3. 25 landmarks in corporate governance

TRANSCRIPT

Landmarks in the Emergence of Corporate

Governance

Corporate Governance Committees

Over a period of time, a change had come in the perception of people about corporate governance from the exclusive benefits of shareholders to the benefit of all stakeholders.

Corporate governance gained importance in the US after the Watergate scandal that involved US corporates making political contributions and offering bribes to government officials

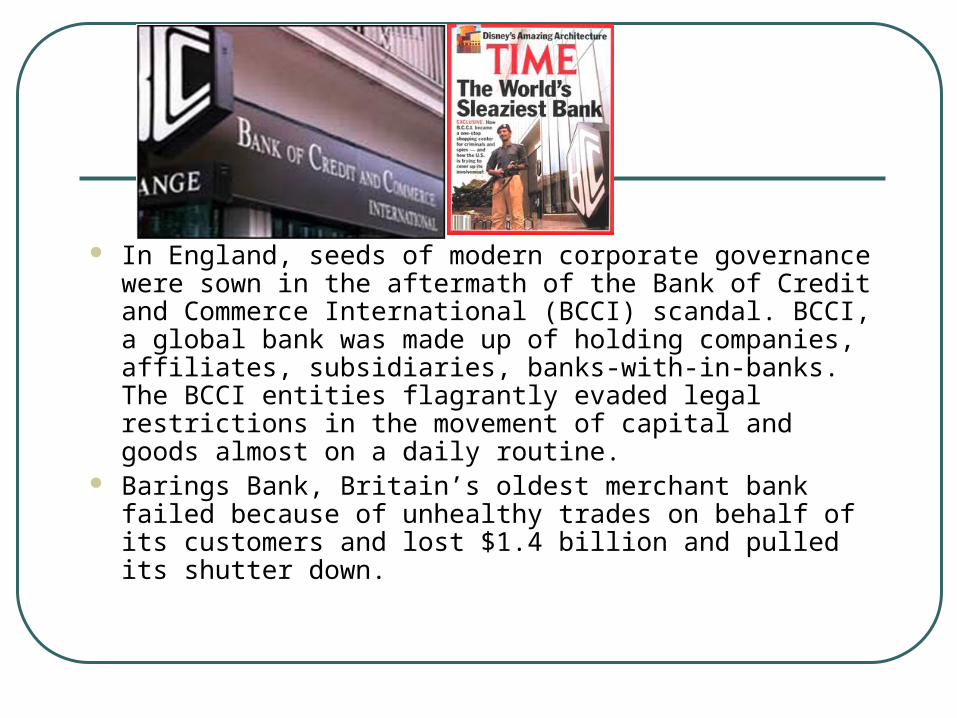

In England, seeds of modern corporate governance were sown in the aftermath of the Bank of Credit and Commerce International (BCCI) scandal. BCCI, a global bank was made up of holding companies, affiliates, subsidiaries, banks-with-in-banks. The BCCI entities flagrantly evaded legal restrictions in the movement of capital and goods almost on a daily routine.

Barings Bank, Britain’s oldest merchant bank failed because of unhealthy trades on behalf of its customers and lost $1.4 billion and pulled its shutter down.

Corporate Governance Committees

Throughout the US, UK, and other countries a number of committees got appointed to recommend reforms and regulations in corporate governance. They are all known by the names of the individuals that had chaired the committees.

The Cadbury Committee on Corporate Governance, 1992 - Sir Adrian Cadbury

Stated Objective was “to help raise the standards of corporate governance and the level of confidence in financial reporting and auditing by setting out clearly what it sees as the respective responsibilities of those involved and what it believes is expected of them”.

The Cadbury committee investigated the accountability of the board of directors to shareholders and to the society. The Cadbury Code of best Practices had 19 recommendations in the nature of guidelines to the board of directors, non-executive directors, executive directors and such other officials.

The Paul Ruthman Committee The Greenbury Committee, 1995 The Ron Hampel Committee, 1995 The Combined Code (1998) was derived from

Hampel’s report, Cadbury report, and Greenbury report. The combined is mandatory for all listed companies in the UK. The stipulations of the combined code required the boards should maintain a sound system of internal to safeguard the shareholders’ investment and company assets.

The directors should annually conduct a review of the effectiveness of the group’s system of internal control covering all controls , including financial, operational, and compliance and risk management, and report to the shareholders that they have done so.

The Turnbull Committee (1999) was set up by the Institute of Chartered Accountants in England and Wales to provide guidance to assist companies in implementing the requirements of the Combined Code relating to internal control.

World Bank guidelines for Corporate Governance

The world bank report on corporate governance recognizes the complexity of the very concept of corporate governance and focuses on the principles such as transparency, accountability, fairness, and responsibility which are universally applicable.

It could be argued that international investors and capital markets are bringing about a degree of convergence over governance practices worldwide.

Corporate governance ideally should hold the balance between economic and social goals and between individual and communal goals. The governance should encourage the efficient use of resources and equally to require accountability for the stewardship of those resources.

States would permit investments from the global corporations if only their activities would encourage economic development and discourage fraud and mismanagement. The foundation of any corporate governance structure has to be disclosure as openness is the basis of public confidence in the corporate system and funds will flow to the those centers of economic activity which inspire trust.

The Organization for Economic Cooperation and development (OECD)

The Organization for Economic Co-operation and Development (OECD) is an international organization of 30 countries that accept the principles of representative democracy and free-market economy. Most OECD members are high-income economies with a high HDI and are regarded as developed countries.

The Organization for European Economic Co-operation (OEEC) was founded in 1948 to help Marshall Plan for the reconstruction of Europe after World War II. The headquarters was in the Chateau de la Muette in Paris, France. As the Marshall Plan was out of date , the OEEC focused on economic questions

The OECD, a non-governmental body spelled out recommendations providing voluntary principles and standards for responsible business conduct for multinational corporations operating in or from countries adhered to the Declaration. The Guidelines are legally non-binding. Originally the Declaration and the Guidelines were adopted by the OECD on 1976 and revised on 1979, 1982, 1984, 1991 and 2000.

OECD spelled out principles and practices that should govern corporates in their goals to attain long-tern shareholder value.

OECD recommendations contained following aspects of corporate governance:

Rights of shareholders Equitable treatment of all shareholders Role of stakeholders in corporate governance Disclosure and transparency Responsibilities of the board

McKinsey Survey on Corporate Governance

McKinsey, the international management consultant organization, conducted a survey with a sample size of 188 companies from six emerging markets (India, Malaysia, Mexico, South Korea, Taiwan, and Turkey) to determine the correlation between good corporate governance and the market valuation of the company. The results of the survey pointed out a positive correlation between the two.

McKinsey had evaluated the performance of the companies based on:

Accountability: transparent ownership, board size, board accountability, ownership neutrality

Disclosure and transparency of the board: timely and accurate, independent directors

Shareholder equality: one share-one vote

Following results of the survey indicated that good corporate governance increased market valuation

Increasing financial performance Transparency of dealing, thereby reducing

the risks the boards will serve their own self-interest

Increasing investor confidence

Sarbanes-Oxley Act, 2002

Sox came into existence after a series of corporate scandals in the US. The act calls for protection to those who have the courage to expose frauds. It is an attempt to address all issues associated with failures to achieve quality governance and to restore investor’s confidence.

Important provisions of SOX

1. Establishment of Public Company Accounting Oversight Board (PCAOB) – all accounting firms are to register with this Board. The accounting firms have to provide details of fees collected for audit and non-audit services, financial information of the firms, staff details etc. The board will conduct periodical inspections of the firms.

The Board reports to US Securities & Exchange Commission (SEC)

2. The SOX provides for a new improved audit committee – committees composed of independent directors – are responsible for appointment, fixing fees, and oversight of the work of the independent auditors

3. Conflict of interests – firms should not perform any audit services to a company wherein its CEO, CFO, etc were working for the accounting firms one year prior to the initiation of audit

4. Audit partner rotation of lead/coordinating partner of the accounting firm once every 5 years

5. Improper influence on conduct of audits – unlawful for any executive or director of the company to fraudulently influence, coerce, manipulate, or mislead any auditor engaged in auditing

6. Prohibition of non-audit services- auditors prohibited from providing non-audit services concurrently with audit financial services review

7. CEOs and CFOs required to affirm/certify financials filed with SEC. If there are instances of ‘material’ non-compliance as result of misconduct, the CEOs/CFOs will have to return to the company bonuses and incentives received. False and improper certification can invite fines like $1 million to 5 million or up to 10 years imprisonment

8. Loans to Directors- Companies making or arranging new personal loans. Existing loans

may be found okay unless material modifications or renewable of loans are involved.

9. Attorneys dealing with the publicly traded companies are required to report evidence of material violation of securities law or breach of fiduciary duty or similar violations by the firms

10. The SOX requires disclosure of conflict of interests by the securities analysts and brokers and dealers whether: Do they have investments in the companies Any compensation received by them are appropriate in

the public interest and consistent with the protection investors

The company (issuer) has been a client of the broker or dealer

Etc.

Penalties

Penalties prescribed under SOX for any wrong doing is very stiff. Penalties for willful violations are even stiffer.

Indian Committees and Guidelines