2016 china – russia business seminar. new opportunities & new challenges

TRANSCRIPT

2016 China – Russia Business Seminar

New Opportunities & New Challenges

www.pwc.com

PwC Russia

Agenda

1. Investing into Russia - Opportunities for Chinese investors

2. China Tax Reform Blueprint and development & outbound investment crisis management (only Chinese version available)

3. Doing business in Russia - corporate, antimonopoly, employment and migration aspects

4. Tax and non-tax incentives available in Russia

5. Changing customs environment and modern instruments for supporting importers in Russia

6. Forensic review of the proper use of funds & due diligence of third parties

2

19 January 2016

PwC Russia

Investing into Russia − Opportunities for Chinese investors

3

19 January 2016

PwC Russia

1. Russian economy at a glance

2. Russia-China economic relations

3. Key industry segments and opportunities for Chinese companies

4. PwC in Russia

Agenda

4

19 January 2016

PwC Russia

1. Russian economy at a glance

5

19 January 2016

PwC Russia

Relative growth of BRICS countries GDP in 2000-2014 (against 2000)

Russia has historically been growing faster than the world’s average and in line with the peers form BRICS

9.8%

4.1%

3.2%

CAGR 2000-2014 Historical growth drivers

Upward trend in a global commodities cycle

Growth in consumption and development of consumer markets

Improvement of institutional environment (incl. WTO accession in 2012)

Development of financial markets

Vulnerable to changes in commodity prices in short-run, but outperformed world-average in 2000-2014 (4.1% vs 3.7%)

7.1%

3.1%

Source: EIU, PwC analysis

Growth pattern

Brazil

China

India

Russia

SouthAfrica

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2000 2002 2004 2006 2008 2010 2012 2014

USD

t

6

19 January 2016

PwC Russia

Certain megatrends will likely drive transformation of the Russian economy in the future

Source: Gazprombank, Census, CBR, Lukoil, HelgiLibrary, PwC analysis

Mining and O&G are shifting eastward Infrastructure challenge

Aging population Financial deepening

By 2025 25% of oil and 50% of natural gas extraction will come from new fields (Yamal, Arctic shelf, East Siberia)

1

Development of new world-class coal, copper and gold projects in underway in the Russian Far East and Eastern Siberia

2

More projects are targeting Asian markets. There is a demand for equity and debt investments to finance development

Russia shall invest USD 100b pa (4% GDP) in infrastructure to secure economic growth

1

Only 2% of total infrastructure investments were private in 2014

3

Due to the budget deficit (2,8% in 2015), the government will foster private investments in infrastructure

Large projects include high speed railways, FIFA 2018, new pipelines and ports

2

By 2030 over 20% of population will be senior (vs 13% today) – 28 mln people

1

Consumer power of new senior generation will be significantly higher

2

Pharma, senior hospitality and healthcare markets will grow faster than GDP. Profile of an average consumer will change

Bank assets to GDP ratio in Russia (84% in 2013) is significantly below the peers (250-300%) in the EU and China

1

Bank assets to GDP shall exceed 130% by 2020 -potential for double-digit growth rates and returns in selected segments of financial market

7

19 January 2016

PwC Russia

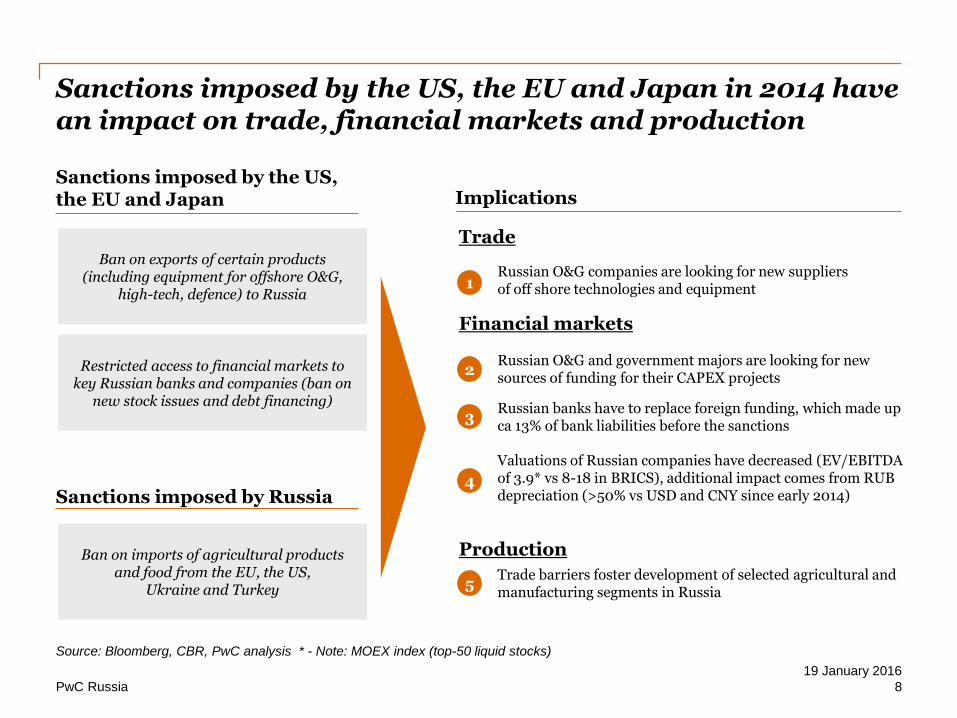

Sanctions imposed by the US, the EU and Japan in 2014 have an impact on trade, financial markets and production

Ban on exports of certain products (including equipment for offshore O&G,

high-tech, defence) to Russia

Sanctions imposed by the US, the EU and Japan

Restricted access to financial markets to key Russian banks and companies (ban on

new stock issues and debt financing)

Implications

Russian banks have to replace foreign funding, which made up ca 13% of bank liabilities before the sanctions

Russian O&G companies are looking for new suppliers of off shore technologies and equipment

Valuations of Russian companies have decreased (EV/EBITDA of 3.9* vs 8-18 in BRICS), additional impact comes from RUB depreciation (>50% vs USD and CNY since early 2014)

4Sanctions imposed by Russia

Ban on imports of agricultural products and food from the EU, the US,

Ukraine and Turkey

1

Russian O&G and government majors are looking for new sources of funding for their CAPEX projects

3

2

Trade

Financial markets

Source: Bloomberg, CBR, PwC analysis * - Note: MOEX index (top-50 liquid stocks)

Production

Trade barriers foster development of selected agricultural and manufacturing segments in Russia

5

8

19 January 2016

PwC Russia

Sanctions and oil slump will make 2015 a tough year for the Russian economy, recovery is expected starting from 2017

Key factors driving the forecast

2015 is a tough year for the economy due to continuing sanctions, oil slump, weak RUB and sovereign ratings downgrade

Nominal GDP will decrease greater than real GDP due to RUB depreciation (>50% vs USD/CNY)

The economy shall start recovering in 2017

Nominal GDP forecast and real growth rates

Potential opportunities

Strike deals on very favorable conditions as assets can potentially be undervalued

EIU forecast, 2015-2019

Ride the emerging trends (changing consumer behaviors, financial constrains, less competitive imports)

Source: EIU 5-year forecast as of Oct 2015, PwC analysis

4.5% 4.3%

3.4%

1.3%0.6%

(3.6%)

(0.6%)

2.0%1.5% 1.5%

1.5

1.92.0 2.1

1.9

1.3 1.21.4

1.51.7

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2010 2011 2012 2013 2014 2015F 2016F 2017F 2018F 2019F

Real GDP growth rate,% Nominal GDP (USD trillion)

9

19 January 2016

PwC Russia

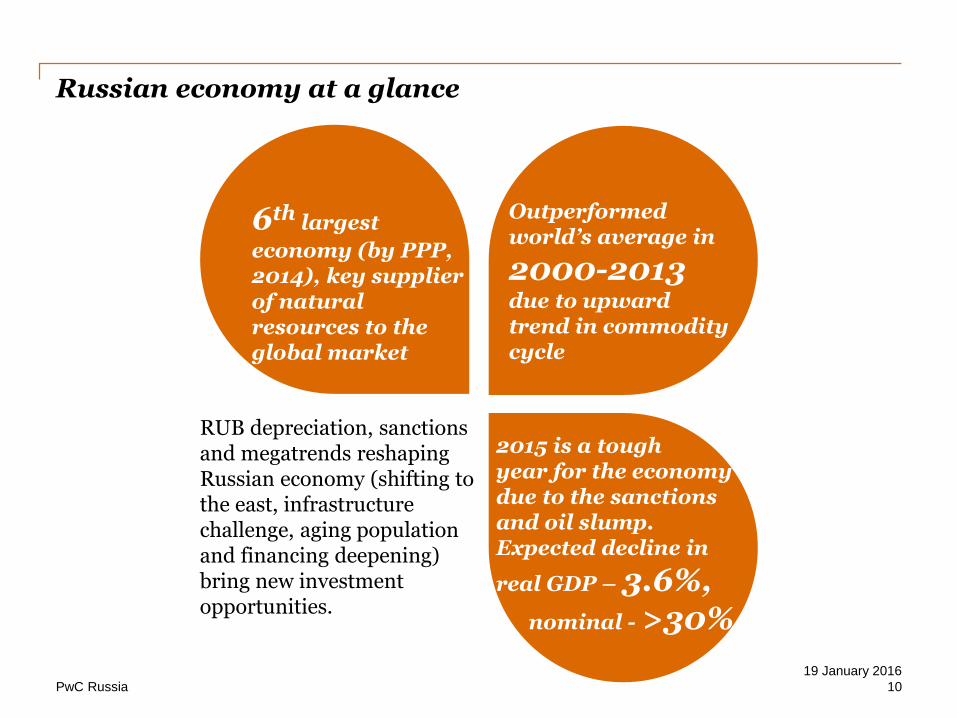

Russian economy at a glance

RUB depreciation, sanctions and megatrends reshaping Russian economy (shifting to the east, infrastructure challenge, aging population and financing deepening) bring new investment opportunities.

6th largest

economy (by PPP, 2014), key supplier of natural resources to the global market

Outperformed world’s average in

2000-2013due to upward trend in commodity cycle

2015 is a tough year for the economy due to the sanctions and oil slump. Expected decline in

real GDP – 3.6%, nominal - >30%

10

19 January 2016

PwC Russia

2. Russia – China economic relations

11

19 January 2016

PwC Russia

Russia-China economic relations have been limited due to geography and lack of infrastructure

Source: roebuckclasses., PwC analysis

Economic cooperation has historically been limited by As a result

Russia makes up only 2% of Chinese international trade

There is no substantial export of Russian natural gas to the Chinese market

Trans-border economic cooperation is limited

Geography - 3.5k km of the border is located in a remote sparsely populated area

Lack of infrastructure (different rail gauges, no cross-border bridges over Heilong Jiang or pipelines)

Limited involvement of both countries in international trade before 00-s

1

2

3

Several large infrastructure projects are underway/proposed

Bridge over Heilong Jiang

Natural gas pipeline East Siberia –China

Expansion of ports in the Russian Far East and railroad infrastructure

12

19 January 2016

PwC Russia

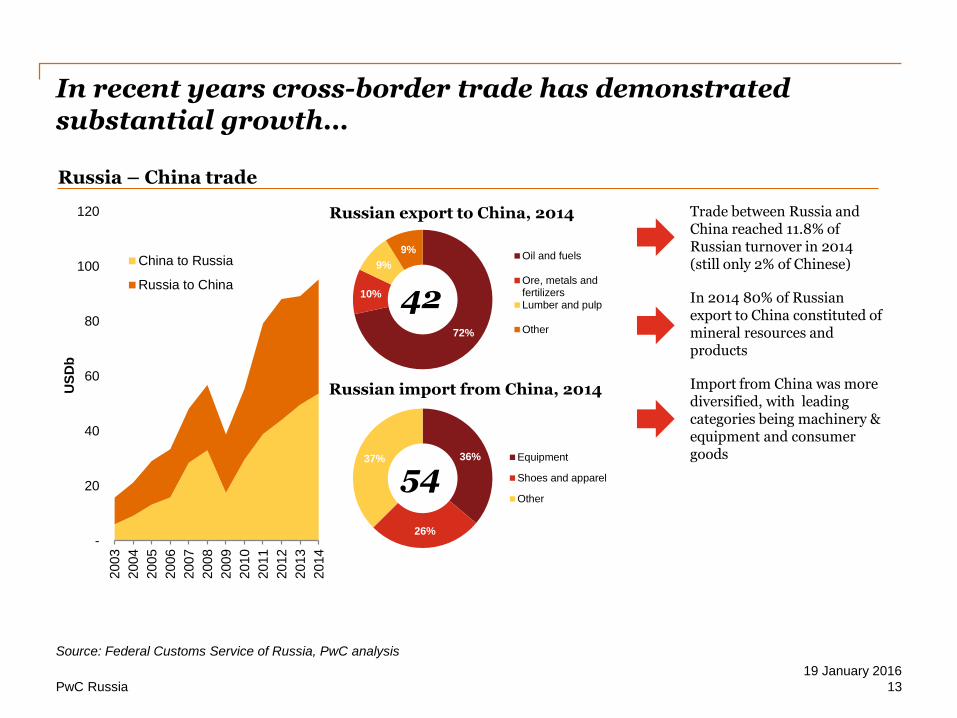

In recent years cross-border trade has demonstrated substantial growth…

Russia – China trade

Trade between Russia and China reached 11.8% of Russian turnover in 2014 (still only 2% of Chinese)

In 2014 80% of Russian export to China constituted of mineral resources and products

Import from China was more diversified, with leading categories being machinery & equipment and consumer goods

Source: Federal Customs Service of Russia, PwC analysis

-

20

40

60

80

100

120

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

US

Db

China to Russia

Russia to China

36%

26%

37%

54Equipment

Shoes and apparel

Other

Russian export to China, 2014

Russian import from China, 2014

72%

10%

9%

9%

42

Oil and fuels

Ore, metals andfertilizersLumber and pulp

Other

13

19 January 2016

PwC Russia

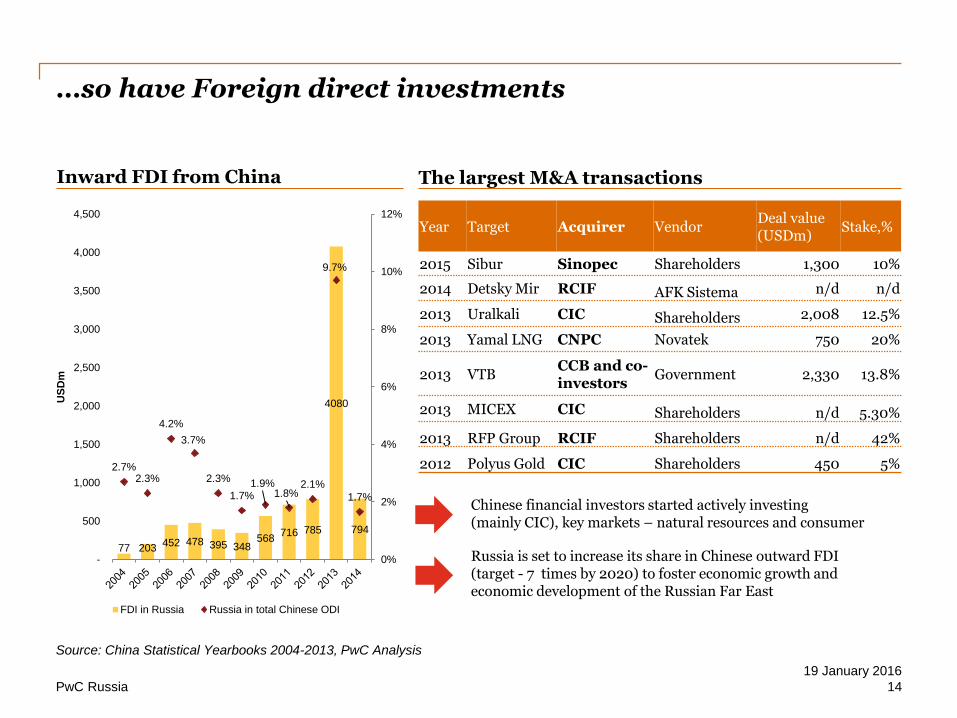

…so have Foreign direct investments

Inward FDI from China

Source: China Statistical Yearbooks 2004-2013, PwC Analysis

Chinese financial investors started actively investing (mainly CIC), key markets – natural resources and consumer

Russia is set to increase its share in Chinese outward FDI (target - 7 times by 2020) to foster economic growth and economic development of the Russian Far East

Year Target Acquirer VendorDeal value (USDm)

Stake,%

2015 Sibur Sinopec Shareholders 1,300 10%

2014 Detsky Mir RCIF AFK Sistema n/d n/d

2013 Uralkali CIC Shareholders 2,008 12.5%

2013 Yamal LNG CNPC Novatek 750 20%

2013 VTBCCB and co-investors

Government 2,330 13.8%

2013 MICEX CIC Shareholders n/d 5.30%

2013 RFP Group RCIF Shareholders n/d 42%

2012 Polyus Gold CIC Shareholders 450 5%

The largest M&A transactions

77 203452 478 395 348

568716 785

4080

794

2.7%2.3%

4.2%

3.7%

2.3%

1.7%1.9%

1.8%2.1%

9.7%

1.7%

0%

2%

4%

6%

8%

10%

12%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

US

Dm

FDI in Russia Russia in total Chinese ODI

14

19 January 2016

PwC Russia

Wide range of institutions to support Chinese business and investors in Russia were established in recent years

Top-level political cooperation lays foundation for partnership in various business areas

Russia-China trade chamber

Russian-Chinese Business Council

Russia China Investment Fund

The Russian-Chinese center of trade and economic cooperation

Intergovernmental Russian–Chinese Investment Cooperation Commission

Major institutions Mission

“Coordinate efforts of all participants of bilateral economic relations”

Facilitate trade in machinery & equipment and innovations

“Promote joint economic projects” and “facilitate cooperation between Russian and Chinese business community”

“… Investing in projects that advance bilateral economic cooperation between Russia and China”

Facilitate investment projects and decrease administrative and trade barriers

Source: PwC analysis

15

19 January 2016

PwC Russia

Russia-China economic relations

Economic cooperation has historically been limited by lack of infrastructure and geography

In recent years bilateral trade and investments have surged (China is the Russia’s largest trade partner, 11.8% of total exports)

Russian government is set to expand cooperation with Chinese companies to foster economic growth and development of the Russian Far East

Several institutions have been set up; co-investment from RDIF/RCIF is available for Chinese companies and banks

16

19 January 2016

PwC Russia

3. Key industry segments and opportunities for Chinese companies

17

19 January 2016

PwC Russia

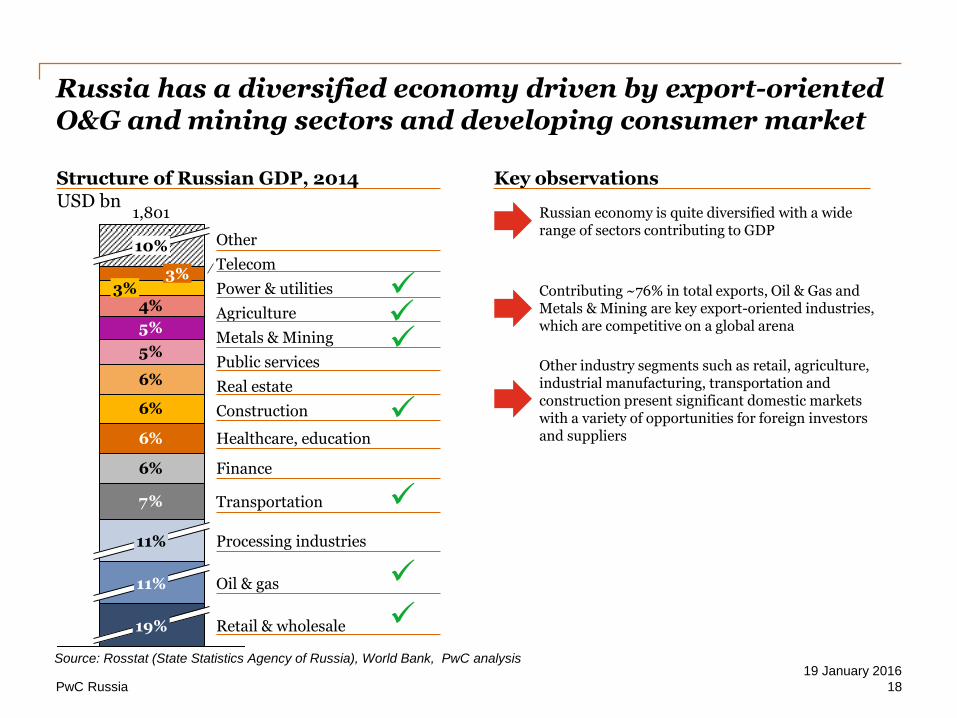

Russia has a diversified economy driven by export-oriented O&G and mining sectors and developing consumer market

7%

6%

6%

6%

6%

5%

5%

4%

Retail & wholesale

Oil & gas

Processing industries

Transportation

Finance

Healthcare, education

Construction

Real estate

Public services

Metals & Mining

Agriculture

Power & utilities

Telecom

Other

1,801

19%

11%

11%

3%3%

10%

Key observationsStructure of Russian GDP, 2014

Contributing ~76% in total exports, Oil & Gas and Metals & Mining are key export-oriented industries, which are competitive on a global arena

Other industry segments such as retail, agriculture, industrial manufacturing, transportation and construction present significant domestic markets with a variety of opportunities for foreign investors and suppliers

Russian economy is quite diversified with a wide range of sectors contributing to GDP

USD bn

Source: Rosstat (State Statistics Agency of Russia), World Bank, PwC analysis

18

19 January 2016

PwC Russia

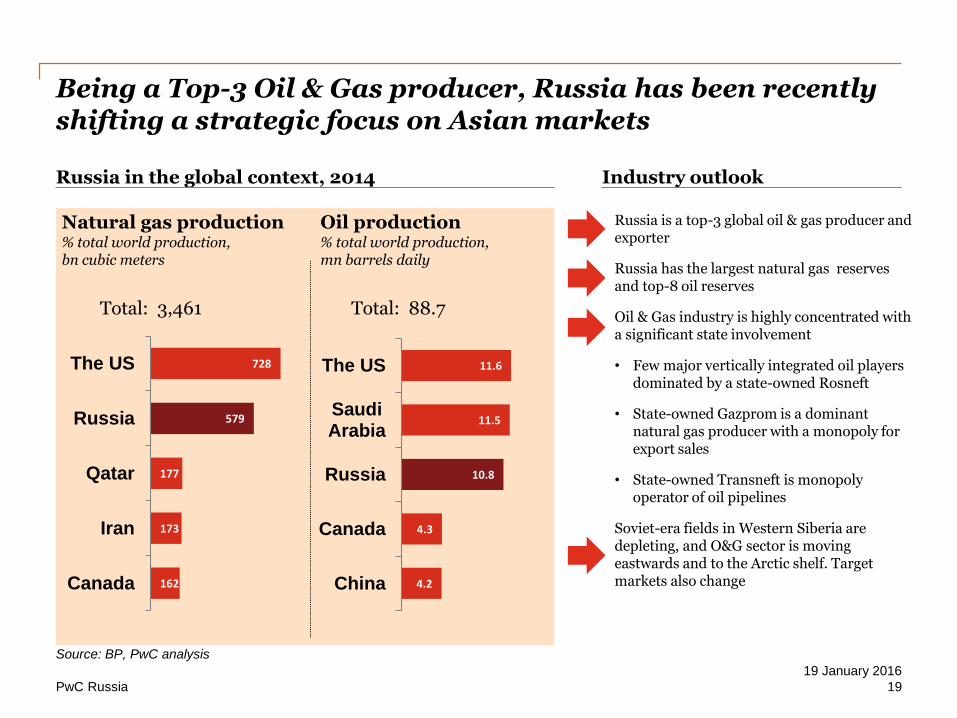

Being a Top-3 Oil & Gas producer, Russia has been recently shifting a strategic focus on Asian markets

Russia in the global context, 2014 Industry outlook

Natural gas production% total world production,bn cubic meters

Oil production% total world production,mn barrels daily

Russia is a top-3 global oil & gas producer and exporter

Russia has the largest natural gas reserves and top-8 oil reserves

Oil & Gas industry is highly concentrated with a significant state involvement

• Few major vertically integrated oil players dominated by a state-owned Rosneft

• State-owned Gazprom is a dominant natural gas producer with a monopoly for export sales

• State-owned Transneft is monopoly operator of oil pipelines

Soviet-era fields in Western Siberia are depleting, and O&G sector is moving eastwards and to the Arctic shelf. Target markets also change

Source: BP, PwC analysis

Total: 3,461 Total: 88.7

162

173

177

579

728

Canada

Iran

Qatar

Russia

The US

4.2

4.3

10.8

11.5

11.6

China

Canada

Russia

SaudiArabia

The US

19

19 January 2016

PwC Russia

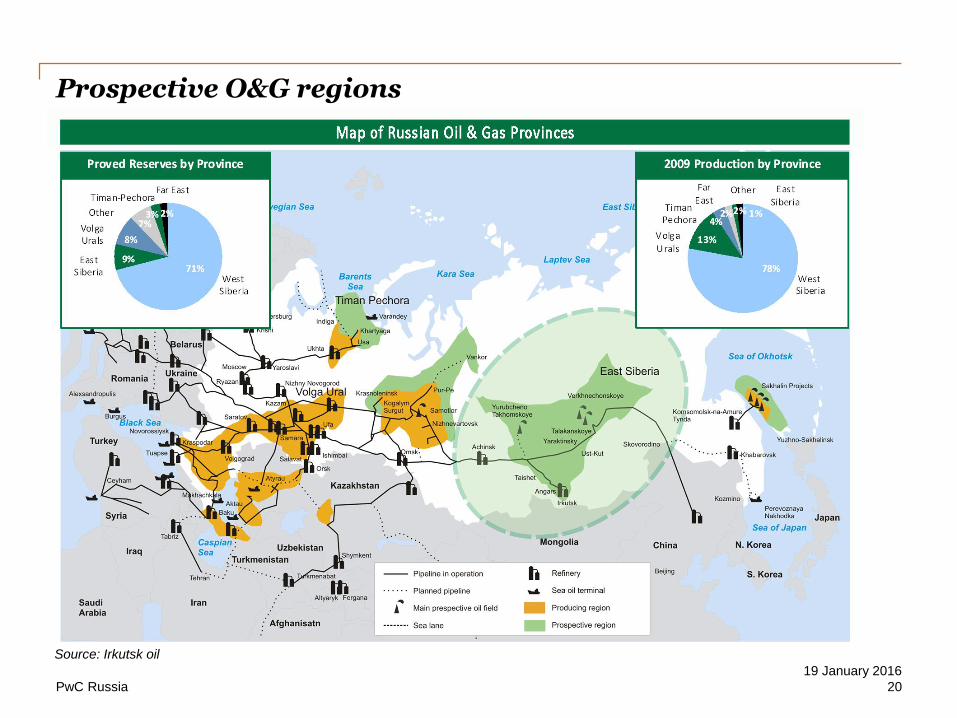

Prospective O&G regions

Source: Irkutsk oil

20

19 January 2016

PwC Russia

Existing cooperation and potential opportunities for Chinese companies in Oil & Gas

Contractors in infrastructure & pipelines

JV/ investments in upstream

Supply of equipment and technology

• Yamal LNG-CNPC;

• CNPC - Rosneft (Vankor)

• Chinese contractors & suppliers are expected to participate

• Oil & Gas infrastructure development is on top of the agenda, i.e. investment into Russia – China gas pipeline is expected at ~$55 bn

• Russian O&G companies need to make significant investments in new fields (East Siberia, Arctic shelf) to sustain production volumes

• Financing is constrained due to the sanctions

• Potential for Chinese O&G equipment suppliers and service providers to gain market share from Western competitors

• Supplies and equipment spending of only Rosneft reached $6 bn in 2014

• Hilong investment in coating business in Russia

Seg

men

t p

ote

nti

al

Rec

ent

dea

ls

Source: PwC analysis

21

19 January 2016

PwC Russia

Russia is a top global producer across a wide range of minerals with a solid resource base

17%

Nickel 14%

Copper 4%

Gold 7%

Iron ore 6%

Coal 5%

Steel 4%

Potash

4%

35%

8%

10%

15%

18%

n/a

Rank

#2

#3

#3

#6

#4

#2

Mineral and steel production Mineral reserves% in world’s % in world’s

Russia in the global context Industry outlook

• Russia is among global leaders in metals and mining

RUB depreciation improves cash margins and NPV of Russian mining projects

There are over 40 large-scale mining projects in the Russian Far East on exploration and development stages, namely: Udokan (copper), Baimskoe and Natalka (gold), Tuva and Elga coal projects, Timir (iron ore)

• Focus on export, but Russia makes up ca. 2% of Chinese imports of metals

n/a

Rank

#5

#5

#4

#6

#1

#2

#5

Source: PwC analysis

22

19 January 2016

PwC Russia

Source: PwC analysis

1

2

3

45

6

7

89

10

11

12

13

14

15

16

17 18

19

20

21

22

23

24

25

26

272829

30

31

32

33

3435

36 37

38

39

40

41

42

43

44

45

46

47

China

Mongolia

KazakhstanJapan

Republic

of Korea

DPRK

Moscow

Iran

Iraq

Turkey

Ukraine

Large-scale mining projects in Russia on exploration and development stages

Exploration

and designDevelopment Mining

Coal

Cu

Fe

Ni

Au

Mo

Ti

Zn,Pb

Other

23

19 January 2016

PwC Russia

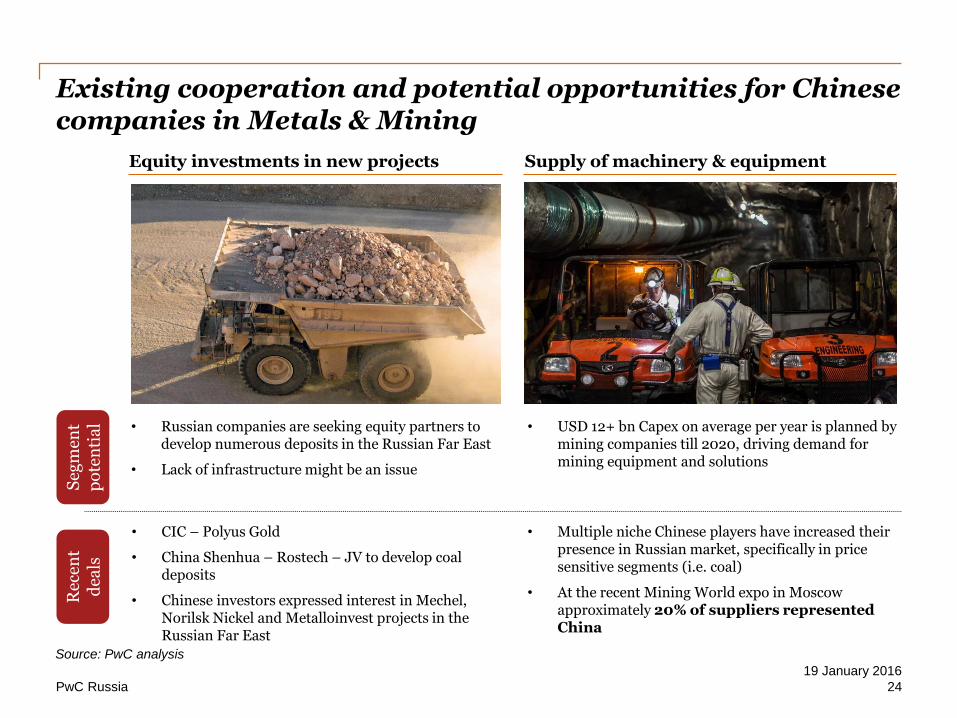

Existing cooperation and potential opportunities for Chinese companies in Metals & Mining

Equity investments in new projects Supply of machinery & equipment

• CIC – Polyus Gold

• China Shenhua – Rostech – JV to develop coal deposits

• Chinese investors expressed interest in Mechel, Norilsk Nickel and Metalloinvest projects in the Russian Far East

• USD 12+ bn Capex on average per year is planned by mining companies till 2020, driving demand for mining equipment and solutions

• Russian companies are seeking equity partners to develop numerous deposits in the Russian Far East

• Lack of infrastructure might be an issue

Seg

men

t p

ote

nti

al

Rec

ent

dea

ls

• Multiple niche Chinese players have increased their presence in Russian market, specifically in price sensitive segments (i.e. coal)

• At the recent Mining World expo in Moscow approximately 20% of suppliers represented China

Source: PwC analysis

24

19 January 2016

PwC Russia

Agricultural might have a good potential, although there are certain restrictions for the foreign investors

Source: FAO trade statistics, PwC analysis

Russia in the global context Industry outlook

Russian agricultural ban fosters development of aquaculture market which barely exists now

There is a number of large (>USD 1b in revenue) agricultural holdings in Russia potentially available for sale

Oil and grains

Fishery

Russia has the 3rd largest arable land area globally, and one of the highest arable area per capita in the world

Russia has become the 3rd largest exporter of wheat (>20 mt pa) and sunflower oil (ca 3.2 m t) since the Soviet era

Key market – Middle East, shipped through grain terminals in Black sea

5th largest catch in the world and abandoned biological resources (Russian Pacific coast)

Russia makes up 30% of total Chinese fishery imports (mostly pollock)

1

2

3

1Constraints for foreign investors

There are restrictions on land ownership for foreign companies/individuals. Grain exports is highly regulated

Russian government is interested in attracting Chinese investors

2

25

19 January 2016

PwC Russia

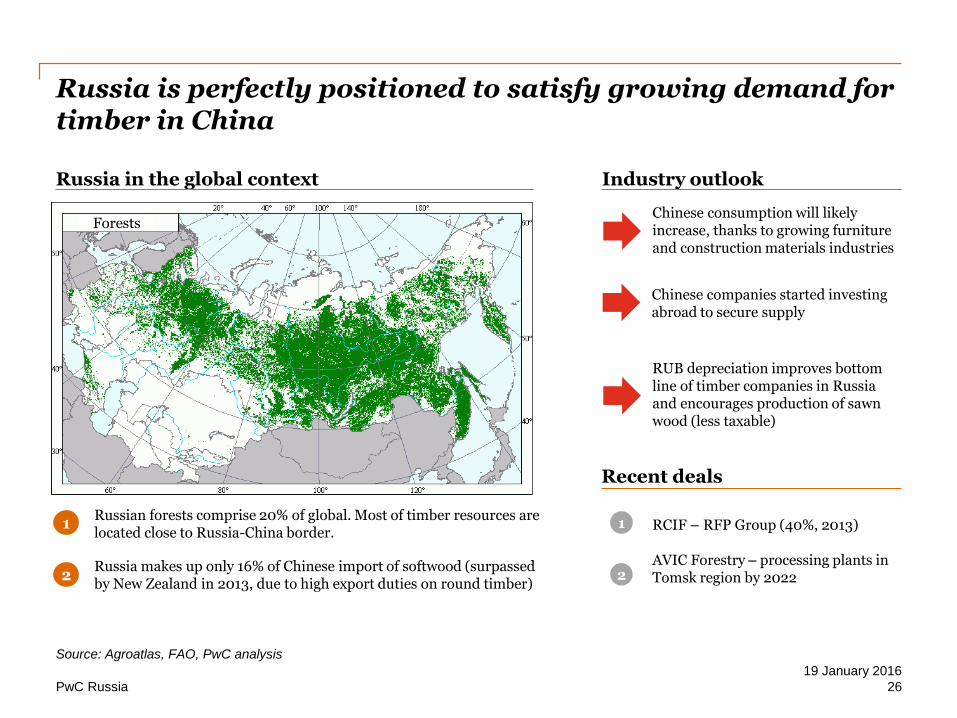

Russia is perfectly positioned to satisfy growing demand for timber in China

Russia in the global context

Forests

Industry outlook

RUB depreciation improves bottom line of timber companies in Russia and encourages production of sawn wood (less taxable)

Chinese consumption will likely increase, thanks to growing furniture and construction materials industries

Chinese companies started investing abroad to secure supply

Recent deals

Source: Agroatlas, FAO, PwC analysis

Russian forests comprise 20% of global. Most of timber resources are located close to Russia-China border.

Russia makes up only 16% of Chinese import of softwood (surpassed by New Zealand in 2013, due to high export duties on round timber)

1

2

RCIF – RFP Group (40%, 2013)

AVIC Forestry – processing plants in Tomsk region by 2022

1

2

26

19 January 2016

PwC Russia

Development of infrastructure is key to unlock natural resources potential of the Russian Far East

Source: PwC analysis

Projects in the Russian Far East Other infrastructure projects

• RCIF invests in construction of first railway bridge over Amur

• Dongfang Electric plans to invest in energy projects with RAO EES Vostoka

• Existing infrastructure in the Russian Far East (ports, bridges, power) is inadequate to fully exploit resource potential

• Development of the infrastructure in the region is on top of the agenda for the Russian government (separate ministry was established in 2012)

• There is a demand for infrastructure investments in other parts of Russia (high-speed railways, FIFA 2018, Moscow underground)

• Certain projects might be suitable for Chinese financial investors (PPP), Chinese contractors might be highly competitive

Seg

men

t p

ote

nti

al

Rec

ent

dea

ls

• China Railway Construction considers participating in expansion of Moscow underground

27

19 January 2016

PwC Russia

Great Wall, Lifan and GAC – plants under construction

Dongfeng, Zotye – contracted assembly starting 2015

Fuyao Glass –a plant launched in 2013

Chinese brands had only 3% sales in 2014 (38% in China);

Lifan, Chery, Geely and Great Wall comprise together 93% of Chinese cars sales in 2014;

Chinese manufacturers have a competitive edge in a price-sensitive market

Russian automotive market is one of the largest in the world. Companies with localized production have advantage

Source:AEB, OICA, PwC Analysis

Russia in the global context

8th largest market in the world (2.3m new light vehicles sold in 2014, 4% of global)

The market is dominated by global conglomerates: Renault-Nissan (31%), VW Group (11%), KIA (8%) and GM Group (8%)

Imported vehicles are subject to high customs duties and make up only 25% of the market

2015 was a very tough (-45%) due to RUB depreciation

Localization:

Localisation proved to be a sound strategy for foreign manufacturers

55% of cars sold in 2014 were foreign brands assembled in Russia (up from 44% in 2012)

1

Industry outlook

Recent activities

1

2

2

3

3

2

1

4

28

19 January 2016

PwC Russia

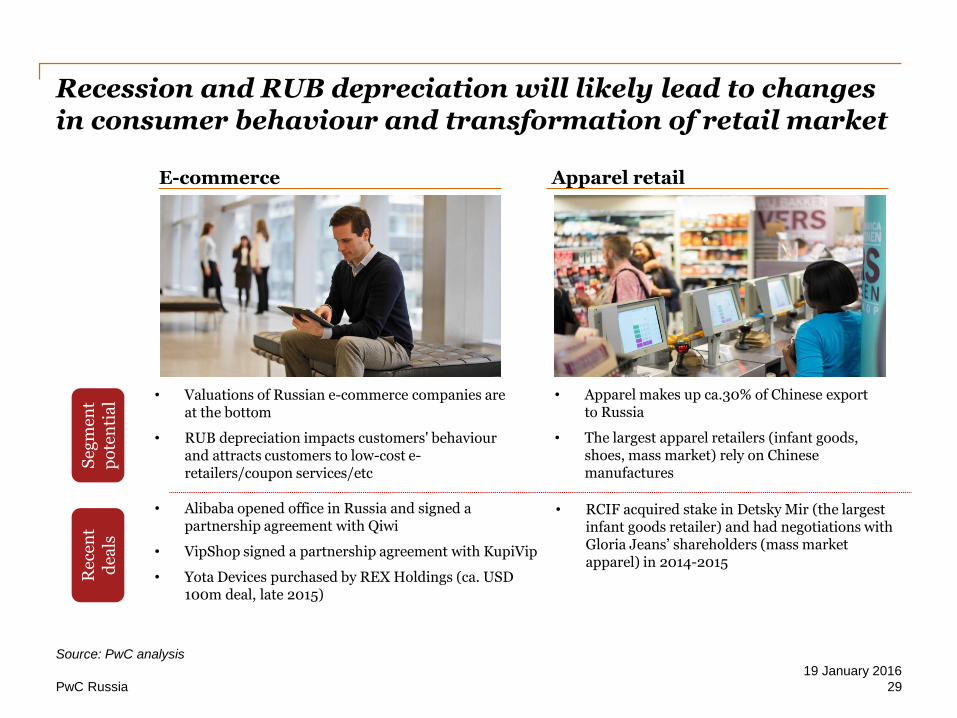

Recession and RUB depreciation will likely lead to changes in consumer behaviour and transformation of retail market

Source: PwC analysis

E-commerce Apparel retail

• Alibaba opened office in Russia and signed a partnership agreement with Qiwi

• VipShop signed a partnership agreement with KupiVip

• Yota Devices purchased by REX Holdings (ca. USD 100m deal, late 2015)

• RCIF acquired stake in Detsky Mir (the largest infant goods retailer) and had negotiations with Gloria Jeans’ shareholders (mass market apparel) in 2014-2015

• Valuations of Russian e-commerce companies are at the bottom

• RUB depreciation impacts customers' behaviour and attracts customers to low-cost e-retailers/coupon services/etc

• Apparel makes up ca.30% of Chinese export to Russia

• The largest apparel retailers (infant goods, shoes, mass market) rely on Chinese manufactures

Seg

men

t p

ote

nti

al

Rec

ent

dea

ls

29

19 January 2016

PwC Russia

Key industry segments and opportunities for Chinese companies

RUB depreciation will drive transformation of Russian e-commerce, automotive and retail markets benefiting cost-efficient market players

Investment opportunities exist in export-oriented

natural resources industries and transforming

consumer markets:

O&G and metals and mining companies are facing financial constraints due to the sanctions and are looking for equity partners for new deposits/fields

Russian forestry and agriculture are well positioned to meet growing demand in China

Infrastructure investments are highly encouraged by the Russian government

30

19 January 2016

PwC Russia

4. PwC in Russia

31

19 January 2016

PwC Russia

PwC posses a wide range of capabilities in Russia to help you investing and creating value

Deal execution

Deal originationRealizing

potential of the investment

Divestiture

• Due diligence: financial, tax, commercial, operational, legal, HR, environmental, IT

• Financial and tax modelling and model review

• Tax and legal structuring

• SPA, shareholder agreement, and other deal documentation

• Negotiation support

• Strategy development

• Operational performance improvement

• Accounting function

• IT systems

• On-going tax and legal consultancy, restructuring

• HR consultancy

• Business restructuring

• Audit and assurance

• Forensic

• Exit support

• Vendor due diligence

• Tax optimisation on exit

• SPA, shareholder agreement and other deal documentation

• Negotiation support

• Market entry strategy

• Target screening

• Feasibility study

• Financing advice

• Bringing co-investors

32

19 January 2016

PwC Russia

We have a proven track record helping Chinese companies to invest in Russia

Indicative value analysis and financial and tax due

diligence of coal mines and a sea coal terminal in Russia

Valuation, financial and tax due diligence

Large Chinese coal company

Large Chinese e-commerce company

Financial and tax due diligence of a potential target

in Russia

Financial and tax due diligence

Large Chinese energy company

Financial and tax due diligence, valuation of

Russian subsidiary of a large European banking group

Financial and tax due diligence, valuation

Russian washing machine market analysis

Sinopec Oil and Gas

Financial advisor on a potential acquisition of a major upstream company

Financial and tax due diligence

Haier

Market analysis

RCIF

Commercial due diligence of a e-commerce company

Commercial due diligence

Hilong

Financial and tax due diligence of a joint venture in

Russia

Financial and tax due diligence

Chinese investment firm

Financial advisor on a potential acquisition of a stake in a mining project

Financial and tax due diligence

33

19 January 2016

PwC Russia

China Tax Reform Blueprint and development & outbound investment crisis management (only Chinese version available)

34

19 January 2016

PwC Russia

Doing business in Russia – corporate, antimonopoly, employment and migration aspects

35

19 January 2016

PwC Russia

Agenda

1. Introduction

2. Russian legal framework

• Corporate aspects• Antimonopoly regulations• Employment law• Migration law

36

19 January 2016

PwC Russia

1. Introduction

37

19 January 2016

PwC Russia

2. Russian legal framework

• Corporate aspects

• Antimonopoly regulations

• Employment law

• Migration law

38

19 January 2016

PwC Russia

2.1. Corporate aspects

39

19 January 2016

PwC Russia

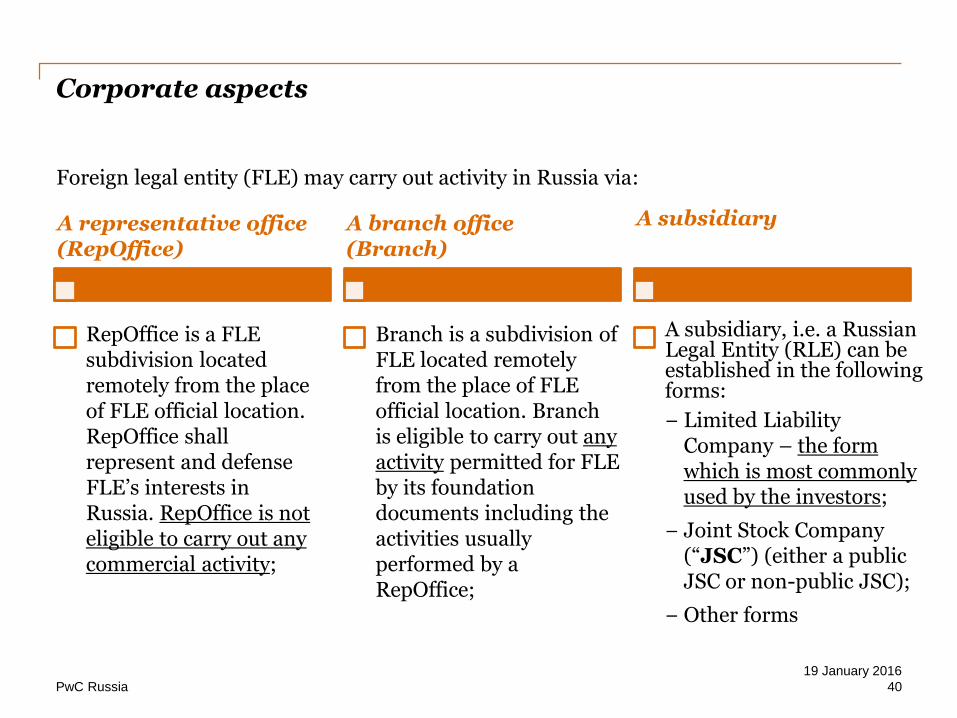

Corporate aspects

A subsidiary, i.e. a Russian Legal Entity (RLE) can be established in the following forms:

− Limited Liability Company – the form which is most commonly used by the investors;

− Joint Stock Company (“JSC”) (either a public JSC or non-public JSC);

− Other forms

A representative office (RepOffice)

Foreign legal entity (FLE) may carry out activity in Russia via:

RepOffice is a FLE subdivision located remotely from the place of FLE official location. RepOffice shall represent and defense FLE’s interests in Russia. RepOffice is not eligible to carry out any commercial activity;

A branch office (Branch)

Branch is a subdivision of FLE located remotely from the place of FLE official location. Branch is eligible to carry out any activity permitted for FLE by its foundation documents including the activities usually performed by a RepOffice;

A subsidiary

40

19 January 2016

PwC Russia

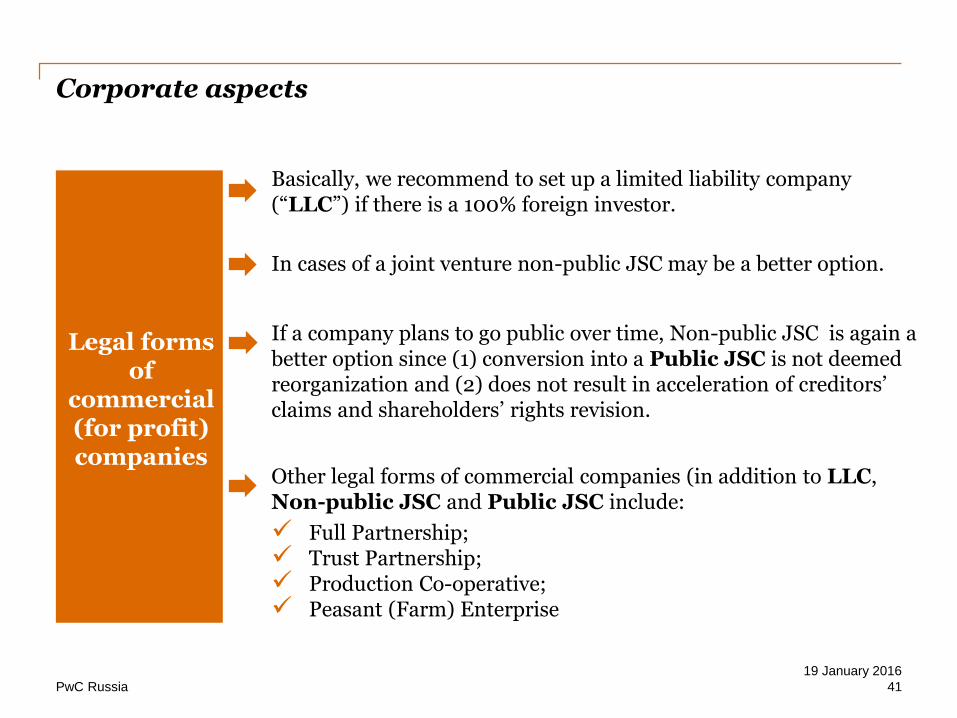

Corporate aspects

Legal forms of

commercial (for profit)companies

Other legal forms of commercial companies (in addition to LLC, Non-public JSC and Public JSC include:

Full Partnership; Trust Partnership; Production Co-operative; Peasant (Farm) Enterprise

Basically, we recommend to set up a limited liability company (“LLC”) if there is a 100% foreign investor.

In cases of a joint venture non-public JSC may be a better option.

If a company plans to go public over time, Non-public JSC is again a better option since (1) conversion into a Public JSC is not deemed reorganization and (2) does not result in acceleration of creditors’ claims and shareholders’ rights revision.

41

19 January 2016

PwC Russia

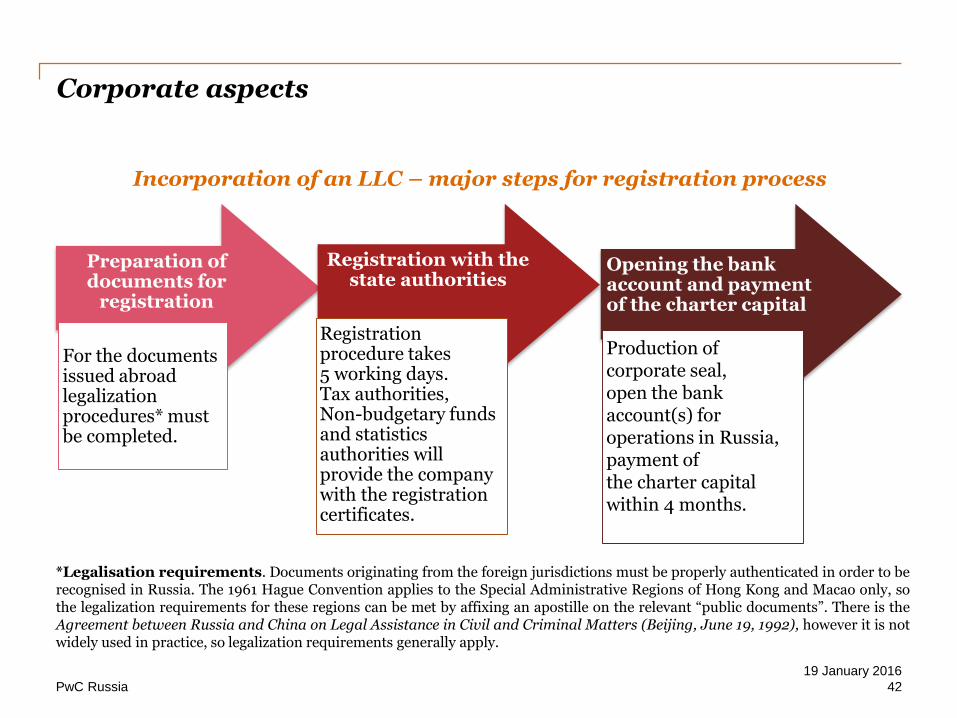

Preparation of documents for

registration

For the documents issued abroad legalization procedures* must be completed.

Registration with the state authorities

Registration procedure takes 5 working days. Tax authorities, Non-budgetary funds and statistics authorities will provide the company with the registration certificates.

Opening the bank account and payment of the charter capital

Production of corporate seal, open the bank account(s) for operations in Russia, payment ofthe charter capital within 4 months.

Corporate aspects

*Legalisation requirements. Documents originating from the foreign jurisdictions must be properly authenticated in order to berecognised in Russia. The 1961 Hague Convention applies to the Special Administrative Regions of Hong Kong and Macao only, sothe legalization requirements for these regions can be met by affixing an apostille on the relevant “public documents”. There is theAgreement between Russia and China on Legal Assistance in Civil and Criminal Matters (Beijing, June 19, 1992), however it is notwidely used in practice, so legalization requirements generally apply.

Incorporation of an LLC – major steps for registration process

42

19 January 2016

PwC Russia

2.2. Antimonopoly regulations

43

19 January 2016

PwC Russia

Antimonopoly regulations

Antimonopoly Regulations in Russia –Key Requirements to Conducting Business

• Modern Russian anti-trust legislation has only 10-year history. Key Russian anti-trust law is the Federal Law No. 135-FZ “On Protection of Competition” (has been significantly amended several times during its existence and likely to change in the future);

• Russian anti-trust authorities (“FAS”) became one of the leading law enforcement agencies in Russia with significant powers (including dawn raids, cooperation with police and other state bodies). It has offices in most of regions of Russia;

• Unlike traditional anti-trust authorities, FAS deals not only with competition matters, but with tariff regulations, state procurement, investments into strategic sectors, food retail;

• Key industries under control include: oil and oil products, chemicals, food, automotive, pharmaceuticals, state procurement, transportation and logistics

44

19 January 2016

PwC Russia

Antimonopoly regulations

Antimonopoly Regulations in Russia –Key Requirements to Conducting Business

• Similarly to most jurisdictions, key Russian anti-trust concepts include:

− abuse of dominant position (key concerns include refusal to deal, discriminatory practices, effect of foreign anti-bribery rules);

− cartels (including various communications in the business associations);

− vertical agreements (key focus is on distribution agreements and various restrictions and exclusive rights; IP-related defense is not always available);

− other prohibited agreements (list is not exhaustive);

− unfair competition;

− merger control (significant number of transactions, even intra-group, may require antimonopoly clearance)

45

19 January 2016

PwC Russia

Antimonopoly regulations

Antimonopoly Regulations in Russia –Key Requirements to Conducting Business

• Careful consideration of planned practices is recommended since claims from FAS may significantly disrupt the business:

− reputational damage;

− turnover penalties (up to 15%) for companies;

− criminal liability for company officers;

− disqualification from office;

− civil suits from damaged party

46

19 January 2016

PwC Russia

2.3. Employment law

47

19 January 2016

PwC Russia

Employment law

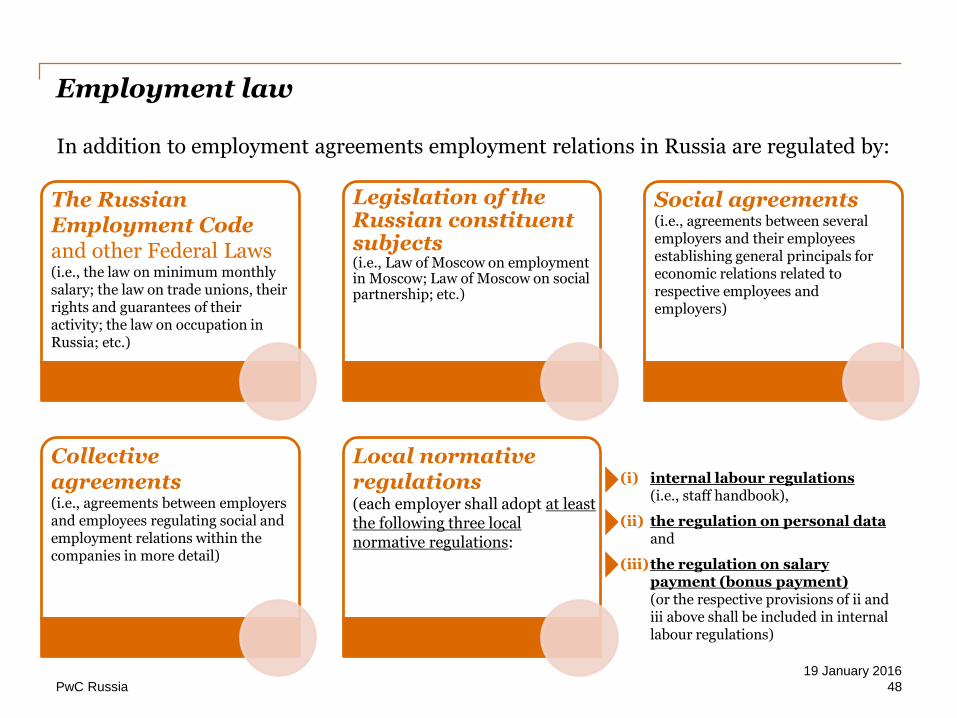

In addition to employment agreements employment relations in Russia are regulated by:

The Russian Employment Codeand other Federal Laws (i.e., the law on minimum monthly salary; the law on trade unions, their rights and guarantees of their activity; the law on occupation in Russia; etc.)

Legislation of the Russian constituent subjects(i.e., Law of Moscow on employment in Moscow; Law of Moscow on social partnership; etc.)

Social agreements(i.e., agreements between several employers and their employees establishing general principals for economic relations related to respective employees and employers)

Collective agreements (i.e., agreements between employers and employees regulating social and employment relations within the companies in more detail)

Local normative regulations(each employer shall adopt at least the following three local normative regulations:

(i) internal labour regulations(i.e., staff handbook),

(ii) the regulation on personal dataand

(iii)the regulation on salary payment (bonus payment)(or the respective provisions of ii and iii above shall be included in internal labour regulations)

48

19 January 2016

PwC Russia

Employment law

• The employment agreement shall include, inter alia, the following terms:

− the place of work;

− job function;

− duration (as a general rule the employment agreement shall be concluded for an indefinite term. If the employment agreement is concluded for a fixed term, the reason for concluding the agreement for the fixed term shall be provided);

− salary payment and compensation terms

• Conclusion of the employment agreement implies:

− familiarization of the employee against the signature with duly local normative regulations (i.e., internal policies);

− actual signature of the agreement by the employer and the employee;

− formalising HR documents (order on employment, labour book, personal card)

• Termination of the employment agreement

− the agreement may be terminated only based on the grounds stipulated in the Russian employment law;

− on the last working day the employer must make all final settlements with the employee and formalize the respective HR documentation

49

19 January 2016

PwC Russia

Employment law

The main guarantees for the employee

• Employer is obliged to pay the salary in RUB not less than every half a month on days established by internal labour regulations, state authorities require to specify and pay salary in RUB;

• Salary and other work related payments (i.e., bonuses) shall be made by the employer, not by a third party (e.g. another company of the employer’s group);

• The employee is entitled to annual paid vacation of duration not less than 28 calendar days, the normal duration of working hours per week shall not exceed 40 hours;

• The employee may be engaged into work on weekends and on public holidays only in accordance with the procedure established by the law (generally employers have to pay twice as much for the employees’ working on weekends and public holidays);

• The employee shall be reimbursed for expenses incurred during a business trip and shall be paid during the period of temporary disability (time of business trips and vacations shall be paid based on average salary)

50

19 January 2016

PwC Russia

Employment law

Administrative liability

For legal entities: administrative fine of up to RUB 50,000, or administrative suspension of the activity for the period up to 90 days

For executives: administrative fine of up to RUB 5,000

Material liability

The employer may be hold materially liable for the violation of the terms for salary payment, payment for vacation, payment due to the termination of the employment agreement and other payments. If this is the case, the employer will be obliged to make respective payments with interest in the amount established by the law for each day of delay starting from the next day after the due payment date.

Compensation of moral damage

The employer shall compensate moral damage caused to the employee by the employer’s unlawful actions or inaction in a monetary form in the amount to be determined upon mutual agreement between parties to the employment agreement.

51

19 January 2016

PwC Russia

2.4. Migration law

52

19 January 2016

PwC Russia

Migration law

Legal status of foreign nationals in the Russian Federation

Foreign nationals in Russia have the same rights and obligations in terms of the employment law as the Russian nationals, except as otherwise provided by law (e.g. it is prohibited for a foreign national to do the military and civil service in Russia).

Most issues regarding the legal status of foreign nationals in Russia are governed by Federal Law "On Legal Status of Foreign Nationals in the Russian Federation" No. 115-FZ of 25 July 2002, other laws and bylaws.

Chinese nationals shall generally obtain visas to entry Russia. The visa, its category, type and the travel purpose should correspond to the real purpose of coming into Russia and the foreigner's activity in Russia.

53

19 January 2016

PwC Russia

Migration law

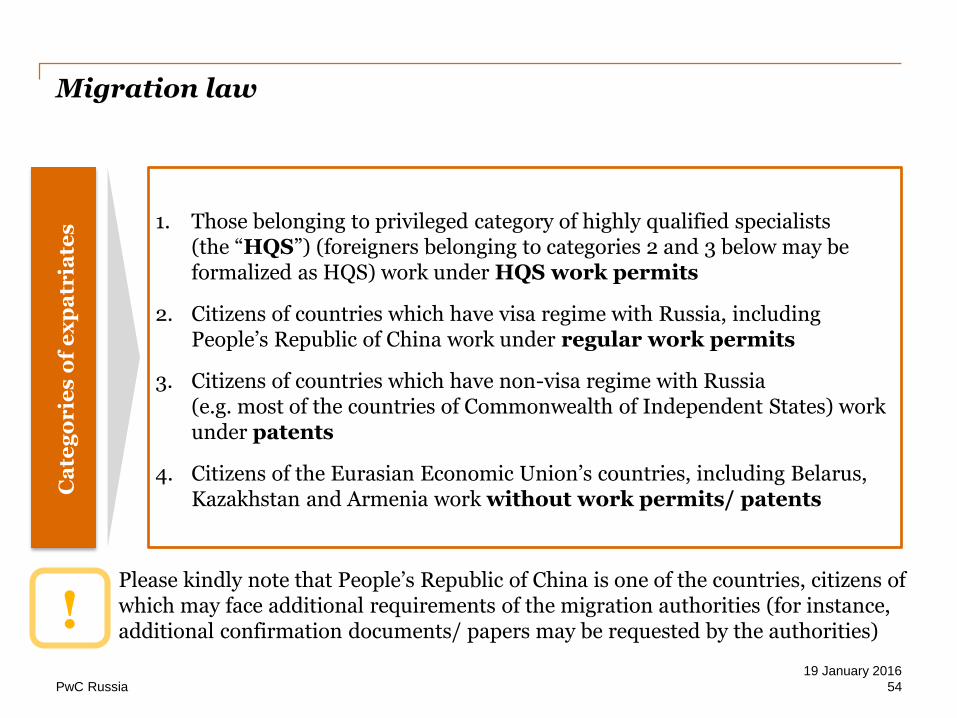

1. Those belonging to privileged category of highly qualified specialists (the “HQS”) (foreigners belonging to categories 2 and 3 below may be formalized as HQS) work under HQS work permits

2. Citizens of countries which have visa regime with Russia, including People’s Republic of China work under regular work permits

3. Citizens of countries which have non-visa regime with Russia (e.g. most of the countries of Commonwealth of Independent States) work under patents

4. Citizens of the Eurasian Economic Union’s countries, including Belarus, Kazakhstan and Armenia work without work permits/ patents

Ca

teg

or

ies

of

ex

pa

tria

tes

Please kindly note that People’s Republic of China is one of the countries, citizens of which may face additional requirements of the migration authorities (for instance, additional confirmation documents/ papers may be requested by the authorities)!

54

19 January 2016

PwC Russia

Migration law

HQS as a privileged category

• Salary level of not less than 167,000 RUB per month payable through a Russian payroll;

• Quarterly reports of salary payments;

• NO quota;

• NO employment permit;

• Generally employer is judging the HQS’ qualification based on its own expectations;

• Multi entry work visa and HQS work permit are issued for up to 3 years;

• Multi entry work visas for accompanying family members are issued for up to 3 years;

• Simplified migration registration requirements;

• The migration authorities formalise HQS work permit within 14 working days

55

19 January 2016

PwC Russia

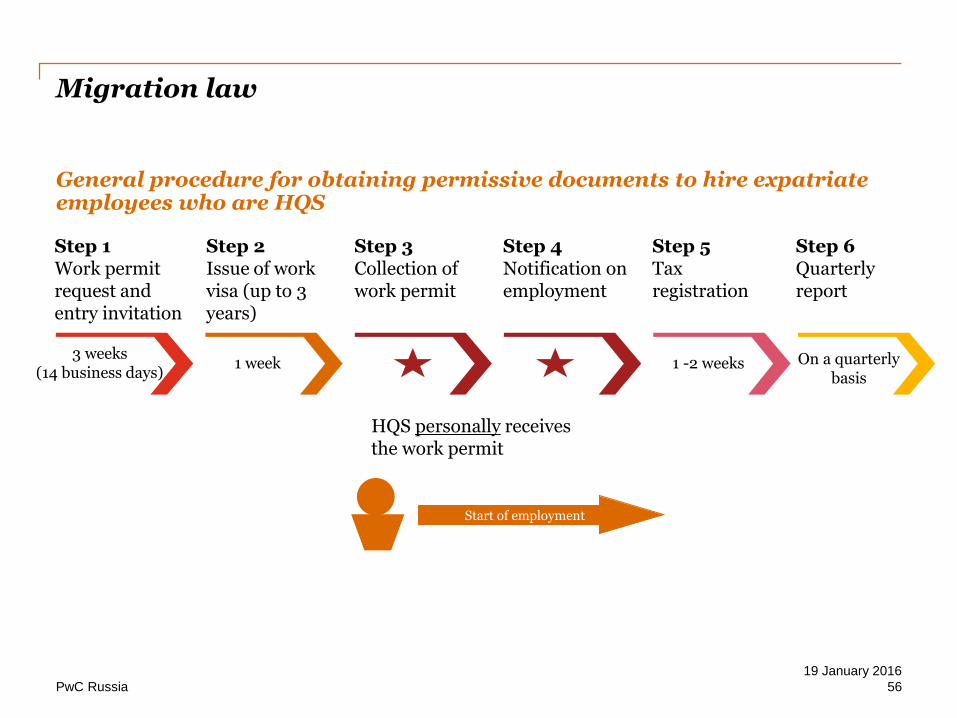

General procedure for obtaining permissive documents to hire expatriate employees who are HQS

Step 1Work permit request and entry invitation

Step 2Issue of work visa (up to 3 years)

Step 4Notification on employment

Start of employment

Step 5Tax registration

Step 6Quarterly report

Step 3Collection of work permit

HQS personally receives the work permit

Migration law

3 weeks(14 business days)

1 week 1 -2 weeks On a quarterly basis

56

19 January 2016

PwC Russia

Business trips aspects to be considered

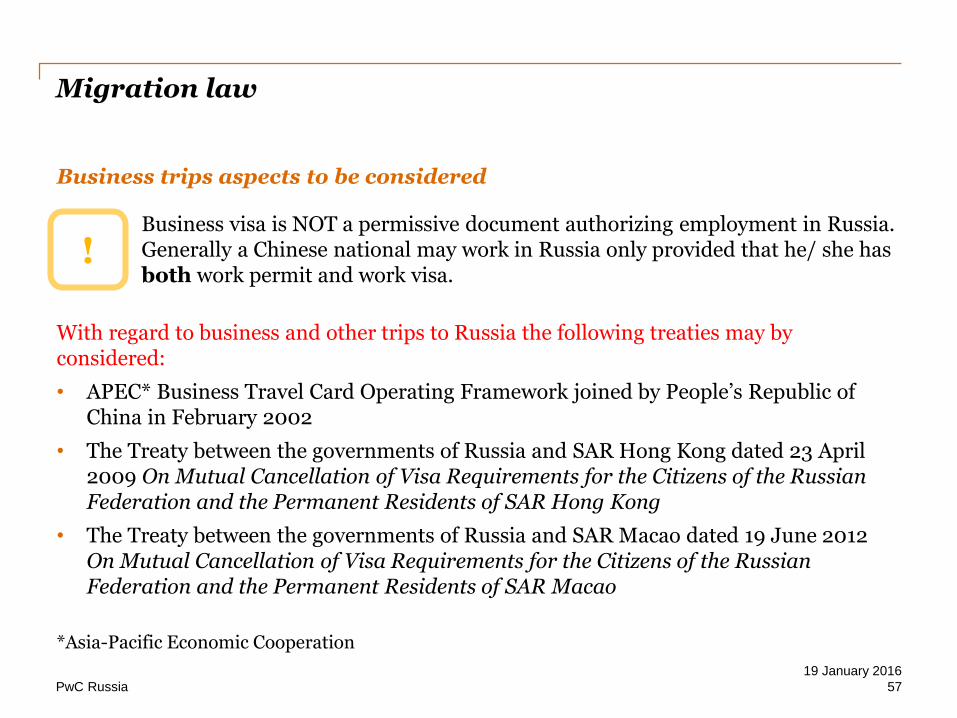

Business visa is NOT a permissive document authorizing employment in Russia. Generally a Chinese national may work in Russia only provided that he/ she has both work permit and work visa.

!

With regard to business and other trips to Russia the following treaties may by considered:

• APEC* Business Travel Card Operating Framework joined by People’s Republic of China in February 2002

• The Treaty between the governments of Russia and SAR Hong Kong dated 23 April 2009 On Mutual Cancellation of Visa Requirements for the Citizens of the Russian Federation and the Permanent Residents of SAR Hong Kong

• The Treaty between the governments of Russia and SAR Macao dated 19 June 2012 On Mutual Cancellation of Visa Requirements for the Citizens of the Russian Federation and the Permanent Residents of SAR Macao

*Asia-Pacific Economic Cooperation

Migration law

57

19 January 2016

PwC Russia

Business trips aspects to be considered

• Business Visa is subdivided into different sub-types of purpose of the visit, e.g. Business Visa sub-type Commercial, Business Visa sub-type Technical Maintenance, etc.;

• If a foreign national entered Russia on the basis of Business Visa sub-type Commercial, he/ she may attend business meetings, participate in auctions, negotiate and sign contracts but may not install, service, or repair the equipment (the activities that are allowed under Business Visa sub-type Technical Maintenance);

• The description of the activities permitted under each sub-type of Business Visa may be found in Purposes of the Visit approved by the Order of the Russian Ministry of Foreign Affairs No. 19723A, Order of the Russian Ministry of Internal Affairs No. 1048, Order of the Russian Federal Security Service No. 922 on 27 December 2003

Migration law

58

19 January 2016

PwC Russia

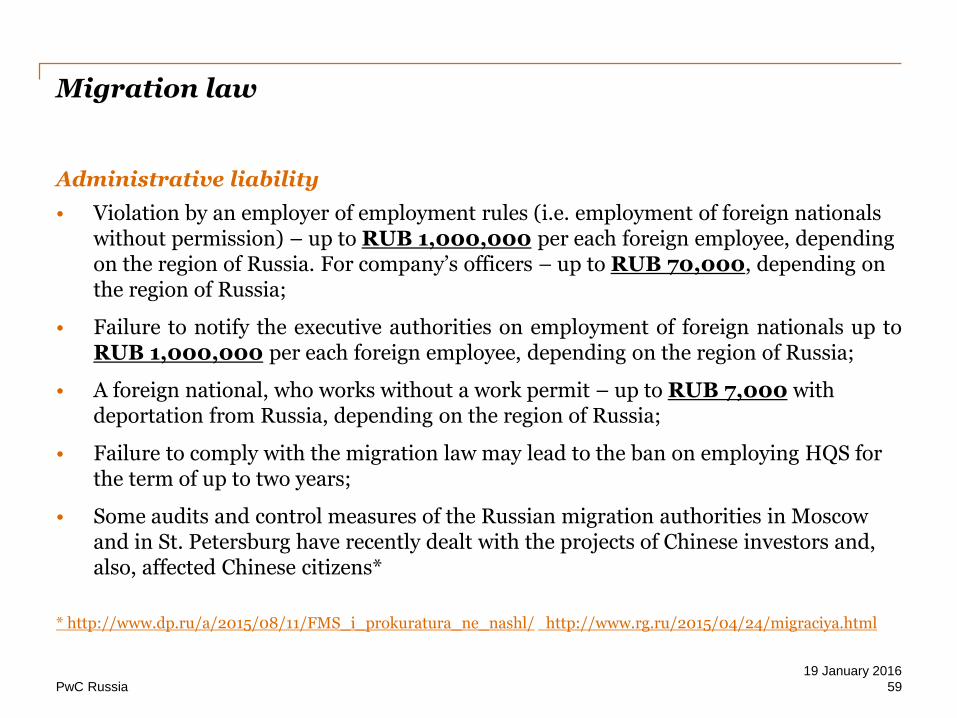

Administrative liability

• Violation by an employer of employment rules (i.е. employment of foreign nationals without permission) – up to RUB 1,000,000 per each foreign employee, depending on the region of Russia. For company’s officers – up to RUB 70,000, depending on the region of Russia;

• Failure to notify the executive authorities on employment of foreign nationals up toRUB 1,000,000 per each foreign employee, depending on the region of Russia;

• A foreign national, who works without a work permit – up to RUB 7,000 with deportation from Russia, depending on the region of Russia;

• Failure to comply with the migration law may lead to the ban on employing HQS for the term of up to two years;

• Some audits and control measures of the Russian migration authorities in Moscow and in St. Petersburg have recently dealt with the projects of Chinese investors and, also, affected Chinese citizens*

* http://www.dp.ru/a/2015/08/11/FMS_i_prokuratura_ne_nashl/ http://www.rg.ru/2015/04/24/migraciya.html

Migration law

59

19 January 2016

PwC Russia

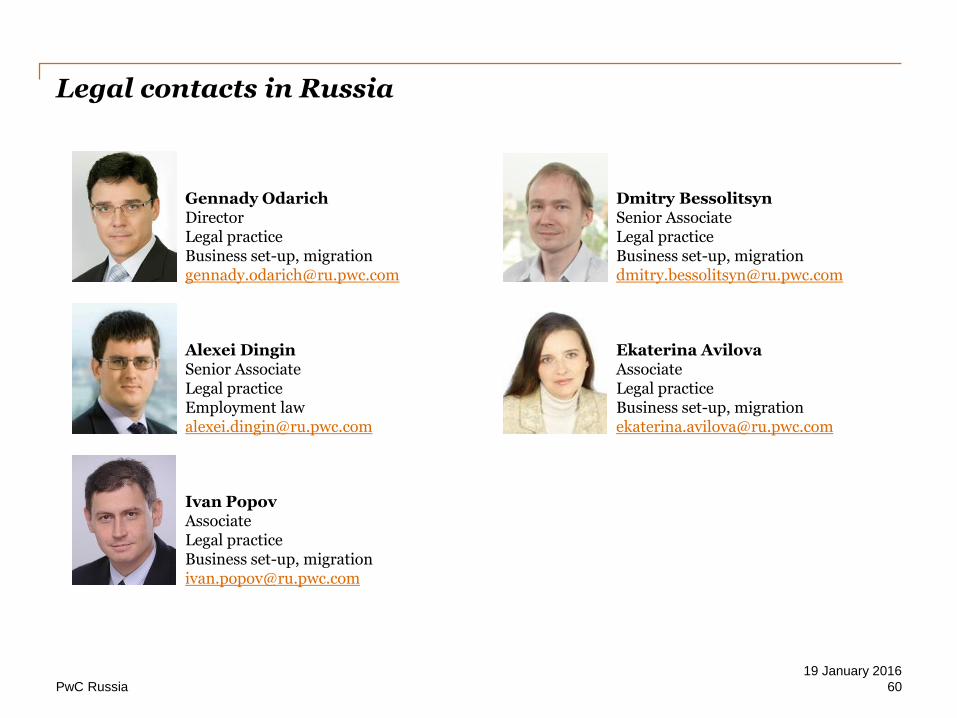

Legal contacts in Russia

Gennady OdarichDirectorLegal practiceBusiness set-up, [email protected]

Dmitry BessolitsynSenior AssociateLegal practiceBusiness set-up, [email protected]

Alexei DinginSenior AssociateLegal practiceEmployment [email protected]

Ekaterina AvilovaAssociateLegal practiceBusiness set-up, [email protected]

Ivan PopovAssociateLegal practiceBusiness set-up, [email protected]

60

19 January 2016

PwC Russia

Tax and non-tax incentives available in Russia

61

19 January 2016

PwC Russia

Types of tax and non-tax incentives available for investors in Russian regions

*All calculations in this presentation made are based on the exchange rate USD 1 = RR 55

Special investment contract

• Special investment contract is established to foster the

development of manufacturing and innovative sectors of the

Russian economy;

• Tax and non-tax incentives (tax and customs incentives, privilege

on rent payment for land plot, grandfather clause etc.);

• Currently is a matter of legislative process.

Some federal non-tax incentives

• Subsidies of part of interests for financing of investment project;

• Free railway transportation to and from Russian Far East.

• Special-purpose loans for investment projects using the

mechanism of project finance.

Free port Vladivostok

• Designed to develop near-bordered Primorsk region;

• Tax incentives (profits tax, social contributions reduced rates);

• Other non-tax incentives (facilitated processes for foreign citizens

etc.);

• Free customs zone.

Advanced development zones

• Designed for investment attraction to Russian Federation and

first implementation planned for Russian Far East and small

towns;

• Tax incentives (profits tax, property tax, social contributions

reduced rates);

• Other non-tax incentives (eg, simplified migration rules for

foreign citizens employment, special land use regime, etc);

• Free customs zone.

Regional investment project

• Established for investment attraction to Russian Far East;

• Tax incentives (profits tax, property tax, land tax).

Industrial special economic zones

• Designed to develop Russian industry;

• Tax incentives (profits tax, property tax, land tax);

• Free customs zone;

• Other non-tax incentives in some regions (eg, simplified

migration rules for foreigners, fixed lease of land payment, etc);

• State and regional guarantees to banks granting loans to

investors.

Regional tax incentives

• Tax incentives (profits tax, property tax, land tax, transport tax);

• Regional monetary subsidies;

• Regional guarantees to banks financing investors;

• Informational support.

62

19 January 2016

PwC Russia

1. Regional tax incentives

63

19 January 2016

PwC Russia

Regional tax incentives and non-tax forms of support for investors: overview

• Russian Tax Law assumes possibility for regions to develop their own systems of tax incentives and non-tax forms of support for investors.

• Such incentives in respect of regional taxes shall be established and abolished by Russian Tax Code and (or) by tax laws of regions of the Russian Federation.

• Under article 56 of Russian Tax Code tax incentives are privileges granted to individual categories of taxpayers and envisaged by the tax legislation as compared with other taxpayers; such privilege includes the possibility not to pay a tax or to pay a smaller amount of tax.

• Non-tax incentives include but are not limited to the following:

− Provision of budget subsidies, investments for the partial compensation of investment expenses;

− Provision of government guarantee to banks granting loans to investors;

− Simplified access to infrastructure facilities;

− Provision of regional property on lease or as concession or as contribution into the charter capital;

− Decrease of rent payments for investors renting land from the regional government;

− Information, administrative and legal support;

− Others.

• As of today many Russian industrial regions have diverse systems of stimulation measures for investors, which generally assume profit, property, transport or land tax exemptions.

64

19 January 2016

PwC Russia

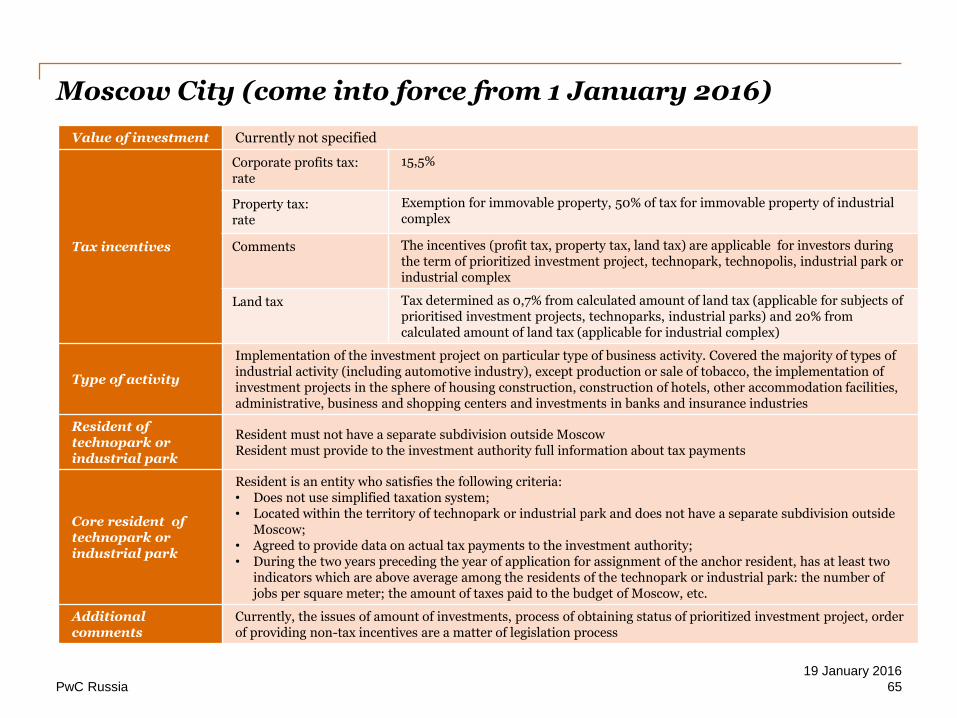

Moscow City (come into force from 1 January 2016)

Value of investment Currently not specified

Tax incentives

Corporate profits tax:rate

15,5%

Property tax:rate

Exemption for immovable property, 50% of tax for immovable property of industrial complex

Comments The incentives (profit tax, property tax, land tax) are applicable for investors during the term of prioritized investment project, technopark, technopolis, industrial park or industrial complex

Land tax Tax determined as 0,7% from calculated amount of land tax (applicable for subjects of prioritised investment projects, technoparks, industrial parks) and 20% from calculated amount of land tax (applicable for industrial complex)

Type of activity

Implementation of the investment project on particular type of business activity. Covered the majority of types of industrial activity (including automotive industry), except production or sale of tobacco, the implementation of investment projects in the sphere of housing construction, construction of hotels, other accommodation facilities, administrative, business and shopping centers and investments in banks and insurance industries

Resident of technopark or industrial park

Resident must not have a separate subdivision outside MoscowResident must provide to the investment authority full information about tax payments

Core resident of technopark or industrial park

Resident is an entity who satisfies the following criteria:• Does not use simplified taxation system;• Located within the territory of technopark or industrial park and does not have a separate subdivision outside

Moscow;• Agreed to provide data on actual tax payments to the investment authority;• During the two years preceding the year of application for assignment of the anchor resident, has at least two

indicators which are above average among the residents of the technopark or industrial park: the number of jobs per square meter; the amount of taxes paid to the budget of Moscow, etc.

Additionalcomments

Currently, the issues of amount of investments, process of obtaining status of prioritized investment project, order of providing non-tax incentives are a matter of legislation process

65

19 January 2016

PwC Russia

2. Special economic zones

66

19 January 2016

PwC Russia

Special economic zones: overview

Russian special economic zones are established to foster the development of manufacturing and innovative sectors of the Russian economy, to develop tourism, health and resort activity, to stimulate the development of new technology and types of products and improve the port and transport infrastructure in Russia

Each type of SEZ provides tax and customs benefits as well as other kinds of economic incentives in order to stimulate economic development of the particular region

• Industrial SEZ (main activity – manufacturing of goods);

• Technological SEZ (main activity – creation of innovative and IT products);

• Tourism SEZ (main activity – construction and development of health and resort facilities);

• Port SEZ (main activity – warehousing, supply services for ships, ships maintenance and service works, wholesale trading, etc.).

The current Russian law on special economic zones (“SEZ”) envisages the following types of SEZ:

1

2

3

67

19 January 2016

PwC Russia

Kaliningrad region

Kaluga region

Samara region

Republic of Tatarstan

Sverdlovsk regionLipetsk region

Pskov region

Moscow

Crimea

Primorsk region

Stupino (Moscow region)

Industrial special economic zones on a map

Astrakhan region

Developing ISEZ

Developed ISEZ

68

19 January 2016

PwC Russia

Industrial special economic zones: overview

• Industrial special economic zones (“ISEZ”) are established by the Government of Russia on the territories of certain regions where (i) a special regime for business activity is applied and (ii) a free customs zone regime is applicable;

• The term of ISEZ is fixed for the period of 49 years and cannot be prolonged though for some regions the period might vary by law;

• Both tax and non-tax incentives are provided to the residents of ISEZ;

• In order to become a resident of ISEZ a candidate company must enter into an agreement with the Russian Ministry of Economic Development on carrying out industrial production and operational activities (“Agreement”);

• The status of the resident of ISEZ may be cancelled only by the court;

• The amount of investment to be eligible for the incentives shall not be less than 40 mln RR (0,73 mln USD) (except for Kaliningrad region where the minimum threshold is set at 150 mln RR (2,7 mln USD));

• Favourable rate of social contribution is established for residents of ISEZ in case of carrying out R&D activity.

69

19 January 2016

PwC Russia

3. Regional investment projects

70

19 January 2016

PwC Russia

Regional investment projects: overview

• Regional investment project is an investment project aimed at production of goods in a number of the East regions of the Russian Federation;

• The amount of investment shall not be less than 50 mln RR (0,91 mln USD) within the first 3 years or 500 mln RR (9.1 mln USD) within the first 5 years of an investment project (thresholds may be increased by regional law);

• Each Regional investment project shall be performed by one company only;

• The participant of a Regional investment project cannot be (i) a resident of SEZ, (ii) a resident of ADZ, (iii) has branches outside the region of Regional investment project, (iv) be in a consolidated group of taxpayers, (v) be non-commercial organisation, bank, insurance company, etc.;

• The federal part of profits tax rate for a participant of a Regional investment project is 0% (standard rate is 2%) during 10 years when the first revenues from sale of goods produced under the Regional investment project were received (these revenues should amount to 90% of all revenues of the participant);

• The regional part of profits tax rate (standard rate is 18%) for a participant of a Regional investment project cannot be more than 10% during first five years of implementation of the Regional investment project and cannot be less than 10% during the following 5 years (specific rates are established by regional law);

• Tax incentives remain in force through 1 Jan 2029 (the period of tax incentives for those investors who invested not less than 50 mln RR (0,91 mln USD) during first three years of implementation of a Regional investment project ends on 1 Jan 2027);

• Regional investment project regime applies to all Russian East Siberia and Far East regions.

71

19 January 2016

PwC Russia

Selected regional investment project on a map

Primorsk region

Moscow

72

19 January 2016

PwC Russia

Regional investment project: Primorsk region

Profits tax incentives

Rate Period Comment

0% 0-5 years

1. If a participant of a Regional investment project having invested 50 mln RR (0,91 mln USD) or more does not receive revenues during the first three years of implementation of the Regional investment project, the profits tax incentives (both in federal and regional parts) will be applicable from the 4th

year from the date of obtaining the Regional investment project participant status.

2. If a participant of a Regional investment project having invested 500 mlnRR (9,1 mln USD) or more does not receive revenues during first five years of implementation of the Regional investment project, the profits tax incentives (both in federal and regional parts) will be applicable from the 6th year from the date of obtaining the Regional investment project participant status.

10% 6-10 years

20%After the 10th year

Property tax incentives 0% (0-5 years) 0,5% (6-10 years)

Land tax incentives in some Primorsk regions (instead of standard 1,5% rate)

Vladivostok Ussuriysk district

500 mln RR (9,1 mln USD) investment within 5 years

0,3% during 5 years

0% during 5 years(tax preference ends 1 Jan 2027)

150 mln RR (2,7 mln USD) investment within 3 years

0,6% during 3 years

Type of activityAny type of activity (except for oil and gas production, transportation of oil and gas, petrol, tobacco and alcohol production)

Investment declaration Required

Investment project Required

73

19 January 2016

PwC Russia

4. Advanced development zones

74

19 January 2016

PwC Russia

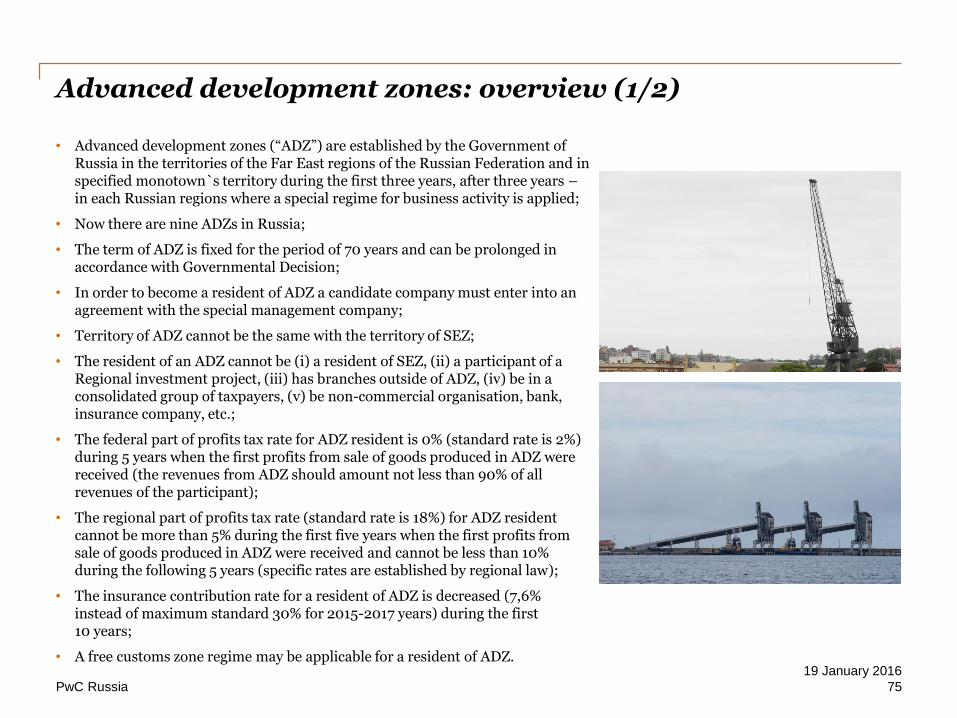

Advanced development zones: overview (1/2)

• Advanced development zones (“ADZ”) are established by the Government of Russia in the territories of the Far East regions of the Russian Federation and in specified monotown`s territory during the first three years, after three years –in each Russian regions where a special regime for business activity is applied;

• Now there are nine ADZs in Russia;

• The term of ADZ is fixed for the period of 70 years and can be prolonged in accordance with Governmental Decision;

• In order to become a resident of ADZ a candidate company must enter into an agreement with the special management company;

• Territory of ADZ cannot be the same with the territory of SEZ;

• The resident of an ADZ cannot be (i) a resident of SEZ, (ii) a participant of a Regional investment project, (iii) has branches outside of ADZ, (iv) be in a consolidated group of taxpayers, (v) be non-commercial organisation, bank, insurance company, etc.;

• The federal part of profits tax rate for ADZ resident is 0% (standard rate is 2%) during 5 years when the first profits from sale of goods produced in ADZ were received (the revenues from ADZ should amount not less than 90% of all revenues of the participant);

• The regional part of profits tax rate (standard rate is 18%) for ADZ resident cannot be more than 5% during the first five years when the first profits from sale of goods produced in ADZ were received and cannot be less than 10% during the following 5 years (specific rates are established by regional law);

• The insurance contribution rate for a resident of ADZ is decreased (7,6% instead of maximum standard 30% for 2015-2017 years) during the first 10 years;

• A free customs zone regime may be applicable for a resident of ADZ.

75

19 January 2016

PwC Russia

Advanced development zones: overview (2/2)

Moscow

Mikhailovskiy(Primorsk region)

Beringovskiy(Chukotka Autonomous okrug)

Kamchatka(the Kamchatka region)

Kangalassy(The Republic of Sakha (Yakutia))

Belogorsk(Amur region)

Priamurskaya(Amur Region)

The number of ADZ has rapidly increased within the last couple of months. The following ADZs have been recently established:

76

19 January 2016

PwC Russia

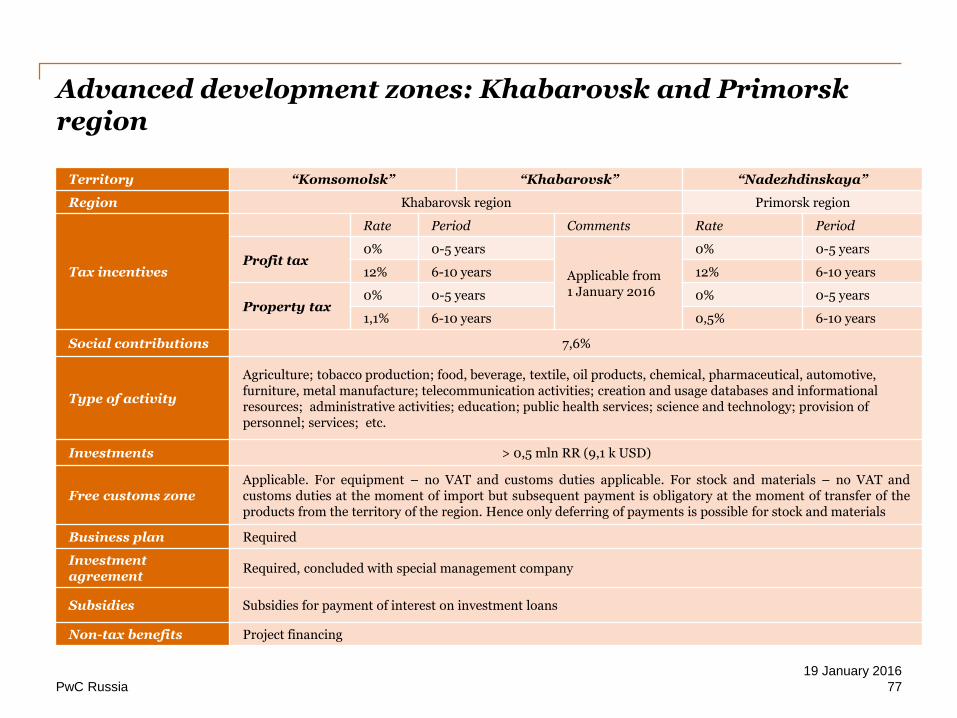

Advanced development zones: Khabarovsk and Primorsk region

Territory “Komsomolsk” “Khabarovsk” “Nadezhdinskaya”

Region Khabarovsk region Primorsk region

Tax incentives

Rate Period Comments Rate Period

Profit tax0% 0-5 years

Applicable from 1 January 2016

0% 0-5 years

12% 6-10 years 12% 6-10 years

Property tax0% 0-5 years 0% 0-5 years

1,1% 6-10 years 0,5% 6-10 years

Social contributions 7,6%

Type of activity

Agriculture; tobacco production; food, beverage, textile, oil products, chemical, pharmaceutical, automotive, furniture, metal manufacture; telecommunication activities; creation and usage databases and informational resources; administrative activities; education; public health services; science and technology; provision of personnel; services; etc.

Investments > 0,5 mln RR (9,1 k USD)

Free customs zoneApplicable. For equipment – no VAT and customs duties applicable. For stock and materials – no VAT andcustoms duties at the moment of import but subsequent payment is obligatory at the moment of transfer of theproducts from the territory of the region. Hence only deferring of payments is possible for stock and materials

Business plan Required

Investment agreement

Required, concluded with special management company

Subsidies Subsidies for payment of interest on investment loans

Non-tax benefits Project financing

77

19 January 2016

PwC Russia

5. Free port Vladivostok

78

19 January 2016

PwC Russia

Free port Vladivostok: overview

• Free port Vladivostok is established by the Government of Russia in the territories of Primorsk region;

• The term of Free port Vladivostok is fixed for the period of 70 years and can be prolonged in accordance with Governmental Decision;

• In order to become a resident of Free port Vladivostok a candidate company must enter into an agreement with the special management company;

• Territory of an Free port Vladivostok cannot be the same with territory of SEZ or ADZ;

• The resident of Free port Vladivostok cannot be (i) a resident of SEZ, (ii) a participant of a Regional investment project, (iii) has branches outside of Free port Vladivostok , (iv) in a consolidated group of taxpayers, (v) non-commercial organisation, bank, insurance company, etc.;

• The federal part of profits tax rate for Free port Vladivostok residents is 0% (standard rate is 2%) during 5 years, social contributions rate for a Free port Vladivostok residents is 7,6% (standard rate is 30 %) during the first 10 years. The regional part of profits tax rate (standard rate is 18%) for Free port Vladivostok residents cannot be more than 5% during the first five years when the first profits from sale of goods produced in Free port Vladivostok were received and cannot be less than 10% during the following 5 years (specific rates are established by regional law);

• A free customs zone regime may be applicable for a resident of Free port Vladivostok;

• The above mentioned provisions will come into force from 1 January 2016.

79

19 January 2016

PwC Russia

Free port Vladivostok

Investments > 5 mln RR (0,9 mln USD)

Property Tax0% 0-5 years

0,5% 6-10 years

Free customs zone (treated as SEZ)

For equipment – no VAT and customs duties applicable. For stock and materials – no VAT and customs duties at the moment of import but subsequent payment is obligatory at the moment of transfer of the products from the territory of the region. Hence only deferring of payments is possible for stock and materials

Business plan Required

Investment agreement

Required, concluded with special management company

Investment projectRequired (or business activity stated by investment agreement should be new for the participant of selection)

Non-tax benefits

Facilitated visa process for foreign citizens (presence within 8 days);Elimination of recruitment permission for foreign citizens;Provision of work permission for foreign citizens without regard to quota;Special management company’s right to protect residents’ legitimate interests.

80

19 January 2016

PwC Russia

6. Special Investment Contracts (SpIC)

81

19 January 2016

PwC Russia

Special Investment Contracts: overview

• Special Investment Contracts are established to foster the development of manufacturing and innovative sectors of the Russian economy;

• The following tax and non-tax incentives will be granted to investors:

− Individual tax benefits valid through the whole period of the special investment contract (but not more than 10 years);

− Beneficial ‘made in Russia’ criteria;

− Non-tax incentives (e. g. access to state tenders);

− Grandfathering tax clause;

− Moratorium on tax audits;

− Other industry stimulation measures.

82

19 January 2016

PwC Russia

7. Main problems facing by investors

83

19 January 2016

PwC Russia

Main problems facing by investors

Therefore detailed analysis of the legislative provisions and the terms of the investment agreement are needed to minimise potential risks.

Investment agreement

The application procedure for conclusion of the investment agreement, the list of documents/ information and criteria are not well elaborated which creates uncertain environment for investors.

Tax audits

Tax authorities may challenge application of tax incentives by investor based on their own interpretation or ambiguity of the regional legislation provisions and terms of the investment agreement..

Grandfathering provisions

Sometimes the changes of "rules of the game" may occur during the lifetime of investment project and the application of grandfathering clauses may not be guaranteed.

Subsidies

Due to budget constraints some of the compensations and subsidies promised by the regional authorities are not received by investor.

Our experience shows that despite all the efforts of Russian Government and regional authorities to create attractive environment for investors, in practice investors can face the following issues:

84

19 January 2016

PwC Russia

Changing customs environment and modern instruments for supporting importers in Russia

85

19 January 2016

PwC Russia

1. Changing customs environment

86

19 January 2016

PwC Russia

Changing customs environment

• Modernized Customs Code is under development;

• Development of unified approach to treatment of license fees from customs perspective.

• Accession of Armenia and Kyrgyzstan to the EAEU expands interconnected market of the EAEU and provides for additional opportunities for business;

• The EAEU Treaty facilitates trade of goods and services within the EAEU by unification of legislative requirements (e.g. regulations related to technical standards and safety requirements, access to the state procurements, etc.).

Expansion and further integration within the Eurasian Economic Union (EAEU)

Further development of common customs legislation

87

19 January 2016

PwC Russia

Changing customs environment

• Some of Kazakhstan’s commitments taken upon accession to WTO differs from the EAEU legislation, which may create additional opportunities or challenges for companies working in Kazakhstan: − Reduction of import customs duties for some goods

imported into Kazakhstan (more than 3,000 customs codes);

− Withdrawal of special incentives programs

• Therefore, influence of Kazakhstani commitments on the current supply chain of companies operating within the EAEU requires further analysis and monitoring.

• Electronic declaration and development of “single window” approach;

• Managing of “low risk” importers;

• Testing of “Green Channel” for goods imported from China.

Approaches of the Russian customs authorities to administration of the customs clearance

Accession of Kazakhstan to the WTO

88

19 January 2016

PwC Russia

Changing customs environmentNew challenges

• New Free Trade Agreement with Vietnam;

• Negotiations with Israel and Egypt regarding Free Trade Agreements;

• Withdrawal from the Free Trade Zone in respect of the Ukrainian goods

Change of the trade regimes

Trade barriers

• Bans on imports into Russia of some goods from a number of countries;

• Introduction of barriers to foreign goods (e.g. for participation in state procurement tenders)

89

19 January 2016

PwC Russia

2. Special Investment Contracts (SpIC) — New instrument to support investors in Russia

90

19 January 2016

PwC Russia

SpIC and spheres of its application

Public Partner (Government)

Encouraging manufacturing activity

Private Investor (Business)Manufacturing of industrial products

Aim

Encouraging investments in manufacturing of industrial products: - ensuring stable business environment;- industry incentives and preferences.

New instrument for realization of the public-private partnership which is used for encouraging industrial-production growth in Russia

91

19 January 2016

PwC Russia

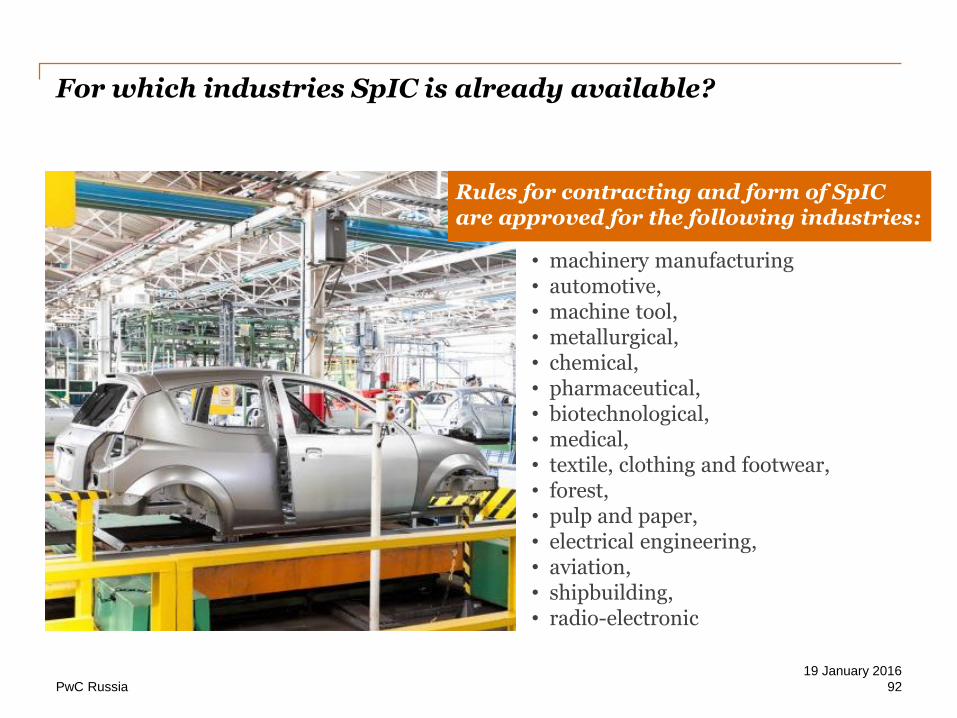

For which industries SpIC is already available?

• machinery manufacturing• automotive,• machine tool, • metallurgical,• chemical,• pharmaceutical,• biotechnological, • medical,• textile, clothing and footwear, • forest, • pulp and paper,• electrical engineering, • aviation, • shipbuilding,• radio-electronic

Rules for contracting and form of SpICare approved for the following industries:

92

19 January 2016

PwC Russia

Mutual guarantees and commitments

Other guarantees Other commitments

To provide priorityto use the stateproperty

To meet the agreed levelof localization

To give various stimulationmeasures

To implement new technology

To provide legalstability

To invest not less than RUB 750 million

Not to increase the overall tax burden

To set up or modernizeproduction facilities

SpIC

InvestorGovernment

93

19 January 2016

PwC Russia

What conditions should be established in a SpIC?

• Validity period (not longer than 10 years)

• Information about the investment project:

− characteristics of the products

− the amount of investments

− share of foreign materials, etc.

• Rights and obligations of the parties

• The control procedure

• The reporting procedure

• The list of incentive measures

• Responsibilities of the parties

94

19 January 2016

PwC Russia

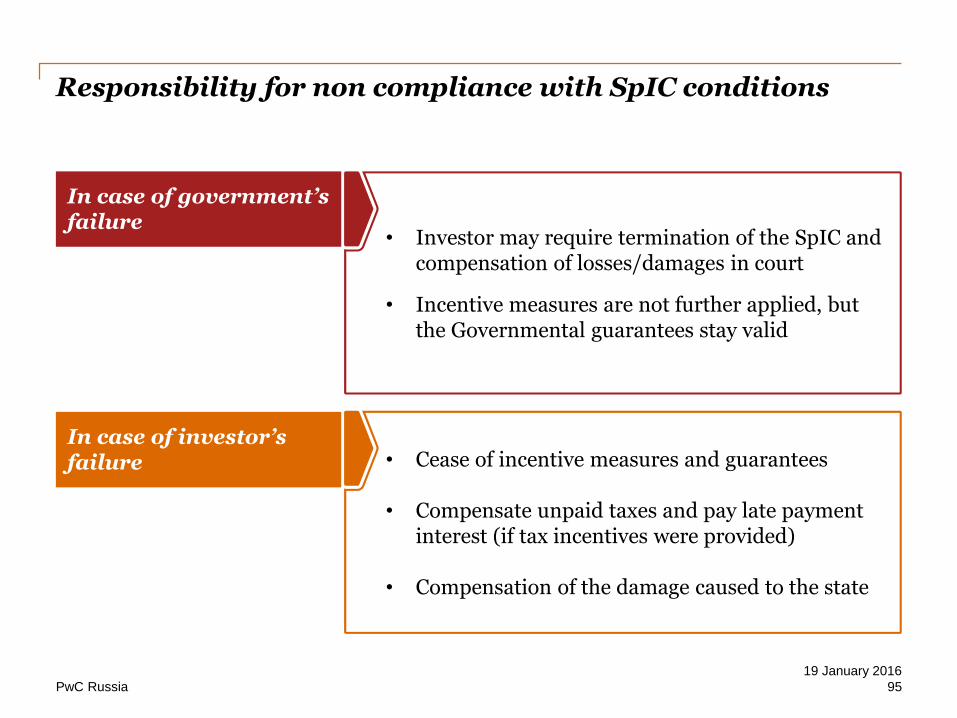

Responsibility for non compliance with SpIC conditions

In case of government’s failure

In case of investor’s failure • Cease of incentive measures and guarantees

• Compensate unpaid taxes and pay late payment interest (if tax incentives were provided)

• Compensation of the damage caused to the state

• Investor may require termination of the SpIC and compensation of losses/damages in court

• Incentive measures are not further applied, but the Governmental guarantees stay valid

95

19 January 2016

PwC Russia

Conclusions

• Dynamic and changing customs environment brings not only challenges but also opportunities for business;

• Business should constantly monitor and analyze changes in order to timely respond the challenges;

• Foreign companies should find out whether it is feasible and realistic to establish productionin Russia in order to enjoy new incentives.

96

19 January 2016

PwC Russia

Forensic review of the proper use of funds & due diligence of third parties

97

19 January 2016

PwC Russia

1. Forensic review of the proper use of funds in joint ventures and joint operations

98

19 January 2016

PwC Russia

Typical schemes for withdrawal of funds

Investment projects

“Black” revenue

Vendors (shell companies)

Loans and borrowings

Intermediaries in offshore

zones and other jurisdictions

Companies, affiliated with management

Salary project and ghost employees

DistributorsAdvance

payments

Withdrawal of funds

from the business

Purchases at artificially high

prices

“Black” revenue

Intermediaries in offshore

zones and other jurisdictions

DistributorsAdvance

payments

99

19 January 2016

PwC Russia

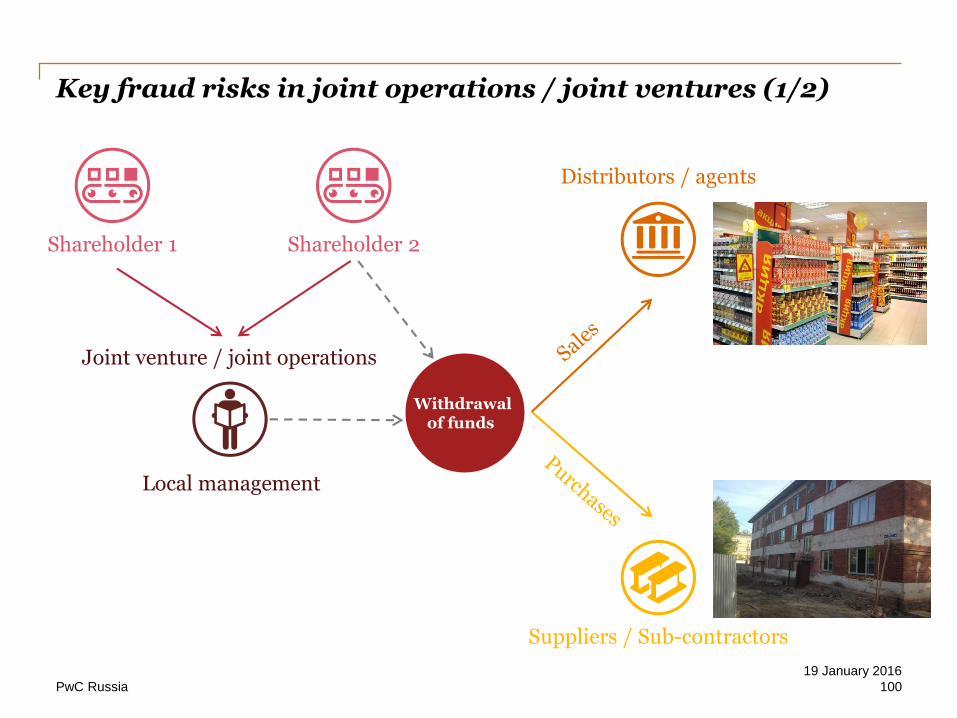

Key fraud risks in joint operations / joint ventures (1/2)

Shareholder 1 Shareholder 2

Local management

Withdrawal of funds

Joint venture / joint operations

Distributors / agents

Suppliers / Sub-contractors

100

19 January 2016

PwC Russia

Key fraud risks in joint operations / joint ventures (2/2)

Ghost employees are on payroll

• Usage of intermediaries affiliated with management

• Lack of economic substance of services purchased or fictitious services (consulting, marketing, legal services)

• Payments for no delivery or poor quality delivery of services by vendors

Procurement

• Sales through agents and intermediaries affiliated with management

• Improper pricing, inadequate usage of discounts / rebates / bonuses leading to the decrease of revenue

Sales of goods

• Overstatement of expenditure scale

• Duplication of construction work

• Fictitious design repair and maintenance works

• Lack of transparency in pricing

• Chain of sub-contractors affiliated with local management

Construction and repair

101

19 January 2016

PwC Russia

Example of a fraud scheme in procurement

Cooperation agreement (marketing) 50%/50%

Producer Local dealer/ Marketing team

Marketing company 1

Marketing company 2

Individual entrepreneur

Potentially connected

• Non-transparent Coop activities cost allocation• Marketing, consulting or legal services provided by low-profile companies, off-shore entities,

individual entrepreneurs• Inflated pricing for marketing services provided• Engaging agents and other third-parties for organising advertising and promotional events

Risk

102

19 January 2016

PwC Russia

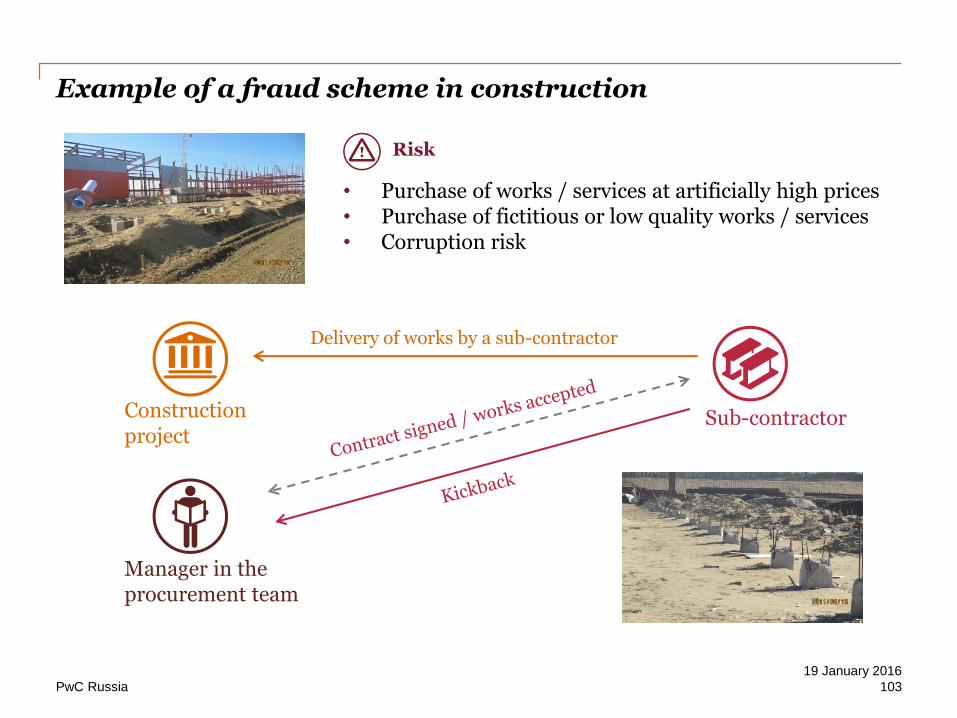

Example of a fraud scheme in construction

Construction project

Delivery of works by a sub-contractor

Manager in the procurement team

Sub-contractor

• Purchase of works / services at artificially high prices• Purchase of fictitious or low quality works / services• Corruption risk

Risk

103

19 January 2016

PwC Russia

Successful strategy of Chinese companies operating in the Russian and CIS market

• Know your customer (due diligence of customers, vendors)

• Control over joint venture activities

• Strong Internal Audit function

• Robust system of internal controls over assets and operations including:

− ‘four eyes’ principle

− contract authorization compliance

• Enhancing corporate culture and business ethics

104

19 January 2016

PwC Russia

How PwC Forensic can help

Review of the proper usage of the funds

Procurement review

Integrity due diligence review of subcontractors, distributors, vendors, customers etc.

Financial analysis and construction contracts review

Forensic support of the internal audit function in the investigation of the misconduct

Review of the overseas transactions

Anti-corruption compliance and remediation

105

19 January 2016

PwC Russia

2. Due diligence of third parties

106

19 January 2016

PwC Russia

Key third-party risks facing foreign investors in Russia (1/4)

Wide spread use of shell companies and/or intermediaries for tax and legal purposes

No requirement for companies to have unique names

Use of mass registration addresses

Close ties to politically exposed persons (PEPs) or ownership or management roles held by family members of PEPs

Sophisticated business structure with offshore element

Potential involvement in non-transparent asset acquisitions; instances of regulatory scrutiny; disqualifications; tax discipline

• Regulatory actions

• Financial losses

• Legal liabilities

• Damage to reputation

Non-transparent ownership structures, possible hidden interests involved

107

19 January 2016

PwC Russia

Example 1 – registration address is a demolition site of Hotel Russia (demolition started in 2006)

Address:

Varvarka street 6, Moscow

According to a Russian corporate database, there are

156 legal entities still

registered at the address of former Hotel Russia.

Key third-party risks facing foreign investors in Russia (2/4)

108

19 January 2016

PwC Russia

Example 2 – Mass registration address

Address:

Garibaldi Street 21, Moscow

The Russian Tax Authorities reports this address as being one of mass registration

(with 314 legal

entities registered there).

Key third-party risks facing foreign investors in Russia (3/4)

109

19 January 2016

PwC Russia

Key third-party risks facing foreign investors in Russia (4/4)

Example 3 – This is a visualization of the corporate structure of a Russian business group with noteworthy affiliations

110

19 January 2016

Thank you for your attention!

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained in

this publication, and, to the extent permitted by law, PwC Russia, its members, employees and