actuaries and the regulatory environment role of the...

TRANSCRIPT

1

Actuaries and the Regulatory Environment Role of the Actuary in the Solvency II framework

IAA Fund Southeast Europe Actuarial Seminar, Zagreb, 3 October 2011

2

Solvency II – primary objectives

fundamental review of EU prudential framework enhanced policyholder protection deepening the single market improved competitiveness of the insurance industry better and more effective regulation creation of a new single legislative basis

3

Solvency II – further objectives

a framework based more on risk exposure incentives for companies to manage risks better increased harmonisation /convergence in EU convergence of financial sectors (e.g. with banks) international harmonisation (IAIS/IASB)

4

Solvency II – Lamfalussy process

new process for financial services legislation Level 1

– principles-based Directive Level 2

– implementing measures Level 3

– convergent implementation by national authorities Level 4

– rigorous enforcement by Commission

5

Solvency II – general principles

risk-based approach total balance sheet assessment Basel II “3 pillars” structure

– 1st pillar: quantitative requirements (technical provisions and capital requirements)

– 2nd pillar: supervisory review process (including supervision of groups)

– 3rd pillar: market discipline (public disclosure)

6

technical provisions (based on expected IFRS4) best estimate plus risk margin market consistent valuation life:

‘risk-free’ market rate for discounting valuing embedded options/guarantees

non-life: discounted technical provisions quantitative benchmarks from market data

Solvency II – Pillar I

7

clarify the role of capital requirements: to provide good security for policyholders but more consistent with economic capital Solvency Capital Requirement (SCR) generic risk-based approach safety net Minimum Capital Requirement use of internal models encouraged incentive of reduced capital requirements …for properly measuring and managing risks

Solvency II – Pillar I

8

Solvency II – Pillar 2

internal control and risk management – develop internal control principles – principles for sound risk management – undertakings should draw up plans for:

• investment policy • asset-liability matching • reinsurance programme • treating policyholders fairly

– risk management function must be established – Own Risk and Solvency Assessment (ORSA – Art.45)

9

Solvency II – Current status

Directive 2009/138/EC of the European Parliament and the Council on the taking-up and pursuit of the business of insurance and reinsurance

Level 2 measures being drafted EIOPA established in 2011 EIOPA considering Level 3 measures including guidelines for actuarial function

aim is “sufficiently high degree of harmonisation” Omnibus Directive in European Parliament

10

risk management function

actuarial function

internal auditing function

internal control function

compliance function

New rules of governance

11

Solvency II article 48 : the actuarial function

1) Insurance and reinsurance undertakings shall provide for an effective actuarial function to undertake the following:

a) To coordinate the calculation of technical provisions; b) To ensure the appropriateness of the methodologies and underlying

models used as well as the assumptions made in the calculation of technical provisions;

c) To assess the sufficiency and quality of the data used in the calculation of technical provisions;

d) To compare best estimates against experience; e) To inform the administrative or management body of the reliability and

adequacy of the calculation of technical provisions; f) To oversee the calculation of technical provisions in the cases set out in

Article 81;

12

Solvency II article 48 : the actuarial function

1) Insurance and reinsurance undertakings shall provide for an effective actuarial function to undertake the following:

g) To express an opinion on the overall underwriting policy; h) To express an opinion on the adequacy of reinsurance arrangements; i) To contribute to the effective implementation of the risk management

system referred to in Article 43, in particular with respect to the risk modelling underlying the calculation of the capital requirements set out in Chapter VI, Sections 4 and 5 and the assessment referred to in Article 44.

13

Article 48 (2) of Solvency II Directive

2) The actuarial function shall be carried out by persons who have knowledge of actuarial and financial mathematics, commensurate with the nature, scale and complexity of the risks inherent in the business of the insurance or reinsurance undertaking, and who are able to demonstrate their relevant experience with applicable professional and other standards.

14

actuarial function has a central place in the governance all insurers required to have an actuarial function life insurers general insurers health insurers reinsurers

actuarial function need not be carried out by actuaries no mention of professional qualifications or membership ‘proportionality’ will be invoked by some regulators but ‘fit and proper’ requirements do apply

Key points about the actuarial function

15

On the threshold?

16

is the actuarial function a step forward?

…or a step backward?

will the actuarial function be carried out by non-actuaries?

will actuaries perform other functions and roles?

no certifying role envisaged for actuarial function

So what really is the role of the actuary?

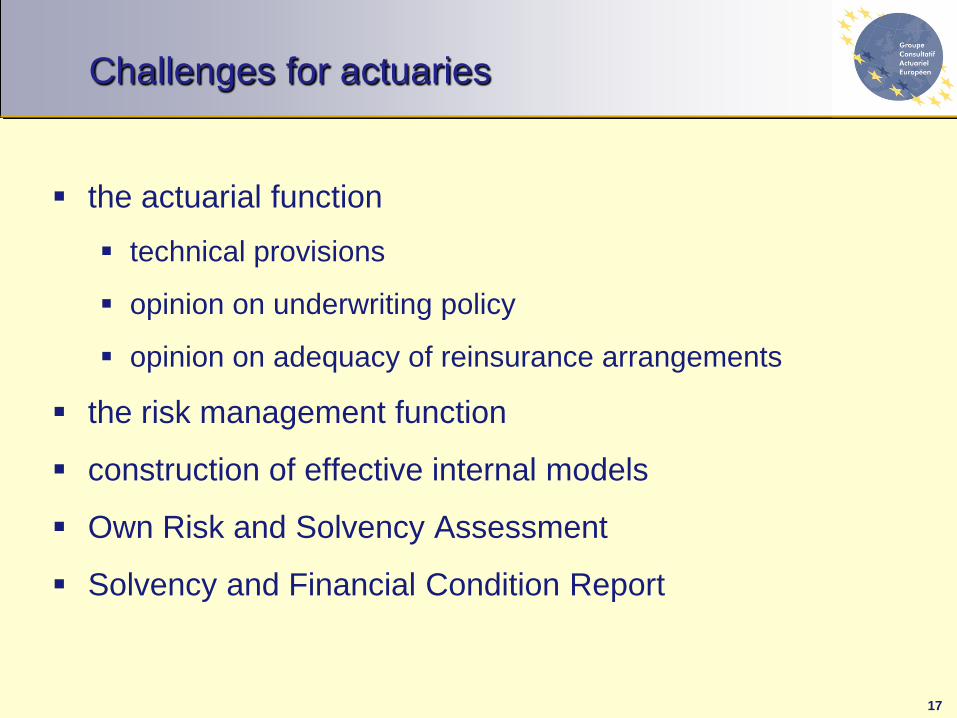

17

the actuarial function

technical provisions

opinion on underwriting policy

opinion on adequacy of reinsurance arrangements

the risk management function

construction of effective internal models

Own Risk and Solvency Assessment

Solvency and Financial Condition Report

Challenges for actuaries

18 18

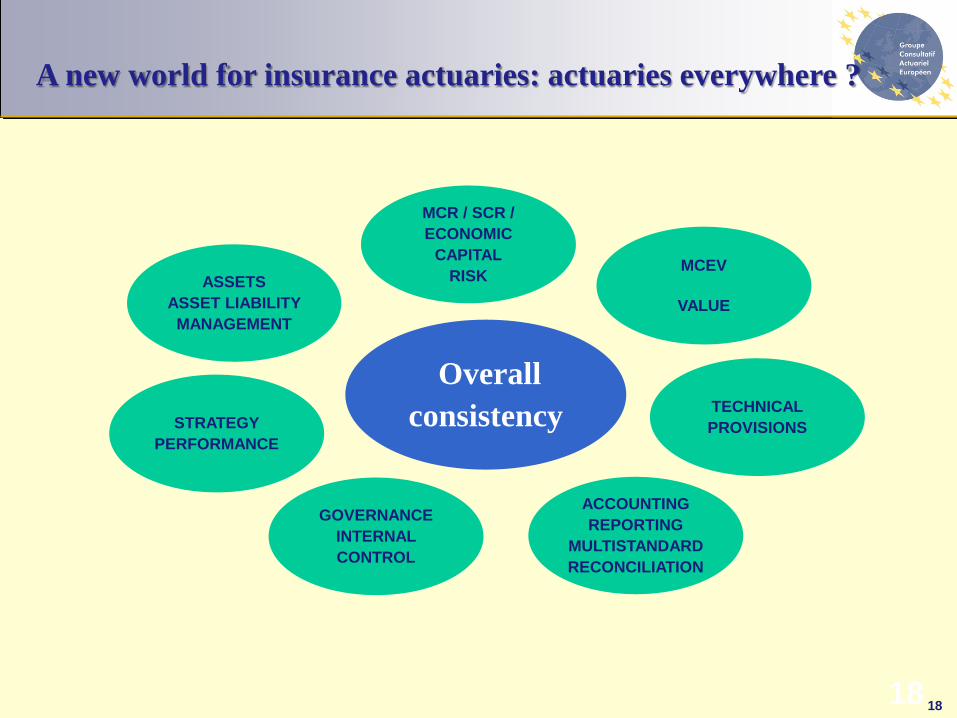

TECHNICAL PROVISIONS

Overall consistency

MCR / SCR / ECONOMIC

CAPITAL RISK

STRATEGY PERFORMANCE

GOVERNANCE INTERNAL CONTROL

ACCOUNTING REPORTING

MULTISTANDARD RECONCILIATION

ASSETS ASSET LIABILITY

MANAGEMENT

MCEV

VALUE

A new world for insurance actuaries: actuaries everywhere ?

19

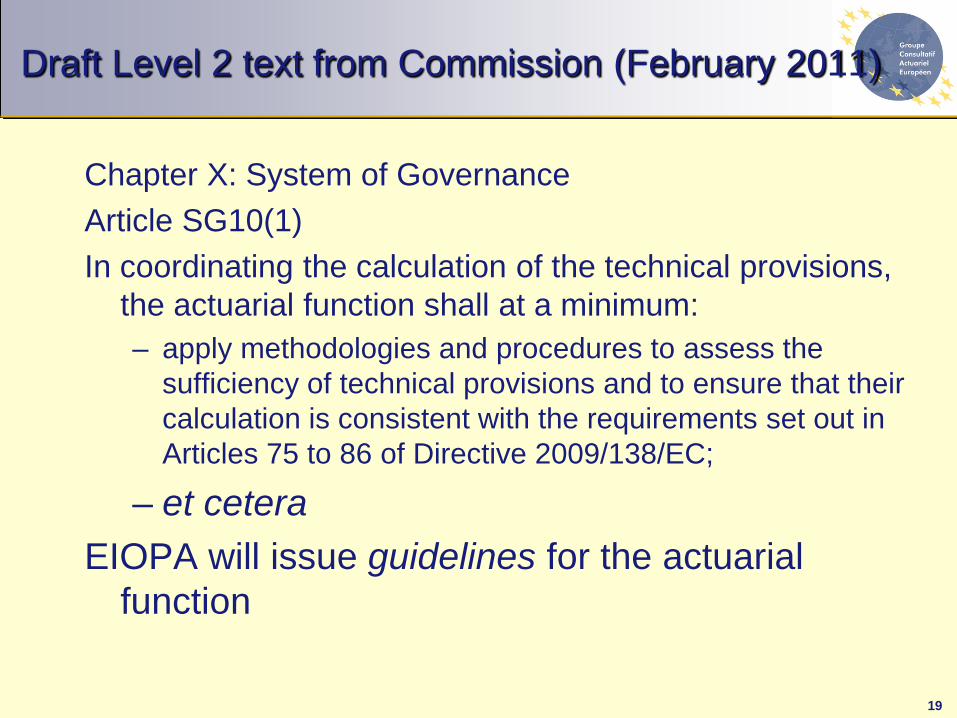

Draft Level 2 text from Commission (February 2011)

Chapter X: System of Governance Article SG10(1) In coordinating the calculation of the technical provisions,

the actuarial function shall at a minimum: – apply methodologies and procedures to assess the

sufficiency of technical provisions and to ensure that their calculation is consistent with the requirements set out in Articles 75 to 86 of Directive 2009/138/EC;

– et cetera EIOPA will issue guidelines for the actuarial

function

20

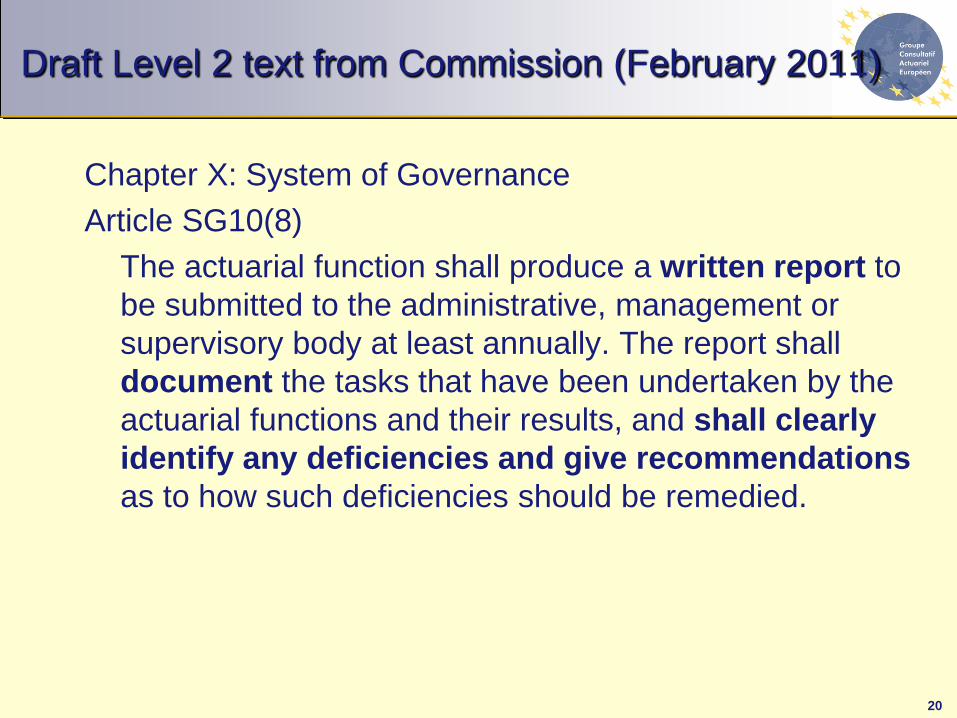

Draft Level 2 text from Commission (February 2011)

Chapter X: System of Governance Article SG10(8) The actuarial function shall produce a written report to

be submitted to the administrative, management or supervisory body at least annually. The report shall document the tasks that have been undertaken by the actuarial functions and their results, and shall clearly identify any deficiencies and give recommendations as to how such deficiencies should be remedied.

21

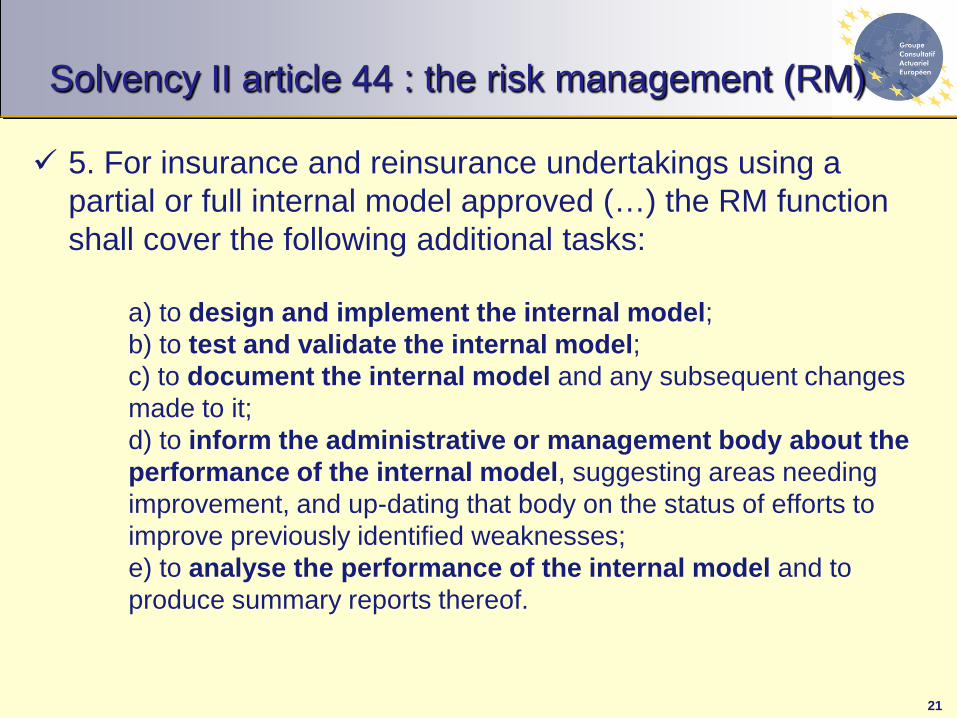

5. For insurance and reinsurance undertakings using a partial or full internal model approved (…) the RM function shall cover the following additional tasks:

a) to design and implement the internal model; b) to test and validate the internal model; c) to document the internal model and any subsequent changes made to it; d) to inform the administrative or management body about the performance of the internal model, suggesting areas needing improvement, and up-dating that body on the status of efforts to improve previously identified weaknesses; e) to analyse the performance of the internal model and to produce summary reports thereof.

Solvency II article 44 : the risk management (RM)

22

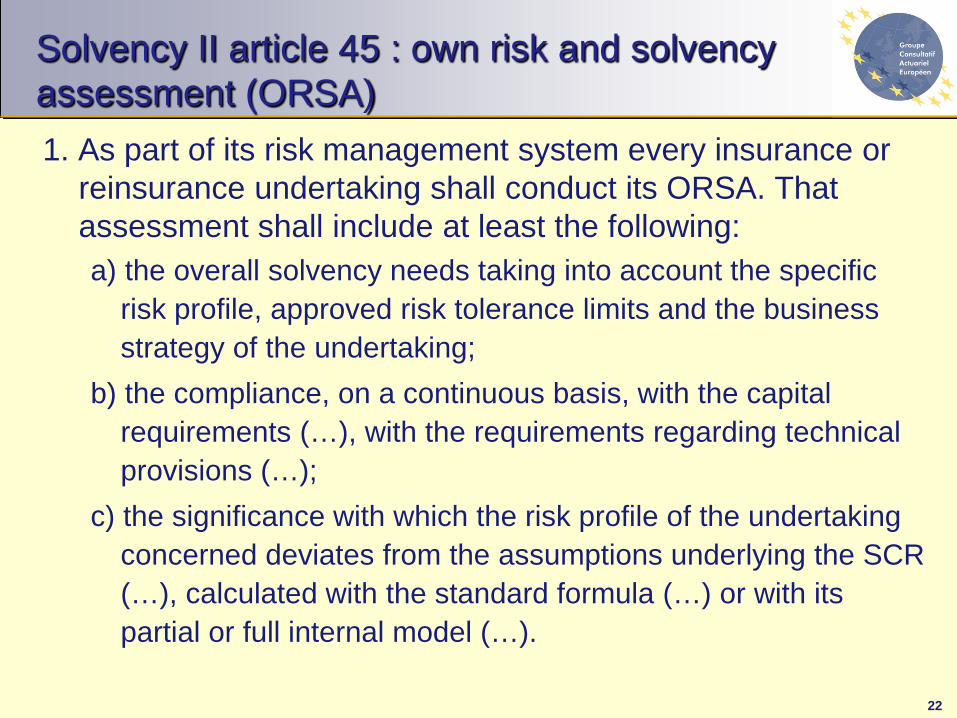

1. As part of its risk management system every insurance or reinsurance undertaking shall conduct its ORSA. That assessment shall include at least the following: a) the overall solvency needs taking into account the specific

risk profile, approved risk tolerance limits and the business strategy of the undertaking;

b) the compliance, on a continuous basis, with the capital requirements (…), with the requirements regarding technical provisions (…);

c) the significance with which the risk profile of the undertaking concerned deviates from the assumptions underlying the SCR (…), calculated with the standard formula (…) or with its partial or full internal model (…).

Solvency II article 45 : own risk and solvency assessment (ORSA)

23

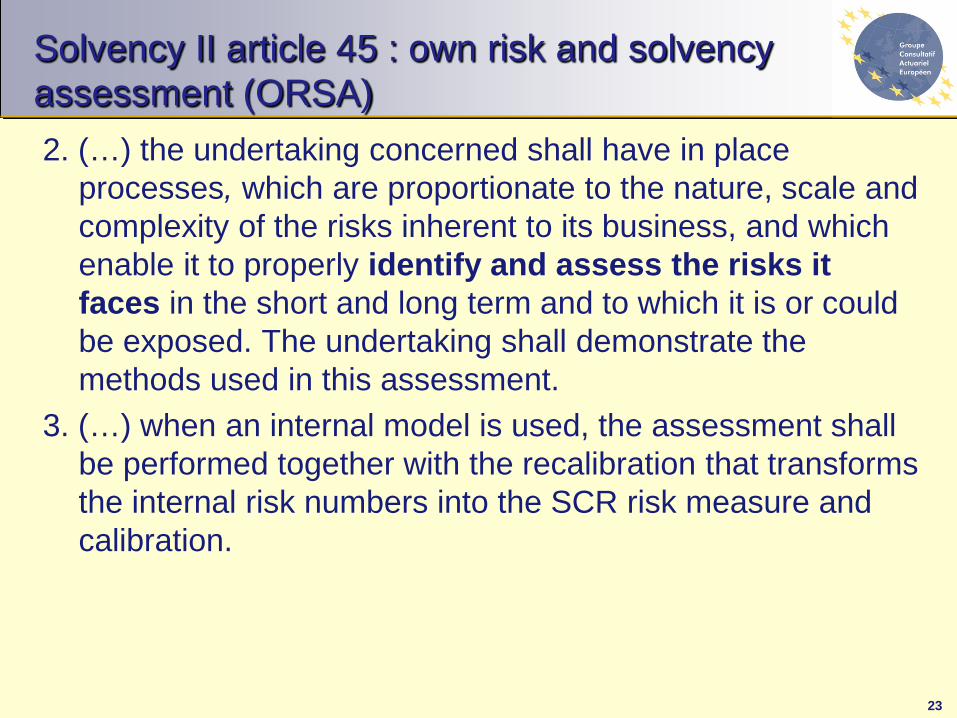

2. (…) the undertaking concerned shall have in place processes, which are proportionate to the nature, scale and complexity of the risks inherent to its business, and which enable it to properly identify and assess the risks it faces in the short and long term and to which it is or could be exposed. The undertaking shall demonstrate the methods used in this assessment.

3. (…) when an internal model is used, the assessment shall be performed together with the recalibration that transforms the internal risk numbers into the SCR risk measure and calibration.

Solvency II article 45 : own risk and solvency assessment (ORSA)

24

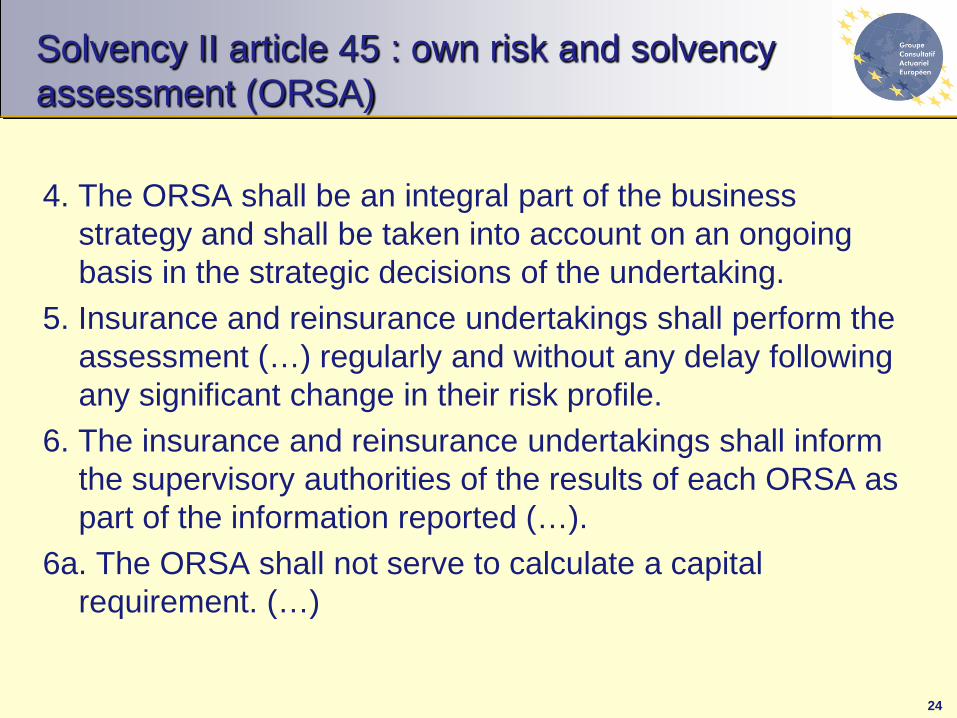

4. The ORSA shall be an integral part of the business

strategy and shall be taken into account on an ongoing basis in the strategic decisions of the undertaking.

5. Insurance and reinsurance undertakings shall perform the assessment (…) regularly and without any delay following any significant change in their risk profile.

6. The insurance and reinsurance undertakings shall inform the supervisory authorities of the results of each ORSA as part of the information reported (…).

6a. The ORSA shall not serve to calculate a capital requirement. (…)

Solvency II article 45 : own risk and solvency assessment (ORSA)

25

technical roles

oversight roles

reporting roles

provision of opinions

advisory roles

reviewing roles

certifying roles

roles going beyond requirements of Solvency II

Summary – different actuarial roles

26

technical roles – assessing the sufficiency and quality of data – ensuring the appropriateness of methodologies/models – ensuring appropriateness of assumptions – calculation of technical provisions – comparing best estimates against experience – development of internal capital models – carrying out calculations for ORSA – asset-liability modelling – evaluating risk mitigation techniques

Summary – technical roles

27

oversight roles – coordinate the calculation of the technical provisions – oversee the calculation of the technical provisions – oversee the preparation of the ORSA (for RM function)

Summary – oversight roles

28

reporting roles – written report to AMSB documenting tasks undertaken by

AF and their results, identifying any deficiencies, with recommendations for remedies

– report an overview of activities undertaken by AF, describing how AF contributes to effective implementation of risk management system

Summary – reporting roles

29

provision of opinions – overall underwriting policy – sufficiency of premiums – impact of options and guarantees – impact of various factors on underwriting policy – impact of anti-selection – adequacy of reinsurance arrangements, including other

instruments of risk mitigation such as SPVs

Summary – provision of opinions

30

advisory roles – advice arising from actuarial function roles – advice on integration of risk models into operations – advice on impact of internal model results – advice on policy options arising from ORSA

Summary – advisory roles

31

Reviewing roles

32

reviewing roles – independent review of actuarial function activities – objective review of Solvency and Financial Condition Report

(SFCR) – objective review of the Report to Supervisor (RTS) – objective review of Quantitative Reporting Templates (QRT) – validation of internal models – advice to external auditor as reviewing actuary

Summary – reviewing roles

33

certifying roles

– formal sign off of Solvency and Financial Condition Report

Summary – certifying roles

34

roles going beyond requirements of Solvency II – treating customers fairly – product design and pricing – distribution of surplus and advice on bonuses – equity between groups of policyholders – market-consistent embedded value (MCEV) – financial reporting in accordance with IFRS4(revised)

Summary – roles beyond Solvency II

35

coverage and detailed content of basic education requirements for Continuing Professional Development code of professional conduct rigorous enforcement through disciplinary scheme actuaries can readily demonstrate ‘fit and proper’ expertise in risk management and internal models actuarial standards of practice (models from GC) EU wide consistency through Groupe Consultatif

Why use actuaries?

36