a closer look by brian hays and kris kesling –hays lic real estate broker lic mortgage lic...

TRANSCRIPT

ACloser Look

By Brian Hays and Kris Kesling –HaysLic Real Estate Broker Lic Mortgage Lic Mortgage Originator Originator

Talking points Who are Brian & Kris Hays?

Brian is a licensed Real Estate Broker and a licensed Mortgage Originator. He has a B.S. degree in Finance from USF.

Kris is a licensed Mortgage Originator and has a B.A. degree in Economics from Rutgers.

They will show you how all of the jargon you are learning from Dr. Schmidt is actually applied in the real world!

What a Realtor Does:

For Buyers – 1. Confirm Property Value; Find right property for wants and needs2. Guide buyer through purchase process and lending process3. Assist in validating condition of property

For Sellers – 1. Market the property through various channels2. Guide seller through sale and lending process3. Ensure legal compliance

www.Prefhomes.net

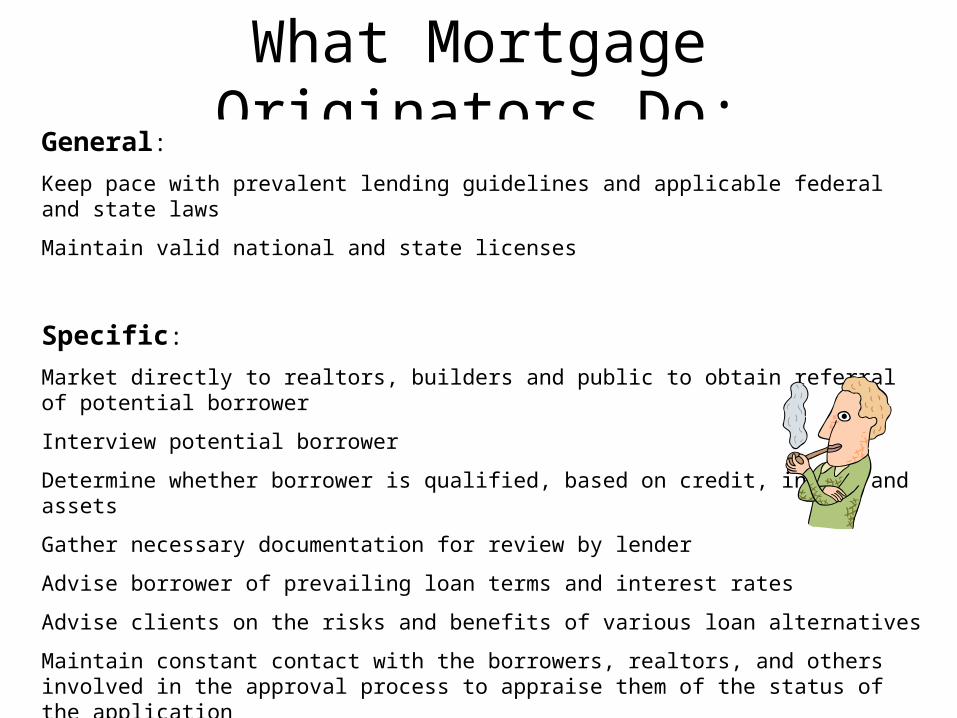

What Mortgage Originators Do:General:

Keep pace with prevalent lending guidelines and applicable federal and state laws

Maintain valid national and state licenses

Specific:

Market directly to realtors, builders and public to obtain referral of potential borrower

Interview potential borrower

Determine whether borrower is qualified, based on credit, income and assets

Gather necessary documentation for review by lender

Advise borrower of prevailing loan terms and interest rates

Advise clients on the risks and benefits of various loan alternatives

Maintain constant contact with the borrowers, realtors, and others involved in the approval process to appraise them of the status of the application

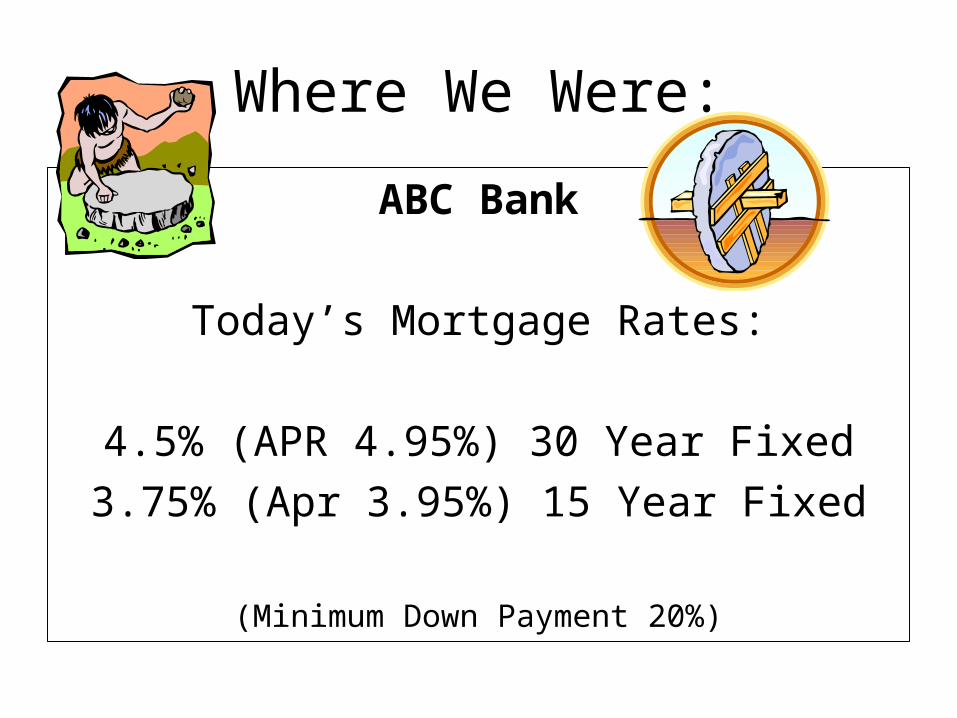

Where We Were:

ABC Bank

Today’s Mortgage Rates:

4.5% (APR 4.95%) 30 Year Fixed

3.75% (Apr 3.95%) 15 Year Fixed

(Minimum Down Payment 20%)

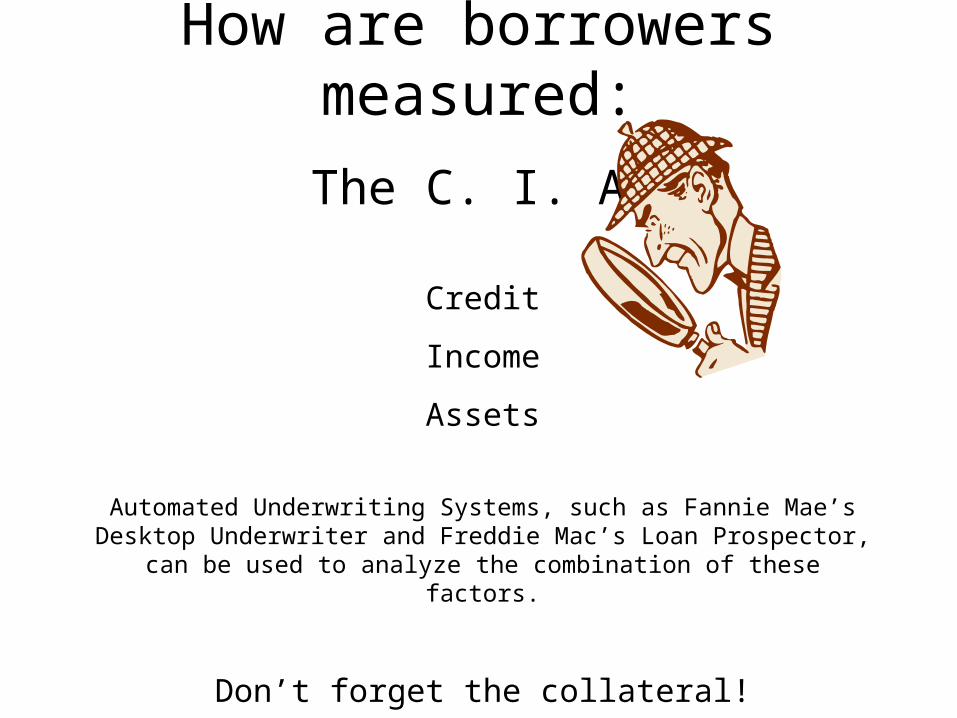

How are borrowers measured:

The C. I. A.

Credit

Income

Assets

Automated Underwriting Systems, such as Fannie Mae’s Desktop Underwriter and Freddie Mac’s Loan Prospector, can be used to analyze

the combination of these factors.

Don’t forget the collateral!

FHA Originations more common now than GSEs

People Needed Lower Down Payments!

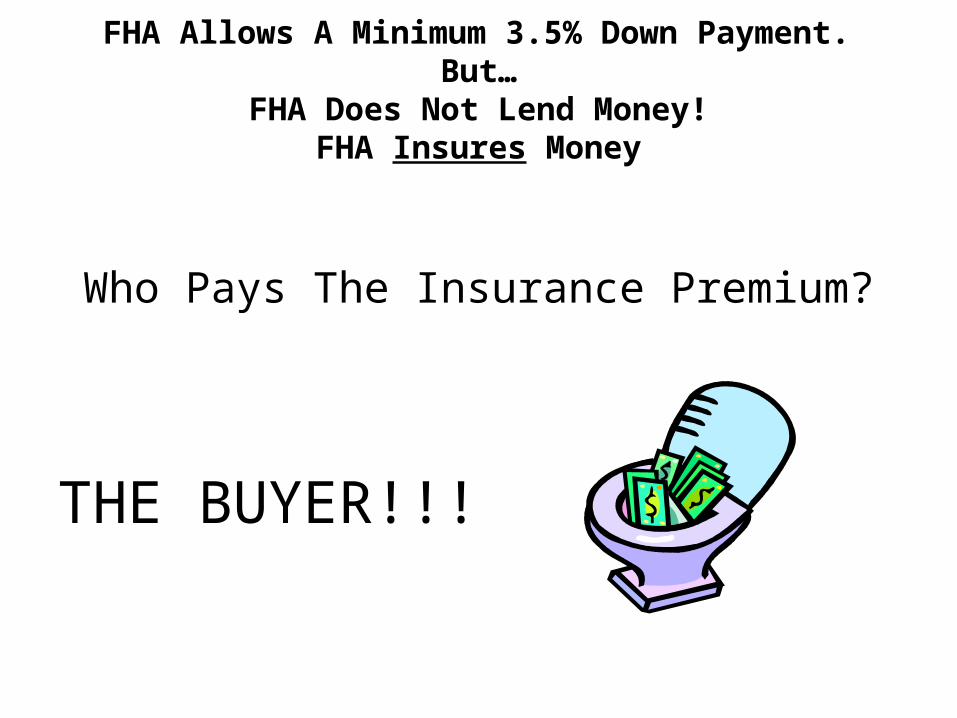

FHA Allows A Minimum 3.5% Down Payment. But…FHA Does Not Lend Money!

FHA Insures Money

Who Pays The Insurance Premium?

THE BUYER!!!

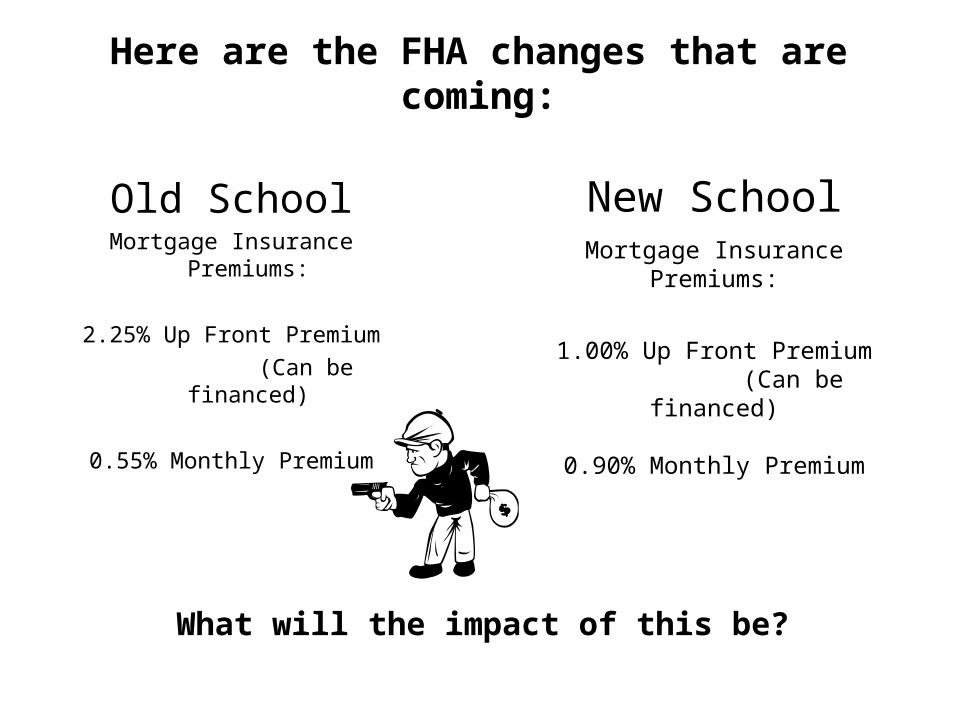

Here are the FHA changes that are coming:

Old SchoolMortgage Insurance Premiums:

2.25% Up Front Premium

(Can be financed)

0.55% Monthly Premium

New SchoolMortgage Insurance Premiums:

1.00% Up Front Premium (Can be financed)

0.90% Monthly Premium

What will the impact of this be?

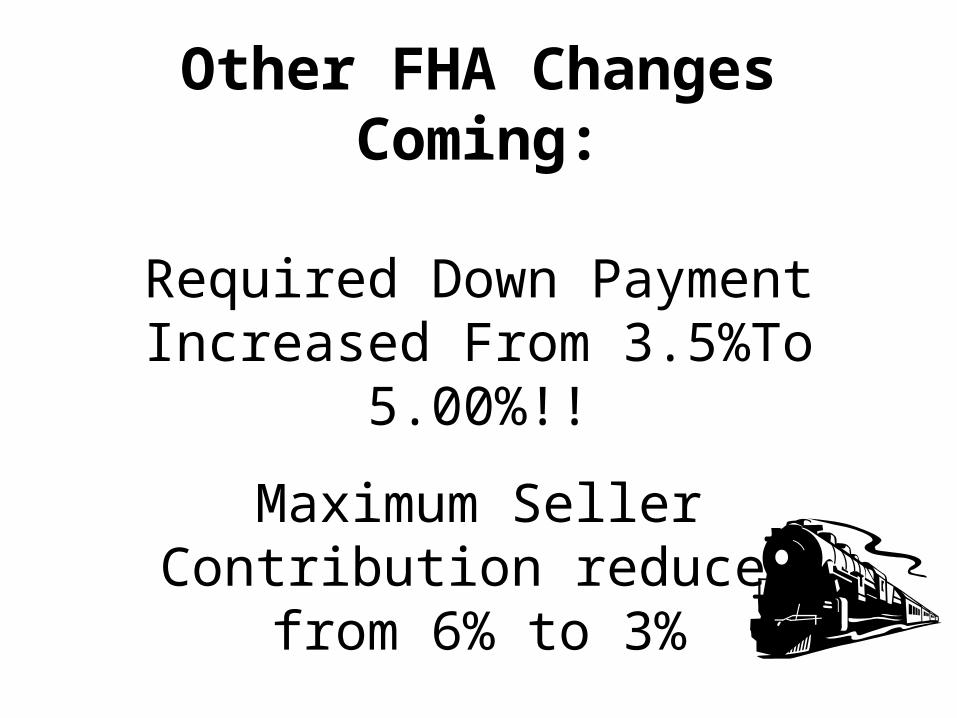

Other FHA Changes Coming:

Required Down Payment Increased From 3.5%To

5.00%!!

Maximum Seller Contribution reduced from 6% to 3%

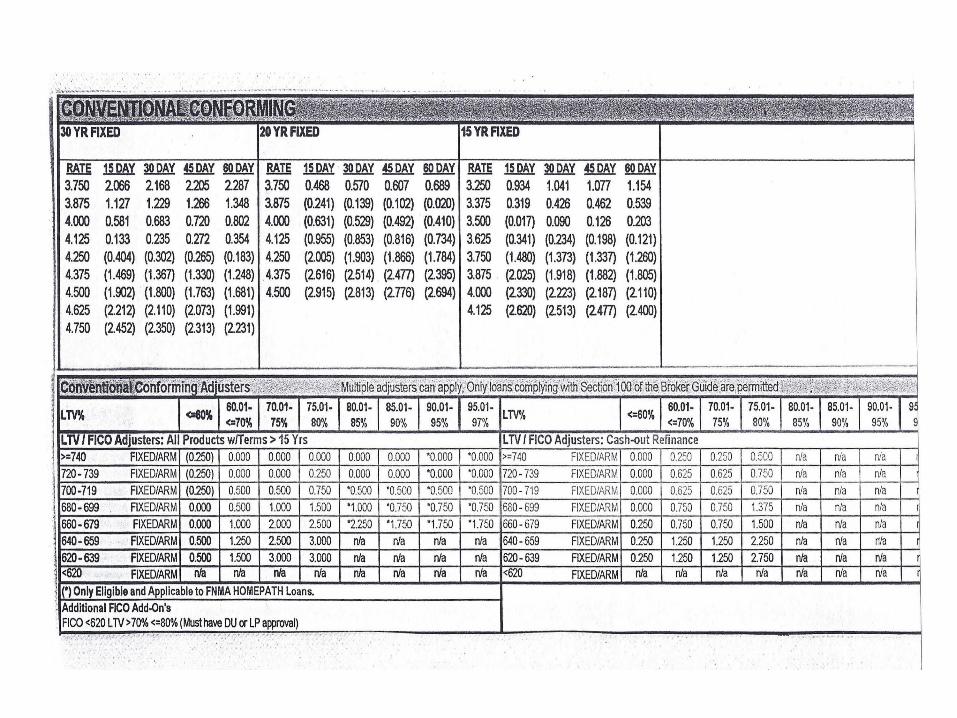

Remember that simple ‘rate sheet’ from ABC Bank?

How about this next one?

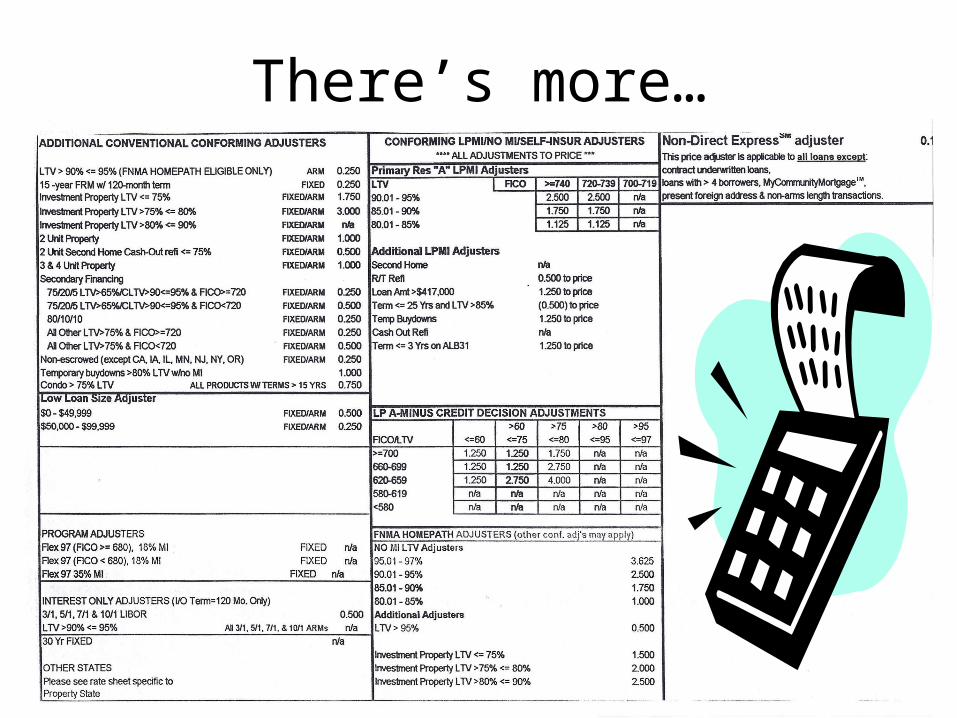

There’s more…

What happened that got us in this mess?

• Loan programs developed that would let almost anyone obtain a mortgage– Easy credit qualification– Stated income documentation– No income documentation– No asset documentation– No employment documentation– Adjustable Rate Mortgages with possible negative

amortization

– Were Mortgage Brokers to blame?

People on Wall Street Were Buying These Loans

Seemed like a good idea at the time!

8/4/09 getting ready to close

• As soon as we receive the final approval of the HUD, I am going to call and set up a closing time with him and let him know how much he needs to bring to closing. The lender is pretty quick to respond so I should have the revised HUD approved shortly.

• And then…………………

• Taylor, Bean & Whitaker Mortgage Corp. is no longer originating, underwriting, or processing loans in any jurisdiction, effective Wednesday, August 5, 2009.

• Taylor, Bean and Whitaker Mortgage Corp. – one of the largest non-bank residential lenders in Florida – has been barred from issuing mortgages in the state by the Florida Office of Financial Regulation.

• The state agency released an emergency cease and desist order Aug. 7 against Ocala-based Taylor Bean, which has 30 offices in Florida. State residents in the middle of the application process should be placed with viable alternate lenders.

• The Wall Street Journal called Taylor Bean the third-largest

underwriter of FHA loans in the country.

What has been done to fix this mess?

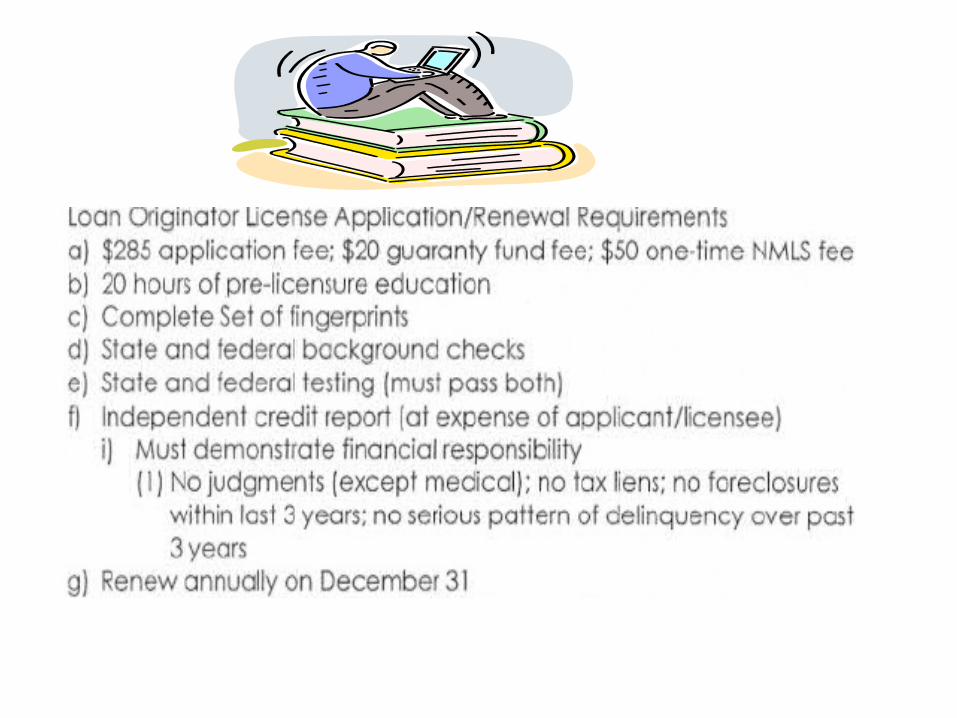

• The SAFE (Secure and Fair Enforcement Act) Act of 2008 Requires Mortgage Originators to be Federally Registered.

• No matter where they go in the USA, they will be identified with a unique identification number

• They need to pass a national test• They need to meet certain minimum credit

history criteria

• Compliance News Recap• Mortgage Licensing Registry Launched

• The House recently passed a predatory-lending bill (H.R. 3915) that requires the creation of a nationwide mortgage licensing system and registry

Licensed Mortgage Originators need a Federal Id Number

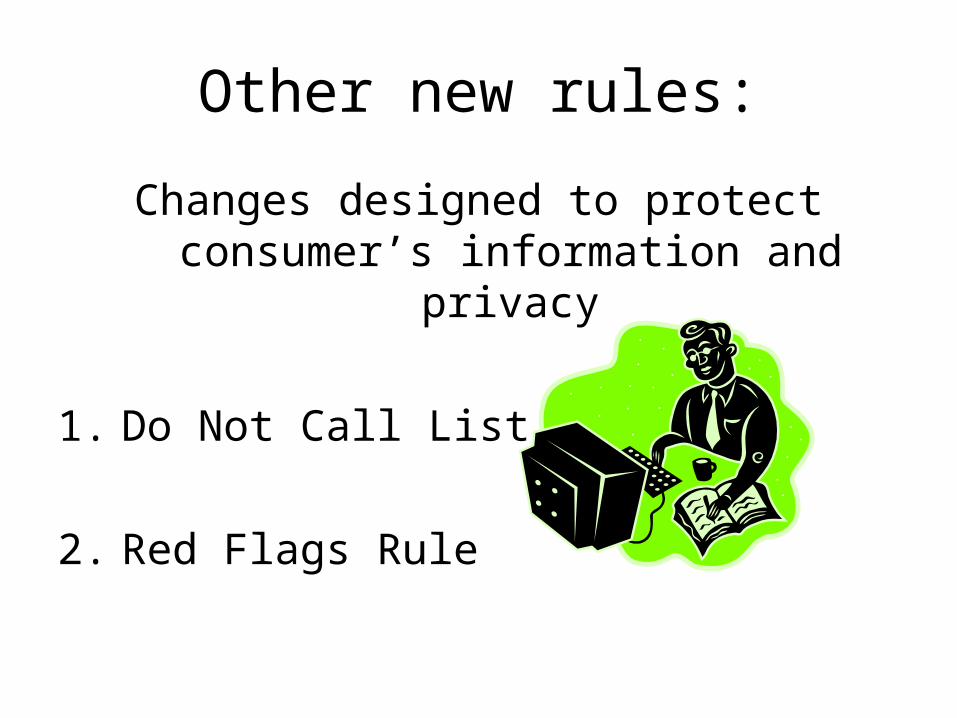

Other new rules:

Changes designed to protect consumer’s information and privacy

1. Do Not Call List

2. Red Flags Rule

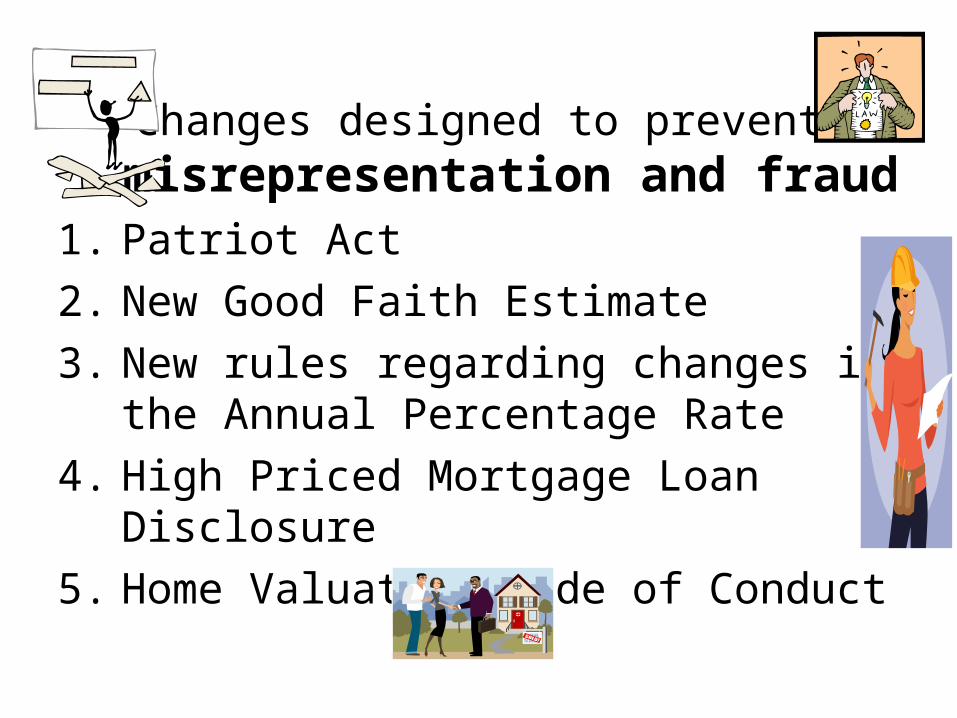

Changes designed to prevent misrepresentation and fraud

1. Patriot Act

2. New Good Faith Estimate

3. New rules regarding changes in the Annual Percentage Rate

4. High Priced Mortgage Loan Disclosure

5. Home Valuation Code of Conduct

How much can be legally charged?

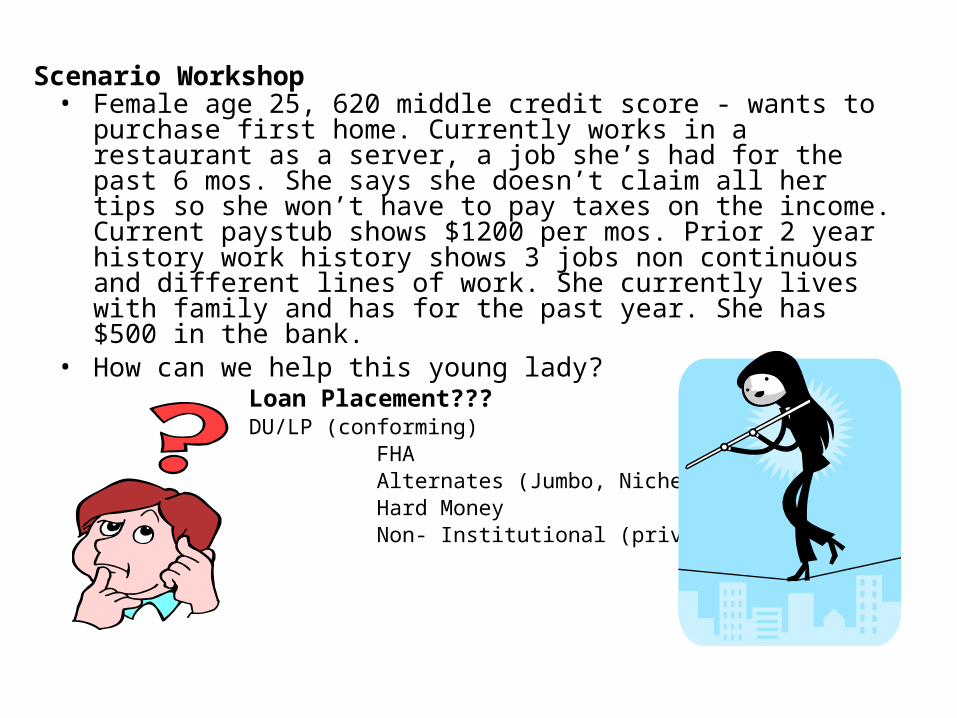

Scenario Workshop • Female age 25, 620 middle credit score - wants to purchase first

home. Currently works in a restaurant as a server, a job she’s had for the past 6 mos. She says she doesn’t claim all her tips so she won’t have to pay taxes on the income. Current paystub shows $1200 per mos. Prior 2 year history work history shows 3 jobs non continuous and different lines of work. She currently lives with family and has for the past year. She has $500 in the bank.

• How can we help this young lady?Loan Placement???DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

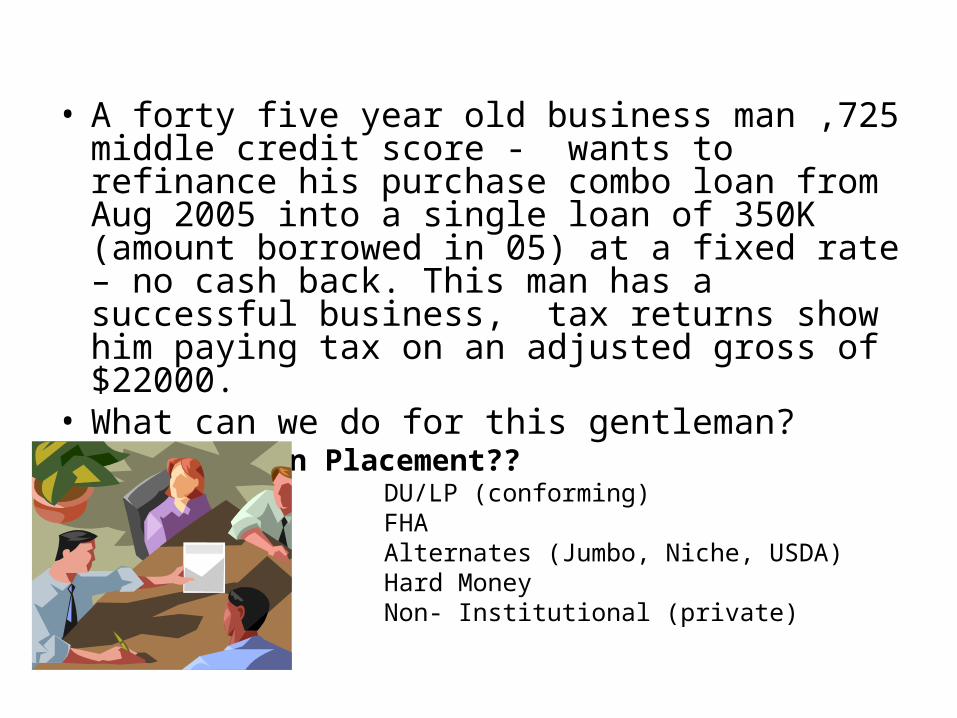

• A forty five year old business man ,725 middle credit score - wants to refinance his purchase combo loan from Aug 2005 into a single loan of 350K (amount borrowed in 05) at a fixed rate – no cash back. This man has a successful business, tax returns show him paying tax on an adjusted gross of $22000.

• What can we do for this gentleman? Loan Placement?? DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

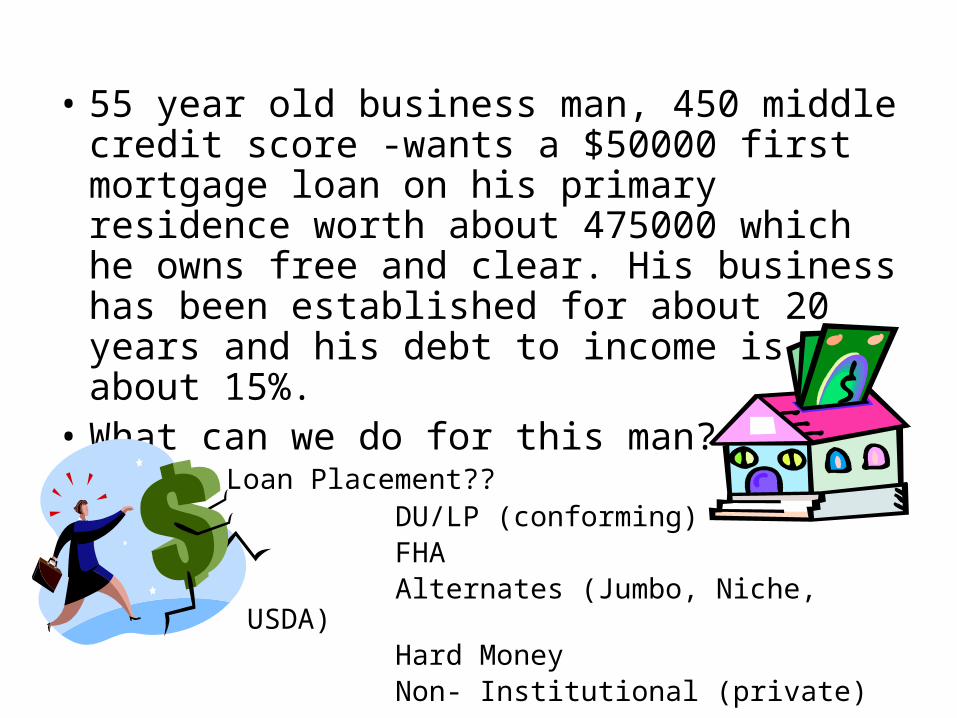

• 55 year old business man, 450 middle credit score -wants a $50000 first mortgage loan on his primary residence worth about 475000 which he owns free and clear. His business has been established for about 20 years and his debt to income is about 15%.

• What can we do for this man?Loan Placement?? DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

• Individual, 680 middle credit score - wishing to buy another investment property (he already owns 16 others). He provides executed leases, which show significantly higher income than he reports on his tax returns. He is prepared to put a 50% down payment, and will still have significant reserves after closing. His qualifying ratio is off the chart using the tax returns.

• What can we do to help this person?Loan Placement??

DU/LP (conforming)

FHA

Alternates (Jumbo, Niche, USDA)

Hard Money

Non- Institutional (private)

• 720 middle credit score, with solid credit history • Has lived in the US for 7 years • Was a self employed physical therapist in NY for 5 years

before moving to FL and obtaining a salaried job in the same line of work

• 80% ltv, purchase of a primary residence• Down payment and closing costs are coming from his

father, who lives in Egypt; bank statements are in Arabic

• What can we do to help this person?Loan Placement?? DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

• Man with 780 middle wishes to buy condo in Sarasota as primary for 74K. In his line of work he travels extensively on the US on a work visa. He currently owns a home in the Northeast worth 250K . He has sufficient assets to pay cash for the property if he desired. Income is not a problem for ratio’s

Loan Placement??

DU/LP (conforming)

FHA

Alternates (Jumbo, Niche, USDA)

Hard Money

Non- Institutional (private)

Bonus Bonus Bonus BonusBonus

• 63 year old woman,450 middle, in foreclosure, house in poor condition, Owes 115000,house worth about 250,000

• Give away hint – We have not discussed this type of loan