accounts receivable program

DESCRIPTION

Audit2TRANSCRIPT

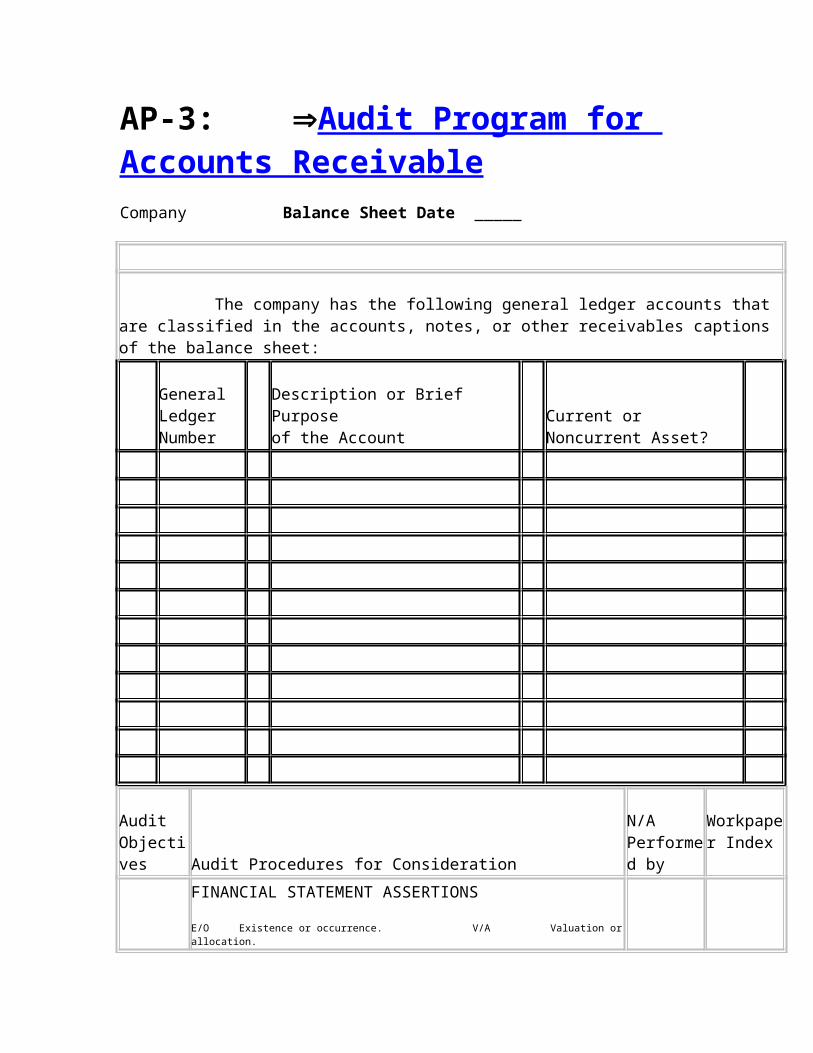

AP-3: Audit Program for Accounts ReceivableCompany Balance Sheet Date

The company has the following general ledger accounts that are classified in the accounts, notes, or other receivables captions of the balance sheet:

GeneralLedgerNumber

Description or Brief Purposeof the Account

Current orNoncurrent Asset?

Audit Objectives

Audit Procedures for Consideration

N/APerformed by

Workpaper Index

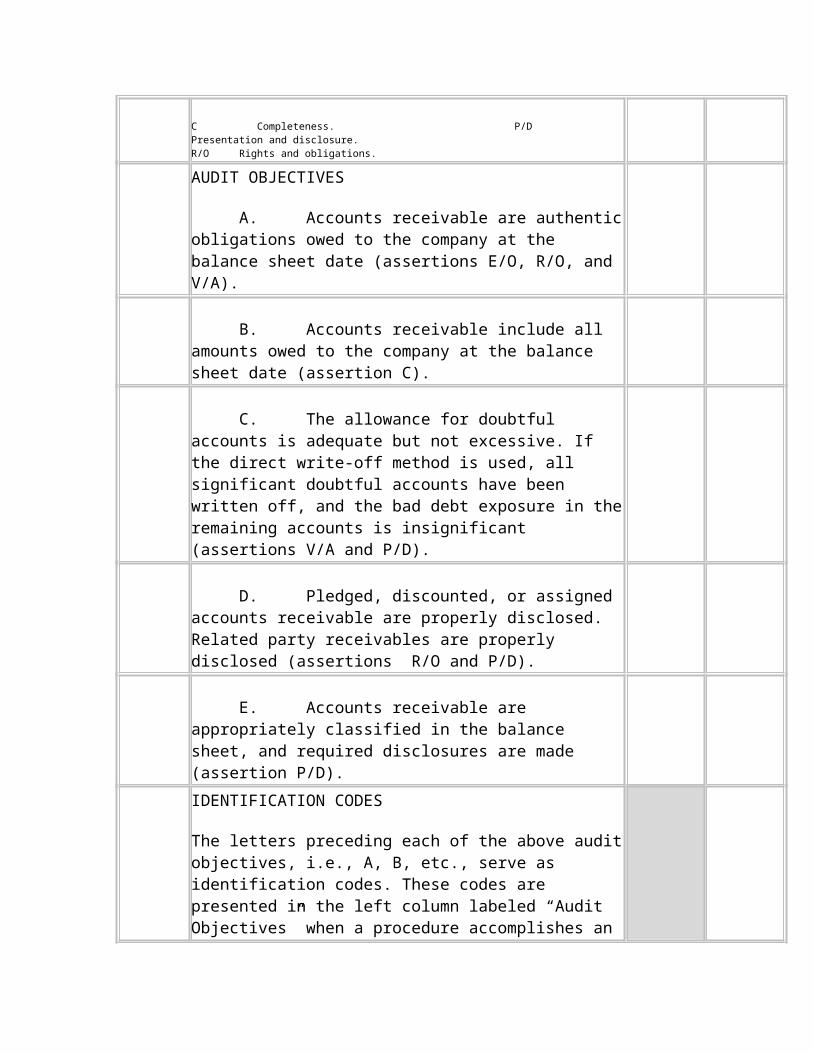

FINANCIAL STATEMENT ASSERTIONS

E/O Existence or occurrence. V/A Valuation or allocation.C Completeness. P/D Presentation and disclosure.R/O Rights and obligations.

AUDIT OBJECTIVES

A. Accounts receivable are authentic obligations owed to the company at the balance sheet date (assertions E/O, R/O, and V/A).

B. Accounts receivable include all amounts owed to the company at the balance sheet date (assertion C).

C. The allowance for doubtful accounts is adequate but not excessive. If the direct write-off method is used, all significant doubtful accounts have been written off, and the bad debt exposure in the remaining accounts is insignificant (assertions V/A and P/D).

D. Pledged, discounted, or assigned accounts receivable are properly disclosed. Related party receivables are properly disclosed (assertions R/O and P/D).

E. Accounts receivable are appropriately classified in the balance sheet, and required disclosures are made (assertion P/D).

IDENTIFICATION CODES

The letters preceding each of the above audit objectives, i.e., A, B, etc., serve as identification codes. These codes are presented in the left column labeled “Audit Objectives” when a procedure accomplishes an objective. If the alpha code appears in a bracket, e.g., [A], [B], etc., the audit procedure only secondarily accomplishes the objective. If an asterisk precedes a procedure, it is a preliminary step or a follow up step that does not accomplish an objective.

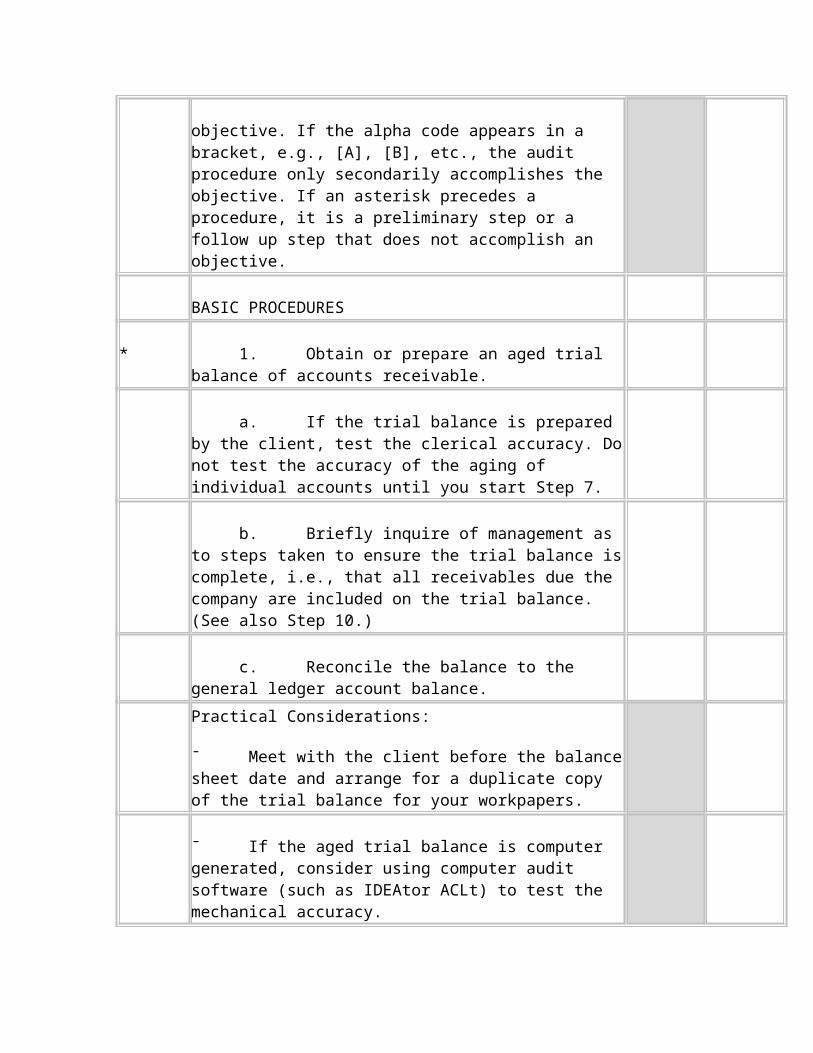

BASIC PROCEDURES

* 1. Obtain or prepare an aged trial balance of accounts receivable.

a. If the trial balance is prepared by the client, test the clerical accuracy. Do not test the accuracy of the aging of individual accounts until you start Step 7.

b. Briefly inquire of management as to steps taken to ensure the trial balance is complete, i.e., that all receivables due the company are included on the trial balance. (See also Step 10.)

c. Reconcile the balance to the general ledger account balance.

Practical Considerations:

¯ Meet with the client before the balance sheet date and arrange for a duplicate copy of the trial balance for your workpapers.

¯ If the aged trial balance is computer generated, consider using computer audit software (such as IDEAtor ACLt) to test the mechanical accuracy.

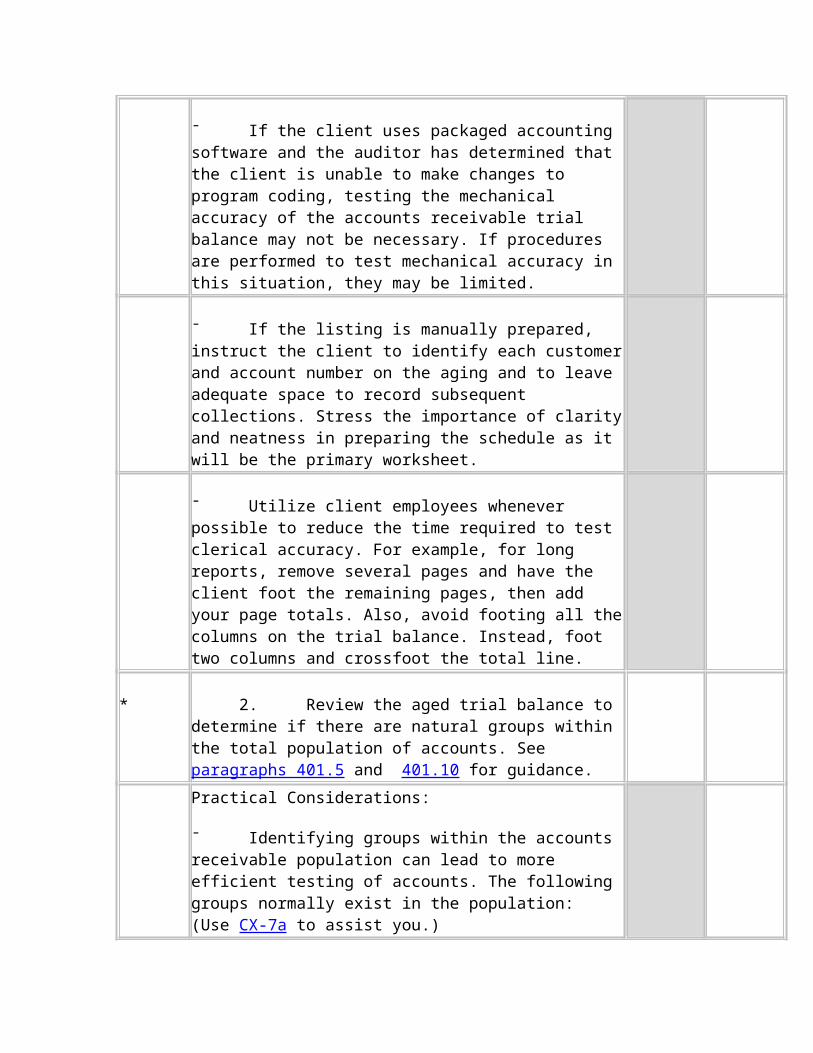

¯ If the client uses packaged accounting software and the auditor has determined that the client is unable to make changes to program coding, testing the mechanical accuracy of the accounts receivable trial balance may not be necessary. If procedures are performed to test mechanical accuracy in this situation, they may be limited.

¯ If the listing is manually prepared, instruct the client to identify each customer and account number on the aging and to leave adequate space to record subsequent collections. Stress the importance of clarity and neatness in preparing the schedule as it will be the primary worksheet.

¯ Utilize client employees whenever possible to reduce the time required to test clerical accuracy. For example, for long reports, remove several pages and have the client foot the remaining pages, then add your page totals. Also, avoid footing all the columns on the trial balance. Instead, foot two columns and crossfoot the total line.

* 2. Review the aged trial balance to determine if there are natural groups within the total population of accounts. See paragraphs 401.5 and 401.10 for guidance.

Practical Considerations:

¯ Identifying groups within the accounts receivable population can lead to more efficient testing of accounts. The following groups normally exist in the population: (Use CX-7a to assist you.)

¯¯ Customers with individually significant account balances or one customer with numerous small account balances that, when totaled, are significant. See paragraph 401.4 for guidance on determining an individually significant amount.

¯¯ Accounts with unusual characteristics other than the dollar amount of the balance. Such characteristics might include significant past due balances, an unusual customer name, accounts prone to misstatement, etc.

¯¯ Accounts with credit balances.

¯¯ Related party accounts.

¯¯ All other accounts.

¯ The groups do not need to be documented or listed in a separate schedule. Tickmarks can be used to identify accounts within a group, or you can simply have a mental awareness of each individual group. Groups may also be identified by simply scanning the trial balance.

A, E,[B], [C]

3. Select those groups that will be confirmed 100% by the use of positive confirmation letters. (Do not confirm accounts until the subsidiary ledger has been reconciled to the general ledger. See Step 1.)

a. Identify the accounts selected on the aged trial balance.

b. Review those accounts selected for confirmation with the owner/manager. If the client objects to a confirmation with a particular customer, determine if this restriction will affect your ability to accomplish the audit objectives for receivables.

c. Have the client prepare the positive confirmation letters reflecting, if possible, on the face of the letter or in an attached statement, the individual invoice number, invoice date, and invoice amounts that make up the customer’s balance.

d. Include the audit firm’s return address on all envelopes to ensure that all confirmation requests that are undeliverable by the post office are returned directly to the audit firm.

e. Be sure that the confirmations are to be returned directly to the auditor and contain a return envelope for this purpose.

f. Control the mailing of the letters.

g. Send second requests approximately 10 days after the first mailing. Determine the cause for confirmation requests returned as undeliverable. If possible, obtain new addresses and remail.

h. Retain copies of all confirmations in the workpapers.

Practical Considerations:

¯ SAS No. 96, Audit Documentation, requires documentation of substantive tests of details involving inspection of documents or confirmation to include identification of the items tested. The authors believe items tested can be identified by listing the items; by including a detail schedule in the workpapers, such as an aged trial balance, on which the items are identified; or by documenting in the workpapers the source and selection criteria. For example:

¯¯ For tests of significant items, documentation may describe the auditor’s scope and the source of the items (for example, all account balances greater than $5,000 from the 12/31/X2 accounts receivable detail).

¯¯ For haphazard or random samples, documentation should include the identifying characteristics of the items (for example, the specific invoice numbers, customer account numbers, etc.).

¯¯ For systematic samples, documentation may indicate the source, starting point, and sampling interval (for example, a selection of accounts from the 12/31/X2 accounts receivable detail, starting with account number 2150 and selecting every 10th account thereafter).

SAS No. 96 is effective for audits of financial statements for periods beginning on or after May 15, 2002, with early application permitted.

¯ There is a presumption auditors will confirm accounts receivable. If accounts receivable are not confirmed, SAS No. 67 requires auditors to document how they overcame that presumption.

¯ Many auditors assign a numerical or alpha code to each

customer selected for confirmation and record this code by the account on the aged trial balance and on the confirmation letter, for example, confirmation 1, 2, 3, etc. This makes check-in of replies easier.

¯ The auditor should obtain photocopies of positive confirmation letters and any attached statements for sending second requests and documenting performance of alternative procedures for nonreplies. The “Confirmation and Correspondence Control” at CX-24 can be used to monitor the status of confirmations.

¯ It may be helpful to record a client code on the return envelope to facilitate routing of the reply to the appropriate client mail file in the auditor’s office. This may be especially helpful during peak periods when the firm has several audits in progress.

¯ Some customers may have different billing vs. shipping addresses. Inquire if the proper address is used.

¯ The wording of the request should be clear and simple. A deadline date can also enhance the response time. See the sample accounts receivable confirmation letters at CL-7 through CL-11. Also, see paragraph 703.4 for other suggestions for improving confirmation responses.

¯ If possible, client personnel should prepare the letters. If there are numerous letters, a word processing mail merge can be used to insert the mailing address, salutation, and account balance into the form letter.

¯ The auditor should mail the letters or accompany the letters to the post office or mail drop. First class mail should be used to facilitate response time.

¯ Special handling procedures should be considered for international mail, for example, both a telex request and a confirmation letter may be appropriate. Also, including one or two international reply coupons (purchased at the post office) with confirmations may increase the response rate. Customers can use the coupons to purchase stamps in their own currency.

¯ If the auditor, based on his or her consideration of fraud risk

factors, decides to modify procedures related to accounts receivable balances, the auditor should consider contacting customers by telephone in addition to sending written confirmations. In addition, the auditor may consider confirming additional information with the customer. For example, relevant contract terms such as acceptance criteria, delivery and payment terms, the absence of future or continuing client obligations, the right to return product, guaranteed resale amounts, and cancellation and refund provisions may also be confirmed. The auditor should also consider confirming that the client and customer do not have any side agreements in addition to stated contract terms.

¯ Accounts receivable often represents one of the best opportunities to use data extraction software in an audit. Both the auditor and the client may save significant time by automating the accounts receivable confirmation process. Data extraction software also can be used to divide the population of accounts into natural groups (see Step 2), review subsequent cash collections and test the accounts receivable aging (see Step 7), and test sales cutoff (see Step 11).

A, E,[B], [C]

4. For the remaining balance that is not confirmed 100% in Step 3, determine if a sample of the accounts making up the balance should be selected for confirmation.

a. If sampling is appropriate, document the sampling selection process.

b. Repeat program Steps 3a through 3h on accounts being sampled.

Practical Considerations:

¯ Review Chapters 4 and 7 before performing a sampling application and determining a sample size. In many situations, sampling the remaining balance may not be necessary. See CX-7a for a worksheet to determine the extent of procedures to apply to the remaining balance.

¯ If sampling is used, consider confirming invoices instead of account balances.

¯ The “Sampling Planning and Evaluation Form—Substantive

Tests,” (CX-7b) can be used to document the sampling process.

A, E,[B], [C]

5. For significant employee receivables, notes receivable, or other receivables not on the aged trial balance, consider mailing positive confirmations. Retain copies of all confirmations in the workpapers.

Practical Consideration:

¯ Normally these receivables are not material, and audit procedures are not warranted. If the owner/manager has a large payable to the company, the auditor should evaluate whether the receivable actually represents salary or a dividend. Confirmation of a loan to an owner/manager can also be obtained in the management representation letter if the owner/manager is the party signing the representation letter.

A, E,[B], [C]

6. Process the confirmation replies:

a. Reconcile differences reported by customers on confirmation replies.

Practical Considerations:

¯ In most instances, it is efficient to have the client’s personnel perform the initial reconciliation of the confirmation replies. In that case, a copy of the confirmation reply should be provided to the client with instructions on the format they should use to reconcile the customer’s balance to the client’s balance. (See CX-21 for a suggested workpaper format that may be used.) If practical, client personnel should be requested to attach supporting documentation, such as validated deposit slips, invoices, and shipping documentation, to each reconciliation to facilitate examination by the auditor.

¯ Respondents sometimes use nontraditional means such as fax machines or e-mail to answer confirmation requests. In those cases, the auditor should consider the following additional steps:

¯¯ Verifying the source and content of the response over the telephone and documenting in the workpapers that this was done.

¯¯ Requesting that the respondent mail the original confirmation directly to the auditor.

b. Perform alternative procedures for those customers that do not respond.

Practical Considerations:

¯ Generally, the following approach can be used to perform alternative procedures for each nonreply:

¯¯ First, examine cash receipts subsequent to the confirmation date.

¯¯ If a portion of the balance has not been collected, examine sales invoices and corresponding shipping documents.

The auditor may also examine shipping documents on the subsequently collected portion if additional evidence about sales cutoff is needed.

¯ If practical, alternative procedures should be performed on all nonreplies. However, if a nonreply will be extremely time-consuming to test, consider classifying the entire nonreply customer balance as a misstatement. In that case, if the nonreply was part of a sampling application, the misstatement should be projected to the population (see Step 6d). Then, if the resulting projected misstatement in the total account is acceptable, additional testing is not necessary.

c. For groups confirmed 100%, summarize the results of confirmation procedures and indicate the total accounts and balances confirmed without exception, confirmations reconciled, nonreplies with alternative procedures performed, and confirmations and nonreplies with misstatements.

d. For accounts receivable groups that were sampled, summarize and evaluate the sample results and project the misstatements in the strata.

e. Based on results of confirmation procedures, determine if additional confirmation or alternative procedures are warranted on untested customer balances.

Practical Considerations:

¯ The “Confirmation Summary Form” (CX-8) can be used to

summarize the confirmation results for sampling or nonsampling applications.

¯ The “Sampling Planning and Evaluation Form—Substantive Tests” (CX-7b) can be used to summarize, as well as evaluate, the results for sampling applications.

C 7. Test the adequacy of the allowance for doubtful accounts:

a. Have the client post subsequent cash collections to your copy of the aged trial balance obtained in Step 1.

b. Test the client’s subsequent collections on major account balances by examining deposit slips and remittance advices. Document the account balances selected for testing.

c. If uncollected accounts are significant, test the aging of the remaining accounts. (It is advisable to use original sales documents to test the propriety of aging.)

d. If practical, for each material past due account, inspect credit files, review customer correspondence, or discuss the status of collection with the client. Identify potentially doubtful accounts.

e. Inquire if there are collection problems likely to occur with accounts that are presently classified as current.

f. If you become aware that individual accounts have been converted to notes, determine if they should be classified as noncurrent assets.

g. Relate your findings in Steps 7a to 7f to the allowance for doubtful accounts and evaluate its adequacy. If meaningful, consider computing prior year bad debt statistics and prior year collection statistics.

h. If the company uses the direct write-off method, evaluate the exposure that significant uncollectible accounts remain in accounts receivable.

Practical Consideration:

¯ The direct write-off method is not GAAP. However, depending on the materiality of the allowance and write-offs during the period, it may approximate GAAP.

i. Consider the collectibility of significant employee receivables, notes receivable, or other receivables not on the aged trial balance.

Practical Considerations:

¯ Comments made by client personnel should not be taken at face value without other evidence to support the accuracy of client comments.

¯ Other considerations or approaches that you may wish to use are:

¯¯ Use alternative approaches to develop an independent estimate.

¯¯ Compare the allowance with actual results after the balance sheet date.

¯¯ Consider the client’s process for estimating the allowance, including the qualifications and experience of the person who determines the amount of the allowance account.

¯¯ Determine whether the estimate of the allowance balance was subjected to management review.

¯¯ Determine what steps the company takes to identify any unusual variations and the reasons therefor.

¯ Statistics regarding bad debt history may be meaningful and can be maintained on a form similar to the “Accounts Receivable Statistics Form,” CX-9.

¯ In evaluating the allowance for doubtful accounts, it may be helpful to determine a range of amounts within which the company’s bad debt allowance would be acceptable. If the company’s balance does not fall in this acceptable range, the potential error would be the difference between the client’s amount

and the closest amount in the acceptable range.

¯ For significant delinquent balances, it may be necessary to evaluate the creditworthiness of the debtor and the value of any collateral pledged to secure payment of the receivable.

D, [A] 8. Based on a review of confirmation replies from financial institutions, loan agreements, minutes, inquiry with the owner/manager, and work performed in other audit areas, determine if there are pledged, discounted, or assigned receivables.

Practical Considerations:

¯ If the above procedures do not indicate the existence of such receivables, consider documenting this by stating “none noted” under the index column of this program.

¯ If existence of such receivables was noted, briefly summarize the financial statement disclosure in a memo or cross-reference to other audit workpapers where such information is summarized.

D, E 9. Based on work performed in previous steps and knowledge obtained in other audit areas, determine that the following accounts are identified for separate classification in the balance sheet.

a. Large credit balances that should be classified as accounts payable.

b. Related party receivables.

c. Material employee receivables.

d. Material notes receivable.

e. Noncurrent receivables that should be reclassified.

B 10. Evaluate whether evidence obtained in the preceding steps and from procedures in the audit of revenue is adequate to support the completeness assertion, i.e., whether all transactions are included in revenue and related accounts receivable balances.

Practical Considerations:

¯ The procedures do not have to be complex or time-consuming. Evidence about completeness can be obtained by inquiry, observation, analytical procedures, tests of transactions, and management’s representations. See Chapters 3 and 7 for additional discussion of these procedures.

¯ The documentation of this step can be a brief memo or note in the workpapers. It should correlate the work performed in other areas such as analytical predictive tests in the revenue area.

A, [B] 11. Perform the following analytical procedures. For any significant differences noted, investigate the nature and cause of the differences and consider whether additional procedures are needed to test sales cutoff:

a. Compare sales for the last month of the fiscal year to sales for the rest of the year and the first month after year end.

b. Compare monthly sales returns and credit memos for the last few months of the fiscal year to the first few months following year end.

Practical Considerations:

¯ Basic accounts receivable confirmation procedures and the preceding analytical procedures are usually adequate to test the sales cutoff. However, the following circumstances warrant consideration of performing additional cutoff tests:

¯¯ When accounts receivable are confirmed as of an interim date.

¯¯ When large quantities of merchandise awaiting shipment are noted during the year-end inventory observation.

¯¯ When there has been a large increase in sales during the last month of the year under audit or in the first month of the new year.

¯¯ When there has been a large increase in sales returns or credit memos in the first few months after year end.

¯¯ When the auditor’s knowledge of the client and/or

understanding of internal control indicates a high risk of material misstatement of sales cutoff.

¯ When an analytical procedure is used as the principal substantive test of a significant financial statement assertion, SAS No. 56, Analytical Procedures, as amended by SAS No. 96, Audit Documentation, requires the auditor to document (1) the expectation and the factors considered in its development (unless readily determinable from the work performed), (2) the results of the comparison between the expectation and recorded amounts, and (3) any additional procedures performed in response to significant unexpected differences and the results of those procedures. SAS No. 96 is effective for audits of financial statements for periods beginning on or after May 15, 2002, with early application permitted.

* 12. Consider the need to apply one or more additional procedures. The decision to apply additional procedures should be based on a consideration of whether information obtained or misstatements detected by performing substantive tests or from other sources during the audit alter your judgment about the need to obtain a further understanding of control activities, the assessed level of risk of material misstatements (whether caused by error or fraud), and on an evaluation of whether the basic procedures have been sufficient to achieve the audit objectives. Attach audit program sheets to document additional procedures.

Practical Considerations:

¯ Certain common additional procedures relating to the following topics are illustrated following this program:

¯¯ Year-end cutoff.

¯¯ Write-offs.

¯¯ Imputed interest.

¯¯ Interest on notes receivable.

¯¯ Related party receivables.

¯¯ Employee travel advances.

¯¯ Analytical procedures.

¯¯ Fair value disclosures.

¯¯ Noncurrent notes and accounts receivable.

¯¯ Collateralized accounts receivable.

¯¯ Accounts receivable confirmed at interim date.

¯¯ Transfers of receivables.

¯¯ Cash receipts.

¯ Practitioners may refer to PPC’s Guide to Fraud Investigations for more extensive fraud detection procedures if it is suspected that the financial statements are materially misstated due to fraud.

* 13. Consider whether procedures performed are adequate to respond to identified fraud risk factors. If fraud risk factors or other conditions are identified that require an additional audit response, consider those risk factors or conditions and the auditor’s response in connection with the performance of Step 11 in AP-1b.

Practical Consideration:

¯ Specific responses to identified fraud risk factors are addressed in individual audit programs. In connection with evaluation and other completion procedures in AP-1b, the auditor considers the need to perform additional procedures based on the results of procedures performed in the individual audit programs and the cumulative knowledge gained from performing those procedures.

* 14. Consider whether the results of audit procedures indicate reportable conditions in internal control and, if so, add to the memo of points for the communication of reportable conditions. (See section 1504 for examples of reportable conditions, and see CX-18 for a worksheet that can be used to document the points as they are encountered during the audit.)

CONCLUSION

We have performed procedures sufficient to achieve the audit objectives for accounts receivable, and the results of these procedures are adequately documented in the accompanying

workpapers. (If you are unable to conclude on any objective, prepare a memo documenting your reason.)

Additional Audit Procedures for Accounts Receivable

Instructions: Additional procedures will occasionally be necessary on some small business engagements. The following listing, although not all-inclusive, represents common additional procedures and their related objectives.

Year-end Cutoff

A, [B] Test the year-end cutoff procedures for sales to determine if receivables are recorded in the appropriate period.

a. Scan the sales journals for one month before and after year end. Investigate any unusual entries.

b. Review the journal for sales returns and credit memos for two months before and after year end. Investigate any unusual entries.

c. Trace the shipping documents for the last five shipments of the year and the first five shipments after year end to the sales journal to determine whether they were recorded in the proper period.

Practical Considerations:

¯ Normally, the shipping documents will have already been identified at the year-end inventory observation. (See basic procedure 6a at AP-5.)

¯ Basic accounts receivable confirmation procedures and the

preceding analytical procedures are usually adequate to test the sales cutoff. However, the following circumstances warrant consideration of performing additional cutoff tests:

¯¯ When accounts receivable are confirmed as of an interim date.

¯¯ When large quantities of merchandise awaiting shipment are noted during the year-end inventory observation.

¯¯ When there has been a large increase in sales during the last month of the year under audit or in the first month of the new year.

¯¯ When there has been a large increase in sales returns or credit memos in the first few months after year end.

¯¯ When the auditor’s knowledge of the client and/or understanding of internal control indicates a high risk of material misstatement of sales cutoff.

Write-offs

C Select individual accounts that were written off during the audit period. Determine that the entries were properly approved by the owner/manager. Document the items tested.

Practical Consideration:

¯ This is a fraud test and should not be performed unless the auditor suspects that improprieties have occurred.

Imputed Interest

A, E Review accounts and notes receivable to determine if any interest should be imputed for significant balances that are due in excess of one year from the balance sheet date. Also consider proper balance sheet classification of such receivables.

Practical Consideration:

¯ Extended term accounts receivable are rare but can arise when a company establishes payment terms for its trade accounts receivable based on a poor economy or difficulty with some key customers. Normally, this type of interest should not be accrued, but instead be recognized on a cash basis.

Interest on Notes Receivable

A, E For significant notes receivable, test the reasonableness of interest earned and any prepaid or accrued interest receivable.

Related Party Receivables

D, [A] If related party receivables are material, prepare or obtain an analysis of advances to directors, officers, employees, stockholders, and other affiliated parties and perform the following steps:

a. Recompute the total balance and determine that it agrees with the balance in the general ledger or the detailed trial balance.

b. Review the list for potential problem accounts or large amounts.

c. Identify the purpose for advances and their potential collectibility. Determine if such advances should be reflected as dividends or salary.

d. If the balances are significant, consider confirmation of several selected individual balances with the employees or affiliated parties and reconcile replies. Retain copies of all confirmations in the workpapers.

e. Determine that such advances have been properly approved by individuals appropriate under the bylaws of the company.

f. Determine the nature of any accounts receivable from such parties that were written off during the audit period but subsequently reinstated to the general ledger.

Practical Consideration:

¯ These steps should be coordinated with the related party procedures in the general program.

Employee Travel Advances

A, [D] Obtain or prepare a schedule of the detailed balances included in employee travel advances and perform the following steps:

a. Recalculate the schedule to determine the clerical accuracy and determine that the total balance agrees with the general ledger.

b. Compare individual information with the source records on a test basis. Document the items tested.

c. Confirm account balances with individual employees if the total amount is significant (this is very rarely the case) and reconcile replies. Retain copies of all confirmations in the workpapers.

d. Determine whether there is a proper cutoff of expense advances with the last payroll for year end.

Practical Consideration:

¯ In most cases, small businesses do not generate a significant amount of employee advances. These advances should normally be cleared on a regular basis and, thus, should not grow to significant amounts.

Analytical Procedures

[A],[B],[C]

Apply analytical procedures to accounts receivable by determining the following and comparing to percentages maintained in the permanent audit file:

a. Trade receivables divided by current assets.

b. Trade receivables divided by total assets.

c. Trade receivables divided by net worth.

d. Net sales divided by trade receivables.

e. Trade receivables divided by (net sales divided by 360).

f. Determine the cause of any significant fluctuations in these percentages.

Practical Consideration:

¯ Normally, these analytical procedures should only be performed when the auditor feels additional evidence is necessary beyond that obtained by basic procedures identified earlier in the program.

Fair Value Disclosures

E Obtain information about the fair values of financial instruments (e.g., trade accounts receivable and notes receivable) for disclosure in the financial statements.

Practical Considerations:

¯ SFAS No. 126, Exemption from Certain Required Disclosures about Financial Instruments for Certain Nonpublic Entities: An Amendment of SFAS No. 107, makes SFAS No. 107’s disclosures about the fair value of financial instruments optional for companies that meet the following criteria:

¯¯ The company is a nonpublic company.

¯¯ The company’s total assets are less than $100 million on the date of the financial statements.

¯¯ The company has no instrument that, in whole or in part, is accounted for as a derivative instrument under SFAS No. 133 during the reporting period.

¯ Unless the client provides extended repayment terms (e.g., in excess of 90 days), the carrying amount of accounts receivable will ordinarily approximate their fair value and no disclosure is required by SFAS No. 107.

¯ The carrying amount of notes receivable will ordinarily approximate fair value. However, if the interest rate on the note is significantly more or less than current market rates, fair value can

be determined by discounting future cash flows at an appropriate rate, considering the relative risk associated with the note. SFAS No. 107 indicates that one option is for the company to use the rate at which the same loan would be made under current conditions.

¯ Fair value may be affected by the risk that the customer or borrower will default. If the risk of default is remote, it is generally possible to value the receivable by discounting future cash flows. If the risk of default is probable, fair value can be determined by valuing the collateral and any secondary sources of repayment (such as payments made by the business owner). However, if the risk of default falls somewhere between remote and probable, fair value estimates will require significant judgment.

¯ Interpretation No. 1 of SAS No. 57, Auditing Accounting Estimates (AU 9342), addresses auditing the client’s fair value estimates for disclosures required by SFAS No. 107. The Interpretation requires that the auditor obtain sufficient competent evidence to provide reasonable assurance that:

¯¯ Valuation principles are in accordance with SFAS No. 107, consistently applied, and supported by underlying documentation.

¯¯ The method of estimation and significant assumptions used are properly disclosed.

¯ Paragraph 60 of SFAS No. 107 allows companies to use simplified assumptions to estimate fair value of financial instruments. Consequently, it is important that the methods and significant assumptions used in the estimates are disclosed.

¯ If a fair value estimate is based on the work of an outside specialist (e.g., an appraiser), the requirements of SAS No. 73, Using the Work of a Specialist, should be followed. The additional procedures to AP-1 contain audit procedures regarding using the work of a specialist.

¯ AU 9342 provides additional guidance for situations in which the client chooses to provide voluntary fair value information in addition to that required by SFAS No. 107.

¯ SFAS No. 107 does not require that fair values of financial instruments be estimated if it is not practicable, or cost effective, to develop the estimates. The decision of whether it is practicable

should consider such things as the importance of the financial instrument to the client’s business activities and the materiality of the carrying amount of the financial instrument to the financial statements.

¯ When it is not practicable to estimate the fair value of a financial instrument, disclosure must be made of:

¯¯ Information pertinent to estimating the fair value of the financial instrument.

¯¯ The reasons why it is not practicable to estimate fair value.

Noncurrent Notes and Accounts Receivable

EFor notes and accounts receivable with maturities greater than one year, perform the following procedures:

a. Evaluate whether the interest and contractual principal payments will be collected in accordance with their contractual terms.

b. If either interest or principal payments will not be collected in accordance with their contractual terms, determine whether an allowance for credit loss has been computed using one of the following methods:

(1) The present value of expected future cash flows discounted at the receivable’s effective interest rate.

(2) The receivable’s observable market price.

(3) The fair value of the collateral (if the receivable is collateral dependent).

Collateralized Accounts Receivable

C If collateralized accounts receivable are significant, examine collateral for existence, ownership, and its fair value.

Practical Considerations:

¯ Some evidence of ownership includes a bill of sale, a title, a deed, or a mortgage.

¯ Depending on the type of collateral being evaluated, the auditor may evaluate the reasonableness of the client’s estimate of the fair value of the collateral by using a security or commodity quotation, appraisal, assayer’s or other expert’s report, blue book, or other general source.

Accounts Receivable Confirmed at Interim Date

A, [B],[C]

If accounts receivable were confirmed at an interim date, perform the following steps:

a. Obtain a detailed aged accounts receivable trial balance at the balance sheet date and perform the following:

(1) Obtain or prepare a reconciliation of the trial balance to the general ledger control account. Examine support for significant reconciling items.

(2) Compare trial balance totals between the balance sheet date and the interim date. Investigate significant variations.

(3) Identify any significant changes in the aging of accounts receivable.

b. Scan receivables activity in the accounting records during the period from the interim date to the balance sheet date. Investigate and explain the nature and origin of any unusual entries.

c. Perform a test of sales cutoff at the balance sheet date.

Practical Considerations:

¯ In most small businesses, it is more efficient to confirm accounts receivable as of the balance sheet date to avoid incurring the additional time necessary to bring the accounts receivable balances forward to year end. Section 207 discusses factors to consider when deciding whether to confirm accounts receivable as of an interim date.

¯ If the results of the rollforward procedures are unsatisfactory,

consider the need to confirm accounts receivable as of the balance sheet date.

Transfers of Receivables

D, E If the company has transferred receivables to a third party, determine whether the transaction has been accounted for in accordance with SFAS No. 140.

Practical Considerations:

¯ Section 302 of PPC’s Guide to Preparing Financial Statements discusses accounting for transfers of receivables in accordance with SFAS No. 140, Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities.

¯ An auditing interpretation of SAS No. 73 (AU 336), Using the Work of a Specialist, titled The Use of Legal Interpretations as Evidential Matter to Support Management’s Assertion That a Transfer of Financial Assets Has Met the Isolation Criterion in Paragraph 9(a) of Financial Accounting Standards Board Statement No. 140, provides guidance to auditors about obtaining evidential matter to determine the proper accounting treatment under SFAS No. 140.

Cash Receipts

* If the auditor, based on his or her consideration of fraud risk factors, decides to modify procedures related to customer cash receipts, consider performing a proof of cash (see additional procedures at AP-2). In addition, consider verifying the following:

a. The dates of cash receipts and deposit tickets are identical.

b. The total amounts on the daily cash receipts list and daily deposit slips agree.

c. The customer’s name and deposit amounts should be the same on the daily cash receipts journal and the subsidiary ledger.

d. Deposit slip totals are accurate.

e. Review customer complaints.

f. Search for write-offs that are unusual, such as write-offs of balances due from continuing customers.

g. Review credit memos.

Practical Consideration:

¯ Practitioners may refer to PPC’s Guide to Fraud Investigations for more extensive fraud detection procedures if it is suspected that the financial statements are materially misstated due to fraud.

Additional Audit Procedures for AccountsReceivable Beginning Balance in Initial Audit

Company Balance Sheet Date

Audit Objectives

Audit Procedures for Consideration

N/APerformed by

Workpaper Index

Instructions: Additional procedures will be necessary in an initial audit. These procedures are applied to opening balances and differ depending on whether you are relying on your review of a predecessor’s work or placing no reliance on a predecessor’s audit. (Section 1803 discusses considerations when replacing a predecessor auditor, including a discussion of what the term reliance means when used in this program.) These procedures may be applied in conjunction with the basic procedures applied to the ending balance. The asterisks preceding the procedures indicate that they are an intermediate step in achieving audit objectives for the ending balance.

* 1. If a predecessor’s audit of the prior period’s financial statements is to be relied on:

a. Review the predecessor’s workpapers containing the aged

trial balance of receivables, including the posting of subsequent cash collections and the summary of confirmation results; consider the adequacy of confirmation coverage and results.

b. Review the predecessor’s workpapers on the adequacy of the allowance for doubtful accounts; consider the adequacy of procedures and the reasonableness of the conclusion on the balance. Note the method of determining the balance and compare to the method used in the current period.

c. Identify significant noncash credits to receivables during the first three months of the current period and consider whether they relate to the prior period. Document any items tested.

* 2. If no reliance on a predecessor’s audit is planned or possible:

a. Scan the aged trial balance of opening accounts receivable, foot the schedule, and trace the total to the general ledger control account.

b. Scan the general ledger control account for significant noncash credits (write-offs or sales returns and allowances) for the first three months of the current period; consider whether they relate to the prior period. Document any items tested.

c. Compare cash collections in the first two months of the current period with the prior period accounts receivable balance.

d. Compare sales in the first month of the current period with sales in the last month of the prior period; consider the reasonableness of the sales cutoff.

e. Obtain and scan a summary of the activity in the allowance for doubtful accounts for the prior period; note the method of determining the balance and compare to the method used in the current period.

f. Compare the following ratios for the current period to the same ratios in the two prior periods.

(1) Age categories to receivables.

(2) Receivables to sales.

(3) Allowance for doubtful accounts to receivables and sales.

Practical Considerations:

¯ Watch for major customers on the prior period trial balance not on the current period closing trial balance, unusually large noncash credits, and indications of improper cutoff.

¯ See the practical considerations for basic procedures 1 and 7.

Prosedur Audit atas Piutang DagangPENGERTIAN PIUTANG USAHAMenurut Donald E. Keiso (2004:386), piutang adalah klaim uang, barang, jasa kepada pelanggan atau pihak – pihak lainnya. Sedangkan menurut Sukrisno Agoes, (2004:173), piutang usaha adalah piutang yang berasal dari penjualan barang dagangan atau jasa secara kredit.Piutang timbul dari beberapa jenis transaksi, di mana yang paling umum ialah dari penjualan barang atau jasa secara kredit. Kredit dapat diberikan dalam bentuk perkiraan terbuka atau berdasarkan instrumen kredit yang sahih, yang disebut surat promes (wesel). Surat promes (promissory note), yang sering disebut wesel (nota), adalah janji tertulis untuk membayar sejumlah uang tertentu atas permintaan atau pada suatu tanggal yang telah ditetapkan.

KLASIFIKASI PIUTANGPiutang dapat diklasifikasikan sebagai berikut :1) Piutang usaha a) Piutang dagang b) Piutang jasa2) Piutang non usaha a) Piutang karyawan b) Piutang deviden c) Piutang pendapatan yang masih harus diterima d) Piutang klaim asuransi e) Piutang wesel f) Piutang lain-lain

PRINSIP AKUNTANSI YANG DITERIMA UMUM UNTUK PENYAJIAN PIUTANG PADA LAPORAN POSISI KEUANGAN

1. Piutang usaha harus disajikan dalam neraca sebesar jumlah yang harus ditagih

2. Jika perusahaan tidak membentuk cadangan piutang usaha, harus mencantumkan pengungkapannya di neraca bahwa saldo piutang usaha tersebut adalah jumlah bersih.

3. Jika piutang usaha bersaldo material pada neraca harus disajikan rinciannya di neraca atau dibuatkan Catatan Atas Laporan Keuangan (CALK).

4. Piutang usaha yang bersaldo kredit terdapat pada kartu piutang pada tanggal neraca disajikan dalam kelompok hutang lancar.

5. Jika jumlahnya material, piutang non usaha harus disajikan terpisah dari piutang usaha

TUJUAN AUDIT PIUTANGMenurut Sukrisno Agoes (2004:173), tujuan audit atas piutang antara lain :

1. Untuk mengetahui apakah terdapat pengendalian intern (internal control) yang baik atas piutang dan transaksi penjualan, piutang dan penerimaan kas.

2. Untuk memeriksa validity (keabsahan) dan authenticity (ke otentikan) dari pada piutang.

3. Untuk memeriksa collectibility (kemungkinan tertagihnya) piutang dan cukup tidaknya perkiraan allowance for bad debts (penyisihan piutang tak tertagih)

4. Untuk mengetahui apakah ada kewajiban bersyarat (contingent liability) yang timbul karena pendiskontoan wesel tagih (notes receivable)

5. Untuk memeriksa apakah penyajian piutang di neraca sesuai dengan prinsip akuntansi yang berlaku umum di Indonesia/Standar Akuntansi Keuangan.

PROSEDUR AUDIT ATAS PIUTANGMenurut Sukrisno Agoes (2004:176), prosedur audit piutang usaha antara lain :

1. Pelajari dan evaluasi internal control atas piutang dan transaksi penjualan, piutang dan penerimaan.

2. Buat Top Schedule dan Supporting Schedule piutang pertanggal neraca.Minta aging shedule dari piutang usaha pertanggal neraca yang antara lain menunjukkan nama pelanggan (customer), saldo piutang, umur piutang dan kalau bisa subsequent collections-nya.

3. Periksa mathematical accuracy-nya dan check individual balance ke subledger lalu totalnya ke general ledger.

4. Test check umur piutang dari beberapa customer ke subledger piutang dan sales invoice.

5. Kirimkan konfirmasi piutang: (1) Tentukan dan tuliskan dasar pemilihan pelanggan yang akan dikirim surat konfirmasi. (2) Tentukan apakah akan digunakan konfirmasi positif atau konfirmasi negatif. (3) Cantumkan nomor konfirmasi baik di schedule piutang maupun di surat konfirmasi. (4) Jawaban konfirmasi yang berbeda harus diberitahukan kepada klien untuk dicari perbedaannya. (5) Buat ikhtisar (summary) dari hasil konfirmasi

6. Periksa subsequent collections dengan memeriksa buku kas dan bukti penerimaan kas untuk periode sesudah tanggal neraca sampai

mendekati tanggal penyelesaian pemeriksaan lapangan (audit field work). Perhatikan bahwa yang dicatat sebagai subsequent collectionshanyalah yang berhubungan dengan penjualan dari periode yang sedang diperiksa.

7. Periksa apakah ada wesel tagih (notes receivable) yang didiskontokan untuk mengetahui kemungkinan adanya contingent liability.

8. Periksa dasar penentuan allowance for bad debts dan periksa apakah jumlah yang disediakan oleh klien sudah cukup, dalam arti tidak terlalu besar dan terlalu kecil.

9. Test sales cut-of dengan jalan memeriksa sales invoice, credit note dan lain-lain, lebih kurang 2 (dua) minggu sebelum dan sesudah tanggal neraca. Periksa apakah barang-barang yang dijual melalui invoice sebelum tanggal neraca, sudah dikirim per tanggal neraca. Kalau belum cari tahu alasannya. Periksa apakah ada faktur penjualan dari tahun yang diperiksa, yang dibatalkan dalam periode berikutnya.

10. Periksa notulen rapat, surat-surat perjanjian, jawaban konfirmasi bank, dan correspondence file untuk mengetahi apakah ada piutang yang dijadikan sebagai jaminan.

11. Periksa apakah penyajian piutang di neraca dilakukan sesuai dengan prinsip akuntansi yang berlaku umum di Indonesia/SAK

12. Tarik kesimpulan mengenai kewajaran saldo piutang yang diperiksa.