66286174 project report on microfinance sector

TRANSCRIPT

1

Microfinance Development Strategy

Self Study Report

Submitted to

Dr. Gyan Prakash

Submitted in partial fulfillment of the requirements for the award of the degree of

Masters of Business Administration

by

Jain Vaibhav

2009MBA-15

ABV Indian Institute of Information Technology and

Management, Gwalior - 474 010, India

2

CONTENTS

1. .Introduction………………………………………………………………………..3

2. Microfinance in the Asian and Pacific Region……………………………………..6

3. Demand for microfinance services………………………………………………….6

4. Supply of microfinance services………………………………………………….....8

5. Emergence of MFIs and the growth of Microfinance Sector in India……………..10

6. Limitation of Government Schemes/Rural Banks ………………………………...12

7. Capacity Building Needs for MFIs………………………………………………...14

8. Women Empowerment through Micro Finance: A Boon for Development……….15

9. Case Study:-SDF Microfinance Methodology……………………………………..24

10. Conclusion and Suggestion…………………………………………………………31

11. References…………………………………………………………………………..32

3

Introduction

Microfinance is the provision of a broad range of financial services such as

deposits, loans, payment services, money transfers, and insurance to poor and low-

income households and, their microenterprises. Microfinance services are provided

by three types of sources:

• Formal institutions, such as rural banks and cooperatives;

• Semiformal institutions, such as nongovernment organizations; and

• Informal sources such as money lenders and shopkeepers.

Institutional microfinance is defined to include microfinance services provided by

both formal and semiformal institutions. Microfinance institutions are defined as

institutions whose major business is the provision of microfinance services.

The interest in microfinance has burgeoned during the last two decades:

multilateral lending agencies, bilateral donor agencies, developing and developed

country governments, and nongovernment organizations (NGOs) all support the

development of microfinance. A variety of private banking institutions has also

joined this group in recent years. As a result, microfinance services have grown

rapidly during the last decade, although from an initial low level, and have come to

the forefront of development discussions concerning poverty reduction. Despite

this growth, as concluded in the recently completed Rural Asia Study, “rural

financial markets in Asia are ill-prepared for the twenty-first century.”1 About 95

percent of some 180 million poor households in the Asian and Pacific Region (the

Region) still have little access to institutional financial services. Development

practitioners, policy makers, and multilateral and bilateral lenders, however,

recognize that providing efficient microfinance services for this segment of the

population is important for a variety of reasons.

(i) Microfinance can be a critical element of an effective poverty reduction trategy.

Improved access and efficient provision of savings, credit, and insurance facilities

n particular can enable the poor to smoothen their consumption, manage their risks

better, build their assets gradually, develop their microenterprises, enhance their

income earning capacity, and enjoy an improved quality of life Microfinance

services can also contribute to the improvement of resource allocation, promotion

of markets, and adoption of better technology; thus, microfinance helps to

promote economic growth and development.

(ii) Without permanent access to institutional microfinance, most poor households

continue to rely on meager self-finance or informal sources of microfinance,3

4

which limits their ability to actively participate in and benefit from the

development opportunities.

(iii) Microfinance can provide an effective way to assist and empower poor omen,

who make up a significant proportion of the poor and suffer disproportionately

from poverty.

(iv) Microfinance can contribute to the development of the overall financial system

through integration of financial markets.

Developing countries in the Region have used microfinance services to reduce

poverty. About 21 percent of the Grameen Bank borrowers and 11 percent of the

borrowers of the Bangladesh Rural Advancement Committee, a microfinance

NGO, managed to lift their families out of poverty within about four years of

participation These services also had a significant positive impact on the depth

(severity) of poverty among the poor. Extreme poverty declined from 33 percent

to 10 percent among Grameen Bank participants, and from 34 percent to 14

percent among Bangladesh Rural Advancement Committee participants. Without

exclusively targeting the poor, the unit desas of the Bank Rakyat Indonesia (BRI)

have also assisted “hundreds of thousands of households in lifting themselves out

of absolute poverty over the past decade.”5 A 1988 sample survey of unit desa

borrowers showed that microcredit has had a major impact on their families'

standards of living. The study estimated that net household incomes of borrowers

increased by about 76 percent and employment increased by 84 percent with three

years of program participation.6 The studies have, in general, shown that

microfinance services have also had a positive impact on specific socioeconomic

variables such as children‟s schooling, household nutrition status, and women‟s

empowerment

Microfinance institutions (MFIs) have also brought the poor, particularly poor

women, into the formal financial system and enabled them to access credit and

accumulate small savings in financial assets, reducing their household poverty.

However, researchers and practitioners generally agree that the poorest of the poor

are yet to benefit from microfinance programs in most countries partly because

most MFIs do not offer products and services that are attractive to this category.8

Thus, to increase the overall impact of microfinance on poverty reduction, it is

essential to extend a wide range of services on a continuing basis to the poor who

are still excluded from the benefits of microfinance.

5

6

Microfinance in the Asian and Pacific Region

Over 900 million people in about 180 million households in the Region live in

poverty. Most of the Region‟s poor (i.e., those who earn less than $1.00 a day) or

more than 670 million people, live in rural areas although urban poverty is also a

growing problem in virtually all DMCs. Most rural poor people are engaged in

agricultural or related activities as laborers or small-scale farmers. Many are also

involved in a variety of microenterprises. In many countries, women, who are a

significant proportion of the poor and suffer disproportionately from poverty,

operate many of these microenterprises.

Most formal financial institutions do not serve the poor because of perceived high

risks, high costs involved in small transactions, perceived low relative profitability,

and inability of the poor to provide the physical collateral usually required by such

institutions. The business culture of these institutions is also not geared to serve

poor and low-income households. Lacking access to institutional sources of

finance, most poor and low-income households continue to rely on meager self-

finance or informal sources of microfinance. However, these sources limit their

ability to actively participate in and benefit from the development process Thus, a

segment of the poor population that has viable investment opportunities persists in

poverty for lack of access to credit at reasonable costs. The poor also lack access to

institutional credit for consumption smoothening and to other services such as

payments, money transfers, and insurance Most of the poor households also find it

difficult to accumulate financial savings without easy access to safe institutions

that provide deposit services.

Demand for microfinance services

The poor and low-income households and their microenterprises in the Region are

a diverse group. Their demand for microfinance services also reflects this diversity

The collective demand of these groups for financial services is large and the types

of services they demand vary across households and microenterprises and over

time.

This large demand and the heterogeneity of services needed across households and

microenterprises and over time have created scope for commercial financial

intermediation. Poor and low-income households and their microenterprises in

the Region have a large demand for safe and convenient deposit services. This

demand reflects the importance of savings for these households and

7

microenterprises for a variety of reasons. The poor need to save for emergencies,

investment, consumption, social obligations, education of their children and many

other purposes. They have the capacity and willingness to save. Savings are

important for microenterprises and provide them with a major source of investment

funds. The large demand for deposit services among the poor is confirmed by

empirical evidence. For example, the number of savings accounts in unit desas of

BRI increased, from 5.0 million in 1988 to 16.1 million in 1996. Most of these

accounts belong to poor households.

The cooperative rural banks in Sri Lanka had 4.7 million deposit accounts at the

end of 1998; while the Association for Social Advancement, a microfinance NGO

in Bangladesh, had over 1.4 million active savings accounts of poor households at

the end of 1999.

Extensive use of informal savings arrangements by poor households is another

indicator of their demand for savings facilities. In some countries, the poor pay

high prices to those providing deposit services. The demand for deposit services is

particularly strong among poor women in the Region.

The demand for microcredit that originates both from households and

microenterprises is also large. Poor households in the Region require microcredit

to finance livelihood activities, for consumption smoothening, and to finance some

lumpy nonfood expenses for purposes such as education (e.g., school fees and

books), housing improvements, and migration. Many Asian countries have

numerous small farms and their operators also require microfinance services. The

other source of demand is nonfarm microenterprises, which cover a wide array of

activities such as food preparation and processing, weaving, pottery, mat and

basket making, furniture making, and petty trading. The demand for other financial

services among poor and low-income households and their microenterprises could

also be significant.

A good share of rural households borrow, many more save, but all seek to insure

against the vagaries of life and therefore the demand for insurance services among

the poor is vast.11 A private insurance company in Bangladesh that started to

provide micro-insurance services to low-income households on a commercial

basis, for example, found that its client base was expanding rapidly. At the end of

1999, this company had over 800,000 clients, about 50,000 of which are

considered poor. This experience shows that the supply of such services creates its

own demand because the real demand for such services remains hidden when

suitable products are not available in the market.

8

Supply of microfinance services

The market structure in microfinance varies significantly across countries in the

Region depending on their stage of financial development, level of economic

development, policy environment, and other factors (Appendix 4). However,

aspects of the supply, particularly about different types of suppliers, may be

usefully discussed.

The microfinance services are supplied mainly by informal sources. Their

collective outreach, both breadth and depth, is vast in most countries. They supply

mainly short-term credit and charge higher interest rates than semiformal and

formal sources. Because of the relatively greater bargaining power enjoyed by the

informal suppliers in general, the terms and conditions under which services are

provided do not enable the clients to fully harness economic opportunities. The

informal sources operate in highly localized areas. Therefore, their contribution to

financial intermediation and improvement of resource allocation is also limited.

For example, informal sources do not allow savings to be collected from more than

a small group of individuals well known to one another, and they do not move

funds over large distances. Most informal insurance mechanisms are typically

weak, particularly against repeated shocks, and often provide only inadequate

protection to poor households. The involvement of formal sources in microfinance

has increased during the last two decades. This greater involvement has stemmed

from

(i) The expansion of the scope of formal institutions into microfinance through

downscaling and establishment of linkage programs with semiformal

sources of different types;

(ii) The emergence of new formal institutions focused on microfinance, such as

the Grameen Bank of Bangladesh;

(iii) Reforms of state-owned financial institutions such as unit desas of BRI;

and

(iv) The introduction of new microfinance programs by the governments

through nonfinancial institutions. However, the formal operations

Formal microfinance has changed to some extent with increasing

. The Bank Dagang Bali in Indonesia has expanded its microfinance operations and

increased its clientele. Badan kredit-desas, owned by Indonesian villagers, now

reach 1.7 million clients, and the Grameen Bank in Bangladesh, owned largely by

its borrower members, operates in over 38,000 villages with 1,140 branches and

reaches about 2.4 million clients.

9

Cooperatives are also playing a significant role as financial intermediaries in the

Region, particularly in India, Sri Lanka, Thailand, and Viet Nam. The thrift and

credit cooperative societies in Sri Lanka reach about 800,000 households while

primary agricultural cooperative societies in India have about 89 million members.

These cooperatives, among other things, provide microfinance services.13 In many

countries, the cooperatives have begun to explore possibilities for deeper

penetration into the microfinance market and show a greater concern about their

financial viability than they did in the 1980s.

A major feature of semiformal microfinance sources in the Region is the extensive

involvement of NGOs. In virtually all DMCs (except for transitional economies

such as the People's Republic of China and Viet Nam) NGOs have become

important providers of microfinance services Their involvement is important

because their clients in general are poorer than those reached by many formal

institutions, their services are targeted in most countries to serve poor women, and

their credit services are provided largely on the basis of social collateral.

The small average loan sizes of NGOs, which usually range from about $30 to

$150 per active loan account, suggest that their clients include the poorest.14

NGOs in some countries are trying to organize themselves into national coalitions

to improve the industry standards and selfregulation. A few NGOs in the Region

have plans to transform themselves into formal financial institutions.

10

Emergence of MFIs and the growth of Microfinance Sector in India

On 12th July 2002, Prime Minister Atal Behari Vajpayee outlined an eight point

agenda to push the economy on a growth path of eight percent during the 10th plan.

Mr. Vajpayee assured that it would be government‟s endeavour to ensure that “ the

poor and the unorganized sector have access to savings, credit and insurance

services”. This statement itself is a great boost to the microfinance sector, as one

can see the changing perception of the people influencing the policies, toward it.

However, it is still a beginning and to make the sector vibrant, the efforts have to

be still on.

Microfinance is being practiced as a tool to attack poverty the world over. The

term “Microfinance” could be defined as “provision of thrift, credit and other

financial services and products of very small amounts to the poor in rural, semi

urban or urban areas, for enabling them to raise their income levels and improve

living standards” (NABARD 99). Microfinance Institutions (MFIs) are those,

which provide thrift, credit and other financial services and products of very small

amounts mainly to the poor in rural, semi-urban or urban areas for enabling them

to raise their income level and improve living standards. Lately, the potential of

MFIs as promising institutions to meet the consumption and micro-enterprise

demands of the poor has been realized..

Credit Demand of the Poor

It is estimated that in India there exist approximately 7.5 crores poor households,

out of which 6 crores are rural and 1.5 crores urban households. One estimate

assumes that the total annual requirement of credit for the rural poor families

would be at least Rs.15, 000 crores on the basis of a maximum need of Rs.2000/-

per family. Another estimate for requirement of credit (excluding housing) is

Rs.50,000 crores assuming that annual average credit usage are Rs.6000/- per rural

household, and Rs.9000/- for poor urban household. An additional Rs.1000 crore is

estimated to be required for housing per year. Apart from micro-credit, they

11

require savings and insurance also. Meanwhile, bank advances to weaker section

aggregated Rs.9700 crore during 1997-98. MFIs and SHGs are estimated to have

provided about 137 crore (cumulative up to September 1998). 1 The above

scenario, suggests a vast unmet gap in the provision of financial services to the

poor. Moreover, 36% of the rural households are found to be outside the fold of

institutional credit.

Growth of microfinance

The growth of microfinance is visible in many aspects. There are more than 2000

NGOs involved in the NABARD SHG-Bank linkage program. Out of these,

approximately 800 NGOs are involved in some form of financial intermediation.

Further, there are 350 new generation co-operatives providing thrift and credit

services. According to our estimate, the present total outstanding , including Sa-

Dhan members and bank linkages is approximately Rs.700 crores (Rs. 150 crores

of Sa-Dhan members and another Rs. 550 crores from the Banking system). The

total client base is estimated at 6-8 million as opposed to the Government of India

(GOI) intention to reach 25 million clients. The growth of community institutions

has taken place with the role to take social and financial intermediation. A numbers

of community banks have come into existence at village and block levels call '

Federation of Self Help Groups'.

The inadequacies of the formal financial system to cater to the needs of the poor

and the realization of the fact that the key to success lies in the evolution and

participation of community based organizations at the grassroots level led to the

emergence of new generation of MFIs.

One kind of MFI is an NGO engaged in promoting Self Help Groups (SHGs) and

their federations at a cluster level and linking SHGs with Banks under the Scheme.

Examples are Myrada in Karnataka, which has promoted Sanghmitra, a company

of its village saving and credit sanghas, PRADAN which has established a large

12

number of SHGs and federated them under Damodar in Bihar, Sakhi Samiti in

Rajasthan.

Another kind is NGO-MFI directly lending to the poor borrowers, who are either

organized into SHGs or into Grameen Bank type of groups after borrowing bulk

funds from SIDBI, RMK and FWWB. Examples in this category are Rashtriya

Gramin Vikas Nidhi (RGVN) which runs credit and savings programme in Assam

and Orissa on the lines of Grameen Bank, Bangladesh. Also we have SHARE in

AP, ASA in Tamil Nadu under this category.

There are MFIs which are specifically organized as cooperatives, such as over 500

Mutually Aided Cooperative Thrift and Credit Socities (MACTS) in AP, promoted

among others by Cooperative Development Foundation (CDF) and the SEWA

Bank in Gujarat which also runs federations of SHGs in nine districts.

Then we have MFIs, which are organize as Non-Banking Finance Companies

(NBFC) such as BASIX, CFTS Mirzapur, SHARE Microfin. Ltd and Sarvodaya

Nanofinance Ltd.

Limitation of Government Schemes/Rural Banks

In India, numerous government schemes have tried to provide various subsidized

services to the poor households. However, various studies have exposed the

limitation of these programs, showing the lack of access of mainstream financial

services for these poor households and their over-dependence on the local

moneylenders in meeting their consumption and micro-enterprise demands.

According to an estimate, only 16% credit usage was met by the formal sources,

while the remaining 84% was met by the informal services. Despite having a wide

network or rural bank branches in the country and implementation of many credit

linked poverty alleviation programmes, a large number of the very poor continue to

13

remain outside the fold of the formal banking system. Various studies also

suggested that the policies, systems and procedures and the saving and loan

products often did not meet the needs of the very poor. NABARD refinances the

microfinance sector loans by banks, but doesn‟t undertake direct financing. Thus,

its ability to promote innovations or establish any “missing link” units is very

limited. Small Industries Development Bank of India (SIDBI) mainly uses the

network of State Financial Corporations (SFCs) and commercial banks to extend

microfinance sector loans in rural small towns. It also faces the same constraint.

State Financial Corporations (SFCs) largely concentrate on the upper end of SSIs

and that too in urban areas. However, through their district branches, a small

proportion of lending is done to the microfinance sector. hey Their lengthy and

stringent procedures inhibit the poor. Regional Rural Banks (RRBs) are located in

rural areas, have low CD ratio but are suffering immensely from lack of skills,

incentives and infrastructure support. As can be seen from above, while there is no

dearth of institutions and branch network in urban and rural areas, this physical

outreach does not translate into access to credit by microfinance sector producers.

However, wherever mainstream finance institutions are engaged in financing small

borrowers, their experience is characterized by a number of factors. Their

institutional design and mandate, which determines their procedures, do not suit

the poor. The poor find their procedures cumbersome, complicated and unsuitable

for the local environment.. They have also failed to provide a mix of credit for both

consumption and productive loans. Therefore poor feel alienated in dealing with

them. They feel scared to go to them. Repeat loans, except for crop production are

rare, even for the borrowers who have repaid fully. Further, even though the many

of the loans extended to the poor by the public sector financial institutions are

subsidized, their ultimate cost to the borrowers is high which includes payments to

the middle men, wage and business loss due to time spent in getting the loans

approved.

14

Capacity Building Needs for MFIs

It has been observed that, MFIs are able to reach the poor effectively mainly

because they have designed products and channels, which are friendly and suitable

to the need of the poor. However, MFIs outreach is limited in comparison with the

mainstream financial institutions because of the shortage of financial and human

resources. MFIS need grants to build their own capacity as well as that of the

borrowers or SHGs. A vast majority of MFIs are NGOs registered under the

Societies Act or Trust Act, and they cannot mobilize large amount of lending funds

due to the inappropriate legal and financial structure. A few MFIs which have

registered as Non-Banking Finance Companies (NBFCs) are able to mobilize

equity from development financial institutions and leverage these with borrowing

from commercial banks. However, the regulatory framework is not conducive for

these MFIs.

Unfortunately, in India the dominant reform agenda of the mainstream sector

clouds the reform and attention that is required at the bottom end. The past few

years though has seen an appreciable increase and support to this problem. The

present economic advisory team under the leadership of the Prime minister though

(PMO) has brought increasing focus to this problem and a group has been

constituted to deal with these problems.

Sa-Dhan, The Association of Community Development Finance Institutions

(biggest Apex body of Microfinance Institutions in India) had been asking the

Government of India to make more funds available for the capacity building of the

microfinance sector. Though locked into bureaucratic procedures, some of these

funds have been made available. Hence, the need for capacity building of NGOs on

one hand and the capacity building of local communities on the other hand is

needed to ensure effective management. In this context, if the Microfinance

Development Fund (MFDF) of 430 crores is not released in the immediate future,

it will culminate into disaster for the microfinance sector.

15

Women Empowerment Through Micro Finance: A Boon for Development

Under the trickle down theory in the planning process it was expected that women

will equally benefit along with men. This has been belied by actual

developmement. The ninth plan document recognizes that inspite of development

measures and constitutional legal guarantees- women have lagged behind in almost

all sectors.

In India, the emergence of liberalization and globalization in early 1990‟s

aggravated the problem of women workers in unorganized sectors from bad to

worse asmost of the women who were engaged in various self employment

activities have lost their livelihood. Despite in tremendous contribution of women

to the agriculture sector, their work is considered just an extension of household

domain and remains non-monetised.

Microfinance is emerging as a powerful instrument for poverty alleviation in the

new economy. In India, Microfinance scene is dominated by Self Help Group

(SHGs)-Bank Linkage Programme as a cost effective mechanism for providing

financial services to the “Unreached Poor” which has been successful not only in

meeting financial needs of the rural poor women but also strengthen collective self

help capacities of the poor ,leading to their empowerment. Rapid progress in SHG

formation has now turned into an empowerment movement among women across

the country.

Economic empowerment results in women‟s ability to influence or make decision,

increased self confidence, better status and role in household etc. Micro finance is

necessary to overcome exploitation, create confidence for economic self reliance of

the rural poor, particularly among rural women who are mostly invisible in the

social structure.

This paper puts forward how micro finance has received extensive recognition as a

strategy for economic empowerment of women. This paper seeks to examine the

impact of Micro finance with respect to poverty alleviation and socioeconomic

empowerment of rural women. An effort is also made to suggest the ways to

increase

16

Empowerment is a multi-dimensional social process that helps people gain control

over their own lives communities and in their society, by acting on issues that they

define as important. Empowerment occurs within sociological psychological

economic spheres and at various levels, such as individual, group and community

and challenges our assumptions about status quo, asymmetrical power relationship

and social dynamics. Empowering women puts the spotlight on education and

employment which are an essential element to sustainable development.

EMPOWERMENT: FOCUS ON POOR WOMEN

In India, the trickle down effects of macroeconomic policies have failed to resolve

the problem of gender inequality. Women have been the vulnerable section of

society and constitute a sizeable segment of the poverty-struck population. Women

face gender specific barriers to access education health, employment etc. Micro

finance deals with women below the poverty line. Micro loans are available solely

and entirely to this target group of women. There are several reason for this:

Among the poor , the poor women are most disadvantaged –they are characterized

by lack of education and access of resources, both of which is required to help

them work their way out of poverty and for upward economic and social mobility.

The problem is more acute for women in countries like India, despite the fact that

women‟s labour makes a critical contribution to the economy. This is due to the

low social status and lack of access to key resources. Evidence shows that groups

of women are better customers than men, the better managers of resources. If loans

are routed through women benefits of loans are spread wider among the household.

Since women‟s empowerment is the key to socio economic development of the

community; bringing women into the mainstream of national development has

been a major concern of government. The ministry of rural development has

special components for women in its programmes. Funds are earmarked as

“Women‟s component” to ensure flow of adequate resources for the same. Besides

17

Swarnagayanti Grameen Swarazgar Yojona (SGSY), Ministry of Rural

Development is implementing other scheme having women‟s component .They are

the Indira Awas Yojona (IAJ), National Social Assistance Programme (NSAP),

Restructured Rural Sanitation Programme, Accelerated Rural Water Supply

programme (ARWSP) the (erstwhile) Integrated Rural Development Programme

(IRDP), the (erstwhile) Development of Women and Children in Rural Areas

(DWCRA) and the Jowahar Rozgar Yojana (JRY).

The term micro finance is of recent origin and is commonly used in addressing

issues related to poverty alleviation, financial support to micro entrepreneurs,

gender development etc. There is, however, no statutory definition of micro

finance. The taskforce on supportitative policy and Regulatory Framework for

Microfinance has defined microfinance as “Provision of thrift, credit and other

financial services and products of very small amounts to the poor in rural, semi-

urban or urban areas for enabling them to raise their income levels and improve

living standards”. The term “Micro” literally means “small”. But the task force has

not defined any amount. However as per Micro Credit Special Cell of the Reserve

Bank Of India , the borrowal amounts upto the limit of Rs.25000/- could be

considered as micro credit products and this amount could be gradually increased

up to Rs.40000/- over a period of time which roughly equals to $500 – a standard

for South Asia as per international perceptions.

The term micro finance, sometimes is used interchangeably with the term micro

credit. However while micro credit refers to purveyance of loans in small

quantities, the term microfinance has a broader meaning covering in its ambit other

financial services like saving, insurance etc. as well.

The mantra “Microfinance” is banking through groups. The essential features of

the approach are to provide financial services through the groups of individuals,

formed either in joint liability or co-obligation mode. The other dimensions of the

microfinance approach are:

18

- Savings/Thrift precedes credit

- Credit is linked with savings/thrift

- Absence of subsidies

-Group plays an important role in credit appraisal, monitoring and recovery.

Basically groups can be of two types:

Self Help Groups (SHGs) : The group in this case does financial intermediation on

behalf of the formal institution. This is the predominant model followed in India.

Grameen Groups: In this model, financial assistance is provided to the individual

in a group by the formal institution on the strength of group‟s assurance. In other

words, individual loans are provided on the strength of joint liability/co obligation.

This microfinance model was initiated by Bangladesh Grameen Bank and is being

used by some of the Micro Finance Institutions (MFIs) in our country.

WOMEN’S EMPOWERMENT AND MICRO FINANCE: DIFFERENT

PARADIGMS

Concern with women‟s access to credit and assumptions about contributions to

women‟s empowerment are not new. From the early 1970s women‟s movements in

a number of countries became increasingly interested in the degree to which

women were able to access poverty-focused credit programmes and credit

cooperatives. In India organizations like Self- Employed Women‟s Association

(SEWA) among others with origins and affiliations in the Indian labour and

women‟s movements identified credit as a major constraint in their work with

informal sector women workers.

19

The problem of women‟s access to credit was given particular emphasis at the first

International Women‟s Conference in Mexico in 1975 as part of the emerging

awareness of the importance of women‟s productive role both for national

economies, and for women‟s rights. This led to the setting up of the Women‟s

World Banking network and production of manuals for women's credit provision.

Other women‟s organizations world-wide set up credit and savings components

both as a way of increasing women‟s incomes and bringing women together to

address wider gender issues. From the mid-1980s there was a mushrooming of

donor, government and NGO-sponsored credit programmes in the wake of the

1985 Nairobi women‟s conference (Mayoux, 1995a).

The trend was further reinforced by the Micro Credit Summit Campaign starting in

1997 which had „reaching and empowering women‟ as it‟s second key goal after

poverty reduction (RESULTS 1997). Micro-finance for women has recently been

seen as a key strategy in meeting not only Millennium Goal 3 on gender equality,

but also poverty Reduction, Health, HIV/AIDS and other goals.

C

POVERTY REDUCTION PARADIGM

The poverty alleviation paradigm underlies many NGO integrated poverty-targeted

community development programmes. Poverty alleviation here is defined in

broader terms than market incomes to encompass increasing capacities and choices

and decreasing the vulnerability of poor people.

The main focus of programmes as a whole is on developing sustainable

livelihoods, community development and social service provision like literacy,

healthcare and infrastructure development. There is not only a concern with

reaching the poor, but also the poorest.

Policy debates have focused particularly on the importance of small savings and

loan provision for consumption as well as production, group formation and the

possible justification for some level of subsidy for programmes working with

particular client groups or in particular contexts7. Some programmes have

20

developed effective methodologies for poverty targeting and/or operating in remote

areas. Such strategies have recently become a focus of interest from some donors

and also the Microcredit Summit Campaign.

Here gender lobbies have argued for targeting women because of higher levels of

female poverty and women‟s responsibility for household well-being. However

although gender inequality is recognised as an issue, the focus is on assistance to

households and there is a tendency to see gender issues as cultural and hence not

subject to outside intervention.

Although term 'empowerment' is frequently used in general terms, often

synonymous with a multi-dimensional definition of poverty alleviation, the term '

women's empowerment ' is often considered best avoided as being too

controversial and political. The assumption is that increasing women‟s access to

micro-finance will enable women to make a greater contribution to household

income and this, together with other interventions to increase household well-

being, will translate into improved well-being for women and enable women to

bring about wider changes in gender inequality.

FINANCIAL SUSTAINABILITY PARADIGM

The financial self-sustainability paradigm (also referred to as the financial systems

approach or sustainability approach) underlies the models of microfinance

promoted since the mid-1990s by most donor agencies and the Best Practice

guidelines promoted in publications by USAID, World Bank, UNDP and CGAP.

The ultimate aim is large programmes which are profitable and fully self-

supporting in competition with other private sector banking institutions and able to

raise funds from international financial markets rather than relying on funds from

development agencies. The main target group, despite claims to reach the poorest,

is the „bankable poor': small entrepreneurs and farmers. This emphasis on financial

21

sustainability is seen as necessary to create institutions which reach significant

numbers of poor people in the context of declining aid budgets and opposition to

welfare and redistribution in macro-economic policy.

Policy discussions have focused particularly on setting of interest rates to cover

costs, separation of micro-finance from other interventions to enable separate

accounting and programme expansion to increase outreach and economies of scale,

reduction of transaction costs and ways of using groups to decrease costs of

delivery. Recent guidelines for CGAP funding and best practice focus on

production of a „financial sustainability index‟ which charts progress of

programmes in covering costs from incomes.

MICRO FINANCE INSTRUMENT FOR WOMEN’S EMPOWERMENT

Micro Finance is emerging as a powerful instrument for poverty alleviation in the

new economy. In India, micro finance scene is dominated by Self Help Groups

(SHGs) – Bank Linkage Programme, aimed at providing a cost effective

mechanism for providing financial services to the “unreached poor”. Based on the

philosophy of peer pressure and group savings as collateral substitute , the SHG

programme has been successful in not only in meeting peculiar needs of the rural

poor, but also in strengthening collective self-help capacities of the poor at the

local level, leading to their empowerment.

Micro Finance for the poor and women has received extensive recognition as a

strategy for poverty reduction and for economic empowerment. Increasingly in the

last five years , there is questioning of whether micro credit is most effective

approach to economic empowerment of poorest and, among them, women in

particular. Development practitioners in India and developing countries often argue

that the exaggerated focus on micro finance as a solution for the poor has led to

neglect by the state and public institutions in addressing employment and

livelihood needs of the poor.

22

Credit for empowerment is about organizing people, particularly around credit and

building capacities to manage money. The focus is on getting the poor to mobilize

their own funds, building their capacities and empowering them to leverage

external credit. Perception women is that learning to manage money and rotate

funds builds women‟s capacities and confidence to intervene in local governance

beyond the limited goals of ensuring access to credit. Further, it combines the goals

of financial sustainability with that of creating community owned institutions.

Before 1990‟s, credit schemes for rural women were almost negligible. The

concept of women‟s credit was born on the insistence by women oriented studies

that highlighted the discrimination and struggle of women in having the access of

credit. However, there is a perceptible gap in financing genuine credit needs of the

poor especially women in the rural sector.

There are certain misconception about the poor people that they need loan at

subsidized rate of interest on soft terms, they lack education, skill, capacity to save,

credit worthiness and therefore are not bankable. Nevertheless, the experience of

several SHGs reveal that rural poor are actually efficient managers of credit and

finance. Availability of timely and adequate credit is essential for them to

undertake any economic activity rather than credit subsidy.

The Government measures have attempted to help the poor by implementing

different poverty alleviation programmes but with little success. Since most of

them are target based involving lengthy procedures for loan disbursement, high

transaction costs, and lack of supervision and monitoring. Since the credit

requirements of the rural poor cannot be adopted on project lending app roach as it

is in the case of organized sector, there emerged the need for an informal credit

supply through SHGs. The rural poor with the assistance from NGOs have

demonstrated their potential for self help to secure economic and financial

23

strength. Various case studies show that there is a positive correlation between

credit availability and women‟s empowerment.

CHALLENGING ECONOMIC EMPOWERMENT

However impact on incomes is widely variable. Studies which consider income

levels find that for the majority of borrowers income increases are small, and in

some cases negative. All the evidence suggests that most women invest in existing

activities which are low profit and insecure and/or in their husband‟s activities. In

many programmes and contexts it is only in a minority of cases that women can

develop lucrative activities of their own through credit and savings alone.

It is clear that women‟s choices about activity and their ability to increase incomes

are seriously constrained by gender inequalities in access to other resources for

investment, responsibility for household subsistence expenditure, lack of time

because of unpaid domestic work and low levels of mobility, constraints on

sexuality and sexual violence which limit access to markets in many cultures.

These gender constraints are in addition to market constraints on expansion of the

informal sector and resource and skill constraints on the ability of poor men as well

as women to move up from survival activities to expanding businesses. There are

signs, particularly in some urban markets like Harare and Lusaka, that the rapid

expansion of micro-finance programmes may be contributing to market saturation

in „female‟ activities and hence declining profits.

24

CASE STUDY:-

SDF Microfinance Methodology

1 Delivery Model

Sita Devi Foundation(SDF) is following a Joint Liability Group (JLG) lending

methodology for its microfinance programme. The clients was organized in groups

of five to form Joint Liability Groups (JLGs). These JLGs was further organized

in centers (1-centre comprised of 2-JLGs) for effective administration of the

groups. The JLGs meet regularly on weekly basis at a scheduled time and place

for collection of installments. A Credit Officer (CO) from the Branch Office

come to JLG meetings for conducting meeting and collection of loan installments.

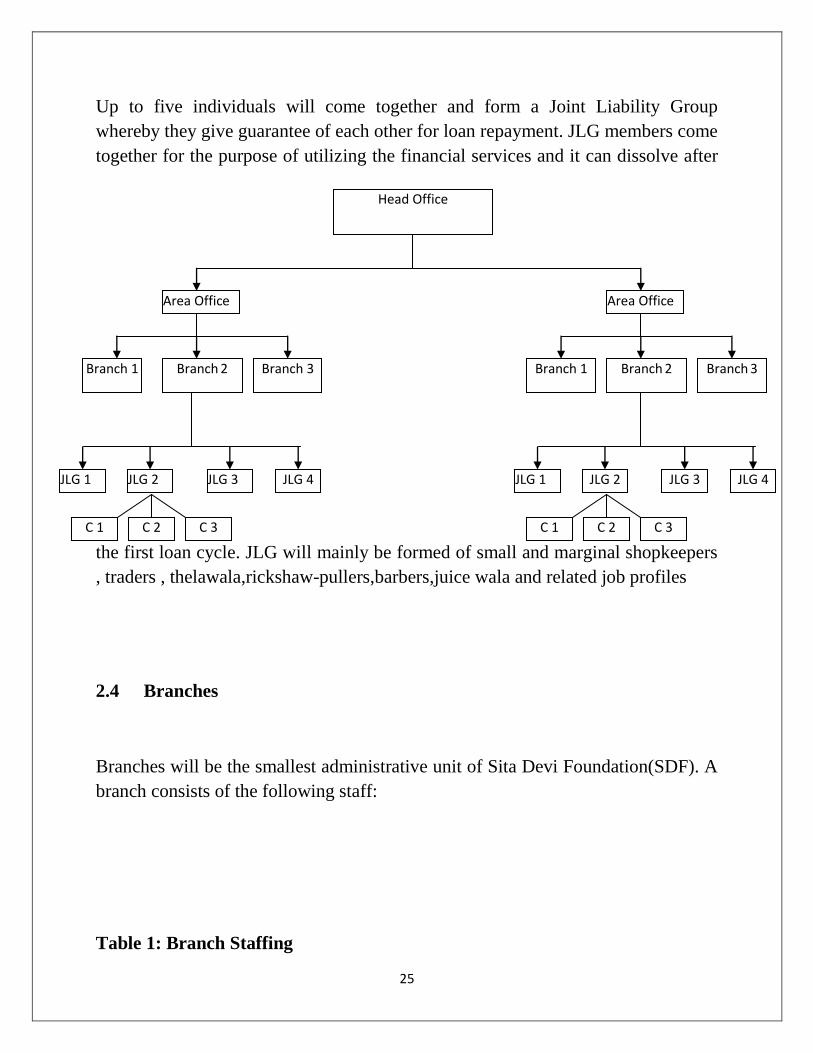

2 Operational Structure

The operational structure defines the different units in the delivery models of Sita

Devi Foundation(SDF). Sita Devi Foundation(SDF) presently operate through 1-

branch. The description of the different units in the operational structure of Sita

Devi Foundation(SDF) is given below: (Chart 1 on the shows the operational

structure of Sita Devi Foundation‟ microfinance operations.)

2.1 Clients

A client is someone who agrees to join Sita Devi Foundation(SDF) and abides by

its rules and regulations. He/she will also become a member a JLG affiliated to Sita

Devi Foundation(SDF). Clients are entitled to use the services of Sita Devi

Foundation(SDF) as per its terms and conditions.

2.2 Joint Liability Group (JLG)

25

Up to five individuals will come together and form a Joint Liability Group

whereby they give guarantee of each other for loan repayment. JLG members come

together for the purpose of utilizing the financial services and it can dissolve after

the first loan cycle. JLG will mainly be formed of small and marginal shopkeepers

, traders , thelawala,rickshaw-pullers,barbers,juice wala and related job profiles

2.4 Branches

Branches will be the smallest administrative unit of Sita Devi Foundation(SDF). A

branch consists of the following staff:

Table 1: Branch Staffing

C 1 C 2 C 3

JLG 1 JLG 3 JLG 4 JLG 2

Head Office

Branch 1 Branch 2 Branch 3

Area Office

Branch 1 Branch 2 Branch 3

Area Office

C 1 C 2 C 3

JLG 1 JLG 3 JLG 4 JLG 2

26

Designation No Responsibilities

Branch Manager 1

All administrative responsibilities

Loan approvals

Target setting and their achievements

Monitoring of Credit Officers

Reporting to the Head Office/Area

Office

Branch

Accountant

(one of the

Credit Officer)

1

Preparation of books of accounts

Preparation of MIS reports

Budgets and variance analysis

Reconciliation of collected amount

Credit Officers 6-8

Formation of JLGGs and their training

Sourcing of loan applications and

preliminary appraisal

Disbursement of loans

Collection of installments

A branch will cater to around 3,000 clients. A branch will have an operational area

of a maximum of 5-8 kilometers.

2.5 Area Offices/Regional Offices

Each Area/Regional Office in future will look after a maximum of eight branches.

Only one Regional Manager and possibly an accountant will man each Area

Office. The responsibility of the Area/Regional Office will be to monitor the

branches and consolidate the reports produced by the Branch Offices to send these

reports further to the Head Office. It is not necessary to have a separate structure

for the Area Office. The Area Office could be based in one of the branches.

2.6 Head Office

27

The Head Office of Sita Devi Foundation(SDF) is based in Delhi. The Head Office

coordinate the functions of all the branches. More specifically the Head Office

perform the following functions:

1. Funds mobilization

2. Financial management

3. Coordinating with the Board of Directors

4. Product development

5. Systems development

6. Internal audit

7. Setting budgets and performing variance analysis

8. Human resource management including trainings

9. Performance management of the Branch as well as new branch opening

Considering the wide variety of functions performed by the Head Office, we are

planning it to divide into different departments. Various departments and their

functions have been shown in the following table. The structure of different

departments will evolve as the scale of operations increases.

These departments will function in coordination with each other through formal

and informal interactions. Initially, the functions of many of these departments will

be combined but with increase in the scale of operations, all these departments will

be separated with a separate head of department for each.

Table 4: Departments and Functions

Department Functions

Finance

Preparation and finalization of books of accounts

Preparation of funding proposals

Negotiation with lenders and investors

Business Planning

Budgets and variance analysis

28

Treasury management

Statutory compliance and reporting

MIS

Collection of reports from the branches

Consolidation

Storage and dissemination of information

Preparation of IT strategy

Purchase and maintenance of hardware

Software development and maintenance

Operations

Formulation of operational strategy

Branch opening

Target setting for branches and other staff

Monitoring of branches and staff as well as

operational reporting

Human

Resources &

Administration

Preparation of HR strategy

Recruitments and training

Payroll accounting

Performance appraisal

Administration

Purchases

Maintenance of fleet

Liaison

Estate management

Internal Audit Audit financial transactions

Audit of non-financial transactions

Review of internal controls

Procedures of group formation, disbursement and collection of loans

Group formation

Sita Devi Foundation(SDF) follows the JLG methodology. Groups made up of 5

individuals. Once an area has been chosen a credit officer and Branch Manager

go to the field and conduct a general meeting. In the general meeting they explain

Sita Devi Foundation(SDF), its products and methods to the people. The Branch

Manager ask the people to form into groups for the next scheduled meeting. For

the second meeting in the field the credit officer go alone. The credit officer

explain the training and finalize groups. Training is then conducted and group

29

members are asked if they accept the group joint liability. If liability is not

accepted the group was disbanded and the process begin again.

Group Recognition Test

Once the training is completed, a test is administered. All group members must be

present for the test to be administered. If a member is missing then the test is

cancelled and rescheduled. The test ensures members have an adequate grasp of

the loan program. A 100% pass percentage is required for a group to join the

microfinance, if there isn‟t a 100% pass rate, the group receives further training

and retake the test. Since the credit officer is the person responsible for the

training, he/she is not allowed to administer the verbal test. The Branch Manager

questions the group on loan specifics as well as the concept of joint liability. The

Branch Manager ensure that each member of the group has participated in the

questioning. He/she must also question the group members on the purpose of their

loan and if these responses match the group verification form.

Loan Application Process

The Credit Officer collects photographs and proof of addresses from each member

to begin the loan application process. If a member is missing any of the documents

the process is cancelled. This enforces the joint liability concept and method. A

family member is then asked to sign the application form. (Other arrangements

can be made in extenuating circumstances for example as in the case of a widow

living alone.) The loan form and group resolution are then filled out. All

documents are then sent for processing.

Loan Disbursement Process

Finally the loans are ready for disbursement. The Branch Manager personally

disbursed the laon at Branch Office to all members of JLG. Once again as before

if all members are not present the meeting will be cancelled. A promissory note is

signed by all members for the loan amounts attesting to their liability. Then loan

cards(pass book) cards are disbursed along with funds. Each Client receives one

passbook mentioning all the details of laon disbursed and their loan repayment

30

schedule. The loan card/pass book will be notated and signed upon each payment.

The loan card/passbook is for the clients records.

Loan Collection Process

Lastly is the collection process. During regular group meetings, members will

decide on loan disbursements and provide payments to the credit officer. The

meetings allows for members to discuss any issues or problems they may be

facing. It also allows the credit officer to discuss any bad debt and the general

progress of the group‟s portfolio. The credit officer will take attendance and

collect cash. Any cash that is short or late must be collected from the other

members

CONCLUSIONS AND SUGGESTIONS

Numerous traditional and informal system of credit that were already in existence

before micro finance came into vogue. Viability of micro finance needs to be

understood from a dimension that is far broader- in looking at its long-term aspects

too .very little attention has been given to empowerment questions or ways in

which both empowerment and sustainability aims may be accommodated. Failure

to take into account impact on income also has potentially adverse implications for

both repayment and outreach, and hence also for financial sustainability. An effort

is made here to present some of these aspects to complete the picture.

31

References

1. Asian Development Bank (ADB). 2000. Rural Asia Study: Beyond the Green Revolution.

Manila: ADB

2. In T. Fisher & M.S. Sriram (Eds.), Beyond micro-credit: Putting development back into micro-

finance

3. Klaus, M. E. (1999). Report of working group on savings mobilization, Bank Rakyat

Indonesia (BRI).

4. Rhyne, E. (2001). Mainstreaming microfinance. Connecticut: Kumarian Press

5. Robinson, M. (2001). The microfinance revolution: Sustainable finance for the poor

6. Sinha, S. (2001). The role of central banks in microfinance in Asia and the Pacific.

Manila: Asian Development Bank

7. Yunus, M. (2003). Some suggestions on legal framework for creating microcredit banks.

Dhaka: Grameen Bank. Journal of Microfinance 112 Volume

32