2015 3q colliers asia pacific office market

TRANSCRIPT

Economic Overview After a series of easing monetary policy moves, the slowdown in China’s economy seems to be starting to stabilize in the first half of 2015. However, downside risks such as the heightened volatility in the stock markets, strong capital outflows and overcapacity in some sectors have put pressure on the economic growth, derailing authorities’ efforts to rebalance the Chinese economy towards consumption and services. As a consequence, the World Banks has trimmed China’s growth forecast to 6.9% this year, below the government’s target of 7%. Meanwhile, in the US, the Federal Reserve had decided not to raise its key interest rate at its October meeting. This decision has been seen as to ease pressure on financial markets across emerging markets on the short term, but at the same time, it has been prolonging uncertainty regarding the timing of the Fed’s first rate hike.

Leasing Market Hiring environment turned slightly more conservative than the first half of this year with the majority of employers in China, Hong Kong and Singapore intending to keep headcount steady in the second half of 2015. According to the latest Hudson report, technology and IT sectors continues to be the most active tenant sector in the region. Other notable sectors include professional services and manufacturing while financial corporates are also expanding selectively with most multinational corporates still cautious. Of the major markets, Hong Kong achieved the strongest quarter-on-quarter (QoQ) growth of 3.9% supported by demand from mainland Chinese financial firms for office premises in Central. This is being followed by Bangkok (2.2% QoQ) and Bengaluru (1.8% QoQ). Rents fell by in Yangon (-2.5% QoQ), Chengdu (-2.2% QoQ) and Shenzhen (-2.0% QoQ) as landlords started lowering rents in view of the large impending supply. Grade A office completions are expected to grow around 100 million sq ft in 2016, with around 70% of the total in China and India.

Sales Market Despite the slower economic growth in China, office real estate investment in Asia came in at US$4.4 billion in 3Q 2015, up 54.3% year-on-year (YoY) from US$2.9 billion the same times last year. Sentiment is improving for core assets in China’s first-tier cities with Shanghai most in demand accounting for 51% of transactions including a couple of en-bloc transactions with the focus primarily on office properties. Investors who previously ventured into the secondary and tertiary markets have focused their radar back to Shanghai as the market tends to be the most liquid and transparent in China. In addition the market offer more stock for sale compared to Beijing with more than 600,000 sq m office supply coming on stream in 2015 and another 790 million sq m by the end of 2016. Cross-border investors continue to be very active with outbound investors showing an unwavering preference for Grade A offices in the core business districts of gateway cities, such as New York, London, Sydney and Melbourne.

Market Outlook While remaining the world’s growth leader in terms of economic growth, Asia Pacific is expected to grow slightly less in 2016. According to the International Monetary Fund, growth in the Asia Pacific markets is expected to hold steady at 5.6% for the full year and to ease slightly to 5.5% in 2016. While growth in India picked up being supported by a healthy monsoon and new investments assuming concrete progress on reform, slowing growth in several large economies, including China, Indonesia and Japan was a counterweight. Going forward, domestic demand and ongoing low oil prices should continue to drive growth in the region over the medium term. However, economic dynamics in Asia will mostly be determined by developments in China. At the same time, we may see increased market turbulence before year end should the US Fed decide to finally move on interest rates.

Asia Pacific

Office Market

Asia Pacific | Office

3Q 2015

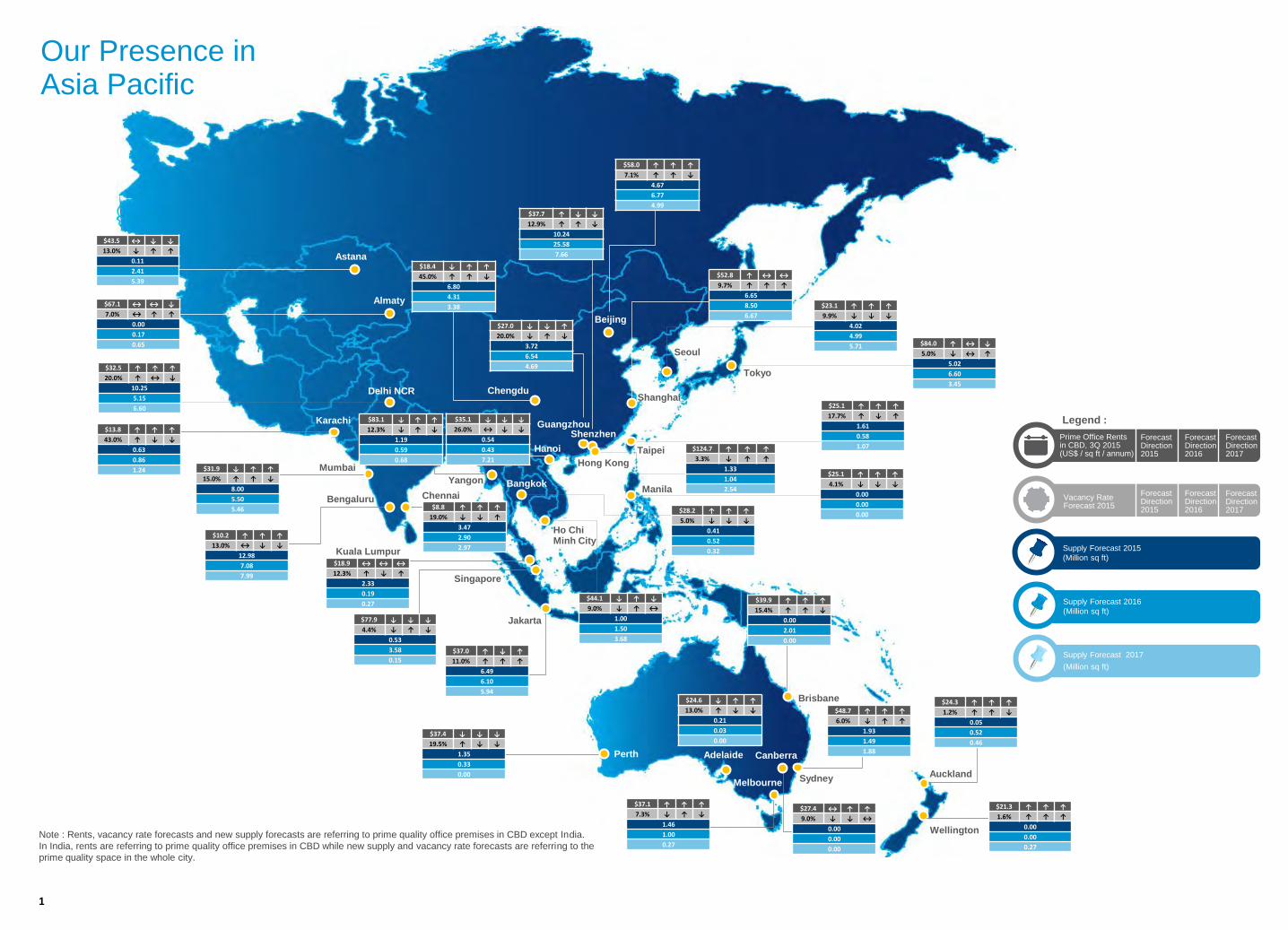

Our Presence in Asia Pacific

1

Mumbai

Bengaluru

Karachi

Kuala Lumpur

Singapore

Ho Chi Minh City

Yangon

Chennai

Wellington

Auckland Sydney

Brisbane

Canberra Perth Adelaide

Melbourne

Almaty

Jakarta

Delhi NCR

Manila

Taipei

Tokyo

Seoul

Beijing

Hong Kong

Shanghai Chengdu

Hanoi

Bangkok

Note : Rents, vacancy rate forecasts and new supply forecasts are referring to prime quality office premises in CBD except India.

In India, rents are referring to prime quality office premises in CBD while new supply and vacancy rate forecasts are referring to the

prime quality space in the whole city.

Supply Forecast 2015

(Million sq ft)

Legend :

Supply Forecast 2016

(Million sq ft)

Prime Office Rents in CBD, 3Q 2015 (US$ / sq ft / annum)

Forecast Direction 2015

Vacancy Rate Forecast 2015

Forecast Direction 2015

Forecast Direction 2016

Forecast Direction 2016

Astana

Supply Forecast 2017

(Million sq ft)

$67.1 ↔ ↔ ↓

7.0% ↔ ↑ ↑

0.00

0.17

0.65

$13.8 ↑ ↑ ↑

43.0% ↑ ↓ ↓

0.63

0.86

1.24 $31.9 ↓ ↑ ↑

15.0% ↑ ↑ ↓

8.00

5.50

5.46

$10.2 ↑ ↑ ↑

13.0% ↔ ↓ ↓

12.98

7.08

7.99

$8.8 ↑ ↑ ↑

19.0% ↓ ↓ ↑

3.47

2.90

2.97

$77.9 ↓ ↓ ↓

4.4% ↓ ↑ ↓

0.53

3.58

0.15

$37.0 ↑ ↓ ↑

11.0% ↑ ↑ ↑

6.49

6.10

5.94

$58.0 ↑ ↑ ↑

7.1% ↑ ↑ ↓

4.67

6.77

4.99

$27.0 ↓ ↓ ↑

20.0% ↓ ↑ ↓

3.72

6.54

4.69

$18.4 ↓ ↑ ↑

45.0% ↑ ↑ ↓

6.80

4.31

3.38

$52.8 ↑ ↔ ↔

9.7% ↑ ↑ ↑

6.65

8.50

6.67

$23.1 ↑ ↑ ↑

9.9% ↓ ↓ ↓

4.02

4.99

5.71 $84.0 ↑ ↔ ↓

5.0% ↓ ↔ ↑

5.02

6.60

3.45

$25.1 ↑ ↑ ↑

17.7% ↑ ↓ ↑

1.61

0.58

1.07

$28.2 ↑ ↑ ↑

5.0% ↓ ↓ ↓

0.41

0.52

0.32

$39.9 ↑ ↑ ↑

15.4% ↑ ↑ ↓

0.00

2.01

0.00

$37.4 ↓ ↓ ↓

19.5% ↑ ↓ ↓

1.35

0.33

0.00

$37.1 ↑ ↑ ↑

7.3% ↓ ↑ ↓

1.46

1.00

0.27

$24.3 ↑ ↑ ↑

1.2% ↑ ↑ ↓

0.05

0.52

0.46

$48.7 ↑ ↑ ↑

6.0% ↓ ↑ ↑

1.93

1.49

1.88

$24.6 ↓ ↑ ↑

13.0% ↑ ↓ ↓

0.21

0.03

0.00

$18.9 ↔ ↔ ↔

12.3% ↑ ↓ ↑

2.33

0.19

0.27

Forecast Direction 2017

Forecast Direction 2017

$27.4 ↔ ↑ ↑

9.0% ↓ ↓ ↔

0.00

0.00

0.00

$83.1 ↓ ↑ ↑

12.3% ↓ ↑ ↓

1.19

0.59

0.68

$25.1 ↑ ↑ ↑

4.1% ↓ ↓ ↓

0.00

0.00

0.00

Guangzhou Shenzhen

$37.7 ↑ ↓ ↓

12.9% ↑ ↑ ↓

10.24

25.58

7.66

$124.7 ↑ ↑ ↑

3.3% ↓ ↑ ↑

1.33

1.04

2.54

$21.3 ↑ ↑ ↑

1.6% ↑ ↑ ↑

0.00

0.00

0.27

$35.1 ↓ ↓ ↓

26.0% ↔ ↓ ↓

0.54

0.43

7.21

$44.1 ↓ ↑ ↓

9.0% ↓ ↑ ↔

1.00

1.50

3.68

$32.5 ↑ ↑ ↑

20.0% ↑ ↔ ↓

10.25

5.15

6.60

$43.5 ↔ ↓ ↓

13.0% ↓ ↑ ↑

0.11

2.41

5.39

Copyright © 2015 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to

ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult

their professional advisors prior to acting on any of the material contained in this report.

$2.3 billion in

annual revenue

502 offices in 67 countries on 6 continents

United States:

Canada:

Latin America:

Asia:

ANZ:

EMEA:

Authors:

Simon Lo

Executive Director | Asia

+852 2822 0511

Jessy Chung

Assistant Manager

+852 2822 0643

140

31

24

39

160

108

$1.70 billion square feet

under management

16,300 Professional

and staff

ASIA

Sam Harvey-Jones

+852 2822 0509

NORTH ASIA

Mainland China

Beijing

Kelvin Chow

+86 10 8518 1633 ext.113

Shanghai

Michael Wu

+86 21 6141 3638

Guangzhou

Eric Lam

+86 20 3819 3988

Shenzhen

Ken Kan

+86 755 8825 8648

Chengdu

Bonnie Chiu

+86 28 8658 6288 ext.810

Hong Kong, HKSAR

Hong Kong

Wendy Lau

+852 2822 0550

(E-141423)

Kowloon

Fiona Ngan

+852 2117 3301

(E-197789)

Japan

Tokyo

Katsuji Tokita

+81 3 5563 2117

South Korea

Seoul

Jay Yun

+82 2 3775 7351

Taiwan

Taipei

Amanda Yang

+886 2 8101 1120

SOUTH EAST ASIA

Indonesia

Jakarta

Bagus Adikusumo

+62 21 521 1400 ext.506

Malaysia

Sam Harvey-Jones

+852 2822 0509

*Based in Hong Kong

Kuala Lumpur

Research data provided by

C H Williams Talhar & Wong

Sdn Bhd

URL : http://www.wtw.com.my

Foo Gee Jen

+603 2616 8888

Philippines

Manila

Jie Espinosa

+632 888 9988 ext.4016

Singapore

Singapore

Calvin Yeo

+65 6531 8671

Thailand

Bangkok

Nattawan Radomyos

+66 2 656 7000

Vietnam

Ho Chi Minh City

Nhung Quan

+84 8 3827 5665

Hanoi

Tri Nhan Nguyen

+84 8 3827 5665

Myanmar

Yangon

Tony Picon

+95 931 491 678

SOUTH ASIA

India

George McKay

+91 22 4050 4553

Vikas Kalia

+91 12 4456 7531

Bengaluru

Goutam Chakraborty

+91 80 4079 5500

Chennai

Shaju Thomas

+91 44 2836 1064

Gurgaon

Vikas Kalia

+91 12 4456 7531

Kolkata

Swapan Dutta

+91 12 4437 5807

Mumbai

Nishith Agarwal

+91 22 4050 4556

New Delhi

Vikas Kalia

+91 12 4456 7531

Pune

Rishav Vij

+91 20 4120 6438

Pakistan

Karachi

S. Fazal Ahmad

+92 21 3561 2550 2

Lahore, Faisalabad

Naveed Khan

+92 42 3662 3312 8 (Lahore)

+92 41 2540 501 4 (Faisalabad)

Kazakhstan

Almaty

Bayan Kuatova

+7 727 311 54 43

AUSTRALIA

Melbourne

Simon Hunt

+61 3 9612 8818

NEW ZEALAND

Auckland

Rob Bird

+64 9 356 8803

Wellington

Jim Pinson

+64 4 470 3917

For further details, please contact: