a view of financial literacy on campuses kelly savoie and david haygood sallie mae

TRANSCRIPT

A View of Financial Literacy on Campuses

Kelly Savoie and David Haygood

Sallie Mae

Agenda

• Review 2014 Survey Results

• Define Financial Literacy Program

• How to Develop a Program

Survey Overview

• Purpose: survey higher education institutions with a goal of understanding if they offer financial literacy tools and resources to their families and, if so, what their priorities are in developing and deploying them

• Survey Respondents: 305

• Note: survey conducted by Sallie Mae April 2014

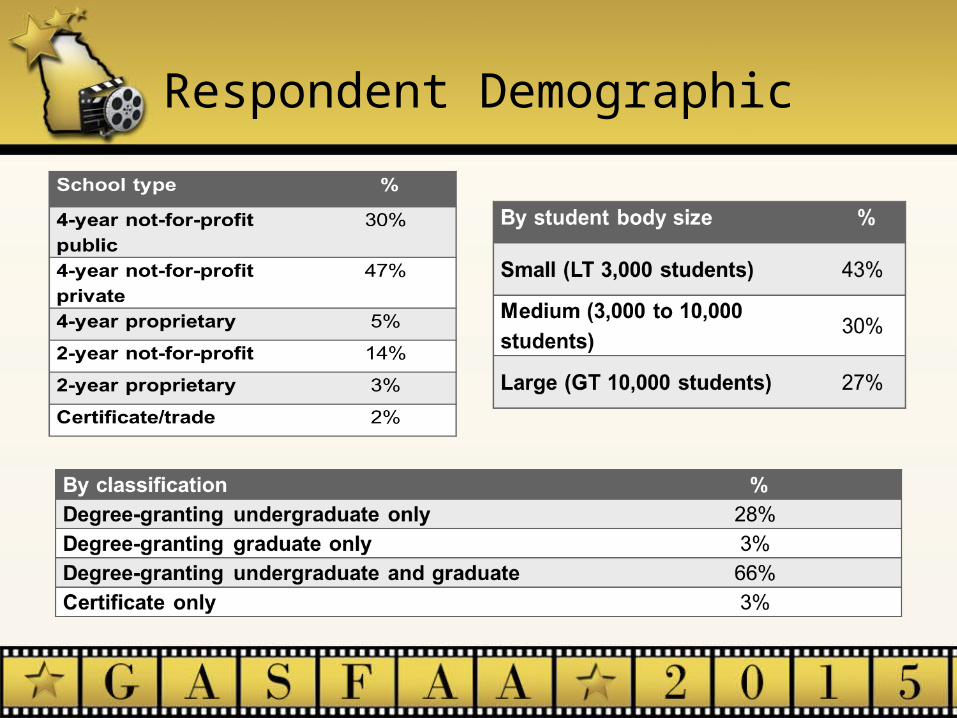

Respondent Demographic

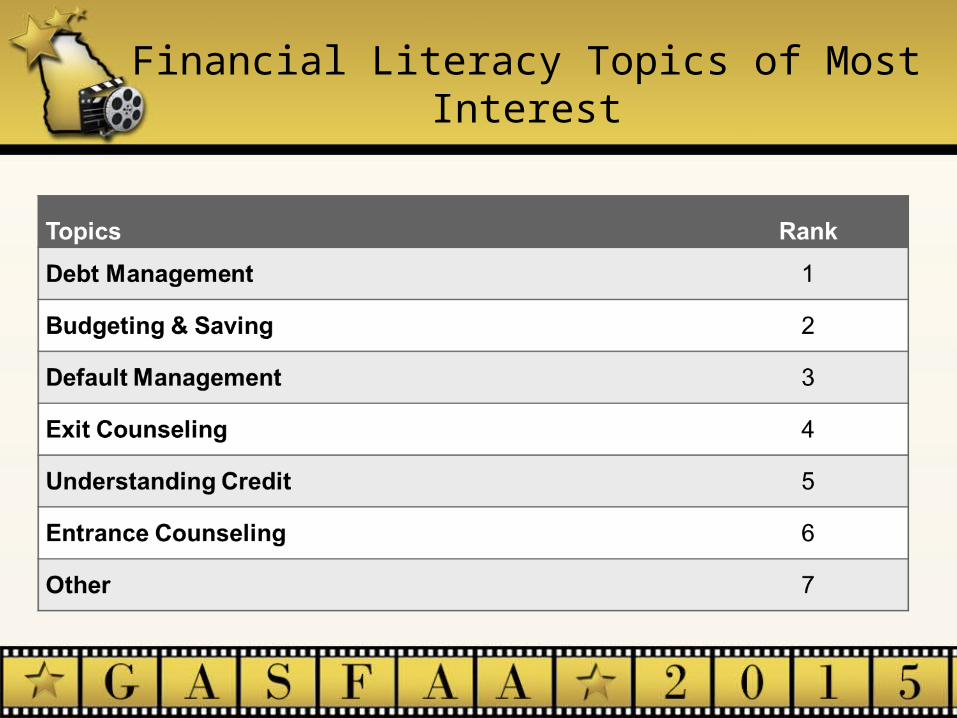

Financial Literacy Topics of Most Interest

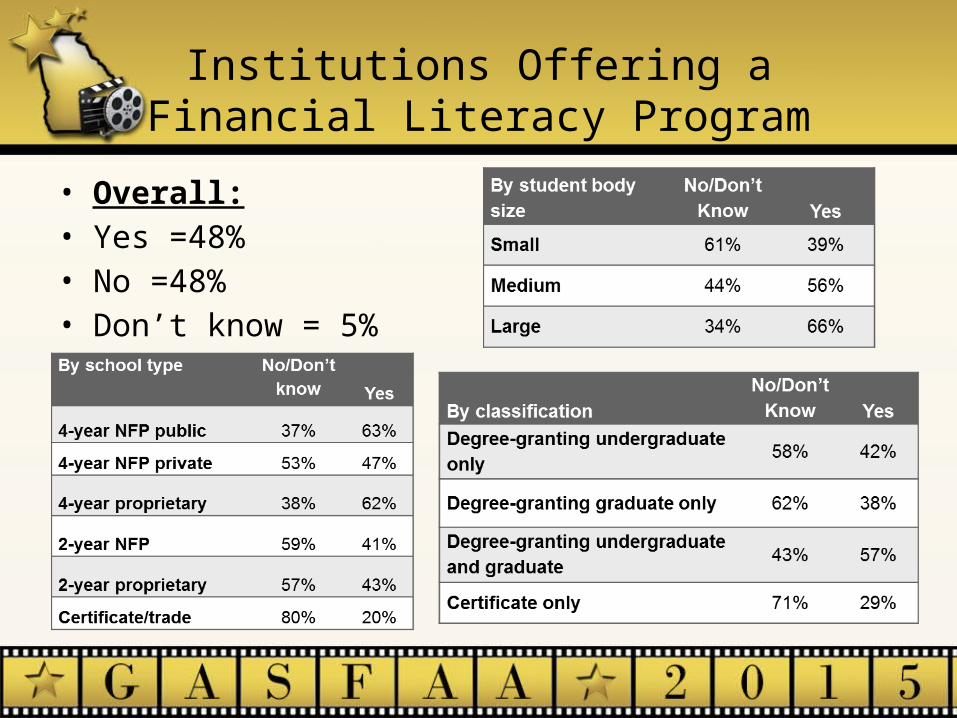

Institutions Offering a Financial Literacy Program

• Overall:• Yes =48%• No =48%• Don’t know = 5%

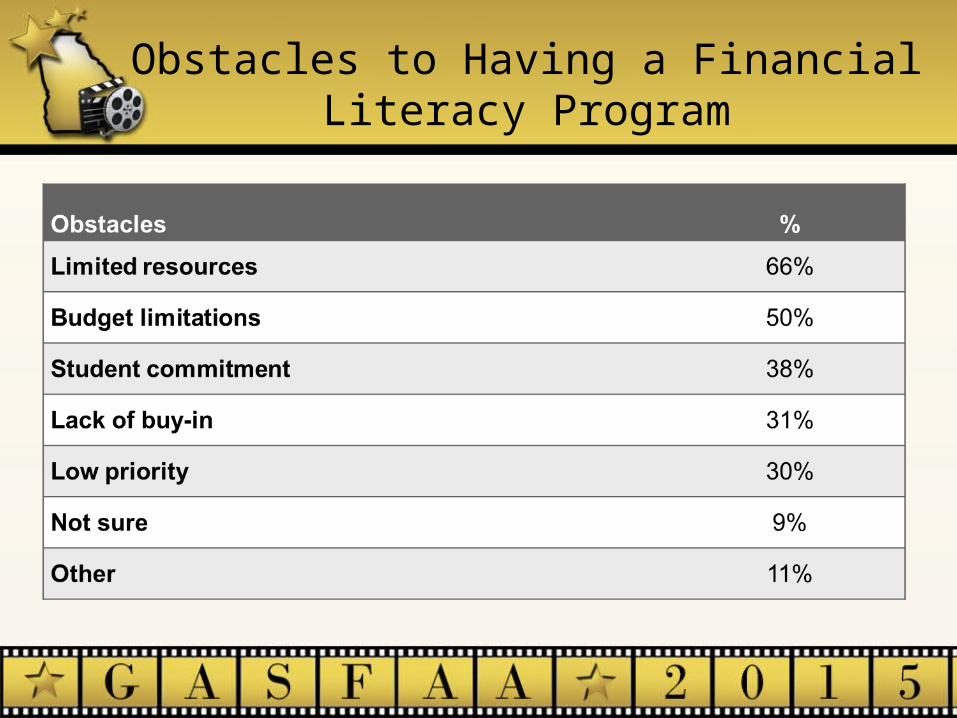

Obstacles to Having a Financial Literacy Program

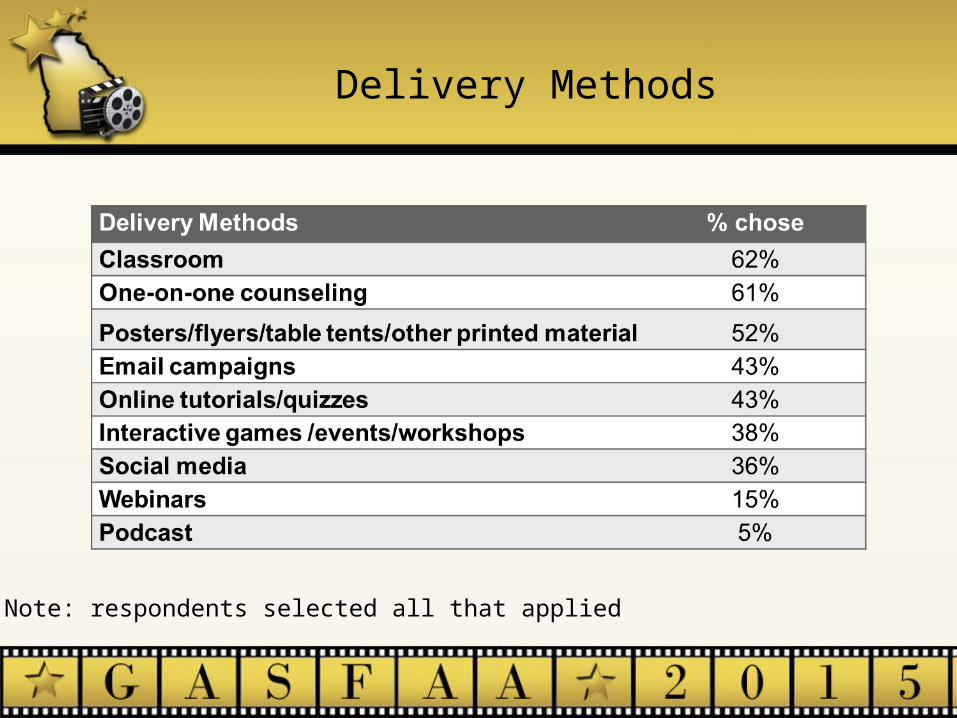

Delivery Methods

Note: respondents selected all that applied

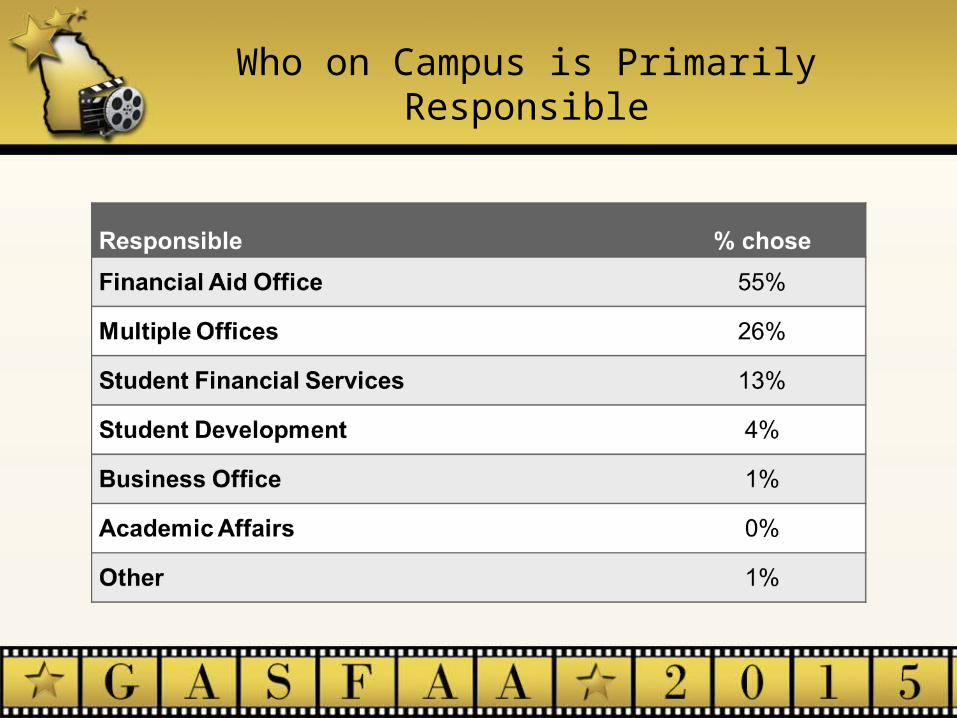

Who on Campus is Primarily Responsible

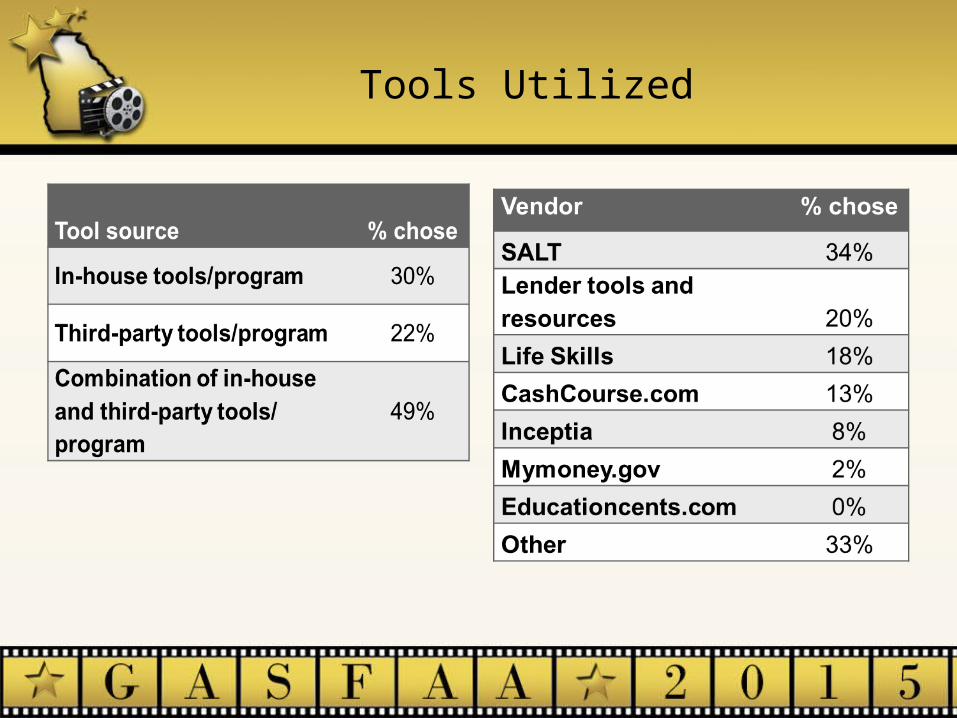

Tools Utilized

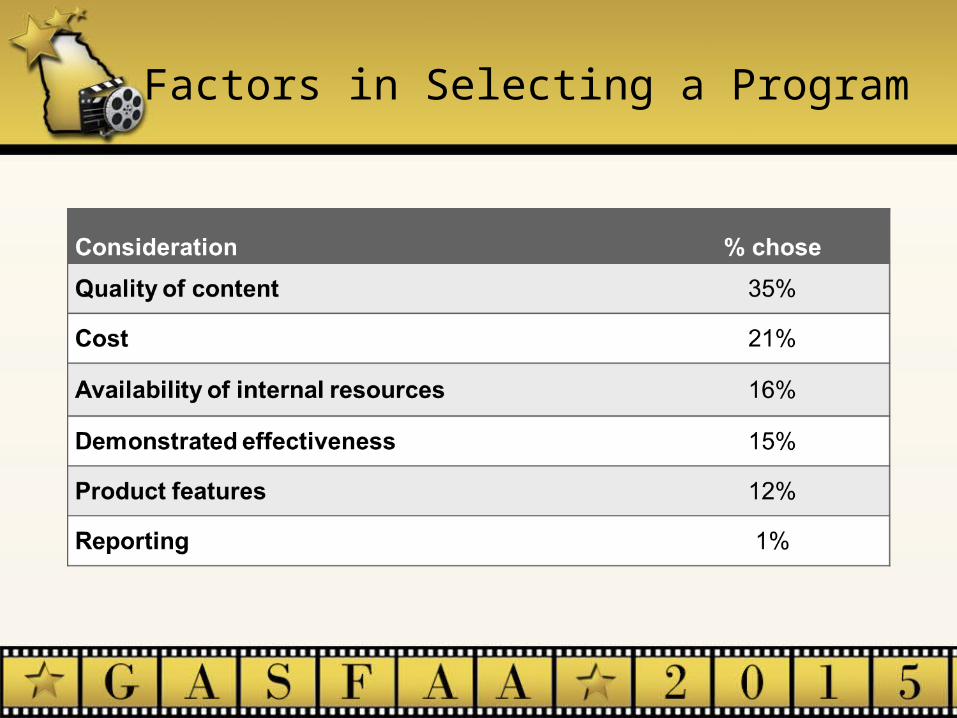

Factors in Selecting a Program

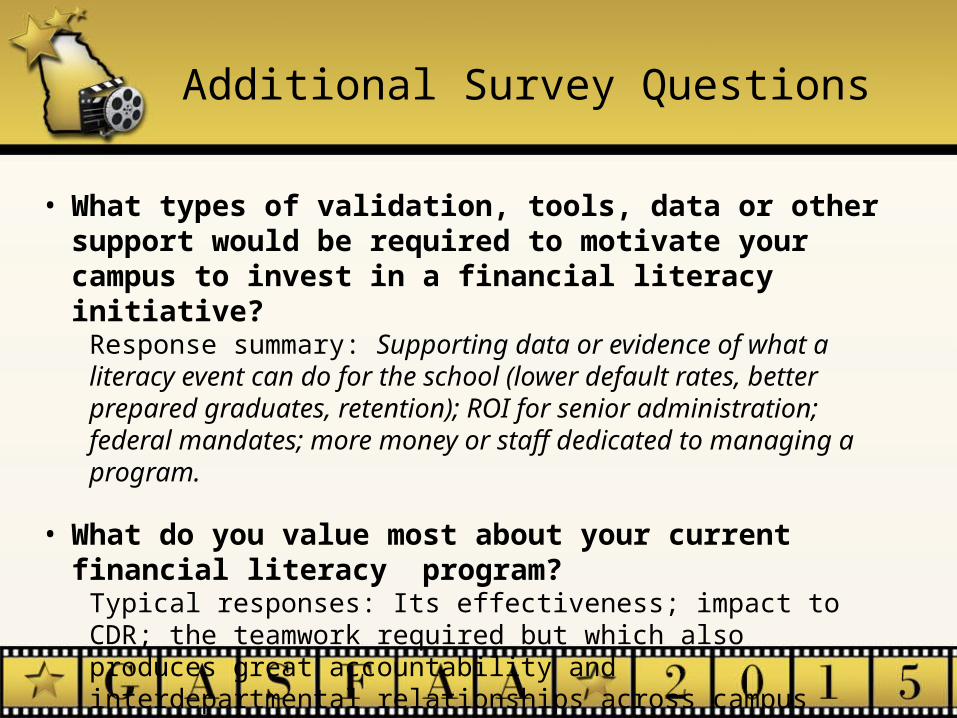

Additional Survey Questions

• What types of validation, tools, data or other support would be required to motivate your campus to invest in a financial literacy initiative?

Response summary: Supporting data or evidence of what a literacy event can do for the school (lower default rates, better prepared graduates, retention); ROI for senior administration; federal mandates; more money or staff dedicated to managing a program.

• What do you value most about your current financial literacy program?

Typical responses: Its effectiveness; impact to CDR; the teamwork required but which also produces great accountability and interdepartmental relationships across campus

Additional Survey Questions, cont.

► How do you engage your students so that they take advantage of the financial literacy program?– Response summary: bribe students with incentives (bookstore gift cards,

scholarships, course credit); peer marketing; gaining access through academics

► How do you measure the outcomes/success of your financial literacy program?– Typical responses: we do not measure success; we measure participant rates

and default rates; we survey participants• Pre and Post tests *UNG Financial Literacy Workshop

► What is not currently available that you would like to see brought to the market?– Response summary: A system that both incentivizes participation and

encourages competition among students in financial literacy

What is a Financial Literacy Program

?

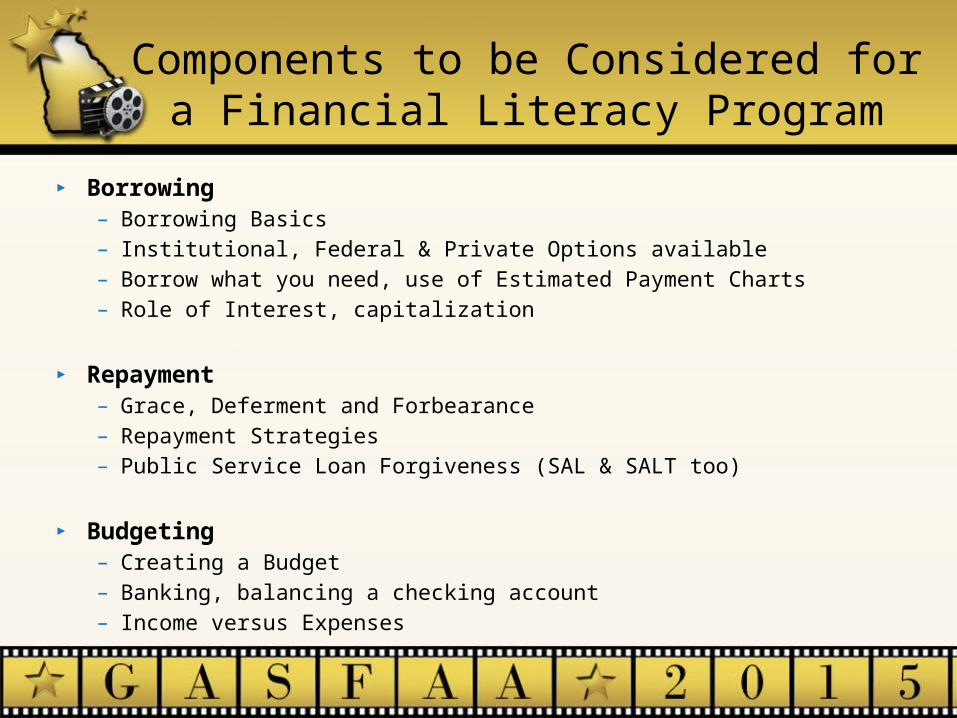

Components to be Considered for a Financial Literacy Program

► Borrowing– Borrowing Basics– Institutional, Federal & Private Options available– Borrow what you need, use of Estimated Payment Charts– Role of Interest, capitalization

► Repayment– Grace, Deferment and Forbearance– Repayment Strategies– Public Service Loan Forgiveness (SAL & SALT too)

► Budgeting– Creating a Budget– Banking, balancing a checking account– Income versus Expenses

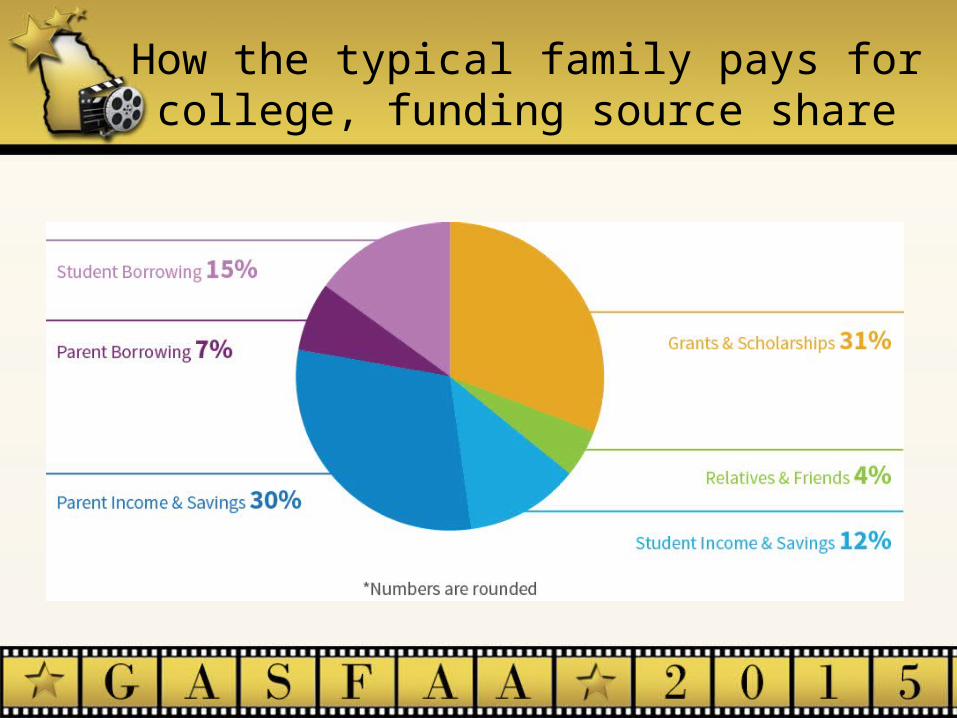

How the typical family pays for college, funding source share

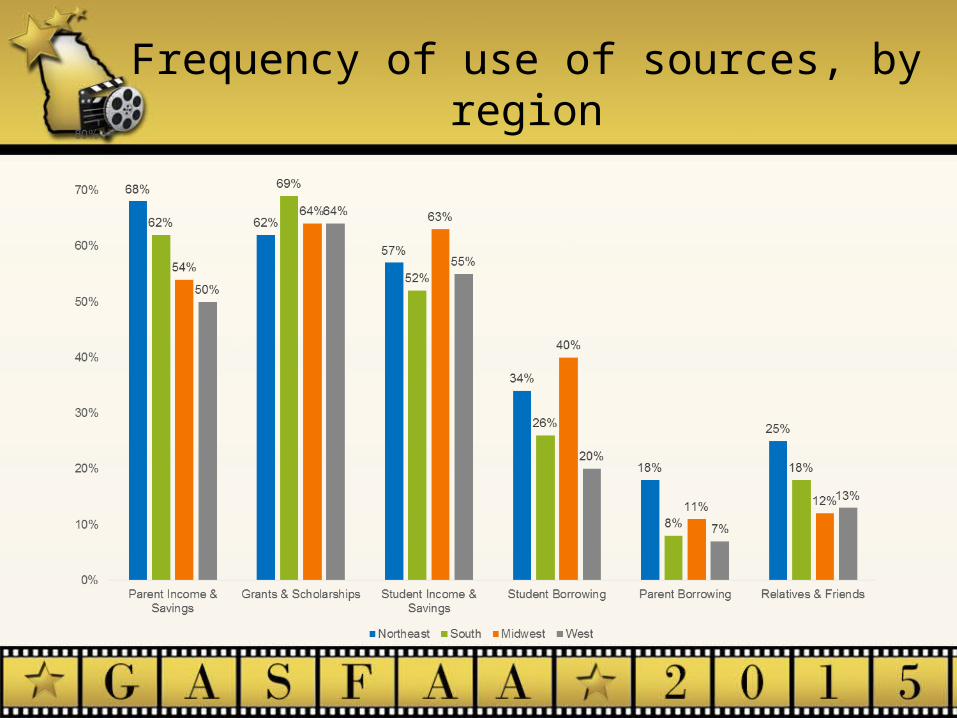

Frequency of use of sources, by region

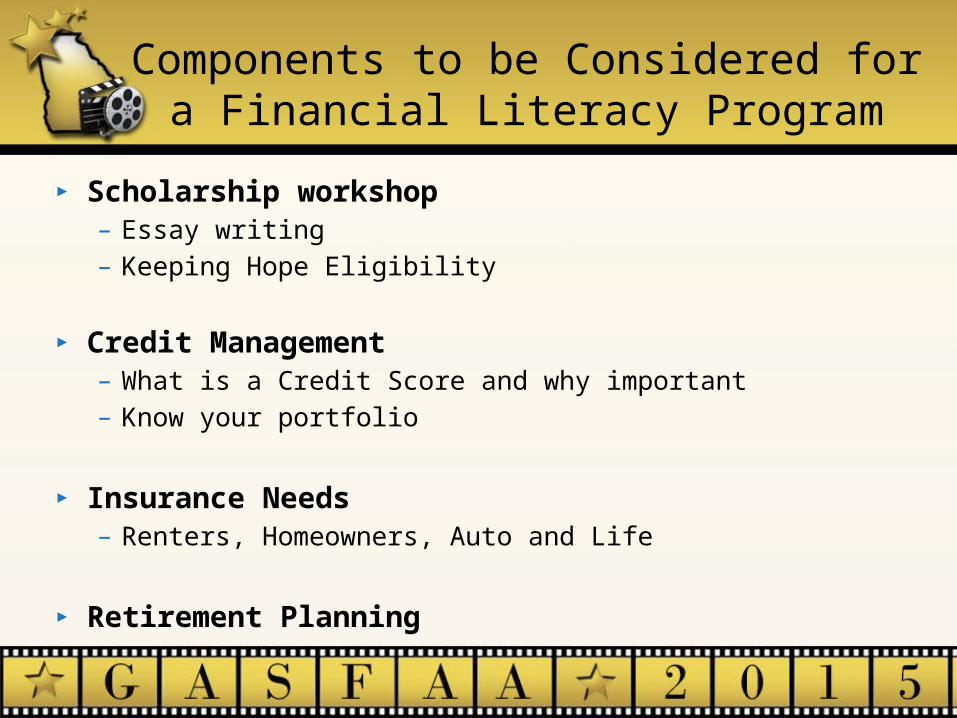

Components to be Considered for a Financial Literacy Program

► Scholarship workshop– Essay writing– Keeping Hope Eligibility

► Credit Management– What is a Credit Score and why important– Know your portfolio

► Insurance Needs– Renters, Homeowners, Auto and Life

► Retirement Planning

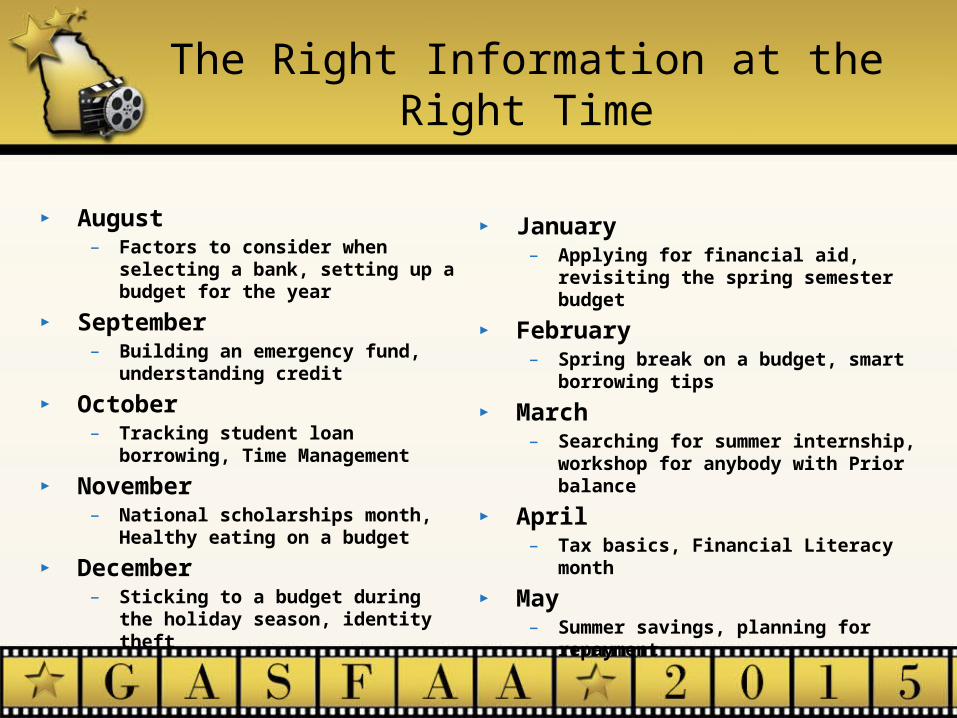

The Right Information at the Right Time

► August– Factors to consider when selecting a

bank, setting up a budget for the year

► September– Building an emergency fund,

understanding credit

► October– Tracking student loan borrowing,

Time Management

► November– National scholarships month, Healthy

eating on a budget

► December– Sticking to a budget during the

holiday season, identity theft

► January– Applying for financial aid, revisiting the

spring semester budget

► February– Spring break on a budget, smart

borrowing tips

► March– Searching for summer internship,

workshop for anybody with Prior balance

► April– Tax basics, Financial Literacy month

► May– Summer savings, planning for

repayment

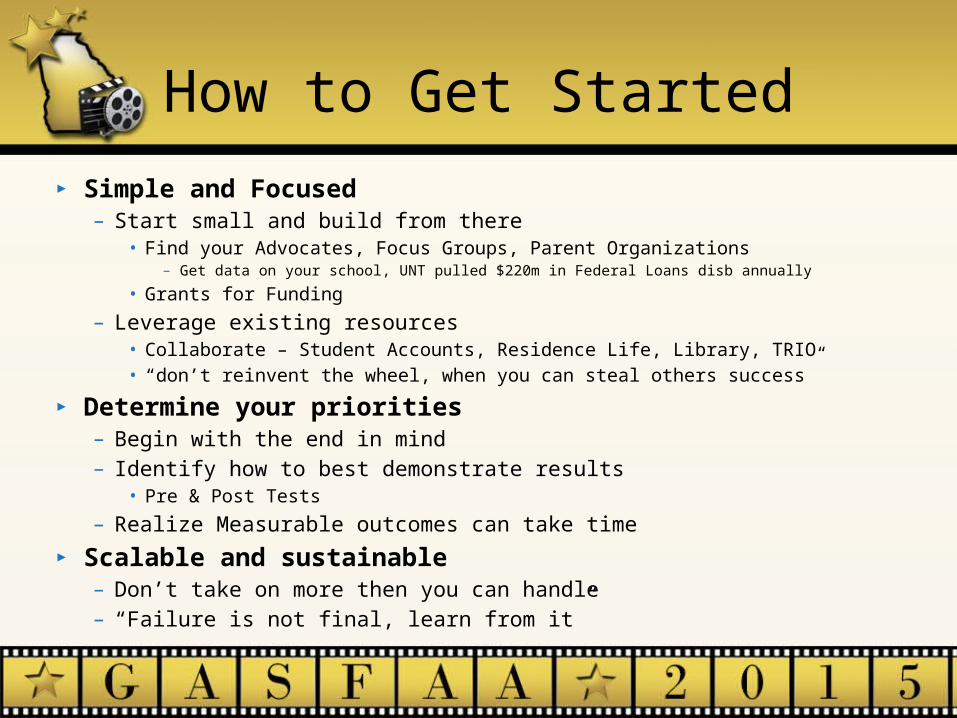

How to Get Started► Simple and Focused

– Start small and build from there• Find your Advocates, Focus Groups, Parent Organizations

– Get data on your school, UNT pulled $220m in Federal Loans disb annually

• Grants for Funding

– Leverage existing resources• Collaborate – Student Accounts, Residence Life, Library, TRIO• “don’t reinvent the wheel, when you can steal others success”

► Determine your priorities– Begin with the end in mind– Identify how to best demonstrate results

• Pre & Post Tests

– Realize Measurable outcomes can take time► Scalable and sustainable

– Don’t take on more then you can handle– “Failure is not final, learn from it”

Ideas

Resources

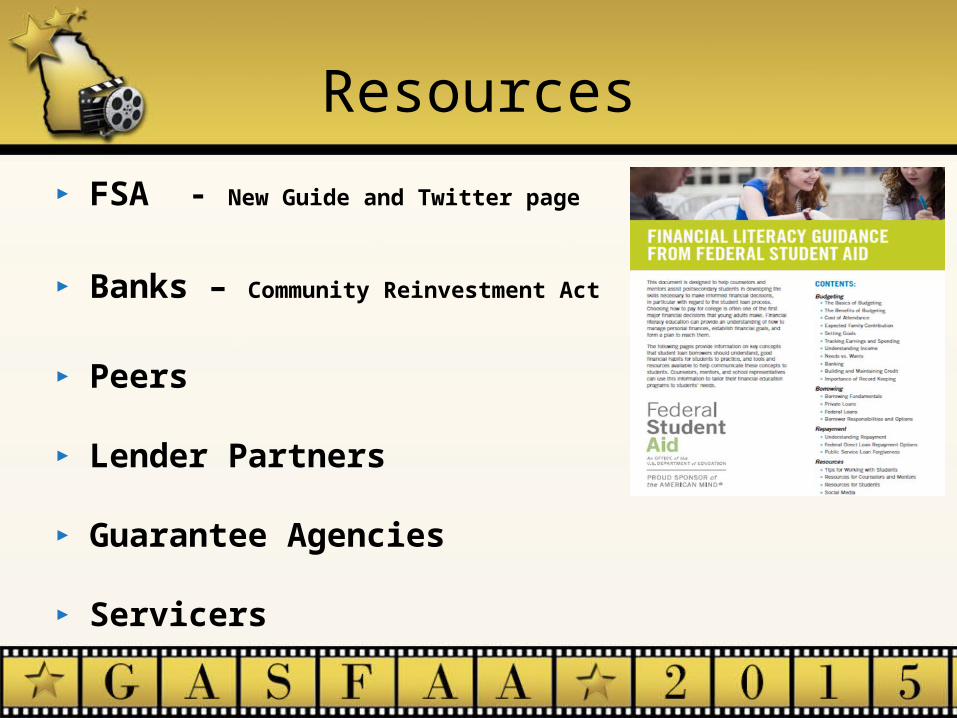

► FSA - New Guide and Twitter page

► Banks – Community Reinvestment Act

► Peers

► Lender Partners

► Guarantee Agencies

► Servicers

“Q&A”

Thank you for watching this presentation!

Financial Literacy is a long term commitment, changing life skills.