accounting profitability and takeover likelihood …...1 accounting profitability and takeover...

TRANSCRIPT

1

Accounting Profitability and Takeover Likelihood

Ashiq Ali [email protected]

The University of Texas at Dallas 800 W Campbell Rd, Richardson, TX 75080

Todd Kravet

[email protected] University of Connecticut

2100 Hillside Road, Unit 1041A, Storrs, CT 06268

Bin Li [email protected]

The University of Texas at Dallas 800 W Campbell Rd, Richardson, TX 75080

This Draft: January 2016

Abstract: We examine the association between accounting profitability and takeover likelihood of a firm. We show that the takeover likelihood is negatively associated with negative industry-adjusted ROA, and is positively associated with positive industry- adjusted ROA. This result suggests that among firms with below industry average profitability, acquirers can unlock more value in firms with poorer performance through efficient management (Palepu 1986). This result also suggests that among firms with above industry average profitability, those with higher accounting profitability are more likely to be acquired, and we argue that it is in part due to managerial opportunism. Consistent with this explanation, the positive association is more (less) pronounced when the benefits (costs) of acquisition to acquirers’ management is greater, and the acquirers’ stock price reaction to the announcement of acquisition is negatively associated with targets’ positive industry-adjusted ROA.

2

Accounting Profitability and Takeover Likelihood

1. Introduction

This paper examines how accounting profitability of a firm is associated with its

acquisition likelihood. Prior research argues that poorer performing firms are more likely

to be acquired, because acquirers can unlock value through efficient management by

taking such actions as increasing monitoring, replacing management, and restructuring

operations (Palepu 1986). Even though several prior studies have examined the

association between accounting profitability and takeover probability, evidence on the

predicted negative relation is inconclusive (e.g., Palepu 1986; Berger and Ofek 1996;

Billett and Xue 2007; Cremers, Nair, and John 2009). We argue that among firms

performing well, which we operationalize as above industry average profitability, those

with higher accounting profitability are more likely to be taken over, because the

acquisitions are motivated by managerial opportunism. Accordingly, we predict that

takeover likelihood is negatively associated with negative industry-adjusted ROA and is

positively associated with positive industry-adjusted ROA. We empirically examine this

prediction and further test whether the positive association is more pronounced when

acquiring managers’ incentives to behave opportunistically are greater.

Why would managers making opportunistic acquisitions prefer targets with higher

accounting profitability? Harford and Li (2007) and Grinstein and Hribar (2004) show

that CEOs’ pay and wealth increases after acquisitions, even if the acquisitions are value

destroying. It is because the value of new grants after an acquisition is greater than the

adverse effects on CEOs’ pre-acquisition equity portfolio. In addition, Harford and

Schonlau (2013) show that the likelihood of becoming directors in other firms increases

3

for CEOs who undertake acquisitions, because of their acquisition related experience,

even if the acquisitions are value destroying. Opportunistic managers’ preference for

targets with higher accounting profitability is consistent with their desire to reduce the

risk of losing their job by ensuring the long run survival of the combined entity,

especially since such acquisitions tend to be value destroying. Evidence in prior studies

support the above argument that firms with higher accounting profitability, specifically

higher industry-adjusted ROA, have lower management turnover, and this association is

incremental to the effect of stock returns on management turnover (Farrell and Whidbee

2003; DeFond and Park 1999). Another reason why opportunistic managers prefer targets

with higher accounting profitability is because it may help meet certain accounting based

benchmarks, such as analysts’ expectation of earnings or previous period’s earnings (e.g.,

Burgstahler and Dichev 1997; Matsumoto 2002; Skinner and Sloan 2002; Donelson et al.

2013).

For the sample period 1990 to 2013, we find a non-linear association between

accounting profitability and takeover likelihood, consistent with our prediction.

Specifically, we observe a negative association between takeover likelihood and negative

industry-adjusted ROA, consistent with the inefficient management hypothesis (Palepu

1986). Additionally, we observe a positive association between takeover likelihood and

positive industry-adjusted ROA, which we argue is driven at least in part by acquiring

firm managers’ opportunism. We provide several additional results that suggest that the

positive association is more pronounced when acquiring firms’ managers have greater

incentive to behave opportunistically.

4

First, we find that the positive association between takeover likelihood and

positive industry-adjusted ROA is more pronounced when acquiring managers are more

likely to benefit from reporting higher accounting profitability; specifically, when the

acquirers are public as against private firms (Klassen 1997; Beatty et al. 2002), when the

time from the acquisition announcement to completion is short1, when the acquirers

report a relatively long string of earnings increases in the periods preceding the

acquisition (Barth et al. 1999; Myers et al. 2007), when acquirers have a higher valuation

premium, measured as PE ratio (Jensen 2005; Chu et al. 2015), and when acquirers are

close to meeting or beating certain earnings benchmarks (Burgstahler and Dichev 1997;

Roychowdhury 2006).

We also find that the positive association between takeover likelihood and

positive industry-adjusted ROA is more pronounced when it is less costly for managers to

make opportunistic acquisitions. The positive association is greater when the acquirers

have a high level of free cash flows and limited growth opportunities, no blockholders,

lower board independence, and healthier financial condition (higher Z-score), so they are

can more likely withstand the destruction in its value that may result from the

opportunistic acquisition.

Finally, we show that acquirers’ stock returns on acquisition announcement date

are significantly lower for acquisitions of targets with positive industry-adjusted ROA

than of targets with negative industry-adjusted ROA, Furthermore, among targets with

positive industry-adjusted ROA, these returns are significantly lower for acquisition of

1 The incentive to quickly complete acquisitions is presumably because on realizing that a shortfall in profitability for the current or the subsequent period is likely to happen, management’s incentive would be to acquire a profitable target as quickly as possible. Furthermore, a quicker completion time results in a decrease in the time available for due diligence.

5

targets with higher positive industry-adjusted ROA. This result suggests that acquiring

firms’ managers sacrifice greater firm value when they acquire targets with higher

accounting profitability, consistent with the notion that such acquisitions are motivated to

a greater extent by the self-interests of the acquirers’ management, and they would

therefore be willing to overpay more for targets with higher accounting profitability.

Collectively, our results support the notion that the positive association between positive

industry-adjusted ROA and takeover likelihood is at least in part driven by managerial

opportunism.

Our study makes the following contributions to the literature. Many important

studies on corporate control use accounting profitability as an explanatory variable in the

takeover likelihood model (see, e.g., Berger and Ofek 1996; Billet 1996; Billet and Xue

2007; Bodnaruk, Massa, and Simonov 2009; Cremer, Nair, and John 2009; and Ivashina,

Nair, Saunders, Massoud, and Stover 2009). Palepu (1986) argues that firms with more

inefficient management are more likely to become takeover targets. He proposed

accounting profitability as a proxy for management efficiency, but obtained an

insignificant coefficient on the variable. Subsequent papers that use accounting

profitability as an explanatory variable in the takeover likelihood models, generally

justify its inclusion by referring to Palepu’s paper. These papers also find that the

coefficients on the accounting profitability variable are generally insignificant, and in a

few cases when they are significant, the signs of the coefficients are mixed. The frequent

use of the accounting profitability variable in prior studies and the lack of conclusive

evidence on its relation with takeover likelihood underscore the importance of examining

this issue. We show that negative industry-adjusted profitability is negatively associated

6

with takeover likelihood. This negative association is consistent with the inefficient

management hypothesis put forward by Palepu (1986). We also provide an explanation

for why prior studies do not find the presumed negative association between accounting

profitability and takeover likelihood. These studies do not specify the non-linearity in the

relation between accounting profitability and takeover likelihood. Specifically, the

association is negative only when industry-adjusted profitability is negative, and it is

positive when industry-adjusted profitability is positive.

Our study also contributes to the literature on the role of managerial opportunism

in merger and acquisition activities. Prior work generally focuses on the characteristics of

the acquiring firms when studying takeover that are motivated by managerial

opportunism. They find that acquirer characteristics such as poor corporate governance,

high-free cash flow, and managerial overconfidence can facilitate managerial

opportunism in acquisition decisions (e.g., Morck et al. 1990; Malmendier and Tate 2008;

Masulis et al. 2007; Chen et al. 2007). There is limited examination of the characteristics

of target firms that facilitates managerial opportunism in acquisitions (Harford et al.

2012). We argue and show that targets with higher accounting profitability are more

likely to be associated with acquisitions motivated by managerial opportunism.

Specifically, our results suggest that the positive association between positive industry-

adjusted ROA and takeover probability is greater when the acquiring firms’ managers

have more opportunistic incentives; meanwhile, we do not observe this type of sensitivity

for the negative relation between takeover likelihood and negative industry-adjusted

ROA. We further show that acquisitions are more detrimental to the acquirers’

shareholders when the targets’ industry-adjusted ROA is higher. These results suggest

7

that acquiring managers end up destroying greater value of their firms upon the

acquisitions of targets with higher accounting profitability, further supporting managerial

opportunism as a reason for the positive relation between positive accounting profitability

and acquisition likelihood.

The remainder of the paper is organized as follows. Section 2 discusses prior

literature and develops the hypotheses. Section 3 and 4 present our research design and

empirical results, and Section 5 concludes.

2. Literature review and hypothesis development 2.1. Inefficient management hypothesis

Prior literature argues that takeover is an important mechanism in capital markets

to replace (and deter) firms that are operating inefficiently (e.g., Jensen 1986). Marris

(1963) and Manne (1965) argue that the failure to optimize operations creates a takeover

opportunity where an acquirer can replace inefficient managers with efficient ones. This

argument suggests that firms with lower accounting profitability are more likely to be

acquired (Palepu 1986). Prior studies, however, find that accounting profitability

measures are generally insignificant when included as independent variables in the

takeover probability models, and in a few cases when they are significant, the signs of the

coefficients are inconsistent.

2.2. Managerial opportunism hypothesis

Prior literature finds that agency conflicts affect acquisition decisions, because

they are large discretionary investments where the effect of the misalignment of

incentives between managers and shareholders of acquiring firms is potentially large (e.g.,

8

Jensen 1986; Morck et al. 1990; Lang et al. 1991; Harford 1999; Grinstein and Hribar

2004; Masulis et al. 2007; Harford and Li 2007; Fich et al. 2014). These studies argue

that the managerial benefits from acquiring create strong incentives to make acquisitions

even if they are not in the interest of shareholders. Furthermore, value-destroying

acquisitions are more likely when acquirers have greater free cash flow and low growth

opportunities (Jensen 1986; Lang et al. 1991; Harford 1999), and when acquirers have

poorer corporate governance and more entrenched managers (Masulis et al. 2007; Chen

et al. 2007).

Chang (1998), Fuller et al. (2002) and Harford et al. (2012) extend the literature

on managerial opportunism by investigating target characteristics related to value-

destroying acquisitions and find that private targets acquired with stock create value for

acquirers because they create a monitoring blockholder. We extend this literature by

examining the role of another target characteristic, the accounting profitability, in

suboptimal acquisitions motivated by managerial opportunism.

Managers have strong incentives to make acquisitions, even when they are value

destroying, because acquisitions increase their compensation, increase their likelihood of

becoming directors on other firms’ boards, and facilitate empire-building (Jensen 1986,

Grinstein and Hribar 2004; Harford and Li 2007; Harford and Schonlau 2013; Fich et al.

2014). Harford and Li (2007) and Fich et al. (2014) argue that CEOs compensation is

favorably affected from making acquisitions even when they are value destroying,

because the value of the flow of new stock grants after an acquisition exceeds the

negative impact on CEOs’ pre-acquisition portfolio from negative stock returns

associated with the acquisition. Harford and Schonlau (2013) argue that even value

9

destroying acquisitions increase CEOs’ likelihood of becoming directors because of their

acquisition related experience. These studies suggest that there are strong incentives to

make opportunistic acquisitions. We argue that managers making opportunistic

acquisitions have a greater preference to acquire targets with higher accounting

profitability because it can reduce the likelihood of post-acquisition management

turnover. The higher the accounting profitability of the target, the better the likelihood of

the survival of the combined entity and hence the lower the employment risk. Consistent

with this argument, Farrell and Whidbee (2003) and DeFond and Park (1999) show that

management turnover is negatively associated with industry-adjusted ROA and this

association is incremental to stock returns.2

A second argument for why firms with higher accounting profitability are more

likely to be acquired for opportunistic reasons is that managers have incentives to

manipulate earnings (e.g., Burgstahler and Dichev 1997; Matsumoto 2002; Skinner and

Sloan 2002; Donelson et al. 2013). Prior research shows that managers take a variety of

real actions for the purpose of earnings manipulation, such as cutting R&D and

advertising expenses, overproducing inventory, and providing sales incentives (e.g.,

Penman and Zhang 2002; Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin

2010). We argue that firms also use acquisitions to manipulate earnings. In general, the

greater the reported profitability of a firm, the more attractive it would be as a target for

2 Desai et al. (2006) find that ROA is negatively associated with turnover and this association is incremental to stock returns. In addition, Bens et al. (2011) find that acquiring managers are more likely to misstate post-acquisition financial statements when making value-destroying acquisitions (negative stock returns), consistent with our argument that post-acquisition accounting profitability is important to managers making opportunistic acquisitions.

10

acquirers seeking to show an increase in their reported profitability.3 Using acquisitions

for opportunistic reasons is plausible, given that prior studies have argued that managers

make acquisitions for empire building and for compensation purposes (Jensen 1986;

Grinstein and Hribar 2004; Harford and Li 2007; Fich et al. 2014). Anecdotal evidence

also suggests firms use acquisitions to meet their earnings benchmarks. General Electric’s

North American Chief of Retailer Financial Services stated that they “may hunt for

acquisitions if his division might miss its annual earnings target” (Smith et al. 1994).

The above arguments suggest that poorly performing firms are likely to be

acquired to enhance efficiency and the well performing firms are likely to be acquired for

opportunistic reasons. We use the industry average accounting profitability as the cutoff

for classifying firms as poorly or well performing. It is a common practice in the

corporate control literature to use variables adjusted for industry averages (Dietrich and

Sorensen 1984; Bruner 2004; Cremer et al. 2009; Chen et al. 2014). For the poorly

performing firms, we predict that the likelihood of acquisition is negatively associated

with the industry-adjusted accounting profitability because the scope of creating value by

improving management efficiency is likely to be greater in poorer performing firms. For

the well performing firms, we predict that the likelihood of acquisition is positively

associated with the industry-adjusted accounting profitability, because the more

profitable firms are more attractive as acquisition targets for opportunistic managers. We

therefore propose:

3 A firm with higher accounting profitability need not always lead to a greater increase in the acquirer’s accounting profitability. This is because the profitability of the combined entity is also affected by the target’s assets marked up from book value to fair value, which leads to additional expenses as well as an increase in the asset base. We expect that the presence of this factor will bias against finding results consistent with our predictions.

11

H1. Negative industry-adjusted accounting profitability is negatively associated with the takeover likelihood and positive industry-adjusted accounting profitability is positively associated with the takeover likelihood.

To further examine whether the positive association between the positive

industry-adjusted accounting profitability and takeover likelihood is driven by managerial

opportunism, we propose several additional hypotheses. In general, these hypotheses

state that this positive association is more pronounced when acquiring firms’ managers

have greater incentive to behave opportunistically. Specifically, their incentives would be

greater when their benefits from such acquisitions are larger and the costs of making such

acquisitions are smaller.

2.3 Factors affecting managerial benefits from acquisition of firms reporting higher profitability

We examine four different factors that are likely to affect the extent to which

managers of acquiring firms benefit from reporting higher reported profitability. First,

prior research argues that managers have strong capital market incentives to report higher

accounting profits (Levitt 1998; Subramanyam 1996; Barth et al. 1999; Skinner and

Sloan 2002). Prior research also shows that capital market pressure to manage reported

profitability is greater for public firms than for private firms (Klassen 1997; Ke et al.

1999; Beatty et al. 2002; Givoly et al. 2010). Furthermore, owners of private firms are

expected to be less likely to rely on earnings-based performance measures in monitoring

and compensating managers (Ke et al. 1999; Beatty et al. 2002). Thus, compared to

private acquirers, public acquirers are more likely to acquire targets for reporting

favorable accounting profitability.

12

H2a. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by public companies than by private companies.

Second, if acquirers use acquisitions to report higher accounting profitability for

the current period, then the time interval between the beginning of transaction

negotiations and the deal completion should be relatively short. For an acquisition to

affect the acquirers’ accounting profitability in the fiscal period of the acquisition

negotiations, the transaction must be completed in that fiscal period, resulting in a

quicker completion time. Moreover, managers making an opportunistic acquisition have

an incentive to shorten the completion time in order to reduce due diligence so that the

board of directors does not learn unfavorable information that can terminate the

acquisitions.

H2b. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions for which the time between the acquisition announcement and its completion date is relatively short.

Third, Barth et al. (1999) and Kasznik and McNichols (2002) find that firms with

patterns of increasing accounting earnings have higher price-earnings multiples than

other firms, and the price-earnings multiples decrease substantially when reported

profitability decreases after a long string of increases. Therefore, managers have

incentives to maintain patterns of increasing earnings, and prior research finds that firms

manage earnings to maintain the increasing pattern (e.g., Myers et al. 2007; Beatty et al.

2002). We predict that acquirers with a pattern of increasing accounting earnings in prior

years are more likely to acquire targets with higher accounting profitability.

H2c. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by companies with a pattern of increase in accounting earnings over prior years than by companies without such a pattern.

13

Fourth, managers with overvalued equity are more likely to make opportunistic

acquisitions (Fu et al. 2013). They would have an incentive to show high accounting

profitability in order to maintain their own equity value (Jensen 2005; Chu et al. 2015).

Thus, acquirers with a higher valuation premium are more likely to acquire targets with

higher accounting profitability.

H2d. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by companies with high price to earnings ratios. Finally, firms have incentives to meet or beat earnings benchmarks (e.g.,

Burgstahler and Dichev 1997; Roychowdhury 2006; Donelson et al. 2013), so firms that

meet or just beat earnings benchmarks are more likely to have managed earnings.

Acquirers making opportunistic acquisitions would avoid missing post-acquisition

earnings benchmarks to reduce scrutiny of their acquisition decision. Thus, we argue that

acquirers that meet or just beat earnings benchmarks in the year of the acquisition are

more likely to have acquired targets with higher accounting profitability.

H2e. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by companies that meet or just beat earnings benchmarks than by other companies. 2.4 Factors affecting costs to managers related to opportunistic acquisition

We examine several factors that are likely to affect the costs incurred by

managers when making opportunistic acquisitions. The smaller these costs, the more

likely managers would make opportunistic acquisitions, and hence more pronounced will

be the association between accounting profitability of a firm and the likelihood of its

acquisition.

14

First, Jensen (1986) argues that firms generating free cash flow but having poor

investment opportunities are likely to invest free cash flow rather than pay dividends or

repurchase shares. Lang et al. (1991) and Harford (1999) find that firms with low Tobin’s

Q and high free cash flow make acquisitions motivated by managerial opportunism,

consistent with Jensen’s (1986) arguments. Thus, we predict that if acquirers are subject

to greater agency costs of free cash flow, it would be less costly for its mangers to make

opportunistic acquisitions.

H3a. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by companies that are subject to greater agency costs of free cash flows.

Second, prior research finds that managers of firms with greater ownership by

institutional investors are less likely to behave opportunistically, presumably due to

stronger monitoring (McConnell and Servaes 1990; Dechow et al. 1996; Bushee 1998;

Roychowdhury 2006; Chen et al. 2007; Zang 2012). Thus, we predict that it would be

more costly for managers of acquiring firms with blockholders to make opportunistic

acquisitions.

H3b. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by companies without blockholders than by companies with blockholders.

Third, greater board independence is also shown to be associated with more

value-enhancing acquisitions (Byrd and Hickman 1992) and less earnings management

(Dechow et al. 1996; Klein 2002). These results suggest that the better monitoring by

boards that are more independent would make it more costly for managers to make

acquisitions motivated by managerial opportunism.

15

H3c. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by companies with less independent board of directors.

Acquisitions motivated by managerial opportunism can severely affect the

survivability of acquiring firms that are already in financial distress, because they have

fewer resources that can be redirected from best use (Zang 2012). The survival risk of the

firm can in turn adversely affect the employment risk of the managers. We therefore

predict the following:

H3d. The proposed positive association between positive industry-adjusted accounting profitability and takeover likelihood is more pronounced for acquisitions by companies that are less financially distressed.

2.5 Acquirer’s stock price reaction to the announcement of acquisition

We argue that acquiring firms’ managers would sacrifice greater firm value when

they acquire targets with higher accounting profitability. This is because the acquisitions

are likely to be motivated to a greater extent by the self-interests of the acquirers’

management, who would be willing to overpay more for targets with higher accounting

profitability.

H4. Among acquisitions of targets with positive industry-adjusted ROA, acquirers’ stock returns at the announcements of the acquisition deals are significantly lower when the targets have more positive industry-adjusted ROA.

3. Research methodology

16

3.1. Takeover model

To examine whether target firms’ accounting profitability is associated with their

likelihood of being acquired, we estimate a modified version of Cremers et al. (2009)

model, which controls for factors that prior literature finds to be associated with takeover

probability (e.g., Dietrich and Sorensen 1984; Palepu 1986; Ambrose and Megginson

1992; Edmans et al. 2012):

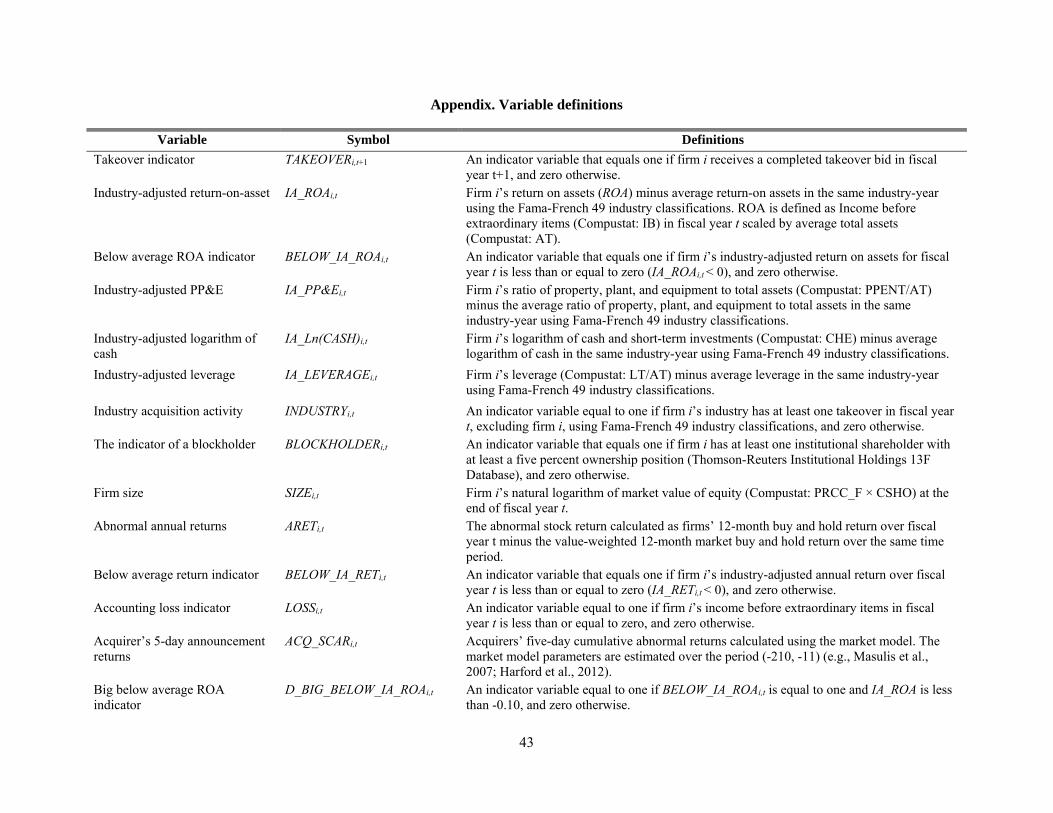

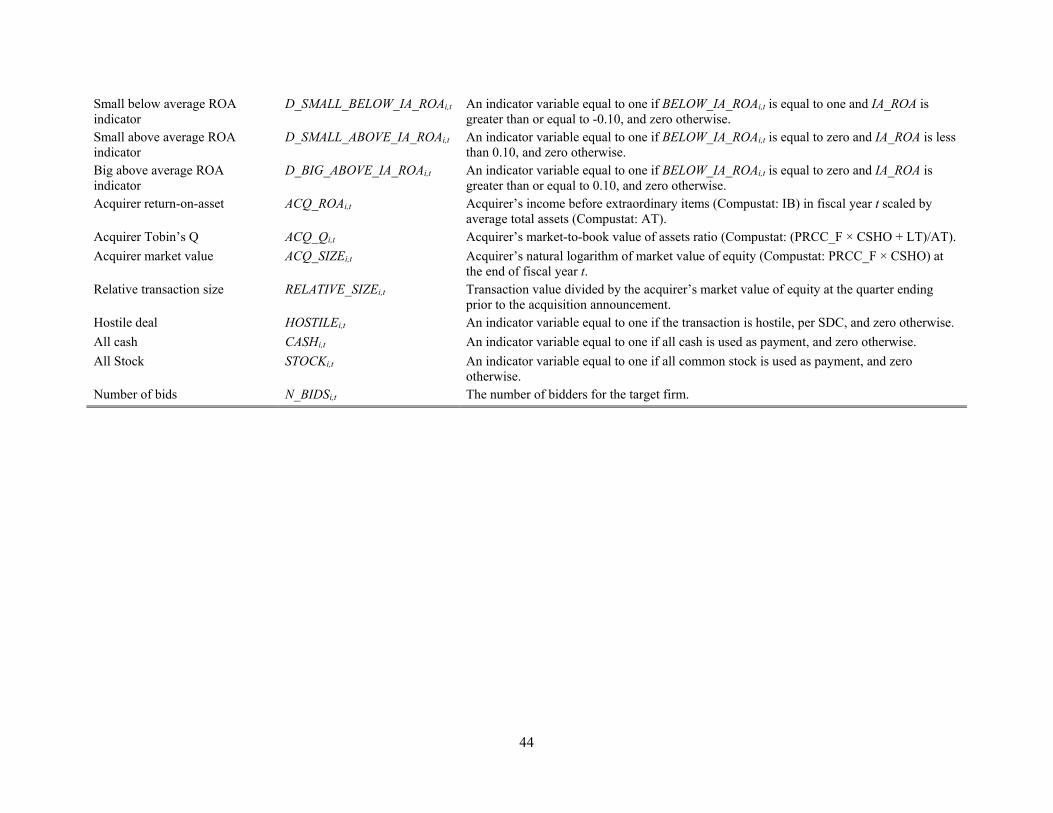

TAKEOVERi,t+1 = α0 + α1 IA_Qi,t + α2 IA_PP&Ei,t + α3 IA_Ln(CASH)i,t + α4 BLOCKHOLDERi,t + α5 SIZEi,t + α6 INDUSTRYi,t + α7 IA_LEVERAGEi,t + α8 ARETi,t + α9 LOSSi,t + α10 IA_ROAi,t + εt ,

(1)

where TAKEOVERi,t is an indicator variable that equals one if firm i receives a completed

takeover bid in fiscal year t+1, and zero otherwise; IA_Qi,t is Tobin’s Q adjusted for the

industry mean for firm i and year t; IA_PP&Ei,t is the ratio of net plant, property, and

equipment (PP&E) to total assets adjusted for industry mean; IA_Ln(CASH)i,t is the

natural logarithm of cash holdings adjusted for the industry mean; BLOCKHOLDERi,t is

an indicator variable that equals one if firm i has at least one institutional shareholder

with at least a five percent ownership position, and zero otherwise; SIZEi,t is the natural

logarithm of the market value of equity at the end of fiscal year t; INDUSTRYi,t is an

indicator variable equal to one if the industry has at least one takeover in fiscal year t, and

zero otherwise; IA_LEVERAGEi,t is the leverage ratio, defined as total liabilities divided

by total assets, adjusted for the industry mean; ARETi,t is the abnormal stock return

calculated as firms’ 12-month buy and hold return over fiscal year t minus the value-

weighted 12-month market return over the same time period. LOSSi,t is an indicator

variable equal to one if income before extraordinary items in fiscal year t is less than or

equal to zero, and zero otherwise. IA_ROAi,t is income before extraordinary items divided

17

by average total assets, adjusted for the industry mean. Our analysis primarily focuses on

industry-adjusted ROA because a target firm’s peers are potential alternative targets for

the acquirer, and the selection of target firms involves an in-depth comparison of peer

firms (Bruner 2004; Pearl and Rosenbaum 2009; Chen et al. 2014). Consistent with this

notion, it is common in the mergers and acquisitions literature to do industry adjustments

when analyzing takeover decisions. All industry-adjusted variables are calculated by

subtracting the industry mean where industries are defined by Fama-French 49 industry

classifications (Fama and French 1997). All continuous variables are winsorized at the 1st

and 99th percentiles, and details of variable definitions are provided in the Appendix.

Since we have opposite predictions for the relations between accounting

profitability and the likelihood of takeover for firms whose ROA is above the industry

average and whose ROA is below the industry average, we modify Eq. (1) in two ways.

We expect a positive correlation between TAKEOVERi,t+1 and IA_ROAi,t (α10 > 0) for

firm-years with IA_ROAi,t ≥ 0 and a negative correlation between TAKEOVERi,t+1 and

IA_ROAi,t (α10 < 0) for firm-years with IA_ROAi,t < 0. First, we include an interaction

term, IA_ROAi,t × BELOW_IA_ROAi,t, to differentiate when firms’ ROA is above or

below the industry average. BELOW_IA_ROAi,t is equal to one if IA_ROAi,t is less than or

equal to zero, and zero otherwise. The coefficient on IA_ROAi,t captures the association

with takeover probability when ROA is above the industry average and we expect the

coefficient to be positive. The coefficient on IA_ROAi,t × BELOW_IA_ROAi,t captures the

difference in the association with takeover probability when ROA is above and below the

industry average and we expect the coefficient to be negative. Second, we estimate Eq. (1)

18

separately for firm-years with IA_ROAi,t ≥ 0 and with IA_ROAi,t < 0 with the expectation

that the coefficient on IA_ROAi,t is positive and negative, respectively.

3.2. Sample selection

Our initial sample consists of all firm-years for the period 1990 to 2012 on the

Compustat annual file with the necessary data available to calculate our variables. We

identify firms that are acquired from 1991 to 2013 using the Securities Data Corporation

(SDC) M&A database. We consider a transaction to be an acquisition when a majority of

the target firm is acquired, which SDC classifies as acquisitions of assets (AA),

acquisitions of majority interest (AM), and mergers (M). Stock return data are obtained

from the CRSP stock files. Our sample begins at 1990 because SDC coverage in the

1980’s is not as complete as in the later periods. We exclude financial firms (SIC codes

6000 through 6999) because they have a different regulatory structure than other firms.

Our final sample consists of 78,073 firm-year observations of which there are 3,533

takeovers.

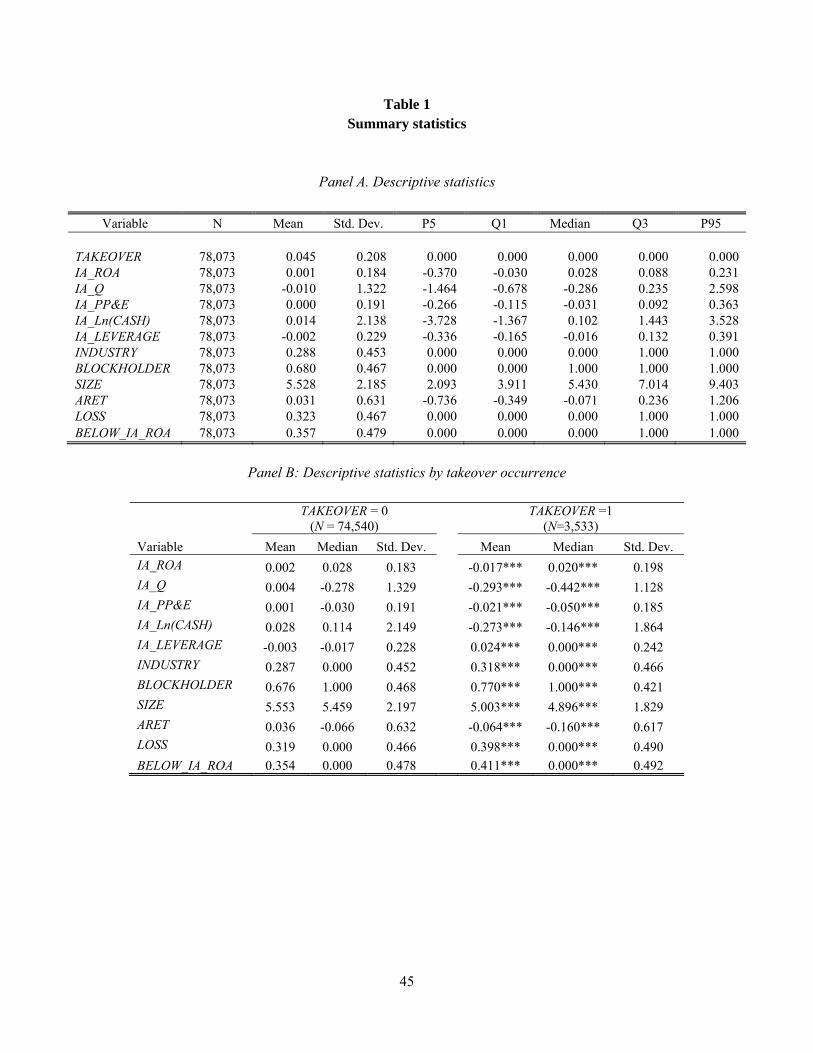

Table 1, Panel A presents the descriptive statistics of our main variables. The

mean value of TAKEOVER indicates that on average firms face a 4.5 percent

unconditional takeover probability. The variables adjusted by industry have mean values

close to zero by construction. The remaining variables mean and median values appear to

be consistent with prior research. Panel B presents the descriptive statistics for takeover

and non-takeover firms separately and tests whether the mean and median values are

significantly different between the two groups. Takeover firms have significantly lower

industry-adjusted ROA than non-takeover firms. Therefore, the univariate statistics are

consistent with the inefficient management hypothesis that firms with poorer

19

performance are more likely to be acquired. The differences in control variables are

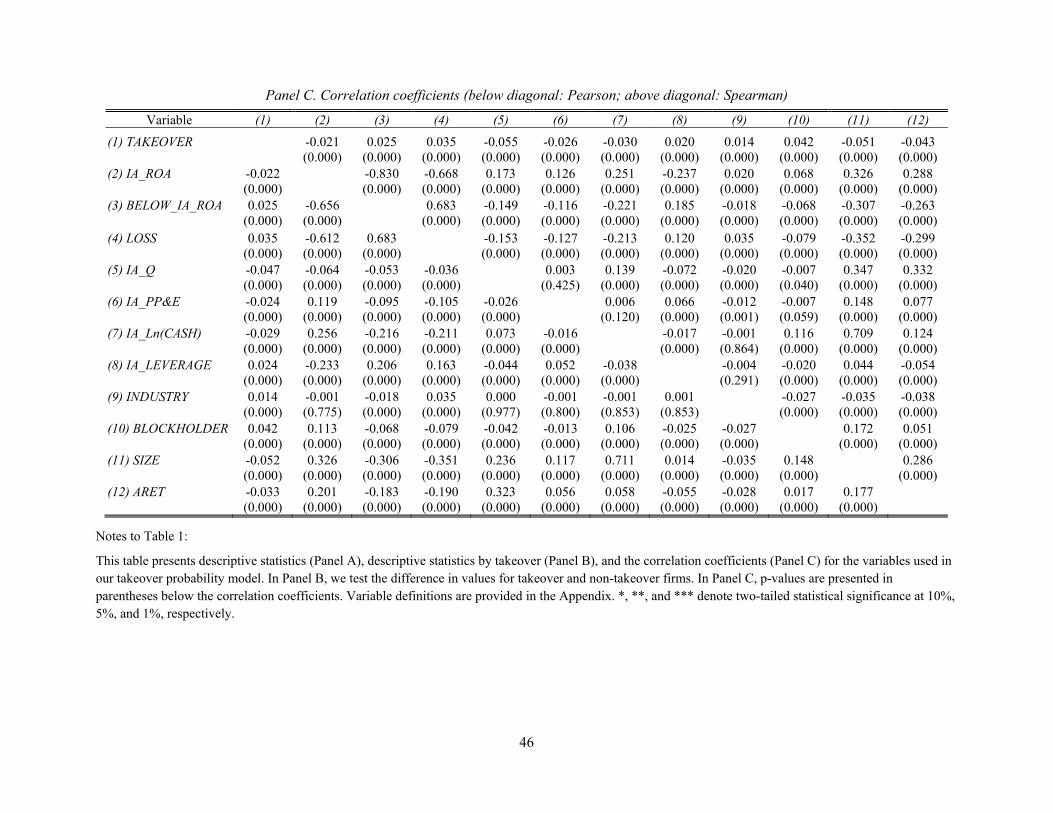

consistent with our expectations. Panel C presents the Spearman and Pearson correlation

coefficients for the variables in our model. IA_ROA is significantly negatively correlated

(Spearman and Pearson) with TAKEOVER, which is also consistent with the inefficient

management hypothesis. We examine this association further in our takeover probability

model.

4. Empirical results

4.1. Test of the piecewise linear relation between accounting profitability and

takeover probability (H1)

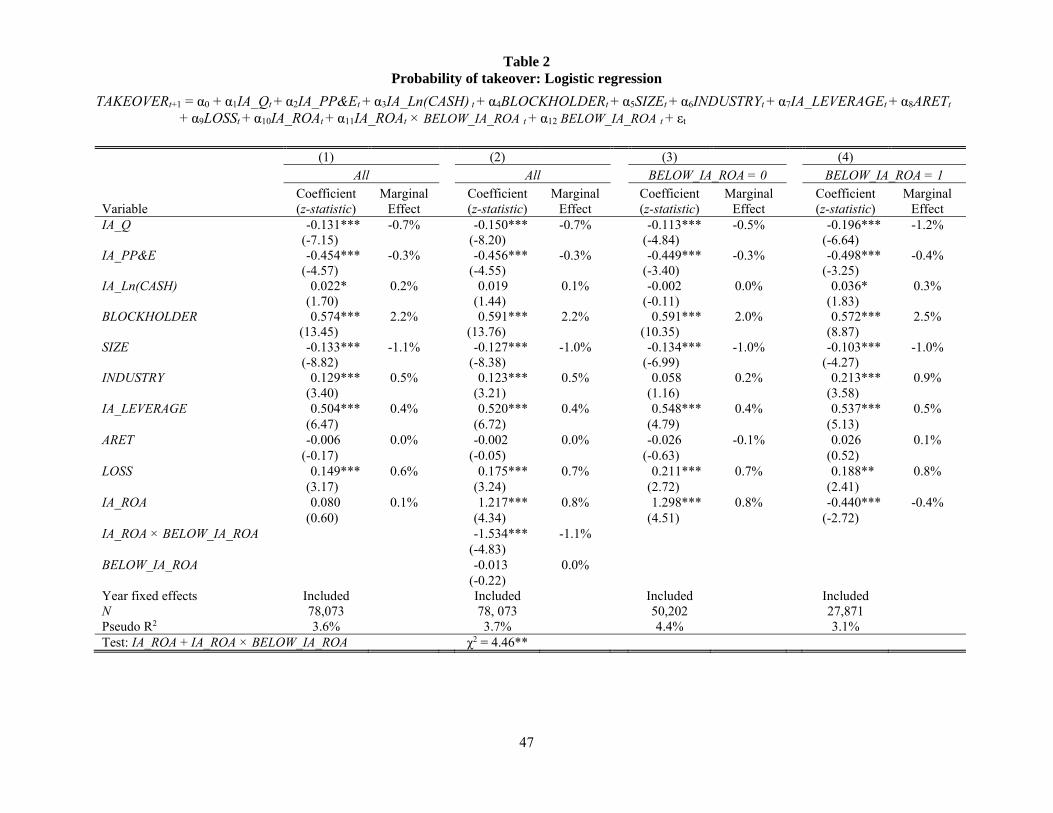

Table 2 presents the results from estimating the takeover probability model. The

main independent variable of interest is industry-adjusted ROA, IA_ROA. The results on

control variables are consistent with prior research (Dietrich and Sorensen 1984; Palepu

1986; Ambrose and Megginson 1992; Cremers et al. 2009; Cai and Tian 2009; Edmans et

al. 2012). The negative coefficient on IA_Q is consistent with more highly valued firms

being less likely to be acquired (Cremers et al. 2009; Edmans et al. 2012). The negative

coefficient on IA_PP&E is consistent with it being costlier to merge firms with fixed

assets than intangible assets (Cai and Tan 2009; Ali and Kravet 2014). We find that the

presence of blockholders is positively associated with takeover (Cremers et al. 2009;

Edmans et al. 2012), consistent with the superior monitoring ability of blockholders

(Shleifer and Vishny 1986). The significantly negative coefficient on firm size is

consistent with greater transaction costs to acquiring larger firms (Palepu 1986; Cremers

et al. 2009). Firms are more likely to be acquired if there was at least one acquisition in

their industry in the prior year (Cremers et al 2009). Consistent with prior research

20

(Cremers et al. 2009; Ali and Kravet 2014), we also find that IA_LEVERAGE is

positively associated with takeover probability consistent with distressed firms becoming

takeover targets because their excessive leverage limits their access to financing.4 Finally,

the coefficient on LOSS is positive and significant, suggesting that loss firms are more

likely to be takeover targets, consistent with the efficient management hypothesis.

The coefficient on IA_ROA in column 1 is 0.080 and not significant at

conventional levels, consistent with the results of prior research. In column 2, we modify

equation 1 to test for non-linearity in the association between TAKEOVER and IA_ROA

by including IA_ROA × BELOW_IA_ROA and BELOW_IA_ROA in the model. The

coefficient on IA_ROA is significantly positive and the coefficient on IA_ROA ×

BELOW_IA_ROA is significantly negative, indicating a non-linear association between

takeover probability and accounting profitability. The coefficient on IA_ROA + IA_ROA

× BELOW_IA_ROA is also significantly negative, indicating that IA_ROA is negatively

associated with takeover probability when ROA is below the industry average.

In columns 3 and 4, we estimate Eq. (1) for observations where BELOW_IA_ROA

is equal to zero and one, respectively. When firms’ ROA is greater than their industry

average ROA (column 3), there is a significantly positive association between IA_ROA

and takeover probability. To illustrate the economic significance of these results, we

report next to each coefficient the change in probability of a takeover due to a one

standard deviation increase in each independent variable (from 0 to 1 for indicator

variables), holding all other variables at their mean value. In column 3, a standard

4 The coefficient on ARET is not significant. However, when we measure abnormal stock returns over the past four-year period, as in Palepu (1986), we obtain a significantly negative coefficient. We use one-year abnormal returns in our models following the specification in recent studies. However, all our results are robust to using abnormal returns over the four-year period.

21

deviation increase in IA_ROA is associated with an increase in takeover probability of 0.8

percent, which is a 17.8 percent increase relative to the unconditional probability of

takeover (4.5 percent) in our sample. The two largest effects for the variables in our

model are 2.0 and -1.0 percent for BLOCKHOLDER and SIZE, respectively, suggesting

that IA_ROA has an economically significant association with takeover probability. When

firms’ ROA are less than their industry average ROA (column 4), there is a significantly

negative association between IA_ROA and takeover probability. When IA_ROA is

negative, a standard deviation decrease in IA_ROA is associated with an increase in

takeover probability of 0.4 percent, which is an 8.9 percent increase relative to the

unconditional probability. In sum, industry-adjusted ROA has a non-linear and

economically significant association with takeover probability.

The negative association between takeover probability and negative industry-

adjusted ROA is consistent with the efficient management hypothesis, in that there is

greater potential to unlock the value of a poorer performing firm through efficient

management.5 We argue that the positive association between takeover probability and

positive industry-adjusted ROA reported in Table 2 is due to managerial opportunism. To

support this argument, we conduct several cross-sectional tests to see whether this

positive association is more pronounced when acquiring managers’ incentives to make

opportunistic acquisitions of targets with higher accounting profitability are greater. We

consider scenarios where the greater incentives are due to greater personal benefits to

5 As noted earlier, the coefficient on LOSS is positive and significant, in all the models, suggesting that loss firms are more likely to be takeover targets, consistent with the efficient management hypothesis. Negative industry-adjusted ROA is also related to the takeover likelihood, presumably because this variable captures the magnitude of poor performance and thus the amount of improvement that is likely through efficient management.

22

managers from making the acquisitions or due to lower costs incurred by managers from

making the acquisitions.

4.2. Benefits from opportunistic acquisitions of profitable targets (hypothesis H2)

We expect that the positive association between takeover likelihood and positive

industry-adjusted ROA is more pronounced under situations when acquirers’ managers

are likely to benefit more from acquisitions of targets with higher accounting profitability.

We propose such situations to be the ones where acquirers are publicly held as against

privately held (H2a), complete the acquisition transaction quickly (H2b), have a long

pattern of earnings increases (H2c), have a high price to earnings ratio (H2d), and just

meet or beat earnings benchmarks (H2e).

To test hypotheses H2b through H2e we estimate a multinomial logistic model

and create a categorical dependent variable, TO_ACQ_BENEFIT, that is equal to one if a

firm receives a completed takeover bid in year t+1 by a publicly held acquirer with

greater benefits to making opportunistic acquisitions to report higher accounting

profitability (Acquirer_Short_Interval, Acquirer_String, Acquirer_High_PE, and

Acquirer_Suspect), equal to two if a firm receives a completed takeover bid in year t+1

by a publicly held acquirer with less benefits to making opportunistic acquisitions to

report higher accounting profitability (Acquirer_Long_Interval, Acquirer_No_String,

Acquirer_Low_PE, and Acquirer_Nonsuspect), equal to three if a firm receives a

completed takeover bid in year t+1 by a private acquirer or an acquirer where data is not

available to calculate the measure of costs to making opportunistic acquisitions to report

higher profitability (Private/Public Unknown), and zero if a firm is not acquired. We

23

discuss below each of the different measures we use for the benefits to making

opportunistic acquisitions to report higher accounting profitability.

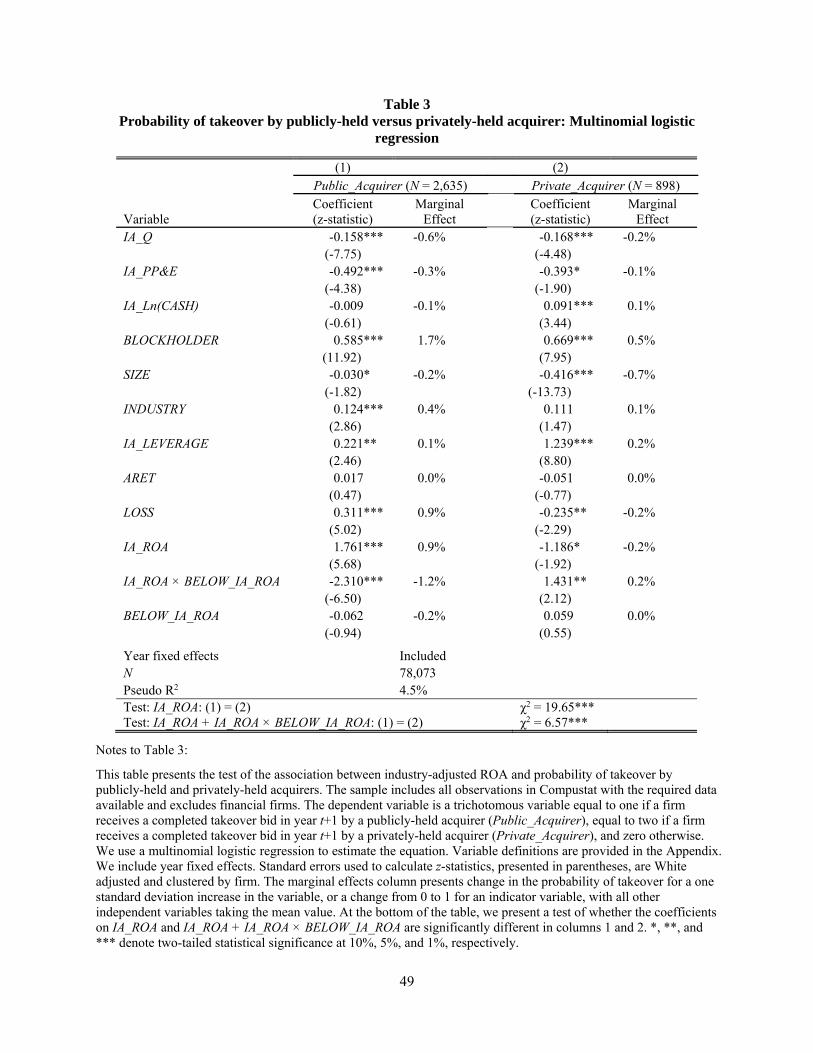

4.2.1. Public versus private acquirers (H2a)

To test hypothesis H2a, we estimate a multinomial logistic model and create a

categorical dependent variable that is equal to one if the firm receives a completed

takeover bid in year t+1 by a public acquirer (Public_Acquirer), equal to two if the firm

receives a completed takeover bid in year t+1 by a private acquirer (Private_Acquirer),

and zero if the firm is not acquired. We expect that, the positive association between

takeover likelihood and positive industry-adjusted ROA is likely to be more pronounced

for public acquirers than for private acquirers. The results are presented in Table 3.

Column 1 and 2 present the coefficient estimates where the outcome is takeover by a

public acquirer and private acquirer, respectively. Column 1 shows a significant non-

linear association between accounting profitability and takeover probability by public

acquirers, similar to the results in Table 2. Interestingly, in column 2, the results on the

accounting profitability variables are opposite to that in column 1. Takeover probability

by private acquirers is negatively associated with positive industry-adjusted ROA, when

this association is positive for acquisitions by public companies. This result can

potentially be explained by targets with higher accounting profitability being less

attractive to private companies, because opportunistic managers of public acquirers are

willing to pay a premium for such firms. Furthermore, the coefficient on IA_ROA +

IA_ROA × BELOW_IA_ROA is significantly more negative in column 1 than column 2.

This result is consistent with the findings in prior literature that private acquirers prefer

24

mature targets with a stable cash flow stream (Jensen 1986; Bargeron et al. 2008; Eckbo

and Thorburn 2008). Bargeron et al. (2008) find that compared to public acquirers,

private acquirers are more likely to select targets with lower growth opportunities and

higher cash flow from operations. Target firms with lower earnings are likely to have

lower free cash flow and thus would be less attractive for private acquirers.6 Overall, the

results suggest that, compared to private acquirers, public acquirers are more likely to

select targets with higher accounting profitability, thus supporting the managerial

opportunism explanation for the positive association between acquisition likelihood and

positive industry-adjusted accounting profitability.

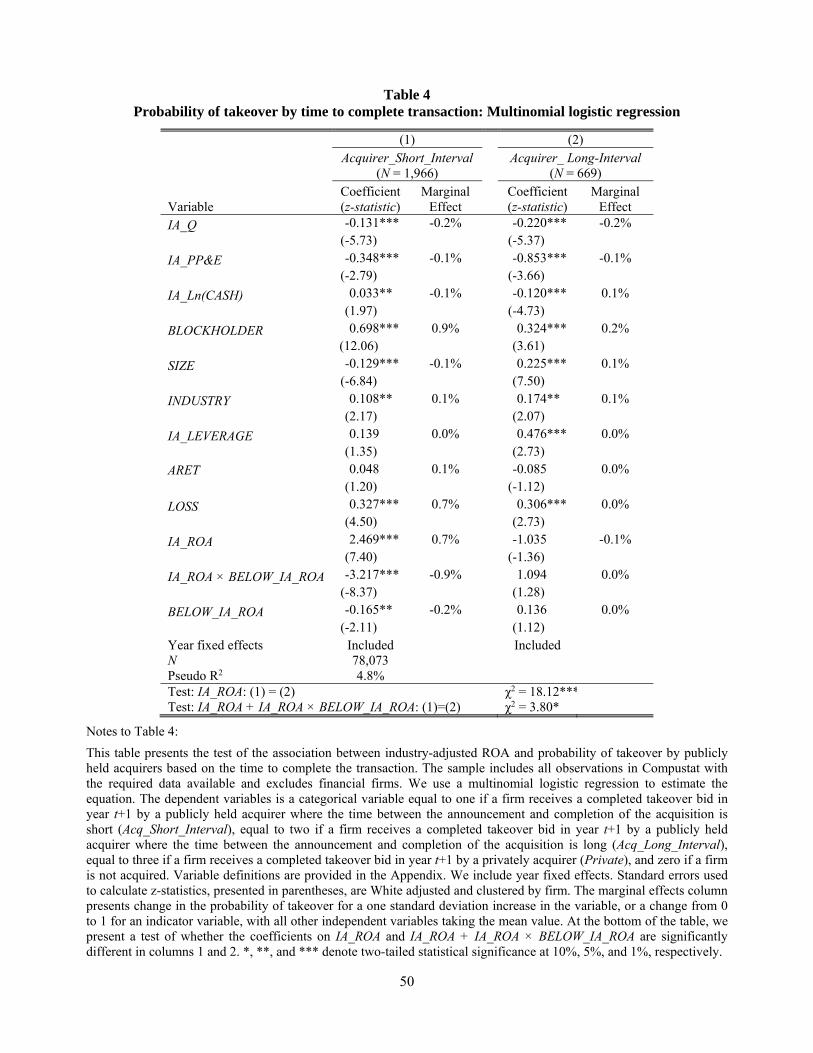

4.2.2. Acquisition completion time (H2b) We predict that the benefits to opportunistically using acquisitions to report

higher profitability are larger when acquisitions are completed faster. We measure

acquisition completion time as the time interval between the acquisition announcement

date and completion date. We consider this time interval as short when it is less than the

third quartile of the distribution in our sample (Acquirer_Short_Interval), and consider it

to be long when it is greater than the third quartile (Acquirer_Long_Interval).7

The results are presented in Table 4. We find that the positive association between

positive industry-adjusted accounting profitability and acquisition likelihood is more

pronounced for acquirers that complete the transaction more quickly. The coefficient on

IA_ROA is significantly positive in column 1 but insignificant in column 2 and the

6 Results for control variables are also consistent with this notion. Firms with more cash and without losses are also more likely to be acquired by private acquirers but not public acquirers. 7 In our sample, the third quartile is a 147 day difference between the acquisition announcement and completion date. Our findings do not change if we use the median value of 98 days.

25

difference in coefficients between column 1 and 2 is statistically significant. These results

are consistent with quick completion time facilitating acquisitions used to report higher

profitability and avoiding due diligence oversight.

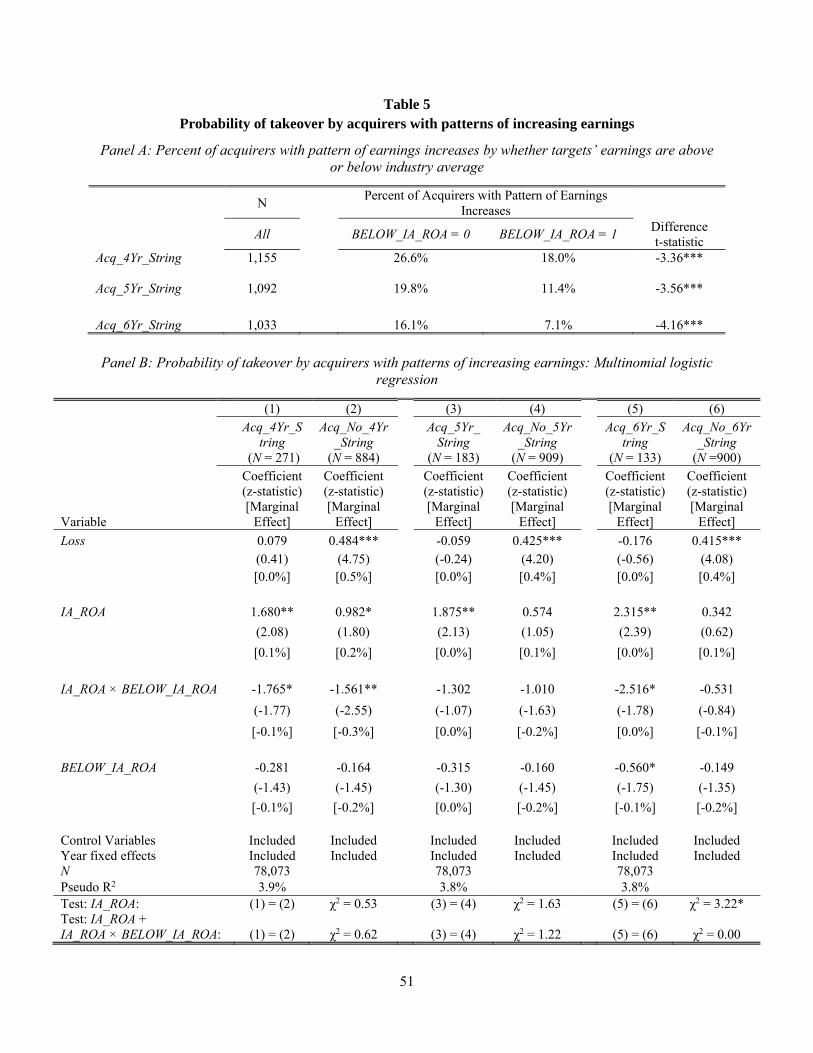

4.2.3. Acquirers with patterns of increasing earnings (H2c)

We expect that the positive association between acquisition likelihood and

positive industry-adjusted accounting profitability is more pronounced for acquirers with

long strings of earnings increases than for acquirers without such a pattern. We examine

four, five, and six years of annual earnings increases, because Barth et al. (1999) show

that firms price-earnings multiples are affected favorably after a string of five annual

earnings increases. If a firm uses an acquisition to opportunistically influence investors’

perception that it has maintained a string of earnings increases, then the time to complete

the acquisition is likely to be short so that the shortfall in the forthcoming earnings of the

acquirer can be addressed. Accordingly, we define an acquirer as having a string of

earnings increases prior to an acquisition when they report a pattern of annual earnings

increases and where the time to completion is below the third quartile for our sample

(Acq_4yr_String, Acq_5yr_String, and Acq_6yr_String). Acquirers reporting at least one

annual earnings decrease in the period before the acquisition announcement are

considered not to have a pattern of earnings increases (Acq_No_4yr_String,

Acq_No_5yr_String, and Acq_No_6yr_String).

Table 5, Panel A presents a comparison of the percentage of acquirers with a

pattern of earnings increases for acquisitions where the target’s ROA are above and

below the industry average. There are 1,155, 1,092, and 1,033 acquisitions where data are

26

available to calculate acquirers’ earnings pattern over four, five, and six years,

respectively. We observe that the percentage of acquirers with patterns of four, five, and

six annual earnings increases is significantly higher when the targets’ earnings are above

the industry average than when they are below the industry average. This result is

consistent with firms making acquisitions of targets with higher ROA to maintain

patterns of earnings increases or firms avoiding acquisitions of targets with lower ROA to

maintain patterns of earnings increases.

Panel B presents the results from the multinomial logistic regressions. Columns 1

and 2 present the results based on four years of earnings increases. For brevity, hereafter

we do not present the coefficients for the probability of being acquired by a private

acquirer or public acquirer without the required data (Private/Public Unknown).8 In this

table, we also do not present coefficients for the control variables. In columns 1 and 2,

the coefficient on IA_ROA is significantly positive. This result indicates that firms with

higher accounting profitability are more likely to be acquired by acquirers with and

without four years of annual earnings increases. In column 3, the coefficient on IA_ROA

is significantly positive while the coefficient on IA_ROA in column 4 is insignificant.

This result indicates that the positive association between positive industry-adjusted

accounting profitability and takeover likelihood is more pronounced for acquirers with

five years of annual earnings increases but not for acquirers without five years of

earnings increases. We find the strongest results in columns 5 and 6 when examining

acquirers with six years of earnings increases. The coefficient on IA_ROA is significantly

positive in column 5 but is insignificant in column 6, and the difference in these

8 When examining the probability of takeover by private acquirers as a separate outcome in this test and those below we find similar results to those reported in Table 3.

27

coefficients is statistically significant. This result is consistent with acquirers with six

years of earnings increases making acquisitions of targets with higher accounting

profitability, presumably to maintain their patterns of earnings growth.

We also find that acquirers without a pattern of earnings increases (columns 2, 4,

and 6) are more likely to acquire targets reporting losses while acquirers with patterns of

earnings increases (columns 1, 3, and 5) are not more likely to acquire targets reporting

losses. This result is consistent with acquirers not reporting patterns of earnings increases

before acquisitions being less likely to make opportunistic acquisitions and therefore,

more likely to acquire loss firms.

In a supplemental untabulated analysis, we find that when targets’ ROA is above

(below) the industry average, there is a positive (no) association between targets’ ROA

before the acquisition completion date and acquirers’ post-acquisition ROA for the three

years subsequent to the acquisition completion. These results are consistent with target’s

ROA persisting in acquirers’ post-acquisition ROA when acquirers are expected to use

acquisitions to increase ROA and not persisting when acquirers are expected to use

acquisitions to restructuring targets so that low profitability does not persist.

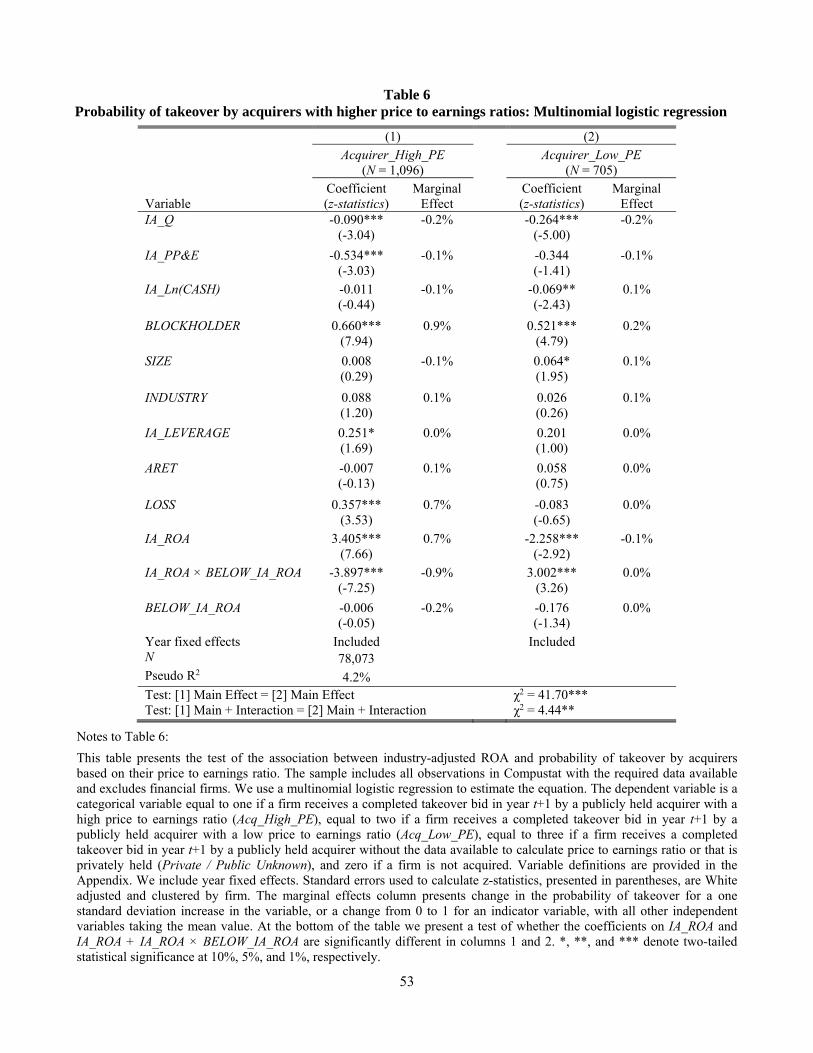

4.2.4. Acquirers with high price to earnings ratios (H2d) We expect that the benefits to making acquisitions to report higher profitability

are greater when acquirers have a high valuation premium. Consistent with Chu et al.

(2015) we use the price to earnings ratio to measure valuation premium. We classify

acquirers’ valuation premium as high when their price to earnings ratio is above the

28

annual industry average (Acquirer_High_PE) and classify it as low when it is below

(Acquirer_Low_PE).

The results are presented in Table 6. We find that the positive association between

positive industry-adjusted accounting profitability and takeover likelihood is more

pronounced for acquirers with a higher valuation premium. The coefficient on IA_ROA is

significantly positive in column 1. Interestingly, the coefficient on IA_ROA in column 2

is significantly negative, indicating that firms with higher accounting profitability are less

likely to be acquired by acquirers with a low valuation premium. This result can

potentially be explained by targets with higher accounting profitability being more costly

to acquire, because high valuation acquirers are willing to pay a premium for such firms.

The coefficient on IA_ROA + IA_ROA × BELOW_IA_ROA is significantly more negative

in column 1 than column 2, which is consistent with low valuation acquirers being

inefficient and less likely to acquire inefficient targets based on the inefficient

management hypothesis.9 Overall, the results are consistent with high valuations creating

an incentive for acquirers to select targets with higher accounting profitability.

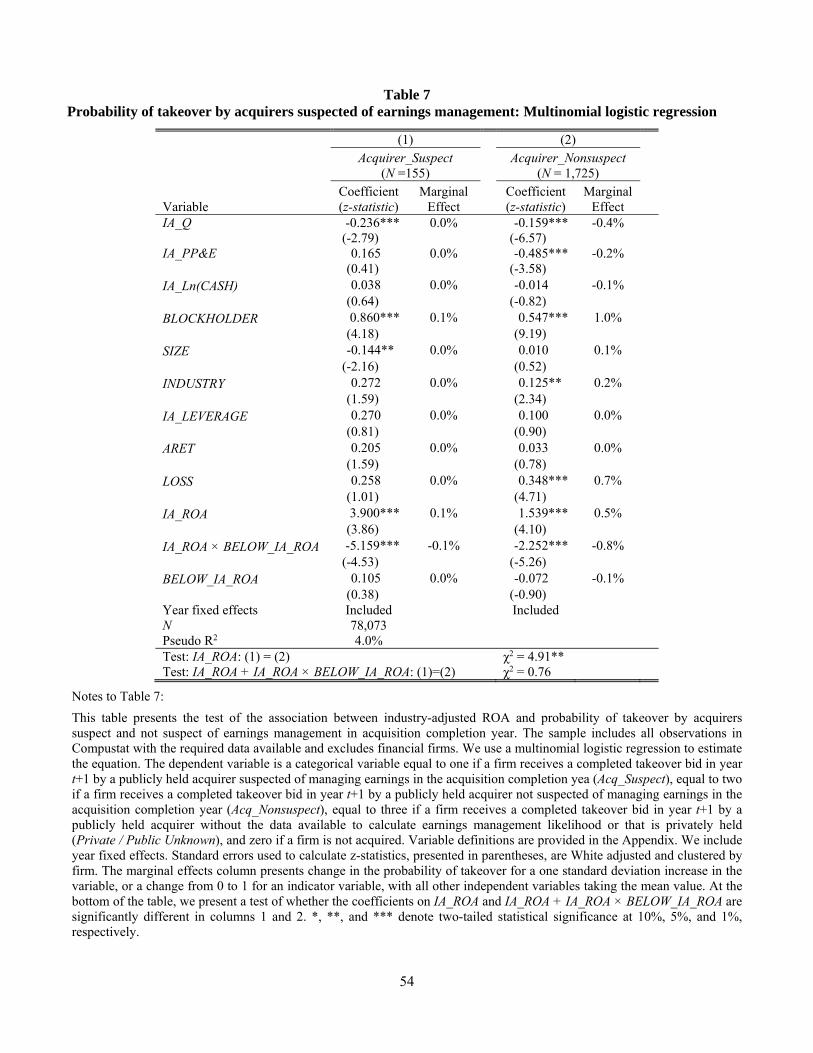

4.2.5. Acquirers suspected of managing earnings to meet or beat earnings benchmarks

in acquisition completion year (H2e) We expect that the benefits to making acquisitions to report higher profitability

are greater when the acquisitions help firms to meet or beat post-acquisition earnings

targets than when the acquisitions do not help firms meet or beat targets. We classify

acquirers as likely using the acquisition to meet or beat earnings targets when acquirers

reporting earnings in the acquisition completion year are suspect of being managed

(Acquirer_Suspect). We follow Cohen et al. (2008) to identify such “suspect” acquirers 9 The inefficient management hypothesis predicts that efficient firms acquire inefficient firms.

29

based on three benchmarks that firms typically have incentives to meet. First, we label an

acquirer as a “suspect” if in the 365-day period after the acquisition completion date it

reports net income before extraordinary items scaled by total assets lies in the interval [0,

0.005). Also, we identify an acquirer as a “suspect” if in the 365-day period after the

acquisition completion date the change in net income before extraordinary items scaled

by total assets lies in the interval [0, 0.005). For the final benchmark, we label an acquirer

as a “suspect” if in the 365-day period after the acquisition completion date analysts’

forecast error (FE) is one cent per share or less ($0.00 ≤ FE ≤ $0.01). We compute the FE

as the difference between actual earnings per share (EPS) and the consensus forecast,

which is the median of the forecasts announced in the 365-day period prior to the

acquisition completion date. We classify acquirers as nonsuspect when they report

earnings in the acquisition completion year that does not meet any of the above criteria

(Acquirer_Nonsuspect).

The results are presented in Table 7. We find that the positive association between

positive industry-adjusted accounting profitability and takeover likelihood is more

pronounced for acquirers with suspect earnings than those without suspect earnings. The

coefficient on IA_ROA is significantly positive in column 1 and 2. However, the

coefficient on IA_ROA is significantly higher in column 1 than column 2, indicating that

targets with higher profitability are more likely to have been acquired by acquirers

suspected of managing earnings than other acquirers. The coefficient on IA_ROA +

IA_ROA × BELOW_IA_ROA is not significantly different in columns 1 and 2. Overall,

the results are consistent with acquirers successfully managing earnings to meet or beat

earnings benchmarks by selecting targets with higher accounting profitability,

30

presumably because these targets enable the acquirers to meet or beat earnings

benchmarks.

4.3. Costs related to opportunistic acquisitions of profitable targets (H3)

We predict that the positive association between industry-adjusted accounting

profitability and takeover likelihood is likely to be less pronounced for acquirers

incurring greater costs in making opportunistic acquisitions. We identify acquirers

incurring lower costs as those that have high free cash flow and low growth opportunities

(H3a), have no blockholders (H3b), have less independent boards (H3c), and are less

financially distressed (H3d). To test hypotheses H3a through H3d, we estimate a

multinomial logistic model and create a categorical dependent variable, TO_ACQ_COST,

that is equal to one if a firm receives a completed takeover bid in year t+1 by a publicly-

held acquirer with lower costs to making opportunistic acquisitions

(Acquirer_HighFCF_LowQ, Acquirer_NoBlock, Acquirer_Brd_NoInd, and

Acquirer_High_Zscore), equal to two if a firm receives a completed takeover bid in year

t+1 by a publicly-held acquirer with higher costs to making opportunistic acquisitions

(Acquirer_Other, Acquirer_Block, Acquirer_Brd_Ind, and Acquirer_Low_Zscore), equal

to three if a firm receives a completed takeover bid in year t+1 by a privately-held

acquirer or an acquirer where data are not available to calculate the measures of costs

related to making opportunistic acquisitions (Private/Public Unknown), and zero if a firm

is not acquired. We discuss below each of the different measures we use for the costs to

making opportunistic acquisitions.

31

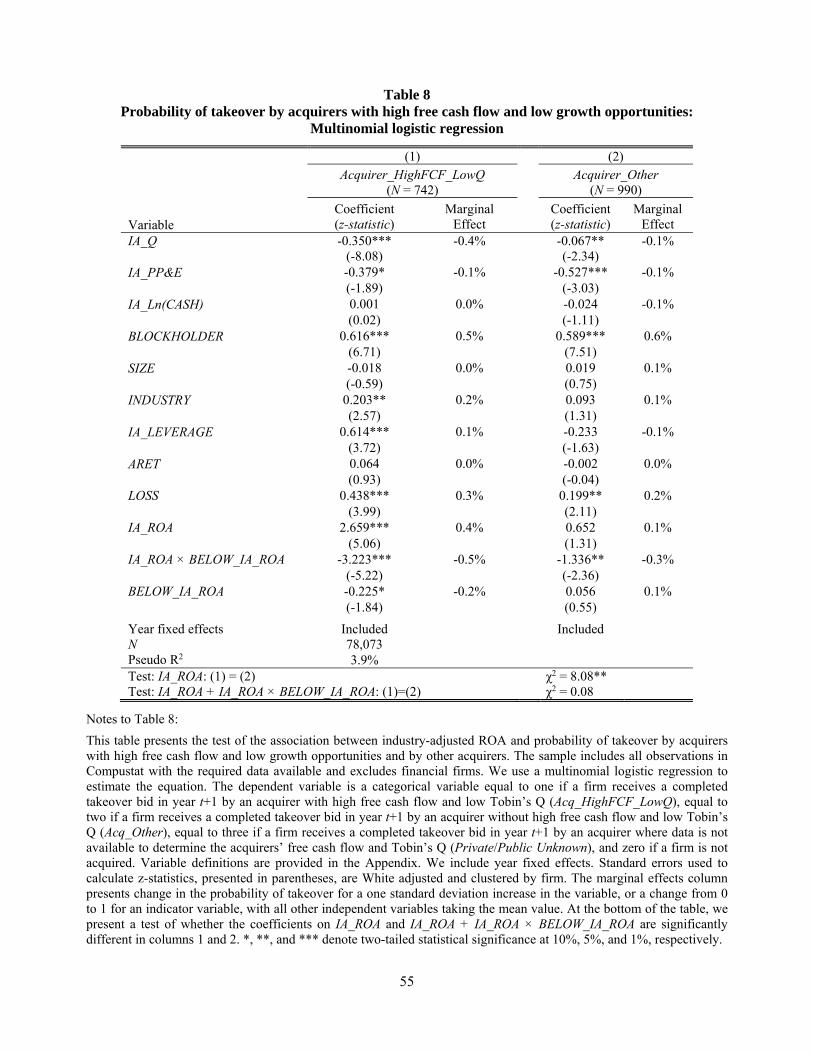

4.3.1. Acquirers with agency costs of free cash flow (H3a)

We expect that it is less costly for managers of acquirers with high free cash flow

and low growth opportunity to make opportunistic acquisitions than for managers of

other acquirers. Acquirers are classified as having high free cash flow and low growth

opportunity when their Tobin’s Q is below the annual industry average and free cash flow

is above the annual industry average (Acquirer_HighFCF_LowQ); all other public

acquirers are classified as having low-agency problem (Acquirer_Other).10 The results

are presented in Table 8. We find that the positive association between positive industry-

adjusted accounting profitability and takeover likelihood is more pronounced for

acquirers with high free cash flow and low growth opportunities than for other acquirers.

Specifically, the coefficient on IA_ROA is significantly positive and significantly higher

in column 1 than in column 2. The difference in the coefficients on IA_ROA + IA_ROA ×

BELOW_IA_ROA in column 1 and 2 is not significant.

4.3.2. Acquirers with blockholders (H3b)

We expect that it is less costly for managers of acquirers with no blockholders to

make opportunistic acquisitions than managers of acquirers with blockholders. We define

acquirers with blockholders as those with at least one institutional shareholder that have

at least a five percent ownership position (Acquirer_Block) and all other acquirers as

those without blockholders (Acquirer_NoBlock). The results are presented in Table 9. We

find that the positive association between positive industry-adjusted ROA and the

likelihood of acquisition is more pronounced for acquirers without blockholders than for

10 Free cash flow is calculated as cash flow from operations minus capital expenditures, scaled by beginning total assets.

32

acquirers with blockholders. Specifically, the coefficient on IA_ROA is significantly

positive and significantly higher in column 1 than in column 2. The difference in the

coefficients on IA_ROA + IA_ROA × BELOW_IA_ROA in column 1 and 2 is not

significant.

4.3.3. Acquirers with less independent boards (H3c)

We expect that it is more costly for managers of acquirers with more independent

boards to make opportunistic acquisitions than managers of acquirers with less

independent boards. We classify firms’ with the percentage of independent board

members below the annual industry average as having non-independent boards

(Acquirer_Brd_NoInd), and above the annual industry average as having independent

boards (Acquirer_Brd_Ind). The results are presented in Table 10. We find that the

positive association between positive industry-adjusted accounting profitability and

takeover likelihood is more pronounced for acquirers with less independent boards than

for acquirers with more independent boards. Specifically, the coefficient on IA_ROA is

significantly positive and significantly higher in column 1 than in column 2. The

difference in the coefficients on IA_ROA + IA_ROA × BELOW_IA_ROA in columns 1

and 2 is not significant.

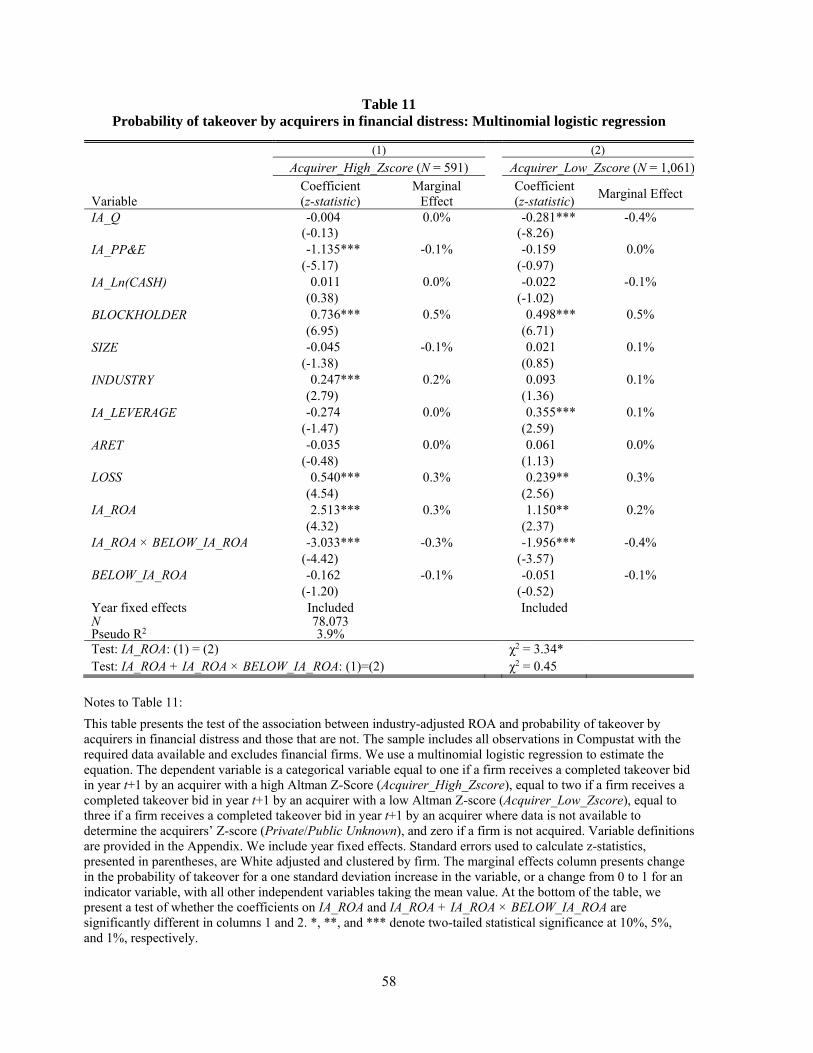

4.3.4. Acquirers’ financial distress (H3d)

We expect that the costs to making opportunistic acquisitions are higher when

acquirers are in financial distress than when they are not in financial distress. We classify

firms with Altman Z-scores below the annual industry average as financially distressed

(Acquirer_Low_Zscore) and those above as financially healthy (Acquirer_High_Zscore).

33

The results are presented in Table 11. We find that the positive association between

positive industry-adjusted accounting profitability and takeover likelihood is more

pronounced for acquirers that are financially healthy than acquirers in financial distress

(i.e., higher costs to making opportunistic acquisitions). Specifically, the coefficient on

IA_ROA in column 1 is significantly positive and significantly higher than the coefficient

on IA_ROA in column 2. Furthermore, the coefficient on IA_ROA + IA_ROA ×

BELOW_IA_ROA is not significantly different between columns 1 and 2.

Overall, the results of tests of H3a to H3d are consistent with lower costs to

management of making opportunistic acquisitions increasing the positive association

between probability of takeover and positive industry-adjusted ROA. However, as

expected, these costs do not have a significant effect on the negative association between

acquisition likelihood and negative industry-adjusted ROA.

4.4. Acquirers’ Announcement Returns (H4)

Next, we examine the acquirers’ returns to acquisition announcements. This

analysis is limited to public acquirers where we can calculate announcement returns.

ACQ_SCAR is the acquirer’s five-day (-2, +2) cumulative abnormal return calculated

using the market model following prior studies (e.g., Masulis et al. 2007; Harford et al.

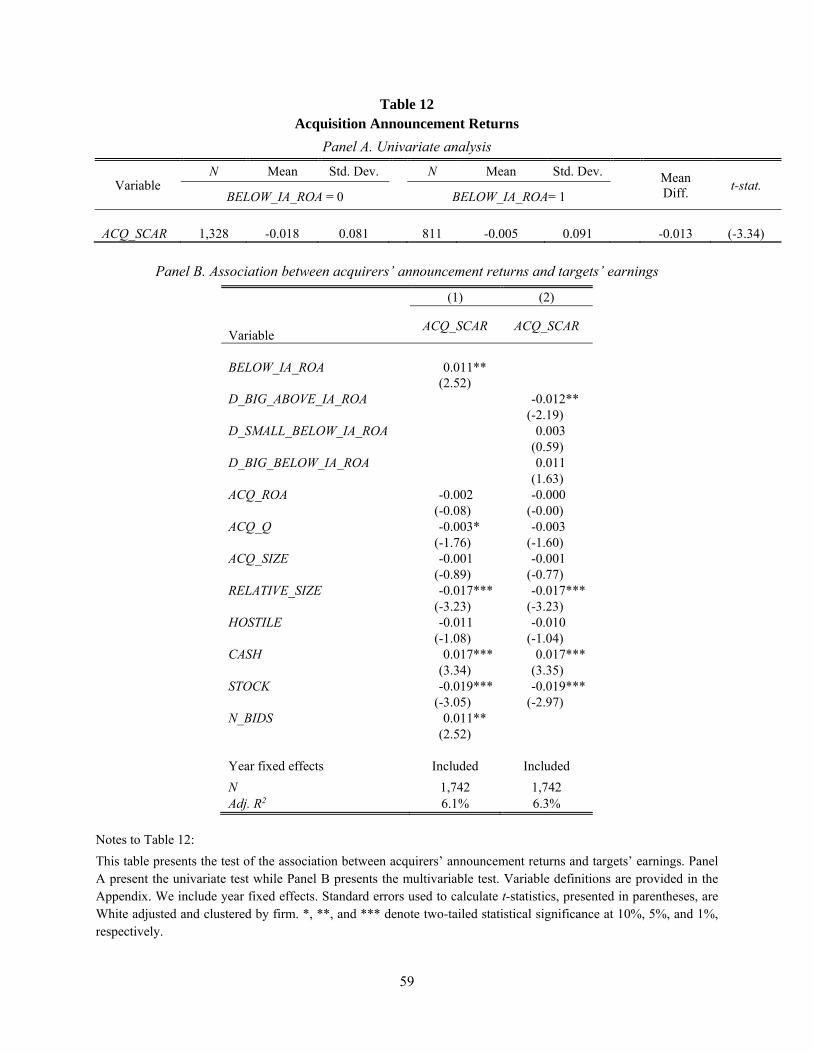

2012). Table 12, Panel A presents a univariate analysis of acquirers’ announcement

returns by whether the target has ROA above or below the industry mean. We find that

the mean acquirer announcement return for acquisitions of targets with ROA below the

industry average is -0.5% while it is -1.8% for acquisitions of targets with ROA above

the industry average. In Panel B, we perform a multivariable test of the association

between targets’ earnings and acquirers’ announcement returns. The dependent variable

34

is ACQ_SCAR. In column 1, our variable of interest is whether target’s earnings are

below the industry average (i.e., BELOW_IA_ROA = 1). In column 2, we group

observations based on targets’ earnings into four groups using a cutoff of 0.10 (-0.10) for

targets’ earnings above (below) the industry average. If firms’ IA_ROA is positive and is

above (below) 0.10, we set BIG_ABOVE_IA_ROA (SMALL_ABOVE_IA_ROA) equal to

one, and zero otherwise. If firms’ IA_ROA is negative and is above (below) -0.10 we set

SMALL_BELOW_IA_ROA (BIG_BELOW_IA_ROA) equal to one, and zero otherwise.

We also control for acquirers’ ROA (ACQ_ROA), acquirers’ Tobin’s Q (ACQ_Q),

acquirers’ size (ACQ_ln(MV)), relative transaction size (RELATIVE_SIZE), hostile bids

(HOSTILE), all cash bids (CASH), all stock bids (STOCK), and the number of bidders

(N_BIDS) (Travlos 1987; Fuller et al. 2002; Moeller et al. 2004; Dong et al. 2006; Chen

et al. 2007).

In column 1, the coefficient on BELOW_IA_ROA is 0.011 and significant at the

5% level, which indicates that acquirers’ announcement returns are significantly lower by

1.1% on average when targets earnings are above the industry average relative to when

earnings are below the industry average. In column 2, we include

D_BIG_ABOVE_IA_ROA, D_SMALL_BELOW_IA_ROA, and D_BIG_BELOW_IA_ROA,

so that the coefficient on each of these variables reflects the comparison with acquisitions

of targets with the lowest positive industry-adjusted ROA (i.e., where

D_SMALL_ABOVE_IA_ROA is equal to one). The estimated coefficient on

D_BIG_ABOVE_IA_ROA is significantly negative indicating among acquisitions of

targets with positive IA_ROA acquirers acquiring the more profitable targets experience

lower announcement returns. These results indicate that acquirers’ announcement returns

35

are significantly lower when they acquire targets with relatively higher accounting

profitability, suggesting that investors view acquiring targets with relatively higher

accounting profitability as more value decreasing. This is consistent with such

acquisitions being more likely to be motivated by managerial opportunism.

5. Conclusion In this paper, we examine the association between firms’ accounting profitability

and their likelihood of being acquired. We find a non-linear relation between industry-

adjusted ROA and takeover probability. Takeover probability is negatively associated

with negative industry-adjusted ROA and positively associated with positive industry-

adjusted ROA. The negative association is consistent with the argument that poorer

performing firms are more likely to be taken over because acquirers can unlock greater

value through efficient management. We further argue that the positive association is

consistent with the notion that firms with higher accounting profitability are more

attractive takeover targets when acquisitions are motivated by managerial opportunism.

A battery of tests is conducted to examine whether the positive relation between

takeover likelihood and positive industry-adjusted accounting profitability is due to

opportunistic acquisitions. We find that this positive relation is greater for acquirers that

benefit more from opportunistic acquisitions and for acquirers with lower costs of making

opportunistic acquisitions. We also show that among targets with positive industry-

adjusted ROA, the acquirers’ acquisition announcement returns are negatively associated

with the targets’ industry-adjusted accounting profitability. This result implies that

acquiring firms’ managers are more likely to overpay for targets when their personal

36

benefits from acquisition is greater. Overall, our results suggest that the greater

acquisition likelihood of targets with higher accounting profitability is driven by

acquiring managers’ opportunism. Furthermore, our findings contribute to the accounting

and finance literature by enhancing the understanding of how accounting profitability of a

firm is associated with its takeover probability.

37

References

Ali, A., and T. D. Kravet. 2014. The Effect of SFAS 141 and 142 on the Likelihood and the Form of Financing of Corporate Takeovers. Working Paper, University of Connecticut and University of Texas at Dallas.

Ambrose, B. W., and W. L. Megginson. 1992. The role of asset structure, ownership structure, and takeover defenses in determining acquisition likelihood. Journal of Financial and Quantitative Analysis 27(04): 575-589.

Bargeron, L. L., F. P. Schlingemann, R. M. Stulz, and C. J. Zutter. 2008. Why do private acquirers pay so little compared to public acquirers? Journal of Financial Economics 89(3): 375-390.

Barth, M. E., J. A. Elliott, and M. W. Finn. 1999. Market rewards associated with patterns of increasing earnings. Journal of Accounting Research 37(2): 387-413.

Beatty, A. L., B. Ke, and K. R. Petroni. 2002. Earnings management to avoid earnings declines across publicly and privately held banks. The Accounting Review 77(3): 547-570.

Bens, D., T. Goodman, and M. Neamtiu. 2011. Does investment-related pressure lead to misreporting? An analysis of reporting following M&A transactions. The Accounting Review 87(3): 839–865.

Berger, P. G., and E. Ofek. 1996. Bustup takeovers of value-destroying diversified firms. The Journal of Finance 51(4): 1175-1200.

Billett, M. T., and H. Xue. 2007. The takeover deterrent effect of open market share repurchases. The Journal of Finance 62(4): 1827-1850.

Bodnaruk, A., M. Massa, and A. Simonov. 2009. Investment banks as insiders and the market for corporate control. Review of Financial Studies 22(12): 4989-5026.

Bruner, R. F. 2004. Applied mergers & acquisitions. New Jersey: John Wiley & Sons.

Burgstahler, D., and I. Dichev. 1997. Earnings management to avoid earnings decreases and losses. Journal of Accounting and Economics 24(1): 99-126.

Bushee, B. J. 1998. The influence of institutional investors on myopic R&D investment behavior. Accounting Review: 305-333.

Byrd, J. W., and K. A. Hickman. 1992. Do outside directors monitor managers?: Evidence from tender offer bids. Journal of Financial Economics 32(2): 195-221.

38

Cai, Y., and X. Tian. 2009. Firm Locations and Takeover Likelihood. Working Paper, University of North Carolina and Indiana University.

Chang, S. 1998. Takeovers of privately held targets, methods of payment, and bidder returns. The Journal of Finance 53(2): 773-784.

Chen, C. W., D. W. Collins, T. D. Kravet and R. D. Mergenthaler. 2014. Financial Statement Comparability and the Efficiency of Acquisition Decisions. Working Paper, University of Connecticut and University of Iowa.

Chen, X., J. Harford, and K. Li. 2007. Monitoring: Which institutions matter? Journal of Financial Economics 86(2): 279-305.

Chu, J., P. Dechow, K.W. Hui, and A.Y. Wang. 2015. The valuation premium for a string of positive earnings surprises: The role of earnings manipulation. Working Paper, Hong Kong University of Science and Technology, University of California, Berkeley, and University of Cambridge.

Cohen, D. A., A. Dey, and T. Z. Lys. 2008. Real and accrual-based earnings management in the pre- and post-Sarbanes-Oxley periods. The Accounting Review 83(3): 757-787.

Cohen, D. A., and P. Zarowin. 2010. Accrual-based and real earnings management activities around seasoned equity offerings. Journal of Accounting and Economics 50(1): 2-19.

Cremers, K. J. M., V. B. Nair, and K. John. 2009. Takeovers and the cross-section of returns. The Review of Financial Studies 22(4): 1409-1445.

Dechow, P. M., R. G. Sloan, and A. P. Sweeney. 1996. Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research 13(1): 1-36.

DeFond, M. L., and C. W. Park. 1999. The effect of competition on CEO turnover. Journal of Accounting and Economics 27: 35-56.

Desai, H., C. E. Hogan, and M. S. Wilkins. 2006. The reputational penalty for aggressive accounting: Earnings restatements and management turnover. The Accounting Review 81(1): 83-112.

Dietrich, J. K., and E. Sorensen. 1984. An application of logit analysis to prediction of merger targets. Journal of Business Research 12(3): 393-402.

Donelson, D. C., J. M. McInnis, and R. D. Mergenthaler. 2013. Discontinuities and earnings management: Evidence from restatements related to securities litigation. Contemporary Accounting Research 30(1): 242-268.

39

Dong, M., D. Hirshleifer, S. Richardson, and S. H. Teoh. 2006. Does investor misvaluation drive the takeover market? The Journal of Finance 61(2): 725-762.

Eckbo, B. E., and K. S. Thorburn. 2008. Corporate restructuring: Breakups and LBO’s. In Handbook of empirical corporate finance: Empirical corporate Finance, ed. B. E. Eckbo. New York: Elsevier/North Holland.

Edmans, A., I. Goldstein, and W. Jiang. 2012. The real effects of financial markets: The impact of prices on takeovers. The Journal of Finance 67(3): 933-971.

Fama, E.F., French, K.R., 1997. Industry costs of equity. Journal of Financial Economics 43, 153-193.

Farrell, K. A., and D. A. Whidbee. 2003. Impact of firm performance expectations on CEO turnover and replacement decisions. Journal of Accounting and Economics 36: 165-196.

Fich, E. M., L. T. Starks, and A. S. Yore. 2014. CEO deal-making activities and compensation. Journal of Financial Economics, forthcoming.

Fu, F., L. Lin, and M. Officer. 2013. Acquisitions driven by stock overvaluation. Journal of Financial Economics 109 (1): 24-39.

Fuller, K., J. Netter, and M. Stegemoller. 2002. What do returns to acquiring firms tell us? Evidence from firms that make many acquisitions. The Journal of Finance 57(4): 1763-1793.

Givoly, D., C. K. Hayn, and S. P. Katz. 2010. Does public ownership of equity improve earnings quality? The Accounting Review 85(1): 195-225.

Grinstein, Y., and P. Hribar. 2004. CEO compensation and incentives: Evidence from M&A bonuses. Journal of Financial Economics 73(1): 119-143.

Harford, J. 1999. Corporate cash reserves and acquisitions. The Journal of Finance 54(6): 1969-1997.

Harford, J., M. Humphery-Jenner, and R. Powell. 2012. The sources of value destruction in acquisitions by entrenched managers. Journal of Financial Economics 106: 247-261.

Harford, J., and K. Li. 2007. Decoupling CEO wealth and firm performance: The case of acquiring CEOs. The Journal of Finance 62(2): 917-949.

Harford, J., and R. J. Schonlau. 2013. Does the director labor market offer ex post settling-up for CEOs? The case of acquisitions. Journal of Financial Economics 110: 18-36.

40

Ivashina, V., V.B. Nair, A. Saunders, N. Massoud, and R. Stover. 2009. Bank debt and corporate governance. Review of Financial Studies, 22(1): 41-77.

Jensen, M. C. 1986. Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review 76(2): 323-329.

Jensen, M. C. 2005. Agency costs of overvalued equity. Financial Management 34(1): 5-19.

Kasznik, R., and M.F. McNichols. 2002. Does meeting earnings expectations matter? Evidence from analyst forecast revisions and share prices. Journal of Accounting Research 40(3): 727-759.

Ke, B., K. Petroni, and A. Safieddine. 1999. Ownership concentration and sensitivity of executive pay to accounting performance measures: Evidence from publicly and privately held insurance companies. Journal of Accounting and Economics 28(2): 185-209.

Klassen, K. J. 1997. The impact of inside ownership concentration on the trade-off between financial and tax reporting. Accounting Review 72(3): 455-474.

Klein, A. 2002. Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics 33(3): 375-400.

Lang, L. H., R. Stulz, and R. A. Walking. 1991. A test of the free cash flow hypothesis: The case of bidder returns. Journal of Financial Economics 29(2): 315-335.

Levitt, A. 1998. The numbers game. Speech delivered at the NYU Center for Law and Business, New York, NY, September 28.

Malmendier, U., and G. Tate. 2008. Who makes acquisitions? CEO overconfidence and the market’s reaction. Journal of Financial Economics 89: 20-43.

Manne, H. G. 1965. Mergers and the market for corporate control. The Journal of Political Economy 73: 110-120.

Marris, R. 1963. A model of the" managerial" enterprise. The Quarterly Journal of Economics 77: 185-209.

Masulis, R., C. Wang, and F. Xie. 2007. Corporate governance and acquirer returns. The Journal of Finance 62 (4): 1851-1889.

Matsumoto, D. A. 2002. Management's incentives to avoid negative earnings surprises. The Accounting Review 77(3): 483-514.

41

McConnell, J. J., and H. Servaes. 1990. Additional evidence on equity ownership and corporate value. Journal of Financial Economics 27: 595-612.

Moeller, S. B., F. P. Schlingemann, and R. M. Stulz. 2004. Firm size and the gains from acquisitions. Journal of Financial Economics 73(2): 201-228.

Morck, R., A. Shleifer, and R. Vishny. 1990. Do managerial objectives drive bad acquisitions? The Journal of Finance 45(1): 31–48.

Myers, J. N., L. A. Myers, and D. J. Skinner. 2007. Earnings momentum and earnings management. Journal of Accounting, Auditing & Finance 22(2): 249-284.

Palepu, K. G. 1986. Predicting takeover targets: A methodological and empirical analysis. Journal of Accounting and Economics 8(1): 3-35.

Pearl, J., and J. Rosenbaum. 2009. Investment banking: Valuation, leveraged buyouts, and mergers and acquisitions. New Jersey: John Wiley & Sons.

Penman, S. H., and X. Zhang. 2002. Accounting conservatism, the quality of earnings, and stock returns. The Accounting Review 77(2): 237-264.