a successful intermodal rail corridor -...

TRANSCRIPT

Innovative Logistics Consultancy �

Solutions for Your Success

A successful Intermodal Rail CorridorHamburg � South East European Countries

Key Factors and Best Practices

Madrid, 12th November 2009

© TransCare AG 2

1. Key success Factors of Railway Supply Chains

2. Volumes and Volume Balance

3. Points of Consolidation

4. Integrated Rail-Roading

5. Impact of Liberalization

6. Summary

Content

3© TransCare AG

Introduction

� Railways grew traditionally in conventional business

� Intermodalism in Europe started not with the first Container arriving in Bremen in the late 50�s

� Only �Eckelmann�, the owner of a bulk port area in Hamburg (Eurokai), started investing in port facilities to handle containers in the early 60�s, while anybody around him was smiling: �What a crazy guy!�

� Eurokai, today Eurogate, became the largest container terminal operator in Europe

� Rail started 6 years later in 1967 to transport the first containers

� The rail share of containers compared to road was far less than 10% overall in Europe

� Only with the upcoming Liberalization in the central European States in the early 90�s, private activities and competition, the modal split grew in favor of rail

There are 4 key factors for success in rail transport: Volume �Consolidation � Supply chain orientation - Competition

1. Key success Factors of Railway Supply Chains

© TransCare AG 4

1. Key success Factors of Railway Supply Chains

2. Volumes and Volume Balance

3. Points of Consolidation

4. Integrated Rail-Roading

5. Impact of Liberalization

6. Summary

Content

5© TransCare AG

Rail�

� � is competitive transporting 1.000 tons or >70 TEUs

� � is competitive transporting with regular frequency (5 days a week)

� � needs constant high utilization because of the high share of fixed costs

� � needs outbalanced flows to cover costs and to keep frequency

� � needs more planning activities than road

� � creates higher supply chain complexity

� � needs smart order management � �JIT should not degenerate to the stupidity to order in time!�

� � needs consolidation of volumes to create the necessary mass of transport

� � has plenty of market opportunities (corridors) to gain business

Success to gain volumes is a question of consequent management

2. Volumes and Volume Balance

6© TransCare AG

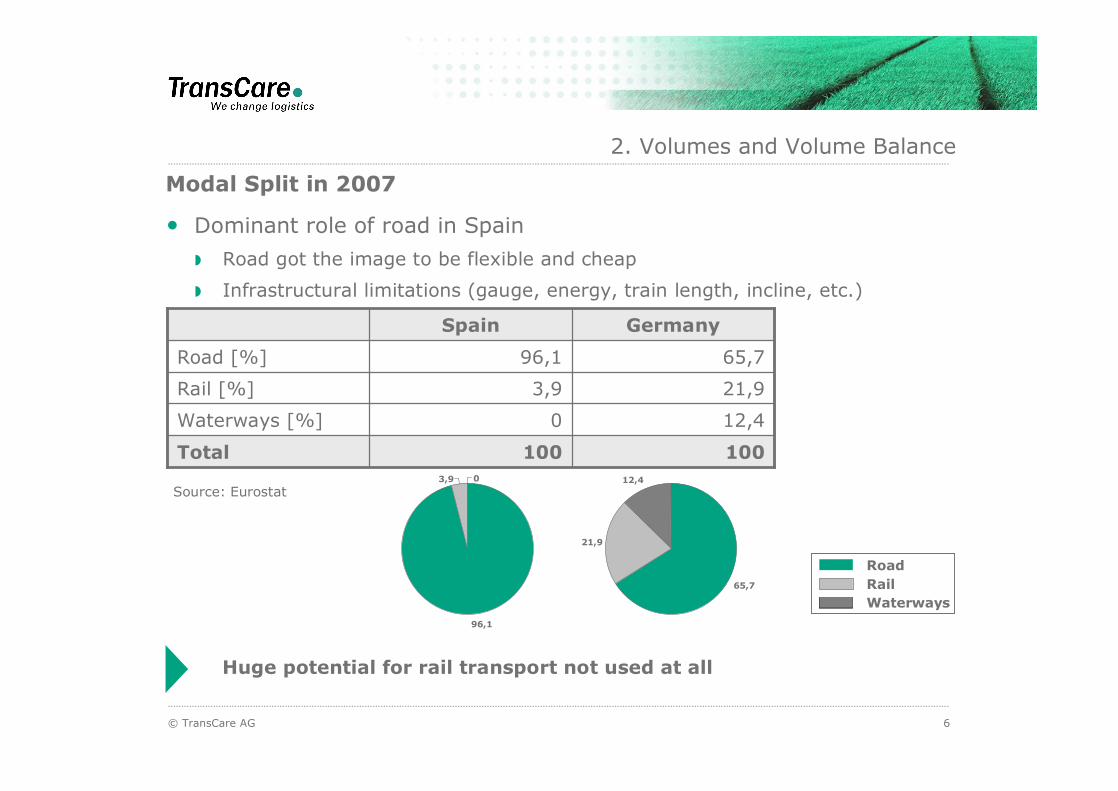

Modal Split in 2007

� Dominant role of road in Spain

Road got the image to be flexible and cheap

Infrastructural limitations (gauge, energy, train length, incline, etc.)

2. Volumes and Volume Balance

100100Total

12,40Waterways [%]

21,93,9Rail [%]

65,796,1Road [%]

GermanySpain

Huge potential for rail transport not used at all

65,7

21,9

12,4

96,1

3,9 0

Waterways

RoadRail

Source: Eurostat

7© TransCare AG

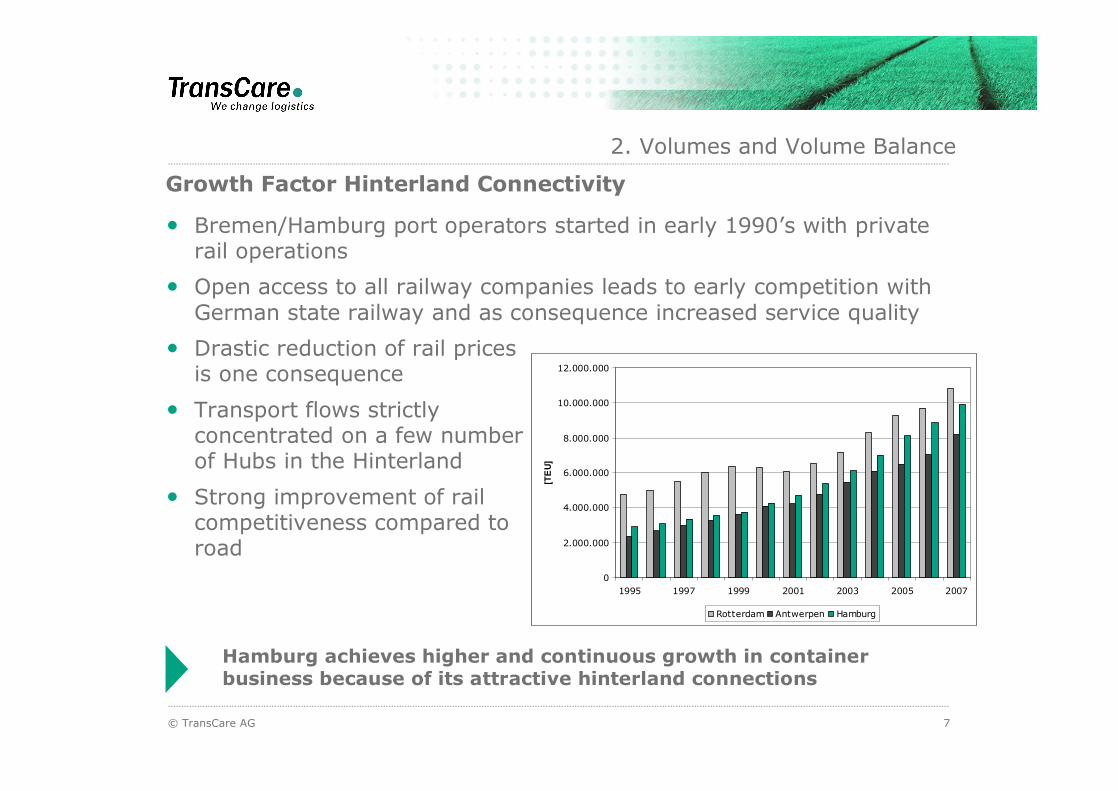

Growth Factor Hinterland Connectivity

� Bremen/Hamburg port operators started in early 1990�s with private rail operations

� Open access to all railway companies leads to early competition with German state railway and as consequence increased service quality

� Drastic reduction of rail prices is one consequence

� Transport flows strictly concentrated on a few numberof Hubs in the Hinterland

� Strong improvement of rail competitiveness compared to road

2. Volumes and Volume Balance

Hamburg achieves higher and continuous growth in container business because of its attractive hinterland connections

0

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

1995 1997 1999 2001 2003 2005 2007

[TE

U]

Rotterdam Antwerpen Hamburg

8© TransCare AG

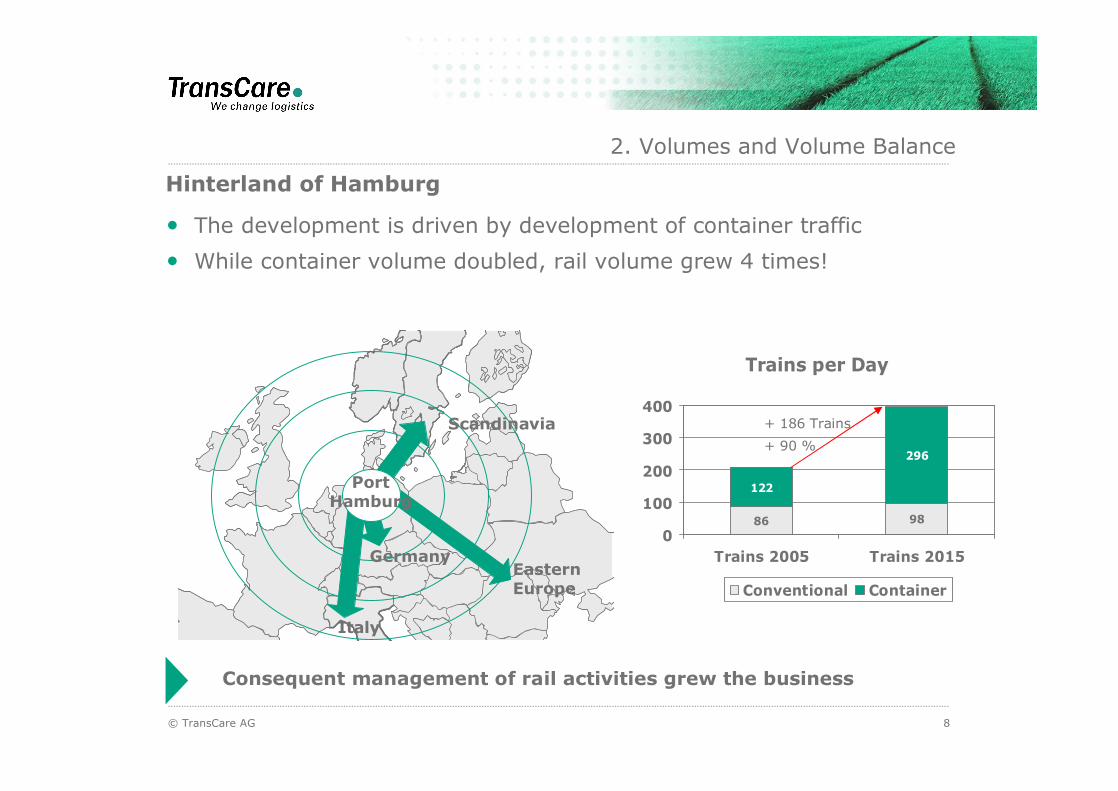

Hinterland of Hamburg

Consequent management of rail activities grew the business

Trains per Day

86 98

122

296

0

100

200

300

400

Trains 2005 Trains 2015

Conventional Container

+ 186 Trains

+ 90 %

� The development is driven by development of container traffic

� While container volume doubled, rail volume grew 4 times!

PortHamburg

Italy

Scandinavia

GermanyEastern Europe

2. Volumes and Volume Balance

9© TransCare AG

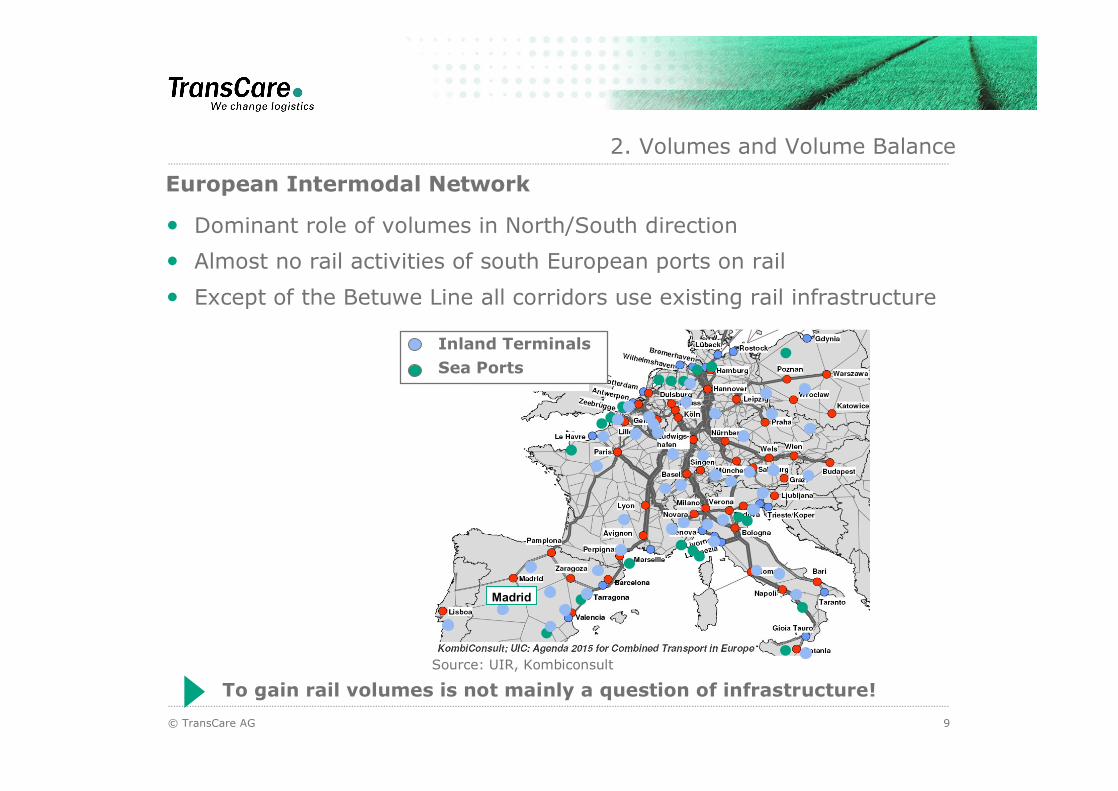

European Intermodal Network

� Dominant role of volumes in North/South direction

� Almost no rail activities of south European ports on rail

� Except of the Betuwe Line all corridors use existing rail infrastructure

2. Volumes and Volume Balance

Madrid

Source: UIR, Kombiconsult

Inland TerminalsSea Ports

To gain rail volumes is not mainly a question of infrastructure!

© TransCare AG 10

Optimal Connection between Port and Hinterland

1. Key success Factors of Railway Supply Chains

2. Volumes and Volume Balance

3. Points of Consolidation

4. Integrated Rail-Roading

5. Impact of Liberalization

6. Summary

Content

11© TransCare AG

Corridors need Consolidation Points

� Container hinterland transportation is the ideal example for rail corridors

� Corridors needs a high level �entrance� and �exit� - terminals

� Terminals and their surrounding markets are consolidation pointsalong the rail corridors

Sea ports with well integrated intermodal terminals

Transshipment terminals for rearranging of containers

Hinterland hubs and satellites for local supply

3. Points of Consolidation

Corridors are defined as the link between strong economic areas

12© TransCare AG

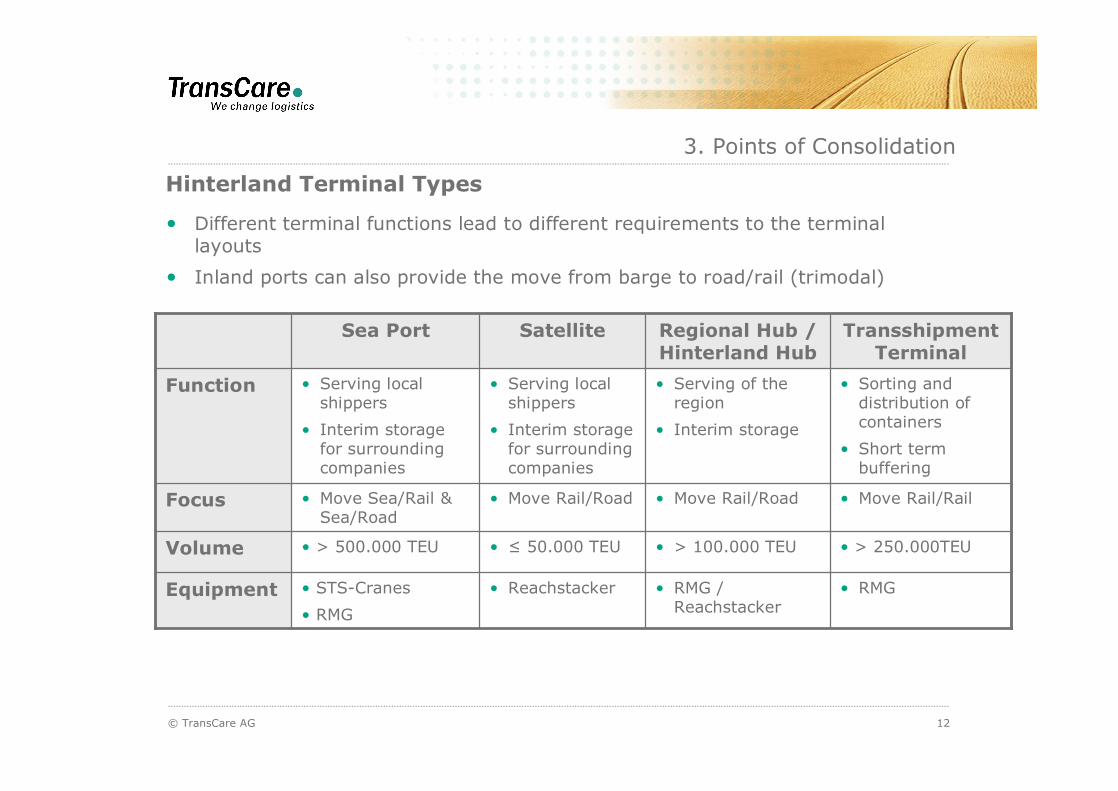

Hinterland Terminal Types

� Different terminal functions lead to different requirements to the terminal layouts

� Inland ports can also provide the move from barge to road/rail (trimodal)

� STS-Cranes

� RMG

� > 500.000 TEU

� Move Sea/Rail & Sea/Road

� Serving local shippers

� Interim storage for surrounding companies

Sea Port

� RMG� RMG / Reachstacker

� ReachstackerEquipment

� > 250.000TEU� > 100.000 TEU� ≤ 50.000 TEUVolume

� Move Rail/Rail� Move Rail/Road� Move Rail/RoadFocus

� Sorting and distribution of containers

� Short term buffering

� Serving of the region

� Interim storage

� Serving local shippers

� Interim storage for surrounding companies

Function

Transshipment Terminal

Regional Hub / Hinterland Hub

Satellite

3. Points of Consolidation

13© TransCare AG

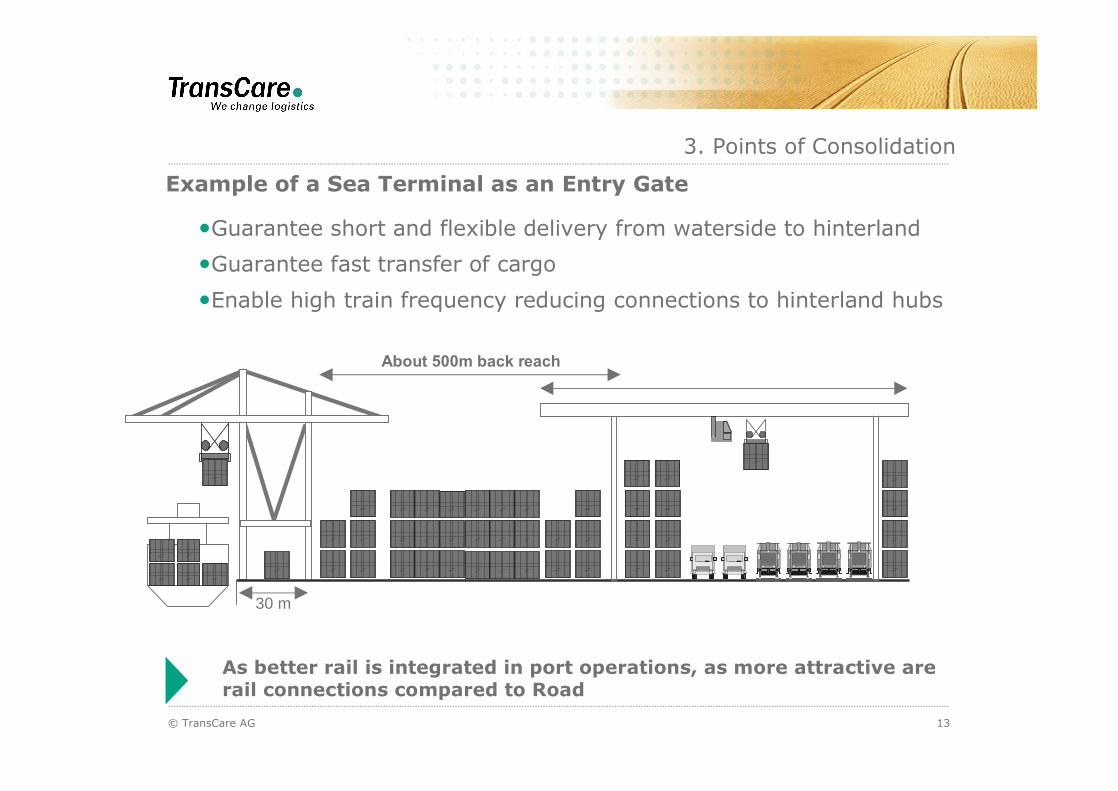

Example of a Sea Terminal as an Entry Gate

�Guarantee short and flexible delivery from waterside to hinterland

�Guarantee fast transfer of cargo

�Enable high train frequency reducing connections to hinterland hubs

3. Points of Consolidation

30 m

About 500m back reach

As better rail is integrated in port operations, as more attractive are rail connections compared to Road

14© TransCare AG

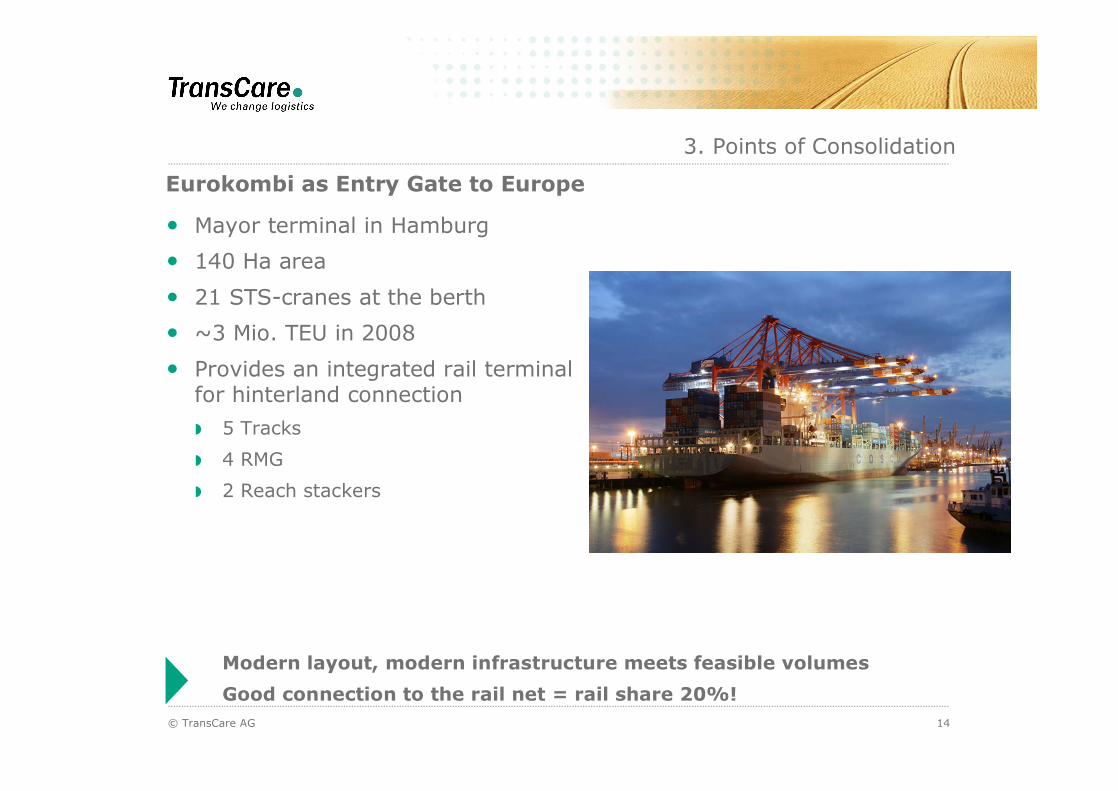

Eurokombi as Entry Gate to Europe

� Mayor terminal in Hamburg

� 140 Ha area

� 21 STS-cranes at the berth

� ~3 Mio. TEU in 2008

� Provides an integrated rail terminalfor hinterland connection

5 Tracks

4 RMG

2 Reach stackers

3. Points of Consolidation

Modern layout, modern infrastructure meets feasible volumes

Good connection to the rail net = rail share 20%!

15© TransCare AG

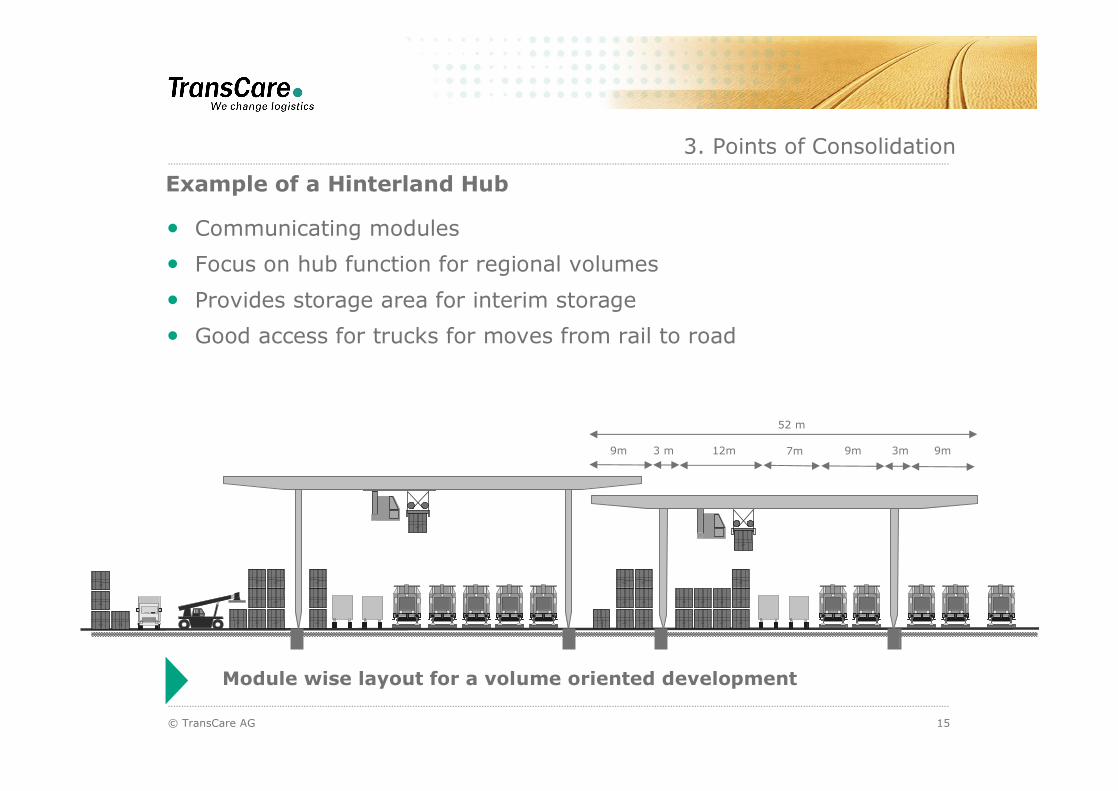

Example of a Hinterland Hub

� Communicating modules

� Focus on hub function for regional volumes

� Provides storage area for interim storage

� Good access for trucks for moves from rail to road

3. Points of Consolidation

52 m

3 m 12m 7m 9m 3m 9m9m

Module wise layout for a volume oriented development

16© TransCare AG

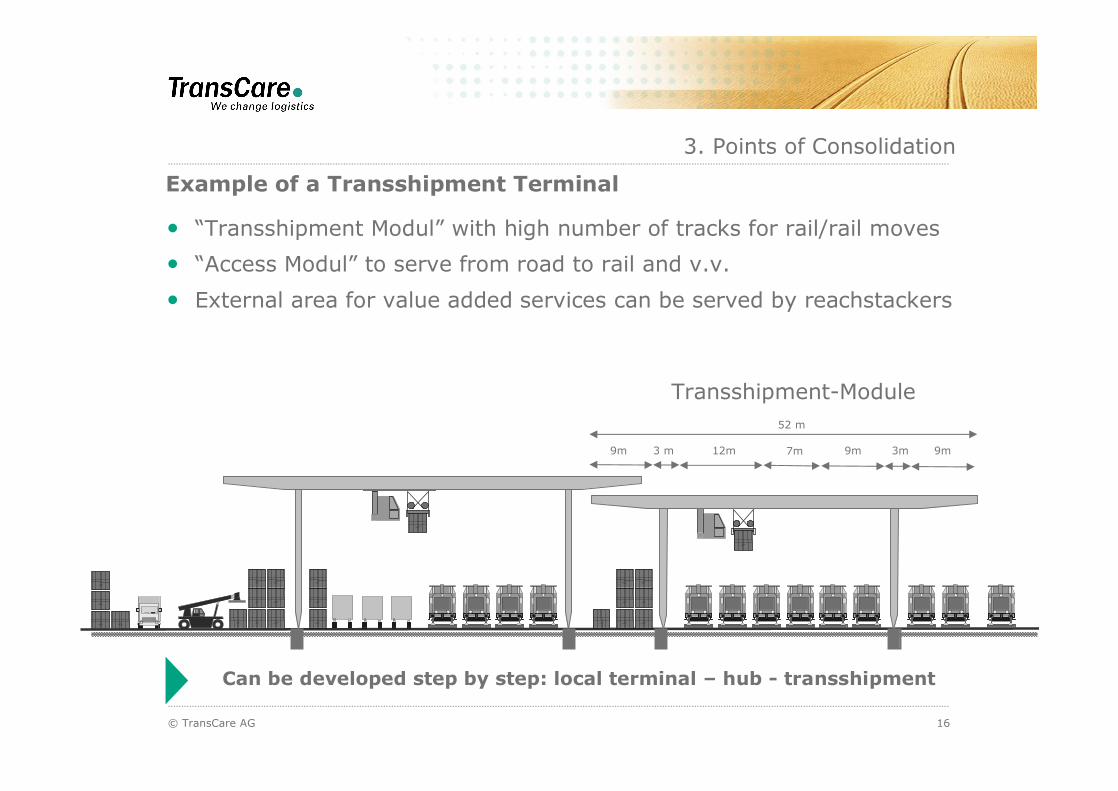

Example of a Transshipment Terminal

� �Transshipment Modul� with high number of tracks for rail/rail moves

� �Access Modul� to serve from road to rail and v.v.

� External area for value added services can be served by reachstackers

3. Points of Consolidation

9m

52 m

3 m 12m 7m 9m 3m 9m

Transshipment-Module

Can be developed step by step: local terminal � hub - transshipment

17© TransCare AG

Nuremberg as Gate Way to Eastern Europe

� Nuremberg is a hinterland hub with additional transshipment shares

Ideal consolidation point for volumes from Hamburg/Bremerhaven to move to Austria, Italy and Eastern Europe

� Success factors

Geographical position at the rail corridor to South and East Europe

Feasible rail infrastructure in all directions

Modern terminal layout with efficient processes

Transparent tariff policy an discrimination free access for all rail companies

3. Points of Consolidation

Good management develops a successful terminal from a ideal starting point

18© TransCare AG

KTL � Kombiterminal Ludwigshafen

Success Factors:

� Module wise construction referring to the volume development

� Communicating Modules

Details:

� 2 Modules

� 8 Tracks

� 4 communicating cranes

� External area for trailers'

� Integrated warehouse concept

3. Points of Consolidation

Integrated and extendable concept based on the logistics needs

Start 2000 = 70.000TEU/2009 = 350.000TEU/2015 = 800.000TEU!

© TransCare AG 19

Optimal Connection between Port and Hinterland

1. Key success Factors of Railway Supply Chains

2. Volumes and Volume Balance

3. Points of Consolidation

4. Integrated Rail-Roading

5. Impact of Liberalization

6. Summary

Content

20© TransCare AG

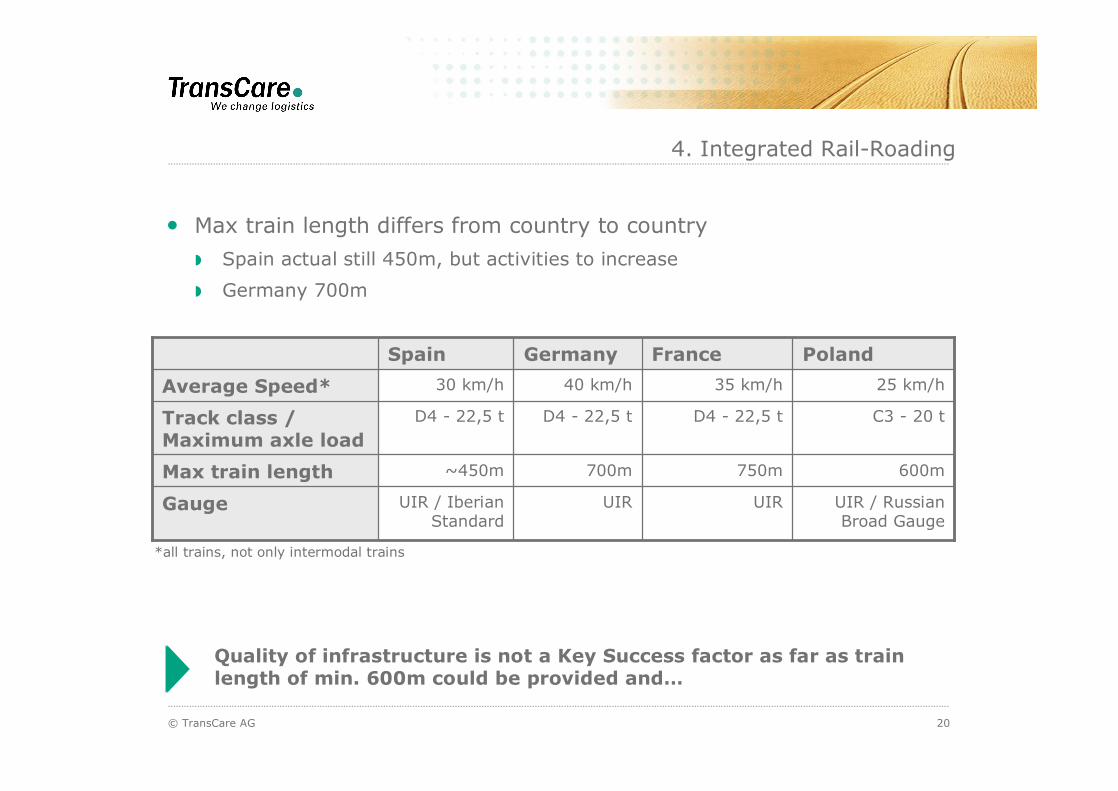

� Max train length differs from country to country

Spain actual still 450m, but activities to increase

Germany 700m

4. Integrated Rail-Roading

UIR / Russian Broad Gauge

UIRUIRUIR / Iberian Standard

Gauge

600m750m700m~450mMax train length

C3 - 20 tD4 - 22,5 tD4 - 22,5 tD4 - 22,5 tTrack class / Maximum axle load

25 km/h35 km/h 40 km/h 30 km/hAverage Speed*

PolandFranceGermanySpain

Quality of infrastructure is not a Key Success factor as far as train length of min. 600m could be provided and�

*all trains, not only intermodal trains

21© TransCare AG

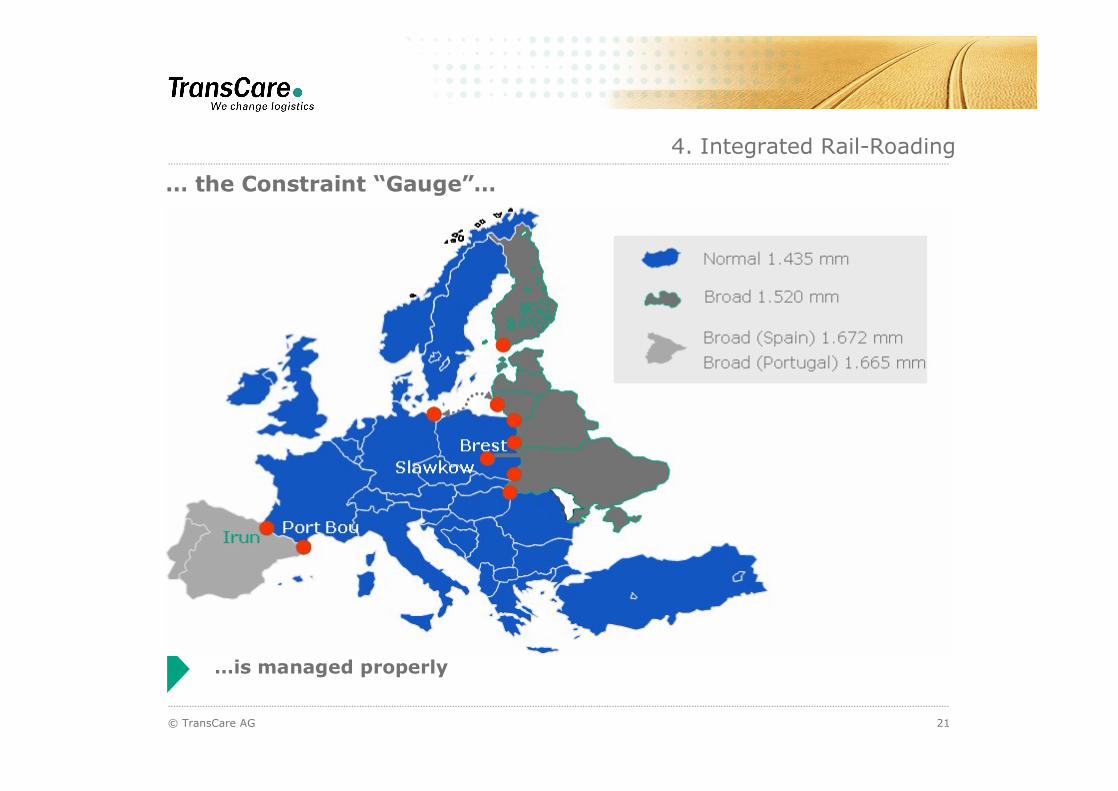

�is managed properly

� the Constraint �Gauge��

4. Integrated Rail-Roading

22© TransCare AG

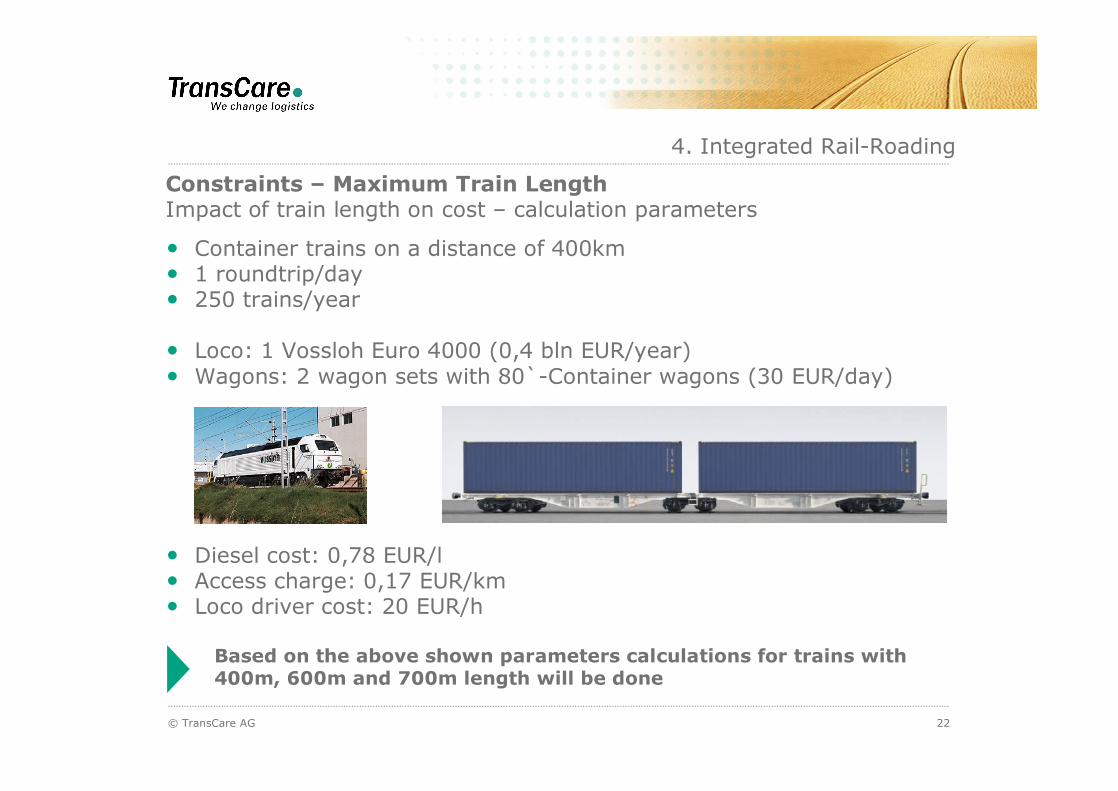

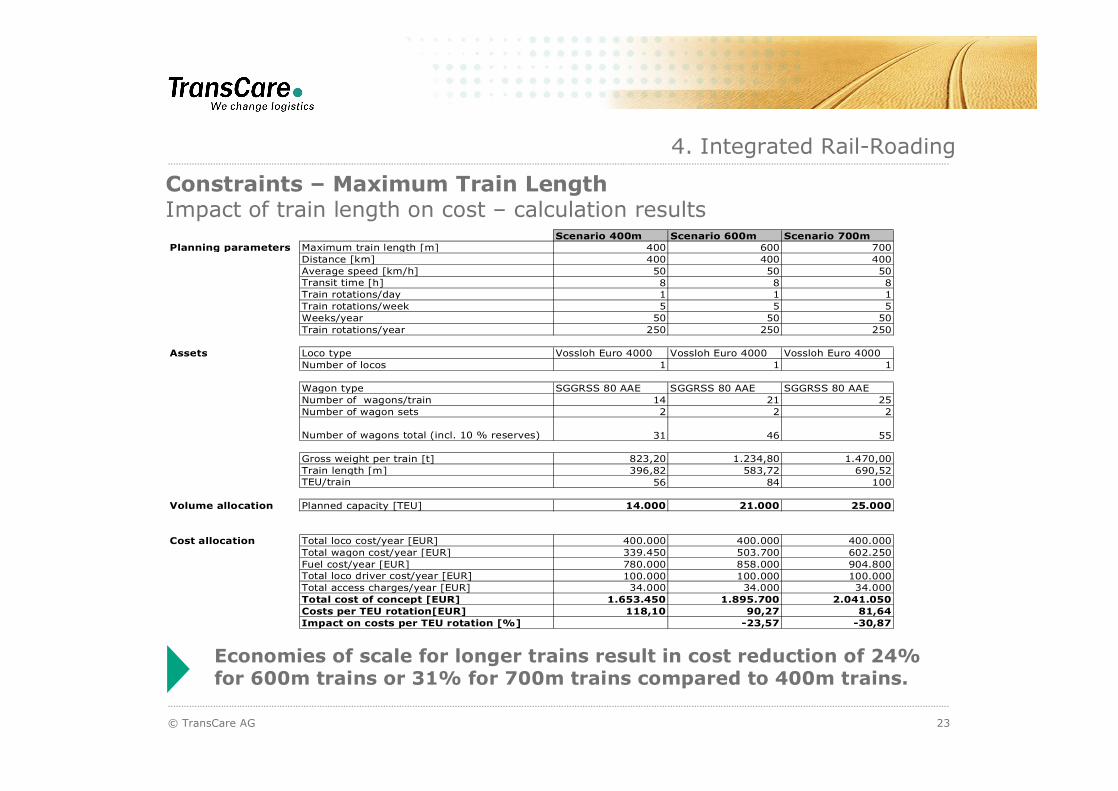

Based on the above shown parameters calculations for trains with400m, 600m and 700m length will be done

4. Integrated Rail-Roading

Constraints � Maximum Train LengthImpact of train length on cost � calculation parameters

� Container trains on a distance of 400km� 1 roundtrip/day� 250 trains/year

� Loco: 1 Vossloh Euro 4000 (0,4 bln EUR/year)� Wagons: 2 wagon sets with 80`-Container wagons (30 EUR/day)

� Diesel cost: 0,78 EUR/l� Access charge: 0,17 EUR/km� Loco driver cost: 20 EUR/h

23© TransCare AG

Economies of scale for longer trains result in cost reduction of 24% for 600m trains or 31% for 700m trains compared to 400m trains.

Scenario 400m Scenario 600m Scenario 700mPlanning parameters Maximum train length [m] 400 600 700

Distance [km] 400 400 400Average speed [km/h] 50 50 50Transit time [h] 8 8 8Train rotations/day 1 1 1Train rotations/week 5 5 5Weeks/year 50 50 50Train rotations/year 250 250 250

Assets Loco type Vossloh Euro 4000 Vossloh Euro 4000 Vossloh Euro 4000Number of locos 1 1 1

Wagon type SGGRSS 80 AAE SGGRSS 80 AAE SGGRSS 80 AAENumber of wagons/train 14 21 25Number of wagon sets 2 2 2

Number of wagons total (incl. 10 % reserves) 31 46 55

Gross weight per train [t] 823,20 1.234,80 1.470,00Train length [m] 396,82 583,72 690,52TEU/train 56 84 100

Volume allocation Planned capacity [TEU] 14.000 21.000 25.000

Cost allocation Total loco cost/year [EUR] 400.000 400.000 400.000Total wagon cost/year [EUR] 339.450 503.700 602.250Fuel cost/year [EUR] 780.000 858.000 904.800Total loco driver cost/year [EUR] 100.000 100.000 100.000Total access charges/year [EUR] 34.000 34.000 34.000Total cost of concept [EUR] 1.653.450 1.895.700 2.041.050Costs per TEU rotation[EUR] 118,10 90,27 81,64Impact on costs per TEU rotation [%] -23,57 -30,87

4. Integrated Rail-Roading

Constraints � Maximum Train LengthImpact of train length on cost � calculation results

24© TransCare AG

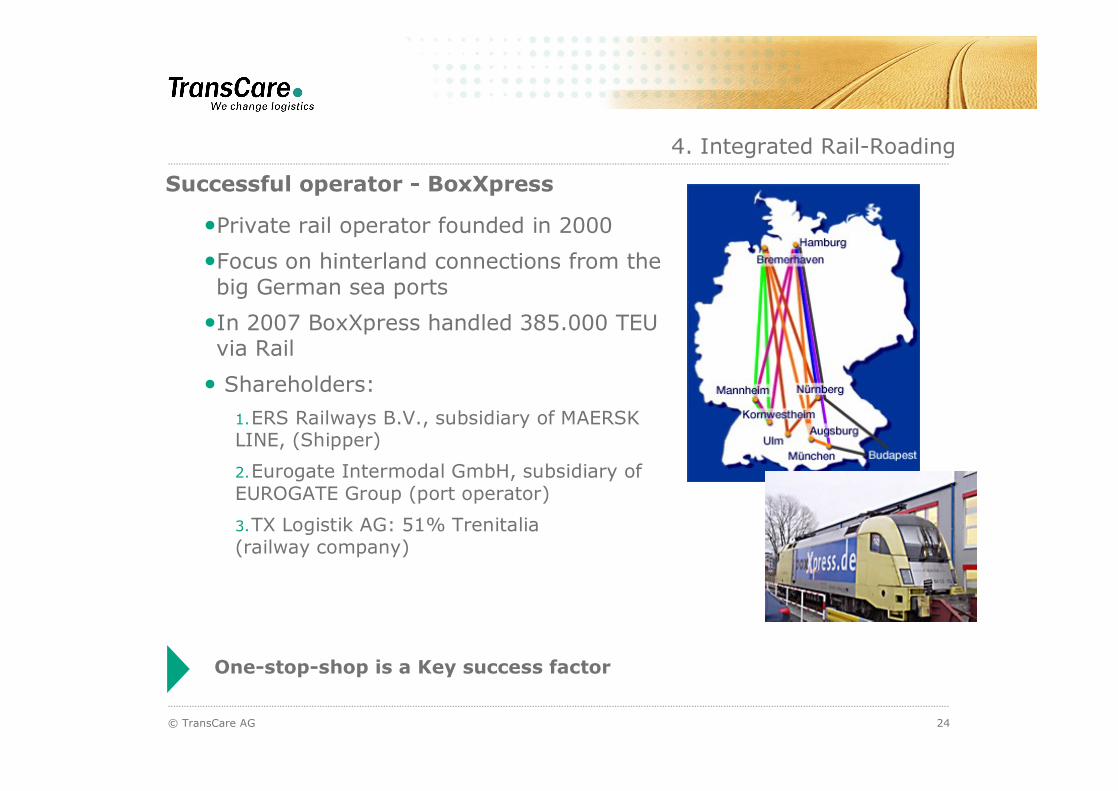

�Private rail operator founded in 2000

�Focus on hinterland connections from the big German sea ports

�In 2007 BoxXpress handled 385.000 TEU via Rail

� Shareholders:

1.ERS Railways B.V., subsidiary of MAERSK LINE, (Shipper)

2.Eurogate Intermodal GmbH, subsidiary of EUROGATE Group (port operator)

3.TX Logistik AG: 51% Trenitalia(railway company)

One-stop-shop is a Key success factor

4. Integrated Rail-Roading

Successful operator - BoxXpress

25© TransCare AG

Hinterland Hub

Main Line

Sea Port Terminal

4. Integrated Rail-Roading

Final Road Haulage

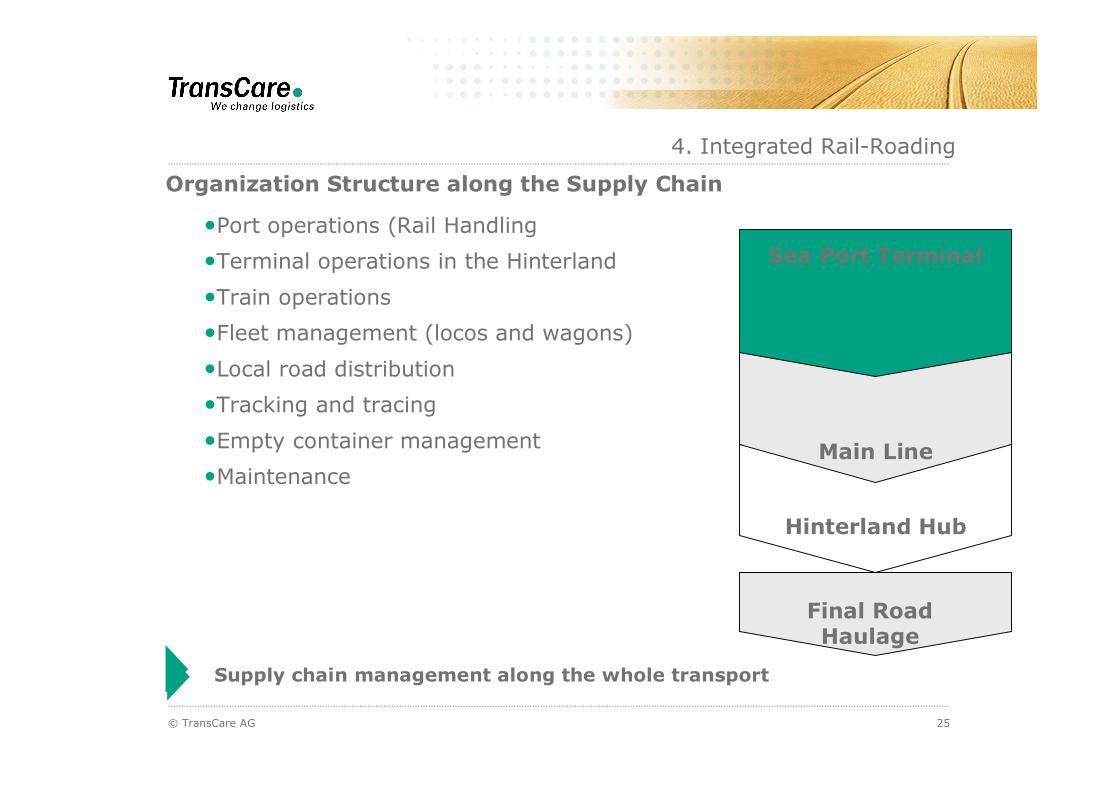

�Port operations (Rail Handling

�Terminal operations in the Hinterland

�Train operations

�Fleet management (locos and wagons)

�Local road distribution

�Tracking and tracing

�Empty container management

�Maintenance

Supply chain management along the whole transport

Organization Structure along the Supply Chain

© TransCare AG 26

Optimal Connection between Port and Hinterland

1. Key success Factors of Railway Supply Chains

2. Volumes and Volume Balance

3. Points of Consolidation

4. Integrated Rail-Roading

5. Impact of Liberalization

6. Summary

Content

27© TransCare AG

Impact of Liberalization on Rail Transport

� New players mean alternatives for the industries (for example in cases of strikes)

� New alliances and structures of cooperation

� Increased competition leads to increased quality and productivity

� Horizontal competition increased even vertical competitiveness

� Competition reduced the costs, pricing more competitive compared to Road

Establishing liberalization offers great chances for the Rail industry

5. Impact of Liberalization

28© TransCare AG 28

Source: IBM Global Business Services, Rail Liberalisation Index 2007

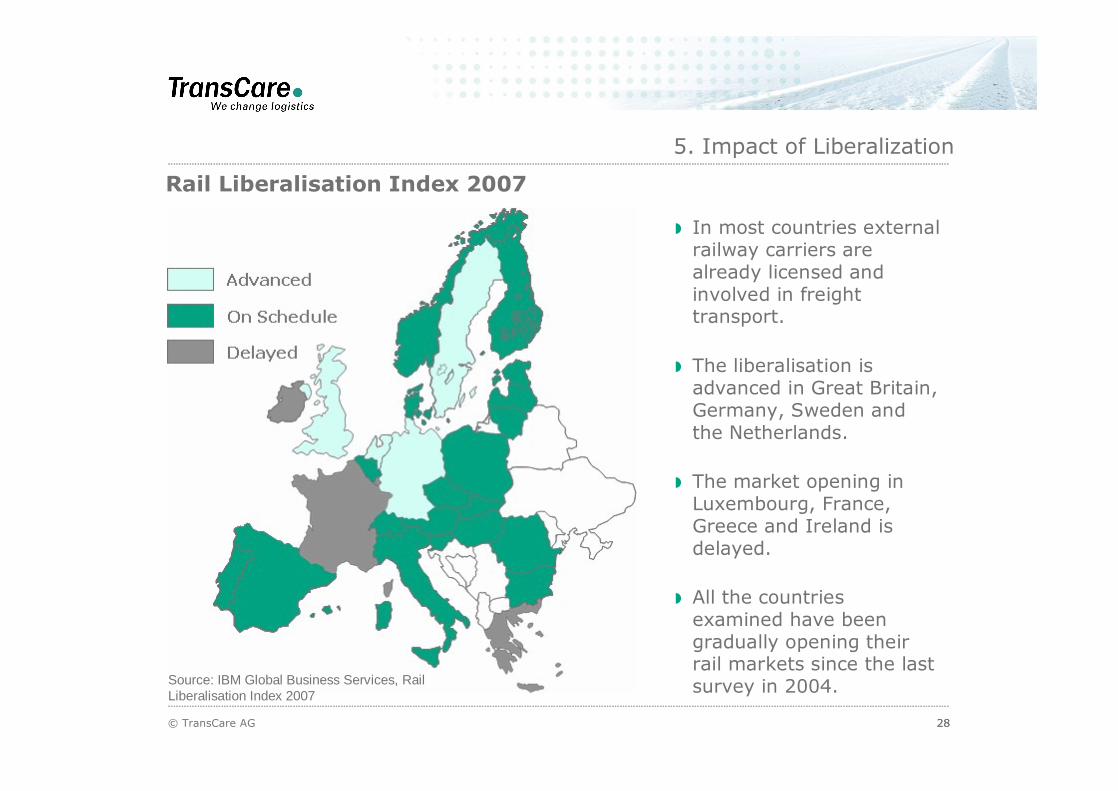

Rail Liberalisation Index 2007

In most countries external railway carriers are already licensed and involved in freight transport.

The liberalisation is advanced in Great Britain, Germany, Sweden and the Netherlands.

The market opening in Luxembourg, France, Greece and Ireland is delayed.

All the countries examined have been gradually opening their rail markets since the last survey in 2004.

5. Impact of Liberalization

29© TransCare AG

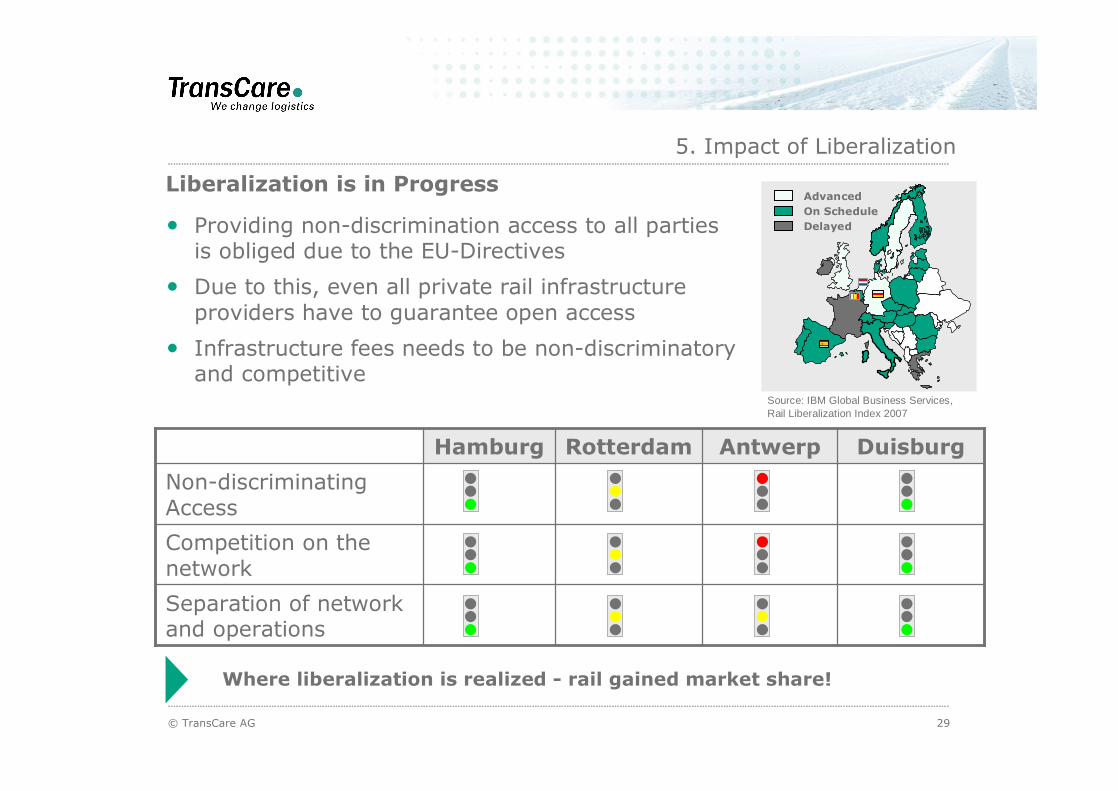

Liberalization is in Progress

Source: IBM Global Business Services, Rail Liberalization Index 2007

AdvancedOn ScheduleDelayed� Providing non-discrimination access to all parties

is obliged due to the EU-Directives

� Due to this, even all private rail infrastructureproviders have to guarantee open access

� Infrastructure fees needs to be non-discriminatoryand competitive

Where liberalization is realized - rail gained market share!

Separation of network and operations

Competition on the network

Non-discriminating Access

DuisburgAntwerpRotterdamHamburg

5. Impact of Liberalization

30© TransCare AG

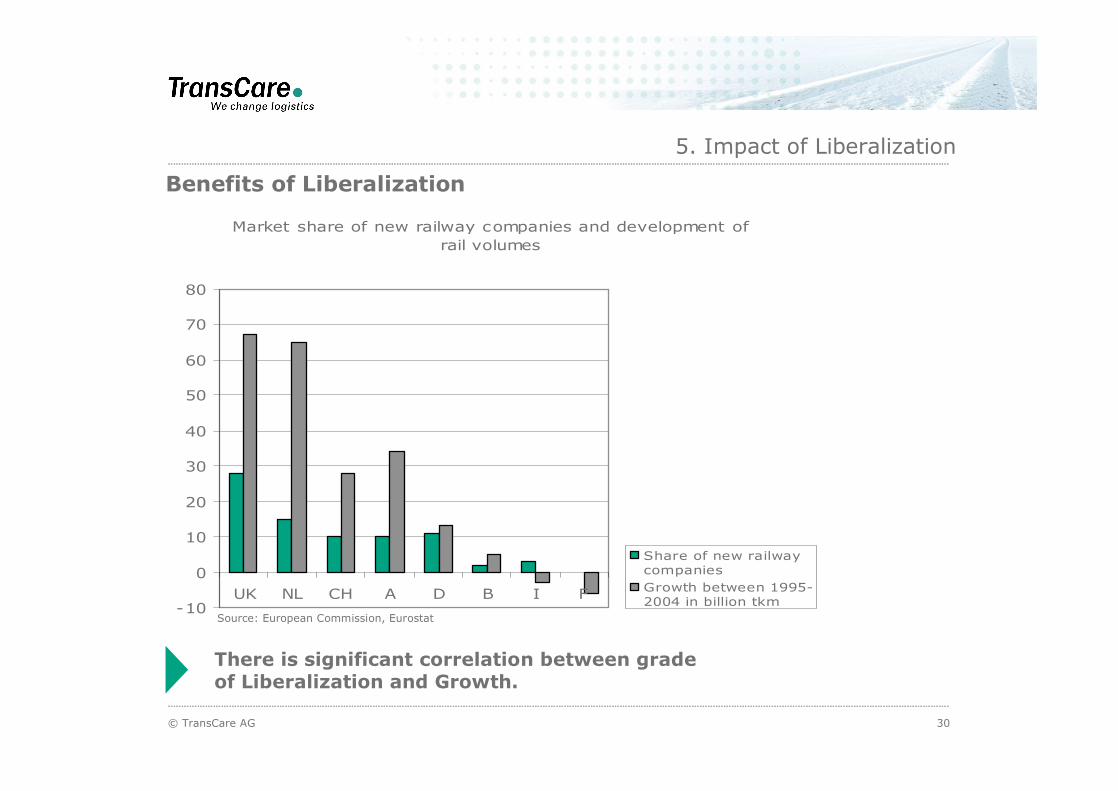

Benefits of Liberalization

There is significant correlation between grade of Liberalization and Growth.

Market share of new railway companies and development of rail volumes

-10

0

10

20

30

40

50

60

70

80

UK NL CH A D B I F

Share of new railwaycompaniesGrowth between 1995-2004 in billion tkm

Source: European Commission, Eurostat

5. Impact of Liberalization

31© TransCare AG

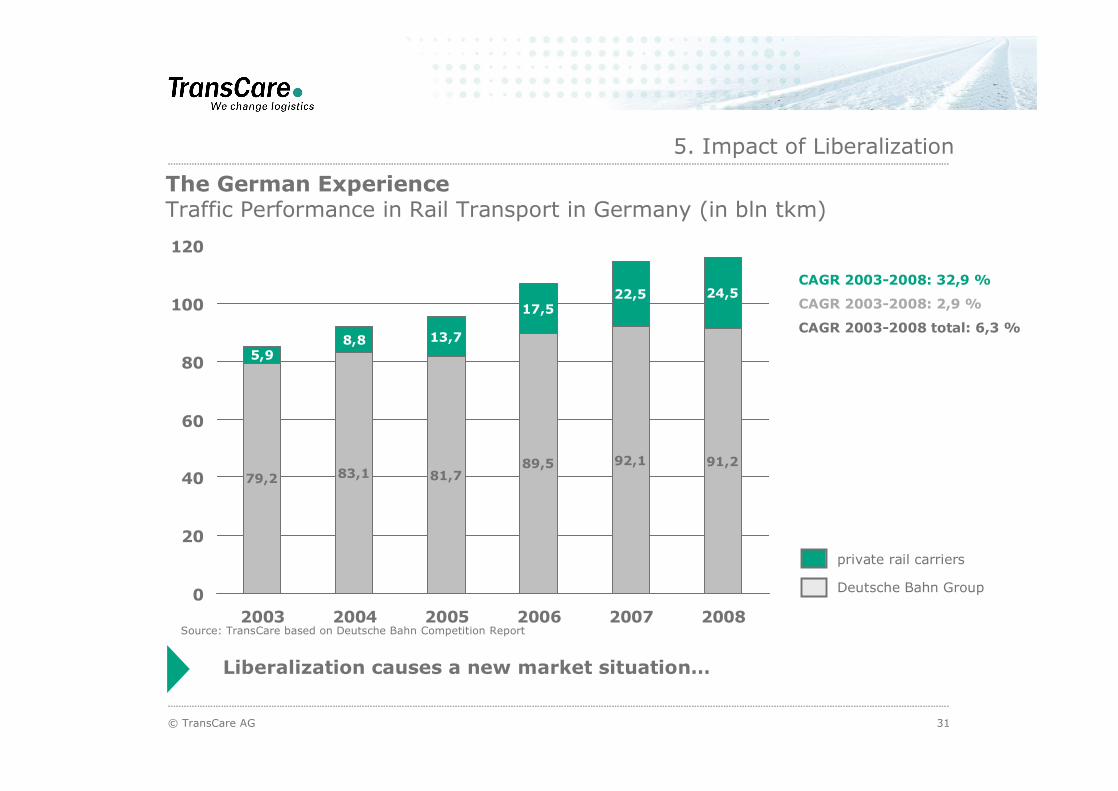

The German ExperienceTraffic Performance in Rail Transport in Germany (in bln tkm)

CAGR 2003-2008: 32,9 %

CAGR 2003-2008: 2,9 %

CAGR 2003-2008 total: 6,3 %

5. Impact of Liberalization

79,2 83,1 81,789,5 92,1 91,2

5,98,8 13,7

17,522,5 24,5

0

20

40

60

80

100

120

2003 2004 2005 2006 2007 2008

Liberalization causes a new market situation�

private rail carriers

Deutsche Bahn Group

Source: TransCare based on Deutsche Bahn Competition Report

32© TransCare AG

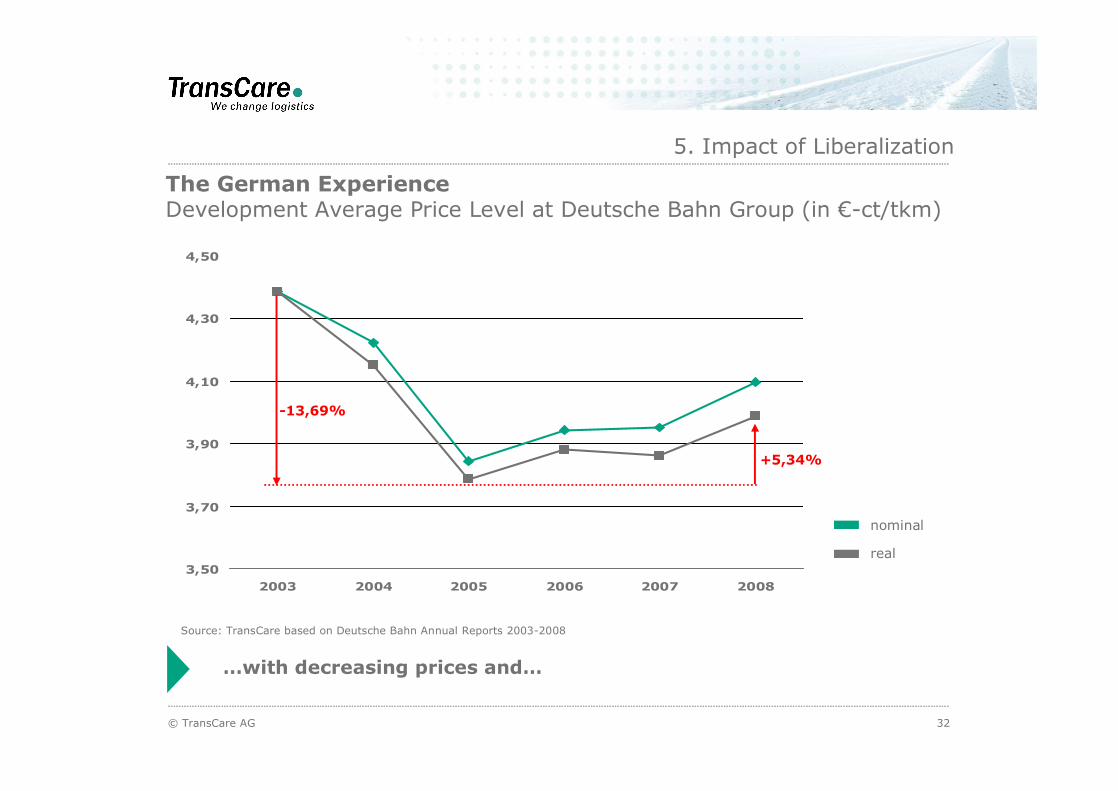

The German ExperienceDevelopment Average Price Level at Deutsche Bahn Group (in �-ct/tkm)

5. Impact of Liberalization

�with decreasing prices and�

3,50

3,70

3,90

4,10

4,30

4,50

2003 2004 2005 2006 2007 2008

nominal

real

-13,69%

+5,34%

Source: TransCare based on Deutsche Bahn Annual Reports 2003-2008

33© TransCare AG

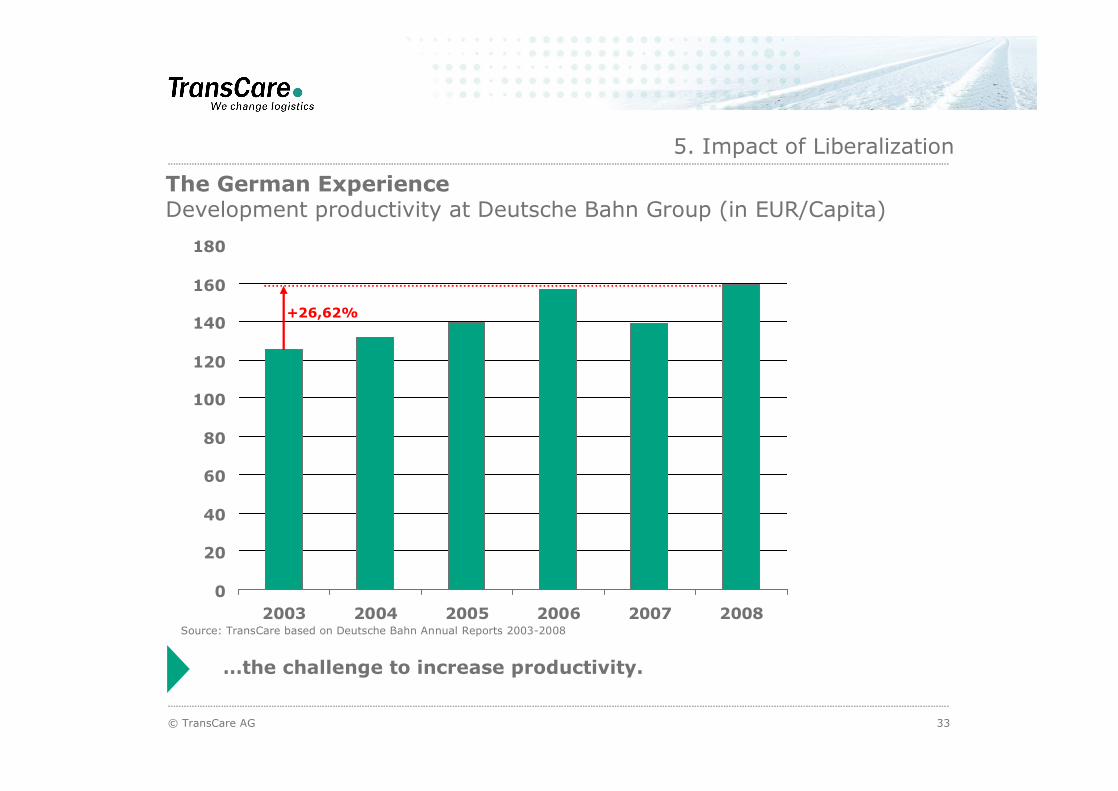

The German ExperienceDevelopment productivity at Deutsche Bahn Group (in EUR/Capita)

5. Impact of Liberalization

�the challenge to increase productivity.

0

20

40

60

80

100

120

140

160

180

2003 2004 2005 2006 2007 2008

+26,62%

Source: TransCare based on Deutsche Bahn Annual Reports 2003-2008

© TransCare AG 34

Optimal Connection between Port and Hinterland

1. Key success Factors of Railway Supply Chains

2. Volumes and Volume Balance

3. Points of Consolidation

4. Integrated Rail-Roading

5. Impact of Liberalization

6. Summary

Content

35© TransCare AG

Ports are not providing integrated rail terminals for intermodalhandling

Road market is not interested in rail

Railways are not really in competition � lack of private operators

Industry does not care � as far as road delivers

Nobody is taking consequently the initiative

There are great chances for rail transport in Spain! Small share of rail in transportation

Reasonable volumes

Long distances

Huge investments in infrastructure

Interest of big European players in Spanish market

Significant increase of intermodalism is possible

6. Summary

The lack of intermodal Transports in Spain is �House-made�

© TransCare AG 36

Thank you for your attention!