3096 members review booklet 2014 v4 for screen

DESCRIPTION

ÂTRANSCRIPT

Members’Review 2014

2

The photographs in our Members’ Review were taken by Paolo Ferla www.ferlapaolo.com

Bath in Bloom. Bath has been in the “Bloom” business for a very long time, in fact the City was the first winners of the Britain in Bloom competition 50 years ago back in 1964. Since then it has won 13 times and has been finalists 17 times. Bath has also won the South West in Bloom title an amazing 22 times, and is known as “The Floral City”!

In 2014 Bath made history by winning Gold and category winner in the Britain in Bloom competition, and Gold and category winners in the South West in Bloom competition.

The Bath in Bloom committee has encouraged and helped 22 local community groups to get involved in the Royal Horticultural Society “It’s your neighbourhood” scheme during 2014 and 11 of the groups received a level 5 “Outstanding” award. Over 60 groups were involved in the scheme across Bath and North East Somerset.

The Bath in Bloom competition was originally meant for the residents of Bath but for some time now residents and groups from all over Bath and North East Somerset have been able to enter. This has made a huge difference to the towns, villages and community groups across the county, many have gone on to enter South West in Bloom and have enjoyed a huge amount of success.

The Britain in Bloom competition has evolved over the years and today it is much more about communities, biodiversity, recycling and cleanliness, having said that, horticulture still plays an important part in the City’s entry.

The Society is delighted to have sponsored Bath in Bloom in 2014 and continues to do so in 2015. www.bathinbloom.co.uk

3

I am pleased to report that the Society continues to perform very well in a rapidly changing market for financial services this year achieving, once again, record levels of assets, reserves and profit.

For the year ended 31 December 2014

Chairman’s Statement

£24.0m (2013: £21.0m);

Group reserves rose by 14.3% to

Group profit on ordinary activities before taxation rose by 37.4% to

£3.8m (2013: £2.8m);

Assets of the Group increased by 2.5% to

£279.4m (2013: £272.5m).

Liquid assets as a percentage of shares and borrowings reduced to

22.5% (2013: 23.5%);

£218.9m (2013: £210.2m);

Gross mortgage lending of £37.4m (2013: £38.6m) which helped increase the Society’s mortgage book by 4.1% to a record level of

The Chairman’s Statement - for the year ended 31 December 2014

4The Chairman’s Statement - for the year ended 31 December 2014

Whilst the overall UK economy has been picking up, one of the fastest-growing elements has been the housing sector.In 2014 the market saw sharp price rises in the first half - particularly in London - followed by a slowing of demand in the second half. Tougher new rules on borrowing in the form of the Mortgage Market Review have probably contributed to the slowdown and have certainly proved challenging to implement for many lenders. The reform of Stamp Duty that was announced by the Chancellor in his Autumn Statement was a welcome change

...customers are increasingly turning away from branch-based banking and are looking to other methods of managing their money, such as by phone or by using the internet via use of mobile devices...

that should help to stimulate demand once again in 2015 and beyond. Against this backdrop, the Society has continued to steadily grow its mortgage book, and it has been able to retain its distinctive position as a lender focused on the merits of each case, rather than placing reliance on computerised decision-making.

We are extremely mindful of the difficult position for savers with savings rates, already at record low levels as a result of low Bank of England interest rates, being pushed lower still by the availability of low-cost funding from the Government’s Funding for Lending Scheme. We continue to do all we can to offer competitive rates to our existing customers.

Looking to the futureWe are aware that many customers are increasingly turning away from branch-based banking and are looking to other methods of managing their money, such as by phone or by using the internet via use of mobile devices such as tablets and smartphones. Some of these trends have been reflected in our own business and this has brought about the closure of our branch at Larkhall in 2014 as transactions had dipped to a level where maintaining a branch there was uneconomic and was not in the interests of the wider membership. We expect to have branch offices at Moorland Road in Oldfield Park and in the centre of Bath for many years to come, but we do believe that members’ interests will be well served if we increase our investment in technology to extend the range of accounts that can be operated online, and to facilitate the submission of mortgage applications over the internet.

ValuesAs a new member of the Board, I have been impressed by the ethos of the Society’s Board and Management and its focus on its members’ interests: the contrast of the Society’s approach to the reputation of the banking sector is striking. In the few months I have been

5

Hanging baskets at The Abbey in Bath.

The Chairman’s Statement - for the year ended 31 December 2014

6

The Society does offer a very real alternative to the major banks and it is gratifying to see that traditional standards of service and behaviour are valued and appreciated by so many of our customers.

The Chairman’s Statement - for the year ended 31 December 2014

involved with the Society, I have come to recognise it as a very special business in a market where automation and so-called “efficiency measures” have so often been deployed to the detriment of customers. The Society does offer a very real alternative to the major banks and it is gratifying to see that traditional standards of service and behaviour are valued and appreciated by so many of our customers. As a mutual Building Society, we have different priorities to a plc bank. Our focus tends to be longer term and, as your incoming Chairman, I am very aware that my responsibility and that of our Board is to run the Society such that we leave it in better shape than we found it.

Our past Chairman, Christopher Moorsom, who retired at the end of 2014 has done exactly that. Over the years of his chairmanship, the Society has developed in size, in strength and in resilience - no mean feat in the face of the most exacting conditions that the industry has encountered in many generations. On behalf of his Board colleagues, and the staff and members of the Society, I wish him a happy and long retirement. He will be a tough act to follow.

I would also like to take this opportunity to pay tribute to Terry Fussell who served as Society Vice-Chairman for many years before passing away in the summer of 2014. Terry was a tireless supporter of the Society who cared passionately about the interests of its members and the long-term success of the Society. He will be fondly remembered and greatly missed by all who worked with him.

In replacing Christopher and Terry, and to allow for some succession, the Society has taken on three new Non-Executive Directors, including myself. All of the new Directors will stand for election at the 2015 Annual General Meeting. I am excited to work with the newly constituted Board and very much hope to combine the fresh insight of new Board members with the expertise and experience of the established Executive and Non-Executive team.

I am looking forward to serving the members in the months and years ahead. I would like to take this opportunity to thank all involved with the Society - members, staff, suppliers and intermediaries - for your continued support.

Robert Derry-EvansChairman 3 March 2015

7

A flower display in Victoria Park in Bath.

The Chairman’s Statement - for the year ended 31 December 2014

8

For the year ended 31 December 2014

Chief Executive’s Report

The Chief Executive’s Report - for the year ended 31 December 2014

A flower display in Parade Gardens in Bath.

9

MortgagesFollowing years in the doldrums, the mortgage market grew rapidly in 2013 and this strong growth continued into 2014. For various reasons, growth slowed as 2014 progressed but only back towards levels that are more sustainable over the longer term. Government initiatives in the form of the Help-to-Buy programmes and the Funding for Lending Scheme, which has offered cheaper funding to lenders seeking to grow their mortgage assets, have boosted the demand for and supply of mortgages. This has fuelled increases in house prices with virtually all parts of the UK seeing at least some modest growth in property values on a year-on-year basis. Whilst press comment focused on a bubble in house prices developing in London, price rises were more moderate elsewhere. The high levels of house prices in London have caused the Society to introduce measures to slightly restrict lending in the capital given the greater potential for a correction in the London market.

A variety of ‘headwinds’ and ‘tailwinds’ have been at play in driving the housing market in recent years but a likely constraint to demand in the short term will be the fact that real wages have been falling. Moreover, the prospect of interest rate rises is making lenders and borrowers more wary, particularly given the tougher affordability rules introduced by the Financial Conduct Authority in 2014. By contrast, demand will be supported by the failure of the UK housing supply to match the rate of new household formation. Overall the Society expects that the mortgage market will remain reasonably buoyant in the next few years, and this will encourage

an intensification of competition for the Society. The Society will strive to maintain its competitive position through innovation and development of its marketing capability and will resist the temptation to reduce its underwriting standards to attract business.

The Society continues to fulfil a useful role in the market, using its manual underwriting approach to offer loans to creditworthy customers that sometimes find it difficult to obtain loans at acceptable rates from highly automated, computer-driven lenders. This particularly affects some buy-to-let customers, self-employed applicants, those building their own homes and some categories of first-time-buyers. In 2014, the Society reintroduced its insured 95% mortgage product specifically aimed at first-time-buyers and those moving to their second home.

Some seven years ago we introduced our Buy-for-Uni mortgage aimed at students looking to purchase a home rather than rent whilst studying for their degree, and this mortgage remains a popular product offering loans up to 100%, with parental support.

The Society has seen a reduction in the number of arrears cases through 2014. At the start of the year, 19 mortgages had arrears in excess of three months payments. By the end of the year this had fallen to 13 cases. As at the end of 2014 the Society had one property in possession (2013: two). Analysis continues to support the fact that a disproportionately large part of our arrears book comes from loans originated in the 2004-08 period which were adversely impacted by reductions in property values.

The Chief Executive’s Report - for the year ended 31 December 2014

10The Chief Executive’s Report - for the year ended 31 December 2014

The Society continues to offer a wide variety of accounts to consumers, businesses, pension fund administrators, clubs and charities and trusts...

The Society currently has no loans with arrears in excess of three months which were originated since 2012.

Savings and fundingIn 2012, in common with many other Building Societies, the Society decided to join the Bank of England’s Funding for Lending Scheme. The scheme brought considerable benefits to the Society including cheap funding and recourse to contingency funds should this have been necessary. Whilst the Society qualified for substantially more funding from the scheme, as at 31 December 2014 it had drawn down only £17m of funds. In February 2015, the Society repaid £8.5m of funding back to the Bank of England. Further use of the draw down facility of the scheme will be subject to continuing management review.

In the context of the Bank of England’s base rate remaining at 0.5% for much longer than most originally anticipated, our strategy has been to prioritise the relatively small amount of return available to existing savers and the Society remains committed to this approach while market rates are so low. Even though there is a general expectation that rates will gradually rise in the coming two to three years, it is likely that rates will remain below historic pre-2008 levels for some considerable time to come. Although the Society has periodically featured in best buy tables during 2014 it has long been the Society’s policy to offer consistent rates rather than to attract savers with “teaser” rates only to reduce them at the end of an initial period.

A number of existing customers took advantage of the budget provisions announced by the Government to increase the amount allowed in a tax-free ISA to £15,000 which is due to be raised to £15,240 in April 2015. The Society continues to offer a wide variety of accounts to consumers, businesses, pension fund administrators, clubs and charities and trusts, and it considers the breadth of its funding base to be a source of strength.

In the spring of 2014 the Society closed its counter at Larkhall, Bath. All of the Larkhall accounts were transferred to the Society’s Wood Street branch in the centre of Bath. This move reflects changing patterns of customer behaviour where the demand for direct accounts through the post and internet have increasingly displaced branch-based services.

Property letting and financial adviceAt the end of 2014 the Society decided to sell its shareholding in Bath & City Financial Limited, a joint venture business that had been established with City

11The Chief Executive’s Report - for the year ended 31 December 2014

Hanging baskets at the Colonnades in Bath.

12The Chief Executive’s Report - for the year ended 31 December 2014

The Xylem sculpture sponsored by the Society in Parade Gardens in Bath.

13The Chief Executive’s Report - for the year ended 31 December 2014

Financial Planning Limited to offer independent financial advice. Over the years, Bath & City Financial Limited has helped hundreds of clients to take better control of their finances and has been able to offer the Society’s customers a greater range of financial services. The Society has withdrawn from financial advice to concentrate on its core business, but clients of Bath & City Financial Limited will continue to be looked after by City Financial Planning Limited. The Society sold its shareholding in Bath & City Financial Limited for a sum equal to its initial investment in the business.

Bath Property Letting Limited continues to provide letting services to landlords and tenants in and around Bath and is a wholly-owned subsidiary of the Society. Despite incurring an impairment charge of £2,648 (2013: £nil) against goodwill relating to purchased portfolios of properties, profit before tax for this business rose substantially to £121,349 (2013: £93,951) as a result of a strong performance in core letting activity. It remains the intention to grow this business through a combination of acquisitions and organic growth.

Community involvementThe Society has worked with a wide variety of local charities throughout the year.

Through its Charity Awards Scheme, the Society aims to improve the lives of disadvantaged people by helping the good work of small local charities who often find it difficult to raise funds. In 2014, the Society donated £7,000 plus a number of hot air balloon tickets to a diverse range of nine charities. One of the Society’s main

awards was for £1,000 to Bath Gateway Out & About, a charity founded to provide recreational opportunities to adults with learning disabilities. This charity was also nominated to become the Society’s Charity of the Year. Other charities benefiting from the awards included, Keynsham and District Mencap, Greenlinks and Bath FoodCycle.

The Society also sponsored the annual fireworks at Bath Recreation Ground that is organised by The Rotary Club of Bath. The event was highly successful and raised approximately £20,000 for local charities. The Society’s sponsorship also incorporates the children’s Firework Safety Poster Competition designed to impart a lasting message about firework safety to the city’s children. This event will celebrate its 40th anniversary in 2015 and we are grateful to The Rotary Club of Bath for its sound management of this event.

The Society was also involved in sponsoring Bath in Bloom in what was a major anniversary year for an event which has had an impressive track record over many decades. We congratulate the organisers on their excellent success and all involved in making Bath a visual summer delight.

Dick JenkinsChief Executive3 March 2015

14

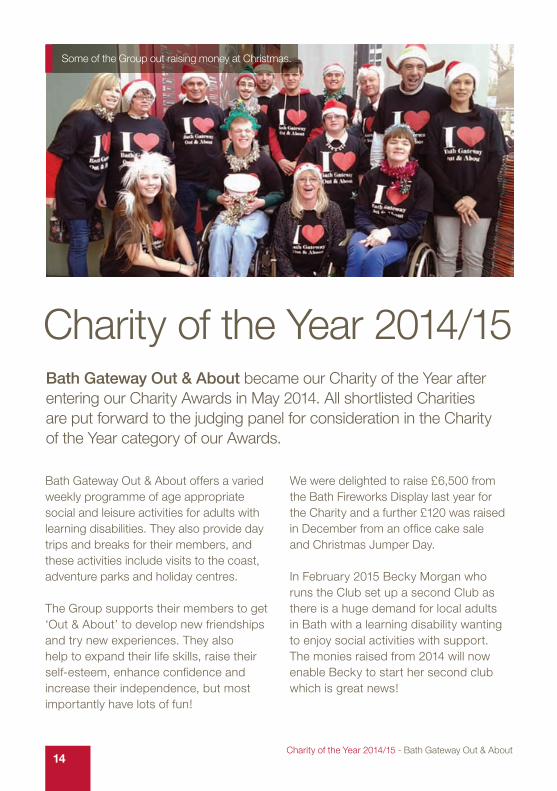

Bath Gateway Out & About offers a varied weekly programme of age appropriate social and leisure activities for adults with learning disabilities. They also provide day trips and breaks for their members, and these activities include visits to the coast, adventure parks and holiday centres.

The Group supports their members to get ‘Out & About’ to develop new friendships and try new experiences. They also help to expand their life skills, raise their self-esteem, enhance confidence and increase their independence, but most importantly have lots of fun!

Charity of the Year 2014/15

Some of the Group out raising money at Christmas.

We were delighted to raise £6,500 from the Bath Fireworks Display last year for the Charity and a further £120 was raised in December from an office cake sale and Christmas Jumper Day.

In February 2015 Becky Morgan who runs the Club set up a second Club as there is a huge demand for local adults in Bath with a learning disability wanting to enjoy social activities with support. The monies raised from 2014 will now enable Becky to start her second club which is great news!

Bath Gateway Out & About became our Charity of the Year after entering our Charity Awards in May 2014. All shortlisted Charities are put forward to the judging panel for consideration in the Charity of the Year category of our Awards.

Charity of the Year 2014/15 - Bath Gateway Out & About

15Report of the Directors on Remuneration - for the year ended 31 December 2014

Report of the Directors on RemunerationFor the year ended 31 December 2014Unaudited informationThe following Report of the Directors on Remuneration will be put to an advisory vote of the members at the forthcoming Annual General Meeting.

The Board is committed to best practice in its remuneration policy for directors. This report explains how the Society applies the principles in the UK Corporate Governance Code relating to remuneration. The Society complies with the code provisions as far as they are applicable to a mutual organisation unless the contrary is stated.

Level and components of remuneration The Society’s remuneration policy is to reward directors through salary according to their expertise, experience and contribution. The Society also carries out benchmarking against other comparable organisations.

Executive Directors’ emolumentsThe remuneration arrangements for Executive Directors consist only of basic salary, annual bonus, pension and other benefits. The Executive Directors do not hold outside directorships that provide an income for the benefit of themselves.

The Nomination and Remuneration Committee designs the Executive Directors’ bonus scheme to align the interests of Executive Directors with the interests of members and provide incentives that recognise corporate and personal performance. If a range of challenging personal and operational targets is achieved, R D Jenkins and K A Gray can achieve a bonus of 10% of basic salary. The Committee has the discretion to reward the Executive Directors with an additional bonus element equivalent to a maximum of 5% of basic salary if exceptional performance is deemed to be delivered.

The Executive Directors benefit from a pension scheme whereby the Society contributes 12%

of basic salary per annum to a money purchase scheme. In lieu of his entitlement to pension contributions, from 1 April 2014 R D Jenkins opted to receive a cash equivalent sum at no extra gross cost to the Society. The Society operates no final salary pension arrangements.

Executive Directors receive other taxable benefits including a car. The aggregate amount of these benefits is included in Table 1 on page 16.

Executive Directors’ contractual termsEach Executive Director has a service contract with the Society, terminable by either party giving six months’ notice.

Non-Executive DirectorsThe level of fees payable to Non-Executive Directors is assessed by the Nomination and Remuneration Committee using information from comparable organisations. These fees are not pensionable. Non-Executive Directors do not participate in any bonus schemes and they do not receive any other benefits. Details of Non-Executive Directors’ emoluments are set out in Table 2 on page 16.

The terms of appointment letter for each Non-Executive Director specifies that either party giving one month’s notice may terminate the agreement.

Procedure for determining remunerationC W J Nott, R Derry-Evans and A Cha constitute the Nomination and Remuneration Committee. It is responsible for setting Executive Director remuneration. In view of the increasing responsibilities and work load of Non-Executive Directors, the Committee approved a 6% rise for 2015.

The Nomination and Remuneration Committee normally reviews basic salaries, annually, by reference to jobs carrying similar responsibilities in comparable organisations and local market conditions generally.

16Report of the Directors on Remuneration - for the year ended 31 December 2014

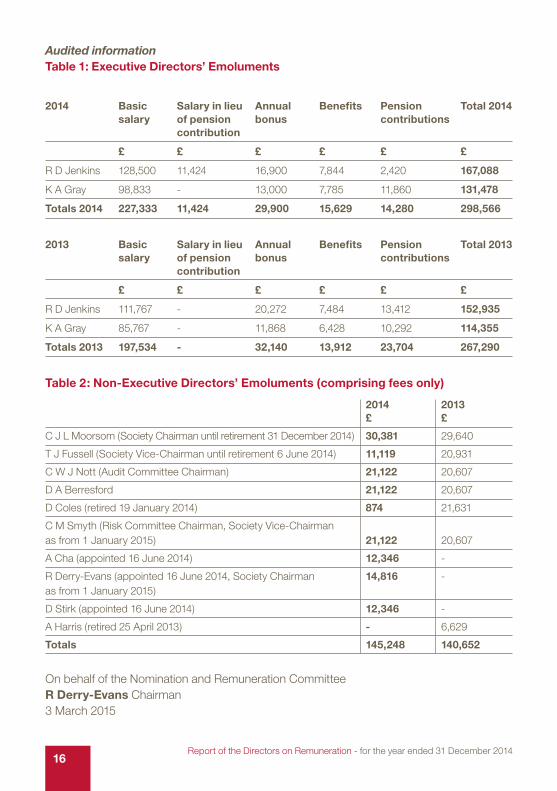

Audited informationTable 1: Executive Directors’ Emoluments

Table 2: Non-Executive Directors’ Emoluments (comprising fees only)

2014 2013 £ £

C J L Moorsom (Society Chairman until retirement 31 December 2014) 30,381 29,640

T J Fussell (Society Vice-Chairman until retirement 6 June 2014) 11,119 20,931

C W J Nott (Audit Committee Chairman) 21,122 20,607

D A Berresford 21,122 20,607

D Coles (retired 19 January 2014) 874 21,631

C M Smyth (Risk Committee Chairman, Society Vice-Chairman as from 1 January 2015) 21,122 20,607

A Cha (appointed 16 June 2014) 12,346 -

R Derry-Evans (appointed 16 June 2014, Society Chairman 14,816 -as from 1 January 2015)

D Stirk (appointed 16 June 2014) 12,346 -

A Harris (retired 25 April 2013) - 6,629

Totals 145,248 140,652

On behalf of the Nomination and Remuneration CommitteeR Derry-Evans Chairman3 March 2015

2014 Basic salary

Salary in lieu of pension contribution

Annual bonus

Benefits Pension contributions

Total 2014

£ £ £ £ £ £

R D Jenkins 128,500 11,424 16,900 7,844 2,420 167,088

K A Gray 98,833 - 13,000 7,785 11,860 131,478

Totals 2014 227,333 11,424 29,900 15,629 14,280 298,566

2013 Basic salary

Salary in lieu of pension contribution

Annual bonus

Benefits Pension contributions

Total 2013

£ £ £ £ £ £

R D Jenkins 111,767 - 20,272 7,484 13,412 152,935

K A Gray 85,767 - 11,868 6,428 10,292 114,355

Totals 2013 197,534 - 32,140 13,912 23,704 267,290

17

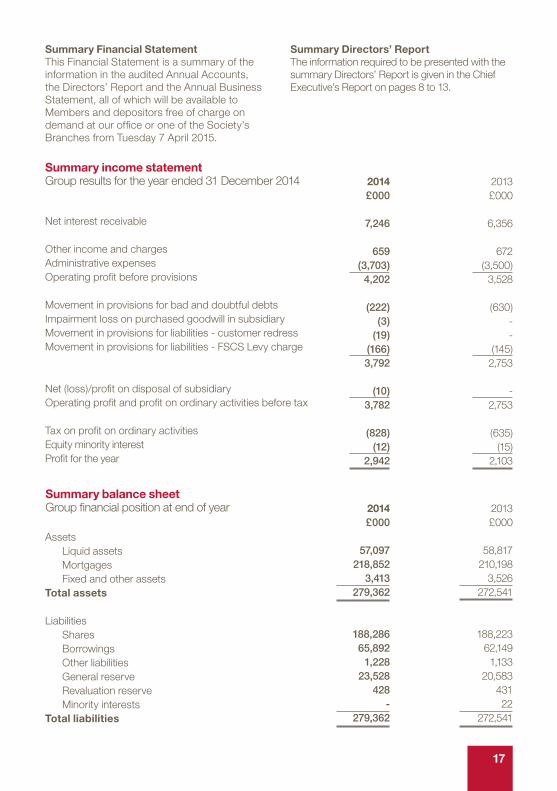

Summary Financial StatementThis Financial Statement is a summary of the information in the audited Annual Accounts, the Directors’ Report and the Annual Business Statement, all of which will be available to Members and depositors free of charge on demand at our office or one of the Society’s Branches from Tuesday 7 April 2015.

Summary Directors’ Report The information required to be presented with the summary Directors’ Report is given in the Chief Executive’s Report on pages 8 to 13.

Net interest receivable

Other income and chargesAdministrative expensesOperating profit before provisions

Movement in provisions for bad and doubtful debtsImpairment loss on purchased goodwill in subsidiaryMovement in provisions for liabilities - customer redressMovement in provisions for liabilities - FSCS Levy charge

Net (loss)/profit on disposal of subsidiaryOperating profit and profit on ordinary activities before tax

Tax on profit on ordinary activitiesEquity minority interestProfit for the year

Summary income statementGroup results for the year ended 31 December 2014 2014

£000

7,246

659(3,703)

4,202

(222)(3)

(19)(166)3,792

(10)3,782

(828)(12)

2,942

2013£000

6,356

672(3,500)

3,528

(630)--

(145)2,753

-2,753

(635)(15)

2,103

Assets Liquid assets Mortgages Fixed and other assetsTotal assets

Liabilities Shares Borrowings Other liabilities General reserve Revaluation reserve Minority interestsTotal liabilities

Summary balance sheetGroup financial position at end of year 2014

£000

57,097218,852

3,413279,362

188,28665,892

1,22823,528

428-

279,362

2013£000

58,817210,198

3,526272,541

188,22362,1491,133

20,58343122

272,541

18

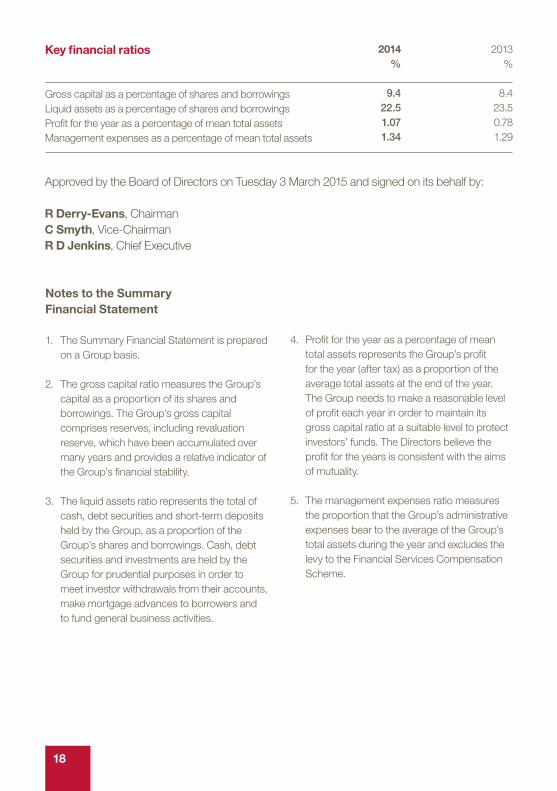

Approved by the Board of Directors on Tuesday 3 March 2015 and signed on its behalf by:

R Derry-Evans, ChairmanC Smyth, Vice-ChairmanR D Jenkins, Chief Executive

Key financial ratios

Gross capital as a percentage of shares and borrowingsLiquid assets as a percentage of shares and borrowingsProfit for the year as a percentage of mean total assetsManagement expenses as a percentage of mean total assets

2014%

9.422.51.071.34

2013 %

8.423.50.781.29

Notes to the Summary Financial Statement

1. The Summary Financial Statement is prepared on a Group basis.

2. The gross capital ratio measures the Group’s capital as a proportion of its shares and borrowings. The Group’s gross capital comprises reserves, including revaluation reserve, which have been accumulated over many years and provides a relative indicator of the Group’s financial stability.

3. The liquid assets ratio represents the total of cash, debt securities and short-term deposits held by the Group, as a proportion of the Group’s shares and borrowings. Cash, debt securities and investments are held by the Group for prudential purposes in order to meet investor withdrawals from their accounts, make mortgage advances to borrowers and to fund general business activities.

4. Profit for the year as a percentage of mean total assets represents the Group’s profit for the year (after tax) as a proportion of the average total assets at the end of the year. The Group needs to make a reasonable level of profit each year in order to maintain its gross capital ratio at a suitable level to protect investors’ funds. The Directors believe the profit for the years is consistent with the aims of mutuality.

5. The management expenses ratio measures the proportion that the Group’s administrative expenses bear to the average of the Group’s total assets during the year and excludes the levy to the Financial Services Compensation Scheme.

19

We have examined the summary financial statement for the year ended 31 December 2014 which comprises the Summary Consolidated Income Statement, Summary Consolidated Balance Sheet and Summary Directors’ Report. This report is made solely to the company’s Members, as a body, in accordance with section 76(5) of the Building Societies Act 1986. Our work has been undertaken so that we might state to the Society’s Members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Society and the Society’s Members as a body, for our audit work, for this report, for our audit report, or for the opinions we have formed. Respective responsibilities of directors and auditorsThe directors are responsible for preparing the summarised financial statements in accordance with applicable United Kingdom law. Our responsibility is to report to you our opinion on the consistency of the summary financial statement within the Members’ Review 2014 with the full annual financial statements, Annual Business Statement and the Directors’ Report, and its

Independent Auditor’s Statement to the Members of Bath Investment & Building Society

compliance with the relevant requirements of section 76 of the Building Societies Act 1986 and the regulations made thereunder. We also read the other information contained in the Members’ Review 2014 as described in the contents section, and consider the implications for our report if we become aware of any apparent misstatements or material inconsistencies with the summary financial statement. We conducted our work in accordance with Bulletin 2008/3 issued by the Auditing Practices Board. Our report on the Group and Society’s full annual financial statements describes the basis of our opinion on those financial statements and on the Directors’ Report. Opinion on summary financial statement In our opinion, the summary financial statement is consistent with the full annual financial statements, the Annual Business Report and the Directors’ Report of Bath Investment & Building Society for the year ended 31 December 2014 and complies with the applicable requirements of section 76 of the Building Societies Act 1986, and the regulations made thereunder. Deloitte LLPChartered Accountants and Statutory Auditors, Bristol, United Kingdom4 March 2015

20

Notice of Annual General Meeting

The 111th Annual General Meeting (AGM) of the Members of Bath Investment & Building Society will be held on Tuesday 28 April 2015, in The Octagon Room at The Assembly Rooms in Bath at 12noon for the following purposes:

Notes

These notes form part of the Notice of the Meeting.

1. Under the Society Rules, a Member entitled to attend the meeting and vote may appoint one proxy to attend and vote on his or her behalf. You may appoint the Chairman of the meeting or anyone else as your proxy. Your proxy may vote for you at the meeting but only on a poll. Your proxy, if other than the Chairman, may not speak at the meeting except in demanding a poll. You may instruct your proxy how to vote at the meeting. Please read the instructions on the proxy form. The voting date is the date of the meeting; Tuesday 28 April 2015, if voting in person, and Tuesday 21 April 2015 if voting by proxy. In order to attend and vote at the meeting, or appoint a proxy, you must qualify to vote.

2. To qualify as a voting shareholding Member, you must be an individual of at least 18 years of age on the voting date; have held share in the Society to the value of at least £100 at 31 December 2014 and continue to hold shares at the voting date; and be the first named on the account in our records.

3. To qualify as a voting borrowing Member you must be an individual of at least 18 years of age on the voting date; have held a mortgage in the Society to the value of at least £100 at 31 December 2014 and hold a mortgage at the voting date; and be the first named on the account in our records.

4. You can only vote once as a Member, irrespective of the number of accounts you hold, whether you hold accounts in the different capacities and whether you qualify to vote as both a shareholding and borrowing Member.

5. Item 3 in the Notice of Meeting relates to a Resolution for Members to vote on the Directors’ Remuneration Report for 2014. As a Building Society we are not obliged to ask Members to vote on this but in accordance with best practice we are asking for an advisory vote and the Board will consider the result and decide what action, if any, will be appropriate.

6. Items 4 to 9 in the Notice of the Meeting relate to Resolutions for re-election and election of Directors.

7. Members attending the meeting must bring evidence of their membership (a current passbook or mortgage statement) in order to obtain admission.

8. If you appoint a proxy, other than the Chairman, to vote on your behalf at the meeting, they must attend the meeting and bring a form of identification, for your vote to count.

1. To receive the Directors’ Report, Annual Accounts and Annual Business Statement for the year ended 31 December 2014.

2. To consider an Ordinary Resolution to re-appoint Deloitte LLP as Auditor of the Society, to hold office until the conclusion of the next AGM at which accounts are laid before the Society and their remuneration be fixed by the Directors.

3. To consider an Ordinary Resolution to approve the Directors’ Remuneration Report.

4. To re-elect Ann Berresford.5. To re-elect Richard Jenkins.6. To re-elect Christopher Smyth.7. To elect Angela Cha.8. To elect Robert Derry-Evans.9. To elect Denzil Stirk.10. To transact any other business permitted

by the Rules of the Society.

By Order of the BoardTonia Lovell, Society Secretary3 March 2015

21

These are the profiles of the Directors to be re-elected and elected to the Board.

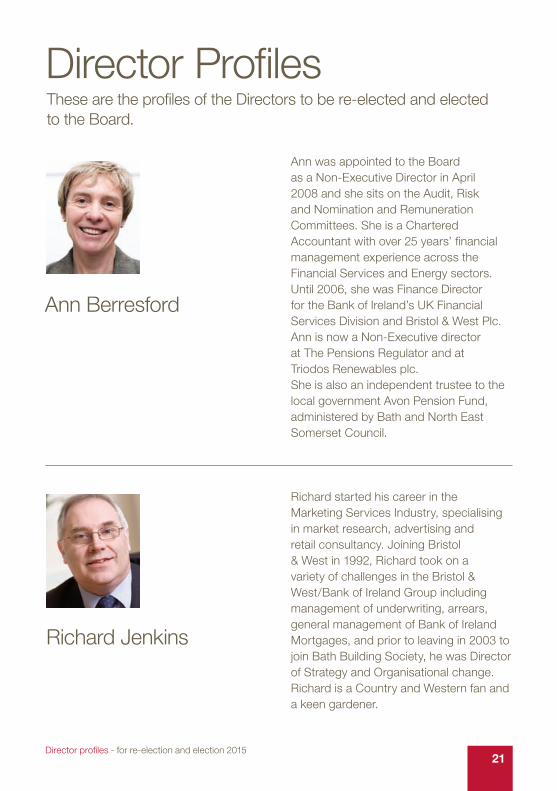

Ann Berresford

Richard Jenkins

Director Profiles

Richard started his career in the Marketing Services Industry, specialising in market research, advertising and retail consultancy. Joining Bristol & West in 1992, Richard took on a variety of challenges in the Bristol & West/Bank of Ireland Group including management of underwriting, arrears, general management of Bank of Ireland Mortgages, and prior to leaving in 2003 to join Bath Building Society, he was Director of Strategy and Organisational change. Richard is a Country and Western fan and a keen gardener.

Ann was appointed to the Board as a Non-Executive Director in April 2008 and she sits on the Audit, Risk and Nomination and Remuneration Committees. She is a Chartered Accountant with over 25 years’ financial management experience across the Financial Services and Energy sectors. Until 2006, she was Finance Director for the Bank of Ireland’s UK Financial Services Division and Bristol & West Plc. Ann is now a Non-Executive director at The Pensions Regulator and at Triodos Renewables plc. She is also an independent trustee to the local government Avon Pension Fund, administered by Bath and North East Somerset Council.

Director profiles - for re-election and election 2015

22

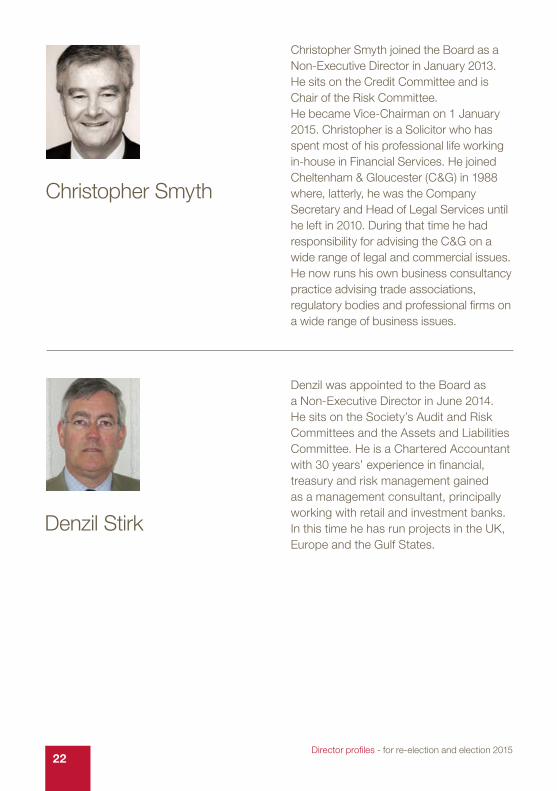

Christopher Smyth joined the Board as a Non-Executive Director in January 2013. He sits on the Credit Committee and is Chair of the Risk Committee. He became Vice-Chairman on 1 January 2015. Christopher is a Solicitor who has spent most of his professional life working in-house in Financial Services. He joined Cheltenham & Gloucester (C&G) in 1988 where, latterly, he was the Company Secretary and Head of Legal Services until he left in 2010. During that time he had responsibility for advising the C&G on a wide range of legal and commercial issues. He now runs his own business consultancy practice advising trade associations, regulatory bodies and professional firms on a wide range of business issues.

Christopher Smyth

Denzil was appointed to the Board as a Non-Executive Director in June 2014. He sits on the Society’s Audit and Risk Committees and the Assets and Liabilities Committee. He is a Chartered Accountant with 30 years’ experience in financial, treasury and risk management gained as a management consultant, principally working with retail and investment banks. In this time he has run projects in the UK, Europe and the Gulf States.

Denzil Stirk

Director profiles - for re-election and election 2015

23

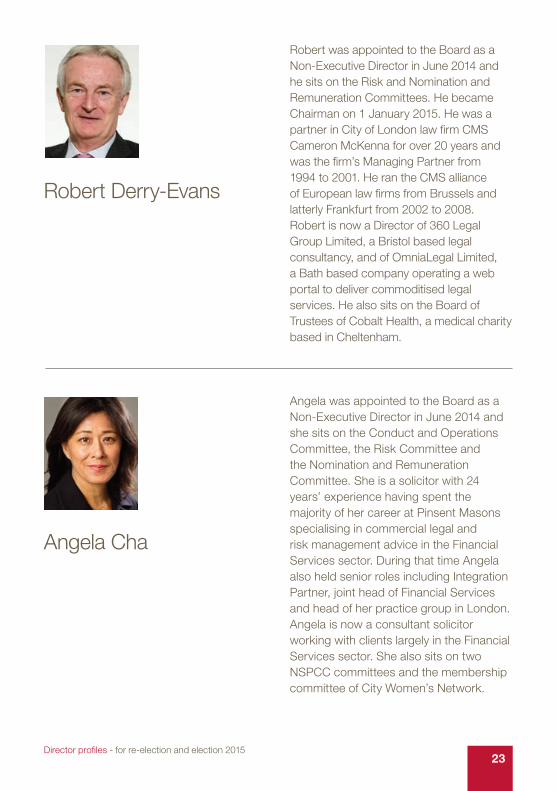

Robert was appointed to the Board as a Non-Executive Director in June 2014 and he sits on the Risk and Nomination and Remuneration Committees. He became Chairman on 1 January 2015. He was a partner in City of London law firm CMS Cameron McKenna for over 20 years and was the firm’s Managing Partner from 1994 to 2001. He ran the CMS alliance of European law firms from Brussels and latterly Frankfurt from 2002 to 2008. Robert is now a Director of 360 Legal Group Limited, a Bristol based legal consultancy, and of OmniaLegal Limited, a Bath based company operating a web portal to deliver commoditised legal services. He also sits on the Board of Trustees of Cobalt Health, a medical charity based in Cheltenham.

Robert Derry-Evans

Angela was appointed to the Board as a Non-Executive Director in June 2014 and she sits on the Conduct and Operations Committee, the Risk Committee and the Nomination and Remuneration Committee. She is a solicitor with 24 years’ experience having spent the majority of her career at Pinsent Masons specialising in commercial legal and risk management advice in the Financial Services sector. During that time Angela also held senior roles including Integration Partner, joint head of Financial Services and head of her practice group in London. Angela is now a consultant solicitor working with clients largely in the Financial Services sector. She also sits on two NSPCC committees and the membership committee of City Women’s Network.

Angela Cha

Director profiles - for re-election and election 2015

Head Office:15 Queen Square, Bath BA1 2HN.

Investment enquiries:Telephone:01225 423271Fax:01225 446914Email:[email protected]

Mortgage enquiries:Telephone:01225 475702Fax:01225 424590Email:[email protected]

Web:www.bathbuildingsociety.co.uk

Telephone calls may be recorded to help the Society to maintain high standards of service delivery.

Bath Investment & Building Society is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority, Registration Number 206026.