5 non-bank financial intermediaries

DESCRIPTION

pb303 politeknikTRANSCRIPT

NON-BANK FINANCIAL INTERMEDIARIES

CHAPTER 5

snurazani/DIS12

• The key players within this segment of the financial system are pension and provident funds, insurance companies and development financial institutions.

• Non-bank financial intermediaries (NBFIs) can be broadly classified into five groups of institutions, namely: – Development Financial Intermediaries

– Saving Institutions

– Employees Provident And Pension Funds,

– Insurance Companies (Including Takaful),

– Other Financial Intermediaries

• Factoring Companies

• Leasing companies

• Unit trusts

• Cagamas

• Credit Institutions,

• Credit Assurance Companies

INTRODUCTION

snurazani/DIS12

snurazani/DIS12

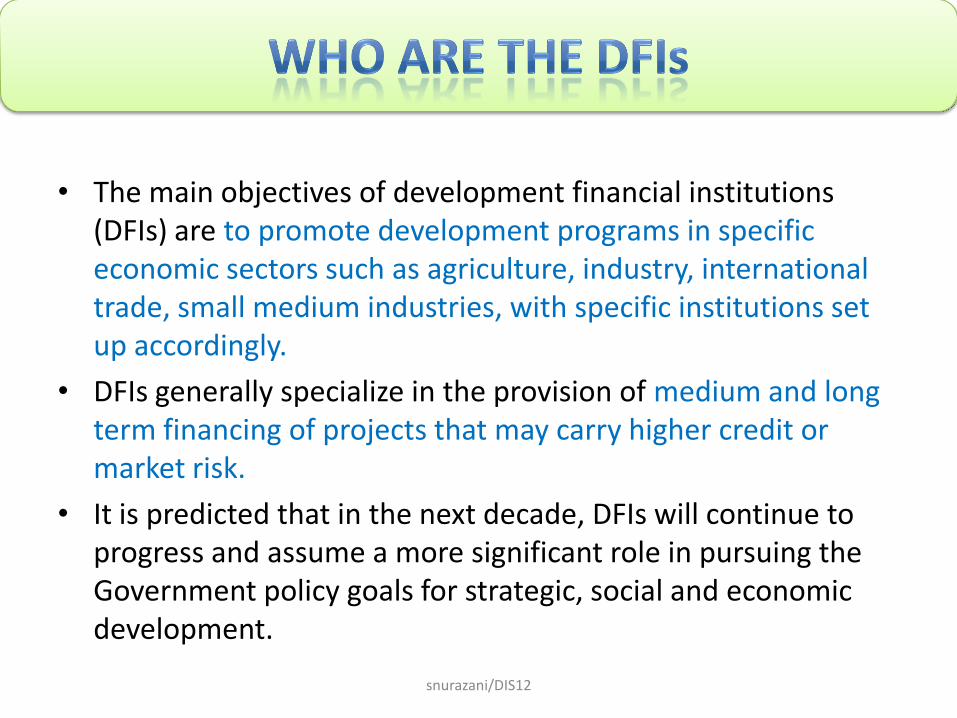

• The main objectives of development financial institutions (DFIs) are to promote development programs in specific economic sectors such as agriculture, industry, international trade, small medium industries, with specific institutions set up accordingly.

• DFIs generally specialize in the provision of medium and long term financing of projects that may carry higher credit or market risk.

• It is predicted that in the next decade, DFIs will continue to progress and assume a more significant role in pursuing the Government policy goals for strategic, social and economic development.

snurazani/DIS12

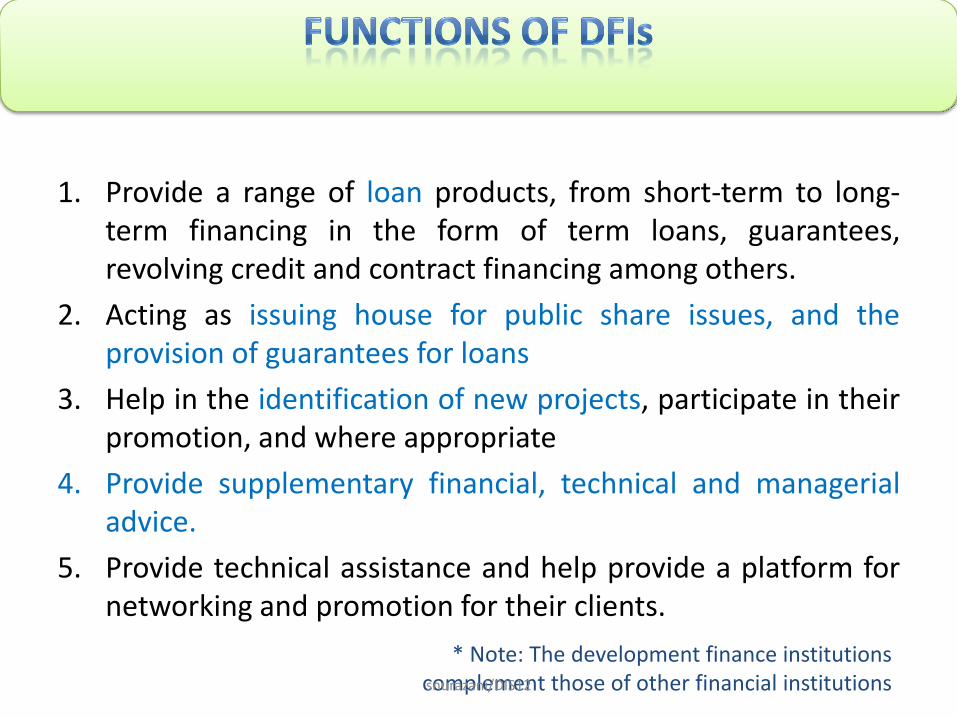

1. Provide a range of loan products, from short-term to long-term financing in the form of term loans, guarantees, revolving credit and contract financing among others.

2. Acting as issuing house for public share issues, and the provision of guarantees for loans

3. Help in the identification of new projects, participate in their promotion, and where appropriate

4. Provide supplementary financial, technical and managerial advice.

5. Provide technical assistance and help provide a platform for networking and promotion for their clients.

* Note: The development finance institutions complement those of other financial institutions snurazani/DIS12

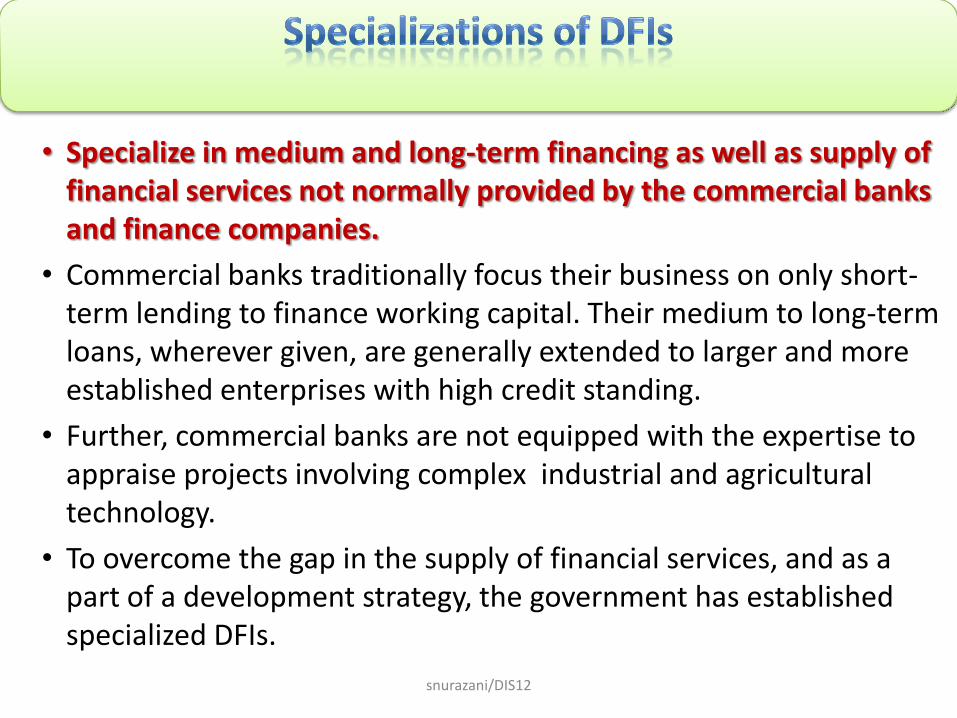

• Specialize in medium and long-term financing as well as supply of financial services not normally provided by the commercial banks and finance companies.

• Commercial banks traditionally focus their business on only short-term lending to finance working capital. Their medium to long-term loans, wherever given, are generally extended to larger and more established enterprises with high credit standing.

• Further, commercial banks are not equipped with the expertise to appraise projects involving complex industrial and agricultural technology.

• To overcome the gap in the supply of financial services, and as a part of a development strategy, the government has established specialized DFIs.

snurazani/DIS12

Bank Pembangunan & Infrastruktur Malaysia Berhad

• The main activity to be the premier financial institution in providing financial facilities to Bumiputeras in the manufacturing sector, services-related industries in the manufacturing sector and also financing the country’s main infrastructure projects.

Malaysian Industrial Development Finance (MIDF)

• MIDF was set up in 1960 and is a semi-government institution providing medium and long-term loans to manufacturing industries in Malaysia.

• promotes the development of the industrial sector in Malaysia through the provision of financing for manufacturing-based and services-based small and medium enterprises.

• The division’s financing products which are generally for the medium-to-long term, include project, machinery, factory mortgage and working capital term loans; industrial higher purchase and leasing facilities to finance acquisition of machinery and equipment as well as revolving credit and factoring facilities for working capital purposes.

* Note: The development finance institutions complement those of other financial institutions snurazani/DIS12

• Malaysian Industrial Development Finance (MIDF)

• Bank Pembangunan & Infrastruktur Malaysia Berhad formely known as Bank Pembangunan Malaysia

• Bank Industri Malaysia Berhad

• Bank Pertanian Malaysia formely known as Agro Bank

• EXIM Bank

• SME Bank

• Borneo Development Corporation

• Sabah Development Bank

• Sabah Credit Corporation

snurazani/DIS12

snurazani/DIS12

• SIs are also complement the commercial banks and finance companies as the major deposit-taking institutions.

• It promote and mobilize savings, especially among the middle and lower-income groups in the rural areas not adequately served by the commercial banks and finance companies

snurazani/DIS12

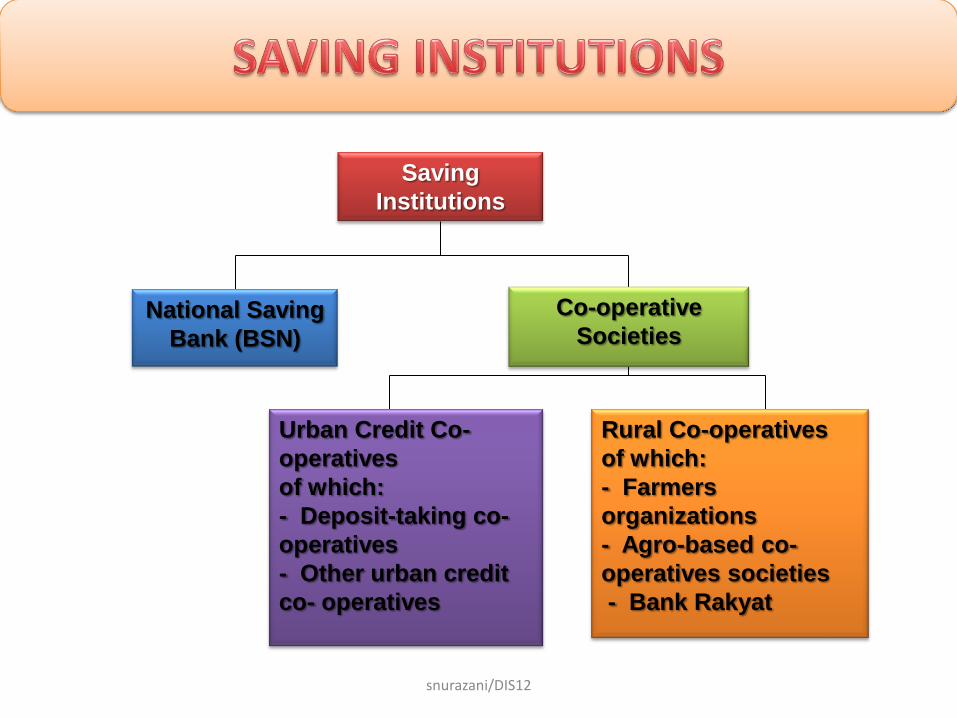

• Examples:

– Bank Simpanan Nasional

– Bank Rakyat

– Tabung Haji

snurazani/DIS12

Saving

Institutions

National Saving

Bank (BSN)

Urban Credit Co-

operatives

of which:

- Deposit-taking co-

operatives

- Other urban credit

co- operatives

Rural Co-operatives

of which:

- Farmers

organizations

- Agro-based co-

operatives societies

- Bank Rakyat

Co-operative

Societies

snurazani/DIS12

• Tabung Haji or Lembaga Tabung Haji is the Malaysian Pilgrim Management and Fund Board. It was formerly known as Lembaga Urusan dan Tabung Haji (LUTH).

• The main function of Tabung Haji is to administer and entirely manage of Malaysian to go for Hajj.

• Tabung Haji also will facilitates savings for the pilgrimage to go to Makkah through investment in Shariah-compliant vehicles.

• Since the investment return is considerably good, some of Malaysian use it as an investment vehicles. Depositors are also allow withdraw part of their EPF saving to be deposit into their Tabung Haji account.

snurazani/DIS12

snurazani/DIS12

• PPFs are a group of financial schemes designed to provide members and their dependents with a measure of social security in the form of retirement, medical, death or disability benefits.

• The major PPFs comprise the Employees Provident Fund (EPF) and other approved private and pension funds

snurazani/DIS12

•The PPFs serve as important mobilizer of long-term savings in the economy for rechanneling into both the public and private sectors to finance long-term investment

snurazani/DIS12

• Several forms of provident and pension funds operate in Malaysia, such as health and medical schemes, compulsory workmen compensation insurance, public provident and pension funds as well as private provident and pension schemes.

snurazani/DIS12

• Employees Provident Fund (EPF),

• Social Security Organisation (SOCSO),

• Armed Forces Fund,

• Pensions Trust Fund

• Teachers Provident Fund

• Other approved private provident and pension funds.

snurazani/DIS12

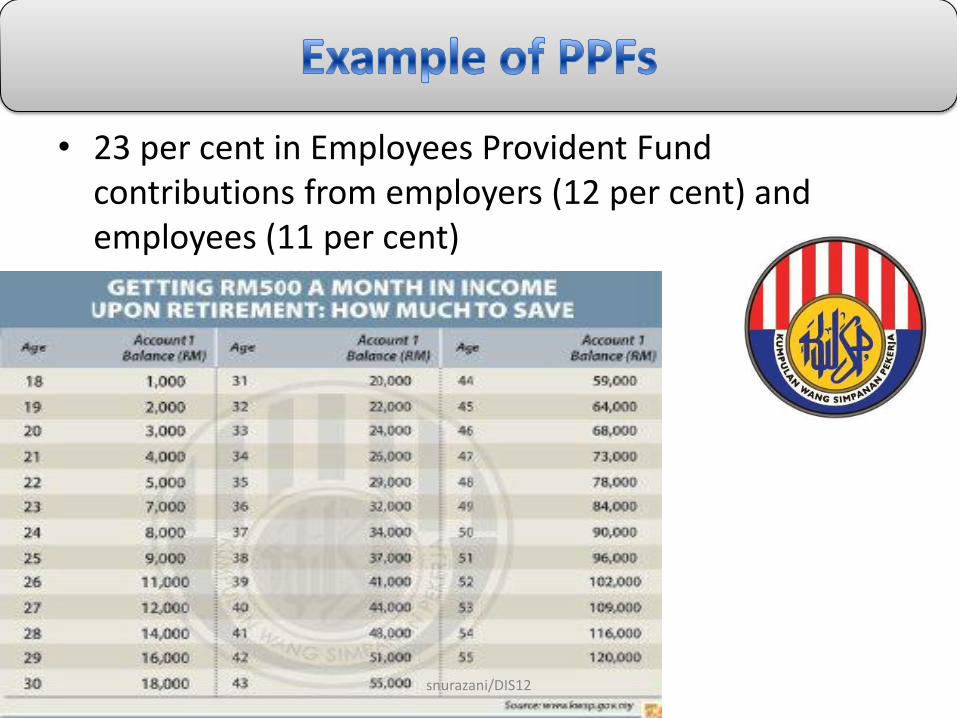

• 23 per cent in Employees Provident Fund contributions from employers (12 per cent) and employees (11 per cent)

snurazani/DIS12

snurazani/DIS12

•Insurance business is a financial service whereby policy holders are given financial protection against loss of property, income or life, for a premium. •Insurance companies have to spread their risks over the insured community and take calculated risks to be able to cover for possible claims •The insurance companies comprise general and life insurance businesses as well as professional reinsurers and insurance intermediaries, such as insurance brokers and adjustors. •In addition, the Takaful industry or Islamic insurance has also been established to operate alongside conventional insurance businesses

snurazani/DIS12

• Life insurance,

• General insurance,

• Reinsurance,

• Insurance Intermediaries

snurazani/DIS12

FACTORING COMPANIES

snurazani/DIS12

• Factoring’s flexibility and effectiveness as a financing instrument is increasingly accepted by the Malaysian business community at large and is seen as an alternative to traditional banking facilities. – A simple financing tool which can be applied as long as there is a creation of

debt. – An alternative source of financing as well as an improved means of working

capital management.

• Today, there are less than 30 factoring companies in Malaysia and almost all of them are owned by financial institutions. The factoring market can be segmented into 2 main sectors, namely :- 1. The private sector (mainly the SMI market, factoring traditional market) 2. The public sector (government and government owned companies)

FACTORING COMPANIES

snurazani/DIS12

• Factoring is simply a sales and purchase transaction between a factor (the factoring company) and its client.

• The factor would not only purchase its client’s trade receivables but gain ownership of the debt as well, thus allowing the factor to collect payments from the client’s

customers.

• DEBT COLLECTION AGENCY

FACTORING COMPANIES

snurazani/DIS12

• The factor gains ownership of its client’s trade debts and thus becomes the new owner of the said debts.

• The client’s customers would then become the debtors of the factor and these debtors would be required to pay the factor directly to discharge their debts.

FACTORING COMPANIES

snurazani/DIS12

– By selling goods or services on credit, a businessman will basically encounter 3 problems, which are :-

• Working capital substantially locked up in trade receivables.

• A sales ledger has to be maintained so that there is an accurate record of debts owed by each customer.

• Customers have to be followed-up and monitored to ensure collections are made on due dates.

FACTORING COMPANIES

snurazani/DIS12

• How its benefits the users?

– Allows a growing company meet its improving sales demand

– Enable the client to obtain cash and quantity discounts from suppliers as well as eliminating expensive prompt payment discounts to customers by still selling to them on credit.

– The client would be released of many administrative burdens as well as enjoy significant savings in personnel, equipments, stationeries, postage and telecommunication expenses, among others due to day-to-day running of the sales ledger, credit management and collection of outstanding book debts.

– All this add up to better profitability for the company.

FACTORING COMPANIES

snurazani/DIS12

• More than 200,000 businesses are currently using factoring to settle trade transactions with some ten million customers worldwide.

• All these companies are obtaining the benefits of factoring i.e. consistent cash flow, lower administration costs, reduced credit risks, more time for core activities.

• These advantages are especially important for the small and medium-sized businesses.

FACTORING COMPANIES

snurazani/DIS12

• This flexible method of managing trade debts enables companies to obtain cash for their domestic and international accounts receivables by selling them to a ‘factor’.

• There are now more than 700 factoring companies many of which offer international or cross-border factoring services as well as domestic. Most are separately incorporated companies, often owned by well-known international banks and other major financial or industrial organizations.

FACTORING COMPANIES

snurazani/DIS12

snurazani/DIS12

• Leasing is a process by which a firm can obtain the use of a certain fixed assets for which it must pay a series of contractual, periodic, tax deductible payments.

• The lessee is the receiver of the services or the assets under the lease contract and the lessor is the owner of the assets.

• The relationship between the tenant and the landlord is called a tenancy, and can be for a fixed or an indefinite period of time (called the term of the lease).

• The consideration for the lease is called rent.

• Leasing is defined as a written contract entered into between a leasing company (called "the Lessor") on the one part and the User of the equipment (called "the Lessee") on the other part whereby the Lessee agrees to pay the Lessor a specified sum of rentals over an obligatory period of time in consideration for the use of capital equipment owned by the Lessor without the Lessee having to purchase or own the equipment.

snurazani/DIS12

Advantages

For businesses, leasing property may have significant financial benefits:

• Leasing is less capital-intensive than purchasing, so if a business has constraints on its capital, it can grow more rapidly by leasing property than it could by purchasing the property outright.

• Capital assets may fluctuate in value. Leasing shifts risks to the lessor, but if the property market has shown steady growth over time, a business that depends on leased property is sacrificing capital gains.

• Leasing may provide more flexibility to a business which expects to grow or move in the relatively short term, because a lessee is not usually obliged to renew a lease at the end of its term.

• In some cases a lease may be the only practical option; such as for a small business that wishes to locate in a large office building within tight locational parameters.

• Depreciation of capital assets has different tax and financial reporting treatment from ordinary business expenses. Lease payments are considered expenses, which can be set off against revenue when calculating taxable profit at the end of the relevant tax accounting period.

snurazani/DIS12

Disadvantages

For businesses, leasing property may have significant drawbacks:

• A net lease may shift some or all of the maintenance costs onto the tenant.

• If circumstances dictate that a business must change its operations significantly, it may be expensive or otherwise difficult to terminate a lease before the end of the term. In some cases, a business may be able to sublet property no longer required, but this may not recoup the costs of the original lease, and, in any event, usually requires the consent of the original lessor. Tactical legal considerations usually make it expedient for lessees to default on their leases. The loss of book value is small and any litigation can usually be settled on advantageous terms. This is an improvement on the position for those companies owning their own property. Although it can be easier for a business to sell property if it has the time, forced sales frequently realise lower prices and can seriously affect book value.

• If the business is successful, lessors may demand higher rental payments when leases come up for renewal. If the value of the business is tied to the use of that particular property, the lessor has a significant advantage over the lessee in negotiations.

snurazani/DIS12

Why choose leasing? • As an additional source of equipment financing, leasing allows conversation of working capital that can then be channeled to other productive business uses. • Lease rentals are tax deductible. • Fixed rental payments assist in budgeting and ease cash flow. • Unlike an overdraft or revolving credit facility, a lease in non-cancelable once it has been executed. • Hedges against inflation as rental payments are fixed and made out of future earnings. • Simplified documentation. • Lease period can be tailored to match the practical useful life of the equipment. • Up to 100% financing for qualified applicant. snurazani/DIS12

What equipment can be leased?

Virtually any movable asset can be leased. However, for easy reference the main items

of equipment for leasing are categorized as follows:-

• Computers and IT-related

• Office Equipment

• Industrial and Manufacturing Equipment

• Commercial and Private Vehicles

• Construction and Heavy Equipment

• Medical Equipment

• Material Handling Equipment

• Others - garage equipment, photography equipment etc.

snurazani/DIS12

Leasing VS Hire Purchase??

The lessor is the owner of leased equipment and the lessee rents the equipment to use by paying the lessor a fixed monthly rental. Ownership stays with the lessor.

In hire purchase, the hirer services installment payment for and is the beneficial owner of the equipment financed. Title to the equipment will pass to the hirer once installment payment is concluded.

Example:

ORIX Leasing Malaysia Berhad

snurazani/DIS12

• Cagamas Berhad, the National Mortgage Corporation and leading securitisation house, was established in 1986 to promote the secondary mortgage market in Malaysia.

• Cagamas Berhad has, through the years, evolved and diversified its business model from that of a national mortgage corporation seeking to aid Malaysians with affordable housing, to becoming a leader in securitisation.

• It issues debt securities to finance the purchase of housing loans and other consumer receivables from financial institutions and non-financial institutions.

• The provision of liquidity at a reasonable cost to the primary lenders of housing loans encourages further financing of houses at an affordable cost.

snurazani/DIS12

• The Cagamas Berhad model is well regarded by the World Bank as the most successful secondary mortgage liquidity facility.

• Cagamas Berhad is the leading issuer of debt instruments, second only to the Government of Malaysia, the largest issuer of AAA debt securities as well as one of the top Sukuk issuers in the world.

• Cagamas Berhad’s debt securities continue to be assigned the highest ratings of AAA and P1 by RAM Rating Services Berhad and AAA/AAAID and MARC-1/MARC-1ID by Malaysian Rating Corporation Berhad, denoting its strong credit quality.

• Website: http://www.cagamas.com.my/

snurazani/DIS12

• To promote home ownership among Malaysians, and to overcome the difficulty faced by young adults to own a house, the Government has intorduced Skim Rumah Pertamaku through Cagamas Berhad which will provide a guarantee on down payment of 10% for houses below RM220,000.

• The scheme is for first-time house buyers with monthly household income of less than RM3,000. It is aimed at young adults who have just joined the workforce.

snurazani/DIS12

• Unit Trust is a collective investment scheme that pools the savings of a large number of investors. The money collected is invested by the fund manager in different types of stocks, bonds, or other securities in various proportions depending upon the objective of the fund.

• The income earned through these investments and the capital appreciation realized by the scheme, after deducting the trading costs and expenses of managing and administering the fund are paid out to the unit holders in proportion to the number of units owned by them.

• Most of the unit trust funds in Malaysia are open-ended funds (the fund sells as many units as you and other investors want to buy and buys as many units you want to sell).

• This makes unit trust funds very liquid investments – though the price at which you sell may be less than your purchase price if the value of the fund has dropped.

snurazani/DIS12

• You can make an initial investment with as little as RM1,000 and buy additional units when you have more money or invest a fixed amount on a regular monthly schedule via a bank account.

• Thus unit trust is the most suitable investment for the common man as it offers an opportunity to invest in a diversified, professionally managed portfolio.

• Example:

– Public Mutual Fund

– Ammutual

– Amanah Saham BSN

– Alliances Investment Management

snurazani/DIS12

• The Credit Guarantee Corporation Malaysia Berhad was incorporated on July 5, 1972 with the main objective of assisting small enterprises to have ready access to credit from the commercial banks.

• The Corporation, which is jointly owned by the Central Bank and the commercial banks, Iaunched its credit guarantee scheme on January 2, 1973 to provide guarantee cover to the commercial banks for designated loans extended to small scale enterprises in the agricultural, commercial and industrial sectors of the economy.

snurazani/DIS12

• This guarantee cover operates automatically once credit facilities under the scheme are provided by the commercial banks and can be invoked as and when the loans extended become nonrecoverable.

• Under the scheme, the commercial banks are required to pay the Corporation a guarantee fee of 0.5 per cent per annum on the loans outstanding.

• ln return, the Corporation covers 60 per cent of the amount of loans in default. The maximum limits on credit made available under the scheme is $200,000 for loans to the bumiputera community and S100,000 to other borrowers, while the maximum rate of interest chargeable on such loans is 8.5 per cent per annum.

snurazani/DIS12