3 diversification of jgb products and investor base · iversification of jgb products and investor...

TRANSCRIPT

Ⅰ FY2015 Debt Management Policies

3 Diversification of JG

B Products and Investor B

ase

36

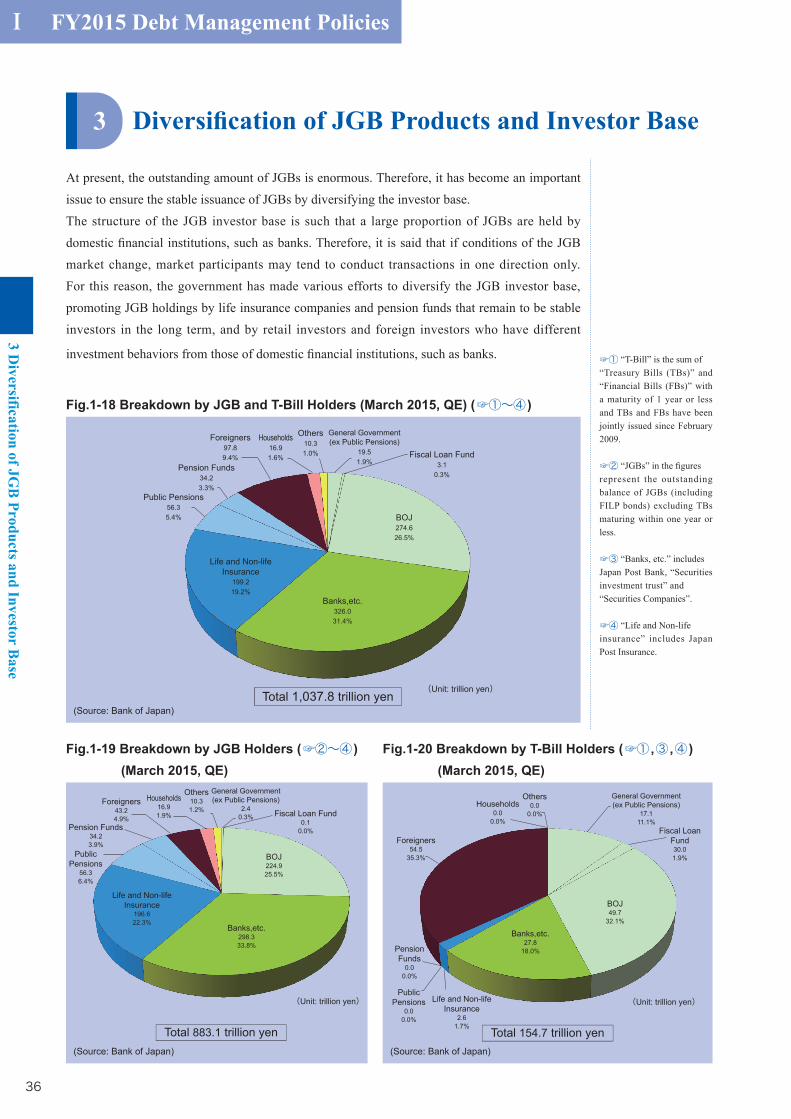

At present, the outstanding amount of JGBs is enormous. Therefore, it has become an important

issue to ensure the stable issuance of JGBs by diversifying the investor base.

The structure of the JGB investor base is such that a large proportion of JGBs are held by

domestic financial institutions, such as banks. Therefore, it is said that if conditions of the JGB

market change, market participants may tend to conduct transactions in one direction only.

For this reason, the government has made various efforts to diversify the JGB investor base,

promoting JGB holdings by life insurance companies and pension funds that remain to be stable

investors in the long term, and by retail investors and foreign investors who have different

investment behaviors from those of domestic financial institutions, such as banks.

3

☞① “T-Bill” is the sum of “Treasury Bills (TBs)” and “Financial Bills (FBs)” with a maturity of 1 year or less and TBs and FBs have been jointly issued since February 2009.

☞② “JGBs” in the figures represent the outstanding balance of JGBs (including FILP bonds) excluding TBs maturing within one year or less.

☞③ “Banks, etc.” includesJapan Post Bank, “Securities investment trust” and“Securities Companies”.

☞④ “Life and Non-lifeinsurance” includes Japan Post Insurance.

Diversification of JGB Products and Investor Base

PublicPensions

56.36.4%

Pension Funds34.23.9%

Foreigners43.24.9%

Households16.91.9%

Others10.31.2%

General Government(ex Public Pensions)

2.40.3% Fiscal Loan Fund

0.10.0%

BOJ224.925.5%

Banks,etc.298.333.8%

Life and Non-lifeInsurance

196.622.3%

Total 883.1 trillion yen

(Unit: trillion yen)

Fig.1-18 Breakdown by JGB and T-Bill Holders (March 2015, QE) (☞①〜④ )

Public Pensions56.35.4%

Pension Funds34.23.3%

Foreigners97.89.4%

Households16.91.6%

Others10.31.0%

General Government(ex Public Pensions)

19.51.9%

Fiscal Loan Fund3.1

0.3%

BOJ274.626.5%

Banks,etc.326.031.4%

Life and Non-lifeInsurance

199.219.2%

Total 1,037.8 trillion yen(Unit: trillion yen)

(Source: Bank of Japan)

Fig.1-19 Breakdown by JGB Holders (☞②〜④ ) (March 2015, QE)

Fig.1-20 Breakdown by T-Bill Holders (☞① ,③ ,④ ) (March 2015, QE)

Total 154.7 trillion yen

PensionFunds

0.00.0%

PublicPensions

0.00.0%

Foreigners54.5

35.3%

Households0.0

0.0%

Others0.0

0.0%

General Government(ex Public Pensions)

17.111.1%

Fiscal LoanFund30.01.9%

BOJ49.7

32.1%

Banks,etc.27.8

18.0%

Life and Non-lifeInsurance

2.61.7%

(Unit: trillion yen)

(Source: Bank of Japan) (Source: Bank of Japan)

Ⅰ FY2015 Debt Management Policies3 D

iversification of JGB

Products and Investor Base

37

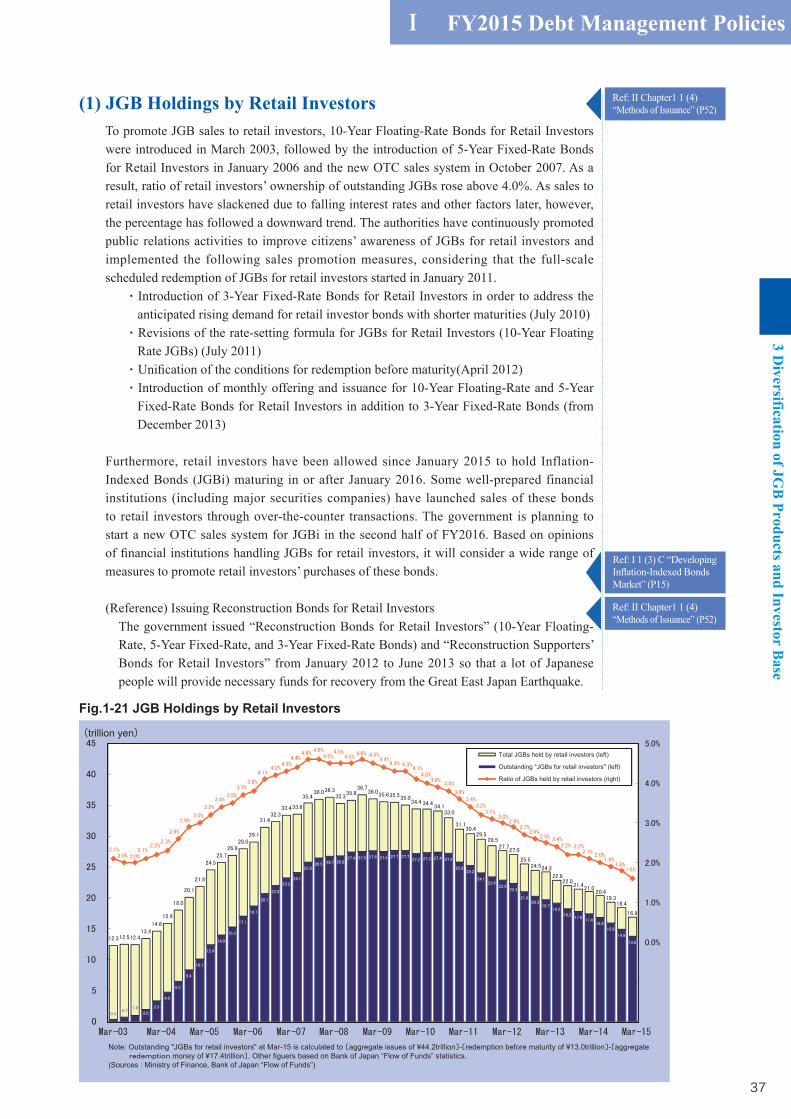

(1) JGB Holdings by Retail InvestorsTo promote JGB sales to retail investors, 10-Year Floating-Rate Bonds for Retail Investors were introduced in March 2003, followed by the introduction of 5-Year Fixed-Rate Bonds for Retail Investors in January 2006 and the new OTC sales system in October 2007. As a result, ratio of retail investors’ ownership of outstanding JGBs rose above 4.0%. As sales to retail investors have slackened due to falling interest rates and other factors later, however, the percentage has followed a downward trend. The authorities have continuously promoted public relations activities to improve citizens’ awareness of JGBs for retail investors and implemented the following sales promotion measures, considering that the full-scale scheduled redemption of JGBs for retail investors started in January 2011.・Introduction of 3-Year Fixed-Rate Bonds for Retail Investors in order to address the

anticipated rising demand for retail investor bonds with shorter maturities (July 2010)・Revisions of the rate-setting formula for JGBs for Retail Investors (10-Year Floating

Rate JGBs) (July 2011)・Unifi cation of the conditions for redemption before maturity(April 2012)・Introduction of monthly offering and issuance for 10-Year Floating-Rate and 5-Year

Fixed-Rate Bonds for Retail Investors in addition to 3-Year Fixed-Rate Bonds (from December 2013)

Furthermore, retail investors have been allowed since January 2015 to hold Inflation-Indexed Bonds (JGBi) maturing in or after January 2016. Some well-prepared financial institutions (including major securities companies) have launched sales of these bonds to retail investors through over-the-counter transactions. The government is planning to start a new OTC sales system for JGBi in the second half of FY2016. Based on opinions of fi nancial institutions handling JGBs for retail investors, it will consider a wide range of measures to promote retail investors’ purchases of these bonds.

(Reference) Issuing Reconstruction Bonds for Retail InvestorsThe government issued “Reconstruction Bonds for Retail Investors” (10-Year Floating-Rate, 5-Year Fixed-Rate, and 3-Year Fixed-Rate Bonds) and “Reconstruction Supporters’ Bonds for Retail Investors” from January 2012 to June 2013 so that a lot of Japanese people will provide necessary funds for recovery from the Great East Japan Earthquake.

Ref: II Chapter1 1 (4) “Methods of Issuance” (P52)

Ref: II Chapter1 1 (4) “Methods of Issuance” (P52)

Ref: I 1 (3) C “DevelopingInfl ation-Indexed BondsMarket” (P15)

Note: Outstanding "JGBs for retail investors" at Mar-15 is calculated to aggregate issues of ¥44.2trillion - redemption before maturity of ¥13.0trillion - agg egate money of ¥17.4trillion . Other figuers based on Bank of Japan “Flow of Funds” statistics.

(Sources : Ministry of Finance, Bank of Japan “Flow of Funds”)

Total JGBs held by retail investors (left)

Outstanding "JGBs for retail investors" (left)

Ratio of JGBs held by retail investors (right)

(trillion yen)

Fig.1-21 JGB Holdings by Retail Investors

Ⅰ FY2015 Debt Management Policies

3 Diversification of JG

B Products and Investor B

ase

38

0

7

14

21

28

-6

-4

-2

0

2

4

6

8

RedemptionIssuanceOutstanding balance

trillion yen

Issu

ance

trillion yen

Outstanding balance (right scale)

Planned redemption amount

Note: Issuance, redemption and outstanding balance amounts in and before FY2014 are actual results. Redemption amounts in and after FY2015 are estimates at end of March 2015.

Red

empt

ion

FY20

02

FY20

03

FY20

04

FY20

05

FY20

06

FY20

07

FY20

08

FY20

09

FY20

10

FY20

11

FY20

12

FY20

13

FY20

14

FY20

15

FY20

16

FY20

17

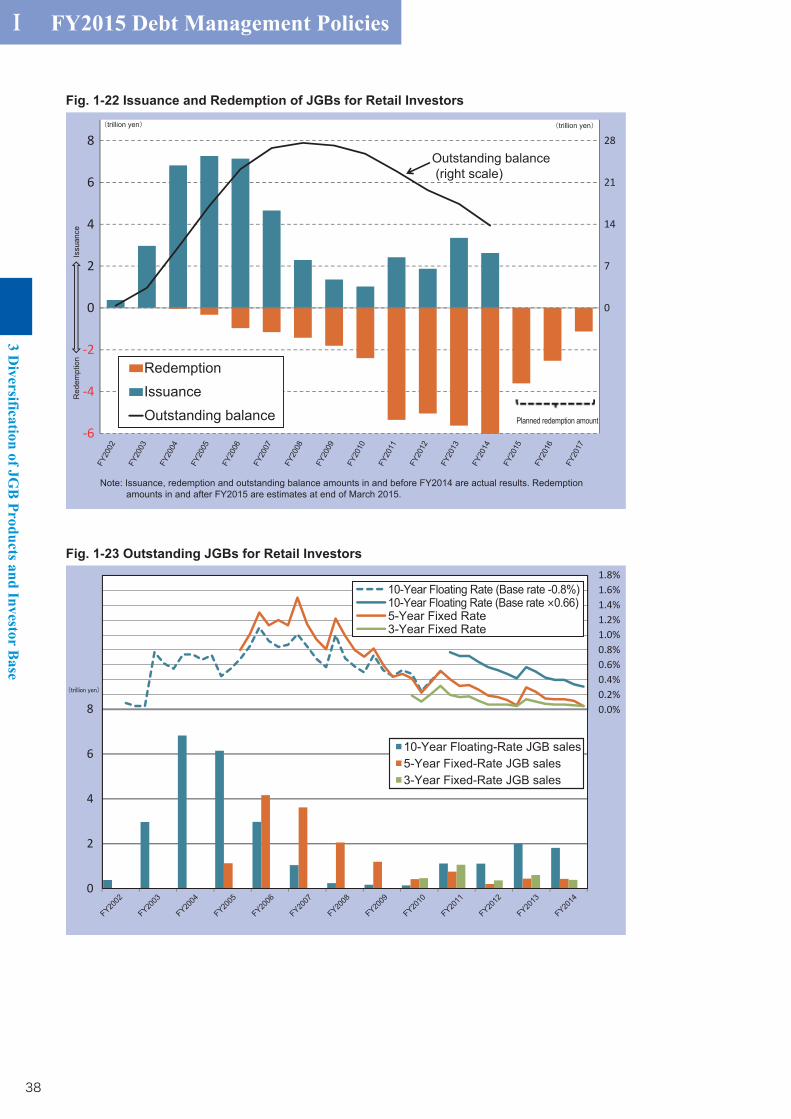

Fig. 1-22 Issuance and Redemption of JGBs for Retail Investors

0

2

4

6

8

10-Year Floating-Rate JGB sales5-Year Fixed-Rate JGB sales3-Year Fixed-Rate JGB sales

0.0%0.2%0.4%0.6%0.8%1.0%1.2%1.4%1.6%1.8%

10-Year Floating Rate (Base rate -0.8%)

5-Year Fixed Rate10-Year Floating Rate (Base rate ×0.66)

3-Year Fixed Rate

FY2002

FY2003

FY2004

FY2005

FY2006

FY2007

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014

Fig. 1-23 Outstanding JGBs for Retail Investors

Ⅰ FY2015 Debt Management Policies3 D

iversification of JGB

Products and Investor Base

39

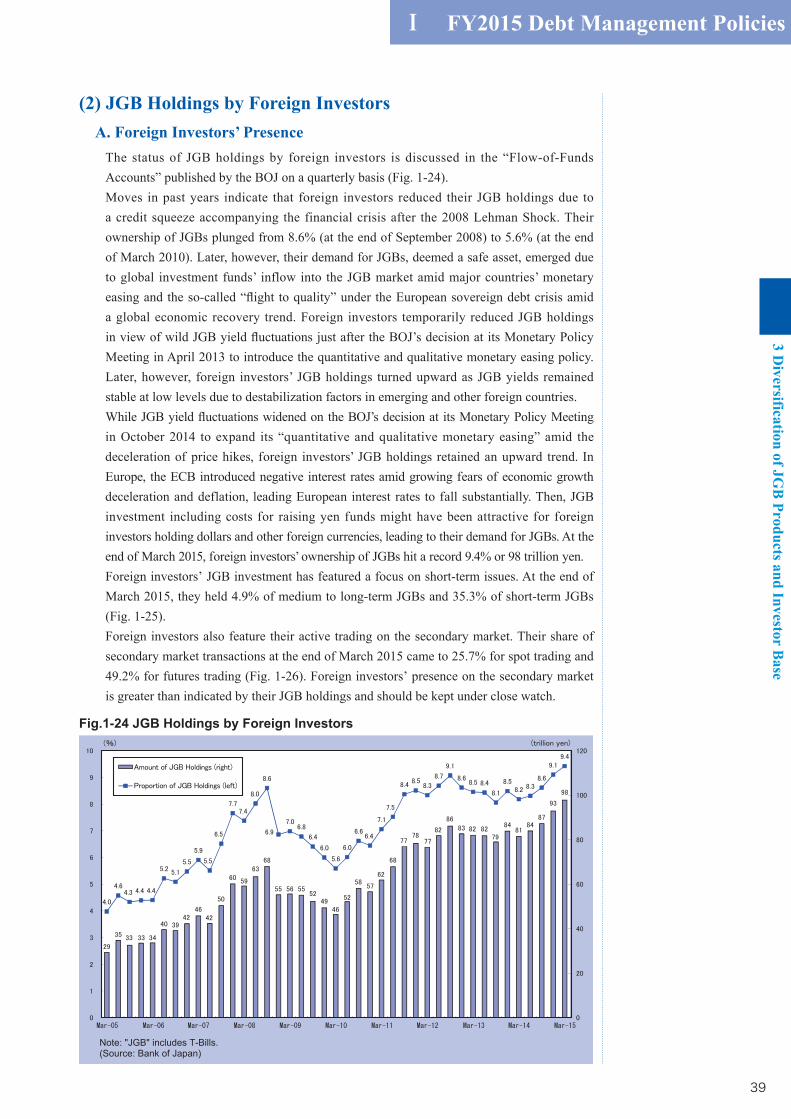

(2) JGB Holdings by Foreign InvestorsA. Foreign Investors’ Presence

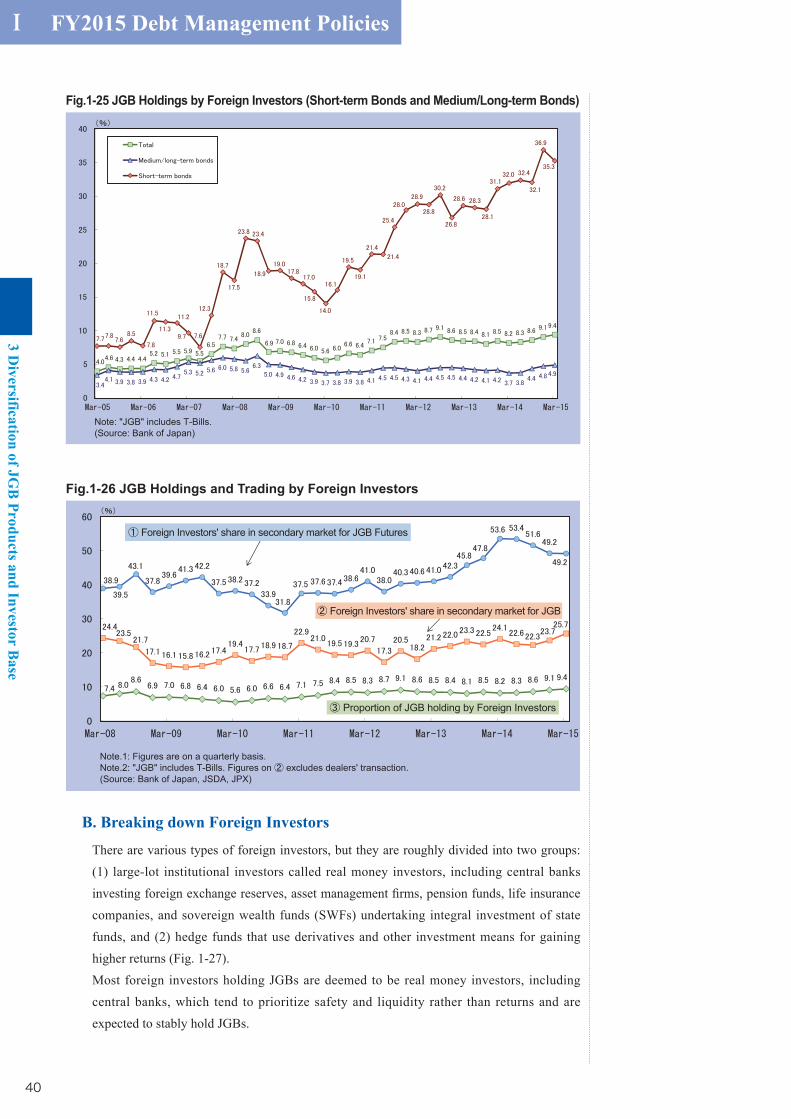

The status of JGB holdings by foreign investors is discussed in the “Flow-of-Funds Accounts” published by the BOJ on a quarterly basis (Fig. 1-24).Moves in past years indicate that foreign investors reduced their JGB holdings due to a credit squeeze accompanying the financial crisis after the 2008 Lehman Shock. Their ownership of JGBs plunged from 8.6% (at the end of September 2008) to 5.6% (at the end of March 2010). Later, however, their demand for JGBs, deemed a safe asset, emerged due to global investment funds’ inflow into the JGB market amid major countries’ monetary easing and the so-called “fl ight to quality” under the European sovereign debt crisis amid a global economic recovery trend. Foreign investors temporarily reduced JGB holdings in view of wild JGB yield fl uctuations just after the BOJ’s decision at its Monetary Policy Meeting in April 2013 to introduce the quantitative and qualitative monetary easing policy. Later, however, foreign investors’ JGB holdings turned upward as JGB yields remained stable at low levels due to destabilization factors in emerging and other foreign countries.While JGB yield fl uctuations widened on the BOJ’s decision at its Monetary Policy Meeting in October 2014 to expand its “quantitative and qualitative monetary easing” amid the deceleration of price hikes, foreign investors’ JGB holdings retained an upward trend. In Europe, the ECB introduced negative interest rates amid growing fears of economic growth deceleration and deflation, leading European interest rates to fall substantially. Then, JGB investment including costs for raising yen funds might have been attractive for foreign investors holding dollars and other foreign currencies, leading to their demand for JGBs. At the end of March 2015, foreign investors’ ownership of JGBs hit a record 9.4% or 98 trillion yen.Foreign investorsʼ JGB investment has featured a focus on short-term issues. At the end of March 2015, they held 4.9% of medium to long-term JGBs and 35.3% of short-term JGBs (Fig. 1-25).Foreign investors also feature their active trading on the secondary market. Their share of secondary market transactions at the end of March 2015 came to 25.7% for spot trading and 49.2% for futures trading (Fig. 1-26). Foreign investorsʼ presence on the secondary market is greater than indicated by their JGB holdings and should be kept under close watch.

Fig.1-24 JGB Holdings by Foreign Investors

Note: "JGB" includes T-Bills.(Source: Bank of Japan)

Ⅰ FY2015 Debt Management Policies

3 Diversification of JG

B Products and Investor B

ase

40

B. Breaking down Foreign Investors

There are various types of foreign investors, but they are roughly divided into two groups:

(1) large-lot institutional investors called real money investors, including central banks

investing foreign exchange reserves, asset management fi rms, pension funds, life insurance

companies, and sovereign wealth funds (SWFs) undertaking integral investment of state

funds, and (2) hedge funds that use derivatives and other investment means for gaining

higher returns (Fig. 1-27).

Most foreign investors holding JGBs are deemed to be real money investors, including

central banks, which tend to prioritize safety and liquidity rather than returns and are

expected to stably hold JGBs.

Fig.1-25 JGB Holdings by Foreign Investors (Short-term Bonds and Medium/Long-term Bonds)

Note: "JGB" includes T-Bills.(Source: Bank of Japan)

Fig.1-26 JGB Holdings and Trading by Foreign Investors

Proportion of JGB holding by Foreign Investors

Note.1: Figures are on a quarterly basis.Note.2: "JGB" includes T-Bills. Figures on excludes dealers' transaction.(Source: Bank of Japan, JSDA, JPX)

Foreign Investors' share in secondary market for JGB Futures

Foreign Investors' share in secondary market for JGB

Ⅰ FY2015 Debt Management Policies3 D

iversification of JGB

Products and Investor Base

41

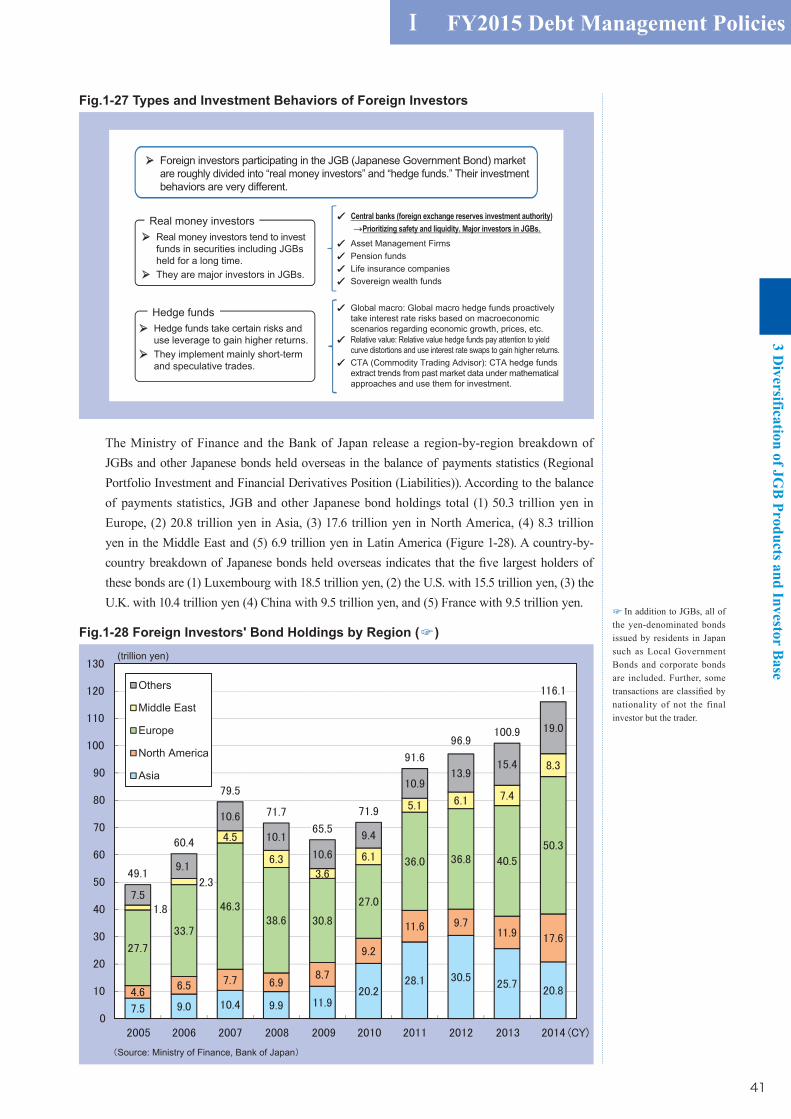

The Ministry of Finance and the Bank of Japan release a region-by-region breakdown of JGBs and other Japanese bonds held overseas in the balance of payments statistics (Regional Portfolio Investment and Financial Derivatives Position (Liabilities)). According to the balance of payments statistics, JGB and other Japanese bond holdings total (1) 50.3 trillion yen in Europe, (2) 20.8 trillion yen in Asia, (3) 17.6 trillion yen in North America, (4) 8.3 trillion yen in the Middle East and (5) 6.9 trillion yen in Latin America (Figure 1-28). A country-by-country breakdown of Japanese bonds held overseas indicates that the fi ve largest holders of these bonds are (1) Luxembourg with 18.5 trillion yen, (2) the U.S. with 15.5 trillion yen, (3) the U.K. with 10.4 trillion yen (4) China with 9.5 trillion yen, and (5) France with 9.5 trillion yen.

☞ In addition to JGBs, all of the yen-denominated bonds issued by residents in Japan such as Local Government Bonds and corporate bonds are included. Further, some transactions are classifi ed by nationality of not the final investor but the trader.

Fig.1-27 Types and Investment Behaviors of Foreign Investors

Foreign investors participating in the JGB (Japanese Government Bond) marketare roughly divided into “real money investors” and “hedge funds.” Their investmentbehaviors are very different.

Hedge funds take certain risks anduse leverage to gain higher returns.They implement mainly short-termand speculative trades.

Hedge funds

Real money investors tend to investfunds in securities including JGBsheld for a long time.They are major investors in JGBs.

Real money investors Central banks (foreign exchange reserves investment authority)Prioritizing safety and liquidity. Major investors in JGBs.

Asset Management FirmsPension fundsLife insurance companiesSovereign wealth funds

Global macro: Global macro hedge funds proactively take interest rate risks based on macroeconomic scenarios regarding economic growth, prices, etc.Relative value: Relative value hedge funds pay attention to yieldcurve distortions and use interest rate swaps to gain higher returns.CTA (Commodity Trading Advisor): CTA hedge funds extract trends from past market data under mathematical approaches and use them for investment.

Fig.1-28 Foreign Investors' Bond Holdings by Region (☞ )(trillion yen)

Others

Middle East

Europe

North America

Asia

Source: Ministry of Finance, Bank of Japan

Ⅰ FY2015 Debt Management Policies

3 Diversification of JG

B Products and Investor B

ase

42

C. Overseas Investor Relations Efforts

Since 2005, the Ministry of Finance has made efforts to enhance relations with foreign investors in JGBs (investor relations activities). The activities aim to diversify the JGB investor base, including foreign investors, for the purpose of stabilizing the JGB market and provide accurate information on a timely basis that meets investorsʼ needs for the purpose of encouraging them to hold JGBs longer and more stably (Fig. 1-29).

In overseas IR activities, we provide various types of investors with information meeting their needs in a fine-tuned manner. For example, central banks are usually and strongly interested in macroeconomic trends and political and diplomatic situations. Institutional investors frequently take up technical matters including JGB characteristics, JGB issuance sizes, JGB issuance plans and the JGB market. Particularly, they seemingly have great interests in market liquidity changes after the implementation of the quantitative and qualitative monetary easing policy and responses to these changes.We have adopted overseas IR activity methods meeting investorsʼ needs, based on trends of overseas investors and market environment changes as well as opinions at such forums as the Advisory Council on Government Debt Management. Initially, we mainly sponsored seminars for a large number of investors at various locations to improve foreign investorsʼ awareness of JGBs. Over recent years, we have not only held seminars but also visited investors in response to improvements in foreign investorsʼ awareness of JGBs. Our direct talks with overseas investors allow us to grasp and respond to investorsʼ needs in a fine-tuned manner and are significant for promoting their understanding of JGBs.

In FY2014, we implemented a total of 10 overseas IR tours for interviews with and seminars for local investors, covering 32 cities of 23 countries in North America, Europe, Asia, etc. In a high-level effort, then State Minister of Finance Yoshihisa Furukawa visited Indonesia and Singapore in June for meetings with the Indonesian central bank chief and the Singapore deputy prime minister (Fig. 1-30). We also participated in international conferences and seminars sponsored by private sector companies, making presentations about Japanese government debt management policy. In addition, we cooperated with the Asian Development Bank to proactively give Asia-Pacific economy-related people explanations about JGBs, considering that Asian investors have rapidly increased investment in Japanese bonds over recent years.

Fig.1-29 Significance and Objectives of Overseas IR Activities

Fig.1-30 Investor Relations Tours(June 2014, Singapore (Yoshihisa Furukawa, State Minister of Finance)

海外IRの目的及び方針

海外投資家は、現在、国内流通市場において活発な取引を行っている。また、これまで国債は国内金融機関を通じて安定的に消化されてきたが、急速な人口の高齢化に伴い家計貯蓄が伸び悩む等、国債の国内における消化を支えてきた諸環境は今後変化していく可能性があり、海外保有比率も上昇していく可能性がある。

こうした状況を踏まえて、引き続き国内での国債消化を重視しつつも、海外IRにおいては、海外投資家の国債に対する正確な理解を促進しつつ、海外投資家の動向・ニーズを的確に把握するとともに、投資家層の多様化により国債の安定消化を図る観点から実施。

国債管理政策に加えて、広く日本の経済政策や財政健全化の取組み等に関しても情報発信を強化。

海外中央銀行(外貨準備)、年金基金、生命保険など国債の安定的な保有が見込まれる投資家を重視。

欧米に加えて、アジア地域・新興国向けのIRを一層強化。

個別投資家との面談を通じて、投資家のニーズを踏まえた的確な情報提供・情報収集。セミナー方式やニュースレターの送信等の方法を適宜組みあわせ、費用対効果の高い海外IRを実施

海外投資家等から得られた情報について、関係部局で幅広く共有。

各国の国債管理当局や国際機関、海外中央銀行との関係強化。

(「国の債務管理の在り方に関する懇談会」議論の整理(平成26年6月18日)をまとめたもの)

1

海外IRの実施方針

海外IRの目的

(Excerpts from documents distributed at the Advisory Council on Government Debt Management (36th Round) on April 17, 2015)

� Foreign investors are trading JGBs actively in the Japanese secondary market. Current stable holdings of JGBs by domestic financial institutions may undergo changes in the future due to factors such as stagnant household savings. Therefore, the ratio of JGBs held by foreign investors may increase in the future.

� We are implementing overseas IR activities with a view to improving foreign investors’ awareness of JGBs, grasping trends in their investments and needs, and ensuring stable issuance of JGBs by diversifying the investor base, while continuing to acknowledge the importance of domestic holdings of JGBs.

( Excerpts from documents distributed at The Advisory Council on Government Debt Management(36th Round) on April 17, 2015)

Objectives of Overseas IR Activities

� Foreign investors are trading JGBs actively in the Japanese secondary market. Current stable holdings of JGBs by domestic financial institutions may undergo changes in the future due to factors such as stagnant household savings. Therefore, the ratio of JGBs held by foreign investors may increase in the future.

� We are implementing overseas IR activities with a view to improving foreign investors’ awareness of JGBs, grasping trends in their investments and needs, and ensuring stable issuance of JGBs by diversifying the investor base, while continuing to acknowledge the importance of domestic holdings of JGBs.

( Excerpts from documents distributed at The Advisory Council on Government Debt Management(36th Round) on April 17, 2015)

Objectives of Overseas IR Activities

海外IRの目的及び方針

海外投資家は、現在、国内流通市場において活発な取引を行っている。また、これまで国債は国内金融機関を通じて安定的に消化されてきたが、急速な人口の高齢化に伴い家計貯蓄が伸び悩む等、国債の国内における消化を支えてきた諸環境は今後変化していく可能性があり、海外保有比率も上昇していく可能性がある。

こうした状況を踏まえて、引き続き国内での国債消化を重視しつつも、海外IRにおいては、海外投資家の国債に対する正確な理解を促進しつつ、海外投資家の動向・ニーズを的確に把握するとともに、投資家層の多様化により国債の安定消化を図る観点から実施。

国債管理政策に加えて、広く日本の経済政策や財政健全化の取組み等に関しても情報発信を強化。

海外中央銀行(外貨準備)、年金基金、生命保険など国債の安定的な保有が見込まれる投資家を重視。

欧米に加えて、アジア地域・新興国向けのIRを一層強化。

個別投資家との面談を通じて、投資家のニーズを踏まえた的確な情報提供・情報収集。セミナー方式やニュースレターの送信等の方法を適宜組みあわせ、費用対効果の高い海外IRを実施

海外投資家等から得られた情報について、関係部局で幅広く共有。

各国の国債管理当局や国際機関、海外中央銀行との関係強化。

(「国の債務管理の在り方に関する懇談会」議論の整理(平成26年6月18日)をまとめたもの)

1

海外IRの実施方針

海外IRの目的海外IRの目的及び方針

海外投資家は、現在、国内流通市場において活発な取引を行っている。また、これまで国債は国内金融機関を通じて安定的に消化されてきたが、急速な人口の高齢化に伴い家計貯蓄が伸び悩む等、国債の国内における消化を支えてきた諸環境は今後変化していく可能性があり、海外保有比率も上昇していく可能性がある。

こうした状況を踏まえて、引き続き国内での国債消化を重視しつつも、海外IRにおいては、海外投資家の国債に対する正確な理解を促進しつつ、海外投資家の動向・ニーズを的確に把握するとともに、投資家層の多様化により国債の安定消化を図る観点から実施。

国債管理政策に加えて、広く日本の経済政策や財政健全化の取組み等に関しても情報発信を強化。

海外中央銀行(外貨準備)、年金基金、生命保険など国債の安定的な保有が見込まれる投資家を重視。

欧米に加えて、アジア地域・新興国向けのIRを一層強化。

個別投資家との面談を通じて、投資家のニーズを踏まえた的確な情報提供・情報収集。セミナー方式やニュースレターの送信等の方法を適宜組みあわせ、費用対効果の高い海外IRを実施

海外投資家等から得られた情報について、関係部局で幅広く共有。

各国の国債管理当局や国際機関、海外中央銀行との関係強化。

(「国の債務管理の在り方に関する懇談会」議論の整理(平成26年6月18日)をまとめたもの)

1

海外IRの実施方針

海外IRの目的

Ⅰ FY2015 Debt Management Policies3 D

iversification of JGB

Products and Investor Base

43

We also prioritize lectures at seminars for foreign investors and direct talks with foreign investors visiting Japan. At seminars held in Japan for foreign investors, senior MOF officials gave lectures emphasizing macroeconomic, fiscal consolidation and debt management policy. We implemented interviews with many foreign investors in FY2014 (Fig. 1-31) as investors increasingly requested meetings with MOF offi cials in response to their growing interest in the Japanese economy in recent years. Through these IR activities, we have received various questions and opinions from foreign investors. These opinions are refl ected in our policies and used effectively (Fig. 1-32).

In this way, the IR activities play a role in giving direct messages to investors about accurate information on Japanese government debt management and economic policies on behalf of the Japanese government, responding to wide-ranging and deep needs for information on not only JGBs but also the economy and fi scal situation. In July 2014, the Ministry of Finance established the Offi ce of Debt Management and JGB Investor Relations in Debt Management Policy Division to enhance communications arrangements to secure even more effective and effi cient IR activities in cooperation with research and analysis offi ces (Fig. 1-33).

Note: These figures are limited to meetings arranged by Office of Debt Management and JGB Investor Relations.

27

56 59

2012 2013 2014 (CY)

Fig.1-31 Interviews with Foreign Investors in Japan Fig.1-32 Major Opinions from Foreign Investors and Responses

Fig.1-33 Future IR Activities Direction

Enhancing communications Explain the key points, points to be emphasized regarding IR activities and points to be highlighted as government debt management, by takinginto account the trends of foreign investors and analysis of their views onJapanese economic policy.Provide investors who are very influential in the secondary market witha wide range of accurate information on JGBs.Improve the current English newsletters.Visit the Japan offices of foreign investors, and implement new IR activities such as video conferences.

Further enhancing IR activities inAsian and emerging countries

Further enhance IR activities for Asia in view of high growth potential in the area.Build a forward-looking network in a strategic manner with investors in emerging countries of great potential.

Enhancing relations with long-term JGB holders

Promote strategic IR activities by giving priority to foreign exchange reserves authorities, pension funds, and other foreign institutional investorsexpected to hold JGB over a long time.Exchange opinions regularly with foreign central banks and their Tokyo offices to enhance relations with them.

Enhancing cooperation with foreign debt management offices and international organizations

Strengthen relations with foreign debt management authorities by exchanging information through IR activities and by attending internationalconferences.Enhance cooperation with international organizations by proactivelyimplementing presentations for foreign authorities and investors at seminars and other meetings hosted by these organizations.

sesnopseRsrotsevni ngierof morf snoinipO

The settlement interval should be shortened In April 2012, the interval between the JGB auction date and issue date in the primary market was shortened from “the auction day plus 3 days” to “the auction day plus 2 days” to meet the secondary market rule.

Information services regarding JGBs, the Japanese economy, macroeconomic policies and other matters should be expanded

Regular provision of newsletters, etc.In response to investors’ interests, the MOF provides up-to-date information on the Japanese economy and macroeconomic policies.

Japan should resume and expand Inflation-Indexed Bonds issuance that have obtained major positions in other advanced countries

In October 2013, the MOF resumed an Inflation-Indexed Bonds issuance with a principal guarantee (deflation floor) upon maturity. In the FY 2014 and FY 2015 JGB Issuance Plan, Inflation-Indexed Bonds issuance is expanded.

Other major opinionsIs there any target for foreign investors’ share of JGB holdings? Is there any target for an average maturity of JGBs? How are Japanese macroeconomic policy prospects (fiscal and monetary policies, growth strategies, the balance of payments, etc.)? Is there any plan to issue JGBs under the Islamic bond system?