201703 b pyxis tankers - company presentation

TRANSCRIPT

COMPANY PRESENTATION March 2017

2

DISCLAIMER FORWARD-LOOKING STATEMENTS & INFORMATION

This presentation contains forward-looking statements and forward-looking information within the meaning of

applicable securities laws. The use of any of the words “expected'', “create”, “scheduled”, “anticipated”, “outlook”,

“grow”, “meet”, “maintain”, “potential”, “continue”, “may”, “will”, “positioned”, “possible”, “believe”, “expand” and

variations of these terms and similar expressions, or the negative of these terms or similar expressions, are intended to

identify forward-looking, information or statements. Forward-looking information is based on the opinions, expectations

and estimates of management of Pyxis Tankers Inc. (“we” or “our”) at the date the information is made, and is based

on a number of assumptions and subject to a variety of risks and uncertainties and other factors that could cause

actual events or results to differ materially from those projected in the forward-looking information. Although we believe

that the expectations and assumptions on which such forward-looking statements and information are based are

reasonable, you should not place undue reliance on the forward-looking statements and information because we

cannot give any assurance that they will prove to be correct. Since forward-looking statements and information

address future events and conditions, by their very nature they involve inherent risks and uncertainties and actual results

and future events could differ materially from those anticipated in such information. Factors that might cause or

contribute to such discrepancy include, but are not limited to, the risk factors described in our Annual Report on Form

20-F for the year ended December 31, 2016 and other filings with the Securities and Exchange Commission (the “SEC”).

The forward-looking statements and information contained in this presentation are made as of the date hereof. We do

not undertake any obligation to update publicly or revise any forward-looking statements or information, whether as a

result of new information, future events or otherwise, except in accordance with U.S. federal securities laws and other

applicable securities laws.

This presentation and any oral statements made in connection with it are for informational purposes only and do not

constitute an offer to buy or sell our securities. For more complete information about us, you should read the information

in this presentation together with our filings with the SEC, which may be accessed at the SEC’s website

(http://www.sec.gov).

3

COMPANY HIGHLIGHTS EMERGING GROWTH - PURE PLAY PRODUCT TANKER COMPANY

►Disciplined, substantially fixed cost structure creates greater earnings power when

rates improve

►Competitive total daily operational costs to peer group

►Moderate capitalization with low cost, long-lived bank debt

►Strong management team with 100+ years of combined industry and capital

markets experience

►Founder/CEO has proven track record and is a substantial shareholder

►Board Members consist of prominent industry figures and/or with significant

experience

►Focus on modern medium range (“MR”) product tankers with “eco” features

►Young tanker fleet of six IMO-certified vessels with weighted average age of 6.0

years (dwt)

►Management may pursue a sale or other strategy relating to the small tankers

►Long-standing relationships with reputable, first-class customers worldwide

►As of March 24, 2017, 39% of remaining available chartering days in 2017 are

covered

►Positioned to capitalize when spot rates improve

Attractive, Modern

Fleet

Reputable Customer

Base & Diversified

Chartering Strategy

Competitive Cost

Structure &

Moderate

Capitalization

Experienced,

Incentivized

Management

& Board

4

►Expand fleet by targeting balanced capital structure of debt and equity

►Maintain commercial banking and expand capital markets relationships

►Meet charterers’ preference for modern and eco tankers, which offer more

operating reliability and efficiency

►Maintain high standards to ensure high level of safety, customer service and

support, while continuing ship level financial discipline

►Focus on acquisition of IMO II and III MR2 class product tankers of eight

years of age or less built in Tier 1 Asian shipyards Grow the Fleet

Opportunistically

Maintain Financial

Flexibility

Focus on the Needs

of our Customers

COMPANY STRATEGY QUALITY, GROWTH, SERVICE & FLEXIBILITY

►Employ vessels primarily through time charters and on the spot market

►Maintain optionality – significant spot exposure currently offers upside during

periods of market strength

►Diversify charters by customer and staggered duration

Utilize Portfolio

Approach to

Commercial

Management

5

FLEET & EMPLOYMENT OVERVIEW POSITIONED FOR UPSIDE OPPORTUNITIES

Our mixed chartering strategy provides upside opportunities through spot trading when rates improve and

stable, visible cash flows from time charters

Vessel Shipyard Vessel

Type Size (dwt) Year Built

Type of

Charter

Anticipated

Redelivery Date (1)

Pyxis Epsilon SPP / S.Korea MR 50,295 2015 Time Dec. 2017

Pyxis Theta SPP / S.Korea MR 51,795 2013 Spot N/A

Pyxis Malou SPP / S.Korea MR 50,667 2009 Spot N/A

Pyxis Delta Hyundai / S.Korea MR 46,616 2006 Time Sep. 2017

Northsea Alpha (2) Kejin / China Small Tanker 8,615 2010 Spot N/A

Northsea Beta (2)(3) Kejin / China Small Tanker 8,647 2010 Time Sep. 2017

Fleet Details

Fleet Employment Overview

(1) These tables are dated as of March 24, 2017 and show gross rates and do not reflect commissions payable.

(2) Management may pursue sale or other long-term strategy for small tankers.

(3) Northsea Beta’s charterer has an option to extend the charter for six additional months at the same charter rate. We may also withdraw the vessel from this charter

upon 30 days’ notice in the event of a sale of the vessel.

As of March 24, 2017, 39% of anticipated available days for the remainder of 2017 are covered.

Vessel 2017

Pyxis Epsilon $13,350 / Day

Pyxis Theta N/A

Pyxis Malou N/A

Pyxis Delta $13,125 / Day

Northsea Alpha N/A

Northsea Beta $7,650 / Day

Fixed Employment Charterers Optional Period Open Days

6

SHIPYARDS BANKS

STRONG RELATIONSHIPS QUALITY VESSELS & OPERATIONS BLUE CHIP CUSTOMERS ATTRACTIVE LENDING TERMS

CUSTOMERS

7

SENIOR MANAGEMENT EXPERIENCED TEAM WITH DECADES OF EXPERIENCE

► Joined Pyxis affiliates in 2013; 19+ years experience in strategic corporate shipping transactions

► Previous 5 years securities and M&A partner at Watson Farley & Williams with particular focus in

shipping industry

► Advised on complex international corporate shipping transactions in New York offices of Orrick,

Herrington & Sutcliffe LLP and Healy & Baillie, LLP and in New York and London offices of Weil, Gotshal

& Manges LLP since 1997

► Former member of Board of Governors & Vice President of the Connecticut Maritime Association

► Joined Pyxis affiliates in 2008; 25+ years of experience in the shipping industry

► Co-founder of Navbulk Shipping S.A., a start-up dry bulk company

► 5 years as Financial Director of Neptune Lines, a car carrier company

► 16 years in various financial and operational positions for other ship owning and services companies

► 25+ years of experience in owning, operating and managing within various shipping sectors,

including product, dry bulk, chemical, as well as salvage and towage

► Founder of Pyxis Tankers in 2015 and Pyxis Maritime Corp. in 2007

► For the last 16 years, Managing Director & Principal of KONKAR SHIPPING AGENCIES S.A., an Athens-

based dry bulk owner-operator established in 1968

► Joined Pyxis affiliates in 2015; 35 years of commercial, investment and merchant banking experience

► Previous investment banking positions include Nordea Markets (Oslo & NY)–Global Sector Head-

Shipping, and Oppenheimer (NY)–Head of Energy & Transportation

Antonios “Tony”

Backos

SVP for Corporate

Development, General Counsel &

Secretary

Konstantinos

“Kostas” Lytras

Chief Operating

Officer

Valentios “Eddie”

Valentis

Chairman & CEO

Henry Williams

CFO & Treasurer

8

PYXIS ORGANIZATIONAL STRUCTURE LEAN, EFFICIENT ORGANIZATIONAL STRUCTURE

Administrative, Commercial &

Ship Management Services (1)

Administrative & Ship

Management Fees

(1) As an affiliate, provides the commercial management for the fleet and supervises the crewing and technical management performed by ITM for all our vessels

(2) Provides technical management for all our vessels

Technical

Management (2)

Quality, Cost Effective Ship Management ►Streamlined structure minimizes costs and allows management to focus on creating

long term shareholder value

►Very competitive ship management fees @ $750/day/vessel provide safe and efficient

operating results compared to peers

MARKET OVERVIEW PRODUCT TANKER INDUSTRY

10

PRODUCT MARKETS OVERVIEW REFINED PRODUCTS OVERVIEW

Source: Drewry

Bitumen

Fuel Oil

Cycle Oils

Diesel/Gasoil

Kerosene

Gasolines

Clean Condensates

Naphthas

Dirty

Products

Clean

Products

Veg

Oils/Chemicals

Crude

Most products tankers can switch

between clean and dirty products

when the tanks are carefully cleaned.

Gasoil is a good clean up cargo when

switching from dirty to clean products.

More sophisticated product tankers

work at this end of the market, some

with the ability to carry products and

certain chemicals.

Crude tankers carry only crude oil and

fuel oils.

Non-oil substances now covered by

revised IBC Code. To carry chemicals,

an IMO Certificate of Fitness is

required.

Refined Products

11

Increases in Long-Haul Routes

• Growth in net refining capacity

expected to further drive demand for

product tankers.

• Low crude / feedstock prices generate

incremental refinery demand.

• Arbitrage between markets create

further opportunities

PRODUCT MARKETS OVERVIEW EVOLVING TRADE LANDSCAPE

Source: Drewry, March 2017

12

PRODUCT MARKETS OVERVIEW CHANGING TRADE ROUTES & PETROLEUM REFINERY LANDSCAPE CREATING INCREMENTAL DEMAND

Source: Drewry, March 2017

* Compound annual growth rate

Mill

ion

To

ns

Billio

n To

n M

iles

Increases in Demand due to Changing Trade Routes & Refining Landscape

4.0% CAGR* in million tons of seaborne trade 5.6% CAGR in ton mile demand

1,500

1,700

1,900

2,100

2,300

2,500

2,700

2,900

3,100

600

650

700

750

800

850

900

950

1,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Seaborne Product Trade - Mil. Tons Ton Mile Demand - Bil. Ton Miles

13

PRODUCT MARKETS OVERVIEW REFINERY CAPACITY INCREASINGLY FURTHER AWAY FROM MANY END USERS

Source: Drewry, March 2017

Expected Petroleum Refinery Capacity Additions Driven by Non-OECD Growth & Exports

Mill

ion

Ba

rre

ls p

er

Da

y

0.0

0.5

1.0

1.5

2.0

2.5

2017 2018 2019 2020 2021

14

PRODUCT MARKETS OVERVIEW U.S. HAS BECOME MAJOR EXPORTER DUE TO SHALE OIL

Source: Drewry, March 2017

Mill

ion

Ba

rre

ls p

er

Da

y

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

United States Saudi Arabia India

15

PRODUCT MARKETS OVERVIEW PRODUCT TANKER VESSEL OVERVIEW

Class of Tanker Cargo Capacity (Dwt) Typical Use

Long Range 2 (LR2) 80,000 +

Short- to medium-haul refined petroleum products

transportations from the North Sea or West Africa to Europe or

the East Coast of the United States, from the Middle East Gulf to

the Pacific Rim.

Long Range 1 (LR1) 55,000 - 79,999Short- to medium-haul crude oil and refined petroleum products

transportations worldwide, mostly on regional trade routes.

Medium Range 2 (MR2) 37,000-54,999

Medium Range 1 (MR1) 25,000-36,999

Small 1,000 - 24,999Short-haul of mostly refined petroleum products worldwide,

usually on local or regional trade routes.

Flexible vessels involved in medium-haul petroleum products

trades both in the Atlantic Basin and the growing intra-

Asian/Middle East/ISC trades. MRs are the work horses of the

product trades.

Source: Drewry

16

Typical Atlantic Basin Triangulated Route

• Emerging markets in South America and

Africa have little to no refining capacity.

• U.S. exports to South America have

grown at CAGR of ~21.8% since 2006.

PRODUCT MARKETS OVERVIEW U.S. HAS BECOME MAJOR SUPPLIER IN ATLANTIC BASIC

Source: Drewry, March 2017

17

PRODUCT MARKETS OVERVIEW DECLINING ORDERBOOK (SUPPLY)

• Total MR vessel orderbook has fallen from a high of ~58% in 2008 of the then existing fleet to 5.3% of the current worldwide fleet, lowest since 2000.

• Record low ordering – 11 MR2’s since 1/1/16.

• Limited capacity additions scheduled beyond 2018 due to shipyard financial problems/restructurings/closures, limited availability of capital and would-be buyers exposure to weaker shipping segments.

• Worldwide MR fleet is expected to grow at an average of 2.2% per annum in 2017 and 2018, without giving effect to scrapping of older vessels and slippage of deliveries.

Product Tanker Delivery Schedule

Source: Drewry, March 2017

Nu

mb

er

of

Ve

sse

ls

0

20

40

60

LR1 MR2 MR1

2017 2018 2019 2020

18

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

< 5 Yrs 5-10 Yrs 10-15 Yrs 15-20 Yrs 20-25 Yrs 25+ Yrs

MR1 MR2 LR1

PRODUCT MARKETS OVERVIEW SCRAPPING IS INEVITABLE

Global Fleet Age Distribution by %

Source: Drewry, March 2017

• Average age of MR2 fleet is 9.5 years.

• 13.4% of MR2 fleet (215 ships) is greater than 20 years of age.

• Significant portion of the fleet is approaching the end of its useful life.

19

► Environmental regulations should lead to increased scrapping

• Besides aging of MR fleet, new IMO environmental regulations should

force owners to either scrap earlier or make significant vessel capital

expenditures

► Ballast Water Treatment System (“BWTS”)

• Ballast sea water is used to stabilize vessels and ensure structural integrity;

Pumped before/after cargo is loaded/unloaded

• Starting September 2017 at next vessel’s special survey, owners will have

to install approved BWTS, which removes inactive organisms from ballast

water prior to discharge

• Retrofits in older tankers can be challenging from a design/installation

standpoint and cost

• Depending on vessel, fully loaded installation costs are expected to be

between $0.50 million to $0.75 million for a MR tanker

► New stricter regulations on sulfur emissions starting January 2020

• Limits reduced from 3.5% to 0.5%

• Owners either i) install expensive scrubber ($3.0 million +) to burn current

grade of fuel, or ii) pay sizeable premium (currently ~ $200 per ton or

$6,000 per day) to burn marine gas oil (MGO) fuel and run vessel at

slower speed

PRODUCT MARKETS OVERVIEW NEW ENVIRONMENTAL REGULATIONS TO DRIVE MORE SCRAPPING

20

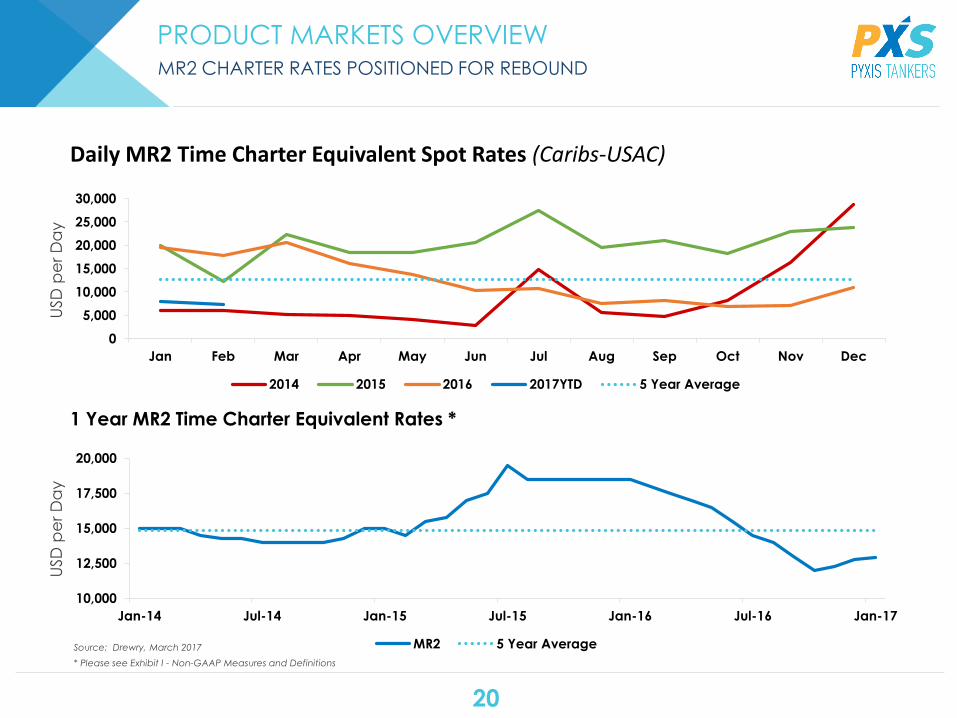

PRODUCT MARKETS OVERVIEW MR2 CHARTER RATES POSITIONED FOR REBOUND

Daily MR2 Time Charter Equivalent Spot Rates (Caribs-USAC)

1 Year MR2 Time Charter Equivalent Rates *

Source: Drewry, March 2017

* Please see Exhibit I - Non-GAAP Measures and Definitions

10,000

12,500

15,000

17,500

20,000

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

MR2 5 Year Average

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 2015 2016 2017YTD 5 Year Average

USD

pe

r D

ay

USD

pe

r D

ay

21

MR2 PRODUCT TANKER MARKET UPDATE POSITIVE NEAR-TERM OUTLOOK

► Current spot charter rates are depressed

► One year time charter rates bounced up in December 2016 but recently

softened $500/d to $12,750/d – still ~ 50% below post-recession high of

$25,000/d and 17% below 2008-16 average*

► Major reasons:

• higher inventories of refined products worldwide

• lack of arbitrage opportunities resulted in less trading

• new tonnage deliveries

► Near-term demand growth estimated at 2.5-3%/yr. led by increasing

global consumption of refined products, modest ton-mile expansion from

changing refinery landscape and increasing U.S. exports

► Net supply growth after new built deliveries, delays/cancellations and

increasing scrapping should result in a balanced supply/demand curve

leading to a better market by Q4 2017, and possible negative net fleet

growth thereafter

* Source: Drewry – March 2017, excludes Jones Act vessels

Positive industry

fundamentals

22

PRODUCT MARKETS OVERVIEW HISTORICAL LOW MR2 ASSET VALUES CREATE ATTRACTIVE ENTRY POINT

MR2 Asset Prices

* Source: Drewry, March 2017

** Exclusive of higher design specifications, yard supervision costs and spares

Type Current * Avg. 2006-16 *

New Build Construction (del. 2H‘18) $32.0 ** $39.5 **

5 yr. old $22.0 $32.900

15

25

35

45

55

65

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

NB Price NB Price Average 06-16 SH Price SH Price Average 06-16

USD

Mill

ion

PYXIS TANKERS FINANCIAL SUMMARY

24

AUDITED FINANCIAL HIGHLIGHTS YEAR ENDED DECEMBER 31, 2016

Year ended

December 31, 2016

In ‘000 USD except for daily TCE rates

Time / spot charter revenue mix 69% / 31%

Voyage revenues $30,710

Voyage related costs and commissions (6,611)

Time charter equivalent revenues *

$24,099

Net loss ** ($5,813)

Loss per share (basic & diluted) ** ($ 0.32)

Adjusted EBITDA* $6,999

Total operating days

1,986

Daily time charter equivalent rate *

$12,134

Fleet Utilization * 91.3%

* Please see Exhibit I – Non-GAAP Measures and Definitions

** Includes $4.0 million non-cash vessel impairment charge or $0.22 loss per share

Remaining time

charters mitigated

poor spot

environment

in 2H 2016

25

(amounts in $) Year Ended

December 31,

2015 2016

Eco-Efficient MR2: (2 units)

Average TCE * 15,631 15,015

Opex * 6,430 5,754

Utilization % 99.4% 97.0%

Eco-Modified MR2: (1 unit)

TCE 17,480 10,705

Opex 6,461 6,255

Utilization % 91.3% 92.9%

Standard MR2: (1 unit)

TCE 17,237 15,504

Opex 6,325 6,772

Utilization % 100.0% 90.5%

Small Tankers: (2 units)

Average TCE 7,622 7,939

Opex 5,358 5,315

Utilization % 98.6% 85.1%

Fleet: (6 units)

TCE 13,597 12,134

Opex 6,058 5,861

Utilization % 97.9% 91.3%

DAILY FLEET DATA YEAR ENDED DECEMBER 31, 2015 & 2016

* Please see Exhibit I – Non-GAAP Measures and Definitions

Consistent &

relatively low

vessel opex

26

TOTAL DAILY OPERATIONAL COSTS/ECO-VESSELS YEAR ENDED DECEMBER 31, 2016

Eco

Twelve Months ended December 31, 2016 Modified Efficient

(amounts in $/day)

Opex * $6,255 $5,754

Technical & commercial management fees 748 748

G&A expenses 1,172 1,172

Total daily operational costs per vessel $8,175 $7,674

* Please see Exhibit I - Non-GAAP Measures and Definitions

Our Eco MR2 tankers’

total daily operational

costs are very

competitive

27

CAPITALIZATION AT YEAR ENDED DECEMBER 31, 2016

At December 31, 2016

In ‘000 USD

Cash and cash equivalents, including restricted cash $ 5,783

Bank debt, net of deferred financing fees 73,430

Promissory note 2,500

Total funded debt $ 75,930

Stockholders' equity 48,753

Total capitalization $ 124,683

Net funded debt $ 70,147

Total funded debt / total capitalization 60.9%

Net funded debt / total capitalization 56.3%

Weighted average interest rate of total debt for the year ended December 31, 2016 was 3.27%

Moderate

leverage at

low interest costs

No balloon

payments until

Q3 2018

28

MANAGEMENT INCENTIVIZED TO ACHIEVE GROWTH FOUNDER/CEO’S SUBSTANTIAL SHAREHOLDINGS

►The shareholder base as of March 24, 2017 was:

Maritime Investors (affiliate of our CEO) 17,002,445 (93.0% of outstanding)

Public 1,275,448 (7.0%)

Total Shares Outstanding 18,277,893 (100%)

► Our common shares are listed on NASDAQ Capital Markets under trading symbol “PXS”

►Our Founder/CEO has substantial shareholdings and his interests are aligned with our

other shareholders

29

COMPANY HIGHLIGHTS EMERGING GROWTH - PURE PLAY PRODUCT TANKER COMPANY

Competitive Cost Structure & Moderate Capitalization

Experienced, Incentivized Management & Board

Attractive, Modern Fleet Including “Eco” Vessels

Reputable Customer Base & Diversified Chartering Strategy

- Currently Positioned for Upside

Industry Fundamentals Look Favorable

NON-GAAP MEASURES AND DEFINITIONS EXHIBIT I

31

EXHIBIT I | NON-GAAP MEASURES AND DEFINITIONS

(in thousands of U.S. Dollars)

Year ended December 31,

2016

Reconciliation of Net income / (loss) to Adjusted EBITDA

Net income / (loss) $ (5,813)

Depreciation 5,768

Amortization of special survey costs 236

Interest and finance costs, net 2,810

EBITDA $ 3,001

Vessel impairment charge 3,998

Adjusted EBITDA $ 6,999

32

EXHIBIT I | NON-GAAP MEASURES AND DEFINITIONS

Earnings before interest, taxes, depreciation and amortization (“EBITDA”) represents the sum of net income / (loss), interest and

finance costs, depreciation and amortization and, if any, income taxes during a period. Adjusted EBITDA represents EBITDA before

vessel impairment charge and stock compensation. EBITDA and Adjusted EBITDA are not recognized measurements under U.S.

GAAP. EBITDA and Adjusted EBITDA are presented as we believe that they provide investors with means of evaluating and

understanding how our management evaluates operating performance. These non-GAAP measures should not be considered in

isolation from, as substitutes for, or superior to financial measures prepared in accordance with U.S. GAAP. In addition, these non-

GAAP measures do not have standardized meanings, and are therefore, unlikely to be comparable to similar measures presented

by other companies.

Daily time charter equivalent (“TCE”) is a standard shipping industry performance measure of the average daily revenue

performance of a vessel on a per voyage basis. TCE is not calculated in accordance with U.S. GAAP. We utilize TCE because we

believe it is a meaningful measure to compare period-to-period changes in our performance despite changes in the mix of charter

types (i.e., spot charters, time charters and bareboat charters) under which our vessels may be employed between the periods.

Our management also utilizes TCE to assist them in making decisions regarding employment of the vessels. We believe that our

method of calculating TCE is consistent with industry standards and is determined by dividing voyage revenues after deducting

voyage related costs and commissions by operating days for the relevant period. Voyage related costs and commissions primarily

consist of brokerage commissions, port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid

by the charterer under a time charter contract.

Vessel operating expenses (“Opex”) per day are our vessel operating expenses for a vessel, which primarily consist of crew wages

and related costs, insurance, lube oils, communications, spares and consumables, tonnage taxes as well as repairs and

maintenance, divided by the ownership days in the applicable period.

We calculate fleet utilization (“Utilization”) by dividing the number of operating days during a period by the number of available

days during the same period. The shipping industry uses fleet utilization to measure a company’s efficiency in finding suitable

employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons other than scheduled repairs or

repairs under guarantee, vessel upgrades, special surveys and intermediate dry-dockings or vessel positioning. Ownership days are

the total number of days in a period during which we owned each of the vessels in our fleet. Available days are the number of

ownership days in a period, less the aggregate number of days that our vessels were off-hire due to scheduled repairs or repairs

under guarantee, vessel upgrades or special surveys and intermediate dry-dockings and the aggregate number of days that we

spent positioning our vessels during the respective period for such repairs, upgrades and surveys. Operating days are the number of

available days in a period, less the aggregate number of days that our vessels were off-hire or out of service due to any reason,

including technical breakdowns and unforeseen circumstances.

Continued

33

CONTACT

Pyxis Tankers Inc.

K.Karamanli 59

Maroussi 15125, Greece

Email: [email protected]

www.pyxistankers.com

Henry Williams

CFO & Treasurer

Phone: +1 516 455 0106/ +30 210 638 0200

Email: [email protected]

Antonios “Tony” Backos

SVP for Corporate Development, General Counsel and Secretary

Phone: +30 210 638 0180

Email: [email protected]