2016 q2 business outlook - barbados

DESCRIPTION

ÂTRANSCRIPT

1

June 2016

CONTACT

Ryan Straughn

Managing Director

Telephone: +1 (246) 251-0811

Email: Ryan.Straughn

@abelianconsulting.com

www.abelianconsulting.com

The next issue of the Business

Outlook is scheduled for re-

lease in August 2016.

B u s i n e s s O u t l o o k

2 0 1 6 Q 2

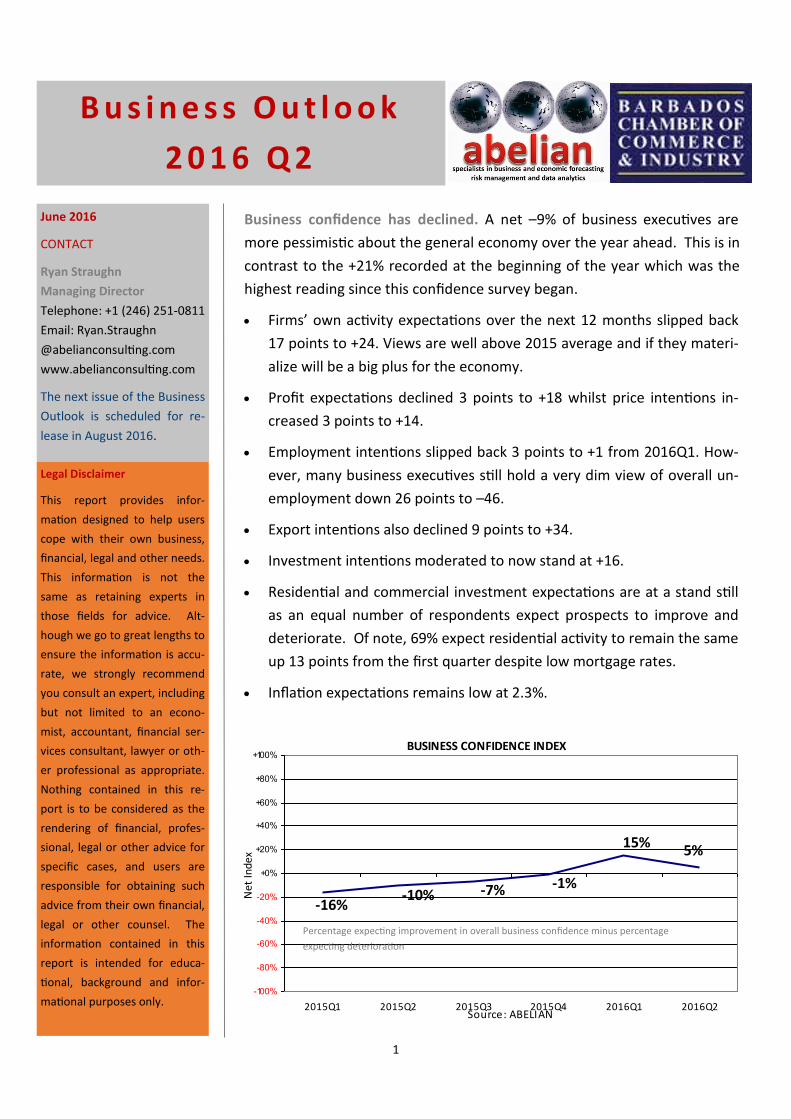

Business confidence has declined. A net –9% of business executives are

more pessimistic about the general economy over the year ahead. This is in

contrast to the +21% recorded at the beginning of the year which was the

highest reading since this confidence survey began.

Firms’ own activity expectations over the next 12 months slipped back

17 points to +24. Views are well above 2015 average and if they materi-

alize will be a big plus for the economy.

Profit expectations declined 3 points to +18 whilst price intentions in-

creased 3 points to +14.

Employment intentions slipped back 3 points to +1 from 2016Q1. How-

ever, many business executives still hold a very dim view of overall un-

employment down 26 points to –46.

Export intentions also declined 9 points to +34.

Investment intentions moderated to now stand at +16.

Residential and commercial investment expectations are at a stand still

as an equal number of respondents expect prospects to improve and

deteriorate. Of note, 69% expect residential activity to remain the same

up 13 points from the first quarter despite low mortgage rates.

Inflation expectations remains low at 2.3%.

BUSINESS CONFIDENCE INDEX

5%15%

-1%-7%-10%-16%

-100%

-80%

-60%

-40%

-20%

+0%

+20%

+40%

+60%

+80%

+100%

2015Q1 2015Q2 2015Q3 2015Q4 2016Q1 2016Q2Source: ABELIAN

Net

Ind

ex

Percentage expecting improvement in overall business confidence minus percentage

expecting deterioration

Legal Disclaimer

This report provides infor-

mation designed to help users

cope with their own business,

financial, legal and other needs.

This information is not the

same as retaining experts in

those fields for advice. Alt-

hough we go to great lengths to

ensure the information is accu-

rate, we strongly recommend

you consult an expert, including

but not limited to an econo-

mist, accountant, financial ser-

vices consultant, lawyer or oth-

er professional as appropriate.

Nothing contained in this re-

port is to be considered as the

rendering of financial, profes-

sional, legal or other advice for

specific cases, and users are

responsible for obtaining such

advice from their own financial,

legal or other counsel. The

information contained in this

report is intended for educa-

tional, background and infor-

mational purposes only.

2

B u s i n e s s O u t l o o k

2 0 1 6 Q 2

Services abelian offers:

Business Analytics

Business Intelligence

Credit Risk Modelling

Data Analytics

Data Management

Data Mining

Econometric Modelling

Economic Insights

Economic Intelligence

Market Research

Operations Research

Retail Modelling

Risk Modelling

Telecoms Modelling

Training courses

Utilities Modelling

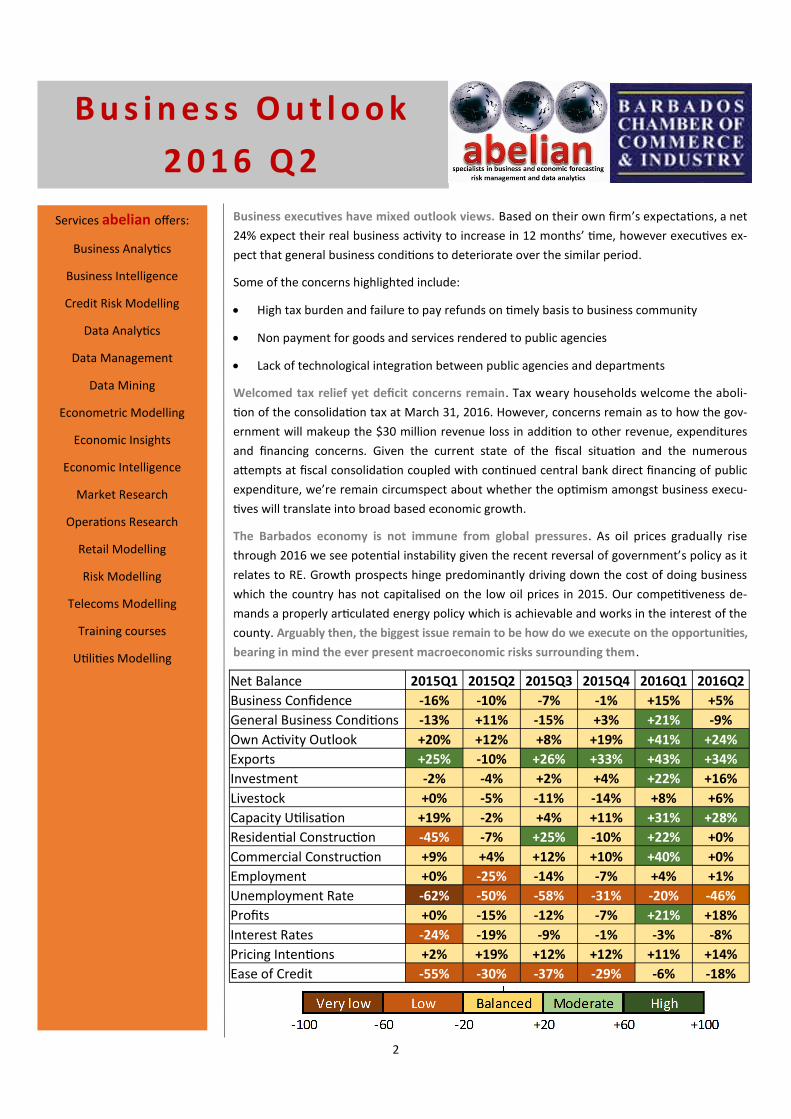

Business executives have mixed outlook views. Based on their own firm’s expectations, a net

24% expect their real business activity to increase in 12 months’ time, however executives ex-

pect that general business conditions to deteriorate over the similar period.

Some of the concerns highlighted include:

High tax burden and failure to pay refunds on timely basis to business community

Non payment for goods and services rendered to public agencies

Lack of technological integration between public agencies and departments

Welcomed tax relief yet deficit concerns remain. Tax weary households welcome the aboli-

tion of the consolidation tax at March 31, 2016. However, concerns remain as to how the gov-

ernment will makeup the $30 million revenue loss in addition to other revenue, expenditures

and financing concerns. Given the current state of the fiscal situation and the numerous

attempts at fiscal consolidation coupled with continued central bank direct financing of public

expenditure, we’re remain circumspect about whether the optimism amongst business execu-

tives will translate into broad based economic growth.

The Barbados economy is not immune from global pressures. As oil prices gradually rise

through 2016 we see potential instability given the recent reversal of government’s policy as it

relates to RE. Growth prospects hinge predominantly driving down the cost of doing business

which the country has not capitalised on the low oil prices in 2015. Our competitiveness de-

mands a properly articulated energy policy which is achievable and works in the interest of the

county. Arguably then, the biggest issue remain to be how do we execute on the opportunities,

bearing in mind the ever present macroeconomic risks surrounding them.

Net Balance 2015Q1 2015Q2 2015Q3 2015Q4 2016Q1 2016Q2

Business Confidence -16% -10% -7% -1% +15% +5%

General Business Conditions -13% +11% -15% +3% +21% -9%

Own Activity Outlook +20% +12% +8% +19% +41% +24%

Exports +25% -10% +26% +33% +43% +34%

Investment -2% -4% +2% +4% +22% +16%

Livestock +0% -5% -11% -14% +8% +6%

Capacity Utilisation +19% -2% +4% +11% +31% +28%

Residential Construction -45% -7% +25% -10% +22% +0%

Commercial Construction +9% +4% +12% +10% +40% +0%

Employment +0% -25% -14% -7% +4% +1%

Unemployment Rate -62% -50% -58% -31% -20% -46%

Profits +0% -15% -12% -7% +21% +18%

Interest Rates -24% -19% -9% -1% -3% -8%

Pricing Intentions +2% +19% +12% +12% +11% +14%

Ease of Credit -55% -30% -37% -29% -6% -18%