 31.8 4.0 2.22 10 4

29 Management of quality (15d) 20.2 43.5 30.8 5.5 2.22

30 Human resource and change

management (15e)

18.2 43.5 31.8 6.5 2.27

31 Financial mathematics (14f) 18.4 40.8 33.2 7.6 2.30 11

32 Standard costing (14b) 23.1 33.8 30.5 12.5 2.32

33 Company law (12d) 15.2 41.0 36.1 7.7 2.36 12

34 The macroeconomic framework (13b) 11.1 44.4 36.8 7.7 2.41 13

35 Tax administration and planning (12e) 15.0 36.8 35.3 12.9 2.46

36 The social and organisational

impact of IS/IT (15h)

11.8 38.6 38.7 10.9 2.49 14

37 The law of employment (12c) 9.7 33.2 46.1 11.1 2.59 15

a1 ¼ ‘of critical importance’; 2 ¼ ‘very important’; 3 ¼ ‘of some importance’; 4 ¼ ‘of little or no importance’

Adapting Management Accounting Knowledge Needs 291

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

Table 3. Ranks of Management Accounting topics and their associated IFAC developmental stage

IFAC Developmental Stagea

1 2 3 4

Cost determination and

financial control

through budgeting and

cost accounting

Provision of information

for planning and control

using decision analysis

and responsibility

accounting

Reduction of resource

waste through process

analysis and cost

management

Creation of value

through effective use

of resources by

examining drivers of

value and innovation

Quartile Topic

1 Budgeting (14e) 1

Decision-making (14i) 2

Forecasting (14g) 3

Implementing and controlling plans (14m) 4

Cost determination (14a) 8

2 Allocation and management of resources (14h) 11

Evaluating strategic options (14l) 12

Costing and accounting systems (14c) 13 13

Investment appraisal (14j) 14

3 Marginal costing and decision-making (14d) 19

Position appraisal and analysis (14k) 26

4 Financial mathematics (14f) 31

Standard costing (14b) 32

Mean rank 17.0 9.5 9.3 19.0

aSummarized from IFAC (1998).

292

P.

Cooper

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

To assess the influence of sectoral and international variation on topic ratings, respon-

dents are characterized using the variables shown in Table 1. The groups within SECTOR

represent comparable types of business plus the public sector and isolate manufacturing

(MFG) as the reference group to highlight the direction of change in knowledge needs

as the proportion of economic activity in this sector diminishes. The COUNTRY variable

represents the country where the respondent works according to its stage of economic

development within the World Bank’s (2005) classification of economies. This approach

yields two non-UK groups of reasonable size which can be compared to the UK as

the reference category with the expectation that any international variation is likely to

be marked between the UK and ‘non-high income’ (NHI) groups but less so between

the UK and ‘other high income’ (OHI) groups. Finally, to control for any impact of experi-

ence on perception, the AGE measure is included as a proxy in preference to ‘years since

qualification’ since CIMA members may qualify at various points in their career.

Variations in topic importance among the above groups are identified in ordered logistic

regressions (see, for example, Powers and Xie, 2000). The regression models are based on

a logistic cumulative density function for the probability of individual i choosing an

importance rating, ri, given J alternatives (with j ¼ 1, . . . , J 2 1) and a vector of the

individual’s characteristics (xi0), i.e. SECTOR, COUNTRY and AGE, such that:

p(ri � jjxi) ¼1

1þ e�(ajþx0ib)

where aj are constants and b the vector of coefficients on xi0. Thus, taking the logarithm of

the odds ratio as the dependent variable yields a linear regression model of the form:

lnp(ri � jjxi)

p(ri . jjxi)

� �¼ aj þ x0ib

so that, given the inverse scale of the ratings, a positive b coefficient for a characteristic

group indicates that its members tend to rate the topic as more important than do members

of the reference group and vice versa for negative coefficients.

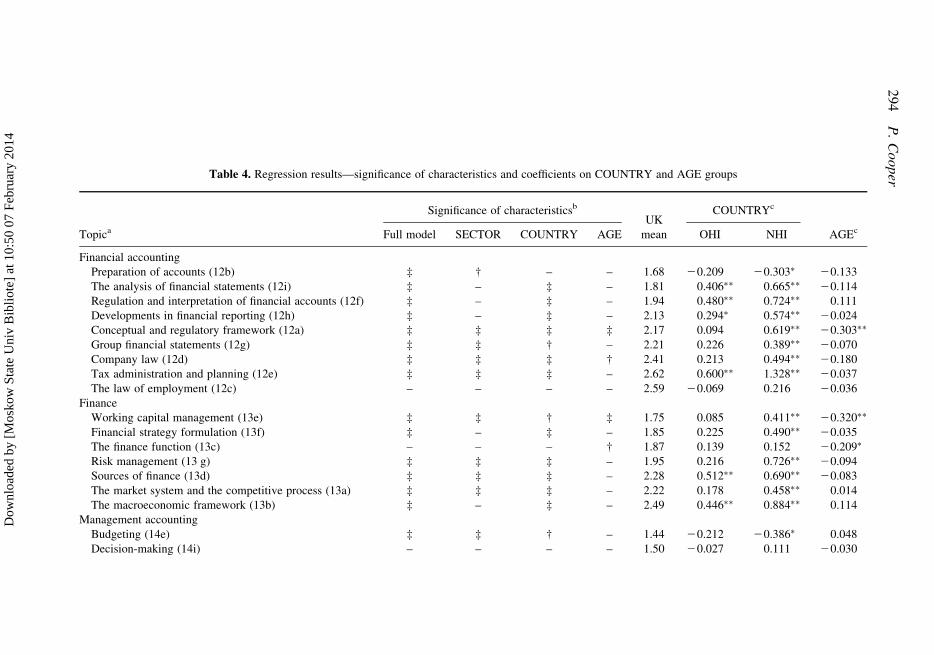

The significance of the model x2 statistics in Table 4 show that variation in at least

one of the characteristics significantly influences the importance rating for the majority

of topics, with SECTOR being associated with significant differences for slightly more

topics than COUNTRY. Coefficients for the characteristic groups, indicating the

sources of the variability relative to the respective reference groups, are also reported

for the COUNTRY and AGE groups in Table 4 and for the SECTOR groups in Table 5.4

As expected, international variation in topic importance compared to the UK group is

most pronounced for those in the NHI group. This is most apparent in more importance

being attributed to the Financial Accounting and Finance subject areas, and to the more

strategic Management Accounting topics. In contrast, differences between the UK and

OHI groups are relatively infrequent; the most significant being concerned with the

fundamentals of finance, tax and financial statement analysis, but there are no significant

differences between these groups for topics in the Management Accounting area.

Age group generally has no effect on perception of topic importance and specifically not

in the cases of budgeting and standard costing where Tan et al. (2004) found some differ-

ence in perception depending on experience.

Sectoral variation in topic importance is most widespread for the public sector group,

which tends to more highly rate Management topics, and less highly topics in other

Adapting Management Accounting Knowledge Needs 293

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

Table 4. Regression results—significance of characteristics and coefficients on COUNTRY and AGE groups

Significance of characteristicsb

UKCOUNTRYc

Topica Full model SECTOR COUNTRY AGE mean OHI NHI AGEc

Financial accounting

Preparation of accounts (12b) ‡ † – – 1.68 20.209 20.303� 20.133

The analysis of financial statements (12i) ‡ – ‡ – 1.81 0.406�� 0.665�� 20.114

Regulation and interpretation of financial accounts (12f) ‡ – ‡ – 1.94 0.480�� 0.724�� 0.111

Developments in financial reporting (12h) ‡ – ‡ – 2.13 0.294� 0.574�� 20.024

Conceptual and regulatory framework (12a) ‡ ‡ ‡ ‡ 2.17 0.094 0.619�� 20.303��

Group financial statements (12g) ‡ ‡ † – 2.21 0.226 0.389�� 20.070

Company law (12d) ‡ ‡ ‡ † 2.41 0.213 0.494�� 20.180

Tax administration and planning (12e) ‡ ‡ ‡ – 2.62 0.600�� 1.328�� 20.037

The law of employment (12c) – – – – 2.59 20.069 0.216 20.036

Finance

Working capital management (13e) ‡ ‡ † ‡ 1.75 0.085 0.411�� 20.320��

Financial strategy formulation (13f) ‡ – ‡ – 1.85 0.225 0.490�� 20.035

The finance function (13c) – – – † 1.87 0.139 0.152 20.209�

Risk management (13 g) ‡ ‡ ‡ – 1.95 0.216 0.726�� 20.094

Sources of finance (13d) ‡ ‡ ‡ – 2.28 0.512�� 0.690�� 20.083

The market system and the competitive process (13a) ‡ ‡ ‡ – 2.22 0.178 0.458�� 0.014

The macroeconomic framework (13b) ‡ – ‡ – 2.49 0.446�� 0.884�� 0.114

Management accounting

Budgeting (14e) ‡ ‡ † – 1.44 20.212 20.386� 0.048

Decision-making (14i) – – – – 1.50 20.027 0.111 20.030

294

P.

Cooper

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

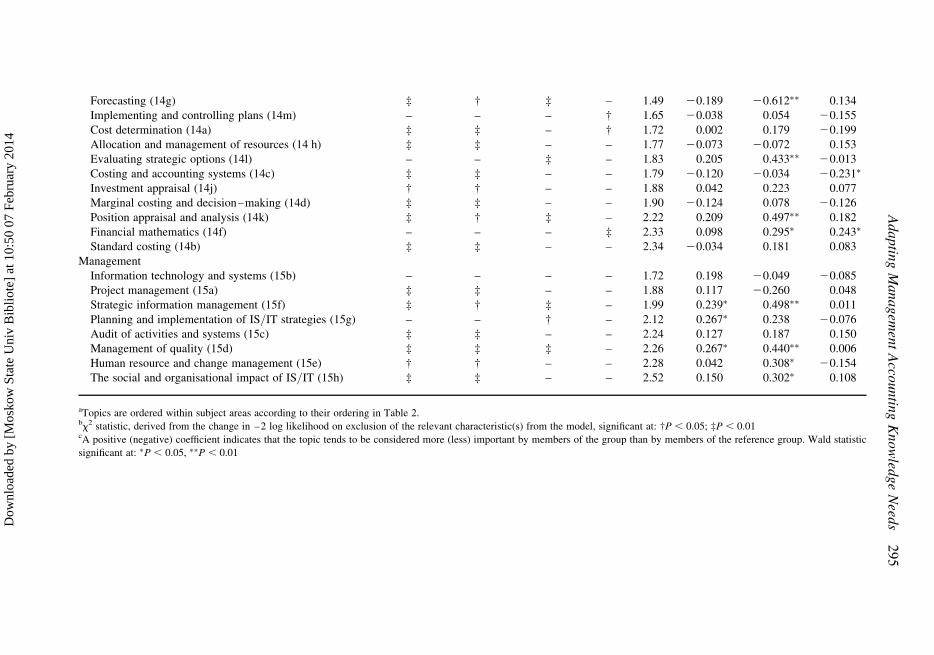

Forecasting (14g) ‡ † ‡ – 1.49 20.189 20.612�� 0.134

Implementing and controlling plans (14m) – – – † 1.65 20.038 0.054 20.155

Cost determination (14a) ‡ ‡ – † 1.72 0.002 0.179 20.199

Allocation and management of resources (14 h) ‡ ‡ – – 1.77 20.073 20.072 0.153

Evaluating strategic options (14l) – – ‡ – 1.83 0.205 0.433�� 20.013

Costing and accounting systems (14c) ‡ ‡ – – 1.79 20.120 20.034 20.231�

Investment appraisal (14j) † † – – 1.88 0.042 0.223 0.077

Marginal costing and decision–making (14d) ‡ ‡ – – 1.90 20.124 0.078 20.126

Position appraisal and analysis (14k) ‡ † ‡ – 2.22 0.209 0.497�� 0.182

Financial mathematics (14f) – – – ‡ 2.33 0.098 0.295� 0.243�

Standard costing (14b) ‡ ‡ – – 2.34 20.034 0.181 0.083

Management

Information technology and systems (15b) – – – – 1.72 0.198 20.049 20.085

Project management (15a) ‡ ‡ – – 1.88 0.117 20.260 0.048

Strategic information management (15f) ‡ † ‡ – 1.99 0.239� 0.498�� 0.011

Planning and implementation of IS/IT strategies (15g) – – † – 2.12 0.267� 0.238 20.076

Audit of activities and systems (15c) ‡ ‡ – – 2.24 0.127 0.187 0.150

Management of quality (15d) ‡ ‡ ‡ – 2.26 0.267� 0.440�� 0.006

Human resource and change management (15e) † † – – 2.28 0.042 0.308� 20.154

The social and organisational impact of IS/IT (15h) ‡ ‡ – – 2.52 0.150 0.302� 0.108

aTopics are ordered within subject areas according to their ordering in Table 2.bx2 statistic, derived from the change in –2 log likelihood on exclusion of the relevant characteristic(s) from the model, significant at: †P , 0.05; ‡P , 0.01cA positive (negative) coefficient indicates that the topic tends to be considered more (less) important by members of the group than by members of the reference group. Wald statistic

significant at: �P , 0.05, ��P , 0.01

Adaptin

gM

anagem

ent

Acco

untin

gK

now

ledge

Need

s295

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

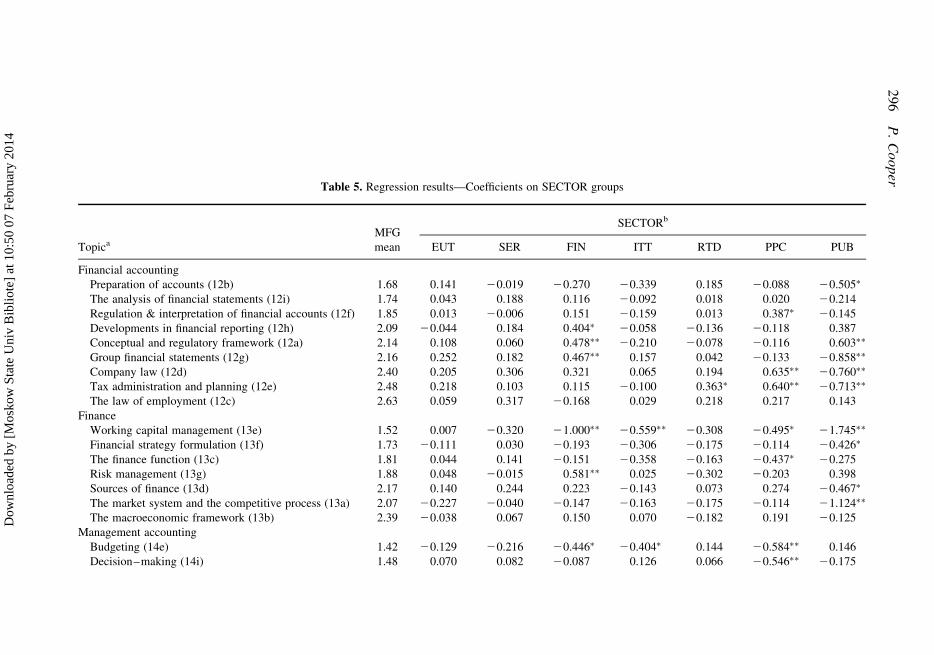

Table 5. Regression results—Coefficients on SECTOR groups

MFGSECTORb

Topica mean EUT SER FIN ITT RTD PPC PUB

Financial accounting

Preparation of accounts (12b) 1.68 0.141 20.019 20.270 20.339 0.185 20.088 20.505�

The analysis of financial statements (12i) 1.74 0.043 0.188 0.116 20.092 0.018 0.020 20.214

Regulation & interpretation of financial accounts (12f) 1.85 0.013 20.006 0.151 20.159 0.013 0.387� 20.145

Developments in financial reporting (12h) 2.09 20.044 0.184 0.404� 20.058 20.136 20.118 0.387

Conceptual and regulatory framework (12a) 2.14 0.108 0.060 0.478�� 20.210 20.078 20.116 0.603��

Group financial statements (12g) 2.16 0.252 0.182 0.467�� 0.157 0.042 20.133 20.858��

Company law (12d) 2.40 0.205 0.306 0.321 0.065 0.194 0.635�� 20.760��

Tax administration and planning (12e) 2.48 0.218 0.103 0.115 20.100 0.363� 0.640�� 20.713��

The law of employment (12c) 2.63 0.059 0.317 20.168 0.029 0.218 0.217 0.143

Finance

Working capital management (13e) 1.52 0.007 20.320 21.000�� 20.559�� 20.308 20.495� 21.745��

Financial strategy formulation (13f) 1.73 20.111 0.030 20.193 20.306 20.175 20.114 20.426�

The finance function (13c) 1.81 0.044 0.141 20.151 20.358 20.163 20.437� 20.275

Risk management (13g) 1.88 0.048 20.015 0.581�� 0.025 20.302 20.203 0.398

Sources of finance (13d) 2.17 0.140 0.244 0.223 20.143 0.073 0.274 20.467�

The market system and the competitive process (13a) 2.07 20.227 20.040 20.147 20.163 20.175 20.114 21.124��

The macroeconomic framework (13b) 2.39 20.038 0.067 0.150 0.070 20.182 0.191 20.125

Management accounting

Budgeting (14e) 1.42 20.129 20.216 20.446� 20.404� 0.144 20.584�� 0.146

Decision–making (14i) 1.48 0.070 0.082 20.087 0.126 0.066 20.546�� 20.175

296

P.

Cooper

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

Forecasting (14g) 1.54 0.260 0.304 20.016 20.156 0.160 20.413� 20.334

Implementing and controlling plans (14m) 1.60 20.198 0.100 20.328 20.196 0.008 20.321 20.139

Cost determination (14a) 1.52 20.414� 20.461�� 21.011�� 20.669�� 20.716�� 20.935�� 20.828��

Allocation and management of resources (14h) 1.82 0.236 0.341� 0.250 0.066 0.062 20.393� 0.678��

Evaluating strategic options (14l) 1.75 20.242 20.012 20.131 20.067 20.078 20.131 20.124

Costing and accounting systems (14c) 1.58 20.375� 20.588�� 21.404�� 20.696�� 20.833�� 20.936�� 20.671��

Investment appraisal (14j) 1.79 20.071 20.098 20.030 0.056 0.092 20.424� 20.650��

Marginal costing and decision–making (14d) 1.65 20.644�� 20.480�� 21.246�� 20.514�� 20.800�� 20.996�� 20.956��

Position appraisal and analysis (14 k) 2.12 20.264 0.016 0.228 0.010 0.144 20.273 20.552��

Financial mathematics (14f) 2.26 20.105 20.045 0.187 20.097 0.066 20.160 20.137

Standard costing (14b) 1.83 21.066�� 21.282�� 21.712�� 21.117�� 21.065�� 21.491�� 21.325��

Management

Information technology and systems (15b) 1.77 0.120 0.309 0.339 0.190 20.080 0.154 0.612��

Project management (15a) 2.00 0.679�� 0.330� 0.384� 0.339 0.150 0.250 0.713��

Strategic information management (15f) 1.99 20.033 0.301 0.315 0.369� 20.154 0.093 0.530�

Planning and implementation of IS/IT strategies (15g) 2.12 0.080 0.257 0.224 0.237 20.163 20.077 0.453�

Audit of activities and systems (15c) 2.26 0.223 0.104 0.174 20.034 0.131 20.266 0.836��

Management of quality (15d) 2.25 0.200 0.180 0.332 0.203 20.071 20.390� 0.621��

Human resource and change management (15e) 2.33 0.167 0.401� 0.121 0.013 0.058 20.022 0.630��

The social and organisational impact of 2.62 0.201 0.382� 0.576�� 0.652�� 0.156 0.219 0.923��

IS/IT (15h)

a,b See Table 4 notes a and c respectively.

Adaptin

gM

anagem

ent

Acco

untin

gK

now

ledge

Need

s297

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

areas. Most other instances of significant variation are topic and group specific, e.g. the

financial services group ascribes more importance to the advanced areas of financial

accounting and to risk management, but less to working capital management and

budgeting, which is consistent with intuition. However, the manufacturing group differs

significantly from all other groups in terms of the four topics connected with costing.

Discussion and Conclusions

The high importance attached to virtually the full range of topics included in the survey

indicates that practitioners possess a much more widely based set of knowledge needs

than might be envisaged in a strict conception of the management accounting curriculum.

Some of the more highly rated topics outside this area, such as in financial accounting,

may be seen as essential to operationalizing management accounting knowledge.

However, the high ranking of others supports the idea of a functional change for the man-

agement accountant, with more emphasis on financial, risk and project management as

well as some strategic topics such as evaluating strategic options.

While topics outside the Management Accounting area are seen as being of significant

importance, the rankings in Table 2 demonstrate that it is those from within this area that

are of the highest importance. Furthermore, the relative rankings of those topics (Table 3)

indicates that topics associated with the later IFAC developmental stages have not fully

supplanted those associated with earlier ones. Therefore, the impact of the changing

role may be characterised as a cumulative broadening of knowledge needs, with the

well-established management accounting topics such as budgeting remaining at the core.

The sources of variation in practice suggested by IFAC (1998) are indeed reflected in

differences in knowledge needs. However, the variations across the sectoral and country

groups (Tables 4 and 5) indicate specific areas of diversity rather than radically different

priorities, except in the case of the public sector (and, to some extent, private practice/con-

sulting). The specific areas of difference have implications for curriculum design depend-

ing on the constitution of the target audience, or indicate the courses that particular groups

of students would be well advised to pursue, but there are some discernible patterns in the

results with potentially wider ramifications. First, costing topics are seen as more import-

ant by those in manufacturing, consistent with the previous findings of Tan et al. (2004)

and Khan et al. (2000), but the current results demonstrate that the distinction extends

beyond services to a range of other sectors. This is not to say that such topics are

viewed as being unimportant outside manufacturing (see Table 2), rather that those in

the manufacturing sector require a greater emphasis on this area. Second, those working

in less developed economies tend to attach greater importance to subject areas outside

Management Accounting and to the more strategic topics within it. This could reflect

respondents in such economies tending to work in smaller organisations where the

management accountant is required to fulfil a broader range of roles, with a concomitant

effect on knowledge needs.

The limited influence of respondents’ age or experience on perceptions of topic import-

ance and the inconsistency between this and other studies in terms of which topics are

apparently so influenced suggest that this characteristic has little, if any, role to play in

understanding perceptions of knowledge needs.

In summary, the results confirm the need for management accounting to be taught as

part of a broad-based curriculum, particularly for students who are preparing for a

career in this field, and highlight areas where courses could be adapted or the broader cur-

riculum designed to accommodate needs for practice, e.g. for students aiming to work in a

particular sector or in an economy at a different stage of development. At the level of an

298 P. Cooper

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

internationally-recognized professional qualification with a standard content, the results

provide some comfort that a single curriculum can meet at least the basic needs of accoun-

tants working in a range of places and operational environments but highlight areas where

students may require post-qualification development to meet specific needs. Notably,

those whose destinations lie in the public sector or in a non-high income economy may

need particular support in this respect.

Future studies will be needed to monitor the position for the effects of further functional

change, with the possibility of shifts in emphasis towards the later IFAC developmental

stages, and more profound structural economic developments (such as those described

by Chua and Baxter, 2000). At the very least, it will be of interest to determine whether

diversity diminishes with further globalisation and whether the development of the

‘new economy’ introduces a countervailing pressure towards more diversity based on sec-

toral variation. Such studies should also consider knowledge needs at a more detailed level

as well as other educational issues such as skill needs and assessment.

In the meantime, this study provides a contemporary insight into the thinking of a broad

sample of practising management accountants, yielding evidence of diversity in knowl-

edge needs rather than the confusion among management accountants indicated by

Boer (2000). The detailed results should also be of use to educators in meeting the

needs of their students.

Acknowledgements

The author is grateful to CIMA for access to data from its survey, which was designed by

Ian Crawford, Richard Fairchild and Steven McGuire at the University of Bath. Comments

on an earlier version of the paper by participants at the British Accounting Association’s

Special Interest Group on Accounting Education Annual Conference in May 2005 and,

subsequently, by the conference chairman, Neil Marriott, are gratefully acknowledged,

as are comments by three anonymous referees.

Notes

1Boer (2000) notes the relevance of this issue to accounting education in the US context.2In common with previous studies, the focus on practitioners disregards the views of users of accounting

information who are not themselves practitioners. This user perspective may be a fruitful area for further

research since it would provide educators with an alternative view of the relative importance of knowledge

needs and potentially define new ones (for example, through identifying limitations in the capacity of

practitioners to meet certain organisational needs which practitioners do not perceive).3The topics are consecutively assigned to ranks according to whether their mean score is significantly

different (at P , 0.01) from that of the top scoring topic in each rank according to the Wilcoxon Signed

Ranks Test. For example, the mean score for topic 6 is significantly different on this basis from that for

topic 4 so a new rank commences with topic 6. The mean scores of topics 7 to 9 are not significantly different

from that of topic 6 and so are assigned the same rank as that topic.4The ‘Other’ sectoral group is excluded from the analysis of variation given the diversity of its membership.

Coefficients for the educators group are not reported in Table 5 since none is significantly different from

those of the manufacturing group.

References

Boer, G. B. (2000) Management accounting education: yesterday, today and tomorrow, Issues in Accounting

Education, 15(2), pp. 313–333.

Chua, W. F. and Baxter, J. (2000) Management accounting—beyond 2000, Pacific Accounting Review, 11(2),

pp. 54–65.

CIMA (2000) The Syllabus (London: Chartered Institute of Management Accountants).

Adapting Management Accounting Knowledge Needs 299

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014

Deakin, E. B. and Summers, E. J. (1975) A survey of curriculum topics relevant to the practice of management

accounting, The Accounting Review, 50(2), pp. 380–383.

DEST (2004) International Higher Education Students: How do They Differ from Other Higher Education

Students? Research Note No.2, Strategic Analysis and Evaluation Group, Higher Education Analysis

Section (Canberra: Department of Education, Science and Training, Australian Government).

Dugdale, D. (1994) Theory and practice: the views of CIMA members and students, Management Accounting,

72(8), pp. 56–59.

Edwards, K. and Emmanuel, C. R. (1990) Diverging views on the boundaries of management accounting,

Management Accounting Research, 1(1), pp. 51–63.

Harman, G. (2004) New directions in internationalizing higher education: Australia’s development as an exporter

of higher education services, Higher Education Policy, 17(1), pp. 101–120.

HESA (2004) Students in Higher Education Institutions 2002/03 (Cheltenham: Higher Education Statistics

Agency).

HESA (1999) Students in Higher Education Institutions 1997/98 (Cheltenham: Higher Education Statistics

Agency).

IFAC (1998) Management Accounting Concepts, International Management Accounting Practice Statement 1

(New York: International Federation of Accountants).

IFAC (2002) Competency Profiles for Management Accounting Practice and Practitioners. Study 12, Financial

and Management Accounting Committee (New York: International Federation of Accountants).

IIE (2003) Open Doors 2003: International Students in the US (New York: Institute of International Education).

Kaplan, R. S. (1995) New roles for management accountants, Journal of Cost Management, 9(3), pp. 6–13.

Khan, Z. U. et al. (2000) A plan for reengineering management accounting education based on the IMA’s practice

analysis, Management Accounting Quarterly, 1(2), pp. 1–6.

Lander, G. R. and Reinstein, A. (1987) Identifying a common body of knowledge for management accounting,

Issues in Accounting Education, 2(2), pp. 264–280.

Maskell, B. and Baggaley, B. (2000) The future of management accounting, Journal of Cost Management, 14(5),

pp. 24–27.

Novin, A. M. (1997) Education for careers in management accounting, auditing, and tax: a comparison, Journal

of Education for Business, 73(1), pp. 29–34.

Novin, A. M. et al. (1990) Improving the curriculum for aspiring management accountants: the practitioner’s

point of view, Journal of Accounting Education, 8(2), pp. 207–224.

ONS (2004) United Kingdom Input-Output Analyses, 2004 Edition (London: Office for National Statistics).

Powers, D. A. and Xie, Y. (2000) Statistical Methods for Categorical Data Analysis (San Diego, CA: Academic

Press).

Tan, L. M. et al. (2004) Management accounting curricula: striking a balance between the views of educators and

practitioners, Accounting Education: an international journal, 13(1), pp. 51–67.

Van den Brink, H. et al. (2003) Teaching management accounting in a competencies-based fashion, Accounting

Education: an international journal, 12(3), pp. 245–259.

World Bank (2005) World Development Indicators 2005 (Washington, DC: World Bank).

Yuskavage, R. E. and Pho, Y. H. (2004) Gross domestic product by industry for 1987–2000: new estimates on the

North American Industry Classification System, Survey of Current Business (Bureau of Economic Analysis),

84(11), pp. 33–53.

300 P. Cooper

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

10:

50 0

7 Fe

brua

ry 2

014