a handbook for trustees (2017 edition) english handbook.pdf · 5 continued on page 6 revocable...

TRANSCRIPT

A Handbook For Trustees(2017 Edition)

Administering a Special Needs TrustTABLE OF CONTENTS

INTRODUCTION AND DEFINITION OF TERMS ................4 Grantor .....................................................4 Trustee .....................................................4 Beneficiary .................................................4 Disability ...................................................4 Incapacity ..................................................4 Revocable Trust ...........................................5 Irrevocable Trust ..........................................5 SocialSecurityDisabilityInsurance ....................5 SupplementalSecurityIncome .........................5 Medicare ...................................................5 Medicaid ....................................................5

THE MOST IMPORTANT DISTINCTION .........................5 “Self-Settled” Special Needs Trusts ....................5 “Third-party”SpecialNeedsTrusts ....................6 The“SoleBenefit”Trust .................................6

THE SECOND MOST IMPORTANT DISTINCTION ..............6 SSDI/Medicare Recipients................................6 SSI/Medicaid Recipients .................................7 Veterans’Benefits ........................................7 Subsidized Housing .......................................7

Federal Subsidized Housing ........................7 Section 8 ..............................................8

TemporaryAssistanceforNeedyFamilies(“TANF”) .8 OtherMeans-TestedBenefitsPrograms ................8

ELIGIBILITY RULES FOR MEANS-TESTED PROGRAMS .......8 Income ......................................................8 Assets ..................................................... 10 Deeming .................................................. 10

“IWANTTOBUYA(PAYFOR)...” .......................... 10 Home, Upkeep and Utilities ........................... 10 Clothing .................................................. 11 Phone, Cable, and Internet Services ................. 11 Vehicle, Insurance, Maintenance, Gas ............... 11

©Copyright,SpecialNeedsAlliance

Pre-paid Burial/Funeral Arrangements .............. 11 Tuition, Books, Tutoring ................................ 11 Travel and Entertainment ............................. 11 Household Furnishings and Furniture ................ 11 Television, Computers and Electronics .............. 11 Durable Medical Equipment ........................... 12 Care Management ...................................... 12 Therapy,Medications,AlternativeTreatments ..... 12 Taxes ...................................................... 12 Legal, Guardianship and Trustee Fees ............... 12

LOANS, CREDIT, DEBIT AND GIFT CARDS .................. 12

TRUST ADMINISTRATION AND ACCOUNTING .............. 12 Trustee’s Duties ......................................... 13

No self-dealing ..................................... 13 Impartiality ......................................... 13 Delegation .......................................... 13 Investment ......................................... 13

Bond ...................................................... 13 Titling Assets ............................................ 14 Accounting Requirements ............................. 14 ReportingtoSocialSecurity ........................... 14 Reporting to Medicaid .................................. 15 Reporting to the Court ................................. 15 ModificationofTrust ................................... 15 Wrapping up the Trust .................................. 15

INCOME TAXATION OF SPECIAL NEEDS TRUSTS ........... 15 “Grantor” Trusts ........................................ 15

Tax ID numbers .................................... 16 Filing tax returns .................................. 16

Non-Grantor Trusts ..................................... 16 Tax ID numbers .................................... 16 Filing tax returns .................................. 16

QualifiedDisabilityTrust ............................... 16 Seeking Professional Tax Advice ...................... 16

FOR FURTHER READING ..................................... 17

4

Introduction and Definition of Terms“Special Needs” trusts are complicated and can be hard tounderstandandadminister.Theyarelikeothertrustsinmanyrespects—thegeneralrulesoftrustaccounting,lawandtaxationapply—butunlikemorefamiliartrustsinotherrespects.Theverynotionof“morefamiliar”typesoftrustswill,formany,beamusing—mostpeoplehave no particular experience dealing with formal trust arrangements, and special needs trusts are often establishedforthebenefitofindividualswhowouldnototherwise expect to have experience with trust concepts.

Theessentialpurposeofaspecialneedstrustisusuallytoimprovethequalityofanindividual’slifewithoutdisqualifyinghimorherfromeligibilityforpublicbenefits.Therefore,oneofthecentraldutiesofthetrustee of a special needs trust is to understand what publicbenefitsprogramsmightbeavailabletothebeneficiaryandhowreceiptofincome,orprovisionoffoodorshelter,mightaffecteligibility.Because there are numerous programs, competing(andsometimesevenconflicting)eligibilityrules,andatleasttwodifferenttypesofspecialneedstrusts to contend with, the entire area is fraught with opportunities to make mistakes. Because the stakes are often sohigh—thepublicbenefitsprogramsmaywellbeprovidingallthenecessitiesoflifetothebeneficiary—agoodunderstanding of the rules and programs iscriticallyimportant.

Before delving into a detailed discussion of special needs trust principles, it might be useful to defineafewterms:

GRANTOR(sometimes“Settlor”or“Trustor”)—thepersonwhoestablishesthetrustandgenerallythepersonwhoseassets fund the trust. There might be more than one grantorforagiventrust.Thetaxagencymaydefinethetermdifferentlythanthepublicbenefitsagency.Specialneeds trusts can make this term more confusing than othertypesoftrusts,sincethetruegrantorforsomepurposesmaynotbethesameasthepersonsigningthetrust instrument. If, for example, a parent creates a trustforthebenefitofachildwithadisability,andtheparent’sownmoneyfundsthetrust,theparentisthegrantor. In another case, where a parent has established a special needs trust to handle settlement proceeds fromapersonalinjurylawsuitorimproperlydirected

inheritance,theminorchild(throughaguardian)oranadult child will be the grantor, even though he or she didnotdecidetoestablishthetrustorsignanytrustdocuments.

TRUSTEE—thepersonwhomanagestrustassetsandadministersthetrustprovisions.Onceagain,theremaybetwo(ormore)trusteesactingatthesametime.Thegrantor(s)mayalsobethetrustee(s)insomecases.Thetrusteemaybeaprofessionaltrustee(suchasabanktrustdepartmentoralawyer),ormaybeafamilymemberortrustedadviser—thoughitmaybedifficulttoqualifyanon-professionaltoserveastrustee.

BENEFICIARY—thepersonforwhosebenefitthetrustisestablished.Thebeneficiaryofaspecialneedstrustwillusually(butnotalways)bedisabled.Whileabeneficiarymayalsoactastrusteeinsometypes

of trusts, a special needs trust beneficiarywillalmostneverbeableto act as trustee.

DISABILITY—formostpurposesinvolving special needs trusts, “disability”referstothestandardusedtodetermineeligibilityforSocialSecurityDisabilityInsuranceorSupplementalSecurityIncomebenefits:theinabilitytoperformanysubstantialgainfulemployment.

INCAPACITY(sometimesIncompetence)—although

“incapacity”and“incompetence”arenotinterchangeable,forourpurposestheymaybothrefertotheinabilityofatrusteetomanagethetrust,usuallybecauseofmentallimitations.Incapacityisusuallyimportantwhenappliedtothetrustee(ratherthanthebeneficiary),sincethetrustwillordinarilyprovide a mechanism for transition of power to a successor trustee if the original trustee becomes unabletomanagethetrust.Incapacityofabeneficiarymaysometimesbeimportantaswell.Noteverydisabilitywillresultinafindingofincapacity;itispossibleforaspecialneedstrustbeneficiarytobedisabled,butnotmentallyincapacitated.Minorsareconsidered to be incapacitated as a matter of law. The ageofmajoritydiffersslightlyfromstatetostate,though it is 18 in all but a handful of states.

AdministeringaSpecialNeedsTrust:A Handbook for Trustees

The essential purpose of a special needs trust is usually

to improve the quality of an individual’s life without

disqualifying him or her from eligibility to receive

public benefits.

5

continued on page 6

REVOCABLE TRUST—referstoanytrustwhichis,byitsown terms, revocable and/or amendable, meaning able tobeundone,orchanged.Manytrustsincommonusetodayarerevocable,butspecialneedstrustsareusuallyirrevocable, meaning permanent or irreversible.

IRREVOCABLE TRUST—meansanytrustwhichwasestablishedasirrevocable(thatis,noonereservedthepowertorevokethetrust)orwhichhasbecomeirrevocable(forexample,becauseofthedeathoftheoriginalgrantor).

SOCIAL SECURITY DISABILITY INSURANCE—sometimesreferredtoasSSDIorSSD,thisbenefitprogramisavailabletoindividualswithadisabilitywhoeitherhavesufficientworkhistorypriortobecomingdisabledorareentitledtoreceivebenefitsbyvirtueofbeinga dependent or survivor of a disabled, retired, or deceased insured worker. There is no “means” test forSSDIeligibility,andsospecialneedstrustsmaynotbenecessaryforsomebeneficiaries—theycanqualifyfor entitlements like SSD and Medicare even though theyreceiveincomeorhaveavailableresources.SSDIbeneficiariesmayalso,however,qualifyforSSI(seebelow)and/orMedicaidbenefits,requiringprotectionoftheirassetsandincometomaintaineligibility.Ofcourse,justbecauseabeneficiary’sbenefitsarenotmeans-tested,itdoesnotfollowthatthebeneficiarywillnotbenefitfromtheprotectionofatrustforotherreasons.

SUPPLEMENTAL SECURITY INCOME—betterknownbytheinitials“SSI,”thisbenefitprogramisavailabletolow-incomeindividualswhoaredisabled,blindorelderlyandhavelimitedincomeandfewassets.SSIeligibilityrulesform the basis for most other government program rules, andsotheybecomethecentralfocusformuchspecialneeds trust planning and administration.

MEDICARE—oneofthetwoprincipalhealthcareprogramsoperatedandfundedbygovernment—inthiscase,thefederalgovernment.Medicarebenefitsareavailabletoallthoseage65andover(providedonlythattheywouldbeentitledtoreceiveSocialSecuritybenefitsiftheychosetoretire,whetherornottheyactuallyareretired)andthose under 65 who have been receiving SSDI for at least twoyears.Medicareeligibilitymayforestalltheneedforor usefulness of a special needs trust. Medicare recipients withoutsubstantialassetsorincomemayfindthattheyhaveadifficulttimepayingformedications(whichhistoricallyhavenotbeencoveredbyMedicarebutbegantobepartiallycoveredin2004)orlong-termcare(whichremainslargelyoutsideMedicare’slistofbenefits).

MEDICAID—thesecondmajorgovernment-runhealthcareprogram.MedicaiddiffersfromMedicareinthreeimportantways:itisrunbystategovernments(thoughpartiallyfundedbyfederalpayments),itisavailabletothosewhomeetfinancialeligibilityrequirementsratherthan being based on the age of the recipient, and it coversallnecessarymedicalcare(thoughitiseasytoarguethatMedicaid’sdefinitionof“necessary”careistoonarrow).Becauseitisa“means-tested”healthcare

program,itscontinuedavailabilityisoftenthecentralfocus of special needs trust administration. Because Medicare covers such a small portion of long-term care costs,Medicaideligibilitybecomescentrallyimportantformanypersonswithdisabilities.

The Most Important Distinction Twoentirelydifferenttypesoftrustsareusuallylumpedtogetheras“specialneeds”trusts.Thetwotrusttypeswillbetreateddifferentlyfortaxpurposes,forbenefitdeterminations, and for court involvement. For most ofthediscussionthatfollows,itwillbenecessarytofirstdistinguishbetweenthetwotypesoftrusts.Thedistinctionisfurthercomplicatedbythefactthatthegrantor(thepersonestablishingthetrust,andtheeasiestwaytodistinguishbetweenthetwotrusttypes)isnotalwaysthepersonwhoactuallysignsthetrustdocument.

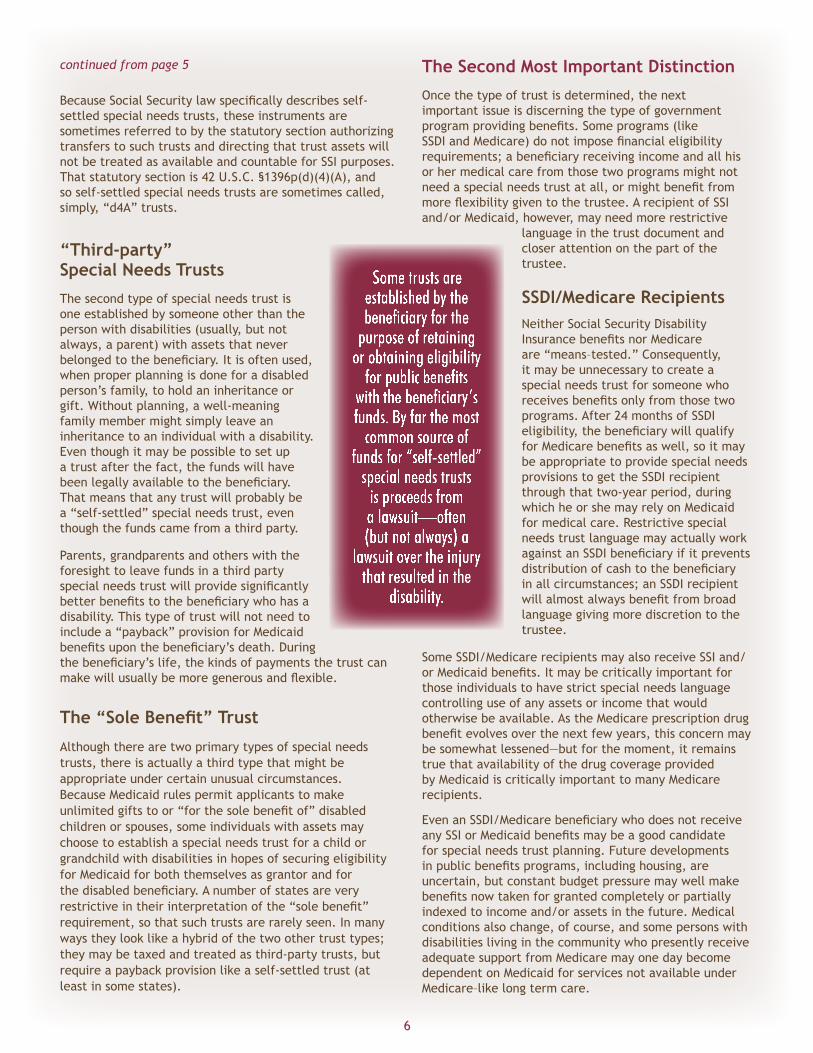

“Self-Settled” Special Needs Trusts Sometrustsareestablishedbythebeneficiary(orbysomeoneactingonhisorherbehalf)withthebeneficiary’sfundsforthepurposeofretainingorobtainingeligibilityforpublicbenefits—suchatrustisusuallyreferredtoasa“self-settled”specialneedstrust.Thebeneficiarymight,forexample,havereceivedanoutrightinheritance,orwonalottery.Byfarthemostcommon source of funds for “self-settled” special needs trusts,however,isproceedsfromalawsuit—often(butnotalways)alawsuitovertheinjurythatresultedinthedisability.Anothercommonscenariorequiringapersonwithadisabilitytoestablishaself-settledtrustiswhentheyreceiveadirectinheritancefromawell-intentioned,but ill-advised relative.

Agiventrustmaybetreatedashavingbeen“established”bythebeneficiaryevenifthebeneficiaryiscompletelyunabletoexecutedocuments,andevenifacourt,familymember,orlawyerrepresentingthebeneficiaryactuallysignedthetrustdocuments.Thekeytestindeterminingwhether a trust is self-settled is to determine whether thebeneficiaryhadtherighttooutrightpossessionofthe proceeds prior to the act establishing the trust. If so, publicbenefitseligibilityruleswilltreatthebeneficiaryas having set up the trust even though the actual implementationmayhavebeenundertakenbysomeoneelseactingontheirbehalf.Virtuallyallspecialneedstrusts established with funds recovered in litigation or through a direct inheritance will be “self-settled” trusts.

Self-settledspecialneedstrustsaredifferentfromthird-partytrustsintwoimportantways.First,self-settledtrusts must include a provision directing the trustee, ifthetrustcontainsanyfundsuponthedeathofthebeneficiary,topaybackanythingthestateMedicaidprogramhaspaidforthebeneficiary.Second,inmanystates, the rules governing permissible distributions for self-settledspecialneedstrustsaresignificantlymorerestrictivethanthosecontrollingthird-partyspecialneeds trusts.

6

BecauseSocialSecuritylawspecificallydescribesself-settled special needs trusts, these instruments are sometimesreferredtobythestatutorysectionauthorizingtransfers to such trusts and directing that trust assets will not be treated as available and countable for SSI purposes. Thatstatutorysectionis42U.S.C.§1396p(d)(4)(A),andso self-settled special needs trusts are sometimes called, simply,“d4A”trusts.

“Third-party” Special Needs Trusts

Thesecondtypeofspecialneedstrustisoneestablishedbysomeoneotherthanthepersonwithdisabilities(usually,butnotalways,aparent)withassetsthatneverbelongedtothebeneficiary.Itisoftenused,when proper planning is done for a disabled person’sfamily,toholdaninheritanceorgift. Without planning, a well-meaning familymembermightsimplyleaveaninheritancetoanindividualwithadisability.Eventhoughitmaybepossibletosetupa trust after the fact, the funds will have beenlegallyavailabletothebeneficiary.Thatmeansthatanytrustwillprobablybea “self-settled” special needs trust, even thoughthefundscamefromathirdparty.

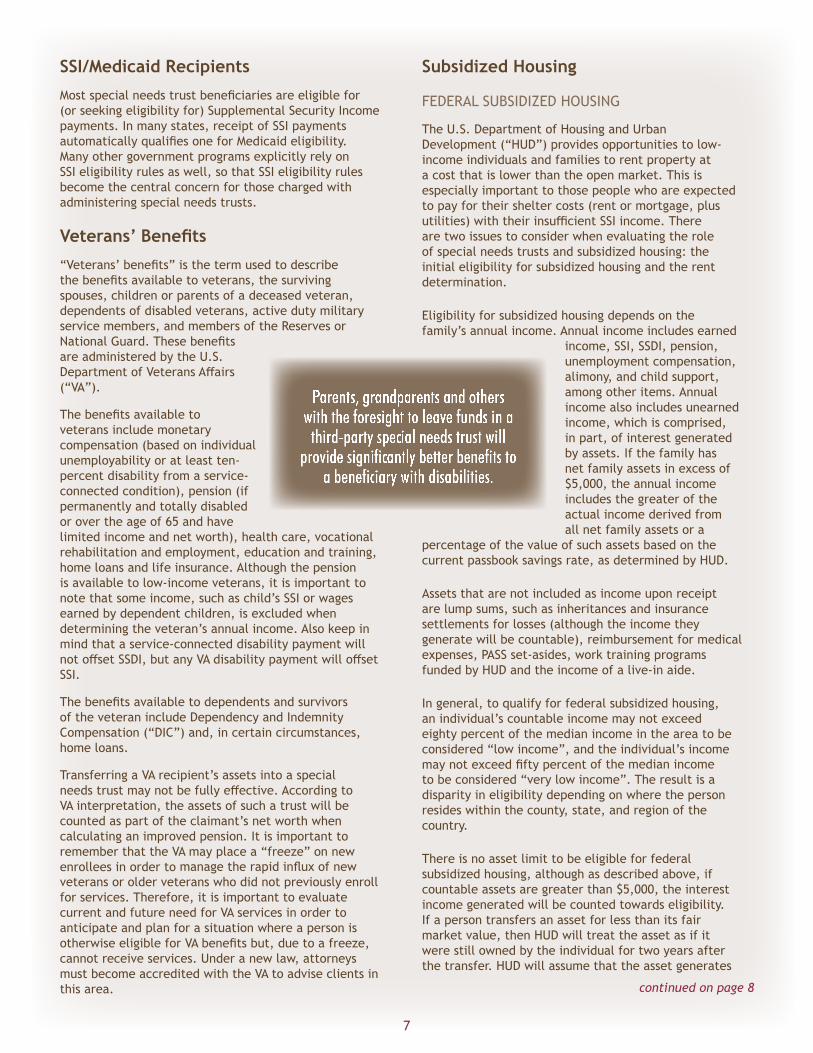

Parents, grandparents and others with the foresighttoleavefundsinathirdpartyspecialneedstrustwillprovidesignificantlybetterbenefitstothebeneficiarywhohasadisability.Thistypeoftrustwillnotneedtoincludea“payback”provisionforMedicaidbenefitsuponthebeneficiary’sdeath.Duringthebeneficiary’slife,thekindsofpaymentsthetrustcanmakewillusuallybemoregenerousandflexible.

The “Sole Benefit” Trust

Althoughtherearetwoprimarytypesofspecialneedstrusts,thereisactuallyathirdtypethatmightbeappropriate under certain unusual circumstances. Because Medicaid rules permit applicants to make unlimitedgiftstoor“forthesolebenefitof”disabledchildrenorspouses,someindividualswithassetsmaychoose to establish a special needs trust for a child or grandchildwithdisabilitiesinhopesofsecuringeligibilityfor Medicaid for both themselves as grantor and for thedisabledbeneficiary.Anumberofstatesareveryrestrictiveintheirinterpretationofthe“solebenefit”requirement,sothatsuchtrustsarerarelyseen.Inmanywaystheylooklikeahybridofthetwoothertrusttypes;theymaybetaxedandtreatedasthird-partytrusts,butrequireapaybackprovisionlikeaself-settledtrust(atleastinsomestates).

The Second Most Important Distinction

Oncethetypeoftrustisdetermined,thenextimportantissueisdiscerningthetypeofgovernmentprogramprovidingbenefits.Someprograms(likeSSDIandMedicare)donotimposefinancialeligibilityrequirements;abeneficiaryreceivingincomeandallhisor her medical care from those two programs might not needaspecialneedstrustatall,ormightbenefitfrommoreflexibilitygiventothetrustee.ArecipientofSSIand/orMedicaid,however,mayneedmorerestrictive

language in the trust document and closer attention on the part of the trustee.

SSDI/Medicare Recipients NeitherSocialSecurityDisabilityInsurancebenefitsnorMedicareare“means–tested.”Consequently,itmaybeunnecessarytocreateaspecial needs trust for someone who receivesbenefitsonlyfromthosetwoprograms. After 24 months of SSDI eligibility,thebeneficiarywillqualifyforMedicarebenefitsaswell,soitmaybe appropriate to provide special needs provisions to get the SSDI recipient throughthattwo-yearperiod,duringwhichheorshemayrelyonMedicaidfor medical care. Restrictive special needstrustlanguagemayactuallyworkagainstanSSDIbeneficiaryifitpreventsdistributionofcashtothebeneficiaryinallcircumstances;anSSDIrecipientwillalmostalwaysbenefitfrombroadlanguage giving more discretion to the trustee.

SomeSSDI/MedicarerecipientsmayalsoreceiveSSIand/orMedicaidbenefits.Itmaybecriticallyimportantforthose individuals to have strict special needs language controllinguseofanyassetsorincomethatwouldotherwise be available. As the Medicare prescription drug benefitevolvesoverthenextfewyears,thisconcernmaybesomewhatlessened—butforthemoment,itremainstruethatavailabilityofthedrugcoverageprovidedbyMedicaidiscriticallyimportanttomanyMedicarerecipients.

EvenanSSDI/MedicarebeneficiarywhodoesnotreceiveanySSIorMedicaidbenefitsmaybeagoodcandidatefor special needs trust planning. Future developments inpublicbenefitsprograms,includinghousing,areuncertain,butconstantbudgetpressuremaywellmakebenefitsnowtakenforgrantedcompletelyorpartiallyindexed to income and/or assets in the future. Medical conditions also change, of course, and some persons with disabilitieslivinginthecommunitywhopresentlyreceiveadequatesupportfromMedicaremayonedaybecomedependent on Medicaid for services not available under Medicare–like long term care.

continued from page 5

Some trusts are established by the beneficiary for the

purpose of retaining or obtaining eligibility

for public benefits with the beneficiary’s funds. By far the most

common source of funds for “self-settled”

special needs trusts is proceeds from a lawsuit—often (but not always) a

lawsuit over the injury that resulted in the

disability.

7

SSI/Medicaid Recipients

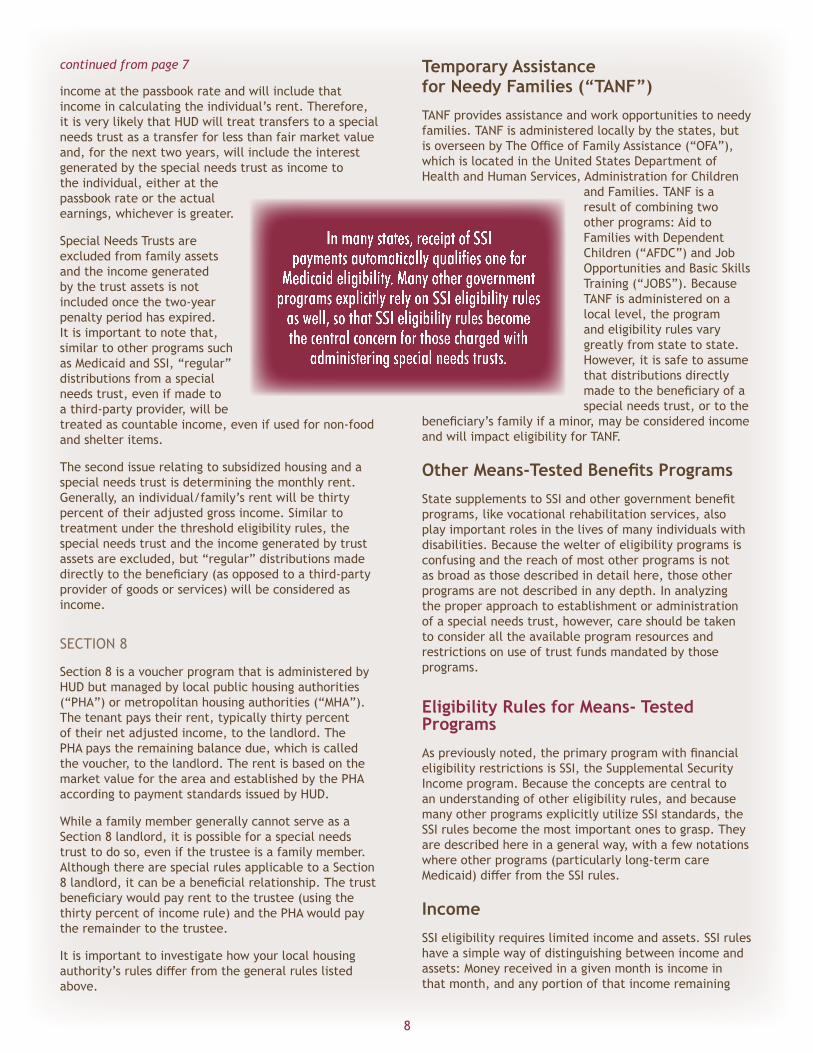

Mostspecialneedstrustbeneficiariesareeligiblefor(orseekingeligibilityfor)SupplementalSecurityIncomepayments.Inmanystates,receiptofSSIpaymentsautomaticallyqualifiesoneforMedicaideligibility.ManyothergovernmentprogramsexplicitlyrelyonSSIeligibilityrulesaswell,sothatSSIeligibilityrulesbecome the central concern for those charged with administering special needs trusts.

Veterans’ Benefits

“Veterans’benefits”isthetermusedtodescribethebenefitsavailabletoveterans,thesurvivingspouses, children or parents of a deceased veteran, dependentsofdisabledveterans,activedutymilitaryservice members, and members of the Reserves or NationalGuard.ThesebenefitsareadministeredbytheU.S.DepartmentofVeteransAffairs(“VA”).

Thebenefitsavailabletoveteransincludemonetarycompensation(basedonindividualunemployabilityoratleastten-percentdisabilityfromaservice-connectedcondition),pension(ifpermanentlyandtotallydisabledor over the age of 65 and have limitedincomeandnetworth),healthcare,vocationalrehabilitationandemployment,educationandtraining,home loans and life insurance. Although the pension is available to low-income veterans, it is important to note that some income, such as child’s SSI or wages earnedbydependentchildren,isexcludedwhendetermining the veteran’s annual income. Also keep in mindthataservice-connecteddisabilitypaymentwillnotoffsetSSDI,butanyVAdisabilitypaymentwilloffsetSSI.

ThebenefitsavailabletodependentsandsurvivorsoftheveteranincludeDependencyandIndemnityCompensation(“DIC”)and,incertaincircumstances,home loans.

Transferring a VA recipient’s assets into a special needstrustmaynotbefullyeffective.AccordingtoVA interpretation, the assets of such a trust will be counted as part of the claimant’s net worth when calculating an improved pension. It is important to rememberthattheVAmayplacea“freeze”onnewenrolleesinordertomanagetherapidinfluxofnewveteransorolderveteranswhodidnotpreviouslyenrollfor services. Therefore, it is important to evaluate current and future need for VA services in order to anticipate and plan for a situation where a person is otherwiseeligibleforVAbenefitsbut,duetoafreeze,cannotreceiveservices.Underanewlaw,attorneysmust become accredited with the VA to advise clients in this area.

Subsidized Housing

FEDERAL SUBSIDIZED HOUSING

The U.S. Department of Housing and Urban Development(“HUD”)providesopportunitiestolow-incomeindividualsandfamiliestorentpropertyata cost that is lower than the open market. This is especiallyimportanttothosepeoplewhoareexpectedtopayfortheirsheltercosts(rentormortgage,plusutilities)withtheirinsufficientSSIincome.Thereare two issues to consider when evaluating the role ofspecialneedstrustsandsubsidizedhousing:theinitialeligibilityforsubsidizedhousingandtherentdetermination.

Eligibilityforsubsidizedhousingdependsonthefamily’sannualincome.Annualincomeincludesearned

income, SSI, SSDI, pension, unemploymentcompensation,alimony,andchildsupport,among other items. Annual income also includes unearned income, which is comprised, in part, of interest generated byassets.Ifthefamilyhasnetfamilyassetsinexcessof$5,000, the annual income includes the greater of the actual income derived from allnetfamilyassetsora

percentage of the value of such assets based on the currentpassbooksavingsrate,asdeterminedbyHUD.

Assets that are not included as income upon receipt are lump sums, such as inheritances and insurance settlementsforlosses(althoughtheincometheygeneratewillbecountable),reimbursementformedicalexpenses, PASS set-asides, work training programs fundedbyHUDandtheincomeofalive-inaide.

Ingeneral,toqualifyforfederalsubsidizedhousing,anindividual’scountableincomemaynotexceedeightypercentofthemedianincomeintheareatobeconsidered “low income”, and the individual’s income maynotexceedfiftypercentofthemedianincometobeconsidered“verylowincome”.Theresultisadisparityineligibilitydependingonwherethepersonresideswithinthecounty,state,andregionofthecountry.

There is no asset limit to be eligible for federal subsidized housing, although as described above, if countable assets are greater than $5,000, the interest incomegeneratedwillbecountedtowardseligibility.If a person transfers an asset for less than its fair market value, then HUD will treat the asset as if it werestillownedbytheindividualfortwoyearsafterthe transfer. HUD will assume that the asset generates

continued on page 8

Parents, grandparents and others with the foresight to leave funds in a

third-party special needs trust will provide significantly better benefits to

a beneficiary with disabilities.

8

income at the passbook rate and will include that income in calculating the individual’s rent. Therefore, itisverylikelythatHUDwilltreattransferstoaspecialneeds trust as a transfer for less than fair market value and,forthenexttwoyears,willincludetheinterestgeneratedbythespecialneedstrustasincometothe individual, either at the passbook rate or the actual earnings, whichever is greater.

Special Needs Trusts are excludedfromfamilyassetsand the income generated bythetrustassetsisnotincludedoncethetwo-yearpenaltyperiodhasexpired.It is important to note that, similar to other programs such as Medicaid and SSI, “regular” distributions from a special needs trust, even if made to athird-partyprovider,willbetreated as countable income, even if used for non-food and shelter items.

The second issue relating to subsidized housing and a specialneedstrustisdeterminingthemonthlyrent.Generally,anindividual/family’srentwillbethirtypercent of their adjusted gross income. Similar to treatmentunderthethresholdeligibilityrules,thespecialneedstrustandtheincomegeneratedbytrustassets are excluded, but “regular” distributions made directlytothebeneficiary(asopposedtoathird-partyproviderofgoodsorservices)willbeconsideredasincome.

SECTION 8

Section8isavoucherprogramthatisadministeredbyHUDbutmanagedbylocalpublichousingauthorities(“PHA”)ormetropolitanhousingauthorities(“MHA”).Thetenantpaystheirrent,typicallythirtypercentof their net adjusted income, to the landlord. The PHApaystheremainingbalancedue,whichiscalledthe voucher, to the landlord. The rent is based on the marketvaluefortheareaandestablishedbythePHAaccordingtopaymentstandardsissuedbyHUD.

WhileafamilymembergenerallycannotserveasaSection 8 landlord, it is possible for a special needs trusttodoso,evenifthetrusteeisafamilymember.Although there are special rules applicable to a Section 8landlord,itcanbeabeneficialrelationship.Thetrustbeneficiarywouldpayrenttothetrustee(usingthethirtypercentofincomerule)andthePHAwouldpaythe remainder to the trustee.

Itisimportanttoinvestigatehowyourlocalhousingauthority’srulesdifferfromthegeneralruleslistedabove.

Temporary Assistance for Needy Families (“TANF”)

TANFprovidesassistanceandworkopportunitiestoneedyfamilies.TANFisadministeredlocallybythestates,butisoverseenbyTheOfficeofFamilyAssistance(“OFA”),which is located in the United States Department of Health and Human Services, Administration for Children

and Families. TANF is a result of combining two otherprograms:AidtoFamilies with Dependent Children(“AFDC”)andJobOpportunities and Basic Skills Training(“JOBS”).BecauseTANF is administered on a local level, the program andeligibilityrulesvarygreatlyfromstatetostate.However, it is safe to assume thatdistributionsdirectlymadetothebeneficiaryofaspecial needs trust, or to the

beneficiary’sfamilyifaminor,maybeconsideredincomeandwillimpacteligibilityforTANF.

Other Means-Tested Benefits Programs

StatesupplementstoSSIandothergovernmentbenefitprograms, like vocational rehabilitation services, also playimportantrolesinthelivesofmanyindividualswithdisabilities.Becausethewelterofeligibilityprogramsisconfusing and the reach of most other programs is not as broad as those described in detail here, those other programsarenotdescribedinanydepth.Inanalyzingthe proper approach to establishment or administration of a special needs trust, however, care should be taken to consider all the available program resources and restrictionsonuseoftrustfundsmandatedbythoseprograms.

Eligibility Rules for Means- Tested Programs

Aspreviouslynoted,theprimaryprogramwithfinancialeligibilityrestrictionsisSSI,theSupplementalSecurityIncome program. Because the concepts are central to anunderstandingofothereligibilityrules,andbecausemanyotherprogramsexplicitlyutilizeSSIstandards,theSSIrulesbecomethemostimportantonestograsp.Theyaredescribedhereinageneralway,withafewnotationswhereotherprograms(particularlylong-termcareMedicaid)differfromtheSSIrules.

Income

SSIeligibilityrequireslimitedincomeandassets.SSIruleshaveasimplewayofdistinguishingbetweenincomeandassets:Moneyreceivedinagivenmonthisincomeinthatmonth,andanyportionofthatincomeremaining

continued from page 7

In many states, receipt of SSI payments automatically qualifies one for

Medicaid eligibility. Many other government programs explicitly rely on SSI eligibility rules

as well, so that SSI eligibility rules become the central concern for those charged with

administering special needs trusts.

9

onthefirstdayofthenextmonthbecomesanasset.SSIrules also distinguish between what is “countable” or “excluded,” “regular” or “irregular,” and “unearned” or “earned” income. “Countable” income means that itisusedtocomputeeligibilityandbenefitamount.“Excluded” means that it is not counted. “Regular” means that it is received on a periodic basis, at least two or more times per quarter or in consecutive months, and “irregular” or “infrequent” means that it is not periodic orpredictable.“Unearned”meansthatitispassivelyreceived,suchasSSDIbenefitsorbankaccountinterest.“Earned” means that work is performed in exchange for the income. An SSI recipient is permitted to receive asmallamountofanykindofincome($20permonth)withoutreducingbenefits.Thatamountissometimesreferred to as the SSI “disregard” amount.

Eachclassificationorgroupinghasasomewhatdifferentrule, and it is an understatement to call these income rules“confusing.”AnyunearnedincomereducestheSSIbenefitbytheamountoftheincome,soinvestmentincomeorgiftedmoneysimplyreducesthebenefitdollarfor dollar, less the disregard. Earned income is treated morefavorably,onlyreducingbenefitsbyabouthalfofthe earnings. This is designed to encourage SSI recipients toreturntotheworkforce.Keepinginmindthatdisabilityisdefinedas“unabletoperformanysubstantialgainfulactivity,”itiseasytoseethatanysignificantamountofearnedincomewilleventuallyimperilSSIeligibilityand,sincetrustadministrationdoesnotusuallyinvolveearnedincomeinanyevent,wewillnotattempttodealwiththose issues here.

SSI also has a concept of “in-kind support and maintenance”(ISM)thatiscentraltomuchunderstandingofspecialneedstrustadministration.Anypaymentfromathirdparty(includingatrust)fornecessitiesoflife—foodorshelter(notethatthefederalgovernmentdeleted“clothing”fromthelistofnecessitiesinMarch2005)toathirdpartyproviderofgoodsorservices—willbetreatedas countable income, albeit subject to special rules for calculatingitseffect.

TheeffectofreceivingISMonSSIbenefitsisdifferentfrom the receipt of cash distributions. Where as cash paymentsreducetheSSIpaymentdollarfordollar,ISMreducesthebenefitbythelesserofthepresumedmaximum value of the items provided or an amount calculatedbydividingthemaximumSSIbenefitbythreeand adding the $20 disregard amount.

For2017themaximumfederalSSIbenefitforasingleperson is $735. One-third of that amount is $245, and sothemaximumreductioninbenefitscausedbyISM(nomatterhowhighthevalue)is$265permonth.Themeaning of that confusing collection of information is bestillustratedusinganexample(CAUTION:somestatesprovideSSIsupplementalpaymentsthataffectthiscalculation).

ConsiderJohn,whoisdisabledasaresultofhisseriousmentalillness.Hehasnoworkhistory,andhedoesnot

qualifyforSSDI.Heisanadult,livingonhisown.HequalifiesforthemaximumfederalSSIbenefitof$735;helives in a state which does not provide an SSI supplement.

IfJohn’smothergiveshim$100cashpermonth(forfoodandcigarettes),heisrequiredtoreportthatascountableunearnedincomeeachmonth.AlthoughSSImaytaketwo or three months to accomplish the adjustment, the programwilleventuallywithhold$80($100minusthe$20disregard)fromhisbenefitforeachmonthinwhichhis mother makes a cash gift to him. The same result will obtainifJohn’smotheristrusteeofaspecialneedstrustforJohnandthecashcomesfromthattrust.

If,however,John’smotherdoesnotgivehimthe$100directly,butinsteadpurchases$70worthoffoodand$30worthofcigaretteseachmonth,onlythefoodwillaffecthisSSIpayment—reducingitby$50($70minusthe$20disregard).Ifshepurchases$20worthoffoodand$80worthofcigarettes,therewillbenoeffectatall—thefoodpurchaseiswithinthe$20monthlydisregardamount.Similarly,ifshepurchases$20worthof cigarettes and $30 worth of movie tickets, there will benoeffect—providedthatthemovieticketscannotbeturnedinforcash(becauseifthemovieticketscanbeconvertedtocash,Johncould—evenifhedoesnot—convertthemovieticketsintopaymentforfoodorshelter).

Inotherwords,theeffectofJohn’smother’spaymentstohimorforhisbenefitchangeswiththenatureofherpayments.Anycashsheprovidestohim(overthe$20monthlyamountignoredbySSI)reduceshisSSIpaymentdirectly.DirectpurchaseofitemsotherthanfoodorshelterdoesnotaffecthisSSI,solongasthepurchaseditemscannotbeconvertedtofoodorshelter.Finally,anypaymentshemakesforfoodorshelterreduceshisSSIcheckaswell,butnotasharshlyascashpaymentsdirectlytoJohn.

NowsupposethatJohn’smotherdecidestogiveupontryingtoworkaroundthestricturesofSSIrules,andshesimplypayshisrentatanadultcarefacilitythatprovideshismeals.Assumethatthefacilitycostsher$1500permonth,whichshepaysfromherownpocket.BecauseoftheISMrules,John’sSSIbenefitwillbereducedbyonly$265permonth,andsohisSSIcheckwillbe$490.Criticallyimportant,however,JohnwillstillqualifyforMedicaidbenefitsinmoststatesbecausehereceivessomeamountofSSI.IftheadultcarehomepaymentcomesfromaspecialneedstrustforJohn’sbenefit,thesame result will occur, assuming that the room and board portionofthepaymentexceeds$265.Incidentally,thesameresultwillalsoobtainifJohn’smothersimplytakeshim in and allows him to live and eat with her without charging him rent.

NowassumethatJohndoeshaveaworkhistorybeforebecomingdisabled,andthathequalifiestoreceive$500per month from SSDI. Because he has been receiving SSDI formorethantwoyears,healsoqualifiesforMedicare.

continued on page 10

10

Because his countable income is less than $735, he continuestoreceive$255inSSIbenefits($20oftheSSDisdisregarded),andqualifiesforMedicaidaswell(wewillignoretheeffectoftheQMBandSLMBprogramsforqualified,speciallow-incomeMedicarebeneficiaries,andtheMedicarePartBpremiumwhichwouldordinarilybewithheldfromhisSSDIcheck).NowifJohn’smotherpayshisrentattheadult care home, or takes him into her own home, he willlosehisSSIaltogether—sinceheisreceivinglessthan$265permonthfromSSI,theeffectoftheISMruleswillbetoknockhimofftheprogram.UnlessheseparatelyqualifiesforMedicaid,hewillalsolosehiscoverage under that program. The income strictures are the same or similar for other programs, with one important exception. In some states, but not all, eligibilityforcommunityorlong-termcareMedicaidis also dependent on countable income. The income testsvary.Insome,youcan“spenddown”excessincome over the limit to become eligible. In others, if countableincomeexceedsthebenefit“cap”(likeSSI),youcannotbecomeeligibleatall.

Some states also attempt to limit expenditures from self-settled(andeventhird-party)specialneedstrusts, and can require amendments to the language of thosetrustsinordertoalloweligibility.Whileagoodargument can be made that the Medicaid program does nothavethatability,asapracticalmatter,thetrusteeof the special needs trust will have to either litigate thatissueoracquiesceintheMedicaidagency’sdemands.

Assets

ThelimitationonassetsforSSIeligibilitymaybesomewhat easier to master, or at least to describe. A single person must have no more than $2,000 in availableresourcesinordertoqualifyforSSI.Sometypesofassetsarenotcountedasavailable(called“non-countable”),includingthebeneficiary’shome,one automobile, household furnishings, prepaid burial amounts plus up to $1500 set aside for funeral expenses(orlifeinsuranceinthatamount),toolsofthebeneficiary’strade,andahandfulofother,lessimportant items. Each of these categories of assets is subjecttospecialrulesandexceptions,soitiseasytobecometangledintheasseteligibilitystructure.

Deeming

The SSI program considers portions of the income and assets of non-disabled, ineligible parents of minor disabled children and of an ineligible spouse living with the SSI recipient as available, and countable for eligibilitypurposes.Thisiscalled“deeming”.Acertainportion of the ineligible person’s income and assets isconsideredasnecessaryforhisorherownlivingexpenses, and therefore is excluded.

As soon as a child reaches age 18, parental deeming no longer occurs, even if the child continues to live in the household.Ifspousesvoluntarilyseparateandliveindifferenthouseholds,thendeemingfromtheseparatespouse or parent also ends. However, in both instances, if the separate person continues to provide support or maintenance to the SSI eligible individual, it will still count as income as described above unless a Court orders ittobedepositeddirectlyintothetrust.Thereisalsoalimitedexceptiontoallparentaldeemingforaseverelydisabled minor child returning home from an institution orwhoseconditionwouldotherwisequalifythemforinstitutionalization, which is called a waiver.

“I Want to Buy a...” or “I Want to Pay for...”

What do these complicated rules mean for expenditures from a special needs trust? In-kind purchases, meaning purchaseofgoodsorservicesforthebenefitofthebeneficiary,onlypotentiallyaffecttheSSIbenefitamount,andnotMedicaidbenefits,althoughtheMedicaidagencymayrestrictexpendituresforapprovedthings.Thereareanumberofspecificpurchasesthatfrequentlyrecur:

Home, Upkeep and Utilities

Keep in mind that SSI’s in-kind support and maintenance (ISM)rulesdealspecificallywithpaymentsfor“foodandshelter.”TheSocialSecurityAdministrationincludesonlytheseitemsasfoodandshelter:

1. Food

2.Mortgage(includingpropertyinsurancerequiredbythemortgageholder)

3.Realpropertytaxes(lessanytaxrebate/credit)

4. Rent

5. Heating fuel

6. Gas

7.Electricity

8. Water

9.Sewer

10. Garbage removal

The rules make special note of the fact that condominium assessmentsmayinsomecasesbeatleastpartialpaymentsforwater,sewer,garbageremovalandthelike.

Inotherwords,apaymentforrentwillimplicatetheISMrules,aswillmonthlymortgagepayments.Theoutright purchase of a home, whether in the name of the beneficiaryorthetrust,willnotcauselossofSSI(althoughitmayreducethebeneficiary’sSSIbenefitforthesinglemonthinwhichthehomeispurchased).Thisbringsup

continued from page 9

11

another consideration. Purchase of a home in the trust’s namewillsubjectittoaMedicaid“payback”requirementonthedeathofthebeneficiary,whereaspurchaseinthenameofthebeneficiarymayallowotherplanningthatwillavoidthehomebecomingpartofthepayback.Thiscomplicatedinterplayoftrustrules,ISMdefinition,estate-recoveryrules,andhomeownershipmakesthisareaofspecialneedstrustadministrationparticularlyfraughtwithdifficulty.

However,theMedicaidstateagency’streatmentofdistributionsfromspecialneedstrustsmaydifferfromtheSocialSecurityinterpretation—especiallywhenthebeneficiaryofaself-settledtrustiseligibleforMedicaidbenefits.Forexample,contrarytoputtingthehouseintheindividual’sname,astatemayrequirethatanypurchaseofahomebysuchatrustwouldresultintitlebeingheldinthetrust’sname,therebyensuringthatthestate will at least receive the proceeds from the sale of theresidenceuponthedeathofthebeneficiary.

Clothing Until March 7, 2005, purchase of clothingbyatrustwasconsideredasISM for SSI, similar to shelter and food. Since then, a clothing purchase for the beneficiarywillnotaffectthebenefitamountoreligibility,whethertheclothing in question is special garments relatedtothedisabilityorjustordinarystreet clothes and shoes. Not all state Medicaidregulationsreflectthischange.

Phone, Cable, and Internet Services Other than those utilities listed above, there is no federal limitationonutilitypayments.Inotherwords,thetrustcanpayforcable,telephone,high-speedinternetconnection, newspaper, and other “utilities” not on the list.

Vehicle, Insurance, Maintenance, Gas Purchaseofavehicleandmaintenance(includinggasandinsurance)ispermittedunderfederallaw.Notethatthereisamechanicaldifficultyinprovidinggasolinewithoutproviding cash that could be converted to food or shelter. One technique which has worked well has been to arrange forthebeneficiarytohaveagas-companycreditcard.Becauseeligibilityforsuchcardsiseasiertomeet,andbecause the cards cannot be used to purchase groceries, administration of the credit account is easier to set up andmonitor,andthecardcanthenbebilleddirectlytothe trust.

Some state Medicaid agencies put limitations on the value,type,andtitleownershipofvehicles,suchasonlyallowing a vehicle valued at up to $5,000, handicapped-equipped,orrequiringalieninfavorofthepaybacktrustonthetitle.TheSSIprogramdoesnotspecificallyrequireor monitor such limitations.

Pre-paid Burial/Funeral Arrangements

Nothing in federal law prohibits or restricts use of special needs trust funds for purchase of burial and funeral arrangementsduringthebeneficiary’slifetime—excepttotheextentthatthebeneficiaryhasaccesstothefundsusedtopayforthearrangements,andtherebysubjecttotheassetlimitationsaffectingSSIrecipients.StateMedicaidagenciesmaylimitthevalueoftheburialcontract. It is important to ask for an “irrevocable, pre-paid” funeral plan.

Tuition, Books, Tutoring

No limit under either federal or state law. This is an excellent use of special needs trust funds.

Travel and Entertainment

Onceagain,nolimitexceptthattheremaybesomeconcernaboutpaymentforhotels.Whenthebeneficiary

still maintains a residence at home, thehotelstayandrestaurantmaybe considered “shelter” and “food” expenses.Somestatesmayimposelimitations on companion travel not found in federal law. These might include not allowing recipients to havethespecialneedstrustpayformore than one traveling companion, thecompanionmustbenecessarytoprovidecare,andthecompanionmaynot be a person obligated to support

thebeneficiarysuchasaminorbeneficiary’sparent.Notethatforeigntravelcanhavetwootheradverseeffects:(1)airlineticketstoforeigndestinations,ifrefundable,will be treated as being convertible into food and shelter, and(2)ifanSSIrecipientisoutofthecountryformorethanamonth,heorshemayloseeligibilityuntilreturn.For those reasons, foreign travel, unlike domestic travel, usuallymustbelimitedintime.

Household Furnishings and Furniture

The trust can be used to purchase appliances, furniture, fixturesandthelike.BeforeMarch2005,therewasatheoretical concern in the SSI program that the value of householdfurnishingsmightexceedanarbitrarylimitandaffectthebeneficiary’seligibility;thatvaluelimithasnow been removed.

Television, Computers and Electronics

Thereisnospecificlimitationonpurchaseofhouseholdtelevisions or other electronic devices, although under SSIrulestheindividualisonlyallowedtoown“ordinaryhousehold goods” that are not kept for collectible value and are used on a regular basis. The trust can also provideacomputerforthebeneficiary,plussoftwareandupgrades.

continued on page 12

As soon as a child reaches age 18, parental deeming

no longer occurs even if the child continues to live in

the household.

12

Durable Medical Equipment

Thereisnofederallimitationonanymedicalrelatedequipment,butindividualstatesmaylimitpurchaseofsomeequipmentasnotbeing“necessary.”Problemareascould be if the equipment could also be considered as recreational, such as a heated swimming pool needed for arthritic or other joint conditions.

Care Management

Nofederallimitation,butmanystatesattempttolimitpaymentsforcareormanagementifmadetoafamilymemberorotherrelative,especiallyifthereisanobligationofsupport(e.g.,parentsofminorchildren).

Therapy, Medications, Alternative Treatments

Same principle as durable medical equipment, above, so long as the state does not regulate the treatment, there is no federal limitation.

Taxes

Nofederallimitation,butstatesmayattempt to direct trust language on what taxes can be paid for, such as taxes incurred as a result of trust assets oratthedeathofthebeneficiary.SinceitisdifficulttoimagineanSSIorMedicaidbeneficiaryhavingsignificantnon-trust income, it is hard to see how this limitation is so much troublesome as it is quarrelsome.

Legal, Guardianship and Trustee Fees

At least some states allow legal, guardianship, and trustee fees to be paid from the trust, although some federallawindicatesthatpaymentofguardian’sfeesorguardian’sattorneyfeesmayreallybenefittheguardianandnotthebeneficiary.Paymentsfortrustadministrationexpenses,includingthetrust’sattorney’sfees,areclearlypermissible under both federal and state law, and are rarelylimitedbeyondreasonablenessstandards.

Loans, Credit, Debit and Gift Cards

Receipt of a “loan” will not count as income for the SSI or Medicaid programs, which means that a trust can make a loanofcashdirectlytoabeneficiary.Therearerulesthatmust be followed for loans to be valid and non-countable. There must be an enforceable agreement at the time that the loan is made that the loan will be paid back at some point,whichusuallymeansthatitshouldbeinwriting.Theagreementtopaybackcannotbebasedonafuture

contingencysuchas,“IonlyhavetopayitbackifIwinthelottery...”Finally,theloanmustbeconsideredas “feasible,” meaning that there is a reasonable expectationthatthebeneficiarywillhavethemeansatsomepointtopaybacktheloan.

If a loan is forgiven, then it would count as income at thattime.Also,ifthebeneficiarystillhastheloanedamount in the following month, it will then count as a resource. However, school loans are not countable as income or as a resource so long as the funds are spent for tuition, room and board, and other education-related expenses within nine months of receipt.

Since goods or services purchased with a credit card are actuallya“loan”thatmustbepaidbacktothecreditcardcompany,theyarealsonotconsideredasincometothebeneficiaryattimeofpurchase.Aslongasthebeneficiarydoesn’tsellthegoodsforcash,thereisalsotheaddedadvantagethatthetrustcanpaybackthecreditcardcompanywithoutthepaymentcountingasincome, except for purchases that are considered as food or shelter. Food and shelter related purchases use thesameISMcountableincomerules(andparticularly

thecountableincomelimits)described above.

Useofadebitcardbyabeneficiarywhen purchases are made for paymentthroughatrust-fundedbank account is income to the beneficiaryfortheamountaccessed.The total amount in the account available to be accessed could possiblybeacountableresource.Isagiftcardpurchasedbyatrustandprovidedtoabeneficiaryconsideredto be a distribution of income, a lineofcredittoavendor(similartoacreditcard),orjustaccessforin-kind purchase of goods or services onbehalfofabeneficiarybythe

trust?SSIrulesarenotyetclearonthispoint,anditisprobablethatdifferentSocialSecurityandMedicaidofficeswilltreattheuseofdebitandgiftcardsdifferentlyuntilpreciseguidelinesareprovidedbytheagencies.Thesafeapproachistousetheminaverylimitedway;iftheyaretobeusedatall,keepreceiptsfor all special needs items, and be prepared for adverse treatment.

Trust Administration and Accounting

Actual administration of a special needs trust is in mostrespectssimilartoadministrationofanyothertrust. A trustee has a general obligation to account to beneficiariesandotherinterestedparties.Taxreturnsmayneedtobefiled(thoughnotalways),andtaxfilingrequirements will be based on the tax rules, not special needstrustrules.Somespecialneedstrusts,butbyno means all, will be subject to court supervision and control.

continued from page 11

It is generally beneficial for a self-settled special needs trust to be a grantor trust. This is true because the tax rates for non-grantor trusts are tightly compressed, and

the highest marginal tax rate on income is reached

very quickly for trusts.

13

Trustee’s Duties

As with general trust law requirements, the trustee of a special needs trust has an obligation not to self-deal, nottodelegatethetrustee’sdutiesimpermissibly,nottofavoreitherincomeorremainderbeneficiariesoveroneanother,andtoinvesttrustassetsprudently.Theobligations of a trustee are well-discussed in several centuries of legal precedent, and cannot be taken lightly.Legalcounsel(andprofessionalinvestment,taxandaccountingassistance)willberequiredinadministrationofalmosteveryspecialneedstrust.

Afewcardinaltrustrulesbearspecialmention:

NO SELF-DEALING

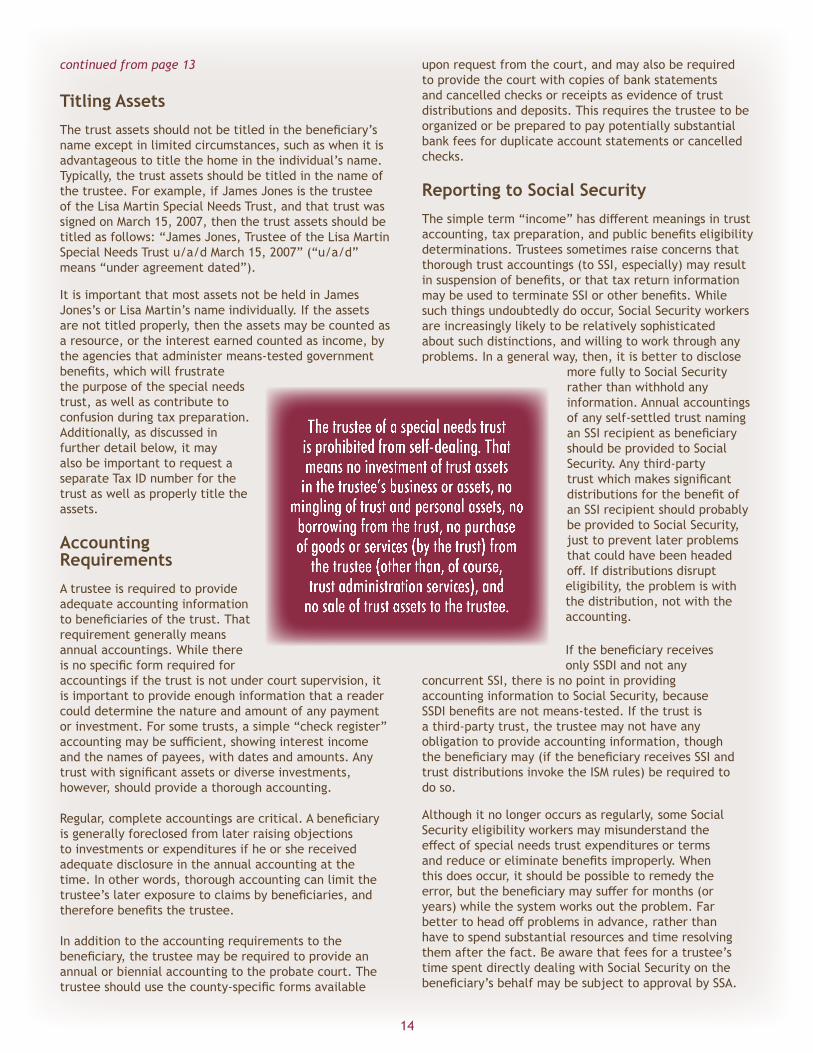

As with other trusts, the trustee of a special needs trust is prohibited from self-dealing. That means no investment of trust assets in the trustee’s business or assets, no mingling of trust and personal assets, no borrowing from the trust, no purchase of goods or services(bythetrust)fromthetrustee(otherthan,ofcourse, trust administration services),andnosaleoftrustassets to the trustee. The samestricturesalsoapplyto the trustee’s immediate familymembers,andtheexistenceofanappraisal,orthe favorable terms of a transaction, do not change these rules.

IMPARTIALITY

Becausethetrusthasbothan“income”beneficiary(thepersonwithdisabilities)anda“remainder”beneficiary(thestate,inthecaseofaMedicaidpaybacktrust,or the individuals who will receive assets when the incomebeneficiarydies),thetrusteehasanecessarilydividedloyalty.Itisimportanttoremainimpartialasbetweenthetrust’sbeneficiaries.Thus,investmentinassetsexclusivelydesignedtomaximizeincomeattheexpenseofgrowth,orviceversa,mayviolatethetrustee’sdutytothenegativelyaffectedclassofbeneficiaries.Notethatatrustmay,byitsterms,make clear that the interests of one or the other class ofbeneficiariesshouldbeparamount—thoughsuchlanguagewillprobablyearnthedisapprovaloftheMedicaidagencyinanyself-settledtrustwhichmustbesubmitted to Medicaid for approval.

DELEGATION

Generallyspeaking,atrusteemaydelegatefunctionsbutmaynotavoidliabilitybydoingso.Inotherwords,whilethetrusteemayhireinvestmentadvisers,taxpreparers and the like, he or she will remain liable for anyfailuresbysuchprofessionals.

Somestatesdolimitthetrustee’sliability.Forexample,in states which have adopted the Uniform Prudent Investor Act,delegatinginvestmentauthoritypursuanttotheActwilllimitthetrustee’sliabilitysothatheorshewillonlyberequiredtocarefullyselectandmonitortheinvestmentadviser.

INVESTMENT AnytrusteeshouldbefamiliarwiththeprinciplesofModernPortfolioTheory,withitsemphasisonrisktoleranceandassetdiversification.Atrusteewhoholdshimself,herself,or itself out as having special expertise in investments or asset management will be held to a higher standard, but anytrusteewillberequiredtounderstandandimplementprudent investment practices. Some courts will institute an investmentpolicythatrequiresapercentageofassetstobeheldinfixedincomeinvestmentsandtheremainderinsecurities(e.g.,a60/40splitiscommon).

Bond Atrustee,especiallyonewho administers a special needstrustsupervisedbyaprobatecourt,mayneedtobebonded.Bondisatypeof insurance arrangement wherebythetrusteepaysapremium in order to guarantee that the trustee manages the trust and carries out his

orherfiduciarydutiescorrectly.Thebondpremiumisanacceptable expense of the trust, and need not come out of the trustee’s own pocket. If the trustee fails to exercise hisorherfiduciarydutyandthetrustlosesmoneyasaresult,theinsurancecompanythatissuedthebondwillcompensate the trust and take action to collect from the trustee.

The bond premium depends on multiple factors, including thecredithistoryofthetrusteeandthevalueofthetrust.Most corporate trustees are exempt from posting bond. Individualtrusteesmust“postbond”;thatis,providewritten documentation to the probate court that the individualisbonded.Thebondistypicallyissuedforasetperiodoftime,forexampleoneyear,andattheexpirationofthetimeperiod,thetrusteemustpayanadditionalpremium or show the bond issuer that bond is no longer requiredbytheprobatecourt.

It is possible in most states, at least when the trust is supervisedbyacourt,toaskthecourtforpermissiontodeposit the assets in a restricted or “blocked” account withafinancialinstitutionratherthanpostingbond.Whilethiscircumventstheissueofbeingbonded,thefinancialinstitutionshouldrequireacertifiedcopyofthecourt’sorder authorizing the expenditure of funds prior to making a distribution from the special needs trust. This can result infrequentin-persontripstothebankbythetrustee,althoughitavoidsthesometimescostlybondpremium.

continued on page 14

A trustee has a general obligation to account to beneficiaries and other interested parties. Tax

returns may need to be filed (though not always), and tax filing requirements will be based on the

tax rules, not special needs trust rules.

14

Titling Assets

Thetrustassetsshouldnotbetitledinthebeneficiary’sname except in limited circumstances, such as when it is advantageous to title the home in the individual’s name. Typically,thetrustassetsshouldbetitledinthenameofthetrustee.Forexample,ifJamesJonesisthetrusteeof the Lisa Martin Special Needs Trust, and that trust was signed on March 15, 2007, then the trust assets should be titledasfollows:“JamesJones,TrusteeoftheLisaMartinSpecialNeedsTrustu/a/dMarch15,2007”(“u/a/d”means“underagreementdated”).

ItisimportantthatmostassetsnotbeheldinJamesJones’sorLisaMartin’snameindividually.Iftheassetsarenottitledproperly,thentheassetsmaybecountedasaresource,ortheinterestearnedcountedasincome,bythe agencies that administer means-tested government benefits,whichwillfrustratethe purpose of the special needs trust, as well as contribute to confusion during tax preparation. Additionally,asdiscussedinfurtherdetailbelow,itmayalso be important to request a separate Tax ID number for the trustaswellasproperlytitletheassets.

Accounting Requirements

A trustee is required to provide adequate accounting information tobeneficiariesofthetrust.Thatrequirementgenerallymeansannual accountings. While there isnospecificformrequiredforaccountings if the trust is not under court supervision, it is important to provide enough information that a reader coulddeterminethenatureandamountofanypaymentor investment. For some trusts, a simple “check register” accountingmaybesufficient,showinginterestincomeandthenamesofpayees,withdatesandamounts.Anytrustwithsignificantassetsordiverseinvestments,however, should provide a thorough accounting.

Regular,completeaccountingsarecritical.Abeneficiaryisgenerallyforeclosedfromlaterraisingobjectionsto investments or expenditures if he or she received adequate disclosure in the annual accounting at the time. In other words, thorough accounting can limit the trustee’slaterexposuretoclaimsbybeneficiaries,andthereforebenefitsthetrustee.

In addition to the accounting requirements to the beneficiary,thetrusteemayberequiredtoprovideanannual or biennial accounting to the probate court. The trusteeshouldusethecounty-specificformsavailable

uponrequestfromthecourt,andmayalsoberequiredto provide the court with copies of bank statements and cancelled checks or receipts as evidence of trust distributions and deposits. This requires the trustee to be organizedorbepreparedtopaypotentiallysubstantialbank fees for duplicate account statements or cancelled checks.

Reporting to Social Security

Thesimpleterm“income”hasdifferentmeaningsintrustaccounting,taxpreparation,andpublicbenefitseligibilitydeterminations. Trustees sometimes raise concerns that thoroughtrustaccountings(toSSI,especially)mayresultinsuspensionofbenefits,orthattaxreturninformationmaybeusedtoterminateSSIorotherbenefits.Whilesuchthingsundoubtedlydooccur,SocialSecurityworkersareincreasinglylikelytoberelativelysophisticatedaboutsuchdistinctions,andwillingtoworkthroughanyproblems.Inageneralway,then,itisbettertodisclose

morefullytoSocialSecurityratherthanwithholdanyinformation. Annual accountings ofanyself-settledtrustnaminganSSIrecipientasbeneficiaryshould be provided to Social Security.Anythird-partytrustwhichmakessignificantdistributionsforthebenefitofanSSIrecipientshouldprobablybeprovidedtoSocialSecurity,just to prevent later problems that could have been headed off.Ifdistributionsdisrupteligibility,theproblemiswiththe distribution, not with the accounting.

IfthebeneficiaryreceivesonlySSDIandnotany

concurrent SSI, there is no point in providing accountinginformationtoSocialSecurity,becauseSSDIbenefitsarenotmeans-tested.Ifthetrustisathird-partytrust,thetrusteemaynothaveanyobligation to provide accounting information, though thebeneficiarymay(ifthebeneficiaryreceivesSSIandtrustdistributionsinvoketheISMrules)berequiredtodo so.

Althoughitnolongeroccursasregularly,someSocialSecurityeligibilityworkersmaymisunderstandtheeffectofspecialneedstrustexpendituresortermsandreduceoreliminatebenefitsimproperly.Whenthisdoesoccur,itshouldbepossibletoremedytheerror,butthebeneficiarymaysufferformonths(oryears)whilethesystemworksouttheproblem.Farbettertoheadoffproblemsinadvance,ratherthanhave to spend substantial resources and time resolving them after the fact. Be aware that fees for a trustee’s timespentdirectlydealingwithSocialSecurityonthebeneficiary’sbehalfmaybesubjecttoapprovalbySSA.

continued from page 13

The trustee of a special needs trust is prohibited from self-dealing. That means no investment of trust assets

in the trustee’s business or assets, no mingling of trust and personal assets, no

borrowing from the trust, no purchase of goods or services (by the trust) from

the trustee (other than, of course, trust administration services), and

no sale of trust assets to the trustee.

15

Reporting to Medicaid

IfthebeneficiaryresidesinastatewherethereceiptofSSIresultsinthebeneficiaryalsobeingautomaticallyenrolled in Medicaid, then no separate accounting requirementneedbemadetotheMedicaidagency.However, if the individual is in a state where SSI and Medicaidarenotinterrelated,thenitmaybenecessarytoaccounttobothagencies.TheMedicaidconsumer(ortheirguardian)isrequiredtonotifyMedicaidofachangeinresourcesorincomewithinasetperiodoftime,usuallyasshortastendays.ThisincludessituationswheretheMedicaid consumer receives an inheritance or settlement andimmediatelytransfersthefundstoaspecialneedstrust.

Thetrusteeofathird-partyspecialneedstrustmaynothavethesamedutytoaccount,butmaychoosetoprovide accounting information to Medicaid rather than risklaterdisqualificationofthebeneficiary,eventhoughMedicaid’spowertoconsidertrustexpendituresmaybesubject to challenge.

Reporting to the Court Manyself-settledspecialneedstrustswillbetreatedinessentiallythesamefashionasaconservatorshiporguardianshipoftheestate.Thisissobecause,typically,thecourtwasinitiallyaskedtoauthorizeestablishmentofthetrust.Mostcourtsexpectanytrustestablishedbythe court to remain under court supervision, including bonding,seekingauthoritytoexpendfunds,andfilingperiodic accountings.

Even if the trust does not require court accounting, some consideration should be given to seeking court involvement. One great advantage of court supervision ofthetrustisthateachyear’saccountingisthenfinalastoallitemsdescribedinthataccounting(provided,of course, that the appropriate notice has been given tobeneficiarieswhomightotherwisecomplainaboutthe trust’s administration and other court procedural requirementsarefollowed).

TheCourtmayalsohaveasetfeeschedulethatgovernsthe amount the trustee can be compensated for providing trust administration services.

Modification of Trust

As explained above, a special needs trust must be irrevocable in order for the trust to be considered an exempt resource. However, that does not preclude the trust itself from permitting the trustee to amend ormodifythetrustinlimitedways,particularlyasitrelatestoprogrameligibilityforthebeneficiary.Thisisparticularlyimportantsincewecannotpredictfuturechangestothelawsgoverningmeans-testedbenefits.Thecourtsmayalsobewillingtomodifyorterminateatrustwhosepurposehasbeenfrustratedbylawchangesor other factors, such as the trust assets being valued at a nominal amount.

Wrapping up the Trust

If the special needs trust is a self-settled trust with a provisionrequiringrepaymentofMedicaidexpenses,itwillobviouslybenecessarytodeterminethe“payback”amountuponthedeathofthebeneficiaryorterminationof the trust. Because Medicaid’s historical experience withthesetrustsisstillslight,stateagenciesmayhavedifficultyprovidingareliableandfinalfigure.Theprudent trustee will request a written statement of the amount due, including evidence showing how it was calculatedandastatementofauthoritytomakethefinaldetermination.Onceanypaybackissueshavebeenaddressed(andrememberthatmostthird-partyspecialneedstrustswillhavenorequirementofrepaymenttothestate),thenterminationofthetrustwillfollowtheusualrequirementsoftaxpreparationandfiling,finalaccountinganddistributionaccordingtothetrustinstrument.Remember,becauseSocialSecurityrequiresthat Medicaid reimbursement and certain tax liabilities mustbesquaredawaybeforethetrusteemayevenpayforthebeneficiary’sfuneral,purchaseduringthebeneficiary’slifetimeofanirrevocablepre-paidfuneraliscritical.

Income Taxation of Special Needs Trusts

Specialneedstrusts,likeothertypesoftrusts,cancomplicateincometaxpreparation.Thefirstquestiontobeaddressediswhether—forincometaxpurposes–thetrustisa“grantor”trustornot.Taxrulesdefining“grantor” trusts are neither simple nor intuitive, but fortunatelytherearesomeeasyrulesofthumbtoapply,andtheywillworkformostspecialneedstrusts.

“Grantor” Trusts

A “grantor” trust is treated for tax purposes as a transparententity.Inotherwords,thegrantorofa“grantor” trust is treated as having received the income directly,eventhoughtheaccountsaretitledtothetrustand all income shows up in the name of the trust.

Generallyspeaking,aself-settledspecialneedstrustwillbeagrantortrustifafamilymemberisthetrustee.Ifthetrustnamesanindependenttrusteeitmaystillbeagrantortrustifoneofseveralspecificprovisionsexistsinthetrust.Aqualifiedaccountantorlawyershouldbeableto tell whether a given trust is a grantor trust at a glance. Ifitis,itremainsagrantortrustforitsentirelife—oratleastuntilthedeathofthegrantor(whenthetrustmayeither terminate or convert into a non-grantor trust as to itsnewbeneficiaries).Untilthetrusthasbeenreviewedbyanexpert,assumethatitisprobablyagrantortrust.

Itisgenerallybeneficialforaself-settledspecialneedstrust to be a grantor trust. This is true because the tax ratesfornon-grantortrustsaretightlycompressed,andthehighestmarginaltaxrateonincomeisreachedveryquicklyfortrusts.Thepracticaldifferencewillbesmall

continued on page 16

16

ifthetrustactuallymakesdistributionsforthebenefitofthebeneficiaryinexcessofitsannualtaxableincome,but the proper tax reporting approach should still be followed.

TAX ID NUMBERS

Agrantortrustmay,butneednot,obtainanEmployerIdentificationNumber(anEIN).Someattorneysandaccountants choose to secure an EIN in each case, while othersresistdoingso—eitherapproachisdefensible.Althoughbanks,brokeragehousesandotherfinancialinstitutionsmayinsistthatthetrustrequiresitsownEIN,theyaresimplywrong.ThereiswidespreadconfusionaboutthenecessityforanEINforirrevocabletrusts,butaconfidentandwell-informedtrustee,attorneyoraccountantshouldbeabletoconvincethefinancialinstitution that no separate EIN is required. Instead, the trusteecansimplyprovidethefinancialinstitutionwiththegrantor’sSocialSecuritynumber.

FILING TAX RETURNS

Agrantortrustordinarilywillnotfileaseparatetaxreturn.IfagrantortrusthasbeenassignedanEIN,itmayfilean“informational”return.Thereturncanincludea paragraph indicating that the trust is a grantor trust, thatallincomeisbeingreportedonthebeneficiary’sindividual return, and that no substantive information will beincludedinthefiduciaryincometaxreturn.Actually,completingthefiduciaryincometaxreturnisnotanoption for a grantor trust, although again there is much confusion on this point, even among some professionals.

Non-Grantor Trusts

Virtuallyallthird-party,andsomeself-settled,specialneeds trusts will be non-grantor trusts. Because income willnotbetreatedashavingbeenearnedbythebeneficiary,afiduciaryincometaxreturn(IRSform1041)will be required.

TAX ID NUMBERS

Anon-grantortrustwillneedtoobtainitsownEINbyfilingafederalformSS-4.Nearlyallthird-partyspecialneedstrustswillbe“complex”trusts—thisdesignationsimplymeansthatthetrustisnotrequiredtodistributeallitsincometotheincomebeneficiaryeachyear.Although the trust will be listed as “complex” on the SS-4,itmayinfactalternatebetween“complex”and“simple”oneachyear’s1041.

FILING TAX RETURNS

Thenon-grantortrustmustfilea1041eachyear.Alldistributionsforthebenefitofthebeneficiaryareconclusivelypresumedtobeofincomefirst,soanytrustexpenditures in excess of deductions will result in a Form

K-1showingincomeimputedtothebeneficiary.Thisshouldnotcauseparticularconcern,sinceSocialSecurity(andevenMedicaid)eligibilityworkersareincreasinglylikelytounderstandthat“income”fortaxpurposesisdifferentfrom“income”forpublicbenefitseligibilitypurposes.Anytaxliabilityincurredbytheindividualbeneficiaryasaresultofthisimputationcanbepaidbythetrust,thoughthetrusteemaynothavetheauthorityto prepare and sign the individual’s tax return.

Administrative and other deductible expenses on an individualtaxreturnmustreach2%ofthetaxpayer’sincome before being deducted at all. The same is not trueofatrusttaxreturn,leadingtoamodestbenefitto treatment as a non-grantor trust in some cases. This benefitmaynotoffsetthecompressedincometaxrateslevied against non-grantor trusts, but each case will be different.Thedifficultyindeterminingtheproper—andthebest—incometaxtreatmentismadeworsewhenoneaddstheconfusingoptionoftreatmentasa“QualifiedDisabilityTrust.”

Qualified Disability Trust

Beginning in 2002, Congress allowed some non-grantor special needs trusts to receive a modest income tax benefit.TrustsqualifyingunderInternalRevenueCodeSection642(b)(2)(C)receiveaspecialbenefit—theyarepermitted to claim a personal exemption on their federal incometaxes.Intaxyear2017,forexample,thepersonalexemption will be $4,050, which means that income up tothatamountwillnotgenerateanytaxliabilityatall.In fact, once the trust uses its exemption and calculates theremainingtaxableincome,itisusuallypassedthroughtothebeneficiary—whogetstoclaimanother$4,050personal exemption.

Coupledwiththegreaterflexibilityavailabletonon-grantor trusts in deducting administrative expenses, QualifiedDisabilityTrusttreatmentmaybeadvantageousinsomecases.Typically,theQualifiedDisabilityTrustelection will be attractive when there is a fair amount ofincomeontrustassets,andrelativelyfewmedicalorotherexpensesincurredonbehalfofthebeneficiary.CarefulreviewwithaqualifiedincometaxprofessionalisusuallynecessarytodeterminewhethertopursueQualifiedDisabilityTrusttreatment.

Seeking Professional Tax Advice

It should be apparent from this brief discussion of taxation of special needs trusts that professional tax preparation and advice are essential. Although most accountantsarequalifiedtopreparefiduciary(trust)income tax returns, most do not have much experience in thefield.Afirstquestiontoaskaprospectiveaccountantmightbe“Howmany1041sdoyoutypicallyprepareinayear?”Followthatwith“CouldyoupleaseexplaintheconceptofQualifiedDisabilityTruststome?”andyouwillquicklylocateanytrulyproficientpractitioner.Youprobablywillnotwanttoautomaticallyrejectan

continued from page 15

17

accountantwhocannottellyouaboutQualifiedDisabilityTrustsimmediately,unlessyouarepreparedtodealwithanaccountantinanothercity—therearesimplynotverymanyaccountantsortaxpreparerswhohaveeverhadoccasiontoclaimthatstatusonanyfiduciaryincometaxreturn.Asalways,youcangetsomeassistanceincomplicatedspecialneedstrustissuesfromtheattorneywhopreparedthedocument,ortheattorneywhoadvisesyouastrustee.MembersoftheSpecialNeedsAlliance® areusuallyamongtheveryfewwhoarefamiliarwiththeseconcepts,andyourattorneymayhaveworkedwithanaccountantinyourareawhoisfamiliarwiththespecial tax treatment of these trusts.

For Further Reading

There are a handful of books and articles, and a growing number of websites, available to aid trustees of special needs trusts. Among our favorites:

SpecialNeedsTrustAdministrationManual:AGuideforTrustees,byJackins,Blank,MacyandShulman—thisguideisamongthebestavailable.ItwaswrittenbyfourMassachusettslawyers,andisfranklyfocusedonMassachusettslawandpractice.Muchofwhattheauthorshavetosay,however,isapplicabletospecialneedstrustsineverystate.

SpecialPeople,SpecialPlanning:CreatingaSafeLegalHavenforFamilieswithSpecialNeeds,byHoytandPollock—providessomegeneraladviceand direction, but is more conversational than detailed. This volume also tends to focus on the “why”morethanthe“how”,whichisanimportantmessage but not as useful to someone who is alreadyadministeringaspecialneedstrust.

SpecialNeedsTrusts:ProtectYourChild’sFinancialFuture,byElias—thisrecentadditiontotheliterature comes from Nolo Press, an organization thatmanylawyersfindannoyingatbest.Wedisagree. This is a plain-language, straightforward explanationofspecialneedstrustsfromalawyerwhodoesn’tevenpracticeinthearea(hispreviousbooks for Nolo Press include explanations of bankruptcy,trademarkandotherareasoflaw).

Phone:520.546.1005Fax:520-546-5119

SNATollFreeNumber:1.877.572.8472

w w w . s p e c i a l n e e d s a l l i a n c e . o r g