2015/16 peoplesoft year-end closing … peoplesoft year-end closing workshop ... 7310 must net to...

TRANSCRIPT

2015/16 PEOPLESOFT YEAR-END CLOSING

WORKSHOPDistrict Financial ServicesFinancial Accounting & ReportingMay 2, 2016

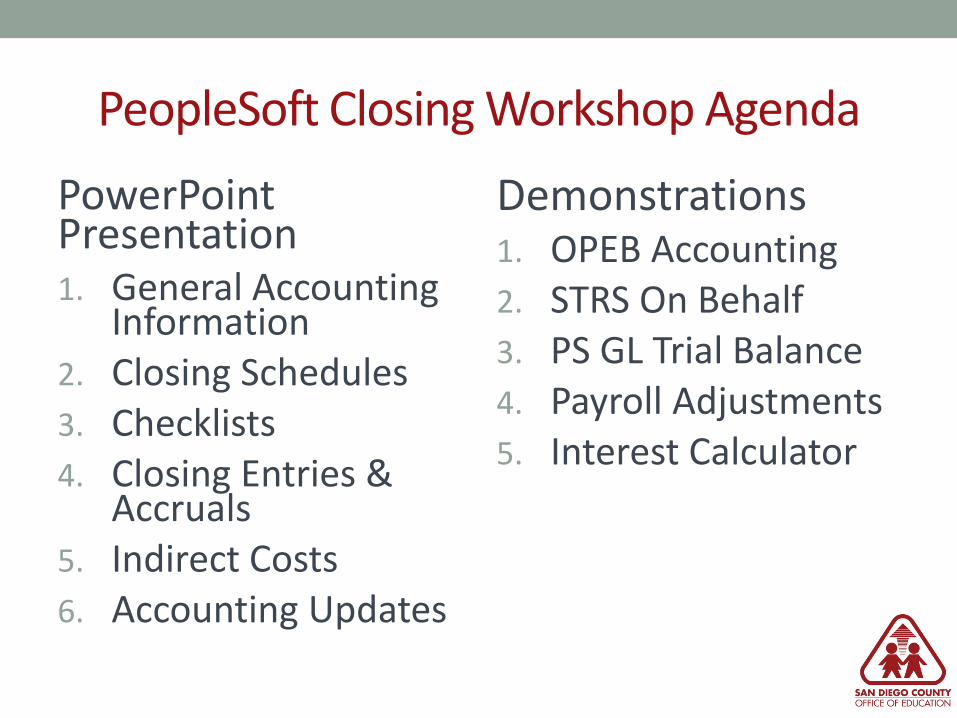

PeopleSoft Closing Workshop AgendaPowerPoint Presentation1. General Accounting

Information2. Closing Schedules3. Checklists4. Closing Entries &

Accruals5. Indirect Costs6. Accounting Updates

Demonstrations1. OPEB Accounting2. STRS On Behalf3. PS GL Trial Balance4. Payroll Adjustments5. Interest Calculator

SECTION 1General Accounting information

4

TITLE• Add text

5

TITLE• Add text

6

TITLE• Add text

7

TITLE

8

SECTION 2Closing Schedules

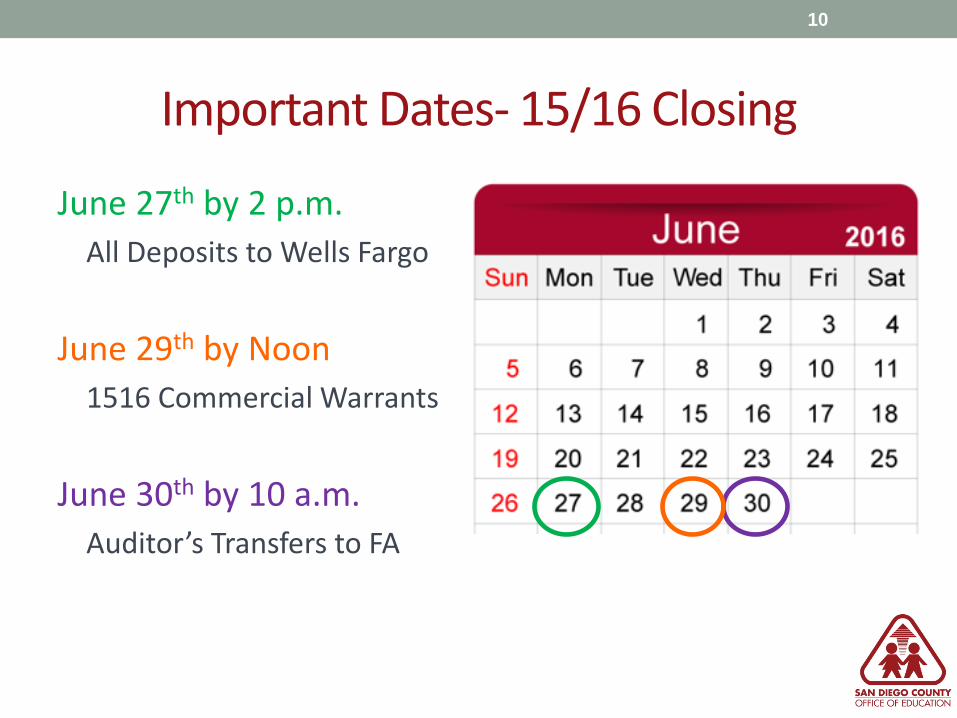

Important Dates- 15/16 Closing

June 27th by 2 p.m.All Deposits to Wells Fargo

June 29th by Noon1516 Commercial Warrants

June 30th by 10 a.m.Auditor’s Transfers to FA

10

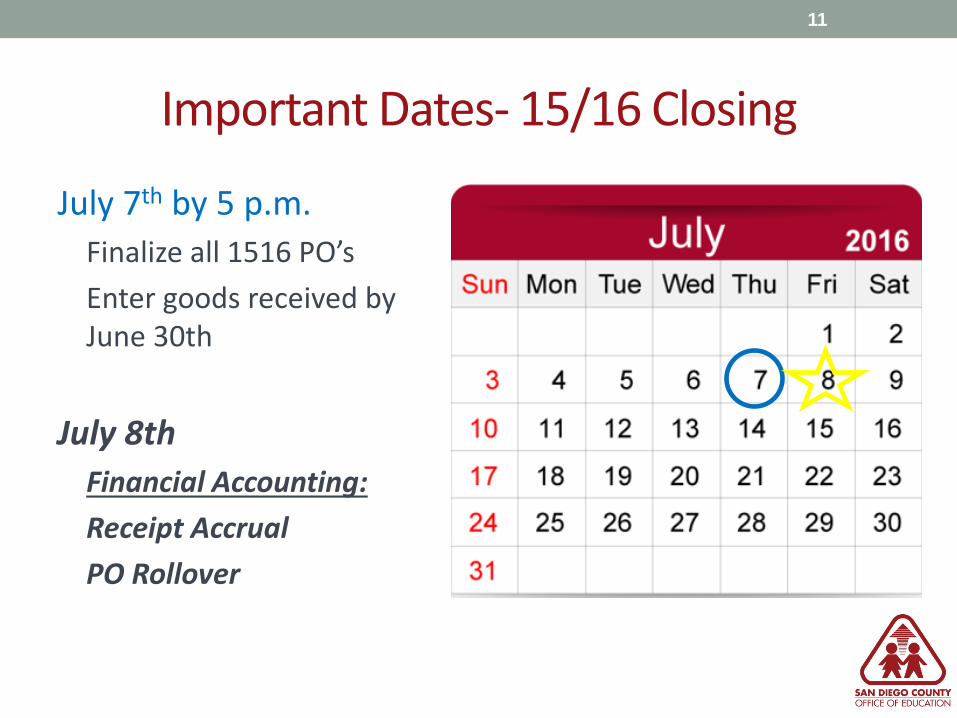

Important Dates- 15/16 Closing

July 7th by 5 p.m.Finalize all 1516 PO’sEnter goods received by June 30th

July 8thFinancial Accounting:Receipt AccrualPO Rollover

11

Important Dates- 16/17 ProcessingJuly 1st

New FY activity beginsNo need to wait 3 days!

July 6thFirst day commercial warrants are issued forFY 16/17

July 15th

Period 12 closes at 5 p.m.

12

NEWIn

PeopleSoft!

Customer Resource Center (CRC )Training

13

• Support Sessions for Year End Closing• Purchasing• Inventory• Finance• Open Labs

• CRC Website• http://crc.sdcoe.net/calendar/yearendclosing

SECTION 3Checklists

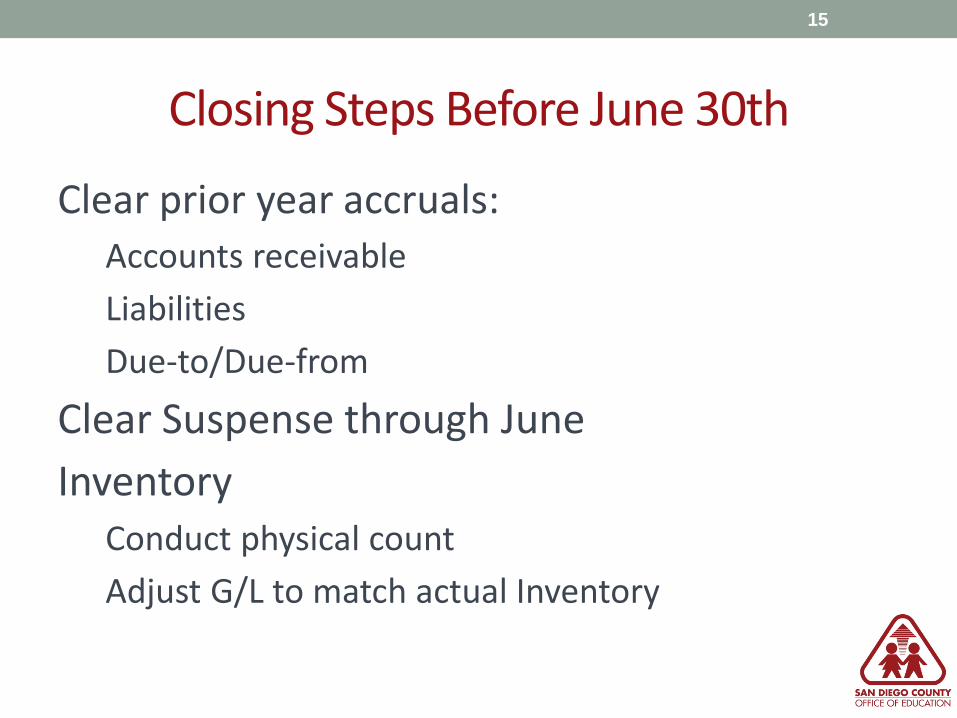

Closing Steps Before June 30th

Clear prior year accruals:Accounts receivable LiabilitiesDue-to/Due-from

Clear Suspense through JuneInventory

Conduct physical countAdjust G/L to match actual Inventory

15

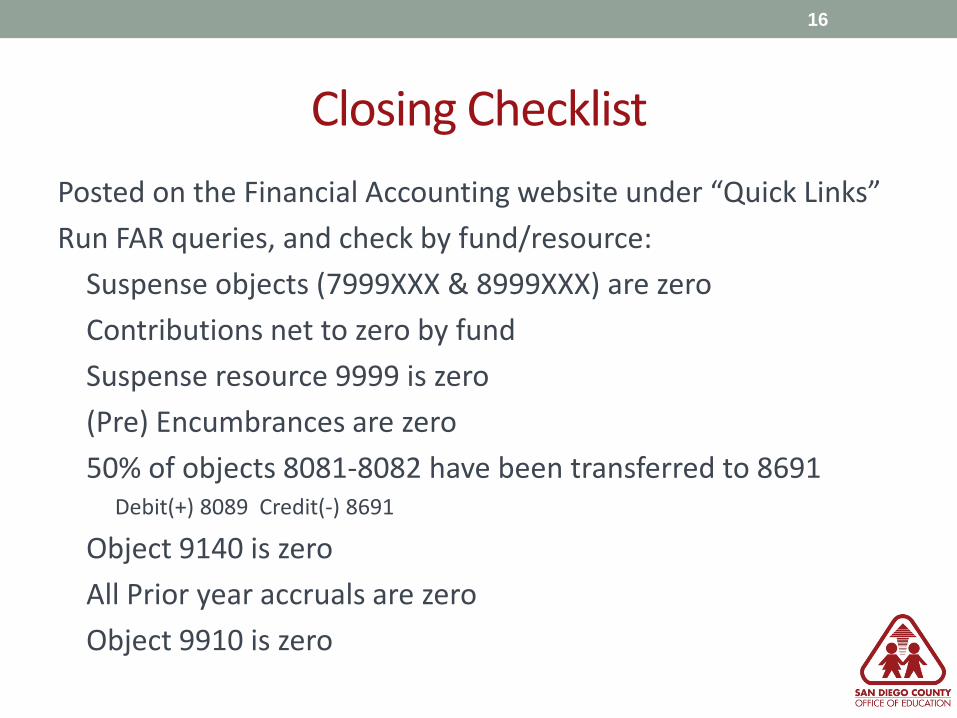

Closing ChecklistPosted on the Financial Accounting website under “Quick Links”Run FAR queries, and check by fund/resource:

Suspense objects (7999XXX & 8999XXX) are zeroContributions net to zero by fundSuspense resource 9999 is zero(Pre) Encumbrances are zero50% of objects 8081-8082 have been transferred to 8691

Debit(+) 8089 Credit(-) 8691

Object 9140 is zeroAll Prior year accruals are zeroObject 9910 is zero

16

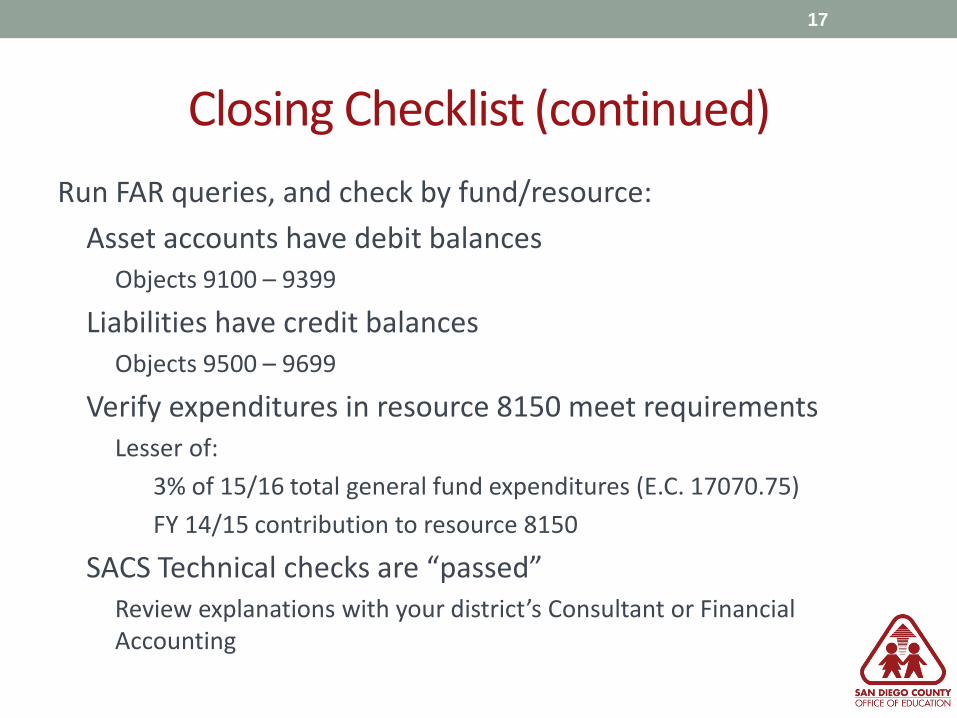

Closing Checklist (continued)Run FAR queries, and check by fund/resource:

Asset accounts have debit balancesObjects 9100 – 9399

Liabilities have credit balancesObjects 9500 – 9699

Verify expenditures in resource 8150 meet requirementsLesser of:

3% of 15/16 total general fund expenditures (E.C. 17070.75)FY 14/15 contribution to resource 8150

SACS Technical checks are “passed”Review explanations with your district’s Consultant or Financial Accounting

17

SECTION 4Closing Entries & Accruals

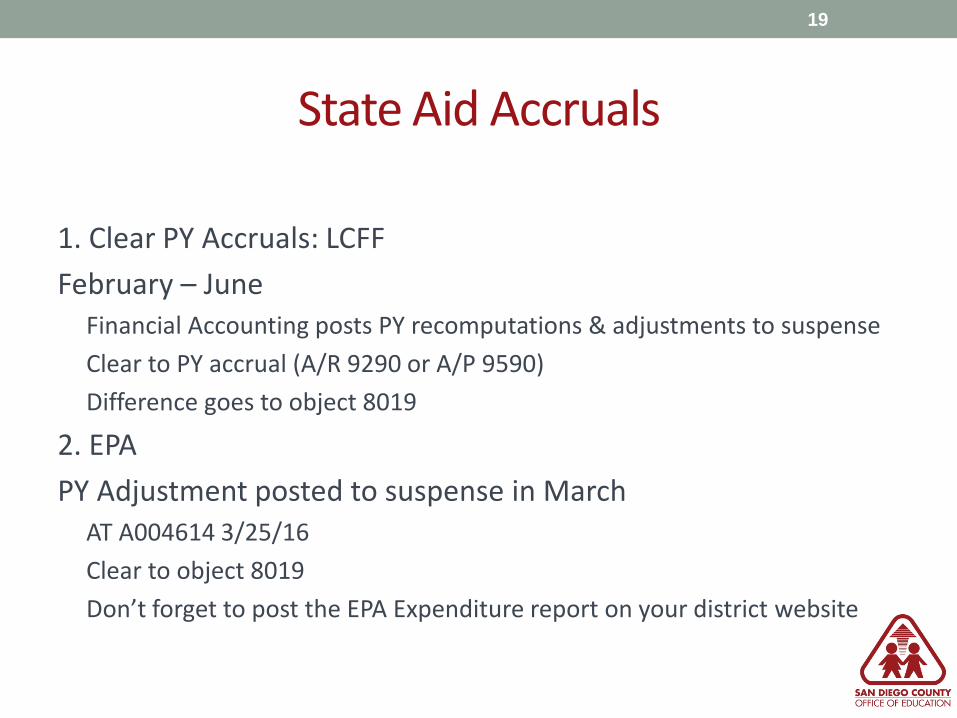

State Aid Accruals

1. Clear PY Accruals: LCFFFebruary – June

Financial Accounting posts PY recomputations & adjustments to suspenseClear to PY accrual (A/R 9290 or A/P 9590)Difference goes to object 8019

2. EPAPY Adjustment posted to suspense in March

AT A004614 3/25/16Clear to object 8019Don’t forget to post the EPA Expenditure report on your district website

19

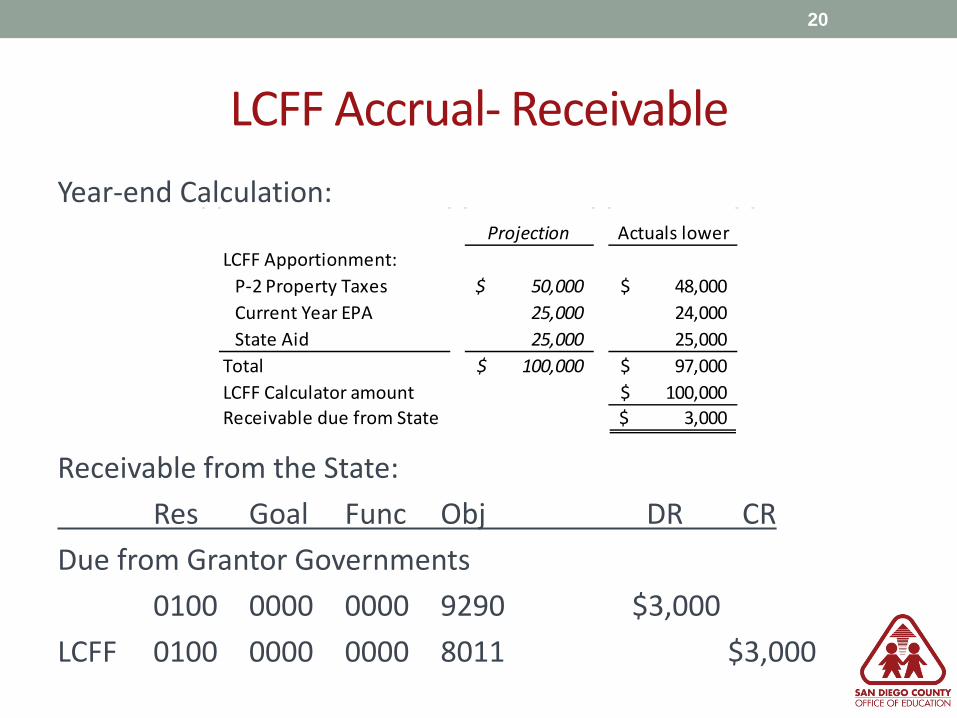

LCFF Accrual- ReceivableYear-end Calculation:

Receivable from the State:Res Goal Func Obj DR CR

Due from Grantor Governments0100 0000 0000 9290 $3,000

LCFF 0100 0000 0000 8011 $3,000

20

Projection Actuals lowerLCFF Apportionment:

P-2 Property Taxes 50,000$ 48,000$ Current Year EPA 25,000 24,000 State Aid 25,000 25,000

Total 100,000$ 97,000$ LCFF Calculator amount 100,000$ Receivable due from State 3,000$

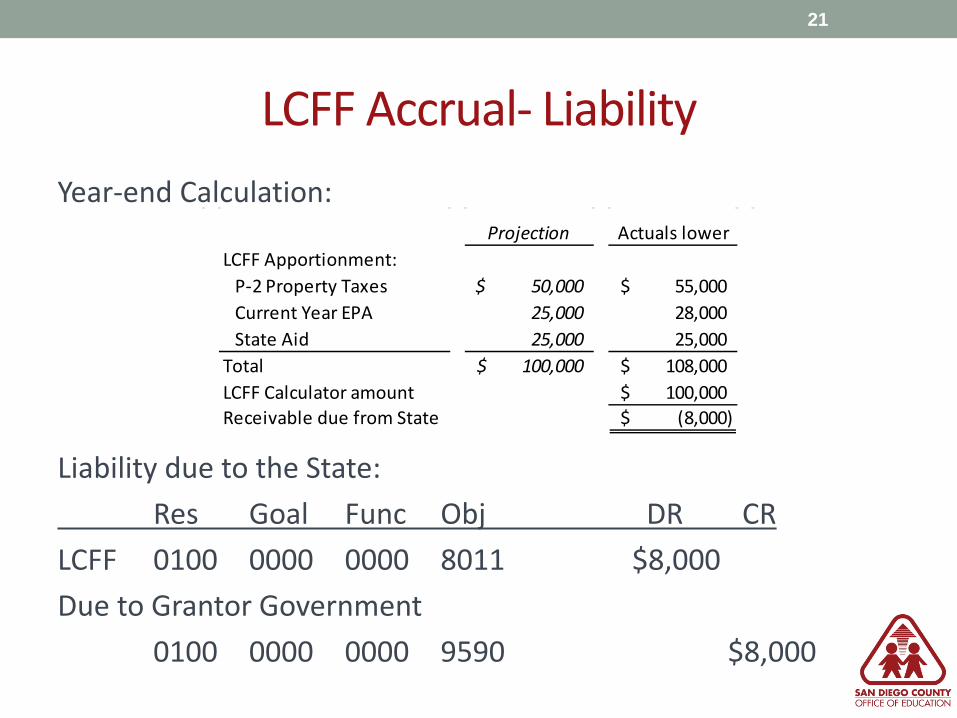

LCFF Accrual- LiabilityYear-end Calculation:

Liability due to the State:Res Goal Func Obj DR CR

LCFF 0100 0000 0000 8011 $8,000Due to Grantor Government

0100 0000 0000 9590 $8,000

21

Projection Actuals lowerLCFF Apportionment:

P-2 Property Taxes 50,000$ 55,000$ Current Year EPA 25,000 28,000 State Aid 25,000 25,000

Total 100,000$ 108,000$ LCFF Calculator amount 100,000$ Receivable due from State (8,000)$

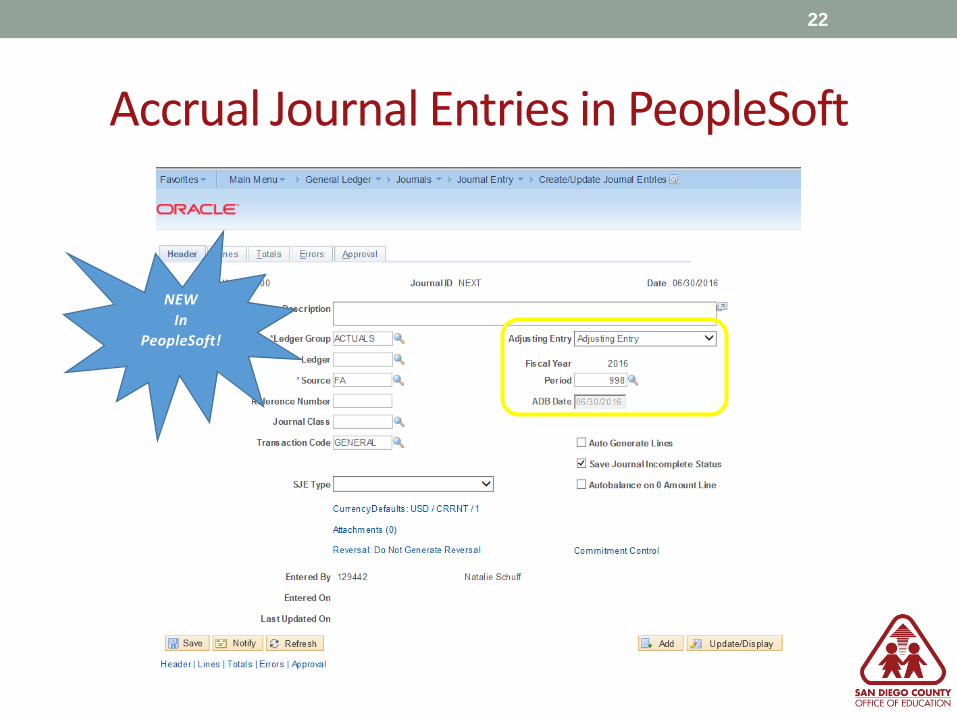

Accrual Journal Entries in PeopleSoft

22

NEWIn

PeopleSoft!

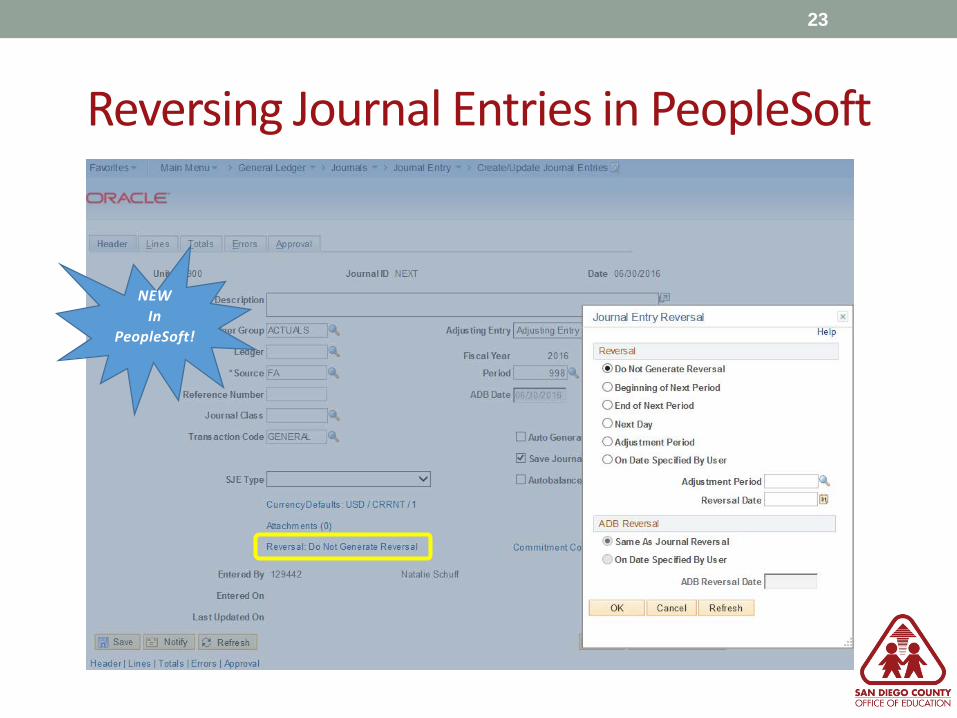

Reversing Journal Entries in PeopleSoft

23

NEWIn

PeopleSoft!

Payroll Accruals

24

• Districts will enter payroll data in July, as usual• Any FY 1516 time entered (ie. June hourly, overtime, adjustments, etc.)

• July payroll runs, as usual• All time worked prior to July will be posted to June as an

accrual• This entry will automatically reverse in July• July payroll processing will clear the negative expenditures

posted as part of the reversal

NEWIn

PeopleSoft!

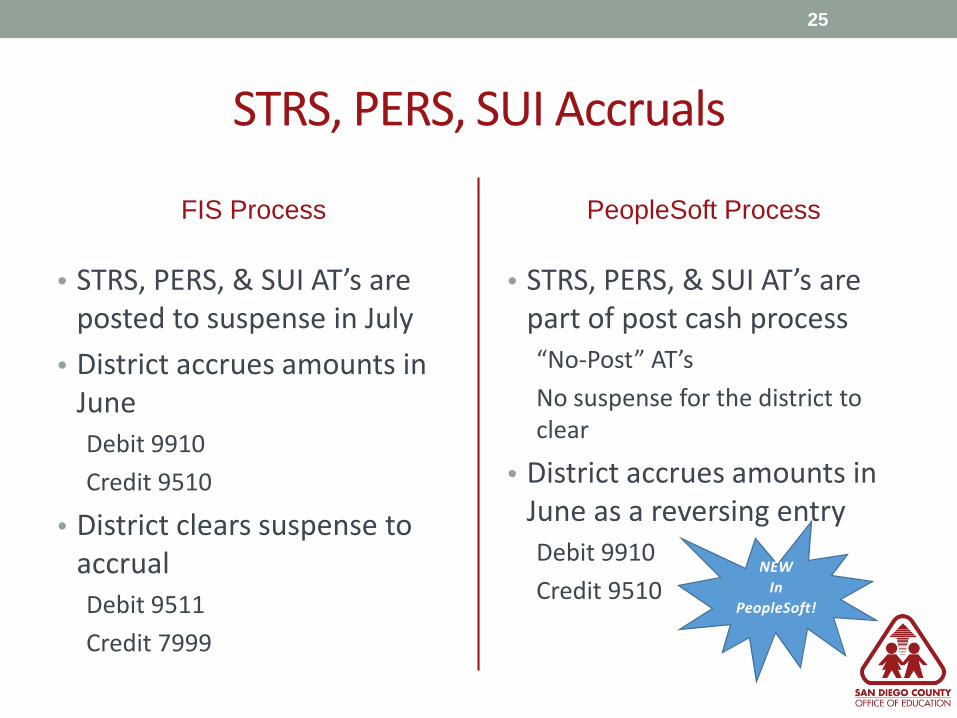

STRS, PERS, SUI Accruals

FIS Process

• STRS, PERS, & SUI AT’s are posted to suspense in July

• District accrues amounts in June Debit 9910Credit 9510

• District clears suspense to accrualDebit 9511Credit 7999

PeopleSoft Process

• STRS, PERS, & SUI AT’s are part of post cash process“No-Post” AT’sNo suspense for the district to clear

• District accrues amounts in June as a reversing entryDebit 9910Credit 9510

25

NEWIn

PeopleSoft!

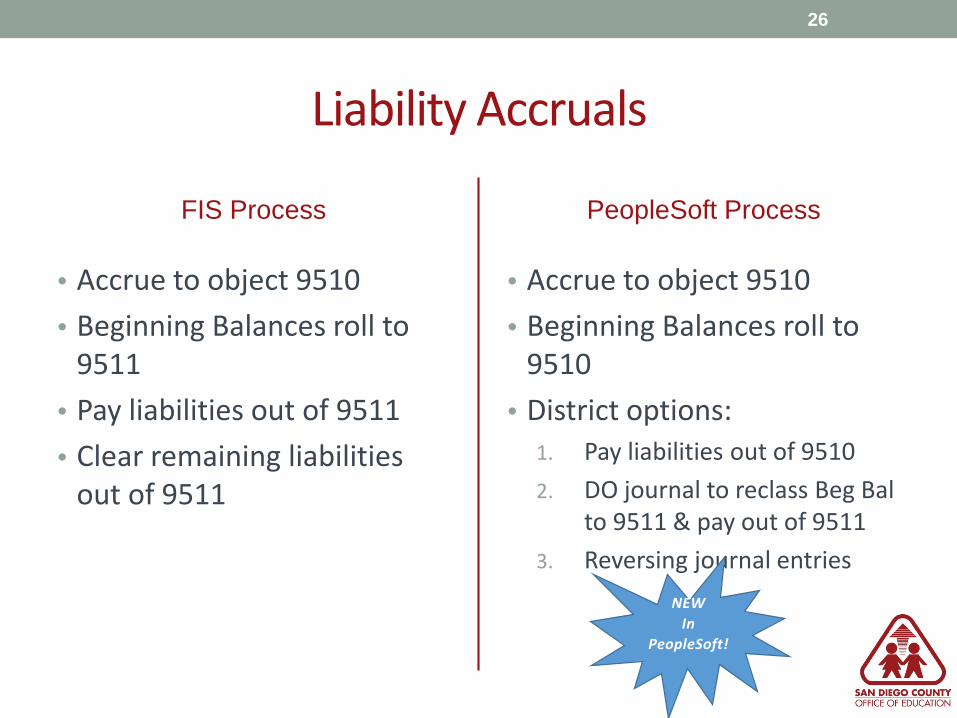

Liability Accruals

FIS Process

• Accrue to object 9510• Beginning Balances roll to

9511• Pay liabilities out of 9511• Clear remaining liabilities

out of 9511

PeopleSoft Process

• Accrue to object 9510• Beginning Balances roll to

9510• District options:

1. Pay liabilities out of 95102. DO journal to reclass Beg Bal

to 9511 & pay out of 95113. Reversing journal entries

26

NEWIn

PeopleSoft!

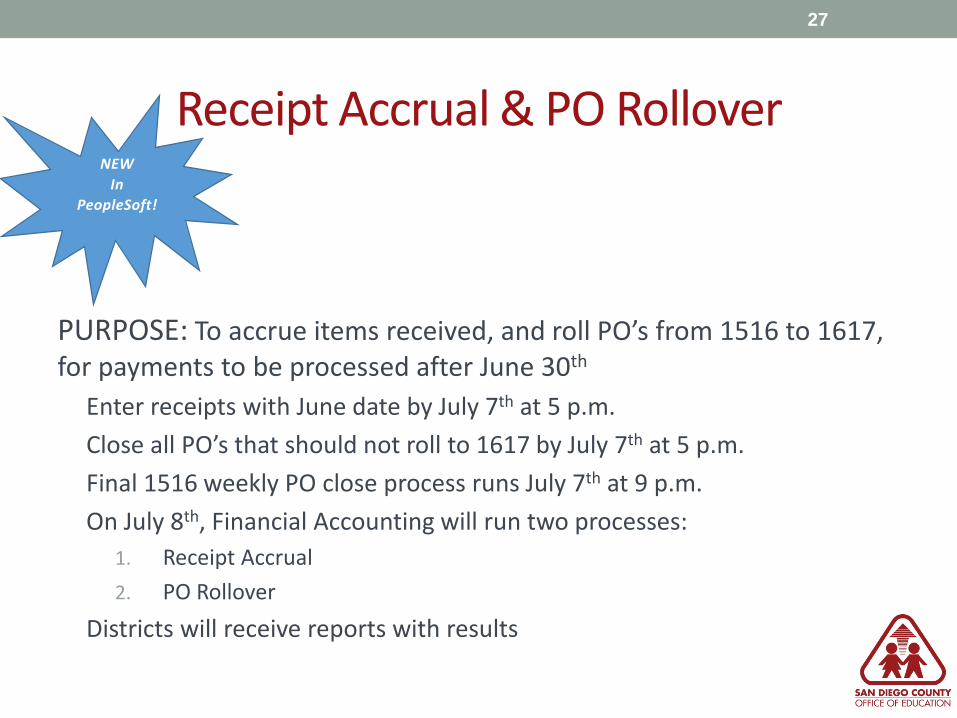

Receipt Accrual & PO Rollover

27

PURPOSE: To accrue items received, and roll PO’s from 1516 to 1617, for payments to be processed after June 30th

Enter receipts with June date by July 7th at 5 p.m.Close all PO’s that should not roll to 1617 by July 7th at 5 p.m.Final 1516 weekly PO close process runs July 7th at 9 p.m.On July 8th, Financial Accounting will run two processes:

1. Receipt Accrual2. PO Rollover

Districts will receive reports with results

NEWIn

PeopleSoft!

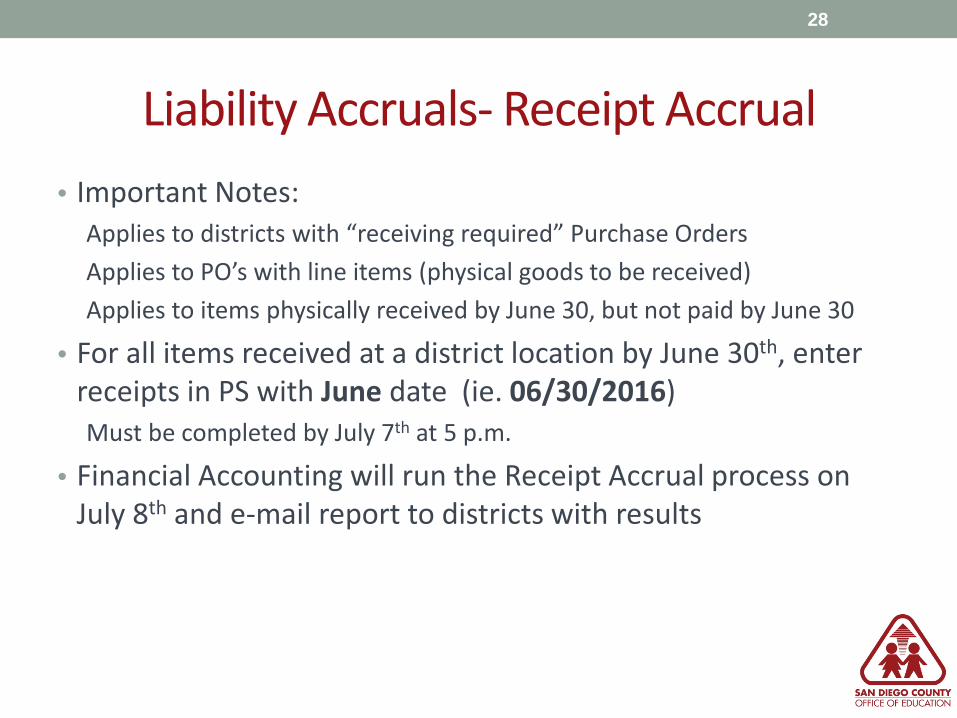

Liability Accruals- Receipt Accrual

28

• Important Notes:Applies to districts with “receiving required” Purchase OrdersApplies to PO’s with line items (physical goods to be received)Applies to items physically received by June 30, but not paid by June 30

• For all items received at a district location by June 30th, enter receipts in PS with June date (ie. 06/30/2016)Must be completed by July 7th at 5 p.m.

• Financial Accounting will run the Receipt Accrual process on July 8th and e-mail report to districts with results

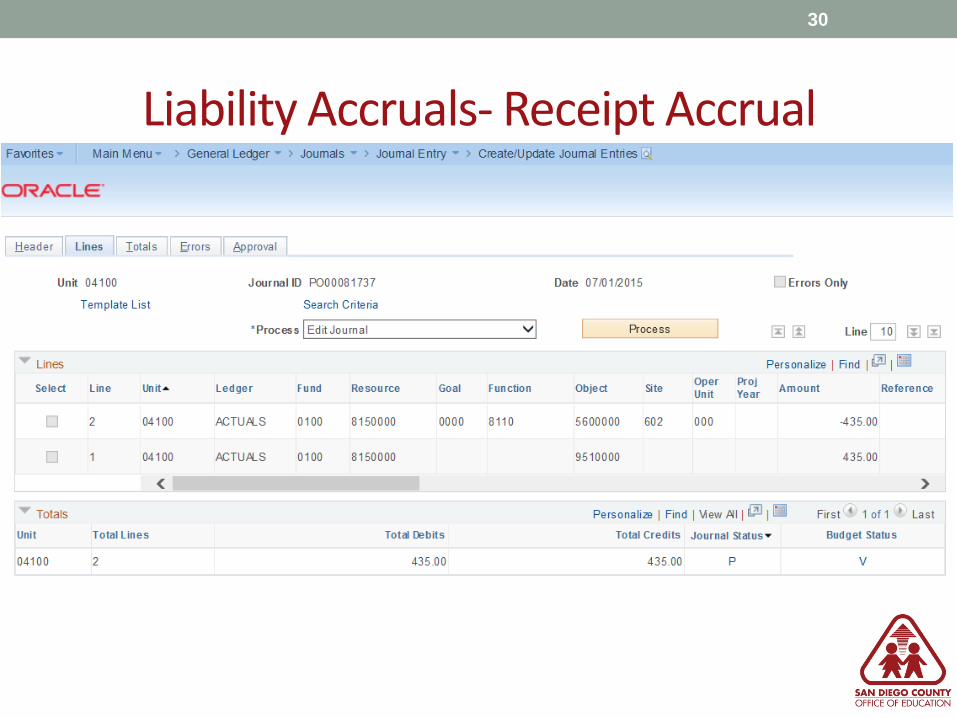

Liability Accruals- Receipt Accrual

29

Liability Accruals- Receipt Accrual

30

Liability Accruals- PO Rollover

31

• Important Notes:Applies to PO’s in Approved or Dispatched status

• Process identifies all PO’s ready to roll• Closes encumbrances in PY• Closes PO’s in PY• Opens encumbrances in CY

Requires valid budget (chartstring) to be set up in new fiscal year

• Opens PO’s in CYPayments can now be applied in new fiscal year

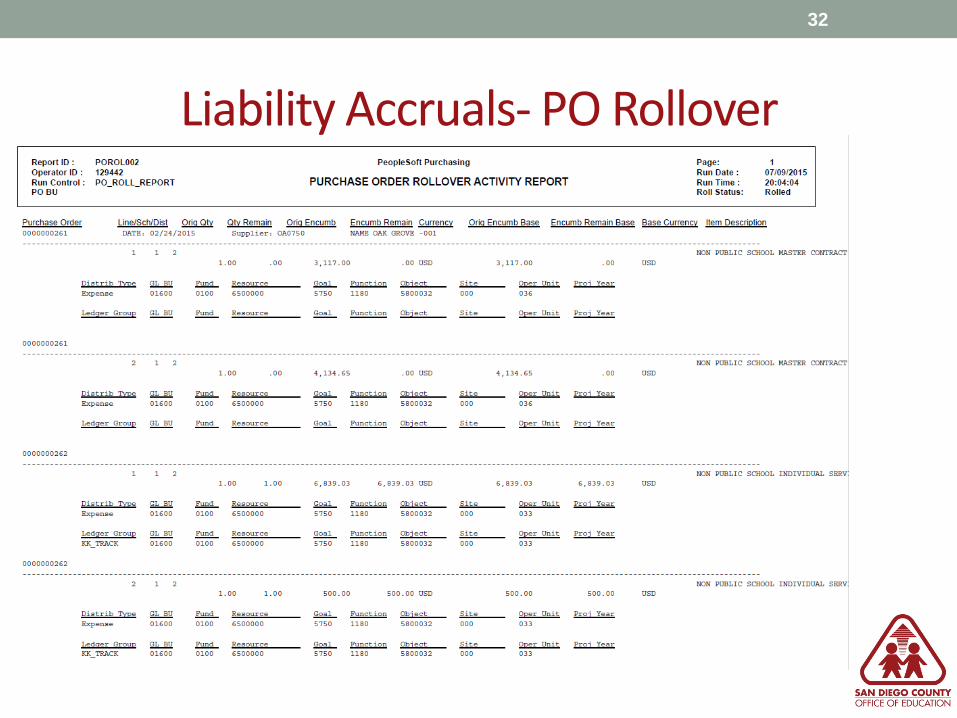

Liability Accruals- PO Rollover

32

SECTION 5Indirect Costs

Indirect Costs

34

• Definition: General management costs consist of administrative activities necessary for the general operation of the agency, such as accounting, budgeting, payroll preparation, personnel services, purchasing, and centralized data processing

• Indirect Cost Rate (ICR): percentage of an organization’s indirect costs to its direct costs and is a standardized method of charging individual programs for their share of indirect costs

• Purpose: standardized, efficient way to recover a share of general management costs from individual (restricted) programs

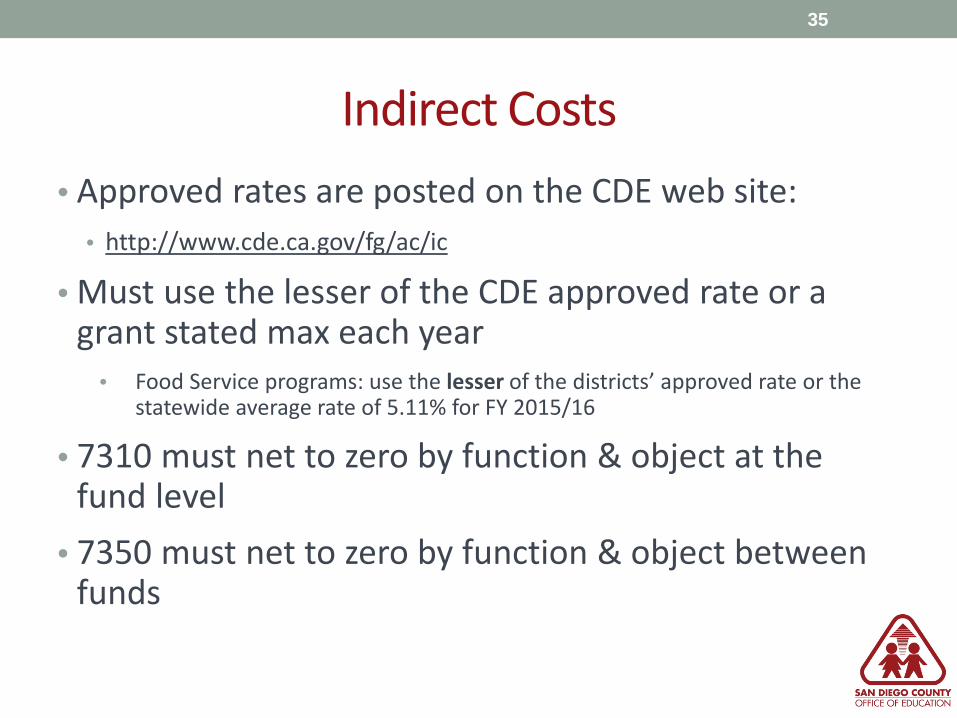

Indirect Costs

35

• Approved rates are posted on the CDE web site:• http://www.cde.ca.gov/fg/ac/ic

• Must use the lesser of the CDE approved rate or a grant stated max each year

• Food Service programs: use the lesser of the districts’ approved rate or the statewide average rate of 5.11% for FY 2015/16

• 7310 must net to zero by function & object at the fund level

• 7350 must net to zero by function & object between funds

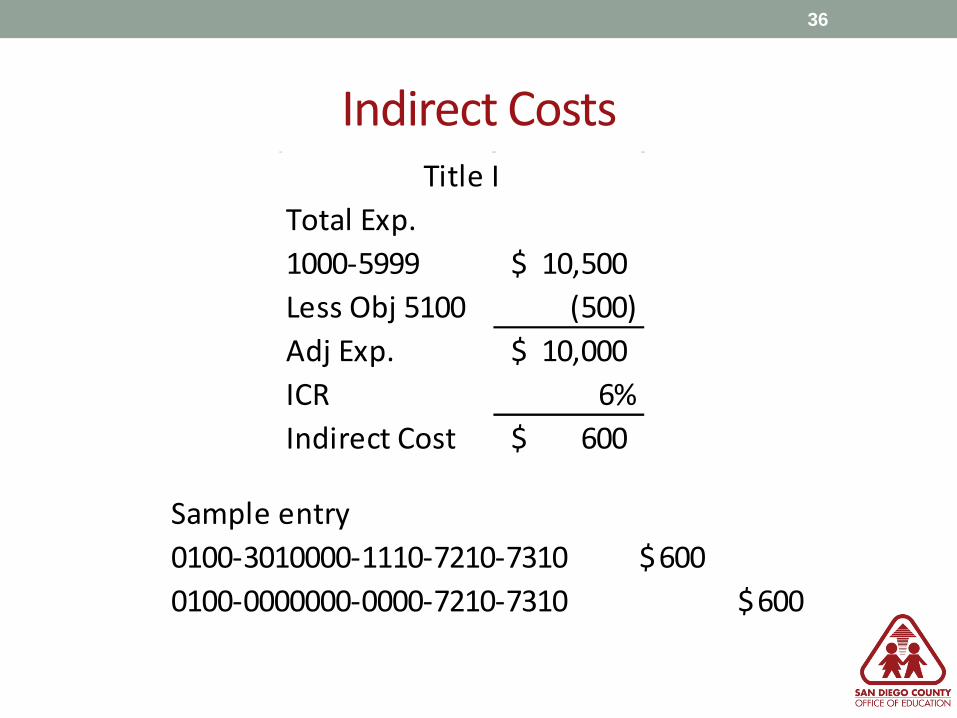

Indirect Costs

36

Total Exp.1000-5999 10,500$ Less Obj 5100 (500) Adj Exp. 10,000$ ICR 6%Indirect Cost 600$

Title I

Sample entry0100-3010000-1110-7210-7310 600$ 0100-0000000-0000-7210-7310 600$

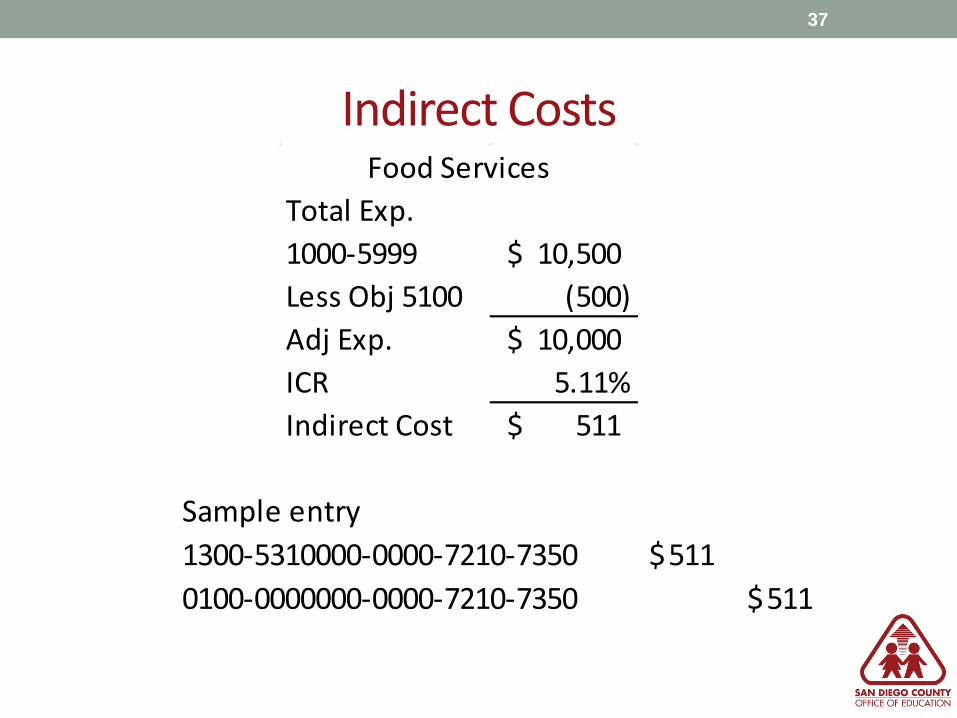

Indirect Costs

37

Total Exp.1000-5999 10,500$ Less Obj 5100 (500) Adj Exp. 10,000$ ICR 5.11%Indirect Cost 511$

Food Services

Sample entry1300-5310000-0000-7210-7350 511$ 0100-0000000-0000-7210-7350 511$

SECTION 6Accounting Updates

Prop 39 Energy Fund

39

• Resource 6230: California Clean Energy Jobs Act• Funding based on approved expenditure plan

• Districts have been encouraged to complete construction, some times ahead of receipt of funds

• Funding has not been appropriated in the State budget beyond the current year• Does not qualify as Accounts Receivable

• CDE recommends leaving the resource with a negative ending balance at FYE if district has expenditures, but not revenue• Contributions are considered one-way transfer of funds, so this is also

not a recommended solution

E-Rate Accounting

40

• New guidance in 2016 edition of CSAM• See Procedure 560 & November 2015 SACS Forum meeting

minutes for further information• LEA’s should now report costs of telecommunications goods &

services at gross• E-Rate subsidy is local revenue

• Fund 01, Unrestricted Resource, Object 8699

• Federal Programs exception• Only NET expenditure should be charged to the Federal resource• Remaining expenditure and corresponding E-Rate subsidy should be

recorded in General Fund unrestricted

GASB 68

41

• STRS On-Behalf Journal Entry• Required entry in the District’s books before closing• Resource 7690 will be valid in all funds with the SACS2016ALL

software• CDE created Excel template to create journal entry• 1516 STRS on-behalf rate: 7.125890%• To calculate the district’s STRS on-behalf amount, multiply

2013/14 STRS creditable compensation by the 1516 rate of 7.125890%, and round to the nearest dollar

• Find the STRS reports on SDCOE’s Retirement Reporting website: http://www.sdcoe.net/business-services/financial-services/retirement-reporting/Pages/retirement-reporting.aspx

42

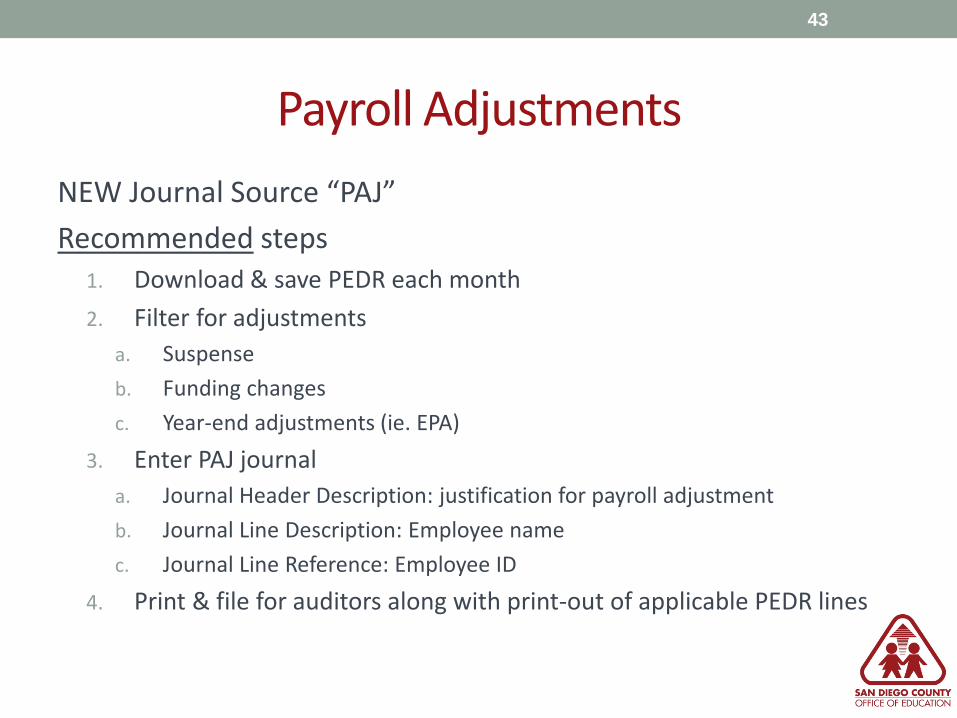

Payroll Adjustments

43

NEW Journal Source “PAJ”Recommended steps

1. Download & save PEDR each month2. Filter for adjustments

a. Suspenseb. Funding changesc. Year-end adjustments (ie. EPA)

3. Enter PAJ journala. Journal Header Description: justification for payroll adjustmentb. Journal Line Description: Employee namec. Journal Line Reference: Employee ID

4. Print & file for auditors along with print-out of applicable PEDR lines

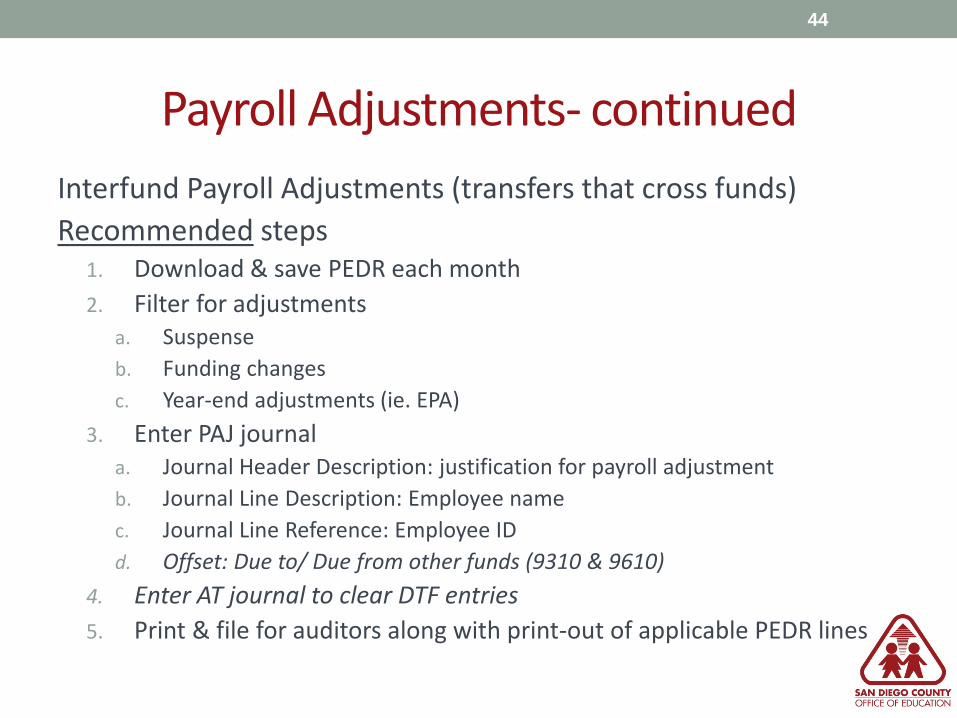

Payroll Adjustments- continued

44

Interfund Payroll Adjustments (transfers that cross funds)Recommended steps

1. Download & save PEDR each month2. Filter for adjustments

a. Suspenseb. Funding changesc. Year-end adjustments (ie. EPA)

3. Enter PAJ journala. Journal Header Description: justification for payroll adjustmentb. Journal Line Description: Employee namec. Journal Line Reference: Employee IDd. Offset: Due to/ Due from other funds (9310 & 9610)

4. Enter AT journal to clear DTF entries5. Print & file for auditors along with print-out of applicable PEDR lines