2015 3q colliers asia: asia market snapshots

TRANSCRIPT

ASIA CApItAl MArketS AND INveStMeNt ServICeS

Asia Market Snapshot Q3 2015

2 | ASIA MArket SNApShot

FEARS of a hard landing for the Chinese economy, reinforced by poor economic trade figures as well as an unexpected depreciation of the yuan, hit global equities market in August 2015. Stock exchanges from Sydney, Tokyo, London to New York endured heart-stopping plunges, with investors heading for the exit in droves.

Despite the nerve-wrecking volatility in the equities market, real estate transaction volumes in key Asian cities remained resilient in 3Q 2015. For the quarter alone, there were 8 significant deals done in Shanghai, Beijing and Chengdu, of which Shanghai accounted for six of these en-bloc transactions with the focus primarily on office properties.

Similarly, most of the en-bloc buildings changing hands in Hong Kong were office buildings. Among these, the transaction of Wincome Centre which represents a unit price of HK$33,000 (US$4,250) per square foot, had set a new record high unit price for an en-bloc office deal in Hong Kong.

Singapore saw its first successful collective sale this year. The Thong Sia Building near Orchard Road had conditionally been sold for US$269 million or US$1,719 per square foot over the existing gross floor area. This property could be redeveloped into a mixed-use development with at least 60% for residential or serviced apartments, and the rest commercial space.

In this issue of our Asia Market Snapshot, we provide information on the latest trends, along with advice from my colleagues in Asian markets to help you make more informed investment decisions.

We note several other notable key trends across Asia :

• The buoyant office sector in China and Hong Kong is expected to persist, as investors continue to chase quality office properties.

• Sustained levels of global liquidity from previous quantitative easing measures will support investor demand and Asian real estate prices.

• Outbound Asian investors continue to show an unwavering preference for Grade A offices in the core business districts of gateway cities such as New York, London, Sydney and Melbourne.

Introduction

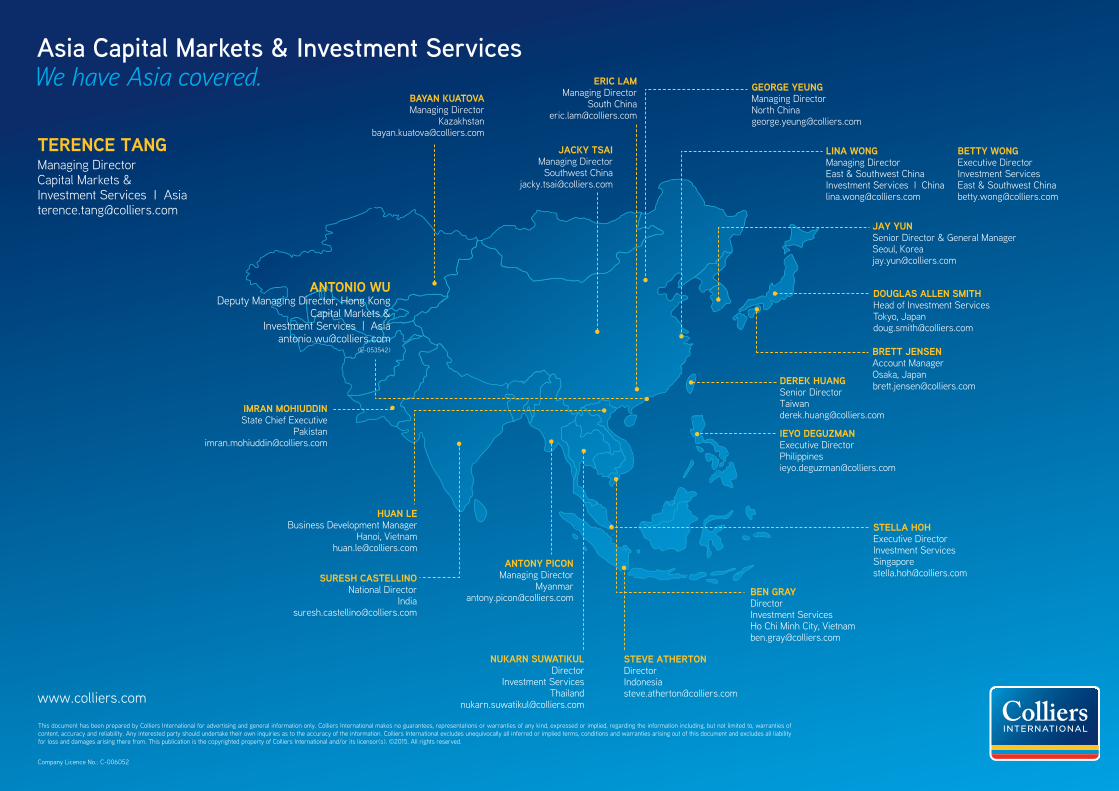

Terence TangManaging DirectorCapital Markets & Investment Services I Asia

ASIA MArket SNApShot | 3

Betty Wong

Buoyed by strong office-transaction activity, Shanghai’s overall investment market remained active in Q3 2015. The quarter saw the conclusion of six en-bloc transactions, including four en-bloc office deals. The office market saw two types of purchasers: real estate investment trusts (REITs), which are looking for income-producing core offices in CBDs to produce long-term income; and owner-occupiers, who are in search of vacant buildings in DBDs for self-use. As a result, two of the four offices that changed hands this quarter (Corporate Avenue 1 & 2 and Hongjia Tower) are in the core CBD, purchased by two well-known REITs, while the other two deals are in DBDs (Guoco Changfeng City and Vanke Center Xuhui T1), purchased in each case by an owner-occupier. The serviced-apartment sector registered one en-bloc transaction, as the central government relaxed its policies towards residential real

George Yeung

There was one en-bloc transaction in Q3 2015. Cinda China purchased the Guoson Centre, which sits in a prime location in Dongzhimen, from GuocoLand China for 10.5 billion yuan (US$1.65 billion). The project is an integrated development complex with a planned gross floor area of 510,000 square meters, comprising a shopping center, apartments, office tower and hotel.

BeijingShanghai

For the foreseeable future, the serviced apartment/residential investment market is

expected to attract attention in light of rising residential sales prices, but the office sector will

continue to be the main investment focus.

Given the limited number of tradable core assets and hardening yields in traditional submarkets, increasing numbers of investors have started looking at opportunities for value-added assets in decentralised areas such as Tongzhou and Shangdi. Beijing’s investment market is expected to remain active for the remainder of 2015.

the Beijing investment market continued to draw interest from investors, with office property remaining the most popular sector, even though overseas investors turned cautious amid increasing concern over the depreciation of the yuan.estate and residential sentiment improved.

Given the limited supply of residential land in Shanghai, many developers look to invest in strata-sale serviced-apartment properties, in an effort to profit from the improving residential market. As opposed to the office and residential sectors, the retail investment sector was relatively calm, resulting from the lack of investable retail assets.

Office

4 | ASIA MArket SNApShot

Antonio Wu/Reeves Yan The Hong Kong investment market saw strong growth in transaction volume for Q3. A number of en-bloc buildings changed hands, most of them office buildings. The major deals include Emperor’s acquisition of Wincome Centre in Central for HK$1.3 billion (US$170 million), Hong Kong Resort’s purchase of Park Building in Cheung Sha Wan for HK$998 million (US$129 million), ITC’s acquisition of Cheuk Nang Plaza in Wan Chai for HK$785 million (US$101 million) as well as the transaction of the L.plaza in Sheung Wan for HK$810 million. (US$105 million) The above en-bloc buildings are trading at initial yields of 2.5% to 3.0%. In terms of price, the transaction of Wincome Centre represents a unit price of HK$33,000 (US$4,250) per square foot, which sets a new record high unit price for an en-bloc office deal in Hong Kong. The activity shows that investors are positive about the office sector and expect a rental hike in the next 12 to 18 months. On the other hand, retail and hotel investment transactions fell dramatically due to the decline in tourism. We expect that situation will continue, so investors will continue to focus on chasing quality office properties.

Hong Kong

Jacky TsaiIn general, Chengdu’s investment market remains slow due to oversupply and China’s economic slowdown. However, there was one significant deal in Q3 that saw Evergrande Group purchase an investment company and three Chengdu projects from Chinese Estates Holdings for a total of HK$6.5 billion (US$840 million).

There is an obvious “Matthew Effect” in the Chengdu real estate market – the sectors that are doing well attract even more interest, while those that are underperforming get ignored. The residential market has picked up in activity since Q2 while the commercial market is still under pressure. Most well-known developers prefer project-transfer opportunities that have a higher residential proportion instead of a large commercial component.

Chengdu

Derek HuangIn Q3 2015, market transactions have been mainly driven by occupational needs. Chinatrust Banking Corporation (CTBC) forward-purchased an industrial office building in Neihu at NT$5.14 billion (US$160 million). At the same time, CTBC spent NT$15 billion (US$460 million) for a 40-year lease on commercial land in the Nangang Economic and Trade Park in Taipei, aiming to ride the potential upside of the rapid development of the area. Prices

Taiwan

Douglas Lin Shenzhen’s major economic indicators rose in the first half of the year, supporting Shenzhen’s office property. Shenzhen’s Grade A office property was an active one in Q2 2015, with a number of new leases in Nanshan and Futian districts, and strong investment demand for a strata-title building in Qianhai.

Shenzhen

The limited availability is expected to lead to an increase in prices, given the strong demand seen in Q2. The en-bloc investment market will remain quiet, with a lack of high-quality, wholly owned buildings offered for sale.

Strata-title sales will continue to dominate the investment market.

in Taipei’s CBD have risen significantly over the past decade, and many tenants in Grade B office buildings have lost their premises as they are converted to hotels or for new development. What new office development there is in the CBD is at the prime end of the market, so tenants and investors have started to consider decentralized locations for offices with cheaper prices and rents. With infrastructure projects such as the high-speed railway sub-hub, the Nangang Exhibition Center and the Taipei Pop Music Center due for completion in the near future, the Nangang area has gradually attracted the attention of many investors as an up-and-coming commercial district in Taipei.

ASIA MArket SNApShot | 5

Stella HohSingapore’s growth had been subdued due to the city-state’s soft exports and ongoing weakness in the housing sector.

The recent changes in public-housing policy are likely to affect the sales of private condominiums. This is worrisome for developers who have already seen sales of private condominiums plunge almost 21% in the first half of 2015, compared with the previous year, due to existing cooling measures.

Apartment-vacancy rates in Singapore are close to a 10-year high, with about 9.2% of units sitting empty in Q2 2015, the highest rate since 9.8% at the end of 2005. This is partly due to the record number of home completions, putting rents under pressure. The slowdown in the global economy could worsen matters with many potential lease terminations for expatriates in industries such as oil and gas and banking.

The office leasing market has also been soft, with declining rents and most of the activity from renewals. With plenty of supply due for delivery in 2016, occupiers may hold off expansion, anticipating better rental conditions later in the year.

Retail sales in Singapore have been lackluster with soft inbound tourism.

The Thong Sia Building near Orchard Road marked the first successful collective sale this year, conditionally sold for S$380 million (US$269 million) or some S$2,430 (US$1,719) per square foot over the existing gross floor area. This property could be redeveloped into a mixed-use development with at least 60% for residential or serviced apartments, and the rest commercial space.

We anticipate that investment activity in Singapore property will be restrained due to the expectation of an interest-rate rise in the United States, Singapore’s slowing economy, prevailing cooling measures and supply-driven issues.

SingaporeDoug SmithThe market continues to be active with cap rates across all asset classes at near record lows, with the hotel sector particularly active. This phenomenon is not being driven by the upcoming Olympics, but is primarily a function of the weaker yen.

Japan

According to the Japan National Tourism Organization, the number of international visitors to Japan reached more than 1.6 million in June 2015, an increase of 51.8% over the previous year. The total number of visitors from January to June has reached 9.14 million, up 46%. Most notably, Chinese visitors reached 462,300 in June, an increase of 167.2% compared with 2014.

We expect the yen to remain at attractive levels for foreign travellers. This together with the government’s efforts to encourage inbound visitors, such as by easing visa requirements, will continue to push visitor numbers, occupancy and average daily rates higher. That in turn will spur development and the conversion of property to accommodate the demand.

The weaker yen has now made hotels, food and shopping cheaper in Tokyo than many other major Asian cities.

It has also encouraged Japanese travellers to vacation at home rather than abroad.

6 | ASIA MArket SNApShot

Suresh Castellino

India

VietnamBen GrayVietnam is continuing to demonstrate that it is picking up and moving forward. Local developers have halved their unsold residential inventory from US$6 billion at the peak of the crisis in 2013. Local investors are continuing to invest in Vietnamese equities ahead of the removal of foreign-ownership caps on local listed and unlisted companies, due mid-September. This streamlines the process of mergers and acquisitions, and will lead to stronger transaction volumes in the next 12-18 months. Interest in income-producing assets is still strong, with strong regional interest being generated. Yield compression, as highlighted in Q2, is continuing across all sectors and affecting valuations accordingly. We are still a frontier market, which equates to good returns for those with the right risk profile.

Ieyo DeguzmanThe Philippine economy gained 5.6% in Q2 2015, with the local property market at the forefront of renewed activity. The government has ramped up infrastructure spending, supporting a private sector that remains robust, leading to accelerating growth. Public construction expenditure climbed 20.4%, turning around a decline of 24% in Q1. There was also double-digit growth in private construction, which rose 10.2%

Main pillars of the economy – robust dollar remittances, low interest rates, and strong demand from the Business Process Outsourcing industry – continue to further development. As such, vacancies for both office and residential real estate remain low in the business districts of metro Manila despite record levels of new space. Also, both sectors posted healthy and stable rental growth during the quarter, at roughly 2%.

Philippines

Nukarn SuwatikulThe overall Thai economy is growing at a slow pace due to both domestic and international factors. The government is continually revising downwards its estimates of economic growth in 2015, from an initial high of 3-4% to around 2-2.5% today, while consumer confidence continues to weaken. Nevertheless, domestic liquidity remains reasonably high, and many of the country’s key economic indicators (including its current accounts, international reserves and even export performance) are doing better than many peer nations in the region. Key concerns remain political stability, foreign investment trends, currency fluctuations and domestic demand.

In the first half of 2015, the property sector remained fairly buoyant due to high liquidity in the market and pent-up demand filtering in to the system, with a large number of project completions. Activity has been particularly strong at the high end of the market, with record prices achieved for both condominiums and land. But the low- and middle-income property markets have started to show signs of stress due primarily to high levels of household debt and low commodity prices.

Thailand

In Q3 2015, the office market continued to see increased momentum. Occupiers are leasing larger office spaces and demanding bigger floor plates, taking much of that space off the market.This trend is expected to continue for a while. However residential developers are under pressure due to sluggish sales, a mounting backlog of stock and cash-flow issues. Developers are deploying a variety of marketing strategies, and are also reducing the average size of apartments across all major cities to ensure that homes are more-affordable for buyers. Private-equity investors, who are in the process of raising fresh funds, are increasing their equity commitments. They have been infusing capital into projects, looking for better returns and long-term commitments. This will limit the burden of regular loan servicing on their projects, permitting the developer to concentrate on execution. There have also been renewed efforts from the government, securities regulators and the central Reserve Bank of India to boost the sector, with further rate cuts expected. REITs continue to remain grounded due to various taxation concerns.

ASIA MArket SNApShot | 7

Steve Atherton The last 60 days have witnessed a dramatic shift of sentiment in Indonesian property. Like other emerging markets, Indonesia’s economy has been hurt by the instability of Chinese stock markets, the devaluation of the Chinese yuan, lower commodity prices, particularly for oil, and the potential U.S. rate hike. The Indonesian rupiah fell to around 14,100 per U.S. dollar in early September, a level last seen in 1998. We also have new regulation from Bank Indonesia requiring the use of rupiah in all property transactions within Indonesia. This forced 19 prime office buildings in the Jakarta CBD to convert their U.S. dollar pricing to rupiah pricing, creating a 35% quarter-on-quarter increase in local-currency average rents from 278,133 rupiah to 375,024 rupiah per square meter per month. While increasing rupiah rental rates normally would indicate a strengthening market, here we have a softening market with impending record amounts of new office supply between 2015 and 2018. New tenancies may secure discounts to asking rates, and office occupancy rates will likely fall several percentage points. The retail-mall moratorium in Jakarta remains in place. The slowing economy is causing lower retail sales, with reports of automobile and motorcycle sales falling more than 20%, and sales of basic items like noodles and cigarettes dropping even more. Retailers of imported items will find it difficult to increase local prices to match the currency depreciation. Industrial land sales have slowed dramatically. New apartment supply in 2015 is expected to touch 30,000 units. With slowing sales and little to no increase in prices, we expect more pressure on the apartment sector. Hotel occupancies have softened in the last few quarters from 64.8% to 57.9% in Jakarta, with average daily rates down 2-3%.

IndonesiaAntony Picon General investment activity remains subdued, with landmark elections due in November 2015 leading to a period of uncertainty. Government activity has slowed as ministers concentrate on campaigning. Investors are still looking into real-estate development and preparing the groundwork in the event of a positive election outcome. The suspension of five large-scale projects, the most-prominent being Dagon City 1, by the government due to their proximity to the revered Shwe Dagon Pagoda has also fed the general unease about doing business in Myanmar. Promises of compensation, probably in the form of alternative land plots, should allay these concerns.

Myanmar

Government land continues to be the main source of potential plots for development. Most investors have struggled dealing with private individuals because they are asking for high rates for their land and there is a general lack of clarity in doing business. The euphoria in the wake of the opening of the country in 2012 has ended, and a sober analysis of investing in the country is taking place from both local landowners and foreign investors. However, many investors, notably in Asia, remain confident in Myanmar’s ability to transform itself from a frontier market to a more-stable emerging market.

Government land continues to be

the main source of potential land plots for

development

Douglas allen smiThHead of Investment ServicesTokyo, [email protected]

Ben grayDirectorInvestment ServicesHo Chi Minh City, [email protected]

sTella hohExecutive DirectorInvestment [email protected]

nukarn suwaTikulDirector

Investment ServicesThailand

This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. Any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. This publication is the copyrighted property of Colliers International and/or its licensor(s). ©2015. All rights reserved.