a clash of cultures: the governance and valuation effects ... · a clash of cultures: the...

TRANSCRIPT

A Clash of Cultures: The Governance and Valuation Effects of Multiple Corporate Cultures

Stephen P. Ferris Trulaske College of Business

University of Missouri Email: [email protected]

Narayanan Jayaraman

Scheller College of Business Georgia Institute of Technology

Email: [email protected]

Teng Zhang Scheller College of Business

Georgia Institute of Technology Email: [email protected]

11 April 2017

We are grateful for helpful comments and suggestions from Andras Danis, Ronald Masulis, Chris Parsons, Paul Smeets, and seminar participants at the American Finance Association 2017 annual meeting and seminar participants at the Georgia Institute of Technology. Any errors or omissions are our own.

A Clash of Cultures: The Governance and Valuation Effects of Multiple Corporate Cultures

Abstract

This study investigates the effect of multiple corporate cultures on a firm’s governance and valuation. Estimating two cultural distances: (1) between the CEO and the board and (2) between the CEO and stakeholders, we find both explain CEO turnover and firm value. Increased cultural distance is associated with greater CEO turnover, but also with higher firm value. We conclude that greater cultural distance between a CEO and the board results in less empathy for the CEO, but produces greater monitoring with consequently increased firm value. These results are robust to a variety of tests for selection bias and endogeneity.

JEL Codes: G34 Keywords: culture; turnover; CEO

1

A Clash of Cultures: The Governance and Valuation Effects of Multiple Corporate Cultures

1. Introduction

The existing literature on culture and finance establishes the role that national culture

exerts on various corporate polices, activities, and decisions.1 Given the importance of culture

for our understanding of corporate finance, it is useful to examine how differences in national

cultures might explain differences in various global corporate behaviors. Existing studies

suggest that cultural differences between countries have impacts on foreign direct investment

(Guiso, Sapienza, and Zingales, 2009), equity investment (Hwang, 2011), venture-capital flows

(Bottazzi, DaRin, and Hellmann, 2010), borrowing costs (Giannetti and Yafeh, 2012), and

merger activity (Ahern, Daminelli, and Fracassi, 2015). But unlike these studies, we contend

there is not just a single national culture affecting a firm’s actions. Rather, there is a multiplicity

of cultures operating within a given firm that reflects the culture of the firm’s management, its

board of directors, and its stakeholders. Each of these separate cultures must be considered to

determine the effect of culture on a firm.

This study focuses on the three cultures that are most likely to affect a firm’s behavior

and value. These are: (1) the culture associated with the CEO, (2) the dominant culture of the

board of directors, and (3) the culture of the firm’s stakeholders. To assess the relevance of

1 For instance , Weber, Shenkar, and Raveh (1996), Ahern, Daminelli, and Fracassi (2015), and Chakrabarti, Gupta-Mukherjee, and Jayaraman (2009) examine the role of culture on merger and acquisitions activity, while Stulz and Williamson (2003) describe culture’s effect on the nature of creditor rights within a country. Doidge, Karolyi, and Stulz (2007) relate culture to the governance ratings of firms. More recent studies show that cultural attributes such as the legal regime (Licht, 2014), language (Chen, 2013), the level of trust (Pevzner, Xie, and Xin, 2015), integrity and customer orientation (Guiso, Sapienza, and Zingales, 2015), and attitudes towards risk and uncertainty (Pan, Siegel, and Wang, 2015), and national traits (e.g., Bryan et al., 2015; El Ghoul and Zheng, 2016; Zheng et al., 2012) are important determinants of corporate decisions and the design of governance infrastructure. In addition, national cultural values have important impacts on stock market participation and stock price momentum (Guiso, Sapienza, and Zingales, 2008; Chui, Titman, and Wei, 2010).

2

culture for corporate decision-making and value, we consider the simultaneous interplay of

these three cultures. We contend that culture’s effect on the firm occurs from the interaction of

these sub-cultures that co-exist within the organization. Because of this tri-cultural perspective,

our analysis provides a more comprehensive and insightful examination of culture’s influence

on corporate behavior than what presently exists in the finance literature.

We examine the role of these cultures in a corporate setting by focusing on the differences

between them. The importance of relative differences is recognized in the psychology and

human resources literatures as a critical component of incentive and behavioral modification

programs (e.g., Gudykunst and Ting-Toomey, 1988). The presence of multiple corporate

cultures create differences in the attitudes and perceptions of the various corporate agents such

as the CEO, the board of directors, or external stakeholders. We refer to these differences in

culture between the corporate agents as cultural wedges. In this study, we analyze how cultural

wedges between the CEO, the board, and the firm’s stakeholders affect corporate governance

and firm value. More specifically, we examine the cultural wedges that exist between: (1) the

CEO and the board of directors, and (2) the CEO and the firm’s stakeholders.

The first cultural wedge occurs due to the cultural distance that exists between the CEO

and the board of directors. We refer to this cultural distance as the leadership wedge, which

measures the difference in culture between the CEO and the board of directors. As the cultural

distance widens between a CEO and the board, the leadership wedge correspondingly increases.

The homophily principle of McPherson, Smith-Lovin, and Cook (2001) asserts that individuals

tend to bond with those who are culturally similar. People sharing a common culture are more

likely to experience affinity between themselves. Cultural similarity can serve as an accelerator

for developing connections and linkages among individuals. When the CEO and the board share

3

a common culture, they are more likely to share similar values, beliefs, and attitudes. This

sharing can produce a greater sense of teamwork between the board and the CEO. Thus, a

smaller cultural wedge between the CEO and the board can reduce internal information

gathering costs (Giannetti and Yafeh 2012) and result in more efficient decision-making. This

can ultimately generate an increase in firm value (Adams and Ferreira, 2007).

A smaller leadership wedge, however, might reduce corporate value. This can occur due

to weaker monitoring by the board when cultural commonality impairs directors’ independence

or their willingness to discipline errant executives. Fracassi and Tate (2012) use evidence from

executive external networking and show that close CEO-director ties reduce firm value by

encouraging managers to engage in more value-destroying acquisitions.

The second cultural wedge we examine is that between the CEO and the firm’s

stakeholders. We refer to this cultural distance as the citizenship wedge. A smaller citizenship

wedge implies a greater cultural affinity between the CEO and the firm’s employees, managers,

and investor “citizens”. This citizenship wedge has implications for the level of empathy and

acceptance that investors might have for a CEO since it measures the cultural similarities that

they share. Consequently, the citizenship wedge has the potential to affect valuation since

empathy and acceptance are directly related to the amount of optimism that an individual holds

regarding another (Diether, Malloy, and Scherbina, 2002; Ciccone, 2003; Ferris, Jayaraman,

and Sabherwal, 2013). The investment and behavioral literatures then show that increased

optimism results in higher equity valuations (Brinthaupt, Moreland, and Levine, 1991;

Schweizer, Beck-Seyffer, and Schneider, 1999; Lyubomirsky, Kennon, and Schkade, 2005).

We use the six cultural dimensions developed by Hofstede (1980, 2001) to construct our

measures of the leadership and citizenship wedges. These wedges are calculated from the

4

numerical values of the six Hofstede dimensions: individualism, uncertainty avoidance, power

distance, masculinity, long-term orientation, and indulgence. We assign cultural values to

individual directors and the CEO based on their nationalities and assign cultural values to the

firm’s stakeholders based on the firm’s country of incorporation.2 To quantify the cultural

distances, we apply a Euclidean estimation model. Specifically, we average the distances on

each of these dimensions between the individual directors and the CEO to obtain the leadership

wedge for a given firm. We follow a similar approach to calculate the citizenship wedge

between the CEO and the firm’s country of incorporation. In robustness tests we re-estimate

our wedge measures using the seven Schwartz (2006) values which represent a different way

of conceptualizing national cultures and their measurement. Nevertheless, we obtain

qualitatively similar results using these alternative measures of cultural wedges.

We use these two cultural wedges for our analysis of corporate governance and firm value.

CEO turnover is our measure of corporate governance since replacement of the CEO can result

in changes in transparency levels, disclosure policies, and the working relationship with the

board. Since similarity creates bonds between individuals (McPherson et al., 2001), we argue

that smaller cultural wedges imply greater tolerance and increased levels of empathy. Larger

cultural wedges imply increased dissimilarity, with reduced tolerance and lower levels of

empathy. Therefore, we hypothesize that there is a positive relation between the size of the

cultural wedge and the likelihood of CEO replacement.

2 We proxy the culture of the firm’s stakeholders with that of the firm’s country of incorporation for several reasons: First, the culture of the country of incorporation is the culture that establishes the legal and regulatory procedures that the firm must follow. Second, many of the employees and subordinate managers are likely to share the culture of the country of incorporation since they are living and working in that country. Finally, it is likely that many of the firm’s investors will share the culture of the country of incorporation.

5

We then investigate how cultural wedges might affect corporate value. The effect of

cultural wedges on firm value, however, is a priori uncertain. Because of greater empathy and

understanding, smaller cultural wedges can reduce information asymmetry, accelerate

information flow, and allow for operational consensus. This suggests a positive effect on firm

value. Alternatively, smaller wedges can create a false sense of CEO competence, a desire to

avoid conflict, and a reduction in the willingness to monitor. Such behavioral result can generate

an adverse effect on firm value.

Our empirical findings show that larger leadership wedges are associated with a higher

probability of CEO turnover and greater firm values. These findings support the view that

greater cultural distance leads to increased monitoring, and ultimately enhanced firm

performance. In this sense, these results are consistent with the general predictions of agency

theory regarding the importance of managerial monitoring for the creation of firm value. We

also find that larger citizenship wedges are associated with lower firm values. This is consistent

with the view that investors prefer CEOs with whom they have greater cultural affinity (Kumar

et al. 2015) and this ultimately results in higher firm valuation. Further, we find greater

sensitivity of CEO turnover to financial performance for firms having larger cultural wedges.

This result is consistent with our argument that cultural wedges imply less tolerance and

reduced levels of empathy for CEOs by their boards and stakeholders.

Possible selection bias can arise from the fact that firms with foreign executives or

directors might be inherently different due to some unobserved characteristics. We address this

possibility by using firm fixed effects and a Heckman selection model. The results from these

econometric adjustments confirm that greater CEO turnover and firm values are not driven by

heterogeneity in unobserved characteristics.

6

We also recognize the possibility of endogeneity due to bi-directional causality. It might

be that the CEO anticipates a firm’s future value and accordingly make changes in the board’s

composition. Consequently, we estimate a set of instrumented regressions. Specifically, we

follow Ahern, Daminelli, and Fracassi (2015) and instrument for cultural distances using

genetic differences across populations. We find that our results remain robust to this adjustment

and continue to conclude that a larger cultural wedge between a firm’s CEO and its board of

directors is associated with increased with firm value.

Our study directly contributes to the growing literature on cultural effects in corporate

decision-making (Guiso, Sapienza, and Zingales, 2006, 2008, 2009; Chui, Titman, and Wei,

2010; Gorodnichenko and Roland, 2010; Li, Griffin, Yue, and Zhao, 2011; Giannetti and Yafeh,

2012; Ahern, Daminelli, and Fracassi, 2015). However, unlike this prior literature that explores

the effects of a single country’s culture across firms, we focus on the multiple cultural

differences that exist within a firm and which we label as cultural wedges. Our emphasis on

these cultural wedges allows us to examine the three most influential cultures (i.e., cultures

possessed by the CEO, the board, and the firm’s stakeholders) that exist within a firm and how

the differences between them affect corporate behavior and value.

The remainder of our study is organized as follows. Section 2 discusses our hypotheses

regarding the effect of cultural wedges on CEO turnover and firm value. Section 3 describes

our data sources and the methods we use to construct our two cultural wedges. Section 4 and 5

present our most important empirical findings. Robustness checks are discussed in Section 6.

Section 7 presents concluding remarks.

7

2. The Effect of Cultural Distances

2.1 CEO and the board of directors

The cross-culture literature in psychology and linguistics (e.g., Ruben, 1977; Tannen,

1984) establishes that there are distinct cultural patterns in both what is communicated and how

that communication is achieved. It is not easy to bridge these cultural divides and requires

significant effort by both the sender and receiver to achieve understanding.

When there is a large difference between the cultures of a CEO and the board, the costs

of collecting and processing internal information are higher (Giannetti and Yafeh 2012). Thus

with a larger leadership wedge, there is greater potential for misunderstanding. This is

consistent with the findings of Earley and Mosakowski (2000) who report that diversity in

nationality can undermine communication effectiveness and provoke group conflict. Cultural

distance between a CEO and the board can also produce friction or conflict when there is

hostility or mistrust between the directors and the CEO, and the likelihood of executive turnover

increases (Weisbach, 1988; Parrino, 1997; Goyal and Park, 2002).

Further, given the existing evidence that similarity creates connections among individuals

(McPherson, Smith-Lovin, and Cook, 2001), homogeneity in cultural backgrounds is likely to

foster mutual understanding (Knoke, 1990; Huckfeldt and Sprague, 1995). For instance, Kumar,

Niessen-Ruenzi, and Spalt (2015) find that the U.S. investors trust mutual fund managers with

American-sounding names more than those who are foreign-named. In a corporate context, Lee,

Lee, and Nagarajan (2014) find that alignment in political orientation between a CEO and the

board is associated with a reduced likelihood of dismissing poorly performing CEOs. This

alignment between the CEO and the board can reduce the likelihood of turnover even in the

presence of poor performance by the CEO.

8

We contend that the size of the leadership wedge affects the likelihood of CEO

termination. Larger wedges make it more difficult for a CEO to develop positive relations with

the firm’s directors. Leadership wedges also influence the extent to which directors are willing

to be tolerant of CEO shortcomings. As discussed in studies of affinity in consumer lending

such as Hunter and Walker (1996), it is easier to be understanding and forgiving of individuals

who are similar to ourselves.

The effect of the leadership wedge on firm value, however, is uncertain. CEOs face a

trade-off in their relationships with directors who are required to both advise and monitor

management. Homogeneity in cultural backgrounds between managers and directors can

produce an increased level of mutual acceptance. This can result in better advice from the board,

quicker decisions from the directors, and easier board approval of the CEO’s strategies. These

advantages might then be capitalized into increased firm value (Adams and Ferreira, 2007).

However, a higher level of mutual acceptance between the CEO and the board can reduce the

quality of monitoring, limit critical thinking, or discourage dissenting opinions. The desire for

consensus and understanding can cause directors to avoid difficult dialogues with CEOs,

ultimately resulting in less effective monitoring by the board. This result is suggested by Coles,

Daniel, and Naveen (2015) who find that increased cohesiveness among directors inversely

affects firm value.

2.2 CEO and the firm’s stakeholders

The citizenship wedge is especially important for its measurement of the cultural affinity

that exists between the CEO and the firm’s stakeholders. Greater cultural similarity between a

CEO and the firm’s stakeholders can result in a greater acceptance of managerial strategies,

more rapid implementation of executive decisions, and fewer incidences of miscommunication.

9

Greater cultural affinity can lead to increased trust in the manager by stakeholders and a

consequently more favorable view of the firm. If the citizenship wedge is large, however,

communication and behaviors are more likely to be misinterpreted or misunderstood. Cultural

wedges can distort the signals that a CEO elects to send to the market.

The citizenship wedge also helps to determine the location and the size of group fault

lines that exist between directors and the CEO. Kaczmarek et al. (2012) define group fault lines

as those characteristics “that split a group into relatively homogeneous subgroups based on

group members’ alignment along their multiple attributes”. Fault lines can occur based on

culture, leading to friction between the CEO and the board with a consequent adverse effect on

the ability of the board to monitor or to provide advice.

We contend that the size of the citizenship wedge can influence the decision to terminate

a CEO’s employment. Cultural distance influences the effectiveness of communications

between a CEO and the firm’s investors, how the CEO’s activities are seen by other managers

and employees, and even how analysts and competitors interpret the CEO’s behaviors. Cultural

distance affects the extent to which these other stakeholders are willing to be empathetic or

understanding, especially in the presence of adverse corporate events or poor performance.

Thus, we believe that the citizenship wedge is also relevant for an understanding of CEO

turnover.

The citizenship wedge can also affect firm valuation because this wedge influences how

investors perceive the CEO since it is a measure of the cultural similarities they share. For

example, the citizenship wedge can affect how investors and other stakeholders react to the

CEO’s decisions about operations and resource allocations. Because this wedge influences the

amount of empathy and acceptance that stakeholders have regarding the CEO, it can affect the

10

level of optimism that stakeholders have about the CEO, and more generally, the firm (Diether,

Malloy, and Scherbina, 2002; Ciccone, 2003; Ferris, Jayaraman, and Sabherwal, 2013).

Existing studies in the investment and behavioral literatures have established the view that

increased level of optimism leads to higher valuations (Brinthaupt, Moreland, and Levine, 1991;

Schweizer, Beck-Seyffer, and Schneider, 1999; Lyubomirsky, Kennon, and Schkade, 2005).

3. Data Sources and Cultural Measure Constructions

3.1 Data and sample

Our sample consists of firms from 17 European countries: Austria, Belgium, Denmark,

Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Norway, Portugal,

Spain, Sweden, Switzerland, and the U.K. Cultural scores assigned to each country used to

estimate our two cultural wedges are obtained from Geert Hofstede’s website. Data used for the

CEO and the board characteristics are from the BoardEx database.3 We construct financial

variables using data obtained from the Compustat Global. We exclude firms in the utility and

financial sectors from our sample. Given the initial availability of data from the BoardEx, we

set our sample period from 1999 to 2012. The total number of firm-years in our sample is 25,119.

We select these 17 countries as they have the most firm-year observations in our sample

and provide a high coverage of European firms. Our choice of a European sample is motivated

by three reasons. First, custom and prior practice are arguably more important than formal

regulation in European countries (Jenkinson, Morrison, and Wilhelm, 2006). This emphasis on

tradition makes it likely that cultural distance matters for firms operating in these countries.

3 The BoardEx database contains biographical information for directors and executives of a set of global public and private firms, and is used in a number of studies. See, e.g., Cohen, et al., 2010, Fernandes et al., 2013, and Knyazeva et al., 2013.

11

Second, due to the economic liberalization associated with the creation of the European Union,

there are more foreign CEOs and directors in these nations relative to other regions of the world.

Finally, by excluding the U.S., we can be confident that our results are not driven by one mega-

economy and that our findings are insightful regarding cultures’ influence to a more global set

of firms.

3.2 Measuring cultural wedges

Starting from the CEO of the firm, the center of corporate leadership, we construct two

measures of cultural distance. The first is that between the CEO and the firm’s board of directors

which we term the leadership wedge. The second is the cultural gap between the CEO and the

country in which the firm is incorporated which we label as the citizenship wedge.

3.2.1 Leadership wedge

We construct our leadership wedge based on a Euclidean distance using all six of the

Hofstede published dimensions.4 We assign Hofstede cultural dimension values to each CEO

and individual director based on their nationality records as contained in the BoardEx database.5

In each year, we estimate cultural differences between the CEO and each of the individual

directors for a given firm. We then calculate the average across all of these pairwise distances.

We refer to this average value as the leadership wedge between the CEO and the board of

4 According to Hofstede (2001), there are six dimensions to a country’s culture. This represents an expansion from the four dimensions he originally developed in 1980. Power Distance is defined as the extent to which the less powerful members of institutions and organizations within a country expect and accept that power is distributed unequally. Individualism is the degree of interdependence a society maintains among its members. Masculinity captures an individuals’ motivation: wanting to be the best (masculine) or liking what you do (feminine). Uncertainty Avoidance reflects the extent to which members of a culture feel threatened by ambiguous or unknown situations and create beliefs or institutions that try to avoid them. Long Term Orientation describes how a culture maintains links to its past and traditions. Indulgence is defined as the extent to which people try to control their desires and impulses. 5 By assigning cultural scores based on individuals’ nationalities we implicitly assume that culturally transmitted preferences are determined early in life and are persistent (Giavazzi et al., 2014).

12

directors for the given firm-year. More specifically, the leadership wedge for firm i in year t is

constructed in a Euclidean format as follows:

Leadership wedge i,t = ∑𝐾𝐾,𝑡𝑡𝑘𝑘,𝑡𝑡=1 �∑ (𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡 − 𝑆𝑆𝐵𝐵𝐵𝐵𝐵𝐵 𝑖𝑖,𝑘𝑘,ℎ,𝑡𝑡)26

ℎ=1

6 × 𝐾𝐾𝐾𝐾’ (1)

where SCEO i,h,t refers to the Hofstede cultural score for a CEO at firm i on cultural dimension h

in year t. SBRD i,k,h,t refers to the Hofstede cultural score for director k at firm i on dimension h

in year t. Kt is the total number of directors at firm i in year t. Since our focus is on the aggregate

level of cultural distance, we weigh each of the cultural dimensions equally.

The leadership wedge reflects the extent to which there are differences in cultural values

between the CEO and the board of directors. As the cultural wedge widens, there is increased

potential for miscommunication or misunderstanding between the manager and the board.

Consequently, information or signals shared by the CEO can be misunderstood by the board,

causing the CEO to become reluctant to release information to directors (Adams and Ferreira,

2007). Therefore, we hypothesize that as the leadership wedge widens, the board of directors

engages in tougher monitoring on the firm’s management.

3.2.2 Citizenship wedge

To measure the cultural distance between a CEO and the firm’s stakeholders, i.e., the

citizenship wedge, we use the Hofstede cultural scores assigned to the country in which the

firm is incorporated as the proxy for the culture of the firm’s stakeholders. This choice of proxy

for the culture of the firm’s stakeholders is justifiable for several reasons. First, the culture of

the country of incorporation is the culture that establishes the legal and regulatory procedures

that the firm must follow. Second, many of the employees and subordinate managers are likely

to share the culture of the country of incorporation since they will be living and working in that

country. Finally, given the well know home bias present in the portfolio holdings of investors

13

(Merton, 1987; Kang and Stulz, 1997; Coval and Moskowitz, 1999) and the cognizance

limitations of investors (Kang and Stulz, 1997; van Nieuwerburgh and Veldkamp, 2009), it is

likely that many of the firm’s investors will share the culture of the country of incorporation.

Thus, the culture of the country in which the firm is incorporated is likely to be the most

influential culture for many of the firm’s stakeholders.

More specifically, the citizenship wedge for firm i in year t is constructed in a format

similar with the leadership wedge as follows:

Citizenship wedgei, t = �∑ (𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡 − 𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡)26

ℎ=1

6’ (2)

where SCEO i,h,t denotes the Hofstede cultural score for a CEO at firm i on dimension h in year t.

SCTY i,h,t refers to the Hofstede cultural score for the country where firm i is incorporated on

dimension h in year t. A large citizenship wedge implies that the CEO culturally deviates from

the dominant culture of the firm’s stakeholders.

3.3 The distribution of cultural distance scores

Table 1 reports summary statistics for the leadership and citizenship wedges for the firms

in each of our sample countries. The number of observations, mean, median, and standard

deviation are obtained using firm-year data within the specific sample country. We observe

considerable cross-country heterogeneity in these cultural wedge measures: Luxembourg has

the largest average leadership (2.78) and citizenship wedges (4.11) among our 17 sample

countries. Greece has the smallest leadership wedge (0.34), and Portugal has the smallest

citizenship wedge (0.09). These results for Greece and Portugal are consistent with the

prevalence of family firms in these economies (La Porta et al, 1999).

3.4 Domestic and non-domestic firms

14

For those firms with an absolute cultural homogeneity, the culture of the CEO, the board

of directors, and the country of incorporation is the same. In these cases, both the leadership

and cultural wedges are zero. We refer to these firm-year observations where both the

leadership and citizenship wedges have a zero value as domestic. Otherwise, the firm-year

observations are classified as non-domestic. In other words, for non-domestic firm-years either

the leadership, citizenship, or both wedges have positive values.

Panel B of Table 1 shows the number and percentage of domestic and non-domestic firm-

year observations aggregated at the country level. We find that Norway has the highest

percentage of domestic firm-years (62.15%) while Switzerland has the highest percentage of

non-domestic firm-year observations. In terms of numbers, the U.K. reports the highest number

of domestic observations, perhaps reflecting the large size of its capital market. Interestingly,

the U.K has the largest number of non-domestic observations as well. This might be due to the

historical global nature of the London capital markets.

Panel C of Table 1 presents a time-series of the distribution of domestic and non-domestic

observations. Our results indicate a downward trend in the percentage of firm-years classified

as domestic over the sample period. The percentage of domestic observations appears to rise

over the early years of our sample, peaking at 52.4% in 2003. It then follows with a monotonic

decline for the remainder of the sample period, terminating at 29.2% in 2012. We believe that

these results are consistent with the effects of increased globalization and the maturation of the

European Union. Both factors facilitate the international movement of human capital, especially

management talent, which results in a greater cultural diversity in the executive and board suites.

Table 2 presents summary statistics of the variables used in our analysis for the full

sample as well as the domestic and non-domestic subsamples. We have 9,786 observations in

15

the domestic subsample and 15,333 observations contained in the non-domestic subsample. The

average level of the leadership wedge across all 25,119 firm-year observations is 0.861 with an

obvious value of zero for domestic firms and 1.41 for non-domestic firms. The mean of the

citizenship wedge is 0.730 for the full sample, zero for domestic firm-years, and 1.19 for the

non-domestic subsample of firm-years. The variables presented in Table 2 are described more

completely in the Appendix.

4. Cultural Distance and Corporate Governance

4.1 Firm type and CEO turnover

Our focus in this section is the effect that a firm’s cultural differences exert on the

likelihood of CEO turnover. We begin with a comparison of culturally domestic and non-

domestic firms. Specifically, we estimate the following linear probability model for firm i in

year t:

Turnoveri,t = β0 + β1 Domestici,t-1 + CEO & Board controlsi,t-1 + Firm controlsi,t-1

+ δt + αcountry + ηindustry + ϵi,t , (3)

where Turnover=1 if the firm replaces its CEO during the year. We use general turnovers (i.e.,

both forced and voluntary turnovers) as well as forced turnovers determined by an age of 65 as

the cutoff (more details will be discussed later). Domestic is an indicator variable that assumes

a value of one for a given firm-year observation if both its leadership and citizenship wedges

are zero. To control for CEO and board characteristics, we include CEO age, CEO tenure, the

percentage of independent board directors, total number of directors, and a dummy variable

indicating whether the CEO also holds the position of chairman of the board. To control for the

16

national diversity of the board, we further add a board homogeneity Herfindahl Hirschman

Index (HHI) measure. This variable is estimated as the sum of the various squared ratios of the

number of board directors from a given country divided by the total number of directors on the

board. We also control for firm-level financial characteristics by including the logarithm of firm

size, firm age, industry-adjusted EBIT scaled by total assets, the market-to-book ratio, return

on assets, book leverage which is defined as the ratio of the book value of total debt to the book

value of total assets, the logarithm of sales, the firm’s prior year stock return, stock return

volatility, the firm’s capital expenditures, and R&D expenses.6 Definitions for these control

variables are provided in Panels B and C of the Appendix. In addition, we add year, country,

and industry fixed effects denoted by δt , αcountry, and ηindustry, respectively. Since there might be

additional unobserved industry-level effects in the residual, we cluster the standard errors at the

industry level.7

Table 3 presents the results from our linear probability estimation of equation (3). A major

advantage of the linear probability model over the logistic model is the ease of its

interpretability.8 Panel A of Table 3 examines the effect of firm type on CEO turnover using

both forced and voluntary turnovers. The dependent variable is a binary indicator variable with

a value of one if the CEO turnover occurs for a given firm in the second half of a given fiscal

year or in the first half of the subsequent fiscal year, and zero otherwise. Column 1 presents the

6 Given a large number of missing values for firm age, we follow DeAngelo, DeAngelo, and Stulz (2006) and use retained earnings scaled by the book value of total assets as a proxy for firm age. To mitigate the effect of missing values for R&D expenses, we follow Koh and Reeb (2015) and replace the missing R&D observations with its median value, and create Missing R&D Dummy that takes a value of one if R&D is missing in a given firm-year. 7 We report the results of clustering standard errors at the industry level since it produces more conservative t-statistics. We also cluster standard errors at the firm level and obtain similar results. 8 In a linear probability model, one can directly infer the percentage change in the dependent variable from the coefficient estimates. The coefficient estimate can be interpreted as the change in the probability that the dependent variable is equal to one given a unit change in the independent variable. To further check the robustness of our results, we also estimate a logistic probability model and obtain results with comparable statistical significance.

17

regression results only controlling for year, industry, and country fixed effects. The coefficient

estimate, -0.042, is statistically significant at the 1% level and indicates that the CEO at a

domestic firm is 4.2% less likely to be terminated from her position than her peer at a non-

domestic firm. Columns 2 and 3 show that this inverse relation between domestic status and the

likelihood of CEO turnover is robust to the inclusion of the CEO, board, and firm controls. In

column 4 we add the board HHI which captures the national diversity of the board as a control

variable. One legitimate concern is that a nationally homogenous board is more united in its

demands, making it easier for the CEO to satisfy it. Thus, our turnover result can be driven by

nationally diversified boards that make it harder for the CEO to meet heterogeneous demands.

We find, however, that our result remains robust to the inclusion of the board HHI.

In Panel B we continue our analysis of the domestic status and CEO turnover by

examining its effect on forced resignations. The dependent variable is a forced turnover

indicator variable equal to one if the CEO is forced to quit her job. Consistent with Parrino

(1997) and Jenter and Kanaan (2015), we use the CEO’s age at the time of departure as a proxy

for forced turnover. Specifically, we classify a turnover as forced if the age of the departing

CEO is less than 65.9 Column 1 shows that the domestic indicator variable is significantly and

inversely associated with the likelihood of forced turnover. Columns 2 and 3 show that this

result is robust to the inclusion of an extensive set of CEO, board, and firm-level controls and

year, industry, and country fixed effects. In column 4, we further control for board national

homogeneity by including our HHI board measure and determine that its inclusion does not

affect the likelihood of forced turnover. The coefficient on the domestic dummy variable

9 To address the concern that the legal retirement ages might vary across our sample countries, we use alternative ages ranging from 60 to 64. We obtain similar results regardless of which retirement age we use to define forced turnover.

18

decreases to -0.043, compared to -0.028 in column 4 of Panel A. This decline in the coefficient

value implies that domestic status has a larger impact on forced than general turnover.

In aggregate, the findings presented in Table 3 show that the CEO who is culturally

identical to her board and stakeholders enjoys a reduced likelihood of turnover. These results

are consistent with the view that smaller cultural wedges imply more tolerance and greater

empathy between the CEO and her various monitors. This increased understanding ultimately

results in greater position longevity for the CEO.

4.2 Cultural distance and CEO turnover

Table 4 further examines the effects of cultural distances on CEO turnover by separately

investigating the effect of the leadership and citizenship wedges. Panel A of Table 4 presents

our analysis for general turnovers including forced and voluntary ones. Column 1 examines

how CEO turnover can be explained by the leadership wedge after controlling for year, country,

and industry fixed effects. The significant coefficient for the leadership wedge, 0.013, suggests

that a larger cultural distance between the CEO and the board leads to a higher likelihood of

CEO turnover. The economic magnitude of the coefficient is nontrivial: a one standard

deviation increase in the leadership wedge is associated with a 2.3% increase in the probability

of turnover. Column 2 shows that this result is robust to the inclusion of a full set of CEO, board,

and firm controls.

Columns 3 and 4 examine the effect of the citizenship wedge on CEO turnover. The

relation between the CEO and the firm’s stakeholders is not as direct as that between the CEO

and the board. Further, stakeholders lack the direct legal responsibility for monitoring managers.

Therefore, we expect that the influence of citizenship wedge on CEO termination will be

smaller. Our results are consistent with this argument. Specifically, column 3 shows that the

19

coefficient for the citizenship wedge, 0.006, is significantly positive. It is smaller, however,

than the 0,013 value reported in column 1. This coefficient indicates that a one standard

deviation increase in the citizenship wedge leads to a 1.4% increase in the likelihood of turnover.

Column 4 confirms the robustness of this result to the inclusion of various firm control variables.

In column 5 of Panel A, we include both the leadership and citizenship wedges as well as

their interaction term. The magnitude of the leadership wedge increases to 0.022, compared to

0.013 in column 1. The interaction term between these two wedges is negatively associated

with turnover likelihood. This suggests a concave relation between cultural distances and CEO

turnover.

Panel B of Table 4 sharpens our analysis by focusing solely on forced turnovers. The

dependent variable is a forced turnover indicator that is equal to one if the age of a departing

CEO is less than 65.10 Columns 1 and 3 present significantly positive coefficients for the

leadership and citizenship wedges, respectively. Columns 2 and 4 show that these results are

robust to controlling for a full set of governance and firm characteristics. In column 5, we add

both cultural wedges and their interaction term. These results suggest that both wedges can

contribute to CEO termination, although the cultural distance with a firm’s leadership team

appears to be the more dominant effect. We conclude from Table 4 that cultural distances between individuals have a distinct and

measurable effect on the likelihood of CEO turnover. The cultural wedges between the CEO

and the board as well as that between the CEO and the firm’s stakeholders influence the

likelihood of CEO turnover. Our findings also suggest that the leadership wedge has a larger

10 Again, our results remain robust to alternative departing CEO ages from 60 to 64.

20

impact on explaining turnover than the citizenship wedge. This is consistent with the legal

responsibilities of the board for monitoring and replacing the firm’s CEO.

4.3 Omitted variables and selection bias

It might be that the inverse effect of a firm’s status as a domestic (i.e., no leadership or

citizenship wedge) on CEO turnover is due to unobserved characteristics of firms having

foreign directors or executives. Thus, the issue of omitted variables arises as a possible

explanation for our findings. We address this possibility by employing two econometric

adjustments. First, we include firm-level fixed effects that act as a control for cross-firm

heterogeneity and possible unobserved characteristics. Second, we estimate a two-stage

Heckman model to address possible selection bias.

Column 5 in Panel A of Table 3 presents regression results using firm and year fixed

effects. It shows that the coefficient for the domestic indicator remains significantly negative

and its magnitude is similar to those in columns 2 through 4. Column 5 in Panel B of Table 3

confirms this finding when we use the forced turnover indicator as the dependent variable.

In Panel C of Table 3 we estimate a Heckman probit model to further address the selection

bias concern.11 Our use of this procedure involves estimating the likelihood that a firm is

matched with a foreign CEO in the first stage and then controlling for this likelihood in the

second stage. To capture variation in this likelihood that is independent of factors that can affect

CEO turnover, we employ an instrument --the population of the country in which the firm is

headquartered.12 The intuition of the instrument is that, given a larger population in the country,

11 Since the dependent variable is a binary indicator rather than a continuous variable, we use the Heckman Probit model, which reports results from the Wald test with the null hypothesis that the outcome is not significantly different from the outcome obtained by fitting the probit and selection models separately. 12 We obtain the population data for a given country-year from the World Bank database.

21

the board of a firm can pick domestic CEO candidates from a larger pool. Thus they are more

likely to find a talented target. There is, however, no obvious reason why the population level

is directly related to CEO turnover.

The first-stage estimates in columns 1 and 3 of Panel C confirm that the coefficient for

population is statistically significant and negatively correlated with the probability that a firm

hires a foreign CEO. In the second stage presented in Columns 2 and 4, the coefficient of the

domestic status variable remains significantly negative. Furthermore, the p-values of the Wald-

statistic indicate that the selection bias does not drive our results.

To address omitted variable concerns in our analysis of the effect of cultural wedges on

CEO turnover reported in Panels B and C of Table 4, we use firm fixed effects. Panel C of

Table 4 shows that our results remain quantitatively identical after including firm fixed effects.

The likelihood of general turnover (columns 1-3) and forced turnover (columns 4-6) increases

with the size of the leadership and citizenship wedges. Overall, we conclude that the effect of

these cultural wedges on CEO turnover is not attributable to omitted variables concerns.

4.4 Further analysis of CEO turnover

Although the preceding empirical analysis establishes the inverse relation between

cultural distance and CEO turnover after controlling for a number of board and firm

characteristics, we provide further analyses including a robustness check using hand-collected

turnover information, the mechanism of cultural distance’s impact on turnover, and ruling out

alternative explanations.

4.4.1 Direct identification of turnover

As a robustness test regarding our measurement of forced turnover, we hand-collect data

for a random selection of 15% of our sample CEO turnovers. Specifically, we search the

22

LexisNexis Academic database for CEO turnover news using the CEO name, company name,

and turnover date as search terms. All press releases that describe the CEO’s departure as fired,

pushed out, or a resignation due to firm performance, scandals, or investor pressure are

classified as forced. Departures are classified as voluntary if the press reports the reason for

departure as death, poor health, or the acceptance of a new position outside the firm. Consistent

with Parrino (1997) and Jenter and Kanaan (2015), we exclude CEO turnovers due to mergers

and spin-offs. This sub-sample contains only those turnovers for which the reason for departure

is clearly identified from press releases, consisting of 436 forced and 3,402 voluntary turnovers.

In un-tabulated results, we obtain statistically and economically comparable results to

those reported in Tables 3 and 4 with this hand-collected sub-sample of CEO turnovers. In the

baseline regressions for the cultural wedges, both the leadership and citizenship wedges are

positively correlated with forced turnover. Their coefficients are statistically significant at the

five percent level even after controlling for CEO, board, and firm characteristics and year,

industry, and country fixed effects.

4.4.2 Firm performance and cultural distance

Having documented the inverse relation between the cultural wedges and CEO turnover,

this subsection examines the mechanism behind this inverse relation. As we argue that cultural

wedges imply less tolerance and reduced levels of empathy, we formally test the heterogeneity

of CEO turnover-performance sensitivity across firms with different cultural wedges.

To test this possibility, we follow Kato and Long (2006) and estimate the following

executive turnover model:

Turnoveri,t = β0 + β1 Performancei,t-1 + β2 Cultural Wedgei,t-1 + β3 Performancei,t-1 * Cultural Wedge i,t-1

+CEO & Board controlsi,t-1 + Firm controlsi,t-1 + δt + αcountry + ηindustry + ϵi,t , (4)

23

where Turnover can be either general turnover or forced turnover as defined earlier.

Performance is the firm’s stock return in the previous year. Cultural wedge can be either

leadership wedge or citizenship wedge as defined earlier. We also control for the same set of

CEO, board, and firm characteristics as in Equation (3). In addition, we add year, country, and

industry fixed effects. Standard errors are clustered at the industry level.

Table 5 provides the estimates of Equation (4). The two cultural wedges, leadership and

citizenship are positive and statistically significant at the 1% level. And when we interact

performance with either our leadership or citizenship wedge, the interaction term becomes

consistently negative and highly significant. These findings indicate that not only does a larger

leadership/citizenship wedge increase turnover likelihood, but the magnitude of this effect is

larger for worse performance. In other words, CEOs are more likely to be terminated from their

positions for poor financial performance when that performance is accompanied by a cultural

distance from the board or the firm’s stakeholders. We conclude that these results are

inconsistent with the argument that the effect of cultural distance on CEO turnover is due to

financial performance. These results provide micro-level evidence linking culture distances and

CEO turnover.

4.4.3 Governance quality

An alternative explanation of our results regarding cultural distance and turnover is the

influence of the quality of the firm’s governance. For example, it is possible that the majority

of CEOs in domestic firms are well-entrenched or working with a friendly board, so the inverse

relation between cultural distance and turnover really captures weak corporate governance.

We test for such a possibility by comparing a set of sub-samples based on governance

quality measures. Specifically, we compare the coefficients for the domestic indicator variables

24

across subsamples stratified on three different measures of corporate governance quality widely

recognized in the literature (Berger, Ofek, and Yermack 1997; Hu and Kumar 2004). These

measures are: (1) the fraction of independent directors on a board, (2) the CEO-chair duality

indicator variable, and (3) CEO tenure. Independent directors have less personal ties with the

CEO and thus can be more demanding monitors. The CEO who has a longer tenure with the

firm or simultaneously holds the board chairmanship is likely to be well entrenched in the firm

and widely accepted as a powerful manager.

We construct tercile subsamples based on these governance quality measures and present

our results in Table 6. If governance quality determines CEO turnover rather than a firm’s

domestic status, the coefficients on the domestic indicator variable should not remain

statistically significant for the high-quality subsamples. In column 2 we examine the high-

quality subsamples with high percentage of independent directors. In column 3 we study the

high quality firms without CEO-chair duality. In column 5 we analyze those high quality firms

whose CEOs have a low level of job tenure. The results for each of these subsamples show that

the domestic indicator variable remains significantly negative. . These findings convince us

that the quality of corporate governance does not explain the inverse relation between cultural

distance and CEO turnover.

4.5 Cultural persistence

There is an extensive socio-psychological literature (Wenzel, 2001; Garcia et al., 2005;

Garcia and Ybarra, 2007) establishing an affinity effect in personnel decisions such as hiring.

That is, individuals prefer working with people like themselves. Might this tendency be

reflected in a desire not to widen existing cultural distances with the hire of a new CEO?

Consequently, we examine whether the departing CEO is more likely to be replaced by an

25

individual of identical nationality, thus maintaining the cultural distances that exist within the

firm.

To examine the possibility of cultural persistence among CEOs, we estimate a set of

transition matrices in Table 7. In Panel A we use our full sample of general turnovers. For 2,668

domestic departing CEOs, 2,011 (75.37%) of them are replaced by domestic successors. Only

657 (24.63%) domestic CEOs are followed by non-domestic CEOs. For non-domestic CEOs,

the persistence is even more pronounced. From a total of 3,775 non-domestic CEOs, 3,376

(89.43%) of them are followed by a non-domestic successor.

In Panels B and C we examine persistence separately for the forced and voluntary

turnover subsamples. Again, we classify a turnover as forced if the age of the departing CEO is

less than 65. We find that successor patterns are qualitatively similar across the two sub-samples.

Both domestic and non-domestic CEOs are more likely to be replaced by a culturally similar

successor. Overall, these initial univariate results reveal a remarkable cultural persistence in the

hiring of CEOs. Boards of directors appear to prefer CEOs who are culturally identical to their

predecessor.

We confirm these findings regarding cultural persistence by formally estimating a linear

probability model with our results contained in Table 8. The dependent variable is a binary

indicator variable that is equal to one if the firm that hires the successor CEO is classified as

domestic after the new hire, and zero if the firm is classified as non-domestic after the turnover.

Column 1 of Table 8 shows that conditioning on a turnover event, a domestic firm is 62.1%

more likely to hire a CEO with a cultural background that is identical to that of the board and

the firm’s country of incorporation. Columns 2 through 5 confirm this finding after controlling

for a various sets of controls and various fixed effects. Overall, Table 8 offers strong evidence

26

of a cultural persistence in CEO succession. We find that the domestic/non-domestic status of

the departing CEO serves as a reliable predictor of the status of the successor CEO. We

conclude from this evidence that there is a significant cultural memory in the CEO succession

process consistent with an affinity effect in executive hiring.

5. Cultural Distance and Firm Value

5.1 Valuation effects of culture

In this section, we investigate the effect of cultural distance on firm valuation. Since we

have established that cultural distance between individuals affects the extent to which they share

mutual understanding and empathy, we expect that cultural distance can influence how the

board or shareholders view the value creation potential of a CEO’s investments and decisions.

To test this relation between cultural distance and firm value, we estimate the following model:

Tobin’s Q i,t = β0 + β1 Domestici,t + CEO & Board controlsi,t + Firm controlsi,t

+ δt + αcountry + ηindustry + ϵi,t , (5)

where the dependent variable is Tobin’s Q for firm i in year t. We define Q value as the ratio

of the market value of the firm to the book value of the firm’s assets. Domestic=1 if the

leadership and cultural wedges are zero for a given year. We include all of the control variables

for the CEO, board, and firm characteristics described in Equation (3). In addition, the model

includes year, country, and industry fixed effects. Standard errors are clustered at the industry

level.

Table 9 reports the results for our analysis of the domestic status on firm value. In Panel

A we provide our regression estimates for cultural distance’s effect on firm value. For columns

27

1-3, the dependent variable is Tobin’s Q of firm i in year t. Column 1 includes controls for CEO

and board characteristics. We observe that the domestic indicator is significantly and inversely

related to a firm’s Q. In column 2, we further control for firm financial and accounting

characteristics. Our results remain robust to these additions. In columns 4 through 6 we use an

industry-adjusted Tobin’s Q as the dependent variable.13 We continue to obtain significantly

negative coefficients for the domestic indicator variable.

Our findings for the domestic indicator variable also have meaningful economic

consequences. For a change from zero to one in the domestic indicator variable, Tobin’s Q

across all firm-years falls by 0.131. For the same change in the domestic indicator, the industry-

adjusted Tobin’s Q, on average, falls by 0.132. These are large effects, given the mean Tobin’s

Q in our sample is 1.828. Based on this average Q value, a coefficient change of -0.131 implies

a 7.17% decline in the firm’s Q. This suggests that reduced executive monitoring due to cultural

affinity can produce large value losses to the firm.

It is possible that domestic firms differ in some way from those that are not domestic and

hence have a cultural wedge. In columns 3 and 6 we introduce firm fixed effects and the

coefficients for the domestic indicator variable remains significantly negative. These findings

suggest that our results are not driven by unobserved heterogeneity.

We further address the selection issue by estimating a Heckman two-stage model. We use

the population of the country in which the firm is head-quartered as our instrument. Our

identifying assumption is that the population of a country in a given year should not be directly

related to how investors value that firm. Panel B of Table 9 reports the results. The first stage

results in columns 1 and 3 show that the probability that a firm hires a domestic CEO increases

13 Since we use industry-adjusted Tobin’s Q, we do not include industry fixed effects in columns 4 and 5. .

28

with a nation’s population. In columns 2 and 4 we show that the coefficient for the domestic

indicator variable in the second stage remains significantly negative after controlling for the

selection probability.

Overall, our findings in Table 9 shows that cultural homogeneity within a firm can

adversely affect firm value. This result implies that the cultural affinity which creates

connections between individuals (e.g., the CEO and the board) results in less effective

monitoring by the board. Because of shared cultural views, directors might be less willing to

challenge or confront their CEO, which can lead to a partial abandonment of their duties of care,

skill, and diligence. We conclude from these findings that greater cultural distance tends to

encourage more effective executive monitoring by the board, and hence can create value for the

firm.

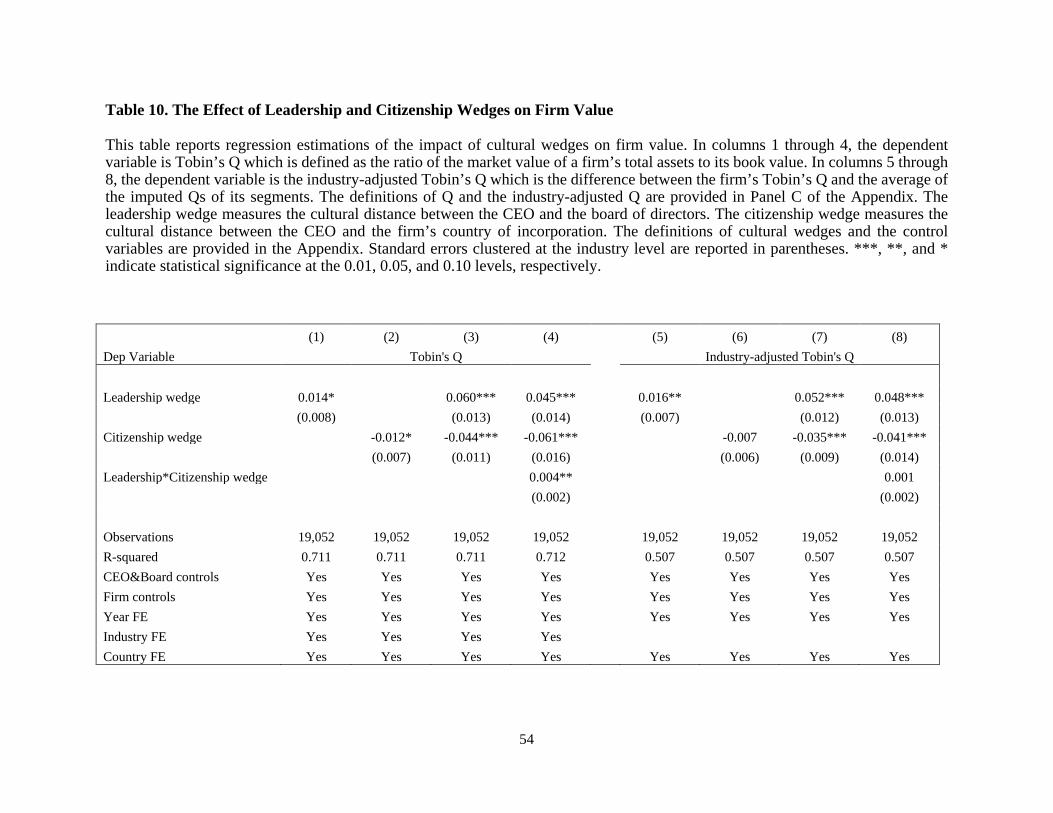

In Table 10, we separately examine the effect of the leadership and citizenship wedges

on corporate value creation. Column 1 shows that Q increases with increases in the leadership

wedge. Column 2 reports an inverse relation between the citizenship wedge and Q. Column 3

includes both cultural wedges and confirms that the leadership wedge is positively associated

with firm value while the citizenship wedge is inversely affects it. The economic consequences

of cultural distance are large. A one-standard-deviation increase in the leadership (citizenship)

wedge is associated with a 0.105 increase (0.106 decline) in Q.

Columns 5 through 8 further test the robustness of this result by using an industry-

adjusted Tobin’s Q as the dependent variable. The results confirm our earlier findings using the

unadjusted Q. That is, we find that firm value is positively related to the leadership wedge, but

inversely related to the citizenship wedge.

29

The result that smaller leadership wedges are associated with a decline in firm value

supports the view that a culturally distant board enhances shareholder value because of more

rigorous monitoring and disciplining of the CEO. Our findings for the citizenship wedge show

that investors prefer CEOs with whom they have greater cultural affinity and this ultimately

results in higher firm valuation. This result is consistent with the findings of Kumar, Niessen-

Ruenzi, and Spalt (2015) who report that fund managers with foreign-sounding names have

lower fund flows relative to those with non-foreign-sounding names.

5.2 Causal regressions

Even though we have previously addressed possible selection bias, it might be that our

results suffer from a reverse causality in the relation between firm value and cultural distance.

It could be that a CEO anticipates a firm’s projected valuation and as a response makes

adjustments in the board’s composition. Thus, the leadership wedge could change in

anticipation of changes in the firm’s future value. It might also be that our measures of cultural

distance reflect the effect of other omitted variables. That is, cultural differences might proxy

for unobserved firm characteristics which influence value.

To address these concerns we use the methodology of Guiso, Sapienza, and Zingales

(2009) and Ahern, Daminello, and Fracassi (2015) and estimate a two-stage least squares

instrumental variable regression using genetic distances as instruments for the leadership and

citizenship wedges. Specifically, we use the probability that two random alleles (DNA

variations) from two populations will be different (Cavalli-Sforze, Menozzi, and Piazza, 1994;

Spolaore and Wacziarg, 2009) as our instrument. Each country pair is assigned with a genetic

distance score and in each firm-year we calculate the average distance between the CEO and

the board based on their nationality. We use this average as the leadership genetic distance to

30

instrument for the leadership wedge. Similarly, we use the genetic distance score between the

CEO and the country where the firm is headquartered as the citizenship genetic distance.

Columns 1 and 2 in Table 11 report the first-stage results for the leadership wedge and

citizenship wedge, respectively. These findings clearly indicate that genetic distances are

significantly correlated with cultural wedges. Therefore, our models do not suffer from a weak

instrument problem. Column 3 reports the second-stage results for our instrumented cultural

wedges where the dependent variable is Tobin’s Q.

These tests further confirm our earlier results of a positive effect by the leadership wedge

and an inverse effect by the citizenship wedge on firm value. Overall, the results of these

regressions support our claim that the relation between cultural distance and firm valuation does

not suffer from reverse causality or an omitted variable.

6. Robustness Analysis and Tests

6.1 Alternative measurement of the cultural wedges

As a robustness test we repeat our analyses regarding turnover and valuation using an

alternative measure of cultural distance. Schwartz (2006) develops a theory of cultural

orientation that centers around seven different cultural values. 14 We use these Schwartz values

instead of Hofstede values to calculate cultural distance by using the same Euclidean approach

as described in Equations (1) and (2). Based on these Schwartz values, we construct two cultural

distances that correspond to our leadership and citizenship wedges.15

14The seven cultural dimensions of Schwartz (2006) are Embeddedness, Harmony, Egalitarian Commitment, Intellectual Autonomy, Affective Autonomy, Mastery, and Hierarchy. 15 Our first cultural distance measure is that between the CEO and the board:

31

The results from this empirical analysis are presented in Table 12. In columns 1-4 of

Panel A, the dependent variable is the CEO turnover indicator. The results confirm our earlier

findings from the Hofstede-based measures and show that cultural distance is a significant

factor in explaining CEO turnover. The likelihood of CEO turnover increases with both the

leadership and citizenship wedges. In columns 5 through 8, we focus exclusively on forced

turnover. Using age 65 as our proxy for forced turnover, we find that the effect of cultural

distance remains strong, both economically and statistically.

In Panel B we test for the relation between cultural distance and firm value to determine

if our previous results are robust to the use of the Schwartz values. Columns 3 and 4 show that

a larger leadership wedge leads to an increased value of Q. A smaller citizenship wedge is

associated with a higher firm value. The coefficient estimates are statistically significant at the

one percent level. Columns 5 through 8 further confirm the robustness of these findings by

using an industry-adjusted measure of Q.

6.2 The effect of domestic firms

Since domestic firms (whose leadership and citizenship wedges are both zero) account

for a large number of firm-year observations in our sample, one possible concern is that our

results might be driven by the presence of domestic firms. To address this possibility, we

exclude all domestic firm-years from our sample and repeat our analyses of CEO turnover and

Schwartz Leadership wedge i,t = ∑𝐾𝐾,𝑡𝑡𝑘𝑘,𝑡𝑡=1 �∑ (𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡 − 𝑆𝑆𝐵𝐵𝐵𝐵𝐵𝐵 𝑖𝑖,𝑘𝑘,ℎ,𝑡𝑡)27

ℎ=1

7 × 𝐾𝐾𝐾𝐾’

where SCEO i,h,t refers to the Schwartz cultural score for a CEO at firm i on cultural dimension h in year t . SBRD i,k,h,t refers to the Schwartz cultural score for director k at firm i on dimension h in year t. Kt is the total number of directors at firm i in year t. The second cultural distance measure is that between CEO and the firm’s country of incorporation:

Schwartz Citizenship wedge i,t = �∑ (𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡 − 𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡)27

ℎ=1

7’

where SCEO i,h,t denotes the Schwartz cultural score for a CEO at firm i on dimension h in year t. SCTYi,h,t refers to the Schwartz cultural score for the country where firm i is headquartered on dimension h in year t.

32

firm valuation on a subsample of firm-years where neither the leadership nor citizenship wedge

is zero. Table 13 shows that our results remain comparable to the baseline regressions as

reported in Tables 4 and 10. Hence, we establish that our earlier conclusions regarding cultural

distance, firm value, and CEO turnover are not attributable to the effect of domestic firms.

7. Summary and Discussion

This study is an innovative examination of the role that national culture has on corporate

decision-making and value. Unlike the many studies that examine culture distance at the macro

level or cross firms (e.g., Guiso, Sapienza, and Zingales, 2006, 2008, 2009; Chui, Titman, and

Wei, 2010; Gorodnichenko and Roland, 2010; Li, Griffin, Yue, and Zhao, 2011; Giannetti and

Yafeh, 2012; Ahern, Daminelli, and Fracassi, 2015), we introduce the simultaneous interaction

of the multiple cultures that operate within a firm. Specifically, we elect to examine what we

believe are the three most important: the CEOs’ culture, that of the board, and that of the firm’s

stakeholders. This view that there are multiple national cultures competing to shape the identity

of the firm is an innovation in the way we think about the issue and the influences brought to

bear on corporate decisions.

To examine how these different cultures interact and influence corporate behaviors, we

measure the distance between them by constructing two measures of cultural distance: (1) the

cultural distance between the CEO and the board, the leadership wedge; and (2) the cultural

distance between the CEO and the firm’s stakeholders, the citizenship wedge. This approach

provides explicit recognition of the fact that there are multiple cultures operating within a firm,

but it is the differences between them that influence the firm. We initially determine that the

extent to which CEOs are culturally near or remote from their boards and stakeholders varies

33

across firms and countries. Further, we discover a remarkable cultural persistence in the hiring

of CEOs across our sample firms.

Overall, we find that cultural distance is critical to our understanding of CEO turnover.

Similarity in cultural orientation between the CEO and the board of directors reduces the

likelihood of CEO turnover, especially in the case of forced turnover. We attribute this to the

greater empathy and acceptance that occurs when there is less cultural distance. Our results

continue to hold even after controlling for turnover-performance sensitivity. We find this result

intuitively appealing since the board has the legal responsibility to both hire and fire the firm’s

executives. We further show that these results are robust to the use of an alternate set of cultural

values developed by Schwartz (2006). In a related analysis, we discover a heretofore unreported

cultural persistence in the hiring of successor CEOs. For our overall sample, 75.37% of CEOs

are replaced by culturally identical individuals.

In our analysis of the relation between cultural distance and firm value, we first find that

a smaller leadership wedge has an adverse effect on firm value. We attribute this result to the

reduced monitoring and discipline that occurs when greater cultural affinity exists between the

CEO and the board. With less oversight of the CEO by the board, it is likely that the agency

costs inherent in the corporate organizational form increase, thus reducing firm value. Secondly,

we find that greater cultural alignment between the CEO and stakeholders increases firm value.

This result is consistent with home bias effects, the cognizance limitations of investors, and the

more accurate processing of executive signals by culturally aligned stakeholders.

We conclude from this study that cultural effects are both present and relevant for

understanding firm behavior and value. There might be a multiplicity of cultures present in the

firm other than the three cultures that we believe are the three most important. More extensive

34

studies can be done to explore the culture of stakeholders with greater granularity, separately

examining the cultural distances between the firm and its stakeholders such as major customers,

suppliers, and transnational regulators. Further research can examine the effect of multiple

cultures on corporate decisions such as investments, capital structure, or dividend payment.

35

Appendix: Variable Definitions

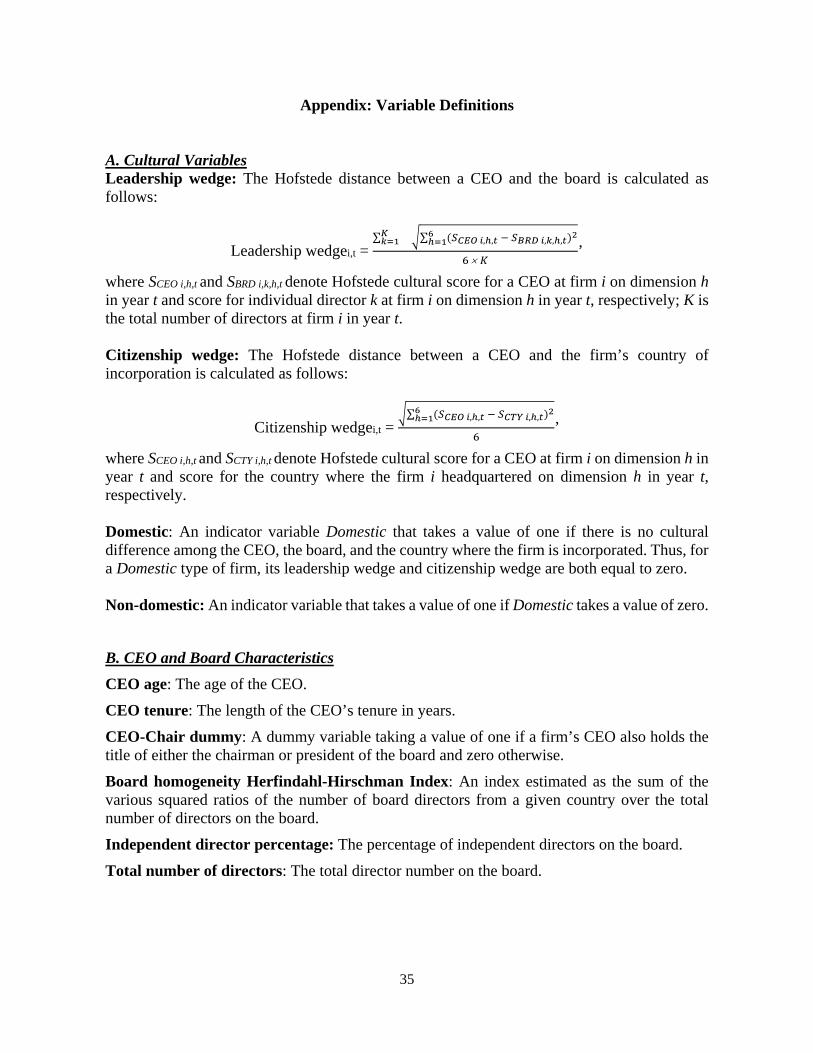

A. Cultural Variables Leadership wedge: The Hofstede distance between a CEO and the board is calculated as follows:

Leadership wedgei,t = ∑𝐾𝐾𝑘𝑘=1 �∑ (𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡 − 𝑆𝑆𝐵𝐵𝐵𝐵𝐵𝐵 𝑖𝑖,𝑘𝑘,ℎ,𝑡𝑡)26

ℎ=1

6 × 𝐾𝐾’

where SCEO i,h,t and SBRD i,k,h,t denote Hofstede cultural score for a CEO at firm i on dimension h in year t and score for individual director k at firm i on dimension h in year t, respectively; K is the total number of directors at firm i in year t. Citizenship wedge: The Hofstede distance between a CEO and the firm’s country of incorporation is calculated as follows:

Citizenship wedgei,t = �∑ (𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡 − 𝑆𝑆𝐶𝐶𝐶𝐶𝐶𝐶 𝑖𝑖,ℎ,𝑡𝑡)26

ℎ=1

6’

where SCEO i,h,t and SCTY i,h,t denote Hofstede cultural score for a CEO at firm i on dimension h in year t and score for the country where the firm i headquartered on dimension h in year t, respectively. Domestic: An indicator variable Domestic that takes a value of one if there is no cultural difference among the CEO, the board, and the country where the firm is incorporated. Thus, for a Domestic type of firm, its leadership wedge and citizenship wedge are both equal to zero. Non-domestic: An indicator variable that takes a value of one if Domestic takes a value of zero.

B. CEO and Board Characteristics CEO age: The age of the CEO. CEO tenure: The length of the CEO’s tenure in years. CEO-Chair dummy: A dummy variable taking a value of one if a firm’s CEO also holds the title of either the chairman or president of the board and zero otherwise. Board homogeneity Herfindahl-Hirschman Index: An index estimated as the sum of the various squared ratios of the number of board directors from a given country over the total number of directors on the board. Independent director percentage: The percentage of independent directors on the board. Total number of directors: The total director number on the board.

36

C. Firm Characteristics Firm age proxy: Retained earnings scaled by total assets (DeAngelo, DeAngelo, and Stulz, 2006). Industry-adjusted EBIT/assets: Earnings before interest and tax adjusted by industry median and scaled by total book assets. Investment: The ratio of capital expenditure (CAPEX) to total assets (AT). Leverage (book): The ratio of the book value of total debt (DLC+DLTT) to the book value of a firm’s total assets (AT). Log(assets): The natural logarithm of the book value of a firm’s total assets (AT). Log(sales): The natural logarithm of the sales over total assets ratio. Tobin’s Q: The ratio of the market value of a firm’s total assets to its book value. The market value of common stock is obtained from the firm’s fiscal year-end stock price and shares outstanding. Preferred stock and debt are assumed to have a market value equal to book value. Replacement cost is estimated from the book value of the firm’s assets. Industry-adjusted Q: Difference between the firm’s Tobin’s q and the asset-weighted average of the imputed Qs of its segments, where a segment’s imputed Q is the industry average q. Industry averages are computed at the most precise SIC level for which a minimum of five single-segment firms in the industry-year is required to be considered in calculation. R&D: The ratio of research and development expense (XRD) to the book value of a firm’s total assets (AT). Specifically, we also construct R&D Full by replacing missing R&D observations with R&D median value, and we create Missing R&D Dummy that takes a value of one if R&D is missing in a given firm-year (see, for example, Koh and Reeb, 2015). ROA: The ratio of operating income before depreciation (OIBDP) to the book value of a firm’s total assets (AT). Stock volatility: The volatility of daily net equity returns in the 12-month period ending at each fiscal year-end. Daily equity returns are obtained from the Compustat Global.

37